Embed Size (px)

Citation preview

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 1/21

1

Corporate Law Update: December 30, 2012

Analysis of Companies Bill 2011

CUSTOMISED DELIVERY | OBJECTIVE ADVICE | KNOWLEDGE INSIGHT | CLEAR FORESIGH

On December 18, 2012,

Sabha approved Companies

2011 (Bill No. 121-C of 2011),

bid to make sweeping changes

the existing 56 years old law, T

Companies Act, 1956. The

objects of the new legislation

to protect interest of sm

investors, encourage companto undertake social welfare a

promote societal interests. T

Bill is expected to be passed

Rajya Sabha early next ye

Thereafter, the Bill will be ca

Companies Act, which will co

into force from the date to

notified by Government. We h

analysed the salient features

the Bill in this Update.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 2/21

2

Table of Contents

I. Executive Summary – Salient features of Bill ...................................................................3

II. Impact of Companies Bill on various stakeholders ............................................................9

III. Detailed Analysis .............................................................................................................11

IV. Our Comments ................................................................................................................20

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 3/21

3

I. Executive Summary – Salient features of Companies Bill

CORPORATE SOCIAL RESPONSIBILITY:

Obligatory for company having net worth of Rs.500 crores or more or turnover of

Rs.1000 crores or more or net profit of Rs.5 crores or more during any financial year to

constitute a committee for Corporate Social Responsibility

Committee to formulate and recommend activities to be undertaken as per Schedule VII

for eradicating extreme hunger and poverty, promotion of education, gender equality and

empowering women, ensuring environmental sustainability, etc.

Board to ensure that company spends in each financial year atleast 2% of the average

net profits of three immediately preceding financial years. Company shall give

preference to local area and areas around it where it operates.

Failure to implement – cite reasons for failure

DIRECTORS

Mandatory for prescribed class of companies to have at least one woman director

Every company to have at least one director who has stayed in India for 182 days

or more in previous calendar year

Maximum number of directors increased to 15. Further increase after passing special

resolution

Duties of directors have been defined

Resignation by notice to company. Resignation with detailed reasons to be forwarded to

Registrar Ever listed company and other prescribed classes of companies to have independent

directors

Independent directors not entitled to stock options

Tenure restricted to two consecutive terms of 5 years, eligible for re-appointment after 3

years

The company and independent directors to abide by Code for independent

directors -Code of professional conduct – guidelines, role and functions, duties,

etc. defined

'Independent Directors' shall be excluded for the purpose of computing 'one third of

retiring Directors'

Independent director to be held liable only for acts of omission or commission by

company which had occurred with his knowledge, attributable through board

process and with his consent or connivance or where he had not acted diligently

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 4/21

4

MANAGERIAL PERSONNEL

Every company belonging to such class as may be prescribed shall have whole time keymanagerial personnel

Managing or whole-time director or manager not eligible for appointment if

sentenced to imprisonment for any period or to a fine exceeding Rs.1000 for

conviction of any offence under any acts namely Indian Stamp Act, Central Excise

Act, Securities Contracts Regulation Act, Customs Act, FEMA, Income-tax Act,

etc.

Unless articles provide otherwise, individual shall not be chairperson as well as

Managing Director or Chief Executive Officer of company at the same time. A class of

companies having multiple business and separate divisional managing directors to

appoint same person as chairman as well as managing director

Failure to appoint key managerial personnel to attract penalty

Managerial remuneration – maximum limit of 11% of net profits

Companies with no profits or inadequate profits, remuneration payable as per new

schedule of Remuneration

Remuneration : Except general meeting approval,

to any one managing director or whole-time director or manager shall not exceed

5% of net profits

If more than one such director – shall not exceed 10% of net profits to all such

directors and managers taken together

Other than managing directors or whole-time directors – 1% of net profit if there

is managing or whole-time director or manager, 3% in other cases

AUDIT AND AUDITORS

Internal Audit mandatory for class of companies as may be prescribed – CA or

Cost Accountant or such other professional as may be decided by Board to

conduct audit

Limited Liability Partnerships may be appointed as auditors

Maximum number of companies in which a person may be appointed as auditor - 20

companies

Appointment of auditors for 5 years – appointment subject to ratification bymembers at every Annual General Meeting

Mandatory rotation of auditors for listed company and other prescribed classes of

companies - after 5 years for individual CA and 10 years in case of CA firm

Rotation of auditing partner and his team (in case of an audit firm) as may be resolved

by members

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 5/21

5

Restrictions on Auditor to provide either directly or indirectly non-audit services

such as accounting and book keeping, design and implementation of any financial

information system, management services, investment advisory services,

investment banking services, rendering of outsourced financial services, etc. to

the company, its holding company and subsidiary company.

Resignation of auditors – statement in prescribed form to be filed with company as well

as ROC indicating reasons and other facts as may be relevant, failure to attract fine

Tribunal may direct company to change auditors if satisfied that auditor acted in

fraudulent manner or abetted or colluded in any fraud by or in relation to company or its

directors or officers

Duties of auditor/secretarial auditor/cost auditor to report to Central Government

where fraud is committed or being committed on company. Failure to report to

attract fine

Liability of auditors

Contravention of certain provisions – fine Knowingly or willful contravention with the intent to deceive company,

shareholders, creditors, tax authorities – imprisonment and fine

Convicted for offence – liable to refund remuneration and pay damages for loss

arising out of incorrect or misleading statements in audit report

Central Government to specify any statutory body/authority/officer for ensuring

prompt payment of damages

In case of audit firm – if it proved that audit partner/s have acted in fraudulent

manner or abetted or colluded in any fraud, the liability, civil or criminal, would be

of audit partner/s concerned as well as of the firm jointly and severally.

