Embed Size (px)

Citation preview

An overview of energy efficiency and demand side management in South Africa

30 January 2012

Tom Skinner

Overview of presentation

• Eskom and the South African Environment

• The State of the System as Driver for EE

• Energy Sectors and Activities

• Capabilities, Successes and Funding

• EEDSM Funding Mechanisms and Programmes

• Lessons Learned

• Future Focus Areas

2011/11/09 2

INTRODUCTIONEskom and the South African Environment

2011/11/09 4

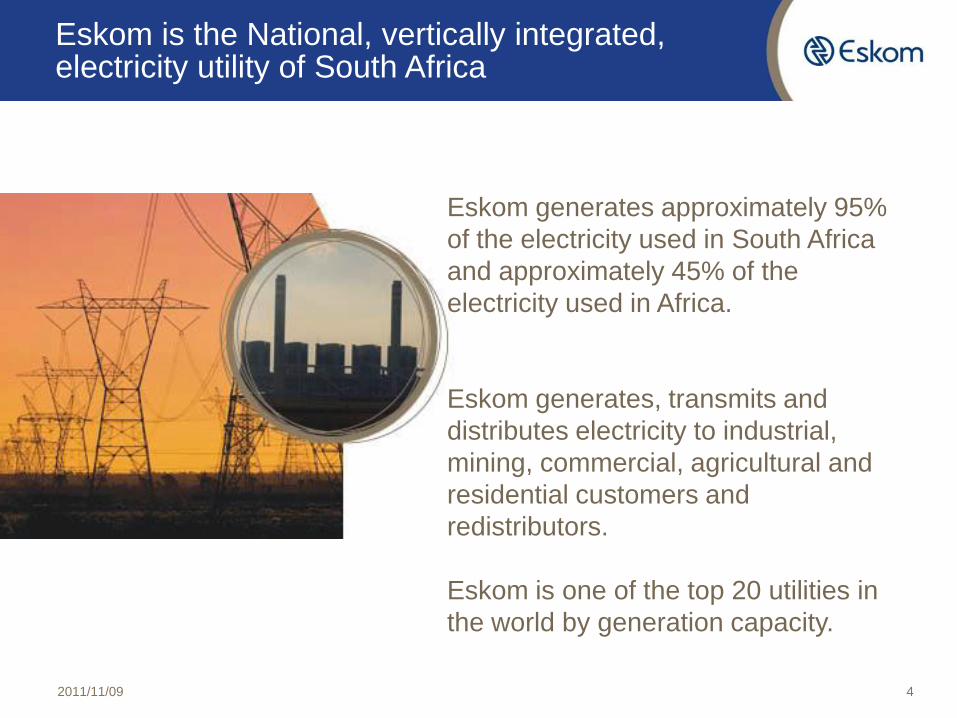

Eskom is the National, vertically integrated, electricity utility of South Africa

Eskom generates approximately 95%

of the electricity used in South Africa

and approximately 45% of the

electricity used in Africa.

Eskom generates, transmits and

distributes electricity to industrial,

mining, commercial, agricultural and

residential customers and

redistributors.

Eskom is one of the top 20 utilities in

the world by generation capacity.

5

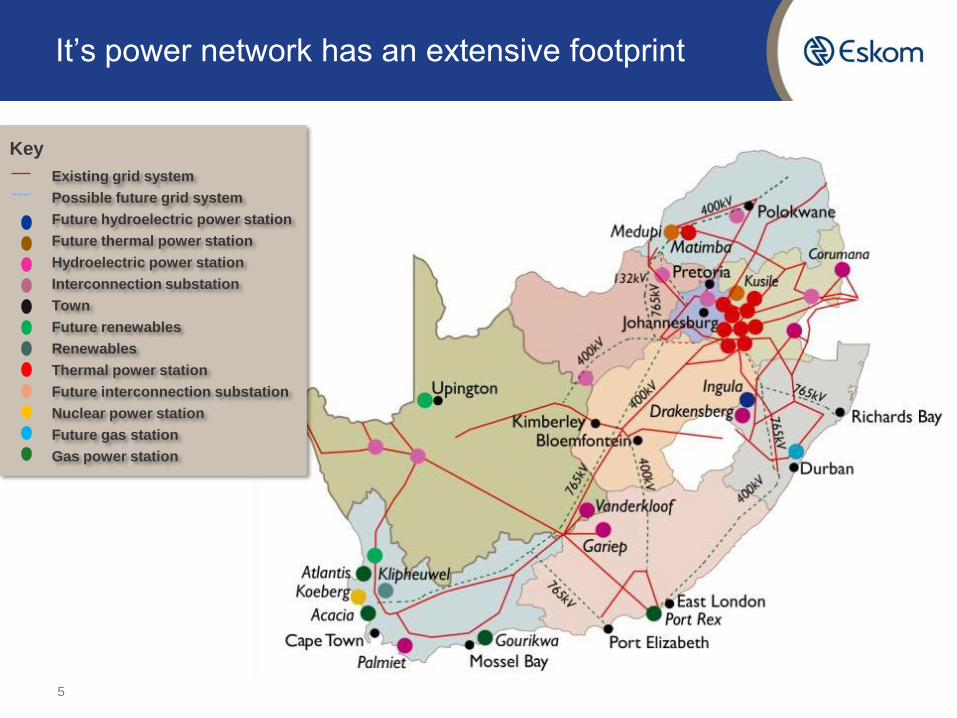

It’s power network has an extensive footprint

Key

Existing grid system

Possible future grid system

Future hydroelectric power station

Future thermal power station

Hydroelectric power station

Interconnection substation

Town

Future renewables

Renewables

Thermal power station

Future interconnection substation

Nuclear power station

Future gas station

Gas power station

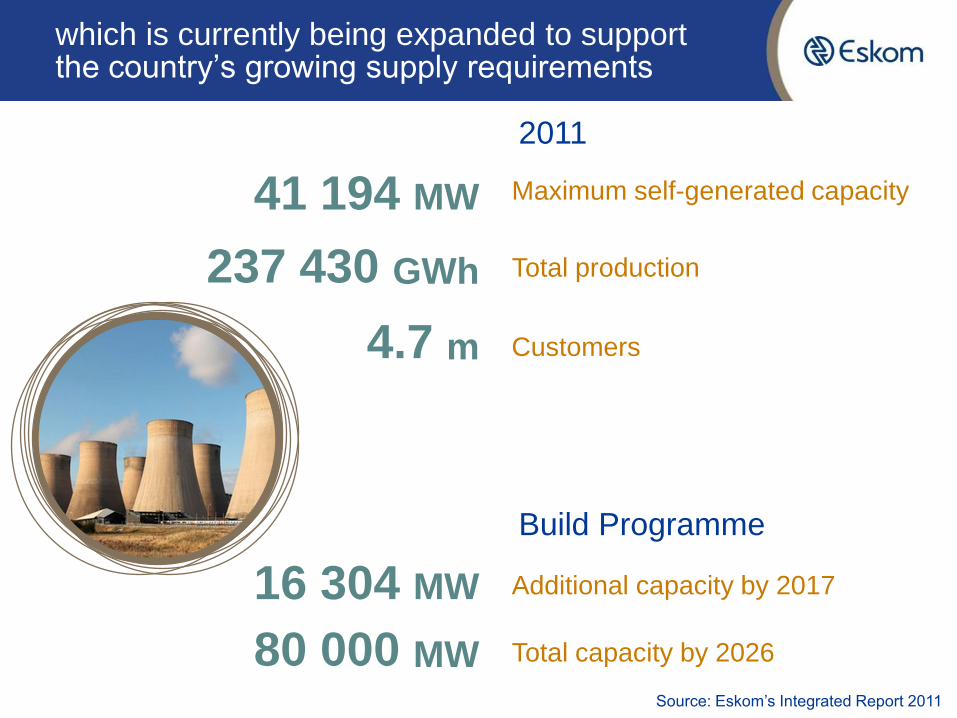

which is currently being expanded to support the country’s growing supply requirements

