Embed Size (px)

Citation preview

An Overview of Recent U.S Tax LawChanges Affecting Offshore

Planning

“Going offshore” should never be tax driven; U.S. tax

neutral.

U.S. citizens/residents must report worldwide income on

form 1040 annually.

U.S. citizens/residents may be able to achieve deferral of

U.S. income tax if they engage in a foreign active trade or

business through a foreign corporation; not with APT that

generates passive income.

Different tax treatment between active trade or business

income and passive income in IRC.

U.S. Citizens And Residents

Must Report Their World Wide Income

Active trade or business offshore (e.g., U.S.. person

manufactures shirts offshore and sells products only to

Bolivians); foreign source income through foreign corp.

APT planning; Tax neutral.

» Deferral of U.S. income taxes if APT invests in bona fide retirement

investments offshore (e.g., Qualified annuities, life insurance

contracts) Tax neutrality.

» Tax considerations on funding an APT:

Income tax considerations.

Estate and gift tax considerations.

Reasons For Going Offshore

U.S. persons residing offshore and working

offshore are entitled to exempt income earned

from services outside U.S. . IRC section 911.

The aforesaid exemption is subject to

limitations.

U.S. Persons Working Outside U.S.

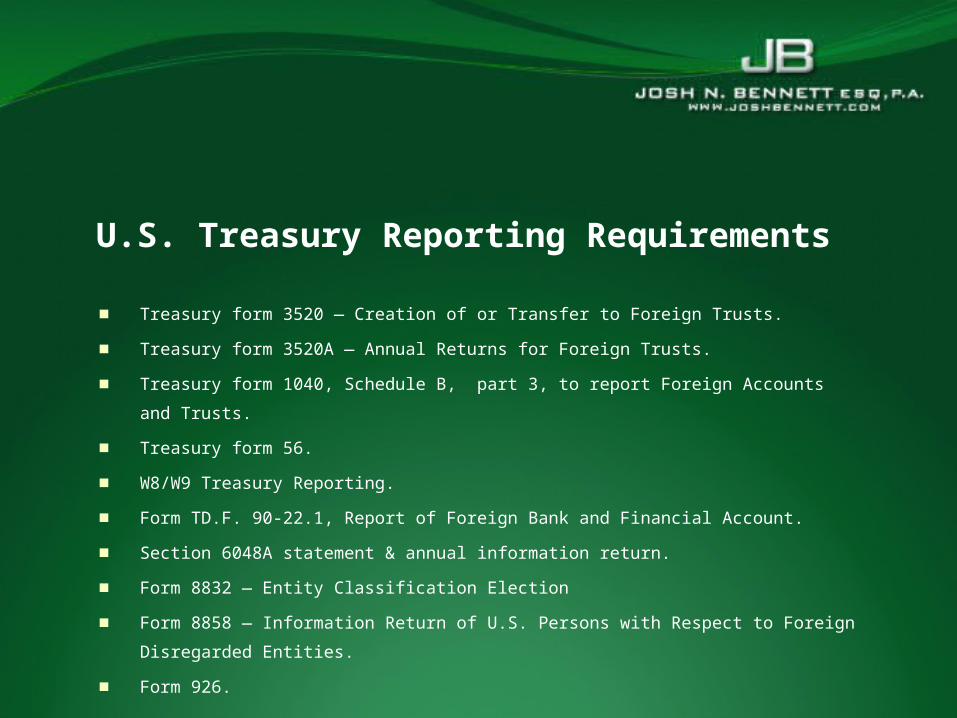

Treasury form 3520 — Creation of or Transfer to Foreign Trusts.

Treasury form 3520A — Annual Returns for Foreign Trusts.

Treasury form 1040, Schedule B, part 3, to report Foreign Accounts

and Trusts.

Treasury form 56.

W8/W9 Treasury Reporting.

Form TD.F. 90-22.1, Report of Foreign Bank and Financial Account.

Section 6048A statement & annual information return.

Form 8832 — Entity Classification Election

Form 8858 — Information Return of U.S. Persons with Respect to Foreign Disregarded

Entities.

Form 926.

