Embed Size (px)

Citation preview

Analysis onLimited Liability

Partnership

CA.V.M.V.Subba Rao

Chartered Accountant

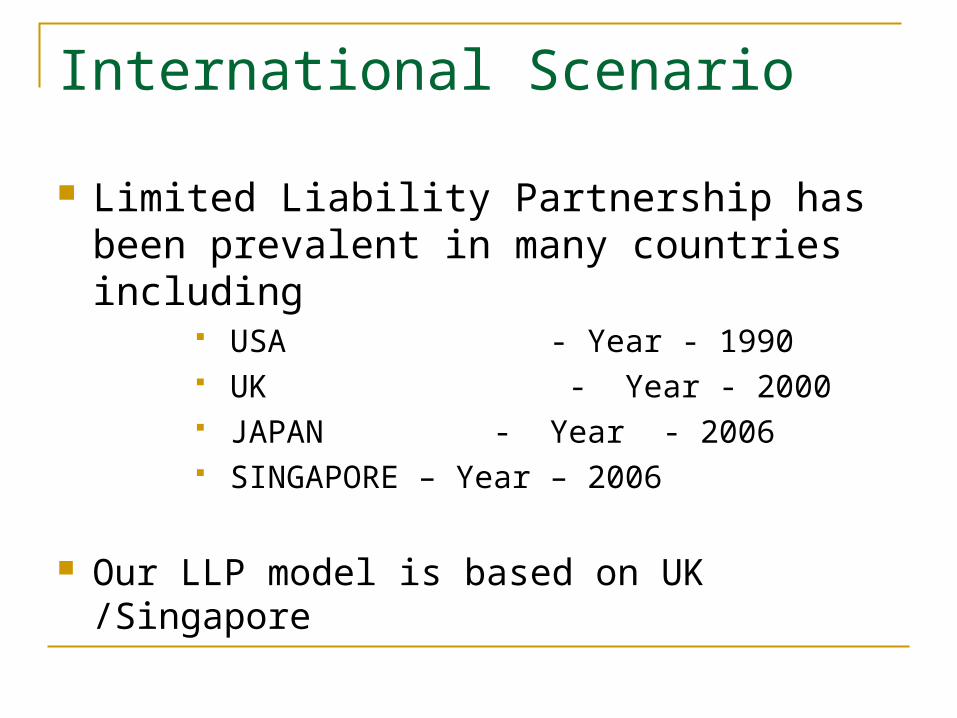

International Scenario

Limited Liability Partnership has been prevalent in many countries including

USA - Year - 1990 UK - Year - 2000 JAPAN - Year - 2006 SINGAPORE – Year – 2006

Our LLP model is based on UK /Singapore

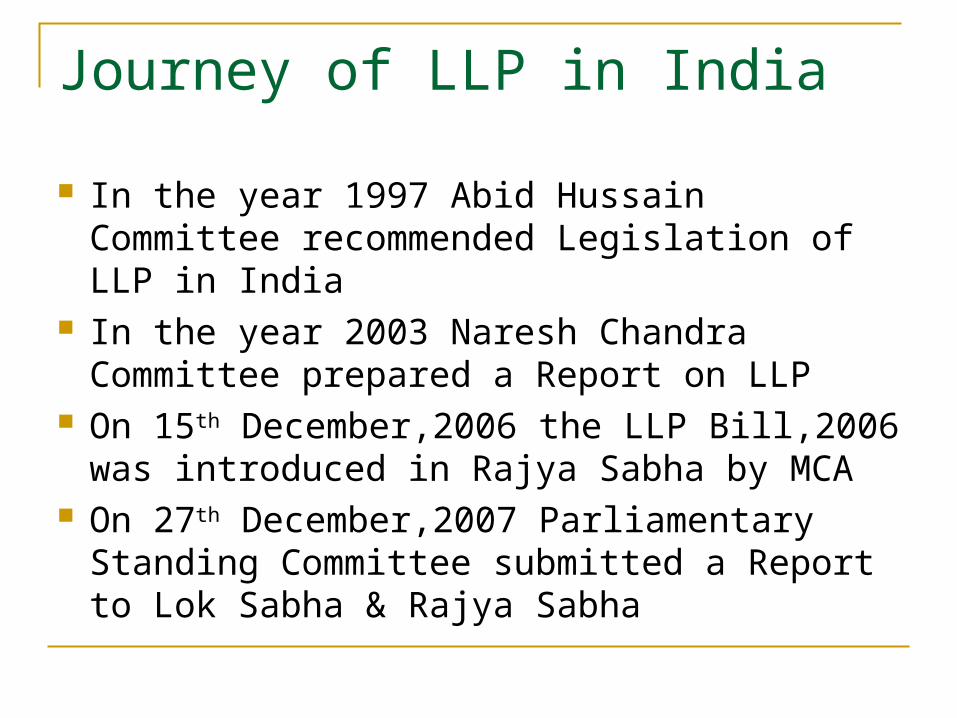

Journey of LLP in India

In the year 1997 Abid Hussain Committee recommended Legislation of LLP in India

In the year 2003 Naresh Chandra Committee prepared a Report on LLP

