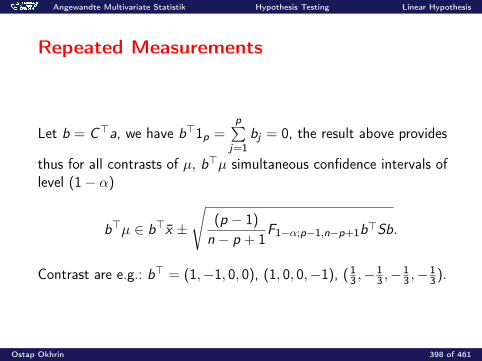

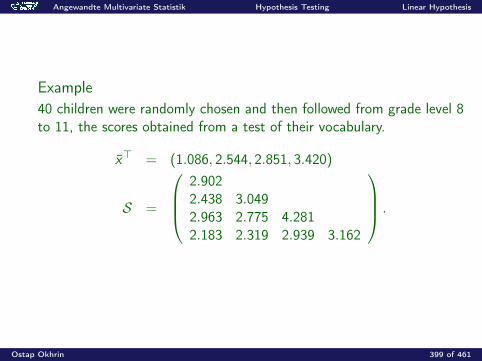

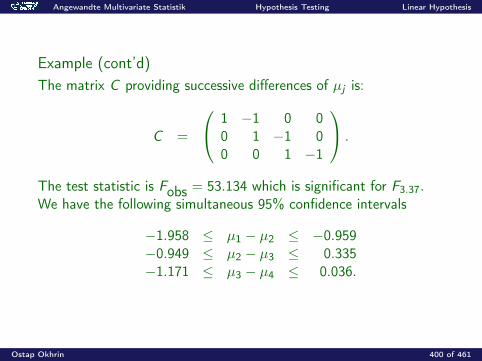

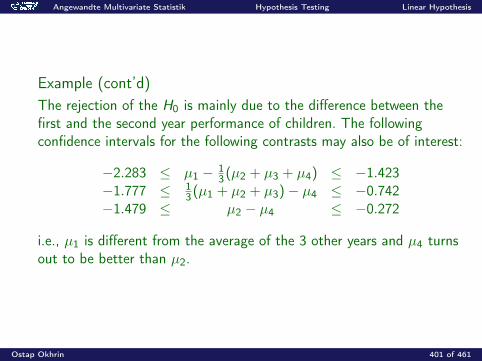

Embed Size (px)

Citation preview

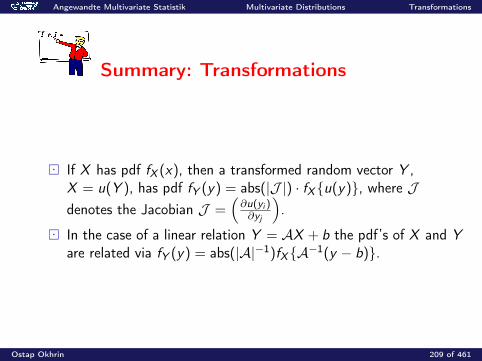

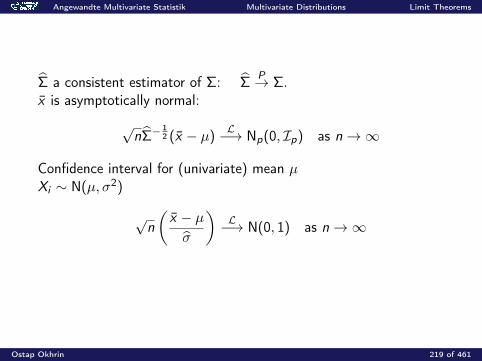

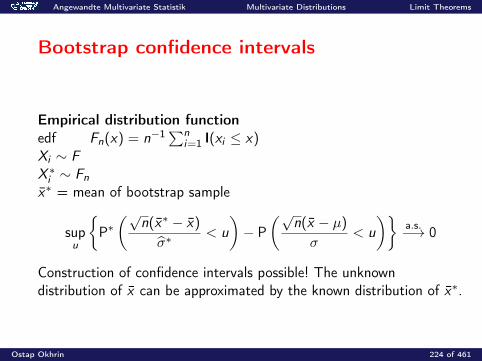

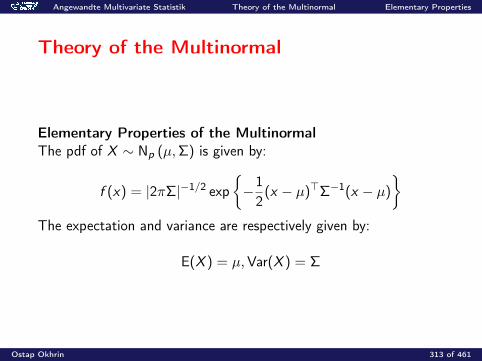

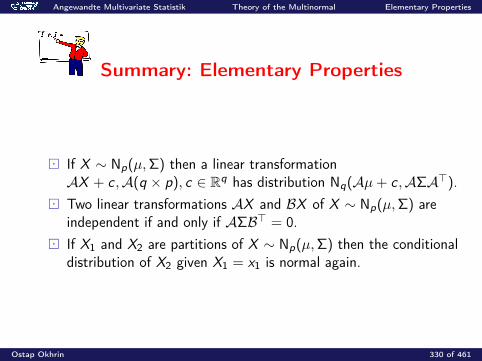

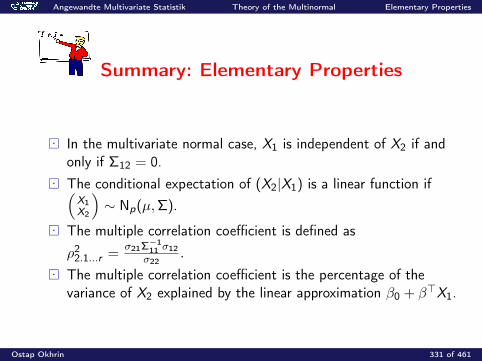

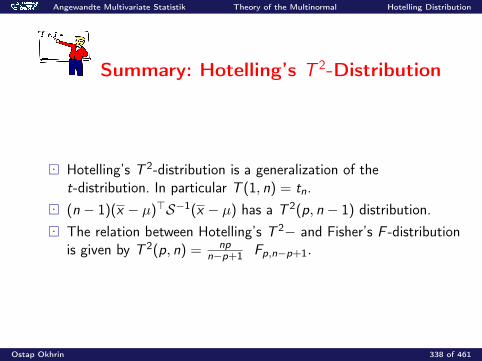

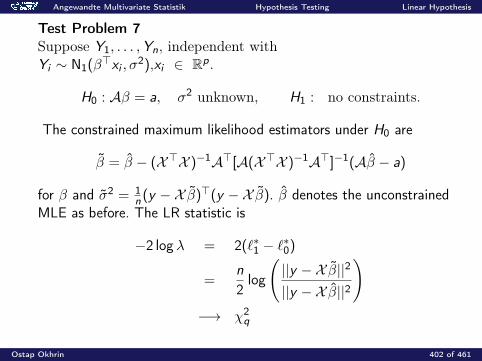

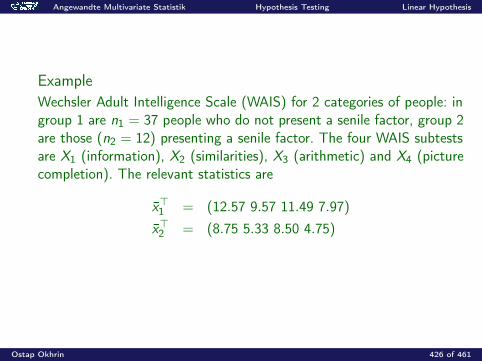

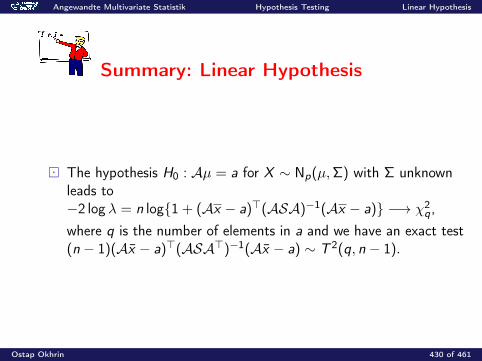

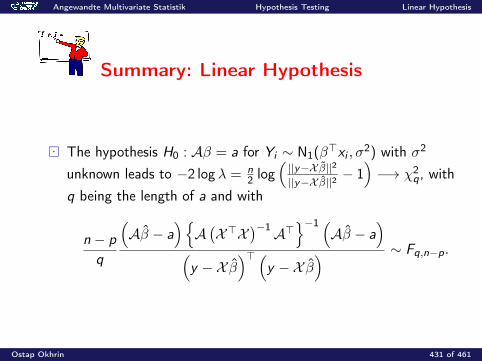

Angewandte Multivariate Statistik

Angewandte Multivariate Statistik

Prof. Dr. Ostap Okhrin

Ostap Okhrin 1 of 461

Angewandte Multivariate Statistik

Basis

These slides strongly based on those made by Ladislaus vonBortkiewicz Chair of Statistics, Humboldt University Berlin

Applied Multivariate Statistical Analysis(W.Härdle, L.Simar)- lvb.wiwi.hu-berlin.de

Ostap Okhrin 2 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

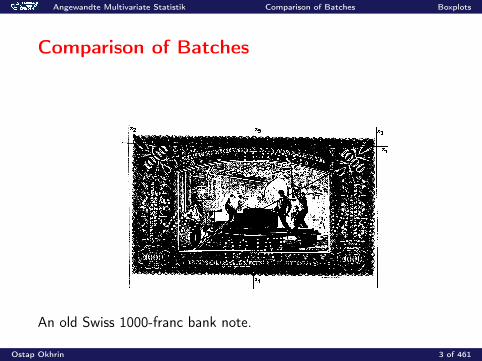

Comparison of Batches

An old Swiss 1000-franc bank note.

Ostap Okhrin 3 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

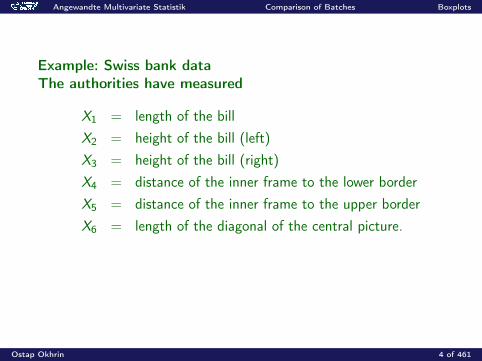

Example: Swiss bank dataThe authorities have measured

X1 = length of the billX2 = height of the bill (left)X3 = height of the bill (right)X4 = distance of the inner frame to the lower borderX5 = distance of the inner frame to the upper borderX6 = length of the diagonal of the central picture.

Ostap Okhrin 4 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

Example: (cont.)The dataset consists of 200 measurements on Swiss bank notes. Thefirst half of these bank notes are genuine, the other half are forgedbank notes.It is important to be able to decide whether a given banknote isgenuine.We want to derive a good rule that separates the genuine andcounterfeit banknotes.Which measurement is the most informative? We have to visualize thedifference.

Ostap Okhrin 5 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

Boxplots

Boxplot is a graphical technique for displaying the distribution of variables. helps us in seeing location, skewness, spread, tail length and

outlying points. is particularly useful in comparing different batches. is a graphical representation of the Five Number Summary.

Ostap Okhrin 6 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

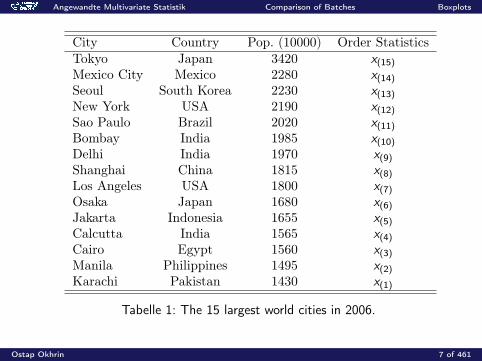

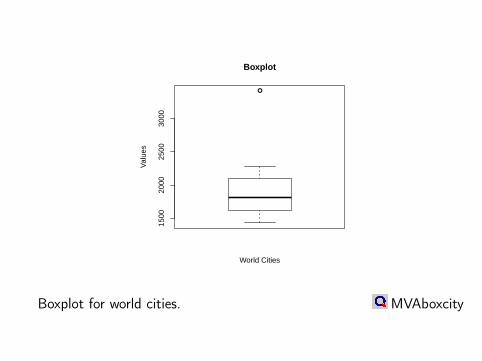

City Country Pop. (10000) Order StatisticsTokyo Japan 3420 x(15)

Mexico City Mexico 2280 x(14)

Seoul South Korea 2230 x(13)

New York USA 2190 x(12)

Sao Paulo Brazil 2020 x(11)

Bombay India 1985 x(10)

Delhi India 1970 x(9)

Shanghai China 1815 x(8)

Los Angeles USA 1800 x(7)

Osaka Japan 1680 x(6)

Jakarta Indonesia 1655 x(5)

Calcutta India 1565 x(4)

Cairo Egypt 1560 x(3)

Manila Philippines 1495 x(2)

Karachi Pakistan 1430 x(1)

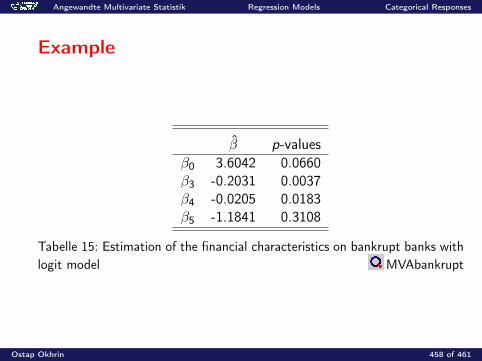

Tabelle 1: The 15 largest world cities in 2006.

Ostap Okhrin 7 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

Five Number Summary

Upper quartile FU

Lower quartile FL

Median = deepest point Extremes

Consider the order statistics→ Depth of a data value x(i): mini , n − i + 1

depth of fourth =[depth of median] + 1

2

Ostap Okhrin 8 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

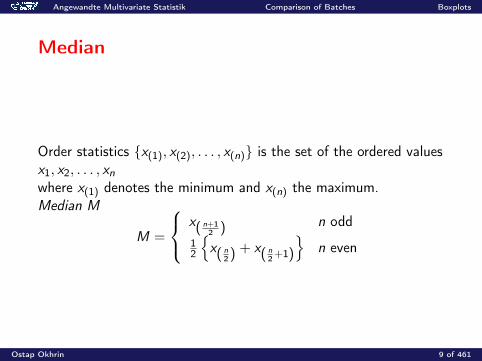

Median

Order statistics x(1), x(2), . . . , x(n) is the set of the ordered valuesx1, x2, . . . , xnwhere x(1) denotes the minimum and x(n) the maximum.Median M

M =

x( n+12 ) n odd

12

x( n

2) + x( n2+1)

n even

Ostap Okhrin 9 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

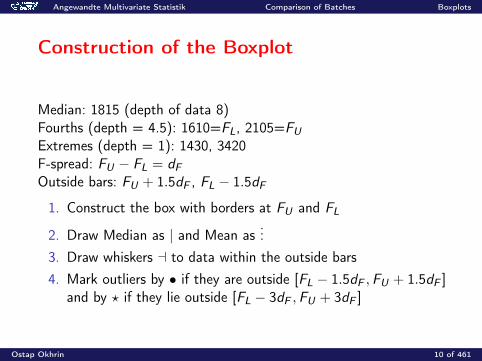

Construction of the Boxplot

Median: 1815 (depth of data 8)Fourths (depth = 4.5): 1610=FL, 2105=FUExtremes (depth = 1): 1430, 3420F-spread: FU − FL = dFOutside bars: FU + 1.5dF , FL − 1.5dF

1. Construct the box with borders at FU and FL

2. Draw Median as | and Mean as...

3. Draw whiskers a to data within the outside bars4. Mark outliers by • if they are outside [FL − 1.5dF ,FU + 1.5dF ]

and by ? if they lie outside [FL − 3dF ,FU + 3dF ]

Ostap Okhrin 10 of 461

1500

2000

2500

3000

World Cities

Val

ues

Boxplot

Boxplot for world cities. MVAboxcity

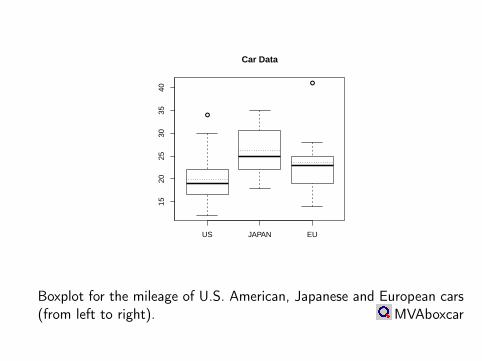

US JAPAN EU

1520

2530

3540

Car Data

Boxplot for the mileage of U.S. American, Japanese and European cars(from left to right). MVAboxcar

GENUINE COUNTERFEIT

138

139

140

141

142

Swiss Bank Notes

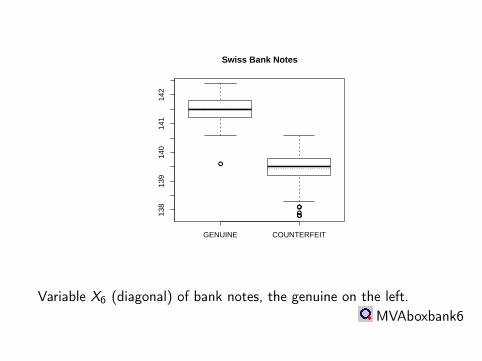

Variable X6 (diagonal) of bank notes, the genuine on the left.MVAboxbank6

GENUINE COUNTERFEIT

214

214.

521

521

5.5

216

Swiss Bank Notes

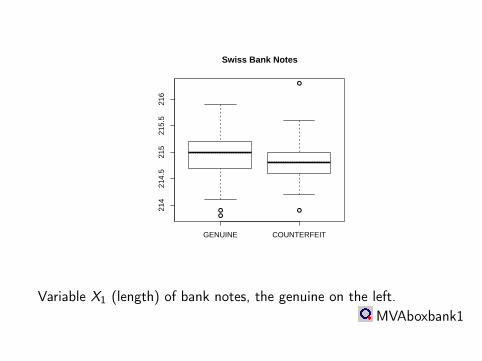

Variable X1 (length) of bank notes, the genuine on the left.MVAboxbank1

Angewandte Multivariate Statistik Comparison of Batches Boxplots

Summary: Boxplots

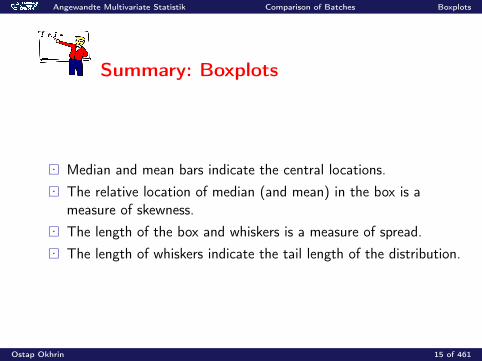

Median and mean bars indicate the central locations. The relative location of median (and mean) in the box is a

measure of skewness. The length of the box and whiskers is a measure of spread. The length of whiskers indicate the tail length of the distribution.

Ostap Okhrin 15 of 461

Angewandte Multivariate Statistik Comparison of Batches Boxplots

Summary: Boxplots

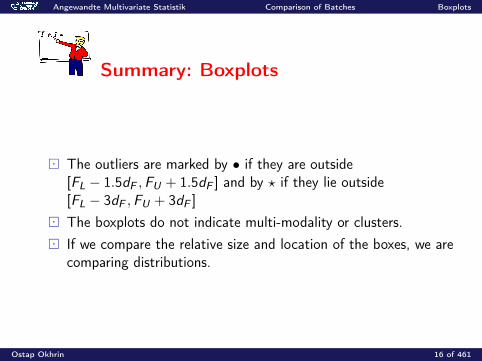

The outliers are marked by • if they are outside[FL − 1.5dF ,FU + 1.5dF ] and by ? if they lie outside[FL − 3dF ,FU + 3dF ]

The boxplots do not indicate multi-modality or clusters. If we compare the relative size and location of the boxes, we are

comparing distributions.

Ostap Okhrin 16 of 461

Angewandte Multivariate Statistik Comparison of Batches Histograms

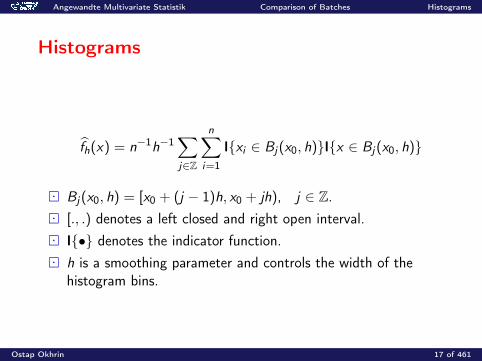

Histograms

fh(x) = n−1h−1∑j∈Z

n∑i=1

Ixi ∈ Bj(x0, h)Ix ∈ Bj(x0, h)

Bj(x0, h) = [x0 + (j − 1)h, x0 + jh), j ∈ Z. [., .) denotes a left closed and right open interval. I• denotes the indicator function. h is a smoothing parameter and controls the width of the

histogram bins.

