Embed Size (px)

Citation preview

Annual Financial Statements 2016

CHARTING A NEW COURSE

Contents

Annual financial statements

Directors’ responsibility statement 2

Secretarial certification 2

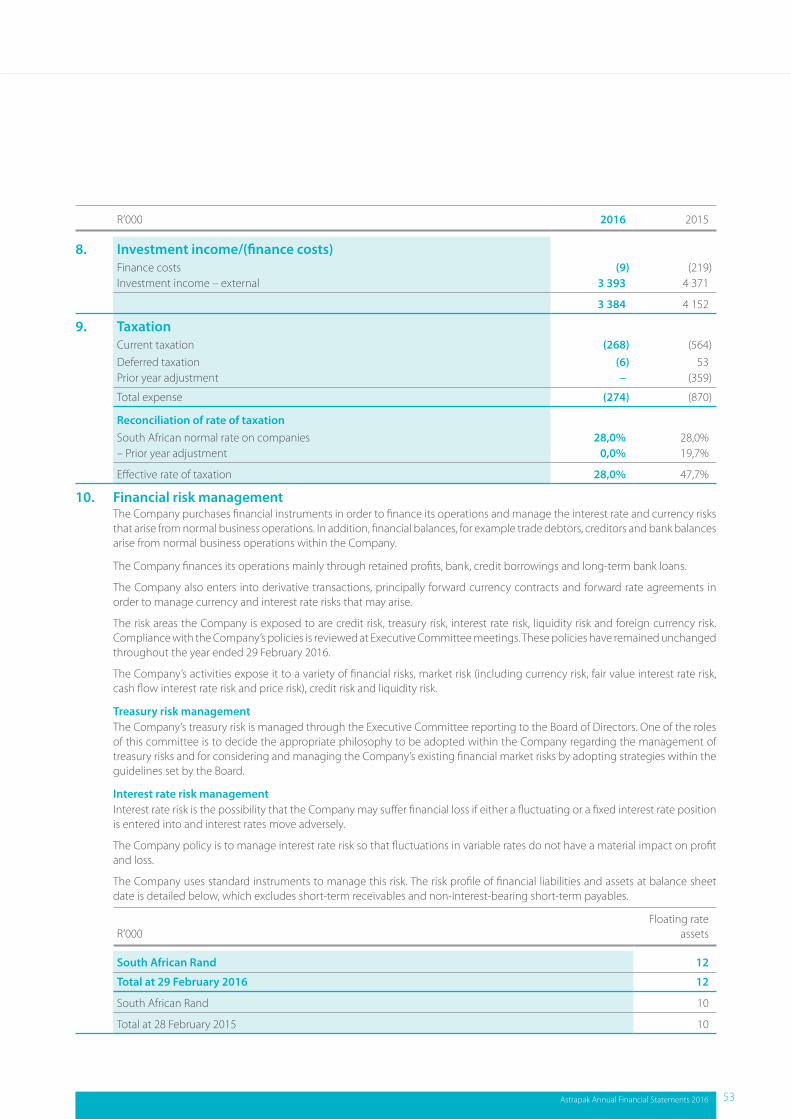

Independent auditors’ report 3

Directors’ report 4

Directors’ interest in shares 6

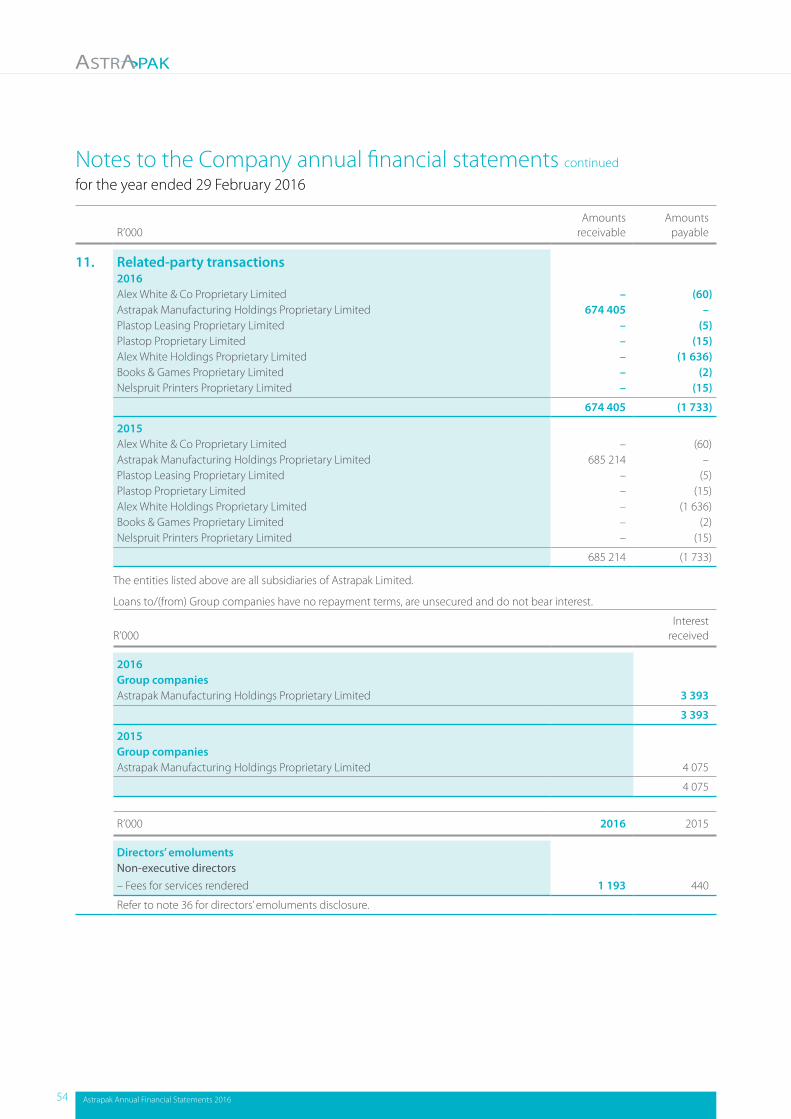

Audit Committee report 7

Group statement of financial position 8

Group statement of comprehensive income 9

Group statement of changes in equity 10

Group statement of cash flows 11

Significant accounting policies 12

Notes to the Group annual financial statements 21

Company annual financial statements 50

Annexure 1 – Related parties 58

Annexure 2 – Details of land and buildings 59

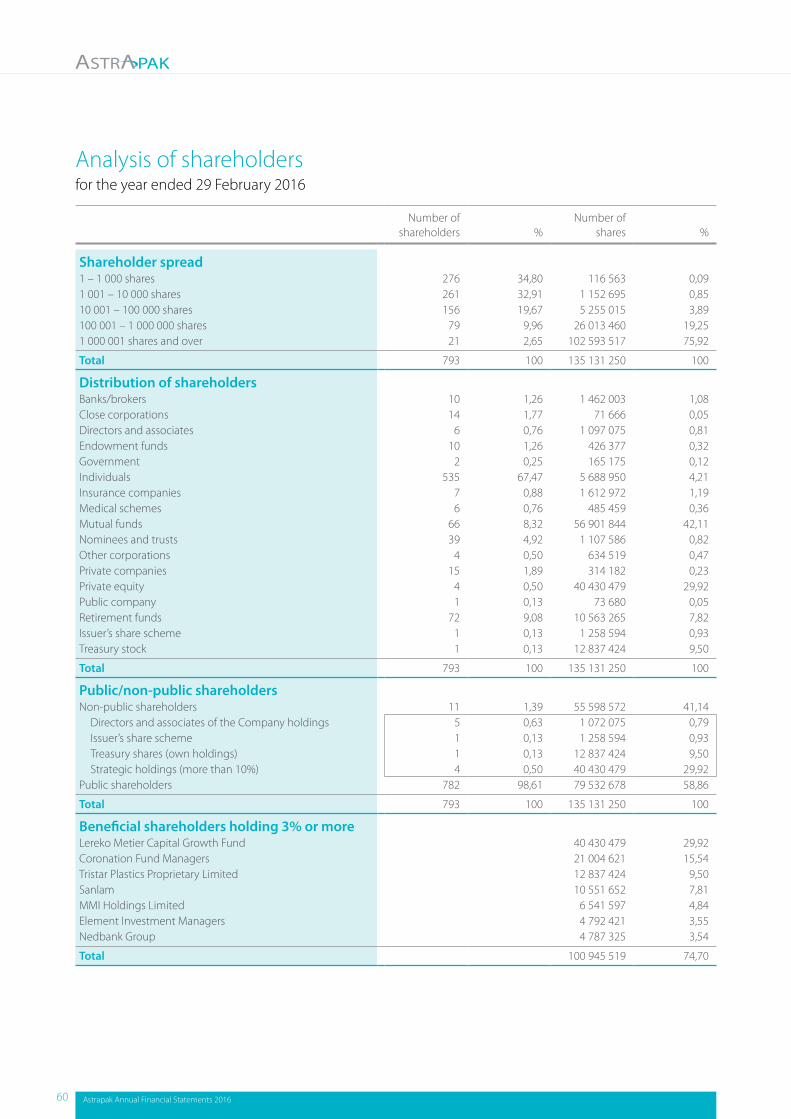

Analysis of shareholders 60

General information IBC

Shareholders’ diary IBC

Astrapak Annual Financial Statements 2016 1

Directors’ responsibility statementfor the year ended 29 February 2016

safeguard, verify and maintain accountability of assets, and to prevent and detect material misstatement and loss. The systems are implemented and monitored by suitably trained personnel with an appropriate segregation of authority and duties. Nothing has come to the attention of the directors to indicate that any material breakdown in the functioning of these controls, procedures and systems has occurred during the year under review.

The consolidated and separate financial statements are prepared on a going-concern basis. Nothing has come to the attention of the directors to indicate that the Group and Company will not remain going concerns for the foreseeable future.

These consolidated and separate financial statements were prepared by Salome Ratlhagane CA(SA) (Group Financial Manager) under the supervision of Manley Diedloff (Group Managing Director and Chief Financial Officer).

The directors of the Company are responsible for the maintenance of adequate accounting records and the preparation and integrity of the annual financial statements and related information. The annual financial statements have been prepared in accordance with the Companies Act of South Africa, International Financial Reporting Standards of the International Accounting Standards Board, SAICA Financial Reporting Guide as issued by the Accounting Practices Committee and the Interpretations issued by the IFRS Interpretations Committee.

The Group’s independent auditors, Deloitte & Touche, have audited the annual financial statements and their unmodified report appears on page 3.

The directors are also responsible for the systems of internal control. These are designed to provide reasonable, but not absolute, assurance as to the reliability of the annual financial statements, and to adequately

These financial statements were audited in compliance with section 29(1)(e)(i)(aa) of the Companies Act, No 71 of 2008.

The financial statements set out on pages 8 to 57 were approved by the Board of Directors and are signed on its behalf by:

M DiedloffGroup Managing Director and Chief Financial Officer

R MooreChief Executive Officer

Denver19 April 2016

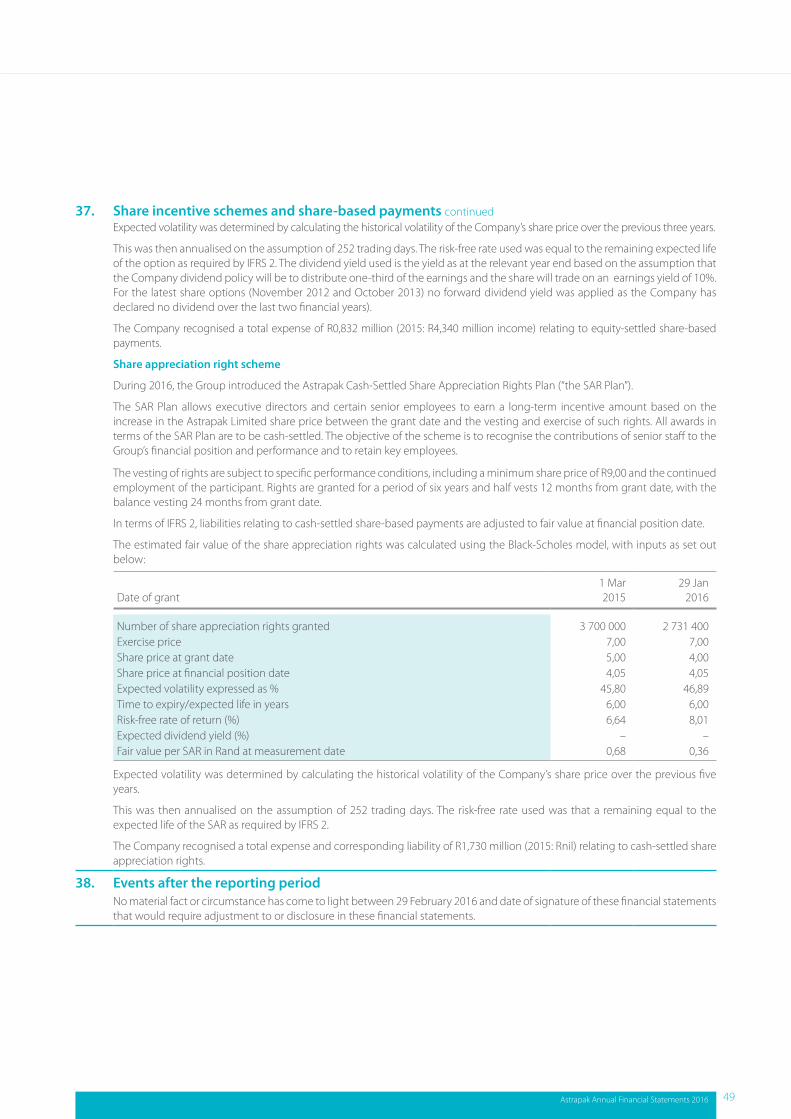

In accordance with section 88(2)(e) of the Companies Act, No 71 of 2008, it is hereby certified that, to the best of my knowledge, the Company has lodged with the Registrar of Companies all such returns as are required of a public company in terms of the Act and that such returns are true and correct for the financial period ended 29 February 2016.

Salome RatlhaganeCompany Secretary

Denver19 April 2016

Secretarial certificationfor the year ended 29 February 2016

2 Astrapak Annual Financial Statements 2016

Independent auditors’ report for the year ended 29 February 2016

material misstatement of the financial statements, whether due to fraud or error. In making those risk assessments, the auditor considers internal control relevant to the entity’s preparation and fair presentation of the financial statements in order to design audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the entity’s internal control. An audit also includes evaluating the appropriateness of accounting policies used and the reasonableness of accounting estimates made by management, as well as evaluating the overall presentation of the financial statements.

We believe that the audit evidence we have obtained is sufficient and appropriate to provide a basis for our audit opinion.

OpinionIn our opinion, the consolidated and separate financial statements present fairly, in all material respects, the consolidated and separate financial position of Astrapak Limited as at 29 February 2016, and its consolidated and separate financial performance and consolidated and separate cash flows for the year then ended in accordance with International Financial Reporting Standards and the requirements of the Companies Act of South Africa.

Other reports required by the Companies ActAs part of our audit of the consolidated and separate financial statements for the year ended 29 February 2016, we have read the directors’ report, the Audit Committee’s report and secretarial certification for the purpose of identifying whether there are material inconsistencies between these reports and the audited consolidated and separate financial statements.

TO THE SHAREHOLDERS OF ASTRAPAK LIMITEDWe have audited the consolidated and separate financial statements of Astrapak Limited as set out on pages 8 to 57 which comprise the statements of financial position as at 29 February 2016, and the statements of comprehensive income, the statements of changes in equity, the statements of cash flows for the year then ended, and the notes which include a summary of significant accounting policies and other explanatory information.

Directors’ responsibility for the consolidated financial statements The Company’s directors are responsible for the preparation and fair presentation of these consolidated and separate financial statements in accordance with International Financial Reporting Standards and the requirements of the Companies Act of South Africa, and for such internal control as the directors determine is necessary to enable the preparation of consolidated and separate financial statements that are free from material misstatement, whether due to fraud or error.

Auditors’ responsibilityOur responsibility is to express an opinion on the consolidated and separate financial statements based on our audit. We conducted our audit in accordance with International Standards on Auditing. Those standards require that we comply with ethical requirements and plan and perform the audit to obtain reasonable assurance about whether the financial statements are free from material misstatement.

An audit involves performing procedures to obtain audit evidence about the amounts and disclosures in the financial statements. The procedures selected depend on the auditor’s judgement, including the assessment of the risks of

These reports are the responsibility of the respective preparers. Based on reading these reports, we have not identified material inconsistencies between these reports and the audited consolidated and separate financial statements. However, we have not audited these reports and accordingly do not express an opinion on these reports.

