Embed Size (px)

Citation preview

ANALYST DAY

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

4

RECENT HISTORY/ MAIN EVENTS

1964 1974 1979 1982 1987 19931994 1997 1998 2009

Military Government Redemocratization President FHC President Lula

-5%

0%

5%

10%

15%

Global Events

Domestic Events

1st Oil Shock

2nd Oil Shock

External

Debt Default

Black

Monday

“Plano Real”

Mexican

Crisis

Asian

Crisis

Russian/

LTCM crisis

Global

Financial

Crisis

GPD Growth

RESILIENCE AGAINST CREDIT CRISISTHE “LIFO” EFFECT

GDP growing above 4% from 2010 onwards

Inflation rate below 5% (2010-2012)

Interest rate slowly increasing, reaching 10.5% by 2012

Exchange rate below R$ 2/US$ during the period (2010-2012)

GDP Growth – QoQ Annualized

Global Financial

Crisis-10,0%

-5,0%

0,0%

5,0%

10,0%

Source: IBGE and Itau Unibanco estimates

-15,0%

1Q08 2Q08 3Q08 2Q09 3Q09 4Q09 e 1Q10 e 2Q10 e 3Q10 e 4Q10 e

-12.9%

-3.9%

7.8%6.1% 5.3%

7.8% 7.8%6.1%

4.9% 4.9% 4.9% 4.9%

4Q08 1Q09

5

BRAZILIAN POPULATIONIn 2008

98,6% of the houses has Eletrictricity

6

Poverty1991 – 35%

2008 – 15,5%

Illiteracy1991 – 16,4%

2008 – 9,1%

84% of the houses has Running Water

78,1% of the population has Mobile Phones (168 million phones)

CONSUMER TRENDS

A (US $70,000)

B (US $22,275)

C (US $8,515)

D (US $4,390)

E (US $2,470)

48.5%

74.2%

Growth of Middle Income Classes

Source: Study “Brazil in focus IPC Target 2008” (Target Marketing) and IBGE 2001

Expansion of the Middle Income Class

2001 2008

13.2%

33.8%

30.9%

17.6%

4.5%

19.5%

45.8%

28.4%

4.6%

1.8%

Income per Year

7

8

Middle Income

Class

Over the last 2 years, 22,5 million people were added to this segment

The Middle Income Class pepople took advantage of this ascension to enjoy for the first time categoriesto witch they had no previous access

1,5 million formal jobs were created in 2008,

1 million in 2009 and more than 2 million are expected for 2010

Social programs have enhanced the living standards of poor families: Since 2003 the minimum wage has risen