237 430 GWh

41 194 MW

4.7 m

Maximum self-generated capacity

Total production

Customers

2011

80 000 MW

16 304 MW Additional capacity by 2017

Total capacity by 2026

Build Programme

Source: Eskom’s Integrated Report 2011

In support of national policy direction, Eskom administers a large scale EEDSM programme

2011/11/09 7

NEEA

Department of Energy

National Energy

Regulator of South Africa National Energy

Efficiency Agency

THE STATE OF THE SYSTEMAs a Driver for EE and DSM in the Country

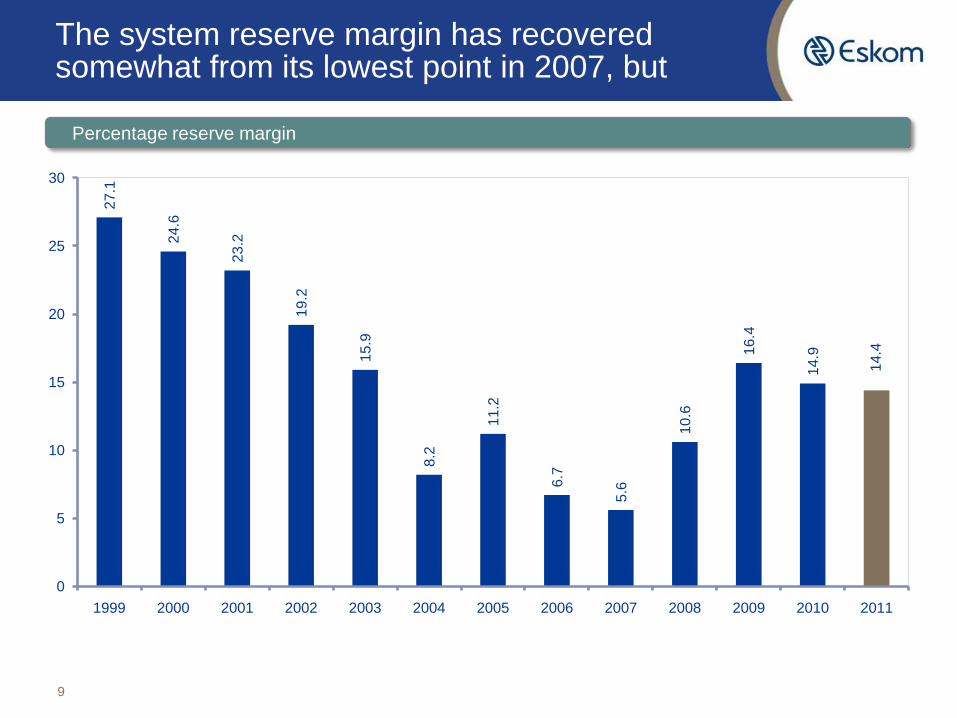

The system reserve margin has recovered somewhat from its lowest point in 2007, but

9

27.1

24.6

23

.2

19.2

15.9

8.2

11.2

6.7

5.6

10

.6

16.4

14.9

14.4

0

5

10

15

20

25

30

1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Percentage reserve margin

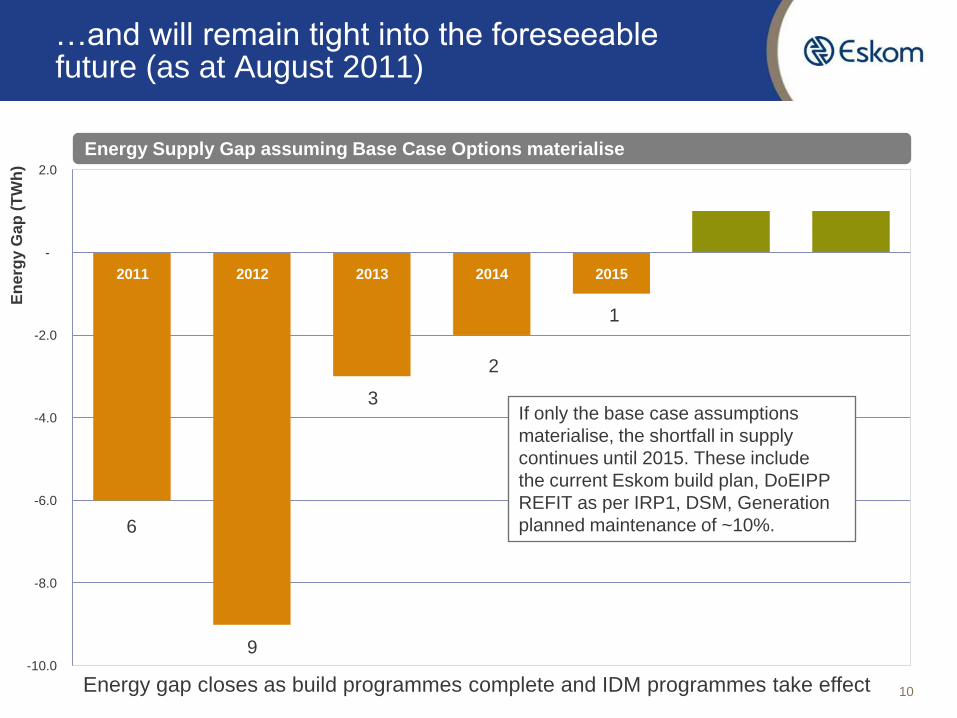

-10.0

-8.0

-6.0

-4.0

-2.0

-

2.0

2011 2012 2013 2014 2015 2016 2017

En

erg

y G

ap

(T

Wh

)

If only the base case assumptions

materialise, the shortfall in supply

continues until 2015. These include

the current Eskom build plan, DoEIPP

REFIT as per IRP1, DSM, Generation

planned maintenance of ~10%.

