Embed Size (px)

Citation preview

Joh. Berenberg, Gossler & Co.

BERENBERG BANK

founded 1590Private Bankers

Neuer Jungfernstieg 20D-20354 HamburgPhone +49 40 350 60 -0Fax +49 40 35 21 32www.berenbergbank.de [email protected]

Hamburg • Bremen • Frankfurt/M. • Luxembourg • Shanghai • Zurich

400 years Experience builds the future

Annual Report2002

Joh. Berenberg, Gossler & Co.

BERENBERG BANK

founded 1590Private Bankers

1467

1676

13

73

491

659

413

851

56,4%

268

1568

1772

10

77

578

681

440

903

52,6%

260

1571

1802

8

82

537

667

499

841

64,3%

259

1581

1849

9

84

548

673

523

837

70,7%

255

1480

1708

14

87

427

691

398

861

66,9%

252

1515

1684

16

89

419

707

318

914

59,1%

263

1494

1684

18

95

372

751

299

1037

57,5%

280

1623

1800

39

110

419

796

174

1243

42,7%

319

1772

1968

41

118

458

840

161

1377

43,1%

359

1943

2134

41

125

554

796

122

1512

44,7%

365

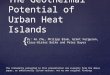

Summary of Balance Sheet positions (in million EUR)

Balance Sheet total

Business volume total

Retainted profit

Liable equity funds

Claim on

banks

customers

Liabilities

banks

customers

Cost -income ratio

Average numberof Employees

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

Joh. Berenberg, Gossler & Co.

BERENBERG BANK

founded 1590Private Bankers

Neuer Jungfernstieg 20D-20354 HamburgPhone +49 40 350 60 -0Fax +49 40 35 21 32www.berenbergbank.de [email protected]

Hamburg • Bremen • Frankfurt/M. • Luxembourg • Shanghai • Zurich

400 years Experience builds the future

Annual Report2002

Joh. Berenberg, Gossler & Co.

BERENBERG BANK

founded 1590Private Bankers

1467

1676

13

73

491

659

413

851

56,4%

268

1568

1772

10

77

578

681

440

903

52,6%

260

1571

1802

8

82

537

667

499

841

64,3%

259

1581

1849

9

84

548

673

523

837

70,7%

255

1480

1708

14

87

427

691

398

861

66,9%

252

1515

1684

16

89

419

707

318

914

59,1%

263

1494

1684

18

95

372

751

299

1037

57,5%

280

1623

1800

39

110

419

796

174

1243

42,7%

319

1772

1968

41

118

458

840

161

1377

43,1%

359

1943

2134

41

125

554

796

122

1512

44,7%

365

Summary of Balance Sheet positions (in million EUR)

Balance Sheet total

Business volume total

Retained profit

Liable equity funds

Claim on

banks

customers

Liabilities

banks

customers

Cost -income ratio

Average numberof Employees

1993 1994 1995 1996 1997 1998 1999 2000 2001 2002

2002Report on the 413th Financial Year

“Looking to the past is only wiseif it serves the future.”

Konrad Adenauer

Joh. Berenberg, Gossler & Co.

BERENBERG BANK

founded 1590Private Bankers

Cornelius Berenberg Johann Hinrich Gossler

3

Contents

Board of Advisers Page 4

Managing Partners, Executive Managers Page 5

Report of the Managing Partners Page 8

Economic overview Page 8

Commercial banking Page 13

Securities business Page 23

Subsidiaries and locations Page 31

Employees Page 35

Review of the year Page 36

Management report Page 38

Financial statements Page 48

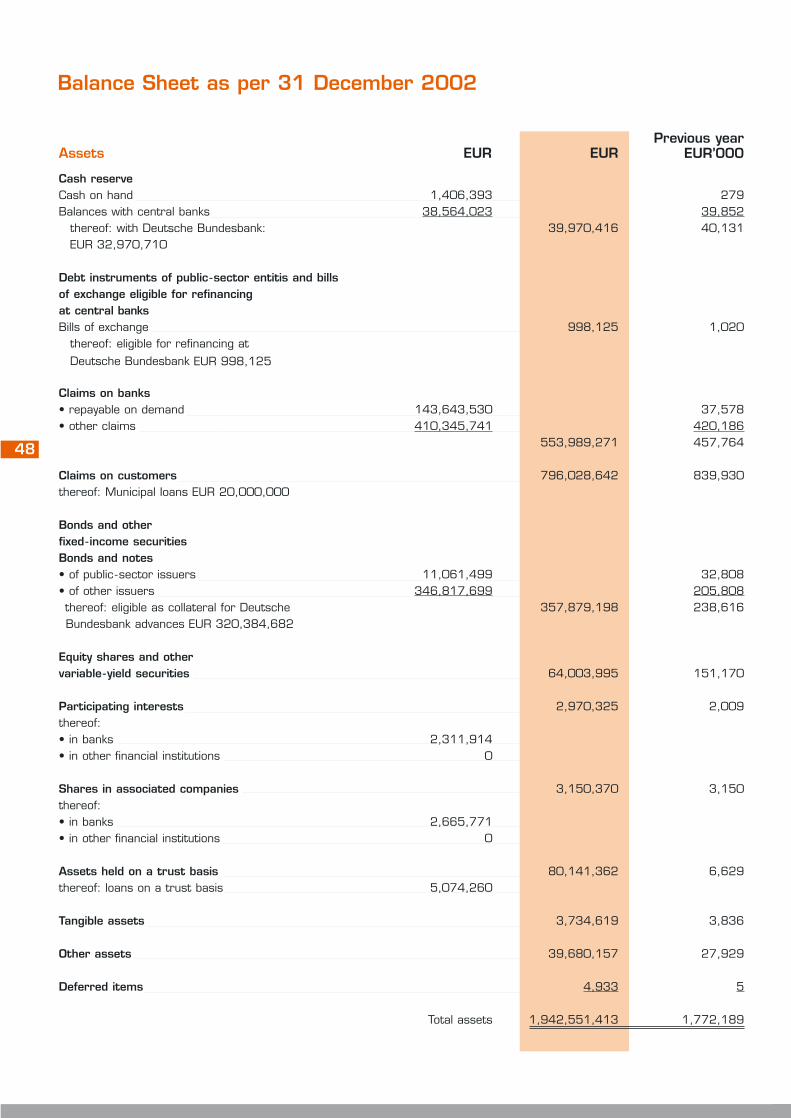

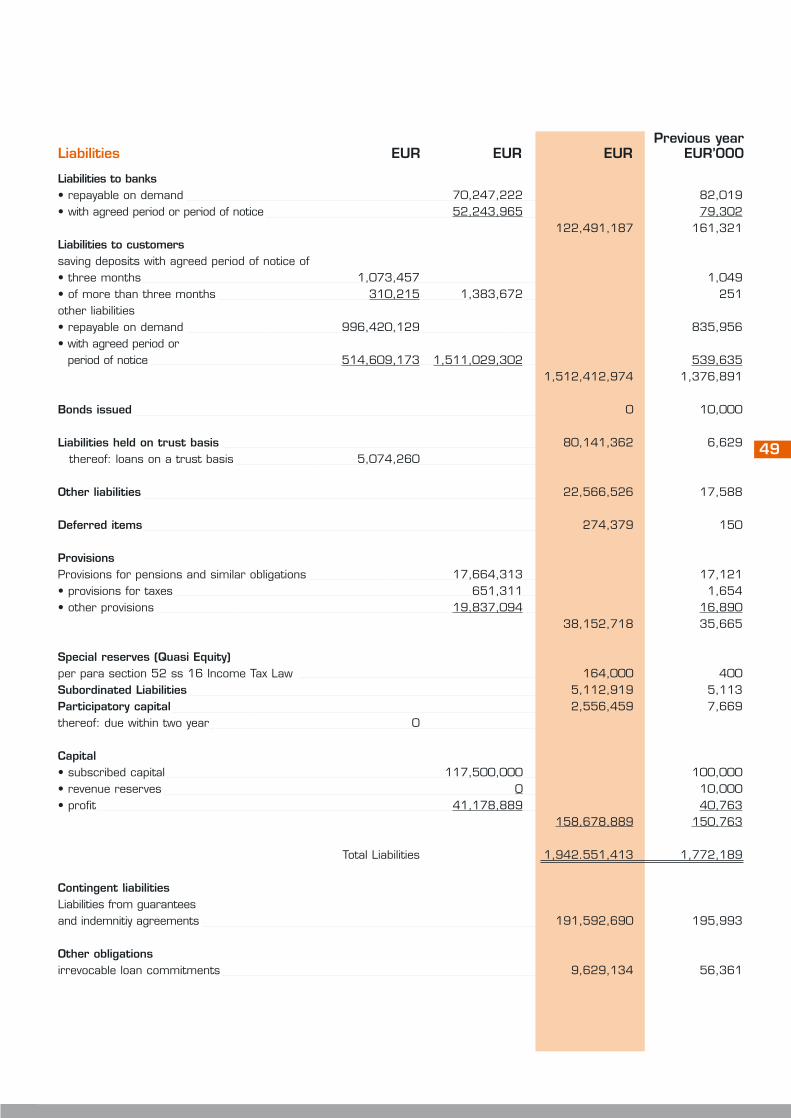

Balance Sheet Page 48

Profit and loss account Page 50

Notes to the accounts Page 52

Auditors’ report Page 60

4

Board of Advisers

Joachim H. Wetzel

Chairman, Hamburg

Dr. h. c. Manfred Bodin

President, Norddeutsche Landesbank Girozentrale, Hanover

Richard Dawids

Member of the Executive Board, Compagnie Mobilière & Foncière du Bois Sauvage, Brussels

Joshua Ruch

Chairman and Chief Executive Officer, Rho Management Company Inc., New York

Dr. Hans-Rüdiger Schewe

President, Fürstlich -Fürstenbergische Gesamtverwaltung, Donaueschingen

Andreas v. Specht

Partner, Egon Zehnder International GmbH, Frankfurt

Dr. Hans Vieregge

Member of the Management Board, Norddeutsche Landesbank Girozentrale, Hanover

Dr. Christian Wilde, LL.M.