46% over inflation

Program “minha casa, minha vida” for people to acquire their first residence

GPA’S SHARES OUTPERFORM THE IBOVESPA, REFLECTING MARKET

APPROVAL OF THE COMPANY´S INITIATIVES

Jan 2008

PCARIbovespa

Stock Evolution

Updated until November, 11th

9

Jan 2009

200%

60%

40%

Dec 2009

180%

160%

80%

PCAR -9,1% e

Ibovespa -41,2%

PCAR +84,8% e

Ibovespa +7,2%

PCAR +103,4% e

Ibovespa +82,4%

140%

120%

100%

PCAR R$34,08 e Ibovespa 63.886 points

PCAR R$30,97 e Ibovespa 37.550 points

PCAR R$63,00 e Ibovespa 68.512 points

CBD (ADR)+100,4%

Dow Jones -21,7%%

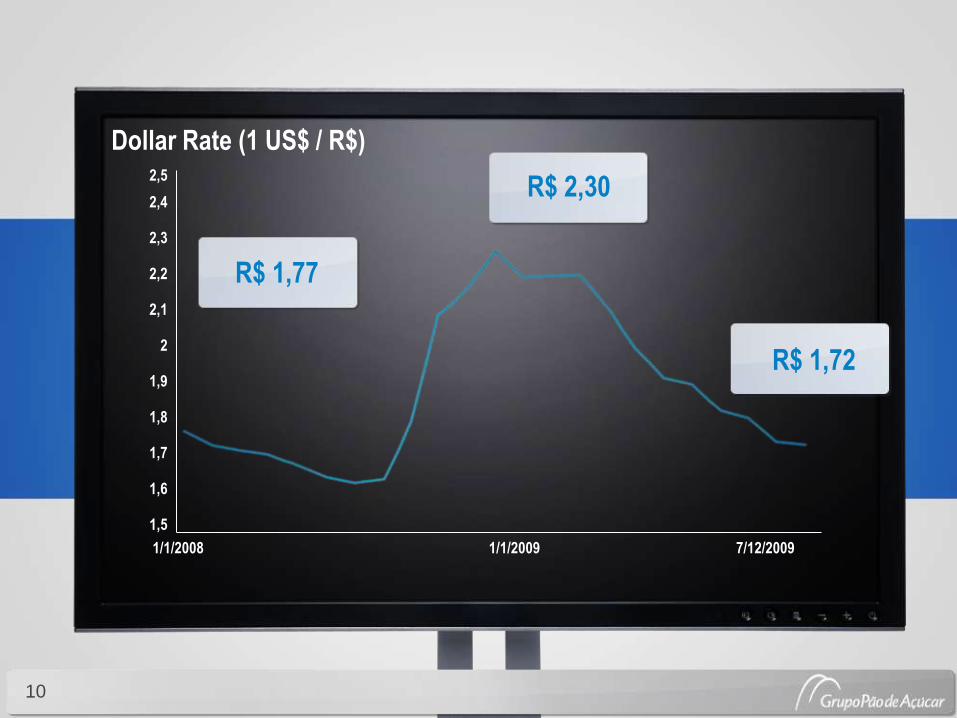

2,4

1/1/2008

10

1/1/2009 7/12/2009

2,3

2,2

1,8

1,7

1,6

1,5

2,1

2

1,9

2,5

R$ 1,77

R$ 2,30

R$ 1,72

Dollar Rate (1 US$ / R$)

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

LFL SalesMarket Share 2008(1)

12

FOOD RETAIL MARKET

CBD

(1) Source: ABRAS – Associação Brasileira de Supermercados

Carrefour Wal-Mart Others

Formal Sector: R$ 158.5 billion – 5.5% do PIB

Informal Sector accounts for approximately50% of total food consumption

Fragmented Market: Small / Medium Chains

Increasing formalization of the market

2006 2007 2008

13,3%

10,4%

10,4%

13,8%

14,1%

11,0%

13,2%

14,2%

10,7%4,3%

10,4%9,7%

2,3%

3,9%

13,2%

4,6%8,5%

10,3%

7,2%

7,8%7,1%

8,6% 8,4%

1Q08 2Q08 3Q08 4Q08 1Q09 2Q09 3Q09

GPA Carrefour

65,9%61,1% 61,9%

13

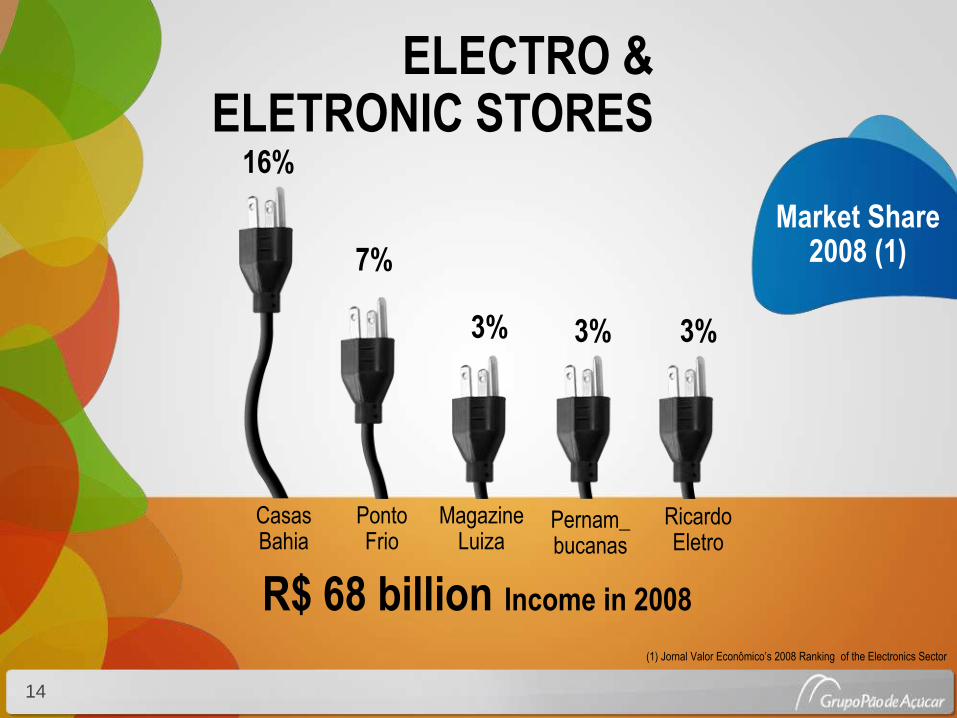

ELECTRO & ELETRONIC

STORES

POTENCIAL AND MARKET SIZE(R$ BILLION)

