Embed Size (px)

Citation preview

AND PETROLEUM PRODUCTION

~9................................. sao,agA Uo!SaaAUOD pug S*!UYI ’saauaaajalI ’sUoI]g!AaaqqV

09 .............................................. k6-966t s.toanpo.tdl tunoio.ilOcI pus [e.~OU!l< I~dpu,~.tcIg

~......so.tv luotuu.toaoD ieao~I Aq ~t~no[o.tlod pu~ sls.tou,~lpV jo onieA pus Al~luen~3 ~

~> ............................................... so!a!pomtuoD .to{~IA[ po~aoiog jo onleA pu~. ~il!lu~n~g

99....................................................... mnolo.~lOd pu~ SlSaOu,~I~ jo onI~A pu~. Xl!lu~n{3[

{[......................... ~.*lsnpuI ~u,*u!~ oR1 ~u!laojjV s.tola~.d l~a~.l~,[OcI pu~ [~!aog

9 ............................................ ~.~lsnpuI ~u,~u!!N otI1 ~u!l,oojjV s.tola~I a!tuouoaE

~.......................... ituouoai~ u~!ie.~lsnV pu~. u~!i~.~lsnv u.~olSOA~ oql jo axo.~ao}I

~NIIiIIaINIORIANIR ~IVIDOS (INIV.[

(I~IOPA.~IIIO~I

LI T OF FIGUR

Figures

1.2

1.3

1.4

2.1

2.2

2.3

2.4

2.5

2.6

2,7

2.8

2.9

2.10

2.11

2.12

2.13

2.14

2.15

2.16

2.17

2.18

2.19

2.20

2.21

2.22

2.23

2.24

2.25

2.26

2.27

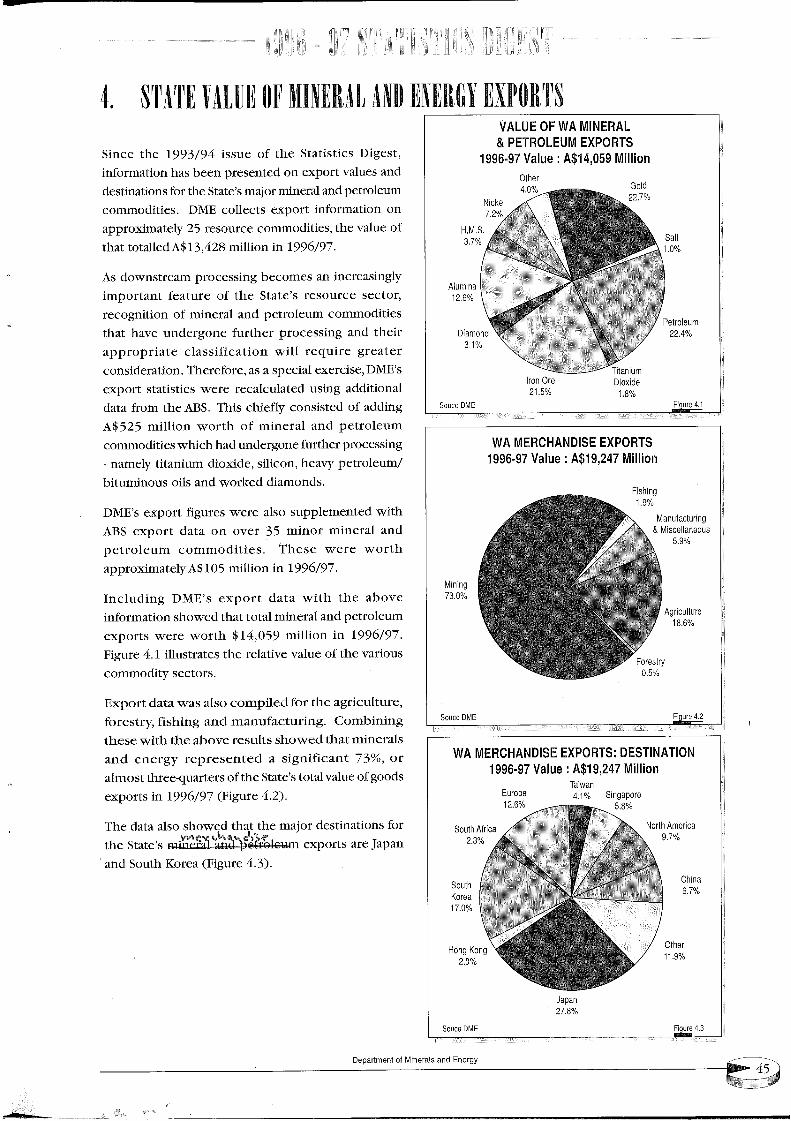

4.1

4.2

4.3

0.1

0,2

Page

Exchange Rate: AS/YEN .................................................................................5

Exchange Rate: A$/$US ..................................................................................5

Local Government Boundaries (map) ........................................................18

Major Mineral and Petroleum Projects in Western Australia ...................19

Petroleum Exports .........................................................................................21

Oil and Condensate: Quarterly Production & Value .................................21

Crude Oil and Condensate Production .......................................................21

Crude Oil Price ..............................................................................................22

Gold Quarterly Production & Value ............................................................23

Gold Production ............................................................................................24

Gold Exports ..................................................................................................24

Gold Price .....................................................................................................25

Cumulative Gold Production ........................................................................25

Iron Ore Quarterly Production & Value .....................................................27

Iron Ore Price ................................................................................................27

Iron Ore Production ......................................................................................28

Iron Ore Exports ............................................................................................28

Alumina Quarterly Production & Value ......................................................30

Alumina Production ......................................................................................30

Alumina Exports ............................................................................................31

Alumina Price .................................................................................................31

Nickel Quarterly Production & Value .........................................................32

Nickel Price ....................................................................................................33

Nickel Production ..............................................................~ ...........................33

Nickel Exports ................................................................................................33

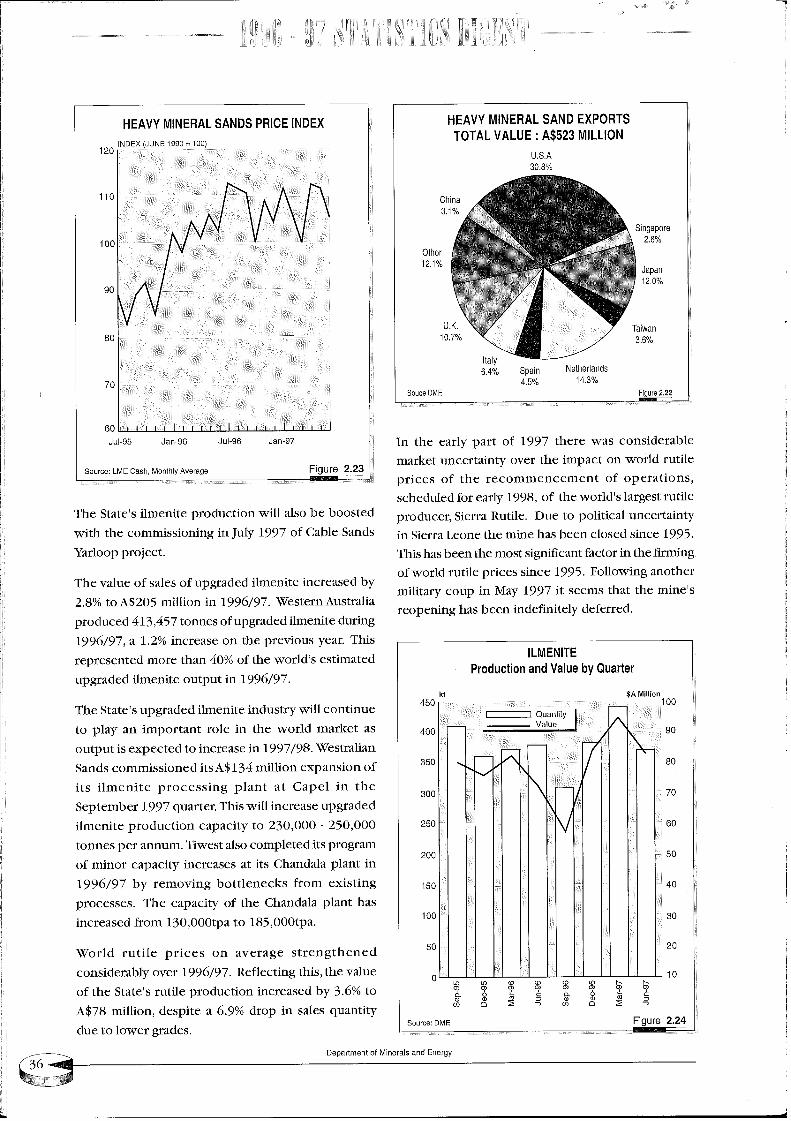

Heavy Mineral Sand Exports ........................................................................36

Heavy Mineral Sands Price Index ................................................................36

Ilmenite Quarterly Production & Value ......................................................36

IlInenite Production .......................................................................................37

Selected WA Mineral Commodities Relative to World Production ..........41

Estimates of Mineral & Petroleum Value of Production to Year 2000-01., 41

Value of WA Mineral and Petroleum Exports ............................................45

WA Merchandise Exports 1996-97 ...............................................................45

WA Merchandise Exports : Destination 1996-97 ........................................45

Comparative Value of Production - 1991-92 and 1996-97 ......................50

Comparative Royalty Receipts - 1991-92 and 1996 - 97 ...........................57

Department of Minerals and Energy

.~aX aa!gsaaans puoaas aql aoj

alms ~u!anpoad i!o lsa~a~I s,g!i~algnvs~ gnl~!g gl! pau!~laa s~q’XI~tg%*dans 1oN "UO!lanpoad X~aaua pu~ Faa .trgu jo anna s,al~lg

aaom sluasaadaa axou aolaas aq& u~aX ~ u.~ lanpoad jo uo!ii.,m 000’gSVU~q!

aaom aanpoad o! Xa!snptq lga!j g,al~!g aql a! ap~m g~q aolaas mnaloalad

a~ans panm.luoa aqa; ’a!~guaptloa pu~ s~ ’i!o aoj 1as spaoaaa uo!lanpoad

q!.~a~’k6/9661 u! palq~!Iq~!q m.~ s~at mnaloalad jo aaumaodm!

aolaag aao uoa! pue mnaloalad aql jo uo!lanpoad pu~ anFa aql m.ag~aaau! ~uoals aql ol alqmnq.~a!!~ Xlm.~m s~ax as!a aqj~ ’uo.q .lgU 00F9Iaaom m k6/966~ u! %/_ Xq asoa uo!lanpoadjo anFa aq~ "ql~uaalg Fuamouaqdgl.t pal~alsuomap u!~ aolaag saaanosaa s,~!i~alsn¥ uaa!SaA~ k6/966I u1

’al~lg aql uo la~dug.plno~ X!!a.~la~ a!mouoaa plao~ tL~ uanlu~op ao{etu ~ XlUO ’~u!ssaaoadmgaa!st~op pas~aaau.~ aoj i~!lualod aq! pu~ ’aoaaas saaanogaa g,al~!gjo XlFaaa!p XqlFaq aql uaa!~ aaaaaxoH "sla~ta~m X!.~pommoa u! sluamdolaaapIguo.~lguaalu! ol alq!ldaasns Xaaa aaojaaaql s.~ Xmouoaa aq! pug aolaasgaaanosaa sa.t jo tll~aoa~ panm.moa aql uo mapuadap s! Xmouoaa s,all~lg

¯ mamXoldma s,almg aql jo ’laaa!pu! pu~ laaa!p q!oq ’ql~.J auo punoa~ aojpalunoaag aolaag saaanosaa aql lgql pa!~a!p~q osI~ Xpn!s 96/g661 V ’luamlgaau~.Im!d~a al~a!ad jo %0g punoa~ pu~ glaodxa Sl.~ jo %05 ul~q! aaom ~lanpoad ssoaoa!~lg jo ’Xllaaa!pu! pu~ Xllaaa!p ’%0{ punoa~ .~o1 ~u.nunoaa~ ’Xmouoaa g,al~lgaql u!d.,apun ol panuBuoa aolaas saaanosaa aql k6/966I uI "Xmouoaa anool uo.~mq!amoa g!! 1o apnl!u~em aq! ~toolaaao ol pu~ maaNdmoa amoaaq olXs~a g.~ 1.~ ’.t~aX aalj~ a~aX’Xl~UOalS ~t .woa.IOjaad Xalsnpm. aaanosaa s, alglg aql q!.~A~

’s086I p!m aql moa~ aolaas aaanosaa lumaodm! ue s~ ~u!&~atua mnaloaladpu~ {s0g6I aql u! uo!lanpoad plo~ u! ag~aaau.~ a.~l~m~ap aql ’.g0k6I aql u!Xalgnpu.~ gu!tunF aql jo luamdolaaap panm.moa aql’.g096I algI aql m. uo!lanpoadia~tag~ pue aao uoa! jo la~ls aql Xq palq~!Iq~!q uaaq s~q attq111~ql aauF qlaxoa9¯ tunuu~ aad %l-I punoae jo a!~a a~aaa~ ue Xq ua~oa~ gl~q Xalsnpu! aaanosaa s,all~lgaq! jo uo!lanpoad jo anFa aq! ga~aX 0{ !gN aql aaao leq! alq~taemaa ~ s! 11

Tv~Ii/N.qD IlOKDRItI(Ipaoju~lt D ~I

IHOAAgHO

In September 1997 the Federal Government introduced the Native Title Bill1997 into the Federal Parliament. The Bill incorporates a number of amendmentswhich are designed to streamline the native title process to make it moreworkable. The outcome of the Native Title Bill is crucial to the long term futureof the industry in Western Australia. Unless we can achieve more workableprocedures there will be an inevitable decline in exploration with adverseconsequences for future mineral and petroleum production in this State.

The matters referred to above are described in some detail within this Digest.The information and statistics were assembled by the Department with assistancefrom the Australian Bureau of Statistics, Australian Bureau of Agricultural andResource Economics and resource companies. I thank these organisations fortheir cooperation and help; it would be impossible to present such acomprehensive pnblication without their assistance.

Lee RanfordDIRECTOR GENERAL

Department of Minerals and Energy

"8661 tu. %g’g ol %g punoae !~ lg~aaaoj g!qlmoao "86/L661 aaAo ttattl~t/aalg ii!~ uo!ldtunsuoa al~at.ad 1~ql pa!aadxa s! !I

’%I’Iol %g’g tuoaj lsBaaaoj qlmoa~ L661 sl! spJ~AXUAxop pas!aaa s~q ’sgalaqlauou’aI ’86//66I Jo jl~q lgat.J aq! ti! aaoadm! ’tIo!ldtunguoa al~a!ad ~lIOa!g jo ~Ia~qaql uo ’I1!~ Xtuouoaa asau~d~f attl saaa.qaq pun~I XamauolN FuoIl~UaaluI aq.l.

