Embed Size (px)

DESCRIPTION

Annual Report 2004-2005

Citation preview

2004-2005Annual Report

2004-2005Annual Report

Office of theCounty Assessor

Lawrence E. Stone, Assessor

Bien Abordo Linda Aguilar Gene Almerido Annabelle Alquiza Oscar Amaya Medel Angel Rhonda Armstrong Virgil Atencio Deborah Atencio Sang Au

Tuan Au Isa Ayala Anita Badger George Balster Fred Baltazar Mai Bang Patty Barber Vanessa Barkin Jeff Barlow Denise Barry Cynthia Bartolino

Michael Bautista Rudy Baya Bart Beckner David Bethel Neeraj Bhardwaj Laura Bird Laynette Blackfield Judith Bliss Ray Bramlette Jon Bredeson

Yvette Briddell John Brigandi Gloria Brown Linda Brown Bev Brown Charmaine Cabuag Henry Cajucom

Carol Cal lahan Carlos Cansino Celerina Celeste Debbie Chavez Conrad Chen Roland Child Frances Chin

Jae Choe Michel le Chou Terry Cisneros Gary Clarke Dick Cloyd Pauline Coleman Dan Collins Laura Colunga

Craig Cooper Mike Conroy Lisa Cortez Maureen Cowan Barbara Davidson Ramon DelaCruz Huong Dinh Jim

DiTomaso Rosita Dones Tony Duong Sal Duran Bob Easley Indira Ebenezer Ben Emata Sandy Emerson Barry Eng

Judy Epstein Rocky Erfe Fe Escalante Rey Eugenio Richelle Feldan-Cayol Richard Fisher Geemin

Fong Gemma Foster Nora Frantz Marie Fuentes Lorna Gabon Nora Galvez Madan Ganti Joseph Garcia David

Ginsborg Frank Giordano Bruce Glenday Teresa Gonzalez Florinda Gonzales Manuela Gonzalez Ken Green Sal Gutierrez Gina Hale Ginny Hamley

Andrea Harris Mike Harris Murray Hartmann Jamie Hill Julius Ho Hollis Holladay Janice Hongsathavij Pam Hopkins Angela Huang Chris Hughes

Nora Huynh Jenny Huynh Tri Huynh Richard Itow Sandra Cordy Jellison Dee Jimenez Herb Jubin Judy Junaidy Leslie Kennedy Carol Kested David

King Joan Kirkpatrick Bowman Kong Melissa Kong Jack LaCorte Sue-ee Lai Fred Lam Sue Lambrecht Jack Lee Gilbert Lee Kristen Leglu Kathy

LeGrande Judith Lentz Richard Leong Annie Leung Melody Luong

Eileen Lin Sherry Lin Debbie Loennquist Fraser Louie Trinh

Luu-Nguyen Jacelyn Ma John Maag Joe Machado Bob Madalena

Manuel Mandapant Tracy Martinez Bessie Mascardo

Eric Matsuda Sandra Cordy

M c C u l l o c h Chuck McDonald

Lyn McLain Bob McKibbin Tom

McMullen Karen McPherson Mark

McPherson Rita Medina Rich

M e n d o z a George Mil ler

Chuck Mirrasoul Theresa Montenegro Greg

Monteverde Matt Moore Dale Murphy Susan Murphy Lewis

Nance Manny Natividad Mary Dam Nguyen Wayne Nguyen

Robert Norman Clint Nottingham Brian O’Nei l l Josie Ol ivarez

Richard Osborn Kathleene Ozawa Thelma Paet Ed Palacio Lydia

Paquiz Diane Paskert Imelda Pea Sylvia Pedraza Jyot i Pendse

Stephanie Perez Xuanhuong Pham Phu Phan Arika Pineda

Janene Pratt Grace Quilty John Recchio Marty Reinders Jackie

Regala Carol Rivas Delia Rivas Jim Rizzo Carolynn Roberts

Sylvain Roberts Lisa Rodriguez Romeo Rodriguez Manuela

Rosalez Rebecca Ross Marlene Ross Mohit Sabherwal Gabriel

Sainz Elizabeth Samaro Suzanne

Sanchez Tony Sanchez Ford

Sandberg Patti Santillanez Maria

Sarabia Selu Sataraka Laura

Scott Alfredo Semene Walt

Senter Naren Shah David

Shank Marian Shank Cathy

Sheridan Helen Si lva John Sleeman Bertha Sol iz Mary

Solseng Kimberly Starrett Charlie Steed Marian Stewart Larry Stone

Steven Suehiro Marianne Suriaga Donald Sweet Christine Swensen

Iwona Szatkowska Kevin Tanner Ron Tuel ler Raphael Thomas

Christina Thomas Tara Thomas John Thompkins Karen Tillison

Grace Tolentino Cristina Torio Alan Tran Chuong Tran Khanh

Tran Heather Tran Nicole Tran Alicia Trevino Theresa Trinadad

Joy Tsai Pam Umeda Peter van der Pas Susan Vasconcel los

Jackie Ventimiglia Irene Vera Ben Victorino Al Vieira Susie Vigilante Susie Wang Chris Watts Bob Wellner Jim White Linda Wilson David Wierzba

Barbara Wilcox Linda Wilson Lisa Wong Clyde Wong Andy Wu Lilia Yalong Darleen Yamaki Roger Yamat Laura Yau Will Young Michelle Zaffa Eric

Zamudio Gumer Zavala Janet Zecha

Table of Contents

Message from the Assessor .............................................................. 1

Factors Causing Change to the Assessment Roll ............................. 3

Largest Taxpayers/How Tax Bills are Calculated & Allocated ......... 5

Assessment Roll .............................................................................. 6

Ten-year Roll Summary ................................................................... 7

Assessment Information by City ..................................................... 8

Proposition 8 ................................................................................ 12

Exemptions .................................................................................. 14

Proposition 13 .............................................................................. 15

Department Overview .................................................................. 16

Assessment Information by Property Type ................................... 18

Major New Construction .............................................................. 19

Major Changes in Ownership ........................................................ 19

Frequently Asked Questions ......................................................... 21

Assessment Appeals ...................................................................... 24

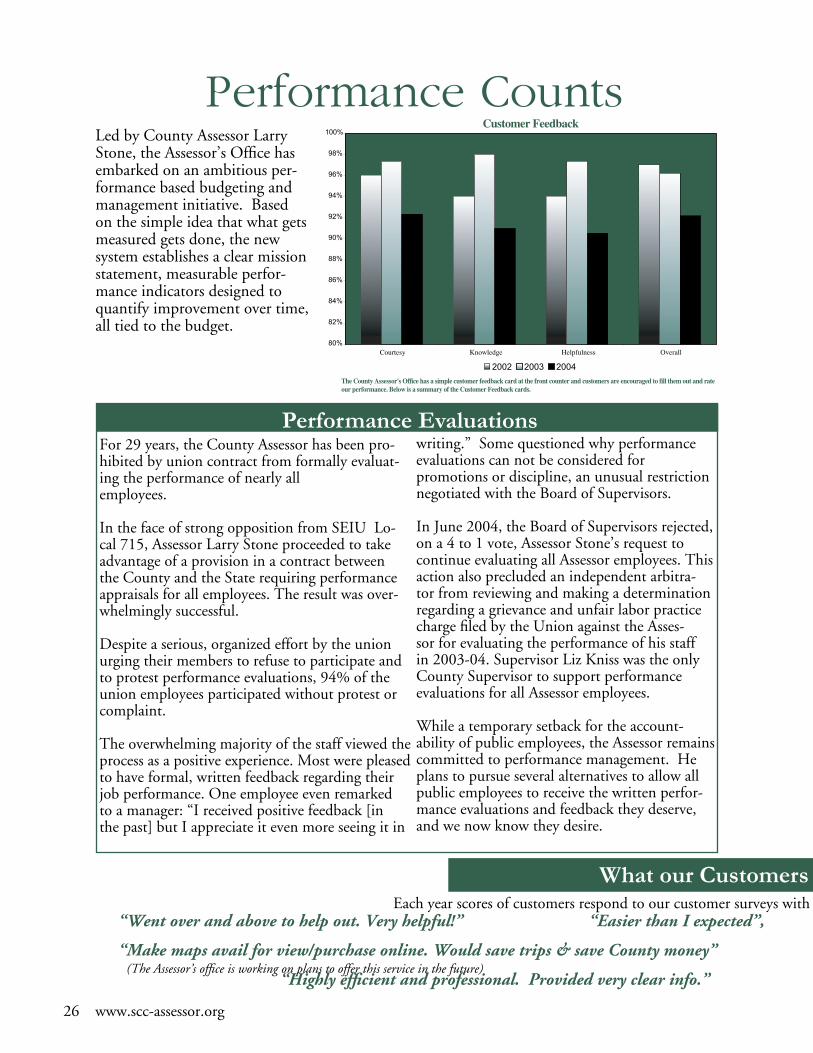

Performance Counts ..................................................................... 26

Summary Bay Area Counties Roll Comparison ............................. 28

Explanation of Terms ................................................................... 29

Above are all the permanent employees that contributed to the closing of the 2004-2005 Assessment Roll. The pictured employees are, clockwise,Bowman Kong, Greg Monteverde, Chuck Mirrasoul, Sylvia Pedraza, Cristina Torio, and Arika Pineda.

Message from the Assessor Lawrence E. Stone

F

www.scc-assessor.org 1

Current Year Roll Growth*

Assessment Roll Value Change:

Local Roll before exemptions

Less: Nonreimbursable exemptions

NET LOCAL ROLL VALUE

2004-2005

$231.60

(9.22)

$222.38

Dollar Change

$5.99

$4.86

2003-2004

$225.61

(8.09)

$217.52

% Change+

2.66%

2.23%

(Exclusive of Public Utility Valuations. Values in Billions.)

2004-2005 Valuation Changes

*Minor discrepancies may occur due to rounding calculations +Percentages based on non-rounded values

or the last five years, Silicon Valley’s economyhas reflected roller coaster type activity reach-ing record heights during the late 90’s only toexperience terrifying drops recently. In 2003,the freefall appears to have ended, or at leastsubsided for many residential property owners.Unfortunately, commercial and industrialproperty values continue to decline without anapparent end in sight.

The Assessor’s Annual Report details thiseconomic phenomena providing a snapshot ofthe region’s economy through a detailedoverview of the 2004-05 assessment roll forSanta Clara County as of January 1, 2004, thelien (valuation) date.

Assessment GrowthThe assessed value of property in Santa ClaraCounty increased by $4.86 billion, 80% lessthan the record increase of $26.91 billion justthree years ago. The total assessed value, netof homeowner exemptions, was $222.38billion, an increase of 2.23% over the previousyear. Not in a decade has the rate of assess-ment roll growth been so low.

Driven by a poorly governed national economyand a struggling local economy, the decline inreal estate values continues to plague ownersof office buildings, shopping centers, industrialproperty, and research and developmentcampuses. At the same time, the market valueof residential property has stabilized, and in

many geographic areas improved. For residen-tial properties to increase while commercial andindustrial properties plummet is an anomaly forSilicon Valley. Typically when the economystalls and unemployment rises, the market valueof all types of properties decline.

In addition, many of the County’s high-technol-ogy businesses either disposed of businessproperty, or did not make major investments intheir physical plants including machinery,equipment, computers and fixtures. In justthree years, the net assessed value of businessproperty has declined almost 25%, from $31billion to $24 billion. This year alone, businessproperty dropped 14% ($3.8 billion), more thantwice the decline experienced in the prior year.

2 www.scc-assessor.org

The impact was also very uneven throughout theCounty. Cities with the largest concentration ofhigh tech companies experienced the greatestdecline. Sunnyvale, Santa Clara, Milpitas andMountain View, with populations totaling morethan a third of the county, experienced negativegrowth in the assessment roll ranging from -5%to just under -1%. Just three years ago the rateof assessment roll growth for all 15 cities in SantaClara County exceeded 10%, and in some cities,topped 20%. The City of Santa Clara, forexample, went from 19% roll growth in 2001,to -5% in 2004.

It is truly an unusual and hopefully an uncommonphenomenon for a city to experience negativeassessment growth. In contrast, residential com-munities like Los Altos and Los Altos Hillsexperienced growth in excess of 8%.

The decline was more severe for property inredevelopment agencies (RDA) at the center ofSilicon Valley’s commercial and industrial high-technology industry. For example, the followingRDAs all experienced negative assessment growth;San Jose, -11.5%; Santa Clara, -11.28%; Moun-tain View, -7.74%; Cupertino, -4.70%; andCampbell, -1.04%. San Jose topped the list atalmost $2 billion less than the previous year.

The growth in the assessment roll is also impor-tant to the “basic aid” school districts in SantaClara County. A basic aid school district is adistrict in which the property tax revenue gener-ated locally exceeds the State’s formula for schooldistrict funding. Consequently, basic aid schooldistricts have more funds at their disposal becauseof direct access to greater local property tax rev-enue. However, the revenue these school districtsreceive can fluctuate according to changes in theassessed value of property within the districts’ taxrate areas. The basic aid school districts in SantaClara County are: Fremont Union High SchoolDistrict, Lakeside Joint Elementary School Dis-trict, Los Altos Elementary School District, LosGatos Union Elementary School District, LosGatos-Saratoga Joint Union High School District,Mountain View-Los Altos Union High SchoolDistrict, Palo Alto Unified School District,Saratoga Union Elementary School District, SantaClara Unified School District and SunnyvaleElementary School District. Ten of California’s 67basic aid school districts are located in Santa ClaraCounty.

Role of the County Assessor’s OfficeThe Assessor’s Office is responsible for deter-mining the assessed value of all real and businesspersonal property within Santa Clara County.Each year the Assessor’s professional staff pro-vides accurate assessments of all secured andunsecured property. The assessment roll, whichincludes more than 500,000 roll units of realproperty and business assessments, is the basisupon which property taxes are levied.

Property taxes, in turn, provide an essentialsource of revenue to support basic publicservices provided by schools and local govern-ments. These are the public institutions thatform the foundation of our region’s qualityof life.

The Annual Report presents a summary of the2004-2005 assessment roll as of the January 1,2004, lien (valuation) date. The annual assess-ment roll, delivered by the Assessor to theFinance Agency Director on July 1, 2004, is avaluable resource for budgeting and financialplanning by local governmental agencies.

Information in this report reflects all, locallyassessed property, both secured and unsecured.The statistical data also distinguishes betweenbusiness personal property and real property.It summarizes current assessments of the variouscities and unincorporated areas compared toprior years, and illustrates the trends in assess-ment appeals. Assessments of public utilities arethe responsibility of the California State Boardof Equalization, and therefore are not includedin this report.

Factors in Assessment GrowthAssessment roll growth is a result of severalmajor components.

“Real property” is assessed to reflect fair marketvalue when there is a change in ownership ornew construction. The change in assessed valueof individual properties reflects the net differ-ence between the prior assessed value and thenew market value resulting from the change inownership or new construction. Reappraisal asa result of new construction reflects only thevalue added by the new construction.

www.scc-assessor.org 3

Unless property changes ownership or issubject to new construction, Proposition 13limits any increase in assessed value to nomore than 2% annually or the California CPI(1.867% in 2004), whichever is lower. Con-sequently, the value of the assessment roll issignificantly less than the fair market value ofall property in Santa Clara County.

When economic conditions cause a decline inproperty values, the Assessor is required toadjust assessed values to reflect that decline. Ifthe market value of a property as of the lien(valuation) date, January 1, 2004, was lessthan the assessed value, the impacted propertyowner is entitled to a temporary adjustment.This year, the assessed values for 24,743properties were reduced for a total reductionof $10.6 billion from the assessment roll. Bycomparison in 1995, the “bottom” of the lastmajor economic decline, the assessed values of98,000 properties were reduced, reflecting a$5 billion decline in the assessment roll.