Partner, Freshfields, Bruckhaus, Deringer, Hamburg

5

Managing Partners

Joachim v. Berenberg -Consbruch

Claus -G. Budelmann

Dr. Hans -Walter Peters

Executive Managers

Hendrik Riehmer

Wilfried Schnoor

Michael Schramm

Rüdiger K. Schultz

Jürgen Witt

Senior Managers

Lars Andersen (Frankfurt)

Manuel Bally

Dr. Jan Böhm

Jürgen Brockmann

Andreas Brodtmann

Graeme Davies

Beate Gerdes

Managers

Sven Albrecht

Michael Graf zu Dohna

Manfred Dulitz

Erhard Gold

Michael Große Siebenbürgen

Hartmuth Höhn

Klaus -Detlef Holbein

As at: 1 January 2003

Jürgen Hauser

Eberhard Hofmann

Hans-Jürgen Köcher

Hans P. Rajner

Klaus Schröder

Gerd Simon

Dr. Klaus D. Thiedig, General Counsel

Edmund Krug

Dr. Jörg -C. Liesner

Dieter Lügering

Dieter Rusch

Dieter Schlichting

Andreas Schultheis

Uwe Schwedewsky

6

‘02

‘02

7

Dear customers and business friends,

The changes which have been taking place in the banking landscape

for some years now have continued to gather pace. The main reason

for the structural crisis is the surplus capacity within the banking sec-

tor in Germany. In times like these, more and more customers appre-

ciate the special level of service and the range of services that a pri-

vate bank offers.

Berenberg Bank is a medium-sized company. Smaller companies

have the benefit of flexibility and manoeuvrability. As a “fast mover”,

we are able to adjust more easily to changes in market conditions.

Entrepreneurial thinking dictates the way we carry out our business.

We cultivate the contact between business people, and we have com-

mitted and highly professional employees, who know their customers

and who assist them year - in, year -out.

Thus in 2002, we again succeeded in expanding our business divi-

sions further. The securities business in particular has again recor-

ded an outstanding result, but in commercial banking too, we were

able to display proof of our skills and achieve success.

With a cost - income ratio of 44.7%, another successful annual

result of EUR 41 million was achieved. The balance sheet total rose

by 9.6% to EUR 1,900 million, and the equity capital currently stands

at EUR 125 million.

Balance Sheet total

1515 14941623

1772

‘98 ‘99 ‘00 ‘01

Retained profit

1618

39 41

‘98 ‘99 ‘00 ‘01

Liable equity funds

89 95110 118

‘98 ‘99 ‘00 ‘01

in million EUR

1943

41

125

‘02

Joachim v. Berenberg - Consbruch Claus - G. Budelmann Dr. Hans -Walter Peters

Report of the Managing Partners

Economic overview

The economy is a human creation and economic activity is driven by

humans. It is a generally accepted fact that psychological factors

account for at least 50% of every economic performance. The trans-

fer of national monetary policies to the European Central Bank ECB

and the Maastricht agreements have considerably restricted the free-

dom that countries have to plan their own finances. Consequently, the

possibilities of direct economic management have continued to

decrease throughout almost the whole of Europe. The economy is

therefore more dependent on other factors, such as on the economic

well - being of our trading partners on the one hand and the general

sentiment of business leaders and consumers on the other.

2002 will be remembered above all as the year of deep mistrust,

extremes and crises: debt crises in Argentina and Turkey, the banking

and economic growth crisis in Japan, budget crises in Portugal, Italy,

Germany and France. Then the risk of war in Iraq intensified, followed

by an increase in energy costs by 50% as the year progressed to

crude oil prices of US$ 33/barrel. The capital markets also witnes-

sed a general confidence crisis, fuelled by the aftermath of the spe-

culation bubble bursting, the terrorist attacks and lastly the account-

ing scandals at US companies in particular. Risk aversion became the

name of the game.

Companies were not confident that an economic revival would last.

They reduced their inventory levels. There was hardly any build up of

new capacity. Cost -cutting and debt - reduction took centre stage. Jobs

were cut. In the USA, in excess of another million jobs were cut, while

in Germany the figure totalled roughly 200,000. Consumers reacted

with appropriate caution, at least on this side of the Atlantic. Although

the introduction of euro notes and coins was quickly deemed a tech-

8

Report of the Managing Partners

9

nical success, the public were often annoyed by the perceptible price

rises for services and food especially. „Teuro“ (literally ‘expensive

euro’) became the most unpopular neologism of the year. The result

was a noticeable reluctance to buy. The German retail trade describes

2002 as the worst year since the end of the Second World War.

Sales remained almost 2% down on revenue from the previous year.

Growth in domestic demand was accordingly weak, not just in

Germany but throughout the whole of continental Europe with the

exception of most of the EU entry candidates from central and

eastern Europe and the Baltics. In these countries, the convergence

process had a regenerating effect as a result of falling interest rates

and high direct investment.

Most of the growth areas outside of Europe were to be found in

Asia. From India to China, growth rates of between 4% and 8% were

recorded.

Traditionally, the German export economy is very competitively pla-

ced in this region. The official inauguration, right at the very start of

2003, of the first Transrapid line in Shanghai, will be remembered in

particular. The line has a truly symbolic character.

Despite the weakened trend throughout the year, it was once again

exports which provided the main support to the economy. They again

grew by 1% to EUR 647 billion and, with imports falling, ensured a

record surplus in the trade balance of EUR 127 billion. A slide into

recession was again narrowly averted. However, talk of growth is hard

when gross domestic product increases by barely more than 0.2%.

The economic predictions of all professional forecasters – issued twel-

ve months previously – proved in the event to be far too optimistic.

Official tax estimates were thus also too high. As a result, Germany

has failed to achieve the net debt ceiling of 3% of GDP in 2002.

Against this background, the German government, re -elected to

office by an extremely narrow margin, were forced into implementing

a mixture of tax increases which will restrict growth. More compre-

hensive structural reforms have so far remained in their initial stages.

10

Thus, the growth potential of our economy looks set to remain unex-

hausted for the foreseeable future.

The number of people – especially abroad – drawing parallels to

what happened in Japan following the bursting of the financial market

and property bubble from 1990 onwards is already growing. Even

twelve years later, Japan still shows no signs of escaping the deflation-

ary spiral. Prices are generally falling by approximately 1% p.a. The

banking crisis remains unresolved and national debt is threatening to

get out of hand. The country was again unable to make any contribu-

tion towards a more positive development of the global economy.

The performance of the European Economic Area was also disap-

pointing. Growth slowed from a moderate 1.4% in 2001 to below 1%.

In addition to Germany, Italy in particular performed especially poorly.

What is noticeable is the above -average strength of the Scandi-

navian countries and Great Britain, which have so far remained out-

side of the euro. Here, overall economic performance has expanded

by almost 2%. The same applies to Spain, Ireland and Greece.

In comparison, in view of the chain of detrimental factors, the resist-

ance of the US economy remained highly noteworthy. In the twelve

months following the September attacks, GDP grew by 3% on aver-

age. The slide into a new recession, a topic of intense discussion on

the equity and debt markets, was decisively averted. However, the

recovery was not a straightforward affair. Following six strong

months, there followed a period of weakness in the spring. As the

accelerated nosedive of the capital markets and the growing fear of

war threatened to cripple investor and consumer activity, central

banks again cut their base rates. At 1.25%, base rates in the USA

are at their lowest levels since the Cuban crisis in 1962. In the euro

zone, rates have remained considerably higher than in the USA, most

recently standing at 2.75%. Given the economic weakness in the euro

zone, this appears somewhat astonishing. However, account should

be taken of the very heterogeneous inflation trend in Europe. At the

end of 2002, the rates ranged between less than one percent in

Germany and almost three percent and over in Spain, Italy or the

Netherlands.

Report of the Managing Partners

11

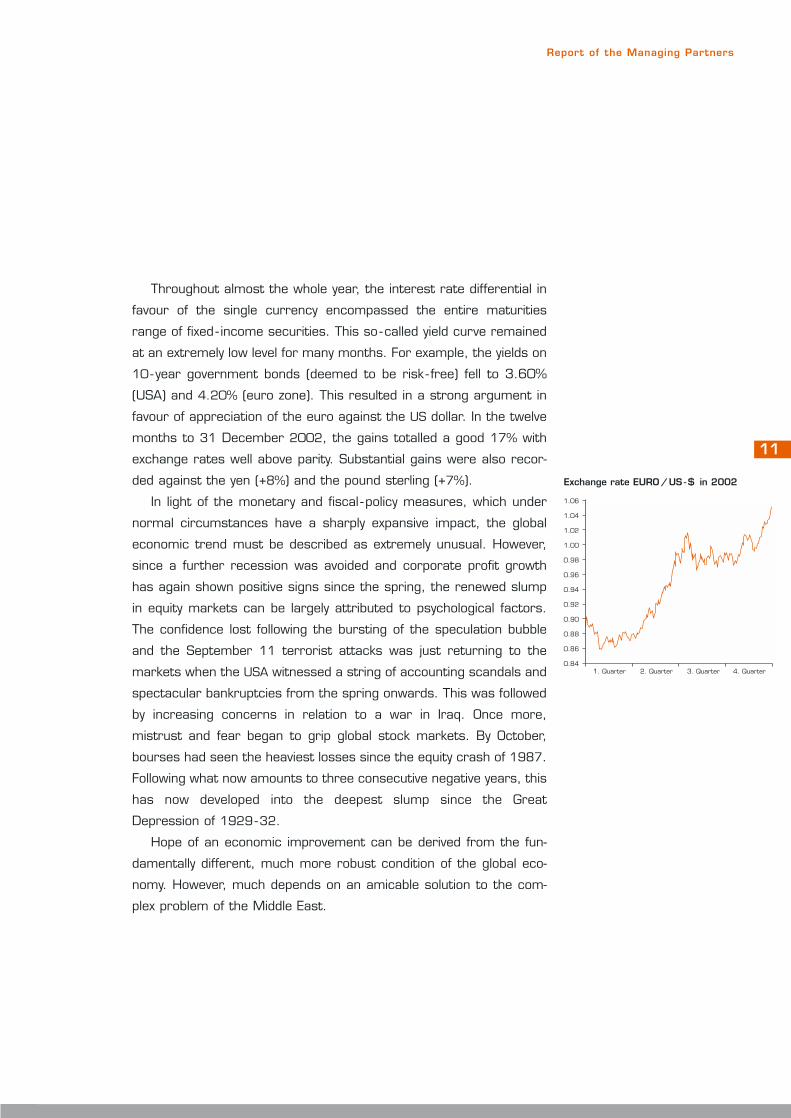

Throughout almost the whole year, the interest rate differential in

favour of the single currency encompassed the entire maturities

range of fixed - income securities. This so -called yield curve remained

at an extremely low level for many months. For example, the yields on

10- year government bonds (deemed to be risk - free) fell to 3.60%

(USA) and 4.20% (euro zone). This resulted in a strong argument in

favour of appreciation of the euro against the US dollar. In the twelve

months to 31 December 2002, the gains totalled a good 17% with

exchange rates well above parity. Substantial gains were also recor-

ded against the yen (+8%) and the pound sterling (+7%).