U.S. Treasury Reporting Requirements

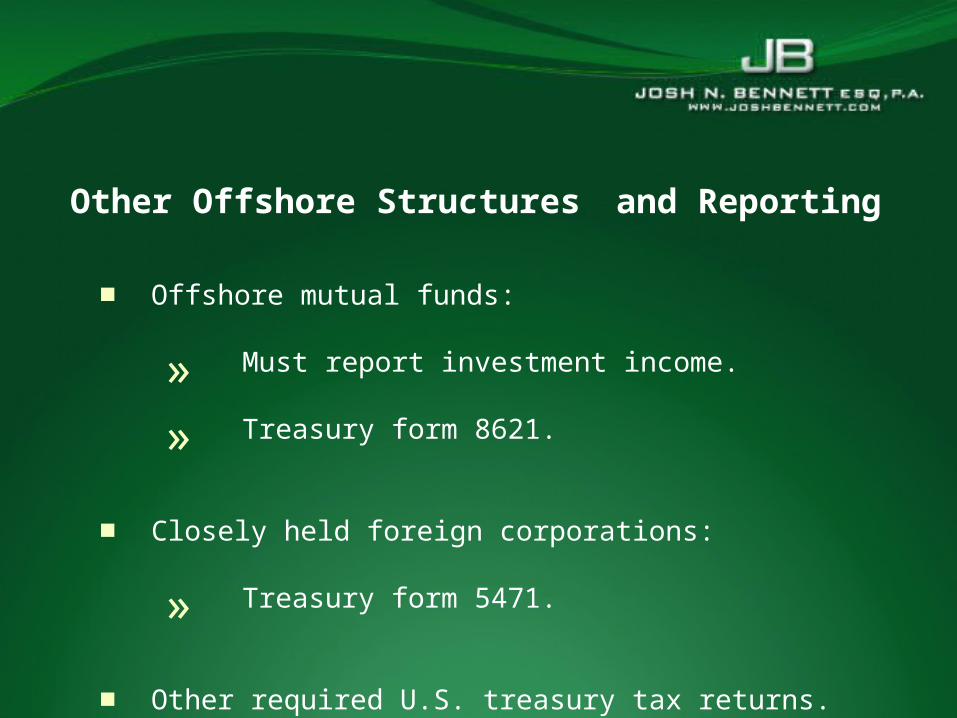

Offshore mutual funds:

» Must report investment income.

» Treasury form 8621.

Closely held foreign corporations:

» Treasury form 5471.

Other required U.S. treasury tax returns.

Offshore life insurance products and annuities.

Other Offshore Structures and Reporting

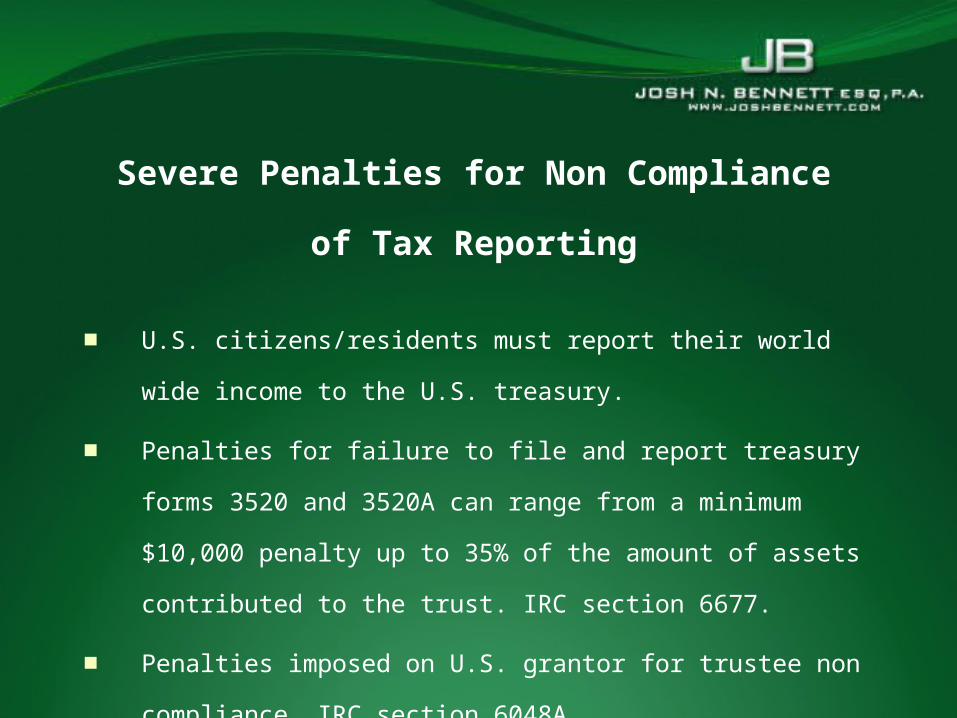

U.S. citizens/residents must report their world wide income

to the U.S. treasury.

