Embed Size (px)

Citation preview

I S S U E 4 8 • F A L L 2 0 0 8 • I S S N 1 2 0 3 - 7 7 2 9

I N T H I S I S S U E

PENSIONc onn e c t i o n

T H E

A newsletterfor the pensionersof the OPSEUPension Trust

Good news about your pension plan.OPTrust’s most recent actuarialvaluation has identified a funding

surplus of $470 million in the Plan, as ofDecember 31, 2007. The surplus is theresult of $841 million in gains realizedover three years from 2004 to 2007. Partof the gains was also used to eliminatethe remainder of the Plan’s $428 millionfunding deficit.

Sponsors reach a decisionOPSEU and the Government of Ontariohave chosen to allocate their shares ofthe surplus to the Plan’s stabilization funds.As a result, the stabilization funds haveincreased to $383 million for OPTrust’smembership, and $495 million for thegovernment.

1 OPTrust identifiesfunding surplus andeliminates deficit

1 Facts About. . . PensionIncome Splitting

4 Protect yourself frominvestment fraud

4 Reminder: UpdateYour Personal TaxCredits

5 Retiree Profile:Patricia Waugh

5 What will you receivefrom CPP?

6 You asked. . .

7 Your OPTrust ID andyour security

7 Pension Connectione-updates to keepyou in the know

7 Seniors CanadaOnline Resources

8 New Board Chair andVice-Chair

OPTrust identifies funding surplusand eliminates deficit

> Funding surplus... continued on page 3

Facts About... Pension Income Splitting

The federal government introducedpension income splitting in the 2007budget to give Canadian retirees an

option to reduce their taxes each year.So what does this mean for you and yourOPTrust pension? Do you think you mightbenefit from income splitting?

The new tax rule allows retirees to splittheir pension income with their partnerwhich may reduce overall taxes. Let’ssay your income is higher than yourspouse’s, then you can allocate up toone-half of your OPTrust pensionincome to your spouse for tax purposes.

> Pension income spitting... continued on page 2

Good news about your pension plan!

2 T H E P E N S I O N C O N N E C T I O N

When should you consider pension incomesplitting?You and your spouse may want to consider splittingpension income in the following situations if:• one spouse is in a higher tax bracket. At a

minimum, you will save the difference in thetax rates between each spouse’s tax bracket.

• one spouse is not fully using the pension creditamount.

• the spouse with the pension income to betransferred is affected by social benefitsrepayment (e.g. OAS repayment for net incomehigher than $63,511) or a reduced age creditamount.

• one spouse is paying provincial surtax.

In each of these cases, pension income splittingmay reduce your combined income tax and may beworth considering.

When will pension income splitting notbenefit you?If both you and your spouse have eligible pensionincome, are fully using the pension income amount,and are in the same tax bracket, there may be nobenefit to pension splitting. If neither spouse’sincome is taxable, pension splitting will not bebeneficial.

Other points to considerThe amount of pension income that can be splitis indicated on the Joint Election to Split PensionIncome (T1032 form). Pension income does nothave to be split equally (50/50). You can choosethe most beneficial amount to transfer to yourspouse, as long as it does not exceed 50% of youreligible pension income.

Pension splitting can impact other tax credits andcalculations. You should review the following claims,with either a financial advisor or tax specialist,before and after transferring pension income:

• age

• medical expenses

• donations and gifts

• social benefits repayment

• spouse or common-law partner credit

• pension income amount

• amounts transferred from your spouse orcommon-law partner.

EligibilityUnder the federal government’s requirement, youand your spouse or common-law partner can electto split your eligible pension income received in theyear if you meet the following conditions:• you are married or in a common-law partnership

with each other in the year and are not livingseparate and apartfrom each other.

• you are both residentsin Canada onDecember 31st.

If you want to split yourincome for the 2008 taxyear, you and your spousewill need to complete aJoint Election to SplitPension Income (T1032form) available from theCanada Revenue Agencywebsite.

> Pension income splitting... continued from page 1

Let’s look at an example

EXAMPLE

Note this example is based on the 2007 tax rates.

Retiree: age 65, $30,000 pension income

Spouse: age 60, $10,000 pension income

Pension splitting Amount split Tax saving

Max 50% split $ 15,000 $ 562

Split to equalizeincome

$ 12,500 $ 535

Optimal split $ 12,500 $ 535

This couple could earn an estimated tax savings of$535 by splitting their income.