Ostap Okhrin 17 of 461

Swiss Bank Notes

h = 0.1

Dia

gona

l

138 139 140 141

04

8

Swiss Bank Notes

h = 0.3

Dia

gona

l

138 139 140 141

010

2030

Swiss Bank Notes

h = 0.2

Dia

gona

l

138 139 140 141

05

15

Swiss Bank Notes

h = 0.4D

iago

nal

138 139 140 141

020

40

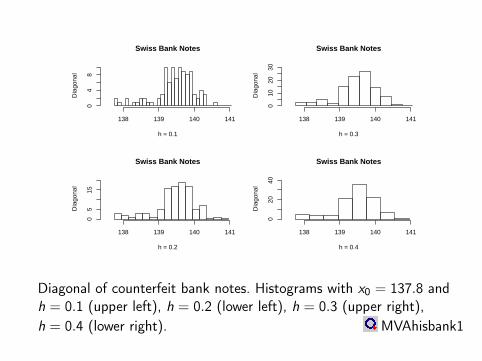

Diagonal of counterfeit bank notes. Histograms with x0 = 137.8 andh = 0.1 (upper left), h = 0.2 (lower left), h = 0.3 (upper right),h = 0.4 (lower right). MVAhisbank1

Swiss Bank Notes

x_0 = 137.65

Dia

gona

l

138 139 140 141

020

40

Swiss Bank Notes

x_0 = 137.85

Dia

gona

l

138 139 140 141

020

40

Swiss Bank Notes

x_0 = 137.75

Dia

gona

l

138 139 140 141

020

40

Swiss Bank Notes

x_0 = 137.95D

iago

nal

138 139 140 141

020

40

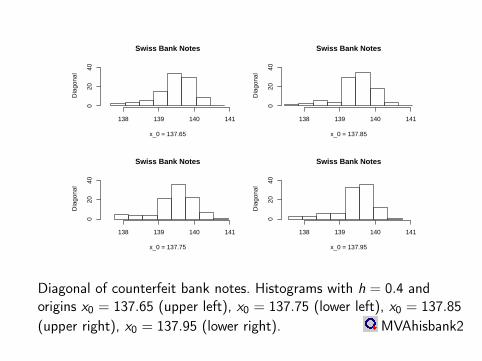

Diagonal of counterfeit bank notes. Histograms with h = 0.4 andorigins x0 = 137.65 (upper left), x0 = 137.75 (lower left), x0 = 137.85(upper right), x0 = 137.95 (lower right). MVAhisbank2

Angewandte Multivariate Statistik Comparison of Batches Histograms

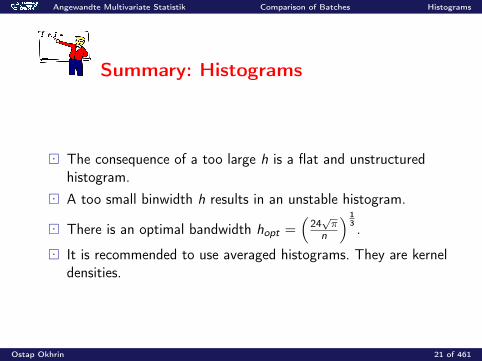

Summary: Histograms

Modes of the density are detected with a histogram. Modes correspond to strong peaks in the histogram. Histograms with the same h need not be identical. They also

depend on the origin x0 of the grid. The influence of the origin x0 is drastic. Changing x0 creates

different looking histograms.

Ostap Okhrin 20 of 461

Angewandte Multivariate Statistik Comparison of Batches Histograms

Summary: Histograms

The consequence of a too large h is a flat and unstructuredhistogram.

A too small binwidth h results in an unstable histogram.

There is an optimal bandwidth hopt =(

24√π

n

) 13 .

It is recommended to use averaged histograms. They are kerneldensities.

Ostap Okhrin 21 of 461

Angewandte Multivariate Statistik Comparison of Batches Kernel densities

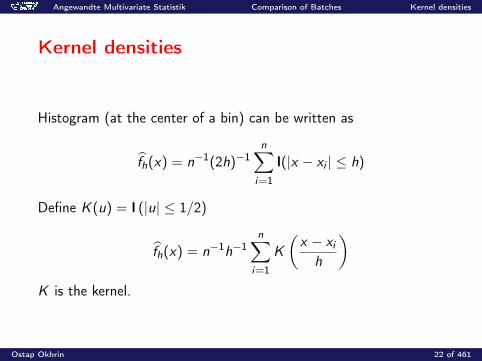

Kernel densities

Histogram (at the center of a bin) can be written as

fh(x) = n−1(2h)−1n∑

i=1

I(|x − xi | ≤ h)

Define K (u) = I (|u| ≤ 1/2)

fh(x) = n−1h−1n∑

i=1

K

(x − xi

h

)K is the kernel.

Ostap Okhrin 22 of 461

Angewandte Multivariate Statistik Comparison of Batches Kernel densities

Kernel functions

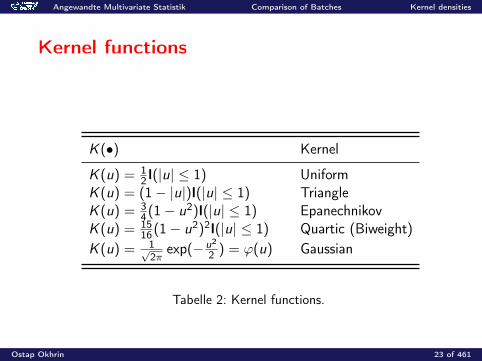

K (•) Kernel

K (u) = 12 I(|u| ≤ 1) Uniform

K (u) = (1− |u|)I(|u| ≤ 1) TriangleK (u) = 3

4(1− u2)I(|u| ≤ 1) EpanechnikovK (u) = 15

16(1− u2)2I(|u| ≤ 1) Quartic (Biweight)K (u) = 1√

2πexp(−u2

2 ) = ϕ(u) Gaussian

Tabelle 2: Kernel functions.

Ostap Okhrin 23 of 461

Angewandte Multivariate Statistik Comparison of Batches Kernel densities

Kernel functions

−2 0 20

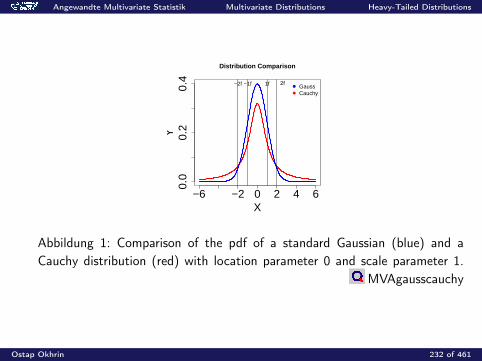

0.5

1

Uniform

−2 0 20

0.5

1

Triangle

−2 0 20

0.5

1

Epanechnikov

−2 0 20

0.5

1

Quartic (biweight)

−2 0 20

0.5

1

Gaussian

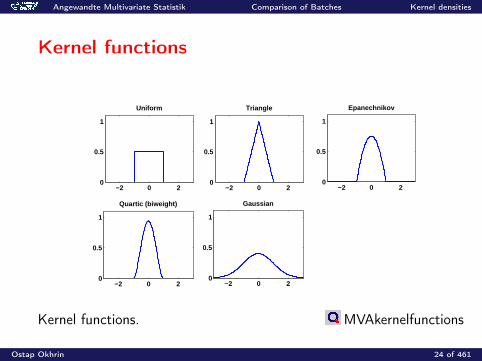

Kernel functions. MVAkernelfunctions

Ostap Okhrin 24 of 461

137 138 139 140 141 142 143

0.0

0.2

0.4

0.6

0.8

Swiss bank notes

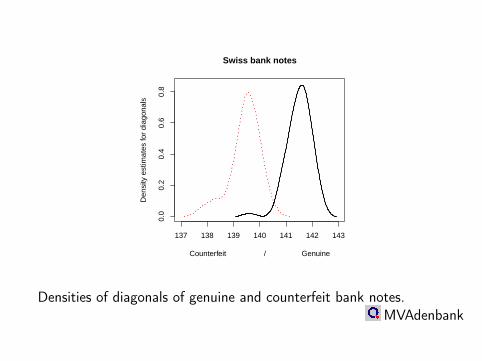

Counterfeit / Genuine

Den

sity

est

imat

es fo

r di

agon

als

Densities of diagonals of genuine and counterfeit bank notes.MVAdenbank

Angewandte Multivariate Statistik Comparison of Batches Kernel densities

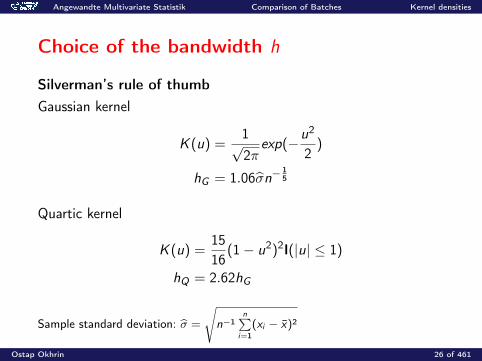

Choice of the bandwidth h

Silverman’s rule of thumbGaussian kernel

K (u) =1√2π

exp(−u2

2)

hG = 1.06σn−15

Quartic kernel

K (u) =1516

(1− u2)2I(|u| ≤ 1)

hQ = 2.62hG

Sample standard deviation: σ =

√n−1

n∑i=1

(xi − x)2

Ostap Okhrin 26 of 461

0.02 0.04 0.06

0.08

0.1

0.1

0.12

0.12

0.14

0.14

0.16

0.16

0.18

9 10 11 12

138

139

140

141

142

143

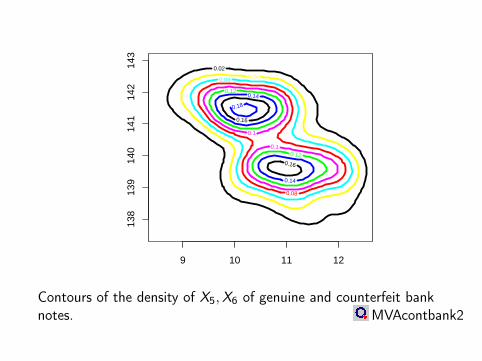

Contours of the density of X5,X6 of genuine and counterfeit banknotes. MVAcontbank2

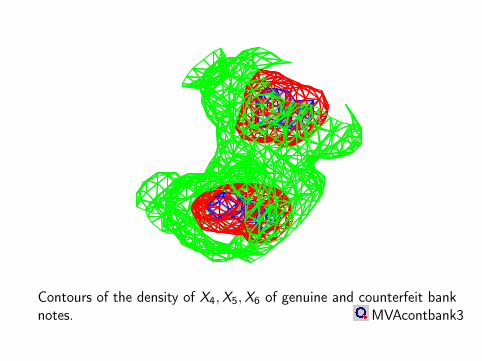

Contours of the density of X4,X5,X6 of genuine and counterfeit banknotes. MVAcontbank3

Angewandte Multivariate Statistik Comparison of Batches Kernel densities

Summary: Kernel densities

Kernel densities estimate distribution densities by the kernelmethod.

The bandwidth h determines the degree of smoothness of theestimate f .

Kernel densities are smooth functions and they can graphicallyrepresent distributions (up to 3 dimensions).

Ostap Okhrin 29 of 461

Angewandte Multivariate Statistik Comparison of Batches Kernel densities

Summary: Kernel densities

A simple (but not necessarily correct) way to find a goodbandwidth is to compute the rule of thumb bandwidthhG = 1.06σn−1/5. This bandwidth is to be used only incombination with a Gaussian kernel ϕ.

Kernel density estimates are a good descriptive tool for seeingmodes, location, skewness, tails, asymmetry, etc.

Ostap Okhrin 30 of 461

Angewandte Multivariate Statistik Comparison of Batches Scatterplots

Scatterplots

Scatterplots - bivariate or trivariate plots of variables against eachother

Rotation of data Separation lines Draftman’s plot Brushing Parallel coordinate plots

Ostap Okhrin 31 of 461

7 8 9 10 11 12 13

138

139

140

141

142

Swiss bank notes

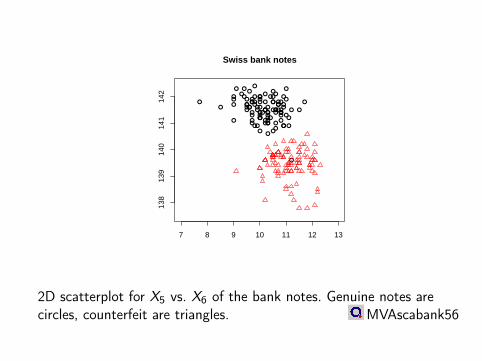

2D scatterplot for X5 vs. X6 of the bank notes. Genuine notes arecircles, counterfeit are triangles. MVAscabank56

Swiss bank notes

8 10 11 13 14 8 9 10 11 12

139

140

140

141

142

Lower inner frame (X4) Upper inner frame (X5)

Dia

gona

l (X

6)

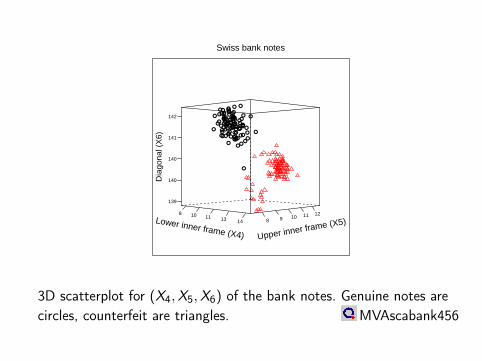

3D scatterplot for (X4,X5,X6) of the bank notes. Genuine notes arecircles, counterfeit are triangles. MVAscabank456

3

X

Y

128.5 129.0 129.5 130.0 130.5 131.0 131.5

78

910

1112

13

X

Y

128.5 129.0 129.5 130.0 130.5 131.0 131.5

78

910

1112

13

X

Y

128.5 129.0 129.5 130.0 130.5 131.0 131.5

137

138

139

140

141

142

143

7 8 9 10 11 12

129.

012

9.5

130.

013

0.5

131.

0

X

Y

4

X

Y

7 8 9 10 11 12 13

78

910

1112

13

X

Y

7 8 9 10 11 12 13

137

138

139

140

141

142

143

8 9 10 11 12

129.

012

9.5

130.

013

0.5

131.

0

X

Y

8 9 10 11 12

78

910

1112

X

Y

5

X

Y

7 8 9 10 11 12 13

137

138

139

140

141

142

143

138 139 140 141 142

129.

012

9.5

130.

013

0.5

131.

0

X

Y

138 139 140 141 142

78

910

1112

X

Y

138 139 140 141 142

89

1011

12

X

Y

6

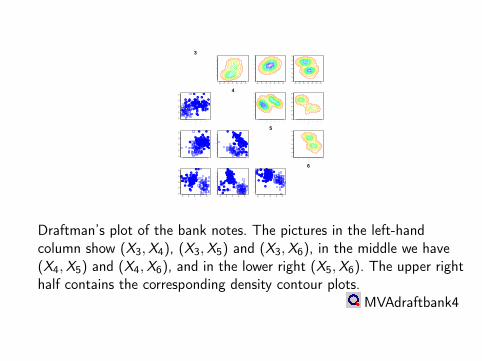

Draftman’s plot of the bank notes. The pictures in the left-handcolumn show (X3,X4), (X3,X5) and (X3,X6), in the middle we have(X4,X5) and (X4,X6), and in the lower right (X5,X6). The upper righthalf contains the corresponding density contour plots.

MVAdraftbank4

Angewandte Multivariate Statistik Comparison of Batches Scatterplots

Summary: Scatterplots

Scatterplots in two and three dimensions help us in seeingseparated points, clouds or sub-clusters.

They help us in judging positive or negative dependence. Draftman scatterplot matrices are useful for detecting structures

conditioned on values of certain other variables. As the brush of a scatterplot matrix is moving in the point cloud

we can study conditional dependence.

Ostap Okhrin 35 of 461

Angewandte Multivariate Statistik Comparison of Batches Chernoff-Flury faces

Chernoff-Flury Faces

Index

91

Index

92

Index

93

Index

94

Index

95

Index

96

Index

97

Index

98

Index

99

Index

100

Index

101

Index

102

Index

103

Index

104

Index

105

Index

106

Index

107

Index

108

Index

109

Index

110

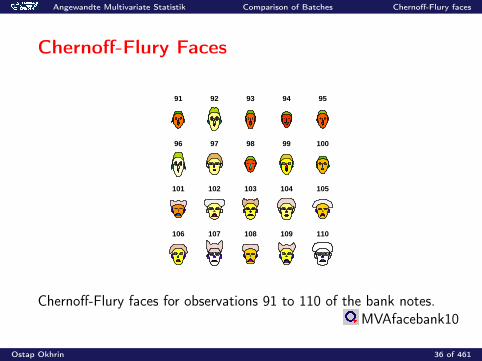

Chernoff-Flury faces for observations 91 to 110 of the bank notes.MVAfacebank10

Ostap Okhrin 36 of 461

Angewandte Multivariate Statistik Comparison of Batches Chernoff-Flury faces

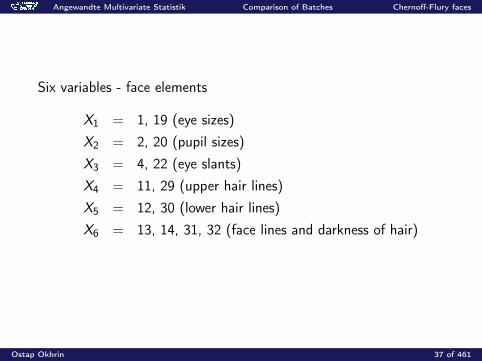

Six variables - face elements

X1 = 1, 19 (eye sizes)X2 = 2, 20 (pupil sizes)X3 = 4, 22 (eye slants)X4 = 11, 29 (upper hair lines)X5 = 12, 30 (lower hair lines)X6 = 13, 14, 31, 32 (face lines and darkness of hair)

Ostap Okhrin 37 of 461

Index

1

Index

2

Index

3

Index

4

Index

5

Index

6

Index

7

Index

8

Index

9

Index

10

Index

11

Index

12

Index

13

Index

14

Index

15

Index

16

Index

17

Index

18

Index

19

Index

20

Index

21

Index

22

Index

23

Index

24

Index

25

Index

26

Index

27

Index

28

Index

29

Index

30

Index

31

Index

32

Index

33

Index

34

Index

35

Index

36

Index

37

Index

38

Index

39

Index

40

Index

41

Index

42

Index

43

Index

44

Index

45

Index

46

Index

47

Index

48

Index

49

Index

50

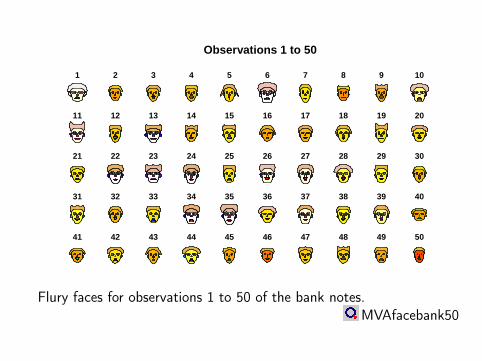

Observations 1 to 50

Flury faces for observations 1 to 50 of the bank notes.MVAfacebank50

Index

51

Index

52

Index

53

Index

54

Index

55

Index

56

Index

57

Index

58

Index

59

Index

60

Index

61

Index

62

Index

63

Index

64

Index

65

Index

66

Index

67

Index

68

Index

69

Index

70

Index

71

Index

72

Index

73

Index

74

Index

75

Index

76

Index

77

Index

78

Index

79

Index

80

Index

81

Index

82

Index

83

Index

84

Index

85

Index

86

Index

87

Index

88

Index

89

Index

90

Index

91

Index

92

Index

93

Index

94

Index

95

Index

96

Index

97

Index

98

Index

99

Index

100

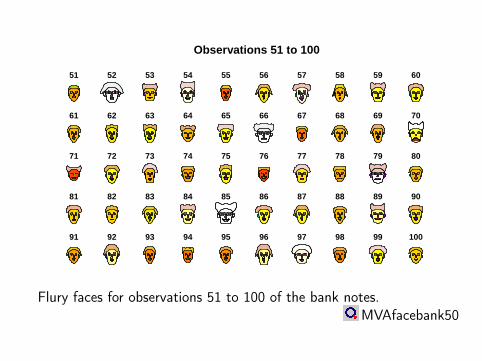

Observations 51 to 100

Flury faces for observations 51 to 100 of the bank notes.MVAfacebank50

Index

101

Index

102

Index

103

Index

104

Index

105

Index

106

Index

107

Index

108

Index

109

Index

110

Index

111

Index

112

Index

113

Index

114

Index

115

Index

116

Index

117

Index

118

Index

119

Index

120

Index

121

Index

122

Index

123

Index

124

Index

125

Index

126

Index

127

Index

128

Index

129

Index

130

Index

131

Index

132

Index

133

Index

134

Index

135

Index

136

Index

137

Index

138

Index

139

Index

140

Index

141

Index

142

Index

143

Index

144

Index

145

Index

146

Index

147

Index

148

Index

149

Index

150

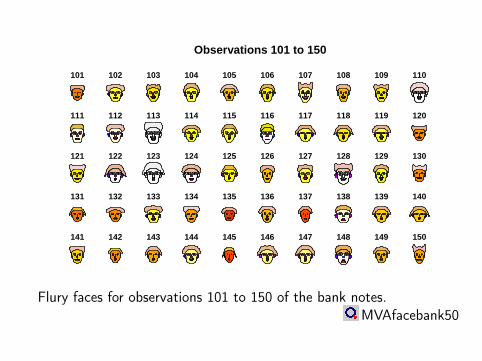

Observations 101 to 150

Flury faces for observations 101 to 150 of the bank notes.MVAfacebank50

Index

151

Index

152

Index

153

Index

154

Index

155

Index

156

Index

157

Index

158

Index

159

Index

160

Index

161

Index

162

Index

163

Index

164

Index

165

Index

166

Index

167

Index

168

Index

169

Index

170

Index

171

Index

172

Index

173

Index

174

Index

175

Index

176

Index

177

Index

178

Index

179

Index

180

Index

181

Index

182

Index

183

Index

184

Index

185

Index

186

Index

187

Index

188

Index

189

Index

190

Index

191

Index

192

Index

193

Index

194

Index

195

Index

196

Index

197

Index

198

Index

199

Index

200

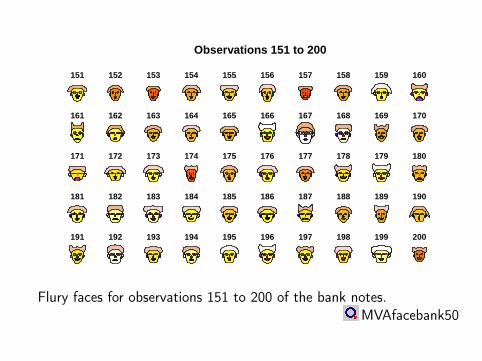

Observations 151 to 200

Flury faces for observations 151 to 200 of the bank notes.MVAfacebank50

Angewandte Multivariate Statistik Comparison of Batches Chernoff-Flury faces

Summary: Faces

Faces can be used to detect subgroups in multivariate data. Subgroups are characterized by similar looking faces. Outliers are identified by extreme faces (e.g. dark hair, smile or

happy face). If one element of X is unusual, the corresponding face element

changes significantly in shape.

