Embed Size (px)

Citation preview

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 101

ANALYSIS OF THE ACCURACY OF BANKRUPTCY

PREDICTION WITH GROVER ALTMAN Z-SCORE, SPRINGATE,

ZMIJEWSKI, AND OHLSON MODEL ON MANUFACTURING

COMPANIES LISTED IN JAKARTA ISLAMIC INDEX

(Case Study at PT. Indofood CBP Sukses Makmur, Tbk)

Halkadri Fitra1)

1)

1)

Economic Faculty, Universitas Negeri Padang

ABSTRACT

The purpose of this study was to determine the accuracy of the use of

bankruptcy prediction model includes Grover Model, Altman Z-score

model, Springate Model, Zmijewski Model and Ohlson Model in predicting

corporate bankruptcies PT. Indofood CBP Sukses Makmur, Tbk, which is

one of the companies listed in the Jakarta Islamic Index (JII). This type of

research is classified as descriptive quantitative comparative data collection

techniques used are documentation method of secondary data such as the

statement of financial position, income statement, statement of changes in

equity, cash flow statements, notes to the financial statements and the

market value of equity ranging from 2010 to 2015. The results showed that

all models : Grover Model, Altman Z-score Model, Springate Model,

Zmijewski Model and Ohlson Model provides predictive results stating that

PT. Indofood CBP Sukses Makmur, Tbk is not bankrupt. Based on the

research results and condition of the company are still listed in the Indonesia

Stock Exchange and the Jakarta Islamic Index, it can be concluded that the

model used in this study have the accuracy for predicting corporate

bankruptcies.

Keywords: bankruptcy prediction, Grover, Altman Z-Score, Springate, Zmijewski,

Ohlson

BACKGROUND

A healthy company is the hope of all parties so that all efforts should be done

for survival. Instead bankruptcy is a word so feared by the parties related to the

company such as management companies, owners, creditors and government so that

they will make every effort to avoid it. For that attempt to predict the bankruptcy of the

company since its inception has been the fair thing to do.

The financial report is a report describing the financial condition and results of

operations of a company at a certain time or a certain period of time (Harahap; 2009)

became one of the tools that can be used to predict corporate bankruptcy. It is also in

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 102

accordance with the opinion of Fahmi (2013: 2) which states that the financial report is

an information describing the financial condition of a company, and further information

can be used as an overview of the company's financial performance.

The use of financial statements for predicting bankruptcy of companies is

already widely used by experts thus creating various bankruptcy prediction model.

Grover, Altman Z-Score, Springate, Zmijewski and Ohlson Model is an analytical

models bankruptcy frequently used and is known for its accuracy in determining fairly

accurate prediction of bankruptcy and how relatively easy. The fifth model is

operationalized through a comparison of the financial ratios to get the final result of

bankruptcy prediction. All these models have their advantages and disadvantages of

each in the determination of the model. Some research has been done related to the

accuracy of the use of Model Predicts Bankruptcy for such Hastuti (2015), Christianti

(2013), Wulandari, et al (2014), Jayanti and Rustiana (2014), explains that the use of

prediction models of bankruptcy is very important to do

Formulation of Problem

Based on the research background, the formulation of the problem in this

research are:

a. How the accuracy of prediction of bankruptcy PT. Indofood CBP Sukses

Makmur, Tbk based Grover Model?

b. How the accuracy of prediction of bankruptcy PT. Indofood CBP Sukses

Makmur, Tbk based Altman Z-Score Model?

c. How the accuracy of prediction of bankruptcy PT. Indofood CBP Sukses

Makmur, Tbk based Springate Model?

d. How the accuracy of prediction of bankruptcy PT. Indofood CBP Sukses

Makmur, Tbk based Zmijewski Model?

e. How the accuracy of prediction of bankruptcy PT. Indofood CBP Sukses

Makmur, Tbk based Ohlson Model?

Research Purposes

Based on the formulation of the problem, then the purpose of this research are:

a. To determine the accuracy of the predicted bankruptcy of PT. Indofood CBP

Sukses Makmur, Tbk based Grover Model

b. To determine the accuracy of the predicted bankruptcy of PT. Indofood CBP

Sukses Makmur, Tbk based Altman Z-Score Model

c. To determine the accuracy of the predicted bankruptcy of PT. Indofood CBP

Sukses Makmur, Tbk based Springate Model

d. To determine the accuracy of the predicted bankruptcy of PT. Indofood CBP

Sukses Makmur, Tbk based Zmijewski Model

e. To determine the accuracy of the predicted bankruptcy of PT. Indofood CBP

Sukses Makmur, Tbk based Ohlson Model

LITERATURE STUDY

Jakarta Islamic Index (JII)

Jakarta Islamic Index (JII), is one of the existing index in the Indonesia Stock

Exchange (BEI) using 30 issuers included in Shari'ah criteria selected by the Islamic

Shari'a and includes stocks that have large capitalization and high liquidity. The Islamic

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 103

principles of which prohibit a company whose shares are listed for the conduct of

business activity on the basis of gambling, speculation, conducting conventional

banking system, produce or trade food / drinks are forbidden, providing goods / services

that damage morale and health. Criteria shares are included in the category of sharia is :

a. Do not perform business activities which contradict Islamic sharia

b. No trade is not accompanied by the delivery of goods / services and trade with

supply and demand false

c. Do not exceed the following financial ratios

1) Total interest-based debt compared with total equity of not more than

82% (interest-based debt compared with total equity of not more than

45%: 55%)

2) Total interest and other lawful income does not compare to total income

(revenue) not more than 10%

Shares included JII amounted to 30 and will be evaluated every six months

based on financial statements, market capitalization, and Islamic principles held.