Want moreinformation?

For more information,visit the CanadaRevenue Agency’swebsite atwww.cra-arc.gc.ca.You should alsocontact a financialadvisor or taxspecialist to help youdecide if pensionincome splitting isright for you.

•

•

The sponsors’ decision to increase thePlan’s stabilization funds is a prudent one.With the increase in market volatilitysince mid-2007 – and the possibility ofsignificant investment losses in 2008 –setting aside substantial reserves is oneimportant way to manage the risk offuture funding shortfalls.

These funds can be used by each sponsorto limit or avoid contribution increasesthat would be required if the Plan’sexperiences a funding loss. This couldhappen if the Plan’s investment resultsfall short of the OPTrust’s 6.75% targetreturn, or if the cost of members’ andretirees’ pensions increases faster thanexpected. The stabilization funds canalso be used to reduce member andemployer contribution rates or enhanceplan benefits in the future.

Actuarial valuationWhile OPTrust carries out an actuarialvaluation every year, the valuationmust be filed with Ontario’s pensionregulators at least once every three years.The purpose is to determine whetherinvestment assets are sufficient to meetthe pension promise for all members andretirees, today and in the future.

These valuations provide a snapshotof the Plan’s funded status and a tallyof gains or losses experienced since thelast valuation.

OPTrust’s primary goal is to ensurethat money is available to pay currentand future retirees’ pensions over theirlifetimes, while maintaining stablecontribution rates for plan membersand employers.

Shared risks and rewardsWhen the OPSEU Pension Plan wasestablished, its sponsors – the Governmentof Ontario and the Ontario Public ServiceEmployees Union (OPSEU) – agreed thatany gains or losses would be shared betweenthe Government and the Plan’s membersand pensioners.

Deficit eliminatedThe Plan went from a deficit of $428million in 2004 – due to poor investmentreturns between 2000 and 2002 – to asurplus of $470 million at the end of 2007.The shortfall in 2004 would have normallytriggered an immediate increase in pensioncontribution rates for members andemployers. However, both OPSEU andthe Government of Ontario had set asidea substantial portion of the past fundinggains in a separate rate stabilization fund.Since 2002, these funds have been used tokeep member and employer contributionrates stable.

Online survey rated your opinionIn August 2008, OPSEU surveyed morethan 81,000 members and pensioners to rateseven proposed options on temporary andpermanent benefit improvements. OPSEUlooked at a cost-efficient, convenient andsecure way to distribute the survey and optedto go online, given the short timeframe tofile the valuation.

OPTrust worked with OPSEU to deliver thesurvey in its secure Online Services website.It was designed to prevent duplication andmake the tally of results more efficient andreliable. OPTrust did not share individualrecords or responses with OPSEU, onlystatistics for each question.

> Funding surplus... continued from page 1

T H E P E N S I O N C O N N E C T I O N 3

OPTrust’s primarygoal is to ensurethat money isavailable to paycurrent and futureretirees’ pensionsover their lifetimes,while maintainingstable contributionrates for planmembers andemployers.

4 T H E P E N S I O N C O N N E C T I O N

Protecting your finances and investmentsfrom scam artists is critical at any stage butit’s important to be aware of what to look out

for in retirement too. That’s where a new bookletfrom the Canadian Securities Administrators (CSA)comes in handy. Protect your money, Avoiding fraudsand scams outlines what to watch for and how toprotect yourself from investment fraud, includingtips for protecting your money.

What to watch out for

The CSA1 advises retirees to watch out for thesewarning signs:• any financial transaction completed on your

behalf without your consent• transactions for which you have no record• someone who promises or guarantees you a high

return or future price• someone who suggests that an investment will

eventually be listed on a stock exchange• back-dated purchase orders• anyone asking you to pre-sign blank forms• guarantees of any kind or promises to refund

purchase price

Protect yourself from investment fraud

A s part of the retirement process, you completed provincial and federalPersonal Tax Credits Return (TD1/TD1ON) forms to claim tax creditsin retirement. However, if your circumstances have changed since you

retired, it could have an impact on your tax credits. For example, if you’ve turned65 or your spouse has died or maybe you’ve become a caregiver, you shouldupdate this information on a TD1 form to ensure the appropriate amount of taxis withheld from your pension payment.