Even more dramatic is the fact that 1,352non-residential properties accounted for awhopping 83% ($8.8 billion) of the totalreduction of assessed values. Consequently,while residential properties have experiencedsome volatility, the collapse of commercialand industrial market has been unprec-edented. More than a third of the decreasein assessed values ($4.3 billion) occurred inthe county’s nine redevelopment agencies.

Business personal property, which includescomputers, machinery, equipment and fixtures,also experienced a precipitous decline of $3.8billion, a 14% reduction. Assessed values ofbusiness personal property is determined fromproperty statements filed annually by 55,000businesses in Santa Clara County.

AccomplishmentsDuring the current economic recession, themost serious challenge for the Assessor is toproactively respond to changes in the market-place. The result is a dramatic increase inworkload, accomplished without compromisingproductivity and performance. A sample of ourmajor accomplishments includes:

• Completed the annual assessment roll bythe deadline mandated by law.

• Reduced the assessed values of 24,743properties as mandated by law.

• Completed 98.9% of real propertyvaluations.

• Completed 99.7% of the business personalproperty assessment and audits.

• Completed 99.6% of eligible exemptions.• Resolved a record number of business

personal property assessment appeals.• Continued to enhance the Assessor’s on-line

property “look-up” feature on the Assessor’sweb site (scc-assessor.org), allowing prop-erty owners to access property records anytime of the day or night from a convenientlocation. The site remains among theCounty’s top five most-visited sites.

+ Reflects those properties that did not establish a new base year value.* Net of CPI

** Changes due to Assessment Appeal Board actions, real property requiring annual reassessment, roll corrections, etc.Note: A limited portion of new construction is reflected in the change in ownership figures.

Dollar % ofChange Change

Proposition 8 net change+ -$1.76 22.0%Business Personal Property -3.79 47.4%Exemptions -1.11 13.9%Other Net changes** -1.34 16.8%Subtotal, declines in values -$8.0 100.0%

Factors Causing Change to the 2004-2005 Assessment Roll(in Billions)

Dollar % of Change Change

Change in ownership* $8.02 62.4% New Construction* 1.61 12.5% CPI factor (1.87%) 3.23 25.1%

Subtotal, increases in value $12.86 100.0% Grand Total of Changes to Assessment Roll $4.86

4 www.scc-assessor.org

• Audited 99.4% of the 1,192 businessaccounts required by the CaliforniaRevenue and Taxation Code, reflecting anincrease of 17% over the prior year.

• Updated 1,702 Assessor Maps, a 41%increase including 307 new parcel maps.

• Processed 105,467 deeds, creating 114,928title documents, a 9.1% increase over theprior year.

• Achieved full utilization of documentimaging for the processing of homeownerexemption claims, deeds and businessproperty statements.

• Reduced serious backlogs in both map-ping and deed processing throughworkflow streamlining initiatives.

• Successfully implemented the County’snew, on-line paperless accounting system.

• Trained certified appraisers and auditorsbeyond the statutorily required minimum.

• Completed performance evaluations forall employees for the first time in 29 years.

• Launched customer satisfaction surveysfor all divisions.

• Progressed on the design of a new com-puter information system, to meet thechallenges of the next generation.

Trends and Future Goals

With Silicon Valley and the State of Californiamired in deep economic crisis, the Assessor’sOffice, now more than ever, is focused ondeveloping and implementing creative andinnovative solutions to improve efficiency andproductivity while reducing costs.

Some of the major challenges include:• The departure of a significant number of

our most experienced professionals hascreated a major “brain drain.” Twenty-nine employees responded to a “goldenhandshake” incentive offered by theBoard of Supervisors, creating a seriousstaffing crisis.

Many of the mission critical professionalscannot be replaced easily as several years ofdirect involvement is required to appraiselarge commercial, industrial and multifamily properties and to audit major corpo-rations. Regrettably the Board rejected theAssessor’s request for additional resources toencourage the recruitment of new talent.

The 15 cities in Santa Clara County, theCounty itself and public schools will bearthe brunt of the “brain drain”, especially ifthe economy improves and there are insuffi-cient resources to respond to positivechanges in the market place.

• We are committed to replacing the 25 year-old legacy computer system with a modern,state of the art system that will efficientlymeet both the immediate and long-termneeds of the department and Countygovernment.

• We will implement a major reorganizationand consolidation of the Assessor’s publicservice responsibilities to improve bothcustomer service and office security.

Finally, as County Assessor, I will focus attentionand resources on continuous improvementinitiatives based on quality, service, innovation,accountability, and relevant partnerships. TheAssessor’s Office contains a group of employeesthat I believe are among the most talented anddedicated public servants anywhere in govern-ment.

It is our primary objective to treat all propertyowners and tax payers with the highest degreeof courtesy and professionalism.

Lawrence E. StoneAssessor

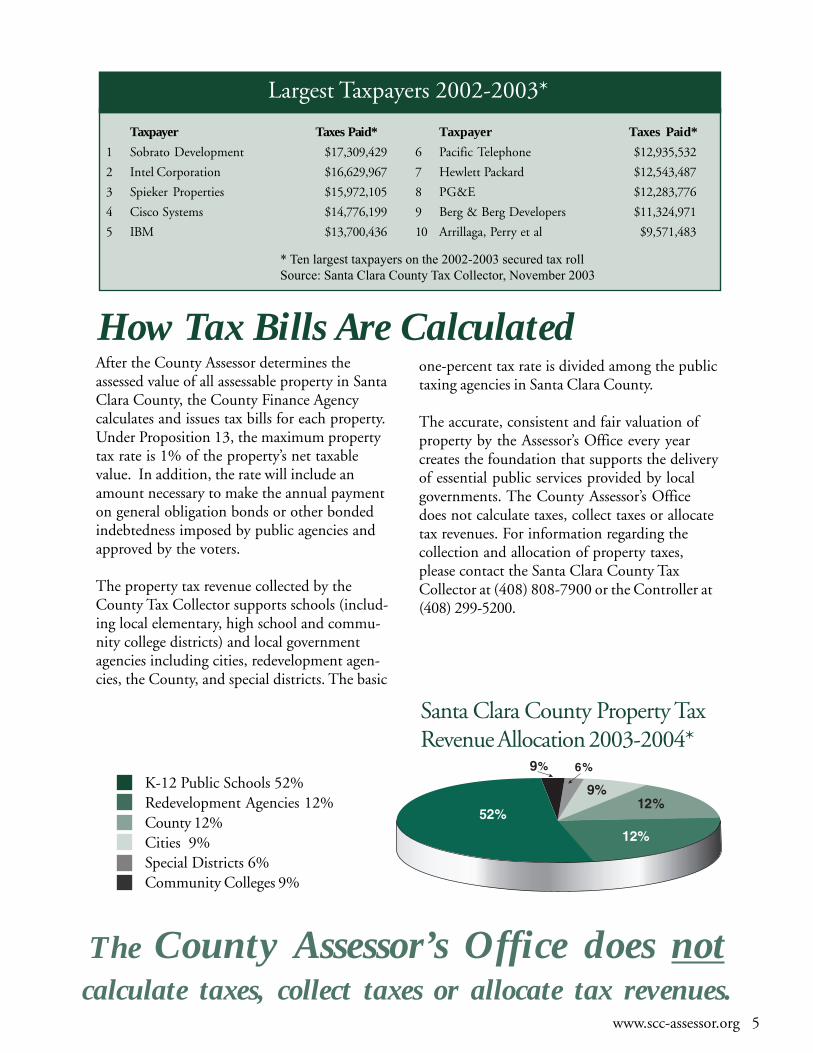

After the County Assessor determines theassessed value of all assessable property in SantaClara County, the County Finance Agencycalculates and issues tax bills for each property.Under Proposition 13, the maximum propertytax rate is 1% of the property’s net taxablevalue. In addition, the rate will include anamount necessary to make the annual paymenton general obligation bonds or other bondedindebtedness imposed by public agencies andapproved by the voters.

The property tax revenue collected by theCounty Tax Collector supports schools (includ-ing local elementary, high school and commu-nity college districts) and local governmentagencies including cities, redevelopment agen-cies, the County, and special districts. The basic

The County Assessor’s Office does notcalculate taxes, collect taxes or allocate tax revenues.

Santa Clara County Property TaxRevenue Allocation 2003-2004*

K-12 Public Schools 52%Redevelopment Agencies 12%County 12%Cities 9%Special Districts 6%Community Colleges 9%

one-percent tax rate is divided among the publictaxing agencies in Santa Clara County.

The accurate, consistent and fair valuation ofproperty by the Assessor’s Office every yearcreates the foundation that supports the deliveryof essential public services provided by localgovernments. The County Assessor’s Officedoes not calculate taxes, collect taxes or allocatetax revenues. For information regarding thecollection and allocation of property taxes,please contact the Santa Clara County TaxCollector at (408) 808-7900 or the Controller at(408) 299-5200.

How Tax Bills Are Calculated

Taxpayer Taxes Paid*

1 Sobrato Development $17,309,429

2 Intel Corporation $16,629,967

3 Spieker Properties $15,972,105

4 Cisco Systems $14,776,199

5 IBM $13,700,436

* Ten largest taxpayers on the 2002-2003 secured tax roll

Source: Santa Clara County Tax Collector, November 2003

Largest Taxpayers 2002-2003*

Taxpayer Taxes Paid*

6 Pacific Telephone $12,935,532

7 Hewlett Packard $12,543,487

8 PG&E $12,283,776

9 Berg & Berg Developers $11,324,971

10 Arrillaga, Perry et al $9,571,483

www.scc-assessor.org 5

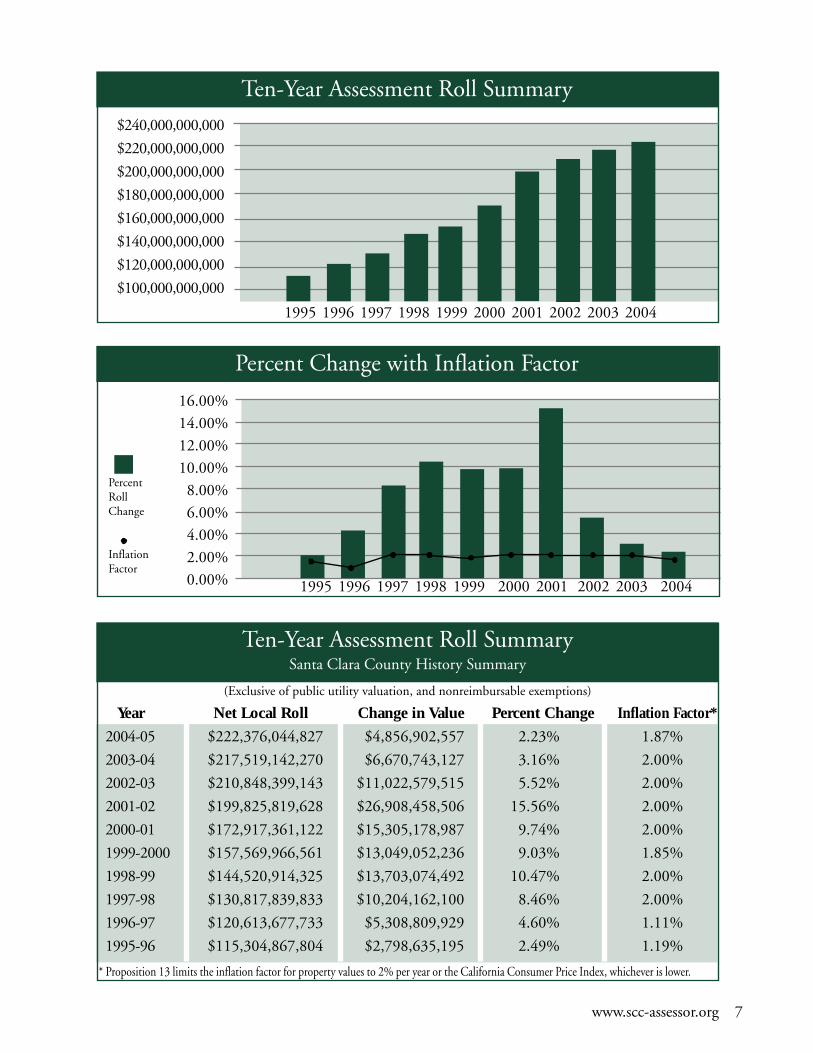

Over the past fifteen years, Santa Clara County’sannual roll growth has ranged from more than15% to less than 1%. The local economy has asignificant impact on property transfer transac-tions and building permit activity. This yearchanges in property ownership accounted for62% of the total increase in assessed value overlast year’s assessment roll. Under Proposition13, once a base value is established as a result ofa change in ownership or new construction, theassessed value of a property can increase by nomore than 2% annually based on an inflationfactor, tied to the California Consumer PriceIndex (CPI). Since the implementation ofProposition 13 in 1978, the CPI has been lessthan 2% five times: in 1983, 1995, 1996, 1999and 2004.

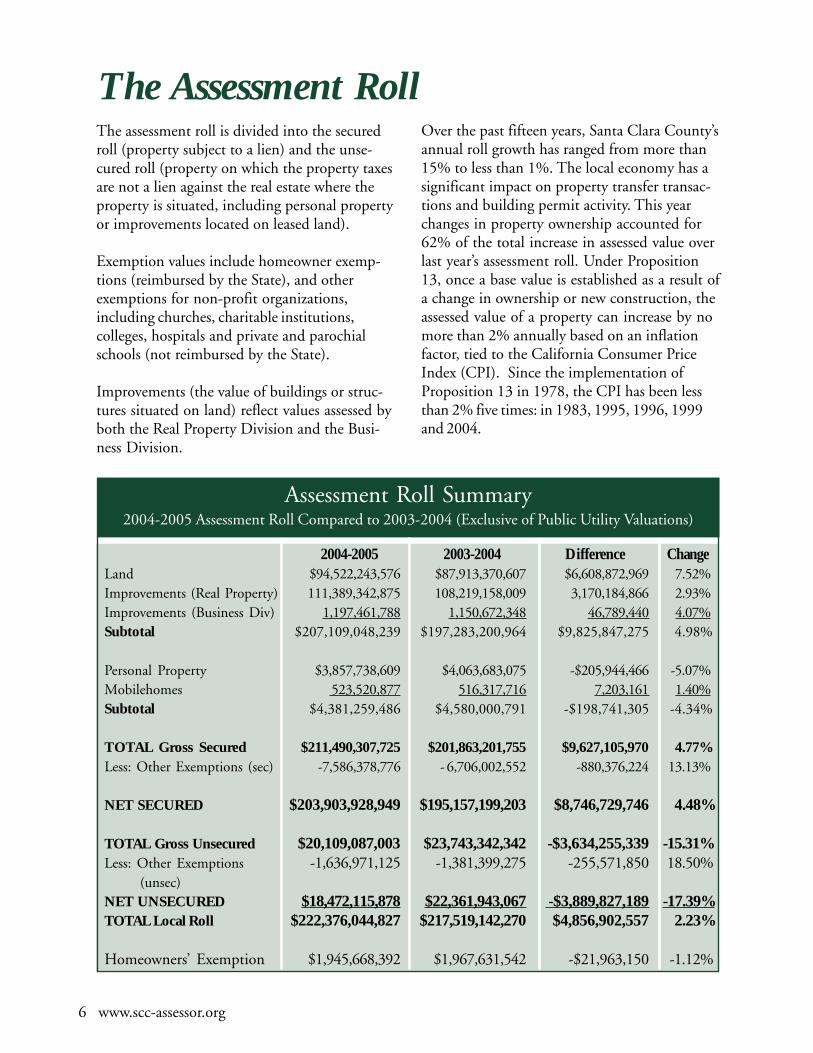

The Assessment RollThe assessment roll is divided into the securedroll (property subject to a lien) and the unse-cured roll (property on which the property taxesare not a lien against the real estate where theproperty is situated, including personal propertyor improvements located on leased land).