…and will remain tight into the foreseeable future (as at August 2011)

10

Energy Supply Gap assuming Base Case Options materialise

6

9

3

2

1

Energy gap closes as build programmes complete and IDM programmes take effect

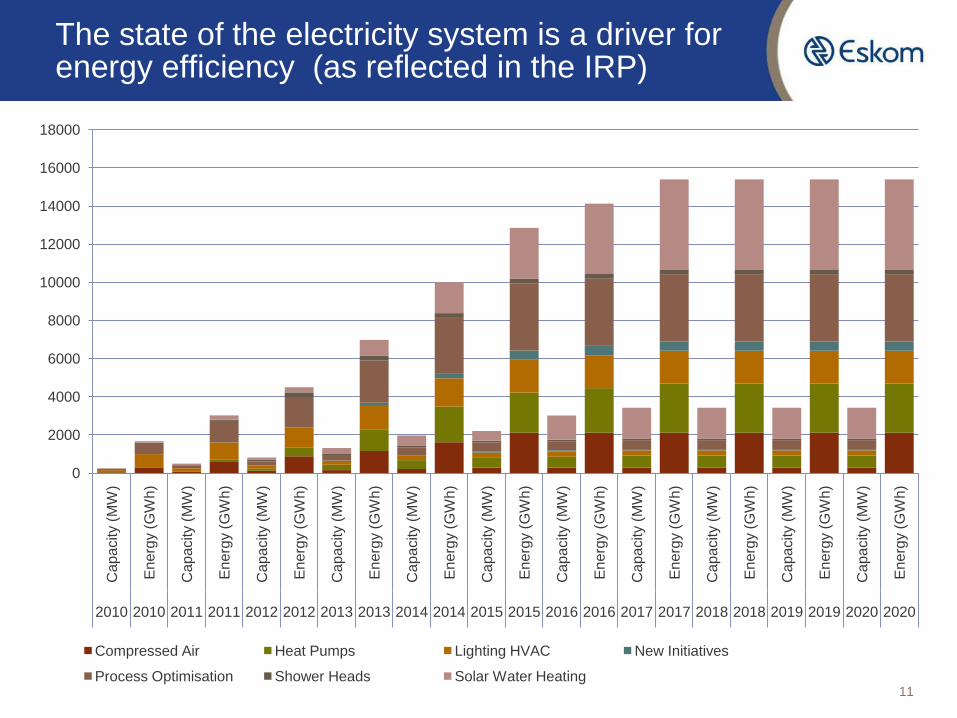

The state of the electricity system is a driver for energy efficiency (as reflected in the IRP)

11

0

2000

4000

6000

8000

10000

12000

14000

16000

18000

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

Ca

pa

city (

MW

)

Energ

y (

GW

h)

Ca

pa

city (

MW

)

En

erg

y (

GW

h)

2010 2010 2011 2011 2012 2012 2013 2013 2014 2014 2015 2015 2016 2016 2017 2017 2018 2018 2019 2019 2020 2020

Compressed Air Heat Pumps Lighting HVAC New Initiatives

Process Optimisation Shower Heads Solar Water Heating

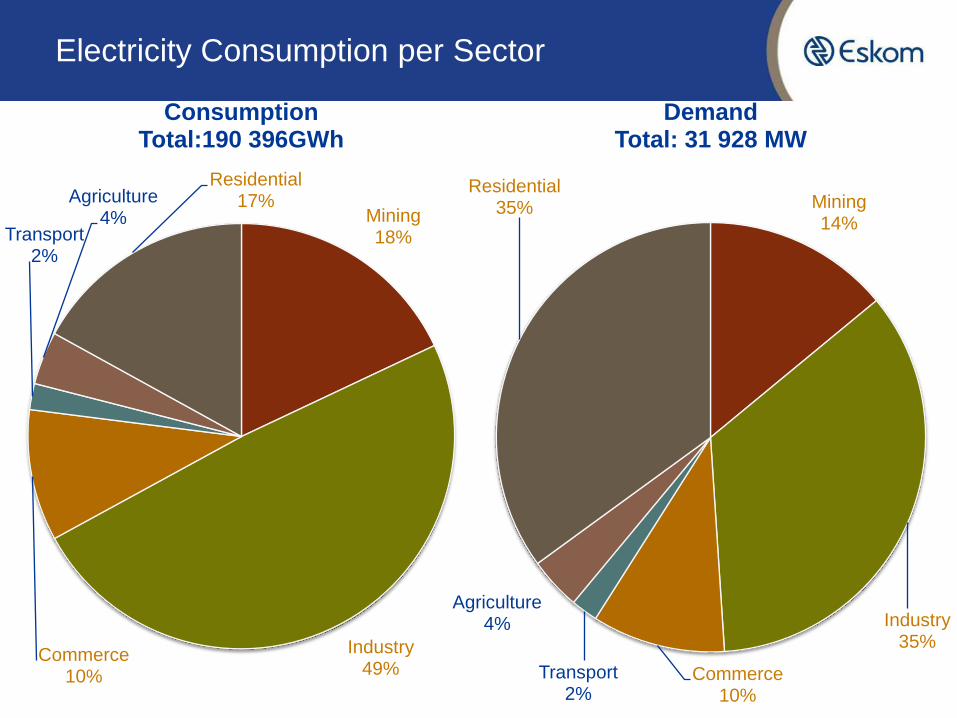

INDUSTRIESEnergy Sectors and Activities

Mining 18%

Industry 49%

Commerce 10%

Transport 2%

Agriculture 4%

Residential 17%

ConsumptionTotal:190 396GWh

Electricity Consumption per Sector

Mining 14%

Industry 35%

Commerce 10%

Transport 2%

Agriculture 4%

Residential 35%

DemandTotal: 31 928 MW

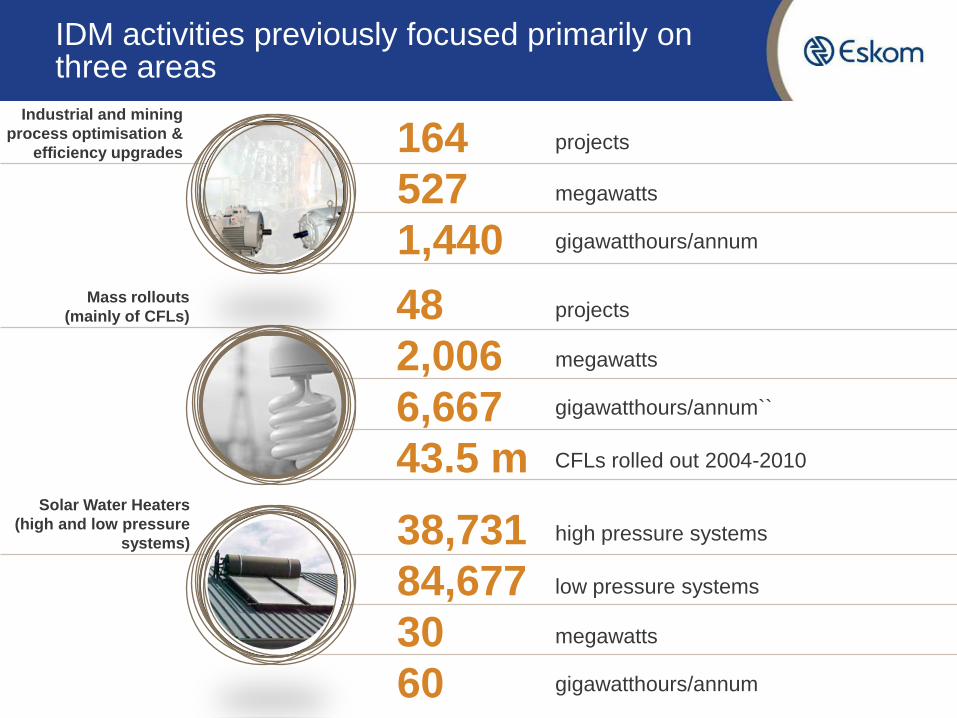

IDM activities previously focused primarily on three areas

164

527

1,440

Industrial and mining

process optimisation &

efficiency upgrades

48

2,006

6,667

43.5 m

38,731

84,677

30

60

Mass rollouts

(mainly of CFLs)