Report on other legal and regulatory requirementsIn terms of the Independent Regulatory Board for Auditors (“IRBA”) Rule published in Government Gazette Number 39475 dated 4 December 2015, we report that Deloitte & Touche has been the auditor of Astrapak Limited for 21 years.

Deloitte & ToucheRegistered AuditorsPer Corinne RingwoodPartner

19 April 2016

National executive: *LL Bam (Chief Executive),*AE Swiegers (Chief Operating Officer), *GM Pinnock (Audit), *N Sing (Risk Advisory), *NB Kader (Tax), TP Pillay (Consulting), S Gwala (BPaaS), *K Black (Clients and Industries), *JK Mazzocco (Talent and Transformation), *MJ Jarvis (Finance), *M Jordan (Strategy), *MJ Comber (Reputation and Risk), *TJ Brown (Chairman of the Board)*Partner and Registered Auditor

A full list of partners and directors is available on request.

B-BBEE rating: Level 2 contributor in terms of Chartered Accountancy Profession Sector Code

Associate of Deloitte Africa, a member of Deloitte Touche Tohmatsu Limited

Astrapak Annual Financial Statements 2016 3

Directors’ reportfor the year ended 29 February 2016

plastic packaging products. The Group has manufacturing facilities in all main centres of South Africa and has annualised revenues of R1,348 million. The operations are grouped into various

DirectorsThe names of directors of Astrapak are listed on page IBC of these annual financial statements.

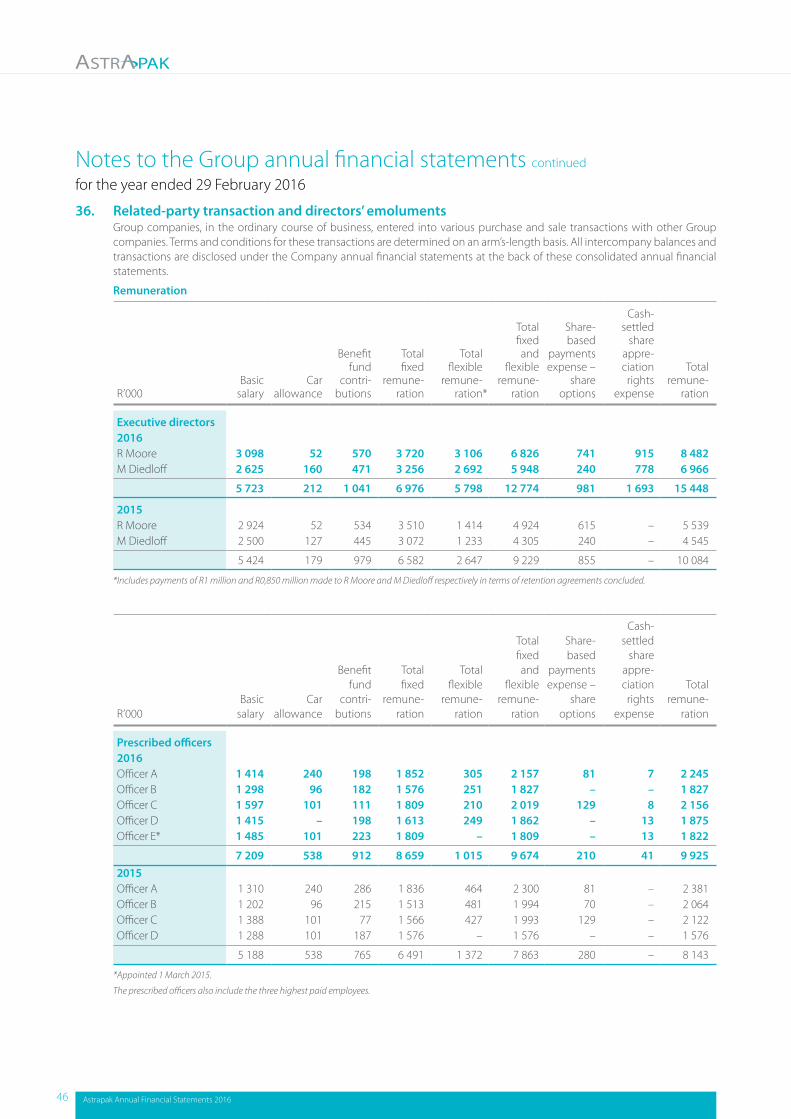

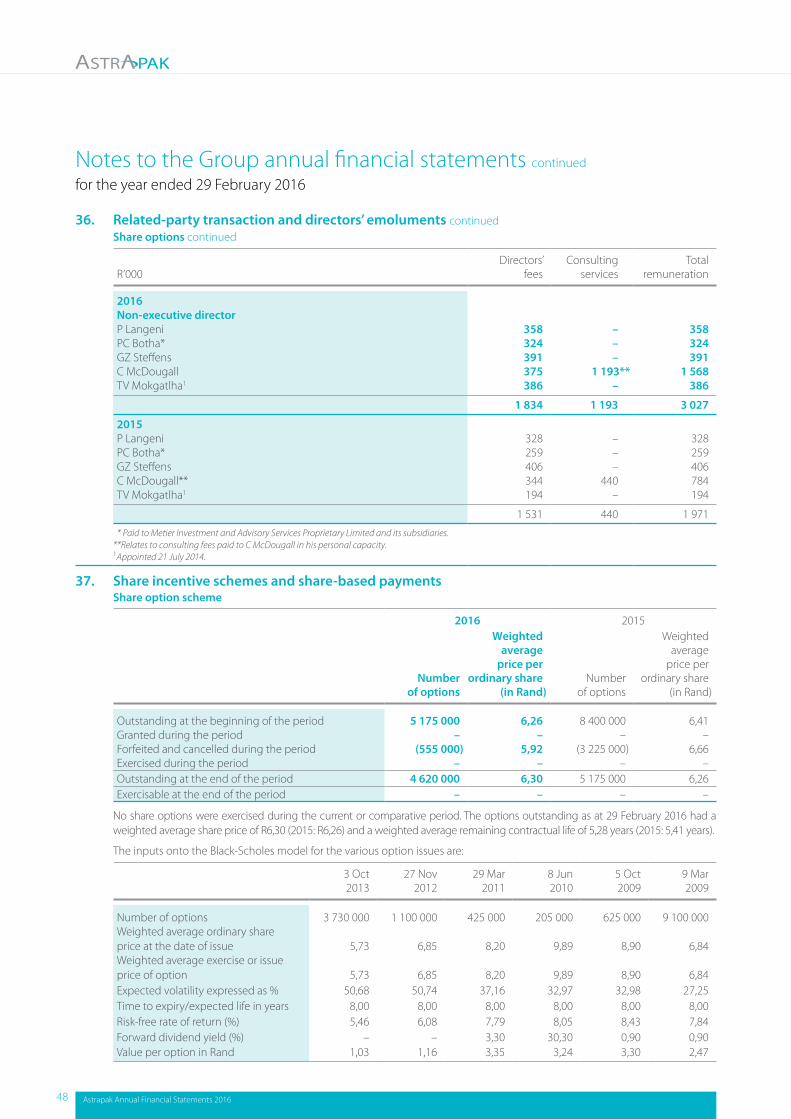

Directors’ remunerationThe aggregate remuneration and benefits paid to the executive and non-executive directors of the Group for the year ended 29 February 2016 are set out in note 36 of these financial statements.

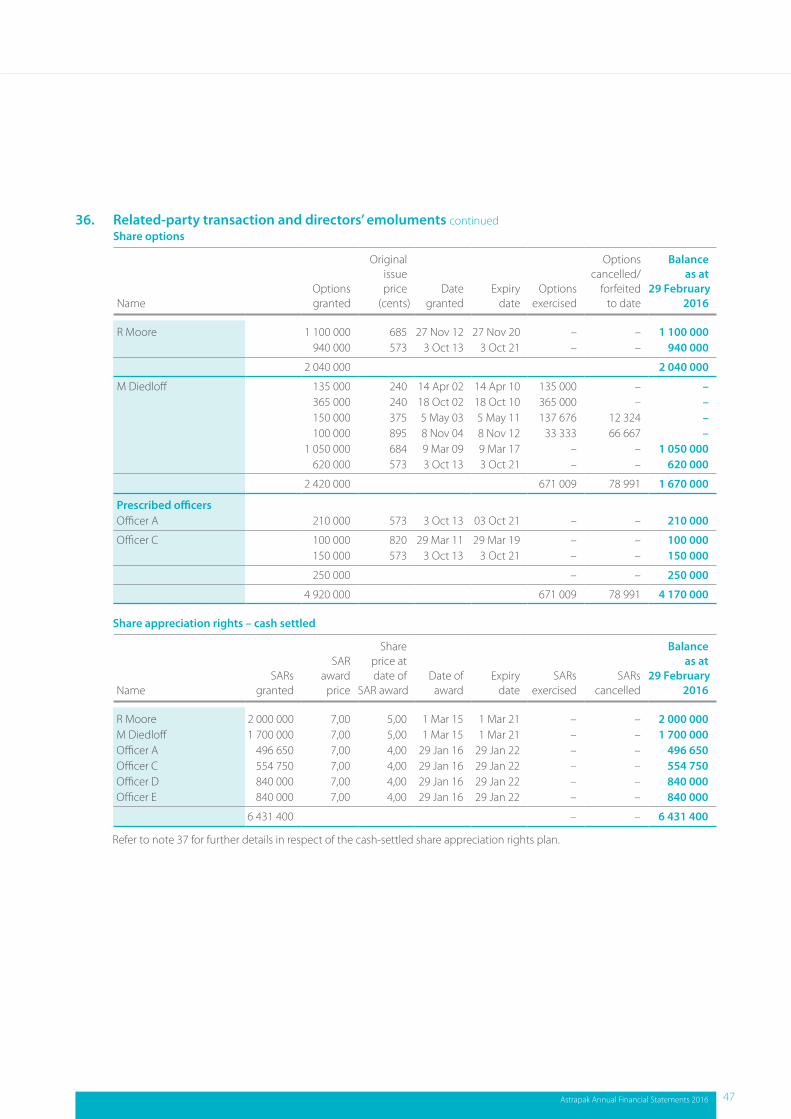

Astrapak Limited Share Option SchemeFurther details on the Astrapak Limited Share Option Scheme (“the scheme”) and the number of options issued to executive directors in terms of such scheme are set out in note 36 of these annual financial statements.

Property, plant and equipmentDuring the year, the Group acquired property, plant and equipment to the value of R132,4 million (2015: R158,0 million).

Nature of businessAstrapak Limited and its subsidiaries (“Astrapak” or the “Company” or the “Group”) are manufactures and distributors of an extensive range of

Authorised and issued share capitalDetails of the authorised share capital are given in note 11 to the financial statements. No changes occurred during the year.

Preference sharesThe non-redeemable, non-participating, cumulative preference shareholders will receive, if declared, dividends which are payable by 31 March and 30 September each year. Dividends are calculated based on 88,89% of the average daily prime rate which prevailed in respect of the relevant period for which the dividend is calculated.

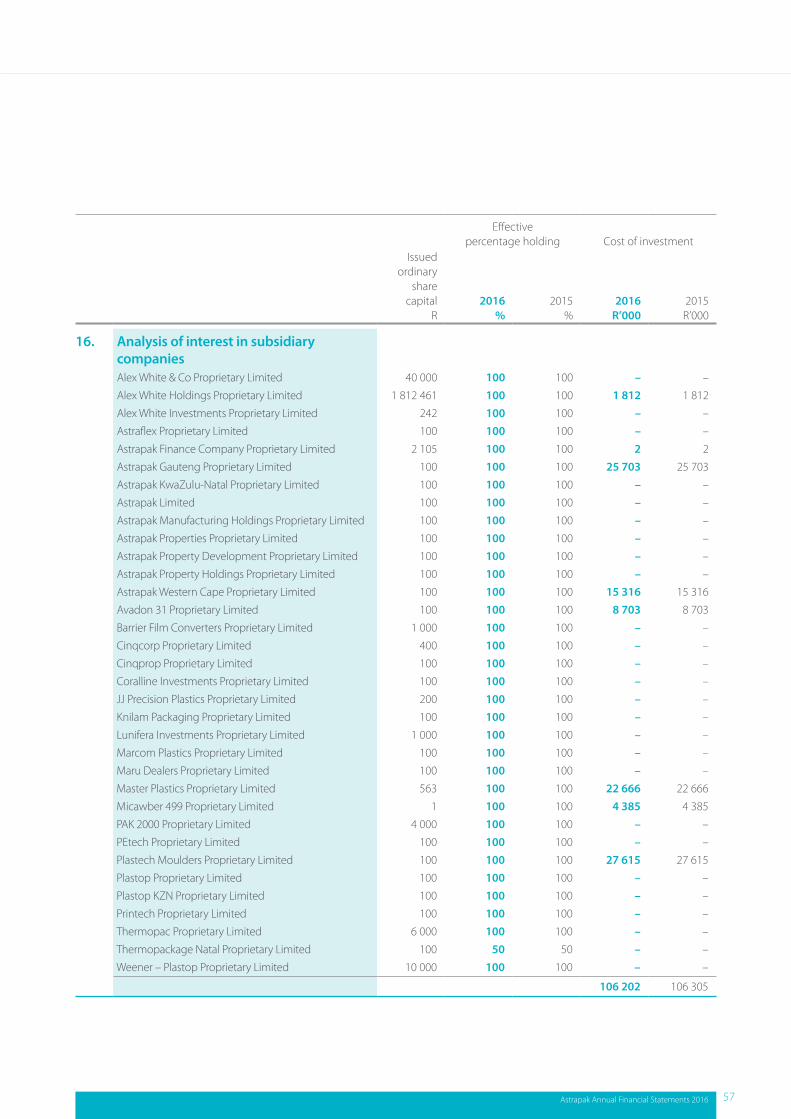

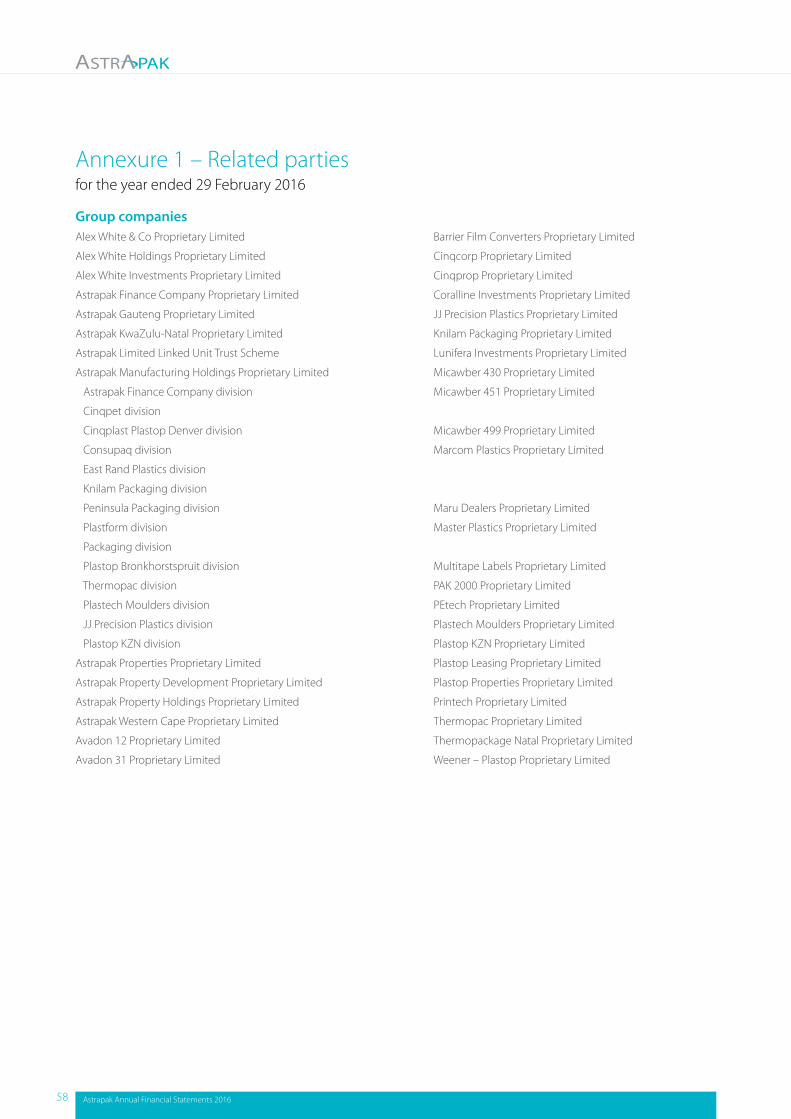

SubsidiariesThe list of all parties related to the Company during the year ended 29 February 2016 is disclosed in Annexure 1 to the financial statements.