In light of the monetary and fiscal - policy measures, which under

normal circumstances have a sharply expansive impact, the global

economic trend must be described as extremely unusual. However,

since a further recession was avoided and corporate profit growth

has again shown positive signs since the spring, the renewed slump

in equity markets can be largely attributed to psychological factors.

The confidence lost following the bursting of the speculation bubble

and the September 11 terrorist attacks was just returning to the

markets when the USA witnessed a string of accounting scandals and

spectacular bankruptcies from the spring onwards. This was followed

by increasing concerns in relation to a war in Iraq. Once more,

mistrust and fear began to grip global stock markets. By October,

bourses had seen the heaviest losses since the equity crash of 1987.

Following what now amounts to three consecutive negative years, this

has now developed into the deepest slump since the Great

Depression of 1929-32.

Hope of an economic improvement can be derived from the fun-

damentally different, much more robust condition of the global eco-

nomy. However, much depends on an amicable solution to the com-

plex problem of the Middle East.

Report of the Managing Partners

1.06

1.04

1.02

1.00

0.98

0.96

0.94

0.92

0.90

0.88

0.86

0.841. Quarter 2. Quarter 3. Quarter 4. Quarter

Exchange rate EURO/ US -$ in 2002

The flashpoints must not be allowed to escalate. We might then

see a rapid return to crude oil prices being defined without a war pre-

mium. The future would again appear more secure to business lead-

ers and consumers. Investors would then be more prepared to as-

sume longer - term risks. Economic and capital markets would have a

more solid basis for a lasting upturn.

Quite apart from all this, the need for a move away from situation-

driven short - term policies at federal level in favour of a dedicated

commitment to implement reforms aimed at removing the structural

imbalances within our society remains desirable.

Report of the Managing Partners

12

Commercial banking

The structural changes within the German banking sector have con-

tinued at an accelerated pace. Completed or planned mergers or

takeovers, together with the decision of a few banks to give up or

reduce corporate banking activity mean that there is a reduced choice

of banks, particularly for medium-sized companies.

Against this background we have clearly stated that corporate

banking activity continues to be one of the fundamental pillars of

Berenberg Bank, and this has been to our advantage, working close-

ly with many contacts and gaining a large number of new customers.

Lending activities

Foreign trade The financing and processing of foreign trading trans-

actions continues to be of particular significance for us, for example

letters of credit, short - term bridging finance and hedging of currency

risks.

While the demand for import letters of credit has fallen, interna-

tional payments have risen sharply. This is reflected by the increased

level of trust between foreign manufacturers and domestic impor-

ters, resulting from many years of business relations. We see a grow-

ing wave of mergers/cooperation among importers, since industrial

processors and retailers are focusing their purchases on importers

who meet the high demands with regard to quality and punctuality

of delivery.

One focal point of import activity continues to be in commodities,

i.e. crude oil products, coffee, wood products, chemicals, pharma-

ceutical products. Our know -how both of the products and also the

markets makes us an expert partner for these demanding import

customers . By granting special finance facilities, we are able to react

quickly and with flexibility to our customers’ requirements.

13

Consumer demand for so -called special offer goods has increased.

In this area non - food items are imported from all over the world in

large volumes and sold onward across Europe to chain retailers with

good credit ratings. Despite the general reluctance to buy, technical

goods and textiles in particular are in increasing demand from con-

sumers as a substantial price -benefit ratio has been built in this area.

Funding these transactions has become one of our core areas.

Working capital finance Traditional working capital finance facilities

for national and international groups and corporate customers are of

less significance for us because of the expected levels of lending and

the narrow interest margins, and have reduced in volume. We provi-

de these customers not only with integral solutions as part of short-

term financing, including off - balance -sheet structures, but also with

a complex range of products for investing any available short, medium

and long - term liquidity in various currencies, securities and with inno-

vative instruments.

Our customer base among medium-sized industrial companies has

shown pleasing growth. With domestic demand either stagnating or

falling sharply, many of these old-established companies are looking

for new sales channels abroad for their often technically pioneering

products. The main focus of interest is Asia, and in particular China.

Our experience in the export business means that we are able to pro-

vide these companies with useful addresses of both foreign buyers

and banks in the export country. In this respect, our representative

office in Shanghai has proven to be particularly useful.

Shipping Another encouraging increase in the number of our custo-

mers has been recorded in the domestic and international shipping

sector. The high level of employee expertise and a rapid international

payments service are convincing factors for our customers. In addi-

tion to prefinancing freight revenue and working capital, we have also

provided medium and long - term loans in cooperation with institutes

Report of the Managing Partners

14

specialising in such funding, and, in exceptional cases, even granted

funds directly. These funds are collateralised with ship mortgages.

Construction finance This area has continued to record good growth

despite the stagnating economic climate. Along with traditional lend-

ing activities, it forms an established part of our business, making a

stable contribution to the results. For a few selected property devel-

opers and construction companies, we provide loans for property

purchases and bridging finance for the construction of housing and

commercial properties in north Germany (mainly Hamburg) and

Berlin. We accept only good and very good residential, office or busi-

ness sites which are divided equally between residential and commer-

cial areas. At the start of the construction phase, the properties have

generally either been pre - let on a long - term basis, or even pre -sold,

thus restricting our risk. The construction project and its progress are

closely monitored by an experienced team.

Stock market lending Working closely with the Private Banking

department, securities lending granted to selected customers pro-

vides a good opportunity to exploit the volatility of share prices with

short - term transactions. With markets remaining volatile throughout

2002, and significant losses proving to be a trend, a specially devel-

oped computer program designed to identify risks at an early stage,

has proved itself through intensive and timely monitoring of risks.

Volume of lending We have maintained our deliberate policy of pru-

dent lending. As planned, this has led to a slight decline (- 4.7%) in

the volume of lending, with falling cash advances (- 5.2%) contrasting

with an increase in the number of guarantees furnished.

The quality of the loan book remains satisfactory.

Report of the Managing Partners

15

Lending activities once again made an encouraging contribution to

results.

Credit rating As a result of an improved information policy by all

banks – especially via the Association of German Banks – it has been

possible to convince most medium-sized companies of the necessary

introduction of credit ratings, in accordance with legal provisions. The

impression sometimes gained by the public that credit ratings could

spell an end to lending to medium-sized companies, was thus effec-

tively countered.

In explanatory discussions with our customers, they have shown

particular interest in how they can improve their own rating assess-

ment through financial and structural measures.