Financial Statements

The financial statements portray the financial condition and results of operations

of a company at a certain time or a certain period of time (Harahap, 2009). Also

according Soemarso (2010), states that the financial statements are statements that Sare

designed for decision makers, especially parties outside the company, regarding the

financial position and results of operations of the company. Meanwhile, according to

PSAK No. 1 Paragraph 7 (Revised 2009), defines the financial statements are a

structured representation of the financial position and financial performance of an

entity.

The objective of financial statements is to provide information regarding the

financial position, financial performance and cash flows of an entity that is useful for

the majority of reports among users in making economic decisions. The financial

statements also show the results of management accountability for the use of resources

entrusted to them. According to PSAK No. 1 Paragraph 7 (Revised 2009), "in order to

achieve the objective of financial statements, financial statements provide information

about an entity that includes: assets, liabilities, equity, revenues and expenses, including

gains and losses, contributions from and distributions to owners in it is the owner and

cash flows ". That information, along with other information contained in the notes to

the financial statements, to help users report in predicting future cash flows and in

particular, the timing and certainty of obtaining cash and cash equivalents

Bankruptcy

According Mamduh (2008; 638), the notion of bankruptcy can be seen from

the approach flow and the stock approach. Using a stock, the company can be declared

bankrupt if total liabilities exceed its total assets. While the approach cash flow, the

company would go bankrupt if it can not generate sufficient cash flow. From the point

of view of the stock, the company can be declared bankrupt although it may still

generate sufficient cash flow, or have good prospects in the future.

For companies that go public bankruptcy of the company is very sensitive,

because companies that go public should be ready to implement all the obligations by

the capital markets. Definition of bankruptcy by Yani (2004: 153) is a condition when

the company has insufficient funds to run its business. A company can be said to be

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 104

bankrupt, if you have some indicators as revealed by Surjanto (2003: 184), a mark that

can be seen if a company experienced difficulties in running the business, among others:

a. Sales or revenues have decreased significantly.

b. The decline in earnings and cash flow from operations.

c. The decline in total assets.

d. Stock market prices declined significantly.

e. Fallibility in the industry, or high risk.

f. Young company, the company of his young age generally experience difficulties

in the early years of operation, so that if not supported by strong capital

resources will be able to experience serious financial difficulties and ended with

bankruptcy.

g. Significant cuts in dividends.

In law, the term bankruptcy is identified with insolvent. According to Law No. 4

of 1998, which was renewed by Act No. 37 of 2004 on bankruptcy and suspension of

payment obligation, declared a bankruptcy is a situation where an institution is declared

by a court decision if the debtor has two or more creditors and did not pay at least one

debt that has matured and could be charged.

Delisting According to the Decision of the Board Jakarta Stock Exchange Inc. Number:

Kep-308 / BEJ / 07-2004 concerning Rule Number II concerning the delisting (delisted)

and recording back (relisting) shares in the stock is a delisting is the elimination of the

effects of the list of securities listed on exchange so that these effects can not be traded

on exchanges

Grover Model

Grover Model is a model created by designing and reassessment of the model

of the Altman Z-Score. Jeffrey S. Grover using a sample in accordance with the model

of the Altman Z-score in 1968, adding thirteen new financial ratios. Samples used as

many as 70 companies to 35 companies that went bankrupt and 35 companies that are

not bankrupt in 1982 until 1996. Grover formula is as follows :

Score = 1,650X1 + 3,404X3 – 0,016ROA + 0,057

X1 = Working capital/Total assets

X3 = Earnings before interest and taxes/Total assets

ROA = net income/total assets

Grover Model categorizes companies into insolvency with a score less than or

equal to -0.02 (Z ≤ -0.02). While the value for the companies that fall within the state is not broke is greater than or equal to 0.01 (Z ≥ 0.01).

Altman Z-Score Model Altman Z-Score Model is a multivariate formula used to measure the financial

health of a company. Altman found five types of financial ratios that can be combined

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 105

to see the difference between a company that went bankrupt and were not bankrupt.

Discriminant function discovered by Altman Z are as follows: (Weston & Copeland,

2008: 255):

Z= 1,2X1 + 1,4X2 + 3,3X3 + 0,6X4 + 0,999X5

Z = bankrupcy index

X1 = working capital / total asset

X2 = retained earnings / total asset

X3 = earning before interest and taxes / total asset

X4 = market value of equity / book value of total debt

X5 = sales / total asset

With the following criteria:

a. If the value of Z <1.81, then including a bankrupt company.

b. If the value 1.81 <Z <2.99 can not be determined whether the company is

healthy or bankruptcy).

c. If the value of Z> 2.99 then include companies that are not bankrupt.

Based on the results of research conducted, the Altman Z Score Altman method

of use, it has reached 95% accuracy when using the data one year before financial

distress.

Springate Model Springate has formulated bankruptcy prediction model in 1978. In its

formulation, Springate using the same method with Altman, namely Multiple

Discriminant Analysis (MDA). At first model of the S-Score consists of 19 financial

ratios popular. After going through the same test performed Altman, Springate choose

to use four ratios that can reliably distinguish between companies that went bankrupt

and were not bankrupt. The resulting model is as follows (Hadi 2008 in Bayu, 2014):

S = 1.03A + 3.07B + 0.66C + 0.4D

S= Bankrupcy index

A= Working Capital / Total Asset

B= Earning Before Interest and Tax /Total Asset

C= Earning Before Tax / Current Liabilities

D= Sales / total asset

With the following criteria:

a. if the value of S <0.862, the indication of companies face a serious threat

of bankruptcy (bankruptcy),

b. if the value of S> 0,862 then it shows the company in a sound financial

condition and have no problems with finances (not insolvent).

Research that has been done by this method has been used a sample of companies

Different asset value. Botheras (1979) tested this model on 50 companies whose assets

exceeded an average of US $ 2.5 million and found the accuracy rate of 88%. Sands

(1980) tested this model at 24 companies on average assets of US $ 63.4 million and

found the accuracy rate of 83.3%.