Penalties for failure to file and report treasury forms 3520

and 3520A can range from a minimum $10,000 penalty up

to 35% of the amount of assets contributed to the trust. IRC

section 6677.

Penalties imposed on U.S. grantor for trustee non

compliance. IRC section 6048A.

Criminal penalties.

Severe Penalties for Non Compliance

of Tax Reporting

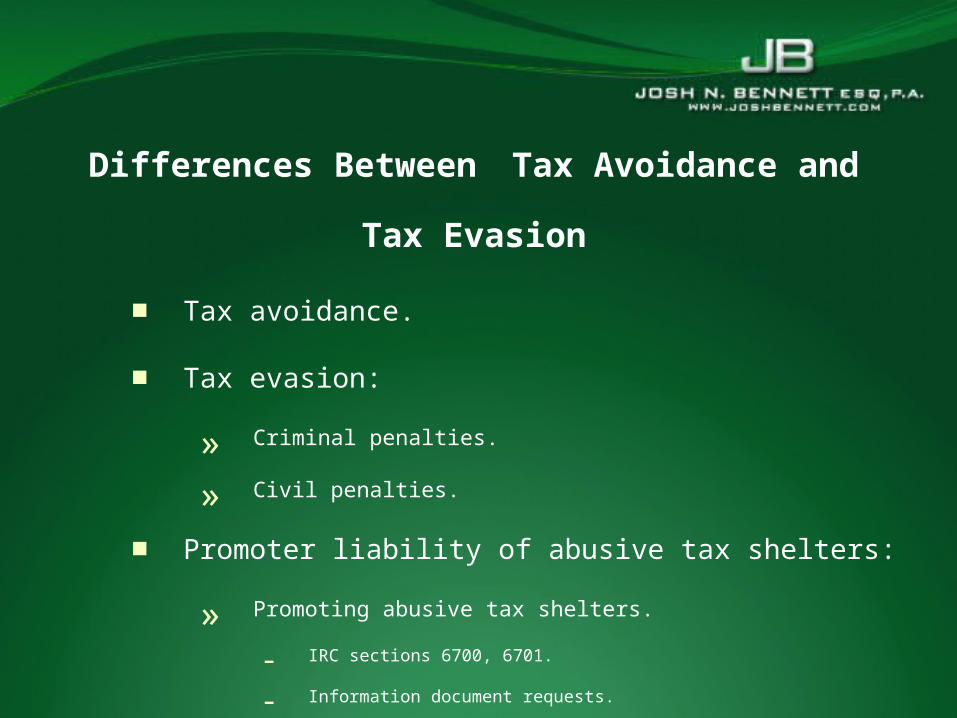

Tax avoidance.

Tax evasion:

» Criminal penalties.

» Civil penalties.

Promoter liability of abusive tax shelters:

» Promoting abusive tax shelters.

- IRC sections 6700, 6701.

- Information document requests.

- Criminal indictment investigations.

Different examples of each term.

Differences Between Tax Avoidance and

Tax Evasion

Signed into law on March 18, 2010.

Implemented certain new withholding tax and information reporting laws to the Internal Revenue Code (“Code”), most commonly referred to as the Foreign Account Tax Compliance Act (“FATCA”).

The Hiring Incentives to Restore Employment (“HIRE”) Act

HIRE Act adds new §§1471 through 1474. For U.S. accounts, a withholding agent must withold

30% of the amount of any withholdable payment to a foreign financial institution ( an “FFI”) which does not comply with certain reporting requirements.

Generally effective for payments made after December 31, 2012, subject to certain grandfathering rules.

Under new §1471, a, FFI may comply by entering into an agreement with the IRS to obtain information on each of its accounts, follow verification and due diligence procedures, respond to information requests, and report annually on any such account, including (but not limited to) the name, address, and TIN of each U.S. person account holder, the account number , balance or value, and gross receipts or withdrawals or payments.

New Foreign Financial Institution Rules

FFIs must impose withholding on any passthrough payment to a recalcitrant account holder on a non participating FFI; and, if any foreign laws prevents its compliance, to try to obtain from each U.S. account holder a waiver of that law and to close the account if it is unable to do so.

