Embed Size (px)

Citation preview

Analysts Meet – Non Fuel Initiatives

3rd August 2016

1

No information contained herein has been verified for truthfulness completeness, accuracy, reliability or

otherwise whatsoever by anyone. While the Company will use reasonable efforts to provide reliable

information through this presentation, no representation or warranty (express or implied) of any nature is

made nor is any responsibility or liability of any kind accepted by the Company or its directors or

employees, with respect to the truthfulness, completeness, accuracy or reliability or otherwise

whatsoever of any information, projection, representation or warranty (expressed or implied) or

omissions in this presentation. Neither the Company nor anyone else accepts any liability whatsoever for

any loss, howsoever, arising from use or reliance on this presentation or its contents or otherwise arising

in connection therewith.

This presentation may not be used, reproduced, copied, published, distributed, shared, transmitted or

disseminated in any manner. This presentation is for information purposes only and does not constitute

an offer, invitation, solicitation or advertisement in any jurisdiction with respect to the purchase or sale of

any security of BPCL and no part or all of it shall form the basis of or be relied upon in connection with

any contract, investment decision or commitment whatsoever.

The information in this presentation is subject to change without notice, its accuracy is not guaranteed, it

may be incomplete or condensed and it may not contain all material information concerning the Company.

We do not have any obligation to, and do not intend to, update or otherwise revise any statements

reflecting circumstances arising after the date of this presentation or to reflect the occurrence of

underlying events, even if the underlying assumptions do not come to fruition.

Disclaimer

1

2

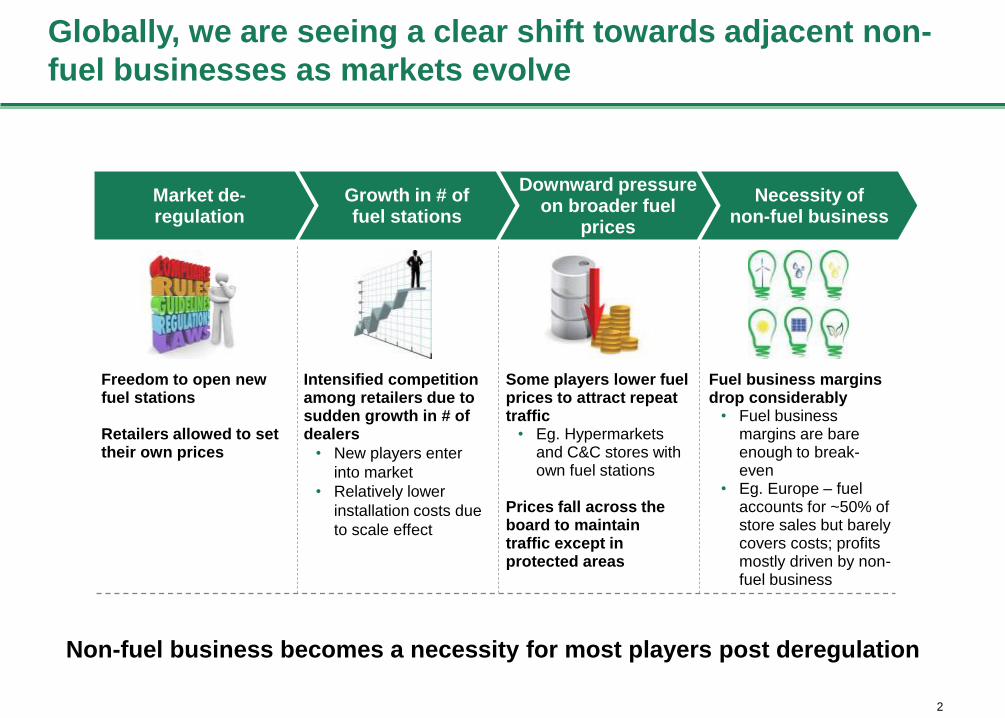

Globally, we are seeing a clear shift towards adjacent non-

fuel businesses as markets evolve

Freedom to open new fuel stations

Retailers allowed to set their own prices

Intensified competition among retailers due to sudden growth in # of dealers

• New players enter

into market

• Relatively lower

installation costs due

to scale effect

Some players lower fuel prices to attract repeat traffic• Eg. Hypermarkets

and C&C stores with own fuel stations

Prices fall across the board to maintain traffic except in protected areas

Fuel business margins drop considerably • Fuel business

margins are bare enough to break-even

• Eg. Europe – fuel accounts for ~50% of store sales but barely covers costs; profits mostly driven by non-fuel business

Market de-regulation

Growth in # of fuel stations

Downward pressure on broader fuel

prices

Necessity of non-fuel business

Non-fuel business becomes a necessity for most players post deregulation

3

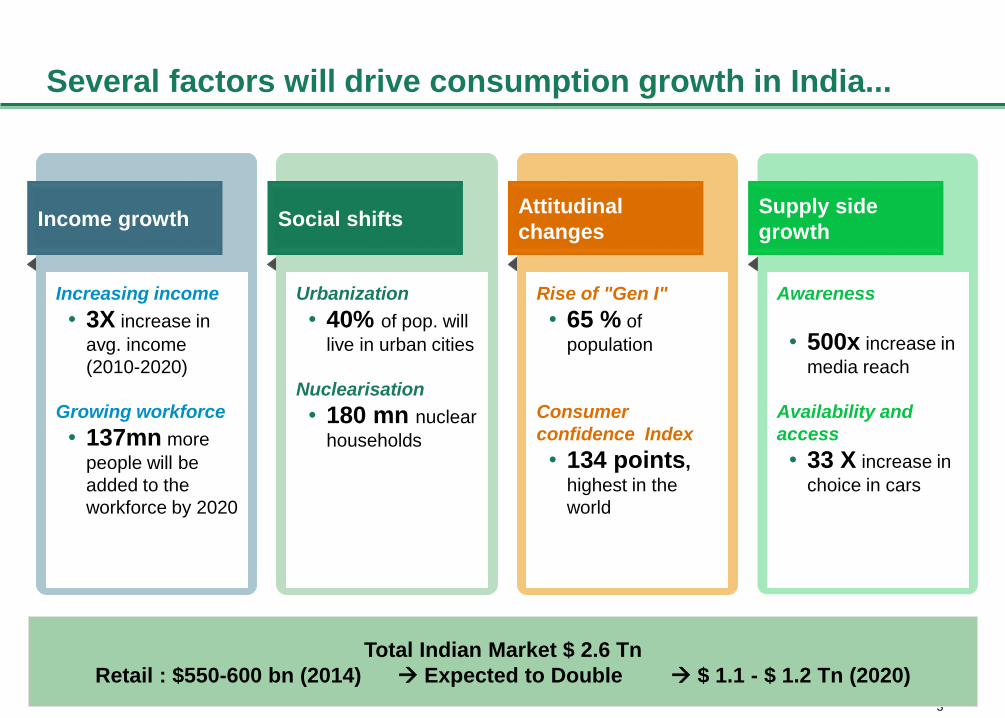

Several factors will drive consumption growth in India...