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 106

Zmijewski Model

Zmijewski (1984) using a ratio analysis, measuring the performance leverage,

profitability, and liquidity of an enterprise to model predictions. Zmijewski using

analysis applied to 40 companies that have gone bankrupt and 800 companies that still

survive at that time. The model successfully developed by Zmijewski namely

(Margaretta Fanny and Sylvia Saputra, 2005: 4):

X = -4,3 - 4,5X1 + 5,7X2 – 0,004X3

X = bankrupcy index

X1 = ROA (Return on Asset)

X2 = Leverage (Debt Ratio)

X3 = Likuiditas (Current Ratio)

With the assessment criteria:

a. if the score obtained a company from bankruptcy prediction model exceeds 0, the

company predicted the potential bankruptcy.

b. if a company has a score that is less than 0 then the company predicted no

potential for bankruptcy.

Zmijewski (1984) have measured the accuracy of the model itself, and gain

accuracy value of 94.9%

Ohlson Model

Ohlson using logistic analysis to develop a bankruptcy prediction model with

nine independent variables. The ratio used is the leverage ratio, liquidity, and

profitability based on the sample of 105 companies went bankrupt and in 2058 the

company is not bankrupt (Grice and Dugan, 2003:79). Logit model is a further

development of the linear probability model that explains that the logit model analysis

used to estimate the probability of a phenomenon by reducing the weaknesses found in

the linear probability.

Bankruptcy prediction research conducted by Ohlson (1980: 114) using

multivariate models were built to have 9 variables consist of several financial ratios and

dummy variables. Y-Score equation is formulated as follows (Ohlson, 1980: 117-118):

Y-Score = -1,32 - 0,407X1 + 6,03X2 – 1,43X3 + 0,0757X4 – 2,37X5 – 1,83X6

+0,285X7 – 1,72X8 – 0,521X9

X1 = SIZE (LOG total assets/GNP level index)

X2 = Total liabilities/total assets

X3 = Working capital/total assets

X4 = Current liabilities/current assets

X5 = 1 if total liabilities >total assets; 0 otherwise

X6 = Net income/total assets

X7 = Cash flow from operations/total liabilities

X8 = 1 if net income negatif; 0 otherwise

X9 = (NIt – NIt-1) / (NIt + NIt-1), NIt is net income for this period

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 107

Ohlson (1980) stated that this model has the optimal cutoff point at a value of

0.38. Ohlson chose this cutoff because of these values, the number of errors can be

minimized. The purpose of this cutoff is that companies that have a value of Y-Score

more than 0.38 means the company predicted bankruptcy. Conversely, if the value of

the company Y-Score of less than 0.38, the company predicted without bankruptcy.

Net Working Capital to Total Asset This ratio is the ratio between the net working capital (current assets minus

current liabilities) divided by total assets shows the company's ability to generate net

working capital of the overall total assets. Negative net working capital were likely to

face problems in covering short-term liabilities due to the unavailability of sufficient

liquid assets to cover those obligations conversely, companies with net working capital

is positive rarely face difficulties in meeting their obligations

Retained Earnings to Total Assets This ratio is the ratio between retained earnings to total assets is useful to

measure the cumulative benefit of the lifetime of companies that demonstrate the power

of income. This ratio indicates the company's ability to generate retained earnings of the

total assets of the company. Retained earnings is an undistributed profits to

shareholders. In other words, the retained earnings shows how much revenue a company

that is not paid out as dividends to shareholders

Earning Before Interest and Tax to Total Asset This ratio is the ratio between earnings before interest and taxes (EBIT) to total

assets indicate the company's ability to generate profits from the company's assets,

before interest payments and taxes

Market Value of Equity to Book Value of Debt This ratio is the ratio between the market value of equity and book value of debt

shows the company's ability to meet the obligations of the market value of equity

(common stock). The market value of the equity itself is obtained by multiplying the

number of outstanding common shares at the market price per share of common stock.

The book value of debt is obtained by summing current liabilities with long-term

liabilities

Sales / Total Asset

This ratio is the ratio between the total sales / revenue with total assets indicate

whether the company generates sufficient business volume compared to investment in

total assets. This ratio reflects the overall management efficiency in the use of corporate

assets to generate sales in order to make a profit.

Earning Before Tax / Current Liabilities

This ratio is the ratio between earning before taxes (EBT) by total current

liabilities, which indicates the company's ability to generate profit from short-term debt

prior to the payment of taxes

ROA (Return on Asset)

This ratio is the ratio between net profit and total assets of companies that

demonstrate the company's ability to generate profits with the use of assets

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 108

Debt Ratio

This ratio is the ratio between total debt to total assets owned by the company

and shows the composition of the company's debts. This ratio can also be interpreted

from the total amount of assets owned by the company how much sourced from debt

Current Ratio

This ratio shows the ratio between current assets compared to current liabilities,

and shows the company's ability to cope with short-term debt to total current assets held

Gross Domestic Product

Gross domestic product (GDP) is the market value of all goods and services

produced by a country in a given period. GDP is one method for calculating the national

income. Gross Domestic Product (GDP) is the total production of goods and services

produced by the production units in an area at a particular time. Gross Domestic Product