Cost audit to be mandatory for class of companies engaged in production of such goodsor providing such services as prescribed and which have a net worth of such amount as

may be prescribed or a turnover of such amount as may be prescribed

Auditing and cost auditing standards made mandatory

Mandatory Secretarial audit for listed companies and such class of companies as

may be prescribed by Company Secretary in Practice

E-GOVERNANCE

Maintenance and allowing inspection of documents by companies in electronic form

Participation of directors in board meetings through video conferencing or other

electronic means

Voting through electronic means by members

Registration process made faster and compatible with e-governance

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 6/21

6

INVESTOR PROTECTION MEASURES

Issue and transfer of securities and non-payment of dividend by listed companies to beadministered by SEBI

Punishment for falsely inducing a person to invest money (including inducing to enter

into any agreement with bank or financial institution, with a view to obtaining credit

facilities) – imprisonment which may extend to 10 years and fine not less than three

times the amount involved in fraud

Suit may be filed by any person affected by any misleading statement or inclusion or

omission of any matter in prospectus

Class action suits – specified number of members or class of members or

depositors may file an application before Tribunal, if they are of the opinion that

management or control of affairs of company are conducted in manner prejudicial

to interest of company or members or creditors or depositors

Investigation into affairs of company by Serious Fraud Investigation Office. Investigation

report filed with court for framing of charges shall be treated as report filed by Police

Officer

Prohibition on insider trading of securities

Directors and Key Managerial personnel prohibited from forward dealings in

securities of company

ACCOUNTS

Financial statements to include balance sheet, profit & loss account, cash flowstatement, statement of changes in equity, explanatory notes

Voluntary revision of financial statement or Board’s report of three preceding

financial years after obtaining approval of Tribunal

Reopening of accounts if order made by Court or Tribunal to the effect that earlier

accounts were prepared in fraudulent manner or affairs were mismanaged casting a

doubt on financial statements

National Financial Reporting Authority responsible for monitoring and enforcing

compliance with accounting and auditing standards, empowered to investigate

into professional or other misconduct of CAs

Depreciation to be provided as per Schedule II which provides for useful lives of assets

to compute depreciate

Consolidation of accounts of subsidiaries including associate company, joint venture

mandatory

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 7/21

7

OTHER IMPORTANT PROVISIONS

Concept of One Person Company introduced – subjected to lesser stringentframework

Definition of subsidiary company – company in which holding company

Controls composition of board of directors

Exercises or controls more than half of total share capital either at its own or

together with one or more of its subsidiary companies

Such class or classes of holding companies as may be prescribed shall not have

layers of subsidiaries beyond such numbers as may be prescribed

Related party defined to include any person on whose advice, directions or

instructions a director or manager is accustomed to act (not applicable to advice,

directions or instructions in professional capacity) Term 'Private Placement' defined – to mean offer of securities or invitation to subscribe

securities by company satisfying certain conditions such as offer or invitation is to select

group of persons, it is through issue of private placement letter, etc.

Unless otherwise provided, company not to make investment through more than two

layers of investment companies

Articles of Association may contain provision for entrenchment – more restrictive

procedure for altering certain provisions of articles

Rate of interest on inter corporate loans to be prevailing rate of interest on dated

Government Securities. Audit Committee to act on terms of reference which shall include

scrutiny of inter-corporate loans and investments

Mandatory for listed companies and other classes of companies as prescribed to have Audit Committee, Nomination and Remuneration Committee and Stakeholder’s

Relationship Committee

The Board’s report to disclose the composition of an Audit Committee and where

the Board had not accepted any recommendation of the Audit Committee, the

same shall be disclosed along with the reasons

Approval of the Tribunal shall be required for consolidation and division of share capital

only if the voting percentage of shareholders changes consequent on such

consolidation.

Vigil mechanism for directors and employees to report genuine concerns to be

established for every listed company or class of companies as may be prescribed Adequate safeguards against victimization of persons who use such mechanism

Make provision for direct access to chairperson of Audit Committee in

appropriate or exceptional cases

Details of establishment of such mechanism to be disclosed on website and in

Board’s report

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 8/21

8

Valuation of any property, stock, shares, debentures, securities or goodwill or net worth

of company or its assets to be done by registered valuer appointed by audit committee

or in its absence by board of directors

Schedules provided for General instructions for preparation of balance sheet and

statement of profit and loss of company, code for independent directors, infrastructural

projects/infrastructural facilities for issue of preference shares exceeding 20 years,activities which may be included in Corporate Social Responsibility Policies

Cross border mergers with foreign company allowed

For speedy trial of offences, Central Government empowered to establish special courts

