Embed Size (px)

Citation preview

Andean Highway Pass Program

Financial and Economic

Appraisal

prepared for

Inter-American Development Bank

As a subcontract to

Louis Berger International, Inc.

Final Report June 12, 1998

Table of Contents

Chapter Topics Page 1 Introduction 4-5 2 Analytical Framework 6-9 2.1 Program Description and Strategic Options 6 2.2 Analytical Approach 9 3 The Macroeconomic Environment 10-14 3.1 Introduction 10 3.2 Framework 11 3.3 Empirical Results of Macroeconomic Growth Forecasts 11 3.4 Trade Growth Forecasts and Trade Distribution 12 3.5 Role of the Passes 14 4 Economic Benefit and Cost Flows 15-21 4.1 Identification of Costs and Benefits 15 4.2 Economic Benefits from Cargo Traffic 15 4.3 Economic Benefits for Passengers 18 4.4 Other Economic Benefits 18 4.5 Economic Costs of Capital and Foreign Exchange 19 4.6 Economic Costs of Labor, Tradable, Non-Tradable Inputs 19 4.7 Economic Cost of Transportation 21 5 Economic Appraisal of Alternative Passes 22-31 5.1 Introduction and Methodology 22 5.2 Analysis of Individual Passes 23 5.3 Analysis of Combined Passes 24 5.4 Determination of the Recommended Investments 29 5.5 The Recommended Program of Investments 31 6 Distributional Impacts 32-36 6.1 Distribution by Country 32 6.2 Distribution by Sectors 34 7 Fiscal Impacts 37-38 7.1 Introduction 37 7.2 Methodology and Key Assumptions 37 7.3 Empirical Results 38 8 Sensitivity and Risk Analysis 39-45 8.1 Introduction 39 8.2 Methodology 39 8.3 Empirical Results 40 9 Conclusions 46-47

2

Appendices Page A The Macroeconomic Forecast 48-81 B Economic Benefits of Cargo Traffic 84-87 C The Economic Cost of Foreign Exchange 88-100 D The Economic Cost of Labor 101-105 E Economic Costs of Tradable and Non-Tradable Goods 106-108 F The Conversion Factors of Transportation Services 109-111

3

1 INTRODUCTION

Argentina and Chile share one of the longest borders in the world -- more than

5,000 km. Since the beginning of civilization, the Andes Mountains have restricted land

transportation between the two countries. The Andean Highway Pass Program is

designed to provide permanent crossings for trucks and passenger cars under all weather

conditions between cities in the two countries.

The Program is a pure public sector infrastructure investment. There are many

possibilities for passes between the two countries and the construction or improvement of

them should involve both governments. The main objectives of this report are to assess

the economic viability of investments in various passes and the associated fiscal

implications for the governments of Argentina and Chile, respectively.

There will be no conventional financial appraisal of the investments from the

private perspective, since no private ownership of the investment is involved in this

Program. Nevertheless, the technical designs and the engineering cost estimates should

provide important data for economic analysis of the public investments. Furthermore, the

forecasts of cargo and passenger traffic should form an important component of the

economic appraisal.

The economic appraisal evaluates the investment of individual passes and

combined passes from the viewpoint of the Argentinean and Chilean economy,

respectively, as well as of the southern Latin American region as a whole. It starts with

financial costs and develops a series of adjustments for the most important externalities to

reflect the economic costs and benefits for each of the two countries. The streams of

these net economic costs over the life of the investment project are then weighed against

a series of economic benefits generated by incremental vehicle traffic resulting from the

reduction in transportation costs and travel time. The results constitute the total

economic net benefits, from which a recommended program of investments will be

derived.

4

Sensitivity and risk analyses of the investment potential of the recommended

passes are also provided, demonstrating the expected effect of important variables.

The report is organized as follows: Section 2 presents the analytical approach and

framework of the public sector investment program. Section 3 discusses economic

growth and its relationship to trade flows among countries over the life of the project.

Details of economic costs and benefits are presented in Section 4. Section 5 presents

empirical results of the economic appraisal and the recommended program of

investments. Distributive benefits by country and sector of the economy are provided in

Section 6. Section 7 presents fiscal implications for the governments of Argentina and

Chile, respectively. Section 8 provides the outcome of the sensitivity and risk analyses

for key variables in the projects. Conclusions are summarized in the final section.

5

2 ANALYTICAL FRAMEWORK

The Andean High Pass Program will be evaluated as a pure public sector

infrastructure investment. Since each pass crosses the territory of Argentina to Chile, it is

considered a bi-national investment. Each investment may affect not only the economies

of Argentina and Chile, but also those of other countries, especially countries located in

the lower half of South America. Since the Program is a public sector investment, the focus of the analysis will be

on economic evaluation. The analysis is organized around the two major stakeholders in

the project: Argentinean residents and Chilean residents. Each pass is constructed jointly

by the Argentinean and Chilean governments, but the economic costs and benefits are

estimated separately for Argentina, Chile and the rest of the world.

2.1 Program Description and Strategic Options

There were 13 passes under initial consideration in the Andean Highway Pass

Program. As of the completion of this report, decisions on whether or not to proceed with

construction on several passes have been made. The Technical Group agreed not to

improve the Coihaique pass, while it has already begun construction of the Cardenal

Samore pass, which is expected to be fully paved by the end of 1998. Once completed,

the pass should serve both light and heavy vehicles throughout the year. Current capital

expenditures on the Cardenal Samore pass will not be included in the program, but are

considered part of the “do nothing” scenario under the evaluation.

The remaining 11 passes may all be paved. Some passes, such as the Sico, San

Francisco, Pircas Nigra and Huemules, may be coated with gravel rather than paved.

Capital investment for covering with gravel is less than for paving. The amount of annual

maintenance costs, however, may well be more for gravel than for paving.

In the initial analysis, all passes are assumed to be paved. In cases where

empirical results show paving to be economically unfeasible, alternative gravel roads will

be considered. The length of time and the expected investment costs for each pass,

expressed in 1998 prices, are provided for Argentina and Chile, in Table 2-1. The cost

6

estimates are for paved roads. One can calculate the capital expenditures per kilometer to

see whether one pass is more expensive than another.

It may be noted that there are no capital expenditures associated with the paving

of the Chilean side of the Cristo Redentor and Huemules passes. For the Cristo Redentor

pass, the Chilean side is already paved. The Huemules pass is entirely within Argentina.

It is of interest only to Argentina and all the expenditures would be incurred by the

Argentinean government.

Table 2-1 Length and Investment Cost of Passes

Name of Distance Capital Costs

Pass Argentina Chile Total Argentina Chile Total (km) (thousands of US dollars) Jama 255 156 441 50,816 54,000 104,816

Sico 266 217 483 59,078 59,241 118,319 San Francisco 199 260 459 36,522 45,355 81,877 Pricas Negras 186 200 386 73,136 59,000 132,136

Agua Negra 91 149 240 50,327 31,500 81,827 Cristo Redentor 134 66 200 42,091 0 42,091 Pehuenche 76 173 249 32,528 32,900 65,428 Pino Hachado 53 179 232 6,686 15,400 22,086 Huemules 134 46 180 37,708 0 37,708 Integración Austr 54 43 97 19,786 4,256 24,042 San Sebastián 13 161 174 3,319 42,665 45,984

The maintenance costs required for the passes depend upon several factors, such

as the type of pass, the height and curve of the pass, and the type of snow removal to be

used. Because paved road is considered first in the study, we present the annual

maintenance costs for paved road in Table 2-2. The costs include wages; salaries;

materials such as asphalt, gravel, cement, fuel, lubricants, and steel; rental of equipment,

and other.

7

Table 2-2 Annual Maintenance Costs of Each Pass

(thousands of 1998 US dollars)

Name of Pass Argentina Chile Total Jama 340 188 528

Sico 356 261 617 San Francisco 308 368 676 Pricas Negras 273 224 497

Agua Negra 269 417 687 Cristo Redentor 296 136 433 Pehuenche 156 317 473 Pino Hachado 88 276 364 Huemules 180 56 235 Integración Austr 93 59 151 San Sebastián 22 249 271

When each pass is considered, one must assess the substitution and

complementary effects of the particular investment on the traffic and on the economy. If

there is a substitution effect, then the incremental effect of the investment on the pass in

question should be less than its independent effect. Presumably, the pass competes with

existing passes, and the net incremental economic benefits should therefore be smaller

than if the pass were evaluated on its own.

To the contrary, if there is a complementary effect from improving the pass, the

incremental impact of the investment on traffic and on the economy should be greater

than if the impact of the pass is assessed independently.

Out of the 11 passes, five have been studied in depth by the technical group of the

Program and expected to be constructed sooner than the others. These passes - Jama,

Agua Negra, Cristo Redentor, Pehuenche, and Integracion Austral, will each be evaluated

for economic feasibility, and a determination will be made on when to begin

construction.

The remaining six passes will be considered in the future, pending the evaluation

of analytical results.

8

2.2 Analytical Approach

Since no toll will be charged for the newly paved passes, and there will be no

financial revenue from the investments, there will be no traditional financial appraisal of

this program. However, there will be fiscal implications of this public sector investment

for the governments of Argentina and Chile.

The economic appraisal will assess the program in terms of its economic impact.

Since each pass represents a joint investment by Argentina and Chile, the net economic

benefits should accrue principally to the residents of Argentina and Chile, but also to the

rest of southern Latin America. While the benefits to individual countries are an

important concern, the total benefit to the region should be the prime consideration for

investment decision-making.

In this analysis, each pass will first be assessed independently in economic terms.

The individual assessments will then be followed by an evaluation of the combined

passes and recommended investments for the Program.

9

3 The Macroeconomic Environment

3.1 Introduction

The key determinants for the economic appraisal of the Andean Pass Program are

the volumes of freight and passenger traffic and the costs of investment. Among the

important variables determining the level of traffic that is expected to benefit from the

passes are current levels of income, trade flows between Argentina, Chile and other

countries, and the future growth path of these variables. Due to the time value of money,

the levels of income, trade flows and their growth in the near future should have a much

bigger impact on the demand for highway services and the feasibility of the investment

than prospective income growth rates 10 to 20 years after the pass is improved.