Solar Water Heaters

(high and low pressure

systems)

projects

megawatts

gigawatthours/annum

projects

megawatts

gigawatthours/annum``

low pressure systems

megawatts

gigawatthours/annum

high pressure systems

CFLs rolled out 2004-2010

CAPABILITIESPast EESM Successes

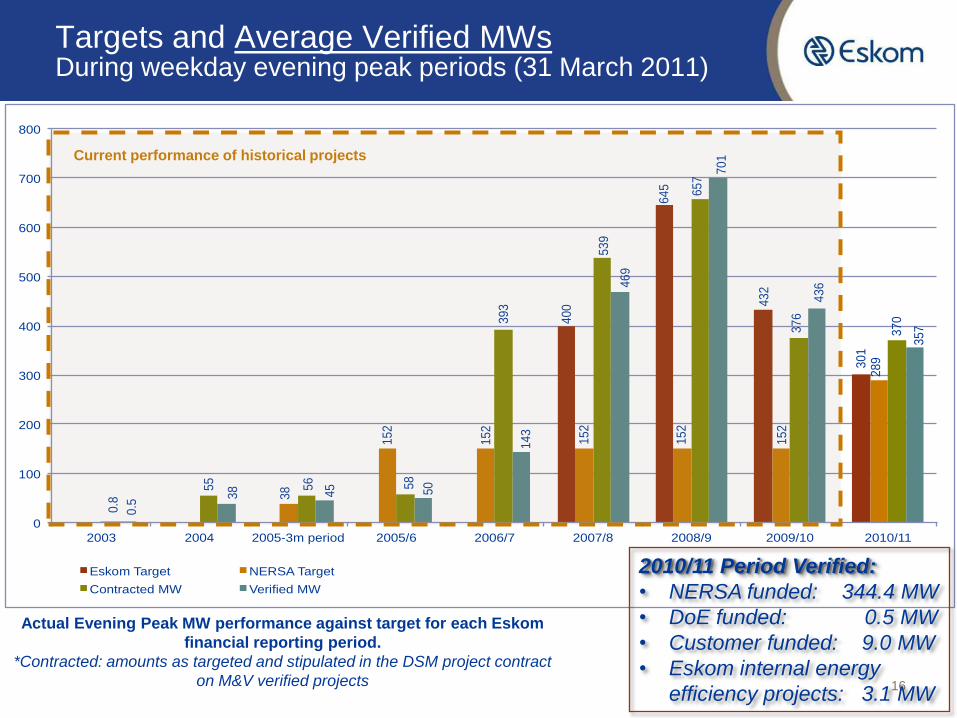

400

64

5

432

301

38

152

152

152

152

152

289

0.8

55

56

58

393

539

657

37

6

370

0.5

38

45

50

14

3

469

701

436

357

0

100

200

300

400

500

600

700

800

2003 2004 2005-3m period 2005/6 2006/7 2007/8 2008/9 2009/10 2010/11

Eskom Target NERSA Target

Contracted MW Verified MW

16

Targets and Average Verified MWs During weekday evening peak periods (31 March 2011)

Actual Evening Peak MW performance against target for each Eskom

financial reporting period.

*Contracted: amounts as targeted and stipulated in the DSM project contract

on M&V verified projects

Current performance of historical projects

2010/11 Period Verified:

• NERSA funded: 344.4 MW

• DoE funded: 0.5 MW

• Customer funded: 9.0 MW

• Eskom internal energy

efficiency projects: 3.1 MW

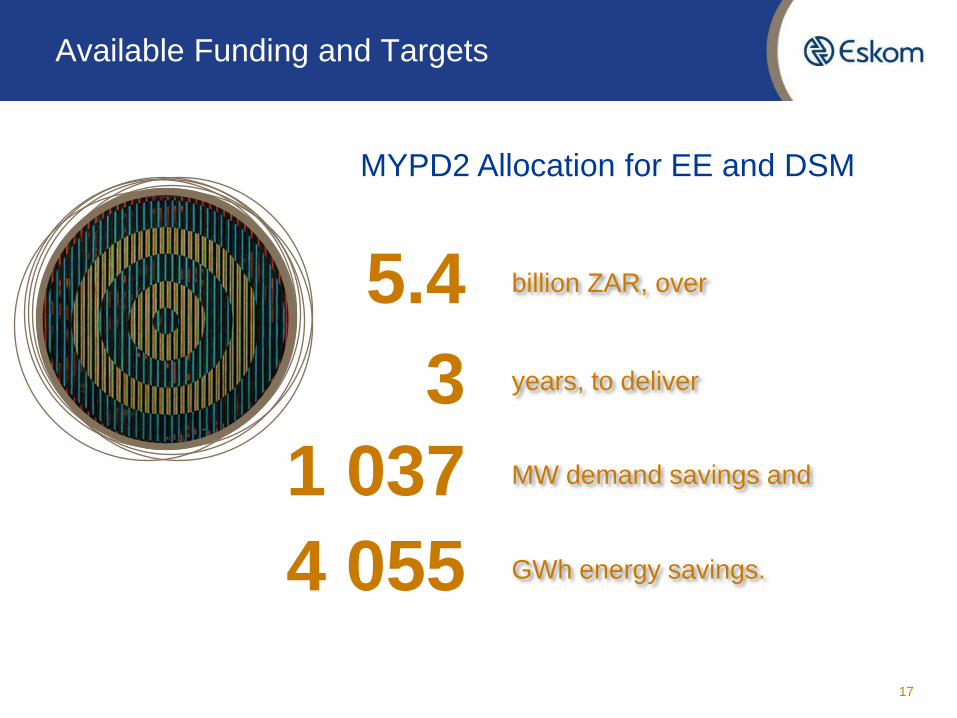

Available Funding and Targets

17

3

5.4

4 055

1 037

billion ZAR, over

years, to deliver

MW demand savings and

GWh energy savings.