On 15th December,2006 the LLP Bill,2006 was introduced in Rajya Sabha by MCA

On 27th December,2007 Parliamentary Standing Committee submitted a Report to Lok Sabha & Rajya Sabha

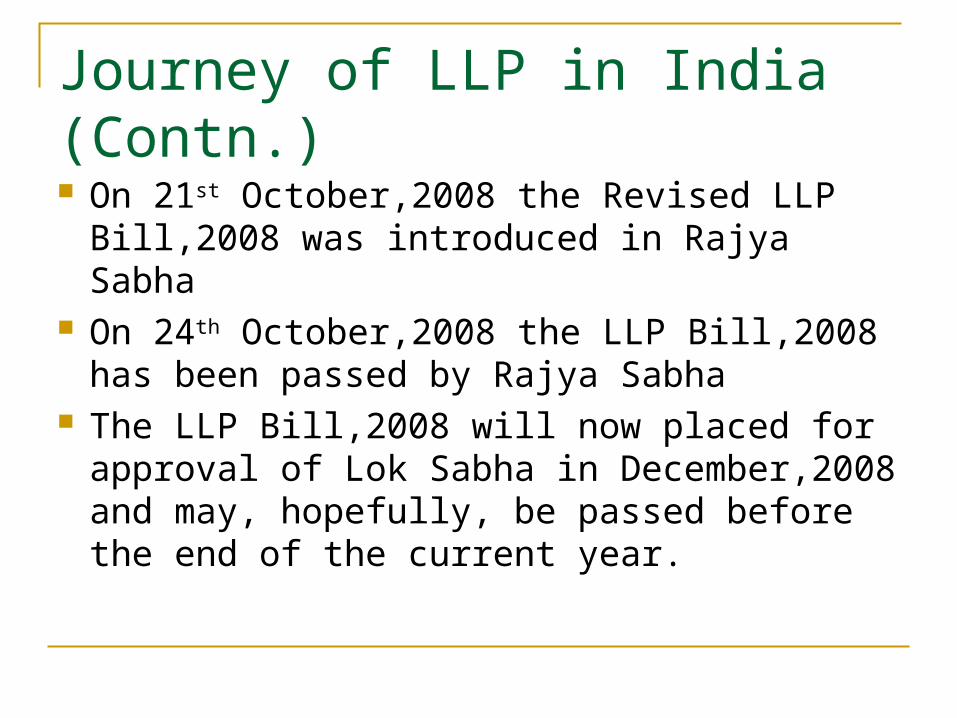

Journey of LLP in India (Contn.) On 21st October,2008 the Revised LLP

Bill,2008 was introduced in Rajya Sabha On 24th October,2008 the LLP Bill,2008 has

been passed by Rajya Sabha The LLP Bill,2008 will now placed for

approval of Lok Sabha in December,2008 and may, hopefully, be passed before the end of the current year.