Ostap Okhrin 42 of 461

Angewandte Multivariate Statistik Comparison of Batches Andrews’ Curves

Andrews’ Curves

Each multivariate observation Xi = (Xi ,1, ..,Xi ,p) ∈ Rp is transformedinto a curve as follows

p odd

fi (t) =Xi,1√

2+Xi,2 sin(t)+Xi,3 cos(t)+. . .+Xi,p−1 sin

(p − 1

2t

)+Xi,p cos

(p − 1

2t

)

p even

fi (t) =Xi,1√

2+ Xi,2 sin(t) + Xi,3 cos(t) + . . .+ Xi,p sin

(p2t)

such that the observation represents the coefficients of a so-calledFourier series, t ∈ [−π, π].

Ostap Okhrin 43 of 461

Angewandte Multivariate Statistik Comparison of Batches Andrews’ Curves

Andrews’ Curves

Subgroups are characterized by similar curves. Outliers are characterized by single curves. Order plays an important role in the interpretation.

Ostap Okhrin 44 of 461

Angewandte Multivariate Statistik Comparison of Batches Andrews’ Curves

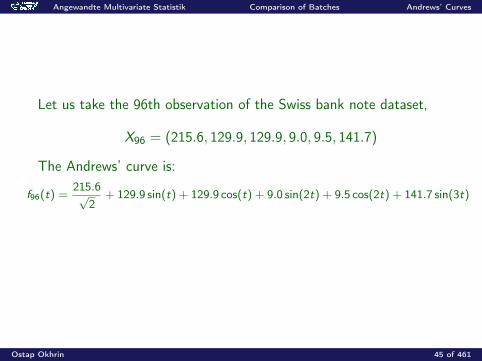

Let us take the 96th observation of the Swiss bank note dataset,

X96 = (215.6, 129.9, 129.9, 9.0, 9.5, 141.7)

The Andrews’ curve is:

f96(t) =215.6√

2+ 129.9 sin(t) + 129.9 cos(t) + 9.0 sin(2t) + 9.5 cos(2t) + 141.7 sin(3t)

Ostap Okhrin 45 of 461

Andrews curves (Bank data)

−0.

250

0.25

0.5

0 1 2 3 4 5 6

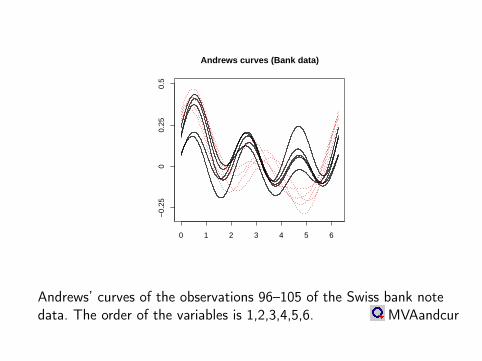

Andrews’ curves of the observations 96–105 of the Swiss bank notedata. The order of the variables is 1,2,3,4,5,6. MVAandcur

Angewandte Multivariate Statistik Comparison of Batches Andrews’ Curves

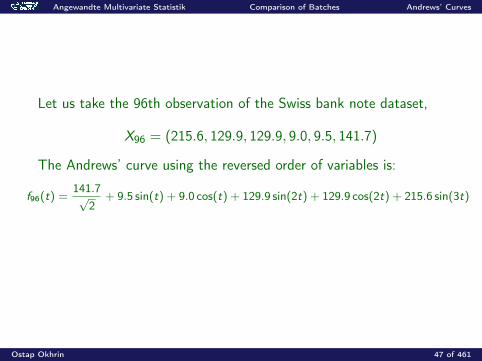

Let us take the 96th observation of the Swiss bank note dataset,

X96 = (215.6, 129.9, 129.9, 9.0, 9.5, 141.7)

The Andrews’ curve using the reversed order of variables is:

f96(t) =141.7√

2+ 9.5 sin(t) + 9.0 cos(t) + 129.9 sin(2t) + 129.9 cos(2t) + 215.6 sin(3t)

Ostap Okhrin 47 of 461

Andrews curves (Bank data)

−0.

250

0.25

0.5

0 1 2 3 4 5 6

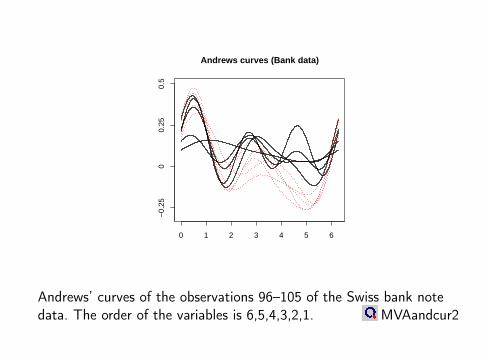

Andrews’ curves of the observations 96–105 of the Swiss bank notedata. The order of the variables is 6,5,4,3,2,1. MVAandcur2

Angewandte Multivariate Statistik Comparison of Batches Andrews’ Curves

Summary: Andrews’ Curves

Outliers appear as single Andrew’s curves, which looks differentfrom the rest.

A subgroup is characterized by a set of similar curves. The order of the variables plays an important role for

interpretation. The order of variables may be optimized by Principal Component

Analysis. For more than 20 observations we obtain a bad ”signal-to-ink-

ratio”, which means we cannot see the structure of so manycurves obtained.

Ostap Okhrin 49 of 461

Angewandte Multivariate Statistik Comparison of Batches Parallel coordinate plots

Parallel Coordinate Plots

Parallel Coordinate Plots Are not based on an orthogonal coordinate system Allow to see more than four dimensions

IdeaInstead of plotting observations in an orthogonal coordinate systemone draws their coordinates in a system of parallel axes. This way ofrepresentation is however sensitive to the order of the variables.

Ostap Okhrin 50 of 461

Parallel coordinates plot (Bank data)

V1 V2 V3 V4 V5 V6

00.

20.

40.

60.

81

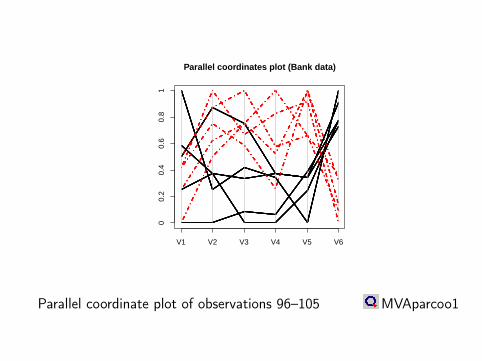

Parallel coordinate plot of observations 96–105 MVAparcoo1

Parallel coordinates plot (Bank data)

V1 V2 V3 V4 V5 V6

00.

20.

40.

60.

81

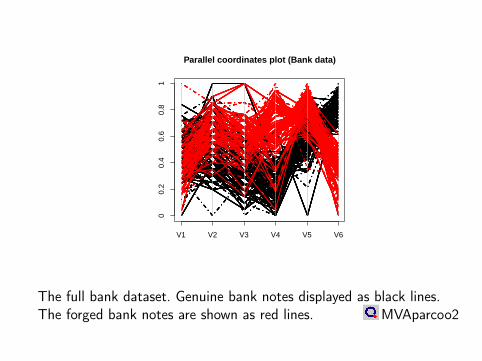

The full bank dataset. Genuine bank notes displayed as black lines.The forged bank notes are shown as red lines. MVAparcoo2

Angewandte Multivariate Statistik Comparison of Batches Parallel coordinate plots

Summary: Parallel coordinate plots

Parallel coordinate plots overcome the visualisation problem ofthe Cartesian coordinate system for dimensions greater than 4.

Outliers are seen as outlying polygon curves. The order of variables is still important for detection of subgroups. Subgroups may be screened by selective coloring in an interactive

manner.

Ostap Okhrin 53 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

A Short Excursion into Matrix Algebra

A(n×p) =

a11 · · · a1p...

. . ....

an1 · · · anp

Ostap Okhrin 54 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

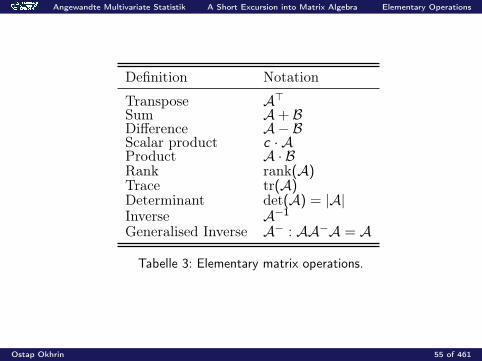

Definition Notation

Transpose A>Sum A+ BDifference A− BScalar product c · AProduct A · BRank rank(A)Trace tr(A)Determinant det(A) = |A|Inverse A−1

Generalised Inverse A− : AA−A = A

Tabelle 3: Elementary matrix operations.

Ostap Okhrin 55 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

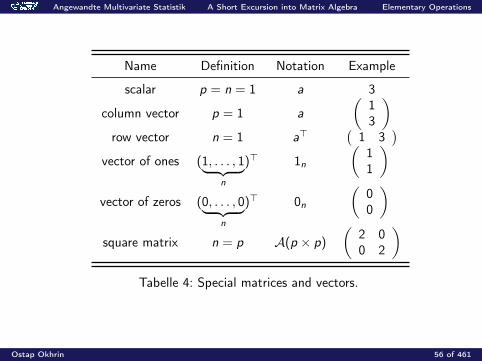

Name Definition Notation Example

scalar p = n = 1 a 3

column vector p = 1 a

(13

)row vector n = 1 a>

(1 3

)vector of ones (1, . . . , 1︸ ︷︷ ︸

n

)> 1n

(11

)vector of zeros (0, . . . , 0︸ ︷︷ ︸

n

)> 0n

(00

)square matrix n = p A(p × p)

(2 00 2

)Tabelle 4: Special matrices and vectors.

Ostap Okhrin 56 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

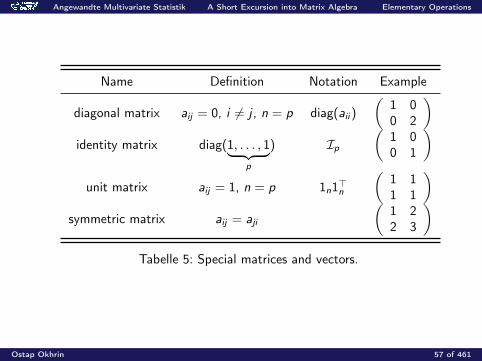

Name Definition Notation Example

diagonal matrix aij = 0, i 6= j , n = p diag(aii )

(1 00 2

)identity matrix diag(1, . . . , 1︸ ︷︷ ︸

p

) Ip(

1 00 1

)unit matrix aij = 1, n = p 1n1>n

(1 11 1

)symmetric matrix aij = aji

(1 22 3

)Tabelle 5: Special matrices and vectors.

Ostap Okhrin 57 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

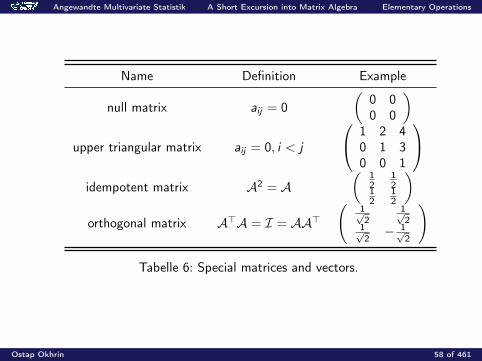

Name Definition Example

null matrix aij = 0(

0 00 0

)upper triangular matrix aij = 0, i < j

1 2 40 1 30 0 1

idempotent matrix A2 = A

( 12

12

12

12

)orthogonal matrix A>A = I = AA>

(1√2

1√2

1√2− 1√

2

)

Tabelle 6: Special matrices and vectors.

Ostap Okhrin 58 of 461

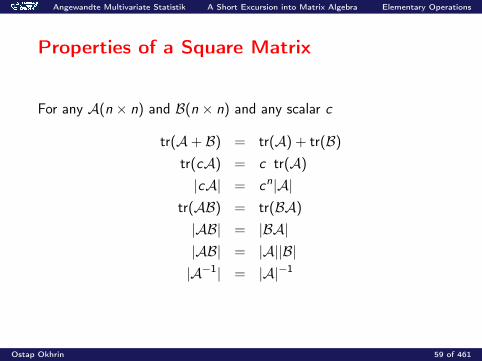

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

Properties of a Square Matrix

For any A(n × n) and B(n × n) and any scalar c

tr(A+ B) = tr(A) + tr(B)

tr(cA) = c tr(A)

|cA| = cn|A|tr(AB) = tr(BA)

|AB| = |BA||AB| = |A||B||A−1| = |A|−1

Ostap Okhrin 59 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

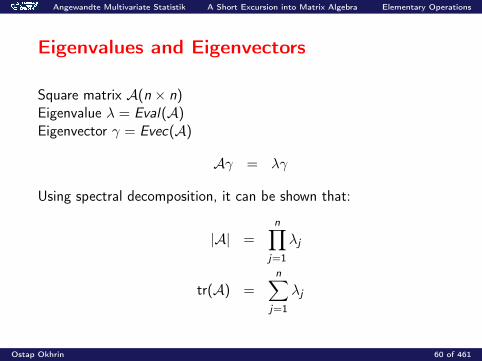

Eigenvalues and Eigenvectors

Square matrix A(n × n)Eigenvalue λ = Eval(A)Eigenvector γ = Evec(A)

Aγ = λγ

Using spectral decomposition, it can be shown that:

|A| =n∏

j=1

λj

tr(A) =n∑

j=1

λj

Ostap Okhrin 60 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Elementary Operations

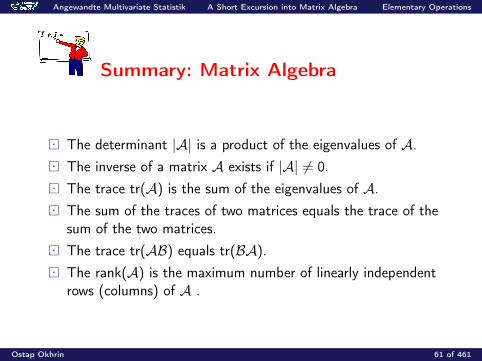

Summary: Matrix Algebra

The determinant |A| is a product of the eigenvalues of A. The inverse of a matrix A exists if |A| 6= 0. The trace tr(A) is the sum of the eigenvalues of A. The sum of the traces of two matrices equals the trace of the

sum of the two matrices. The trace tr(AB) equals tr(BA). The rank(A) is the maximum number of linearly independent

rows (columns) of A .

Ostap Okhrin 61 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

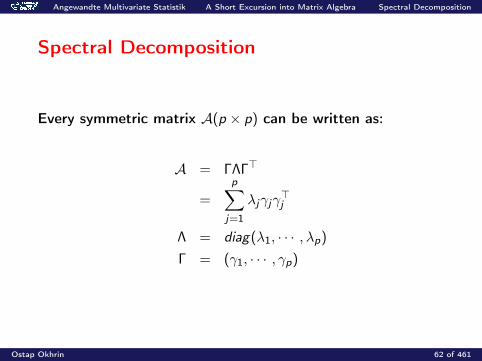

Spectral Decomposition

Every symmetric matrix A(p × p) can be written as:

A = ΓΛΓ>

=

p∑j=1

λjγjγ>j

Λ = diag(λ1, · · · , λp)

Γ = (γ1, · · · , γp)

Ostap Okhrin 62 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

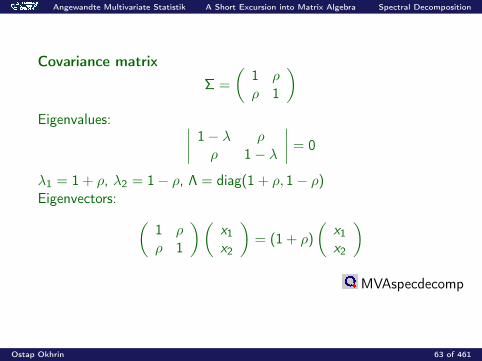

Covariance matrix

Σ =

(1 ρρ 1

)Eigenvalues: ∣∣∣∣ 1− λ ρ

ρ 1− λ

∣∣∣∣ = 0

λ1 = 1 + ρ, λ2 = 1− ρ, Λ = diag(1 + ρ, 1− ρ)Eigenvectors: (

1 ρρ 1

)(x1x2

)= (1 + ρ)

(x1x2

)MVAspecdecomp

Ostap Okhrin 63 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

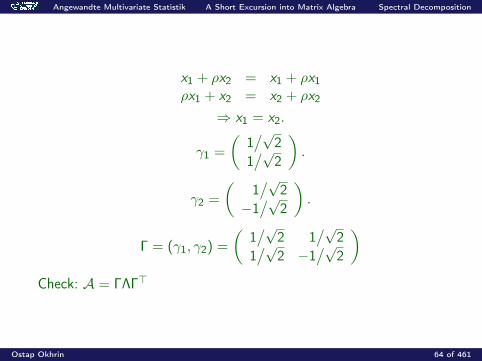

x1 + ρx2 = x1 + ρx1ρx1 + x2 = x2 + ρx2

⇒ x1 = x2.

γ1 =

(1/√

21/√

2

).

γ2 =

(1/√

2−1/√

2

).

Γ = (γ1, γ2) =

(1/√

2 1/√

21/√

2 −1/√

2

)Check: A = ΓΛΓ>

Ostap Okhrin 64 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

Eigenvectors

The direction of the first eigenvector is the main direction of the pointcloud. The second eigenvector is orthogonal to the first one.

This eigenvector direction is in general different from the LSregression shape line.

Ostap Okhrin 65 of 461

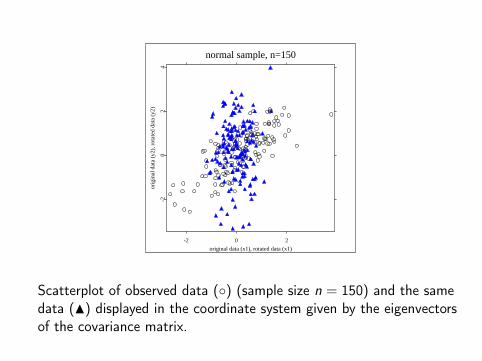

normal sample, n=150

-2 0 2

original data (x1), rotated data (x1)

-20

24

orig

inal

dat

a (y

2), r

otat

ed d

ata

(y2)

Scatterplot of observed data () (sample size n = 150) and the samedata (N) displayed in the coordinate system given by the eigenvectorsof the covariance matrix.

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

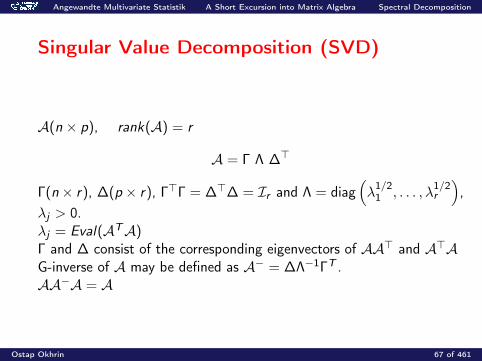

Singular Value Decomposition (SVD)

A(n × p), rank(A) = r

A = Γ Λ ∆>

Γ(n× r), ∆(p × r), Γ>Γ = ∆>∆ = Ir and Λ = diag(λ

1/21 , . . . , λ

1/2r

),

λj > 0.λj = Eval(ATA)Γ and ∆ consist of the corresponding eigenvectors of AA> and A>AG-inverse of A may be defined as A− = ∆Λ−1ΓT .AA−A = A

Ostap Okhrin 67 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

Summary: Spectral Decomposition

The spectral (Jordan) decomposition gives a representation of asymmetric matrix in terms of eigenvalues and eigenvectors.

The eigenvectors belonging to the largest eigenvalues point intothe "main directionöf the data.

The Jordan decomposition allows to easily compute the power ofa matrix A: Aα = ΓΛαΓ>.

A−1 = ΓΛ−1Γ>, A1/2 = ΓΛ1/2Γ>.

Ostap Okhrin 68 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Spectral Decomposition

Summary: Spectral Decomposition

The singular value decomposition (SVD) is a generalization of theJordan decomposition to non-quadratic matrices.

The direction of the first eigenvector of the covariance matrix of atwo-dimensional point cloud is different from the least squaresregression line.

