Embed Size (px)

Citation preview

Analysing Competitiveness Performance in the Wine

Industry: The South African case

Johan van Rooyen, Lindie Stroebel, Dirk Esterhuizen

Johan van Rooyen is a professor in Agricultural Economics at the University of Stellenbosch, Stellenbosch, South Africa Lindie Stroebel is the manager of Economic intelligence at the Agricultural Business Chamber and a PhD candidate at the University of the Free State, Pretoria, South Africa Dirk Esterhuizen is an agricultural specialist at the United States Department of Agriculture, Foreign Agricultural Services, and Pretoria, South Africa.

January 2010

Paper for the pre-AARES conference workshop on The World’s Wine Markets by 2030: Terroir, Climate Change, R&D and Globalization, Adelaide Convention Centre, Adelaide, South Australia, 7-9 February 2010.

ANALYSING COMPETITIVENESS PERFORMANCE IN THE WINE INDUSTRY: THE SOUTH AFRICAN CASE

Johan van Rooyen1, Lindie Stroebel2, Dirk Esterhuizen3

ABSTRACT Competitiveness is defined as the ability to sustain trade in the local and global environment. The RELATIVE TRADE ADVANTAGE (RTA) formula is firstly used to measure competitive performance in the South African wine industry since 1960. The PORTER MODEL is then applied to analyse 2005 & 2008 views and opinions of South African wine executives on factors enhancing and constraining competitiveness. Strategic approaches to sustain competitiveness, based on these trends are identified. KEYWORDS SOUTH AFRICAN WINE INDUSTRY COMPETITIVENESS ANALYSIS WINE EXECUTIVE SURVEY 2005-2008 PORTER ANALYSIS: 2005-2008 WINE BUSINESS CONFIDENCE STRATEGIES TO SUSTAIN COMPETITIVENESS 1. INTRODUCTION The paper explores trade competitiveness and competitive performance in the South African wine industry. First, a definition of competitiveness is proposed. This is followed by a short background to the South Africa wine industry. The measurement and analysis of competitiveness and business confidence in the wine industry is then discussed. Finally, strategies and mechanisms to create and sustain competitiveness in the South African wine industry are proposed. (Wine) industries and firms are competitive when they are able to continue to trade globally, at qualities and prices that are as good as or better than their competitors; and they are able to attract sufficient sources of capital, land, labour, technology and management from other competing economic activities. Short-term efforts such as opportunistic ‘price wars and cost cutting’ seldom sustain a competitive position. Long-term or sustained performances are therefore relevant in defining and analysing competitiveness as quoted above (Boehlje, 1996; Cho & Moon, 2002). In short, to be 1 Johan van Rooyen is a professor in Agricultural Economics at the University of Stellenbosch, Stellenbosch, South Africa 2 Lindie Stroebel is the manager of Economic intelligence at the Agricultural Business Chamber and a PhD candidate at the University of the Free State, Pretoria, South Africa 3 Dirk Esterhuizen is an agricultural specialist at the United States Department of Agriculture, Foreign Agricultural Services, and Pretoria, South Africa. The inputs of MS Yvette vd Merwe, South African Wine Industry Information Systems are acknowledged with appreciation.

2

competitive in today’s world is to continue to be in a position to trade successfully (Esterhuizen & Van Rooyen, 2008). An analytical framework, developed by the authors to measure competitiveness performance and to analyse the major constraints and enhancements, and to consider the business confidence levels prevailing in the industry are applied in this article (Esterhuizen, 2006; Van Rooyen and Esterhuizen,2007; and also based on the method used by the World Competitive Report, IMD). 2. THE SOUTH AFRICAN WINE INDUSTRY AT A GLANCE The wine industry contributed an estimated R20 billion (around US$ 1.6 billion) to South Africa’s gross domestic product (GDP) in 2009. This figure rises to R23.5 billion when tourism is included. An amount of R4.2 billion per annum (2008) is contributed to government revenue via excise taxes. Producers’ income amounts to R3.32 billion in 2008. The industry sustains about 275 000 job opportunities (including 20% through wine tourism), although some of this is seasonal in nature. Investment capital is in excess of R50 billion (US$5 billion). In 2008, some 3,839 producers and 83304

cellars in South Africa – mostly in the Western Cape province, with some in the Northern Cape and Free State – produced 1,089 million litres of wine, brandy and grape juice concentrate from a harvest of 1,4 million tonnes of grapes, making South Africa the world’s 7th largest wine producer. About 63 million litres of drinking wine were produced from this harvest, of which 38% was red and 62% was white wine, compared to a yield of 12% red wine as late as 1995.

The wine industry entered the global marketplace as major shifts were underway in production and consumption. While global wine production has declined over the past two decades, the share of wine production that is traded internationally has more than doubled. This trend has opened up new opportunities for South African wine exports, provided that they are able to demonstrate a competitive edge in the world market. South Africa produces 3.7% of the world’s wines and exports 54% of its wine production (411.8 million litres in 2008) to the value of R6.27 billion (US$385 million) per annum. The UK (27%), Germany (17%) and the Netherlands (7%) are currently the major export destinations for South African wines. Per capita consumption of wine in South Africa is 7.5 litres in comparison with 53.9 litres in France, 22.4 litres in Australia, 28.1 litres in Argentina and 8.5 litres in the USA. A summary of the most important statistics of the South African wine industry is shown below: 124,993ha cultivated (2008) 3,839 (2008) wine grape farmers 870 cellars (2009) 349 million vines of the vinifera varieties 1.4 million tonnes annual harvest (2008)