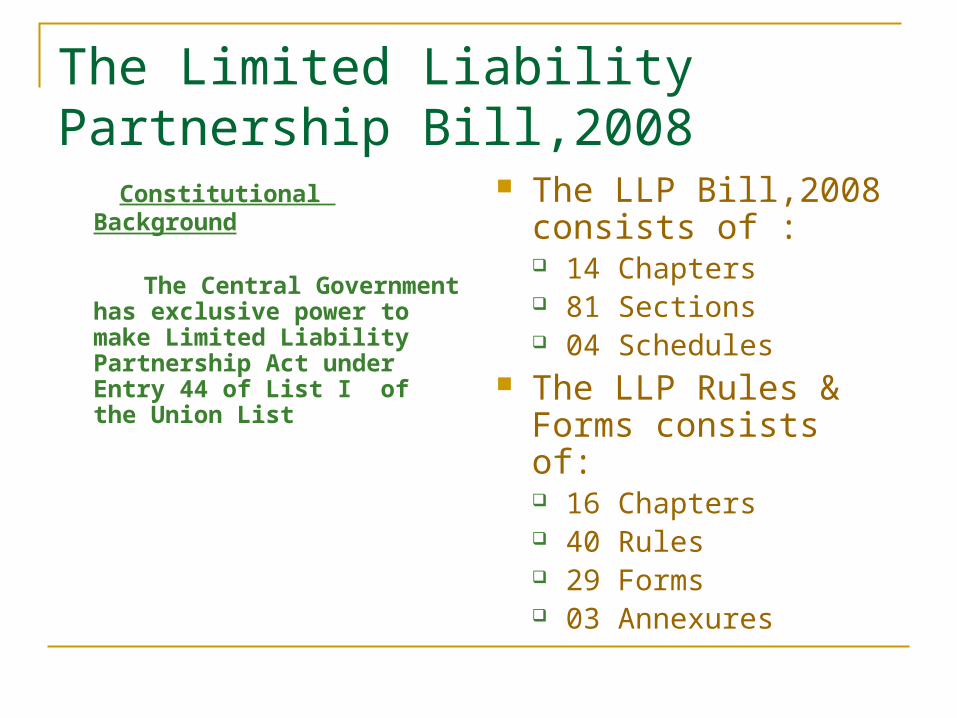

The Limited Liability Partnership Bill,2008 Constitutional Background

The Central Government has exclusive power to make Limited Liability Partnership Act under Entry 44 of List I of the Union List

The LLP Bill,2008 consists of : 14 Chapters 81 Sections 04 Schedules

The LLP Rules & Forms consists of: 16 Chapters 40 Rules 29 Forms 03 Annexures

Basic Features of LLP

LLP is a Body Corporate having perpetual succession.

LLP is a legal entity separate from its partners.

Any Change in partners of a LLP shall not affect the existence, rights or liabilities of the LLP.

No partner is personally liable to liabilities of the LLP

Basic Features of LLP

Liability of LLP is not liability of individual partners. LLP must have at least two partners No maximum Limit of partners Any Individual or Body Corporate may be a partner

in LLP. Partner is an agent of LLP but not of other partner. Ministry of Corporate Affairs is administrating

Authority

Basic Features of LLP

The Provisions of Indian Partnership Act,1932 shall not apply to a LLP.

The Provisions of Companies Act,1956 can be made applicable with suitable modification by issuing a notification to LLP

If the number of partners fall below two, the surviving partner will have to admit at least one more partner within 6 months. If he does not do so, his liability will become unlimited and LLP will be wound up.

Designated Partners

* Every LLP shall have two (2) Designated Partners.* At least one of such designated partner shall be resident individual..* Every Designated Partner shall obtain DPIN / DIN from MCA.

Incorporation Document - Form 2 Name of LLP Proposed Business Address of Regd. Office Names and addresses

of Partners Designated Partners

Any other information prescribed

Similar to MOA No provision to amend

Incorporation Document

Provision to Change Name, Business & Registered Office

Certificate of Incorporation by ROC is conclusive evidence

Liabilities of Designated Partners Responsible for compliance of the provisions

of the LLP Act including filing of various returns and documents specified in the Act.

Liable to all penalties imposed on the LLP for any contravention of those provisions.

L L P Agreement - Form 4

Limited Liability Partnership Agreement means any written agreement between the partners of the LLP or between the LLP and its partners and its partners which determines the mutual rights and duties in relation to that LLP.

After incorporation, the LLP may have the LLP agreement.

The LLP agreement is similar to A O A of Company.