’86/L66I 5o JI~q asa~.J aq! m. panpqns m.~tuaa o1 suo!l!puoa ssau!snqaaadxa sa.m~duaoa 8tqama~snu~tu ~!q 1~q! sa!~a!pu! luatu!luas ssam.snqso xapu!tI~)lU~j, aiD s~u!!!ag Aa.qod a.m~ouoaa luaaana s,lt~attruaaAoo aq! jo spa~axaaaql d~aa uoos Ilpa u~d~f 1~ql papnlauOa s~q (L66I aaqtualdag) Aaaans u~d~f5o }Iu~t ~ algtAk ’luatu!luas ssau!snq ~u!la~dtu! Alasaaap~ aa~ uo!lNn~aaapo! SaAOtU panu!ll~Oa sa! g~ IIa~a s~ g~U!alaS Aa!lod Fas!J lq~!t s,luatuuaaaoo aq~

"L6/9661 tq %I’S Xq axaa~ d(IO ’atuoamo aala~nb L661 d(IO aunfaood aql al!dsa(I ’uo!ldtunsuoa aa~a!ad tO. IF5 aql ao5 patu~Iq ~aaq s~q L66II!ad¥ u! %g o1%{ tuoaj xm uo!ldtunsuoa aq! tq as~aaau.~ aq~ ’uo!ldtunsuoaa!~a!ad pu~ luatulsaau! ~u!snoq pu~ ssau!gnq u! IFJ ~ ol anp AIa~aNatuoalno aqj~ ’~iaoqs l~.O lsa!5 g,plaoax aq! ~upaOllOJ ’#L6I 5o aalaenb lga!Jaau!s aan~!j qlmoa~ Alaaaa~nb !sao~ aq! s~ax %6"g sn .ugu jo atuoalno d(ID aq.l."m~p qlmoa8 a.mlouoaa L661 aalamtb aunf aql 5o as~alaa aql tI1!~ pa!~ao!aalapg~q ’la)Ia~tu aaodxa lga~a~I g,al~lg aql ’u~d~f ao5 )Ioollno a!tuouoaa aq.l~

¯ OlqV.moa#fa.~ o4oan~u.~ guo!l.~puoo o.~utouoo~

tunuu~ aad %9’g 5° ql~oa8 aSeaaa~ una-~uoIspaaaxa s!q~ "/66t u! %g’{ Xq axoa8 ol palaadxa s! Xtuouoaa aq~ "suo!l!puoapu~map a!lsatuop lu~Xonq Xq XI!aetut.ad uaa!ap ~u!aq tll~Oa8 ql!~ ’XI~UOalStuaosaad ol sanu!luoa Xu~ouoaa gfl aq! 1~ql lsa~ns saol~a!pu! a!tuouoaa

slaodxa X{~jatIa pu~ [~aauItU S,all~lg aql jo spJ!q! o~al ueql aaotu~twA. ~1 la)ta~tu laodxa lu~ .uguopaad g,al~lg aid gu!~tuaa l~!g¥ ’slaodxa I1~!ol jo %04tI~ttl aaotu aoj lunoaa~ ol anu!luoa slaodxa XSaaua pu~ Faau.rm g,a!~lg

’uo! .lIgU 00g’gISVpmto.t~ !~ pools gnldans ap~al as.~pu~qaaam s,a!~lS aql’sgal Allu~a~ .ffga~!s pa!aodttt!1! uaa!8 pu~ ’!anpoadso qlaoaX UO.qI~tU 0~g’6[ $¥palaodxa al~lg aq! 16/966I uI

’XlI~aaua8~!Falsnv ao5 u~q! suo!l!puoa a!tuouoaa pIaoax uo lu~!laa aaotu ’aaosaaaqlg!aadsoad ltlmoa~ aanlnj s,almg aqL ’~!Fa!snyaoj %gI punoa~ o! paa~dmoa ~*tuouoaa s,~!Falsnyuaaasa?ASo %�{ aoj palunoaa~ sl.todxa uS!aaoj/6/966I uI

cno.fao~I £u~ouoa~t pl.~odi I’I

¯ u.,#gaooun s., u~d~[aOf alOOflno o!zuouooa aqZ

’Vg;1 acfl aof sloodso.~4

qlmo,�R olq#.moat~d

"UO!ll!U¢ OO g’g l S V1~ snlc[.ms ap~2l s, og~gS

J A gWA OHIAA 9 IVI )OS IIA V )IWOA O )9 ’I

South East Asia currencyproblems createuncertainty in regionalgrowth.

Maastricht criteria for monetary union. In pursuing monetary union a numberof European Central Banks have been diversifying their investment portfoliosaway from gold. Their actions have placed considerable uncertainty on thegold price over the latter half of 1996/97.

Economic growth inWestern Europe is expected to rise from 1.4% in 1996 to2.2% in 1997. In 1998 growth is estimated at 2.5%.

Germany’s economy recorded moderate growth of 1.4% in 1996. GDP growthdata for the first half of 1997 suggests the economy is picking up. Businessinvestment and exports remain the main sources of growth but consumerspending remains weak. The German economy is expected to grow by 2.2%in 1997 rising to 2.8% in 1998.

The United Kingdom, now in its sixth year of economic expansion, isexperiencing higher than average economic growth. Growth of 3.2% isexpected for 1997, up from 2.1% in 1996. Consumer spending remains highon the basis of strong employment and rising incomes. Although inflationremained subdued over the first three quarters of 1996/97 the Bank of Englandincreased UK interest rates in response to early signs of accelerating pricegrowth in the June 1997 quarter. Growth of 2.7% is estimated in .1998.

In Eastern Europe, three major emerging market economies - Poland, CzechRepublic and Hungary- continued to benefit from market reforms, privatisationprograms, trade withWestern Europe and foreign investment. Average annualgrowth across these three countries continued in 1997 at around 4% to 4.5%.Growth of this magnitude can be expected to continue in the near future.

Russia’s economic downturn which commenced in the early 1990s is expectedto bottom out in 1997.The economy is expected to grow by around 2% in1998.

Economic activity continues to be dominated by export growth, underpinnedby increased global economic activity. Nonetheless, there is considerableuncertainty about the short term outlook for some Asian economies. Therehas been a sharp depreciation in the value of South East Asian currencies inthe September 1997 quarter and this is creating some problems in the region.The IMF is currently reassessing its role in the Asian region. It has indicatedthat it will step up its financial monitoring role to avoid further currencyturmoil in the region. "

Asian governments are having to adjust their economic policies in order toreduce current account imbalances and inflationary pressures.

On the whole, however, Asian growth has been quite strong. It is forecast ataround 7% in 1997 and 1998, somewhat lower than the 7.8% recorded in1996.

China’s growth for 1997 and 1998 is expected to remain at around its 1996level of 9.7%. Taiwan and Singapore are also estimated to grow by between6% and 7% in both 1997 and 1998. Hong Kong’s growth rate is estimated tostay around its 1996 level of 5% for both 1998 and 1999.

Department of Minerals and Energy

"ZO0~ o! ~’d %~’~ s! q!~oa~ pIJo~ jo ls~3aJoj mJal ra!!pare

ql~oa~ plao~ lg~aaaoj ggq (5661 aaqmaldag) punk Xamauo~ I~UOll~mamI

’9661 pue L661 qloq m. %g ol %0"~at lstaaaoj s! sdjjN s,altlg aql u! qa~oa~ a.mJouoa.q ’alqtanoAtJ aq Ol anm.luoa’slaodxa k6/9661 s,almg aql jo saalatnb-aaaql punoat aoj palunoaa~ qa!q~’(sdJJ~) sJau!al;d ~u!ptal gI .io{tm s,t.li~alsnvll.talsaAXti!, suo!l!pttoa a!ttlouoa}~

"uo!II!q I SgKl punoa~ aq lI~.~lgo.tlnq.t.IlUOa s,~!igalsnyXia:~..i s! 1F q!!~ papaaaoad JI ’~!sauopuI aoj punjanasaa ~ ~u!aap!suoa ogle aaa~ ~Iu~{{ plaopApu~ dINI aq! L66I aaqolao a!~I uI

put aaodg~u!g jo 1~ql sFnba t~o!II!q I $SFI to ~Jo!mq!aauoa s,~!Falsn¥ ’Xalunoaaaq!o Xug utql sam!l aaom anoj ’uo!Ii!q }$gLl ~u!lnq!amoa s! ~Jtdtf ’tto!ii!q9I SgFl ~u.qImoa punj anasaa t pas!u~ao s~q pranj XamauoIN I~UO!a~uaaluI’&ttouoaa aq! as!i!qms ol aapao uI "966I m. papaoaaa %5"9 aql moa1*a~aop’9661put 566I qloq u! %{ pu~ %g’g ~Jaa~alaq aq o! palaadxa s! q!~oa~ s,pu~p.~qj,¯ putI!eqj~ uo latdm! aaal~as Xia~ina!latd ~ p~q aa~tt smalqoad Xauaaana

’%I’9 1~ !staaaoj ql~oa~ ql!~ 866Im. uaq!~uaals ii!a~ ~{mouoaa aql ltql palaadxa s! !! ql~oa~ laodxaolu.~ saa!I!J tlOI.l.ISOd aa!!!ladmoa paaoadm! sl.t s¥ ’/66I u! %{’g Ol 966I u! %I’kmoat lI~J ol palaadxa s! ql~oa~ sl! ’maal laoqs aql u! uo!!~!aaadap XauaaJnas!! jo llnsaa t s~ aaoadm! o! palaadxa s! ssauaa!l!ladmoa s,taao~ qlnog aI!q?A

Australia’s and Western

Australia’s growth

moderated in 1996/9Z

State business investn2ent

down, but, expected to

rebound in 199 7/98.

Inflation under control.

Lower official interestrates.

Continued improvementin Australia’s balance ofpayments and Budgetdeficit positions.

1.2 Review of the Western Australian and AustralianEconomy

The Australian national economy’s growth moderated to 2.8% in 1996/97.This was lower than the 3.25% growth rate estimated in the 1997/98Commonwealth Budget, delivered in May 1997. Nonetheless, the 1996/97GDP outcome represents the sixth sustained year of Australia’s economicrecovery. Despite this, the average unemployment rate has been stuck at anunacceptably high level. Indeed, it rose marginally in 1996/97 to 8.7%.

Following the strong rates of economic growth of the past 3 years,WesternAustralia’s growth moderated to 3.1% in 1996/97. This outcome was weakerthan the 5% forecast in the 1997/98 State Budget, delivered inApri11997. Themain causes for the State’s lower than expected 1996/97 growth were thesluggish growth in the State’s retail sales, lower than expected businessinvestment and higher imports.

Surprisingly, business investment fell by a modest 2.1% in 1996/97. This fallwas largely the result of the 7.5% decrease in business investnlent in the June1997 quarter. The main reason for the fall was the timing of investment. Stronggrowth in imports of investment goods in the June 1997 quarter are consistentwith a substantial pickup in investment spending in the first half of 1997/98.This suggests the original investment profile underlying the 1997/98 StateBudget investment profile remains accurate but has been moved back onequarter. This is likely to have been the result of unexpected delays in theconstruction of some of the State’s large resource projects.

On a positive note there are tentative signs that housing activity, which hasbeen falling over the last two years, is beginning to recover. Despite falling by0.1% in 1996/97 dwelling investment activity increased in the latter half of1996/97 to reach its highest level since March 1995.

WesternAustralia’s employment growth increased from 1.8% in 1995/96 to2.3% in 1996/97. WesternAustralia’s average unemployment rate in 1996/97remained at around its 1995/96 level of 7.5%, still the lowest rate inAustralia.

In 1996/97 Australia’s headline inflation rate increased by 1.3%. Australianaverage weekly earnings for full time employees also rose by 3.9%. Growth inWestern Australia’s headline inflation rate and average weeMy earnings forfull time employees eased over the second half of 1996/97 with the finaloutcomes being 1.4% and 2.3% respectively.

On the back of a low inflationary environment, favourable wages growth andconcerns over Australia’s high level of unemployment, the Reserve Bank ofAustralia initiated four cuts in official interest rates in 1996/97. Official interestrates were cut by another 0.55 percentage points in July 1997. Reflecting theofficial interest rate cuts the yield on 90-day bank bills has fallen from around7.6% in June 1996 to 4.9% inAugust 1997.

In 1996/97 there has been a substantial improvement inAustralia’s balance ofpayments as well as in the Commonwealth Government’s budget deficitposition. In 1996/97 Australia’s current account deficit totalled A$16,500million, downA$4,000 million on 1995/96. Whilst this accounted for 3.2% ofAustralia’s GDP in 1996/97, significantly lower than the 5.8% figure recorded

Department of Minerals and Energy

Z6-uep96-1n1’96-uep£6-1npOZ

O8

~BJeu~3 pue SlmeU!~ Jo ~uauJiJede(3

~’L eJn6!=lU~elln8 Mua8 eAJesaEI :aomo£

Z6-uep96-1nf’96-uep£6-1np

N::IA/$V BlVI:I :IONVHOXB

o£

O9

O2.

08

06

00~

’fi6/566I m. %gL’~ aq ol pal3adxa ql~oJ~ qlDx ~m.~gJno3uo ~agaog s~dso~d tll~o~ ~tI~ ~iFgI!uqS ’tO/O00g ol 86/L661 moaj mnuug ~od

%9 pu~ %~ u~nxl~q ~u~J ol pm~dx~ s! q!~xoJ~ ~lm~ ’86//661 u! dn

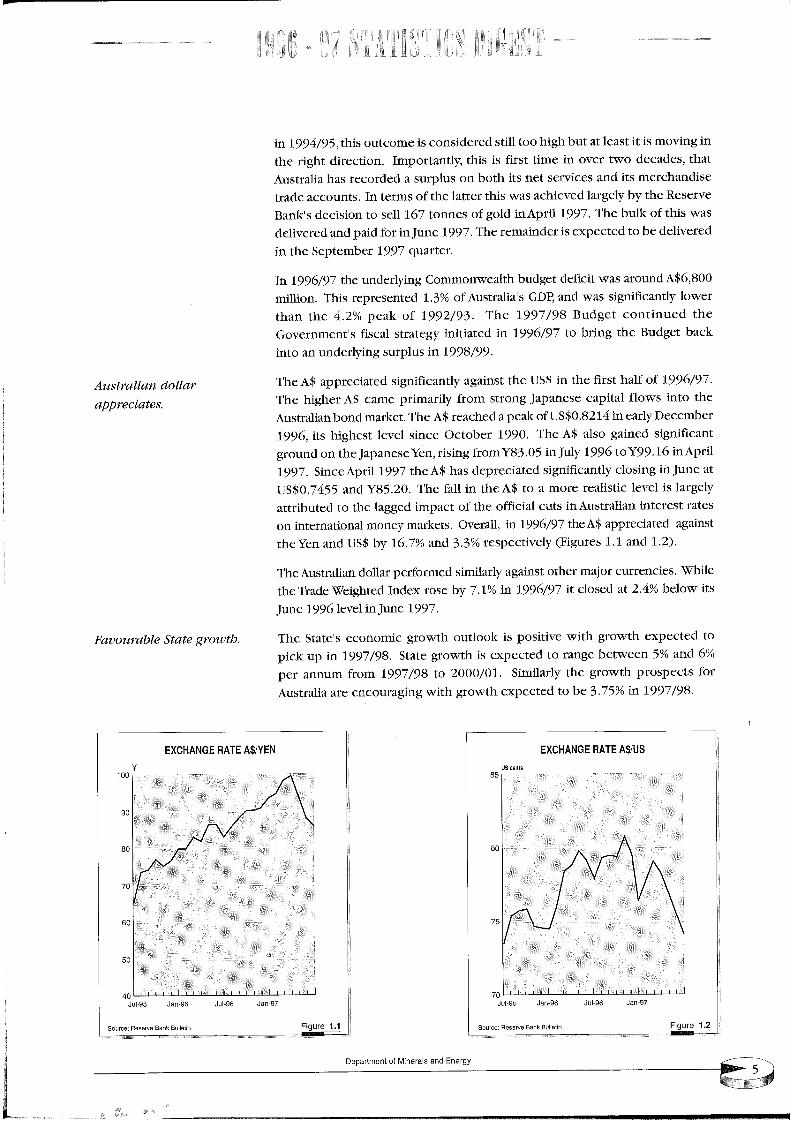

’/66[ aunf m. Iaaa19661 aunf

sl! aXolaq %}’~ le pasola !! 16/9661 m. %1’l XqalgtAk ’sa!auaaana ao[em aaqlo lsm.e~l; Xlae .l!m!s patu.*ojaad aeI[Op ue!Iealsnv aqz