4 Indications are that more than 170 new cellars were established since 2006.

3

1.089 billion litres (2008) 70% used for the production of wine 1.7% of the world’s vineyards 7th largest producer of wine in the world (2006) 54% of South African wine is exported 411.8 million litres exported in 2008 3. RESULTS AND ANALYSIS 3.1 MEASURING COMPETITIVENESS PERFORMANCE Competitiveness based on trade performance, is measured by the application of the Relative Trade Advantage (RTA) formula (Balassa, 1989, and applications by Volrath, 1991, ISMEA, 1999, Esterhuizen, 2006 and Esterhuizen and Van Rooyen, 1999, 2001, 2004, 2006). In this quantitative method, it is argued that competitive advantage could be indicated by the trade performance of individual commodities, value chains and countries in the sense that the commodity trade pattern reflects relative market costs as well as differences in non-price competitive factors, such as subsidies, government policies and other public support measures. The Relative Trade Advantage method allows for the measurement of competitiveness under real world trade situations to include the realities of “uneven economic playing fields”, distorted economies and different trade regimes and are therefore most suited for measuring business based competitiveness status of an industry and firm. This method supports the above definition on competitiveness. To measure how competitive the wine industry in South Africa is, it is necessary to determine how successful the industry traded its products over time in the local and global environment relative to other competitors. This approach considers trade performance, i.e. the ‘ability to continue to trade in a competitive global environment’ and is based on the ratio of trade in wine (by country A/firm A) vs the global trade in wine, relative to the ratio of trade (by country A/firm A). Data is drawn from FAOSTAT. The long-term competitiveness index and the trends in competitiveness for the wine industry in South Africa as measured by Relative Revealed Trade Advantage (RTA) are shown in Table 1. In Figure 1 the trend is illustrated. From this it is clear that South Africa’s wines are increasingly internationally competitive with a sustainable and positive trend since 1990, with a high point in 2005. Recently some decline is being recorded to levels just above 2002. Table 1: The competitiveness index of the wine industry in South Africa (2000 – 2008) based on the Relative Revealed Trade Advantage (RTA)

Product RTA 2008

RTA 2007

RTA 2006

RTA 2005

RTA 2004

RTA 2003

RTA 2002

RTA 2001

RTA 2000

Wine 4.55 4.42 4.74 5.84 5.36 4.96 4.31 3.76 4.05 Source: Own calculation based on data from FAOSTAT.

4

Notes: Competitive (RTA > 1), marginal competitive (1 > RTA > -1), not competitive (RTA < -1); ‘+’ Positive trend; ‘-‘negative trend.

(1.00)

-

1.00

2.00

3.00

4.00

5.00

6.00

7.00

19611963

19651967

19691971

19731975

19771979

19811983

19851987

19891991

19931995

19971999

20012003

20052007

Phase 1Phase 2

Phase 3

Phase 4

Phase 5

Phase 6

Figure 1: The competitiveness of the wine industry in South Africa (1960 – 2008) The impacts of the regulation period and political sanctions (from early 1990s) when political liberation and access to global markets was achieved, are dramatically captured in the countries competitive performance, as well as recent events related to changing consumer preferences and style changes, trade policies, exchange rate fluctuations and technological innovation and constraints in these. A number of phases in competitiveness in the South African wine industry since 1960 are identified and described i.e. a short recent history of the South African wine industry is given (Van Rooyen, 2007 and in interviews with prominent wine analysts, and industry seminars): Phase 1 - Regulated competitiveness - 1970): During this period ( effectively starting in the late 1930s), the South African wine industry was heavily regulated through varietal choices and vine material, wine and wine grape production quotas, surplus removal schemes and price agreements. The KWV (Koperatiewe Wijnboere Vereniging), established in 1918, was granted statutory powers to regulate supply in the industry. This

5

period was characterised by a focus on high volume production of relative lower quality wines and an overall orientation towards brandy and fortified wine production (Ponte & Evert, 2007). Phase 2 – Constrained economic and political environment (1970-1990): Increasing political pressures by the international environment during the 1970s and the imposing of “ante-apartheid” sanctions brought the industry almost to a halt. Economic survival was possible through occasional exports of large volumes of low quality wine to Eastern Europe and domestic consumption (Vink, et al, 2004). One important innovation during this period was the introduction of the “Wine of Origin” scheme which brought local wine industry regulations in line with those in European countries. Cultivar based and classic wines became more popular. Wine tourism and ‘wine routes’ was also introduced. Phase 3 – ‘Madiba Magic’ (1990-1995): With the release of Nelson (Madiba) Mandela in 1990, the wine industry started with a remarkable period of activity and transformation. Economic sanctions were lifted, leading to international business exposure, access to international supply chains and increased investments. By 1997 the industry was fully deregulated and operated in a free market environment. The ‘Wine of Origin’ scheme was maintained and the environmentally ‘Integrated production of Wine’ (IPW) programme was widely implemented. International sales of South African wines increased from 20 million litres in 1992 to over 110 million litres (20% of the wine crop). Phase 4 – Facing competitive realities (1996-2000): Despite increased sales (at relative low prices) certain cracks started to appear in the South African wine success story. Renowned wine writers/wine judges called for changes in style and quality and led South Africa to produce internationally accepted wines – fruity, non-grassy, less tannins, great consistency, more quality reds (Le Roux, 2007). Australia also became a much more aggressive player in the UK, South Africa’s most important market. All this resulted in a range of innovations including the planting of improved grape varieties and virus-free plant material; the terroir system was extended, together with cultivar specific site solutions and the planting of more red varieties. Supply chain reliability also became a major success factor. By the end of the 1990s, the South African wine industry again responded positively, producing wines in the ‘new world’ style, but with a distinctly South African character (SAWB, 2002). Exports rose from 110 million litres in 1997 to 141 million litres in 2000 (26% of the wine crop). Phase 5 – Towards becoming a global player (2000 - 2005): The industry mobilised and jointly decided on a strategic ‘course for excellence’ through the acceptance of ‘Vision 2020’, the institution of the SA Wine Industry Council and the setting of a framework for a partnership with government through the ‘Wine Industry Strategy Plan’ (WIP) in 2003. This phase records a sustained increase in exports, in particular to the UK, Netherlands and Germany. Brand development and promotion became noted business strategies, with a particular effort by the wine industry to establish unique ‘Brand SA’ properties for South African wines, emphasising the great diversity and value for money of the wine. ‘Variety is our nature’ with an increasing environmental focus and social responsibility (the Wine Transformation Charter, 2006). Concepts such as integrity, authenticity and sustainability became key pointers in the industry (see the SA Wine Industry Directory, 2003-2008) as