Making a precise long-term macroeconomic forecast for different countries is

difficult and possibly unrealistic, because many unknown factors influence the

performance of the economy in question. This is especially true when the countries’

formerly highly protected economies are in the process of opening up to international

competition. In this situation, when the governments are launching major economic

policy initiatives, many factors can change prospects for economic growth rather

suddenly.

Given the history of volatile economic policies in these countries over the past 50

years, it is difficult to forecast with any degree of certainty future economic policies for

the region and the likely economic outcomes from these policies. Our model is designed

to address the forecasts and beliefs of the decision-makers which will be factors in

determining the future of the investment.

For the highway project, forecasts of the real gross domestic product for

Argentina, Chile, and other members of Mercosur may not be as important as the forecast

of trade flows among these countries. The growth in trade flows in the short run should

be highly dependent on both trade and real exchange rate policies. Over the longer run,

they should depend on the level of integration of the respective countries’ economies,

which reflects an equilibrium situation for them.

10

For an economic analysis, one needs to develop a series of scenarios in order to

understand the nature of economic outcomes of the project and to communicate these

interrelationships. To do this, one needs to develop forecasts of GDP that will serve as

the basis for the forecasts of demand for the services of the passes. In the analysis that

follows, the likely range of growth rates in these countries has been based on the

fundamental determinants of economic growth in the countries, tempered by the short-

term policy constraints they currently face.

3.2 Framework

Our analytical framework is based on the hypothesis that an increase in GDP can

be measured by the sum of the increase in factor incomes – real wage and capital income

– and a residual item that can be categorized as the reduction in real costs, or an increase

in factor productivity.1

To make a forecast of the economic growth rate of a country for the future, one

must obtain values for each of the above three components. These values must reflect not

only the past experiences of the country in question, but also its economic expectations

for the future. As one can expect, a reduction in real costs may be influenced by many

factors other than productivity. For example, major economic reforms and political

instability are not represented in the first two components, but they are certain to have an

effect on the economic growth of the country.

3.3 Empirical Results of Macroeconomic Growth Forecasts

In Appendix A, a detailed analytical framework is developed, and an empirical

estimation is made for construction of the bands of low, most likely and high growth rates

for Argentina and Chile. It is our conclusion that for Argentina, the range of growth rates

that fits these bands is 3, 4 and 5 percent, respectively. In the case of Chile, the growth

rates are expected to be higher. The corresponding ranges are 3.5, 5.0 and 6.5 percent,

respectively. For the purpose of this analysis, we assume that the annual growth rates for

Brazil, Paraguay and Bolivia will range from 3 to 5 percent.

11

The GDP growth forecasts, as well as the growth rates for the past several years,

are summarized in Table 3-1.

Table 3-1

Annual Growth Rates of Real GDP

Year Argentina Chile High Base Low High Base LowActual

1990 0.06 1991 8.90 7.30

1992 8.65 11.00 1993 6.03 6.30 1994 7.42 4.20 1995 -4.40 8.50 1996 4.25 7.20 Estimated*

1997 7.50 6.00

Forecast 1998 5.00 4.00 3.00 6.50 5.00 3.50 1999 5.00 4.00 3.00 6.50 5.00 3.50 2000 5.00 4.00 3.00 6.50 5.00 3.50 2010 5.00 4.00 3.00 6.50 5.00 3.50 2020 5.00 4.00 3.00 6.50 5.00 3.50

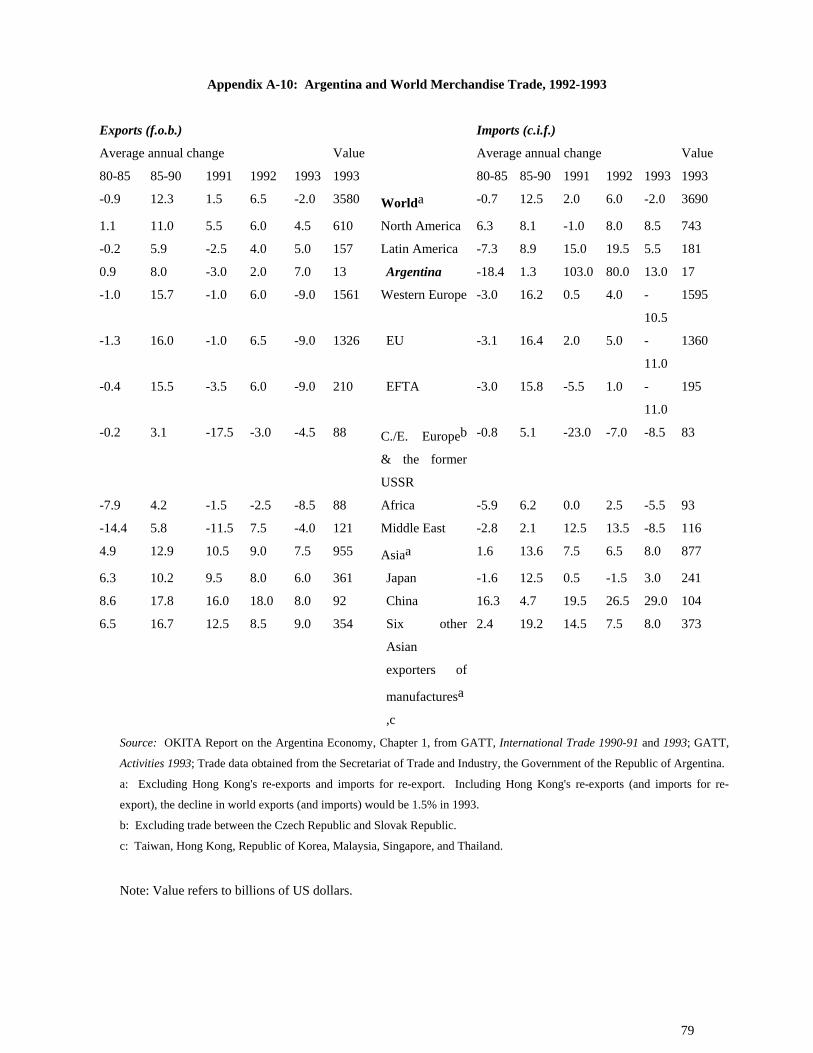

3.4 Trade Growth Forecasts and Trade Distribution

Trade is closely related to economic growth rates. Over the past two decades,

Chile has developed a relatively open economy. Several recent studies show us that the

aggregate trade elasticities relative GDP range from 1.01 to 1.82 for exports and from

1.07 to 1.74 for imports2, respectively. For the purpose of this study, we are assuming

that the trade elasticities for exports and imports are 1.75 over the next 10 years and 1.50

in the remaining years of the Program, for both Argentina and Chile.

At present, Argentina engages in a significant amount of trade with the rest of the

Mercosur members and the European countries. We expect there to be a slight shift in

terms of percentage distributions of trade to Asia and members of North American Free

1 Details can be found in Arnold C. Harberger, “Reflections on Economic Growth in Asia and the Pacific”, Journal of Asian

Economics, (1996). 2 See Appendix A, “The Macroeconomic Environment of the Andean Highway Passes Program”, Table 3.

12

Trade Agreement (NAFTA). The forecasts of such trade distribution flows between

Argentina and other countries or regions are displayed in Table 3.2.

Table 3.2

Argentinean Trade Distribution by Region (percentage)

Rest of Rest of South Rest of NAFTA Chile Mercosur America Europe Asia World

Exports 1994 12.6 6.0 29.1 5.3 25.2 8.4 13.4 1996 9.6 7.4 33.3 4.9 19.5 10.0 15.1 2010 14.0 8.0 34.0 4.0 19.0 12.0 9.0 2010 14.0 8.0 34.0 4.0 19.0 12.0 9.0 Imports 1994 23.3 3.6 22.5 1.6 31.6 10.3 7.1 1996 23.4 2.4 24.5 1.9 30.4 9.7 7.7 2010 24.0 4.0 26.0 1.0 29.0 11.0 5.0 2010 24.0 4.0 26.0 1.0 29.0 11.0 5.0

Chile’s major trading partners have been the countries of Europe and NAFTA.

Trade among these countries is expected to continue to grow. In the meantime, trade

between Chile and members of the Mercosur region is expected to be enhanced at the

expense of the rest of South America. Chilean trade with other countries and regions are

shown in Table 3.3.

Table 3.3

Chilean Trade Distribution by Region (percentage)

Rest of Rest of South Rest of NAFTA Argentina Mercosur America Europe Asia World

Exports 1994 19.5 5.4 6.1 6.6 24.4 15.8 22.1 1996 18.5 4.6 6.9 6.6 24.6 17.0 21.8 2010 20.0 6.0 7.0 6.0 24.0 17.0 20.0 2010 20.0 6.0 7.0 6.0 24.0 17.0 20.0

13

Rest of Rest of South Rest of NAFTA Argentina Mercosur America Europe Asia World

Imports 1994 27.4 8.3 9.5 4.9 22.9 9.6 17.4 1996 31.4 9.4 6.8 5.3 21.7 10.5 14.9 2010 31.0 10.0 9.0 5.0 21.0 12.0 12.0 2010 31.0 10.0 9.0 5.0 21.0 12.0 12.0

3.5 Role of the Passes

As mentioned earlier, the demand for freight traffic is expected to be determined

by the magnitude of trade between Argentina, Chile and other countries. Once the passes

are improved, the relationship between Argentina, Chile and other members of the

Mercosur region should strengthened.

By the same token, but to a lesser extent, the improvement of passes should lower

transportation costs and enable passengers to have access to roads between Argentina and

Chile.

14

4 Economic Benefit and Cost s

4.1 Identification of Costs and Benefits

The measurement of economic benefits and costs is typically based on

information developed in the financial analysis from the total investment viewpoint.

However, there will not be a traditional financial analysis in this Program, because no

financial revenues will be generated by this public sector infrastructure investment.

In the economic appraisal, all the prices of goods and services used in the project

are measured in economic terms. Conversion factors, used to calculate economic prices

as a function of their financial values, are calculated for Argentina and Chile,

respectively. The economic price of foreign exchange, for example, differs in each

country from its market value because of a variety of distortions associated with the

markets for traded goods.

In the Andean highway Passes program, primary sources of economic benefit are

generated by cargo and passenger traffic. Secondary benefits may arise due to taxes and

other distortions in the markets affected by the construction or maintenance of the passes,

but these should be small relative to the direct benefits arising from the traffic flow.