"(UI pue 1"I saan~!a) ~Iaa!laadsaa %~’~ pue %l"9I Xq SSFI pue uaxaqllsu!e~e pale!aaadde svaql L6/966I u! ’IFaaaO ’gla}laeEI ~auottI IeUO!lemalu! uosalea lgaaalu! t~e!Fa!snvu! gma F.*a!jjo aql jo laedttq, pa~eI aql o! palnq!a!!~~ia~aei s! iaaaI a!!s!Faa aaom e ol SV aql u! IFJ aq3~ "0UgSX pue1~ aunf m. ~u!sola Xlluea!~u~!s pal~!aaadap seq SV aql k661 p.adv aau!s ’k66Ii!adv u! 91’66X ol 9661 ~Inf u! g0’ {R_&moa~I ~u!s!a ’uaxasaued~f aq! uo punoa~luea!~u~!s pam.e~ ogle SV aq~ ’066I aaqolao aau!s IaaaI !satI~.rq sl! ’966[aaqmaaa(I Alaea tq. ~1 ER’0$SFIJO ~tead e paqaeaa SV aq.l, ’la}Iaem puoq ue!Falsnvaql or!! S~OlJ Im!d~a asauedef ~uoals moaj XI!.,em!ad atu~a SV aaq~!q aqiL

’k6/9661 ~o JI~q asa!~ aql u! ~gFl aql lsu!~e Xllu~a!~u~!s pale!aaadde ~V

"66/8661 u! snldans ~u!Xlaapun ue oltq.~Iaeq la~pn{t atI1 ~m.aq ol /6/9661 m. pa!~!l!u.~ !~aleals IeaSg s,!tlatuuaaAooaq! panu!luoa la~pn{[ g6/k661 aq& ’{6/~661 jo )lead %g’} aql u~tt!ila_~xoI .~iltleat .oqti~!g geax pue aGO s,e!FalsnvJo %{’1 pamasaadaa g!q~ ’uo.qI!m008’9$vpunoae seax l!a!jap la~pnq 41Ieaaxuotuu~oD ~m.~I.*apun aql L6/9661 u1

aala~nb/66I aaqmaldaspaaaa!iap aq o! palaadxa s! aaptq.emaa att~ ’k661 aunf u! aoj p!ed pue paaaa!Iapgl~ax S!ql jo ~nq aq~ "L661 I!advtq. PIaaaasa~[ aq! Aq Ala~aeI paaa!qae seas g!q! aalleI aql jo smaa! uI ’sltlnoaae apealas!pueqaaam sl! pue saa!aaas latl!~ql ’sapeaap o~al aaao m. amp lsa!ju! ~m.aom s! 1! lgeaI le lnq q~!q oo!

’Wmo.~ al~g~ alq~.¢noa~zt

’sa.w.~oaaddt~.WllOp ZW!l#&*snv

Commodity prices mixed,gold and nickel down,petroleum and iron oreup.

Favourable 1998commodity priceoutlook.

1.3 Economic Factors Affecting the Mining Industry

A major factor affecting the economics of mining and petroleum extractionare the demand prices received for the resources extracted. While demandfor most mineral and energy commodities was strong in 1996/97, in terms ofcommodity prices received, producers’ fortunes in 1996/97 depended onwhich market they were in.

Gold, for example, performed poorly. While the average gold price fell toUS$364 per ounce in 1996/97, down from US$390 per ounce in 1995/96,continued market concerns over gold stocks held and speculative gold salesby Central Banks, saw the gold price fall to US$317 per ounce on July 9,1997,its lowest level in four years.

After US$ nickel prices rose over the previous two years, the price fell byaround 12% in 1996/97. This fall in price was the result of lacklustre nickeldemand by stainless steel producers generated by a drawdown in worldstainless steel stocks and the increased availability of stainless steel scrap (asubstitute for nickel).

Petroleum products on the other hand were the best performing commodityin 1996/97, with oil prices reaching a six-year high in December and January1997, trading above US$26/barrel. This outcome was primarily the result ofcold weather concerns in Europe and low inventories. By end June 1997,however, petroleum product prices fell to around US$21. Overall petroleumproduct prices rose by 18% in 1996/97.

Australian negotiated iron ore prices also recorded a 6% increase in 1996/97.

Aluminium prices are showing signs of recovery. While they fell by 9% in

1996/97 aluminium prices recovered in the first half of 1997. In 1997/98they are expected to be 6% higher than the 1995/96 level.

With strong growth expected to continue in most of Asia and major OECDcountries the outlook for commodity prices is favourable. On the back ofcontinuing rising demand and the supply of a number of minerals constrainedin the shorter term by capacity, ABARE predicts average prices for mostAustralian minerals and energy commodities will rise by between 3% and13% in calender year 1998.

For the 1997/98 financial year, however, ABARE has forecast a 2.4% rise inA$average prices received byAustralian mineral and energy exporters. Strongeraverage 1997/98A$ mineral and metal export prices (up 6.8%) are offset by lowerenergy export prices (down 3.7%). The subdued overall 1997/98 outcome,therefore, comes from the anticipated 3.8% 1997/98 depreciation in the US$/

On the back of a 5.4% rise in Australian mine production, ABARE expectsmineral and energy exports to grow by 5.7% in 1997/98 to a new record ofA$38,550 million.

A positive development emerging for mineral commodity markets is that Sovietstockpiles appear to be depleted and there are early signs that pressure on

Department of Minerals and Energy

’866I Xa~nusf I moaj f±o~z: ol paanpaa aq llJ.~ ploqsaaq! s!q~L ’aa!oqaa!aql jo aa.~ddns ss~ aql q!!a~ Xllaaa!p lasaluoa ol alq~ uaaq aastI uo!laatmoaai~u.~g s q~noaql mnuus aad f~00g lssa| 16 ~uPt~l gaamolsna gs~/-66[[ moa~l "saamolsna s~ a~asI .,oj auHad!d ss~ Is.,nlsu Xanqunlt ol aa!dtu~(Iaq! ol gsaaas m. ~u!ssqd jo tusa~oad aql jo uo!lsnm.luoa pus 966[ aaqolaom. pauado XlF!a!jjo ssnx qa!qax amI. ad!d ssO splagploO aq! jo uo!laldmoapapnpu! s!qj~ ’k6/9661 u! la~t.T~m X~aaua aql jo uo!lsln~aaap aaqlanJ aq!aaoadm! ol panu!moa ssauaa!l!ladtuoa Xalgnpu! ~u!m.m g,~!tsa!gnv u.ta!saAk

q!isa~auommoD ao alslg aql aaql!a Aq ua~Isl saansgam jo aaqmnu V

’ql~oa~ a!tuottoaa s,~!lSalsnvuaalgaAk ol slu!od

}’I pps plnoak qlaxoa~ aFJJOUOaa g,u~dsf m. agsaaau! m!od a~muaaaad 0’[g 1~ql palgm!lga uaaq gsq !! ’aldmsxa ao~I "lusa!j!.u~!g aa~ gd~lNguo!l!puoa a.wJouoaa alqsanoasj jo Xmouoaa g,alslg aq!jo lgaa aql aoj glaajja

aa~O-IlJ.dg aqj~ ’gaalaodxa jo la~am u!~m aq! u!~maa llDX pus glaodxapus Faau.rtu g,aaslg aql jo spa!q1 o2A1 usq! aaom ga~lsl Xlluaaana

¯ 2LTlgnpu! ~u!u!m g,aa~lg aql !!jauaq o! anu!luoa plnoqg sa.uuouoaa

aoj ~oollno a.waouoaa aa!lFod aqj~ "pu~map I~!mmgqng ap!aoad o! anm.moa

(sd~IN) saaulasd ~u.tpsa! .Io[gm ’aglna!!agd u! ’saam.m us!isa!snv uaalsaAk ao~I

a~usqaxa u~!aaojjo qaasag u! ga.~l!pommoa jo sad!n [is 1o ~u!dmnp a!lauaaJ pajama!a1 ~ISSflaqlJo asdNloa aql sa~aX luaaaa aaaO "papua s~q ~u.~dmnp la!aog moaj gaa!ad

"uo.~g~ln,ga¢ap(C~.¢ouo ~q polsooq

ssouoa!g!la4utoo

’alOOl!no oa!g!sorf ap!ao.cds.¢oul.w4 8u!p~.q aof~w

Hilmer reforms provide

benefits.

Commonwealth

Government targets the

Diesel Fuel Rebate

Scheme (DFRS) forrevenue savings.

Section 23 (pa)exemption from income

tax for prospectorsremoved.

1997/98 CommomvealtbBudget.

In addition to the developments in the gas market, the State Government is’phasing in access for large electricity producers and consumers to WesternPower’s high voltage electricity transmission and distribution systems. Openaccess is to be provided to large electricity consumers according to a schedulewhich commenced from 1 January 1997. Deregulation of access toWesternPower’s systems is expected to create competitive pressures betweenelectricity generators which should ultimately lead to the supply of cheaperelectricity, providing in turn a further boost to economic development.

More generally, the market framework within which the mining industryoperates had its competitiveness enhanced with all States and Territoriesenacting legislation which subjected their public enterprises to the provisionsof the Trade Practices Act (TPA) from 21 July 1996. This was a major step inNational Competition Policy resulting from the Commonwealth, State andTerritory governments endorsing the 1993 Commonwealth IndependentCommittee of Inquiry into National Competition Policy (the Hilmer Report")and subsequent signing of agreements inApri11995 to put into effect variousmicroeconomic reforms.

As a means to address DFRS’s rising revenue cost, in October 1996 theCommonwealth Government proposed a number of amendments to theScheme. The amendments, amongst others, will make diesel used in all vehiclesunder 3.5 tonnes which are suitable/capable for use on public roads ineligiblefor the rebate. The Bill is being debated in the Commonwealth Parliament.

WesternAustralia is already the State most affected by the proposed October1996 legislative changes to DFRS as its mining industry relies more on dieselfuel than in other States. Any additional changes to DFRS, such as capping itsfuture cost, would further impact on the international competitiveness of theState’s resources sector.

On August 25 1997 the Commonwealth Parliament passed an amendmentwhich removed the exemption previously provided under paragraph 23 (pa)of the Income Tax Assessment Act 1936 to income derived by bona fideprospectors from the sale, transfer or assignment of rights to mine for gold orany other prescribed metal or mineral. Removal of the exemption is beingphased in over the period 19August 1996 to 19August 2001. Over this periodonly the increase in value of mining rights is taxable. The value accrued to 19August 1996 remains exempt until 19 August 2001. After this date theexemption will be completely removed and total value taxable.

The 1997/98 Commonwealth Budget brought down in May 1997 was essentiallya "steady as you go - hands off" approach which, unlike the 1996/97 Budget,inflicted minimal additional pain on business and the community in general.The massive 1996/97 Budget cuts to Government expenditure and industryincentive schemes, such as the reduction in the premium rate of deductionfor research and development expenditures from 150% to 125%, are now havingfull effect. The resultant increased revenue growth is the key factor to theCommonwealth’s expected budgetary improvement for 1997/98 and return tosurplus in 1998/99.

Department of Minerals and Energy

paaa~!al geax lanoD q~!H

qa!qax luatua~ueaae lau Xlajes e atuoatq ,galmg aql laaaoad oa~ ’uo!II!m 000’g$¥punoae PalImO! ga!l~lg II1~ so5 ssoI anuaaaa aqJ~ ’la~pnq g3~!II~algn¥ uaalsa~~ lINaaoqs uo!II.~tu 009~¥ e paa~aaa Alaa!laaJJa uo!s!aap s,aanoD q~!H aqJ~

’ttlaql laaHoa ol ~u~.~.tl II!lg tI! lt~.od alal!I g~x aaaql lgq! paaa~e galelglie ,AiluanbaguoD .ltulqnop geax aonb!I pu~ Ianj uo sd~I~ 5o A!!p!Iea aql leqllueatu Ogle uo!g!aap aql leql pas!~pe Xlluanbagqng IeJauaD gaol!aRog "ga!aol~.aJaJ~pue gaaelg lie uo pala~dm! uo!s!aap s,lanoD q~!H aqJ~ ’p!Ieam. aaa~ Xaql as~.axaue ~aI o! q!I~a~auotuvaoD aql gaxolI~ AlUO uo!ln!t.lguoD aql jo 06 uo!laag geaaojaaaql pue as!axa ue gem g~I~I~ oaaeqo! aqa leql palna AII~!luassa aanoD q~!H

aql leql eH pue puotutueH ga A~gN ~. palna lanoD q~!H aq! L66[ asn~n¥ g uO

~U!l~.qs 5o Aa!Iod sl! gant~.ltloa qlleaaxuotutuoD aq! J1 ’uo.qI!tU I g I ~¥ s! aaeqs

g,e!i~algn¥ u.talga~ ’tuea~oad uo!lanpaa lqap g,qlleaaxuomrttloD aql spae~ol

saeaX aaaqa aaao Ielo1 ~ uo!II!ttt 6gg’I $¥aanq!aluoa o1 paa!nbaa aae sa!aol!aaa~Lptt~ ,gal~lg aq! ttlleaaxuottrttIoD aql q!!ax lua~uaaa~e 9661 ~ aapun ’uo!l!ppe u1

’L6/966I u! %6’0 jo ma Ieaa ~ saXOlIO5 s!q& ’96/L66I aoj sa!aol!aaa&pue sa!~lg aql ol slu~a~ qlleaaxuotutuoD u! lna Ieaa %>’0 ~ 5o aauaaajuoDsaa!tuaad L66I aq! jo atuoalno aql paleaodaoau! la~pn~ aq~ ’sa!aol!aaa&ptle sa!~lg aql oluo lqap gl! ~U!l~.qs Xq s~Iooq ga! ~u!au~Ieq s! q!IeaaxuotutuoDaql aeqa axa!a s,alelg aql gtua!Suoa aa~pn{t q!IeaaxuotmuoD 96/L661 aqj~g&gpnq qgltaOmuoututoD

sagod.,nd uo!lanpaa lqap qlleaaxuotmuoD

Aia~sei pasn aq lI!aX Wjptgax aql leql palea!pu! s~q luatuUaaAO9 q!Iea~uottw~oDaqJ~ ’aoj pala~pnq uo!II!tu 000’95¥ aql paaaxa o! palaadxa aa!adsales Ie!ol aql ql!~x ea!sla.l.Jo ales {/[ aql tttoaJ IIeSpuDx luea!~u~!s ~ aa!aapii~.~ q!ieaaxuoml~oD aqa leql AIa~I!I saeadde 1! la~pn~ aql uaxop ~u!pueq aau!g

CommonwealthGovernment foreshadowsmajor tax reform.

State Governmentintroduces a gold royalty.

The calls for a newAustralian industrypolicy.

Windfall Tax to apply on any refunds of past BFFs paid by companies to theStates. This would prevent companies from undertaking court action to recoverpast BFF payments.

On a positive note the High Court’s decision has provided the CommonwealthGovernment with a catalyst for a wide ranging inquiry into tax reform. Theinquiry will develop tax reform options that the Government can take to theFederal election, due at the latest, in March 1999. The Prime Minister hasindicated that the guiding principles for reform are to include considerationof a broad based indirect tax; reform of Commonwealth/State relations;reductions in personal income tax; and no increase in the overall tax burden.

A priority outcome for the States from the reform of Commonwealth/Statefinancial will be to reduce the States’ dependence on Commonwealth grantsfor their funding. This dependence was further exacerbated by the HighCourt’s decision.

From a State perspective the optimal outcome of the tax inquiry would bethe adoption of a more efficient and effective tax system, one that does notunduly penaliseAustralia’s export sector, as is the case with current tax system.It has been estimated thatAustralia’s existing indirect tax system (ie.wholesalesales tax, diesel fuel excise etc) imposes an additional cost of 5% (i.e. aboutA$3,800 million) on exporters.