6

well as the notion of unique and typical South African wines (Pinotage-red; Chenin Blanc-white). The impact of world market movements (e.g. Australia, 2007) fluctuating exchange rates and the presentation of unique lifestyle experiences (wine + food + tourism + value for money) became integrated in wine business strategies. Efforts to expand the local market are also in progress. Since 2000, exports again increased to 271 million litres in 2005. Towards a next phase? Phase 6 – Operating in a constrained competitive environment (2006 to current): Since the 2005 high point, the wine industry in South Africa is in a declining phase in terms of competitiveness status i.e. relative to its competitors. This negative trend in competitiveness started around 2005 after the definite positive trend in competitiveness which started in 2000. The main reasons for this decline in competitiveness can be found in the broader wine industry environment in which businesses now operates. This constrained environment include factors like the increase in the value of the Rand, global warming/drought conditions and climatically fluctuations, increases in interest rates, high crime and corruption levels, lack of infrastructure maintenance and export facilities, lack of skilled labour and government’s inability to provide sufficient regulatory and support services to the needs of the dynamic wine industry in South Africa – export sectors in general. This downward trend in competitiveness is also in line with the findings of the WEF in their Global Competitiveness Report and with the findings of the IMD in their World Competitiveness Yearbook on South Africa. In the WEF's Global Competitiveness Index, South Africa dropped from 36th position in 2006/07 to 44th position in 2007/08 and is currently (2008/09) in the 45th position. The IMD's World Competitiveness Yearbook for 2007 showed a 12-place drop in South Africa's ranking, from 38th to 50th out of 55 countries. In 2008 South Africa drop another three places to 53, however, in 2009 South Africa gain 5 places and is now 48th out of 57 countries. In explaining South Africa’s drop in global competitiveness rankings, the five most problematic factors for doing business in South Africa were indentified to be: crime and theft, inefficient government bureaucracy, inadequately educated workforce, restrictive labour regulations and inadequate supply of infrastructure. From this it can very well be concluded that the South African wine industry is now operating in a declining phase (phase 6?), as it may have utilised most of its current capacity to reach the previous high point, in 2005 and that restructuring to gain the edge again, will require a more conducive macro environment and general support infrastructure and growth-oriented government policy and support to facilitate sustained competitiveness. The international position: Wine trading (both at import and export levels) is one of the most dynamic and competitive activities in the agro-food environment. Since the late 1980s, the share of wine production that is traded internationally has nearly doubled and wine trade has brought major gains to participants in expanding countries, but pain to many traditional producers (Anderson, 2004). A view of South African competitive performance measured by the RTA, in comparison with some other major wine trading economics is instructive. In Figure 2 the general upward and relative “middle” position of South African is shown. The recent

7

decline relative to other competitors is also shown. Countries with increasing performances are Argentina, New Zeeland and the highly competitive Chile, after their considerable decline from 2000 to 2005

Australia

Chile

(5.00)

-

5.00

10.00

15.00

20.00

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007

Argentina Australia Chile France Italy New Zealand Portugal Spain United States of America South Africa

France

New ZealandPortugal

ItalySpain

South Africa

Argentina

Figure 2: Trends in the competitiveness of selected wine producing countries (1990-2007) 3.2 DETERMINANTS AND FACTORS OF COMPETITIVENESS IN THE SA WINE INDUSTRY Determinants of competitiveness were identified by using survey date on the views of South African wine executives on competitiveness, analysed by using the Porter framework (1990, 1998). The aim is to determine the key success factors that established a competitive advantage and the constraints that impacted negatively on the competitiveness of the wine industry. Porter’s (1990, 1998) theory of competitive advantage is an effort to identify the many factors that influence competitiveness and to show how they relate to each other and to the economic performance of a country’s industries in a global economy. While the traditional and new trade theories provide the important explanation of the locality production and trade patterns, as well as their effects on economic welfare, the work of Porter aims at understanding the process of change and why particular sectors in particular countries have been more successful than others i.e. more competitive.

8

3.2.1 THE WINE EXECUTIVE SURVEY: The focus of this analysis will be at the firm level i.e. individual firms will be requested to participate in the data gathering process through questionnaires. Executive opinions will thus be gathered as this group take the responsibility for the success and failure of strategy and operational action. Whereas the hard data in the previous section is used to measure competitiveness status over a specific period, the survey data measure competitiveness as it is perceived. The survey responses will reflect perceptions of competitiveness and indications for the future by business executives who are dealing with local and global business situations. The WineExecutiveSurvey (WES) will offer many unique measures and will capture the informed judgments of business leaders and decision-makers in the wine industry of South Africa on issues that influence their industry’s competitiveness. In Table 2 and Figure 3 below, all the factors affecting the competitiveness in the wine industry in South Africa in 2008 are indicated. These items were identified and rated through responses from 46 executives in the wine industry [the Agricultural Business Chamber’s Wine Executive Survey (WES, 2008)] to have an enhancing (rating of 7), constraining (1) or a neutral (4) impact on competitiveness. The top 10 most enhancing and constraining factors for 2008, are listed in the table 2 below. The top most constraining factors for the industry were identified to be the confidence and trust in politicians, electricity suppliers, the cost of crime and the competence of personnel in the public sector. The top most enhancing factors for the industry were identified to be the competition in the local market, international competition, the affordability of high quality products and the entry of new competitors. Table 2: The top ten most constraining and enhancing determining factors for the South African wine industry’s competitiveness, 2008. Top 10 most constraining factor Top 10 most enhancing factors Factor Rate Factor Rate 1 Trust/confidence in politicians 1.50 Competition in the local market 6.33 2