Income growth

Increasing income

• 3X increase in

avg. income

(2010-2020)

Growing workforce

• 137mn more

people will be

added to the

workforce by 2020

Social shifts

Urbanization

• 40% of pop. will

live in urban cities

Nuclearisation

• 180 mn nuclear

households

Attitudinal

changes

Rise of "Gen I"

• 65 % of

population

Consumer

confidence Index

• 134 points,

highest in the

world

Supply side

growth

Awareness

• 500x increase in

media reach

Availability and

access

• 33 X increase in

choice in cars

Total Indian Market $ 2.6 Tn

Retail : $550-600 bn (2014) Expected to Double $ 1.1 - $ 1.2 Tn (2020)

4

Project Nishchay

5

Rural marketplace

Integrated fleet management

Personal travel offering

Urban household solutions

6

Rural marketplace

Integrated fleet management

Personal travel offering

Urban household solutions

7

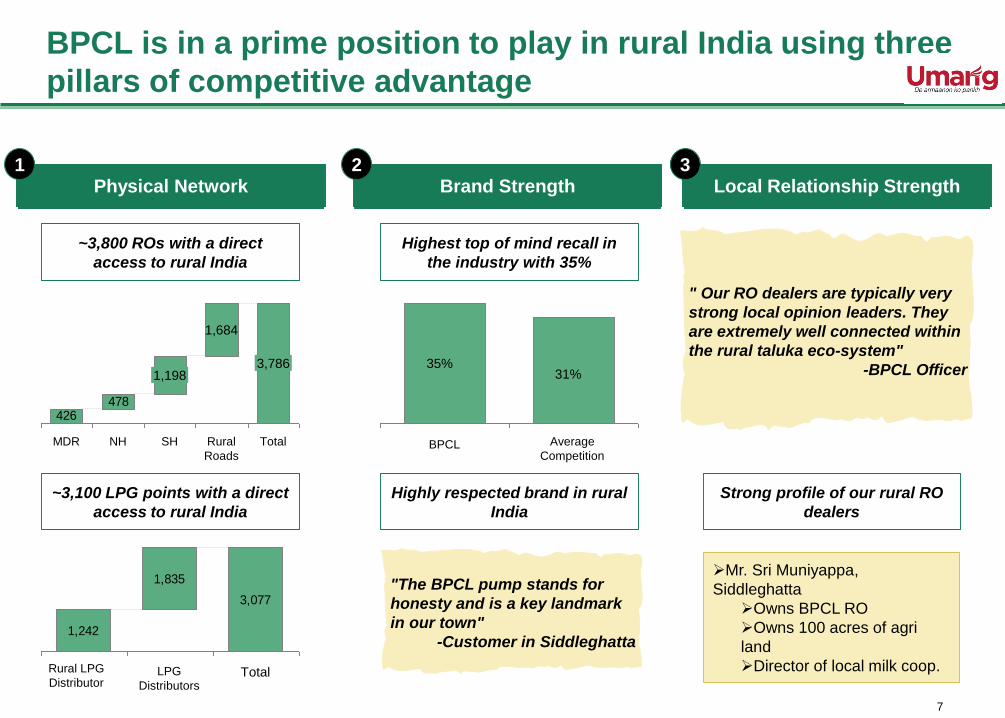

BPCL is in a prime position to play in rural India using three

pillars of competitive advantage

Physical Network

~3,800 ROs with a direct

access to rural India

~3,100 LPG points with a direct

access to rural India

Brand Strength

35%

Average

Competition

31%

BPCL

Highest top of mind recall in

the industry with 35%

Highly respected brand in rural

India

Local Relationship Strength1 2 3

" Our RO dealers are typically very

strong local opinion leaders. They

are extremely well connected within

the rural taluka eco-system"

-BPCL Officer

Strong profile of our rural RO

dealers

Mr. Sri Muniyappa,

Siddleghatta

Owns BPCL RO

Owns 100 acres of agri

land

Director of local milk coop.

"The BPCL pump stands for

honesty and is a key landmark

in our town"