(GDP) is a gauge of economic growth in which gauges economic growth is GDP, GDP

per capita and income per hour Work. As a gauge of economic growth in GDP has the

formula in finding GDP and GDP also has four components as follows:

a. Household consumption

b. Investation

c. government consumption

d. Net exports, which is the difference of total exports and imports

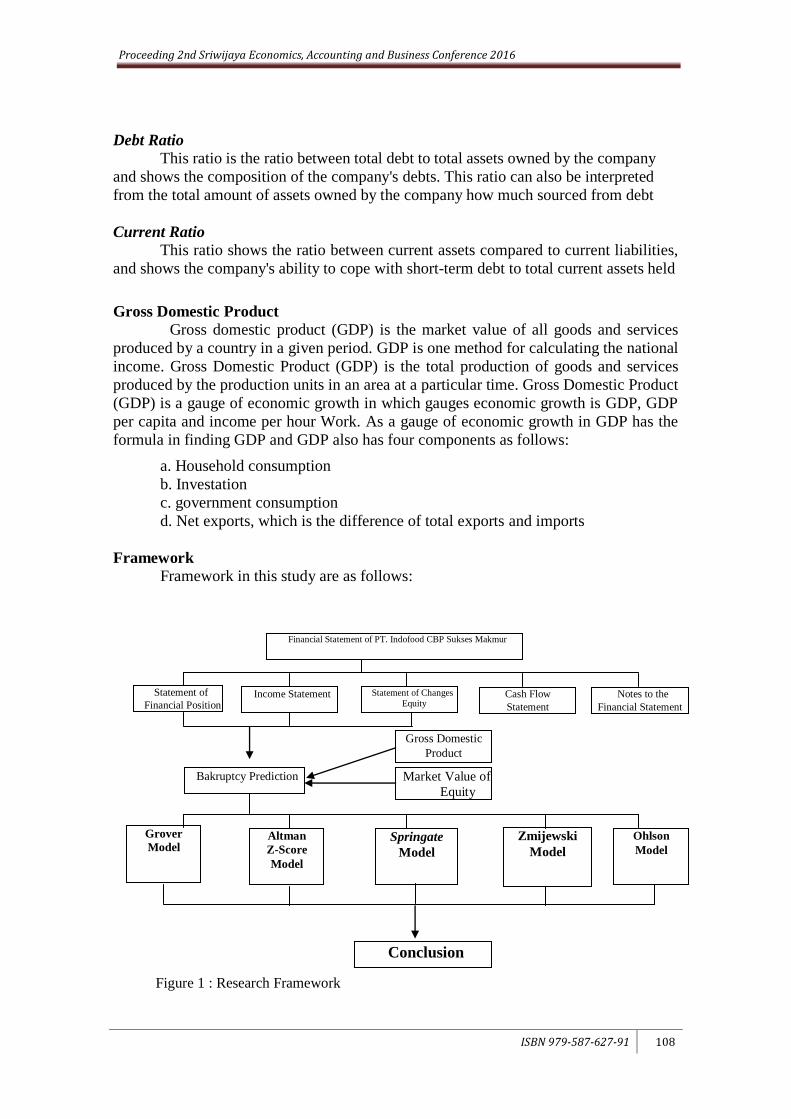

Framework

Framework in this study are as follows:

Financial Statement of PT. Indofood CBP Sukses Makmur

Statement of

Financial Position Income Statement Statement of Changes

Equity Cash Flow

Statement

Notes to the

Financial Statement

Market Value of

Equity

Bakruptcy Prediction

Grover

Model

Springate

Model

Zmijewski

Model

Conclusion

Figure 1 : Research Framework

Gross Domestic

Product

Altman

Z-Score

Model

Ohlson

Model

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 109

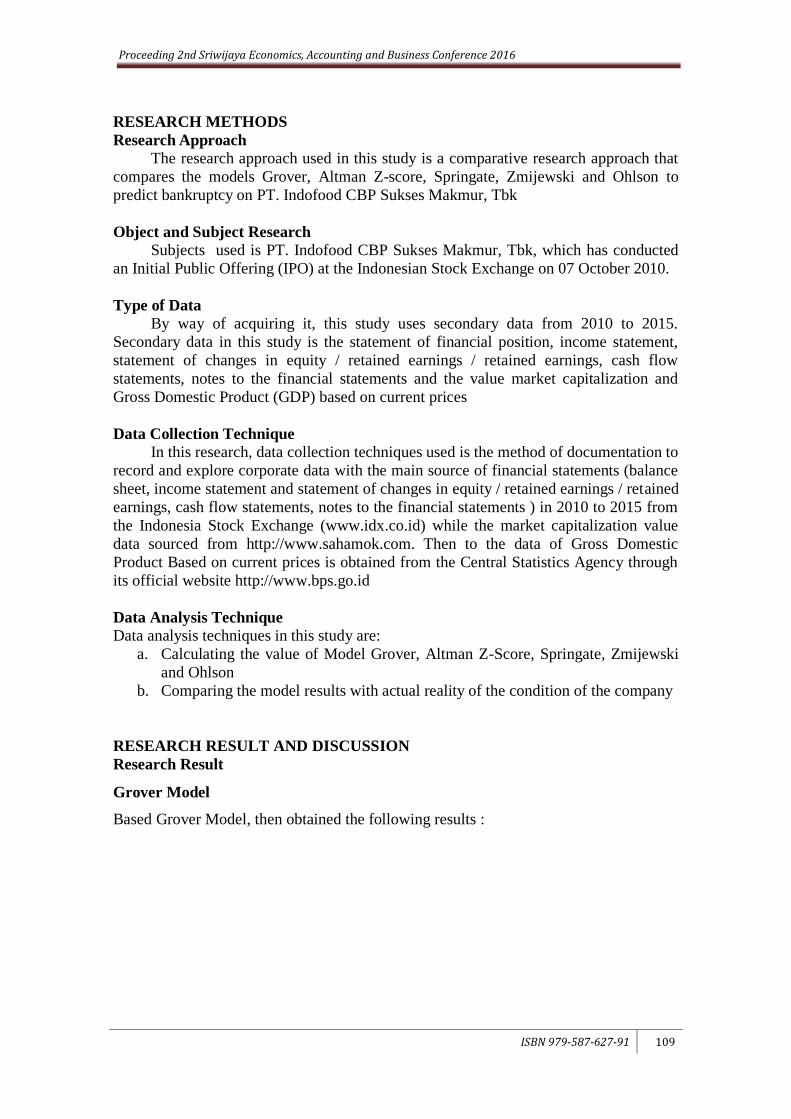

RESEARCH METHODS

Research Approach

The research approach used in this study is a comparative research approach that

compares the models Grover, Altman Z-score, Springate, Zmijewski and Ohlson to

predict bankruptcy on PT. Indofood CBP Sukses Makmur, Tbk

Object and Subject Research

Subjects used is PT. Indofood CBP Sukses Makmur, Tbk, which has conducted

an Initial Public Offering (IPO) at the Indonesian Stock Exchange on 07 October 2010.