Electricity suppliers 1.67 International entry into the local

market 6.15 3 Cost of Crime 1.70 Affordable high quality products 6.15 4 Competence of personnel in the

public sector 1.91

Entry of new competitors 6.09 5 Quality of Unskilled Labour 2.46 Unique services & processes 5.43 6 Labour policy 2.46 Environmental awareness 5.35 7 Cost of Transport 2.48 Invest in staff 5.35 8 Administrative regulations in South

Africa 2.50 Efficiency of technology in production

processes 5.30 9 Cost of financing 2.59 Regulatory standards 5.28 10 Land reform policy 2.70 Availability of Unskilled labour 5.24 Source: Agricultural Business Chamber: Wine Executive Survey 2008

9

Figure 3: Factors of competitiveness for the South African wine industry Source: Agricultural Business Chamber: Wine Executive Survey 2008

10

3.2.2. THE PORTER ANALYSIS According to Porter (1998) four broad sets of competitiveness attributes or determinants must be considered. These are: Factor conditions

: Factors of production, natural resources, level of production costs such as the price of labour, capital, land, water, fuel, pesticides, machinery, the supply chain, knowledge and infrastructure and all transaction costs, necessary to compete in a given industry;

Market conditions

: The nature of demand for a product and service and the ability to capture this demand through marketing and sales, for example, demand composition, demand size and information on trends in demand;

Related and supporting industries

: The presence or absence of supplier industries and related industries that are internationally competitive;

Firm strategy, structure, and rivalry

: The conditions and environment governing how firms are created, organised and managed, and the nature of domestic rivalry;

In addition, government

plays a vital role in orchestrating these determinants - influencing each either positively or negatively, through its policy-making and operational inputs. Indeed, government policy and programmes, as a determinant of an environment which is intended to enhance competitiveness must be viewed apart from the previous four determinants.

Finally there is the role of chance

. Chance/uncertain events are occurrences largely beyond the power of firms (and often the national government) to influence. Events such as wars, diseases, political decisions by foreign governments, large increases in demand, shifts in world financial markets and exchange rates, discontinuity of technology can be described as chance events and would be exploited opportunistically in a competitive manner by highly competitive industries.

In Table 3 the rating of determining factors for 2008, according to the Porter- framework is shown.

11

Table 3: The rating of determinants of competitiveness in the South African wine industry, 2008. (i) Production factor conditions 3.67 (ii) Related & supporting industries 3,91 Quality of Unskilled Labour 2.46 Electricity suppliers 1.67

Cost of Transport 2.48 Collaboration with scientific research institutions in

R&D 3.50 Cost of financing 2.59 Telecommunication firms 3.50 Availability of Skilled Labour 2.87 Suppliers of packaging material 3.63 Overall cost of doing business 2.93 Financial institutions 3.89 Labour administration cost 3.07 Transport companies 3.89 Cost of quality technology 3.11 Internet service providers 4.24 Quality of skilled labour 3.15 Specialised information technology services 4.28 Cost of skilled labour 3.59 Sustainability of local suppliers 4.30 Cost of using infrastructure 3.67 Status of scientific research institutions 4.37 Cost of Unskilled Labour 3.70 Quality of local suppliers 4.52 Efficiency of general infrastructure 4.11 Credit availability 4.63 Availability of quality technology 4.80 Quality of technology 5.00 Availability of water for industrial purposes 5.07 Availability of Unskilled labour 5.24 (iii) Firm strategy, structure & rivalry 5,20 (iv) Government support & policies 3,30 Expenditure on R&D 3.78 Confidence/trust in politicians 1.50 Incentives for management 4.04 Competence of personnel in the public sector 1.91 Flow of information from the customers 4.20 Labour policy 2.46 Information flow from primary suppliers to your company 4.57

Administrative regulations in South Africa 2.50

Substitutes of your company’s product or services 4.78 Land reform policy 2.70 Continuous innovation 5.20 BEE policy 2.87 Regulatory standards 5.28 The tax system 3.04 Efficiency of technology in production processes 5.30 Political changes’ influence 3.91 Environmental awareness 5.35 Environmental regulations 4.09 Invest in staff 5.35 Trade policy 4.09 Unique services & processes 5.43 Macro-economic policy 4.26 Entry of new competitors 6.09 Competition law 4.33 International entry of the local market 6.15 Complying with environmental standards 5.20 Affordable high quality products 6.15 Competition in the local market 6.33 (v) Demand conditions 3,98 (vi) Chance factors 2,92 Growth in local market 3.30 Cost of Crime 1.70 Local market size 3.54 Cost of HIV/Aids 3.11 Local customers demand environmental friendly products 3.89

Exchange rate 3.33

Internationalisation of local buyers 3.96 Global political developments 3.57 Speed of adoption of new products by local buyers 4.24 Local buyers concern of ethics 4.33 Sophistication of local buyers 4.57

Source: Agricultural Business Chamber: Wine Executive Survey 2008

12

Comparing 2005 with 2008 (refer to Notes in Figure 4 below): In both 2005 and 2008 WES’s, the executives in the wine industry indicated that the chance related determinants and the government support and policies were the most constraining factors to their competitiveness. However, in 2008, these two factors were rated higher. Executives rated the production factor conditions, supporting industries and demand/market conditions to have a fairly neutral impact on their competitiveness. However in 2008, these three factors, especially the production factor conditions were rated lower- more constraining- than in 2005. The only factors rated by executives to have had an continued enhancing impact on the competitiveness of the South African wine industry is firm strategy, structure and local rivalry. It was however rated slightly higher in 2008, than in 2005. This supports the view taken in section 3.1 to explain the phase 6 situation above. Figure 4 below indicates the status, as viewed by industry executives, of the major determinants of competitiveness in the South African wine industry in 2005 and 2008, respectively.