L L P Agreement

In the absence of any LLP agreement the provisions set-out in FIRST SCHEDULE is applicable.

If the partnership agreement is executed before registration of LLP the partners will have to ratify this agreement after incorporation of LLP and file with ROC

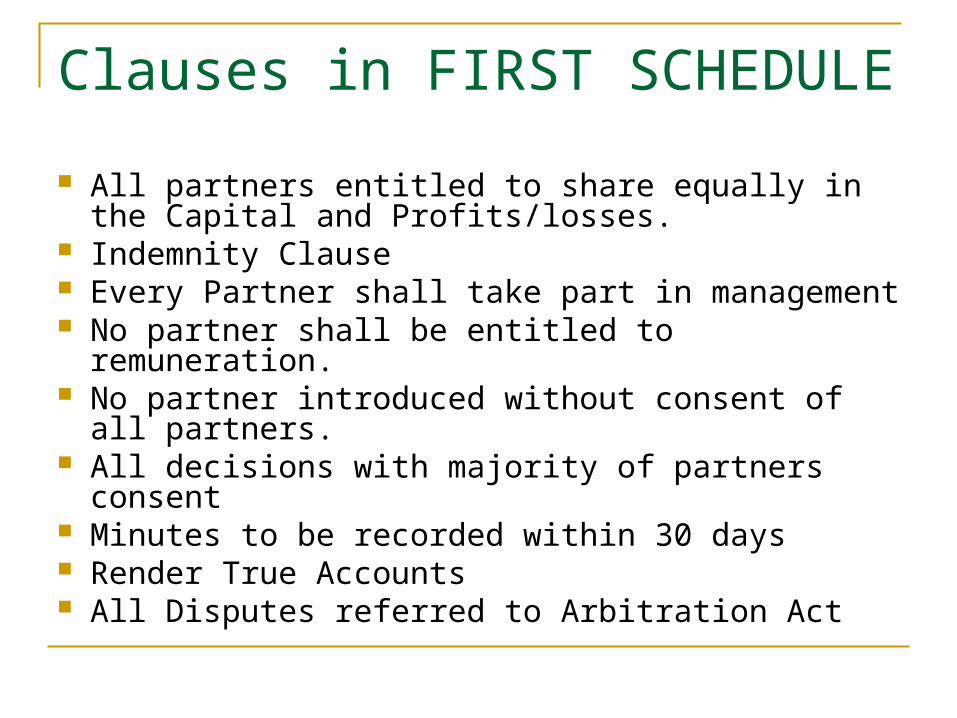

Clauses in FIRST SCHEDULE All partners entitled to share equally in the Capital

and Profits/losses. Indemnity Clause Every Partner shall take part in management No partner shall be entitled to remuneration. No partner introduced without consent of all

partners. All decisions with majority of partners consent Minutes to be recorded within 30 days Render True Accounts All Disputes referred to Arbitration Act