A number of special resolutions were passed by subsidiary companies. None of these resolutions are of significance to the shareholders in assessing the state of affairs of the Group.

business segments and service mainly the food, beverage, personal care, pharmaceutical, agricultural, industrial and retail markets.

Plant and machinery were not impaired in the current year and prior year impairments were R38,6 million.

Directors’ service contractsAll executive directors and prescribed officers have service level agreements in place.

Distribution to ordinary shareholdersAstrapak has not declared an ordinary dividend in respect of the financial year ended 29 February 2016 (2015: Rnil).

Litigation statementIn terms of the JSE Listings Requirements, the directors, whose names appear on page IBC of these financial statements, have confirmed that they are not aware of any legal or arbitration proceedings, including proceedings that are pending or threatened, that may have or have had in the recent past, being at least the previous 12 months, a material effect on the Group’s financial position.

Trading results2016

R’0002015R’000

Revenue 1 348,4 1 388,6Profit from operations before exceptional items 44,3 61,5Profit/(loss) for the year 21,2 (122,3)Loss attributable to ordinary shareholders (3,3) (138,5)Attributable to preference shareholders of the parent 12,7 10,9Loss per ordinary share (cents) (2,7) (114,4)Headline loss per ordinary share (cents) (14,1) (71,5)

4 Astrapak Annual Financial Statements 2016

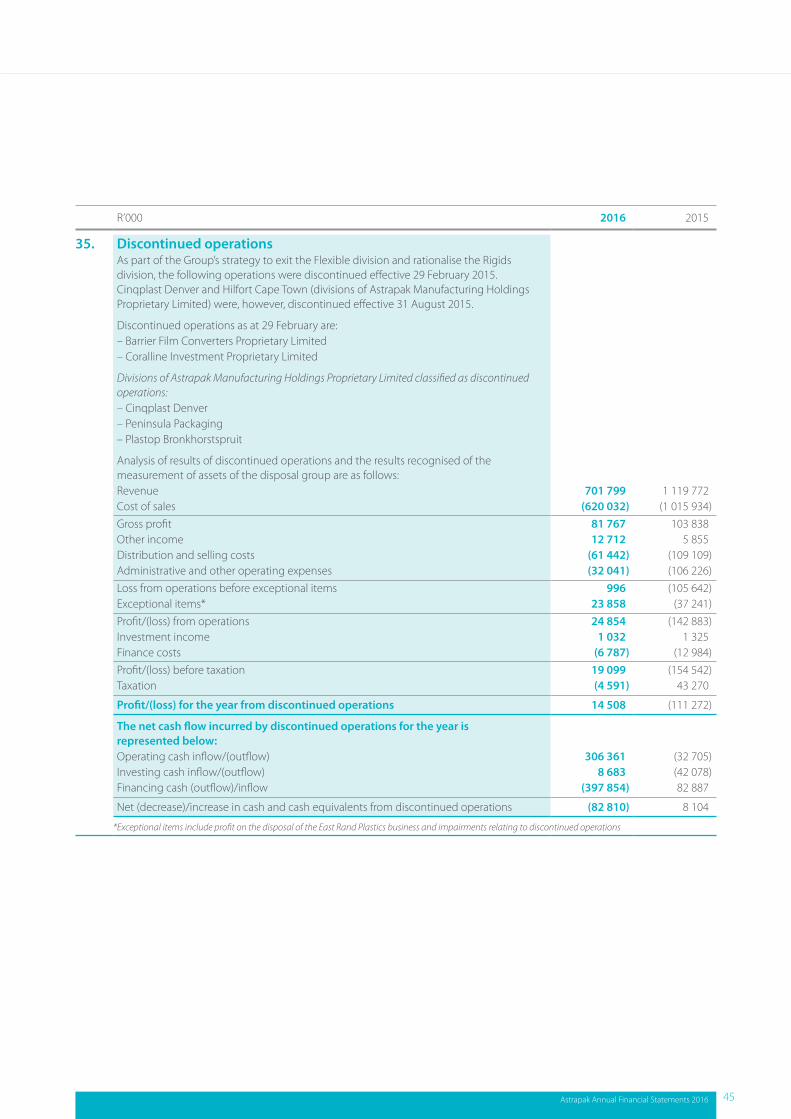

As at 29 February 2016, entities included in discontinued operations and assets classified as held-for-sale are as follows:

Flexible › Barrier Film Converters Proprietary

Limited (held-for-sale). › Coralline Investment Proprietary

Limited (held-for-sale).

Flexible divisions which are divisions of Astrapak Manufacturing Holdings Proprietary Limited › Peninsula Packaging (held-for-sale).

Rigids divisions which are divisions of Astrapak Manufacturing Holdings Proprietary Limited › Cinqplast Denver (discontinued).

Plastop Bronkhorstspruit (discontinued).

Going concernThe directors report that, after having considered a wide range of factors, they have reasonable expectation that the Group and Company have adequate resources and facilities available to continue in operation for the foreseeable future. For this reason, the Group continues to adopt the going-concern basis in preparing its financial statements.

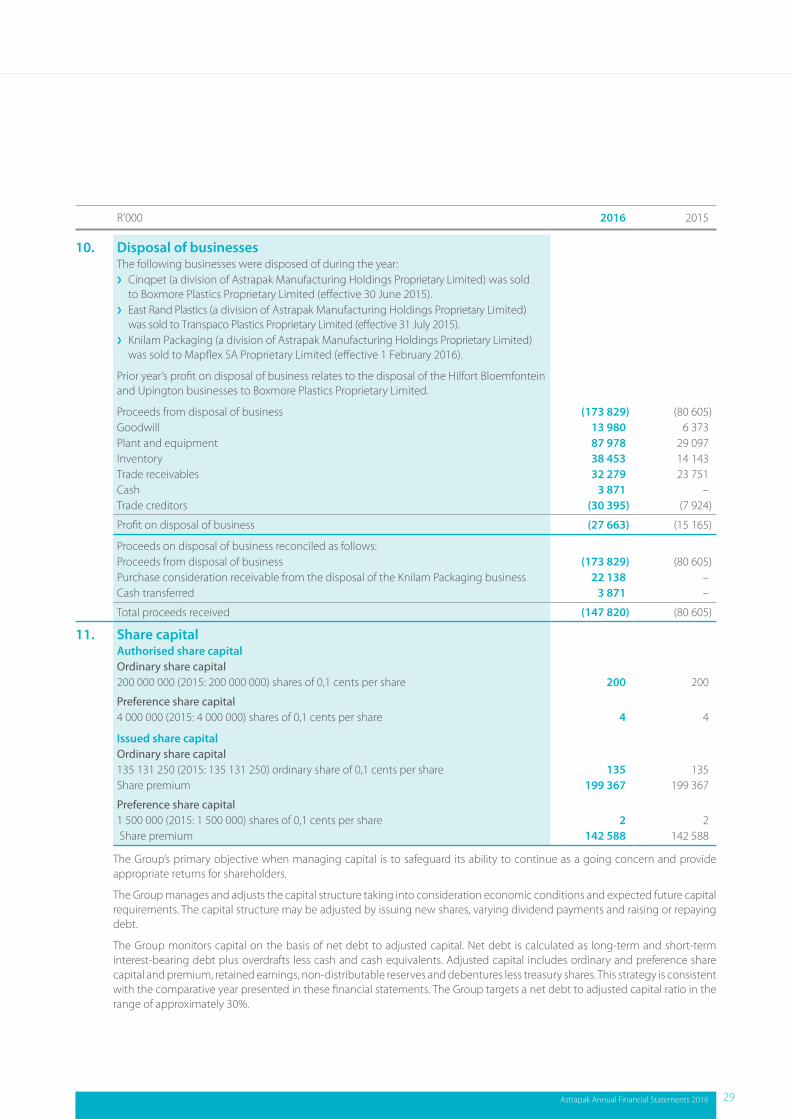

Discontinued operationsDuring the 29 February 2016 financial year, the following entities were disposed of: › Cinqpet. › East Rand Plastics. › Knilam Packaging.

Events after the reporting periodNo material fact or circumstance has come to light between 29 February 2016 and date of signature of these financial statements that would require adjustment to or disclosure in these financial statements.

Astrapak Annual Financial Statements 2016 5

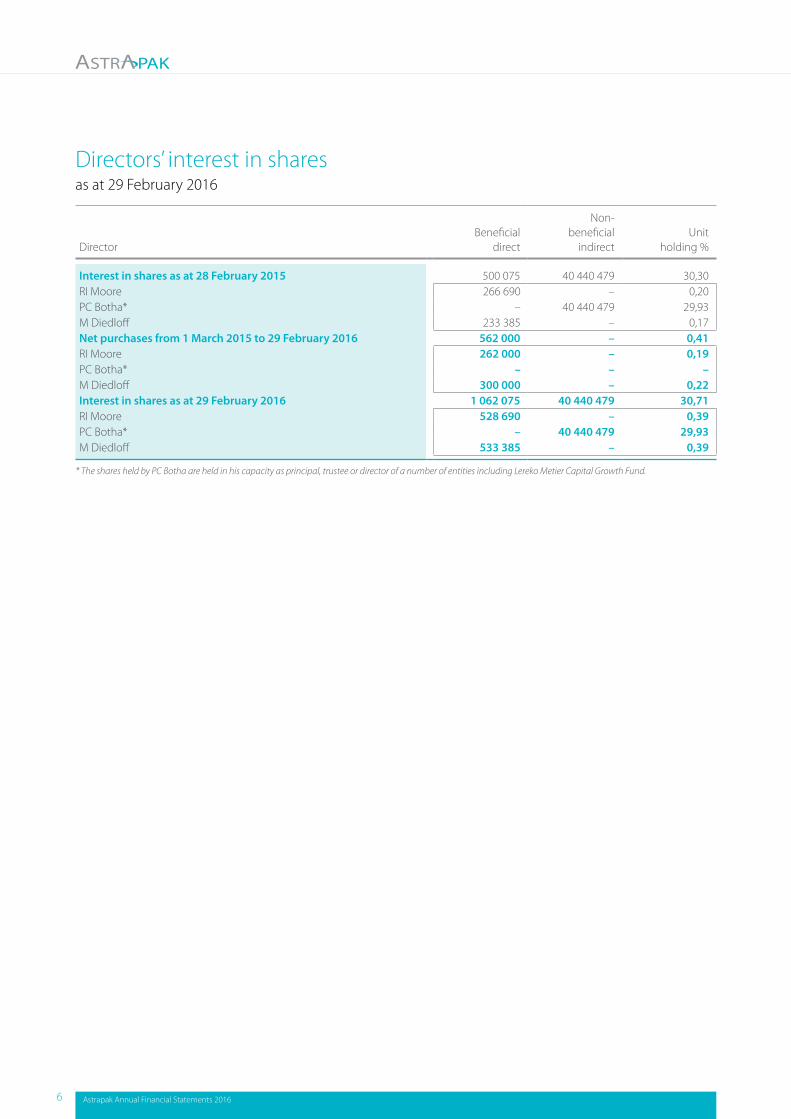

DirectorBeneficial

direct

Non-beneficial

indirectUnit

holding %

Interest in shares as at 28 February 2015 500 075 40 440 479 30,30RI Moore 266 690 – 0,20PC Botha* – 40 440 479 29,93M Diedloff 233 385 – 0,17Net purchases from 1 March 2015 to 29 February 2016 562 000 – 0,41RI Moore 262 000 – 0,19PC Botha* – – –M Diedloff 300 000 – 0,22Interest in shares as at 29 February 2016 1 062 075 40 440 479 30,71RI Moore 528 690 – 0,39PC Botha* – 40 440 479 29,93M Diedloff 533 385 – 0,39

* The shares held by PC Botha are held in his capacity as principal, trustee or director of a number of entities including Lereko Metier Capital Growth Fund.

Directors’ interest in sharesas at 29 February 2016

6 Astrapak Annual Financial Statements 2016

Audit Committee reportfor the year ended 29 February 2016

› evaluated the effectiveness of risk management, control and various governance processes;

› verified the independence of the external auditors;

› nominated Deloitte & Touche as auditor and noted the appointment of Mrs Corinne Ringwood as the designated auditor;

› reviewed and approved audit fees and engagement terms of the external auditor;

› considered and determined the nature and extent of non-audit services;

› considered and satisfied itself that the Chief Financial Officer has appropriate expertise and experience and that the composition, experience and skills set of the finance function met the Group’s requirements;

› considered and reviewed the appropriateness of IT risks and controls;

› reviewed and monitored the appropriateness of the Group’s combined assurance model and ensuring that significant risks facing the business were adequately addressed; and

› received and dealt appropriately with any complaints, from within or outside the Company, relating to the accounting practices and internal audit of the Company, to the content or auditing of its financial statements, or any related matter.

The Audit Committee has discharged all its responsibilities and carried out all the functions assigned to it in terms of section 94(7) of the Companies Act, No 71 of 2008 (“the Act”).

The Audit Committee has adopted formal terms of reference, as delegated to it by the Board of Directors (“the Board”), as its Audit Committee Charter.

The Audit Committee herewith confirms that it has discharged the functions in terms of its charter and ascribed to it in terms of the Act in the following manner: › reviewed the interim and year-end

financial results as published and recommended the adoption thereof to the Board;

› reviewed external audit reports on the annual financial statements;

› reviewed the Board-approved internal audit and risk charters;

› reviewed and approved the internal audit plan;

› assessed the independence of the internal audit function;

› reviewed and approved the adopted approach to risk management and the risk registers produced via the risk assessment process;

› reviewed all internal audit and risk management reports;

› reviewed the internal audit and risk management plans and where required made recommendations to the Board on remedial actions to be taken;

In the course of its reviews, the Audit Committee took appropriate steps to ensure that the financial statements were prepared in accordance with International Financial Reporting Standards and in the manner required by the Act. It further considered and made recommendations on internal financial controls, dealt with any concerns or queries of matters financial, audit or risk-related and reviewed and considered all legal matters that could significantly impact on the organisation and the financial results reported or to be reported.

The Audit Committee determined that, during the financial year under review, it had discharged its legal, regulatory and all other responsibilities, as might be defined in its charter and terms of reference. The Board concurs with this assessment.

TV MokgatlhaChairman: Audit Committee

19 April 2016

Astrapak Annual Financial Statements 2016 7

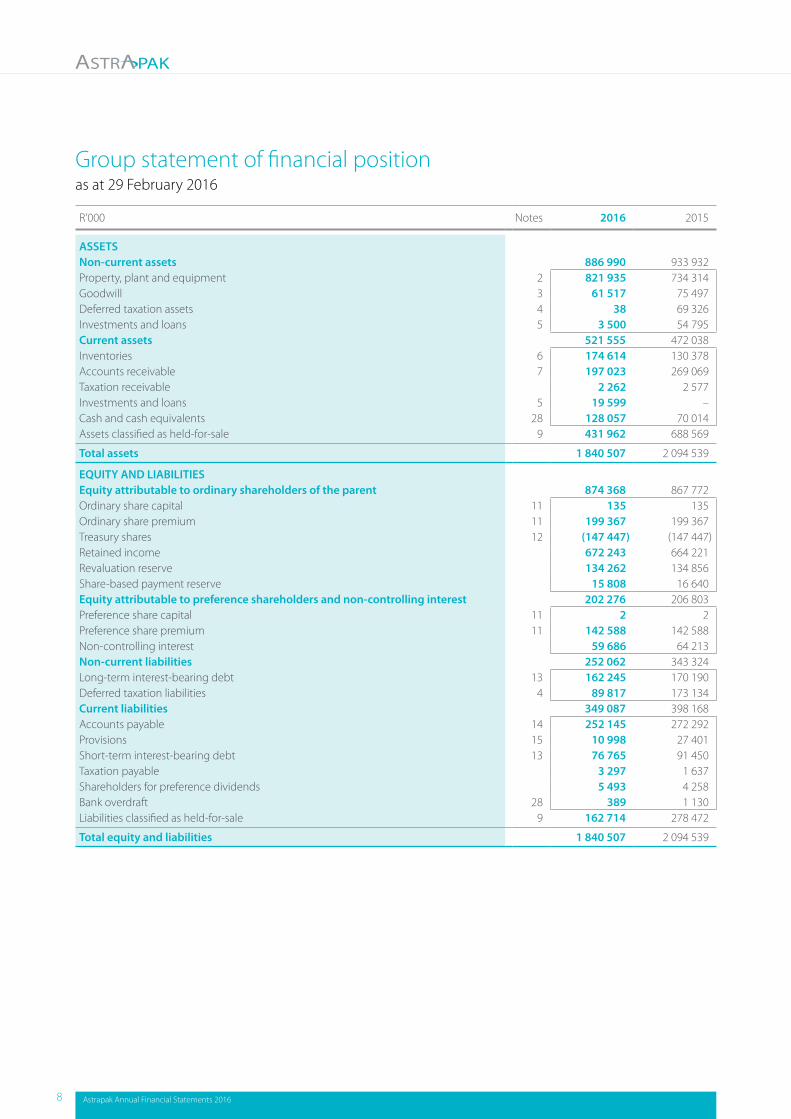

Group statement of financial positionas at 29 February 2016

R’000 Notes 2016 2015

ASSETSNon-current assets 886 990 933 932Property, plant and equipment 2 821 935 734 314 Goodwill 3 61 517 75 497 Deferred taxation assets 4 38 69 326 Investments and loans 5 3 500 54 795 Current assets 521 555 472 038Inventories 6 174 614 130 378 Accounts receivable 7 197 023 269 069 Taxation receivable 2 262 2 577Investments and loans 5 19 599 –Cash and cash equivalents 28 128 057 70 014Assets classified as held-for-sale 9 431 962 688 569