Ostap Okhrin 69 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Quadratic Forms

Quadratic Forms

A(p × p) symmetric matrix can be written as

Q(x) = x>Ax =

p∑i=1

p∑j=1

aijxixj

Definiteness

Q(x) > 0 for all x 6= 0 positive definite (pd),Q(x) ≥ 0 for all x 6= 0 positive semidefinite (psd).

A is pd (psd) iff Q(x) = x>Ax is pd (psd).

Ostap Okhrin 70 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Quadratic Forms

Example:Q(x) = x>Ax = x2

1 + x22 , A =

(10

01

)Eigenvalues: λ1 = λ2 = 1 positive definiteQ(x) = (x1 − x2)2, A =

(1−1−1

1

)Eigenvalues λ1 = 2, λ2 = 0 positive semidefiniteQ(x) = x2

1 − x22

Eigenvalues λ1 = 1, λ2 = −1 indefinite.

Ostap Okhrin 71 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Quadratic Forms

TheoremIf A is symmetric and Q(x) = x>Ax is the corresponding quadraticform, then there exists a transformation x 7→ Γ>x = y such that

x> A x =

p∑i=1

λiy2i ,

where λi are the eigenvalues of A.Lemma

A > 0 ⇔ λi > 0,A ≥ 0 ⇔ λi ≥ 0, i = 1, . . . , p.

Ostap Okhrin 72 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Quadratic Forms

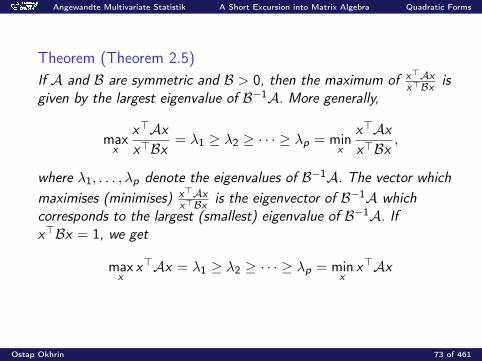

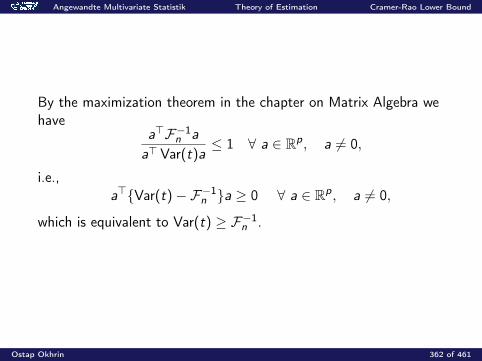

Theorem (Theorem 2.5)If A and B are symmetric and B > 0, then the maximum of x>Ax

x>Bx isgiven by the largest eigenvalue of B−1A. More generally,

maxx

x>Axx>Bx

= λ1 ≥ λ2 ≥ · · · ≥ λp = minx

x>Axx>Bx

,

where λ1, . . . , λp denote the eigenvalues of B−1A. The vector whichmaximises (minimises) x>Ax

x>Bx is the eigenvector of B−1A whichcorresponds to the largest (smallest) eigenvalue of B−1A. Ifx>Bx = 1, we get

maxx

x>Ax = λ1 ≥ λ2 ≥ · · · ≥ λp = minx

x>Ax

Ostap Okhrin 73 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Quadratic Forms

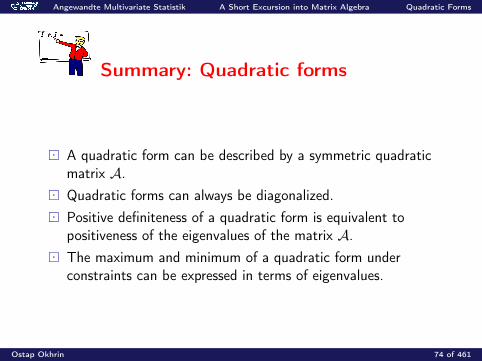

Summary: Quadratic forms

A quadratic form can be described by a symmetric quadraticmatrix A.

Quadratic forms can always be diagonalized. Positive definiteness of a quadratic form is equivalent to

positiveness of the eigenvalues of the matrix A. The maximum and minimum of a quadratic form under

constraints can be expressed in terms of eigenvalues.

Ostap Okhrin 74 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Derivatives

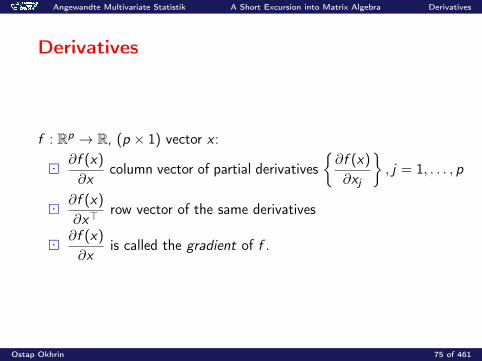

Derivatives

f : Rp → R, (p × 1) vector x :

∂f (x)

∂xcolumn vector of partial derivatives

∂f (x)

∂xj

, j = 1, . . . , p

∂f (x)

∂x>row vector of the same derivatives

∂f (x)

∂xis called the gradient of f .

Ostap Okhrin 75 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Derivatives

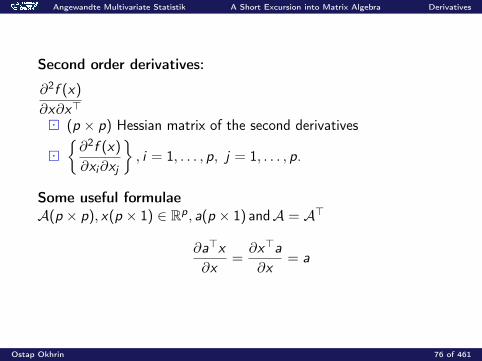

Second order derivatives:

∂2f (x)

∂x∂x>

(p × p) Hessian matrix of the second derivatives

∂2f (x)

∂xi∂xj

, i = 1, . . . , p, j = 1, . . . , p.

Some useful formulaeA(p × p), x(p × 1) ∈ Rp, a(p × 1) andA = A>

∂a>x

∂x=∂x>a

∂x= a

Ostap Okhrin 76 of 461

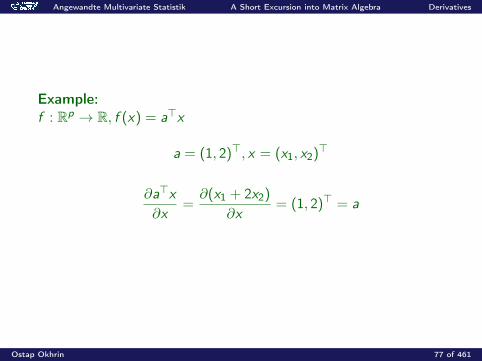

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Derivatives

Example:f : Rp → R, f (x) = a>x

a = (1, 2)>, x = (x1, x2)>

∂a>x

∂x=∂(x1 + 2x2)

∂x= (1, 2)> = a

Ostap Okhrin 77 of 461

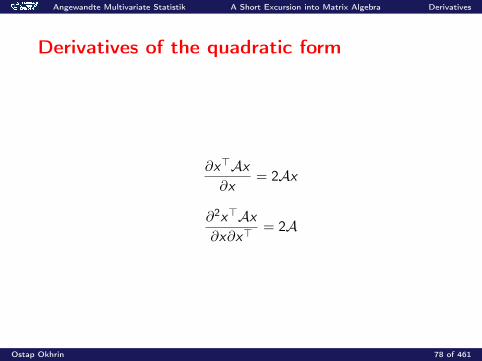

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Derivatives

Derivatives of the quadratic form

∂x>Ax∂x

= 2Ax

∂2x>Ax∂x∂x>

= 2A

Ostap Okhrin 78 of 461

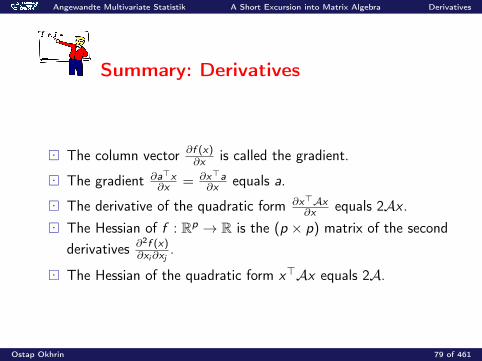

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Derivatives

Summary: Derivatives

The column vector ∂f (x)∂x is called the gradient.

The gradient ∂a>x∂x = ∂x>a

∂x equals a.

The derivative of the quadratic form ∂x>Ax∂x equals 2Ax .

The Hessian of f : Rp → R is the (p × p) matrix of the secondderivatives ∂2f (x)

∂xi∂xj.

The Hessian of the quadratic form x>Ax equals 2A.

Ostap Okhrin 79 of 461

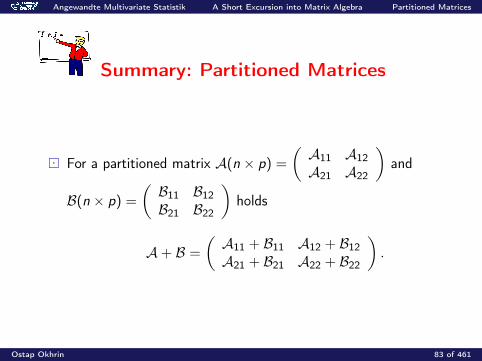

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

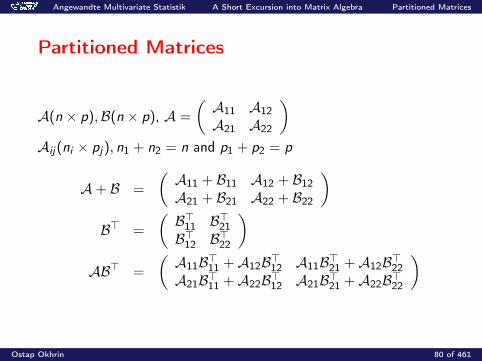

Partitioned Matrices

A(n × p),B(n × p), A =

(A11 A12A21 A22

)Aij(ni × pj), n1 + n2 = n and p1 + p2 = p

A+ B =

(A11 + B11 A12 + B12A21 + B21 A22 + B22

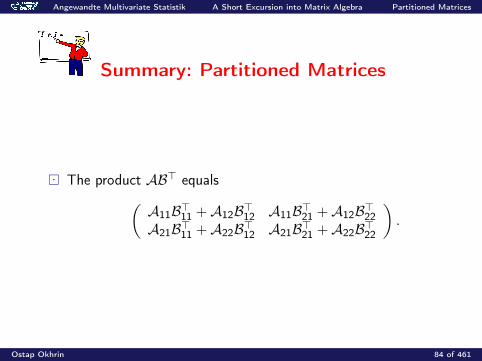

)B> =

(B>11 B>21B>12 B>22

)AB> =

(A11B>11 +A12B>12 A11B>21 +A12B>22A21B>11 +A22B>12 A21B>21 +A22B>22

)

Ostap Okhrin 80 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

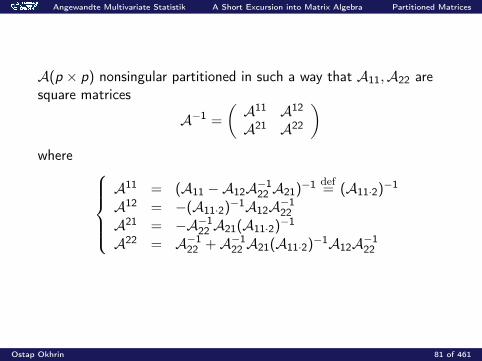

A(p × p) nonsingular partitioned in such a way that A11,A22 aresquare matrices

A−1 =

(A11 A12

A21 A22

)where

A11 = (A11 −A12A−122 A21)−1 def

= (A11·2)−1

A12 = −(A11·2)−1A12A−122

A21 = −A−122 A21(A11·2)−1

A22 = A−122 +A−1

22 A21(A11·2)−1A12A−122

Ostap Okhrin 81 of 461

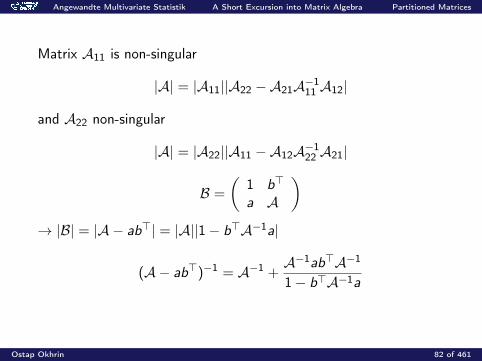

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

Matrix A11 is non-singular

|A| = |A11||A22 −A21A−111 A12|

and A22 non-singular

|A| = |A22||A11 −A12A−122 A21|

B =

(1 b>

a A

)→ |B| = |A − ab>| = |A||1− b>A−1a|

(A− ab>)−1 = A−1 +A−1ab>A−1

1− b>A−1a

Ostap Okhrin 82 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

Summary: Partitioned Matrices

For a partitioned matrix A(n × p) =

(A11 A12A21 A22

)and

B(n × p) =

(B11 B12B21 B22

)holds

A+ B =

(A11 + B11 A12 + B12A21 + B21 A22 + B22

).

Ostap Okhrin 83 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

Summary: Partitioned Matrices

The product AB> equals(A11B>11 +A12B>12 A11B>21 +A12B>22A21B>11 +A22B>12 A21B>21 +A22B>22

).

Ostap Okhrin 84 of 461

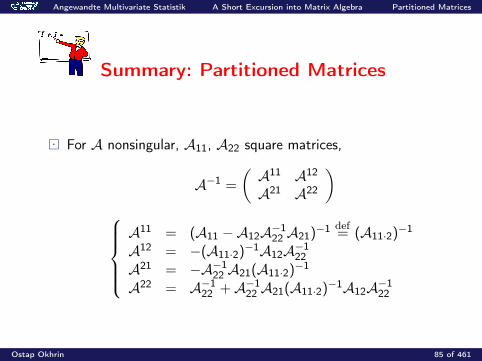

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

Summary: Partitioned Matrices

For A nonsingular, A11, A22 square matrices,

A−1 =

(A11 A12

A21 A22

)A11 = (A11 −A12A−1

22 A21)−1 def= (A11·2)−1

A12 = −(A11·2)−1A12A−122

A21 = −A−122 A21(A11·2)−1

A22 = A−122 +A−1

22 A21(A11·2)−1A12A−122

Ostap Okhrin 85 of 461

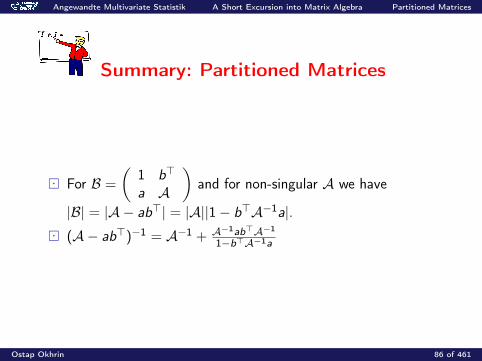

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Partitioned Matrices

Summary: Partitioned Matrices

For B =

(1 b>

a A

)and for non-singular A we have

|B| = |A − ab>| = |A||1− b>A−1a|. (A− ab>)−1 = A−1 + A−1ab>A−1

1−b>A−1a

Ostap Okhrin 86 of 461

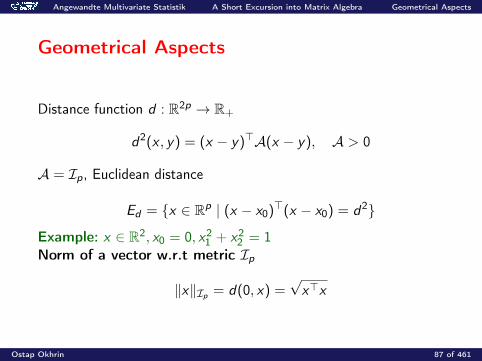

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

Geometrical Aspects

Distance function d : R2p → R+

d2(x , y) = (x − y)>A(x − y), A > 0

A = Ip, Euclidean distance

Ed = x ∈ Rp | (x − x0)>(x − x0) = d2

Example: x ∈ R2, x0 = 0, x21 + x2

2 = 1Norm of a vector w.r.t metric Ip

‖x‖Ip = d(0, x) =√x>x

Ostap Okhrin 87 of 461

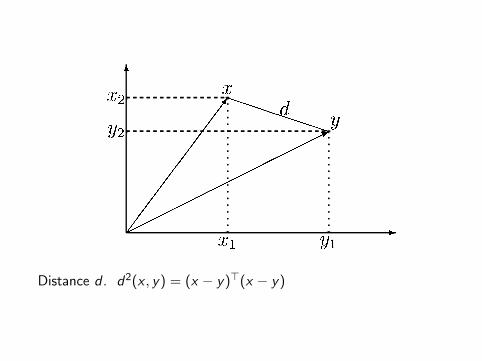

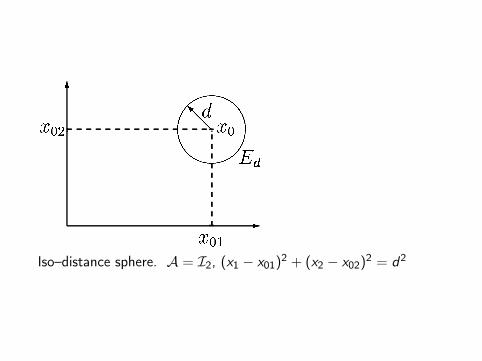

Distance d . d2(x , y) = (x − y)>(x − y)

Iso–distance sphere. A = I2, (x1 − x01)2 + (x2 − x02)2 = d2

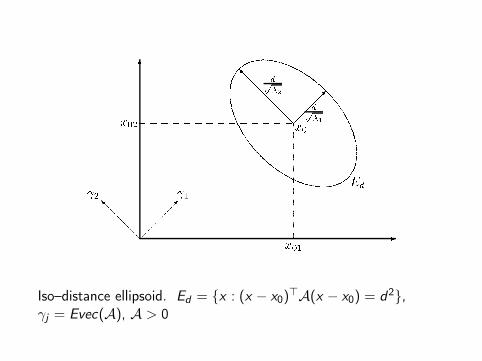

Iso–distance ellipsoid. Ed = x : (x − x0)>A(x − x0) = d2,γj = Evec(A), A > 0

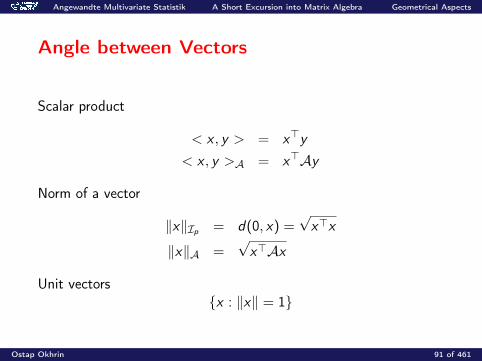

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

Angle between Vectors

Scalar product

< x , y > = x>y

< x , y >A = x>Ay

Norm of a vector

‖x‖Ip = d(0, x) =√x>x

‖x‖A =√x>Ax

Unit vectorsx : ‖x‖ = 1

Ostap Okhrin 91 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

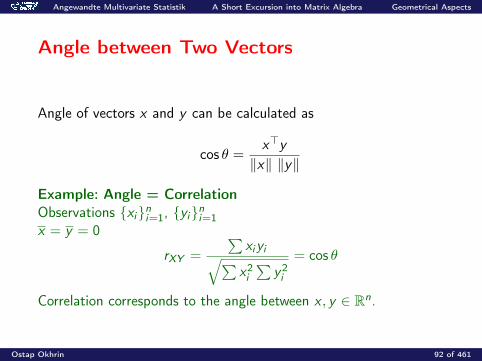

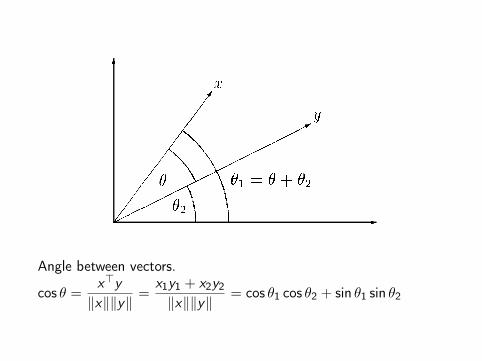

Angle between Two Vectors

Angle of vectors x and y can be calculated as

cos θ =x>y

‖x‖ ‖y‖

Example: Angle = CorrelationObservations xini=1, yini=1x = y = 0

rXY =

∑xiyi√∑x2i

∑y2i

= cos θ

Correlation corresponds to the angle between x , y ∈ Rn.

Ostap Okhrin 92 of 461

Angle between vectors.

cos θ =x>y

‖x‖‖y‖=

x1y1 + x2y2

‖x‖‖y‖= cos θ1 cos θ2 + sin θ1 sin θ2

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

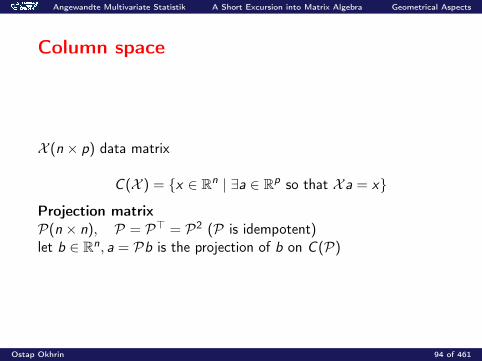

Column space

X (n × p) data matrix

C (X ) = x ∈ Rn | ∃a ∈ Rp so that X a = x

Projection matrixP(n × n), P = P> = P2 (P is idempotent)let b ∈ Rn, a = Pb is the projection of b on C (P)

Ostap Okhrin 94 of 461

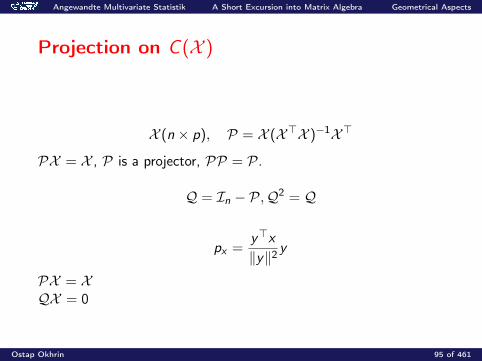

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

Projection on C (X )

X (n × p), P = X (X>X )−1X>

PX = X , P is a projector, PP = P.