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 9/21

9

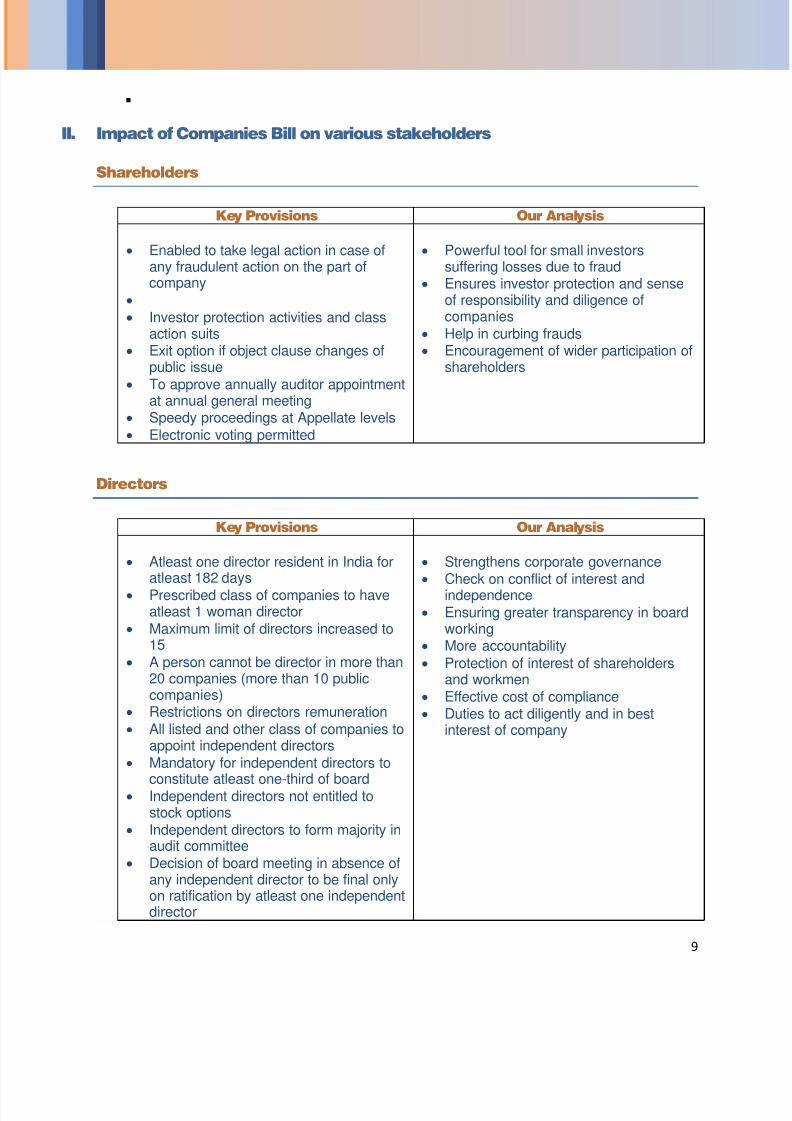

II. Impact of Companies Bill on various stakeholders

Shareholders

Key Provisions Our Analysis

Enabled to take legal action in case ofany fraudulent action on the part ofcompany

Investor protection activities and class

action suits Exit option if object clause changes of

public issue

To approve annually auditor appointmentat annual general meeting

Speedy proceedings at Appellate levels

Electronic voting permitted

Powerful tool for small investorssuffering losses due to fraud

Ensures investor protection and senseof responsibility and diligence ofcompanies

Help in curbing frauds Encouragement of wider participation of

shareholders

Directors

Key Provisions Our Analysis

Atleast one director resident in India foratleast 182 days

Prescribed class of companies to haveatleast 1 woman director

Maximum limit of directors increased to15

A person cannot be director in more than20 companies (more than 10 publiccompanies)

Restrictions on directors remuneration

All listed and other class of companies toappoint independent directors

Mandatory for independent directors to

constitute atleast one-third of board Independent directors not entitled to

stock options

Independent directors to form majority inaudit committee

Decision of board meeting in absence ofany independent director to be final onlyon ratification by atleast one independentdirector