Exemption values include homeowner exemp-tions (reimbursed by the State), and otherexemptions for non-profit organizations,including churches, charitable institutions,colleges, hospitals and private and parochialschools (not reimbursed by the State).

Improvements (the value of buildings or struc-tures situated on land) reflect values assessed byboth the Real Property Division and the Busi-ness Division.

Assessment Roll Summary2004-2005 Assessment Roll Compared to 2003-2004 (Exclusive of Public Utility Valuations)

2004-2005 2003-2004 Difference ChangeLand $94,522,243,576 $87,913,370,607 $6,608,872,969 7.52%Improvements (Real Property) 111,389,342,875 108,219,158,009 3,170,184,866 2.93%Improvements (Business Div) 1,197,461,788 1,150,672,348 46,789,440 4.07%Subtotal $207,109,048,239 $197,283,200,964 $9,825,847,275 4.98%

Personal Property $3,857,738,609 $4,063,683,075 -$205,944,466 -5.07%Mobilehomes 523,520,877 516,317,716 7,203,161 1.40%Subtotal $4,381,259,486 $4,580,000,791 -$198,741,305 -4.34%

TOTAL Gross Secured $211,490,307,725 $201,863,201,755 $9,627,105,970 4.77%Less: Other Exemptions (sec) -7,586,378,776 - 6,706,002,552 -880,376,224 13.13%

NET SECURED $203,903,928,949 $195,157,199,203 $8,746,729,746 4.48%

TOTAL Gross Unsecured $20,109,087,003 $23,743,342,342 -$3,634,255,339 -15.31%Less: Other Exemptions -1,636,971,125 -1,381,399,275 -255,571,850 18.50% (unsec)NET UNSECURED $18,472,115,878 $22,361,943,067 -$3,889,827,189 -17.39%TOTAL Local Roll $222,376,044,827 $217,519,142,270 $4,856,902,557 2.23%

Homeowners’ Exemption $1,945,668,392 $1,967,631,542 -$21,963,150 -1.12%

6 www.scc-assessor.org

Ten-Year Assessment Roll SummarySanta Clara County History Summary

Year

2004-05

2003-04

2002-03

2001-02

2000-01

1999-2000

1998-99

1997-98

1996-97

1995-96

Net Local Roll

$222,376,044,827

$217,519,142,270

$210,848,399,143

$199,825,819,628

$172,917,361,122

$157,569,966,561

$144,520,914,325

$130,817,839,833

$120,613,677,733

$115,304,867,804

Percent Change

2.23%

3.16%

5.52%

15.56%

9.74%

9.03%

10.47%

8.46%

4.60%

2.49%

Change in Value

$4,856,902,557

$6,670,743,127

$11,022,579,515

$26,908,458,506

$15,305,178,987

$13,049,052,236

$13,703,074,492

$10,204,162,100

$5,308,809,929

$2,798,635,195

Inflation Factor*

1.87%

2.00%

2.00%

2.00%

2.00%

1.85%

2.00%

2.00%

1.11%

1.19%

(Exclusive of public utility valuation, and nonreimbursable exemptions)

* Proposition 13 limits the inflation factor for property values to 2% per year or the California Consumer Price Index, whichever is lower.

$240,000,000,000

$220,000,000,000

$200,000,000,000

$180,000,000,000

$160,000,000,000

$140,000,000,000

$120,000,000,000

$100,000,000,000

Ten-Year Assessment Roll Summary

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

16.00%14.00%12.00%10.00%8.00%6.00%4.00%2.00%0.00%

Percent Change with Inflation Factor

1995 1996 1997 1998 1999 2000 2001 2002 2003 2004

PercentRollChange

InflationFactor

www.scc-assessor.org 7

8 www.scc-assessor.org

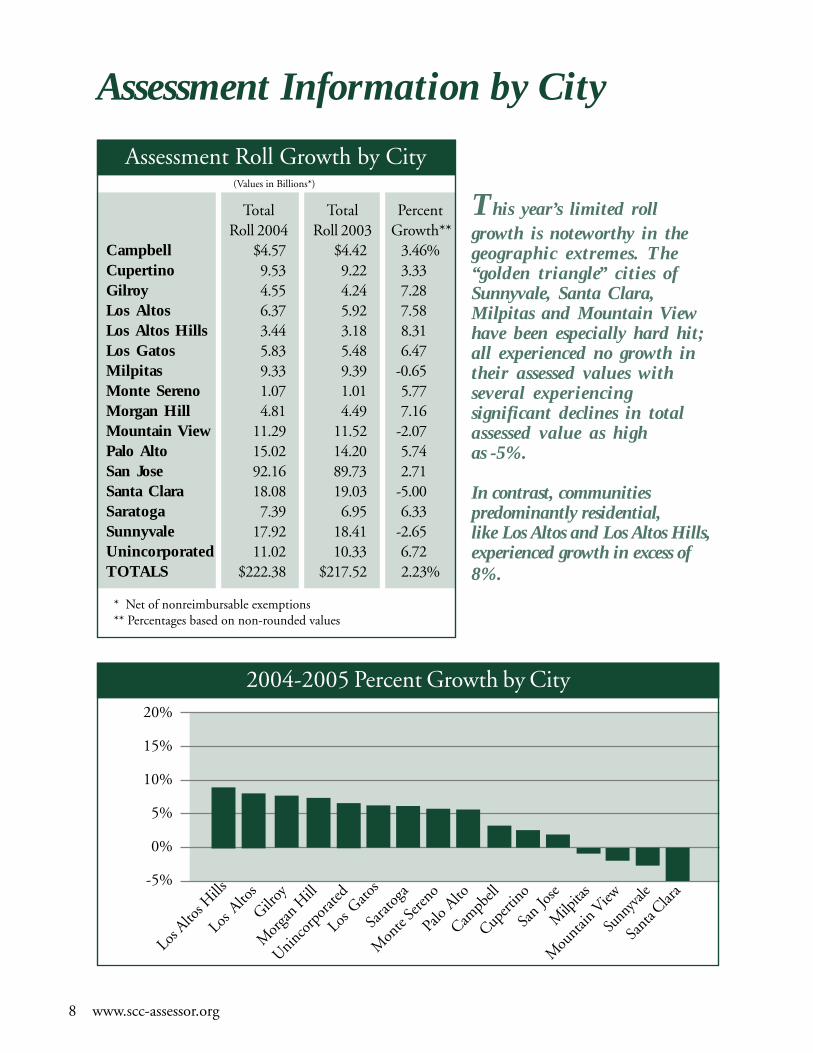

This year’s limited rollgrowth is noteworthy in thegeographic extremes. The“golden triangle” cities ofSunnyvale, Santa Clara,Milpitas and Mountain Viewhave been especially hard hit;all experienced no growth intheir assessed values withseveral experiencingsignificant declines in totalassessed value as highas -5%.

In contrast, communitiespredominantly residential,like Los Altos and Los Altos Hills,experienced growth in excess of8%.

Assessment Information by City

20%

15%

10%

5%

0%

-5%

2004-2005 Percent Growth by City

Sunn

yvale

Mon

te Se

reno

Milp

itas

Sarat

oga

San

Jose

Mor

gan H

ill

Los G

atos

Los A

ltos H

ills

Mou

ntain

View

Los A

ltos

Cupert

ino

Gilroy

Campb

ell

Sant

a Clar

a

Palo

Alto

Uninco

rpor

ated

Assessment Roll Growth by City

* Net of nonreimbursable exemptions** Percentages based on non-rounded values

(Values in Billions*)

Total Total PercentRoll 2004 Roll 2003 Growth**

Campbell $4.57 $4.42 3.46%Cupertino 9.53 9.22 3.33Gilroy 4.55 4.24 7.28Los Altos 6.37 5.92 7.58Los Altos Hills 3.44 3.18 8.31Los Gatos 5.83 5.48 6.47Milpitas 9.33 9.39 -0.65Monte Sereno 1.07 1.01 5.77Morgan Hill 4.81 4.49 7.16Mountain View 11.29 11.52 -2.07Palo Alto 15.02 14.20 5.74San Jose 92.16 89.73 2.71Santa Clara 18.08 19.03 -5.00Saratoga 7.39 6.95 6.33Sunnyvale 17.92 18.41 -2.65Unincorporated 11.02 10.33 6.72TOTALS $222.38 $217.52 2.23%

www.scc-assessor.org 9

$100

$90

$80

$70

$60

$50

$40

$30

$20

$10

$0

2004-2005 Net Assessment Roll Distribution by City

Campb

ell

Gilroy

Los A

ltos H

ills

Mon

te Ser

eno

Sarat

oga

Los A

ltos

Los G

atos

Mor

gan H

ill

Mou

ntain

View

Uninco

rpor

ated

Milp

itas

Cupert

ino

San J

ose

Sant

a Clar

a

Sunn

yvale

Palo

Alto

(Values in Billions)

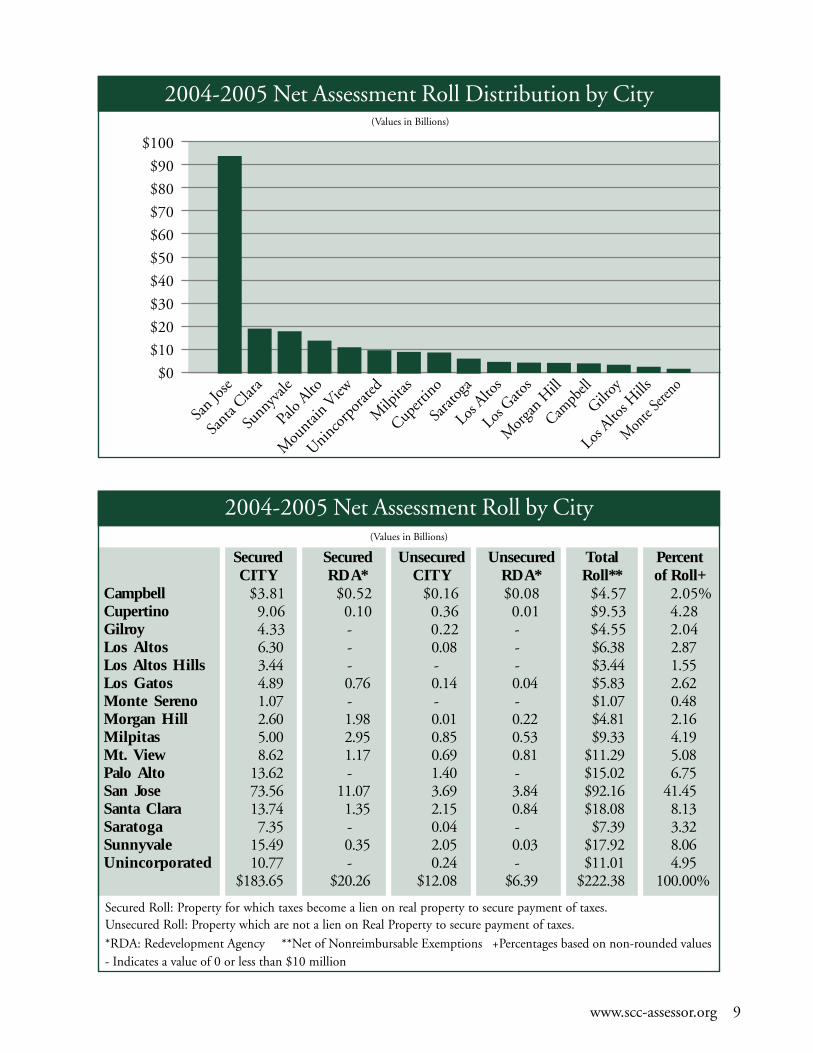

2004-2005 Net Assessment Roll by City(Values in Billions)

Secured Roll: Property for which taxes become a lien on real property to secure payment of taxes.Unsecured Roll: Property which are not a lien on Real Property to secure payment of taxes.

*RDA: Redevelopment Agency **Net of Nonreimbursable Exemptions +Percentages based on non-rounded values- Indicates a value of 0 or less than $10 million

Secured Secured Unsecured Unsecured Total PercentCITY RDA* CITY RDA* Roll** of Roll+

Campbell $3.81 $0.52 $0.16 $0.08 $4.57 2.05%Cupertino 9.06 0.10 0.36 0.01 $9.53 4.28Gilroy 4.33 - 0.22 - $4.55 2.04Los Altos 6.30 - 0.08 - $6.38 2.87Los Altos Hills 3.44 - - - $3.44 1.55Los Gatos 4.89 0.76 0.14 0.04 $5.83 2.62Monte Sereno 1.07 - - - $1.07 0.48Morgan Hill 2.60 1.98 0.01 0.22 $4.81 2.16Milpitas 5.00 2.95 0.85 0.53 $9.33 4.19Mt. View 8.62 1.17 0.69 0.81 $11.29 5.08Palo Alto 13.62 - 1.40 - $15.02 6.75San Jose 73.56 11.07 3.69 3.84 $92.16 41.45Santa Clara 13.74 1.35 2.15 0.84 $18.08 8.13Saratoga 7.35 - 0.04 - $7.39 3.32Sunnyvale 15.49 0.35 2.05 0.03 $17.92 8.06Unincorporated 10.77 - 0.24 - $11.01 4.95

$183.65 $20.26 $12.08 $6.39 $222.38 100.00%

10 www.scc-assessor.org

$90

$80

$70

$60

$50

$40

$30

$20

$10

$0

2004-2005 Real Property Distribution by City

Campb

ell

Gilroy

Los A

ltos H

ills

Mon

te Se

reno

Sarat

oga

Los A

ltos

Los G

atos

Mor

gan H

ill

Uninco

rpor

ated

Mou

ntain

View

Cupert

ino

Milp

itas

San

Jose

Sunn

yvale

Sant

a Clar

a

Palo

Alto

(Values in Billions)

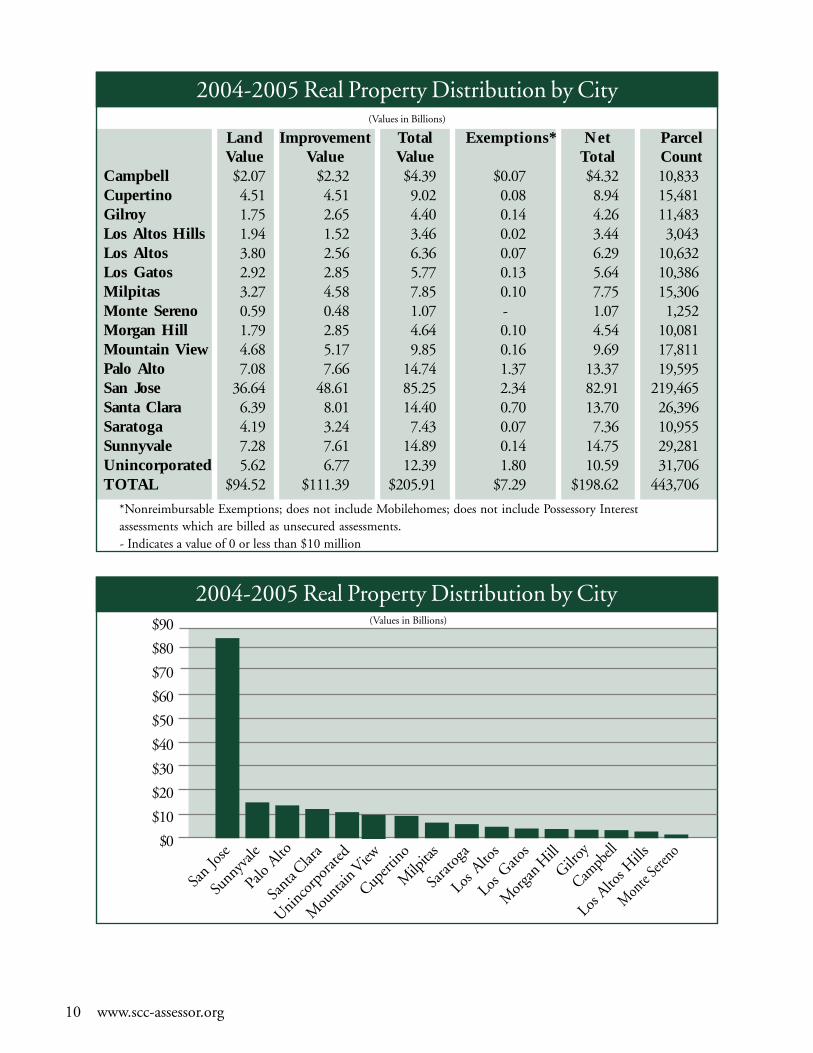

2004-2005 Real Property Distribution by City(Values in Billions)

*Nonreimbursable Exemptions; does not include Mobilehomes; does not include Possessory Interestassessments which are billed as unsecured assessments.