Total assets 1 840 507 2 094 539

EQUITY AND LIABILITIESEquity attributable to ordinary shareholders of the parent 874 368 867 772 Ordinary share capital 11 135 135 Ordinary share premium 11 199 367 199 367 Treasury shares 12 (147 447) (147 447)Retained income 672 243 664 221 Revaluation reserve 134 262 134 856 Share-based payment reserve 15 808 16 640Equity attributable to preference shareholders and non-controlling interest 202 276 206 803 Preference share capital 11 2 2 Preference share premium 11 142 588 142 588 Non-controlling interest 59 686 64 213 Non-current liabilities 252 062 343 324Long-term interest-bearing debt 13 162 245 170 190Deferred taxation liabilities 4 89 817 173 134Current liabilities 349 087 398 168Accounts payable 14 252 145 272 292 Provisions 15 10 998 27 401 Short-term interest-bearing debt 13 76 765 91 450 Taxation payable 3 297 1 637 Shareholders for preference dividends 5 493 4 258 Bank overdraft 28 389 1 130 Liabilities classified as held-for-sale 9 162 714 278 472

Total equity and liabilities 1 840 507 2 094 539

8 Astrapak Annual Financial Statements 2016

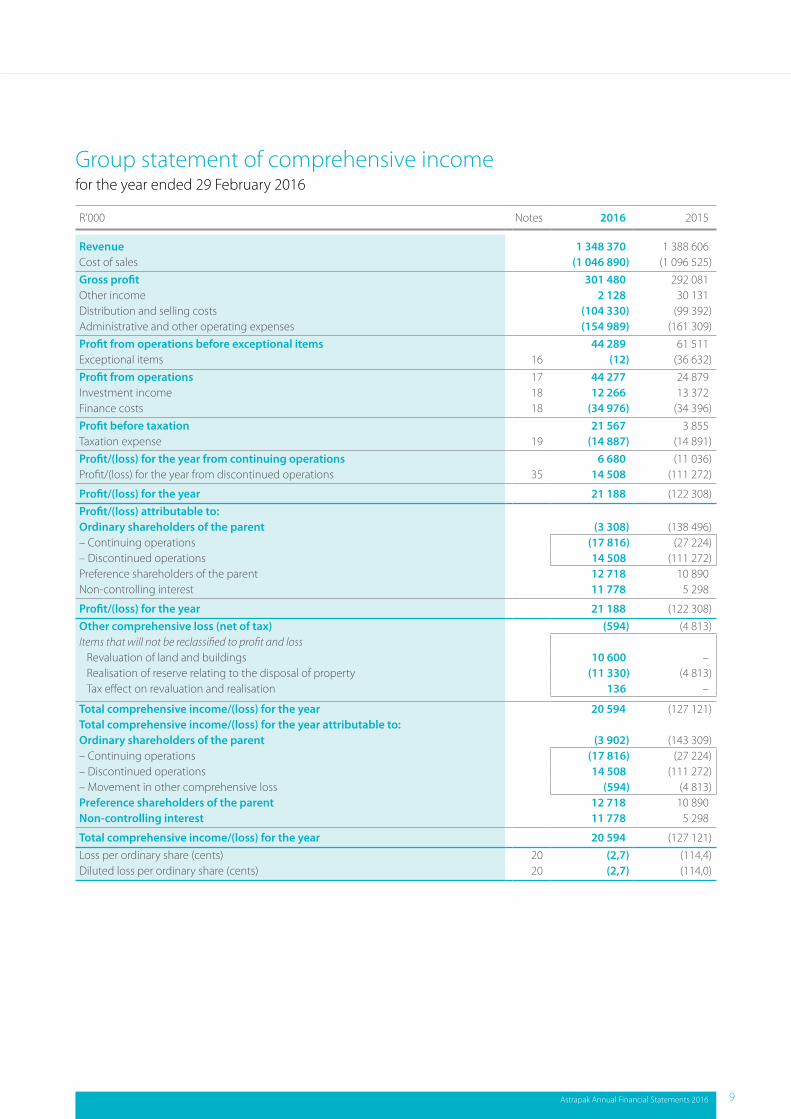

Group statement of comprehensive incomefor the year ended 29 February 2016

R’000 Notes 2016 2015

Revenue 1 348 370 1 388 606 Cost of sales (1 046 890) (1 096 525)Gross profit 301 480 292 081 Other income 2 128 30 131 Distribution and selling costs (104 330) (99 392)Administrative and other operating expenses (154 989) (161 309)Profit from operations before exceptional items 44 289 61 511 Exceptional items 16 (12) (36 632)Profit from operations 17 44 277 24 879 Investment income 18 12 266 13 372 Finance costs 18 (34 976) (34 396)Profit before taxation 21 567 3 855 Taxation expense 19 (14 887) (14 891)Profit/(loss) for the year from continuing operations 6 680 (11 036)Profit/(loss) for the year from discontinued operations 35 14 508 (111 272)

Profit/(loss) for the year 21 188 (122 308)Profit/(loss) attributable to: Ordinary shareholders of the parent (3 308) (138 496)– Continuing operations (17 816) (27 224)– Discontinued operations 14 508 (111 272)Preference shareholders of the parent 12 718 10 890 Non-controlling interest 11 778 5 298

Profit/(loss) for the year 21 188 (122 308)Other comprehensive loss (net of tax) (594) (4 813)Items that will not be reclassified to profit and loss

Revaluation of land and buildings 10 600 –Realisation of reserve relating to the disposal of property (11 330) (4 813)Tax effect on revaluation and realisation 136 –

Total comprehensive income/(loss) for the year 20 594 (127 121)Total comprehensive income/(loss) for the year attributable to:Ordinary shareholders of the parent (3 902) (143 309)– Continuing operations (17 816) (27 224)– Discontinued operations 14 508 (111 272)– Movement in other comprehensive loss (594) (4 813)Preference shareholders of the parent 12 718 10 890 Non-controlling interest 11 778 5 298

Total comprehensive income/(loss) for the year 20 594 (127 121)Loss per ordinary share (cents) 20 (2,7) (114,4)Diluted loss per ordinary share (cents) 20 (2,7) (114,0)

Astrapak Annual Financial Statements 2016 9

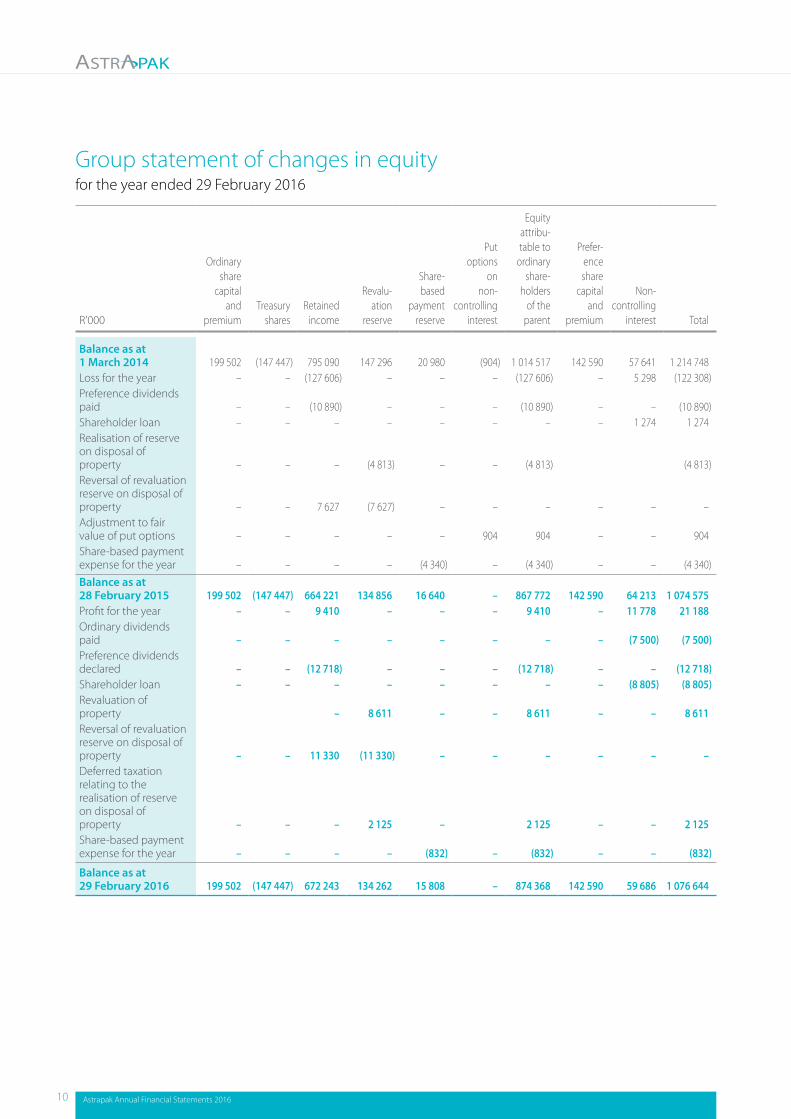

Group statement of changes in equityfor the year ended 29 February 2016

R’000

Ordinary share

capital and

premiumTreasury

sharesRetained

income

Revalu-ation

reserve

Share-based

payment reserve

Put options

on non-

controlling interest

Equity attribu-table to

ordinary share-

holders of the

parent

Prefer-ence share

capital and

premium

Non-controlling

interest Total

Balance as at 1 March 2014 199 502 (147 447) 795 090 147 296 20 980 (904) 1 014 517 142 590 57 641 1 214 748 Loss for the year – – (127 606) – – – (127 606) – 5 298 (122 308)Preference dividends paid – – (10 890) – – – (10 890) – – (10 890)Shareholder loan – – – – – – – – 1 274 1 274 Realisation of reserve on disposal of property – – – (4 813) – – (4 813) (4 813)Reversal of revaluation reserve on disposal of property – – 7 627 (7 627) – – – – – –Adjustment to fair value of put options – – – – – 904 904 – – 904 Share-based payment expense for the year – – – – (4 340) – (4 340) – – (4 340)Balance as at 28 February 2015 199 502 (147 447) 664 221 134 856 16 640 – 867 772 142 590 64 213 1 074 575 Profit for the year – – 9 410 – – – 9 410 – 11 778 21 188 Ordinary dividends paid – – – – – – – – (7 500) (7 500)Preference dividends declared – – (12 718) – – – (12 718) – – (12 718)Shareholder loan – – – – – – – – (8 805) (8 805)Revaluation of property – 8 611 – – 8 611 – – 8 611 Reversal of revaluation reserve on disposal of property – – 11 330 (11 330) – – – – – –Deferred taxation relating to the realisation of reserve on disposal of property – – – 2 125 – 2 125 – – 2 125 Share-based payment expense for the year – – – – (832) – (832) – – (832)

Balance as at 29 February 2016 199 502 (147 447) 672 243 134 262 15 808 – 874 368 142 590 59 686 1 076 644

10 Astrapak Annual Financial Statements 2016

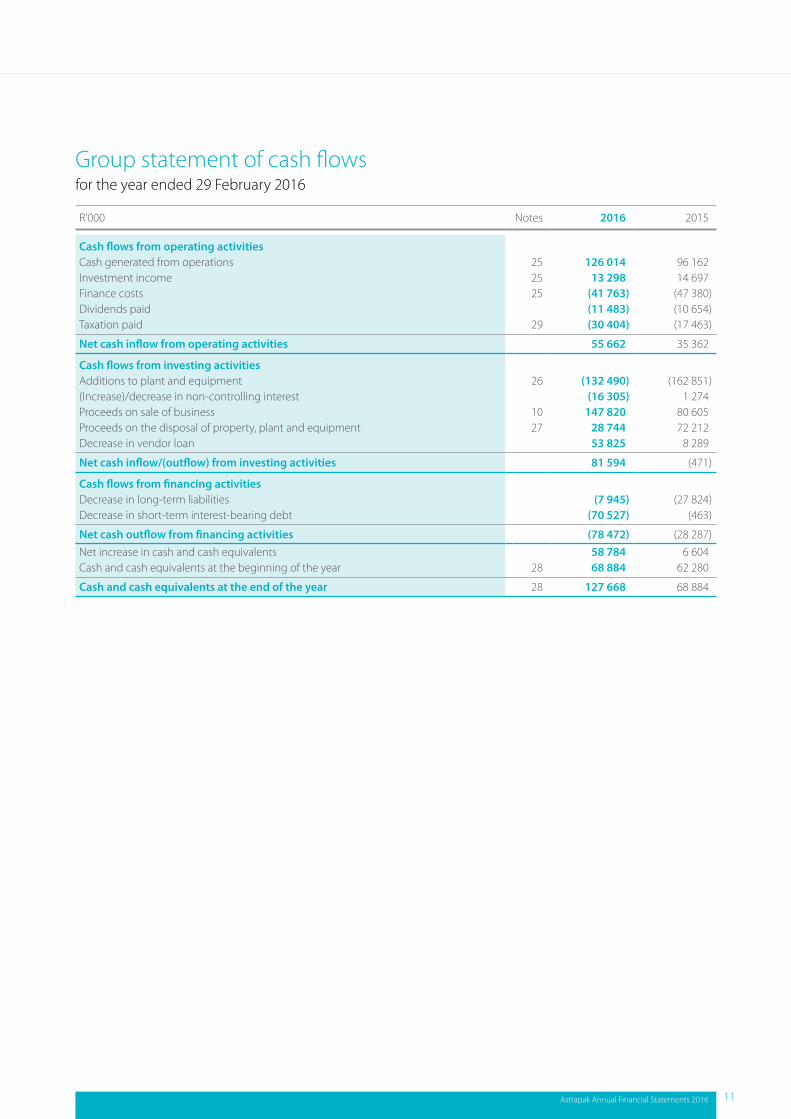

Group statement of cash flowsfor the year ended 29 February 2016

R’000 Notes 2016 2015

Cash flows from operating activitiesCash generated from operations 25 126 014 96 162 Investment income 25 13 298 14 697 Finance costs 25 (41 763) (47 380)Dividends paid (11 483) (10 654)Taxation paid 29 (30 404) (17 463)

Net cash inflow from operating activities 55 662 35 362

Cash flows from investing activitiesAdditions to plant and equipment 26 (132 490) (162 851)(Increase)/decrease in non-controlling interest (16 305) 1 274 Proceeds on sale of business 10 147 820 80 605 Proceeds on the disposal of property, plant and equipment 27 28 744 72 212 Decrease in vendor loan 53 825 8 289

Net cash inflow/(outflow) from investing activities 81 594 (471)

Cash flows from financing activitiesDecrease in long-term liabilities (7 945) (27 824)Decrease in short-term interest-bearing debt (70 527) (463)

Net cash outflow from financing activities (78 472) (28 287)Net increase in cash and cash equivalents 58 784 6 604 Cash and cash equivalents at the beginning of the year 28 68 884 62 280

Cash and cash equivalents at the end of the year 28 127 668 68 884

Astrapak Annual Financial Statements 2016 11

Significant accounting policiesfor the year ended 29 February 2016

1. General information Astrapak Limited and its subsidiaries is a company incorporated under the Companies Act of South Africa. The address of the

registered office is given on page IBC. The principal business of the Group is described in the directors’ report.

These financial statements are presented in South African Rand because that is the currency of the primary economic environment in which the Group operates.

Statement of compliance The annual financial statements have been prepared in accordance with the Companies Act of South Africa, International

Financial Reporting Standards and SAICA Financial Reporting Guide as issued by the Accounting Practices Committee and Financial Pronouncements issued by the Financial Reporting Standards Board.

The financial statements have been prepared in a manner that is consistent with the prior year. The historical cost basis has been applied to the preparation of the financial statements except for the revaluation of certain properties and financial instruments to fair value as explained in the accounting policies below.