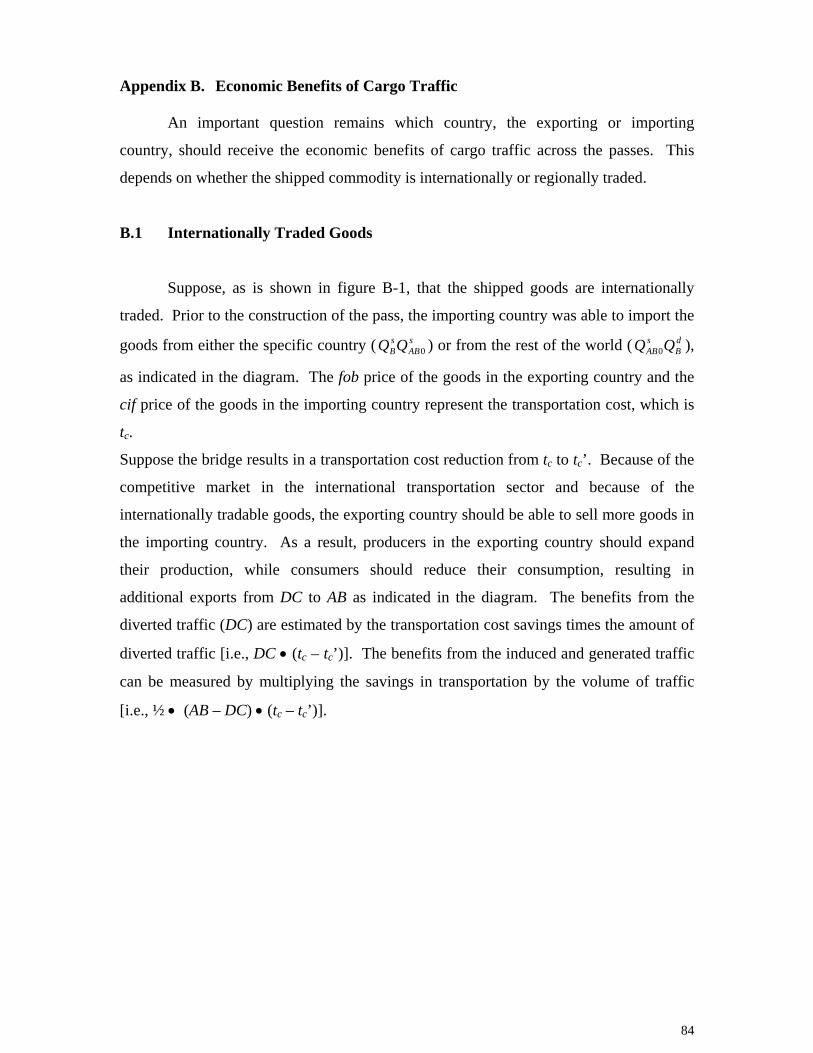

4.2 Economic Benefits from Cargo Traffic

The economic benefits from the cargo traffic on the pass are generated by savings

in transportation costs and logistic costs, including loading/unloading costs and waiting

time.

The cargo demand model is developed in such a way that receivers of freight

minimize the total delivered cost expressed per unit of product shipped. The model

provides calculations for a sample of actual shipments and picks the mode and route to

minimize the total landed cost. The transportation mode or route should change when the

cost of another mode or route becomes cheaper.

In the model, the most important variables for determining the total 15

transportation and logistics costs are distance traveled, waiting time to cross the border

(i.e., customs operations), fuel, labor and harbor loading/unloading (if any). It is the cost-

minimizing features of the model that determine the volume of traffic that will be

diverted and generated by improvement of the passes. The growth in traffic over time is

determined by the growth in international trade in the region.

Demand and total transportation cost savings have been determined in another

module of this study. The important question in this regard is whether the exporting or

importing country is receiving the economic benefits of cargo traffic across the passes.

When the commodity is internationally traded with third countries by the importing

country, the cost savings from the reduction in transportation costs should accrue to the

producers in the exporting country, because the goods can continue to be sold in the

importing country at prices based on world prices. A detailed explanation of these

fundamental relationships is presented in Appendix B.

In terms of measurement, the benefits for diverted traffic are equal to the

reduction in transportation costs times the volume of diverted traffic. For induced and

generated traffic, the benefits are equal to one half of the transportation cost savings

mulplitied by the traffic volume.

If goods are not internationally traded but mainly imported from the exporting

country in the Mercosur region, the benefits resulting from transportation cost reductions

should be shared by producers of the exporting country and consumers of the importing

country, depending upon the magnitude of demand elasticity for imports and supply

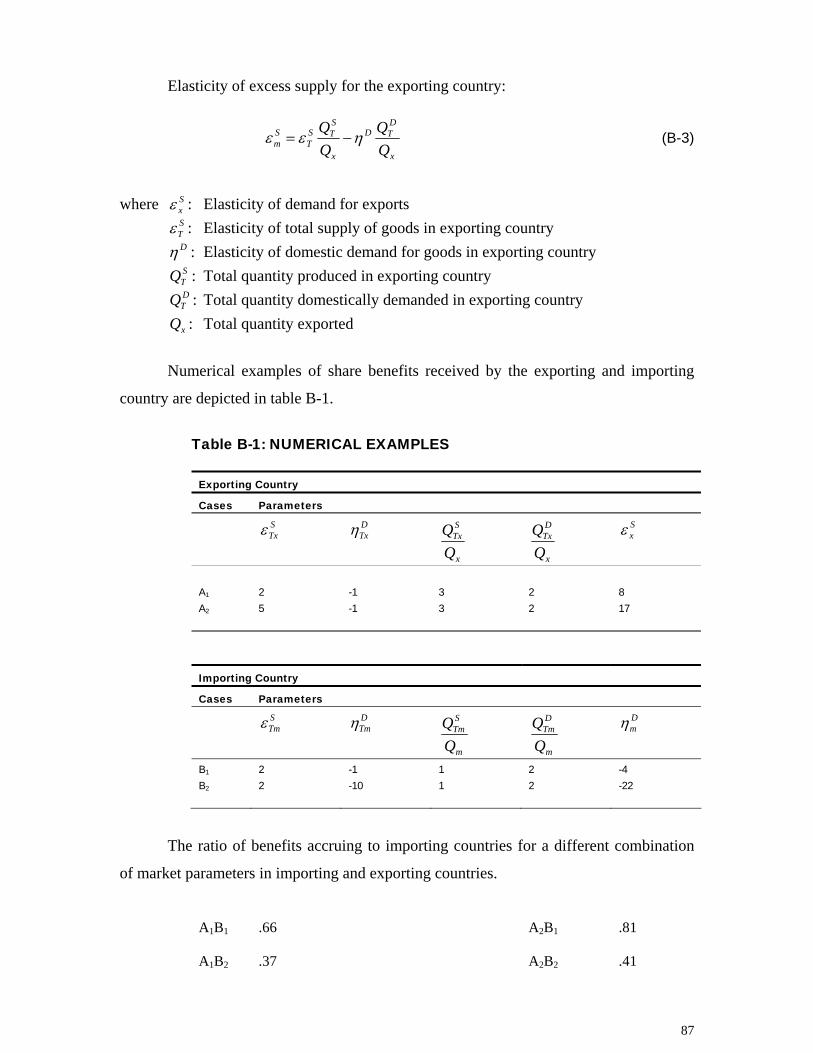

elasticity for exports. The share of benefits received by importing country (λ) can be

measured by:

λ = εsx/[εs

x - ηdx]

where εsx refers to the elasticity of supply of exports from the exporting country and ηd

x

refers to the elasticity of demand for the same commodity from the perspective of the

importing country. (See Appendix B.)

16

Appendix B also reveals that the share of benefits received by the importing

country ranges from 37% to 81% of the total. We can reasonably assume that benefits

resulting from savings in transportation costs should be shared equally by importing and

exporting countries. However, for the purpose of this analysis, all commodities imported

by Argentina and Chile are considered to be internationally traded.

In terms of measurement, the benefits for diverted traffic are measured by the

amount of savings in transportation costs times the traffic. For induced and generated

traffic, the benefits are estimated by multiplying one half of the transportation cost

reduction by the incremental traffic.

Having laid out the basic principles for measuring economic benefits, some

shipments of cargo should receive special attention:

• An incremental shipment from Asia or NAFTA to Argentina via the passes.

Because of transportation cost reductions, cost savings should accrue to

consumers in Argentina, not to producers in the exporting countries of Asia or

NAFTA. This is due to the fact that the exporting country can continue to sell

products at prices based on international prices and that, the prices of goods sold

in the importing country could be lowered to commensurate with the reduction in

transportation costs. Therefore, consumers in Chile should not receive benefits

directly in terms of lower-priced imports, but economic activities in the

transportation and port sector should increase.

• An incremental shipment from Asia or NAFTA to Paraguay, Bolivia or Brazil via

the passes. By the principle outlined above, benefits should accrue to consumers

in the importing countries.

• An incremental shipment originating in Argentina, Paraguay, Bolivia or Brazil

going to Asia or NAFTA. The benefits should accrue to producers in the

exporting countries.

17• A shipment originating and terminating in the same country (either

Argentina or Chile): Although the benefits resulting from savings in

transportation costs should ideally be shared equally by the importing and

exporting regions, in practice they will probably be spread unevenly among the

various countries. This will be true for some of the improved passes.

4.3 Economic Benefits for Passengers

At the present time, passengers between Argentina and Chile travel primarily by

car or plane. The economic benefits of diverted and induced passenger traffic are

measured by savings in vehicle operating costs and in time savings gained through use of

the improved passes, as well as by the value of any taxes or distortions associated with

vehicle and time costs incurred to use the passes.

In addition, lost or gained tax revenue associated with foregone operating costs

(because of the reduction in activity of the alternative modes due to the quantity of traffic

diverted to the pass) is accounted for in the analysis.

4.4 Other Economic Benefits

In addition to the economic benefits for cargo and passenger traffic, one has to

identify the project’s externalities by subtracting the financial costs from the real

economic costs. The analysis considers the benefits that Argentina and Chile should

receive from the sale of goods and services to the project in exchange for resources

generated by producing those goods and services, including the benefits and costs of

using foreign exchange, labor and other business inputs that can be expressed in

conversion factors.