Figure 4: The status of the determinants of competitiveness in the South African wine industry- 2005-2008. Source: Agricultural Business Chamber: Wine Executive Survey 2005, 2008 Note 1: 2005 scale: 1 = Constraint 2 = Moderate 3 = Enhancement Note 2: 2008 scale: 1 = Constraint 4 = Moderate 7 = Enhancement Note 3: work in progress to align 2005 &2008 scales.

(i) Production factor conditions: The average score in 2008 achieved for production factor conditions is 3,67 which means that on average the factor conditions in South Africa have a moderate, to slightly constraining effect on the wine industry’s competitiveness.

13

In 2005 the factor conditions were also rated as moderate, with quality of skilled labour, the high cost of capital and the high cost of doing business in South Africa most constraining. In 2008, the most constraining factors were rated to be quality of unskilled labour, cost of transport and financing, availability of skilled labour and overall cost of doing business. The factors that have an enhancing impact on the competitiveness of the wine industry in South Africa in both 2005 and 2008 are the availability/cost of unskilled labour and the cost, quality and availability of technology in South Africa. In 2005 the location of the wine industry in South Africa in terms of the international market were considered to have the most enhancing effect, and in 2008 the availability of water for industrial purposes were considered to have the most enhancing impact. (ii) Related and supporting industries: The related and supporting industries, as a determinant of competitiveness in 2008, were rated 3,91, which states that the related and supporting industries also have moderate to slightly constraining impact on the South African wine industry in 2008. In 2005 this factor were rated to have contributed positively and have a positive impact on the industry’s competitiveness. The ongoing electricity crisis, experienced since 2008, constrained the industry largely and the electricity supplies were rated to have the most constraining impact since 2005. The only enhancing factor in 2008, even though rather unconvincingly so, is the quality of local suppliers. This however is also rated less than in 2005. All other factors had a moderate impact only in 2008. (iii) Firm strategy, structure and rivalry: The third broad determinant of competitive advantage in an industry is the context in which firms are created, organized and managed as well as the nature of rivalry. With an average score of 5,20 for 2008, firm strategy, structure and rivalry as a whole, have a strong enhancing impact on competitiveness of wine businesses in South Africa. The only constraining factor, even though only slight constraining is the expenditure on research and development. This determinant were also rated as enhancing in 2005, with the strong enhancing factors the regulatory structures and standards in the industry, integrity systems, intense internal competition, entry of new competitors on a regular basis, the production of affordable high quality products, firm level investment in human resources, employment of quality technology, the production of unique products, services and processes, the production of environmental friendly products, and continuous technical innovation. In 2008, the most enhancing factors were the ease of entry of new competitors, international entry into the local market, affordability of high quality products and the fierce competition in the local market.

14

(iv) Government support and policies: The wine industry in South Africa is highly regulated and legalised and to a large degree dependent on sound partnership arrangements with government. Government policy and support on matters related to export and trading, science and innovation, empowerment and transformation, tax and excise duties, natural resources such as land and water, labour relations, financial arrangements to name some, impacts directly on this sensitive and highly market orientated industry. With an average score of 3,30 in 2008, government services, policies and support systems are viewed to act in a constraining manner to the competitive success of the wine industry in South Africa. Similar findings were made in the Agricultural Business Chamber’s Wine Executive Survey in 2005. In 2005, the major constraining factors were: burdensome administrative regulations, the impact of legal change, the competence of personnel in the public sector, South Africa’s tax system’s impact on investment and risk-taking, South Africa’s resources policy (labour and land) and clarity on BEE transformation policy and the scorecard system. In 2008, the trust in the honesty of politicians, competence of personnel in the public sector, the current impact of the labour policies, administrative regulation in South Africa, the land reform process and unclear BEE policy and the tax system were considered the most constraining factors. It is interesting to note that the South Africa’s environmental regulations were rated by the wine industry in South Africa in 2005 to have a positive impact on their competitiveness, while macro-economic policy, the current political climate and trade policy are providing moderate enhancements. In 2008, again the compliance with environment standards is considered to enhance their competitiveness. The trade-, and macro-economic policies and competition were once again considered to have a moderate impact, with BEE policy less concerning, inter alia due to the effort of the industry to draft a Wine Transformation Charter and Score Card to manage BEE initiatives. Government however have not formally sanctioned this charter yet (v) Demand conditions: In 2008, the demand conditions had a rating of 3,98, which indicate that the demand conditions has a moderate to slightly constraining effect on the South African wine industry’s competitiveness. The Agricultural Business Chamber’s Wine Executive Survey (WES) in both 2005 and 2008 indicated that the growth in the local market size is constraining the competitiveness of the wine industry in South Africa. The issue of buyers of South African wine being knowledgeable, demanding and buying environmentally friendly products and buyers being concerned over ethics and the integrity of production methods were perceived to have a moderate impact on the South African wine industry’s competitiveness.