Type of Data

By way of acquiring it, this study uses secondary data from 2010 to 2015.

Secondary data in this study is the statement of financial position, income statement,

statement of changes in equity / retained earnings / retained earnings, cash flow

statements, notes to the financial statements and the value market capitalization and

Gross Domestic Product (GDP) based on current prices

Data Collection Technique

In this research, data collection techniques used is the method of documentation to

record and explore corporate data with the main source of financial statements (balance

sheet, income statement and statement of changes in equity / retained earnings / retained

earnings, cash flow statements, notes to the financial statements ) in 2010 to 2015 from

the Indonesia Stock Exchange (www.idx.co.id) while the market capitalization value

data sourced from http://www.sahamok.com. Then to the data of Gross Domestic

Product Based on current prices is obtained from the Central Statistics Agency through

its official website http://www.bps.go.id

Data Analysis Technique

Data analysis techniques in this study are:

a. Calculating the value of Model Grover, Altman Z-Score, Springate, Zmijewski

and Ohlson

b. Comparing the model results with actual reality of the condition of the company

RESEARCH RESULT AND DISCUSSION

Research Result

Grover Model

Based Grover Model, then obtained the following results :

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 110

Table 1 According to Grover Bankruptcy Prediction Model

Year Score Information

2010 1,23289 Not Bankrupt

2011 1,22898 Not Bankrupt

2012 1,18021 Not Bankrupt

2013 1,01298 Not Bankrupt

2014 0,97729 Not Bankrupt

2015 1,06131 Not Bankrupt

Source: Data Processed

Based on the model boundary value Gover ie ≤ - 0.02, the company predicted

bankruptcies and ≥ 0.01 the company predicted no bankruptcy. Based on the results

obtained over the 6 years of data are used, the Grover Model predicts company PT.

Indofood CBP Sukses Makmur, Tbk is not bankrupt.

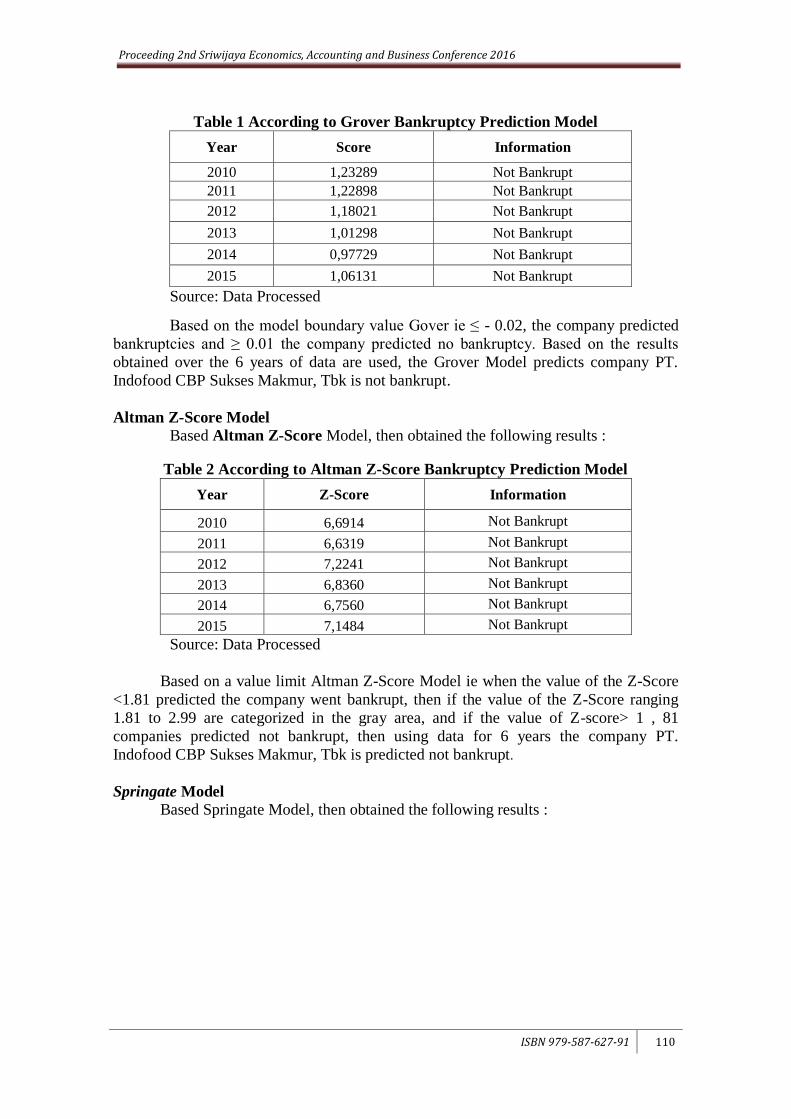

Altman Z-Score Model

Based Altman Z-Score Model, then obtained the following results :

Table 2 According to Altman Z-Score Bankruptcy Prediction Model

Year Z-Score Information

2010 6,6914 Not Bankrupt

2011 6,6319 Not Bankrupt

2012 7,2241 Not Bankrupt

2013 6,8360 Not Bankrupt

2014 6,7560 Not Bankrupt

2015 7,1484 Not Bankrupt

Source: Data Processed

Based on a value limit Altman Z-Score Model ie when the value of the Z-Score

<1.81 predicted the company went bankrupt, then if the value of the Z-Score ranging

1.81 to 2.99 are categorized in the gray area, and if the value of Z-score> 1 , 81

companies predicted not bankrupt, then using data for 6 years the company PT.