MYPD2 Allocation for EE and DSM

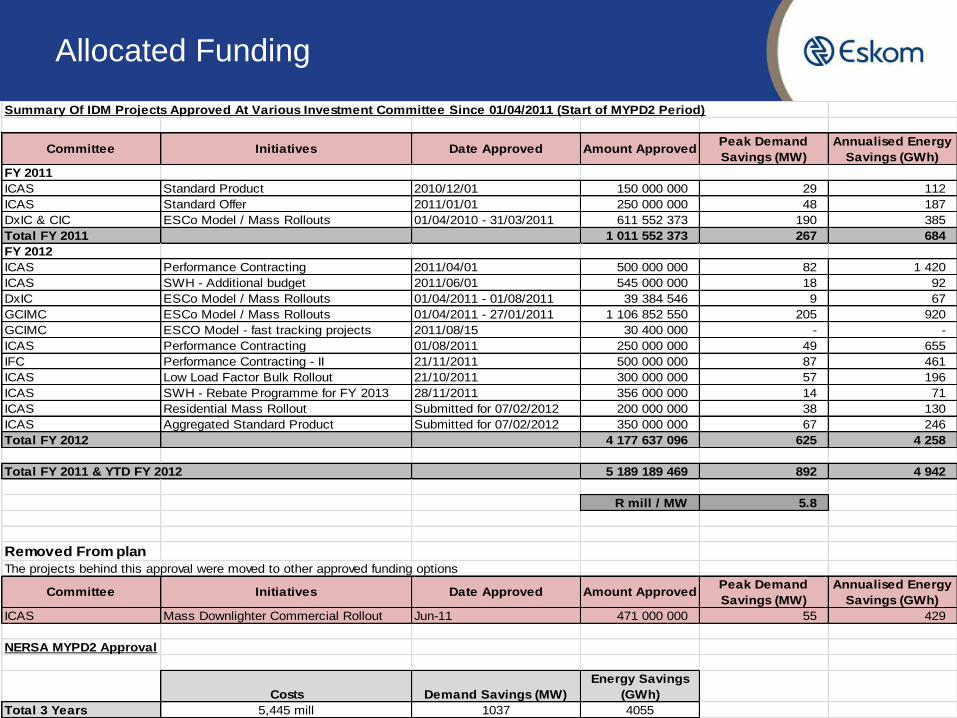

Allocated Funding

Summary Of IDM Projects Approved At Various Investment Committee Since 01/04/2011 (Start of MYPD2 Period)

Committee Initiatives Date Approved Amount ApprovedPeak Demand

Savings (MW)

Annualised Energy

Savings (GWh)

FY 2011

ICAS Standard Product 2010/12/01 150 000 000 29 112

ICAS Standard Offer 2011/01/01 250 000 000 48 187

DxIC & CIC ESCo Model / Mass Rollouts 01/04/2010 - 31/03/2011 611 552 373 190 385

Total FY 2011 1 011 552 373 267 684

FY 2012

ICAS Performance Contracting 2011/04/01 500 000 000 82 1 420

ICAS SWH - Additional budget 2011/06/01 545 000 000 18 92

DxIC ESCo Model / Mass Rollouts 01/04/2011 - 01/08/2011 39 384 546 9 67

GCIMC ESCo Model / Mass Rollouts 01/04/2011 - 27/01/2011 1 106 852 550 205 920

GCIMC ESCO Model - fast tracking projects 2011/08/15 30 400 000 - -

ICAS Performance Contracting 01/08/2011 250 000 000 49 655

IFC Performance Contracting - II 21/11/2011 500 000 000 87 461

ICAS Low Load Factor Bulk Rollout 21/10/2011 300 000 000 57 196

ICAS SWH - Rebate Programme for FY 2013 28/11/2011 356 000 000 14 71

ICAS Residential Mass Rollout Submitted for 07/02/2012 200 000 000 38 130

ICAS Aggregated Standard Product Submitted for 07/02/2012 350 000 000 67 246

Total FY 2012 4 177 637 096 625 4 258

Total FY 2011 & YTD FY 2012 5 189 189 469 892 4 942

R mill / MW 5.8

Removed From plan

The projects behind this approval were moved to other approved funding options

Committee Initiatives Date Approved Amount ApprovedPeak Demand

Savings (MW)

Annualised Energy

Savings (GWh)

ICAS Mass Downlighter Commercial Rollout Jun-11 471 000 000 55 429

NERSA MYPD2 Approval

Costs Demand Savings (MW)

Energy Savings

(GWh)