Strengthens corporate governance

Check on conflict of interest andindependence

Ensuring greater transparency in boardworking

More accountability

Protection of interest of shareholdersand workmen

Effective cost of compliance

Duties to act diligently and in bestinterest of company

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 10/21

10

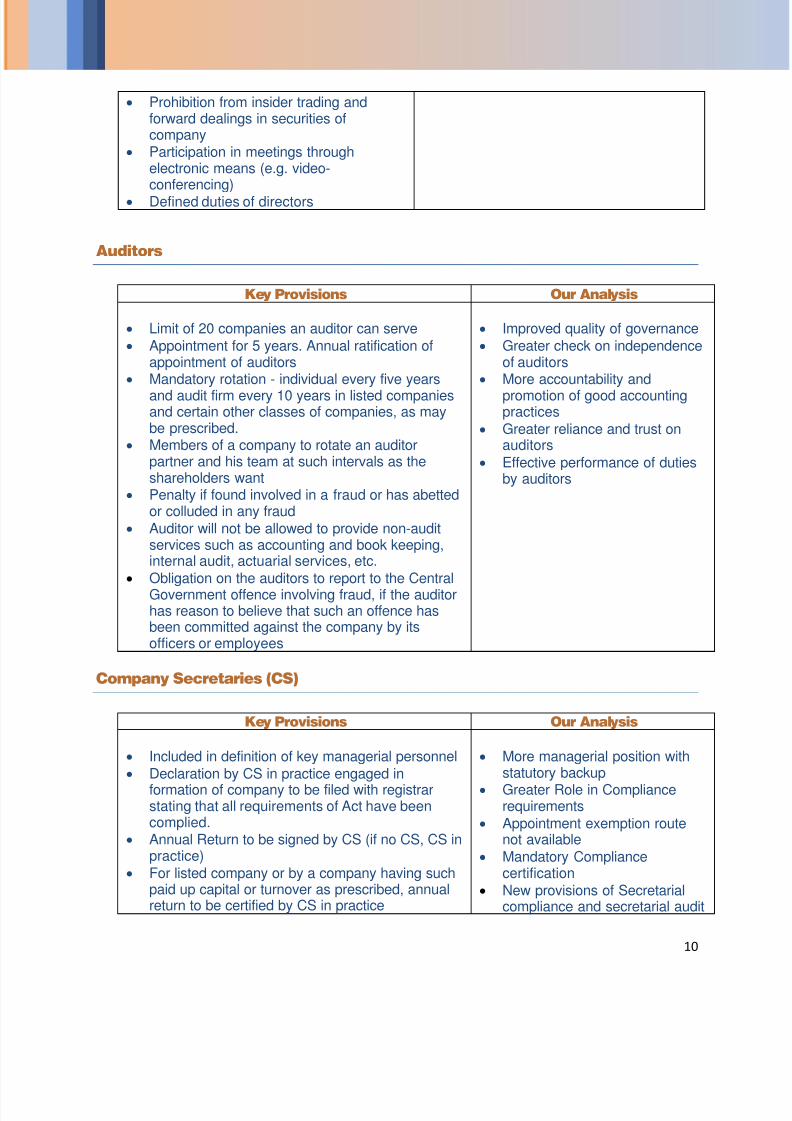

Prohibition from insider trading andforward dealings in securities ofcompany

Participation in meetings throughelectronic means (e.g. video-conferencing)

Defined duties of directors

Auditors

Key Provisions Our Analysis

Limit of 20 companies an auditor can serve

Appointment for 5 years. Annual ratification ofappointment of auditors

Mandatory rotation - individual every five years

and audit firm every 10 years in listed companiesand certain other classes of companies, as maybe prescribed.

Members of a company to rotate an auditorpartner and his team at such intervals as theshareholders want

Penalty if found involved in a fraud or has abettedor colluded in any fraud

Auditor will not be allowed to provide non-auditservices such as accounting and book keeping,internal audit, actuarial services, etc.

Obligation on the auditors to report to the CentralGovernment offence involving fraud, if the auditorhas reason to believe that such an offence hasbeen committed against the company by itsofficers or employees

Improved quality of governance

Greater check on independenceof auditors

More accountability and

promotion of good accountingpractices

Greater reliance and trust onauditors

Effective performance of dutiesby auditors

Company Secretaries (CS)

Key Provisions Our Analysis

Included in definition of key managerial personnel

Declaration by CS in practice engaged in

formation of company to be filed with registrarstating that all requirements of Act have beencomplied.

Annual Return to be signed by CS (if no CS, CS inpractice)

For listed company or by a company having suchpaid up capital or turnover as prescribed, annualreturn to be certified by CS in practice

More managerial position withstatutory backup

Greater Role in Compliancerequirements

Appointment exemption routenot available

Mandatory Compliancecertification

New provisions of Secretarialcompliance and secretarial audit

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 11/21

11

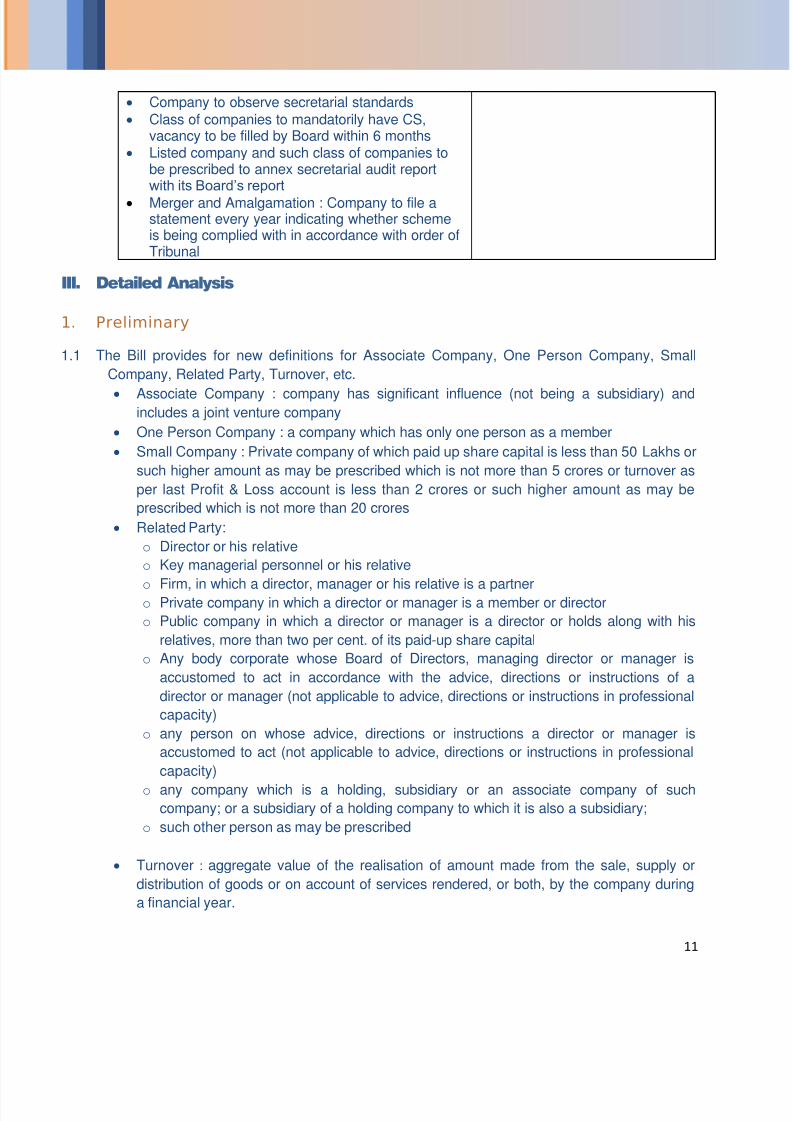

Company to observe secretarial standards

Class of companies to mandatorily have CS,vacancy to be filled by Board within 6 months

Listed company and such class of companies tobe prescribed to annex secretarial audit reportwith its Board’s report

Merger and Amalgamation : Company to file astatement every year indicating whether schemeis being complied with in accordance with order ofTribunal

III. Detailed Analysis

1. Preliminary

1.1 The Bill provides for new definitions for Associate Company, One Person Company, Small

Company, Related Party, Turnover, etc.