Source: Accenture

2002 2003 2004 2005 2006 2007 2008 2013E

AVERAGE GROWTH

2002a – 2007a - 15,0% 2008e – 2013e - 14,6%

3034 40 45 50 59

68

134

Casas Bahia

Ponto Frio

Magazine Luiza

Pernam_bucanas

Ricardo Eletro

14

16%

7%

3% 3% 3%

ELECTRO & ELETRONIC STORES

Market Share 2008 (1)

R$ 68 billion Income in 2008

(1) Jornal Valor Econômico’s 2008 Ranking of the Electronics Sector

NON-FOOD EXPANSION STRATEGY

15

Key dedicated players’ market share and positioning

RankingPositioning by social class

1. Bahia

2. Ponto Frio

3. Magazine Luiza

4. Pernambucanas

5. Ricardo Eletro

6. Insinuante

A B C D E

Strategic decision made in 2007 to expand non-food operations and reinforce/protect core business of GPA

First major strategic move made in June when GPA announced the acquisition of Ponto Frio

Casa Bahia: Complementary market positioning in the durable goods segment:

• Ponto Frio: focus on classes A, B and C• Casa Bahia: focus on classes C and D

PONTO FRIOA successful turnaround

REVERSAL OF THE SALES DOWNTREND

POSITIVE EBITDA

MOTIVATED TEAM

INTEGRATION WITH GPA

16

SYNERGIES Logistics & ITCommercialHead Office Redundancy

INTEGRATION CASAS BAHIA

Extra.com

Ponto Frio.com

PF Wholesale

CB.com

INTERNET INCLUDES:

GPA - 83%¹ CB - 17%

Nova.com - 100%

CB.com

Extra Eletro

Ponto Frio

Casa Bahia

STORE OPERATIONS

INCLUDE:

GPA - 51%² CB - 49%²

Globex- 100%

NCB

1) Does not consider Management stock option

2) Considers total adhesion of Globex to PTO

17

DEALR$ MILLION

18

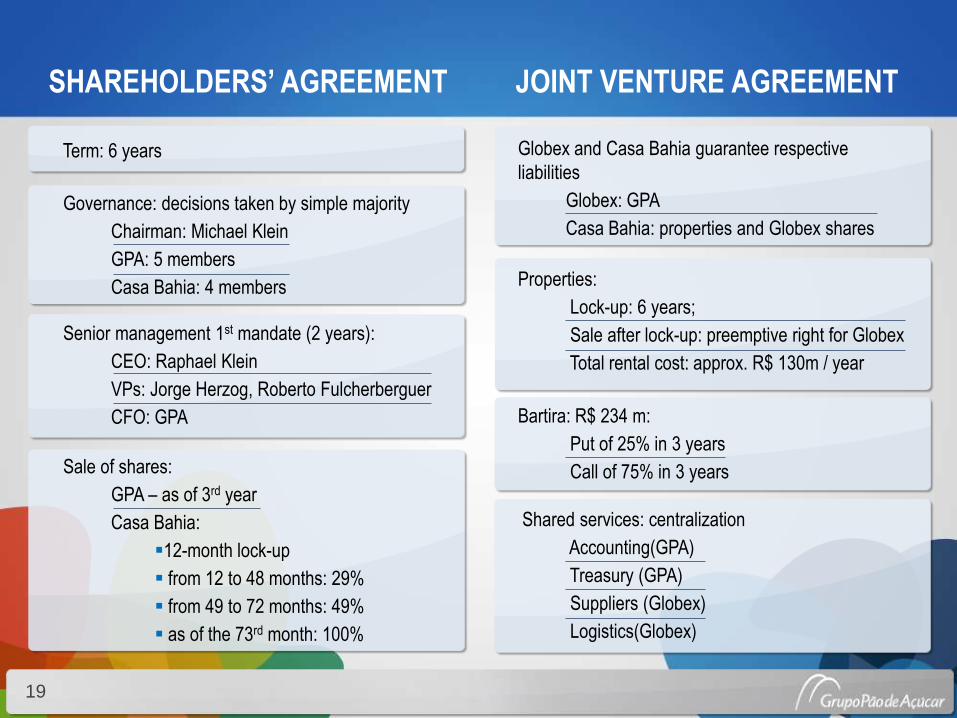

SHAREHOLDERS’ AGREEMENT

Term: 6 years

JOINT VENTURE AGREEMENT

Shared services: centralization

Accounting(GPA)