In a circular issued in December 2002, the Federal Financial

Supervisory Authority laid down the “Minimum Requirements for Bank

Lending Activities” (MAK) to limit the risks from lending activities

taking account of the respective type and scope of business. All banks

need to have complied with these requirements by 30.6.2004 at the

latest. Standards in line with banking practice for loan processing,

loan processing monitoring, intensive support, problem loan proces-

sing and risk provision procedures are being laid down. In addition,

there is a framework for structuring procedures aimed at identifying,

Report of the Managing Partners

16

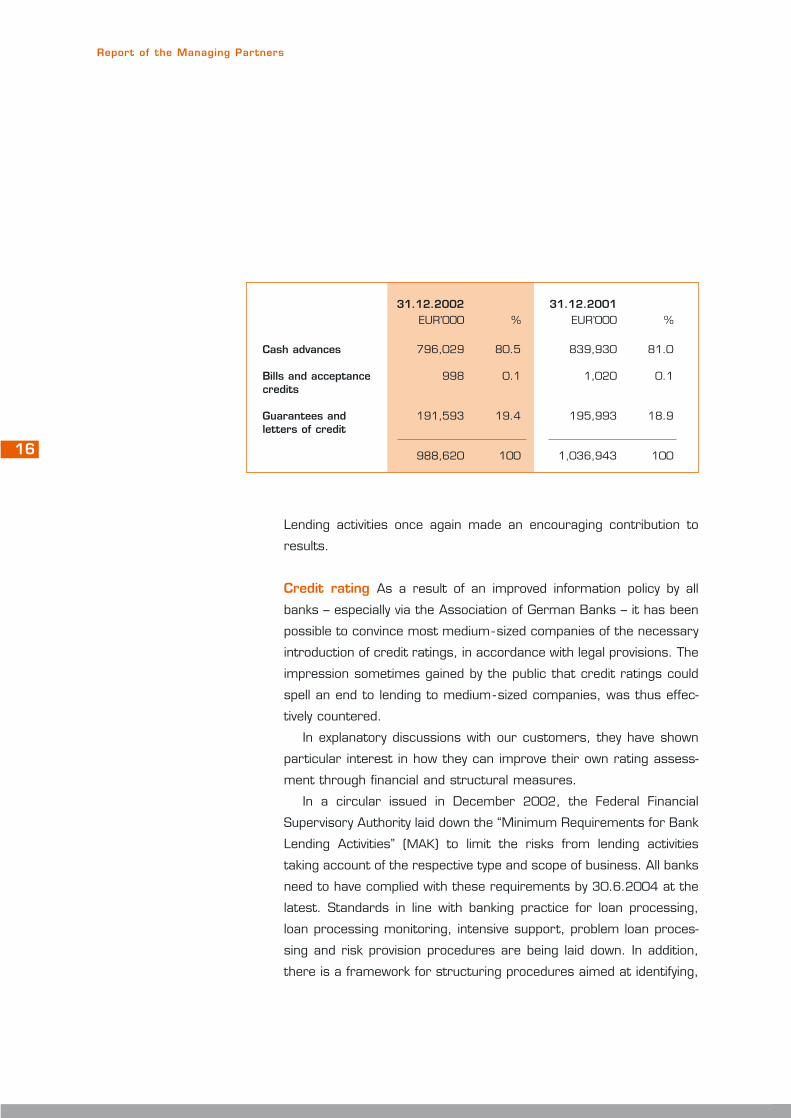

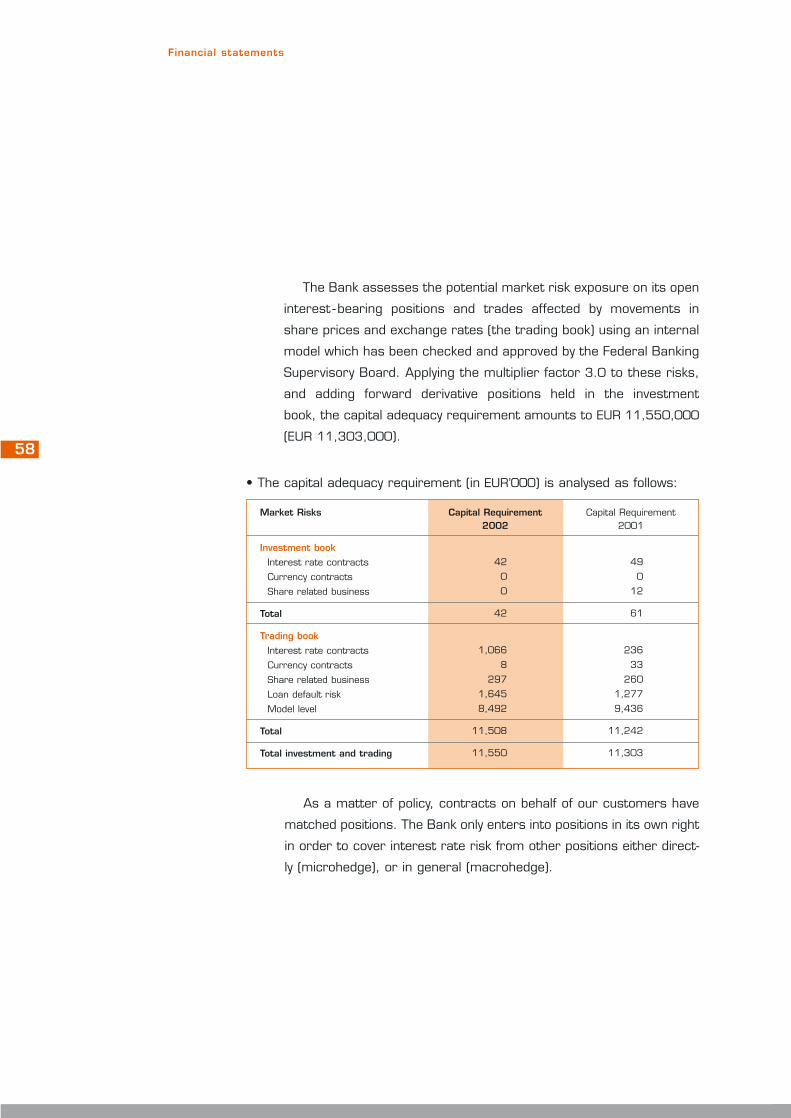

31.12.2002 31.12.2001EUR’000 % EUR’000 %

Cash advances 796,029 80.5 839,930 81.0

Bills and acceptance 998 0.1 1,020 0.1credits

Guarantees and 191,593 19.4 195,993 18.9letters of credit

988,620 100 1,036,943 100

controlling and monitoring risks arising from lending activities and

which, in this respect, requires banks’ internal control systems in par-

ticular to meet certain standards.

We have already arranged for the way in which lending activities

are processed and controlled to be restructured. This will be carried

out within a strict timeframe.

Outlook Given that economic trends remain uncertain, a fact which

is also reflected in the high number of corporate bankruptcies, we

have made provisional plans to reduce lending volumes further for the

current financial year. Our criteria for creditworthiness remain strict

and we are focusing on gaining new clients by targeting medium-sized

firms to which we can offer a flexible and comprehensive service

through our core expertise.

International activities

In a world where banking products are becoming increasingly stand-

ardised, our corporate approach of combining customer proximity

and the personal advice that this requires together with special coun-

try know -how has met with a very pleasing level of acceptance both

among our established relationships and also with new customers. In

this respect, international activities have made a highly satisfactory

contribution to the company’s overall success, despite the cooling off

in the import and export markets.

International payments By making distinctly greater use of electro-

nic systems and continually enhancing these systems, it has been

possible to cope with unit figures and volumes in payment processing,

which up until recently would have been unimaginable for a private

banking organisation.

Report of the Managing Partners

17

Both our domestic and international customers make very active

use of the Multi Cash banking system. The increasing automation for

payments from correspondent banks has impacted very positively on

commission income as well as the increase in productivity.

In view of the increasingly more stringent requirements in relation

to money laundering and anti - terrorism measures, we have intro-

duced computerised safeguards, which enable relevant transactions

to be recognised automatically.

Documentary business We can also report continued pleasing growth

in our documentary business, thanks principally to export letters of

credit in the buoyant correspondent banking business in key regions.

Furthermore, we have become increasingly involved in the collection

business, particularly for our overseas customers. Only the import

letter of credit business failed to meet our expectations, due to the

generally modest situation in the area of consumer goods.

Country activities In connection with processing and financing

export transactions, we were again able to provide a large number of

our customers with the opportunity to hedge the associated risks of

undertaking commercial activity abroad. This is principally through

disclosed and undisclosed confirmation of letters of credit and for-

feiting transactions. It should be stated here that we are for the most

part involved in this segment on a short - term basis.

Our principal involvement is with countries within western Europe

and Asia – particularly China – as well as countries in the Gulf region.

We do not establish a general limit for a particular country but, rath-

er, evaluate the relevant risks of an individual transaction. Conse-

quently, when carrying out customer transactions, for us it is not just

a question of whether we can take the associated risks onto our own

books. We also consider the option of placing risk on international

secondary markets.

Report of the Managing Partners

18

Therefore, we are once again able to report this year that we have

no ongoing business on our books in countries which are currently in

default or engaged in rescheduling negotiations.

The objective for our business with commercial customers abroad

focuses on traditional international trade business as well as cooper-

ation with international shipping companies. However, our relation-

ships with our international correspondent banks in key countries are

also important. Thanks to more extensive travel on the part of our

employees, we endeavour to maintain and increase our close person-

al contacts abroad with individual country desks.

The countries forming our principal focus include those in western,

central and eastern Europe, North and Latin America, the Middle and

Far East as well as Australia and New Zealand.

The numerous contacts in the commercial sector create addition-

al wide - ranging opportunities for business on the investment side,

with private individuals and institutional investors making considerable

use of our Private Banking and Asset Management services.

China Although business at our representative office in Shanghai

started in mid -2001, the official opening celebrations in the pres-

ence of the mayor of Hamburg and high - ranking representatives of

Shanghai’s city government took place in May 2002. Our aim is to

use our presence in Shanghai to further develop our interests in

trading - related activities in this important future market, through

close collaboration with the China Desk in Hamburg.

In this respect, we can report that the representative office has

enjoyed a very pleasing start and has made a considerable contrib-

ution to increasing our documentary business in China.

However, by increasing our country expertise, it is also our wish to

assist our medium-sized customers in their activities in China, and to

support and facilitate their entry into this particular market. Taking

our European tradition as a basis, we would also like to bridge the gap

between these two different cultures. Our Chinese employees in

Shanghai and Hamburg feel a strong obligation to perform this role.

Report of the Managing Partners

19

Since the country continued to prove in 2002 that it is one of the

global economy’s few growth engines, and its entry to the World

Trade Organisation and the staging of EXPO 2010 in Shanghai are

expected to provide further economic impetus, we believe that China

will in future be one of the countries with the greatest potential for

growth. The decisions taken at the 16 th Party Congress appear to

have created the political prerequisites for stable growth. Yet at the

same time, we are all too aware that the country faces decisions

regarding its future direction, in order to maintain control over the

social problems and economic frictions that are becoming apparent.

Shipping activities The shipping sector, traditionally important for us,

has again made a substantial contribution to results in the past finan-

cial year. Our internal structure and the experience and knowledge of

our specialist department enable us to provide our customers both in

Germany and abroad with a tailored range of services, together with

a very flexible and rapid service.

Alongside our commercial settlement banking products, we offer

these customers short - term finance for working capital require-

ments. In exceptional cases we grant medium- term loans for ship

purchases, in which case we obtain a mortgage on the ship as secu-

rity. We are also very active in providing this clientele, which is made

up of shipping companies, ship management companies, shipping

agents and shipbrokers, bunkering firms etc., with foreign currency

hedging products.

Inter -bank business Our company’s inter -bank business on the

money and currency markets is largely based on the commercial trans-

actions of our corporate customers and the general controlling of

liquidity from customer funds. Dealing with foreign banks is restricted

Report of the Managing Partners

20

almost exclusively to institutions in OECD countries. Our applicable

limits are geared very closely to dealing requirements and are regu-

larly adjusted to the level of activity. Because of the short - term nature

of this area of activity, we are able to react very promptly to possible

changes in risk.

Outlook

For the future too, international business is rated as a significant core

element of the Bank’s expertise. In international business, we believe

that it is imperative to guarantee our customers the continuity and

professionalism of a personal service. Even with a constantly growing

volume of business, this requirement will determine our employment

policy.