Land Improvement Total Exemptions* Net ParcelValue Value Value Total Count

Campbell $2.07 $2.32 $4.39 $0.07 $4.32 10,833Cupertino 4.51 4.51 9.02 0.08 8.94 15,481Gilroy 1.75 2.65 4.40 0.14 4.26 11,483Los Altos Hills 1.94 1.52 3.46 0.02 3.44 3,043Los Altos 3.80 2.56 6.36 0.07 6.29 10,632Los Gatos 2.92 2.85 5.77 0.13 5.64 10,386Milpitas 3.27 4.58 7.85 0.10 7.75 15,306Monte Sereno 0.59 0.48 1.07 - 1.07 1,252Morgan Hill 1.79 2.85 4.64 0.10 4.54 10,081Mountain View 4.68 5.17 9.85 0.16 9.69 17,811Palo Alto 7.08 7.66 14.74 1.37 13.37 19,595San Jose 36.64 48.61 85.25 2.34 82.91 219,465Santa Clara 6.39 8.01 14.40 0.70 13.70 26,396Saratoga 4.19 3.24 7.43 0.07 7.36 10,955Sunnyvale 7.28 7.61 14.89 0.14 14.75 29,281Unincorporated 5.62 6.77 12.39 1.80 10.59 31,706TOTAL $94.52 $111.39 $205.91 $7.29 $198.62 443,706

- Indicates a value of 0 or less than $10 million

www.scc-assessor.org 11

$12.0

$10.0

$8.0

$6.0

$4.0

$2.0

$0.0

2004-2005 Business Personal Property Distribution by City

Los Alto

s

Sarat

oga

Mon

te Se

reno

Uninco

rporat

ed

Campb

ell

Mor

gan H

ill

Los G

atos

Palo

Alto

Mou

ntain

View

Cupert

inoGilro

y

San

Jose

Sant

a Clar

a

Sunn

yvale

Milp

itas

(Values in Billions)

Los A

ltos H

ills

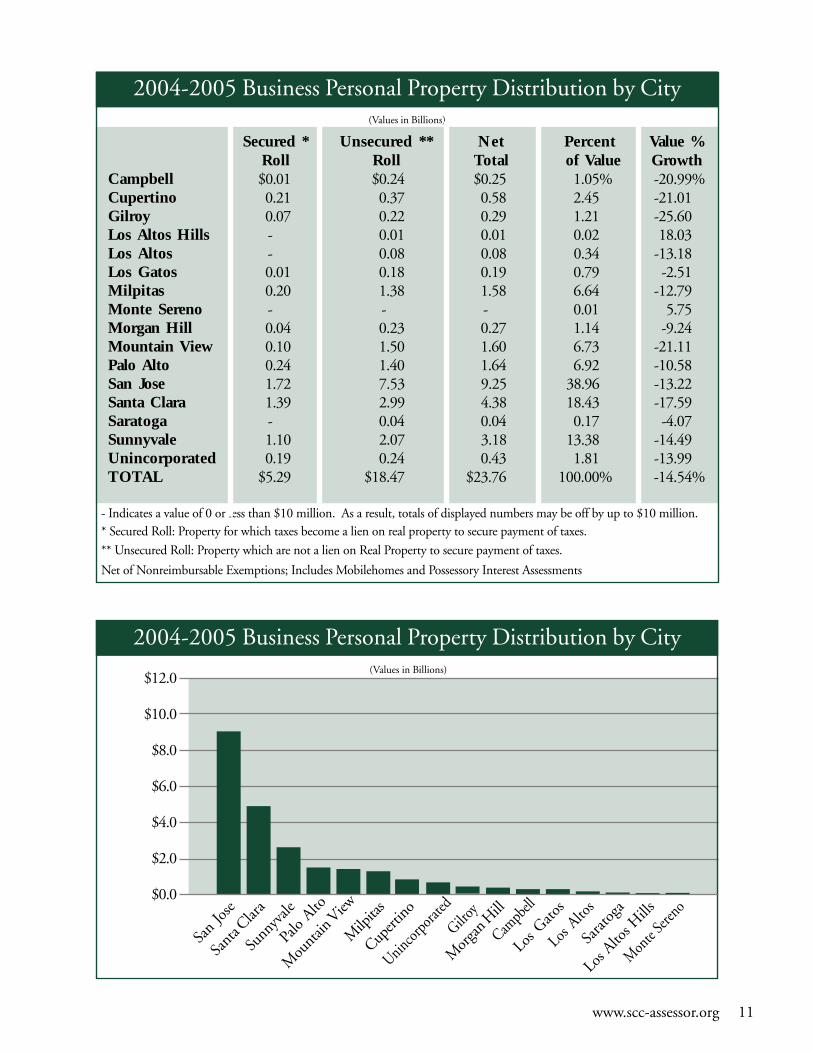

2004-2005 Business Personal Property Distribution by City(Values in Billions)

- Indicates a value of 0 or less than $10 million. As a result, totals of displayed numbers may be off by up to $10 million.* Secured Roll: Property for which taxes become a lien on real property to secure payment of taxes.

** Unsecured Roll: Property which are not a lien on Real Property to secure payment of taxes.

Net of Nonreimbursable Exemptions; Includes Mobilehomes and Possessory Interest Assessments

Secured * Unsecured ** Net Percent Value %Roll Roll Total of Value Growth

Campbell $0.01 $0.24 $0.25 1.05% -20.99%Cupertino 0.21 0.37 0.58 2.45 -21.01Gilroy 0.07 0.22 0.29 1.21 -25.60Los Altos Hills - 0.01 0.01 0.02 18.03Los Altos - 0.08 0.08 0.34 -13.18Los Gatos 0.01 0.18 0.19 0.79 -2.51Milpitas 0.20 1.38 1.58 6.64 -12.79Monte Sereno - - - 0.01 5.75Morgan Hill 0.04 0.23 0.27 1.14 -9.24Mountain View 0.10 1.50 1.60 6.73 -21.11Palo Alto 0.24 1.40 1.64 6.92 -10.58San Jose 1.72 7.53 9.25 38.96 -13.22Santa Clara 1.39 2.99 4.38 18.43 -17.59Saratoga - 0.04 0.04 0.17 -4.07Sunnyvale 1.10 2.07 3.18 13.38 -14.49Unincorporated 0.19 0.24 0.43 1.81 -13.99TOTAL $5.29 $18.47 $23.76 100.00% -14.54%

12 www.scc-assessor.org

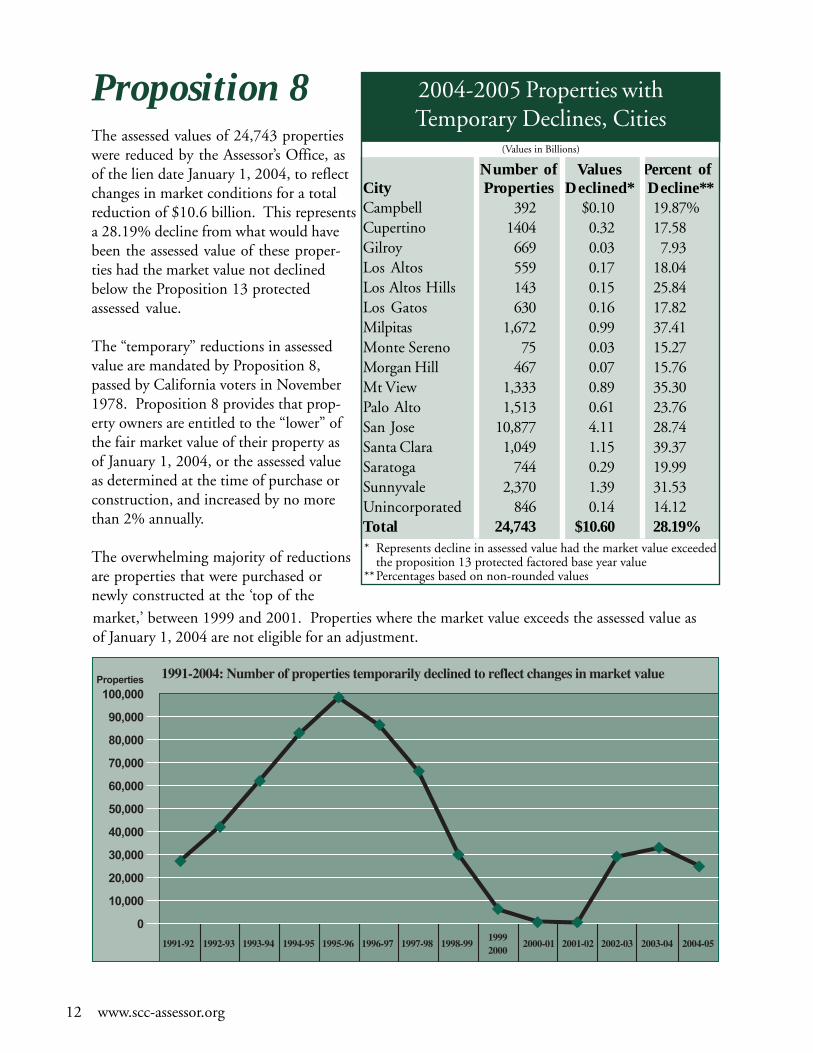

2004-2005 Properties withTemporary Declines, Cities

* Represents decline in assessed value had the market value exceededthe proposition 13 protected factored base year value

**Percentages based on non-rounded values

(Values in Billions)

Number of Values Percent ofCity Properties Declined* Decline**Campbell 392 $0.10 19.87%Cupertino 1404 0.32 17.58Gilroy 669 0.03 7.93Los Altos 559 0.17 18.04Los Altos Hills 143 0.15 25.84Los Gatos 630 0.16 17.82Milpitas 1,672 0.99 37.41Monte Sereno 75 0.03 15.27Morgan Hill 467 0.07 15.76Mt View 1,333 0.89 35.30Palo Alto 1,513 0.61 23.76San Jose 10,877 4.11 28.74Santa Clara 1,049 1.15 39.37Saratoga 744 0.29 19.99Sunnyvale 2,370 1.39 31.53Unincorporated 846 0.14 14.12Total 24,743 $10.60 28.19%

Proposition 8The assessed values of 24,743 propertieswere reduced by the Assessor’s Office, asof the lien date January 1, 2004, to reflectchanges in market conditions for a totalreduction of $10.6 billion. This representsa 28.19% decline from what would havebeen the assessed value of these proper-ties had the market value not declinedbelow the Proposition 13 protectedassessed value.

The “temporary” reductions in assessedvalue are mandated by Proposition 8,passed by California voters in November1978. Proposition 8 provides that prop-erty owners are entitled to the “lower” ofthe fair market value of their property asof January 1, 2004, or the assessed valueas determined at the time of purchase orconstruction, and increased by no morethan 2% annually.

The overwhelming majority of reductionsare properties that were purchased ornewly constructed at the ‘top of the

market,’ between 1999 and 2001. Properties where the market value exceeds the assessed value asof January 1, 2004 are not eligible for an adjustment.

Properties

100,000

90,000

80,000

70,000

60,000

50,000

40,000

30,000

20,000

10,000

0

1991-2004: Number of properties temporarily declined to reflect changes in market value

1991-92 1992-93 1993-94 1994-95 1995-96 1996-97 1997-98 1998-99 2000-01 2001-02 2002-03 2003-04 2004-0519992000

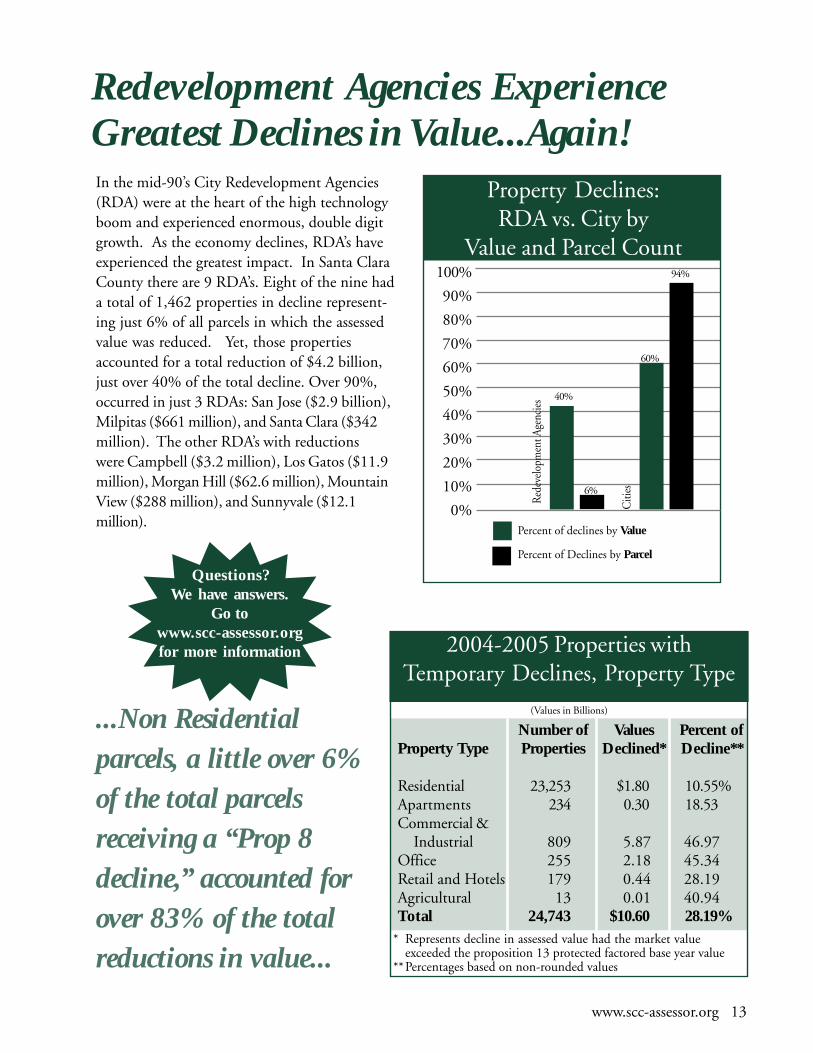

Redevelopment Agencies ExperienceGreatest Declines in Value...Again!

...Non Residentialparcels, a little over 6%of the total parcelsreceiving a “Prop 8decline,” accounted forover 83% of the totalreductions in value...