Treasury (GPA)

Suppliers (Globex)

Logistics(Globex)

Sale of shares:

GPA – as of 3rd year

Casa Bahia:

12-month lock-up

from 12 to 48 months: 29%

from 49 to 72 months: 49%

as of the 73rd month: 100%

Governance: decisions taken by simple majority

Chairman: Michael Klein

GPA: 5 members

Casa Bahia: 4 members

Senior management 1st mandate (2 years):

CEO: Raphael Klein

VPs: Jorge Herzog, Roberto Fulcherberguer

CFO: GPA

Globex and Casa Bahia guarantee respective

liabilities

Globex: GPA

Casa Bahia: properties and Globex shares

Properties:

Lock-up: 6 years;

Sale after lock-up: preemptive right for Globex

Total rental cost: approx. R$ 130m / year

Bartira: R$ 234 m:

Put of 25% in 3 years

Call of 75% in 3 years

19

CB brings operational assets to NCB;

CB brings assets and the CB.com brand to the subsidiary;

CB

Stores + DCs (~1.4 million m2)

75% stake of Bartira (furniture factory)

Receivables ~ R$ 1 billion

Other non-operational assets

NCB

Operational assets / liabilities

Approximately R$ 950 million Net Debt

Lease Agreement 10 years + 10

Approximately R$ 130 million/year;

25% furniture factory

Furniture supply agreement for 3 years

Cost price;

Fixed fee: R$ 18 million/year

SETTING-UP OF NEW CASA BAHIA (NCB)

20

SETTING-UPOF GLOBEX

GPA brings Extra Eletro operations to Globex;

Globex split up: PF.com + wholesale/ Ponto Frio + Extra Eletro;

GPA brings Extra.com to PF.com;

PF.com includes• Extra.com• Wholesale

Globex includes• Ponto Frio• Extra Eletro

1 Considers total adhesion of Globex to PTO and

does not consider management stock option

2 Considers total adhesion

of Globex to PTO

21

Market leader in durable goods segment

513 stores (3Q09);

Approximately 57,000 employees;

Strong brand, largest advertiser in

Brazil

Strong partnership with suppliers

Well structured business

(commercial, operations, logistics, IT,

contact center, furniture factory)

Focus on low-income

segments (C / D classes)

Largest Consumer Finance operation

in retail: database of 30 million clients

30%

24%

46%3%

9%

9% 32%

28%19%

Casa

Bahia

Gross Rev. (R$ Bn - exc

interest)13.9

Merchandise 12.7

Services 1.2

Stores 548

Sales Area (thousand m²) 1,005

Gross Revenue (R$ mm) /

Stores25.2

Gross Revenue (R$) / m² 13,766

Sales Area m²/Stores 1,834

PF + EE

4.2

4.1

0.1

505

365

8.3

11,525

723

CASAS BAHIA RATIOS (2008)

SALES MIX (2008)

White goods Furniture Electronics

Hard & Software Telecom Others

Household appliances & furniture

Electronics

Photo, video, telecom, software

22

Main Synergies

Centralized purchases

Integration of headquarters,

logistics and IT

E-commerce platform integration

Partnerships with suppliers

Scale gains on advertising in

CBD as a whole

Improved financial services

Rationalization of logistics

New Company’s

magnitude

R$ 18.1 Bn

Gross Revenue

5% normalized¹

EBITDA Margin

Estimated Net

Present Value of

Synergies:R$ 2 Bn

Subject to the approval of Brazilian antitrust authorities

1) % of net sales

The New Company

23

SCHEDULE

December 4, 2009:Signing Day

Disclosure to Market

D + 20: January 11, 2010 CBD Extraordinary Shareholders’ Meeting

Before Closing:

Creation of NCB

Separation of dot.com assets

Contribution of Extra Eletro to Ponto Frio

up to D + 120 : Closing (merger date)

NEXT STEPS

24

Subject to the approval of

Brazilian antitrust authorities

Leadership in the retail durable goods segment with approximately R$ 18,1 billion revenue (including e-commerce)

1.015 stores (3Q09)

28 Distribution Centers

Approximately 68.000 employees

E-commerce Income 2010

R$ 2 bi (including wholesale)

THE NEW COMPANYHighlights

25

26

Casas Bahia

Ponto Frio

Magazine Luiza

Pernam_bucanas

Ricardo Eletro

27

GPA(with Casa

Bahia and PF)