Associate Company : company has significant influence (not being a subsidiary) andincludes a joint venture company

One Person Company : a company which has only one person as a member

Small Company : Private company of which paid up share capital is less than 50 Lakhs or

such higher amount as may be prescribed which is not more than 5 crores or turnover as

per last Profit & Loss account is less than 2 crores or such higher amount as may be

prescribed which is not more than 20 crores

Related Party:

o Director or his relative

o Key managerial personnel or his relative

o Firm, in which a director, manager or his relative is a partner

o Private company in which a director or manager is a member or director

o Public company in which a director or manager is a director or holds along with his

relatives, more than two per cent. of its paid-up share capital

o Any body corporate whose Board of Directors, managing director or manager is

accustomed to act in accordance with the advice, directions or instructions of a

director or manager (not applicable to advice, directions or instructions in professional

capacity)

o any person on whose advice, directions or instructions a director or manager is

accustomed to act (not applicable to advice, directions or instructions in professional

capacity)

o any company which is a holding, subsidiary or an associate company of suchcompany; or a subsidiary of a holding company to which it is also a subsidiary;

o such other person as may be prescribed

Turnover : aggregate value of the realisation of amount made from the sale, supply or

distribution of goods or on account of services rendered, or both, by the company during

a financial year.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 12/21

12

1.2 Some of the other new definitions introduced are CEO, CFO, control, promoter, interested

director, key managerial personnel, etc.

1.3 Financial Year - It can be only April to March for every financial year. The relaxation is available

to holding or subsidiary of a company outside India following different financial year for

consolidation. Approval of Tribunal is required for following different financial year.

1.4 The limit on number of maximum members of private company is raised to 200. 1.5 Officer in default liable to penalty or punishment to include director/s giving consent in writing to

board, any person under the immediate authority of board or key management personnel

having responsibility of maintenance, filing of accounts, records, etc. who actively participates

or knowingly permits or fails to take corrective steps (i.e. Chief Financial Officer), any person

in accordance with whose advice, directions or instructions the Board of Directors of the

company is accustomed to act (advice other than in professional capacity), directors who are

aware of the default by way of participation in board meeting or receiving the minutes without

objecting to the same, share transfer agents, registrars and merchant bankers to the issue or

transfer of shares.

2. Relating to Incorporation and connected matters

2.1 Concept of Small companies have been introduced which shall be subjected to a lesser

stringent regulatory framework

2.2 In the Memorandum of Association of the Company, there is no requirement as to bifurcation

of the objects clause into main, ancillary and other objects. Only objects for which company is

incorporated along with matters considered necessary for its furtherance shall be mentioned.

2.2 A declaration, in the prescribed form, required to be filed with the Registrar at the time of

registration of a company that all the requirements of the Act in respect of registration and

matters precedent or incidental thereto have been complied with, will be required to signed by

both – a person named in the articles as a director, manager or secretary of the company aswell as by an advocate, a chartered accountant, cost accountant or company secretary in

practice, who is engaged in the formation of the company.

2.3 For commencement of business by a company having share capital, following needs to be

filed with the registrar of companies

Declaration by director in prescribed form providing that the subscribers have paid the

value of shares agreed to be taken by them

Paid up share capital is not less than 5 Lakhs for public company and 1 Lakh for private

company

Confirmation that the company has filed a verification of its registered office, with the

Registrar.

2.4 Company, which has raised money from public through prospectus and still has any unutilisedamount out of the money so raised, shall not change its objects for which money was raised

unless a special resolution is passed by the company and other requirements of

advertisement (in newspaper and website) and exit opportunity to dissenting shareholders is

complied with.

2.5 Articles can have entrenchment to the effect that specified provisions in Articles can be altered

only if restrictive conditions as specified are met.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 13/21

13

3. Securities

3.1 Issue of all types of securities covered and not just shares and debentures.

3.2 A public company can only issue securities by following the provisions related to public offer

or Private Placement or by way of bonus or right issue. A Private company may issuesecurities only through private placement by complying with the provisions.

3.3 A company shall not, at any time, vary the terms of a contract referred to in the prospectus or

objects for which the prospectus was issued, except subject to the approval of, or except

subject to an authority given by the company in general meeting by way of special resolution.

If terms are varied, the company shall not use any amount raised by it through prospectus for

buying, trading or otherwise dealing in equity shares of any other listed company and shall

also provide an exit opportunity to the dissenting shareholders.

3.4 Companies can now file Shelf Prospectus to be prescribed by SEBI.

3.5 Any person who makes or abets making of multiple applications to a company in

different names or in different combinations of his name or surname for acquiring or

subscribing for its securities shall be liable for action under the provisions of Bill.3.6 A company may, after passing a special resolution in its general meeting, issue depository

receipts in any foreign country subject to conditions, as may be prescribed.

3.7 Qualified Institutional buyers not covered under provisions of private placement.

3.8 The number of persons to which company may make an offer or invitation of securities to a

section of the public otherwise than through issue of a prospectus, by way

of private placement basis and maximum investment size in such case, shall be prescribed by

way of rules.

3.9 A company making an offer or invitation shall allot securities within 60 days from the date of

receipt of the application money for such securities.

4. Share Capital

4.1 Company cannot issue shares at discount other than as sweat equity.

4.2 Company may issue preference shares for a period exceeding 20 years for infrastructure

projects, subject to the redemption of such percentage of shares as may be prescribed on an

annual basis at the option of such preferential shareholders.