In the 1997/98 State Budget, brought down inApril 1997, the Government’schallenge was to meet the State’s revenue shortfall resulting from the continuedcuts in Commonwealth grants to Western Australia. The State Governmentfaced difficult fiscal decisions and this has led to the gradual removal of theexemption from royalty payments on gold production.

The 1997/98 State Budget indicated that a gold royalty option was beingexamined but the final makeup of the royalty was still subject to industryconsultation.

After consulting with industry groups the final makeup of the royalty wasdecided by Cabinet and announced on 28 July 1997.

The royalty will now commence from 1 July 1998 at a rate of 1.25%. The fullroyalty of 2.5% has also been delayed until 1 July 2000 and will be conditionalon the gold price exceeding an average A$450 for the quarter. The royaltywill be unconditional from 2005. These concessions are worth aboutA$ 56 million over the next three years, and up toA$160 million over the nextseven years.

The State’s gold royalty is also deductible for Federal company tax purposes.At 1.25% and 2.5% the effective rate of gold royalty translates to 0.8% and1.6% respectively.

Over the last five years the consensus among industry is that Commonwealthgovernments have lacked an industry policy direction. Industry believes thatthe lack of a coordinated industry policy will impact onAustralla’s internationalcompetitiveness in the near future.

Department of Minerals and Energy

’%gI ~q osad

sau!ddR!qd aqa put %11 ~q a!~m.a ug!SAglgla~ aq~’.%LI Aq qg!dna ug!sauopuIaqa :%{{ Aq ualIgJ sgtI lqgg pugI!gq& aql L661 lsn~n¥ o1 L66I Alnf moaeI

¯ Xa!lod Xalsnpu! aa!laajja put luaaaqoasl! ~ slaodaa asaql ~m.aap!suoa Xlmaaana s! mamuaaao9 qlFa~t~ommoD

X~OlOUtpa! uo!lgm.*oju!jo luamdolaaap put qaagasaa uo uo!ssaanoa xgl %00g g aoj [gsodoadg ~u!pnlau! ’aa!laa!qo s!ql aaa!tpg ol suo!ssaauoa xm aoDm spuammoaaa1I ’.4~o[otlqaal uo!lgmaojtI! u! tlo!lgaouu! jo alga g,~.~I~a!sn¥ aaoadm! olX~algals ~ ql!~ mammaao9 sap!aoad (5661 lsn~n¥) laoda}t ~qlaoaxsplo9 aqj~

"L6/9661 u! glaodaa jo aaqmnt~g pat~o!ss!mmoa luamuaaao9 qllga~t, ommoD aq! pt~noa~Iagq s!ql lsu!g~V

Minin8 outlook isfavourable.

According toAustralian Bureau of Statistics (ABS) data mining profits growthfell from 27% in 1995/96 to 2.5% in 1996/97. Profitability levels in the miningindustry are expected to improve in 1998.

TheABS’sAustralian Business Expectations Survey suggests that mining profitsare expected to be around 35% higher in the September quarter 1998compared with the September quarter 1997. This suggests that most miningcompanies responding to the survey expect a more favourable internationaleconomic climate and commodity price outlook in 1998. It is also expectedthat Australia’s new mining investment will rise by 19% in 1997/98.

Department of Minerals and Energy

,~6Jeuq pue sleJeU!lAI ~.o ~ueLuiJede(]

¯aanpaaoad alg!lo~au ol lq~!a

aaao suo!lga!Iddg lIg ’sasgaI asodand Faaua~ pug sasgaI ~t .mqm jo asga aql uI

’aanpaaoad

alg!lo~att ol lq~!a aql tD!aX aaugpaoaag tq paaaoad !snm aallgtu aql uaql’QLJ~NNI)Funq!a£ al!!J~ aa!lgNI Iguo!lgNI aql Aq plaqdn s! uo!laa!qo aqa pugail!l aa!agu pa.*aas!~aa g Aq apgm s! aanpaaoad pa!!padxa aq! ol uo!aaa[qo

’paltlga~ S! lUamauaa aq! po!aad uo!lgag!.!ou qluom-o~!

sa!lagd lugaalaa pug (~I~(1) X~aault pug SlgaatqIN jo auatulagda(I aql Xq pas!laaapgaag stIO!lga!Iddg alt!1 IIg ’sasgaaoad ¥&N aqa o! Salad ~tn.u!tu pug uo!lgaoldxa

69L’8 atuos paaaajaa pgq luamlagda(I aq! L66I asn~n¥ EI oz ’g661 qaagIN 9Ijo uo!s!aap lanoD q~!H aq! aau!s (¥&N) aagall!&aa!lgN s,luamuaaaoD Igaapa~

aql ql!~ ltlals!sttoa saanpaaoad pgq sgq luamttaaAoD ug!Igalsn¥ tlaalSaAk aqj~

pa~poI sru!gp axau I8 aaam aaaqa L6/966I u1 ’uoIlgs!Faa .ugu u~omIjo sgaJg lsolxt ~Lqpniau! g!lgalsnv uaalSaAk jo %08 aaAO ~U!JaaOa sm!gla 011!1aa!lgu 6gE aaa~ aaaq! L661 aunfjo pua aql !¥ ’saolaas mnaloalad pug ~u!tn.maql uo lagdm! sl! pug ai1!1

"so.mpoooadol~.~logou ol ¢q~ta

~(Tq &, plaq suo!¢vO.Zl&[Vos~ol ~tqu.~Ig

¯ uaoouoo ~ u.toutaa

Three NTA ruling in1996/9 7 will furtherimpact on the number oftenements the State cangrant.

During 1996/97 there were three significant decisions which had a detrimentalimpact on the number of tenements which could be granted under the State’sMining Act 1978.

First,inAugust 1996 the NNTT found that theWesternAustralian Government

had not fulfilled its obligations to negotiate in"good faith" and as a result over900 mining lease applications subject to the NNTT’s right to negotiate at thetime of the ruling have had to restart their progress through the negotiationprocess.

Secondly, on 23 December 1996 the ttigh Court provided its long awaitedruling (Wik decision) on the key issue forWesternAustralia of whether pastoralleases extinguish native title. Despite the Court’s ruling this remains largelyunresolved. The High Court ruled that pastoral leases in CapeYork in northernQueensland did not necessarily extinguish the native title claimed by theWikpeople. It concluded that, because the nature of theWik people’s native titleclaim had not yet been determined and because the pastoral lease in questionwas a limited grant of rights, there was potential for native and pastoral rightsto co-exist. Therefore, the lease may not have extinguished native title. It alsoruled that where the rights under a pastoral lease were inconsistent withthose of native title, the rights of pastoral leases would prevail.

CommonwealthGovernment moves toamend the NTA.

Thirdly, on 8 May 1997 the Federal Court (the Dann decision) upheld that theNNTT should consider the rights bestowed by the grant of a tenement, ratherthan the intended use of the tenement by the applicant, when making adecision as to whether the expedited procedure (or fast tracldng) shouldapply. As a result of this, if a native title party objects to the expeditedprocedure applying to any exploration title then the full right to negotiateprocess will apply.

WesternAustralian officials have been working with the Commonwealth andother States in an attempt to identify amendments to the NTA which wouldmake the system more workable.

In October 1996 the Prime Minister announced a number of proposedamendments to the Native Title Act 1993. Those amendments aimed tostreamline the NTA so as to make it more workable by, amongst others, makingall native title claims subject to a threshold test so as to determine theirlegitimacy; allowing once-only right to negotiate for mining companies anddevelopers; and excluding exploration companies and prospectors from rightto negotiate obligations.

On 28April 1997 the Prime Minister announced a 10 pointWik plan strategy.While the strategy does not extinguish native title on pastoral leases it attemptsto define those pastoral activities which are viewed as being inconsistentwith native title rights.

In September 1997 the Federal Government introduced the Native Title Bill1997 into the Federal Parliament. The Bill incorporates the proposed October1996 NTA amendments and the so calledWik 10 point strategy.

Department of Minerals and Energy

suo.~!~aap!st, oa lt~att~dolaaap ttsql aaqll;a uo!laaloadspa~o!’asnoquaaa~ se qans ’sanss! lu~laodm.~ uo sal~qap paaxa~Is luamuaaao~sno!aaad aq! 11~ql ja!Iaq sl! s! qa~oadd~ s,luamuaaaoD luasaad aql m. l!a!IdtuI¯ saa!aaa[qo luamdolaaap pu~ I~luamuoa!Aua aaueI~q-aa o! ~tL~ldmaale uaaqauamuaaaoD qlleaaxuomtuoD axau aq! 966I qaa~lR m. aaaxod ol ~ .u~oa

"slo,~luoo

sax~laa qllPamuoututoD

s!~as a.~aqla~im o! alqs aaaax ’asnoH aaddfl aq! ol palaala saaqmam axau aql uaq~’k66IA~ Ig uo laajja ~IOOl s!qa. ’Aaols!q Sl.t tl.t am!l lsa!j aql aoj asnoH aadd~l atI!jo ioaluoa 1goI t~o!l!lgoD aqa uo!laaI~ a!l;lg 9661 aql jo atuoalno aql ~u!aaalJa~d

"966I.taqutaoa~I u.~ uo.~g.tlVOO

’VAN lUaaana aq! aapun slusm!sla ql!axaas!lo~au o! anu!luoa ol paau ii.~ax Xalsnpm. aq! uaql I!lUfl ’(paaaa{aa ao) passsdass sluatttpuams VAN aql aaojaq attt!l attlos aq pInoa !! s.~olsuaS luapuadapu!Oral ao/pus sa!!asd aou.m~ aql jo laoddns aq! saa!nbaa uo!lsls!~al aDDaa!lsu s,luattn~aaaoD qllsaaxuommoD aq! jo a~ssssd aq! lsq! t~aa!~’ssalaqlauoN

sa~aA aananj u!~ padoIaaap aq

aaom ~ 1~q! Xl!lT.q!ssod atttos aajjo Aaq.l~ "luam~!Ia~d qlI~aaxuomt~oD aql aaojaq

AllUaaana VJAI aq! ol sluampuatt~ L66I aql slaoddns Xip~oaq

position was dealt a major blow when Japan, which had been previouslyreceptive to Australia’s position, called for a 5% reduction in greenhouse gasesbelow 1990 levels. It therefore remains to be seen what the outcome of furthernegotiation will be.

1992 NationalGreenhouse Response

Strategy to be revamped.

Australia has, in the past, attempted to contribute in a fair and equitable wayto the international response on greenhouse. In 1992 a National GreenhouseResponse Strategy (NGRS) was adopted byAustralian governments. Followinga 1996 review of the strategy it was concluded that governments, stakeholdersgroups and the community need to do more to reduceAustralia’s greenhousegas emissions and to prepare for the potential impacts of climate change.

In 1997 a discussion paper - Future Directions for Australia’s GreenhouseStrategy - was released for public comment by the IntergovernmentalCommittee on Ecologically Sustainable Development. The paper providespossible actions across a range of industry sectors and sets out potentialmeasures on community information and education with the aim of reducinggreenhouse gas emissions.

Nonetheless, as of September 1997, the suggestions contained in the paperhave not been formally considered by Australian governments. The NGRS isexpected to be finalised later this year but it may need to be modified toincorporate Kyoto outcomes.

WA Government giveslegislative backing to itsMat’ine Parks policy.

The State Government has continued its policy of balancing environmentaland development objectives.

In November 1994 the State Government outlined its new policy for managingthe marine environment in a policy document titled"New Horizons in MarineManagement". As part of the process of framing the policy the Governmentannounced that year that future drilling exploration in the Ningaloo MarinePark was prohibited.

Key elements of the marine management strategy include: the provision ofclear access guidelines for petroleum explorers and developers in marineconservation reserves; a three-tiered approach to marine conservation reservecategories; and the establishment of a Marine ParksAuthority in which marineconservation reserves will be vested under the Conservation and LandManagementAct.

A key aspect of the policy was that the Minister for the Environment wouldobtain the consent of the Minister for Mines before creating any marine reserveor management zone within a reserve that would preclude petroleumexploration and development activities.

The November 1994 policy has been given legislative backing by amendments

to the Conservation and Land(CALM)Act and theWesternAustralian Petroleum

Acts. These amendments, applying both to petroleum and mineral exploration

and development,were proclaimed on 29August 1997. Drilling and sea floor

sampling is now prohibited in Marine Nature Reserves and Recreation and

some special purpose zones of Marine Parks.

sau!iap!n~ dn axaap 1! ’aaojaq ugql aaqlga’aaltg ~m.llnSuoa sg~a Dd.qN aq! lgql pau!gldtuoa pgq AalsnpuI ’Dd~N aq! Xquo!lgllnguoa aa!laq aot ’Xalgnpu!. ~u!u!m aql ~u!pnpu! ’Xalgnpu! moaj aanggaad~ttoalg pa~olIoJ g!q~ ’sINdRN aanlnt jo luamggagsg a!mouoaa pug’ImUamuoa!aua aql aot gau!iap!n~ uo pug gaanggam IgUO!lgu uoggau!gnq pug ~h!unmmoa aoj gloao!oad paaoaddg pug gal!gjo lttattlggaggg uo IA~d~N ~au g palg!l.m! ogle I!aunoa aq~ ’Xaoluaau! luglnllodiguo!lgtt g .toj (INd,[N) aanggam uo!laaload luamuoa!aua Igtlo!lgu g dolaaap o!paaYag 966I aaqmaaoN t~ Dd~IN aqlJo ~tn.laaKt V ’uo!lglg!~aI Imuamuoa!.aua~Iao~atttg.~j lualg!guoa ~ ap!aoad ol aaqla~Ol ~u.~f.to~ gaalg!u!m lUatuuoa!aua!~ol!aaa~pug almg ’l~aapa~I 1o slg!guoa Dd~IN aq~ ’~poq iguo!lgu Xpu! g 1!’966I aaqmaldag u! (Dd}tN) I!aunoD uo!laalOad luamuoa!auR IgUO!lgN aq! pau!o[

i!aunoD Ig!aals!m.I~pug luamuoa!au~qang’VH~agaaotaq’!Insaa g g¥ ’/-66I aaqmaldag ~;I uo pau~!g gg~ (VI-I~{Ig) gaaya~m!aaH

’Houno~9 uo!gaogo.tdll~guoutuo2,~au~

l~UO!l~N aql su.~of VAt

ala*aCl~ aql

Figure 1.3

LOCAL GOVERNMENT BOUNDARIES

SCALE

0 25 5O 75

MAP 2

100 125

SCALE

MAP 1

LEGEND

LOCAL GOVERNMENTBOUNDARtES (S) --TOWN OR CITY OLOCAL GOVERNMENT STATUS

(S) -SH~RE(T) -TOWN(C) -CITY

Department of Minerals and Energy

OleluJn!ql!’l - uJnlm, Uel - U!l

lies

NOI991~10 L$V =10 $S3OX3 NI NOI/ORC]Ot:::ld 90 9RqVA 9VIqNNV NV H/I/W

Vl-IVl=llSrlv N~1~3133/~ NISlO=lrOHd INn=l’101d13d QNV "IVIg=INIIN ~IOPVIN

REVIEW OF MAJOR MINERALS AND PETROLEUM IN WA

2.1 Overview and Outlook

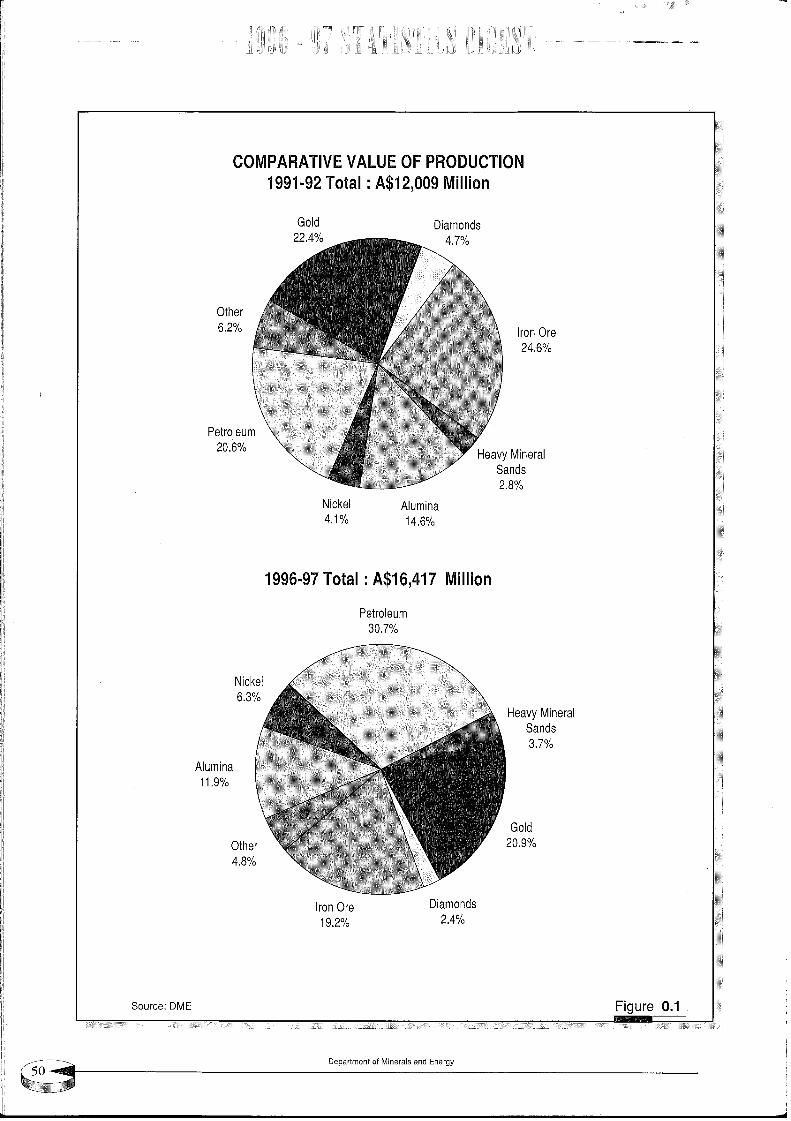

The value of mining and petroleum productionincreased by 7.0% in 1996/97 toA$16.4 billion.