-Customer in Siddleghatta

478426

3,786

Total

1,684

Rural

Roads

MDR SH

1,198

NH

1,242

1,835

3,077

Rural LPG

DistributorTotalLPG

Distributors

8

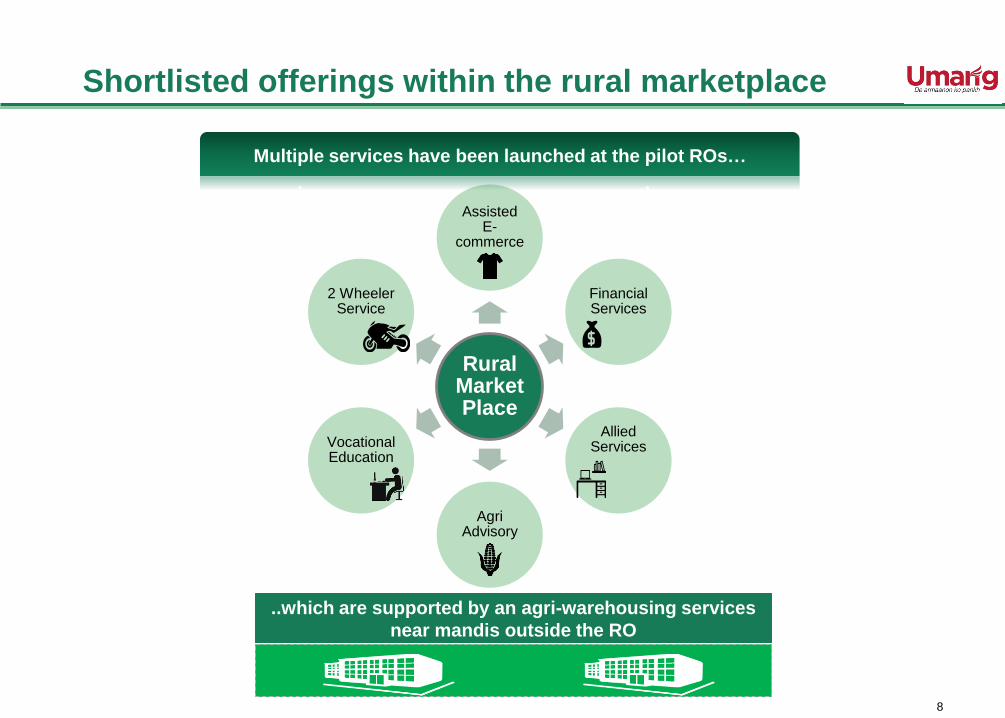

Rural MarketPlace

Assisted E-

commerce

Financial Services

Allied Services

AgriAdvisory

Vocational Education

2 Wheeler Service

Shortlisted offerings within the rural marketplace

Multiple services have been launched at the pilot ROs…

..which are supported by an agri-warehousing services

near mandis outside the RO

9

10

11

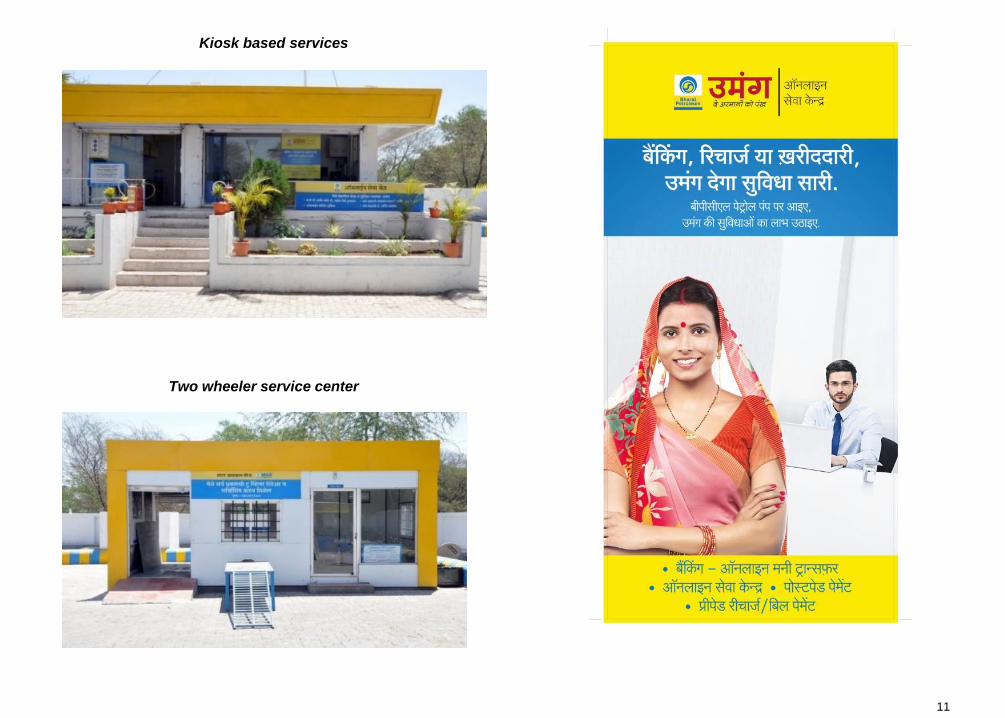

Kiosk based services

Two wheeler service center

12

Rural marketplace

Integrated fleet management

Personal travel offering

Urban household solutions

13

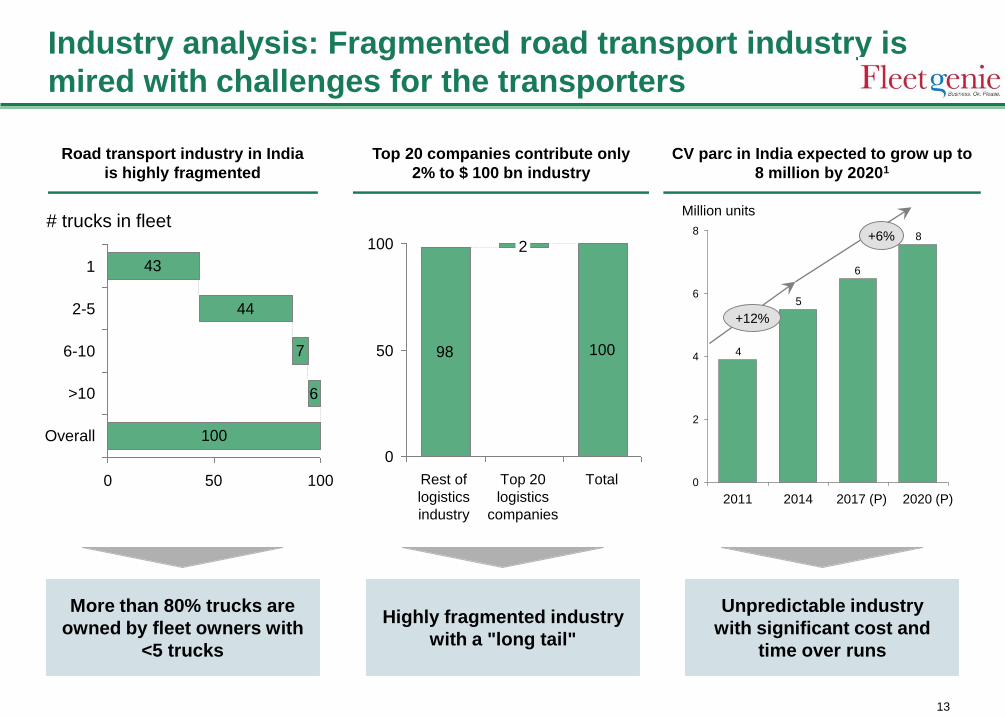

43

44

7

6

100

0 50 100

# trucks in fleet

2-5

1

Overall

>10

6-10

More than 80% trucks are

owned by fleet owners with

<5 trucks

Industry analysis: Fragmented road transport industry is

mired with challenges for the transporters

Highly fragmented industry

with a "long tail"

Unpredictable industry

with significant cost and

time over runs

Road transport industry in India

is highly fragmented

Top 20 companies contribute only

2% to $ 100 bn industry

98 100

0

50

100

Rest of

logistics

industry

2

Top 20

logistics

companies

Total

8

6

5

4

0

2

4

6

8

+12%

Million units

2014

+6%

2020 (P)2017 (P)2011

CV parc in India expected to grow up to

8 million by 20201

14

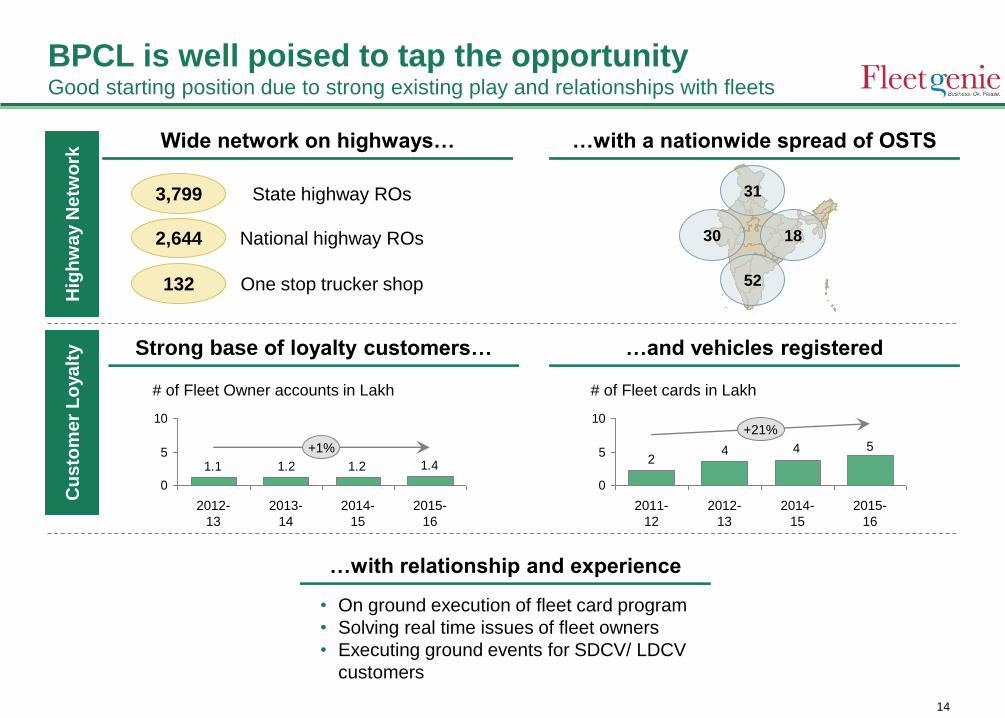

BPCL is well poised to tap the opportunityGood starting position due to strong existing play and relationships with fleets