IRS is authorized to terminate any agreement upon a determination of non-compliance.

FFI may elect to be withheld upon rather than to withhold.

New Foreign Financial Institution Rules

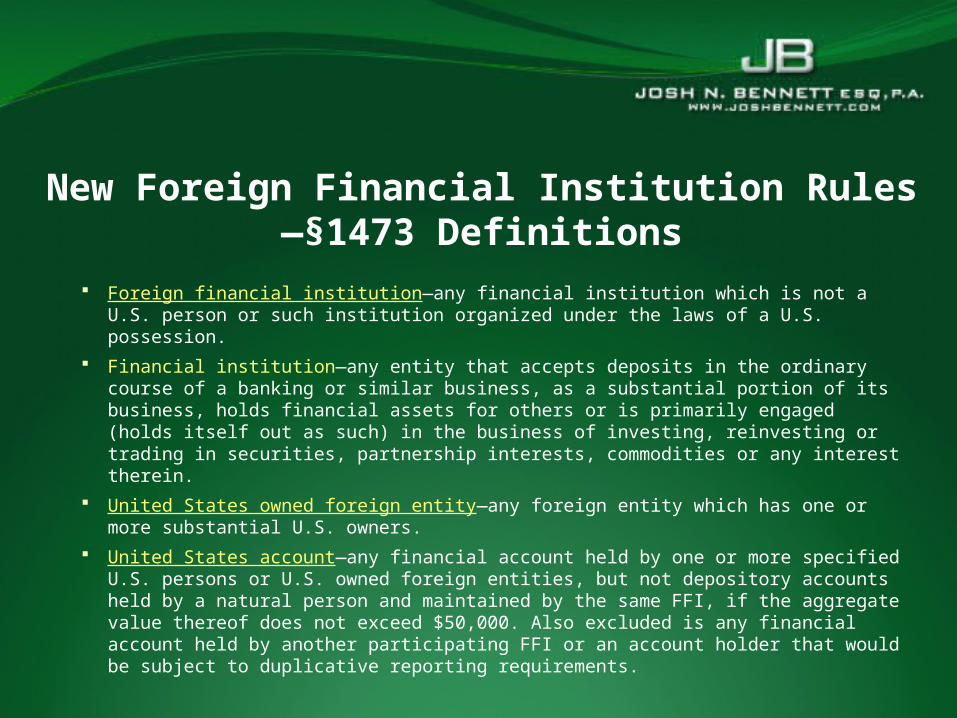

Foreign financial institution—any financial institution which is not a U.S. person or such institution organized under the laws of a U.S. possession.

Financial institution—any entity that accepts deposits in the ordinary course of a banking or similar business, as a substantial portion of its business, holds financial assets for others or is primarily engaged (holds itself out as such) in the business of investing, reinvesting or trading in securities, partnership interests, commodities or any interest therein.

United States owned foreign entity—any foreign entity which has one or more substantial U.S. owners.

United States account—any financial account held by one or more specified U.S. persons or U.S. owned foreign entities, but not depository accounts held by a natural person and maintained by the same FFI, if the aggregate value thereof does not exceed $50,000. Also excluded is any financial account held by another participating FFI or an account holder that would be subject to duplicative reporting requirements.