Total 3 Years 5,445 mill 1037 4055

EEDSM FUNDINGMechanisms and Programmes

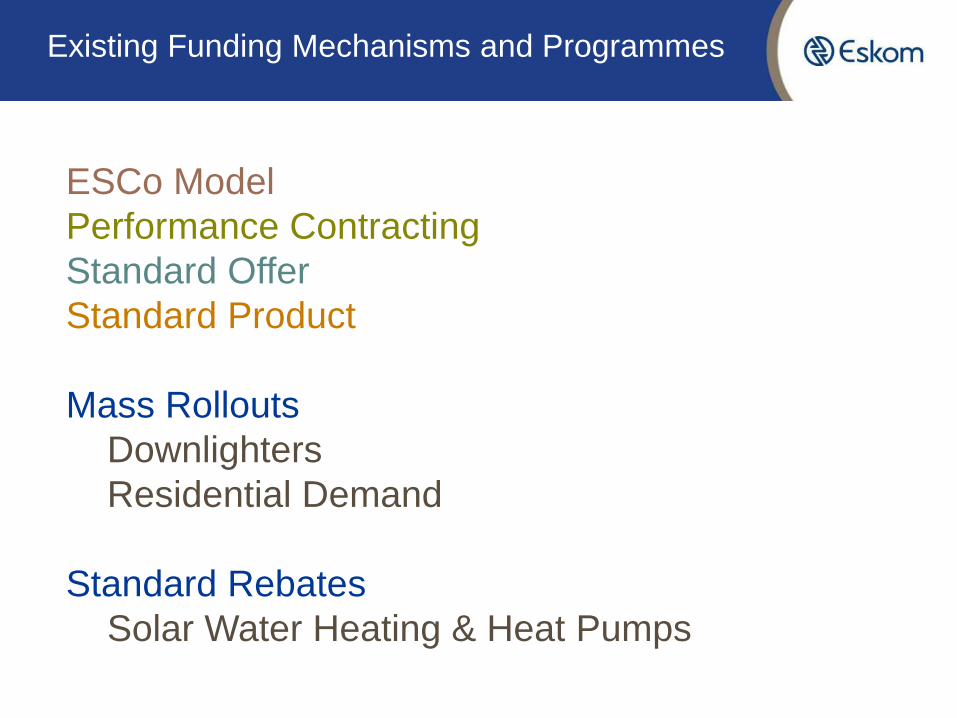

Existing Funding Mechanisms and Programmes

ESCo Model

Performance Contracting

Standard Offer

Standard Product

Mass Rollouts

Downlighters

Residential Demand

Standard Rebates

Solar Water Heating & Heat Pumps

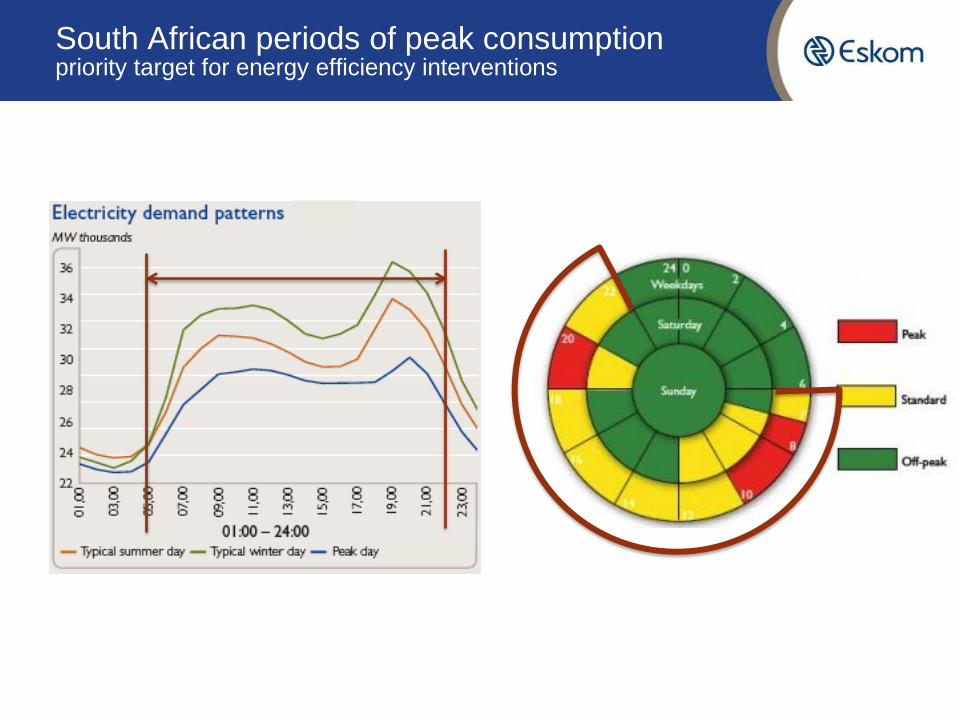

South African periods of peak consumption priority target for energy efficiency interventions

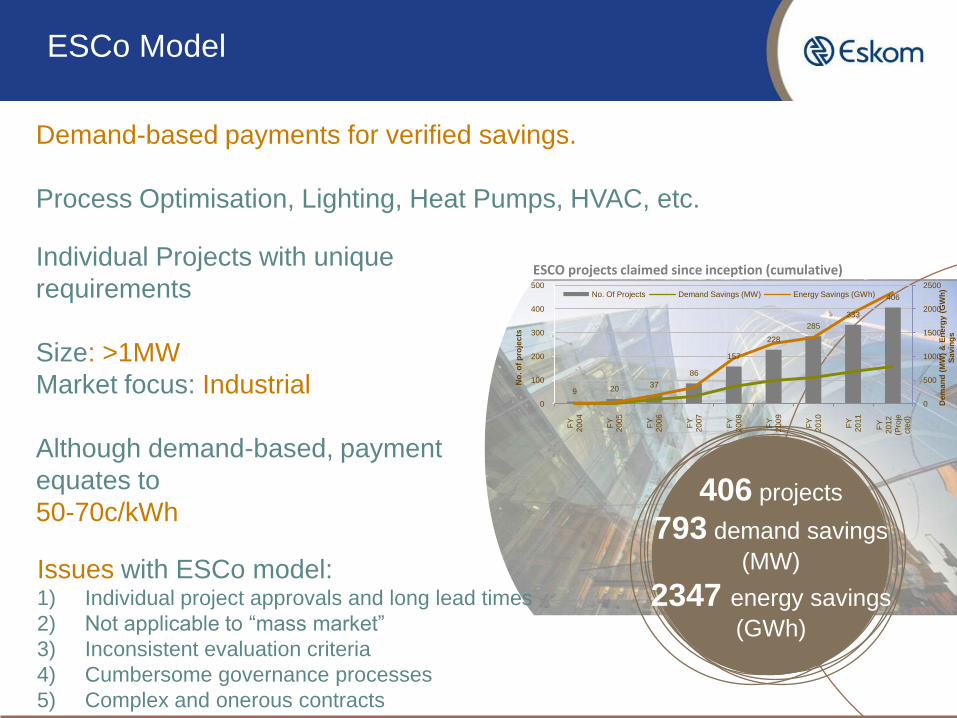

ESCo Model

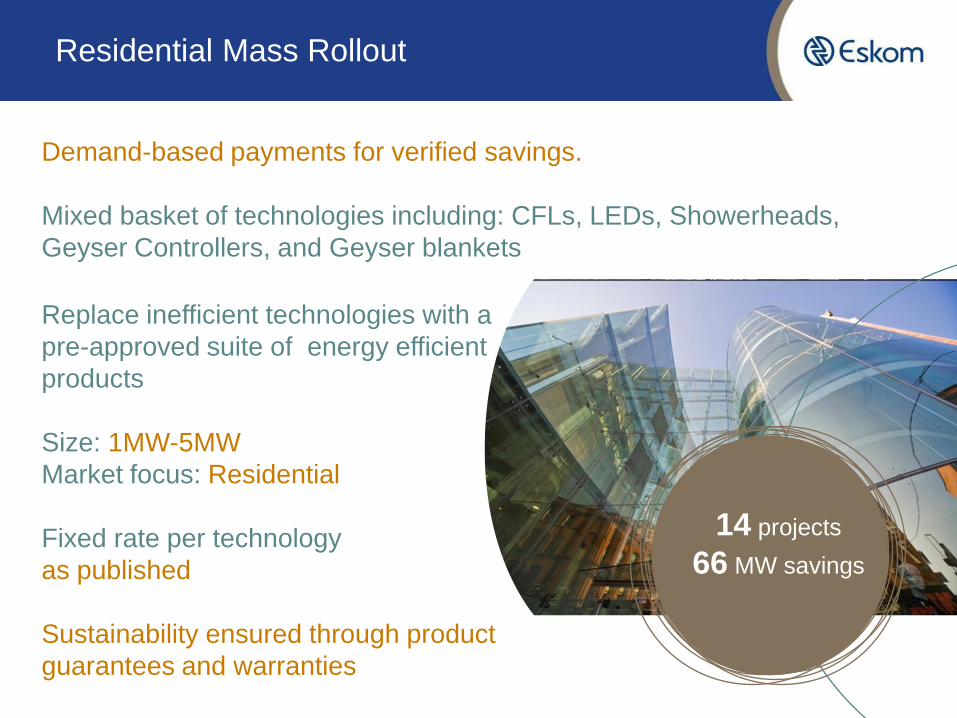

Demand-based payments for verified savings.

Process Optimisation, Lighting, Heat Pumps, HVAC, etc.