The key sector contributing to this growth waspetroleum (upA$965 million) and iron ore (upA$235million). Commodity prices were mixed in theirmovements over 1996/1997, but the appreciation intheA$ over the year uniformly eroded the returns formost of the State’s mineral and energy producers.

Undoubtedly the highlight of 1996/97 was thecontinued surge in the petroleum sector, making itthe State’s first industry to produce more thanA$ 5,000million of product in a year. The petroleum industryhas entrenched its position as the State’s leadingresource industry and it now produces more than 30%of the State’s total value of mineral and petroleumproduction. Against this background it is notsurprising that Western Australia has maintained itsposition for the second consecutive year asAustralia’slargest oil producer.

Conditions in world iron markets improved in thelatter half of 1996/97 and this was reflected in a 8.1%rise in the value of iron ore. The gathering pace ofdownstream processing and increasing prominenceof newAsian markets augur well for an exciting future.

After alumina spot prices fell by 34% in 1996 priceshave firmed over the first half of 1997. Ironically theState’s alumina sector was protected from the eventsin world spot alumina markets because of highercontract prices settled prior to the 1996 drop in spotprices. As a result the value of the State’s aluminaproduction increased by 2% in 1996/97, due largelyto a 1.4% increase in production. The State’s goldindustry also increased its value of production by 1%,but this was achieved through higher output tocounteract a year of lower prices and a higherA$.

Other sectors were mixed. The nickel industrysuffered from lower prices, while buoyant marketshelped mineral sands to increase its value by 3.3%despite mineral sands production falling.

Deregulation of the gas market, commencement ofgas deliveries via the Goldfields Gas Pipeline coupledwith, in general, a favourable outlook forAsian growth

and commodity prices all suggest that the outlookfor WesternAustralia’s mineral and petroleum sectorsis bright.

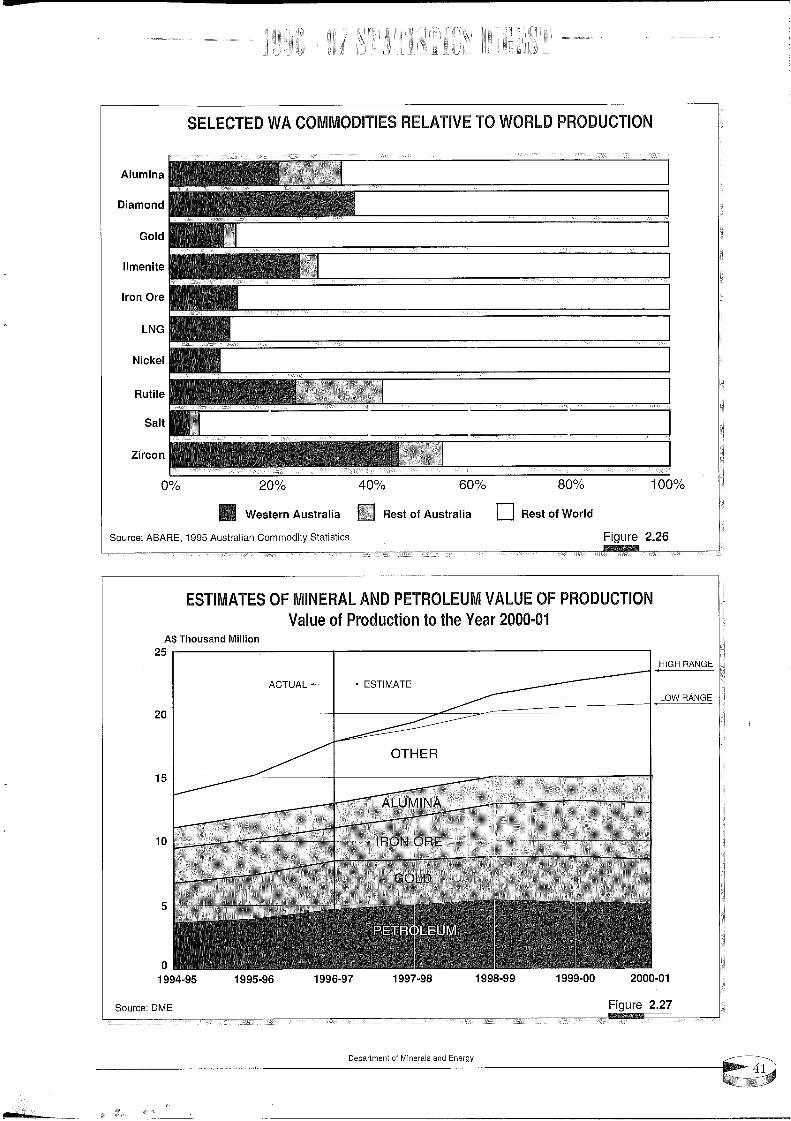

Western Australia is expected to continue to be asignificant world player on many internationalcommodity markets. In 1996/97, Western Australiasupplied (by quantity) around 14% of the world’s ironore production, 10% of its gold production, 7% to 10%of its LNG production, 18% of its alumina production,12% of its nickel production; 32% of its zirconproduction and 30% to 40% of its diamond production(Figure 2.26).

The State’s prominence on the international mineralsscene is expected to be maintained well into the 21stcentury.

As of the June quarter 1997 the value of State miningand petroleum projects under construction was morethan A$5,000 million. In addition, as of June 1997,more than A$30,000 million worth of resourceprojects were either under consideration or listed asa possibility for Western Australia.

The Department of Minerals and Energy (Februaw 1997)has estimated that the value of the State’s mineraland energy industry is estimated to be in the rangeof AS21 -AS 24 billion in 2000/01. This translates intoan average annual rate of growth in production from1995/96 to 2000/01 of 7% to 9%. These forecasts areof course predicated on particular price assumptionsand most importantly, on the likelihood of newprojects advancing. For example, the value of aluminaproduction in a low growth scenario is estimated toincrease at an average annual rate of 6% based oncurrent facilities and production levels. However, ina high growth scenario, where it is assumed that allnew expansion plans reach fruition, the averageannual growth rate to 2000/01 for the value ofalumina output could be around 13% (Figure 2.27).

Department of Minerals and Energy

£6~eu3 pue SleJeU!lR ~o ;uetu#eda(]

~’~ oJn6!-Iaurar ~, u~a ’alaa :aoJnos

08

NOIIONOOEIa =IlVSN=IONOO ON~ 710 =IONEIO

%6’8%~,’L

%k’g JeqlopueleeZ

~eN

%L’69ued~r

NOl’l’lll/! I.SI.’t;$V : ~Q’IVA "lV.LO.LSIHOdX=I INn=JTOl:ll~]d

aseaaatq, a~aeI g!q£ "%gg punoae dn gem lndlno joanleA slI "lanpoad luea~u~F 1sore aql sgm’uo~I~[{ [ 6’ I SVPale~!sa u~ qlaom’uo~lanpoad I~O apnaD

’({’Z ~ Z’g

uo~lanpoad se~ s,~Wa!snvJo %0g punoa~ saanpoadOgle al~!g aql glsa~ns el~p 9661 aaqmaaaO¯ uo~!anpoad alesuapuoa pue Ho apnaas,~iealsnV jo %gg Xlale~!xoadd~ aoj palunoaaeal~lg aR! L6/966[ u1 ’aaanpoad E~naloalad

papnIau~ L6/966I aaao Aalsnpu!mnaioalad ue!iealgnV uaalga#A aq! jo glqS!IqS!H

oo£

slqo~!lqo~!H rdqsnlauI u;nalo.qad Z6/966I

"(I’E: aan~!~ (%6) ueax!e~ pue (%09) uedef 8u!aqguoIleU!lsap .~o{et[t aql qlDa slanpoad mnaloa!ad joqlao~a uo!II!tU [ g I ’{ $¥pmaodxa rams aqa’k6/9661 uI

uo!lanpoad u~naloalad

paluagaadaa g!q~£ ’uO!IlgU g{0’g$¥ qaeaa o! %~ Aq~u!g!a L6/966I u! mdlno jo anlea aq! qlpApue se~ ’I!o aoj lag aaa~ gpaoaaa alea uo!lanpoad

oR1 uaaq geq tunaloalad ~m.uuna aeaA pa!ql aq! ao~I

utnalo.,lad ~’~

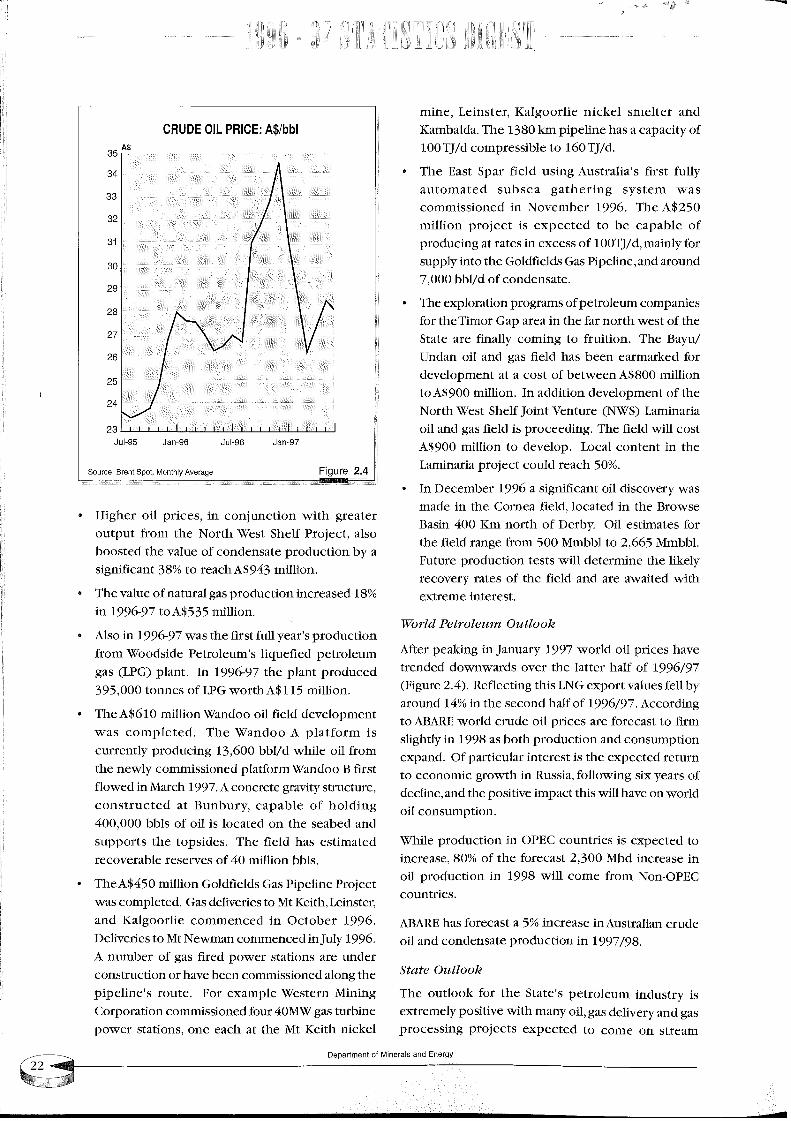

CRUDE OIL PRICE: A$/bbl

33

32

31

29

27 II

26

!

24

Jul-95 Jan-96 Jul-96 Jan-97

Source: Brent Spot, Monthly Average Figu re 2.4

¯ Higher oil prices, in conjunction with greateroutput from the North West Shelf Project, alsoboosted the value of condensate production by asignificant 38% to reachA$943 million.

¯ The value of natural gas production increased 18%in 1996-97 toA$535 million.

¯ Also in 1996-97 was the first full year’s productionfrom Woodside Petroleum’s liquefied petroleumgas (LPG) plant. In 1996-97 the plant produced395,000 tonnes of LPG worth A$115 million.

° TheA$610 millionWandoo oil field developmentwas completed. The Wandoo A platform iscurrently producing 13,600 bbl/d while oil fromthe newly commissioned platformWandoo B firstflowed in March 1997. A concrete gravity structure,constructed at Bunbury, capable of holding400,000 bbls of oil is located on the seabed andsupports the topsides. The field has estimatedrecoverable reserves of 40 million bbls.

TheA$450 million Goldfields Gas Pipeline Projectwas completed. Gas deliveries to Mt Keith, Leinster,and Kalgoorlie commenced in October 1996.Deliveries to Mt Newman commenced in July 1996.A number of gas fired power stations are underconstruction or have been commissioned along thepipeline’s route. For example Western MiningCorporation commissioned four 40MW gas turbinepower stations, one each at the Mt Keith nickel

mine, Leinster, Kalgoorlie nickel smelter andKambalda. The 1380 km pipeline has a capacity of100 TJ/d compressible to 160 TJ/d.

The East Spar field using Australia’s first fullyautomated subsea gathering system wascommissioned in November 1996. The A$250million project is expected to be capable ofproducing at rates in excess of 100TJ/d, mainly forsupply into the Goldfields Gas Pipeline, and around7,000 bbl/d of condensate,

¯ The exploration programs of petroleum companiesfor theTimor Gap area in the far north west of theState are finally coming to fruition. The Bayu/Undan oil and gas field has been earmarked fordevelopment at a cost of between A$800 millionto A$900 million. In addition development of theNorth West Shelf Joint Venture (NWS) Laminariaoil and gas field is proceeding. The field will costA$900 million to develop. Local content in theLaminaria project could reach 50%.