Contribution

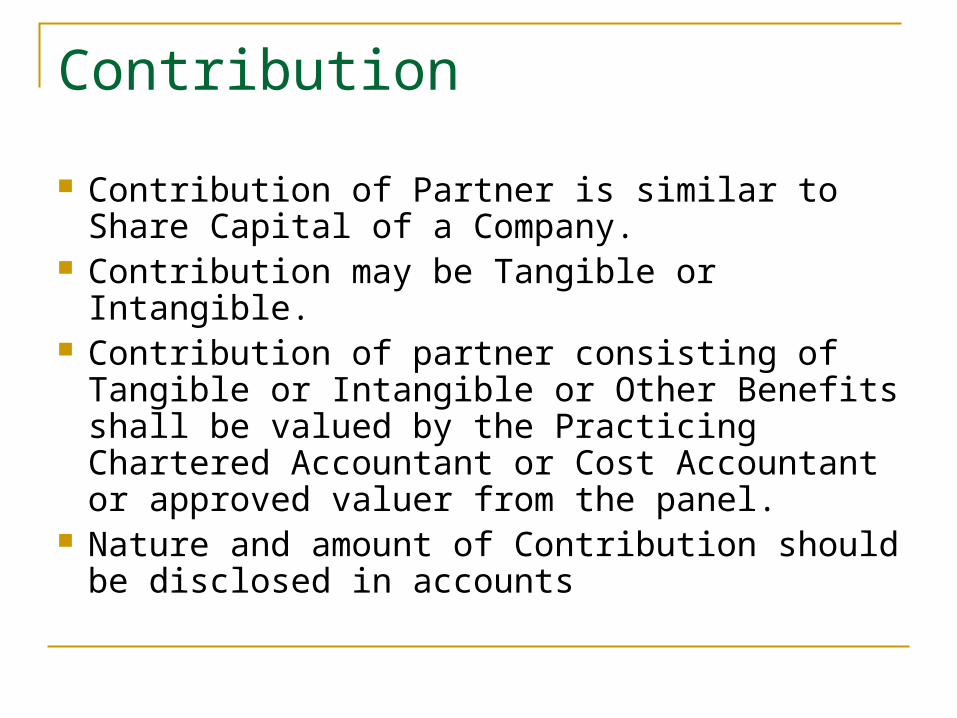

Contribution of Partner is similar to Share Capital of a Company.

Contribution may be Tangible or Intangible. Contribution of partner consisting of Tangible

or Intangible or Other Benefits shall be valued by the Practicing Chartered Accountant or Cost Accountant or approved valuer from the panel.

Nature and amount of Contribution should be disclosed in accounts

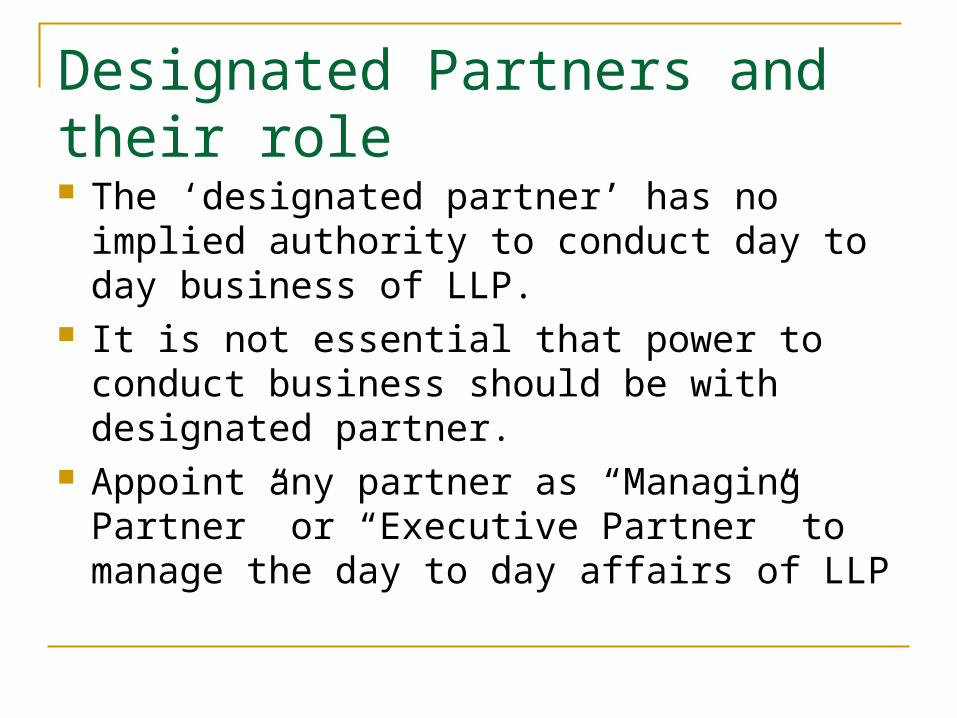

Designated Partners and their role The ‘designated partner’ has no implied

authority to conduct day to day business of LLP.

It is not essential that power to conduct business should be with designated partner.