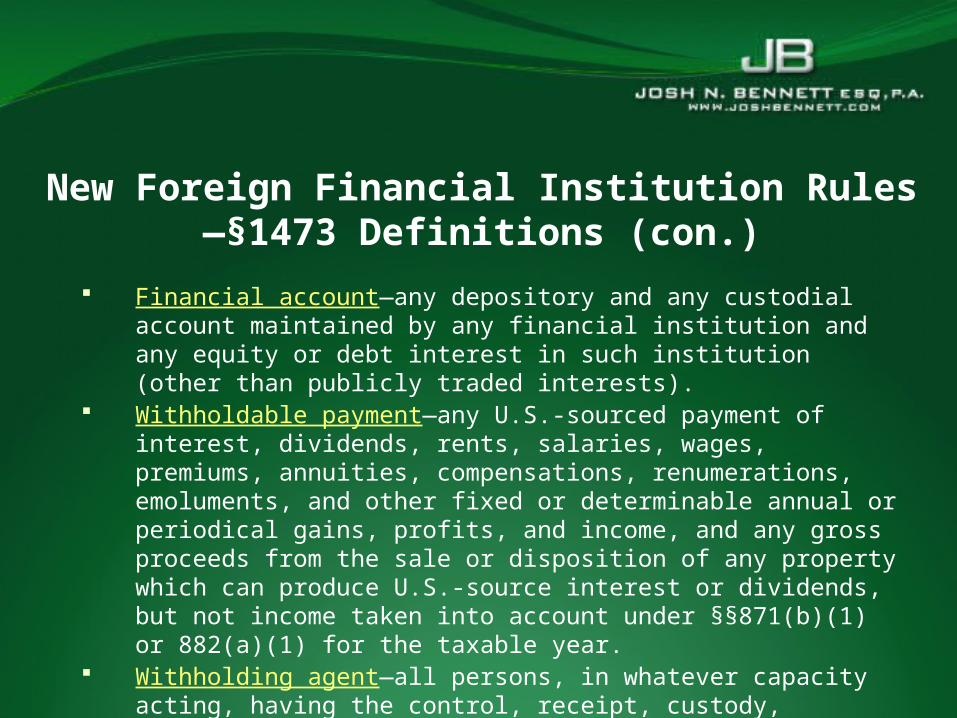

New Foreign Financial Institution Rules—§1473 Definitions

Financial account—any depository and any custodial account maintained by any financial institution and any equity or debt interest in such institution (other than publicly traded interests).

Withholdable payment—any U.S.-sourced payment of interest, dividends, rents, salaries, wages, premiums, annuities, compensations, renumerations, emoluments, and other fixed or determinable annual or periodical gains, profits, and income, and any gross proceeds from the sale or disposition of any property which can produce U.S.-source interest or dividends, but not income taken into account under §§871(b)(1) or 882(a)(1) for the taxable year.

Withholding agent—all persons, in whatever capacity acting, having the control, receipt, custody, disposal, or payment of any withholdable payment.

New Foreign Financial Institution Rules—§1473 Definitions (con.)

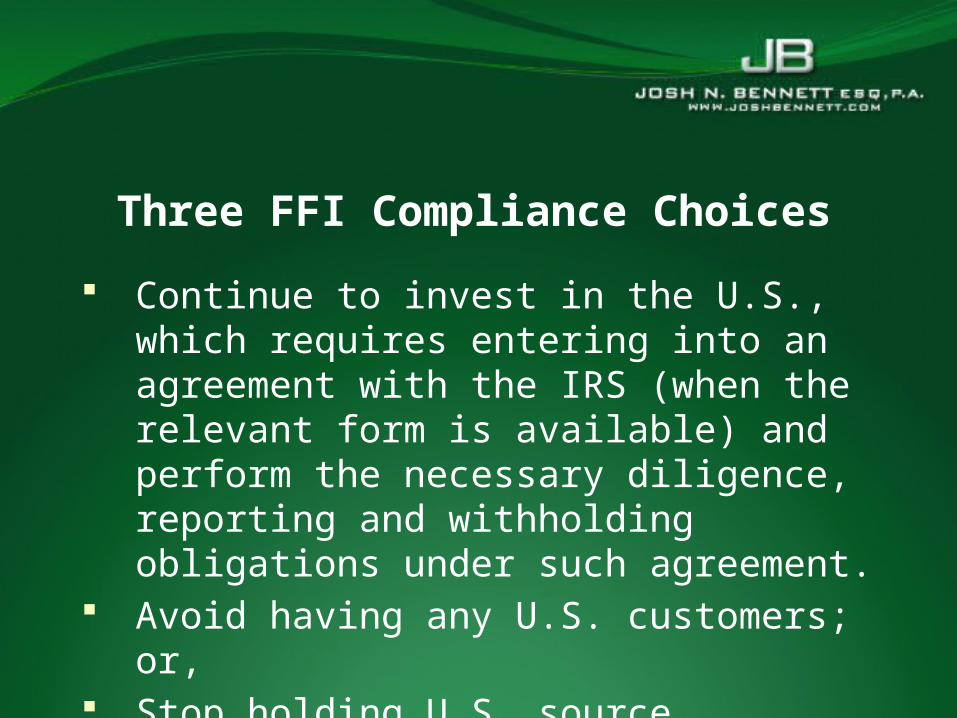

Continue to invest in the U.S., which requires entering into an agreement with the IRS (when the relevant form is available) and perform the necessary diligence, reporting and withholding obligations under such agreement.