Indofood CBP Sukses Makmur, Tbk is predicted not bankrupt.

Springate Model

Based Springate Model, then obtained the following results :

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 111

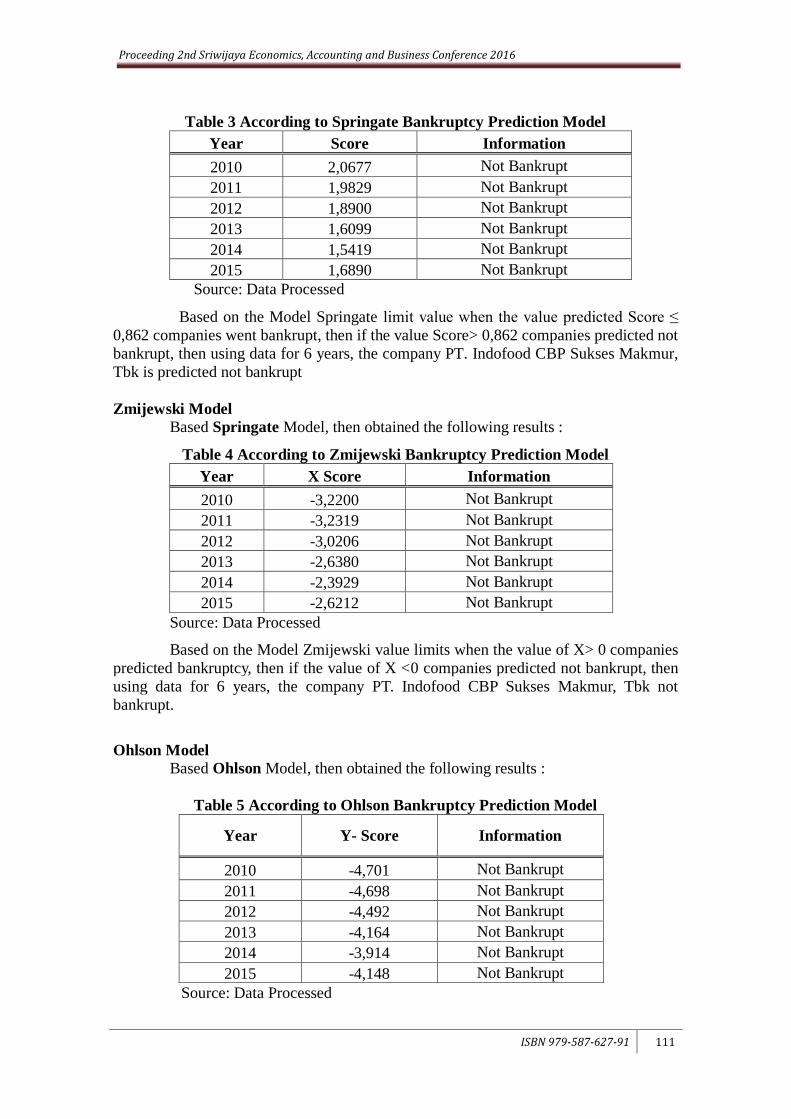

Table 3 According to Springate Bankruptcy Prediction Model

Year Score Information

2010 2,0677 Not Bankrupt

2011 1,9829 Not Bankrupt

2012 1,8900 Not Bankrupt

2013 1,6099 Not Bankrupt

2014 1,5419 Not Bankrupt

2015 1,6890 Not Bankrupt

Source: Data Processed

Based on the Model Springate limit value when the value predicted Score ≤

0,862 companies went bankrupt, then if the value Score> 0,862 companies predicted not

bankrupt, then using data for 6 years, the company PT. Indofood CBP Sukses Makmur,

Tbk is predicted not bankrupt

Zmijewski Model

Based Springate Model, then obtained the following results :

Table 4 According to Zmijewski Bankruptcy Prediction Model

Year X Score Information

2010 -3,2200 Not Bankrupt

2011 -3,2319 Not Bankrupt

2012 -3,0206 Not Bankrupt

2013 -2,6380 Not Bankrupt

2014 -2,3929 Not Bankrupt

2015 -2,6212 Not Bankrupt

Source: Data Processed

Based on the Model Zmijewski value limits when the value of X> 0 companies

predicted bankruptcy, then if the value of X <0 companies predicted not bankrupt, then

using data for 6 years, the company PT. Indofood CBP Sukses Makmur, Tbk not

bankrupt.

Ohlson Model

Based Ohlson Model, then obtained the following results :