Individual Projects with unique

requirements

Size: >1MW

Market focus: Industrial

Although demand-based, payment

equates to

50-70c/kWh

9 2037

86

157

228

285

333

406

0

500

1000

1500

2000

2500

0

100

200

300

400

500

FY

2

00

4

FY

2

00

5

FY

2

00

6

FY

2

00

7

FY

2

00

8

FY

2

00

9

FY

2

01

0

FY

2

01

1

FY

2

01

2

(Pro

jecte

d)

Dem

an

d (

MW

) &

En

erg

y (

GW

h)

Sa

vin

gs

No

. o

f p

roje

cts

No. Of Projects Demand Savings (MW) Energy Savings (GWh)

ESCO projects claimed since inception (cumulative)

406 projects

793 demand savings

(MW)

2347 energy savings

(GWh)

Issues with ESCo model:1) Individual project approvals and long lead times

2) Not applicable to “mass market”

3) Inconsistent evaluation criteria

4) Cumbersome governance processes

5) Complex and onerous contracts

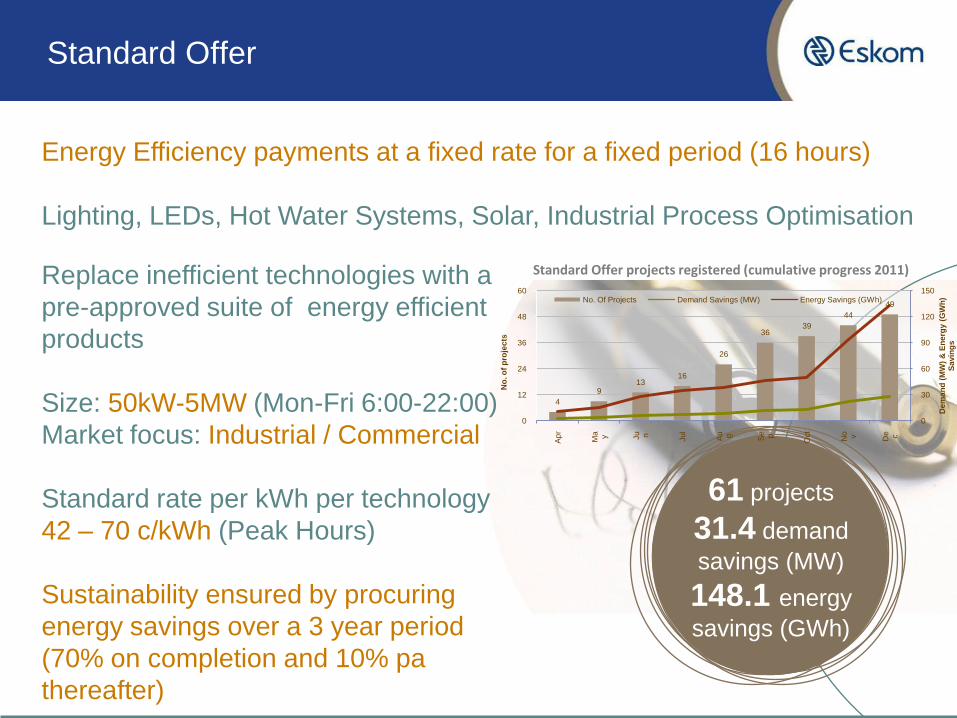

Standard Offer

Replace inefficient technologies with a

pre-approved suite of energy efficient

products

Size: 50kW-5MW (Mon-Fri 6:00-22:00)

Market focus: Industrial / Commercial

Standard rate per kWh per technology

42 – 70 c/kWh (Peak Hours)

Sustainability ensured by procuring

energy savings over a 3 year period

(70% on completion and 10% pa

thereafter)

Energy Efficiency payments at a fixed rate for a fixed period (16 hours)

Lighting, LEDs, Hot Water Systems, Solar, Industrial Process Optimisation

Standard Offer projects registered (cumulative progress 2011)

61 projects

31.4 demand

savings (MW)

148.1 energy

savings (GWh)

4

913

16

26

3639

44

49

0

30

60

90

120

150

0

12

24

36

48

60

Ap

r

Ma y Ju n

Ju

l

Au g Se p

Oct

No v De c

Dem

an

d (

MW

) &

En

erg

y (

GW

h)

Sa

vin

gs

No

. o

f p

roje

cts

No. Of Projects Demand Savings (MW) Energy Savings (GWh)

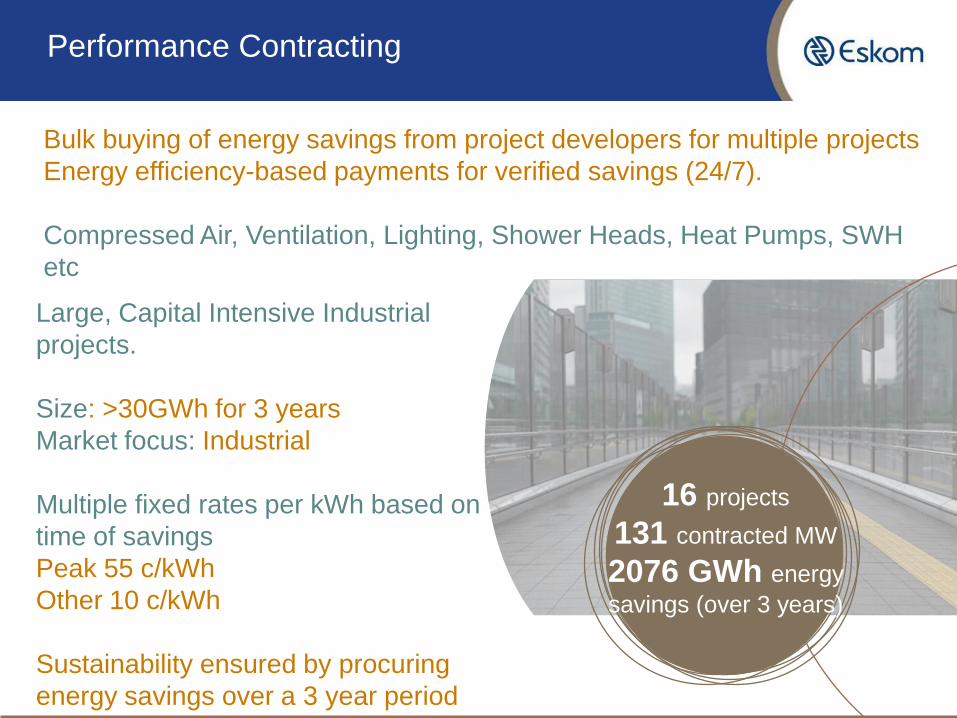

Performance Contracting

Bulk buying of energy savings from project developers for multiple projects

Energy efficiency-based payments for verified savings (24/7).

Compressed Air, Ventilation, Lighting, Shower Heads, Heat Pumps, SWH

etc

Large, Capital Intensive Industrial

projects.