In the mid-90’s City Redevelopment Agencies(RDA) were at the heart of the high technologyboom and experienced enormous, double digitgrowth. As the economy declines, RDA’s haveexperienced the greatest impact. In Santa ClaraCounty there are 9 RDA’s. Eight of the nine hada total of 1,462 properties in decline represent-ing just 6% of all parcels in which the assessedvalue was reduced. Yet, those propertiesaccounted for a total reduction of $4.2 billion,just over 40% of the total decline. Over 90%,occurred in just 3 RDAs: San Jose ($2.9 billion),Milpitas ($661 million), and Santa Clara ($342million). The other RDA’s with reductionswere Campbell ($3.2 million), Los Gatos ($11.9million), Morgan Hill ($62.6 million), MountainView ($288 million), and Sunnyvale ($12.1million).

www.scc-assessor.org 13

Questions?We have answers.

Go towww.scc-assessor.orgfor more information 2004-2005 Properties with

Temporary Declines, Property Type(Values in Billions)

Number of Values Percent ofProperty Type Properties Declined* Decline**

Residential 23,253 $1.80 10.55%Apartments 234 0.30 18.53Commercial & Industrial 809 5.87 46.97Office 255 2.18 45.34Retail and Hotels 179 0.44 28.19Agricultural 13 0.01 40.94Total 24,743 $10.60 28.19%

* Represents decline in assessed value had the market valueexceeded the proposition 13 protected factored base year value

**Percentages based on non-rounded values

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0% Citi

es

40%

6%

60%

94%

Percent of declines by Value

Percent of Declines by Parcel

Property Declines:RDA vs. City by

Value and Parcel Count

Red

evel

opm

ent A

genc

ies

14 www.scc-assessor.org

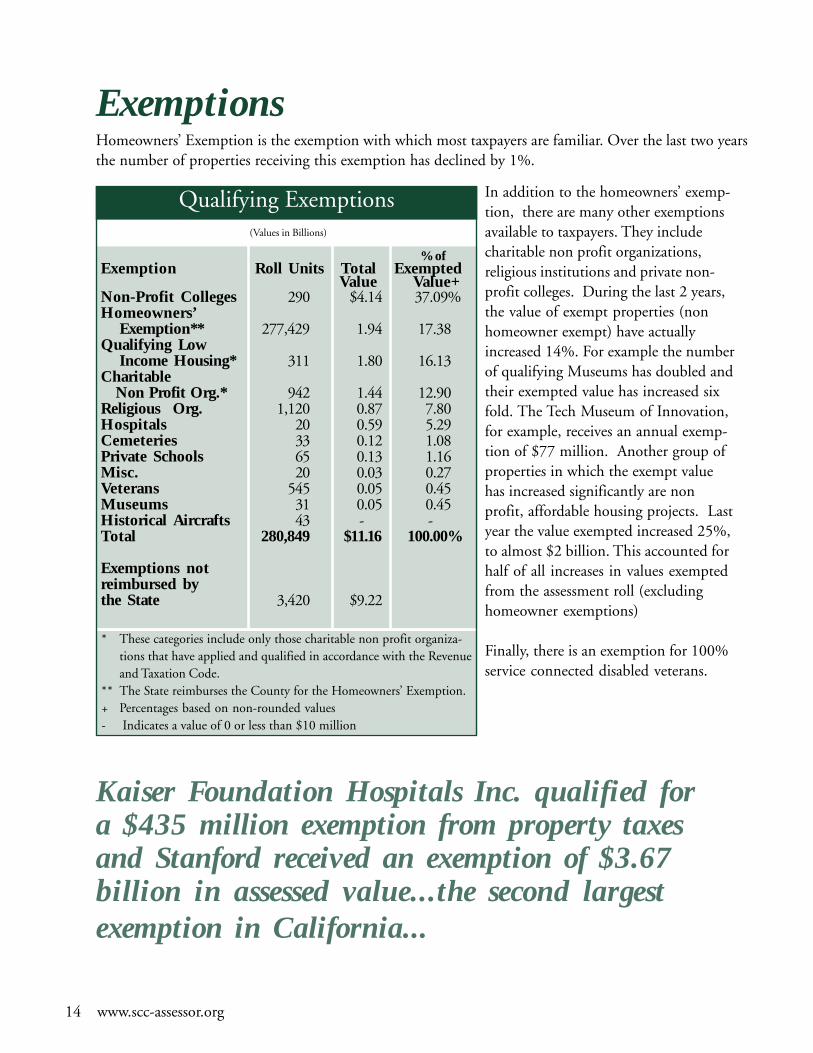

Kaiser Foundation Hospitals Inc. qualified fora $435 million exemption from property taxesand Stanford received an exemption of $3.67billion in assessed value...the second largestexemption in California...

Qualifying Exemptions

% ofExemption Roll Units Total Exempted

Value Value+Non-Profit Colleges 290 $4.14 37.09%Homeowners’ Exemption** 277,429 1.94 17.38Qualifying Low Income Housing* 311 1.80 16.13Charitable Non Profit Org.* 942 1.44 12.90Religious Org. 1,120 0.87 7.80Hospitals 20 0.59 5.29Cemeteries 33 0.12 1.08Private Schools 65 0.13 1.16Misc. 20 0.03 0.27Veterans 545 0.05 0.45Museums 31 0.05 0.45Historical Aircrafts 43 - -Total 280,849 $11.16 100.00%

Exemptions notreimbursed bythe State 3,420 $9.22

(Values in Billions)

* These categories include only those charitable non profit organiza-tions that have applied and qualified in accordance with the Revenueand Taxation Code.

** The State reimburses the County for the Homeowners’ Exemption.+ Percentages based on non-rounded values- Indicates a value of 0 or less than $10 million

In addition to the homeowners’ exemp-tion, there are many other exemptionsavailable to taxpayers. They includecharitable non profit organizations,religious institutions and private non-profit colleges. During the last 2 years,the value of exempt properties (nonhomeowner exempt) have actuallyincreased 14%. For example the numberof qualifying Museums has doubled andtheir exempted value has increased sixfold. The Tech Museum of Innovation,for example, receives an annual exemp-tion of $77 million. Another group ofproperties in which the exempt valuehas increased significantly are nonprofit, affordable housing projects. Lastyear the value exempted increased 25%,to almost $2 billion. This accounted forhalf of all increases in values exemptedfrom the assessment roll (excludinghomeowner exemptions)

Finally, there is an exemption for 100%service connected disabled veterans.

ExemptionsHomeowners’ Exemption is the exemption with which most taxpayers are familiar. Over the last two yearsthe number of properties receiving this exemption has declined by 1%.

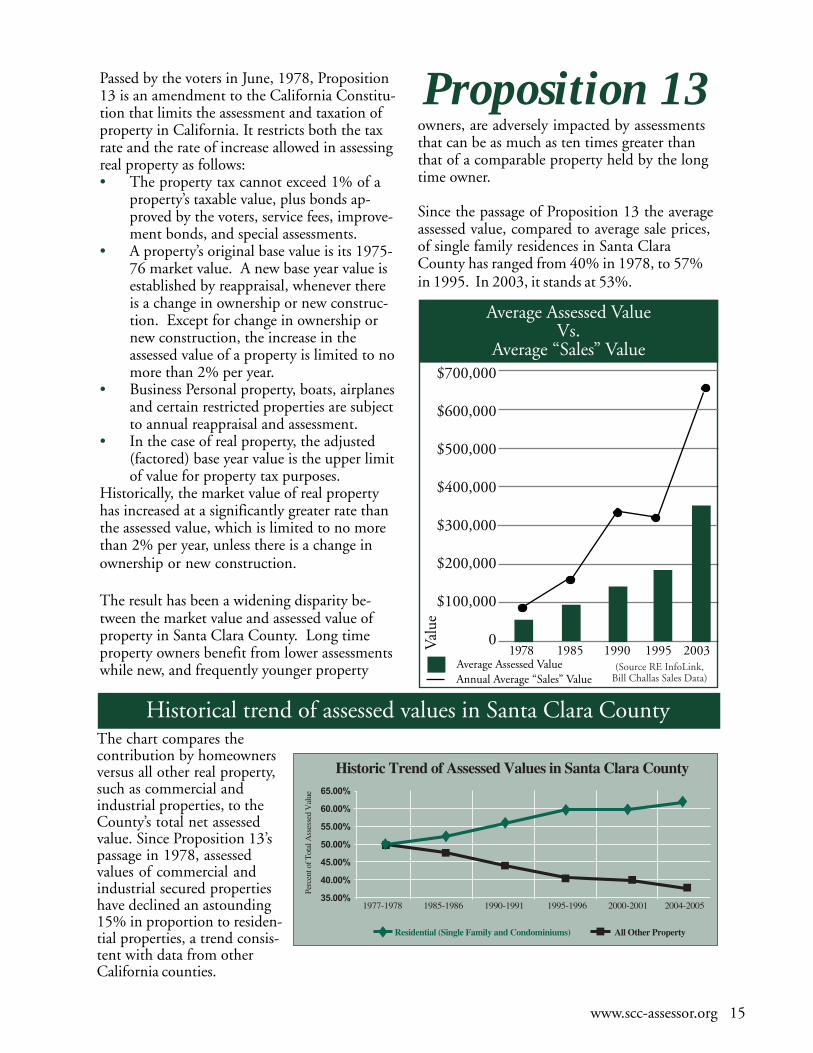

Passed by the voters in June, 1978, Proposition13 is an amendment to the California Constitu-tion that limits the assessment and taxation ofproperty in California. It restricts both the taxrate and the rate of increase allowed in assessingreal property as follows:• The property tax cannot exceed 1% of a

property’s taxable value, plus bonds ap-proved by the voters, service fees, improve-ment bonds, and special assessments.

• A property’s original base value is its 1975-76 market value. A new base year value isestablished by reappraisal, whenever thereis a change in ownership or new construc-tion. Except for change in ownership ornew construction, the increase in theassessed value of a property is limited to nomore than 2% per year.

• Business Personal property, boats, airplanesand certain restricted properties are subjectto annual reappraisal and assessment.

• In the case of real property, the adjusted(factored) base year value is the upper limitof value for property tax purposes.

Historically, the market value of real propertyhas increased at a significantly greater rate thanthe assessed value, which is limited to no morethan 2% per year, unless there is a change inownership or new construction.

The result has been a widening disparity be-tween the market value and assessed value ofproperty in Santa Clara County. Long timeproperty owners benefit from lower assessmentswhile new, and frequently younger property

owners, are adversely impacted by assessmentsthat can be as much as ten times greater thanthat of a comparable property held by the longtime owner.

Since the passage of Proposition 13 the averageassessed value, compared to average sale prices,of single family residences in Santa ClaraCounty has ranged from 40% in 1978, to 57%in 1995. In 2003, it stands at 53%.

Historical trend of assessed values in Santa Clara CountyThe chart compares thecontribution by homeownersversus all other real property,such as commercial andindustrial properties, to theCounty’s total net assessedvalue. Since Proposition 13’spassage in 1978, assessedvalues of commercial andindustrial secured propertieshave declined an astounding15% in proportion to residen-tial properties, a trend consis-tent with data from otherCalifornia counties.

Proposition 13

www.scc-assessor.org 15

1978 1985 1990 1995 2003

$700,000

$600,000

$500,000

$400,000

$300,000

$200,000

$100,000

0

Average Assessed ValueVs.

Average “Sales” Value

Average Assessed Value

Val

ue

(Source RE InfoLink,Bill Challas Sales Data)Annual Average “Sales” Value

65.00%

60.00%

55.00%

50.00%

45.00%

40.00%

35.00%

Perc

ent o

f Tot

al A

sses

sed

Val

ue

Historic Trend of Assessed Values in Santa Clara County

1977-1978 1985-1986 1990-1991 1995-1996 2000-2001 2004-2005

Residential (Single Family and Condominiums) All Other Property

16 www.scc-assessor.org

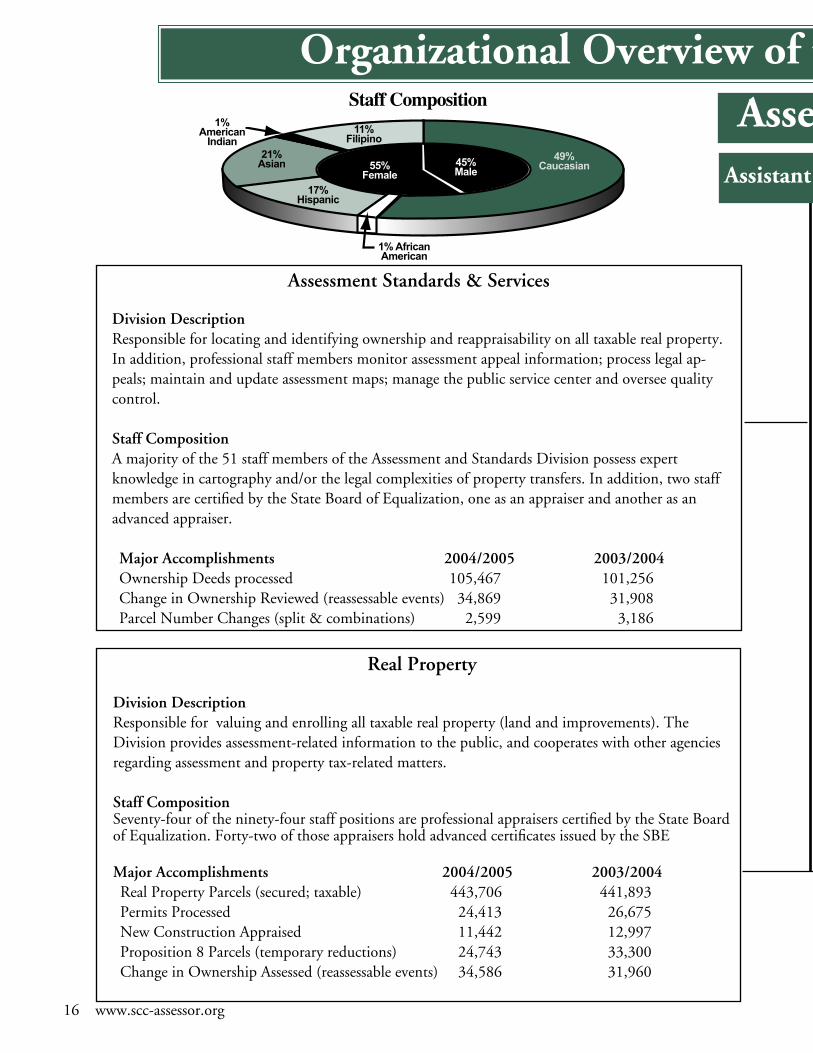

Assessment Standards & Services

Division DescriptionResponsible for locating and identifying ownership and reappraisability on all taxable real property. In addition, professional staff members monitor assessment appeal information; process legal ap-peals; maintain and update assessment maps; manage the public service center and oversee quality control.

Staff CompositionA majority of the 51 staff members of the Assessment and Standards Division possess expert knowledge in cartography and/or the legal complexities of property transfers. In addition, two staff members are certified by the State Board of Equalization, one as an appraiser and another as an advanced appraiser.

Major Accomplishments 2004/2005 2003/2004 Ownership Deeds processed 105,467 101,256 Change in Ownership Reviewed (reassessable events) 34,869 31,908 Parcel Number Changes (split & combinations) 2,599 3,186

Real Property

Division DescriptionResponsible for valuing and enrolling all taxable real property (land and improvements). The Division provides assessment-related information to the public, and cooperates with other agencies regarding assessment and property tax-related matters.