Table 5 According to Ohlson Bankruptcy Prediction Model

Year Y- Score Information

2010 -4,701 Not Bankrupt

2011 -4,698 Not Bankrupt

2012 -4,492 Not Bankrupt

2013 -4,164 Not Bankrupt

2014 -3,914 Not Bankrupt

2015 -4,148 Not Bankrupt

Source: Data Processed

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 112

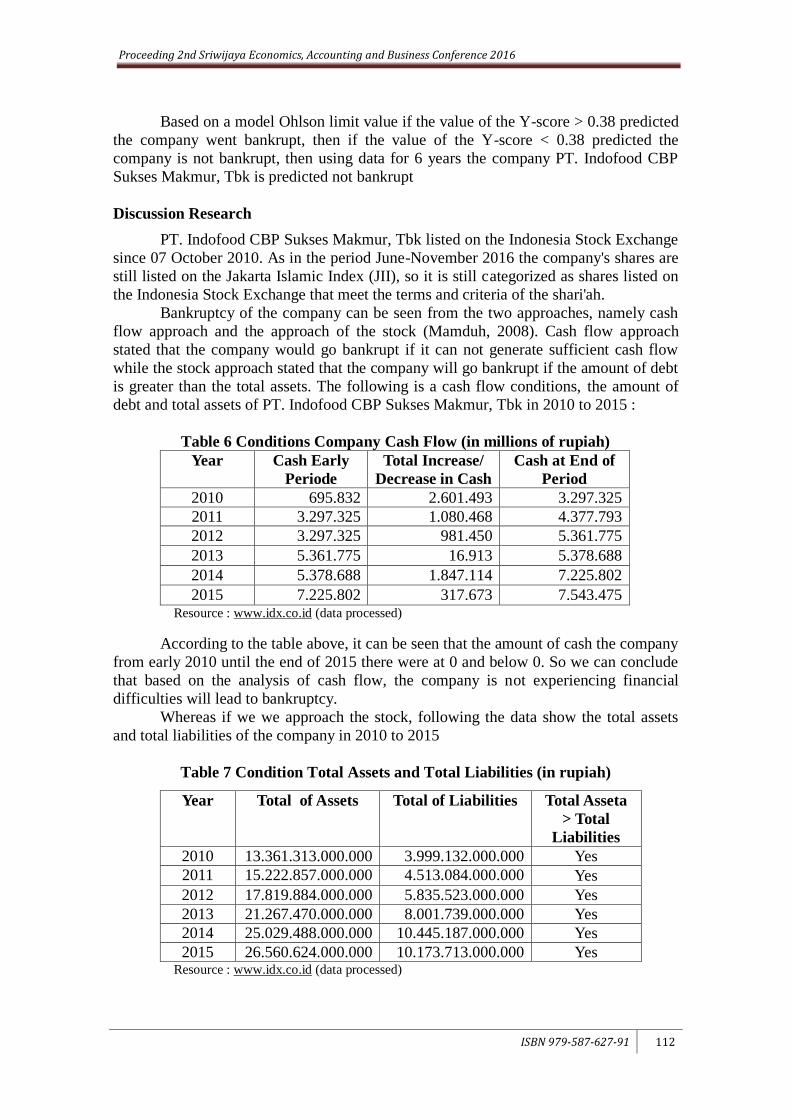

Based on a model Ohlson limit value if the value of the Y-score > 0.38 predicted

the company went bankrupt, then if the value of the Y-score < 0.38 predicted the

company is not bankrupt, then using data for 6 years the company PT. Indofood CBP

Sukses Makmur, Tbk is predicted not bankrupt

Discussion Research

PT. Indofood CBP Sukses Makmur, Tbk listed on the Indonesia Stock Exchange

since 07 October 2010. As in the period June-November 2016 the company's shares are

still listed on the Jakarta Islamic Index (JII), so it is still categorized as shares listed on

the Indonesia Stock Exchange that meet the terms and criteria of the shari'ah.

Bankruptcy of the company can be seen from the two approaches, namely cash

flow approach and the approach of the stock (Mamduh, 2008). Cash flow approach

stated that the company would go bankrupt if it can not generate sufficient cash flow

while the stock approach stated that the company will go bankrupt if the amount of debt

is greater than the total assets. The following is a cash flow conditions, the amount of

debt and total assets of PT. Indofood CBP Sukses Makmur, Tbk in 2010 to 2015 :

Table 6 Conditions Company Cash Flow (in millions of rupiah)

Year Cash Early

Periode

Total Increase/

Decrease in Cash

Cash at End of

Period

2010 695.832 2.601.493 3.297.325

2011 3.297.325 1.080.468 4.377.793

2012 3.297.325 981.450 5.361.775

2013 5.361.775 16.913 5.378.688

2014 5.378.688 1.847.114 7.225.802

2015 7.225.802 317.673 7.543.475 Resource : www.idx.co.id (data processed)

According to the table above, it can be seen that the amount of cash the company

from early 2010 until the end of 2015 there were at 0 and below 0. So we can conclude

that based on the analysis of cash flow, the company is not experiencing financial

difficulties will lead to bankruptcy.

Whereas if we we approach the stock, following the data show the total assets

and total liabilities of the company in 2010 to 2015

Table 7 Condition Total Assets and Total Liabilities (in rupiah)

Year Total of Assets Total of Liabilities Total Asseta

> Total

Liabilities

2010 13.361.313.000.000 3.999.132.000.000 Yes

2011 15.222.857.000.000 4.513.084.000.000 Yes

2012 17.819.884.000.000 5.835.523.000.000 Yes

2013 21.267.470.000.000 8.001.739.000.000 Yes

2014 25.029.488.000.000 10.445.187.000.000 Yes

2015 26.560.624.000.000 10.173.713.000.000 Yes Resource : www.idx.co.id (data processed)

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 113

According to the table above, it can be seen that the total assets in 2010 to 2015

is greater than the total liabilities. So that we can conclude that based approach to the

stock, the company is not experiencing financial difficulties will lead to bankruptcy.

Furthermore, based on Law Number 37 Year 2004 on bankcruptcy and

Postponement of Debt Payments which states that companies that declare bankruptcy

should report to the Court and then the Court who decide whether a company is not

bankrupt or insolvent by a variety of considerations that exist. Implications of

companies that declare bankruptcy is an indication of companies experiencing financial

difficulties and will be bankrupt. However, based on observations of investigators to the

Notes to Financial Statements of the Company in 2010 and 2015 can not be found a

statement declaring their extraordinary events related to the condition of the company's

financial difficulties continued by reporting to the Court. In addition, the condition that

the company that became the object of research is still actively registered in the

Indonesia Stock Exchange until Q2 2016 and the absence of events outside promulgated

by the Capital Market Supervisory Agency against these three companies, it can be

concluded the company is in condition healthy and is not indicated for bankruptcy.

CONCLUSIONS AND RECOMMENDATIONS

Conclusions

Based on the research results, it could be concluded as follows:

a. Bankruptcy prediction model used is the model Grover, Altman Z-Score Model,

Model Springate, Zmijewski Model and Ohlson Model predicts that PT.