In the economic analysis, the benefits and costs are expressed in U.S. dollars. The

net present value (NPV) of the net economic benefits of the project will be the criteria

used for decision-making and ranking of the investment potential of the various passes.

To calculate the NPV of the economic benefits and costs of the highway project, the

respective economic costs of capital for Argentina and Chile are employed. These

18

parameters are used to discount a series of economic benefits and costs over the life of

the project.

4.5 Economic Costs of Capital and Foreign Exchange

The economic cost of capital is determined as a weighted average of the foregone

consumption, the gross-of-tax returns on domestic investment, and the marginal costs of

foreign borrowing. This parameter is used to discount the net economic benefit stream

arising from investment in the passes in order to derive the economic net present value

for each country. The economic cost of capital is assumed to be 12 percent real for

Argentina and Chile.3

The economic cost of foreign exchange is calculated in Appendix C. The

economic cost of foreign exchange in 1998 to date is 10.88% higher than the official

exchange rate in Argentina and 15% higher than the rate Chile. This foreign exchange

premium is due in part to the impact of net import tariffs and value added taxes. The

premium for Argentina should slightly decline over time until 2001 because of the

Mercosur Treaty and the global trade liberalization. In the case of Chile, the foreign

exchange premium should depend upon future trade and tax policies. Free trade with

either Mercosur or NAFTA calls for a reduction in import tariffs and should lower the

foreign exchange premium. However, in order to have revenue-neutrality in the public

sector budget, the reduction of import duties should lead to an increase in indirect taxes

levied on domestic consumption of goods and services, thereby raising the foreign

exchange premium. Therefore, the foreign exchange premium used in the evaluation of

this Program is approximately 15%.

4.6 Economic Costs of Labor, Tradable and Non-Tradable Inputs

Investment and operating cost components consist of individual item costs such as

labor, tradable machinery, equipment and material, and non-tradable goods. The

conversion factors for these individual items must be calculated, so that their financial

193 From the Inter-American Development Bank in the terms of the contract.

costs can be translated to reflect the economic prices of business inputs and so that the

associated distortions can be quantified.

Economic Cost of Labor

The economic cost of labor for the project varies by type of skill required and by

type of labor market. There are three skill levels of construction worker required for the

project during the two to three years of construction. Similarly, there are three types of

operating worker required over the life of the operating/maintenance phase.

There are competitive labor markets in Argentina and Chile. This analysis uses

the private price of labor to induce people to work for a project as the fundamental

determinant of the economic cost of labor.4 It is then adjusted for any gain or loss in

taxes and social security contributions paid to the government, exclusive of any direct

pension benefits gained by workers upon their retirement.

The assumptions and calculation of the economic cost of labor can be found in

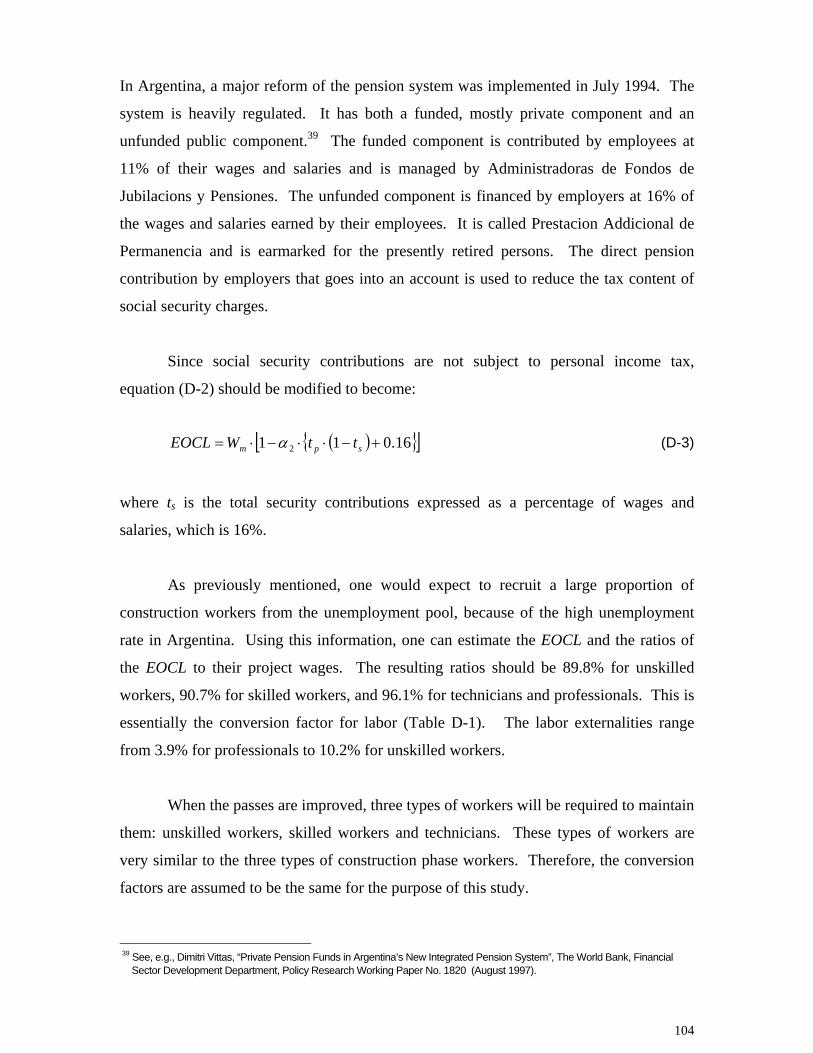

Appendix D. The results indicate that the economic cost of labor is approximately 96%

of the wage bill for professionals, 91% for skilled and 90% for unskilled workers in

Argentina and Chile. In other words, the net labor externalities from employment in this

program would be 4% of the wages for professionals, 9% for skilled and 10% for

unskilled workers.

Economic Cost of Tradable Inputs

During the construction period of the highway project, all machinery and

equipment or rented property used in the project are considered tradable inputs. Thus, the

financial price of each input should be adjusted for the foreign exchange premium. For

example, the foreign exchange premium for Chile in 1998 was estimated to be 15%. The

20

conversion factor for tradable inputs is equivalent to 0.878, because imports in Chile are

all subject to an 11% tariff, an 18% value-added tax, and a 15% foreign exchange

premium. Thus, the economic price for tradable inputs such as steel is 12.2% lower than

the financial cost.

All of the conversion factors for tradable inputs used in the operational period of

the highway passes are calculated for both Argentina and Chile. These items including

fuels, lubricants and tires are related mainly to vehicle maintenance costs. They are

adjusted for the foreign exchange premium, tariff and value added tax. For example,

gasoline in Argentina is subject to a 70% excise tax and 21% of the VAT rate. Its

conversion factor for 1998 is equal to 0.5390 [=(1/((1.7)*(1.21)))*(1.1088)]. For diesel

fuel, it is 0.689. For Chile, the conversion factor for gasoline is estimated at 0.6968 and

for diesel, at 0.6124.

Details can be found in Appendix E.

Economic Cost of Non-Tradable Inputs

In the case of non-tradable goods, the economic cost is estimated as a weighted

average of the value of the resources used in the production of additional supply and the

value of consumption foregone by the existing demand. For the purpose of this study, we

assume an equal weight for demand and supply. For example, the conversion factor for

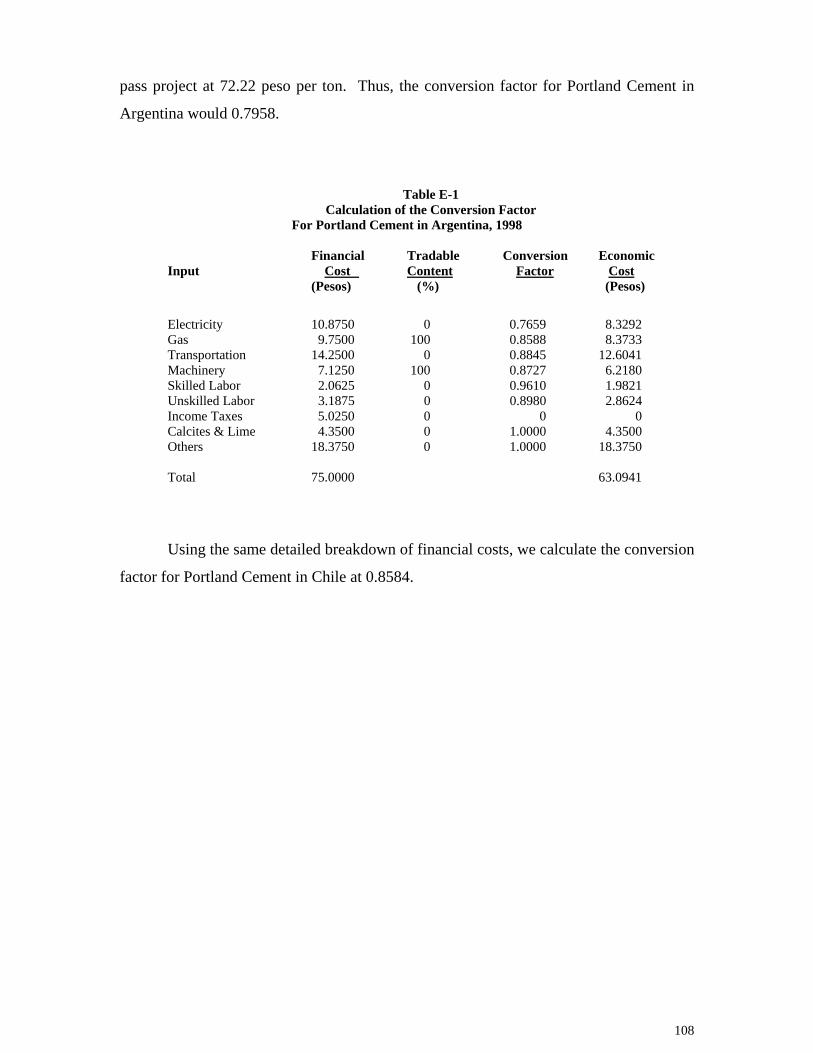

Portland cement would be 0.7958 for Argentina and 0.8584 for Chile.