Hig

hw

ay N

etw

ork

Cu

sto

me

r L

oya

lty

3,799

2,644

132

State highway ROs

National highway ROs

One stop trucker shop

30

52

18

31

1.41.21.21.1

0

5

10

# of Fleet Owner accounts in Lakh

+1%

2012-

13

2013-

14

2015-

16

2014-

15

442

5

0

5

10

# of Fleet cards in Lakh

+21%

2014-

15

2012-

13

2011-

12

2015-

16

• On ground execution of fleet card program

• Solving real time issues of fleet owners

• Executing ground events for SDCV/ LDCV

customers

Wide network on highways… …with a nationwide spread of OSTS

Strong base of loyalty customers… …and vehicles registered

…with relationship and experience

15

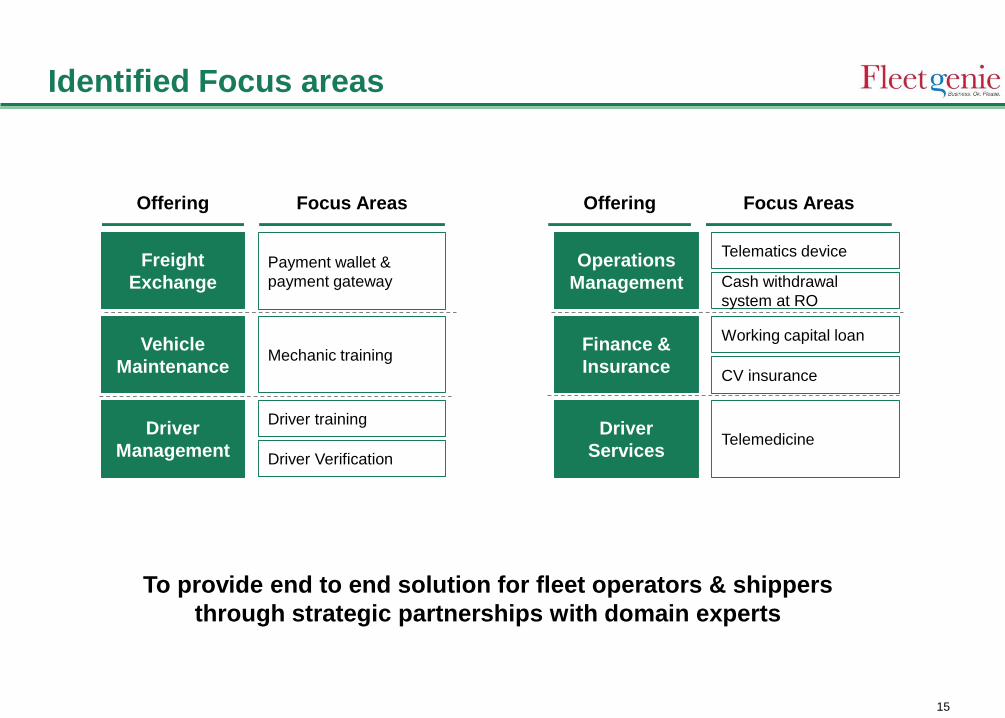

Identified Focus areas

Freight

Exchange

Vehicle

Maintenance

Driver

Management

Operations

Management

Driver

Services

Offering Focus Areas

Payment wallet &

payment gateway

Mechanic training

Driver training

Driver Verification

Telematics device

Cash withdrawal

system at RO

Telemedicine

Finance &

Insurance

Working capital loan

CV insurance

Offering Focus Areas

To provide end to end solution for fleet operators & shippers

through strategic partnerships with domain experts

16

• Enhance customer base and fuel wallet share of fleet owners in emerging competitive scenario

• Increase fuel sales & alternative revenue potential for dealers through services at RO

• Increase lubricant visibility & sales through empanelled QSCs & FSCs

• Increase business relationship with BPCL B2B customers by enrolling as shipper for freight exchange

Our Aspiration

Drive sales &

customer

relationship

for core

businesses

~1000

ROs

~500

kiosks

~400

QSCs

~Top 20

NH

15 K+

fleet

customers

~100

FSCs

Fleet genie is the #1 fleet management brand delivering end-to-end solutions

to drive greater customer engagement and loyalty in 5 years

17

Rural marketplace

Integrated fleet management

Personal travel offering

Urban household solutions

18

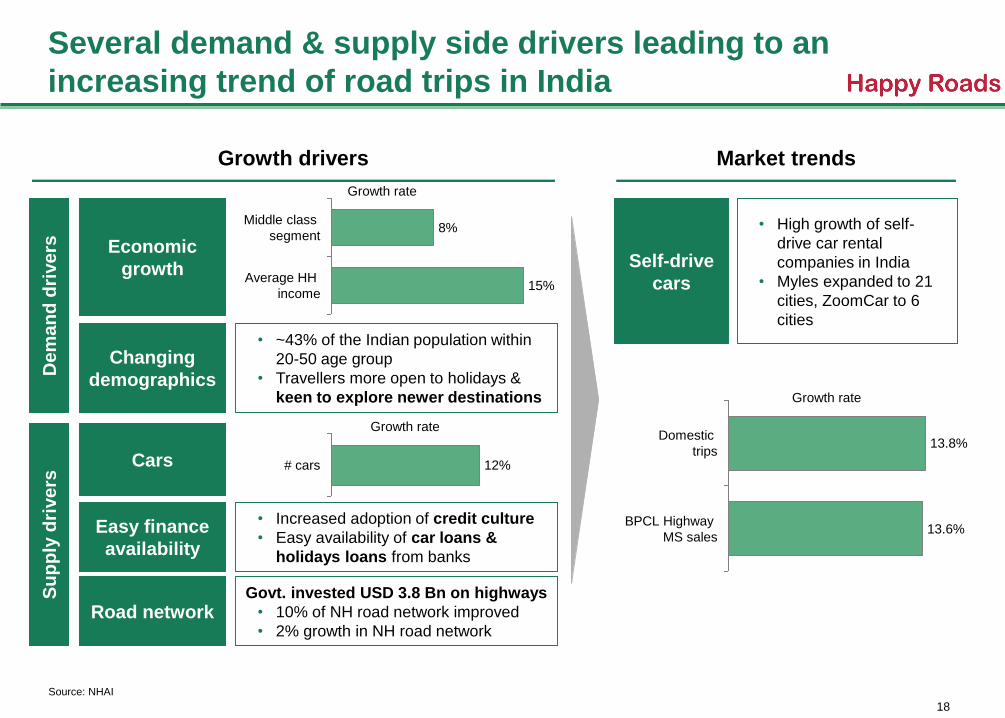

Several demand & supply side drivers leading to an

increasing trend of road trips in India

Growth drivers Market trends

• ~43% of the Indian population within

20-50 age group

• Travellers more open to holidays &

keen to explore newer destinations

• Increased adoption of credit culture

• Easy availability of car loans &

holidays loans from banks

Middle class

segment8%

Growth rate

Average HH

income15%

Growth rate

# cars 12%

Economic

growth

Changing

demographics

Easy finance

availability

Cars

De

ma

nd

dri

ve

rsS

up

ply

dri

ve

rs

Road networkGovt. invested USD 3.8 Bn on highways

• 10% of NH road network improved

• 2% growth in NH road network

Self-drive

cars

• High growth of self-

drive car rental

companies in India

• Myles expanded to 21

cities, ZoomCar to 6

cities

Domestic

trips13.8%

Growth rate

BPCL Highway

MS sales13.6%

Source: NHAI

19

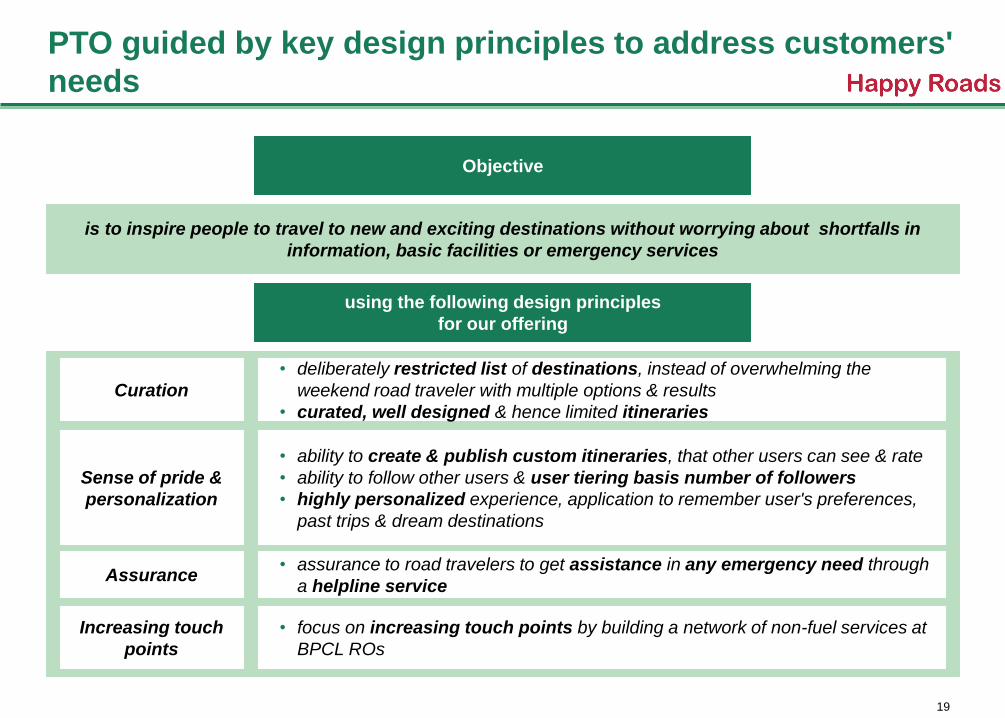

PTO guided by key design principles to address customers'

needs

Objective

is to inspire people to travel to new and exciting destinations without worrying about shortfalls in

information, basic facilities or emergency services

using the following design principles

for our offering

Sense of pride &

personalization

• ability to create & publish custom itineraries, that other users can see & rate