1.1 Basis of consolidation The consolidated financial statements incorporate the financial statements of the Astrapak Limited Group (“the Company”) and

entities controlled by the Company (its subsidiaries) as at 28 February each year. Control is achieved where the Company has the power to govern the financial and operating polices of an investee entity so as to obtain benefits from its activities.

On acquisition, the assets and liabilities and contingent liabilities of a subsidiary are measured at their fair values at the date of acquisition. The acquisition of subsidiaries is accounted for using the purchase method. Any excess of the cost of acquisition over the fair values of the identifiable net assets acquired is recognised as goodwill. Any deficiency of the cost of acquisition below the fair values of the identifiable net assets acquired (that is discount on acquisition) is credited to profit or loss in the period of acquisition.

The results of subsidiaries acquired or disposed of during the year are included in the consolidated statement of comprehensive income from the effective date of acquisition or up to the effective date of disposal, as appropriate. Total comprehensive income of subsidiaries is attributed to the owner of the Company and to the non-controlling interests even if this results in the non-controlling interest having a deficit balance.

If the subsidiary uses accounting policies other than those adopted in the consolidated financial statements for like transactions and events in similar circumstances, appropriate adjustments are made to its financial statements in preparing the consolidated financial statements.

All intra-group transactions, balances, income and expenses are eliminated in full on consolidation.

Transactions with non-controlling interests The Group treats transactions with non-controlling interests as transactions with equity owners of the Group. For purchases from

non-controlling interests, the difference between any consideration paid and the relevant share acquired of the carrying value of net assets of the subsidiary is recorded in equity. Gains or losses on disposals to non-controlling interests are also recorded in equity. Any increase or decrease in ownership interest in subsidiaries without a change in control is recognised as equity transactions in the consolidated financial statements. Accordingly, any premium or discount on subsequent purchases of equity instruments from or sales of equity instruments to non-controlling interests are recognised directly in equity of the parent shareholder.

Put options on non-controlling interests Changes in fair value of put options on non-controlling interests are reflected through equity.

1.2 Goodwill Goodwill arising on consolidation represents the excess of the cost of acquisition over the Group’s interest in the fair value of the

identifiable assets and liabilities of a subsidiary, or jointly controlled entity, at the date of acquisition.

Goodwill arising on an acquisition of a business is carried at cost as established at the date of acquisition of the business less accumulated impairment losses, if any.

Whenever negative goodwill arises, the identification and measurement of the acquired identifiable assets, liabilities and contingent liabilities are reassessed. If negative goodwill still remains, it is recognised in profit or loss immediately.

12 Astrapak Annual Financial Statements 2016

Goodwill is not amortised. For the purposes of impairment testing, goodwill is allocated to each of the Group’s cash-generating units (or groups of cash-generating units) that is expected to benefit from the synergies of the combination.

A cash-generating unit to which goodwill has been allocated is tested for impairment annually, or more frequently when there is indication that the unit may be impaired. If the recoverable amount of the cash-generating unit is less than its carrying amount, the impairment loss is allocated first to reduce the carrying amount of any goodwill allocated to the unit and then to the other assets of the unit on a pro rata basis based on the carrying amount of each asset in the unit. Any impairment loss for goodwill is recognised directly in profit or loss in the consolidated statement of comprehensive income/income statement. An impairment loss recognised for goodwill is not reversed in subsequent periods.

On disposal of the relevant cash-generating unit, the attributable amount of goodwill is included in the determination of the profit or loss on disposal. The same principle is applicable for partial disposals where there is a change in ownership, in other words, a portion of the goodwill is expensed as part of the cost of disposal. For partial disposals and acquisitions with no change in ownership, goodwill is recognised as a transaction with equity holders.

1.3 Non-controlling interests The Group presents non-controlling interests in its consolidated statement of financial position within equity, separately from

the equity of the owners of the parent and attributes the profit or loss and each component of other comprehensive income to the owners of the parent and to the non-controlling interests. The proportion allocated to the parent and non-controlling interests is determined on the basis of present ownership interests.

1.4 Revenue recognition Revenue is measured at the fair value of the consideration received or receivable and represents amounts receivable for goods

and services provided in the normal course of business, net of trade discounts, rebates and other sales-related taxes.

Sales of goods are recognised when goods are delivered and title has passed.

Interest income is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable.

1.5 Leasing Leases are classified as finance leases whenever the terms of the lease transfer substantially all the risks and rewards of ownership

to the lessee. Finance leases are capitalised. All other leases are classified as operating leases.

Assets held under finance leases are recognised as assets of the Group at their fair value or, if lower, at the present value of the minimum lease payments, each determined at the inception of the lease. The corresponding liability to the lessor is included in the statement of financial position as a finance lease obligation. Lease payments are apportioned between finance charges and reduction of the lease obligation so as to achieve a constant rate of interest on the remaining balance of the liability. Finance charges are charged directly against income, unless they are directly attributable to qualifying assets, in which case they are capitalised in accordance with the Group’s general policy on borrowing costs.

Rentals payable under operating leases are charged to income on a straight-line basis over the term of the relevant lease.

Benefits received and receivable as an incentive to enter into an operating lease are also spread on a straight-line basis over the lease term.

1.6 Foreign currencies Transactions in currencies other than South African Rand are recorded at the rates of exchange prevailing on the dates of the

transactions. At each year-end date, monetary assets and liabilities that are denominated in foreign currencies are translated at the rates prevailing on the year-end date. Non-monetary assets and liabilities carried at fair value that are denominated in foreign currencies are translated at the rates prevailing at the date when the fair value was determined. Gains and losses arising on translation are included in net profit or loss for the period, except for exchange differences arising on non-monetary assets and liabilities where the changes in fair value are recognised directly in equity.

To hedge its exposure to certain foreign exchange risks, the Group enters into forward contracts and options.

Astrapak Annual Financial Statements 2016 13

Significant accounting policies continued

for the year ended 29 February 2016

1.7 Borrowing costs Borrowing costs directly attributable to the acquisition, construction or production of qualifying assets, which are assets that

necessarily take a substantial period of time to prepare for their intended use or sale, are added to the cost of those assets, until such time as the assets are substantially ready for their intended use or sale. Investment income earned on the temporary investment of specific borrowings, pending their expenditure on qualifying assets, is deducted from the borrowing costs eligible for capitalisation.

All other borrowing costs are recognised in profit or loss in the period in which they are incurred.

1.8 Government grants Government grants are recognised at their fair value where there is reasonable assurance that the grant will be received and all

attaching conditions will be complied with.

Government grants are recognised as income over the periods necessary to match them with the costs they are intended to compensate on a systematic basis.

1.9 Exceptional items Exceptional items are material items which derive from events or transactions that fall outside the ordinary trading activities of

the Group and which individually or, if of a similar type, in aggregate, need to be disclosed by virtue of their size or incidence, if the financial statements are to give a true and fair view.

1.10 Retirement benefit costs Under defined contribution plans, the Group’s legal or constructive obligation is limited to the amount that it agrees to contribute

to the fund. Consequently, the actuarial risk that benefits will be less than expected and the investment risk that assets invested will be insufficient to meet expected benefits is borne by the employee.

Payments to defined contribution retirement benefit schemes are charged as an expense as they fall due.

1.11 Impairment of assets, excluding goodwill At the end of each reporting period, the Group reviews the carrying amounts of its tangible and intangible assets to determine

whether there is any indication that those assets have suffered an impairment loss. If any such indication exists, the recoverable amount of the asset is estimated in order to determine the extent of the impairment loss (if any). Where it is not possible to estimate the recoverable amount of an individual asset, the Group estimates the recoverable amount of the cash-generating unit to which the asset belongs. Where a reasonable and consistent basis of allocation can be identified, corporate assets are also allocated to individual cash-generating units, or otherwise they are allocated to the smallest group of cash-generating units for which a reasonable and consistent allocation basis can be identified.

Intangible assets with indefinite useful lives and intangible assets not yet available for use are tested for impairment at least annually, and whenever there is an indication that the asset may be impaired.

Recoverable amount is the higher of fair value less costs to sell and value-in-use. In assessing value-in-use, the estimated future cash flows are discounted to their present value using a pre-tax discount rate that reflects current market assessments of the time value of money and the risks specific to the asset for which the estimates of future cash flows have not been adjusted.

If the recoverable amount of an asset (or a cash-generating unit) is estimated to be less than its carrying amount, the carrying amount of the asset (or the cash-generating unit) is reduced to its recoverable amount. An impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the impairment loss is treated as a revaluation decrease.

Where an impairment loss subsequently reverses, the carrying amount of the asset (or a cash-generating unit) is increased to the revised estimate of its recoverable amount, but so that the increased carrying amount does not exceed the carrying amount that would have been determined had no impairment loss been recognised for the asset (or the cash-generating unit) in prior years. A reversal of an impairment loss is recognised immediately in profit or loss, unless the relevant asset is carried at a revalued amount, in which case the reversal of the impairment loss is treated as a revaluation increase.

14 Astrapak Annual Financial Statements 2016

1.12 Taxation The taxation expense represents the sum of the taxation currently payable and deferred taxation.

The taxation currently payable is based on taxable profit for the year. Taxable profit differs from profit as reported in the statement of comprehensive income because it excludes items of income or expense that are taxable or deductible in other years and it further excludes items that are never taxable or deductible. The Group’s liability for current taxation is calculated using taxation rates that have been enacted or substantively enacted by the statement of financial position date.

Deferred taxation is the taxation expected to be payable or recoverable on differences between the carrying amounts of assets and liabilities in the financial statements and the corresponding taxation bases used in the computation of taxable profit, and is accounted for using the statement of financial position liability method.

Deferred taxation liabilities are generally recognised for all taxable temporary differences and deferred taxation assets are recognised to the extent that it is probable that taxable profits will be available against which deductible temporary differences can be utilised. Such assets and liabilities are not recognised if the temporary difference arises from goodwill or from the initial recognition (other than in a business combination) of other assets and liabilities in a transaction that affects neither the taxation profit nor the accounting profit.

Deferred taxation liabilities are recognised for taxable temporary differences arising on investments in subsidiaries and associates, and interests in joint ventures, except where the Group is able to control the reversal of the temporary difference and it is probable that the temporary difference will not reverse in the foreseeable future.

The carrying amount of deferred taxation assets is reviewed at each reporting date and reduced to the extent that it is no longer probable that sufficient taxable profits will be available to allow all or part of the asset to be recovered.

Deferred taxation is calculated at the taxation rates that are expected to apply in the period when the liability is settled or the asset is realised. Deferred taxation is charged or credited in the statement of comprehensive income, except when it relates to items charged or credited directly to equity, in which case the deferred taxation is also dealt with in equity.

Deferred taxation assets and liabilities are offset when there is a legal enforceable right to offset current taxation assets against liabilities and when the deferred taxation relates to the same fiscal authority.

Additional income taxes that arise from the distribution of dividends are recognised at the same time as the liability to pay the related dividend is recognised.

1.13 Property, plant and equipment Plant and equipment is accounted for at cost less accumulated depreciation and any accumulated impairment. All direct costs,

including finance costs relating to major capital projects, are capitalised up to the date of commissioning.

Property is accounted for using the revaluation model.

Under the revaluation model, property is carried at the revalued amount, being its fair value at the date of the revaluation less subsequent depreciation and impairment.

Increases are value credited to other comprehensive income and accumulated in equity and reversal of a revaluation decrease previously recognised as an expense should be recognised as income.

Decreases arising from the revaluation are recognised as an expense to the extent that it exceeds the amount previously credited to the revaluation surplus.

The cost of replacing part of an item of property, plant and equipment is recognised in the carrying amount of the item if it is probable that the future economic benefits embodied within the part will flow to the Group and its cost can be measured reliably. The costs of day-to-day servicing of property, plant and equipment are recognised in profit or loss as incurred.

Depreciation is charged so as to write off the cost of assets, other than freehold land, over their estimated economic useful lives, using the straight-line method. Depreciation is not provided for on freehold land.

Residual values and estimated useful lives are assessed on an annual basis and, if expectations differ from previous estimates, adjusted prospectively as a change in accounting estimate.

Astrapak Annual Financial Statements 2016 15

Significant accounting policies continued

for the year ended 29 February 2016

1.14 Inventories Inventories are stated at the lower of cost and net realisable value. Cost comprises direct materials and, where applicable, direct

labour costs and those overheads that have been incurred in bringing the inventories to their present location and condition. Cost is calculated using the first-in first-out method. Net realisable value represents the estimated selling price less all estimated costs of completion and costs to be incurred in marketing, selling and distribution.

1.15 Financial instruments Financial assets and financial liabilities are recognised on the Group’s statement of financial position when the Group has become

a party to contractual provisions of the instruments.

Financial assets and financial liabilities are initially measured at fair value. Transaction costs are directly attributable to the acquisition or issue of financial assets and liabilities (other than financial assets and financial liabilities at fair value through profit or loss) are added to or deducted from the fair value of financial assets or financial liabilities, as appropriate, on initial recognition. Transaction costs directly attributable to the acquisition of financial assets or financial liabilities at fair value through profit or loss or recognised immediately in profit or loss.

Financial assets are fair value through profit or loss (“FVTPL”) Financial assets are classified at FVTPL when the asset is either held-for-trading or does not satisfy the criteria for hedge

accounting or is designated at FVTPL.

A financial asset is designated at FVTPL on initial recognition if this designation provides more useful information because: › such designation eliminates or significantly reduces a measurement or recognition inconsistency that would otherwise arise; or › the financial asset is part of a group of financial assets, financial liabilities or both, that is managed and its performance

evaluated on a fair value basis in accordance with a documented risk/investment management strategy, and the information regarding this grouping is reported internally to key management on this basis; or

› it forms part of a contract containing one or more embedded derivatives, and IAS 39 permits the entire combined contract to be designated as at FVTPL.

Financial assets measured at FVTPL are recognised at fair value. Any subsequent gains or losses are recognised in profit or loss.

Trade receivables and payables are measured at initial recognition at fair value, and are subsequently measured at amortised cost using the effective interest rate method. Appropriate allowances for estimated irrecoverable trade receivables are recognised in profit or loss when there is objective evidence that the asset is impaired.

Appropriate allowances for estimated irrecoverable trade receivables are recognised in profit or loss when there is objective evidence that the asset is impaired.

Cash and cash equivalents comprise the net of cash on hand and overdrafts, demand deposits, and other short-term highly liquid investments that are readily convertible to a known amount of cash and are subject to an insignificant risk of changes in value. Interest-bearing bank loans and overdrafts are recorded at the proceeds received, net of direct issue costs. Finance charges, including premiums payable on settlement or redemption, are accounted for on an accrual basis to the statement of comprehensive income using the effective interest rate method and are added to the carrying amount of the instrument to the extent they are not settled in the period in which they arise.

Equity instruments are recorded at the proceeds received, net of direct issue costs. The Group uses derivative financial instruments, primarily foreign currency forward contracts, to hedge its risks associated with foreign currency. The Group does not use derivative financial instruments for speculative purposes. The fair value of these derivatives is recorded and remeasured at each reporting date. Changes in fair value of derivative financial instruments that are designated and effective as hedges of future cash flows relating to firm commitments and forecast transactions are recognised directly in equity. If the hedged firm commitment or forecast transaction results in the recognition of an asset or a liability, then, at the time the asset or liability is recognised, the associated gain or loss on the derivative that had previously been recognised in equity is included in the initial measurement of the asset or liability.

Hedge accounting is discontinued when the hedging instrument expires or is sold, terminated, exercised or no longer qualifies for hedge accounting. At that time, any cumulative gain or loss on the hedging instrument recognised in equity is retained in equity until the forecast transaction occurs. If a hedged transaction is no longer expected to occur, the net cumulative gain or loss recognised in equity is transferred to net profit or loss for the period.

Changes in fair value of derivative financial instruments that do not qualify for hedge accounting are recognised in the statement of comprehensive income as they arise.

16 Astrapak Annual Financial Statements 2016

1.16 Provisions and contingencies Provisions are recognised when the Group has a present obligation (legal or constructive) as a result of a past event, it is probable

that the Group will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

The amount recognised as a provision is the best estimate of the consideration required to settle the present obligation at the end of the reporting period, taking into account the risks and uncertainties surrounding the obligation. When a provision is measured using the cash flows estimated to settle the present obligation, its carrying amount is the present value of those cash flows (where the effect of the time value of money is material).

When some or all of the economic benefits required to settle a provision are expected to be recovered from a third party, a receivable is recognised as an asset if it is virtually certain that reimbursement will be received and the amount of the receivable can be measured reliably.