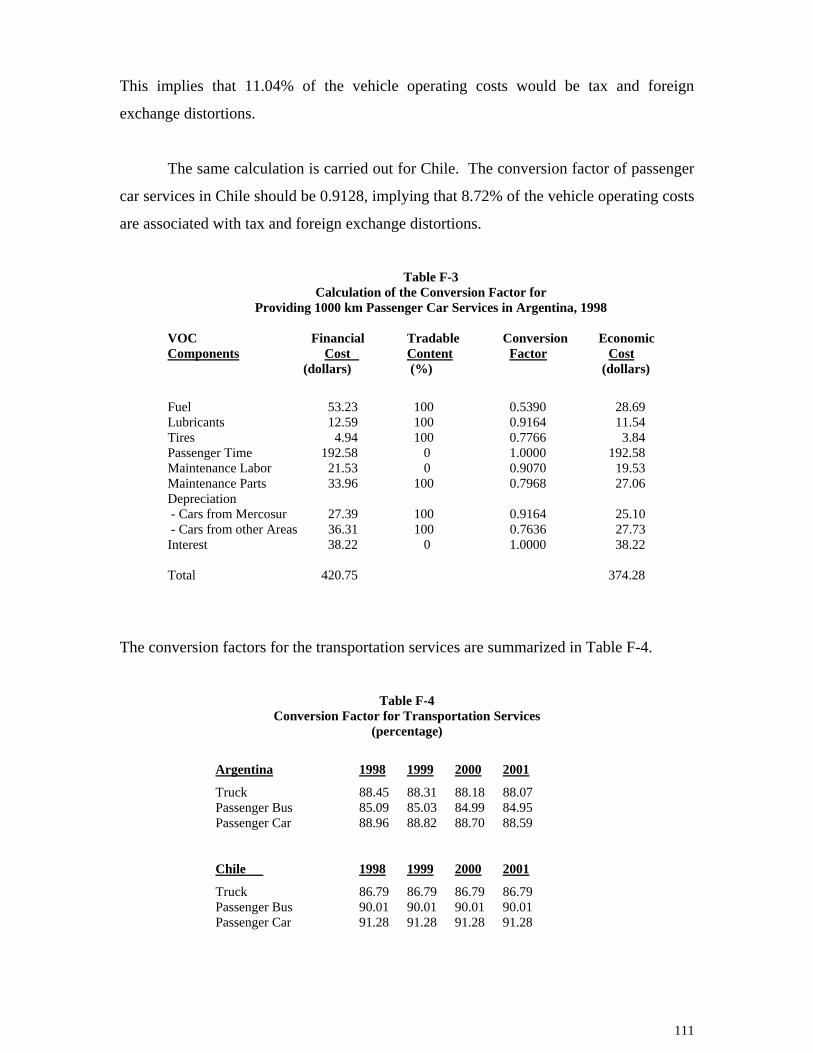

4.7 Economic Cost of Transportation Services

Transportation services are major inputs for the highway project. The calculation

of conversion factors for passenger cars, passenger buses and truck transport are based on

a detailed breakdown of vehicle operating financial costs per 1,000 vehicle km. They are

0.8896, 0.8509, and 0.8845, respectively, for Argentina. The corresponding figures for

Chile are 0.9128, 0.9001, and 0.8679, respectively. (See Appendix F.)

21

4 See A. C. Harberger, “On the Social Opportunity Cost of Labor”, in Project Evaluation: Collected Papers, (Chicago: University of

Chicago Press, 1972); and A. C. Harberger, “The Social Opportunity Cost of Labour, Problems of Concept and Measurement as

5 Economic Appraisal of Alternative Passes

5.1 Introduction and Methodology

The economic appraisal of an investment focuses on the economic costs and

benefits of the investment for participating countries. To achieve this objective, the

financial costs incurred in the project have to be converted into economic costs, which

will affect the economy of the countries. In addition, there should be an accounting of

the net economic benefits generated specifically from changes in the demand for cargo

and passenger traffic.

As previously discussed, the highway project is expected to have a direct impact

on the economy of Argentina and Chile and an indirect effect on Brazil, Paraguay,

Bolivia and Uruguay. In this section, the economic appraisal will focus on the total net

economic benefits of a specific investment in the region rather than on the benefits

accruing to the individual economies of Argentina and Chile. The distributive benefits of

the investment will be covered in the next section.

The economic principles developed in the field of welfare economics are utilized

extensively in this highway project. In the economic analysis, all prices are measured in

economic terms. Conversion factors, used to calculate economic prices as a function of

their financial values, were calculated in Section 4 for Argentina and Chile, respectively.

Resources used over the life of the project are all expressed in economic prices. In

addition, the economic benefits generated from changes in cargo and passenger traffic as

a result of savings in transportation are taken into account in the overall economic

appraisal of the specific investments in question.

The present value of the total net economic benefits of the investment will be the

principal criterion for the determination of the recommended investments in this

Program.

Seen from a Canadian Perspective”, paper prepared for the Task Force on Labour Market Development, the Government of

22

5.2 Analysis of Individual Passes

As mentioned in Section 2, the Cardenal Samoré pass is currently being paved on

the Argentinean side and will be fully paved by the end of 1998. The Chilean

government plans to pave access to the Pass on the Chilean side in order to complement

the work being undertaken on the Argentinean side. Since these works are all underway,

the capital expenditures for this pass are not considered part of the program of

investments. In other words, this pass is assumed to have been improved and is

considered as part of the “do nothing” scenario under the evaluation of this Program.

First, the capital investments of each pass are evaluated individually. The results,

presented in Table 5.1, show the combined economic benefits for Argentina, Chile and all

other countries of the investment from each pass individually. This is the incremental

economic benefit of each pass in addition to the improvement of the Cardenal Samoré

pass.

Construction on all passes is assumed to begin in 1999. The results are based on

the most likely economic growth scenario and a modest trade elasticity. That is, the

annual GDP growth rates are 5% for Chile and 4% for Argentina and the rest of southern

Latin America over the life of the project. The trade elasticity is 1.5 for exports and

imports for both Argentina and Chile.

Table 5.1

The Economic NPV of Each Pass For the Base Case Scenario

(thousands of 1998 US dollars)

Jama 86,678 Sico 80,571 San Francisco (589) Pircas Negras 8,905 Agua Negra 94,756 Cristo Redentor 55,420 Pehuenche 200,967 Pino Hachado 142,692 Huemules 2,219 Integración Austral 10,379 San Sebastian 15,545

23

Canada, (July 1981).

24

The ranking of individual passes in terms of combined economic benefits is:

Pehuenche, Pino Hachado, Agua Negra, Jama, Sico, Cristo Redentor, San Sebastián,

Integración Austral, Pircas Negras, Huemules and San Francisco. With the exception of

San Francisco, all the passes generate a positive net present value individually. This

means that the improvement of each pass (other than San Francisco), if evaluated in

isolation, would result in economic benefits.

Having said this, one should be aware that the above assessment may not be

totally accurate, because no substitute or complementary effects have been taken into

account. In other words, the ranking presented above may eventually be altered when

subsequent passes are considered.

5.3 Analysis of Combined Passes

Consideration of the substitute and complementary effects is vital when

subsequent passes are assessed for possible implementation. For example, the Pehuenche

and Pino Hachado passes were considered the best two passes individually, but if these

passes are improved at the same time, the total benefits (US$283,692 thousand) are

smaller than the sum of each individual passes (US$ 200,967 thousand plus US$142,692

thousand). This implies that these two passes are to some extent competitive pairs.

Another extreme example is that of Jama and Sico. Their net economic benefits

would be US$86,678 and US$80,571, respectively, if they were constructed

independently. However, if these two passes were improved simultaneously, the total net

benefits would be US$26,506, which is less than either pass by itself. This results from

two factors. First, there would be a marginal increase in traffic expected if both passes

were improved and opened, compared to opening one pass with more traffic. For

example, the total annual volume of trucks crossing Jama and Sico would be only slightly

greater than that of either Jama or Sico alone (i.e., 51,830 vs. 49,640 or 48,910 vehicles).

Similarly, the increase in the annual volume of passenger auto traffic would also be

marginal (i.e., 100,740 vs. 98,915 or 98,550 vehicles). This can be seen from the daily

traffic shown in Table 5.2 for the most likely economic growth scenario in

Table 5.2 Estimates of Total Demand for Vehicle Traffic Through Various Passes in 2010

-- With the Improvement of the Jama and Sico Passes -- (daily traffic)

Improvement of Jama Improvement of Sico Improvement of Jama and Sico

Trucks Buses Cars Total Trucks Buses Cars Total Trucks Buses Cars Total Jama 131 8 270 408 20 - 1 21 76 4 148 228 Sico 5 - 1 6 114 8 269 391 66 4 128 198 San Francisco - - 1 1 - - 1 1 - - 1 1 Picas Negras - - - - - - - - - - - - Agua Negra - - 14 14 - - 14 14 - - 14 14 Cristo Redentor 795 218 1,047 2,059 795 218 1,047 2,060 789 217 1,044 2,051 Rehuenche - - 2 2 - - 2 2 - - 2 2 Pino Hachado 28 7 59 94 28 7 59 94 28 7 59 94 Cardenal Samoré 79 39 525 643 79 39 525 643 79 39 525 643 Coihaique - 1 69 70 - 1 69 70 - 1 69 70 Huemules 18 1 50 69 18 1 50 69 18 1 50 69 Integracion Austral 119 23 387 529 119 23 387 529 119 23 387 529 San Sebastian 77 18 158 252 77 18 158 252 77 18 158 252 Total 1,251 318 2,581 4,147 1,249 315 2,582 4,145 1,251 314 2,584 4,150

the year 2010. Similar results are obtained for other years. Second, with virtually no

increase in traffic when the second pass is improved, all resources spent on the second

pass would be redundant and the total combined net economic benefits would decrease,

rather than increase.

Alternative pairs of competing passes are examined using the most likely

economic growth scenario and the year 1999 as the first year of construction. Included

are Jama vs. Sico, Pircas Nigras vs. San Francisco, Pehuenche vs. Cristo Redentor and

Pehuenche vs. Pico Hachado. There are considered competing because the total net

economic benefits resulting from the paving of the two passes are forecast to be less than

the sum of the net economic benefits from the two independent passes. These pairs have

varying degrees of competition. Some pairs are substantially independent, such as

Pehuenche and Cristo Redentor, and Pehuenche and Pino Hachado. The summary results

can be found in Table 5.3.