• ability to follow other users & user tiering basis number of followers

• highly personalized experience, application to remember user's preferences,

past trips & dream destinations

Curation

• deliberately restricted list of destinations, instead of overwhelming the

weekend road traveler with multiple options & results

• curated, well designed & hence limited itineraries

Increasing touch

points

• focus on increasing touch points by building a network of non-fuel services at

BPCL ROs

Assurance• assurance to road travelers to get assistance in any emergency need through

a helpline service

20

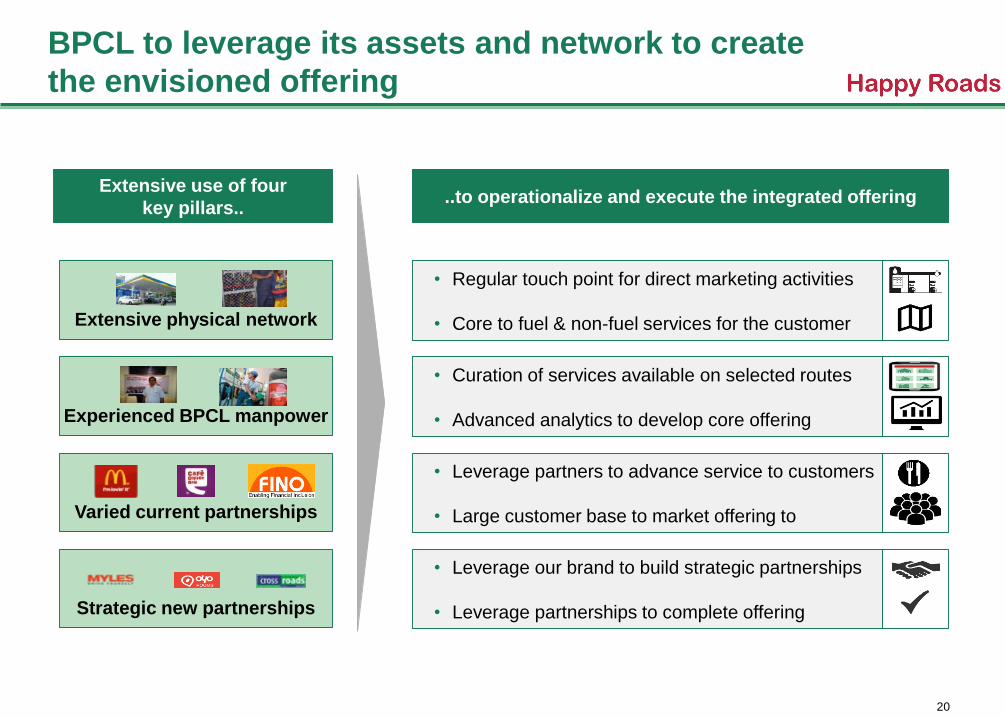

BPCL to leverage its assets and network to create

the envisioned offering

Extensive use of four

key pillars....to operationalize and execute the integrated offering

Extensive physical network

• Regular touch point for direct marketing activities

• Core to fuel & non-fuel services for the customer

Experienced BPCL manpower

• Curation of services available on selected routes

• Advanced analytics to develop core offering

Varied current partnerships

• Leverage partners to advance service to customers

• Large customer base to market offering to

Strategic new partnerships

• Leverage our brand to build strategic partnerships

• Leverage partnerships to complete offering

21

Bengaluru selected as pilot location due to favourable

demographics, avenues for tourism & BPCL strengths

Bengaluru

High Employment, car ownership

• 44% of total population engaged in regular

employment

• 1.1 Mn car owners among 3.8 Mn working

population

Young and Digitally Savvy

• 54% population in 20-50 age group

• 36% households with internet penetration

• 26% of population employed in IT

Favourable

Demographics

Tourist

destinations

`Multiple tourist destinations nearby

• Mysuru

• Ooty

• Coorg

• Pondicherry

• Kochi

• Madurai

• Tirupati

• Shivasamudram

falls

• Hogenakkal falls

• Hampi

BPCL network

Strong BPCL network in & around Bengaluru

• 118 retail outlets in Bengaluru

• 2 OSTTS around Bengaluru – BP Channapatna, BP Hosur

Potential for tie-

ups

Easy availability of start-ups & businesses across different business ideas for potential

partnerships, e.g. self-drive cars, driver on demand, trip planning, etc.