Onerous contracts Present obligations arising under onerous contracts are recognised and measured as provisions. An onerous contract is

considered to exist where the Group has a contract under which the unavoidable costs of meeting the obligations under the contract exceed the economic benefits expected to be received from the contract.

Contingent liabilities A contingent liability is a possible obligation that arises from past events and whose existence will be confirmed only by the

occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the Group, or a present obligation that arises from past events but is not recognised because it is not probable that an outflow of resources embodying economic benefits will be required to settle the obligation; or the amount of the obligation cannot be measured with sufficient reliability. If the likelihood of an outflow of resources is remote, the possible obligation is neither a provision nor a contingent liability and no disclosure is made.

Contingent assets A contingent asset is a possible asset that arises from past events and whose existence will be confirmed only by the occurrence

or non-occurrence of one or more uncertain future events not wholly within the control of the Group. Such contingent assets are only recognised in the financial statements where the realisation of income is virtually certain. If the inflow of economic benefits is only probable, the contingent asset is disclosed as a claim in favour of the Group but not recognised in the statement of financial position.

Provisions for royalties, distribution commissions and credit notes Provisions for royalties, distribution commissions and credit notes are recognised when the Group has a present obligation (legal

or constructive) as a result of a past event and when it is probable that the Group will be required to settle the obligation, and a reliable estimate can be made of the amount of the obligation.

1.17 Share-based payments The Group has applied the requirements of IFRS 2 Share-based Payments.

An expense is recognised where the Group receives goods or services in exchange for shares or rights over shares (equity-settled transactions).

Employees, including directors, of the Group receive remuneration in the form of share-based payment transactions, whereby employees render services in exchange for shares or rights over shares (equity-settled transactions).

The cost of equity-settled transactions with employees is measured by reference to the fair value at the date at which they are granted. The fair value is determined by an external value using the binomial model. In valuing equity-settled transactions, no account is taken of any performance conditions, other than conditions linked to the price of the shares of the Group (market conditions). The expected life used in the model has been adjusted, based on management’s best estimate, for the effects of non-transferability, exercise restrictions and behavioural considerations.

The cost of equity-settled transactions is recognised, together with a corresponding increase in equity, on a straight-line basis over the period in which the non-market performance conditions are fulfilled, ending on the date on which the relevant employees become fully entitled to the award (vesting date).

Astrapak Annual Financial Statements 2016 17

Significant accounting policies continued

for the year ended 29 February 2016

No expense is recognised for awards that do not ultimately vest, except for awards where vesting is conditional upon a market condition, which are treated as vesting irrespective of whether or not the market condition is satisfied, provided that all other performance conditions are satisfied.

Where the terms of an equity-settled award are modified, as a minimum, an expense is recognised as if the terms had not been modified. In addition, an expense is recognised for any increase in the value of the transaction as a result of the modification, as measured at the date of modification. Where an equity-settled award is cancelled, it is treated as if it had vested on the date of cancellation, and any expense not yet recognised for the award is recognised immediately. However, if a new award is substituted for the cancelled award, and designated as a replacement award on the date that it is granted, the cancelled and new awards are treated as if they were a modification of the original award. The dilutive effect of outstanding options is reflected as additional share dilution in the computation of diluted earnings per share.

1.18 Non-current assets held-for-sale and discontinued operations Assets (or disposal groups) that are classified as held-for-sale are measured in accordance with IFRS 5 Non-current Assets Held-for-

sale and Discontinued Operations. Non-current assets and disposal groups are classified as held-for sale if the carrying amount will be recovered principally through a sale transaction rather than through continuing use. This condition is regarded as met only when the asset is available for immediate sale in its present condition subject only to terms that are usual and customary for sales of such assets and its sale is highly probable. The directors must be committed to the sale, which should be expected to qualify for recognition as a completed sale within one year from the date of classification.

IFRS 5 requires that the sale must be highly probable within 12 months of classification as held-for-sale. For the sale to be highly probable, management must be committed to selling the asset and must be actively looking for a buyer. It is possible that the sale may not be completed within one year, but the delay effectively must be caused by events beyond the entity’s control and the entity must still be committed to selling the asset.

1.19 Segmental reporting The Group’s reportable segments are strategic business units that offer different types of products. They are managed separately,

because these units require different technology and address different market segments.

Flexible The Flexible segment is a manufacturer of blown and cast mono and multilayer polyolefin films for bags, sheet, tubing, shrink,

stretch and barrier applications. Products also include stand-up pouches and modified atmospheric packaging (“MAP”).

Rigids The Rigids segment is a manufacturer of a range of closures, jars, bottles, tottles, tubes, trays, cups, tubs, and other plastic

containers up to a size of 5 litres through the processes of extrusion blow moulding (“EBM”), injection stretch blow moulding (“ISBM”), injection blow moulding (“IBM”), injection moulding (“IM”), sheet extrusion and thermoforming.

1.20 Headline earnings per share The Group has followed the recommendation contained in Circular 2/2015 Headline Earnings issued by SAICA and has published

headline earnings per share in addition to attributable earnings per share. Headline earnings per share has been calculated in accordance with the requirements of Circular 2/2015. Attributable profit per share has been based on earnings attributable, including interest, to ordinary shareholders.

1.21 Judgements and estimates In the application of the Group’s accounting policies, which are described above, the directors are required to make judgements,

estimates and assumptions about the carrying amounts of assets and liabilities that are not readily apparent from other sources. The estimates and associated assumptions are based on historic experience and other factors that are considered to be relevant. Actual results may differ from these estimates.

The estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised in the period in which the estimate is revised if the revision affects only that period, or in the period of the revision and future periods if the revision affects both current and future periods.

Property, plant and equipment Property valuations In determining the fair value of the property, given it is owner occupied and unencumbered by a lease, an income capitalisation

rate ranging from 10,25% to 12,00%.

18 Astrapak Annual Financial Statements 2016

The method requires a market derived projection of economic net annual income for the property, which is then capitalised into perpetuity using a market-related capitalisation rate to determine the market value estimate.

It was further assumed that the improvements at the property can be utilised by an alternate user with minimal repair and conversion costs.

The level of rental income achievable from the property is limited by its age, condition and design. We are of the opinion that good demand exists for premises of this nature.

For the purposes of this valuation, an average gross monthly rental of R30,48/m2 was applied on a through rate basis, which is in line with statistics and opinions canvassed from brokers.

The following property expense elements were taken into account in the valuation: › Rates and taxes. › Insurance. › Repairs and maintenance. › Sundry expenses of 2,0% of gross income, which includes audit fees and leasing commission management fee of 1,0% of

gross income. This fee would be paid to an external management company to manage the property on the owner’s behalf.

Impairment of property, plant and equipment The Group evaluates its non-current assets for impairment annually whenever events or changes in circumstances indicate that

the carrying amount of the asset may not be recoverable. Judgements regarding the existence of impairment indicators are based on market conditions and operational performance of the business. Future events could cause management to conclude that impairment indicators exist.

Residual values The Group is required to measure the residual value of an item of property, plant and equipment. An estimation is made of the

amount it would receive currently for the asset if the asset was already of the age and condition expected at the end of its useful life.

The residual value of an asset is the estimated amount that an entity would currently obtain from the disposal of the asset after deducting the estimated costs of disposal, if the asset was already of the age and in the condition expected at the end of its useful life.

IAS 16 requires residual values (if material) to be estimated first at the date of acquisition and thereafter to be reviewed at each reporting date. If these change from the prior period, the depreciation charge is adjusted prospectively.

Useful life The useful life of an asset is the period over which the Group expects to use the asset, and not necessarily the asset’s economic life.

Useful lives of assets are reviewed annually. If these change from the prior period, the depreciation charge is adjusted prospectively.

The Group uses the following indicators to determine useful lives: › Expected usage of assets. › Expected physical wear and tear. › Technical or commercial obsolescence.

Impairment of goodwill Determining whether goodwill is impaired requires an estimation of the value-in-use of the cash-generating units to which

goodwill has been allocated. The value-in-use calculation is based on an estimate or the future cash flows expected to arise from the cash-generating units discounted at a suitable pre-tax rate in order to calculate the present value of the cash-generating units.

Provisions Provisions are required to be recorded when the Group has a present legal or constructive obligation as a result of past events,

for which it is probable that an outflow of economic benefits will occur, and where a reliable estimate can be made of the amount of the obligation.

Astrapak Annual Financial Statements 2016 19

Significant accounting policies continued

for the year ended 29 February 2016

Best estimates, being the amount that the Group would rationally pay to settle the obligation, are recognised as provisions at statement of financial position date. Risks, uncertainties and future events are taken into account by management in determining the best estimates. Provisions are discounted where the effect of discounting is material. The discount rate used is the rate that reflects current market assessments of the time value of money and, where appropriate, the risks specific to the liability, all of which requires management’s judgement. All provisions are reviewed at each statement of financial position date.

Various uncertainties can result in obligations not being considered probable or estimable for significant periods of time. As a consequence, potentially material obligations may have no provisions and a change in facts or circumstances that result in an obligation becoming probable or estimable can lead to a need for the establishment of material provisions. In addition, where estimated amounts vary from initial estimates the provisions may be revised materially, up or down.

The Group is required to record provisions for legal contingencies when the occurrence of the contingency is probable and the amount of the loss can be reasonably estimated. Liabilities provided for legal matters require judgements regarding projected outcomes and ranges of losses based on historical experience and recommendations of legal counsel. Litigation is, however, unpredictable and actual costs incurred could differ materially from those estimated at the statement of financial position date.

Doubtful debts A debtor or group of debtors is regarded as doubtful if there is objective evidence, as a result of one or more events that occurred

after initial recognition. The Group assesses at each statement of reporting date whether there is objective evidence for doubtful debts.

Deferred taxation assets The carrying amount of deferred taxation assets is reviewed at each reporting date and is adjusted to the extent that it is no

longer probable that sufficient taxable profit will be available to allow all or part of the asset to be recovered.

1.22 Accounting standards and interpretations adopted impacting the annual financial statements The Group did not adopt any new or revised accounting standards or interpretations in the current year that have had a

significant impact on the amounts or disclosures reported in these annual financial statements.

1.23 Impact of standards and interpretations not yet adopted At the reporting date or signing date, the following new and/or revised accounting standards and interpretations were in issue

but not yet effective: › IFRS 1 First-time Adoption of International Financial Reporting Standards (amended) › IFRS 5 Non-current Assets Held-for-sale and Discontinued Operations (amended) › IFRS 7 Financial Instruments: Disclosures (amended) › IFRS 8 Operating Segments (amended) › IFRS 9 Financial Instruments › IFRS 10 Consolidated Financial Statements (amended) › IFRS 12 Disclosure of interests in Other Entities (amended) › IFRS 14 Regulatory Deferral Accounts (amended) › IFRS 16 Leases › IAS 1 Presentation of Financial Statements (amended) › IFRS 15 Revenue from Contracts with Customers › IAS 16 Property, Plant and Equipment (revised) › IAS 19 Employee Benefits (amended) › IAS 24 Related Party Disclosures (amended) › IAS 27 Separate Financial Statements (amended) › IAS 38 Intangible Assets (amended) › IAS 39 Financial Instruments: Recognition and Measurement (amended) › IAS 40 Investment Property (amended).

The Group did not early adopt any new, revised or amended accounting standards or interpretations. The accounting standards, amendments to issued accounting standards and interpretations, which are relevant to the Group but not yet effective at 29 February 2016, are being evaluated for the impact of these pronouncements.

20 Astrapak Annual Financial Statements 2016

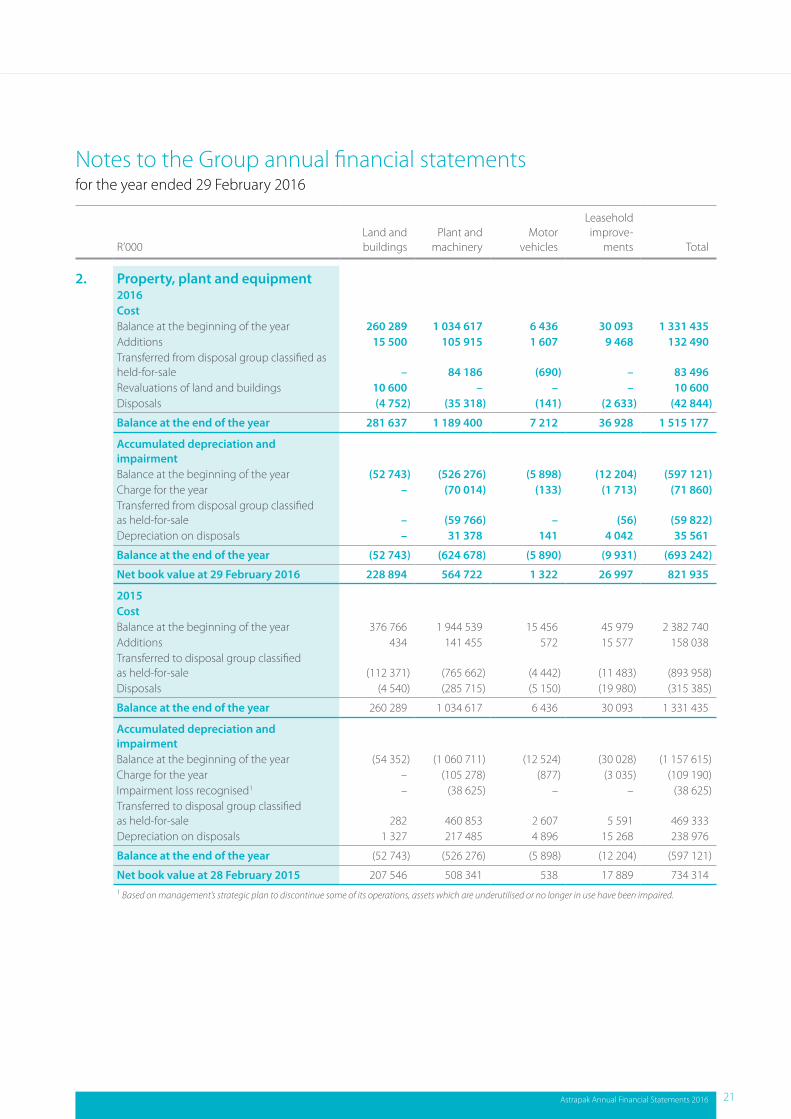

Notes to the Group annual financial statementsfor the year ended 29 February 2016

R’000Land and buildings

Plant and machinery

Motor vehicles

Leasehold improve-

ments Total

2. Property, plant and equipment2016CostBalance at the beginning of the year 260 289 1 034 617 6 436 30 093 1 331 435 Additions 15 500 105 915 1 607 9 468 132 490 Transferred from disposal group classified as held-for-sale – 84 186 (690) – 83 496 Revaluations of land and buildings 10 600 – – – 10 600 Disposals (4 752) (35 318) (141) (2 633) (42 844)

Balance at the end of the year 281 637 1 189 400 7 212 36 928 1 515 177

Accumulated depreciation and impairmentBalance at the beginning of the year (52 743) (526 276) (5 898) (12 204) (597 121)Charge for the year – (70 014) (133) (1 713) (71 860)Transferred from disposal group classified as held-for-sale – (59 766) – (56) (59 822)Depreciation on disposals – 31 378 141 4 042 35 561

Balance at the end of the year (52 743) (624 678) (5 890) (9 931) (693 242)

Net book value at 29 February 2016 228 894 564 722 1 322 26 997 821 935

2015CostBalance at the beginning of the year 376 766 1 944 539 15 456 45 979 2 382 740 Additions 434 141 455 572 15 577 158 038 Transferred to disposal group classified as held-for-sale (112 371) (765 662) (4 442) (11 483) (893 958)Disposals (4 540) (285 715) (5 150) (19 980) (315 385)

Balance at the end of the year 260 289 1 034 617 6 436 30 093 1 331 435

Accumulated depreciation and impairmentBalance at the beginning of the year (54 352) (1 060 711) (12 524) (30 028) (1 157 615)Charge for the year – (105 278) (877) (3 035) (109 190)Impairment loss recognised1 – (38 625) – – (38 625)Transferred to disposal group classified as held-for-sale 282 460 853 2 607 5 591 469 333 Depreciation on disposals 1 327 217 485 4 896 15 268 238 976

Balance at the end of the year (52 743) (526 276) (5 898) (12 204) (597 121)

Net book value at 28 February 2015 207 546 508 341 538 17 889 734 3141 Based on management’s strategic plan to discontinue some of its operations, assets which are underutilised or no longer in use have been impaired.