16%

7%

3% 3% 3%

26%ELECTRO & ELETRONIC MARKET

Market Share 2008 (1)

R$ 68 billion Income in 2008 (1) Jornal Valor Econômico’s 2008 Ranking of the

Electronics Sector

RANKING GLOBAL

Rank Company Headquarter Sales 2008

(US Bi) Stores

1

2

3

4

5

6

7

8

9

10

11

Best Buy

Media-staturn

Expert

DSG International

Euronics

Yamada Denki

Gome

Suning

Kesa Electricals

Nova Globex

Edion

USA

Germany

Switzerland

UK

Netherlands

Japan

China

China

UK

Brazil

Japan

45.1

33.0

21.7

20.3

19.1

16.6

15.7

15.5

11.4

10.3

7.8

4,096

768

6,902

1,638

11,824

1,360

1,263

820

713

1,015

1,178

Nova Globex 18.5 1.8

R$ Bi 1 US$/ R$

28

Source: Accenture

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

GPA

Gross Sales(annualized based in 2008):

R$ 26 billion

1.069 stores, located in 18 States and the Federal District:

Current Profile

More than 80.000 employees

520 million tickets per year

1,7 million sqm of sales areas

30

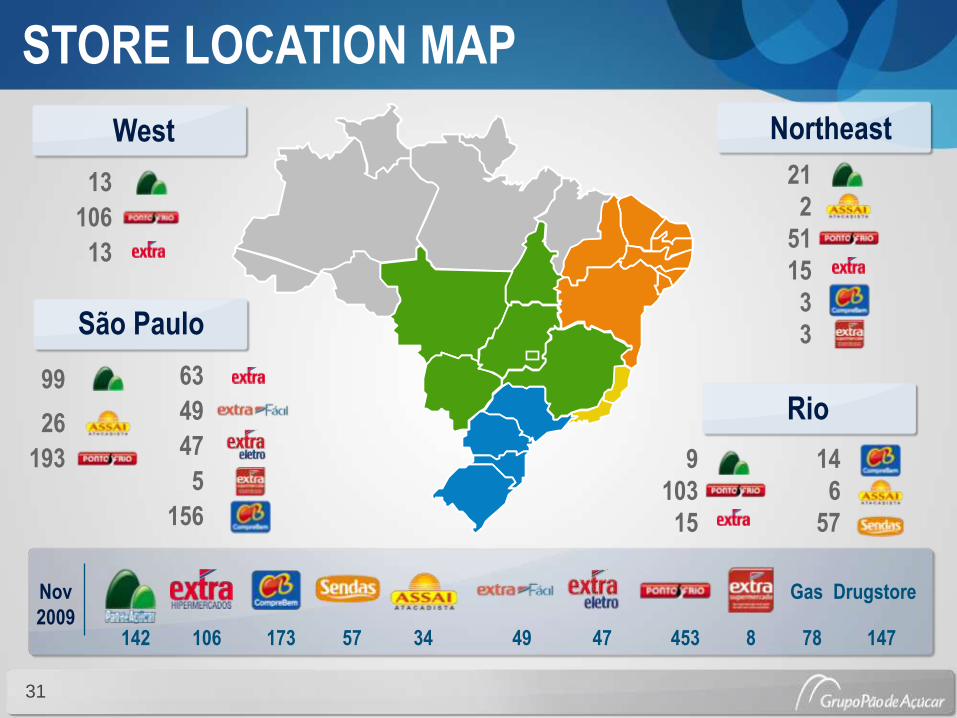

With Ponto Frio and Without Casas Bahia

STORE LOCATION MAP

31

13

106

13

78 147

Nov

2009142 106 173 4757 4934 453

Gas Drugstore