Young and Digitally savvyHigh employment, car ownership

Strong BPCL network in & around Bengaluru

22

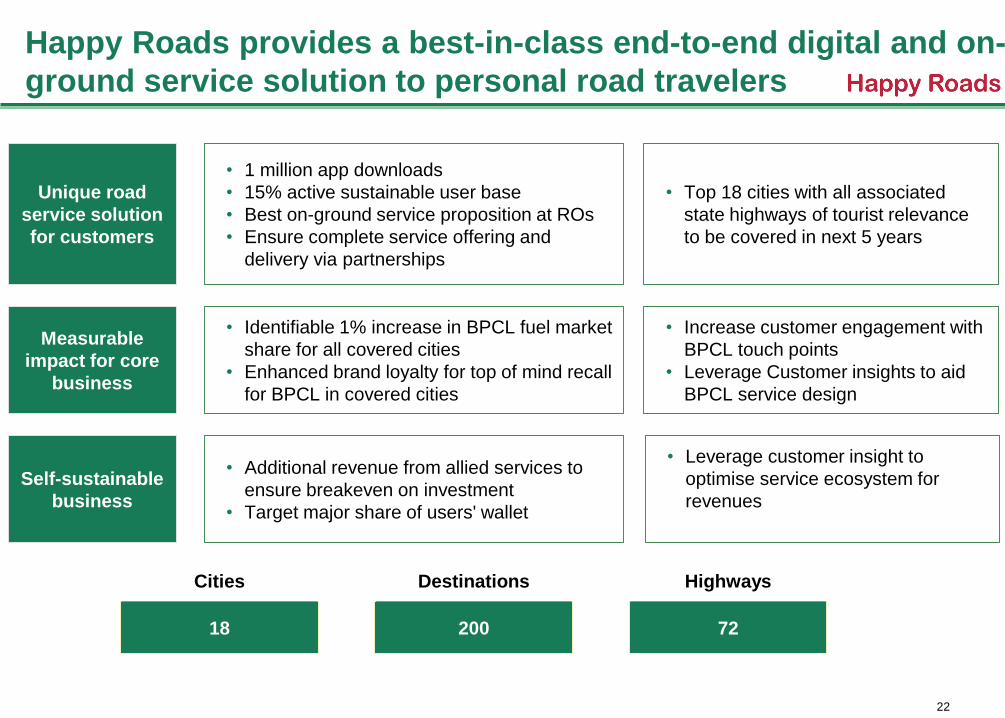

Happy Roads provides a best-in-class end-to-end digital and on-

ground service solution to personal road travelers

Unique road

service solution

for customers

Measurable

impact for core

business

Self-sustainable

business

• 1 million app downloads

• 15% active sustainable user base

• Best on-ground service proposition at ROs

• Ensure complete service offering and

delivery via partnerships

• Identifiable 1% increase in BPCL fuel market

share for all covered cities

• Enhanced brand loyalty for top of mind recall

for BPCL in covered cities

• Additional revenue from allied services to

ensure breakeven on investment

• Target major share of users' wallet

• Top 18 cities with all associated

state highways of tourist relevance

to be covered in next 5 years

• Increase customer engagement with

BPCL touch points

• Leverage Customer insights to aid

BPCL service design

• Leverage customer insight to

optimise service ecosystem for

revenues

7220018

HighwaysDestinationsCities

23

Rural marketplace

Integrated fleet management

Personal travel offering

Urban household solutions

24

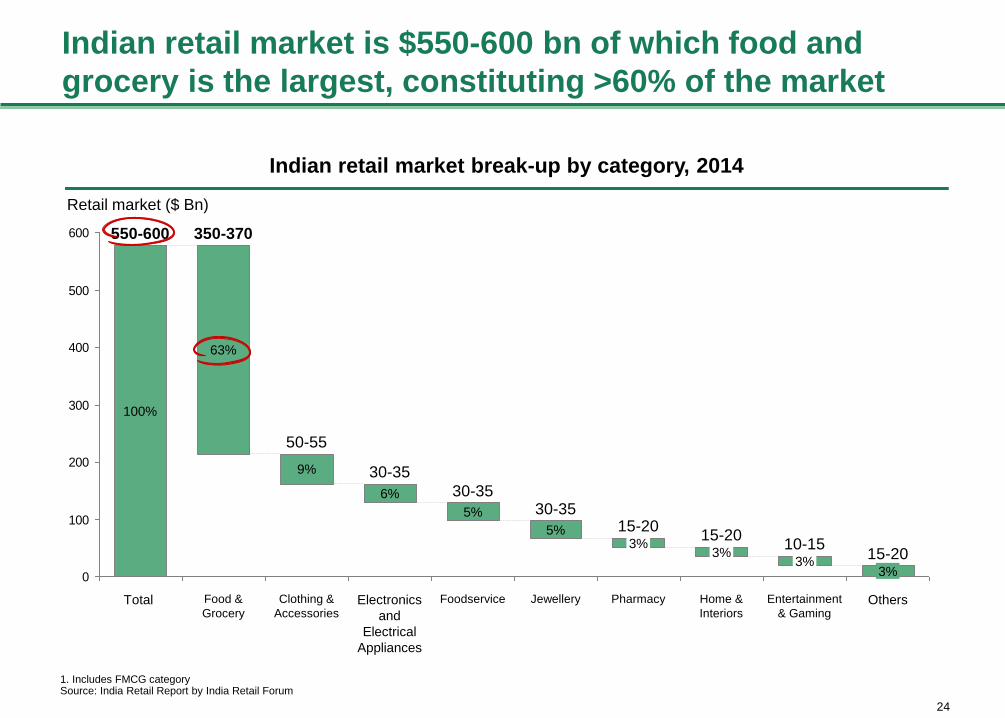

Indian retail market is $550-600 bn of which food and

grocery is the largest, constituting >60% of the market

Indian retail market break-up by category, 2014

1. Includes FMCG category Source: India Retail Report by India Retail Forum

0

100

200

300

400

500

600

10-153%

Home &

Interiors

15-203%

Pharmacy

15-203%

Jewellery

30-35

5%

Foodservice

30-35

5%

Electronics

and

Electrical

Appliances

30-35

6%

Clothing &

Accessories

50-55

9%

Retail market ($ Bn)

350-370

63%

Total

550-600

Food &

GroceryOthers

15-203%

Entertainment

& Gaming

100%

25

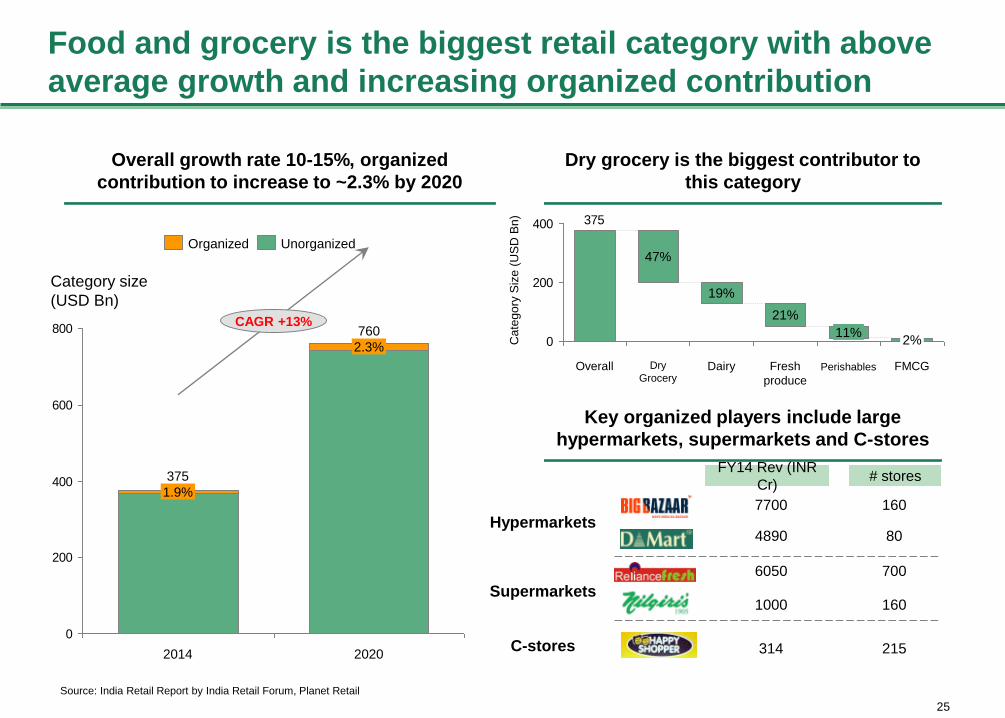

Food and grocery is the biggest retail category with above

average growth and increasing organized contribution

Overall growth rate 10-15%, organized

contribution to increase to ~2.3% by 2020

Dry grocery is the biggest contributor to

this category

0

200

400

600

800

Category size

(USD Bn)

CAGR +13%

2020

760

2.3%

2014

375

1.9%

UnorganizedOrganized

375

0

200

400

Cate

go

ry S

ize

(U

SD

Bn

)

FMCG

2%

Perishables

11%

Fresh

produce

21%

Dairy

19%

Dry

Grocery

47%

Overall

Source: India Retail Report by India Retail Forum, Planet Retail

Key organized players include large

hypermarkets, supermarkets and C-stores

Hypermarkets

FY14 Rev (INR

Cr)# stores

Supermarkets

C-stores

7700 160

804890

6050 700

1000 160

314 215

26

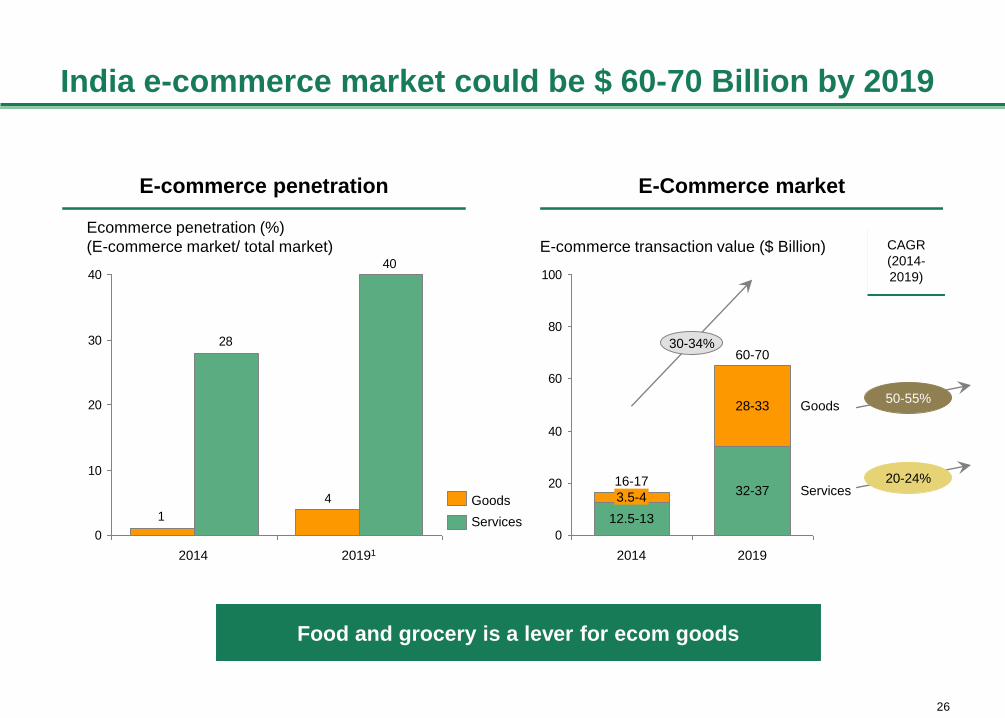

India e-commerce market could be $ 60-70 Billion by 2019

E-commerce penetration E-Commerce market

0

20

40

60

80

100

E-commerce transaction value ($ Billion)