Deposits

Customer deposits increased by EUR 135,522 million to EUR 1,512

millon, thus representing 92.5% of total deposits.

Treasury/Derivatives

The marketing of equity - linked, structured products has remained

the focal point of activities. Despite the difficult market conditions,

the volume of business in the area of structured equity products

increased.

The level of activity in trading OTC share options for the account of

a public fund for our subsidiary Berenberg Lux Invest S.A. has risen

thanks to a high inflow of funds.

The investment strategy in the Bank’s own portfolio continued to

focus primarily on government bonds and mortgage bonds. The inter-

est rate trend in the last financial year led to an increase in hidden

reserves.

Report of the Managing Partners

21

At the end of the year, the Treasury and Derivatives Departments

were separated for strategic reasons.

Foreign exchange trading

The euro moved in a very narrow band during the first quarter of the

year. The long -awaited turnaround came in May and the price rose

sharply against the US dollar until it reached parity. The accounting

irregularities which were uncovered in the United States, and a global

economy that continued to weaken provided the backdrop for this

turnaround. These facts, together with developments in Iraq, caused

securities markets to weaken considerably, which in turn took its toll

on the US exchange rate.

Under these difficult circumstances, we more than justified our

position. Although the level of business in commercial foreign curren-

cy trading was down as a result of the economic situation, we never-

theless generated very pleasing levels of income and were thus able

to achieve the previous year’s result.

Report of the Managing Partners

22

Securities business

Private Banking

Private Banking Germany This year too saw extreme upheaval

dominate the international capital markets. In spite of the difficult

market conditions, Private Banking can look back on an extremely suc-

cessful financial year. There was a further considerable increase in

the inflow of new customer money, with results even clearly exceeding

the record levels of 2000. With company disposals especially, we

were able to convince business leaders in their new financial situa-

tion, of our discrete, personal and professional service.

It is clear to us that Private Banking does not just comprise invest-

ment consulting. Instead, it is much more about providing a compre-

hensive advisory and support service to high net -worth private inves-

tors. The difficult market conditions directly revealed the importance

of an adequate level of risk diversification. That is why we have contin-

ued to widen our approach to integral investment consulting.

- Participating interests: Based on a comprehensive analysis of the

investment market carried out by Berenberg Finanzanlagen GmbH,

we have added international commercial real estate and private equi-

ty investments in particular to our customers portfolios.

- Real estate: Real estate forms a stabilising and significant compo-

nent of our strategic portfolio allocation. By carrying out an individual

analysis of real estate holdings, we have also strengthened our con-

sulting activities in this area in order to optimise the real estate struc-

ture of our customers in terms of expected yields and tax efficiency.

- Life insurance: Our life insurance policies include arranging tax -effi-

cient portfolio management for our investors.

23

In addition, our customers were able to benefit from individual

attention which underpins our approach to consulting. Our advisory

teams have been structured according to customer requirements. In

this way, the interests of business leaders, wealthy individuals, sports-

men and women or artists are served by teams possessing the very

highest degree of specialist know -how. Accordingly, our financial stra-

tegies are prepared exactly in line with our customers’ needs and per-

sonal circumstances. This approach to consulting takes account of

the increasing complexity involved in integral investment consulting.

We are convinced that, by adopting this approach, we will continue to

be able to provide our customers with added value in the future.

In the area of portfolio management too, we succeeded in extend-

ing the successful trend of the previous year. The volume of customers

we advise saw another substantial rise. Thanks to our disciplined in-

vestment approach and our consistent controlling of performance, we

were able to at least cushion the poor performance of the international

equity markets. A competence centre has been created by integrating

secondary research into portfolio management. In future, this will en-

able significant improvements in efficiency to be made, both in terms

of quality and quantity. The successful cooperation strategy, which

includes acquiring portfolio management mandates from other banks

and savings banks, has been further expanded.

This year, we continued to build on our expertise in managing the

assets of foundations. We provide our customers with a comprehen-

sive, made - to -measure advisory service on forming, managing, analy-

sing and organising a foundation. Working in tandem with the cus-

tomers’ lawyers and tax consultants, we consider any tax or legal

details. As far as we are concerned, responsible management of a

foundation’s assets includes innovative investment strategies and real

estate investments. For this reason, we were able to fulfil our cus-

tomers’ objectives – namely the maintenance of the foundation’s

assets and high, continuous dividends – with particular success this

year. The further considerable rise in volumes may be seen as proof

of the professional nature in which we manage foundation assets.

24

Report of the Managing Partners

Given our clear strategic positioning and our individual approach to

consulting, we believe that we have positioned ourselves very well in

the market. Which is why we are looking to the next financial year with

optimism.

Publicly offered investment funds returned a pleasing performance

last year. The number of funds we manage increased by two to 17.

In particular, the collaboration with portfolio managers and financial

service providers had a stabilising effect on the business division amid

difficult market conditions in 2002.

Within the equity funds sector, we continue to pursue the strategy

of being a specialist provider. As a result, as part of the Berenberg

Concept Portfolio, we have been one of the first German banks to

develop an investment fund in discount certificates.

In the area of fund -of - fund activities we have acquired new con-

sulting mandates from reputable insurance companies. In addition, by

the end of the year we had received a considerable inflow of funds in

the special funds managed by us, which are based on fund -of - funds.

As a result of the outperformance and the above -average place-

ment of our investment funds -of - funds, we are confident that we will

be able to acquire a further inflow of funds and more consulting man-

dates next year.

International Private Banking Despite continuing difficult market

circumstances, International Private Banking recorded an extraordi-

narily pleasing performance. Our company benefited from various

strategic restructuring on the part of our competitors, some of

whom even exited the market. Besides Greece and Great Britain, the

regional focus of growth was once again Latin America and the

Middle East. Working together with select local partners has proved

to be the right move and something we will build on.

With a personal service geared towards providing continuity, indi-

vidual advice and product independence, assets under management

have been increased by more than 30%. In this respect, the invest-

Report of the Managing Partners

25

ment philosophy behind Berenberg Bank’s international private bank-

ing activities is drawn from Anglo -Saxon and Swiss investment philos-

ophies in equal measure. By making use of alternative investment pro-

ducts, our conservative portfolio managers were largely able to achie-

ve satisfactory results. On the other hand, the comprehensive con-

sulting service to our customers in all asset classes, markets and

individual securities took on an important role.

The clear strategic positioning and the continued performance of

our services should also strengthen our market position in 2003 in

the regions we manage.

Institutional customers

• Capital markets

Institutional Sales Irrespective of the difficult sector environment,

Institutional Sales again strengthened its marketing activities last year.

More than 30 road shows with the directors of renowned German

companies enabled those institutional investors under our manage-

ment to engage in individual talks or round table discussions, and

thereby find out information regarding the business prospects for

these companies.

The road shows, which were held in the financial centres listed below,

Frankfurt London Vienna

Hamburg Paris Stockholm

Cologne Copenhagen Gothenburg

Munich Zurich Brussels

Stuttgart Geneva Luxembourg

were an interesting bonus for our customers, giving them the chan-

ce to very quickly find out about the outlook for the companies con-

cerned. In addition to the company road shows, we staged over 20

road shows with our sector analysts.

This active customer support has enabled our employees to gain

30 institutional investors as new customers in 2002, and this despite

the very volatile capital markets.

Report of the Managing Partners

26

Our success in acquiring new customers is based not least on the

many years of market experience and the high level of training that we

give our sales employees. Despite sharp price falls – the most impor-

tant German stock market indices fell in value by between 35 and

80% over the course of the year – the success in acquiring new cus-

tomers and expanding our market presence among mid -cap companies

partly compensated for the drop in volumes. Nevertheless, sales with

institutional investors were down on the previous year.

Thanks to the very stringent customer focus, results reached the

previous year’s level.

As was the case in the previous financial year, we aim to specifi-

cally strengthen Institutional Sales, so as to continue to exploit the ex-

isting competitive opportunities in a targeted manner.

Research The expansion of the Research Department, begun in

1999, was largely completed during the last financial year, by improv-

ing the quality of the analyst team. With a team of twelve analysts at

present, we cover all the major sectors of the German equity market.

By combining a sectoral approach with sector -wide analysis of mid-

cap companies, we have successfully positioned ourselves as special-

ists in German equities.

An assessment carried out by the independent British ratings

agency AQ Publications into the accuracy of results forecasting re-

vealed Berenberg Bank’s team of analysts to be one of the leaders

in this field.

Working in conjunction with the members of the institutional sales

team, the analysts support selected institutional buy side analysts and

fund managers and achieve considerable success in customer service

and acquisition. With its role in helping to arrange the two investor

conferences held annually in Hamburg, the Research Department

makes an important contribution to overall success.

At the Mid -Cap Conference in March 2002, the management

boards of the following companies AWD Holding AG, Tecis Holding AG,

Singulus AG, Aixtron AG and Rhön Klinikum AG gave a presentation

to a select number of institutional customers on the prospects for

their companies.

Report of the Managing Partners

27

Then in September, the management boards of the DAX- listed com-

panies Volkswagen AG, E.ON AG, MLP AG, DaimlerChrysler AG, SAP

AG and Deutsche Telekom AG provided institutional investors with an

insight into why their respective business models enjoy lasting success.

The Special Issues publications devoted to the problems of valua-

tion and accounting were the subject of particular interest and cov-

ered the following topics:

- Valuation methods – practical approaches

- Hocus Pocus Accounting – accounting in the grey area

- Show us your options!

All of this helped convince our customers of the capabilities of our

Research Department.

Proprietary trading Over the last few years, the Bank’s proprietary

trading activities have been extremely limited. The income from equi-

ty trading contributed to the overall result, despite the difficult condi-

tions. Own -account trading in bonds and convertible bonds performed

particularly well. Here there was a sharp increase in earnings. The

Designated Sponsor department has two accounts, as was the case

last year. We do not plan to expand our activity in this area.

Syndicate business: In the syndicate business, two mandates are

currently under management, to structure and improve the capital

market communications of those companies concerned.