Q = In − P,Q2 = Q

px =y>x

‖y‖2y

PX = XQX = 0

Ostap Okhrin 95 of 461

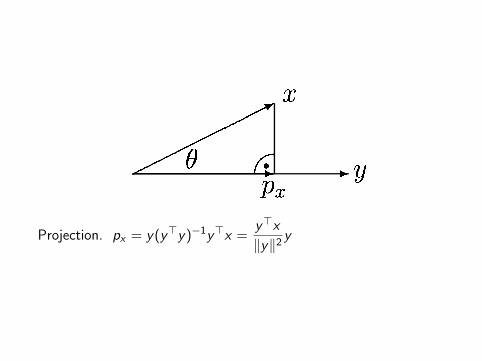

Projection. px = y(y>y)−1y>x =y>x

‖y‖2y

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

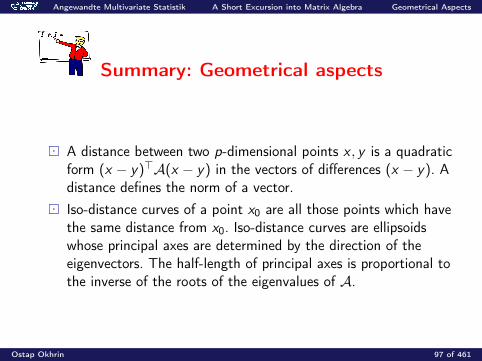

Summary: Geometrical aspects

A distance between two p-dimensional points x , y is a quadraticform (x − y)>A(x − y) in the vectors of differences (x − y). Adistance defines the norm of a vector.

Iso-distance curves of a point x0 are all those points which havethe same distance from x0. Iso-distance curves are ellipsoidswhose principal axes are determined by the direction of theeigenvectors. The half-length of principal axes is proportional tothe inverse of the roots of the eigenvalues of A.

Ostap Okhrin 97 of 461

Angewandte Multivariate Statistik A Short Excursion into Matrix Algebra Geometrical Aspects

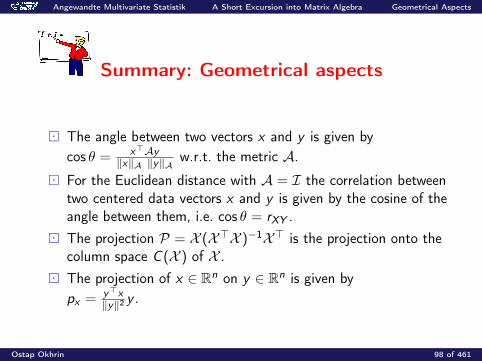

Summary: Geometrical aspects

The angle between two vectors x and y is given bycos θ = x>Ay

‖x‖A ‖y‖A w.r.t. the metric A. For the Euclidean distance with A = I the correlation between

two centered data vectors x and y is given by the cosine of theangle between them, i.e. cos θ = rXY .

The projection P = X (X>X )−1X> is the projection onto thecolumn space C (X ) of X .

The projection of x ∈ Rn on y ∈ Rn is given bypx = y>x

‖y‖2 y .

Ostap Okhrin 98 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

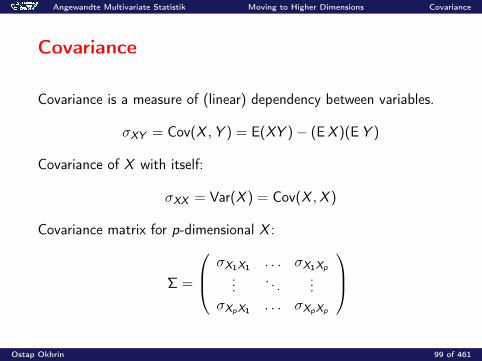

Covariance

Covariance is a measure of (linear) dependency between variables.

σXY = Cov(X ,Y ) = E(XY )− (EX )(EY )

Covariance of X with itself:

σXX = Var(X ) = Cov(X ,X )

Covariance matrix for p-dimensional X :

Σ =

σX1X1 . . . σX1Xp

.... . .

...σXpX1 . . . σXpXp

Ostap Okhrin 99 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

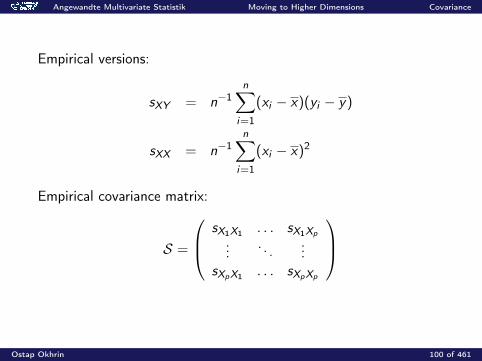

Empirical versions:

sXY = n−1n∑

i=1

(xi − x)(yi − y)

sXX = n−1n∑

i=1

(xi − x)2

Empirical covariance matrix:

S =

sX1X1 . . . sX1Xp

.... . .

...sXpX1 . . . sXpXp

Ostap Okhrin 100 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

Example: Swiss bank data

X1 = length of the billX2 = height of the bill (left)X3 = height of the bill (right)X4 = distance of the inner frame to the lower borderX5 = distance of the inner frame to the upper borderX6 = length of the diagonal of the central picture.

Ostap Okhrin 101 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

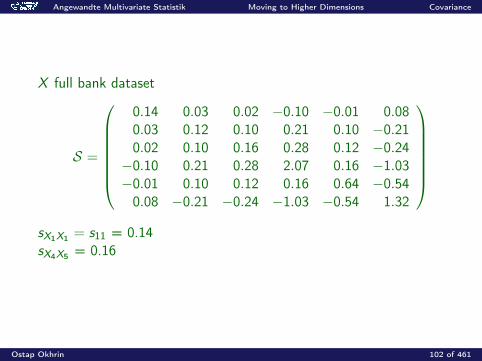

X full bank dataset

S =

0.14 0.03 0.02 −0.10 −0.01 0.080.03 0.12 0.10 0.21 0.10 −0.210.02 0.10 0.16 0.28 0.12 −0.24−0.10 0.21 0.28 2.07 0.16 −1.03−0.01 0.10 0.12 0.16 0.64 −0.540.08 −0.21 −0.24 −1.03 −0.54 1.32

sX1X1 = s11 = 0.14sX4X5 = 0.16

Ostap Okhrin 102 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

Scatterplots with point clouds that are ”upward-sloping” areshowing variables with positive covariance.

Scatterplots with ”downward-sloping” structure are showingnegative covariance.

Ostap Okhrin 103 of 461

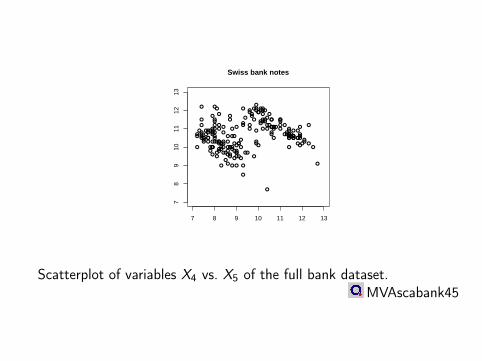

7 8 9 10 11 12 13

78

910

1112

13

Swiss bank notes

Scatterplot of variables X4 vs. X5 of the full bank dataset.MVAscabank45

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

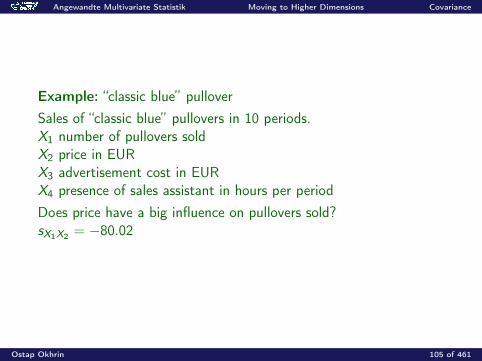

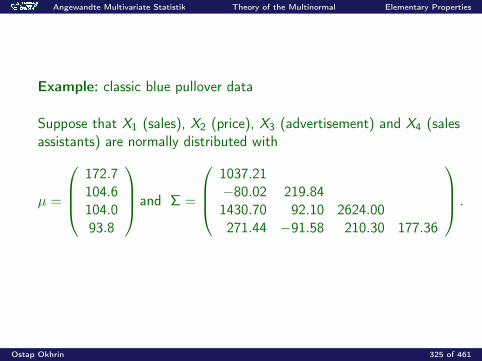

Example: “classic blue” pulloverSales of “classic blue” pullovers in 10 periods.X1 number of pullovers soldX2 price in EURX3 advertisement cost in EURX4 presence of sales assistant in hours per periodDoes price have a big influence on pullovers sold?sX1X2 = −80.02

Ostap Okhrin 105 of 461

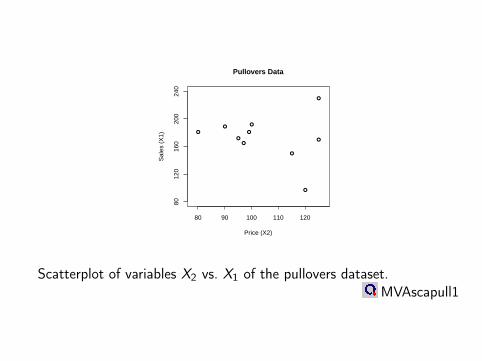

Pullovers Data

Price (X2)

Sal

es (

X1)

8012

016

020

024

0

80 90 100 110 120

Scatterplot of variables X2 vs. X1 of the pullovers dataset.MVAscapull1

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

Summary: Covariance

The covariance is a measure of dependence. Covariance measures only linear dependence. There are nonlinear dependencies that have zero covariance. Zero covariance does not imply independence. Independence implies zero covariance. Covariance is scale dependent.

Ostap Okhrin 107 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Covariance

Summary: Covariance

Negative covariance corresponds to downward-slopingscatterplots.

Positive covariance corresponds to upward-sloping scatterplots. The covariance of a variable with itself is its variance

Cov(X ,X ) = σXX . For small n we should replace the factor 1

n for the computation ofthe covariance by 1

n−1 .

Ostap Okhrin 108 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

Correlation

ρXY =Cov(X ,Y )√Var(X )Var(Y )

The empirical version of ρXY :

rXY =sXY√sXX sYY

Ostap Okhrin 109 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

Correlation matrix:

P =

ρX1X1 . . . ρX1Xp

.... . .

...ρXpX1 . . . ρXpXp

Empirical correlation matrix:

R =

rX1X1 . . . rX1Xp

.... . .

...rXpX1 . . . rXpXp

Ostap Okhrin 110 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

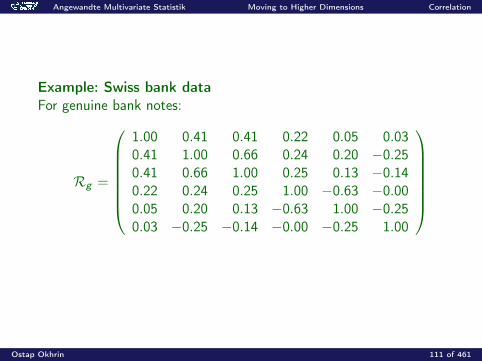

Example: Swiss bank dataFor genuine bank notes:

Rg =

1.00 0.41 0.41 0.22 0.05 0.030.41 1.00 0.66 0.24 0.20 −0.250.41 0.66 1.00 0.25 0.13 −0.140.22 0.24 0.25 1.00 −0.63 −0.000.05 0.20 0.13 −0.63 1.00 −0.250.03 −0.25 −0.14 −0.00 −0.25 1.00

Ostap Okhrin 111 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

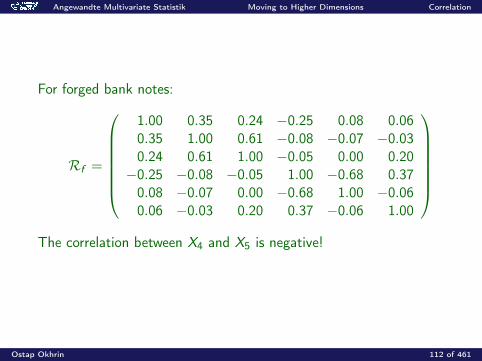

For forged bank notes:

Rf =

1.00 0.35 0.24 −0.25 0.08 0.060.35 1.00 0.61 −0.08 −0.07 −0.030.24 0.61 1.00 −0.05 0.00 0.20−0.25 −0.08 −0.05 1.00 −0.68 0.370.08 −0.07 0.00 −0.68 1.00 −0.060.06 −0.03 0.20 0.37 −0.06 1.00

The correlation between X4 and X5 is negative!

Ostap Okhrin 112 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

If X and Y are independent, then Cov(X ,Y ) = ρ(X ,Y ) = 0.

The converse is not true in generalExample:

standard normal distributed random variable X

random variable Y = X 2 which is surely not independent of X

Cov(X ,Y ) = E(XY )− E(X )E(Y ) = E(X 3) = 0

(because E(X ) = 0 and E(X 2) = 1) and therefore ρ(X ,Y ) = 0, too.

Ostap Okhrin 113 of 461

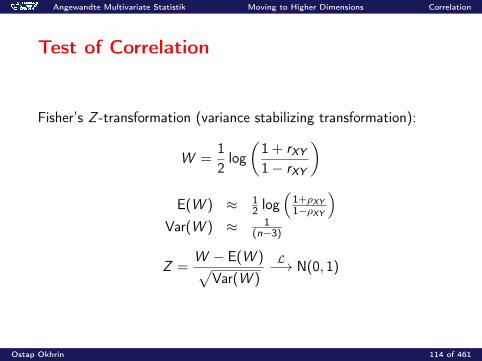

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

Test of Correlation

Fisher’s Z -transformation (variance stabilizing transformation):

W =12log(1 + rXY1− rXY

)E(W ) ≈ 1

2 log(

1+ρXY1−ρXY

)Var(W ) ≈ 1

(n−3)

Z =W − E(W )√

Var(W )

L−→ N(0, 1)

Ostap Okhrin 114 of 461

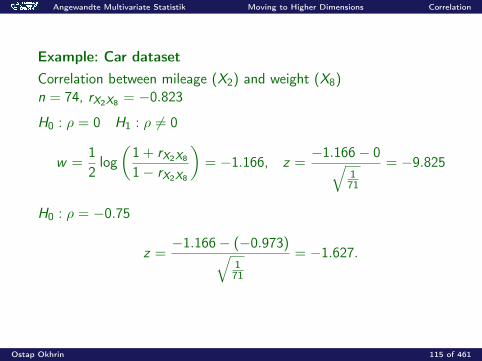

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

Example: Car datasetCorrelation between mileage (X2) and weight (X8)n = 74, rX2X8 = −0.823

H0 : ρ = 0 H1 : ρ 6= 0

w =12log(1 + rX2X8

1− rX2X8

)= −1.166, z =

−1.166− 0√171

= −9.825

H0 : ρ = −0.75

z =−1.166− (−0.973)√

171

= −1.627.

Ostap Okhrin 115 of 461

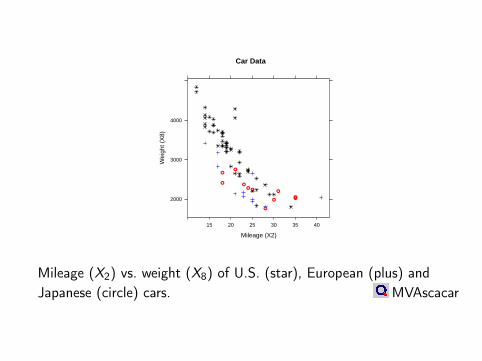

Car Data

Mileage (X2)

Wei

ght (

X8)

2000

3000

4000

15 20 25 30 35 40

Mileage (X2) vs. weight (X8) of U.S. (star), European (plus) andJapanese (circle) cars. MVAscacar

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

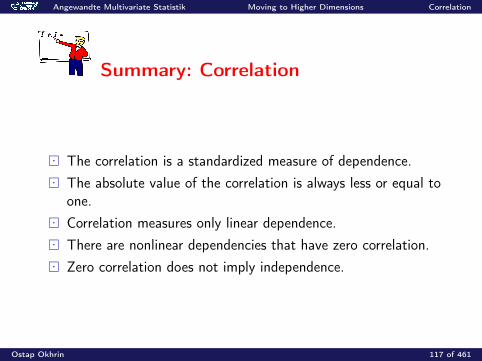

Summary: Correlation

The correlation is a standardized measure of dependence. The absolute value of the correlation is always less or equal to

one. Correlation measures only linear dependence. There are nonlinear dependencies that have zero correlation. Zero correlation does not imply independence.

Ostap Okhrin 117 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Correlation

Summary: Correlation

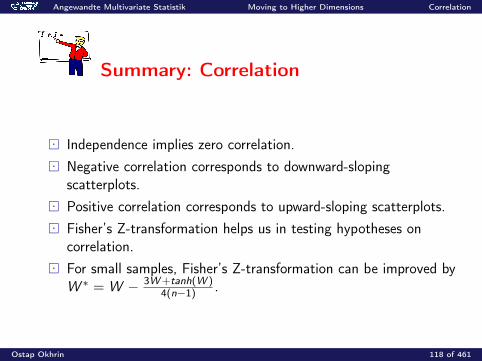

Independence implies zero correlation. Negative correlation corresponds to downward-sloping

scatterplots. Positive correlation corresponds to upward-sloping scatterplots. Fisher’s Z-transformation helps us in testing hypotheses on

correlation. For small samples, Fisher’s Z-transformation can be improved by

W ∗ = W − 3W+tanh(W )4(n−1) .

Ostap Okhrin 118 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

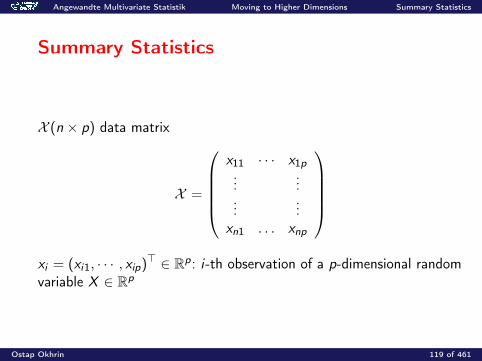

Summary Statistics

X (n × p) data matrix

X =

x11 · · · x1p...

......

...xn1 . . . xnp

xi = (xi1, · · · , xip)> ∈ Rp: i-th observation of a p-dimensional randomvariable X ∈ Rp

Ostap Okhrin 119 of 461

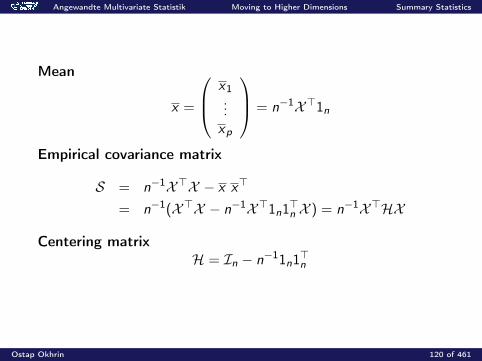

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

Mean

x =

x1...xp

= n−1X>1n

Empirical covariance matrix

S = n−1X>X − x x>

= n−1(X>X − n−1X>1n1>n X ) = n−1X>HX

Centering matrixH = In − n−11n1>n

Ostap Okhrin 120 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

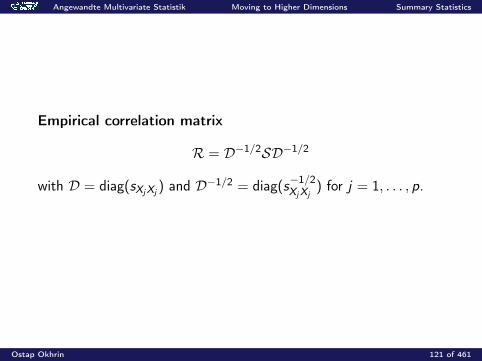

Empirical correlation matrix

R = D−1/2SD−1/2

with D = diag(sXjXj) and D−1/2 = diag(s

−1/2XjXj

) for j = 1, . . . , p.

Ostap Okhrin 121 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

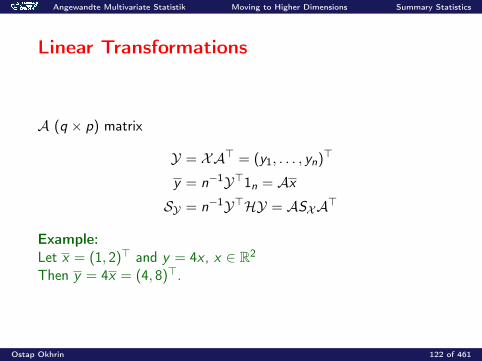

Linear Transformations

A (q × p) matrix

Y = XA> = (y1, . . . , yn)>

y = n−1Y>1n = AxSY = n−1Y>HY = ASXA>

Example:Let x = (1, 2)> and y = 4x , x ∈ R2

Then y = 4x = (4, 8)>.