Indofood CBP Sukses Makmur, Tbk is not bankrupt.

b. Under the conditions of the cash flow and assets of PT. Indofood CBP Sukses

Makmur, Tbk in 2010 to 2015 were good, and remain listed on the Indonesia

Stock Exchange and the Jakarta Islamic Index, so it can be categorized as the

company is not bankrupt.

c. Based on the conclusions point a and point b, then the Bankruptcy Prediction

Model Model Grover, Altman Z-Score Model, Model Springate, Zmijewski

Model and Model Ohlson has accuracy for predicting corporate bankruptcies.

Recommendations

a. The number of companies that became the object of research is limited to one

type of company, which is expected next researcher to add a number of

companies that became the object of research.

b. The models used in predicting bankruptcy is limited to 5 kinds of models, so it is

advisable to further researchers to add other corporate bankruptcy prediction

model.

REFERENCES

Altman, Edward I. (1968). Financial Ratios, Discriminant Analysis And The Prediction

Of Corporate Bankruptcy. Blackwell Publishing For The American Finance

Association.

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 114

.................... (1983). Corporate Financial Distress: A Complete Guide to Predicting,

Avoiding and Dealing with Bankruptcy (Wiley Finance). JohnWiley & Sons:New

Jersey Canada.

Bayu, Stevanus Aditya. (2014). Perbandingan Model Prediksi Kebangkrutan

Perusahaan Publik (Model Altman, Springate Dan, Ohlson). Tesis, Universitas

Atma Jaya Yogyakarta, Yogyakarta

Christianti, Ari. (2013). Akurasi Prediksi Financial Distress: Perbandingan Model

Altman Dan Ohlson. Jurnal Ekonomi & Bisnis (JEB). STIE YKPN Yogyakarta.

Fahmi, Irham. (2013). Analisis Laporan Keuangan. Bandung: Alfabeta.

Grice, J. Stephen, Jr & Dugan. M.T. (2003). Re-Estimations of The Zmijewski and

Ohlson Bankruptcy Prediction Models. Journal of Advance in Accounting,20: 77-

93

Harahap, Sofyan Syafri. (2009). Analisis Kritis Atas Laporan Keuangan. Jakarta: Raja

Grafindo Persada

Hastuti, Rini Tri. (2015). Analisis Komparasi Model Prediksi Financial Distress

Altman, Springate, Grover Dan Ohlson Pada Perusahaan Manufaktur Yang

Terdaftar Di Bursa Efek Indonesia Periode 2011-2013. Jurnal Ekonomi/Volume

XX, No. 03, November 2015: 446-462.

IDX Yearly, 2010, 2011, 2012, 2013, 2014, 2015

Ikatan Akuntansi Indonesia. (2009). ED PSAK No. 01 (Revisi 2009). Jakarta . Salemba

Empat..

Indonesian Capital Market Directory, 2012, 2013, 2014, 2015

Jayanti, Queenaria dan Rustiana.(2014). Analisis tingkat akurasi Model-model prediksi

kebangkrutan Untuk memprediksi voluntary Auditor Switching. http://e-journal.

uajy. ac. id/ 6178/ 1/jurnal.pdf

Keputusan Direksi PT. Bursa Efek Jakarta Nomor : Kep-308/BEJ/07-2004 tentang

Peraturan Nomor I-I Tentang Penghapusan Pencatatan (Delisting) dan Pencatatan

Kembali (Relisting)

Mamduh, M. Hanafi. 2008. Manajemen Keuangan, Edisi 1, Cetakan

Kedua.Yogyakarta:BPFE

Margaretta, Fanny dan Sylvia Saputra. (2005). Opini Audit Going Concern: Kajian

Berdasarkan Model Prediksi Kebangkrutan, Pertumbuhan Perusahaan, dan

Reputasi Kantor Akuntan Publik (Studi pada Emiten BEJ).

Ohlson, J. (1980). Financial Ratios and The Probabilistic Prediction of Bankruptcy. Journal

of Accounting Research, Vol. 18, No. 1, page 109-131.

Soemarso S.R. (2010). Akuntansi : Suatu Pengantar , Cetakan Keempat, Jakarta :

Salemba Empat

Suharman, H. (2007). Analisis Risiko Keuangan untuk Memprediksi Tingkat Kegagalan

Usaha Bank. Jurnal Imiah ASET, Vol. 9, No. 1 Februari

Proceeding 2nd Sriwijaya Economics, Accounting and Business Conference 2016

ISBN 979-587-627-91 115

Surjanto, R. L. (2003). Financial Performance Analyzing . PT. Gramedia: Jakarta.

Undang-Undang Republik Indonesia Nomor 4 Tahun 1998 Tentang Kepailitan Dan

Penundaan Kewajiban Pembayaran Utang

Undang-Undang Republik Indonesia Nomor 37 Tahun 2004 Tentang Kepailitan Dan

Penundaan Kewajiban Pembayaran Utang

Yani, W. (2004). Seri Hukum Bisnis Kepailitan. Jakarta: PT. Raja Grafindo Persada.

Weston. J. Fred dan Copeland, Thomas E. (2008). Manajemen Keuangan Edisi

Kesembilan, Penerjemah : Jaka Wasana. Jakarta : Bina Rupa Aksara

Wulandari, Veronita et al, (2014), Analysis Of Comparison Financial Distress Prediction

Models Altman, Springate, Ohlson , Fulmer, CA-Score and Zmijewski, (Empiric

Study On Listed Food And Beverages Firms In Indonesia Stock Exchange Period

2010-2012). JOM FEKON Vol. 1 No. 2 Oktober 2014.

www.bps.go.id

www.idx.co.id ( 28 Agustus 2015)

www.sahamok.com (1 September 2015)

Zmijewski, M. E. (1984). Methodological Issues Related to the Estimation of Financial Distress

Prediction Models. Journal of Accounting Research 24 (Supplement): 59 - 82