The Special Issues publications on various capital market problems:

- Duties of listed companies

- Industrial and convertible bonds – a brief introduction

- Squeeze -out – compensation for minority shareholders

- German stock market sectors

- Directors Dealings – legal duty to provide notification

and publication since 1 July 2002

were extremely popular with our customers.

Report of the Managing Partners

28

29

• Asset Management

The Asset Management department comprises our institutional

portfolio management activities and offers institutional customers in

Germany and abroad bespoke investment solutions in the form of spe-

cialist funds, securities portfolios and publicly offered investment

funds. Institutional customers’ take -up of these strategies remained

high in 2002.

The dynamic rate of growth in fund volumes continues undimin-

ished, as has been the case in recent years. Again, we were able to

improve the result year on year in spite of the difficult trend in the

capital markets.

In view of persistently high levels of volatility in the equity markets

and weak economic data, institutional investors have been particular-

ly interested in hedging strategies. Therefore, in March 2002, we

launched Berenberg - Institutional Euro Challenge -Universal, a publicly

offered investment fund especially for institutional investors. The hedg-

ing strategy is also offered to institutional investors as part of a direct

transaction or specialist fund mandate. Depending on the investor’s

risk tolerance level, up to 100% of the equity investments in the

specialist and publicly offered funds are hedged through the use of

futures.

All in all, the Asset Management team is responsible for the spe-

cialist funds, the securities portfolios and seven publicly offered invest-

ment funds. In addition to traditional bond fund investments – nation-

al, international and near -money market funds – we also offer themed

funds. These include two funds which focus on euro - convergence

countries and corporate bonds.

Two European equity funds with different investment styles round

off the product range. The equities for the Berenberg -Universal - Euro

equity fund, for example, are selected based on a quantitative model

and a combination of growth and value criteria.

Report of the Managing Partners

The Berenberg - Institutional Euro Challenge -Universal fund adopts

a different investment style: the sector weighting is calculated by

means of a top -down approach which analyses national economic

data and corporate ratios. Stocks are picked from within the individu-

al sectors using a bottom-up approach and based on the results of

technical and fundamental analyses. So that the funds also grow at

as stable a rate as possible during difficult periods in the market,

financial derivatives are deliberately used to hedge the fund assets.

The funds are launched together with Universal - Investment -

Gesellschaft mbH in Frankfurt or at Berenberg Lux Invest S.A. in

Luxembourg.

30

Report of the Managing Partners

31

Subsidiaries and locations

Berenberg Bank (Schweiz) AG Our Swiss subsidiary, which is active

in international portfolio management and investment advice, success-

fully concluded its fourteenth financial year. Amid difficult market

conditions, it was able to further increase the volume of customers

served.

As in previous years, the entire net profit for the year has been

transferred to reserves.

Berenberg Capital Management G.m.b.H. This subsidiary is respon-

sible for acquiring institutional business customers and for customer

service for all the Bank’s asset management mandates. With this in

mind, it has further extended its cooperation with the Asset

Management division.

2002 saw another successful series of forums and conferences

organised especially for institutional investors. Capital market issues

and current investment strategies met with a great deal of interest

among the participants, as did health as an economic factor.

The subsidiary was able to further improve its result in spite of dif-

ficult market conditions.

Berenberg Consult G.m.b.H. 2002, like the year before it, was domi-

nated by considerable uncertainty among market participants. With

the world economy in a subdued state and political conditions difficult

to predict, M&A activity continued to drop off sharply. Against this

backdrop, we were particularly pleased to have successfully con-

cluded seven transactions during 2002, the majority of which involved

US buyers.

In the course of last year, we advised on transactions in the mer-

gers & acquisitions, privatisation and buyout segments. 2002 was

the first year in which no transaction was concluded in the buyout

segment.

For 2003, we will strengthen our team by adding staff with exper-

tise in derivative financing instruments. We look to the coming finan-

cial year with confidence even though economic conditions do not sig-

nal an easier year for the dwindling M&A market.

Berenberg Finanzanlagen Beratungs- und Vermittlungsgesell-

schaft m.b.H. We continued to broaden our activities by successful-

ly placing Berenberg Private Capital No.1, a fund -of - funds for priva-

te equity investment programs. A significant increase in the volume of

investment products also contributed to the good result for the year.

Aware of the tax changes and focusing on “safe” capital investments,

investors turned to real estate funds, particularly foreign funds.

Furthermore, we were able to meet requirements with regard to

inheritance/gifts and address problems resulting from company sales

by offering our customers individual solutions.

The range of services offered by the Financial Planning department

was significantly extended. The knowledge gained from the analysis of

closed real estate funds was used to develop a real estate tool with

a view to advising on rental properties. As well as offering tax optimis-

ation processes, this company is able to calculate financing alternati-

ves and illustrate different scenarios for the letting and sale of pro-

perties. It has also been possible to evaluate the remuneration con-

sulting service on the basis of the analysis and assessment of existing

holdings.

Due to the findings of a number of interviews between customers

and advisors and the results from the Financial Planning division, the

issue of asset structuring is being more closely examined. Customers

increasingly seek competent, product - independent advice that goes

beyond investment advice to include aspects such as securing their

standard of living and preserving their assets. This has resulted in the

newly developed SIGMA asset model, which is based on Markowitz’s

modern portfolio theory. The analysis now includes not only the com-

mon asset classes, i.e. equities, bonds and cash, but also shipping

Report of the Managing Partners

32

investments, commercial real estate, residential real estate, priva-

te equity and insurance. This model helps us to identify the weak-

nesses in a portfolio and put forward suggestions for the portfolio’s

optimisation.

Berenberg Lux Invest S.A. This investment company, a subsidiary of

our Bank, issues public funds under Luxembourg law. We have now

issued a series of speciality funds for institutional customers and

wealthy private individuals.

Berenberg Real Estate Services G.m.b.H. This company achieved

a satisfactory result in a weak economic environment. The Brokerage

department’s transaction with an American fund management com-

pany that purchased a logistics portfolio in Germany is worth high-

lighting in this report. Taking this successfully concluded transaction

as an example, the company intends to win American pension funds

for further and larger investments in Germany. Meanwhile, talks are

being held with German sales companies with the aim of placing US

real estate funds in the multi - family segment in Germany.

In 2002, a link with the Private Banking department was formal-

ised – in conjunction with an increase in headcount – in an effort to

firmly establish real estate investments as a component of financial

planning for private customers. Last year, the cooperation generated

four transactions. In 2003, the emphasis will be placed on rental pro-

perty investments.

The other areas of activity, such as asset management and invest-

ments, developed according to plan.

Report of the Managing Partners

33

Branches and representative offices

Our branches and representative offices in Germany, which are active

in regional portfolio management and investment advice, experienced

different business trends. We have therefore concentrated our

resources on those regions which we believe harbour promising mar-

ket potential.

Frankfurt Amid difficult conditions, the Frankfurt branch achieved a

result on a par with the previous year. The number of staff was increased

in order to strengthen customer service and business development

activities. We will continue to pursue our strategy of targeting both

wealthy private customers and independent portfolio managers in

central and southern Germany.

Bremen Once again, our representative office in Bremen achieved

pleasing results in each of its business divisions. The office was able

to build up relationships with new customers and thereby significant-

ly increase the volume of customers it serves. Consequently, we have

further increased the number of staff at this representative office.

Luxembourg Our branch in Luxembourg was able to maintain its

position in a worsening business environment. The focus remains on

our internationally - orientated and increasingly institutional clientele.

In future, the branch will also focus on the “large region” beyond

Luxembourg’s borders.

Shanghai Hamburg’s First Mayor, Ole von Beust, officially opened our

representative office in Shanghai during a state visit to China in May.

We will continue to attach particular importance to China as a main

market in future (see also commentary on page 19).

Report of the Managing Partners

34

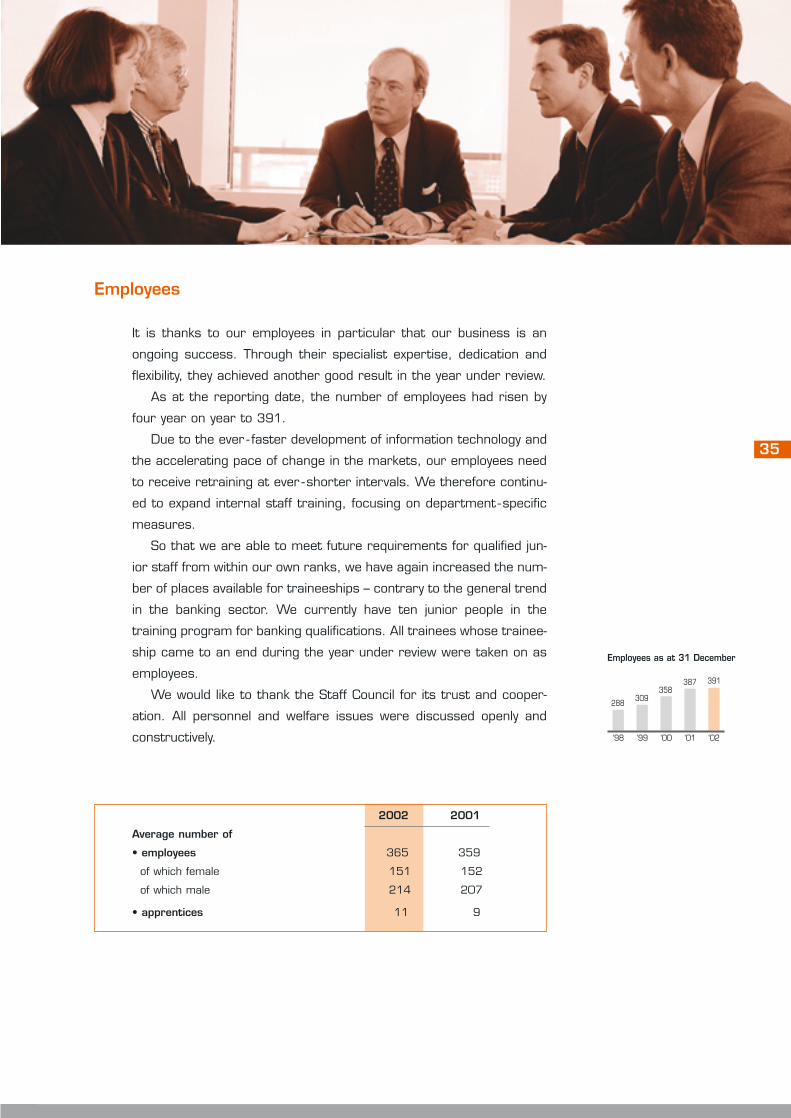

Employees

It is thanks to our employees in particular that our business is an

ongoing success. Through their specialist expertise, dedication and

flexibility, they achieved another good result in the year under review.