Avoid having any U.S. customers; or, Stop holding U.S. source generating

investments.

Three FFI Compliance Choices

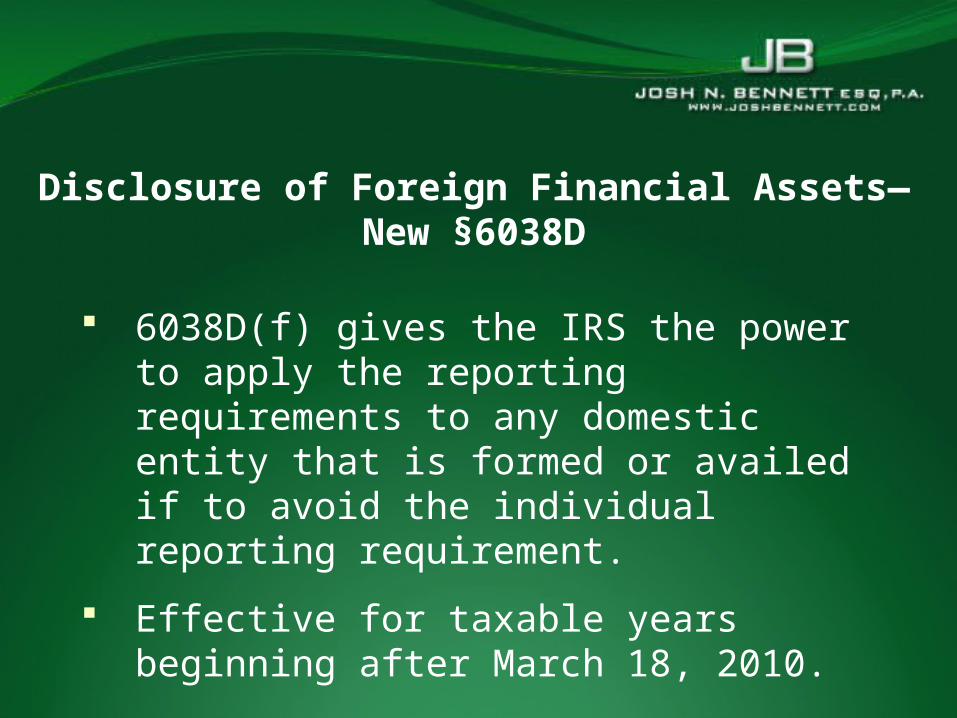

Disclosure of Foreign Financial Assets—New §6038D

6038D(f) gives the IRS the power to apply the reporting requirements to any domestic entity that is formed or availed if to avoid the individual reporting requirement.

Effective for taxable years beginning after March 18, 2010.