¯ In December 1996 a significant oil discovery wasmade in the Cornea field, located in the BrowseBasin 400 Km north of Derby. Oil estimates forthe field range from 500 Mmbbl to 2,665 Mmbbl.Future production tests will determine the likelyrecovery rates of the field and are awaited withextreme interest.

World Petroleum Outlook

After peaking in January 1997 world oil prices havetrended downwards over the latter half of 1996/97(Figure 2.4). Reflecting this LNG export values fell byaround 14% in the second half of 1996/97. Accordingto ABARE world crude oil prices are forecast to firmslightly in 1998 as both production and consumptionexpand. Of particular interest is the expected returnto economic growth in Russia, following six years ofdecline, and the positive impact this will have on worldoil consumption.

While production in OPEC countries is expected toincrease, 80% of the forecast 2,300 Mbd increase inoil production in 1998 will come from Non-OPECcountries.

ABARE has forecast a 5% increase inAustralian crudeol and condensate production in 1997/98.

State Outlook

The outlook for the State’s petroleum industry isextremely positive with many oil, gas delivery and gasprocessing projects expected to come on stream

Department of Minerals and Energy

~6JaU3 pue SleJaU

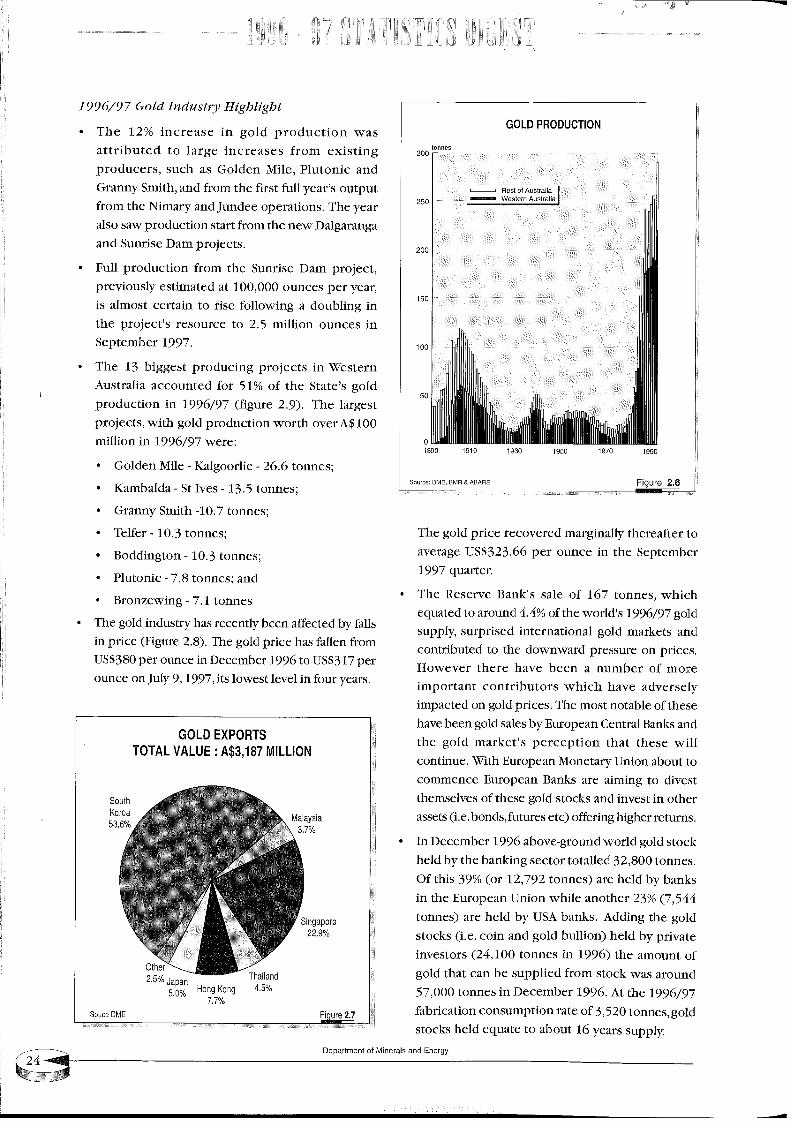

I9~96/9 7 Gold Industry Highlight

¯ The 12% increase in gold production wasattributed to large increases from existingproducers, such as Golden Mile, Plutonic andGranny Smith, and from the first full year’s outputfrom the Nimary and Jundee operations. The yearalso saw production start from the new Dalgarangaand Sunrise Dam projects.

¯ Full production from the Sunrise Dam project,previously estimated at 100,000 ounces per year,is almost certain to rise following a doubling inthe project’s resource to 2.5 million ounces inSeptember 1997.

The 13 biggest producing projects in WesternAustralia accounted for 51% of the State’s goldproduction in 1996/97 (figure 2.9). The largestprojects, with gold production worth over AS 100million in 1996/97 were:

¯ Golden Mile - Kalgoorlie - 26.6 tonnes;

° Kambalda - St 1yes - 13.5 tonnes;

tonnes3OO

GOLD PRODUCTION

250

200

150

lO0

5O

o189o 191o 193o 195o 197o 199o

Source: DME, BMR & ABARE Figure 2.6

° Granny Smith -10.7 tonnes;¯ Teller- 10.3 tonnes;¯ Boddington- 10.3 tonnes;° Plutonic - 7.8 tonnes; and° Bronzewing - 7.1 tonnes

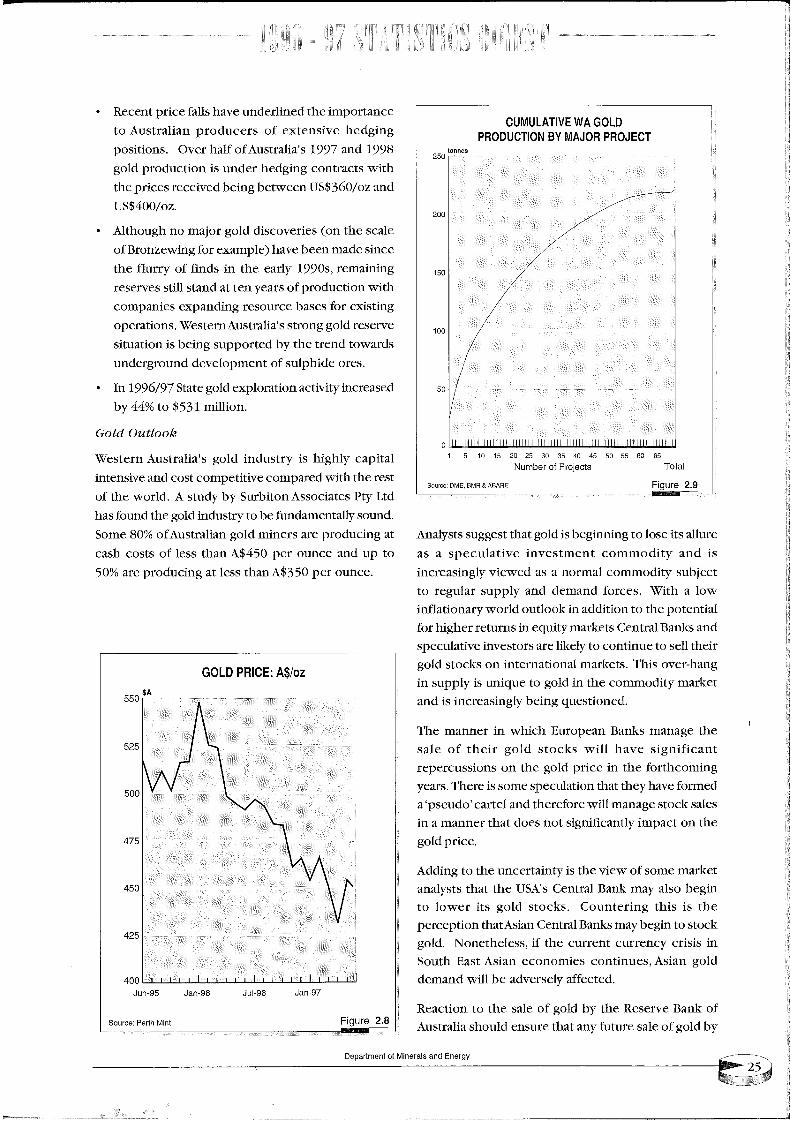

The gold industry has recently been affected by fallsin price (Figure 2.8). The gold price has fallen fromUS$380 per ounce in December 1996 to US$317 perounce on July 9, 1997, its lowest level in four years.

GOLD EXPORTSTOTAL VALUE : A$3,187 MILLION

SouthKorea53.6%

Malaysia3.7%

Singapore22.9%

OthE2.5% Japan

5.0% Hong Kong7.7O/o

Souce DME

Thailand4.5%

The gold price recovered marginally thereafter toaverage US$323.66 per ounce in the September1997 quarter.

The Reserve Bank’s sale of 167 tonnes, whichequated to around 4.4% of the world’s 1996/97 goldsupply, surprised international gold markets andcontributed to the downward pressure on prices.However there have been a number of moreimportant contributors which have adverselyimpacted on gold prices. The most notable of thesehave been gold sales by European Central Banks andthe gold market’s perception that these willcontinue. With European Monetary Union about tocommence European Banks are aiming to divestthemselves of these gold stocks and invest in otherassets (i.e. bonds, futures etc) offering higher returns.

In December 1996 above-ground world gold stockheld by the banking sector totalled 32,800 tonnes.Of this 39% (or 12,792 tonnes) are held by banksin the European Union while another 23% (7,544tonnes) are held by USA banks. Adding the goldstocks (i.e. coin and gold bullion) held by privateinvestors (24,100 tonnes in 1996) the amount ofgold that can be supplied from stock was around57,000 tonnes in December 1996. At the 1996/97fabrication consumption rate of 3,520 tonnes, goldstocks held equate to about 16 years supply.

Department of Minerals and Energy

~6Jeu~ pue Sl£Jeu!~ JO ;UaLU#edeG

6"~ eJn6!-I

lelO/£1oe[oJd ~o JeqLunN

Illl+lllllllHlllHIlillllllllllllllIIIllllltlllllll[litllttllllll[tll

seuuo

/O:lrOSd 8orvR h8 NOI/OllOOSd0"109 VA~ :IAI/V’IN~NO

o£

OOb

0£~

00~

8’g eJn6!-IlU!~ qpad :aoJnos

Z6-uep96-1np96-uep£6-unp00#

00£

¯ aauno aad 0g{$vu~ql ssaI 1~ ~u!anpoad aat %0go1 dn put aauno aad 0g>$V utq! ssaI jo slsoa qs~a1~ ~u!anpoad aa~ saau!m plo~ ut!Falsnyjo %08 amos¯ punos XIItluammptlrU aq o! !~iasnput. pio~ aql punoj s~q

PYl Ald sale!aossvuo!!q.mg Aq Apnls ¥ ’pFo~a aqa jolsaa aql q!!~ paatdmoa aa!l!ladmoa lsoa pu~ aA!sualu!.i~l!dta Xlq~!q s! Xalsnpu! p[o~ s,~!ltalsnv uaalsaAk

alOOllnO plOD

’zo/oo~$gIq_put zo/09~ $SI1 uaaaxaaq ~u!aq palqaaas saa,adql!~ sla~aluoa ~u!~paq aapun s! uo!lanpoad plo~~66I pu~ L66I s,t!I~alsnvJo JFR aaaO "stto!!!sod~u!~paq aA!suaaxa jo saaanpoad u~!Italsn¥ olaaumaodm! aql pau!Fapun aatq SlFJ aa!ad luaaaH

major Central Banks will be done in coordinatedmanner so as to reduce the current volatility in worldgold prices. It is not in the interests of Central Banksto dump gold haphazardly on international marketsas this could open them up to huge losses if the priceof gold were to fall significantly from current levels.World gold market analysts are uniting in their viewthat Central Banks have fixed an unofficial ceilingprice on gold of around US$330 per ounce. Australianproducers are cushioned somewhat from this lowergold price through the AS depreciation in 1997/98.

The likelihood of European Central Banks’ managingthe sale of their gold stocks is further strengthenedby the international market reaction to an October1997 report commissioned by Switzerland’s FinancialMinistry. The Report recommended the sale of 1,400tonnes of gold over a 10 year period commencing1999. While it is only a recommendation, which is yetto be formally considered by the Swiss Governmentand its Central Bank, the Report triggered a fall inthe gold price to US$307/oz in late October 1997,its lowest level in 12 years.

With international markets already concerned over theimpact on Australia’s growth of Asia’s currency crisis,the Report contributed to the AS falling belowUS$0.70. As a result the AS gold price remainedrelatively unchanged with gold trading at aroundA$450/oz in late October 1997.

According to ABARE in 1998 world gold productionis expected to rise by 3.8% to 2,502 tonnes. Demandis forecast to rise by 5.2% to 3,701 tonnes. The supply/demand imbalance will be made up from the sale ofstocks. The price of gold is expected to increase by2,7% to US$345 per ounce in 1998. Nonetheless,ABARE’s forecasts were done prior to the release ofthe Report by the Swiss Financial Ministry.

Despite a low gold price Australian gold productionis forecast byABARE to rise by 5.2% to 314.4 tonnesin 1997/98. A 3.8% depreciation in the US$/A$ will inpart recoup some of the gold price losses recorded inthe second half of 1996/97.

Growth over the next three years will be primarilyderived from existing gold projects and committednew projects. This expected production growth isthe result of several historical factors. Most importantwas the rapid increase in exploration expenditure,which to a large extent brought about the

development of a number of newly discovereddeposits such as Bronzewing (WA), Jundee (WA),Nimary (WA) and Cadia Hill (NSW).

The high levels of exploration expenditure, largelydriven by excellent cash margins, resulted inAustralia’s demonstrated resources ol~gold expandingfrom 2,129 tonnes in 1990 to more than 4,200 tonnesin 1996 - resources on which pr0ductlon growth inthe next three years will be principally based.

Despite the positive short term production outlook,

the Australian gold industry seems to have entered a

period of rising costs. This is a reversal of the early

1990s experience where production costs were falling.

Factors contributing to increasing costs include:

¯ a greater proportion of production being drawnfrom underground and deeper open cutoperations;

¯ increasing depth of operations result inincreased proportion of sulphide ore processedwhich raises processing costs; and

¯ likely increase in depth of new discoveries,raising exploration and mine developmentcosts.

These factors, together with a lower real gold price,are expected to result in a margin squeeze. ABAREforecasts suggest real cash margins for the Australiangold industry will fall byA$40 fromA$131 in 1996 toA$91 in 2002.

The changing world market trading environment forgold is likely, in future, to lead to further amalgamationswithin the Australian gold industry. By doing so theindustry will be able to enjoy better economies ofscale, hence lower production costs. If this strategyis pursued by the industryABARE’s real cash marginforecasts to 2002 are unlikely to eventuate. To date,the most significant amalgamation is betweenNormandy Mining and Great Central Mines. Underan August 1997 deal Normandy Mining will bankrolltwo separate takeover bids by Central Mines worthA$350 million (A$240 million for Eagle Mining andA$110 million for Wiluna Mines Ltd). In return,Normandy will acquire a 25% stake in Central Mines.If Great Central’s takeover bids of Eagle and Wilunaare successful the "amalgamated" company wouldbecome one the world’s largest gold producers. Asof 31 October 1997 the deal was as yet to becompleted.