Staff CompositionSeventy-four of the ninety-four staff positions are professional appraisers certified by the State Board of Equalization. Forty-two of those appraisers hold advanced certificates issued by the SBE

Major Accomplishments 2004/2005 2003/2004 Real Property Parcels (secured; taxable) 443,706 441,893 Permits Processed 24,413 26,675 New Construction Appraised 11,442 12,997 Proposition 8 Parcels (temporary reductions) 24,743 33,300 Change in Ownership Assessed (reassessable events) 34,586 31,960

AssessorAssistant Assessor

Organizational Overview of the County Assessor’s Office

1%AmericanIndian

21%Asian

17%Hispanic

1%AfricanAmerican

45%Male

55%Female

����� �����������

49%Caucasian

11%Filipino

www.scc-assessor.org 17

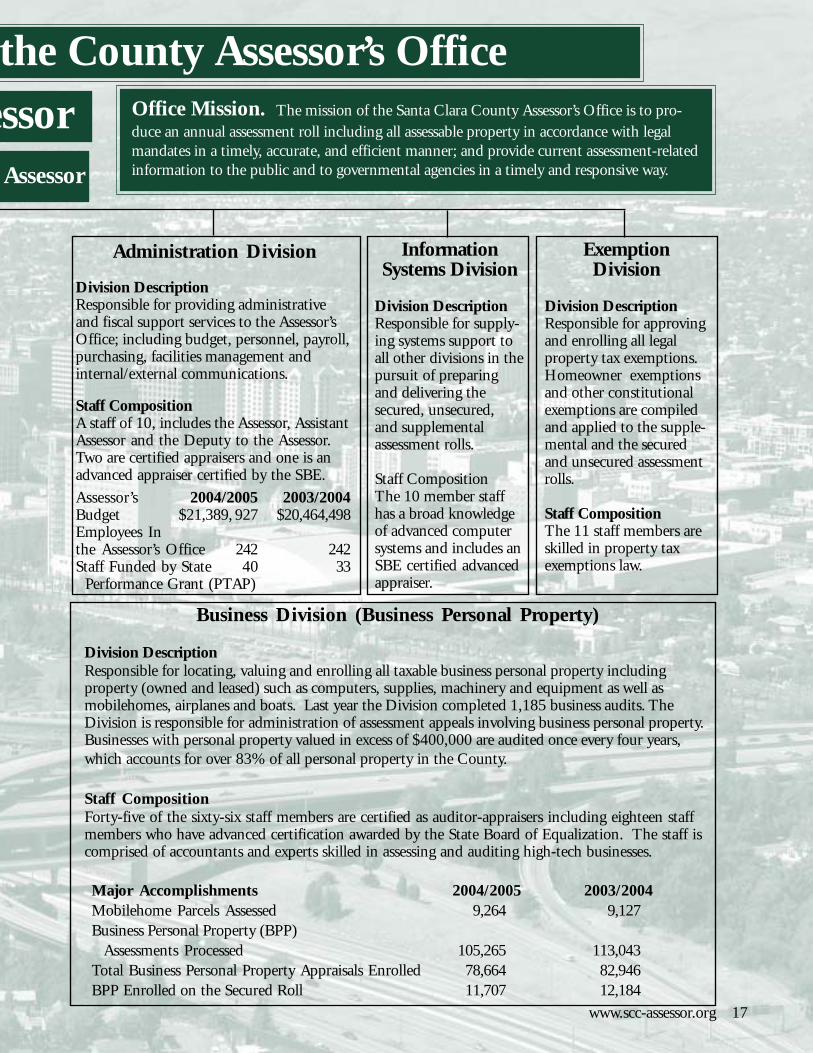

Office Mission. The mission of the Santa Clara County Assessor’s Office is to pro-duce an annual assessment roll including all assessable property in accordance with legalmandates in a timely, accurate, and efficient manner; and provide current assessment-relatedinformation to the public and to governmental agencies in a timely and responsive way.

Business Division (Business Personal Property)

Division DescriptionResponsible for locating, valuing and enrolling all taxable business personal property includingproperty (owned and leased) such as computers, supplies, machinery and equipment as well asmobilehomes, airplanes and boats. Last year the Division completed 1,185 business audits. TheDivision is responsible for administration of assessment appeals involving business personal property.Businesses with personal property valued in excess of $400,000 are audited once every four years,which accounts for over 83% of all personal property in the County.

Staff CompositionForty-five of the sixty-six staff members are certified as auditor-appraisers including eighteen staffmembers who have advanced certification awarded by the State Board of Equalization. The staff iscomprised of accountants and experts skilled in assessing and auditing high-tech businesses.

Major Accomplishments 2004/2005 2003/2004Mobilehome Parcels Assessed 9,264 9,127Business Personal Property (BPP) Assessments Processed 105,265 113,043Total Business Personal Property Appraisals Enrolled 78,664 82,946BPP Enrolled on the Secured Roll 11,707 12,184

Administration Division

Division DescriptionResponsible for providing administrativeand fiscal support services to the Assessor’sOffice; including budget, personnel, payroll,purchasing, facilities management andinternal/external communications.

Staff CompositionA staff of 10, includes the Assessor, AssistantAssessor and the Deputy to the Assessor.Two are certified appraisers and one is anadvanced appraiser certified by the SBE.

Assessor’s 2004/2005 2003/2004Budget $21,389, 927 $20,464,498Employees Inthe Assessor’s Office 242 242Staff Funded by State 40 33 Performance Grant (PTAP)

InformationSystems Division

Division DescriptionResponsible for supply-ing systems support toall other divisions in thepursuit of preparingand delivering thesecured, unsecured,and supplementalassessment rolls.

Staff CompositionThe 10 member staffhas a broad knowledgeof advanced computersystems and includes anSBE certified advancedappraiser.

ExemptionDivision

Division DescriptionResponsible for approvingand enrolling all legalproperty tax exemptions.Homeowner exemptionsand other constitutionalexemptions are compiledand applied to the supple-mental and the securedand unsecured assessmentrolls.

Staff CompositionThe 11 staff members areskilled in property taxexemptions law.

essorAssessor

the County Assessor’s Office

18 www.scc-assessor.org

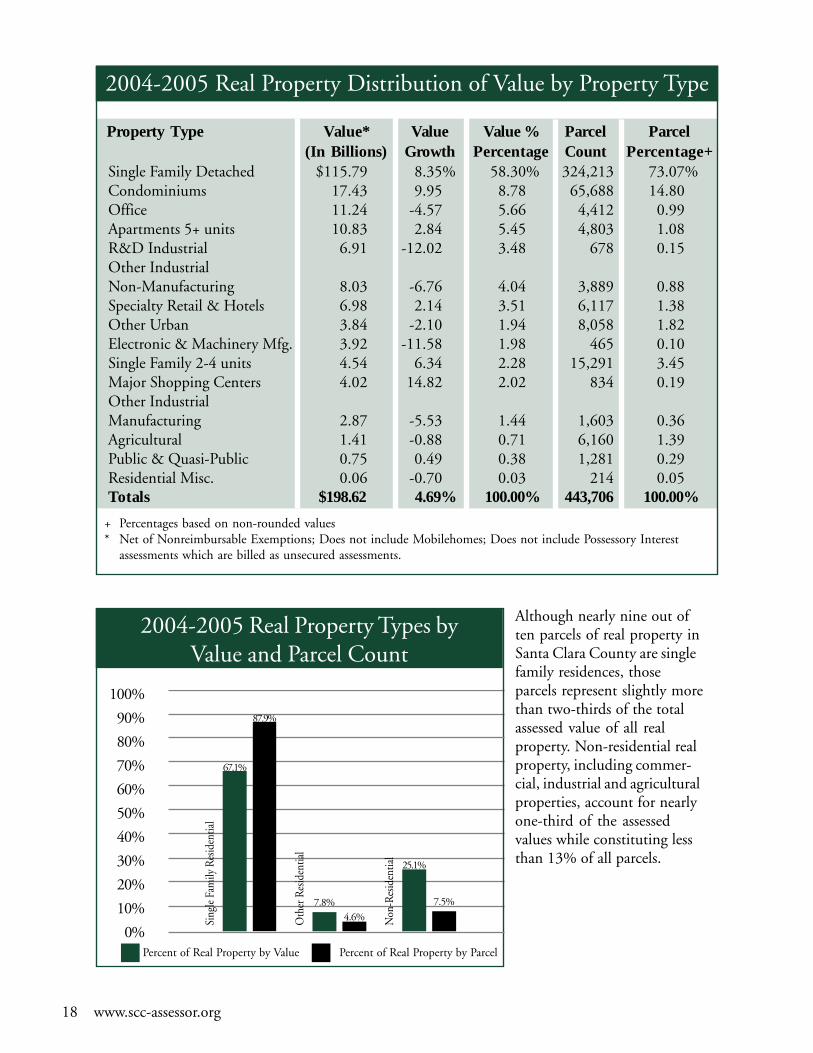

Although nearly nine out often parcels of real property inSanta Clara County are singlefamily residences, thoseparcels represent slightly morethan two-thirds of the totalassessed value of all realproperty. Non-residential realproperty, including commer-cial, industrial and agriculturalproperties, account for nearlyone-third of the assessedvalues while constituting lessthan 13% of all parcels.

+ Percentages based on non-rounded values* Net of Nonreimbursable Exemptions; Does not include Mobilehomes; Does not include Possessory Interest

assessments which are billed as unsecured assessments.

2004-2005 Real Property Distribution of Value by Property Type

Single Family Detached $115.79 8.35% 58.30% 324,213 73.07%Condominiums 17.43 9.95 8.78 65,688 14.80Office 11.24 -4.57 5.66 4,412 0.99Apartments 5+ units 10.83 2.84 5.45 4,803 1.08R&D Industrial 6.91 -12.02 3.48 678 0.15Other IndustrialNon-Manufacturing 8.03 -6.76 4.04 3,889 0.88Specialty Retail & Hotels 6.98 2.14 3.51 6,117 1.38Other Urban 3.84 -2.10 1.94 8,058 1.82Electronic & Machinery Mfg. 3.92 -11.58 1.98 465 0.10Single Family 2-4 units 4.54 6.34 2.28 15,291 3.45Major Shopping Centers 4.02 14.82 2.02 834 0.19Other IndustrialManufacturing 2.87 -5.53 1.44 1,603 0.36Agricultural 1.41 -0.88 0.71 6,160 1.39Public & Quasi-Public 0.75 0.49 0.38 1,281 0.29Residential Misc. 0.06 -0.70 0.03 214 0.05Totals $198.62 4.69% 100.00% 443,706 100.00%

Property Type Value* Value Value % Parcel Parcel(In Billions) Growth Percentage Count Percentage+

100%

90%

80%

70%

60%

50%

40%

30%

20%

10%

0%

Sing

le F

amily

Res

iden

tial

Oth

er R

esid

entia

l

Non

-Res

iden

tial

67.1%

87.9%

7.8%4.6%

25.1%

7.5%

2004-2005 Real Property Types byValue and Parcel Count

Percent of Real Property by Value Percent of Real Property by Parcel

www.scc-assessor.org 19

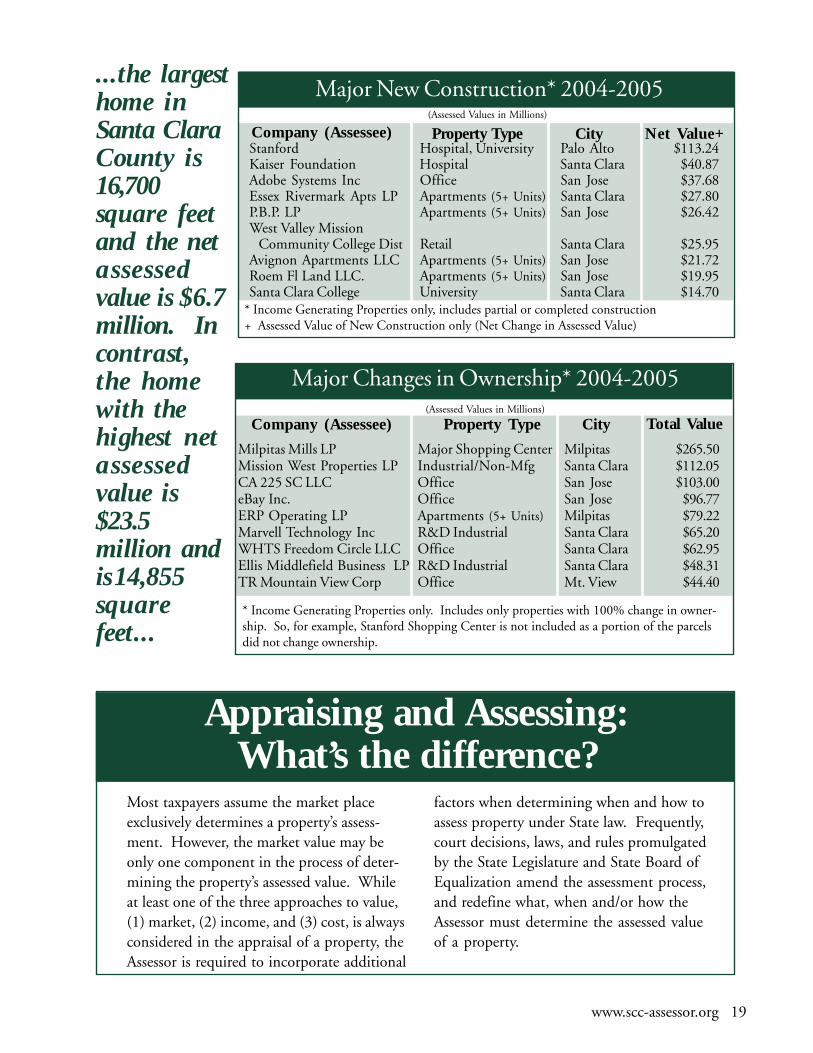

...the largesthome inSanta ClaraCounty is16,700square feetand the netasse s sedvalue is $6.7million. Incontrast,the homewith thehighest netasse s sedvalue is$23.5million andis 14,855squarefeet...

Appraising and Assessing:What’s the difference?

Most taxpayers assume the market placeexclusively determines a property’s assess-ment. However, the market value may beonly one component in the process of deter-mining the property’s assessed value. Whileat least one of the three approaches to value,(1) market, (2) income, and (3) cost, is alwaysconsidered in the appraisal of a property, theAssessor is required to incorporate additional

factors when determining when and how toassess property under State law. Frequently,court decisions, laws, and rules promulgatedby the State Legislature and State Board ofEqualization amend the assessment process,and redefine what, when and/or how theAssessor must determine the assessed valueof a property.

Milpitas Mills LP Major Shopping Center Milpitas $265.50Mission West Properties LP Industrial/Non-Mfg Santa Clara $112.05CA 225 SC LLC Office San Jose $103.00eBay Inc. Office San Jose $96.77ERP Operating LP Apartments (5+ Units) Milpitas $79.22Marvell Technology Inc R&D Industrial Santa Clara $65.20WHTS Freedom Circle LLC Office Santa Clara $62.95Ellis Middlefield Business LP R&D Industrial Santa Clara $48.31TR Mountain View Corp Office Mt. View $44.40

Major New Construction* 2004-2005

Company (Assessee)

* Income Generating Properties only, includes partial or completed construction+ Assessed Value of New Construction only (Net Change in Assessed Value)

Net Value+CityProperty TypeStanford Hospital, University Palo Alto $113.24Kaiser Foundation Hospital Santa Clara $40.87Adobe Systems Inc Office San Jose $37.68Essex Rivermark Apts LP Apartments (5+ Units) Santa Clara $27.80P.B.P. LP Apartments (5+ Units) San Jose $26.42West Valley Mission Community College Dist Retail Santa Clara $25.95Avignon Apartments LLC Apartments (5+ Units) San Jose $21.72Roem Fl Land LLC. Apartments (5+ Units) San Jose $19.95Santa Clara College University Santa Clara $14.70

Company (Assessee)

* Income Generating Properties only. Includes only properties with 100% change in owner-ship. So, for example, Stanford Shopping Center is not included as a portion of the parcelsdid not change ownership.