Reminder: Update YourPersonal Tax Credits

• failure to provide a prospectus• secretive behaviour or requests for silence.

You can download various publications onprotecting your finances and avoiding frauds andscams from the Ontario Securities Commissionwebsite at www.checkbeforeyouinvest.ca. Eachprovince has its own regulator that works intandem under the CSA.

1 Protecting Your Finances, Canadian Securities Administrators

You can update your TD1 information through OPTrust’s secure Online Services website. The federal and Ontarioforms are also available on the OPTrust website at www.optrust.com under the “Pensioner” section. If you live inanother province, you will need to complete the TD1 form from that government. All forms are available on theCanada Revenue Agency website at www.cra-arc.gc.ca. Please send your updated forms to OPTrust so that wecan update your tax deduction information on record.

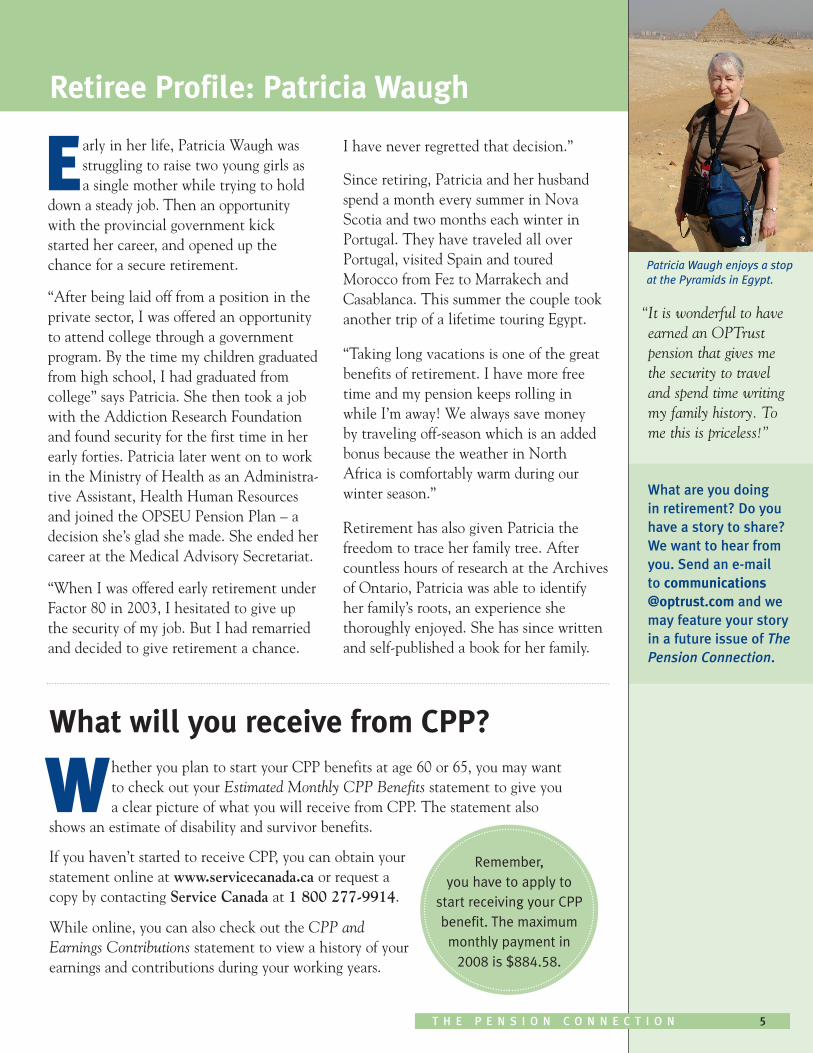

Retiree Profile: Patricia Waugh

What are you doingin retirement? Do youhave a story to share?We want to hear fromyou. Send an e-mailto [email protected] and wemay feature your storyin a future issue of ThePension Connection.

T H E P E N S I O N C O N N E C T I O N 5

Early in her life, Patricia Waugh wasstruggling to raise two young girls asa single mother while trying to hold

down a steady job. Then an opportunitywith the provincial government kickstarted her career, and opened up thechance for a secure retirement.