Astrapak Annual Financial Statements 2016 21

Notes to the Group annual financial statements continued

for the year ended 29 February 2016

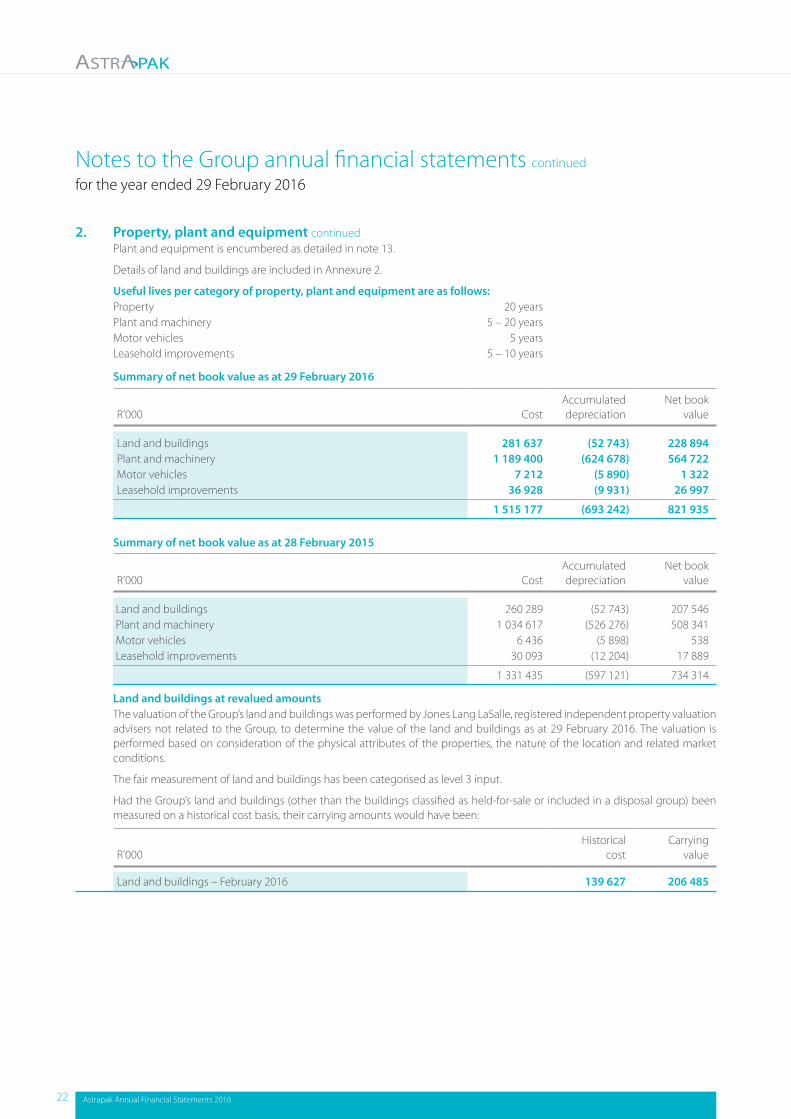

2. Property, plant and equipment continuedPlant and equipment is encumbered as detailed in note 13.

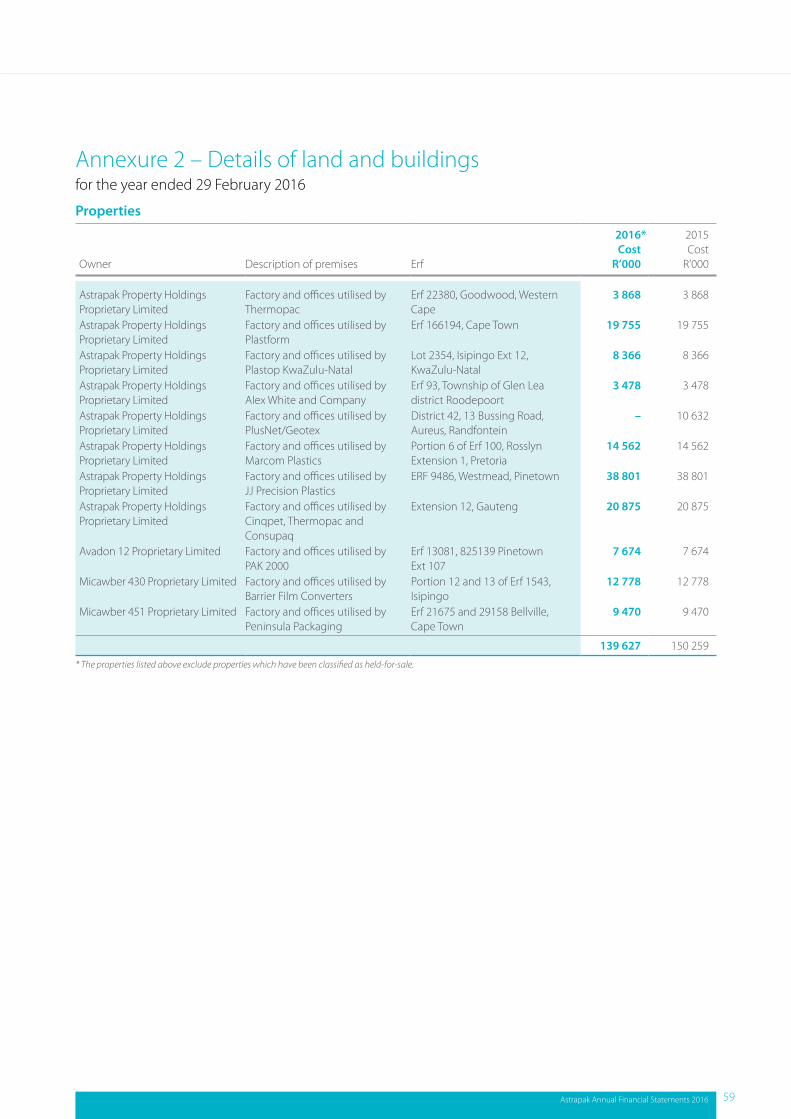

Details of land and buildings are included in Annexure 2.

Useful lives per category of property, plant and equipment are as follows: Property 20 years Plant and machinery 5 – 20 years Motor vehicles 5 years Leasehold improvements 5 – 10 years

Summary of net book value as at 29 February 2016

R’000 Cost Accumulated

depreciation Net book

value

Land and buildings 281 637 (52 743) 228 894Plant and machinery 1 189 400 (624 678) 564 722Motor vehicles 7 212 (5 890) 1 322 Leasehold improvements 36 928 (9 931) 26 997

1 515 177 (693 242) 821 935

Summary of net book value as at 28 February 2015

R’000 Cost Accumulated

depreciation Net book

value

Land and buildings 260 289 (52 743) 207 546 Plant and machinery 1 034 617 (526 276) 508 341 Motor vehicles 6 436 (5 898) 538 Leasehold improvements 30 093 (12 204) 17 889

1 331 435 (597 121) 734 314

Land and buildings at revalued amounts The valuation of the Group’s land and buildings was performed by Jones Lang LaSalle, registered independent property valuation advisers not related to the Group, to determine the value of the land and buildings as at 29 February 2016. The valuation is performed based on consideration of the physical attributes of the properties, the nature of the location and related market conditions.

The fair measurement of land and buildings has been categorised as level 3 input.

Had the Group’s land and buildings (other than the buildings classified as held-for-sale or included in a disposal group) been measured on a historical cost basis, their carrying amounts would have been:

R’000Historical

costCarrying

value

Land and buildings – February 2016 139 627 206 485

22 Astrapak Annual Financial Statements 2016

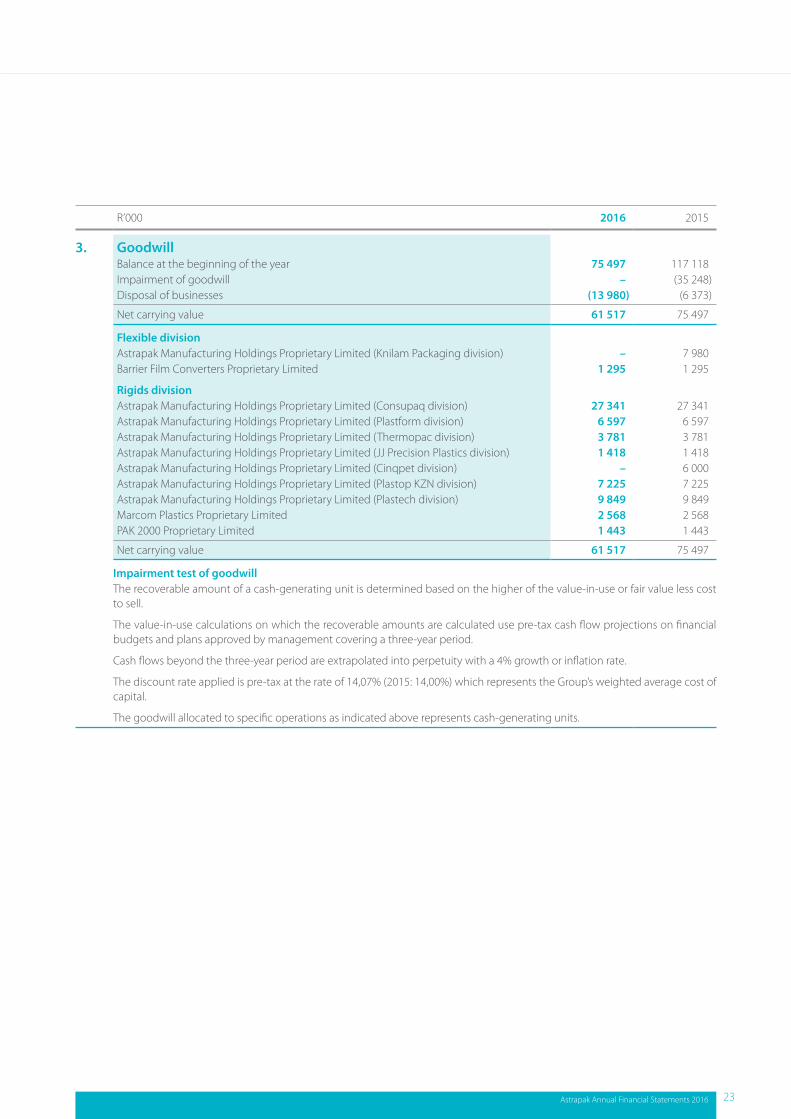

R’000 2016 2015

3. GoodwillBalance at the beginning of the year 75 497 117 118 Impairment of goodwill – (35 248)Disposal of businesses (13 980) (6 373)

Net carrying value 61 517 75 497

Flexible division Astrapak Manufacturing Holdings Proprietary Limited (Knilam Packaging division) – 7 980 Barrier Film Converters Proprietary Limited 1 295 1 295

Rigids divisionAstrapak Manufacturing Holdings Proprietary Limited (Consupaq division) 27 341 27 341 Astrapak Manufacturing Holdings Proprietary Limited (Plastform division) 6 597 6 597 Astrapak Manufacturing Holdings Proprietary Limited (Thermopac division) 3 781 3 781 Astrapak Manufacturing Holdings Proprietary Limited (JJ Precision Plastics division) 1 418 1 418 Astrapak Manufacturing Holdings Proprietary Limited (Cinqpet division) – 6 000 Astrapak Manufacturing Holdings Proprietary Limited (Plastop KZN division) 7 225 7 225 Astrapak Manufacturing Holdings Proprietary Limited (Plastech division) 9 849 9 849 Marcom Plastics Proprietary Limited 2 568 2 568 PAK 2000 Proprietary Limited 1 443 1 443

Net carrying value 61 517 75 497

Impairment test of goodwillThe recoverable amount of a cash-generating unit is determined based on the higher of the value-in-use or fair value less cost to sell.

The value-in-use calculations on which the recoverable amounts are calculated use pre-tax cash flow projections on financial budgets and plans approved by management covering a three-year period.

Cash flows beyond the three-year period are extrapolated into perpetuity with a 4% growth or inflation rate.

The discount rate applied is pre-tax at the rate of 14,07% (2015: 14,00%) which represents the Group’s weighted average cost of capital.

The goodwill allocated to specific operations as indicated above represents cash-generating units.

Astrapak Annual Financial Statements 2016 23

Notes to the Group annual financial statements continued

for the year ended 29 February 2016

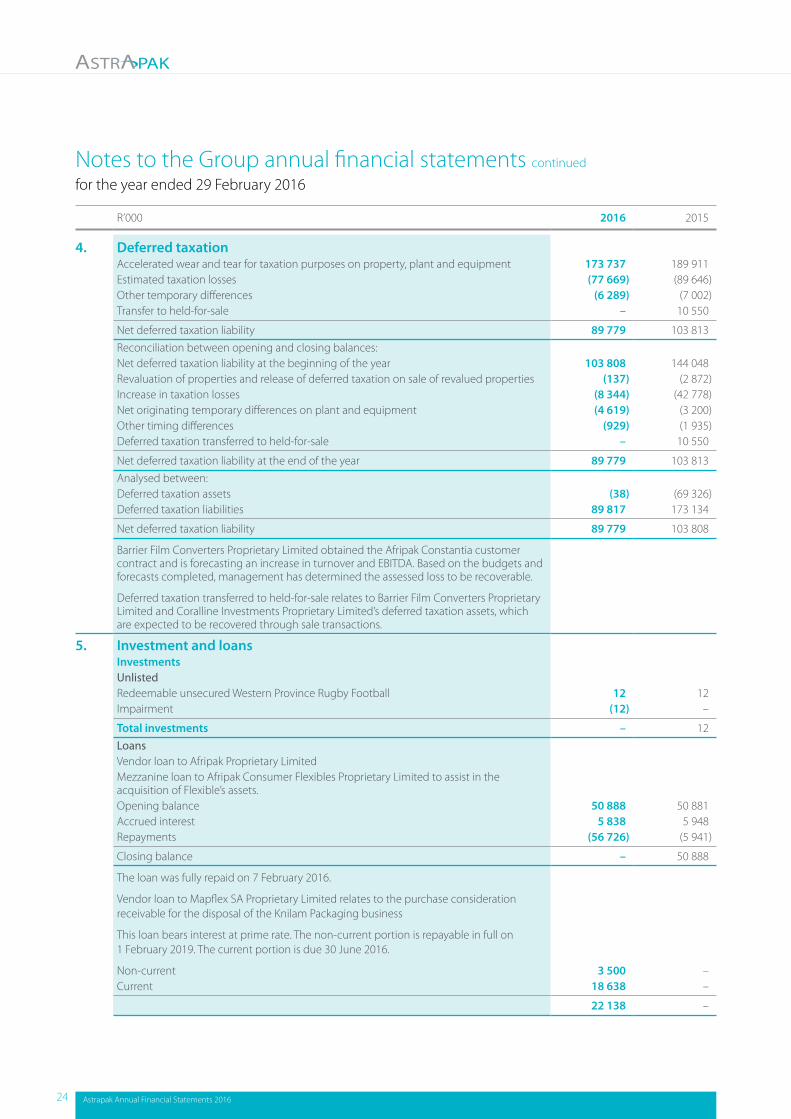

R’000 2016 2015

4. Deferred taxation Accelerated wear and tear for taxation purposes on property, plant and equipment 173 737 189 911 Estimated taxation losses (77 669) (89 646)Other temporary differences (6 289) (7 002)Transfer to held-for-sale – 10 550

Net deferred taxation liability 89 779 103 813 Reconciliation between opening and closing balances:Net deferred taxation liability at the beginning of the year 103 808 144 048 Revaluation of properties and release of deferred taxation on sale of revalued properties (137) (2 872)Increase in taxation losses (8 344) (42 778)Net originating temporary differences on plant and equipment (4 619) (3 200)Other timing differences (929) (1 935)Deferred taxation transferred to held-for-sale – 10 550

Net deferred taxation liability at the end of the year 89 779 103 813 Analysed between:Deferred taxation assets (38) (69 326)Deferred taxation liabilities 89 817 173 134

Net deferred taxation liability 89 779 103 808

Barrier Film Converters Proprietary Limited obtained the Afripak Constantia customer contract and is forecasting an increase in turnover and EBITDA. Based on the budgets and forecasts completed, management has determined the assessed loss to be recoverable.

Deferred taxation transferred to held-for-sale relates to Barrier Film Converters Proprietary Limited and Coralline Investments Proprietary Limited’s deferred taxation assets, which are expected to be recovered through sale transactions.