As at the reporting date, the number of employees had risen by

four year on year to 391.

Due to the ever - faster development of information technology and

the accelerating pace of change in the markets, our employees need

to receive retraining at ever - shorter intervals. We therefore continu-

ed to expand internal staff training, focusing on department - specific

measures.

So that we are able to meet future requirements for qualified jun-

ior staff from within our own ranks, we have again increased the num-

ber of places available for traineeships – contrary to the general trend

in the banking sector. We currently have ten junior people in the

training program for banking qualifications. All trainees whose trainee-

ship came to an end during the year under review were taken on as

employees.

We would like to thank the Staff Council for its trust and cooper-

ation. All personnel and welfare issues were discussed openly and

constructively.

35

2002 2001

Average number of

• employees 365 359

of which female 151 152

of which male 214 207

• apprentices 11 9

‘98

Employees as at 31 December

288309

358387 391

‘99 ‘00 ‘01 ‘02

Report of the Managing Partners

36

Review of the year

Companies are increasingly required to show their social commit-

ment. In 2002 we again organised or took part in numerous public

events and activities. A selection:

Prof. Dr. Thomas Straubhaar, President of the Hamburg Institute

of International Economics (HWWA), gave a talk on economic and

interest - rate developments in 2002.

Markus Koch, n - tv correspondent in New York, reported on his expe-

riences and adventures on Wall Street.

“Bremen Chair” visits Berenberg Bank 60 members of “The 1801

Union”, an association for the Bremen business community, made their

annual trip to Berenberg Bank in Hamburg. It is traditional for someone

to sit in the “Bremen Chair” – brought along especially for the occa-

sion – and answer the questions put by the Bremen entrepreneurs.

Berenberg Bank Foundation awards the Culture Prize 1990

Dedicated in particular to promoting young artistic talent, this

foundation was set up in our 400 th year. The Culture Prize 2002

went to cellist Niklas Eppinger (pictured with Joachim v. Berenberg -

Consbruch).

EUR 150,000 for disabled children A princely sum of money was

raised at the charity golf tournament organised in Bad Griesbach by

the Franz Beckenbauer Foundation and the Kids Care Foundation with

the support of Berenberg Bank. Joachim v. Berenberg -Consbruch

presents the cheque to Franz Beckenbauer and Edmund Krix.

Official opening of the representative office in Shanghai Ham-

burg’s First Mayor, Ole von Beust, opened our representative office

during a visit to China. The ceremony was attended by high - ranking

representatives of the city’s government and business community.

Report of the Managing Partners

37

Berenberg Polo Derby Spectators flocked to the Hamburg Polo

Club’s ground in Klein Flottbek for the Berenberg Polo Derby. With the

sun shining overhead, the Berenberg team won the derby cup in what

was the 100 th year of the competition.

Berenberg and n - tv run stock market game for university stu-

dents In cooperation with the news channel n - tv, we run a stock mar-

ket game in which economics students from five universities take

part. n - tv reports each Friday.

Investors conference Representatives of 60 institutional investors

were invited by Berenberg Bank to meet directors of DAX companies

to discuss their strategy and development. Dr. Hans -Walter Peters

with Deutsche Telekom’s finance director, Dr. Karl - Gerhard Eick.

China Weeks Hamburg’s citizens were given the opportunity to learn

more about China at around 100 events organised by the Chinese -

German Society and the East Asian Association. As the main sponsor

of the China Weeks, we exhibited a collection of Chinese snuffboxes

at the Bank.

“A Winter on Majorca” Hannelore Elsner and Sebastian Knauer

(first person to receive a scholarship grant from the Berenberg Bank

Foundation; pictured with Claus -G. Budelmann) presented their new

CD at two events held in Hamburg and Frankfurt. We supported the

CD’s release as part of our cultural support program.

A Thank You to our customers

Our thanks go to our customers and business friends for their trust

and successful cooperation. We will continue to strive to meet their

individual wishes and to be a reliable service - orientated partner.

Management Report

Overview Berenberg Bank was successful in further expanding its

business activities in 2002 – contrary to the general market trend.

More specifically, investment advisory activities and portfolio manage-

ment generated another noteworthy result, reflecting an increase in

commissions. The Bank was able once again to prove its particular-

ly strong expertise in the areas of lending, international business,

securities and foreign currency trading, and derivatives.

Although the expansion of the Bank’s business activities enabled it

to post a good result, this expansion also led to a further increase in

costs, as the average number of employees rose slightly. The Frank-

furt and Luxembourg branches and the representative offices in

Bremen and Shanghai also contributed to this success.

Equity The issued capital was increased by EUR 7.5 million. The reve-

nue reserves of EUR 10 million were, in addition, converted into issued

capital, as a result of which the Bank’s total capital stands at EUR 117.5

million at year -end. Liable equity stands at EUR 125,169,000.

With this equity available to us, we are able to continue fulfilling all

legal requirements with regard to the Bank’s capital. The ratio accord-

ing to Principle I stood at 10.8% at year -end.

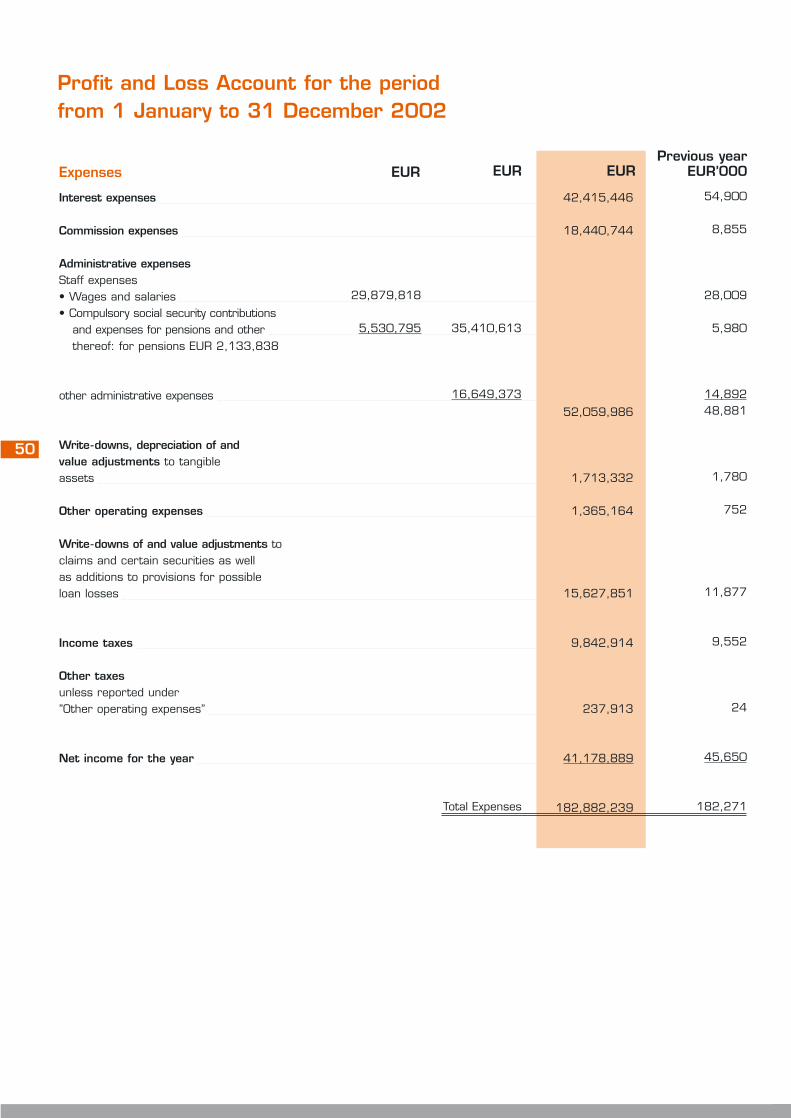

Net profit for the year The net profit for the year rose from EUR

40,763,000 to EUR 41,179,000. However, it must be remembered

that approx. EUR 5 million were transferred to revenue reserves in

2001. Rising staff costs and higher operating expenditure have

caused the ratio of income to costs to fall from 231% to 224%. This

equates to a cost/income ratio of 45% (previous year: 43%). The

ratio of net interest income to net commission income remains

unchanged at 30:70 (30:70).

38

Management report

39

Notes on the income statement

Net interest income Falling interest rates in the money and capital

markets meant deposit operations and investments of equity capital

generated lower margins. This was offset by a further rise in cus-

tomer deposits. The generally gratifying income posted by the Bank’s

subsidiaries has been fully retained. As a result, net interest income

fell 7.8% to EUR 30,153,000.