Table 5.3

The Economic NPV of the Competitive Passes For the Base Case Scenario

(thousands of 1998 US dollars)

Jama 86,678 Sico 80,571 Jama and Sico 26,506 Pircas Negras 8,905 San Francisco (589) Pircas Negras and San Francisco (43,983) Pehuenche 200,967 Cristo Redentor 55,420 Pehuenche and Cristo Redentor 190,036 Pehuenche 200,967 Pino Hachado 142,692 Pehuenche and Pino Hachado 283,692

To the contrary, some pairs of passes may be complementary in the sense that the

total net economic benefits resulting from the paving of the two passes should be

virtually the same or greater than the sum of the net economic benefits from the two

independent passes. The passes which fall into this category include the pairs of

Pehuenche vs. Agua Negra, Pehuenche vs. Jama, Pehuenche vs. Sico, Agua Negra vs.

Cristo Redentor, and Integración Austral vs. San Sebastián. Table 5.4 presents the net

economic benefits of these pairs, using the most likely economic growth scenario and the

year 1999 as the first year of construction.

Examining these pairs more closely, one discovers that most are geographically

distant, serving different markets. The exceptions are the pairs of Agua Negras vs. Cristo

Redentor and Integración Austral vs. San Sebastián. The former pair would serve the

highest levels of traffic between the central regions of Argentina and Chile. The latter

pair is basically additive, because one has to travel both passes in order to reach Tierra

del Fuego from Argentina.

Table 5.4 The Economic NPV of the Complementary Passes

For the Base Case Scenario (thousands of 1998 US dollars)

Pehuenche 200,967 Agua Negra 94,756 Pehuenche and Agua Negra 291,729 Pehuenche 200,967 Jama 86,678 Pehuenche and Jama 288,142 Pehuenche 200,967 Sico 80,571 Pehuenche and Sico 281,971 Agua Negra 94,756 Cristo Redentor 55,420 Agua Negra and Cristo Redentor 145,108 Integración Austral 10,379 San Sebastián 15,545 Integración Austral and San Sebastián 25,924

Other pairs are all independent of each other. The total net economic benefits

resulting from improvements to these pairs of passes are more or less additive compared

to the independent improvement of each pass.

28

5.4 Determination of the Recommended Investments

Argentina and Chile share a border of more than 5,000km, one of the longest in

the world. Because of the Andes Mountains, land transportation between the two

countries is limited. Strategically, an improvement of the northern, central and southern

blocks of passes could be mutually beneficial, because each block of passes serves

independent markets. Therefore, it would be practical to examine the economic impact

of the three blocks in isolation along with the above findings.

In each block, one should be mindful of the complementary pairs of passes

presented in the previous section. As indicated previously, the northern block pair of

Jama and Sico are competitive, serving the same markets, and passing through the same

harbor of Antofagasta. The improvement of Jama would result in greater incremental

economic benefits than the improvement of Sico and is therefore the best choice for

development. It should be noted that adding the Sico pass would result in a decrease in

the net economic benefits, because of the marginal increase in traffic.

In the central block, there are more passes to be considered, because of the

significant existing traffic and expected large future increase in traffic between Argentina

and Chile. Using the analytical results shown in the previous section, Pehuenche and

Cristo Redentor are good selections for improvement. This is reasonable because the

Cristo Redentor pass has already been paved on the Chilean side, and there is a

considerable volume of existing traffic. The construction of the Pehuenche pass should

divert some traffic from the Cristo Redentor pass because of its lower vehicle operating

costs and avoidance of interruptions caused by snow avalanches. The alignment of these

two passes would serve the highest levels of traffic between these two countries, resulting

in the most incremental economic net benefit of the investments.

The next pass to be improved in the central block might be either Pino Hachado

or Agua Negra. The rationale for improving Pino Hachado, on the one hand, reflects its

geographic independence from Cristo Redentor and on the other hand, its competition

with the Pehuenche pass, as pointed out in the previous section.

29

Table 5.6 Total Economic NPV of the Passes in the Central Block

For the Base Case Scenario (thousands of 1998 US dollars)

Pehuenche 200,967 Cristo Redentor 55,420 Pehuenche and Cristo Redentor 190,036 Pehuenche, Cristo Redentor and Agua Negra 281,683

The Agua Negra pass is by and large independent of the Pehuenche and Cristo

Redentor passes. The incremental economic net benefits to be gained by adding the

Agua Negra pass to the Pehuenche and Cristo Redentor passes should be greater than the

benefits of adding the Pino Hachado pass. Therefore, the Agua Negra pass should be

selected for paving prior to the Pino Hachado pass.

Next, consider the Pircas Negras and San Francisco passes. The incremental

benefits of adding either pass would be negative, especially San Francisco, which would

be expected to generate a negative return if improved independently. The alternative is to

improve the highway with gravel instead of paving. Nevertheless, the results still appear

to be unfeasible economically, even though the amount of total capital costs would

decline, because a gravel road would substantially reduce the volume of traffic compared

to a paved road.

Turning to the southern block, the choices are Integración Austral, San Sebastián,

and Huemules. Improving the Huemules pass should generate a marginal positive

economic benefit at the net present value of US$2.22 million over the life of the project,

since the traffic is mostly local within Chile, and its volumes would not be very large.

Nevertheless, the pass should permit the connection between Comodoro Revadavia in

Argentina and Puerto Chacabuco in Chile.

A comparison of the Integración Austral and San Sebastián passes indicates that

improving of the San Sebastian pass should generate a greater net benefit than improving

Integración Austral (i.e., US$15.5 million versus US$10.4 million). As indicated earlier,

these two passes are independent, and a passenger would need to travel both passes to

reach Tierra del Fuego from Argentina. As the Integración Austral pass was designed

30

well in advance of the San Sebastián pass, Integración Austral should be the first selected

for improvements in the southern block. The sequence of the highway investment in the

southern block should be Integración Austral, San Sebastián, and Huemules.

5.5 The Recommended Program of Investments

The above empirical results suggest that the passes with the most economic

benefits would include Jama in the north, Pehuenche, Cristo Redentor and Agua Negra in

the center, and Integracion Austral in the south. These five passes should be the first

paved, not only because they would generate the most economic net benefits but also

because they are substantially advanced in the design process. If these five passes are

constructed in 1999, the total economic net benefits could total approximately US$360.2

million in 1998 prices.

The subsequent paving in the Pino Hachado, San Sebastián and Huemules would

generate further positive net economic benefits in the region. Assuming that these three

passes are also improved beginning in 1999, the additional economic benefits would be

about US$101 million in 1998 prices.

In the case of the Sico, San Francisco and Pircas Negra passes, their paving would

produce a negative economic benefit. This is because the Sico pass is almost completely

competitive with the Jama pass, and the San Francisco pass is competitive with the Pircas

Negra pass. Therefore, they are not recommended for upgrading in 1999. Even if they

were covered with gravel instead of paved, the smaller amount of capital investment

necessary would still not be enough to generate a positive return, because of insufficient

volumes of traffic.

31

6 Distributional Impacts

The impacts presented so far are for the total net economic benefits to the region

as a whole. All passes cross the territories of Argentina and Chile, leading to other parts

of southern Latin America, including Brazil, Uruguay, and Bolivia. Each of them is

expected to have an impact on not only the economies of Argentina and Chile, but also

on other countries in southern Latin America as well. The investments should have an

impact on different sectors of the economy as well. This section of the report assesses

the impact of the recommended program of investments by country and by sector.

An analysis will be carried out for those passes, which are expected to produce a

positive net economic benefit for the region. We will present results for the first five

recommended passes, - Jama, Cristo Redentor, Pehuenche, Agua Negra, and Integración

Austral, - as a group. For the entire Program, we will also present results for all eight

passes as a whole, because the three additional passes, Pino Hachado, San Sebastián and

Huemules, should generate a positive net benefit.

For simplicity, we will present only results based on the most likely economic

growth scenario, starting in 1999.

6.1 Distribution by Countries

Most highway travelers in Argentina, Chile and other Latin American countries

are expected to choose the new passes over other highway routes. Changes from

alternative mode of transportation are not expected and are, therefore ignored for the

purpose of this analysis. The direct benefits for the passenger traffic, autos and buses

should reflect not only savings in traveling time and vehicle operating costs but also

improvements in reliability. All the benefits should be attributed to the passengers’

country of origin.

For cargo traffic, the improved passes should lower transportation and logistics

costs. Because of the competitive market in the international transportation sector and

because of international tradable goods, the exporting country should be able to sell more

32

goods to the importing country. Consequently, producers in the exporting country should

expand. Their operations for diverted traffic, benefits are calculated by multiplying the

reduction in transportation costs by the volume of diverted traffic. For induced and

generated traffic, the benefits are measured by multiplying one-half of the savings in

transportation costs by the volume of traffic.

As explained in the methodology section, for goods shipped from Asia or

NAFTA, benefits should accrue to consumers in the importing countries, because the

exported goods are expected to be sold at established international prices by the exporting

country.

For passenger traffic, all the benefits from the transportation cost savings accrue

to the travelers’ country of origin.

The above economic net benefits should be offset by the economic costs of

resources used for the project. These economic costs are measured in terms of economic

prices of capital goods and operating goods and services used in Argentina and Chile,

respectively. The conversion factors derived in the previous section for the economic

costs of labor, tradable and non-tradable business inputs, will be used to translate

financial costs into economic costs.

The streams of the above economic benefits and costs over the life of the project

should then be discounted by the economic cost of capital in the respective countries.

The economic cost of capital is assumed to be 12% real for both Argentina and Chile.

The economic net benefits for the two sets of recommended programs of

investments are presented in Table 6.1. These results are again based on the most likely

economic growth scenario, starting in 1999.