4.3 Apart from existing shareholders, if the company proposes to increase its subscribed capital

by the issue of further shares, such shares may also be offered to employees by way of ESOP

subject to special resolution passed by company.

4.4 Reduction of capital will not be allowed if the company is in arrears in the repayment of any

deposits accepted by it, either before or after the commencement of this Act, or the interestpayable thereon.

4.5 The buy-back is not prohibited, if the default in repayment of deposit or interest payable,

redemption of debentures or preference shares or payment of dividend to any shareholder or

repayment of any term loan or interest payable to any financial institution or bank is remedied

and a period of 3 years has lapsed after such default ceased to subsist.

4.6 A limited company having a share capital may, if so authorised by its articles, alter its

memorandum in its general meeting to consolidate and divide all or any of its share capital

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 14/21

14

into shares of a larger amount than its existing shares after obtaining approval of Tribunal.

Approval of the Tribunal shall be required for consolidation and division of share capital only if

the voting percentage of shareholders changes consequent on such consolidation.

5. Registration of charge

All types of charges are required to be registered in contrast to specified list which was

necessary to register the charge under Companies Act, 1956.

6. Annual Return

6.1 Every return requires substantial additional information such as particulars of holding,

subsidiary, associate companies, principle business activities, matters relating to certification

of compliances, disclosures, remuneration of directors, key management personnel, meeting

of members, board and various committees along with attendance details, etc.

6.2 The annual return, filed by a listed company or, by a company having such paid-up capital and

turnover as may be prescribed, shall be certified by a company secretary in practice.6.3 Every listed company shall file a return in the prescribed form with the Registrar with respect

to change in the number of shares held by promoters and top 10 shareholders of such

company, within 15 days of such change.

7. Matters related to Management and Administration

7.1 First Annual General Meeting of the Company shall be held within the period of 9

months from closure of its first financial year instead of 18 months from the date of the

Incorporation, as provided in the Companies Act 1956.

7.2 The provisions of Postal Ballot shall be applicable to all companies whether listed or unlisted,

on all such matters which shall be prescribed by Central Government.7.3 The resolution requiring special notice has to be moved by such number of members holding

not less than 1% of total voting power or holding shares on which an aggregate sum of not

less than 1 Lakh has been paid-up.

7.4 Every Company has to follow the Secretarial Standards.

7.5 Members may exercise the right to vote by electronic means.

7.6 Punishment has been provided for falsely inducing a person to enter into any agreement with

bank or financial institution with a view to obtain credit facilities.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 15/21

15

8. Dividend

8.1 The Board of Directors of a company may declare interim dividend during any financial year

out of the surplus in the Profit and Loss Account and out of profits of the financial year in

which such interim dividend is sought to be declared.8.2 If the company has incurred loss during the current financial year up to the end of the quarter

immediately preceding the date of declaration of interim dividend, interim dividend shall not be

declared at a rate higher than the average dividends declared by the company during the

immediately preceding 3 financial years.

8.3 There is no requirement to transfer fixed percentage of profits to reserves before declaring

dividend. Companies have been given discretion to transfer such amounts as they deem fit.

8.4 All shares in respect of which unpaid or unclaimed dividend has been transferred shall also be

transferred by the company in the name of Investor Education and Protection Fund.

9. Accounts

9.1 Consolidated financial statements of the Company and all subsidiaries are required to be laid

before annual general meeting. A separate statement containing the salient features of the

financial statement of its subsidiary is also required to be attached. For these purposes,

subsidiary shall include associate company and joint venture.

9.2 Requirement of attaching annual report of subsidiaries has been dispensed with.

9.3 Central Government may, by notification, constitute a National Financial Reporting Authority to

provide for matters relating to accounting and auditing standards.

9.4 Bill provides for re-opening of books of accounts or re-casting of financial statements if order

is made by Court or Tribunal to the effect that accounts were prepared in fraudulent manner,

affairs were mismanaged casting doubt on reliability of financial statements.

9.5 Director’s report shall have provide various types of additional information like number

of meetings of the Board, Company’s policy on directors’ appointment and

remuneration; explanations or comments by the Board on every qualification,

reservation or adverse remark or disclaimer made by the Company Secretary in his

secretarial audit report, auditor in audit report, particulars of loans, guarantees or

investments etc. For One Person Company the director report will contain explanations

or comments by the Board on every qualification, reservation or adverse remark or

disclaimer made by the auditor in his report.

9.6 Every company having net worth of rupees 500 crore or more, or turnover of rupees 1000

crore or more or a net profit of rupees 5 crore or more during any financial year shall

constitute a Corporate Social Responsibility (CSR) Committee of the Board consisting of 3 ormore directors, out of which at least 1 director shall be an independent director. The

committee shall recommend the policy for CSR to the Board.

9.7 The Board of every company shall ensure that the company spends in every financial

year, at least 2 per cent of the average net profits of the company made during the 3

immediately preceding financial years, in pursuance of its CSR Policy and in case of

failure to do, shall report the necessary reasons for not spending the same in their

Board’s report.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 16/21

16

9.8 Such class or classes of companies as may be prescribed shall be required to appoint

an internal auditor to conduct internal audit of functions or activities of the company.

The Central Government may, by rules, prescribe the manner and the intervals in which

the internal audit shall be conducted and reported to the Board.

10. Audit

10.1 The limit in respect of maximum number of companies in which a person may be appointed as

auditor has been proposed as 20 companies.