15

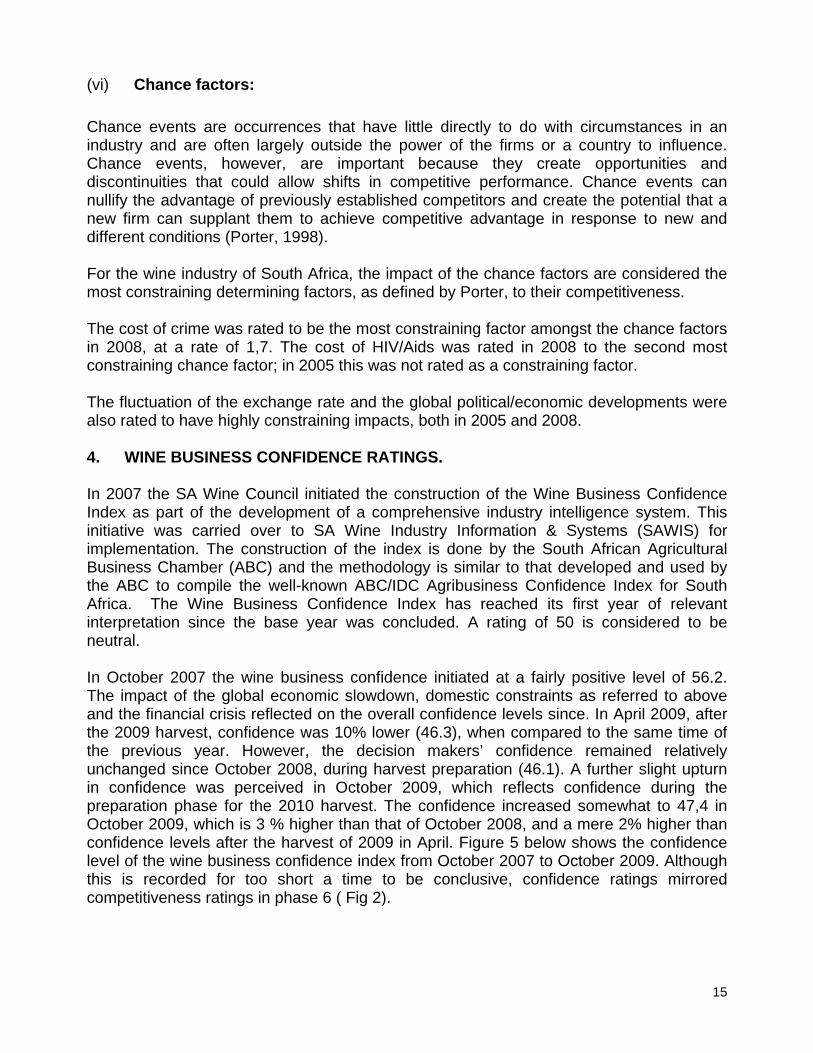

(vi) Chance factors: Chance events are occurrences that have little directly to do with circumstances in an industry and are often largely outside the power of the firms or a country to influence. Chance events, however, are important because they create opportunities and discontinuities that could allow shifts in competitive performance. Chance events can nullify the advantage of previously established competitors and create the potential that a new firm can supplant them to achieve competitive advantage in response to new and different conditions (Porter, 1998). For the wine industry of South Africa, the impact of the chance factors are considered the most constraining determining factors, as defined by Porter, to their competitiveness. The cost of crime was rated to be the most constraining factor amongst the chance factors in 2008, at a rate of 1,7. The cost of HIV/Aids was rated in 2008 to the second most constraining chance factor; in 2005 this was not rated as a constraining factor. The fluctuation of the exchange rate and the global political/economic developments were also rated to have highly constraining impacts, both in 2005 and 2008. 4. WINE BUSINESS CONFIDENCE RATINGS. In 2007 the SA Wine Council initiated the construction of the Wine Business Confidence Index as part of the development of a comprehensive industry intelligence system. This initiative was carried over to SA Wine Industry Information & Systems (SAWIS) for implementation. The construction of the index is done by the South African Agricultural Business Chamber (ABC) and the methodology is similar to that developed and used by the ABC to compile the well-known ABC/IDC Agribusiness Confidence Index for South Africa. The Wine Business Confidence Index has reached its first year of relevant interpretation since the base year was concluded. A rating of 50 is considered to be neutral. In October 2007 the wine business confidence initiated at a fairly positive level of 56.2. The impact of the global economic slowdown, domestic constraints as referred to above and the financial crisis reflected on the overall confidence levels since. In April 2009, after the 2009 harvest, confidence was 10% lower (46.3), when compared to the same time of the previous year. However, the decision makers’ confidence remained relatively unchanged since October 2008, during harvest preparation (46.1). A further slight upturn in confidence was perceived in October 2009, which reflects confidence during the preparation phase for the 2010 harvest. The confidence increased somewhat to 47,4 in October 2009, which is 3 % higher than that of October 2008, and a mere 2% higher than confidence levels after the harvest of 2009 in April. Figure 5 below shows the confidence level of the wine business confidence index from October 2007 to October 2009. Although this is recorded for too short a time to be conclusive, confidence ratings mirrored competitiveness ratings in phase 6 ( Fig 2).