30-34%

Services

Goods

2019

60-70

32-37

28-33

2014

16-17

12.5-13

3.5-44

1

40

28

0

10

20

30

40

Ecommerce penetration (%)

(E-commerce market/ total market)

201912014

Services

Goods

50-55%

20-24%

CAGR

(2014-

2019)

Food and grocery is a lever for ecom goods

27

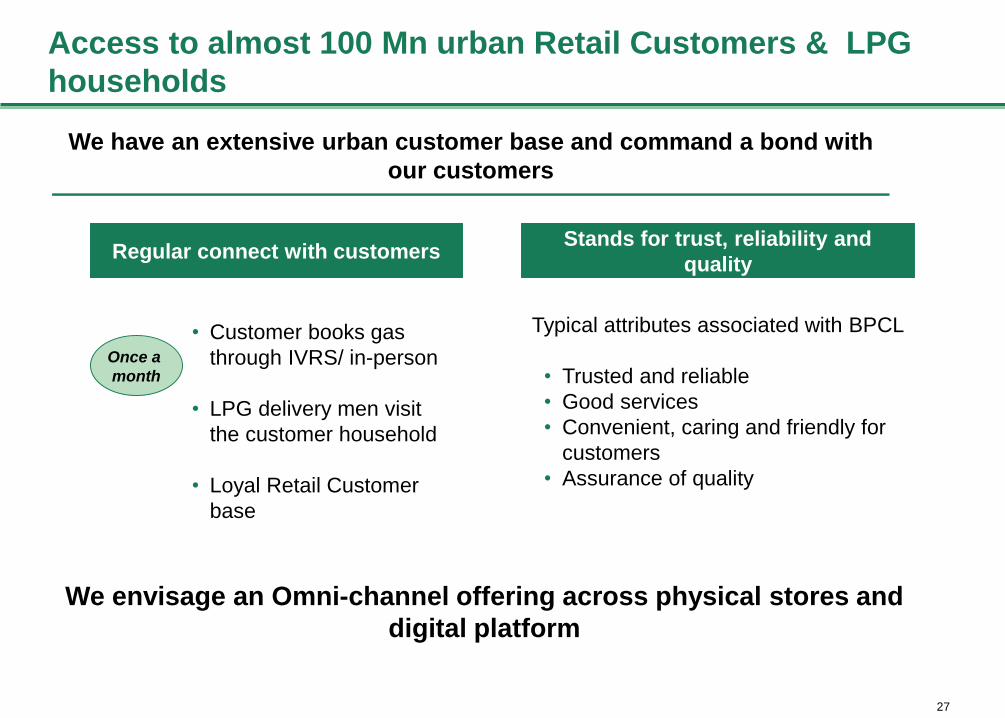

Access to almost 100 Mn urban Retail Customers & LPG

households

We have an extensive urban customer base and command a bond with

our customers

Regular connect with customers

Typical attributes associated with BPCL

• Trusted and reliable

• Good services

• Convenient, caring and friendly for

customers

• Assurance of quality

• Customer books gas

through IVRS/ in-person

• LPG delivery men visit

the customer household

• Loyal Retail Customer

base

Once a

month

Stands for trust, reliability and

quality

We envisage an Omni-channel offering across physical stores and

digital platform

28

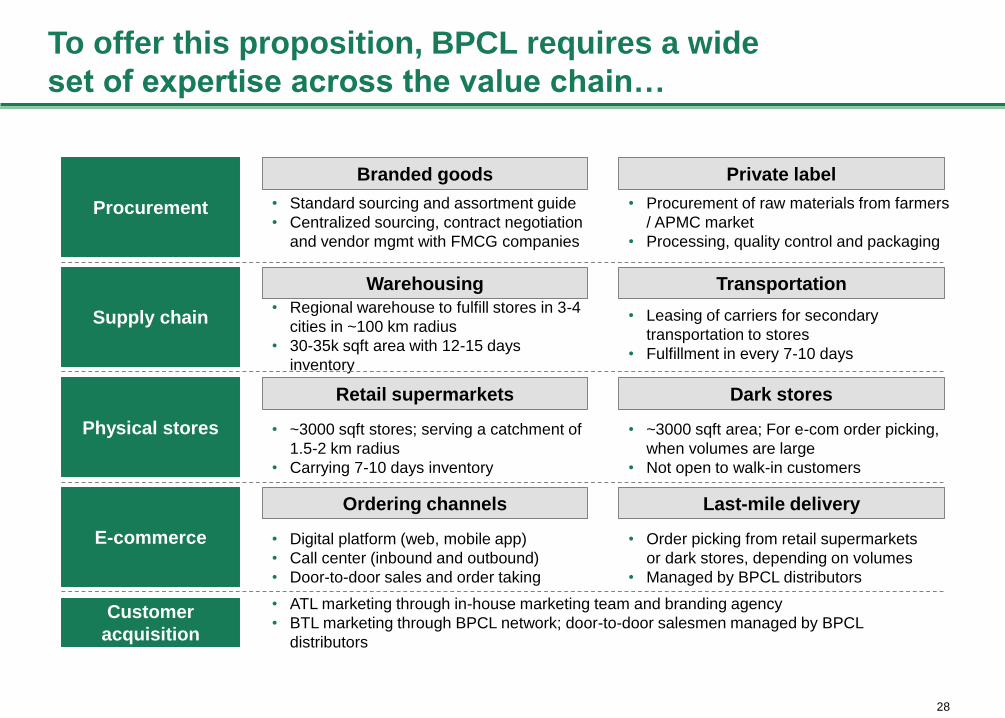

To offer this proposition, BPCL requires a wide

set of expertise across the value chain…

Procurement

Supply chain

Branded goods Private label

• Standard sourcing and assortment guide

• Centralized sourcing, contract negotiation

and vendor mgmt with FMCG companies

• Procurement of raw materials from farmers

/ APMC market

• Processing, quality control and packaging

Warehousing Transportation

• Regional warehouse to fulfill stores in 3-4

cities in ~100 km radius

• 30-35k sqft area with 12-15 days

inventory

• Leasing of carriers for secondary

transportation to stores

• Fulfillment in every 7-10 days

E-commerce

Ordering channels Last-mile delivery

• Digital platform (web, mobile app)

• Call center (inbound and outbound)