33

Table 6.1

The Economic NPV of Various Passes by Country For the Base Case Scenario

(thousands of 1998 US dollars)

Country Five Passes Eight Passes

Argentina 248,439 320,422 Chile 104,472 133,709 Rest of the World 7,295 7,297 Total 360,206 461,428

It is interesting to note that about 69% of the economic benefits should accrue to

Argentina. This is expected, because Argentina is either the exporting or importing

country for incremental shipments of goods as a result of the reduction in transportation

costs. Chile should receive 29% of the total economic net benefits due to the

enhancement of its trade relationships with Argentina and with other members of the

Mercosur region as a result of the improvements in the Andean highway passes.

In addition to Argentina and Chile, it is interesting to note that Brazil, Paraguay

and Bolivia should also benefit from the reduction in transportation costs once the

northern block of passes is paved. Their share of the total benefits should be slightly less

than 2%.

6.2 Distribution by Sectors

In addition to the distribution effects by country, one can distribute the net

benefits generated from the implementation of the project among the major sectors in the

economy. In this analysis, we have apportioned the net economic benefits of the project

among different sectors within each country.

The net economic benefits of this project are contributed by four sectors in the

economy, - producers, pass passengers, consumers and the government. Due to the

savings in cargo transportation costs, producers should experience expansion in

34

production and increased exports. Passengers should benefit, because of their access to

new and reliable passes and savings in vehicle transportation costs. Consumers should

benefit from an increase in the quantity of imported goods resulting from the reduction in

transportation costs and the cheaper imports.

The net benefits which are expected to accrue to the government should be from

externalities, including additional taxes generated, fewer taxes foregone, plus the foreign

exchange premiums associated with net changes in foreign exchange subtracted from

payments for construction and maintenance of the passes. There should be an

employment increase during the construction and the operating phase of the passes.

However, because of competitive labor markets in Argentina and Chile, the differences

between the economic and financial labor costs are expected to reflect income tax and

social security contribution adjustments and are therefore included as part of the benefits

or costs for the government.

The results for the base economic growth scenario are presented in Table 6.2. It

is clear that producers in Argentina are expected to gain the most as a result of the

reduction in transportation and logistics costs. Chilean producers should also gain,

although only about half of the amount gained by Argentina. Producers in Brazil,

Paraguay, Uruguay and Bolivia should gain because of their incremental exports to Chile,

Asia and NAFTA. Highway passengers, especially Argentineans, are expected to benefit

considering since they should have access to improved and reliable roads.

Consumers in both Argentina and Chile should gain because of increased imports

from each country, Asia, and NAFTA countries upon the implementation of the highway

project. The governments are expected to lose most because of the resources which will

be needed for the implementation of highway passes and because the amount of taxes

which will be foregone.

35

Table 6.2 Distributive Benefits and Costs of Various Passes

For the Base Case Scenario (thousands of 1998 US dollars)

Argentina Chile Other Countries Total

Five Passes

Producers 255,132 125,358 1,896 382,386 Passengers 94,671 29,225 3,848 127,744

Consumers 32,598 24,656 1,551 58,805 Government (133,962) (74,767) 0 (208,729)

Total 248,439 104,472 7,295 360,206

Eight Passes Producers 301,118 165,582 1,897 468,597 Passengers 130,429 38,348 3,848 172,625 Consumers 35,907 31,392 1,552 68,851 Governments (147,031) (101,612) 0 (248,643) Total 320,422 133,709 7,297 461,430

In summary, the net economic beneficiaries appear to be the producers and

highway vehicle passengers in both Argentina and Chile. The benefits, however, should

be realized only if Chile and Argentina work together to implement the Program.

36

7 Fiscal Impacts

7.1 Introduction

The Andean Highway Pass Program is a pure public sector infrastructure

investment and there will therefore be no financial appraisal of the investments.

Nevertheless, there are expected to be fiscal implications of the program for the

governments of Argentina and Chile. This section will quantify the fiscal implications of

the recommended program of investments for each of the countries.

7.2 Methodology and Key Assumptions

Over the life of the Program, the Argentinean and Chilean governments should be

responsible for construction and maintenance costs. There are expected to be issues of

financing which should arise as well. For example, all costs could be financed through

taxation or by various other means.

On the revenue side of the government sector, there should be fiscal implications

in terms of fuel taxes because of additional traffic, import duties and domestic sales taxes

associated with tradable and non-tradable goods used in the Program. This is in fact

nothing but the quantification of economic distortions that are used to determine the

conversion factors identified in the economic appraisal.

We assume that the prices of all goods and services purchased for this Program

will increase at the same rates as the general inflation rate. The real exchange rates in

Argentina and Chile are assumed to remain unchanged over the life of the Program, and

the domestic inflation in both countries is assumed to be the same as world inflation. It is

also assumed that the tax systems in Argentina, Chile and other southern Latin American

countries will remain unchanged over the life of the Program. The financial construction

and maintenance costs over the life of the Program are expressed in constant 1998 US

dollars.

37

7.3 Empirical Results

The fiscal implications of the recommended program of investments are shown in

Table 7.1. These figures are expressed in present value terms. In other words, the

streams of taxes and import duties over the life of the projects are discounted at 12% real.

For example, the implementation of the recommended five passes should increase

indirect taxes and import duties by approximately US$33.7 million for Argentina and by

US$23.7 million for Chile, respectively.

Table 7-1

Incremental Taxes and Import Duties Associated with Implementation of the Passes

(thousands of 1998 US dollars) Argentina Chile Total

Five Passes 33,735 23,740 57,475

Eight Passes 38,480 32,397 70,877

38

8 Sensitivity and Risk Analysis

8.1 Introduction

We have conducted a sensitivity analysis in order to identify the expected

variability in the project’s economic outcome, since the project’s outcome is based on

many forecasted variables. The analysis does not take into account the likely impact of

simultaneous and random changes in the values of project variables and the correlation

that may exist among them.

Risk analysis is applied to test the uncertainty surrounding important project

variables. The evaluation of project risk, therefore, depends on the ability to identify and

quantify the nature of the uncertainty surrounding the essential project variables and to

apply suitable statistical tools to measure the possibilities of their influence on the

project. The technique requires the specification of appropriate ranges of values and

probability distributions for the critical variables. Using the specified probability

distributions for the essential variables, a computer simulates the project’s economic

statements through a series of trials. The results from the simulation are used to obtain

estimates of the expected values and their probability distribution for selected outcomes

in the analysis.

In this report, a series of sensitivity and risk analyses are conducted to determine

the impact of changes in key variables on the economic net benefits of the highway

projects.

8.2 Methodology

In the appraisal of the highway program, a deterministic technique for the

sensitivity assessment is used first. In the analysis, the value of each variable is changed

one at a time in order to test its impact on the relevant outcome of the project. Sensivity

analysis allows us to identify the variables that should most likely affect the outcomes of

the highway project by quantifying the extent of their expected impact.

39

Risk analysis, using the Monte Carlo simulation technique, is applied to test how

the economic benefit of the project should respond to potentially significant variables. In

this analysis, 500 spreadsheet simulations are carried out for the traffic demand and

economic evaluation models.

8.3 Empirical Results

In this section, we conduct the sensitivity and risk analyses for changes in key

variables. For purposes of comparison, we report the results of sensitivity and risk

analyses deviating from the base scenario – (i.e. from the situation of most likely

economic growth rate and modest trade elasticity).

Sensitivity Analysis

The sensitivity analysis is carried out for economic growth rate, trade elasticity,

cost overruns and timing of implementation of the Program.

Economic Growth Rate

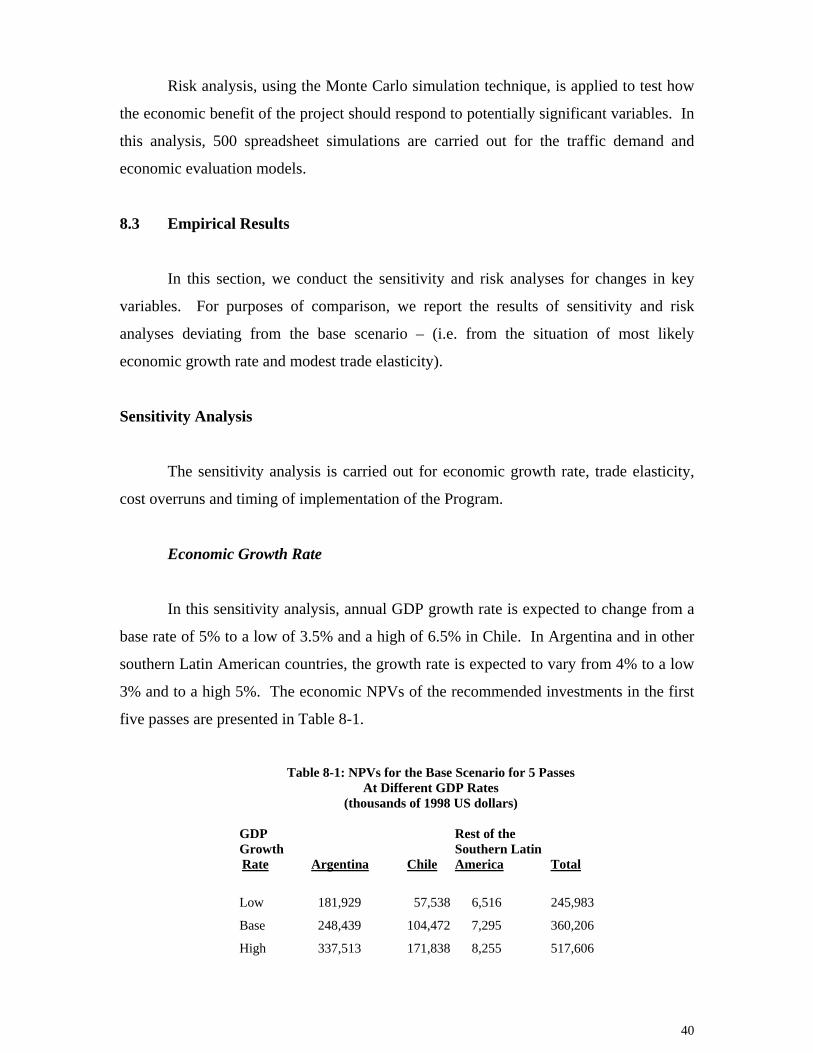

In this sensitivity analysis, annual GDP growth rate is expected to change from a

base rate of 5% to a low of 3.5% and a high of 6.5% in Chile. In Argentina and in other

southern Latin American countries, the growth rate is expected to vary from 4% to a low

3% and to a high 5%. The economic NPVs of the recommended investments in the first

five passes are presented in Table 8-1.