Total ValueCityProperty Type(Assessed Values in Millions)

Major Changes in Ownership* 2004-2005

(Assessed Values in Millions)

20 www.scc-assessor.org

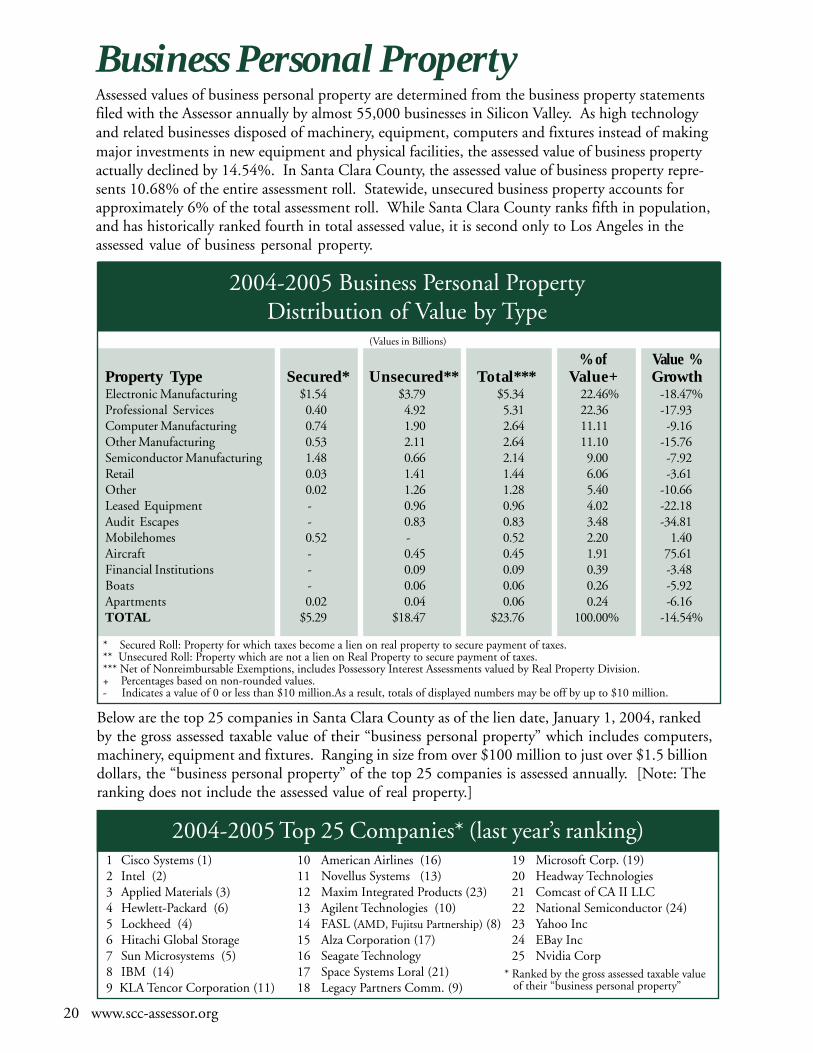

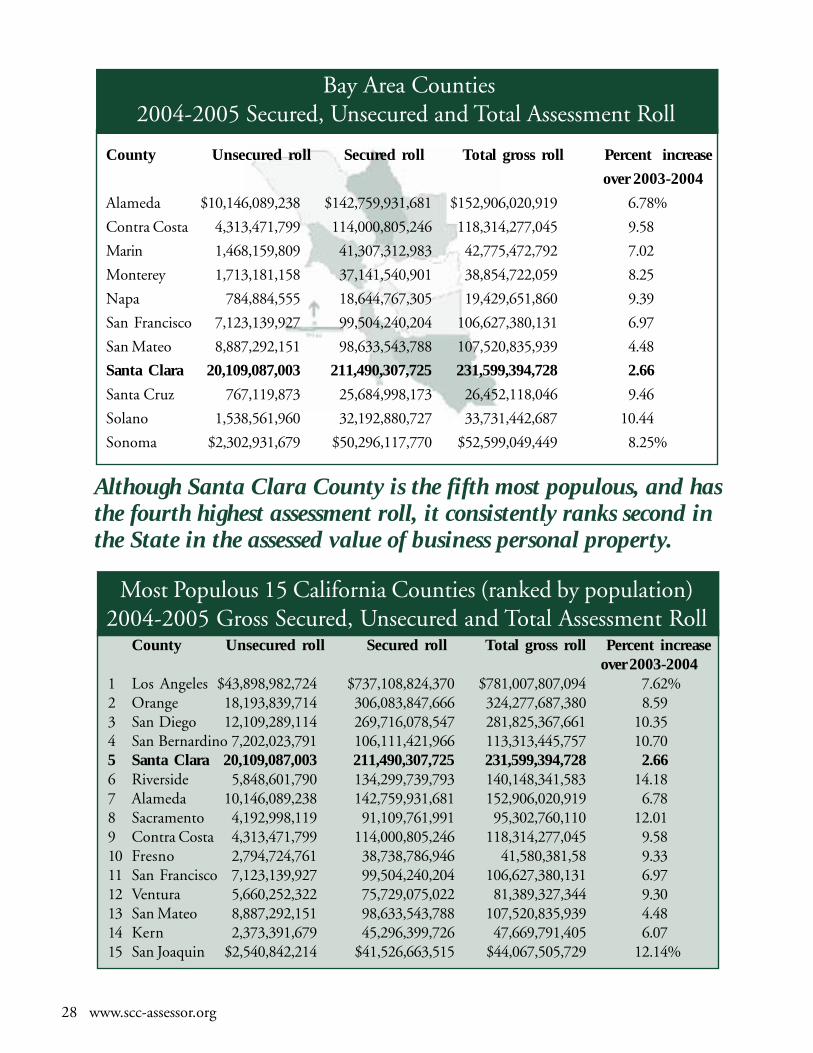

Assessed values of business personal property are determined from the business property statementsfiled with the Assessor annually by almost 55,000 businesses in Silicon Valley. As high technologyand related businesses disposed of machinery, equipment, computers and fixtures instead of makingmajor investments in new equipment and physical facilities, the assessed value of business propertyactually declined by 14.54%. In Santa Clara County, the assessed value of business property repre-sents 10.68% of the entire assessment roll. Statewide, unsecured business property accounts forapproximately 6% of the total assessment roll. While Santa Clara County ranks fifth in population,and has historically ranked fourth in total assessed value, it is second only to Los Angeles in theassessed value of business personal property.

Business Personal Property

Below are the top 25 companies in Santa Clara County as of the lien date, January 1, 2004, rankedby the gross assessed taxable value of their “business personal property” which includes computers,machinery, equipment and fixtures. Ranging in size from over $100 million to just over $1.5 billiondollars, the “business personal property” of the top 25 companies is assessed annually. [Note: Theranking does not include the assessed value of real property.]

1 Cisco Systems (1)2 Intel (2)3 Applied Materials (3)4 Hewlett-Packard (6)5 Lockheed (4)6 Hitachi Global Storage7 Sun Microsystems (5)8 IBM (14)9 KLA Tencor Corporation (11)

10 American Airlines (16)11 Novellus Systems (13)12 Maxim Integrated Products (23)13 Agilent Technologies (10)14 FASL (AMD, Fujitsu Partnership) (8)15 Alza Corporation (17)16 Seagate Technology17 Space Systems Loral (21)18 Legacy Partners Comm. (9)

19 Microsoft Corp. (19)20 Headway Technologies21 Comcast of CA II LLC22 National Semiconductor (24)23 Yahoo Inc24 EBay Inc25 Nvidia Corp

2004-2005 Top 25 Companies* (last year’s ranking)

* Ranked by the gross assessed taxable value of their “business personal property”

2004-2005 Business Personal PropertyDistribution of Value by Type

* Secured Roll: Property for which taxes become a lien on real property to secure payment of taxes.** Unsecured Roll: Property which are not a lien on Real Property to secure payment of taxes.*** Net of Nonreimbursable Exemptions, includes Possessory Interest Assessments valued by Real Property Division.+ Percentages based on non-rounded values.- Indicates a value of 0 or less than $10 million.As a result, totals of displayed numbers may be off by up to $10 million.

% of Value %Property Type Secured* Unsecured** Total*** Value+ GrowthElectronic Manufacturing $1.54 $3.79 $5.34 22.46% -18.47%Professional Services 0.40 4.92 5.31 22.36 -17.93Computer Manufacturing 0.74 1.90 2.64 11.11 -9.16Other Manufacturing 0.53 2.11 2.64 11.10 -15.76Semiconductor Manufacturing 1.48 0.66 2.14 9.00 -7.92Retail 0.03 1.41 1.44 6.06 -3.61Other 0.02 1.26 1.28 5.40 -10.66Leased Equipment - 0.96 0.96 4.02 -22.18Audit Escapes - 0.83 0.83 3.48 -34.81Mobilehomes 0.52 - 0.52 2.20 1.40Aircraft - 0.45 0.45 1.91 75.61Financial Institutions - 0.09 0.09 0.39 -3.48Boats - 0.06 0.06 0.26 -5.92Apartments 0.02 0.04 0.06 0.24 -6.16TOTAL $5.29 $18.47 $23.76 100.00% -14.54%

(Values in Billions)

Q. My house was destroyed by fire, is property taxrelief available until it’s rebuilt?

A. Yes, assuming you qualify. Owners of realproperty who incur significant damages (atleast ten-thousand dollars or more) as theresult of a natural disaster, such as a fire, floodor earthquake, can file for temporary propertytax relief (reassessment) with the Assessor’sOffice. Applicants must file a written applica-tion within 60 days of the disaster. Items suchas home furnishings, personal effects andbusiness inventories are not assessable realproperty.

Q. What can I do if I think my assessment is toohigh? (i.e., higher than market value)

A. Request an informal review by submitting aone-page “assessment review” form which isavailable on-line for printing or downloading atwww.scc-assessor.org. Any supporting data

(appraisals, comparables, multiple listings, etc.)will be helpful in expediting a reduction if anadjustment is warranted. To file a formal appealwith the Assessment Appeals Board, contactthe Clerk of the Board at www.sccgov.org or(408) 299-5001.

Q. How many properties are still protected byProposition 13, passed by the voters in 1978?

A. All properties in Santa Clara County, andthroughout California, receive the full benefitof Proposition 13. Whether a property waspurchased last year or in 1975, every propertyowner receives the same protections andbenefits. The base year value is established atthe time of purchase or new construction, andincreases in the assessed value are limited to aninflation factor of no more than 2% annually.

Frequently Asked Questions

Do you e-file?e-filing is a new program that

allows taxpayers to confiden-

tially file their Business Prop-

erty Statement on-line, quickly

and easily. Businesses selected

to participate in this program

will be notified in January,

2005. See the Assessor’s

website for moreinformation

www.scc-assessor.org 21

22 www.scc-assessor.org

Sing

le F

amil

yM

obil

ehom

eM

ulti

fam

ily

Indu

stri

al &

Ret

ail

Off

ice

Agr

icul

tura

l/T

otal

Gro

ssO

ther

Hom

eow

ner

Hou

sin

g H

ousi

ngM

anuf

actu

ring

Mis

c.Se

cure

d*E

xem

pti

ons

Exe

mpt

ion

Cam

pbel

lC

ity

AV$2

,574

.46

$2.8

5$5

16.9

7$1

60.8

4$2

78.2

2$2

25.6

8$4

7.11

$3,8

67.9

7$6

1.85

$43.

84A

PN

8,91

048

749

130

185

138

153

10,3

1368

6,16

9R

DA

AV$7

4.89

$0.0

8$6

7.44

$101

.65

$56.

88$2

15.2

3$7

.16

$530

.74

$7.4

2$0

.81

AP

N21

41

2016

868

7424

569

2211

6To

tal

AV$2

,649

.35

$2.9

3$5

84.4

0$2

62.4

8$3

35.1

0$4

40.9

1$5

4.26

$4,3

98.7

1$6

9.27

$44.

65A

PN

9,12

449

769

298

253

212

177

10,8

8290

6,28

5C

uper

tino Cit

yAV

$6,2

81.2

9$0

.00

$675

.99

$850

.31

$305

.70

$836

.15

$107

.38

$9,1

37.5

0$8

0.68

$74.

67A

PN

14,2

410

577

7413

819

324

215

,465

6510

,670

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$95.

35$0

.00

$7.0

1$1

02.3

6$0

.00

$0.0

0A

PN

00

00

140

216

00

Tota

lAV

$6,2

81.2

9$0

.00

$675

.99

$850

.31

$401

.05

$836

.15

$114

.39

$9,2

39.8

6$8

0.68

$74.

67A

PN

14,2

410

577

7415

219

324

415

,481

6510

,670

Gilr

oyC

ity

AV$2

,961

.88

$6.0

1$2

06.4

6$2

90.0

9$4

53.4

2$7

4.71

$334

.58

$4,4

63.5

5$1

36.4

0$4

3.11

AP

N9,

638

108

521

192

308

104

720

11,5

9185

6,16

4R

DA

AV$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0A

PN

00

00

00

00

00

Tota

lAV

$2,9

61.8

8$6

.01

$206

.46

$290

.09

$453

.42

$74.

71$3

34.5

8$4

,463

.55

$136

.40

$43.

11A

PN

9,63

810

852

119

230

810

472

011

,591

856,

164

Los

Alt

os Cit

yAV

$5,7

27.0

5$0

.00

$79.

14$5

.72

$173

.53

$241

.12

$68.

50$6

,368

.47

$73.

41$5

4.93

AP

N9,

863

097

3419

928

815

110

,632

597,

853

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

AP

N0

00

00

00

00

0To

tal

AV$5

,727

.05

$0.0

0$7

9.14

$5.7

2$1

73.5

3$2

41.1

2$6

8.50

$6,3

68.4

7$7

3.41

$54.

93A

PN

9,86

30

9734

199

288

151

10,6

3259

7,85

3Lo

s A

ltos

Hill

sC

ity

AV$3

,316

.88

$0.1

0$0

.00

$1.5

9$0

.00

$0.0

0$1

20.7

1$3

,458

.03

$18.

74$1

5.60

AP

N2,

819

30

160

020

83,

046

142,

230

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

AP

N0

00

00

00

00

0To

tal

AV$3

,316

.88

$0.1

0$0

.00

$1.5

9$0

.00

$0.0

0$1

20.7

1$3

,458

.03

$18.

74$1

5.60

AP

N2,

819

30

160

020

83,

046

142,

230

Los

Gat

os Cit

yAV

$4,0

38.9

1$1

.73

$219

.81

$81.

54$1

27.8

8$2

25.7

0$1

98.6

7$5

,025

.81

$131

.58

$41.

32A

PN

8,01

139

368

5985

292

320

9,17

444

5,90

5R

DA

AV$4

55.1

7$0

.00

$67.

86$4

.78

$158

.32

$61.

97$1

2.56

$767

.72

$7.0

6$3

.95

AP

N87

60

111

814

960

471,

251

1456

4To

tal

AV$4

,494

.09

$1.7

3$2

87.6

7$8

6.32

$286

.20

$287

.67

$211

.23

$5,7

93.5

4$1

38.6

3$4

5.27

AP

N8,

887

3947

967

234

352

367

10,4

2558

6,46

9M

ilpit

as Cit

yAV

$3,2

24.4

1$1

8.47

$275

.08

$1,0

50.5

9$2

29.5

4$9

4.93

$102

.82

$5,0

43.2

0$4

7.38

$55.

47A

PN

11,4

6630

134

219

764

6115

412

,585

587,

929

RD

AAV

$1,0

09.8

1$0

.00

$92.

62$1

,061

.62

$646

.56

$75.

53$6

8.28

$3,0

12.2

5$5

7.83

$12.