Ostap Okhrin 122 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

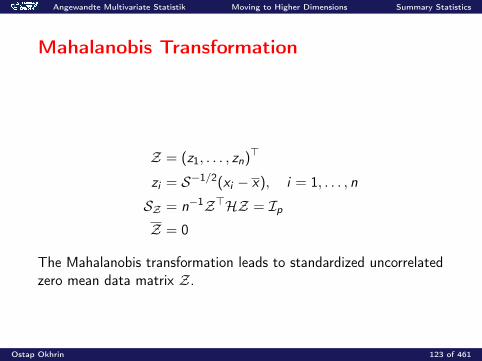

Mahalanobis Transformation

Z = (z1, . . . , zn)>

zi = S−1/2(xi − x), i = 1, . . . , n

SZ = n−1Z>HZ = IpZ = 0

The Mahalanobis transformation leads to standardized uncorrelatedzero mean data matrix Z.

Ostap Okhrin 123 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

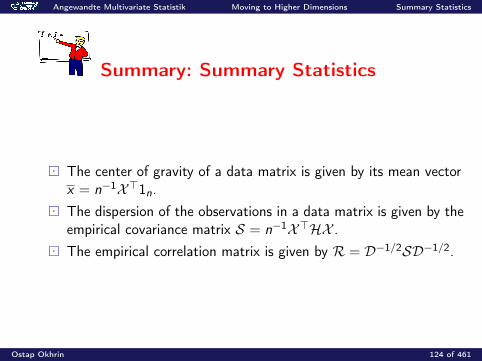

Summary: Summary Statistics

The center of gravity of a data matrix is given by its mean vectorx = n−1X>1n.

The dispersion of the observations in a data matrix is given by theempirical covariance matrix S = n−1X>HX .

The empirical correlation matrix is given by R = D−1/2SD−1/2.

Ostap Okhrin 124 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Summary Statistics

Summary: Summary Statistics

A linear transformation Y = XA> of a data matrix X has meanAx and empirical covariance ASXA>.

The Mahalanobis transformation is a linear transformationzi = S−1/2(xi − x) which gives a standardized, uncorrelated datamatrix Z.

Ostap Okhrin 125 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

One-sample t-test

We have iid observations x1, . . . , xn.Assume that the observations stem from N(µ, σ2).Then xn ∼ N(µ, σ2/n), i.e.

√n

(xn − µ)

σ∼ N(0, 1).

Ostap Okhrin 126 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

H0 : µ = µ0 H1 : µ 6= µ0Assume that σ2 is known:

√n|xn − µ0|

σ∼ N(0, 1)

Show that P(reject H0|H0 is true) = α.

Ostap Okhrin 127 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

Usually σ2 is not known and we have to estimate it:

σ2n =

1n − 1

n∑i=1

(xi − xn)2.

It can be shown that

√n

(xn − µ)

σn∼ tn−1.

Note: t-distribution tn approaches N(0, 1) as n→∞ (parameter n:degrees of freedom).

Ostap Okhrin 128 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

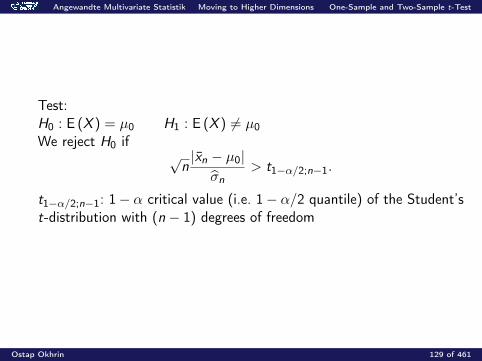

Test:H0 : E (X ) = µ0 H1 : E (X ) 6= µ0We reject H0 if

√n|xn − µ0|

σn> t1−α/2;n−1.

t1−α/2;n−1: 1− α critical value (i.e. 1− α/2 quantile) of the Student’st-distribution with (n − 1) degrees of freedom

Ostap Okhrin 129 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

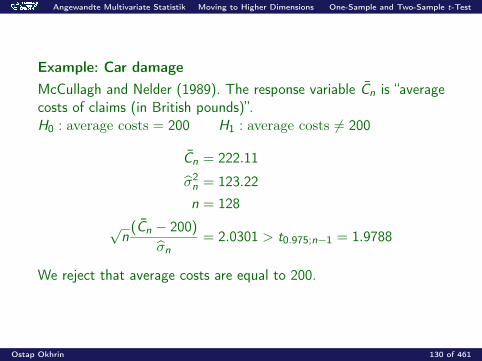

Example: Car damageMcCullagh and Nelder (1989). The response variable Cn is “averagecosts of claims (in British pounds)”.H0 : average costs = 200 H1 : average costs 6= 200

Cn = 222.11

σ2n = 123.22n = 128

√n

(Cn − 200)

σn= 2.0301 > t0.975;n−1 = 1.9788

We reject that average costs are equal to 200.

Ostap Okhrin 130 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

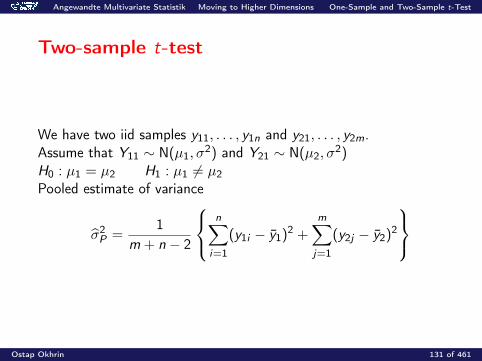

Two-sample t-test

We have two iid samples y11, . . . , y1n and y21, . . . , y2m.Assume that Y11 ∼ N(µ1, σ

2) and Y21 ∼ N(µ2, σ2)

H0 : µ1 = µ2 H1 : µ1 6= µ2Pooled estimate of variance

σ2P =

1m + n − 2

n∑

i=1

(y1i − y1)2 +m∑j=1

(y2j − y2)2

Ostap Okhrin 131 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions One-Sample and Two-Sample t-Test

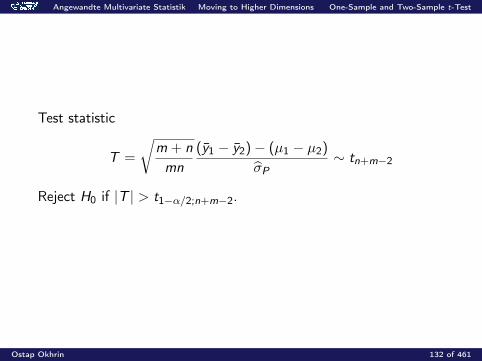

Test statistic

T =

√m + n

mn

(y1 − y2)− (µ1 − µ2)

σP∼ tn+m−2

Reject H0 if |T | > t1−α/2;n+m−2.

Ostap Okhrin 132 of 461

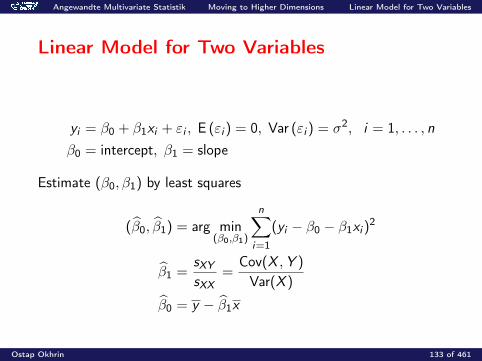

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

Linear Model for Two Variables

yi = β0 + β1xi + εi , E (εi ) = 0, Var (εi ) = σ2, i = 1, . . . , nβ0 = intercept, β1 = slope

Estimate (β0, β1) by least squares

(β0, β1) = arg min(β0,β1)

n∑i=1

(yi − β0 − β1xi )2

β1 =sXYsXX

=Cov(X ,Y )

Var(X )

β0 = y − β1x

Ostap Okhrin 133 of 461

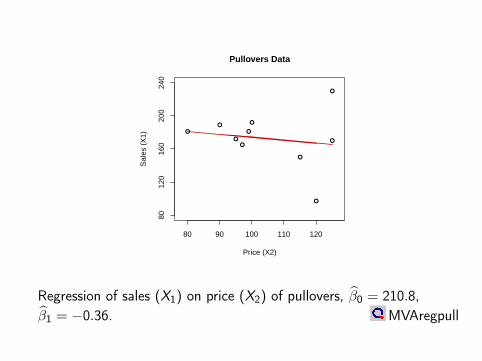

Price (X2)

Sal

es (

X1)

Pullovers Data

8012

016

020

024

0

80 90 100 110 120

Regression of sales (X1) on price (X2) of pullovers, β0 = 210.8,β1 = −0.36. MVAregpull

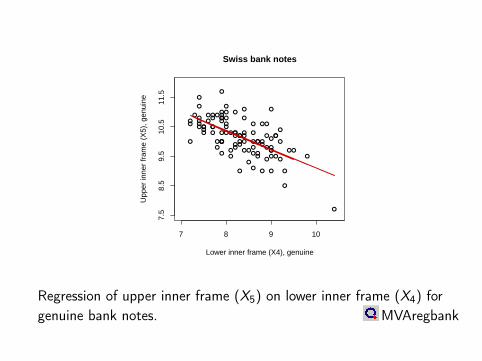

Lower inner frame (X4), genuine

Upp

er in

ner

fram

e (X

5), g

enui

ne

7.5

8.5

9.5

10.5

11.5

7 8 9 10

Swiss bank notes

Regression of upper inner frame (X5) on lower inner frame (X4) forgenuine bank notes. MVAregbank

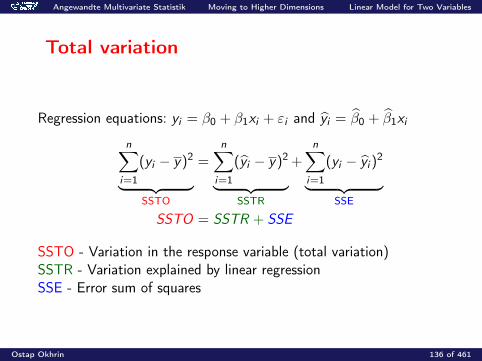

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

Total variation

Regression equations: yi = β0 + β1xi + εi and yi = β0 + β1xi

n∑i=1

(yi − y)2

︸ ︷︷ ︸SSTO

=n∑

i=1

(yi − y)2

︸ ︷︷ ︸SSTR

+n∑

i=1

(yi − yi )2

︸ ︷︷ ︸SSE

SSTO = SSTR + SSE

SSTO - Variation in the response variable (total variation)SSTR - Variation explained by linear regressionSSE - Error sum of squares

Ostap Okhrin 136 of 461

88 90 92 94 96 98 100 102

165

175

185

195

Price (X2)

Sal

es (

X1)

Pullover Data

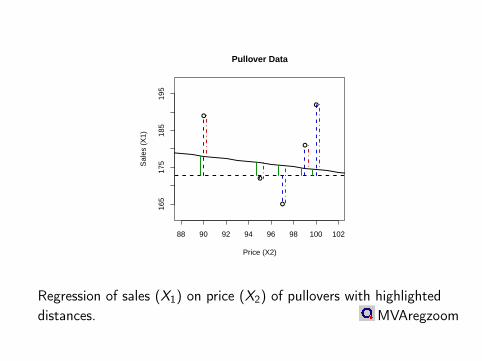

Regression of sales (X1) on price (X2) of pullovers with highlighteddistances. MVAregzoom

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

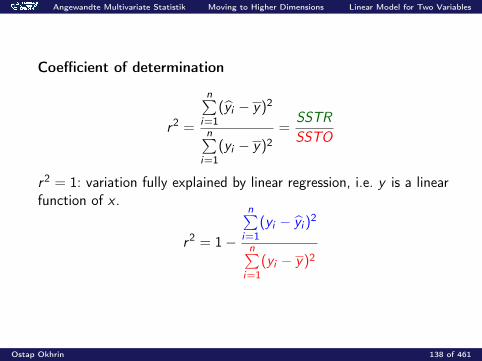

Coefficient of determination

r2 =

n∑i=1

(yi − y)2

n∑i=1

(yi − y)2=

SSTR

SSTO

r2 = 1: variation fully explained by linear regression, i.e. y is a linearfunction of x .

r2 = 1−

n∑i=1

(yi − yi )2

n∑i=1

(yi − y)2

Ostap Okhrin 138 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

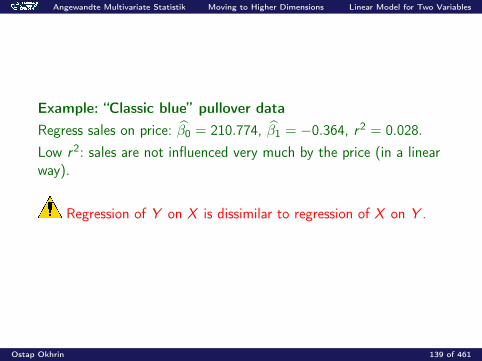

Example: “Classic blue” pullover dataRegress sales on price: β0 = 210.774, β1 = −0.364, r2 = 0.028.Low r2: sales are not influenced very much by the price (in a linearway).

Regression of Y on X is dissimilar to regression of X on Y .

Ostap Okhrin 139 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

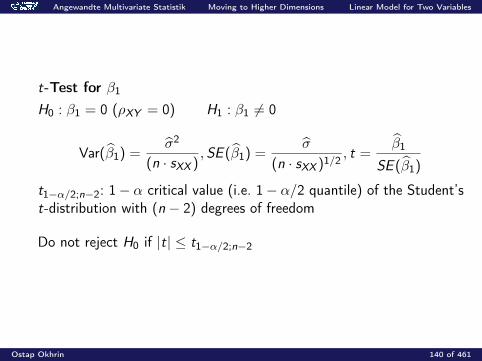

t-Test for β1

H0 : β1 = 0 (ρXY = 0) H1 : β1 6= 0

Var(β1) =σ2

(n · sXX ), SE (β1) =

σ

(n · sXX )1/2 , t =β1

SE (β1)

t1−α/2;n−2: 1− α critical value (i.e. 1− α/2 quantile) of the Student’st-distribution with (n − 2) degrees of freedom

Do not reject H0 if |t| ≤ t1−α/2;n−2

Ostap Okhrin 140 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

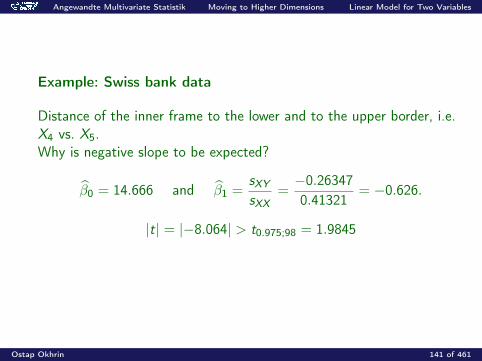

Example: Swiss bank data

Distance of the inner frame to the lower and to the upper border, i.e.X4 vs. X5.Why is negative slope to be expected?

β0 = 14.666 and β1 =sXYsXX

=−0.263470.41321

= −0.626.

|t| = |−8.064| > t0.975;98 = 1.9845

Ostap Okhrin 141 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

Summary: Linear Regression

The linear regression y = β0 + β1x + ε models a linear relationbetween two one-dimensional variables.

The sign of the slope β1 is the same as that of the covariance andthe correlation of x and y .

A linear regression predicts values of Y given a possibleobservation x of X .

Ostap Okhrin 142 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

Summary: Linear Regression

The coefficient of determination r2 measures the amount ofvariation in Y which is explained by a linear regression on X .

If the coefficient of determination is r2 = 1, then all points lie onone line.

The regression line of X on Y and the regression line of Y on Xare in general different.

Ostap Okhrin 143 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Linear Model for Two Variables

Summary: Linear Regression

The t-test for the hypothesis β1 = 0 is t = β1SE(β1)

, where

SE (β1) = σ(n·sXX )1/2

.

The t-test rejects the null hypothesis β = 0 at the level ofsignificance α if |t| ≥ t1−α/2;n−2 where t1−α;n−2 is the 1− α/2quantile of the Student’s t-distribution with (n − 2) degrees offreedom.

The standard error SE (β) increases/decreases with less/morespread in the X variables.

Ostap Okhrin 144 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

Simple Analysis of Variance (ANOVA)

Assumptions

Average values of the response variable y are induced by onesimple factor

Factor takes on p values For each factor level, we have m = n/p observations All observations are independent

Ostap Okhrin 145 of 461

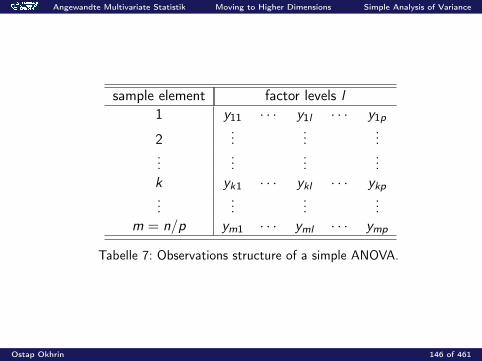

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

sample element factor levels l1 y11 · · · y1l · · · y1p

2...

......

......

......

k yk1 · · · ykl · · · ykp...

......

...m = n/p ym1 · · · yml · · · ymp

Tabelle 7: Observations structure of a simple ANOVA.

Ostap Okhrin 146 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

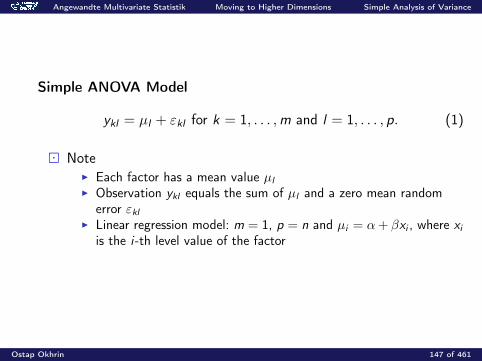

Simple ANOVA Model

ykl = µl + εkl for k = 1, . . . ,m and l = 1, . . . , p. (1)

NoteI Each factor has a mean value µl

I Observation ykl equals the sum of µl and a zero mean randomerror εkl

I Linear regression model: m = 1, p = n and µi = α+ βxi , where xiis the i-th level value of the factor

Ostap Okhrin 147 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

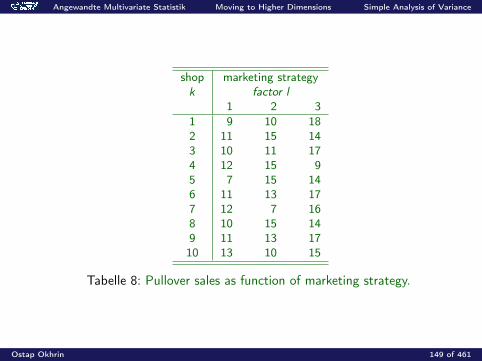

Example: “Classic blue” pullover data

Analyse the effect of three marketing strategies:1. Advertisement in local newspapers2. Presence of sales assistant3. Luxury presentation in shop windows

p = 3 factors, 10 different shops and n = mp = 30 observations

Ostap Okhrin 148 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

shop marketing strategyk factor l

1 2 31 9 10 182 11 15 143 10 11 174 12 15 95 7 15 146 11 13 177 12 7 168 10 15 149 11 13 1710 13 10 15

Tabelle 8: Pullover sales as function of marketing strategy.

Ostap Okhrin 149 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

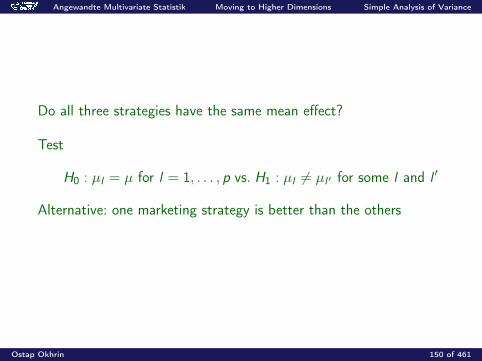

Do all three strategies have the same mean effect?