Table 8-1: NPVs for the Base Scenario for 5 Passes

At Different GDP Rates (thousands of 1998 US dollars)

GDP Rest of the Growth Southern Latin

Rate Argentina Chile America Total

Low 181,929 57,538 6,516 245,983

Base 248,439 104,472 7,295 360,206

High 337,513 171,838 8,255 517,606

40

The net economic benefits should increase in proportion to the GDP growth rates.

For example, the optimistic growth rate scenario should raise the levels of the net

economic benefits for both Argentina and Chile. In terms of percentage distribution of the

economic benefits between the countries, Chilean residents should gain more than

Argentinean residents, because annual GDP growth rates are expected to increase faster

in Chile (30% increase from 5%) than in Argentina (20% increase from 4%). On the

contrary, the pessimistic growth rate scenario is expected to raise the percentage

distribution of total net benefits for Argentina, because her GDP growth rates should not

decline as much as Chile’s.

Trade Elasticity

The import and export elasticities used in the demand model are assumed to be

1.5 for all commodities in Chile. In Argentina, the trade elasticity should range from 1 to

2, depending on the commodity. For the purpose of this analysis, the trade elasticity is

expected to vary by 20%. In other words, the low trade elasticities are assumed to be

80% of those used in the base scenario, while the high trade elasticities area assumed to

be 120% of the base ones. The economic NPVs of these simulations are presented in

Table 8-2.

Table 8-2: NPVs for the Base Scenario for 5 Passes

At Different Trade Elasticities (thousands of 1998 US dollars)

Rest of the Trade Southern Latin Elasticity Argentina Chile America Total

Low 197,170 70,936 6,772 274,878

Base 248,439 104,472 7,295 360,206

High 313,726 147,452 7,928 469,106

41

Trade elasticity also has a significant impact on net economic benefits. The

greater the trade elasticity, the more numerous the benefits that should be received by

Argentina, Chile and other southern Latin American countries. This is not surprising

because the greater level of trade should lead to a greater absolute response to changes in

prices for tradable goods.

Cost Overrun

The estimated costs for the program are based on the analysis of engineering

technical data at varying levels of detail for each pass. These estimates have been used as

the basis for the economic appraisal of the investment program. However, actual costs

could be higher or lower considering, the level of detail of the basic engineering studies

that have been conducted and the known physical conditions of the passes, including

topography and geo-technical conditions.

Considering the various factors affecting the risk of cost overruns, a range of

possible variation has been determined for each of the highway passes recommended for

improvement in the Program. The outer limits of the range are expressed in terms of

percentage variation from the expected value of the construction cost as shown in Table

8-3A.

Table 8-3A

Range of Variation of Construction Cost Estimates (percentage variation from expected Value)

Highway Pass Minimum Maximum

Jama -10.00 +20.00

Agua Negra -15.00 +30.00

Cristo Redentor -5.00 +10.00

Pehuenche -15.00 +30.00

Pino Hachado -10.00 +20.00

Huemules -10.00 +20.00

Integracion Austral -10.00 +20.00

San Sebastian -10.00 +20.00

42

This section examines the sensitivity of minimum and maximum capital costs on

economic viability. The results of these simulations are shown in Table 8-3B.

Table 8-3B: NPVs for the Base Scenario for 5 Passes

At Different Levels of Cost Overruns (thousands of 1998 US dollars)

Rest of the Capital South Latin Costs Argentina Chile America Total

Minimum Costs 264,367 117,189 7,295 388,851

Base 248,439 104,472 7,295 360,206

Maximum Costs 216,583 79,038 7,295 302,916

The economic NPV is expected to be affected by construction cost overruns.

However, the recommended program of investments in the five passes should remain

economically viable, even if cost overruns are high as 30% for all passes, because all the

benefits generated by the increased vehicle traffic should still remain intact.

Timing of the Project

In the analysis so far, the project has been assumed to begin construction in 1999.

In this section, we assume that the program will be delayed by one to two years. The

economic NPVs of these simulations are presented in Table 8-4.

Table 8-4: NPVs for the Base Scenario

At Different Beginning Years of Construction (thousands of 1998 US dollars)

Beginning Rest of the Construction South Latin Year Argentina Chile America Total

1999 248,439 104,472 7,295 360,206

2000 245,245 107,269 6,849 359,363

2001 240,733 108,798 6,424 355,955

43

The results indicate that there should be a reduction in the net economic NPV for

Argentina and other countries in southern Latin America, with the exception of Chile, if

the improvement of the five recommended passes is postponed for one year, because the

benefits generated by traffic will be lost forever, if the opening of the passes is delayed.

Risk Analysis

All the above analyses are based on deterministic values of input variables in the

model. This may not be a realistic assumption. The values of input variables should

vary, depending upon conditions in their respective markets. From the sensitivity

analysis, we found that the most important factors affecting the project’s economic

viability are GDP growth rates and trade elasticities. Cost overruns also affect the

present value of economic benefits, but to a lesser extent. Nevertheless, cost overruns are

always a concern to decision-makers. Therefore, we include these three variables in the

Monte Carlo risk analysis.

After risk variables are modeled, a set of Monte Carlo simulations is carried out.5

The analysis is conducted for the economic appraisal. The probabilities for GDP growth

rates are assumed to be 30, 40 and 30% for rates of 3.5%, 5% and 6.5%, respectively, for

Chile and for rates of 3%, 4% and 5% respectively, for Argentina and other southern

Latin American countries. The probabilities are assumed to be 30, 40 and 30% for the

low, medium and high elasticities. In the case of cost overruns, the probabilities are

calculated from the minimum and maximum ranges of construction cost estimates for

each pass (see Table 8-3A).

The outcome of the analysis is presented in Figure 8-1. The analysis shows that

there is no expectation of a negative economic net present value for the region. The

implementation of the recommended program of investments should significantly

improve the economic welfare of the residents in Argentina, Chile and the rest of

southern Latin America.

5 The risk analysis is done using the risk package called “Crystal Ball”.

44

Figure 8-1: ECONOMIC NPV FOR THE FIVE PASSES

(thousands of 1998 US$)

Summary:

Entire Range is from 171,574 to 738,608

500 Trials

Statistics:

Mean 388,696

Median 364,607

Standard Deviation 143,600

Range Minimum 171,574

Range Maximum 738,608

Cumulative Chart

.000

.250

.500

.750

1.000

0

125

250

375

500

150,000 300,000 450,000 600,000 750,000

500 Trials 0 Outliers

Forecast: Net Economic Benefits NPV

45

9 CONCLUSIONS

In this study, we have developed an analytical framework to evaluate various

passes in the Andean highway program and have suggested a recommended program of

investments. The recommendations reflect the economic net benefits expected for the

region of southern Latin America. The benefits forecast for the economies of Argentina,

Chile and the rest of the region as well as for different sectors of the economy are

presented in the report.

To evaluate the economic viability of the investment projects, we integrate the

engineering cost estimates, the conversion factors for translation from financial costs to

economic costs, and the forecasts of passenger and freight traffic into a stream of

economic costs and benefits over the life of the project. The traffic forecasting is based

on the model developed separately in this study. The traffic forecast, together with

vehicle transportation costs and time savings, are then translated into the measurement of

economic net benefits.

The main conclusions are summarized as follows:

• Ten of the 11 passes under consideration in the Andean highway program (with the

exception of San Francisco), when paved, should each make a positive contribution

to the economy of southern Latin America as a whole. The net present value for

economic benefits ranges from US$201 million (in 1998 prices) for the Pehuenche

pass to US$2.2 million for the Huemules pass. For the San Francisco pass, the net

present value is negative. In other words, from an economic point of view, this

pass should not be improved under the current program.

• Some passes compete with each other, since they serve the same market. Building

them simultaneously would result in a considerable reduction in net economic

benefits. These pairs of passes include: Jama and Sico, Pircas Negra and San

Francisco, Pehuenche and Cristo Redentor, and Pehuenche and Pino Hachado.

This is especially true in the case of Jama and Sico and Pircas Negra and San

Francisco.

46

• The empirical simulations suggest that the recommended program of investments

should include Jama, Pehuenche, Cristo Redentor, Agua Negra and Integracion.

They are expected to generate approximately US$360 million in present value of

net economic benefits, expressed in 1998 prices. These five passes would provide

the greatest economic net benefits, and they are considerably well advanced in

terms of planning. The subsequent investments in three additional passes, Pino

Hachado, San Sebastian and Huemules, should also generate a positive net present

value to the economy of the region. The remaining three passes are not expected to

contribute any economic benefits to the region.

• In terms of distributive benefits, approximately 69% of the economic benefits

should accrue to the economy of Argentina, 29% to the economy of Chile and 2%

to the rest of the southern Latin American countries. Producers in Argentina and

Chile should benefit the most from construction of the highway passes. Passengers

in both countries should also gain access to an improved highway system. The

governments of Argentina and Chile are expected to lose the most from a

government budget perspective, due to expenditures, which will be required for

improving this infrastructure.

• It is interesting to note that with substantial investments in the public sector

infrastructure, the governments of Argentina and Chile should receive taxes and

import duties associated with capital expenditures and maintenance costs in the

present value of US$33.7 million and US$23.7 million, respectively.

• The results of the economic analysis are sensitive to a number of variables such as

economic growth rates and trade elasticities. They are also affected by cost

overruns during the construction period. Nevertheless, with a maximum of 30%

cost overruns, the recommended program of investments should still generate a

considerable amount of economic benefit in the southern Latin America region as a

whole. It should also be noted that there is expected to be a reduction in economic

benefits if the construction of the recommended program of investments is

postponed, because of the associated loss in the value of transportation services

foregone through delay.

47

Appendix A. THE MACROECONOMIC FORECAST A.1 Introduction

A host of internal and external factors determines the economic growth prospects

of an economy. Each factor, by itself, is difficult to predict over a long period of time.

Furthermore, the prospects for future growth often change in the short-term, making the

business of long-term projections a challenging one.

This study uses a standard growth model, derived from a Cobb-Douglas

production function, to construct long-term projections for economic growth in Chile and