West Northeast

Rio

São Paulo

99

26

193

63

49

47

5

156

21

2

51

15

3

3

9

103

15

14

6

57

8

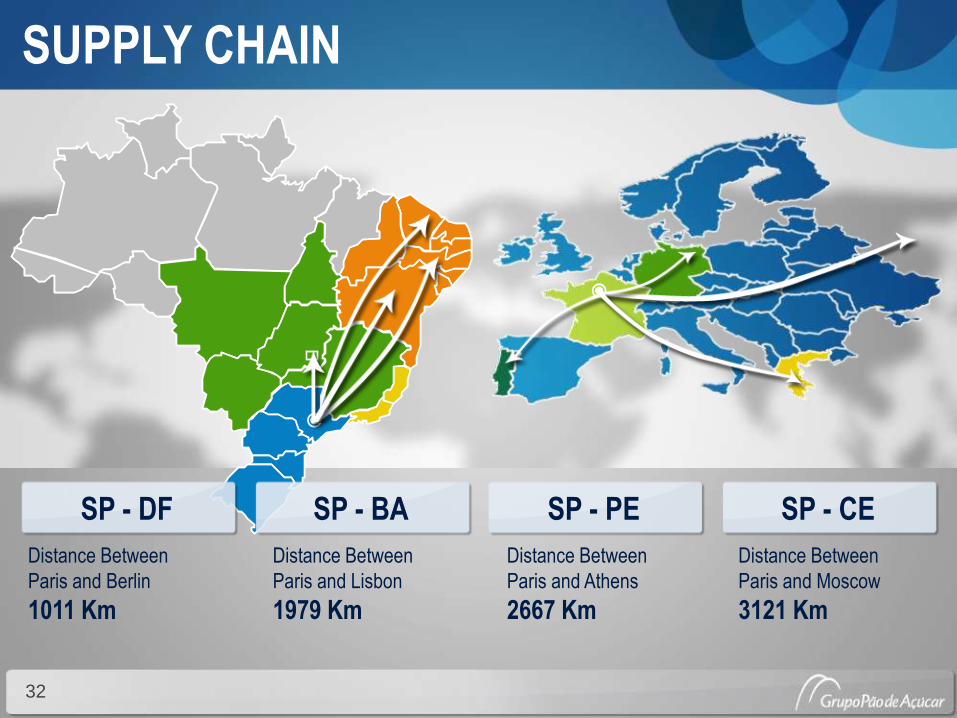

SUPPLY CHAIN

SP - DF

Distance Between

Paris and Berlin

1011 Km

SP - BA SP - PE SP - CE

Distance Between

Paris and Lisbon

1979 Km

Distance Between

Paris and Athens

2667 Km

Distance Between

Paris and Moscow

3121 Km

32

LOYALTY PROGRAMPÃO DE AÇÚCAR MAIS

33

First loyalty program in Brazil -9 years ago

Special offers to clients divided in 11 behavior segments

2,1 million members – 45% of the banner sales

Evolution to Dunnhumby

STRENGHTENING OF EXCLUSIVE BRANDS

Taeq is Leader or second brand in 52% of subcategories

Qualitá is Leader or second brand in 49% of subcategories

Participation in GPA’s total income: 5%

5.000 SKU´s

222 SKU´s Casino

34

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

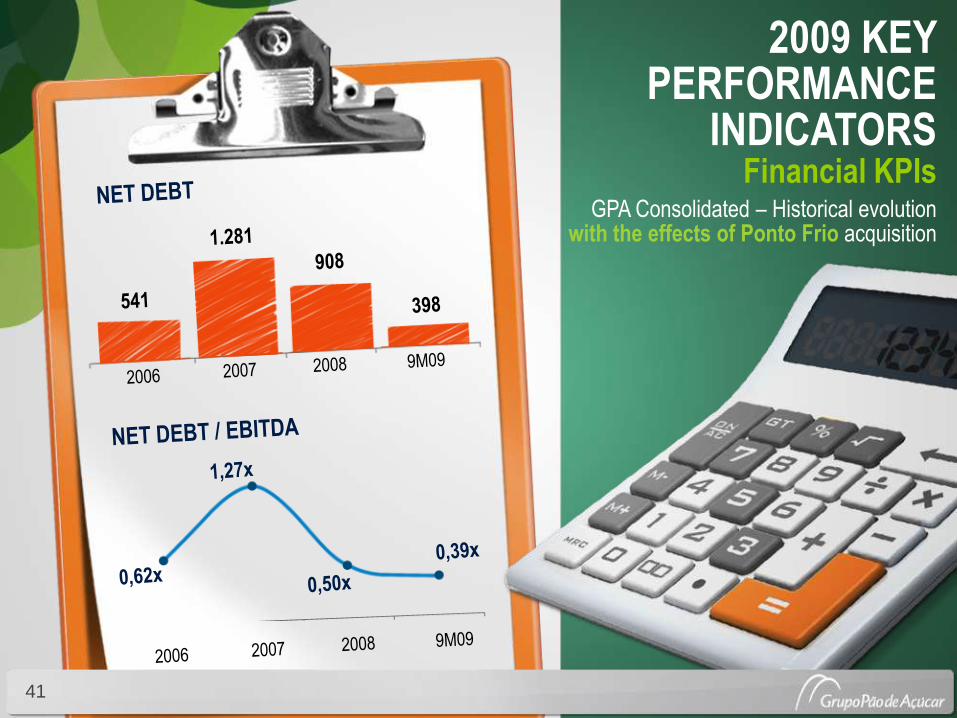

2009 KEY PERFORMANCE

INDICATORS SALES

16.460 17.64320.857

23.000

2006 2007 2008 2009e

7%18%

11%

All storesWithout Ponto Frio

GROSS SALES CAGR 12%

36

Obs: Like for Like Sales include only the stores with 12 months or more in operation