“After being laid off from a position in theprivate sector, I was offered an opportunityto attend college through a governmentprogram. By the time my children graduatedfrom high school, I had graduated fromcollege” says Patricia. She then took a jobwith the Addiction Research Foundationand found security for the first time in herearly forties. Patricia later went on to workin the Ministry of Health as an Administra-tive Assistant, Health Human Resourcesand joined the OPSEU Pension Plan – adecision she’s glad she made. She ended hercareer at the Medical Advisory Secretariat.

“When I was offered early retirement underFactor 80 in 2003, I hesitated to give upthe security of my job. But I had remarriedand decided to give retirement a chance.

I have never regretted that decision.”

Since retiring, Patricia and her husbandspend a month every summer in NovaScotia and two months each winter inPortugal. They have traveled all overPortugal, visited Spain and touredMorocco from Fez to Marrakech andCasablanca. This summer the couple tookanother trip of a lifetime touring Egypt.

“Taking long vacations is one of the greatbenefits of retirement. I have more freetime and my pension keeps rolling inwhile I’m away! We always save moneyby traveling off-season which is an addedbonus because the weather in NorthAfrica is comfortably warm during ourwinter season.”

Retirement has also given Patricia thefreedom to trace her family tree. Aftercountless hours of research at the Archivesof Ontario, Patricia was able to identifyher family’s roots, an experience shethoroughly enjoyed. She has since writtenand self-published a book for her family.

“It is wonderful to haveearned an OPTrustpension that gives methe security to traveland spend time writingmy family history. Tome this is priceless!”

What will you receive from CPP?

Whether you plan to start your CPP benefits at age 60 or 65, you may wantto check out your Estimated Monthly CPP Benefits statement to give youa clear picture of what you will receive from CPP. The statement also

shows an estimate of disability and survivor benefits.

If you haven’t started to receive CPP, you can obtain yourstatement online at www.servicecanada.ca or request acopy by contacting Service Canada at 1 800 277-9914.

While online, you can also check out the CPP andEarnings Contributions statement to view a history of yourearnings and contributions during your working years.

Remember,you have to apply to

start receiving your CPPbenefit. The maximummonthly payment in

2008 is $884.58.

Patricia Waugh enjoys a stopat the Pyramids in Egypt.

6 T H E P E N S I O N C O N N E C T I O N

Question: I completed the OPSEU survey on OPTrust’s gains in August.Why did I have to complete the survey online and provide my SocialInsurance Number?

Answer: OPSEU looked at the most cost-efficient way of carrying out thesurvey while meeting the tight September 30, 2008 deadline to file withprovincial regulators. OPTrust partnered with OPSEU to host the survey on oursecure Online Services website. Retirees who had not registered for OnlineServices were asked to provide their Social Insurance Number. Your SINensured that you had a say in the survey. And it prevented duplication to makethe tally of results more efficient and reliable. It did not identify you personally.

Question: I am concerned about future lossesin the Plan – will my pension drop as a resultof funding losses?

Answer: No. The OPSEU Pension Plan is adefined benefit plan. This means your pension isbased on a formula that’s payable for your lifetime.Your annual pension will not decrease due to anyfuture losses in the Plan. OPTrust’s primary goal isto ensure that money is available to pay currentand future retirees’ pensions over their lifetimes,while maintaining stable contribution rates forplan members and employers. OPTrust is requiredto conduct a funding valuation every three yearsto determine funding requirements to paymembers and retirees’ pensions now and in thefuture.

Question: I have insured benefits coverage.What information do I need to bring if I haveto go to the hospital?

Answer: You will need to bring your Great-WestLife ID card to the hospital to ensure your costsare covered. Your card shows the policy numberand your OPTrust ID.

?YOUASKED

Question: I forgot myOnline Servicespassword. How canI access my account?

Answer: You can retrieveyour forgotten password or userID online by visiting OPTrust’shomepage and click “Log-in now,” right below theOnline Services logo. From there follow the “I forgotmy OPTrust ID or password” link. Enter your e-mailaddress and OPTrust will send you a new temporarypassword to your primary e-mail address to accessyour account.

Question: When can I start receiving my CPPand OAS benefits?

Answer: You can collect CPP at age 65 or asearly as age 60 with reductions in your pension forearly payment. The CPP reduction is 6% per yearfor every year you are less than 65. Old AgeSecurity benefits start at age 65 and cannot betaken earlier. For more information on CPP andOAS benefits visit the Service Canada websiteat www.servicecanada.gc.ca.