16

Figure 5: Wine Business Confidence Index for the South African wine industry from October 2007 to October 2009 Source: Agricultural Business Chamber (ABC) & SA Wine Industry Information & Systems (SAWIS) The confidence index is constructed by measuring 10 sub-indices. When comparing the year-on-year change, which specifically refers to the change in confidence between October 2008 and October 2009, which is the harvest preparation period in the wine industry of South Africa, the economic growth was the biggest contributor to the slight upturn in confidence. The decrease in financing costs also contributed largely. It is relevant to compare the confidence in the post harvest period (April 2009) to the preparation phase for the following harvest, which was in October 2009. Again the expectations of moderate economic growth in the country boosted the general purchasing power of consumers, lifted business and investment confidence in the broader economy and promoted business growth accordingly. The decrease in financing costs, especially during the harvest preparation phase, brought much relieve for the industry in the shorter run. Interestingly the confidence regarding employment also increased in the short run. On the down side, capital investment decrease when compared to the same period of the previous year. This could indicate that, in this slight upturn after the economic/financial crisis, existing assets are being utilised, possibly with slightly more employees, before further capital investments could be incurred in future. Due to the stronger exchange rate and lower international demand, foreign earnings decreased as the volume exported decreased. Wine executives found their market share

17

to decrease, both when compared to the previous year and the post harvest period in April. Unfavourable weather conditions had a negative impact on confidence in the harvest preparation phase in October 2009. Table 4 below indicates the changes in the overall wine business confidence index as well as that of the sub-indices used to compile the overall index. Table 4: Changes in the overall wine business confidence index and its sub-indices for the South African wine industry Year-on-year change Change between Post- and Pre-harvest Turnover -6% Small decrease 1% Unchanged Net operating income 3% Small increase 1% Unchanged Employment 19% Increase 21% Increase Capital investment -23% Decrease -15% Small decrease Economic growth in SA 189% Huge increase 89% Large increase Volume exports -38% Decrease -8% Small decrease Agricultural conditions 14% Increase -42% Decrease Market share of the business -49% Decrease -45% Decrease Debtor provision for bad debt -12% Decrease -11% Decrease Financing costs -37% Decrease -25% Decrease Overall Index 3% Small increase 2% Small increase Source: Agricultural Business Chamber (ABC) & SA Wine Industry Information & Systems (SAWIS) Regional differences: There have been significant differences between the confidence levels in different wine producing areas in South Africa since October 2007. Most regions showed a gradual; decrease in confidence over this period, with the exception of the Orange River, Worcester and Breedekloof regions. The Orange River and the Klein Karoo region’s decision makers were the least confident during this period. The Malmesbury region was very confident in the base year, but dropped significantly over the past year. The Worcester region was the most confident in October 2009, followed by the Orange River and Olifants River regions. The Stellenbosch region showed a steady and consistent decrease in confidence over the two year period of measurement. The Paarl region also showed a consistent decrease, but had a slight upturn in October 2009. The changes for the different region, since October 2007, can be seen in the graph below

(Fig.6).

18

Figure 6: The wine business confidence in different producing regions. Source: Agricultural Business Chamber (ABC) & SA Wine Industry Information & Systems (SAWIS) Institutional differences: Different role players in the wine business industry also indicated the different confidence levels. Three different institutional groupings are distinguished in the measurement of the wine business confidence index: Private cellars; producer cellars; and wholesalers. The private cellars, which confidence did dropped significantly since October 2008 are still the most confident group of role players in the industry. Producers’ cellars indicated a consistent drop in confidence between October 2007 and April 2009. Their confidence, however, increased significantly in October 2009. The wholesalers are overall the least confident in the industry. Their levels were, however, higher than those of the producer cellars in October 2007 and April 2009, respectively. Figure 7 below shows the confidence levels of wine executives representing different group of role players within the wine industry.

19

Figure 7: The wine business confidence for different groups of role players in the wine industry Source: Agricultural Business Chamber (ABC) & SA Wine Industry Information & Systems (SAWIS) 5. MAJOR DRIVERS IN THE SOUTH AFRICAN WINE INDUSTRY It is clear from the above industry analysis, that renewal, innovation and the upgrading of physical and social infrastructure is required to enable the South African wine industry to sustain its general positive competitiveness trend since the early 1990’s. Firm action across a broad front however will be required to confirm a positive trajectory. From the above analysis a number of future drivers are listed: (i) Product quality improvement and product integrity: The plantings since 1997/98, the quality upgrading of South African wines and the introduction of measures to effectively establish production authentically and integrity and to combat for example illegal flavouring practices contributed substantially to the current position of strength. Initiatives and measures to enhance such industry level applications will be a future “building block” of success. (ii) ‘Brand SA’ roll-out: The ability to establish a unique “Brand SA” proposition for South African wines will assist in creating a differentiated “playing field” for South African wines. The industry’s efforts to craft a unique and vibrant marketing message based on the diversity of the South African winelands (including social and biodiversity is in progress and provide exciting opportunities). Furthermore, the inclusion of biodiversity codes at farm and cellar levels in the “Integrated Wine Production” system gives substantiation to this particular drive; social and transformation codes will follow soon, with the gazetting of the Wine Transformation Charter. (iii) A sharper market segment focus: The exposure of wine producers and marketers to evolving preferences and the focus on “doing-the-right-things right” is driving the export initiative of South African wines. It is however clear that the increased understanding of the

20

evolving market will be required to survive in a highly competitive global environment. The selection of appropriate countries, market segments in particular and price points and a clear comprehension of the required business systems to operate successfully in the selected segment will be necessary to give operational effect to a “Brand SA” strategy. Market segmentation will be a key in this focus area with ethical and environmental positioning as an important competitive advantage for South African wines. (iv) Cost effectiveness technology and business systems: South Africa’s wine production cannot position itself as a “high volume-low unit cost” producer. South African wines should thus rather focus on higher quality; higher value points in particular market segments. However, the South African wine industry will still be highly constrained by relative high input cost systems. Technical efforts to increase yield per hectare (without compromising on wine quality) and to reduce supply chain costs and time (delay) costs will require innovative R&D solutions and information systems. (v) Social development and economic transformation: Successful Black Economic Empowerment (BEE) strategy will enhance political commitment and support to the industry and create social stability and productive resource mobilisation. The establishment of entrepreneur oriented ‘black business class’ and top level black business leadership must be considered as a significant driver of the South African wine economy of the future. This will also impact positively on domestic market expansion of the consumption of wines as a lifestyle activity amongst black professionals. (vi) Driving the focus of the South African wines in the global arena: The South African wine industry is strongly linked to global trends that need to be integrated into a South African strategy. The following should be noted: Shifting demand (Consumers want more clarity on the nature and ethics of a product;

and companies need customer loyalty); increasing retail power (supermarkets); increasing competition and creating brand value; reliable supply chain systems.