87A

PN

2,56

50

820

714

230

703,

022

161,

839

Tota

lAV

$4,2

34.2

2$1

8.47

$367

.70

$2,1

12.2

2$8

76.1

0$1

70.4

6$1

71.1

0$8

,055

.46

$105

.21

$68.

34A

PN

14,0

3130

135

040

420

691

224

15,6

0774

9,76

8M

onte

Ser

eno

Cit

yAV

$1,0

52.5

9$0

.00

$0.0

0$0

.54

$0.0

0$0

.00

$15.

54$1

,069

.35

$0.6

8$6

.60

AP

N1,

209

00

20

041

1,25

21

944

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

AP

N0

00

00

00

00

0To

tal

AV$1

,052

.59

$0.0

0$0

.00

$0.5

4$0

.00

$0.0

0$1

5.54

$1,0

69.3

5$0

.68

$6.6

0A

PN

1,20

90

02

00

411,

252

194

4

2004

-200

5 G

ross

Sec

ured

Ass

esse

d V

alue

(AV

) an

d N

umbe

r of

Par

cels

(A

PN)

by C

ity,

Red

evel

opm

ent A

genc

y (R

DA

) and

Maj

or P

rope

rty

Type

(Val

ue in

Mill

ions

)

www.scc-assessor.org 23

Mor

gan

Hill

Cit

yAV

$2,3

89.5

5$9

.97

$22.

96$2

.23

$39.

90$2

4.50

$108

.38

$2,6

17.2

5$1

9.77

$31.

72A

PN

5,89

613

022

321

528

06,

357

224,

381

RD

AA

V$8

90.9

7$9

.97

$167

.24

$528

.17

$195

.85

$71.

36$1

18.9

4$2

,067

.54

$85.

05$1

3.25

AP

N2,

827

241

282

223

173

7027

94,

095

371,

891

Tota

lAV

$3,2

80.5

2$1

9.94

$190

.19

$530

.40

$235

.75

$95.

87$2

27.3

2$4

,684

.79

$104

.82

$44.

96A

PN

8,72

337

130

422

619

475

559

10,4

5259

6,27

2M

t. V

iew Cit

yAV

$4,8

46.9

0$1

9.47

$1,4

29.8

2$1

,152

.74

$535

.11

$524

.70

$109

.91

$8,7

62.2

1$1

43.5

7$7

4.18

AP

N14

,671

359

1,53

837

638

625

420

517

,789

7710

,591

RD

AAV

$62.

63$1

0.20

$23.

69$6

13.0

6$6

8.30

$362

.05

$31.

77$1

,198

.24

$26.

53$1

.38

AP

N13

716

519

6577

6716

546

219

7To

tal

AV$4

,909

.54

$29.

68$1

,453

.51

$1,7

65.8

0$6

03.4

1$8

86.7

4$1

41.6

8$9

,960

.45

$170

.10

$75.

56A

PN

14,8

0852

41,

557

441

463

321

221

18,3

3579

10,7

88Pa

lo A

lto Cit

yAV

$8,3

29.8

4$0

.06

$741

.00

$1,7

47.5

5$9

72.1

7$1

,559

.30

$266

.59

$15,

018.

54$1

,402

.04

$88.

09A

PN

17,2

017

891

235

480

442

346

19,6

0220

012

,587

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

AP

N0

00

00

00

00

0To

tal

AV$8

,329

.84

$0.0

6$7

41.0

0$1

,747

.55

$972

.17

$1,5

59.3

0$2

66.5

9$1

5,01

8.54

$1,4

02.0

4$8

8.09

AP

N17

,201

789

123

548

044

234

619

,602

200

12,5

87Sa

n Jo

se Cit

yAV

$56,

430.

60$2

55.8

3$5

,971

.70

$3,5

49.7

7$3

,902

.85

$1,7

04.1

0$1

,745

.12

$75,

716.

58$2

,156

.60

$947

.29

AP

N19

5,72

24,

971

10,0

031,

646

2,82

51,

380

3,59

822

0,14

51,

090

135,

016

RD

AA

V$7

59.9

3$4

1.28

$909

.09

$5,6

75.0

3$8

32.6

6$2

, 367

.64

$484

.13

$11,

359.

09$2

89.3

2$1

3.71

AP

N2,

310

785

108

939

368

239

327

5,07

646

1,95

9To

tal

AV$5

7,19

0.54

$297

.11

$6,8

80.7

9$9

,224

.80

$4,7

35.5

2$4

,071

.74

$2,2

29.2

3$8

7,07

5.66

$2,4

45.9

2$9

61.0

0A

PN

198,

032

5,75

610

,111

2,58

53,

193

1,61

93,

925

225,

221

1,13

613

6,97

5Sa

nta

Cla

raC

ity

AV$5

,642

.83

$0.1

2$1

,679

.69

$4,4

48.0

8$7

60.5

1$1

,006

.18

$202

.64

$14,

543.

77$8

03.7

1$1

08.5

8A

PN

22,3

941

1,99

793

547

723

023

126

,265

173

15,5

12R

DA

AV$0

.00

$0.0

0$1

6.95

$143

.34

$182

.86

$975

.36

$28.

86$1

,359

.70

$12.

34$0

.00

AP

N0

01

1822

7912

132

40

Tota

lAV

$5,6

42.8

3$0

.12

$1,6

96.6

4$4

,591

.41

$943

.38

$1,9

81.5

3$2

31.5

0$1

5,90

3.47

$816

.05

$108

.58

AP

N22

,394

11,

998

953

499

309

243

26,3

9717

715

,512

Sara

toga C

ity

AV$7

,062

.16

$0.0

5$6

.39

$18.

67$7

9.92

$84.

69$1

02.0

1$7

,427

.65

$73.

75$5

6.99

AP

N10

,390

123

4473

8534

010

,956

518,

146

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

AP

N0

00

00

00

00

0To

tal

AV$7

,062

.16

$0.0

5$6

.39

$18.

67$7

9.92

$84.

69$1

02.0

1$7

,427

.65

$73.

75$5

6.99

AP

N10

,390

123

4473

8534

010

,956

518,

146

Sunn

yval

eC

ity

AV$7

,426

.24

$145

.71

$2,1

06.2

0$4

,157

.20

$772

.23

$642

.96

$241

.50

$15,

626.

67$1

34.6

2$1

40.1

2A

PN

25,2

772,

057

2,07

570

436

519

126

530

,934

101

20,0

21R

DA

AV$6

8.43

$0.0

0$3

0.22

$0.0

0$1

17.3

1$1

35.3

7$2

.71

$366

.40

$12.

35$0

.96

AP

N23

80

340

7653

340

43

137

Tota

lAV

$7,4

94.6

7$1

45.7

1$2

,136

.42

$4,1

57.2

0$8

89.5

4$7

78.3

4$2

44.2

1$1

5,99

3.06

$146

.98

$141

.09

AP

N25

,515

2,05

72,

109

704

441

244

268

31,3

3810

420

,158

Uni

ncor

pora

ted

Cit

yAV

$8,6

05.7

1$1

.13

$139

.60

$128

.43

$86.

27$4

9.25

$1,7

64.3

2$1

2,57

8.38

$1,8

03.7

0$1

16.2

1A

PN

23,0

2647

522

360

256

777,

461

31,7

4921

416

,607

RD

AAV

$0.0

0$0

.00

$0.0

0$0

.00

$0.0

0$0

.00

$1.3

2$1

.32

$0.0

0$0

.00

AP

N0

00

00

04

40

0To

tal

AV$8

,605

.71

$1.1

3$1

39.6

0$1

28.4

3$8

6.27

$49.

25$1

,765

.64

$12,

579.

70$1

,803

.70

$116

.21

AP

N23

,026

4752

236

025

677

7,46

531

,753

214

16,6

07Sa

nta

Cla

ra C

ount

yC

ity

AV$1

29,9

11.3

1$4

61.5

2$1

4,07

0.79

$17,

645.

87$8

,717

.24

$7,2

93.9

5$5

,535

.77

$190

,724

.95

$7,0

88.4

8$1

,898

.73

AP

N38

0,73

48,

072

19,7

255,

007

5,86

23,

740

14,7

1543

7,85

52,

322

270,

725

RD

AAV

$3,3

21.8

5$6

1.53

$1,3

75.1

1$8

,127

.63

$2,3

54.1

0$4

,264

.51

$762

.72

$20,

765.

36$4

97.9

0$4

6.93

AP

N9,

167

1,19

258

31,

628

1,08

967

278

415

,115

144

6,70

3To

tal

AV$1

33,2

33.1

7$5

23.0

5$1

5,44

5.90

$25,

773.

51$1

1,07

1.34

$11,

558.

46$6

,298

.49

$211

,490

.31

$7,5

86.3

8$1

,945

.66

AP

N38

9,90

19,

264

20,3

086,

635

6,95

14,

412

15,4

9945

2,97

02,

466

277,

428

* In

clud

es O

ther

Exe

mpt

ions

, Exc

lude

s H

omeo

wne

r E

xem

ptio

n

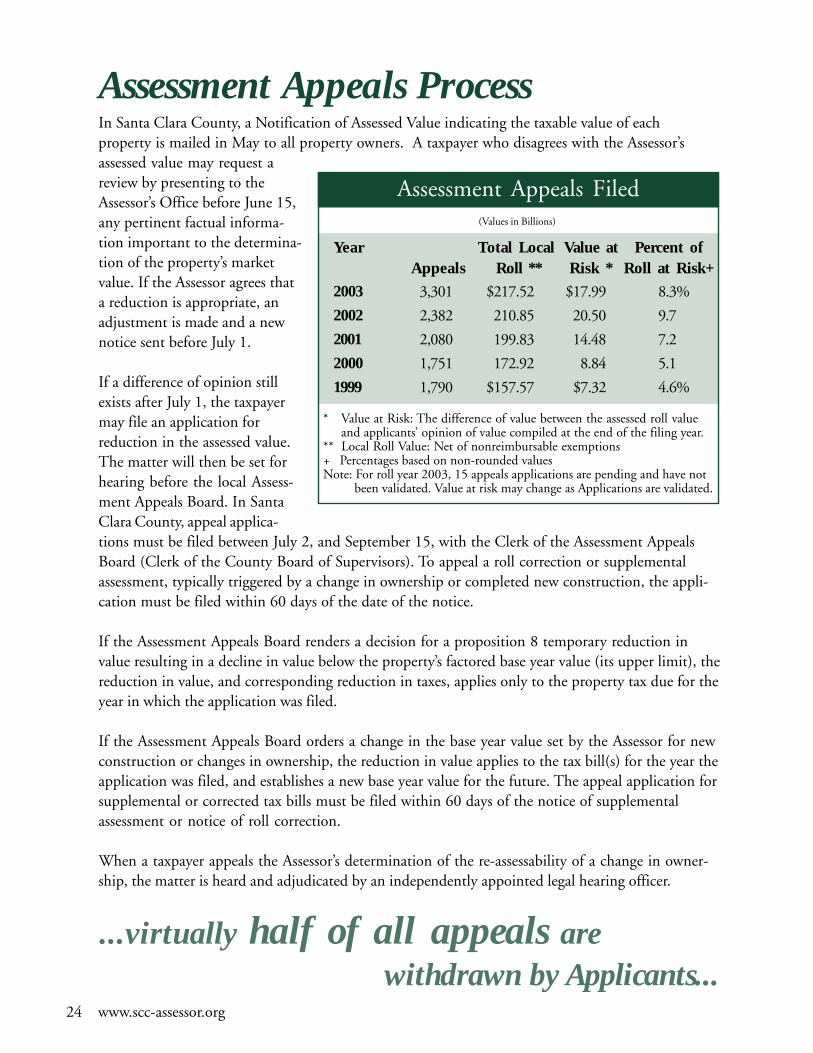

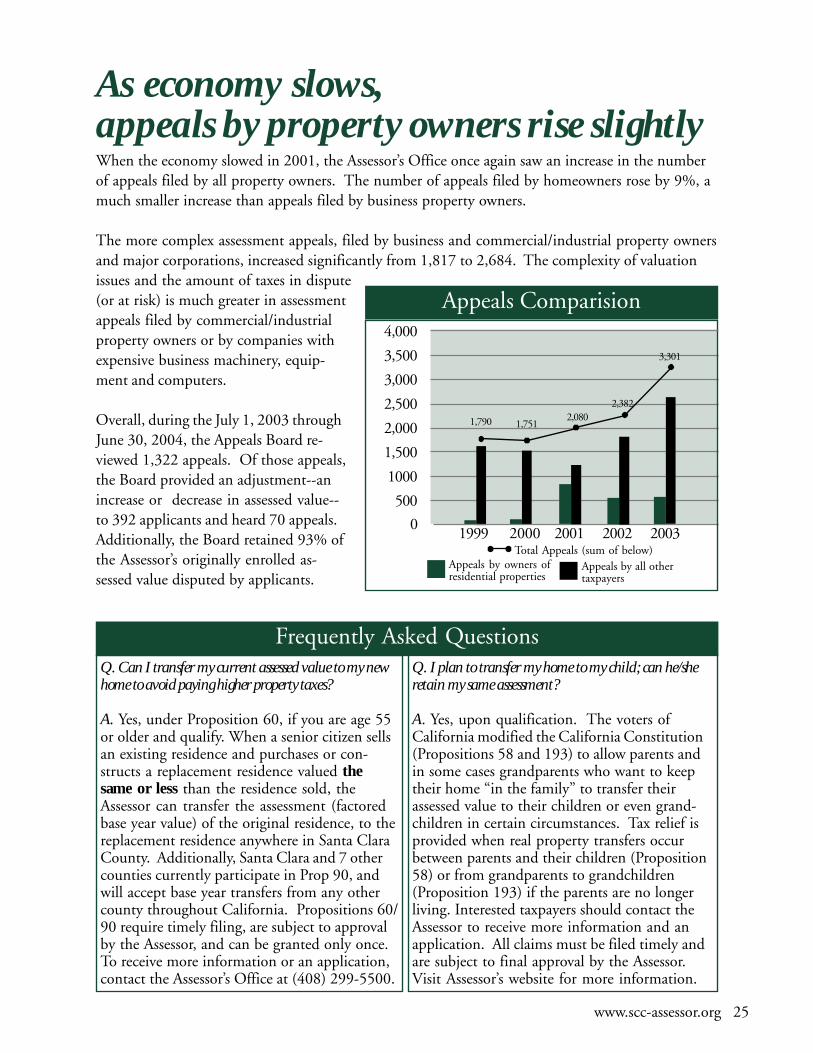

...virtually half of all appeals are withdrawn by Applicants...

Assessment Appeals ProcessIn Santa Clara County, a Notification of Assessed Value indicating the taxable value of eachproperty is mailed in May to all property owners. A taxpayer who disagrees with the Assessor’sassessed value may request areview by presenting to theAssessor’s Office before June 15,any pertinent factual informa-tion important to the determina-tion of the property’s marketvalue. If the Assessor agrees thata reduction is appropriate, anadjustment is made and a newnotice sent before July 1.

If a difference of opinion stillexists after July 1, the taxpayermay file an application forreduction in the assessed value.The matter will then be set forhearing before the local Assess-ment Appeals Board. In SantaClara County, appeal applica-tions must be filed between July 2, and September 15, with the Clerk of the Assessment AppealsBoard (Clerk of the County Board of Supervisors). To appeal a roll correction or supplementalassessment, typically triggered by a change in ownership or completed new construction, the appli-cation must be filed within 60 days of the date of the notice.

If the Assessment Appeals Board renders a decision for a proposition 8 temporary reduction invalue resulting in a decline in value below the property’s factored base year value (its upper limit), thereduction in value, and corresponding reduction in taxes, applies only to the property tax due for theyear in which the application was filed.