Department of Minerals and Energy

"/-661 Alaea tu. paauattraxoaApnls Xl.q.tq.~s~aj-aad uo!IlgU OgSVV "mntm~ aadsauuol uo! .lI~tU gI ol dn aanpoad plnoaaa&qt aqo~t Aq ’uo!iI!m 000’I$¥Jo !goa g lg’a.~sodap s~ia~uV lSaA~ aql jo luamdolaaap

:apnptqasaq~ "~!I~alsnv uaalSaOA u.~ uo!!~aap!suoa aapun aopa!!.tmmoa Almaaana aa~ slaa!oad aao uo~jo aaqtunu V

¯ paa!nbaa osF s.~ L!!a~d~a ~u!p~oI pu~ ~uT.I!d~Iaolsaao jo uo!su~dxa aaaqax ’aa!dm~(I jo laodol a .trgu oopu~aa~l~ luasaad aq! moaj :$*O~AlaU~r4.1s!xa aql Jo tlo!sualxa ttDt£}I ~ snId Jlasl! au.tmaq! aq lI.~ax lsoa laa[oad aq! ~o luauodtuoa u!~tu aqx’666I u.t oa~aals uo amoa o! palaadxa s! aao uoa! jotuntra~ aad atraol UO!l~.m ~ I ~anpoad laa[oad uo.q .I~gOkSVaq~ ’sagqI!d aql u.~ au!m aao uoa! gu!~ooa!pugxaql doIaaap plno~ 1! !~ql paaunouu~ UOalXalsaatu~H ~66I aaqmaldas tq punoa$~Ia~q s!q!

’aIqranoag, IXlamaaaxa s.~ Xaasnpu! aao uoa! S,alglg aql aoj~tOOlmO aql’e.tsVaOJ Alaglna!aaed’sagaA aA.tj 1xagt aq! aojls~aaaoj la~ta~ttt Iaals 8m.uoaSanq ~ ql.DA "adoan,q o!sao~ aapm.~tuaa aql al!q~ g!svaoJ pau.tlsap aag slaodxa

qf!H ’#odekl xe± :aoJnoS

Z6-uep96-1np96-uep£6-1np

9~

L~

8~

l!un e-I/s|ueo :~OIEld iiIElO NOEII

6~

~ I.’~ eJn6H

SIUaO

o

o£g

0SL I

O~

o~

o~

000’ ~UO!ll!~l V$

~a|~eno ~q anle^ pue uo!lonpoM~]l:lO NOEII

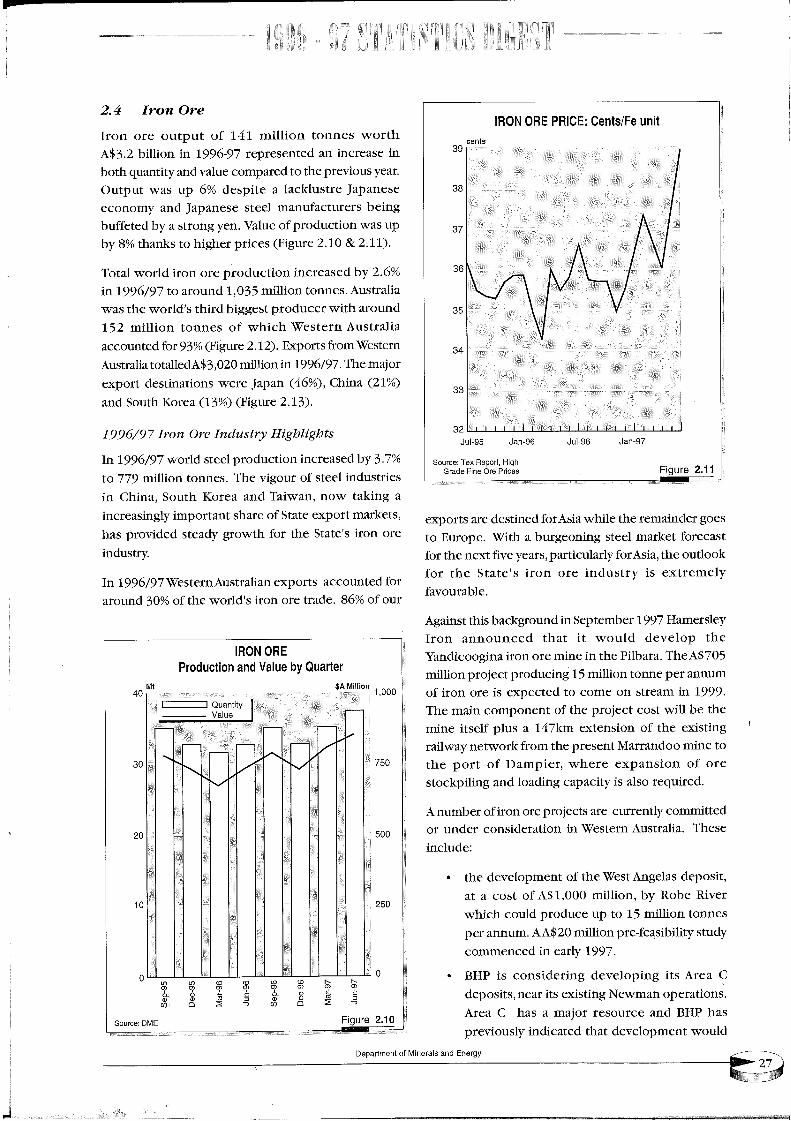

ano ~o %98 ’apgal aao uoa.~ s,pIao~ aq! jo %0{ punoagaoj palunoaa~ slaodxa ug!IgalsnvuaalSaAk k6/966T uI

’Aalsnpm.aao uo.q s,al~lg aql itoJ ql~xoa~’sla~la~m laodxa al~lg jo aa~qs lt,~laodtu.~g ~u!:,Iga ~ou ’ug~x!g~L pug gaao2,I qanos ’gu!qDsa!.ugnpu! iaaas jo ano~!a atlZ ’gauuo! uo!I .lYtU

%L’{ Xq pagga.I~u! uo!aanpoad iotas plao~/_6/966t uI

slqCd.zlqcd.ZH £zlsnpuI aaO uoaI Z6/9661

’({T’Z aan~H) (%{T) gaao2� qlnos pug(%TE) g~qD ’(%9~) ugdgf aaaax suo!lgu!lsap !aodxaao!~m at[L ’L6/966T m. uo!ii.~tu O~0’{$¥PalimO!uaalsaA~ moa~ slaodx.q "(~’Z aan~!~ %{6 aoj palunoaa~g!lgalsnv uaa!saAk qa!qax jo sauuol UO!lI!m EgTpunoae ql!ax aaanpoad !sa~!q pa.~q! s,plaom aqleWalsnv "gauuoa uo! .llFtU g{O’[ punoa~ ol L6/966I

%9"g Xq pag~aaau! uo!lanpoad aao uoa.t plaom ImOX

’Q T’E :~ OT’Z aan~.EI) saa!ad aaq~!q o1 s~tugqa %8 Xqdn sgax uo!aanpoad jo anFA "uaA ~uoals g Xq paaajjnq~u!aq saaanla~jnu~tu Iaaas asauedef pue Xmouoaaasauedef aalsnppeI ~ a!!dsap %9 dn s~ax lndlno:¢~aX sno!aaad aql o1 paaedmoa anFa pue Xl!ltr~nb qaoq~ as~aaau.t u~ paauasaadaa L6-966I u.t UO!lI!q ~’{$Vqlao~a sauuol tIo!lI!tt~ I}[ jo lndlno aao uoaI

/

be in the realm of a 4-5 million tonne a yearoperation, increasing to about 20 million tonnesas demand allowed. BHP is also likely toconsider expanding its Yandi mine from itspresent 15 million tonnes to 35 million tonnesif iron ore demand strengthens.

¯ BHP has committed itself to developing, at acost of AS50 million, the Newman (Orebody18) deposit. Construction commenced inAugust 1997 with the 5 million tonnes perannum mine expected to be operational inJanuary 1998.

° Hancock Resources is also studying a A$450million project aimed at developing the HopeDowns iron ore deposits. If it proceeds theproject could produce up to 30 million tonnesof iron ore per year.

The range of new projects in the Pilbara eithercommitted or under consideration raises the need toseriously consider options such as stand alone, sharingor paralleling of rail facilities in this region. At a costof around A$1 million per line-km, rail makes up asignificant part of capital costs for these projects.Linkages by existing producers are already plannedto spread east and south. Hamersley’s Iron’s spur lineto Marandoo for example, is to be extended to theeast using the infrastructure corridor across KarijiniNational Park, whilst further extensions of BHP’s spurline from the existing Yandi mine to Mining Area Care being planned. The progressive development ofthese infrastructure networks could potentially

IRON ORE EXPORTSTOTAL VALUE : A$3,020 MILLION

Japan46.1

Others0,9%

ChinaEurope 20.6%13.5%

S. Korea Taiwan13.4% 5.4%

Souoe DME ~ I

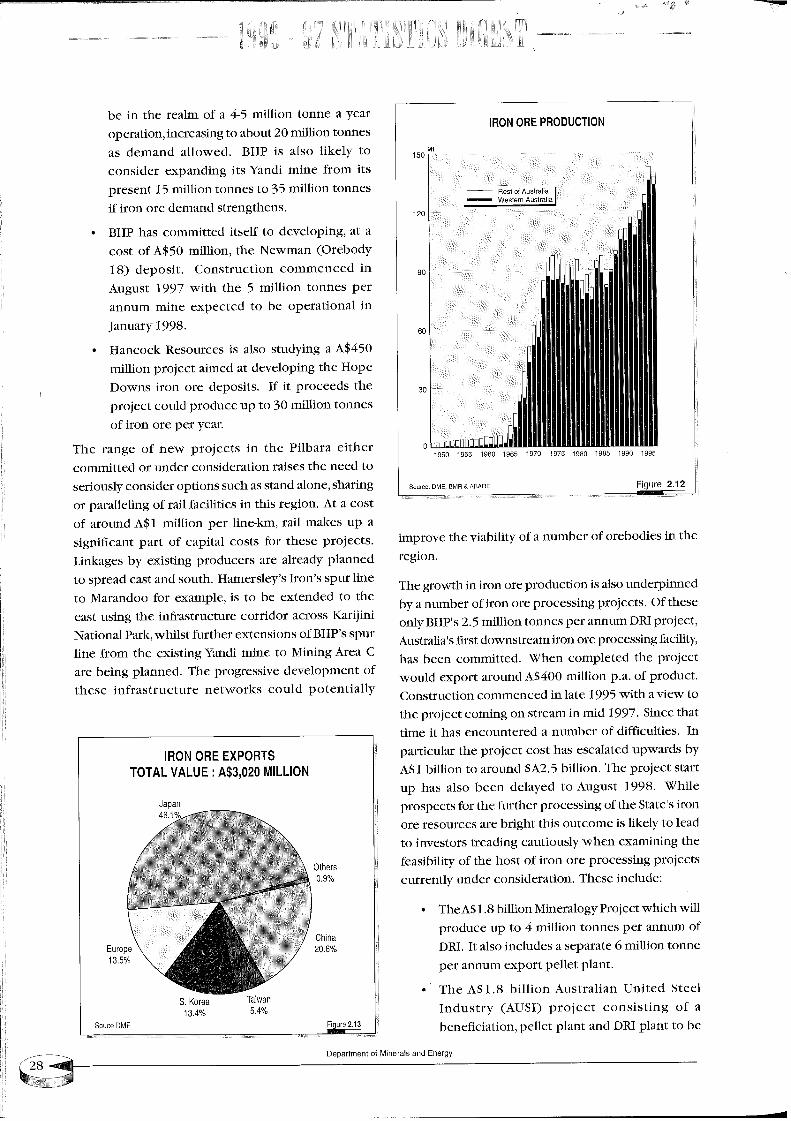

IRON ORE PRODUCTION

Mt150

~ Rest of Australia

90

60

1950 1955 1960 1965 1970 1975 1980 1985 1990 1995

Seurce: DME, BMR & ABARE Figure 2.12

improve the viability of a number of orebodies in theregion.

The growth in iron ore production is also underpinnedby a number of iron ore processing projects. Of theseonly BHP’s 2.5 million tonnes per annum DRI project,Australia’s first downstream iron ore processing facility,has been committed. When completed the projectwould export around A$400 million p.a. of product.Construction commenced in late 1995 with a view tothe project coming on stream in mid 1997. Since thattime it has encountered a number of difficulties. Inparticular the project cost has escalated upwards byA$1 billion to around $A2.5 billion. The project startup has also been delayed to August 1998. Whileprospects for the further processing of the State’s ironore resources are bright this outcome is likely to leadto investors treading cautiously when examining thefeasibility of the host of iron ore processing projectscurrently under consideration. These include:

The AS 1.8 billion Mineralogy Project which willproduce up to 4 million tonnes per annum ofDR[. It also includes a separate 6 million tonneper annum export pellet plant.

The A$1.8 billion Australian United SteelIndustry (AUSI) project consisting of abeneficiation, pellet plant and DR[ plant to be

Department of Minerals and Energy

uoa! ~!d pus RIO ss qans

a!alaala aq ol lssaaaoj aas 010g Aq sassaaoad ~UplStU

Iaals us!sVJO %0{ Xlalstu.~oaddv ’sassaaoadIaals aasua~g aas a!aaaala o1 slj!.qs Alaslna!aasd’~uptstu

Iaaas u! slj!qs Isa!~olouqaal Aq ’aanlnj tg. ’pau.taao~ aqII!ax (Pd(I) uoa! paanpaa laaa!p aoj pustuap pIaom

"g661 u! uo!II!m 6{g’{$V o1%I’E[ Xq assaaau! ol palaadxa s! slaodxa aao uoa! joanFa aq!’$Vaaa~oI g t[l!~ pau!qmoa ’saa!ad aao uoa!tq asia %I’I s jo ~tasq aq! uo "8661 m. %9’g Aq as!a olslaodxa aao uo.q tts.qsalsnvlsgaaaoJ sgq ~IV~V ’866[ u~.%{’g Aq asia ol lssaaaoj uo!lanpoad iaals plaoat ql!Ak

lUallaaXa s! Xalsnpu! aao uoa!s,almS aq! ao3 ~IooDno aq! ’saaoN put ug~!s~’su!qDu! Xlaslna!lagd’apgaap lxau aql aaao s!s¥ u! palaadxas! uo!ldmnsuoa Iaals m. q!a~oa~ ao!gm 1gill tlaA!9

alOoHno

saaanpoad lIs!lgalsnv IIJalSa~ O1

sttanlaa aql u! lasd ltIg!aodttt! US SXsld alga a~usqaxa

~o ;uemlJede(]

s! saa!ad aao uoa! alslS aamaU aoj ~toollno

666I pus 866[ u! saaoN pus usax!ga;’s .uvqD m. an~luoaol paDadxa q!axoa~ pustuap aao uoa! ~uoals ql!A~¯ aao atttj Sl! aoj assaaau! %}’1 s paanaas aaapd aqo11put aao dtunI aoj aa!ad 966I Adf aq! u! aaaOllOa s ’aaoatu./aoj %I’I jo asia s pau!glqo uoaI XalSaamSH pusdHIt "866t qa.~slN o!/66I F.advtuoaj aa!laajja aag putasaA aq! aoj atuoamo alqsanoaN s axes saaanlaNnustuiaals asausdsf pus saaanpoad aao uoa! us!Isalsnv Xqsuo!lsDo~au aa!ad aao uo.q jo punoa k661 Msnugf atlj;

laodxa aoj I~I(I josatmol uo! .llgU EI’0 put l!.Oa PallOa lOqjO tuntrugaad sauuol uo!II!tu k{’I aanpoad II!ax1sag aR~ ’tugtI~Uppol[ lss~ ls palsaoI laa!oadIaalg lasdmoD Ilt(I/Iaalg uo!II!q 6}’15V atI~;

¯ uolpFaa9 asau aa!s~FO ao s~IoouooXuoo!Naaql!a ls palsaoI Al!I!aSJ Ilt(1 tunuusaad auuo! uo!II!tU E s olu! paj pus uosq!91IN ls pau!m aq pinata aao uoaj. tstll patmglds! 1I ’laa[oad Pd(I uosq!9 1IN uo..gl!tu 006$vaq~ ¯

’uolplgaa9

mgaals~u!N ~Uad uv uo!IlIm O0~’gSV aq~L

"I11(Uou~nuus aad satmol UO!lI.rtu } lsotuF ~u!anpoad

2.5 Alumina

The State’s alumina output increased by around 1.5% toreach 8.3 million tonnes. Average contract pricesreceived byAustralian producers in 1996-97 were up by3% on the previous year. Total value of production wastherefore higher by 2% to reachA$2 billion (Figure 2.14).Again, this value could have been greater had it notbeen for the offsetting effect of an appreciatedAustralian currency in 1996-97.