*2009 – Acumulado até Setembro

FOOD AND NON-FOOD SALES PERFORMANCE(Like for Like Sales in Nominal Terms)

1,1%

9,0%12,8%

3,1%

10,1%8,5%

2,4%

3,3%

3,9%4,5%7,6%

9,7%

16,1%

11,9%11,0%

-2,4%

3,7%5,9%

0,6%

11,4%

10,4%

14,3%

1T07 2T07 3T07 4T07 1T08 2T08 3T08 4T08 1T09 2T09 3T09Non-Food

Food

37

2009 KEY PERFORMANCE

INDICATORS P&L

GPA Consolidated without Ponto Frio – Historical evolution

38

EBITDA

Margins Sales

SG&A Expenses

THE CHALLENGE IS FINDING THE RIGHT EQUATION

BETWEEN MARGINS AND SALES GROWTH

39

2009 KEY PERFORMANCE

INDICATORS P&L

GPA Consolidated without Ponto Frio – Historical evolution

40

2009 KEY PERFORMANCE

INDICATORS Financial KPIs

GPA Consolidated – Historical evolution with the effects of Ponto Frio acquisition

41

2009 KEY PERFORMANCE

INDICATORS Financial KPIs

GPA Consolidated – Historical evolution with the effects of Ponto Frio acquisition

42

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

“Back to Basics”Strategy

Sales are a consequence of successful work on these pillars

Focus on Sales Pillars

Assortment Pricing CommunicationCustomerService

44

RE-ENFORCE ITS FOUNDATIONS TO SUSTAIN GROWTH WITH PROFITABILITYNew Management ModelSimplicity, focus, agility, integration and empowerment

Multi-disciplinary groupsPursuit of efficiency

Strengthening regional commercial officesClusterization

Aggressive variable compensationEBITDA based bonus driven by collective and individual goals

Solid structureStrengthening cash position before the crisis and strong investments in IT & LogisticsConservative Financial Policy

45

2008 2009e

New Stores 156 280

Sites 95 154

Renovations 143 154

Infra-structure 109 167

GPA 503 755

CAPEX (R$ million)