The world is looking for quality red wine. Premium red wine products that uplift the

image of a country’s wine industry in total are thus required. Global business consolidation processes are underway - mergers and acquisitions and

joint ventures of wine companies to form bigger brands and to achieve greater market access.

The settings of multi-national wine companies are expected and links with global

supply chains are expected sooner than later in South Africa. (vii) International trade agreements: The global trends and the use of concepts such as “Geographical Indicators” and “Traditional Expressions”, to direct international trade regimes could be significant for global wine trade and South Africa is in a good position to exploit new opportunities but should also guard against the establishment of new ‘trade constraining’ barriers. (viii) Successful and proactive government and industry interaction to establish confidence and an enhancing business and social environment: The wine industry,

21

at a recent workshop on competitiveness, rated an open ‘red telephone line’ to government as vital for a successful and performing wine economy. This partnership will be required to focus on a number of activities. These include market development, regulation and export promotion; the active positioning of ‘Brand SA’ by government agencies (NDA, dti, SAA, Tourism, etc), infrastructure expansion, in particular exportation facilities, transportation networks, research support and technological innovation; economic empowerment and transformation support; trade agreements and policy development; combating crime; and the simplification of regulations and a reduction in bureaucratic ‘red tape’ to name the main areas of concern. 6. CONCLUSION It is important to measure and analyse trends in the competitiveness of an industry in order to support the required country- and firm level strategising required to sustain and improve performance. The analysis traces the improved competitive performance of the South African wine industry and confirms the openness of the South African wine economy where the exchange rate and other global impacts and trends play an important role in competitiveness status. South Africa’s wines are increasingly internationally competitive, with a sustainable and positive trend since 1990. However recently this trend started to show a decline, while business confidence is also declining. To enable the wine industry to attain and sustain such positive trends, and to build the required confidence to compete in a tough global environment, a multi-pronged strategic approach to sustainable growth and development are recommended focussing on five areas: (i) the crafting of a strong and identifiable ‘Brand South Africa’ proposition to portray the uniqueness of South Africa as a quality wine-producing region of excellence, adhering to sound social, environmental and business ethics; (ii) The introduction of measures to counteract the negative impact of a fluctuating exchange rate such as cost effective production processes, effective supply chains, increased productivity and unique marketing strategies; (iii) The implementation and management of transformation through social capital development and successful BEE activities; (iv) The establishment of a sound industry/government partnership to create a competitive framework in order to stimulate investment in infrastructure and development in the sector; and (v) Increase funding for industry level initiatives, especially in market development and research and technological innovation.

22

7. REFERENCES AGRICULTURAL BUSINESS CHAMBER (ABC), (2000). How competitive is the South African agricultural industry? Production, processing, inputs. ABC, P.O. Box 1508, Pretoria, 0001, South Africa. AGRICULTURAL BUSINESS CHAMBER (ABC), (2005). Wine Executive Survey (WES) 2005 AGRICULTURAL BUSINESS CHAMBER (ABC), (2008). Wine Executive Survey (WES) 2008 AGRICULTURAL BUSINESS CHAMBER (ABC) & SA WINE INDUSTRY INFORMATION & SYSTEMS (SAWIS), (2009), Wine Confidence Index data. ANDERSON K (2006). CHELTENHAM, WEDWARD ELGAR. The world’s wine markets: Globalisation at work. BOEHLJE, M. (1996). Industrialisation of Agriculture. What are the implications? Choices. First Quarter, 1996: 30-33. BALASSA, B. (1989). Comparative advantage, trade policy and economic development. London, Harvester/Wheat sheaf. CHO, D.S. & MOON, H.C. (2002). From Adam Smith to Michael Porter. Evolution of Competitiveness Theory. World Scientific, Singapore, New Jersey, London, Hong Kong. ESTERHUIZEN, D. (2006). An inquiry into the competitiveness of the South African agribusiness sector. PhD-theses, University of Pretoria, Pretoria. LE ROUX, E. (2007). Personal discussion, Stellenbosch. PORTER, M.E. (1998). The competitive advantage of nations. London, Macmillan. South African Wine & Brandy Company (SAWB) 2005. The Competitiveness of the South African Wine Industry. www.sawb.co.za, Stellenbosch. VOLRATH, T.L. (1991). A theoretical evaluation of alternative trade intensity measures of revealed comparative advantage. Weltwirtschaftliches Archive 127 (2): 265 – 280. SOUTH AFRICAN WINE & BRANDY COMPANY (SAWB) (2002). Setting the strategic course for excellence. VR Graphics. SOUTH AFRICAN WINE INDUSTRY INFORMATION & SYSTEMS (SAWIS), (2009) SOUTH AFRICA WINE INDUSTRY DIRECTORY (2003-2008). A Winelands publication. ISBN 978-0-620-38730-9.

23

THE WINE INDUSTRY TRANSFORMATION CHARTER (2006). The South African Wine Industry Council, Stellenbosch, July 2006. VAN ROOYEN, C.J. (2007). Considering competitiveness in the wine industry. Keynote paper, Bodegas Argentina, September 2007. Mendoza, Argentina.