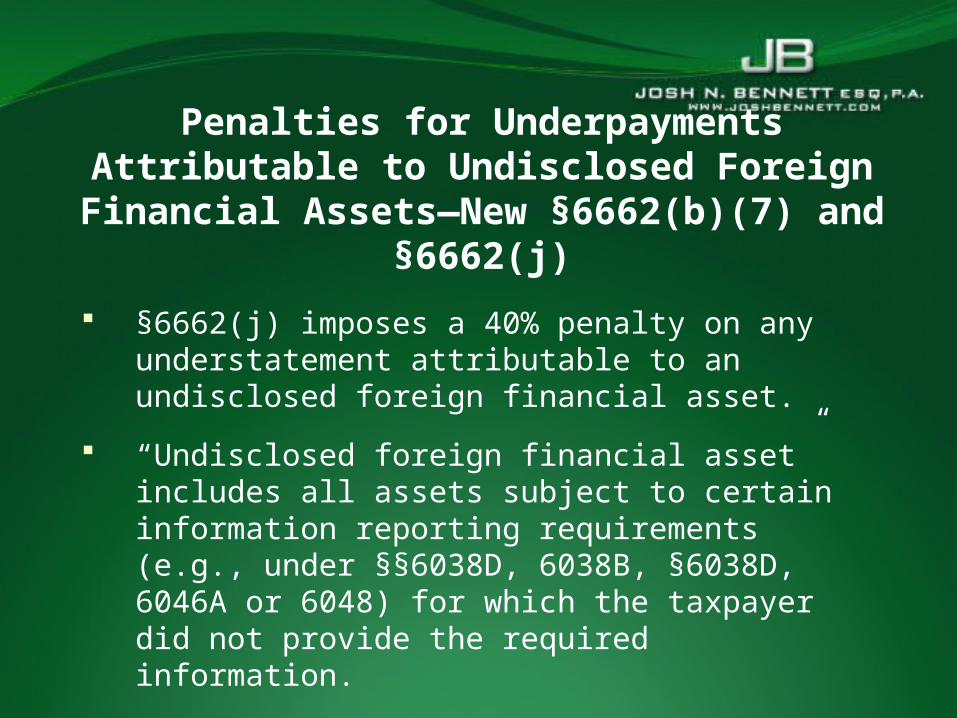

§6662(j) imposes a 40% penalty on any understatement attributable to an undisclosed foreign financial asset.

“Undisclosed foreign financial asset” includes all assets subject to certain information reporting requirements (e.g., under §§6038D, 6038B, §6038D, 6046A or 6048) for which the taxpayer did not provide the required information.

These provisions are effective for taxable years beginning after March 18, 2010 (the date of enactment).

Penalties for Underpayments Attributable to Undisclosed Foreign

Financial Assets—New §6662(b)(7) and §6662(j)

§679 treats a U.S. person transferor of property to a foreign trust having a U.S. beneficiary as the owner of the related portion of such trust. The HIRE Act clarifies in several respects the determination whether the foreign trust has a U.S. beneficiary for this purpose.

§679(c)(1) treats an amount as accumulated for the benefit of a U.S. person even if the U.S. person’s interest in the trust is contingent on a future event.

§679(c)(4) provides that if any person has the discretion (by the trust agreement, power of appointment, or otherwise) to make a distribution from the trust to, or for the benefit of, any person, the trust is treated as having a U.S. beneficiary unless:» The terms of the trust specifically identify the class of

persons to whom such distributions may be made; and,» none of those persons is a U.S. person during the taxable

year.

Foreign Trusts With a U.S. Beneficiary—Revised §679

§679(c)(5) provides that any agreement or understanding (whether written, oral, or otherwise) that may result in the income or corpus of the trust being paid or accumulated to or for the benefit of a U.S. person will be treated as a term of the trust if any U.S. person who directly or indirectly transfers property to the trust is directly or indirectly involved in any such agreement or understanding ie . Letter of Wishes.

§679(d) provides that if a U.S. person directly or indirectly transfers property to a foreign trust (other than certain deferred compensation trusts and charitable trusts), the trust is presumed to have a U.S. beneficiary for purposes of §679, but this presumption does not apply if such U.S. person:

» submits such information as the IRS may require; and,» demonstrates to the IRS’s satisfaction that no trust income or

corpus may be paid or accumulated. Revisions are effective March 18, 2010 (date of enactment).

Foreign Trusts With a U.S.Beneficiary—Revised §679 (con.)

§643(i)(1) treats a loan of cash or marketable securities by a foreign trust to a grantor, beneficiary, or related person who is a U.S. person as a distribution for non-grantor trust purposes.

Under §643(i)(1) and §643(ii)(2)(E), the same distribution treatment applies to the use of any property of a foreign trust by such U.S. person to the extent the trust is paid less than fair market value compensation for such use within a reasonable period of time.

In addition, for purposes of determining whether a foreign trust has a US beneficiary under §679, §679(c)(6) treats a loan of cash or marketable securities or use of any other trust property by a U.S. person as payment from the trust to the U.S. person to the extent such person pays less than market interest on a loan or less than fair market value for the use of trust property within a reasonable period of time.

Effective for loans made and uses of property after March 18, 2010 (the date of enactment).

Uncompensated Use of Trust Property—Revised §643(i) and New §679(c)(6)

§6048(b) now requires a U. S. person that is treated as an owner of any portion of a foreign trust under the grantor trust provisions to provide information as may be required with respect to the trust (in addition to the preexisting obligation of ensuring that the trust complies with its reporting obligations).

Effective for tax years beginning after March 18, 2010.

IRS Notice 2010-60.

Reporting Requirement of United States Owners of Foreign Trusts:

Amended §6048(b)(1)

Seek professional advise from an informed

offshore tax professional such as a CPA or

international tax attorney.

Do not rely on foreign attorneys or other

foreign professionals for US tax advice.

Conclusion

Thank you!