Test

H0 : µl = µ for l = 1, . . . , p vs. H1 : µl 6= µl ′ for some l and l ′

Alternative: one marketing strategy is better than the others

Ostap Okhrin 150 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

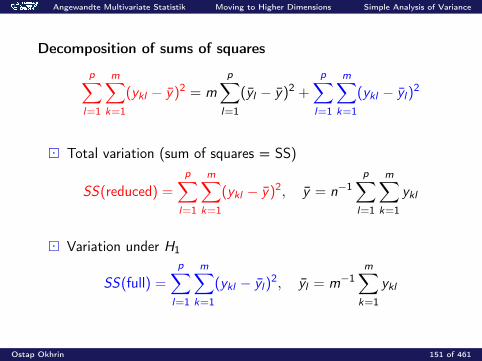

Decomposition of sums of squares

p∑l=1

m∑k=1

(ykl − y)2 = m

p∑l=1

(yl − y)2 +

p∑l=1

m∑k=1

(ykl − yl)2

Total variation (sum of squares = SS)

SS(reduced) =

p∑l=1

m∑k=1

(ykl − y)2, y = n−1p∑

l=1

m∑k=1

ykl

Variation under H1

SS(full) =

p∑l=1

m∑k=1

(ykl − yl)2, yl = m−1

m∑k=1

ykl

Ostap Okhrin 151 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

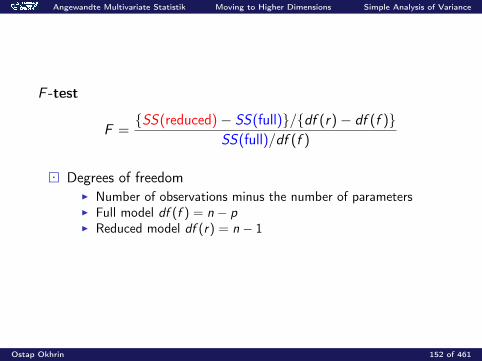

F -test

F =SS(reduced)− SS(full)/df (r)− df (f )

SS(full)/df (f )

Degrees of freedomI Number of observations minus the number of parametersI Full model df (f ) = n − pI Reduced model df (r) = n − 1

Ostap Okhrin 152 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

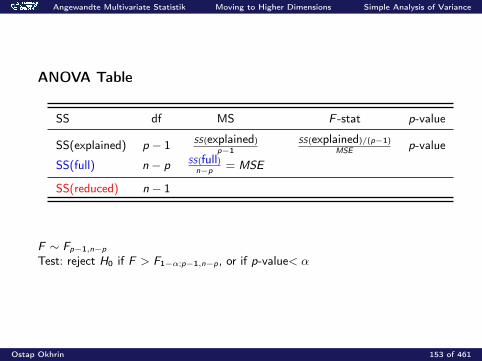

ANOVA Table

SS df MS F -stat p-value

SS(explained) p − 1 SS(explained)

p−1SS(explained)/(p−1)

MSEp-value

SS(full) n − p SS(full)n−p

= MSE

SS(reduced) n − 1

F ∼ Fp−1,n−p

Test: reject H0 if F > F1−α;p−1,n−p, or if p-value< α

Ostap Okhrin 153 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

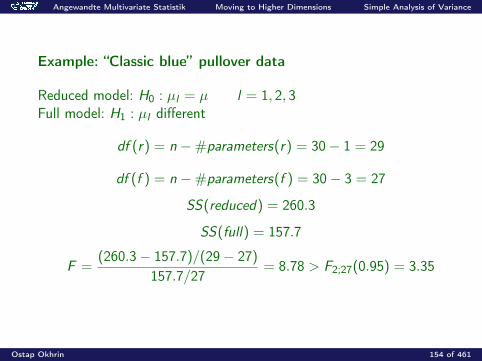

Example: “Classic blue” pullover data

Reduced model: H0 : µl = µ l = 1, 2, 3Full model: H1 : µl different

df (r) = n −#parameters(r) = 30− 1 = 29

df (f ) = n −#parameters(f ) = 30− 3 = 27

SS(reduced) = 260.3

SS(full) = 157.7

F =(260.3− 157.7)/(29− 27)

157.7/27= 8.78 > F2;27(0.95) = 3.35

Ostap Okhrin 154 of 461

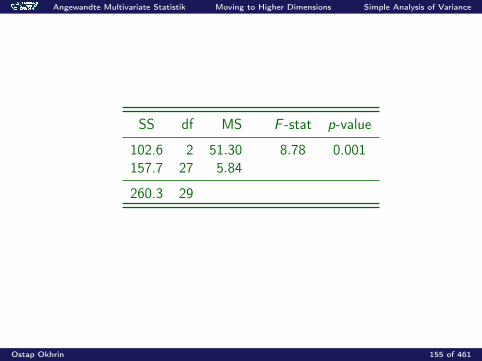

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

SS df MS F -stat p-value

102.6 2 51.30 8.78 0.001157.7 27 5.84

260.3 29

Ostap Okhrin 155 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

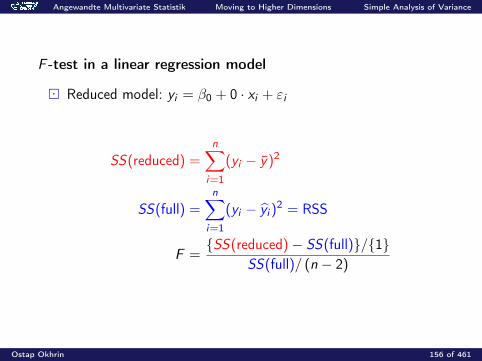

F -test in a linear regression model

Reduced model: yi = β0 + 0 · xi + εi

SS(reduced) =n∑

i=1

(yi − y)2

SS(full) =n∑

i=1

(yi − yi )2 = RSS

F =SS(reduced)− SS(full)/1

SS(full)/ (n − 2)

Ostap Okhrin 156 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

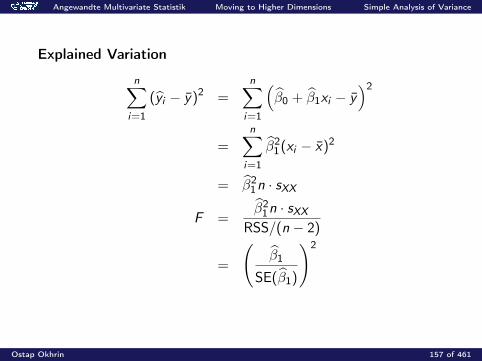

Explained Variation

n∑i=1

(yi − y)2 =n∑

i=1

(β0 + β1xi − y

)2

=n∑

i=1

β21(xi − x)2

= β21n · sXX

F =β2

1n · sXXRSS/(n − 2)

=

(β1

SE(β1)

)2

Ostap Okhrin 157 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

Summary: ANOVA

Simple ANOVA models an output Y as a function of one factor. The reduced model is the hypothesis of equal means. The full model is the alternative hypothesis of different means. The F -test is based on a comparison of the sum of squares under

the full and the reduced models.

Ostap Okhrin 158 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions Simple Analysis of Variance

Summary: ANOVA

The degrees of freedom are calculated as the number ofobservations minus the number of parameters.

The F -statistic is

F =SS(reduced)− SS(full)/df (r)− df (f )

SS(full)/df (f ).

Reject the null if the F -statistic is larger than the(1− α)-quantile of the Fdf (r)−df (f ),df (f ) distribution.

The F -test statistic for the slope of the linear regression modelyi = β0 + β1xi + εi is the square of the t-test statistic.

Ostap Okhrin 159 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

Multiple Linear Model

y(n × 1), X (n × p), β = (β1, . . . , βp)

Approximate y by a linear combination y of columns of XFind β such that y = X β is the best fit of y = Xβ + ε (errors ε)

β = argminβ

(y −Xβ)>(y −Xβ)

= argminβ

n∑i=1

(yi − x>i β)2 =(X>X

)−1X>y ,

if X>X is of full rank.

Ostap Okhrin 160 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

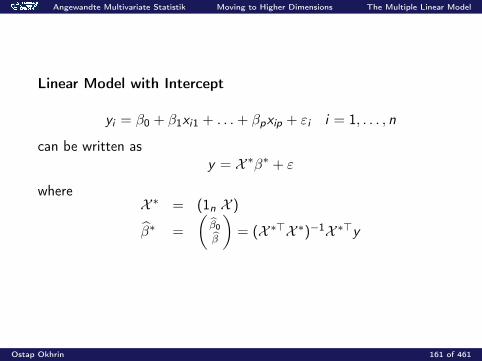

Linear Model with Intercept

yi = β0 + β1xi1 + . . .+ βpxip + εi i = 1, . . . , n

can be written asy = X ∗β∗ + ε

whereX ∗ = (1n X )

β∗ =

(β0β

)= (X ∗>X ∗)−1X ∗>y

Ostap Okhrin 161 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

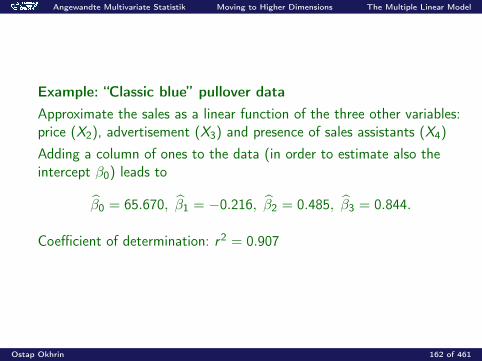

Example: “Classic blue” pullover dataApproximate the sales as a linear function of the three other variables:price (X2), advertisement (X3) and presence of sales assistants (X4)Adding a column of ones to the data (in order to estimate also theintercept β0) leads to

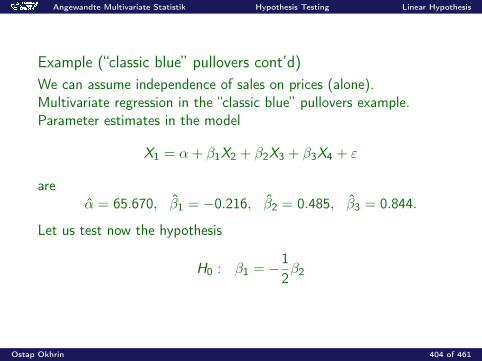

β0 = 65.670, β1 = −0.216, β2 = 0.485, β3 = 0.844.

Coefficient of determination: r2 = 0.907

Ostap Okhrin 162 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

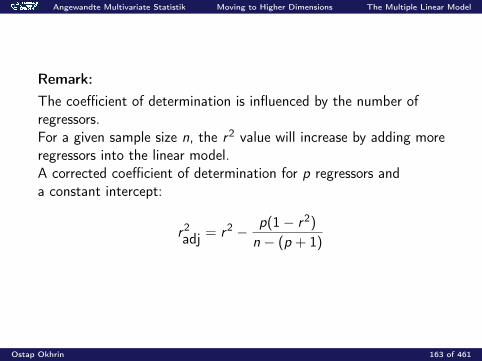

Remark:The coefficient of determination is influenced by the number ofregressors.For a given sample size n, the r2 value will increase by adding moreregressors into the linear model.A corrected coefficient of determination for p regressors anda constant intercept:

r2adj = r2 − p(1− r2)

n − (p + 1)

Ostap Okhrin 163 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

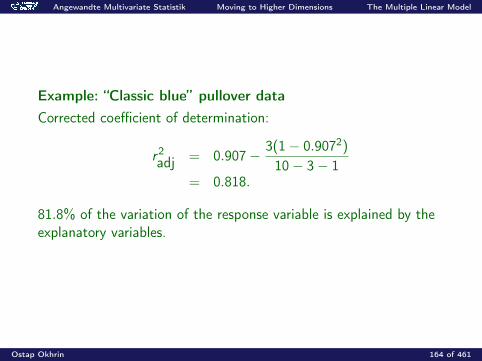

Example: “Classic blue” pullover dataCorrected coefficient of determination:

r2adj = 0.907− 3(1− 0.9072)

10− 3− 1= 0.818.

81.8% of the variation of the response variable is explained by theexplanatory variables.

Ostap Okhrin 164 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

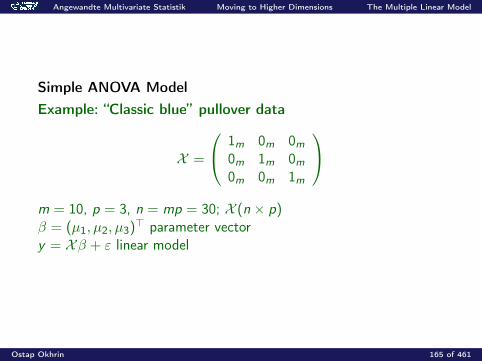

Simple ANOVA ModelExample: “Classic blue” pullover data

X =

1m 0m 0m0m 1m 0m0m 0m 1m

m = 10, p = 3, n = mp = 30; X (n × p)β = (µ1, µ2, µ3)> parameter vectory = Xβ + ε linear model

Ostap Okhrin 165 of 461

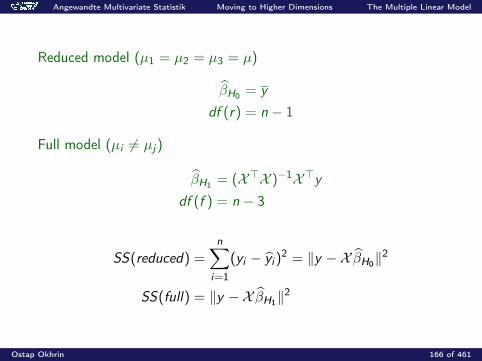

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

Reduced model (µ1 = µ2 = µ3 = µ)

βH0 = y

df (r) = n − 1

Full model (µi 6= µj)

βH1 = (X>X )−1X>ydf (f ) = n − 3

SS(reduced) =n∑

i=1

(yi − yi )2 = ‖y −X βH0‖2

SS(full) = ‖y −X βH1‖2

Ostap Okhrin 166 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

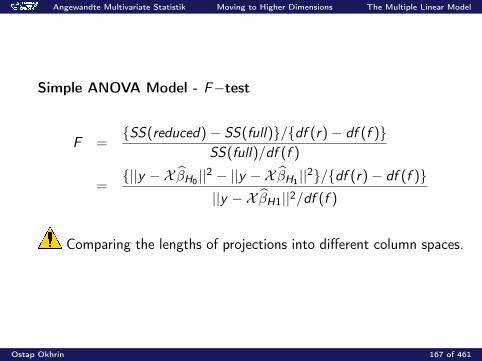

Simple ANOVA Model - F−test

F =SS(reduced)− SS(full)/df (r)− df (f )

SS(full)/df (f )

=||y −X βH0 ||2 − ||y −X βH1 ||2/df (r)− df (f )

||y −X βH1||2/df (f )

Comparing the lengths of projections into different column spaces.

Ostap Okhrin 167 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

Summary: Multiple Linear Model

The relation y = Xβ + ε models a linear relation betweena one-dimensional variable Y and a p-dimensional variable X . Pygives the best linear regression fit of the vector y onto C (X ). Theleast squares parameter estimator is β = (X>X )−1X>y .

The simple ANOVA model can be written as a linear model.

Ostap Okhrin 168 of 461

Angewandte Multivariate Statistik Moving to Higher Dimensions The Multiple Linear Model

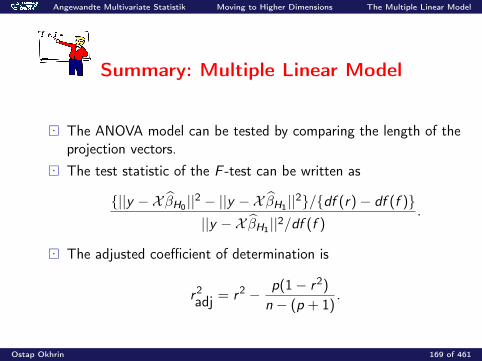

Summary: Multiple Linear Model

The ANOVA model can be tested by comparing the length of theprojection vectors.

The test statistic of the F -test can be written as

||y −X βH0 ||2 − ||y −X βH1 ||2/df (r)− df (f )||y −X βH1 ||2/df (f )

.

The adjusted coefficient of determination is

r2adj = r2 − p(1− r2)

n − (p + 1).

Ostap Okhrin 169 of 461

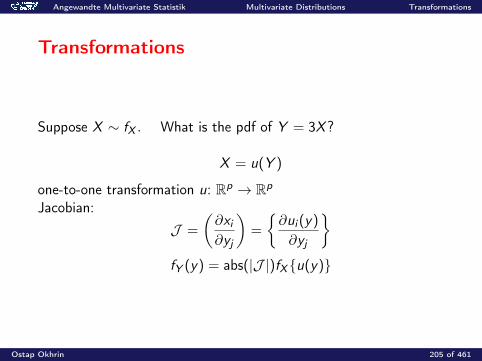

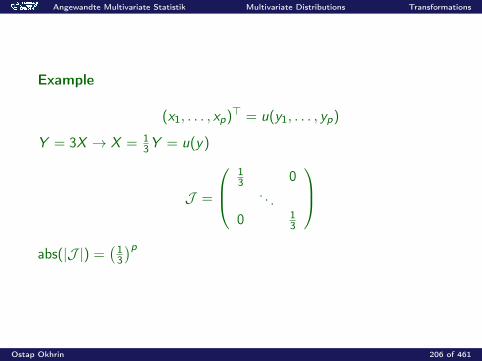

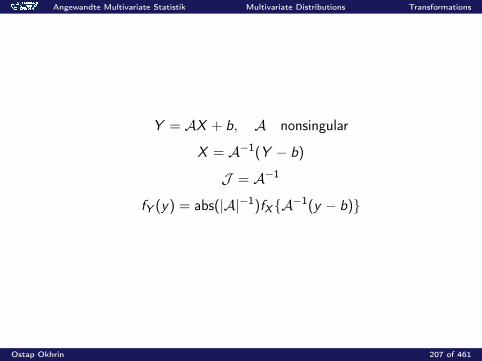

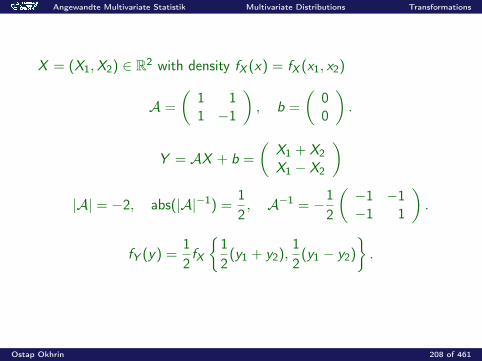

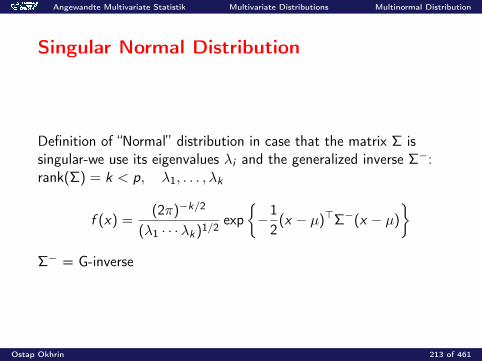

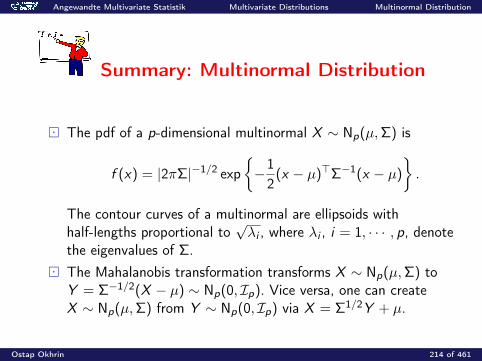

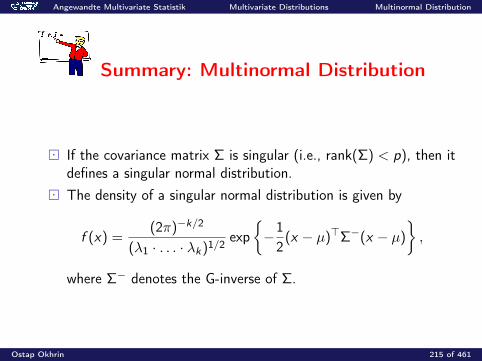

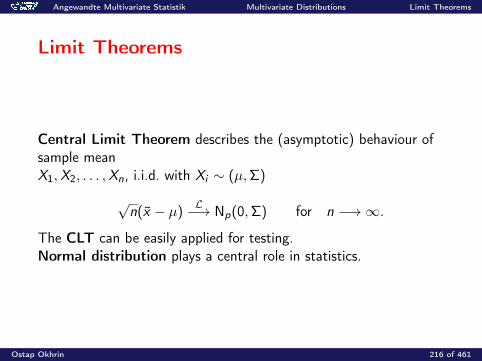

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

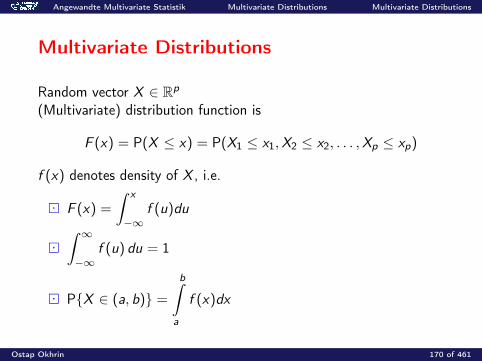

Multivariate Distributions

Random vector X ∈ Rp

(Multivariate) distribution function is

F (x) = P(X ≤ x) = P(X1 ≤ x1,X2 ≤ x2, . . . ,Xp ≤ xp)

f (x) denotes density of X , i.e.

F (x) =

∫ x

−∞f (u)du

∫ ∞−∞

f (u) du = 1

PX ∈ (a, b) =

b∫a

f (x)dx

Ostap Okhrin 170 of 461

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

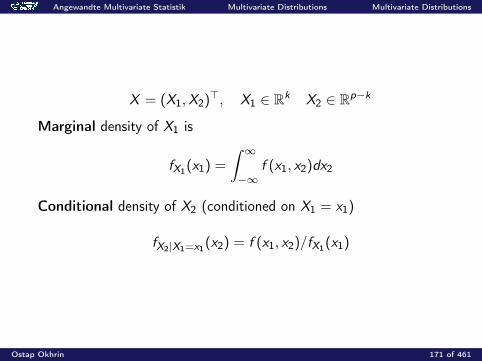

X = (X1,X2)>, X1 ∈ Rk X2 ∈ Rp−k

Marginal density of X1 is

fX1(x1) =

∫ ∞−∞

f (x1, x2)dx2

Conditional density of X2 (conditioned on X1 = x1)

fX2|X1=x1(x2) = f (x1, x2)/fX1(x1)

Ostap Okhrin 171 of 461

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

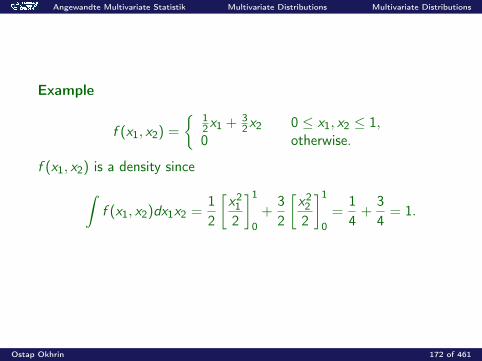

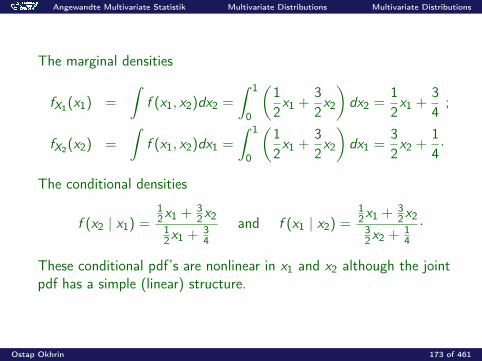

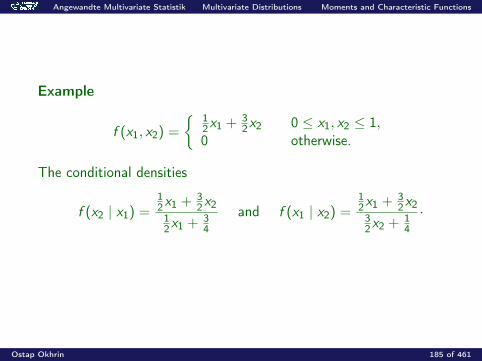

Example

f (x1, x2) =

12x1 + 3

2x2 0 ≤ x1, x2 ≤ 1,0 otherwise.

f (x1, x2) is a density since∫f (x1, x2)dx1x2 =

12

[x212

]1

0+

32

[x222

]1

0=

14

+34

= 1.