WesternAustralia produced 63% of Australia’s aluminain 1996/97 (Figure 2.15).

Around 90% of the State’s production was exportedoverseas. The USA (29%), SouthAfrica (17%), Canada(16%) and Bahrain (9%) were the State’s predominantalumina export markets (Figure 2.16).

1996/9 7 Alumina Industry Highlights

In 1996/97 world alurnininm markets were buoyant.

Production and consumption increased by 3.0% and

4.3% respectively but more importantly aluminiumstocks have been falling. Stocks are expected to fall

to around 6.5 weeks of consumption by the end of

1997, down from 7.9 weeks in 1996. Nonetheless,there is still some speculation in the market that not

all aluminium stocks are accounted for.

With a number of capacity expansions the aluminiumprice fell by 9% to average US$1,513 per tonne in

ALUMINAProduction and Value by Quarter

Mt SA Million600

2.0

1.5

1,0

0.5

5O0

400

300

2O0

100

Source: DME Figure 2.14

1996/97. However the underlying demand strengthin the aluminium market, largely driven by OECD andUSA consumption growth, has resulted in substantialprice increases in the September 1997 quarter, withthe aluminium price closing above US$1,600 pertonne.

ALUMINA PRODUCTION

Mt

12

1960 1965 1970 1975 1980 1985 1990 1995

Source: DME, BMR & ABARE Figure 2,15

In the first half of 1996/97, the alumina market wasalso highlighted by downward pressure on the worldspot price which emanated from increased capacityas producers began to restart projects which weremothballed by the memorandum of understandingreached between aluminium world producers overtwo and a half years ago. With rising demand andcapacity constraints emerging in the second half of1996/97, world alumina spot prices began to risemarkedly (Figure 2.17). Over 1997ABARE has forecastalumina prices to rise by 27% to US$221 per tonne in1997.

In a nutshell, the consensus of forecasters is that in1997/98 both LME and producer aluminiuminventories should decline further as world economicgrowth translates into increased orders for aluminiumproducts by manufacturers.

Manufacturers are also expected to rebuild stocks toensure they can meet rising demand. This translatesinto a positive 1997/98 market outlook for alumina.

Department of Minerals and Energy

~6Jeu9 pue SleJeu!~ jo lueLupedeG

lL’g eJnl~!-I3NVSV :aoJno£

Z6-uep96-1np96-uep£6-1np00~

’I~I00I’EE oaAq asta o1 paaaadxa st uotlanpoad AI~u!puodsaaaoD’/_6/966I uo %9I dn ’auuo! aad I9/-’I $SFI a~gaaag olpmaadxa s! aa!ad aql 86/L66I m. l~t0gI’~ ol %k’{ Aqas!a o1 lsgaaaoj uotldmnsuoa mntu!tunlg plaom

alooBno

3~1~ oono£%6"L%#’9

e!seuopul

qlno£

%6

UO!ll!~ £LL’LSV : onleA lelOiS/HOdXa VNIOnlV

¯ ranting aad sauuo! UOfllttU {’{ ol lndlnoluaJana slt alqnop lsOtUlg plnoax S!ql a~ms puoaasapnput o1 aaam uotsugdxa aql JI ’Altagdga uotlanpoadgt .munlg pFoax aqljo a.tgqs %g~ s!! ol red,no jo sauuol000’0g~ PPg PIhoax uo!sugdxa aBg!s lsa!j uo!II!m0g9$Vaq£ ’Aaau!jaa gutumlg dnaa~e~sl! jo uo!sugdxauOtllttU Ok6$V a~glg-O~al pasodoad g ~u!aap!suoas! ’goaIV ’aaanpoad gu!mnlg aaqlo s,alglg

apgaap g ugql aaom aoj uo!~aa lsaAxqlnoss,almS aq! m. aaa[oad luamdolaaap aaanosaa lsa~agI aqls! uo!sugdxa AalgaOAX aq~L "Fuo!leaadoaauo pa*oldma Og I qlDa suosaad 000’I s! aaaoJ~taoa~uo!aana!suoa ~Igad aq~L "O00E agaX aql aoj paaa~amuo!laldmoa qlpa L66I aaqolao ut lag!s ol palaadxast uotlanalsuoD ’axou mnuug aad gauuoa uotlI!mgk’I tuoaj dn ’agaA aad sauuo! uo! .llfms,Xaau!jaa aql alqnop lSOmlg |IDA uo!sugdxa¯ XaautJaa g!! jo uo!sugdxa uo!iltm OOR$Ve paaunouugAalgaoAx L66I aaqmaadag ut ’auaas igaoi aql uO

growth forecasts have been wound down. Thesituation surrounding Russia is also unclear,specifically, no one is sure of the country’s indigenousdemand situation and hence, Russian metal availablefor export. Foremost is the question regarding howquickly the amount of idle capacity will be returnedto production. Currently around 800,000 tonnes ofworldwide smelter capacity remains idle. The highcost nature of some of this may prevent it from beingrestarted, but considerable potential still exists foradditional production to come on stream relativelyquickly.

The longer term outlook is that high prices willcertainly encourage at least some new production andrising stocks, especially after 1999. This will putrenewed downward pressure on prices depending onthe extent to which current smelter expansions goahead.

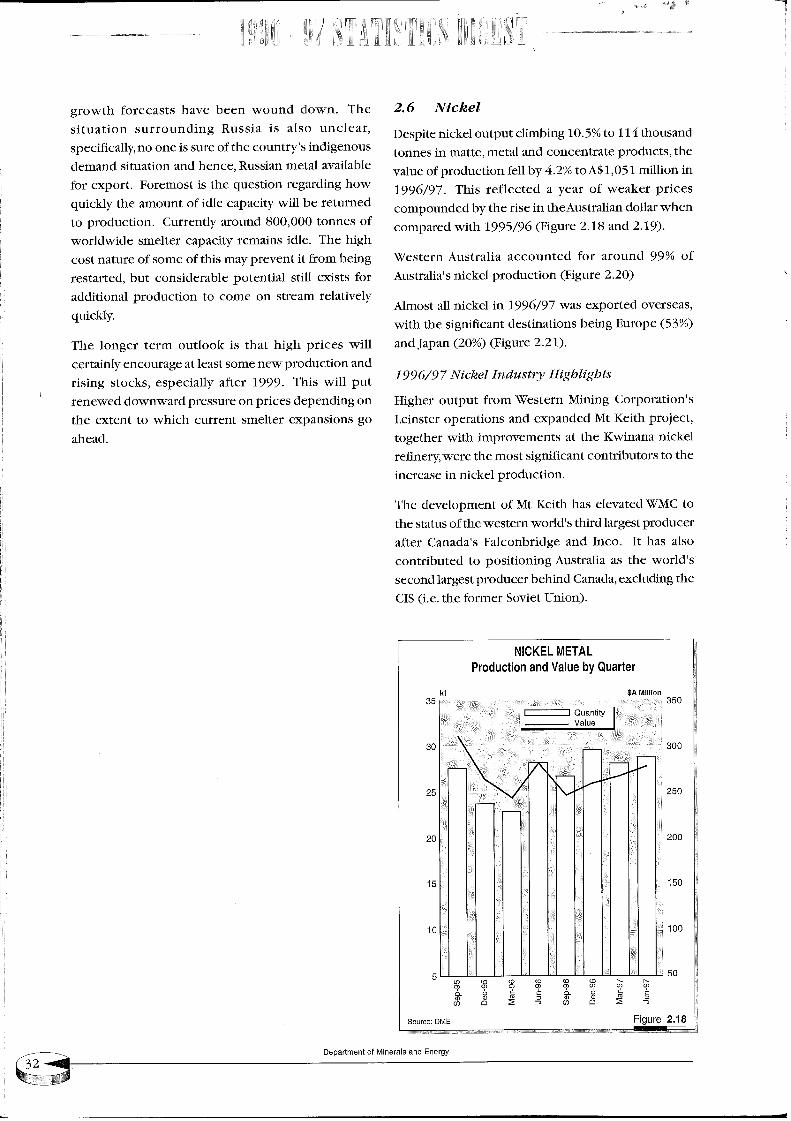

2. 6 Nickel

Despite nickel output climbing 10.5% to 114 thousandtonnes in matte, metal and concentrate products, thevalue of production fell by 4.2% toA$1,051 million in1996/97. This reflected a year of weaker pricescompounded by the rise in theAustralian dollar whencompared with 1995/96 (Figure 2.18 and 2.19).

Western Australia accounted for around 99% ofAustralia’s nickel productiorf (Figure 2.20)

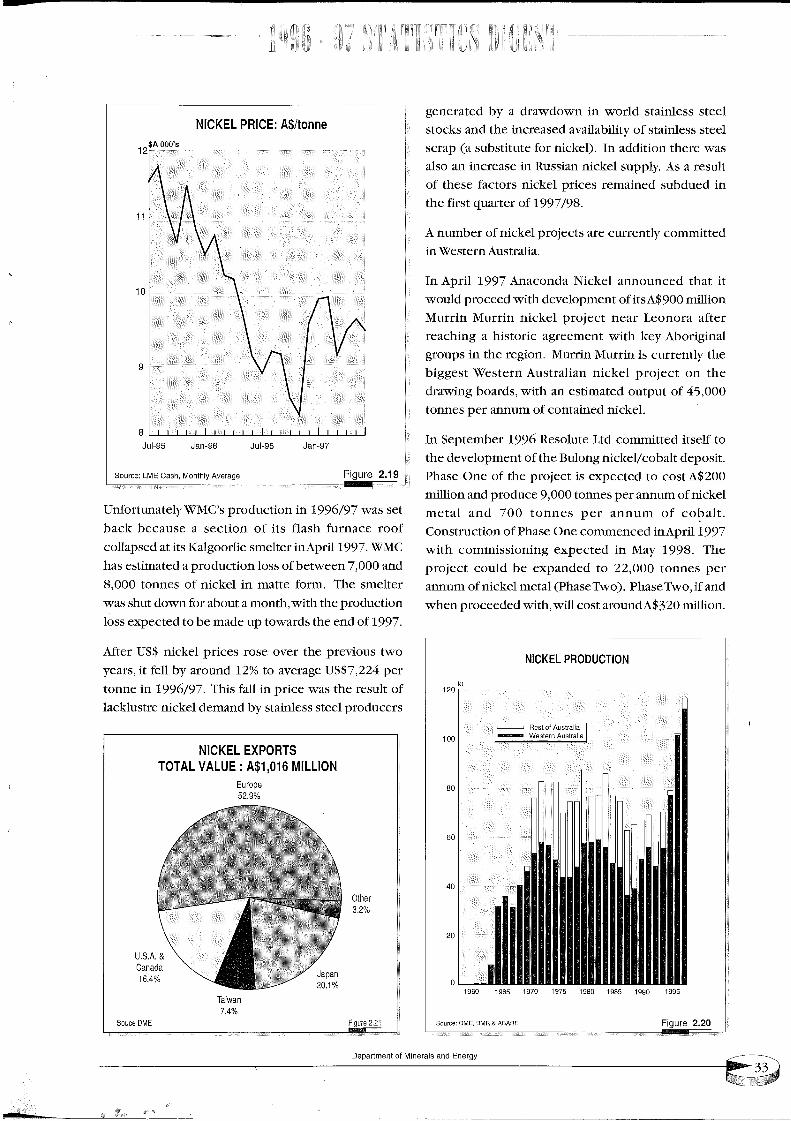

Almost all nickel in 1996/97 was exported overseas,with the significant destinations being Europe (53%)and Japan (20%) (Figure 2.21).

1996/97 Nickel Industry Highlights

Higher output from Western Mining Corporation’sLeinster operations and expanded Mt Keith project,together with improvements at the Kwinana nickelrefinery, were the most significant contributors to theincrease in nickel production.

The development of Mt Keith has elevated WMC tothe status of the western world’s third largest producerafter Canada’s Falconbridge and Inco. It has alsocontributed to positioning Australia as the world’ssecond largest producer behind Canada, excluding theCIS (i.e. the former Soviet Union).

35

NICKEL METALProduction and Value by Quarter

$A Million350

Quantity

25 250

20 200

10 : : : 100

Source: DME Figure 2.

Department of Minerals and Energy

0~’~ ran!!4

0

O~

09

08

NOllOnOOEld 7~DIOIN

a!8(l eono£

JeLI~O

%67£edmn9

NOI’I’IIIR 9W~$V : ~tn’IVA "IV±01Sl~lOdX~ 7=I)IOlN

"uo!I .lgtU 0g{$vpunoat lgoa lI!~’ql!~ papaaaoad uaq~put j.~’o~j~ agtqd "(oH astqd) It!am Ia}Ia!u jo mnuutaad sauuol 000’gg ol paputdxa aq plnoa !aa!oadaqJ~ "866I AtI~ u! palaadxa ~u!uo!s~!mmoa q!!~/-66I lJ.advu! paauammoa auo agtqd jo uo!!ana!suoD¯ !it4oa jo mnuut aad gauuoa 00/- put ltlamia~ia!u jo tuntmt aad gatmo1000’6 aanpoad put uo..qlFtU00gSV !soa o! palaadxa g.~ laa!oad aql jo auo agttId¯ lFodap !ltqoa/la~Ia!U ~uoln{t aq! jo luamdoIaaapo! jlagl! pall.nJJmOa prl amloga~I 9661 aaqmaldag uI

pal!!mmoa Xtluaaana aat glaa!oad Ia}p!u jo aaqmnu V

’/-66t jo pua aq! spat~o! dn aptm aq o! palaadxa ssoIuo!!anpoad art1 tll!~’qluotu t lnoqt aoj u~op lnqg gl~aa!iams aqj~ ’tuaoj allttu u! Ia~ta!u jo sauuo! 000’8put 000’/- uaa~laq jo gso[ tIo!lanpoad t paltttq.lga g~ttDI~Ak ’/-66I l!advu! aalIares aRaoo~FN ~!! It pa~dtlIOa

la~ st~/-6/966I u! uo!Dnpoad ~,DI~AkXlaltunl.~oJUCl

6 V~ eJn6[z]a6ma^v ~lqlUOlA] ’qseo 91A17 :eoJno8

Z6-uep96-1rip96-uep96-1np

8

ouuo1/$V ::~OIl:ld "I=I)IOlN

0~

The A$220 million Cawse nickel/cobalt project isexpected to be commissioned in August 1998. The

project will produce 8,700 tonnes per annum of

nickel and 2,000 tonnes per annum of cobalt (as

sulphide).

Significantly, Bulong, Murrin Murrin and Cawse, arebased on laterite ores. These have been previouslyshunned by Australian producers in favour of moreeasily treated sulphide deposits. The processingmethod proposed for these new laterite nickelprojects inWesternAustralia has the potential to altersignificantly the State’s nickel supply picture.

Some market analysts suggest that because of theimproved processing method, the unit costs of theselaterite deposits will be around US$1/lb less than thoseof Western Mining’s Kambalda operations,which havebeen estimated at US$2.18/lb in 1997/98.

Long term price uncertainty threatens the worldnickel market because a number of projects arecoming on stream, the most important of which isCanada’s Voisey Bay project (discussed below).

The low unit cost of the Bulong, Muffin Murrin andCawse projects will shelter them from a substantialfall in the world nickel price which in June 1997 wasaround US$ 3.25/lb.