46

MEDIUM TERM OUTLOOKS

• Maintain Financial and economic health

• Scale gains increasing productivity of existing stores

• Market Share Growth

• Expansion in consolidated formats

47

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

2008 164% of sales growthThe biggest among the players

2005 2012 E2009 E

1.0%

6.2%

9.3%

Market Share

E-COMMERCER$ 2 billion sales in 2010

Consolidated position as Brazil’s

second larger e-Commerce player

High growth potential

Extra.com

Ponto Frio.com

Ponto Frio wholesale

CasasBahia.com

49

FIC

+R$ 10 billion credit approved for customers

8 million cardholders

12% participation of total sales

R$ 2,8 billion receivables

Itaú had 24 million clients by the end of 2008

R$ 600 millionto GPA from the new agreement

Itaú + GPA believe this could be one of the

largest financing companies in Brazil

INVESTCRED +

50

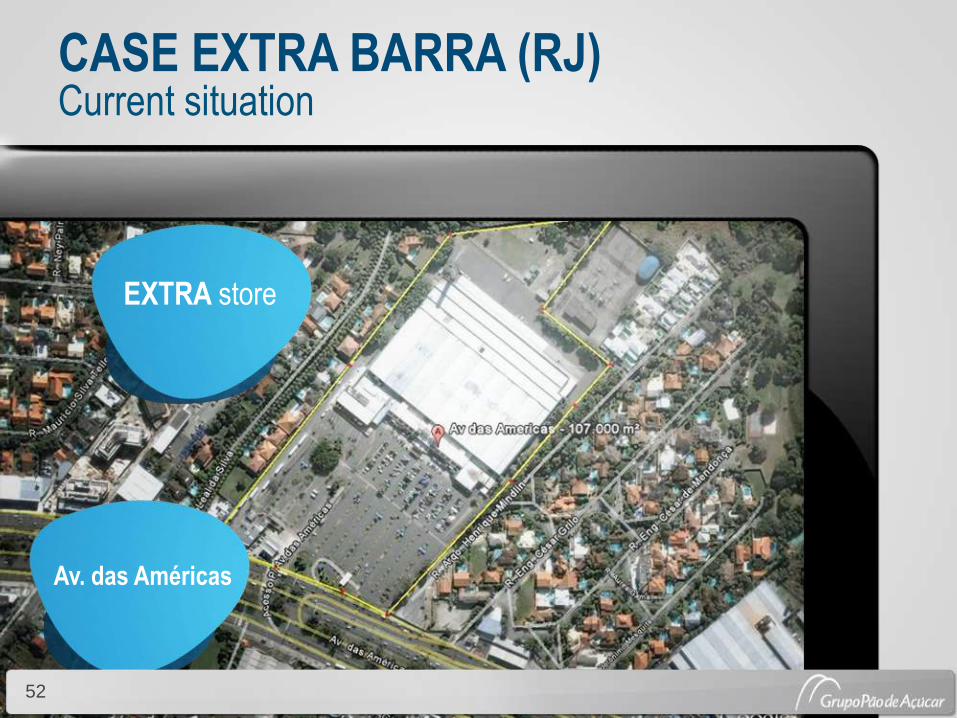

REAL ESTATE

51

TargetTo make the maximum use of our

real estate assets linked with our

retail projects in Grupo Pão de

Açúcar expansion plan

Businesses19 businesses opportunities

identified, 3 of which are being

studied in further detail

“Sweat the asset” Program

CASE EXTRA BARRA (RJ)Current situation

EXTRA store

Av. das Américas

52

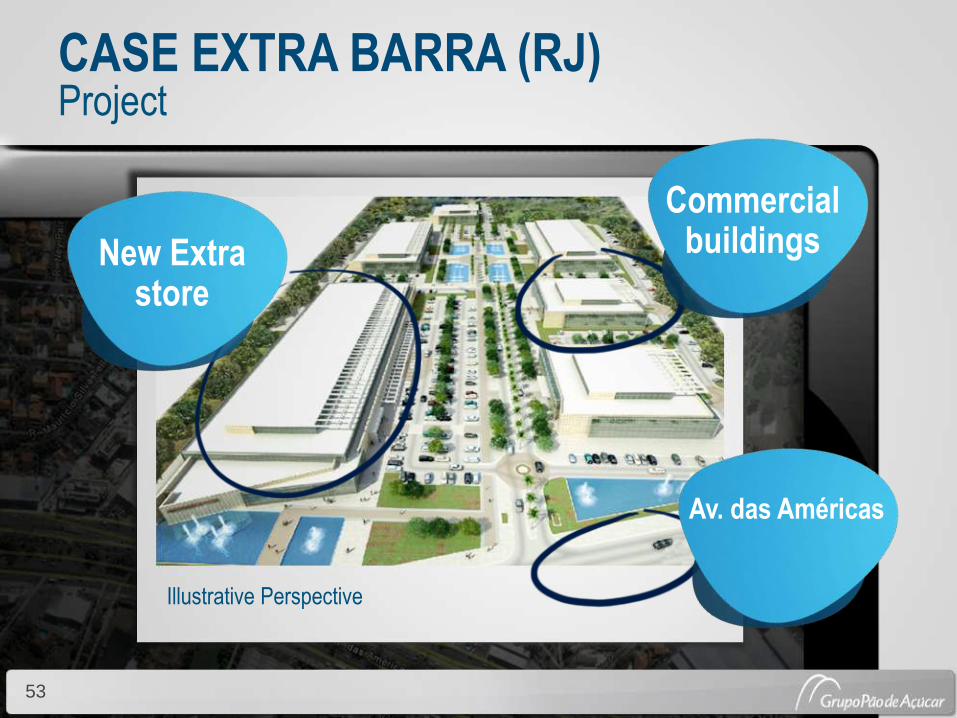

53

New Extrastore

Commercialbuildings

Av. das Américas

CASE EXTRA BARRA (RJ)Project

53

Illustrative Perspective

Q&A

Sustainability

Opportunities

Strategic Priorities and Outlook

Macroeconomic Environment

Company Overview

Retail Market

Financial Information

55

SUSTAINABILITY

Adding Quality of Life

Marathon Relay

Pão de Açúcar Kids

Race

Alimenta Bem Program

Sponsoring athletes

Share with the community

Collecting Donations

NATA

Orchestra

Educational Programs

Multiply consciousness in consumption

Reusable bags

Green Box

Caras do Brasil

Recycling Station

Carbon emission

Q & A

56

ANALYST DAY