Your OPTrust ID and your security

Pension Connection e-updates tokeep you in the know

Want to know the 2009 inflationadjustment before the next issue ofThe Pension Connection? OPTrust has

just introduced Pension Connection e-updatesto keep you informed of what’s going on in yourpension plan between each newsletter issue.For example, if a new trustee is appointed orthere are changes to insured benefits premiums,we’ll send you an e-update by e-mail with thehighlights. The more detailed story will appear in the next issue of The PensionConnection.

Anyone with an Online Services account will automatically receive an e-updatein between newsletter issues.

Not registered yet? Visitour website to completeyour registration or contactour Member and PensionerServices staff to walk youthrough the process.

SeniorsCanada OnlineResourcesLooking for volunteeropportunities? Wantmore information ongovernment programsfor retirees? TheGovernment of Canadaprovides valuableonline informationfor retirees lookingfor information onfederal and provincialprograms and services,including:

• CPP and OASbenefits

• publications• volunteer

opportunities• health and wellness• seniors networks

To find out more,visit the SeniorsCanada website atwww.seniors.gc.ca.

T H E P E N S I O N C O N N E C T I O N 7

Protecting your security and personal information is important to OPTrust. That’swhy we’ve assigned every pensioner and member a unique, nine-digit OPTrustID to identify individual records and personal information on file at OPTrust.

Your OPTrust ID is located on your Pensioner Information Change Statement (PICS),and other OPTrust documents and correspondence. It replaces your Social InsuranceNumber (SIN) as a reference number and further protects the privacy and security ofyour personal data.

Unlike your Social Insurance Number, your OPTrust ID is used only to:• access your personal pension information with OPTrust – on the phone, online

or in person• submit benefit claims to Great-West Life, if you qualify.

Your OPTrust ID is also used to access your personal accountthrough secure Online Services.

Of course, it’s always a good idea to keep this numbersafe as you would with personal details such as yourbanking information and other passwords.

Forgot your number? Don’t know your OPTrustID? Not to worry. Contact our office and ourMember and Pensioner Services staff will provideyou with this information, after asking you somesecurity questions.

If you have any comments orquestions, please contact Memberand Pensioner Services at:

OPSEU Pension Trust1 Adelaide Street East, Suite 1200Toronto, Ontario M5C 3A7E-mail: [email protected]: 416-681-6100 in Toronto1-800-637-0024 toll-freeFax: 416-681-6175

www.optrust.com

The Pension Connection ispublished by OPSEU PensionTrust for its pensioners.

Publications Agreement No. 40052641

Return undeliverable Canadian addresses to:OPSEU Pension Trust1 Adelaide Street East, Suite 1200Toronto, OntarioM5C 3A7

Ressources disponibles en françaisÊtes-vous un participant ou une participante bilingue?Préféreriez-vous recevoir La filière des pensions enfrançais? Vous pouvez choisir une version électroniqueou imprimée. Si vous voulez une copie de la versionfrançaise de La filière des pensions, veuillez envoyer uncourriel à [email protected] ou ouvrir unesession dans votre compte de Services en ligne pourtransmettre un message sécurisé à la FRRS.

A s part of OPTrust’sgovernance structure oneGovernment appointee

and one OPSEU appointeefill the positions of Chair andVice-Chair, with the rolesalternating between Governmentand OPSEU appointees everytwo years.

In September, Tony Ross becamethe new Chair of OPTrust’sBoard of Trustees. Ross was firstappointed to the Board in 2000 by the Government of Ontario. At the same time,Doug Paolini, an OPSEU appointee, was appointed Vice-Chair of the Board. Paolinifirst joined the Board in 2007. David Rapaport, the former Chair, remains on theBoard of Trustees.

New Board Chair and Vice-Chair GO GREEN !

ReceiveThe PensionConnectiononline

Distributing ThePension Connectionelectronically is onemore way OPTrust isworking to reduceour environmentalfootprint. With yourhelp we can continueto reduce paper usageand contribute to agreener future. Onceyou are registered forsecure Online Services,you can make theswitch to receive thenewsletter by e-mailonly.

Tony Ross,Chair

Doug Paolini,Vice-Chair