10.2 Every company shall, at the first annual general meeting, appoint an individual or a firm

as an auditor who shall hold office from the conclusion of that meeting till the

conclusion of its sixth annual general meeting and thereafter till the conclusion of

every sixth meeting. The appointment of auditors for 5 years shall be subject to

ratification by members at every Annual General Meeting.

10.3 In case of listed company & certain other class of companies, as may be prescribed, Bill

provides for provision for compulsory rotation of individual auditors in every 5 years and of

audit firm every 10 years. Individual auditors or audit firm shall not be eligible for re-appointment as auditor in the same company for 5 years from the completion of their term.

10.4 In case of audit firm, members may rotate the partner at such interval as may be resolved by

members.

10.5 As on the date of appointment audit firm having a common partner or partners to the

other audit firm, whose tenure has expired in a company immediately preceding the

financial year, shall not be appointed as auditor of the same company for a period of 5

years.

10.6 A transition period of 3 years has been prescribed to comply with the provision of the

rotation of auditor.

10.7 The Bill provides for certain new disqualifications for the Auditors like a person or a firm who,whether directly or indirectly, has business relationship with the company, or its subsidiary, or

its holding or associate company or subsidiary of such holding company or associate

company of such nature as may be prescribed, indebtedness to holding/subsidiary

companies, etc.

10.8 The Bill provides that Auditor shall comply with auditing standards.

10.9 If an auditor of a company, in the course of the performance of his duties as auditor, has

reason to believe that an offence involving fraud is being or has been committed against the

company by officers or employees of the company, he shall immediately report the matter to

the Central Government. These provisions also apply to Cost Accountant and Company

Secretary in practice.

10.10 Auditor of the company shall not provide directly or indirectly the specified serviceslike internal audit, management services, investment advisory, rendering of outsourced

financial services, etc. to the company, its holding company and subsidiary company.

10.11 Cost records to be mandated for companies engaged in production of such goods or

rendering of such services as may be prescribed.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 17/21

17

11. Appointment and Qualification of Directors

11.1 In prescribed class or classes of companies, there should be atleast 1 woman director.

11.2 Out of all the Directors, atleast 1 director shall be a person who has stayed in India fora total period of not less than 182 days in the previous calendar year.

11.3 Every listed public company shall have at least one-third of the total number of directors as

independent directors. Companies existing as on date of commencement of this Act have

been provided a transition period of 1 year for the compliance of this provision. Independent

Director shall be appointed for a term of 5 consecutive years and shall be eligible for further

term of 5 years. The independent director shall be eligible for appointment after the expiration

of 3 years of ceasing to become an independent director.

11.4 Nominee director nominated by any financial institution, or in pursuance of any agreement, or

appointed by any government to represent its shareholding shall not be deemed to be an

independent director.

11.5 Independent Directors are to be excluded for the purpose of computing ‘one third of retiringDirectors’.

11.6 Only an independent director can be appointed as alternate director to an independent

director.

11.7 Central Government will prescribe the number of independent directors in case of class or

classes of public company.

11.8 The Schedule to the Bill provides the following in respect of an Independent Director

Professional Conduct -

Role & Functions

Duties

Manner of Appointment

Removal & Resignation etc.

11.9 The maximum limit of directors in the Company has been increased to 15 with a power

to add more directors upon passing of Special Resolution.

11.10 The Bill provides for certain new disqualification for the Directors.

11.11 A person cannot become directors in more than 20 companies and out of this 20, he

cannot be director of more than 10 public companies

11.12 A transitional period of 1 year is provided to persons acting as director to comply with

the requirement of maximum number of directorship and they have to intimate their

choice to each of company where they wish to continue as director and also to the

Registrar.

11.13 The Bill prescribes the duties of the directors towards the company.11.14 Whole-time director included in the definition of the term 'key managerial personnel'

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 18/21

18

12. Board – Governance and Meetings

12.1 Every company belonging to such class or classes of companies as may be prescribed shallhave the whole-time key managerial personnel.

12.2 Unless the articles of a company provide otherwise, an individual shall not be the chairperson

of the company as well as the managing director or Chief Executive Officer of the company at

the same time.

12.3 Director can participate in the Board meeting through video conferencing or other audio visual

mode as may be prescribed.

12.2 A notice of not less than 7 days in writing is required to call a board meeting.

12.3 Atleast 4 meeting should be held each year. Not more than 120 days should elapse between

two consecutive meetings.

12.4 The Audit Committee shall consist of a minimum of 3 directors with independent directors

forming a majority. Majority of members of Audit Committee including its Chairperson shall bepersons with ability to read and understand, the financial statement.

12.5 The Board of Directors of every listed company and such other class or classes of companies,

as may be prescribed shall constitute the Nomination and Remuneration Committee

consisting of 3 or more non-executive directors out of which not less than one half shall be

independent directors.

12.6 Board of Directors of a company which consists of more than 1000 shareholders, debenture-

holders, deposit-holders and any other security holders at any time during a financial year

shall constitute a Stakeholders Relationship Committee consisting of a chairperson who shall

be a non-executive director and such other members as may be decided by the Board.

12.7 The meeting of the Board may be called at shorter notice to transact urgent business subjectto the condition that at least one independent director shall be present at the meeting. In case

of absence of independent directors from such a meeting of the Board, decisions taken at

such a meeting shall be circulated to all the directors and shall be final only on ratification by

at least one independent director.

12.8 Disclosure of interest by every director shall be made at the first meeting of the Board in which

he participates as a director and thereafter at the first meeting of the Board in every financial

year or whenever there is any change in the disclosures already made.

12.9 Provisions relating to granting of loans, guarantees, security in connection with loans have

been extended to other persons also. The rate of interest on inter-corporate loans will be

prevailing rate of interest on dated Government Securities.