• Door-to-door sales and order taking

• Order picking from retail supermarkets

or dark stores, depending on volumes

• Managed by BPCL distributors

Physical stores

Retail supermarkets Dark stores

• ~3000 sqft stores; serving a catchment of

1.5-2 km radius

• Carrying 7-10 days inventory

• ~3000 sqft area; For e-com order picking,

when volumes are large

• Not open to walk-in customers

Customer

acquisition

• ATL marketing through in-house marketing team and branding agency

• BTL marketing through BPCL network; door-to-door salesmen managed by BPCL

distributors

29

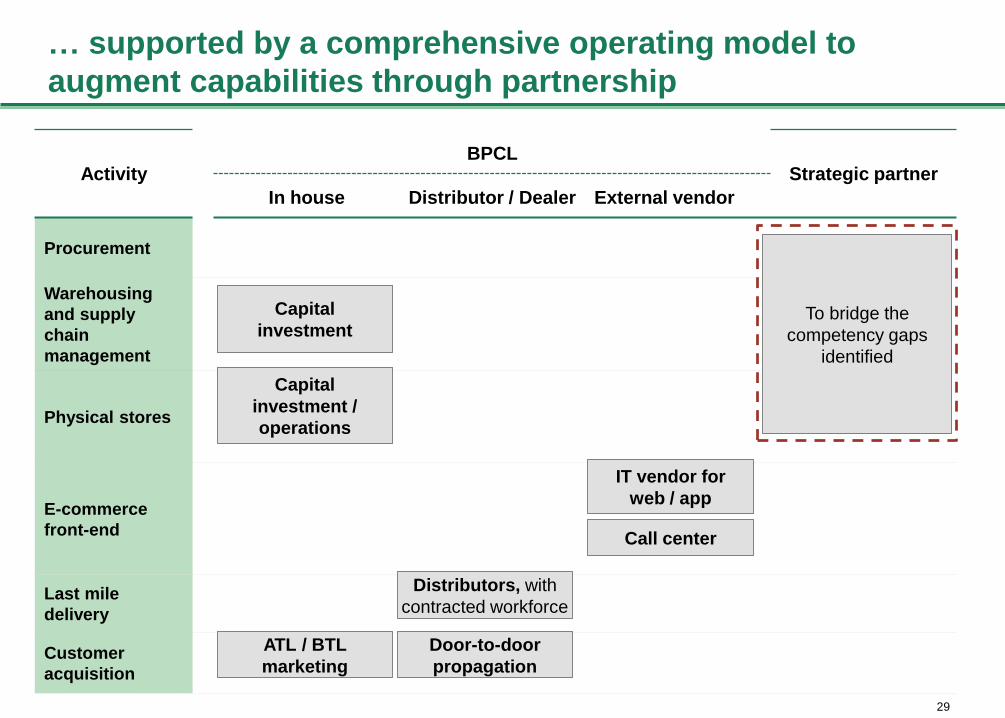

… supported by a comprehensive operating model to

augment capabilities through partnership

ActivityBPCL

Strategic partner

In house Distributor / Dealer External vendor

Procurement

Warehousing

and supply

chain

management

Physical stores

E-commerce

front-end

Last mile

delivery

Customer

acquisition

Capital

investment

Capital

investment /

operations

IT vendor for

web / app

Call center

Distributors, with

contracted workforce

ATL / BTL

marketing

Door-to-door

propagation

To bridge the

competency gaps

identified

30

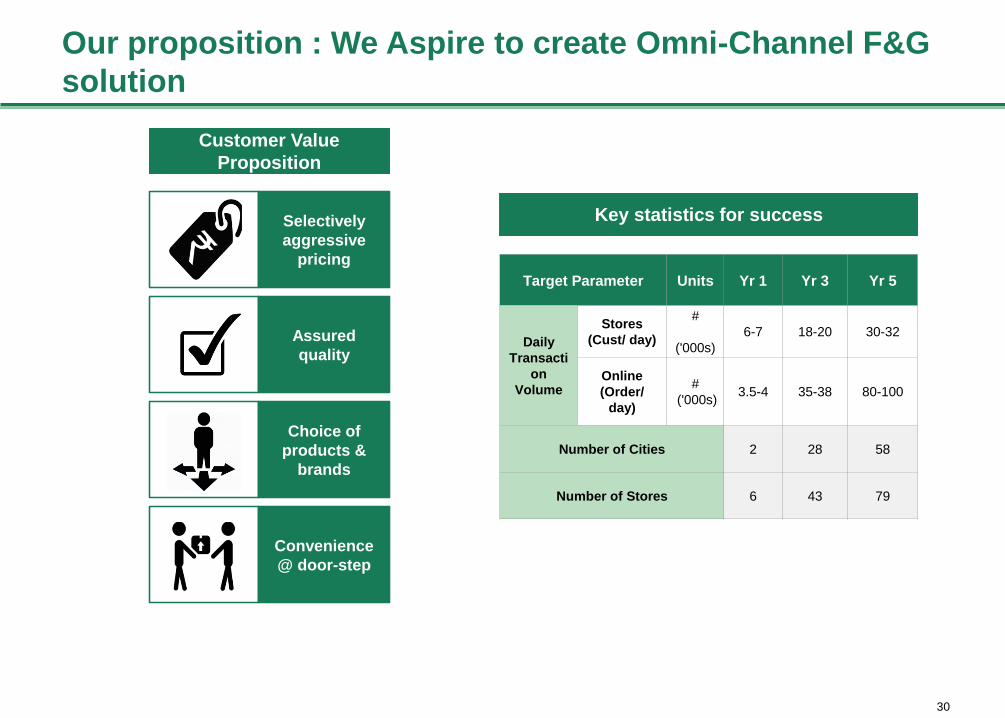

Our proposition : We Aspire to create Omni-Channel F&G

solution

Choice of

products &

brands

Assured

quality

Selectively

aggressive

pricing

Convenience

@ door-step

Customer Value

Proposition

Target Parameter Units Yr 1 Yr 3 Yr 5

Daily

Transacti

on

Volume

Stores

(Cust/ day)

#

('000s)

6-7 18-20 30-32

Online

(Order/

day)

#

('000s)3.5-4 35-38 80-100

Number of Cities 2 28 58

Number of Stores 6 43 79

Key statistics for success

31

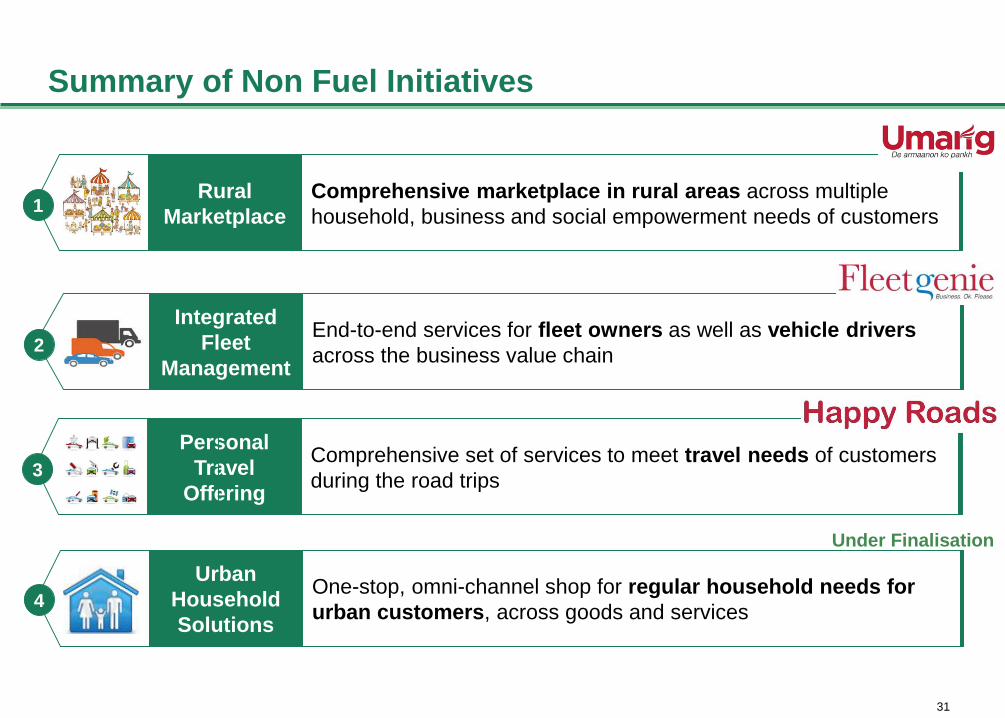

Summary of Non Fuel Initiatives

One-stop, omni-channel shop for regular household needs for

urban customers, across goods and services

Urban

Household

Solutions

End-to-end services for fleet owners as well as vehicle drivers

across the business value chain

Integrated

Fleet

Management2

4

Comprehensive marketplace in rural areas across multiple

household, business and social empowerment needs of customers

Rural

Marketplace1

Personal

Travel

Offering

Comprehensive set of services to meet travel needs of customers

during the road trips3

Under Finalisation

32

Thank You