Ostap Okhrin 172 of 461

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

The marginal densities

fX1(x1) =

∫f (x1, x2)dx2 =

∫ 1

0

(12x1 +

32x2

)dx2 =

12x1 +

34

;

fX2(x2) =

∫f (x1, x2)dx1 =

∫ 1

0

(12x1 +

32x2

)dx1 =

32x2 +

14·

The conditional densities

f (x2 | x1) =12x1 + 3

2x212x1 + 3

4and f (x1 | x2) =

12x1 + 3

2x232x2 + 1

4·

These conditional pdf’s are nonlinear in x1 and x2 although the jointpdf has a simple (linear) structure.

Ostap Okhrin 173 of 461

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

Definition of independence

X1, X2 are independent iff

f (x) = f (x1, x2) = fX1(x1)fX2(x2)

Two random variables may have identical marginals but differentjoint distribution.

Ostap Okhrin 174 of 461

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

Example

f (x1, x2) = 1, 0 < x1, x2 < 1,

f (x1, x2) = 1 + α(2x1 − 1)(2x2 − 1), 0 < x1, x2 < 1, −1 ≤ α ≤ 1.

fX1(x1) = 1, fX2(x2) = 1.∫ 1

01 + α(2x1 − 1)(2x2 − 1)dx2 = 1 + α(2x1 − 1)[x2

2 − x2]10 = 1.

Ostap Okhrin 175 of 461

7 8 9 10 11

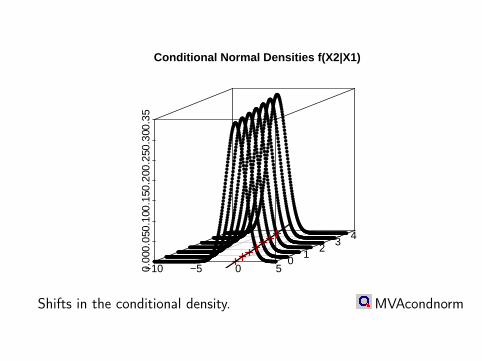

0.0

0.1

0.2

0.3

0.4

0.5

Swiss bank notes

Lower Inner Frame (X4)

Den

sity

7 8 9 10 11 12

0.0

0.1

0.2

0.3

0.4

0.5

0.6

Swiss bank notes

Upper Inner Frame (X5)D

ensi

ty

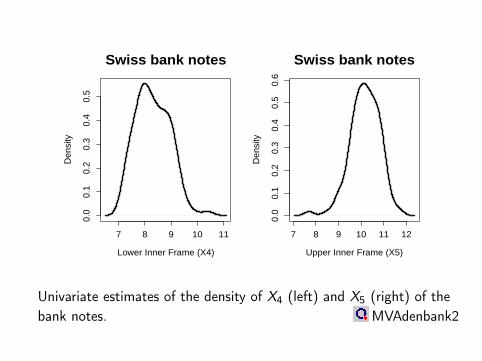

Univariate estimates of the density of X4 (left) and X5 (right) of thebank notes. MVAdenbank2

68

1012

14

810

12

0

0.05

0.1

0.15

0.2

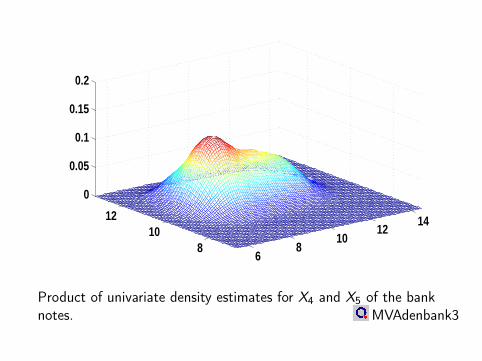

Product of univariate density estimates for X4 and X5 of the banknotes. MVAdenbank3

5

10

15 510

15

0

0.05

0.1

0.15

0.2

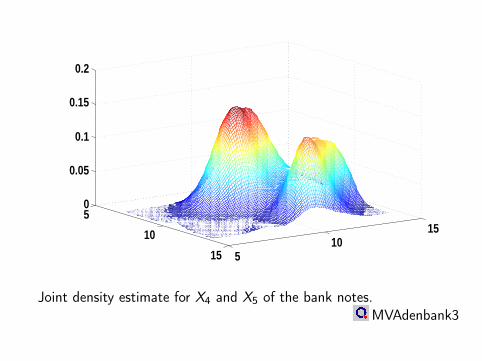

Joint density estimate for X4 and X5 of the bank notes.MVAdenbank3

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

Summary: Distributions

The cumulative distribution function (cdf) is F (x) = P(X < x). If a probability density function (pdf) f exists then

F (x) =

∫ x

−∞f (u)du.

Let X = (X1,X2)> be partitioned in subvectors X1 and X2 withjoint cdf F . Then FX1(x1) = P(X1 ≤ x1) is the marginal cdf of

X1. The marginal pdf of X1 is fX1(x1) =

∫ ∞−∞

f (x1, x2)dx2.

Ostap Okhrin 179 of 461

Angewandte Multivariate Statistik Multivariate Distributions Multivariate Distributions

Summary: Distributions

Different joint pdf’s may have the same marginal pdf’s.

The conditional pdf of X2 given X1 = x1 is f (x2 | x1) =f (x1, x2)

fX1(x1)·

Two random variables X1,X2 are called independent ifff (x1, x2) = fX1(x1)fX2(x2). This is equivalent tof (x2 | x1) = fX2(x2).

Ostap Okhrin 180 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Moments and Characteristic Functions

EX ∈ Rp denotes the p-dimensional vector of expected values of therandom vector X

EX =

EX1...

EXp

=

∫xf (x)dx =

∫x1f (x)dx

...∫xpf (x)dx

= µ.

The properties of the expected value follow from the properties of theintegral:

E (αX + βY ) = αEX + β EY

Ostap Okhrin 181 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

If X and Y are independent then

E(XY>) =

∫xy>f (x , y)dxdy

=

∫xf (x)dx

∫y>f (y)dy = EX EY>

Definition of the covariance matrix (Σ)

Σ = Var(X ) = E(X − µ)(X − µ)>

We say that a random vector X has a distribution with the vector ofexpected values µ and the covariance matrix Σ,

X ∼ (µ,Σ)

Ostap Okhrin 182 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Properties of the Covariance Matrix

Elements of Σ are variances and covariances of the components of therandom vector X :

Σ = (σXiXj)

σXiXj= Cov(Xi ,Xj)

σXiXi= Var(Xi )

Computational formula: Σ = E(XX>)− µµ>Covariance matrix is positive semidefinite, Σ ≥ 0(variance a>Σa of any linear combination a>X cannot be negative).

Ostap Okhrin 183 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Properties of Variances and Covariances

Var(a>X ) = a> Var(X ) a =∑i ,j

aiajσXiXj

Var(AX + b) = A Var(X ) A>

Cov(X + Y ,Z ) = Cov(X ,Z ) + Cov(Y ,Z )

Var(X + Y ) = Var(X ) + Cov(X ,Y ) + Cov(Y ,X ) + Var(Y )

Cov(AX ,BY ) = A Cov(X ,Y ) B>.

Ostap Okhrin 184 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

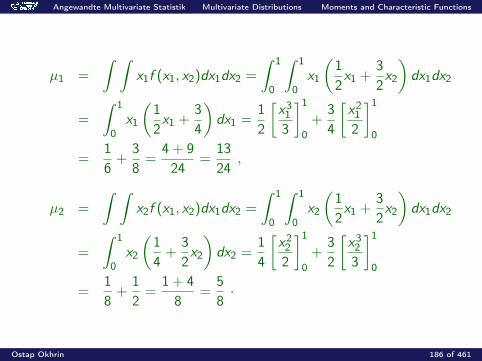

Example

f (x1, x2) =

12x1 + 3

2x2 0 ≤ x1, x2 ≤ 1,0 otherwise.

The conditional densities

f (x2 | x1) =12x1 + 3

2x212x1 + 3

4and f (x1 | x2) =

12x1 + 3

2x232x2 + 1

4·

Ostap Okhrin 185 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

µ1 =

∫ ∫x1f (x1, x2)dx1dx2 =

∫ 1

0

∫ 1

0x1

(12x1 +

32x2

)dx1dx2

=

∫ 1

0x1

(12x1 +

34

)dx1 =

12

[x313

]1

0+

34

[x212

]1

0

=16

+38

=4 + 924

=1324

,

µ2 =

∫ ∫x2f (x1, x2)dx1dx2 =

∫ 1

0

∫ 1

0x2

(12x1 +

32x2

)dx1dx2

=

∫ 1

0x2

(14

+32x2

)dx2 =

14

[x222

]1

0+

32

[x323

]1

0

=18

+12

=1 + 48

=58·

Ostap Okhrin 186 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

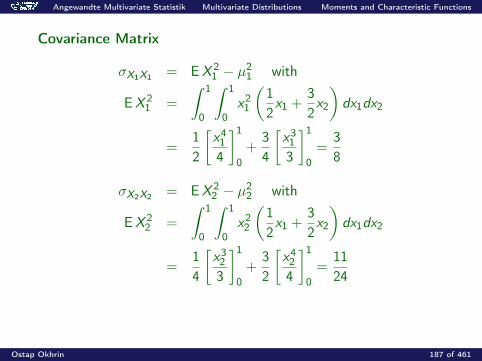

Covariance Matrix

σX1X1 = EX 21 − µ2

1 with

EX 21 =

∫ 1

0

∫ 1

0x21

(12x1 +

32x2

)dx1dx2

=12

[x414

]1

0+

34

[x313

]1

0=

38

σX2X2 = EX 22 − µ2

2 with

EX 22 =

∫ 1

0

∫ 1

0x22

(12x1 +

32x2

)dx1dx2

=14

[x323

]1

0+

32

[x424

]1

0=

1124

Ostap Okhrin 187 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

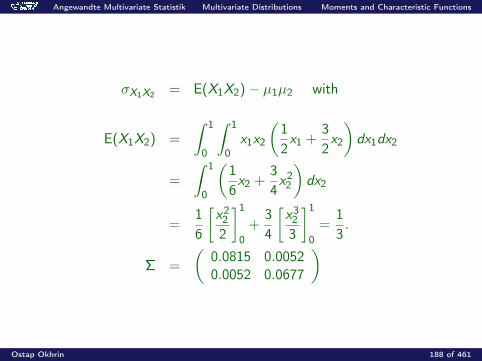

σX1X2 = E(X1X2)− µ1µ2 with

E(X1X2) =

∫ 1

0

∫ 1

0x1x2

(12x1 +

32x2

)dx1dx2

=

∫ 1

0

(16x2 +

34x22

)dx2

=16

[x222

]1

0+

34

[x323

]1

0=

13.

Σ =

(0.0815 0.00520.0052 0.0677

)

Ostap Okhrin 188 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Conditional Expectations

Random vector X = (X1,X2)>, X1 ∈ Rk X2 ∈ Rp−k

Conditional expectation of X2, given X1 = x1:

E(X2 | x1) =

∫x2f (x2 | x1) dx2

and conditional expectation of X1, given X2 = x2:

E(X1 | x2) =

∫x1f (x1 | x2) dx1

The conditional expectation E(X2 | x1) is a function of x1.Typical example of this setup is a simple linear regression, whereE(Y | X = x) = Xβ.

Ostap Okhrin 189 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Error term in approximation:

U = X2 − E(X2 | X1)

(1) E(U) = 0(2) E(X2|X1) is the best approximation of X2 by a function h(X1) of

X1 in the sense of mean squared error (MSE) whenMSE (h) = E[X2 − h(X1)> X2 − h(X1)] andh : Rk −→ Rp−k .

Ostap Okhrin 190 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Summary: Moments

The expectation of a random vector X is µ =∫xf (x) dx , the

covariance matrix Σ = Var(X ) = E(X − µ)(X − µ)>. We denoteX ∼ (µ,Σ).

Expectations are linear, i.e., E(αX + βY ) = αEX + β EY . IfX ,Y are independent then E(XY>) = EX EY>.

Ostap Okhrin 191 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Summary: Moments

The covariance between two random vectors X ,Y is ΣXY =Cov(X ,Y ) = E(X − EX )(Y − EY )> = E(XY>)− EX EY>. IfX ,Y are independent then Cov(X ,Y ) = 0.

The conditional expectation E(X2|X1) is the MSE bestapproximation of X2 by a function of X1.

Ostap Okhrin 192 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

Characteristic Functions

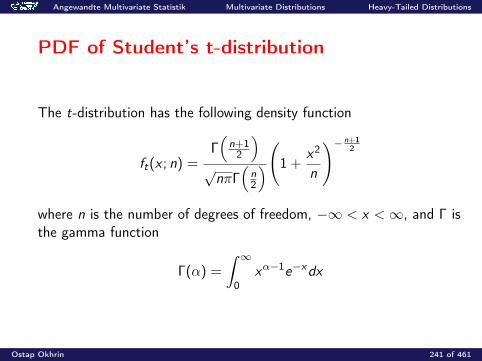

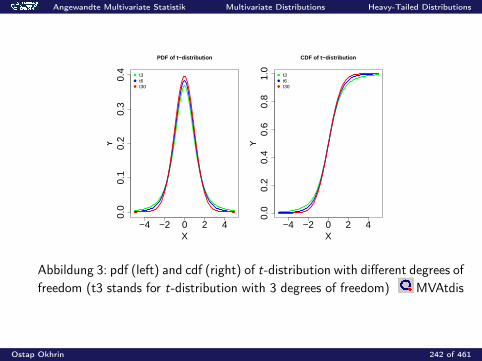

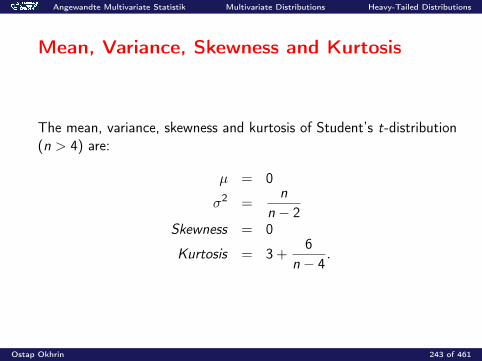

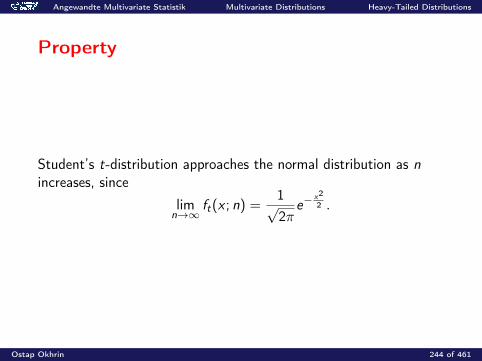

The characteristic function (cf) of a random vector X ∈ Rp is definedas

ϕX (t) = E(e it>X ) =

∫e it>x f (x) dx , t ∈ Rp,

where i is the complex unit: i2 = −1.

Ostap Okhrin 193 of 461

Angewandte Multivariate Statistik Multivariate Distributions Moments and Characteristic Functions

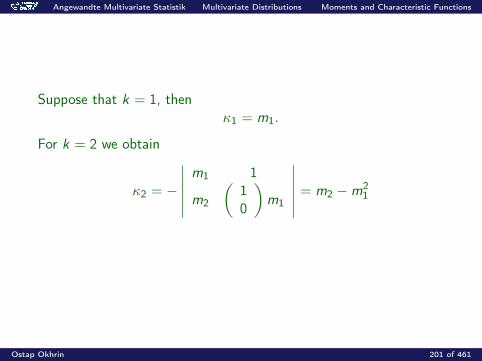

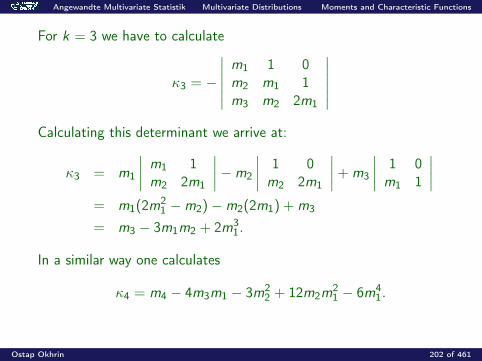

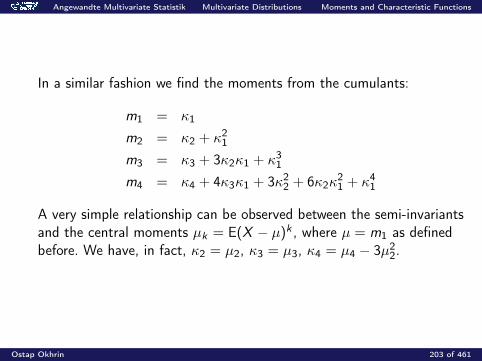

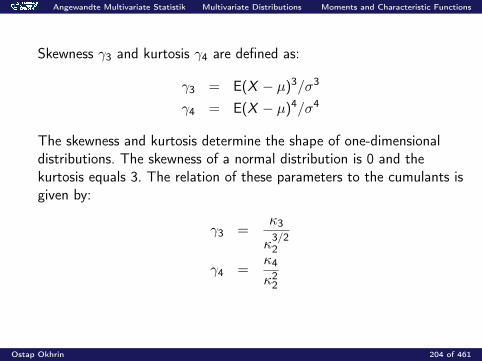

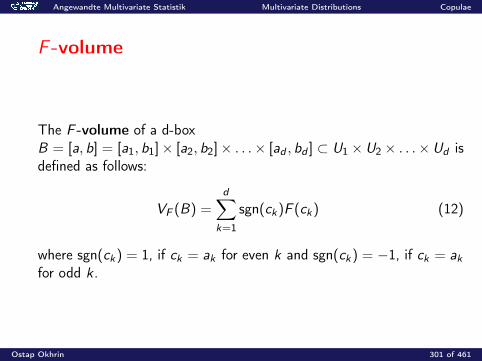

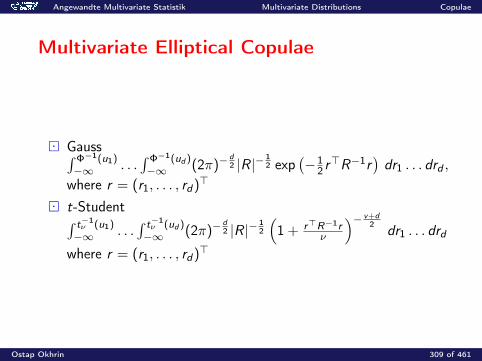

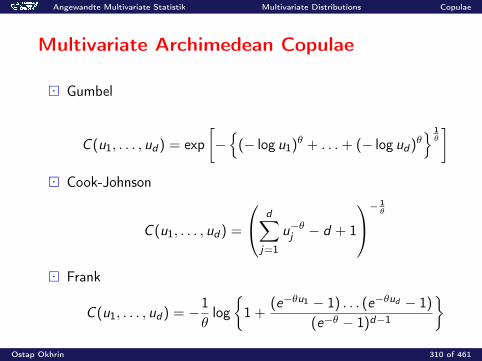

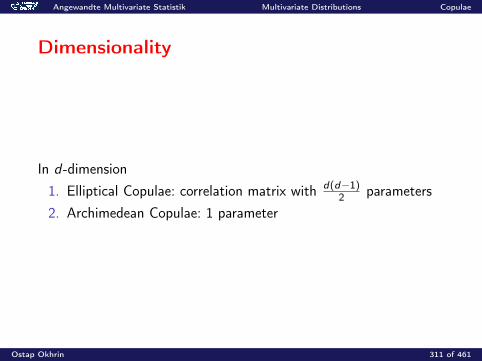

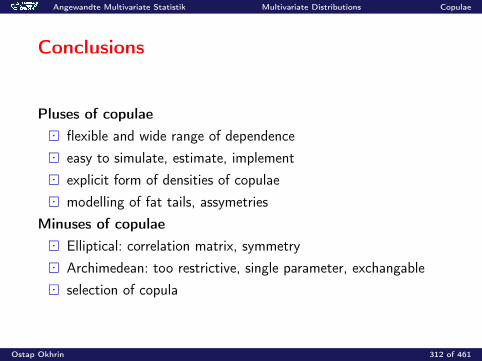

Properties of cf: ϕX (0) = 1, |ϕX (t)| ≤ 1