12.10 A company, unless prescribed, shall not make investments through more than two layers ofinvestment companies. Exceptions are provided for foreign acquisitions and requirement of

multi-layered structure as per any law.

12.11 No approval of central government is required for entering into any related party transactions.

12.12 No approval of central government is required for appointment of any director or any other

person to any office or place of profit in the company or its subsidiary.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 19/21

19

12.13 Every contract or arrangement entered into with a related party shall be referred to in the

Board’s Report along with the justification for entering into such contract or arrangement.

12.14 A company shall not enter into any arrangement by which a director of the company or of its

holding/subsidiary/associate company or any person connected with him can acquire assets

for the consideration other than cash from the company & vice versa without the approval of

company in general meeting.12.15 The Bill provided provision related to prohibition on forward dealings in securities of company

by director and key managerial personnel.

12.16 The Bill now provides the provisions for prohibiting insider trading in the company.

13. Compromise, Arrangement and Amalgamations

13.1 Only persons holding atleast 10 per cent of the shareholding or having outstanding debt

amounting to not less than 5 per cent of the total outstanding debt as per the latest audited

financial statement, shall be eligible to raise any opposition to an arrangement or compromise.

13.2 The Tribunal may dispense with calling of a meeting of creditor or class of creditors where

such creditors or class of creditors, having at least 90 per cent. value, agree and confirm, byway of affidavit, to the scheme of compromise or arrangement.

13.3 Any provision of buyback in any compromise or arrangement shall be in compliance with the

provisions of the Buyback.

13.4 Any takeover offer of listed company under compromise or arrangement shall comply with

SEBI guidelines.

13.5 The Bill now provides that in case of merger of listed company in unlisted company, the

tribunal can order that unlisted company i.e. Transferee Company shall continue to be

unlisted.

13.6 No compromise or arrangement shall be sanctioned by the Tribunal unless a certificate by the

company’s auditor has been filed with the Tribunal to the effect that the accounting treatment,if any, proposed in the scheme of compromise or arrangement is in conformity with the

accounting standards prescribed under section 133.

13.7 Separate provisions have been provided for the merger or amalgamation between two small

companies or between a holding company and a wholly owned subsidiary company.

13.8 The Bill provides provision for cross border amalgamations between Indian Companies and

companies incorporated in the jurisdictions of such countries as may be notified from time to

time by the Central Government

13.9 The Bill provides specific provision for purchase of minority shares in case an acquirer or

person acting in concert with the acquirer becomes holder of 90% or more of the issued

capital of the company, either directly or by virtue of any amalgamation, share exchange,

conversion of securities or any other reason.

14. Other provisions

Apart from the above, the Bill also makes provisions for Appointment and remuneration of

managerial personnel, Inspection, Inquiry and Investigation, Prevention of Oppression and

Mismanagement, Registered Valuer, Revival and Rehabilitation of Sick Companies, National

Company Law Tribunal and Appellate Tribunal, Special Courts, etc.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 20/21

20

IV. Our Comments

In view of the changing economic and commercial environment, Companies Bill is a modern

legislation for growth and regulation of corporate sector in India in line with good governance

practices. Through this new legislation, the government intends to make India an attractive

and safe investment destination. It has wide implications across different sectors,

stakeholders with emphasis on accountability, business responsibility, social welfare and

better governance. This legislation extends the intent of the Business Responsibility Reporting

guidance for the top 100 listed companies by market capitalization on the NSE and the BSE

and Global Reporting Initiative for reporting and disclosure beyond financial performance

indicators – environmental and social behavior compliances. The tone of the legislation is

forward looking and will facilitate responsible growth.

7/28/2019 Analysis of Companies Bill 2011

http://slidepdf.com/reader/full/analysis-of-companies-bill-2011 21/21

21

Disclaimer: The contents of this material are for information purposes only and should not be construed as solicitationor advice in any manner whatsoever. No one should act upon the information provided in this material withoutappropriate professional advice. While Verita Management Advisors Pvt. Ltd. (“Verita”) strives to ensure that theinformation contained herein is accurate, timely and reliable, Verita makes no warranties or representations, expressor implied, including the warranty of merchantability and fitness for a particular purpose, or assumes any liability or

responsibility for the accuracy, completeness, reliability, timeliness or usefulness of the information provided in thismaterial.

This information is not intended to create, and receipt of it does not constitute, an advisor-client relationship. Youacknowledge and agree that all proprietary rights in the material shall remain the property of Verita. The modification,reproduction, redistribution, disclosure, display and transmission of any information contained herein or derivingcommercial use or benefit from the material is strictly prohibited. Verita shall accept no liability for any damages,claims or losses of any nature, arising indirectly or directly, from the use of the data or material or otherwisehowsoever arising.

Learn more about Verita : www.verita.co.inRequest for Information : [email protected]

VERITA MANAGEMENT ADVISORS PVT. LTD Powering transformational insights India Office 441, Kiran Kunj, S.V. Road, Malad (W), Mumbai 400 064 T: +91 22 2864 5500 | F: +91 22 2864 5400

UAE Liaison Office P.O. Box 128235, M-04, Bil Badi Building, Madinet Zayed, Abu Dhabi, United Arab Emirates Oman Liaison Office P.O. Box 385, Jibroo, P.C. 114, Sultanate of Oman

For any query on the above analysis contact:

huzeifa.unwala@ verita.co.in or janhavi.pandit@ verita.co.in

![Companies Bill 2013 [Carocks.wordpress.com]](https://img.pdfslide.us/doc/110x75/577cd9bc1a28ab9e78a40e55/companies-bill-2013-carockswordpresscom.jpg)