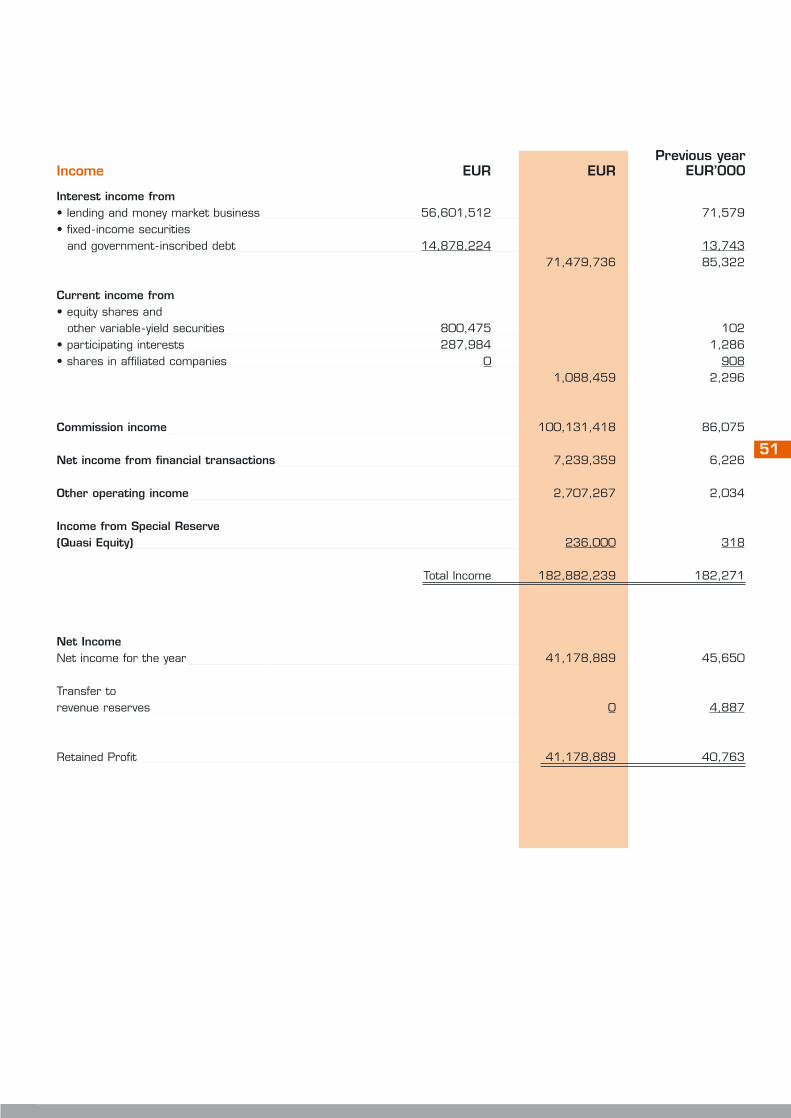

Net commission income Net commission income rose 5.8% in the

year under review, from EUR 77,220,000 to EUR 81,691,000.

Although conditions in the stock markets remained adverse in 2002,

the large volume of new business in each of the securities depart-

ments was more than enough to offset the negative volume effects of

falling stock prices and therefore made a substantial contribution to

the rise in net commission income. The Bank was also able to in-

crease commissions from international business and foreign curren-

cy dealing.

Trading income Again, the low value -at - risk limits were success-

fully applied in each of the trading departments. Consequently, net

income from financial transactions rose from EUR 6,226,000 to

EUR 7,239,000. Although the departments responsible for foreign

currency and derivatives trading improved on their results, the Bank

felt the effects of the principle of imparity, just as it did the year befo-

re. Securities trading also generated a gratifying result in spite of the

conditions in the stock markets.

Administrative expenses Administrative expenses including depre-

ciation and amortisation rose by EUR 3,112,000 to EUR 53,733,000.

Staff costs account for EUR 35,411,000 of the total, an increase of

EUR 1,421,000 or 4.2%. The rise in staff costs is principally a result

of the slight increase in the average number of staff, but there is also

increased remuneration on account of the good results for the year.

The constantly increasing demands on the information systems and

the need for more office space pushed operating expenditure higher.

Provision for risks Sufficient amounts have been added to provisions

and write -downs on loan balances to cover exposure to risk. Specific

tax allowable provisions (§ 340f German Commercial Code) were

again increased at year -end.

We have made adequate provision for all known lending risks using

prudent valuation measures.

Notes on the financial position

Balance sheet total and volume of business The balance sheet

total rose 9.6% in the year under review, from EUR 1,772 million to

EUR 1,943 million. On the assets side, claims on banks rose 21.0%

to EUR 554 million (EUR 458 million), while customer borrowings fell

5.2% to EUR 796 million (EUR 840 million). On the liabilities side,

there was a renewed reduction in liabilities to banks and a further

increase in customer deposits. Thus bank deposits were reduced by

24.1% to EUR 122 million (EUR 161 million), while customer deposits

rose 9.8% to EUR 1,512 million (EUR 1,377 million).

The portfolio of bonds and other fixed - interest securities was

increased by EUR 119.3 million to EUR 357.9 million. Securities which

matured in 2001 were replaced and transactions aimed at replac-

ing loans were conducted in a conscious effort to reduce claims on

customers.

Equities and other variable - rate securities fell by EUR 87.2 million

to EUR 64 million, as special trades were completed as planned. At

year -end, the portfolio contained EUR 30.7 million of equities, but, as

there are pledged deposits and option arrangements (purchase of put

options) in place and given the good standing of the other parties

involved, we do not see any risk associated with these equities.

Management report

40

As part of its liquidity reserves, the Bank also holds EUR 9.7 milli-

on (EUR 9.8 million) in participation certificates issued by German

banks and insurance companies.

The bearer bonds issued in 2001 matured during the year under

review and were duly wound up.

The volume of business increased by 8.4% from EUR 1,968 mil-

lion to EUR 2,134 million, in line with the increase in the balance

sheet.

Volume of lending The Bank’s total volume of lending fell by EUR 48

million during the year under review to EUR 989 million. The principal

lending balances were claims on customers (EUR 796 million) and, to

a lesser extent, securities. Off - balance sheet amounts primarily inclu-

de loan facilities not yet drawn down and contingent claims on guar-

antees and other indemnity commitments. Derivatives business requi-

res relatively small levels of capital maintenance, as the Bank applies

the “internal model”.

Risk monitoring

When conditions in our markets are deteriorating, it is extremely

important to accurately identify, measure and manage each of the

risks associated with the Bank’s business. Only if we adequately meas-

ure our risk exposure in relation to our returns can we operate suc-

cessfully as a business.

For several years now, the Bank has been using a risk -adjusted

system of bank management, which was further refined during the

course of the last financial year. As well as market price, customer

default, liquidity and operational risks, the Bank’s risk management

system also analyses profitability risks.

Management report

41

The risk -based capital (economic capital) available to the Bank is

quantified as part of the annual budgeting process. The exposure of

the Bank’s various business divisions to potential losses is quantified

in respect of each risk category separately according to the value -at -

risk principle.

The Management Board sets out the principles of risk policy. A

central controlling department acting independently of the various

market divisions is responsible for the systems for bank and risk

management. The success of the business divisions is monitored by

means of a monthly overall calculation and analysed by means of vari-

ance analyses.

The risks entered into by the business divisions are quantified by

the Risk Control department. This department is responsible in parti-

cular for monitoring market price risks, which arise from both short-

term positions in the trading book and strategic positions in the

investment book.

- A credit risk management team, independent of the lending

department, monitors exposure to loan default risks.

- The Treasury department is responsible for monitoring and

managing liquidity risks together with the money market desk.

Operational risks are minimised through the use of a comprehensive

procedures manual and through contingency plans.

- The Bank’s internal auditors carry out regular checks to ensure

adherence to the individual organisational procedures.

The Bank’s existing risk management systems are constantly

being enhanced and refined in order to accommodate the imminent

changes to the general requirements set out by industry regulators.

The “Minimum requirements for the lending activities of banks” (MAK),

which are likely to come into force from 2004, and “The new Basel

capital accord” (Basel II) will have a particularly marked impact on the

risk management of lending activities. During the last financial year,

the necessary measures were taken to ensure that, by the time they

finally come into force, we are able to implement the regulations in a

way that accommodates our needs.

Management report

42

Management report

Market price risks Market price risks result from fluctuations in

interest rates, quoted share prices and foreign exchange rates.

The Bank uses its internally - developed risk measurement system

to manage market price risks arising from proprietary trading posi-

tions. This system is recognised by the banking supervisory authori-

ties as an internal risk model in accordance with Principle I for quan-

tifying market price risks from open trading positions.

A Monte Carlo simulation is used to calculate a daily value -at - risk

measure for all positions subject to market price risks. For a particu-

lar level of probability, the value -at - risk calculation indicates the

maximum loss on a portfolio. In accordance with the stipulations of

Principle I, a 99% confidence interval and ten -day holding period are

assumed for these value -at - risk calculations. Risk factors are analy-

sed historically: discount rates for interest calculations, share indices

for the equity element and currency exchange rates for foreign cur-

rency positions.

The quality of the value -at - risk forecasts is checked back against

actual daily outcomes and analysed over time. On the following trading

day, the forecast is compared with the changes in value that would

have occurred assuming the positions were unchanged. Assuming a

confidence level of 99%, the value -at - risk forecast should only be

exceeded by a higher hypothetical loss on 1% of all trading days ana-

lysed. In fiscal 2002, back - testing revealed only one such instance.

This is below what can statistically be expected and therefore meets

the regulator’s requirements.

As the value -at - risk method only indicates the risk status of posi-

tions in “normal” market conditions and fails to take into account

extreme market situations, the analyses are supplemented with daily

worst - case analyses.

43

Every dealing section has worst - case limits in addition to the

value -at - risk limits and these must be adhered to daily. The Risk

Control department, which is separate from the trading divisions right

up to the top management board level, provides a summary of the

risk positions in a single risk report and ensures the appropriate infor-

mation is available to the Management Board daily.

Loan default risks Loan default risks result both from traditional

lending activity as well as from derivative trading.

A credit risk management team, independent of the lending

department, is responsible for overseeing credit risks, although it

does not just carry out regular controlling activities but also casts a

second vote on lending decisions in addition to that cast by the mar-

ket division. As a result, the Bank already fulfils the majority of the

“MAK” requirements with regard to the separation of market divisions

and divisions carrying out subsequent activities. The lending depart-

ment and the credit risk management team are also supported by an

independent financial analysis unit, which carries out regular checks

on the creditworthiness and financial standing. In addition, the Risk

Control department is responsible for analysing entire portfolios.

A rating system, developed by ourselves based on expert know-

ledge and taking into account both financial and qualitative factors, is

used to calculate standard risk costs.

In addition to the statistically expected credit risks, which are taken