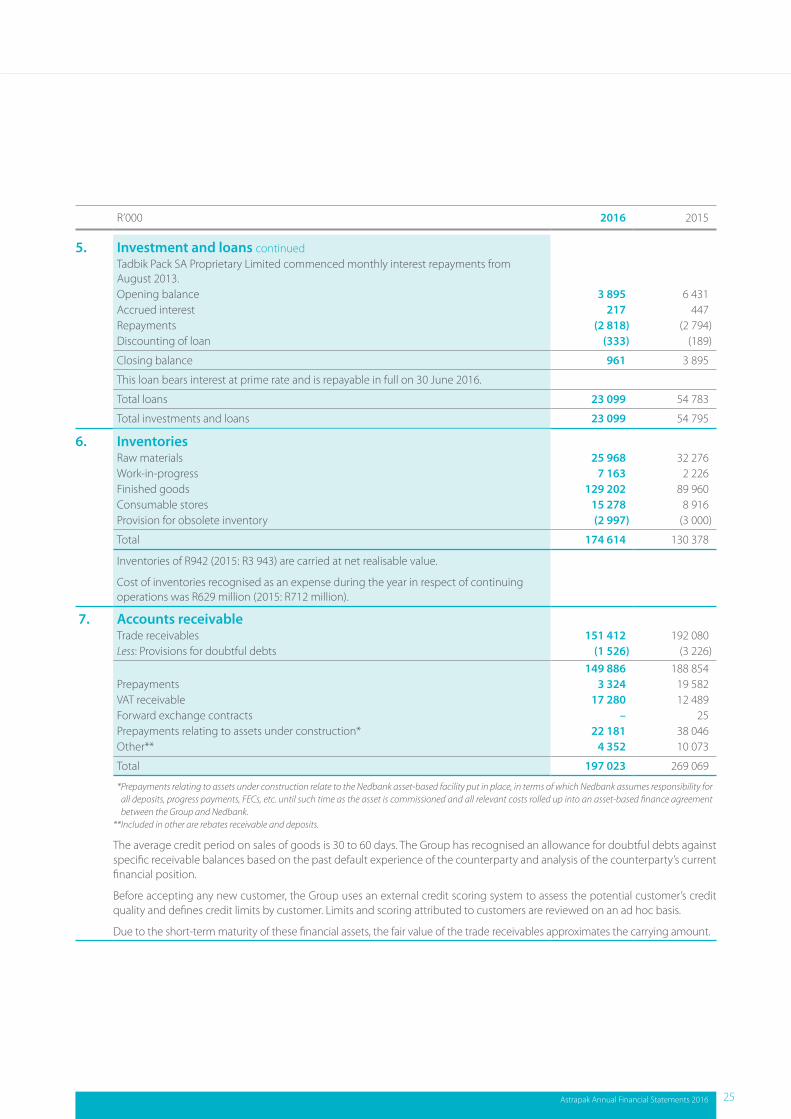

5. Investment and loans Investments Unlisted Redeemable unsecured Western Province Rugby Football 12 12 Impairment (12) –

Total investments – 12 Loans Vendor loan to Afripak Proprietary Limited Mezzanine loan to Afripak Consumer Flexibles Proprietary Limited to assist in the acquisition of Flexible’s assets. Opening balance 50 888 50 881 Accrued interest 5 838 5 948 Repayments (56 726) (5 941)

Closing balance – 50 888

The loan was fully repaid on 7 February 2016.

Vendor loan to Mapflex SA Proprietary Limited relates to the purchase consideration receivable for the disposal of the Knilam Packaging business

This loan bears interest at prime rate. The non-current portion is repayable in full on 1 February 2019. The current portion is due 30 June 2016.

Non-current 3 500 –Current 18 638 –

22 138 –

24 Astrapak Annual Financial Statements 2016

R’000 2016 2015

5. Investment and loans continuedTadbik Pack SA Proprietary Limited commenced monthly interest repayments from August 2013.Opening balance 3 895 6 431 Accrued interest 217 447 Repayments (2 818) (2 794)Discounting of loan (333) (189)

Closing balance 961 3 895

This loan bears interest at prime rate and is repayable in full on 30 June 2016.

Total loans 23 099 54 783

Total investments and loans 23 099 54 795

6. Inventories Raw materials 25 968 32 276 Work-in-progress 7 163 2 226 Finished goods 129 202 89 960 Consumable stores 15 278 8 916 Provision for obsolete inventory (2 997) (3 000)

Total 174 614 130 378

Inventories of R942 (2015: R3 943) are carried at net realisable value.

Cost of inventories recognised as an expense during the year in respect of continuing operations was R629 million (2015: R712 million).

7. Accounts receivable Trade receivables 151 412 192 080 Less: Provisions for doubtful debts (1 526) (3 226)

149 886 188 854 Prepayments 3 324 19 582 VAT receivable 17 280 12 489 Forward exchange contracts – 25 Prepayments relating to assets under construction* 22 181 38 046 Other** 4 352 10 073

Total 197 023 269 069

* Prepayments relating to assets under construction relate to the Nedbank asset-based facility put in place, in terms of which Nedbank assumes responsibility for all deposits, progress payments, FECs, etc. until such time as the asset is commissioned and all relevant costs rolled up into an asset-based finance agreement between the Group and Nedbank.

**Included in other are rebates receivable and deposits.

The average credit period on sales of goods is 30 to 60 days. The Group has recognised an allowance for doubtful debts against specific receivable balances based on the past default experience of the counterparty and analysis of the counterparty’s current financial position.

Before accepting any new customer, the Group uses an external credit scoring system to assess the potential customer’s credit quality and defines credit limits by customer. Limits and scoring attributed to customers are reviewed on an ad hoc basis.

Due to the short-term maturity of these financial assets, the fair value of the trade receivables approximates the carrying amount.

Astrapak Annual Financial Statements 2016 25

Notes to the Group annual financial statements continued

for the year ended 29 February 2016

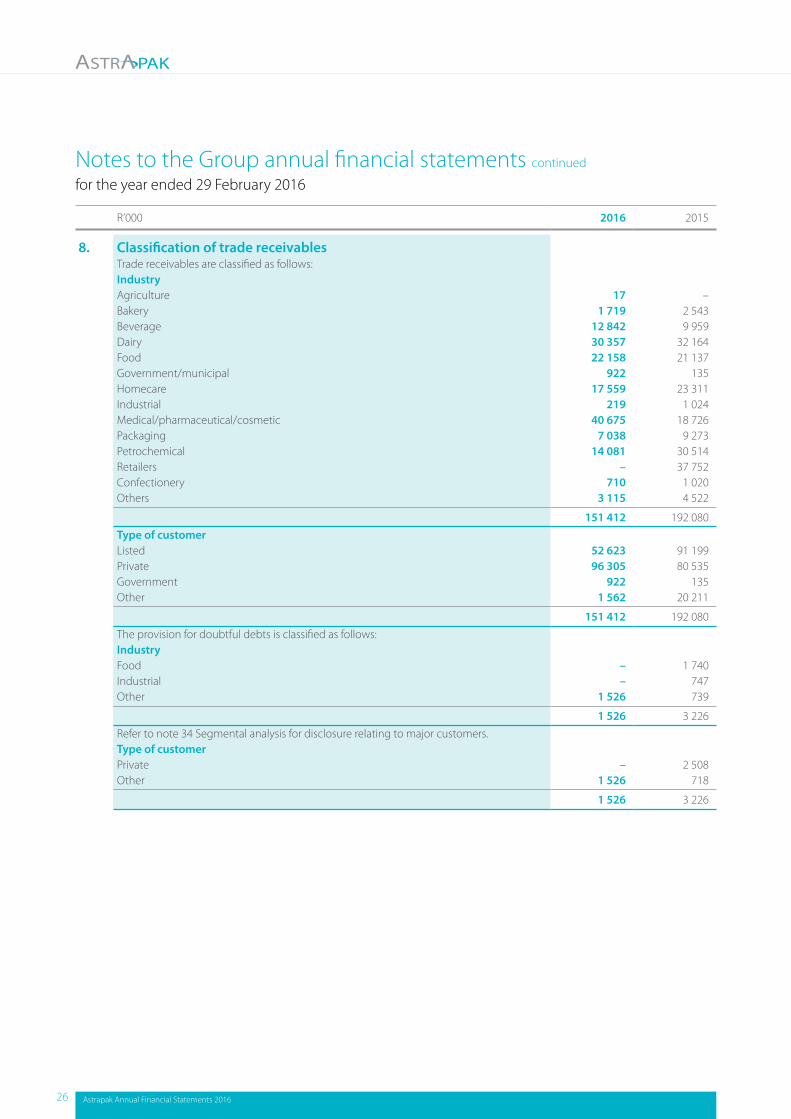

R’000 2016 2015

8. Classification of trade receivables Trade receivables are classified as follows: Industry Agriculture 17 –Bakery 1 719 2 543 Beverage 12 842 9 959 Dairy 30 357 32 164 Food 22 158 21 137 Government/municipal 922 135 Homecare 17 559 23 311 Industrial 219 1 024 Medical/pharmaceutical/cosmetic 40 675 18 726 Packaging 7 038 9 273 Petrochemical 14 081 30 514 Retailers – 37 752 Confectionery 710 1 020 Others 3 115 4 522

151 412 192 080 Type of customer Listed 52 623 91 199 Private 96 305 80 535 Government 922 135 Other 1 562 20 211

151 412 192 080 The provision for doubtful debts is classified as follows: Industry Food – 1 740 Industrial – 747 Other 1 526 739

1 526 3 226 Refer to note 34 Segmental analysis for disclosure relating to major customers. Type of customer Private – 2 508 Other 1 526 718

1 526 3 226

26 Astrapak Annual Financial Statements 2016

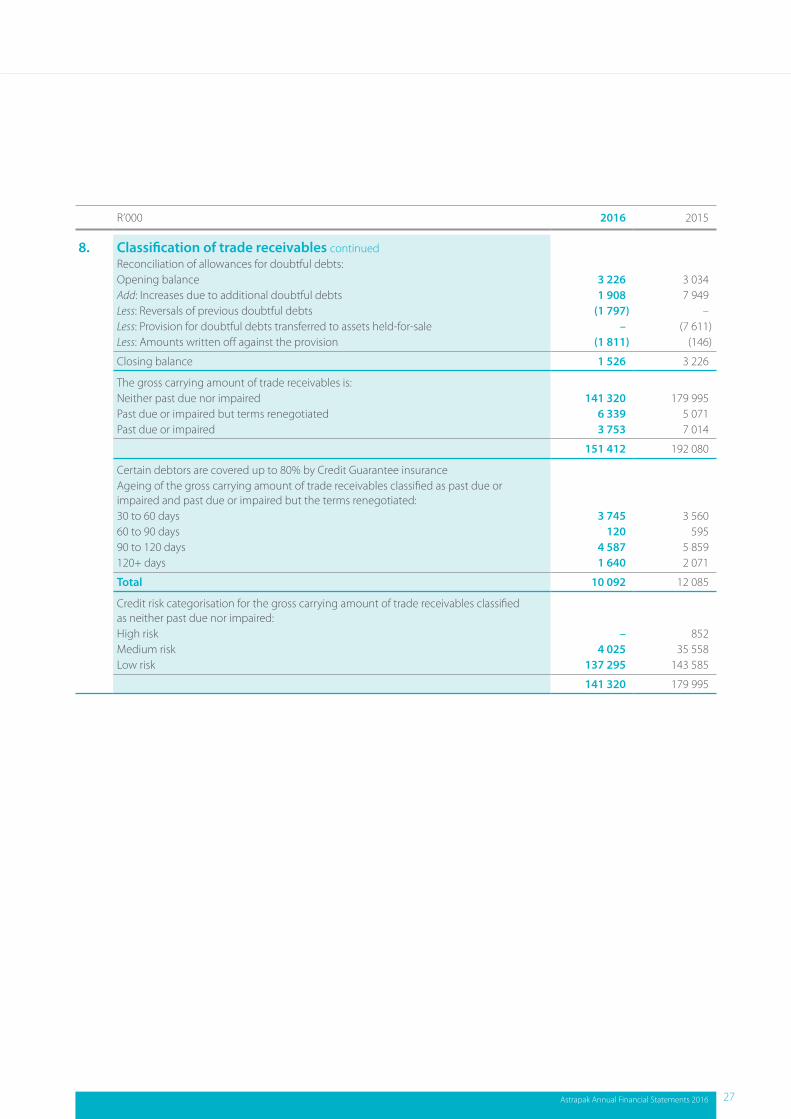

R’000 2016 2015

8. Classification of trade receivables continuedReconciliation of allowances for doubtful debts: Opening balance 3 226 3 034 Add: Increases due to additional doubtful debts 1 908 7 949 Less: Reversals of previous doubtful debts (1 797) –Less: Provision for doubtful debts transferred to assets held-for-sale – (7 611)Less: Amounts written off against the provision (1 811) (146)

Closing balance 1 526 3 226

The gross carrying amount of trade receivables is: Neither past due nor impaired 141 320 179 995 Past due or impaired but terms renegotiated 6 339 5 071 Past due or impaired 3 753 7 014

151 412 192 080

Certain debtors are covered up to 80% by Credit Guarantee insurance Ageing of the gross carrying amount of trade receivables classified as past due or impaired and past due or impaired but the terms renegotiated: 30 to 60 days 3 745 3 560 60 to 90 days 120 595 90 to 120 days 4 587 5 859 120+ days 1 640 2 071

Total 10 092 12 085

Credit risk categorisation for the gross carrying amount of trade receivables classified as neither past due nor impaired: High risk – 852 Medium risk 4 025 35 558 Low risk 137 295 143 585

141 320 179 995

Astrapak Annual Financial Statements 2016 27

Notes to the Group annual financial statements continued

for the year ended 29 February 2016

R’000 2016 2015

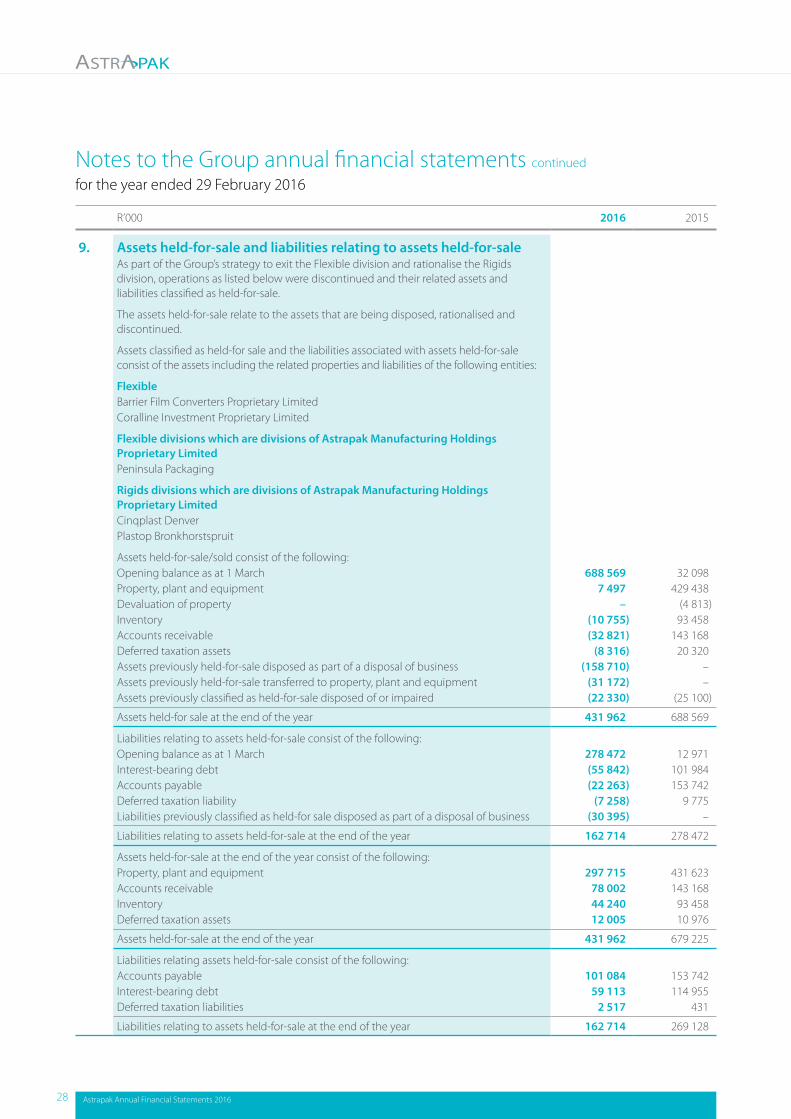

9. Assets held-for-sale and liabilities relating to assets held-for-sale As part of the Group’s strategy to exit the Flexible division and rationalise the Rigids division, operations as listed below were discontinued and their related assets and liabilities classified as held-for-sale.

The assets held-for-sale relate to the assets that are being disposed, rationalised and discontinued.

Assets classified as held-for sale and the liabilities associated with assets held-for-sale consist of the assets including the related properties and liabilities of the following entities:

FlexibleBarrier Film Converters Proprietary LimitedCoralline Investment Proprietary Limited

Flexible divisions which are divisions of Astrapak Manufacturing Holdings Proprietary LimitedPeninsula Packaging