Appoint any partner as “Managing Partner” or “Executive Partner” to manage the day to day affairs of LLP

Accounts and Audit

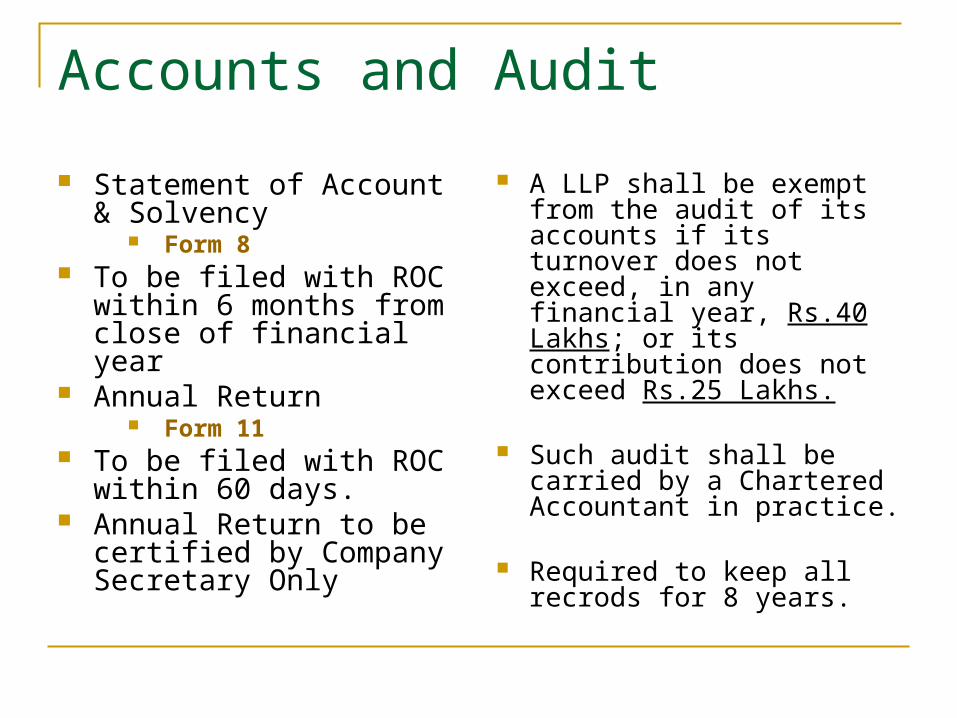

Statement of Account & Solvency

Form 8 To be filed with ROC within

6 months from close of financial year

Annual Return Form 11

To be filed with ROC within 60 days.

Annual Return to be certified by Company Secretary Only

A LLP shall be exempt from the audit of its accounts if its turnover does not exceed, in any financial year, Rs.40 Lakhs; or its contribution does not exceed Rs.25 Lakhs.

Such audit shall be carried by a Chartered Accountant in practice.

Required to keep all recrods for 8 years.

Accounts and Audit

Financial Year means the period from April 1 of a year to the March 31 of following year.

All Accounts, Details and documents are available for public Inspection.

Very heavy fines for delay in filing of Returns – Minimum Rs.25,000/- /Maximum –Rs.5 lacs

Offenses compoundable. Heavy Fees for late filing of documents- Rs.100 per

day. Late filing up to 300 days is permissible

Other Provisions

Compromise, arrangements or reconstruction of LLP

Winding up and dissolution of LLP Strike off defunct LLP Liability of partner by holding out. Whistle Blowing Assignment and transfer of partnership rights.

Other Provisions

Investigation of affairs of LLP Every LLP shall have either the words

“Limited Liability Partnership” or the acronym “LLP” as the last words of its name.

Application of Name availability. Minor can be admitted to the benefits of LLP E-filing of documents. Inspection of documents filed ROC

SECOND SCHEDULE

It Contains provisions for Conversion of existing Partnership Firm into Limited Liability Partnership.

THIRD SCHEDULE

It Contains provisions for Conversion of existing Private Company into Limited Liability Partnership

FOURTH SCHEDULE

It Contains provisions for Conversion of existing Unlisted Public Company Firm into Limited Liability Partnership

TAXATION OF LLP

LLP Act is silent regarding taxation of LLP under the Income-tax Act.

A separate Chapter is required under income-tax on taxation of LLP

Pass-through Concept: Share of each partner should be taxed in the

hands of individual partners (as was the provision in case of partnership up to 1993).

Let us wait and see how LLP and individual partners are made liable to income-tax

THANK YOU

CA. V.M.V.SUBBA RAO

CHARTERED ACCOUNTANT