Size: >30GWh for 3 years

Market focus: Industrial

Multiple fixed rates per kWh based on

time of savings

Peak 55 c/kWh

Other 10 c/kWh

Sustainability ensured by procuring

energy savings over a 3 year period

16 projects

131 contracted MW

2076 GWh energy

savings (over 3 years)

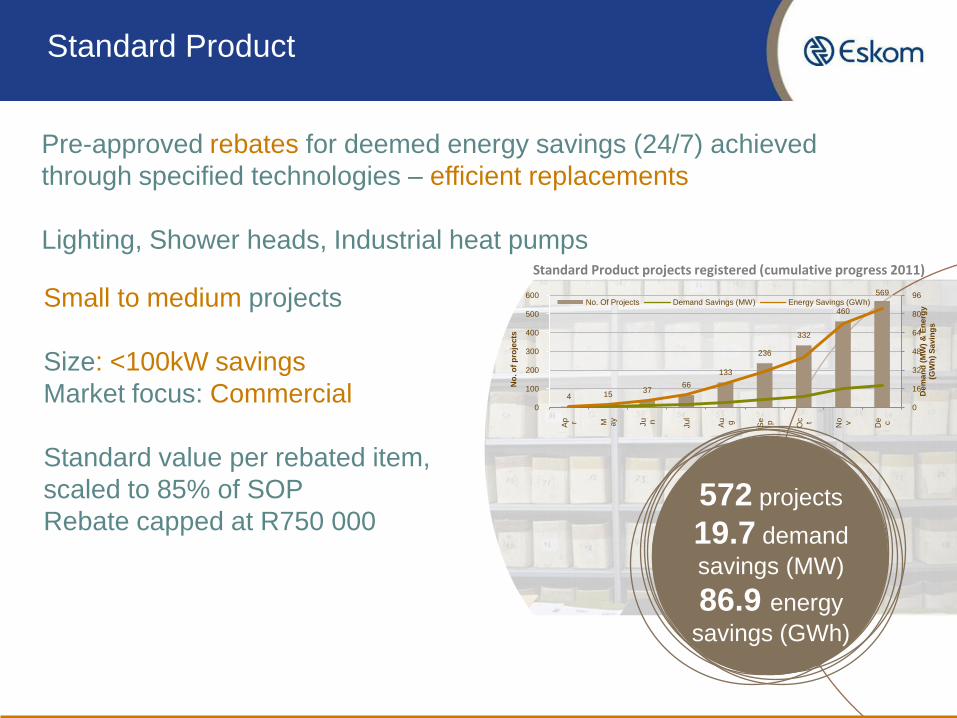

Standard Product

Small to medium projects

Size: <100kW savings

Market focus: Commercial

Standard value per rebated item,

scaled to 85% of SOP

Rebate capped at R750 000

Pre-approved rebates for deemed energy savings (24/7) achieved

through specified technologies – efficient replacements

Lighting, Shower heads, Industrial heat pumpsStandard Product projects registered (cumulative progress 2011)

572 projects

19.7 demand

savings (MW)

86.9 energy

savings (GWh)

4 1537

66

133

236

332

460

569

0

16

32

48

64

80

96

0

100

200

300

400

500

600

Ap r M ay

Ju n

Ju

l

Au g Se p Oc t

No v De c

Dem

an

d (

MW

) &

En

erg

y

(GW

h)

Sa

vin

gs

No

. o

f p

roje

cts

No. Of Projects Demand Savings (MW) Energy Savings (GWh)

Residential Mass Rollout

Replace inefficient technologies with a

pre-approved suite of energy efficient

products

Size: 1MW-5MW

Market focus: Residential

Fixed rate per technology

as published

Sustainability ensured through product

guarantees and warranties

Demand-based payments for verified savings.

Mixed basket of technologies including: CFLs, LEDs, Showerheads,

Geyser Controllers, and Geyser blankets

14 projects

66 MW savings

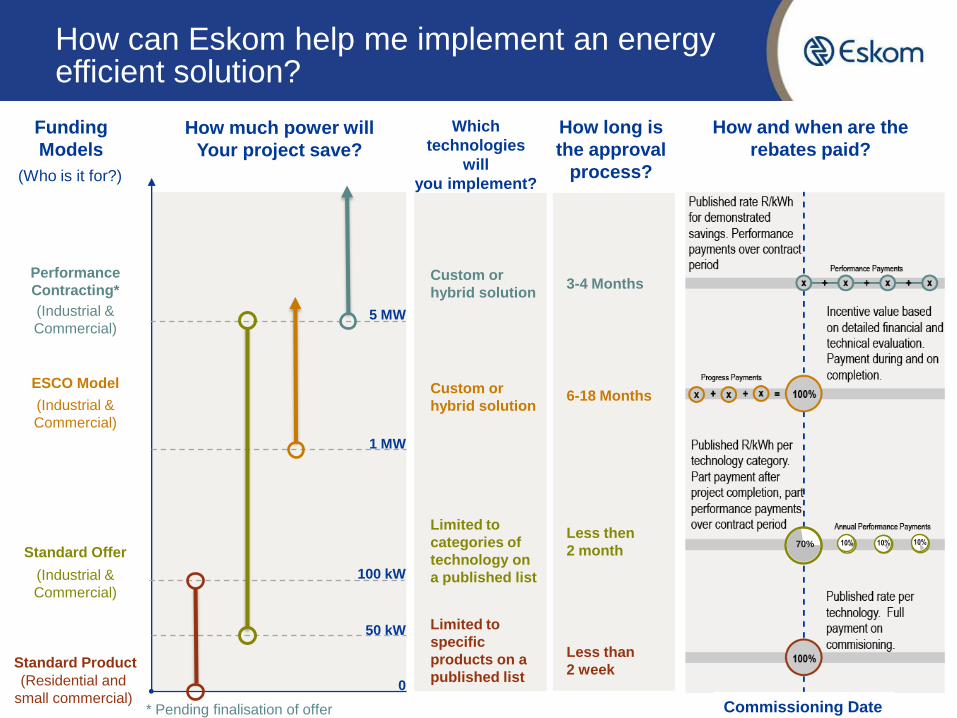

How can Eskom help me implement an energy efficient solution?

3-4 Months

6-18 Months

Less then

2 month

Less than

2 week

* Pending finalisation of offer

Custom or

hybrid solution

Custom or

hybrid solution

Limited to

categories of

technology on

a published list

Limited to

specific

products on a

published list

Performance

Contracting*

ESCO Model

Standard Offer

Standard Product

Funding

Models

How much power will

Your project save?

Which

technologies

will

you implement?

How long is

the approval

process?

How and when are the

rebates paid?

5 MW

1 MW

100 kW

50 kW

0

(Who is it for?)

(Industrial &

Commercial)

(Industrial &

Commercial)

(Residential and

small commercial)

(Industrial &

Commercial)

70% 10% 10% 10%

Commissioning Date

CFL and sustainability

47 million CFLs

fitted across SA (from

2004 – 2011)

1958MW savings

Bulk purchase and issuing of free efficient lamps to households that are

distributed door-to-door or at exchange points.

Replace inefficient, incandescent

lamps with an equivalent,

efficient compact fluorescent

lamp.

Market focus: Residential

Complete project cost (including

lamp procurement and project

implementation activities)

covered to enable free issue.

Carbon revenue used to assist

with project financing.

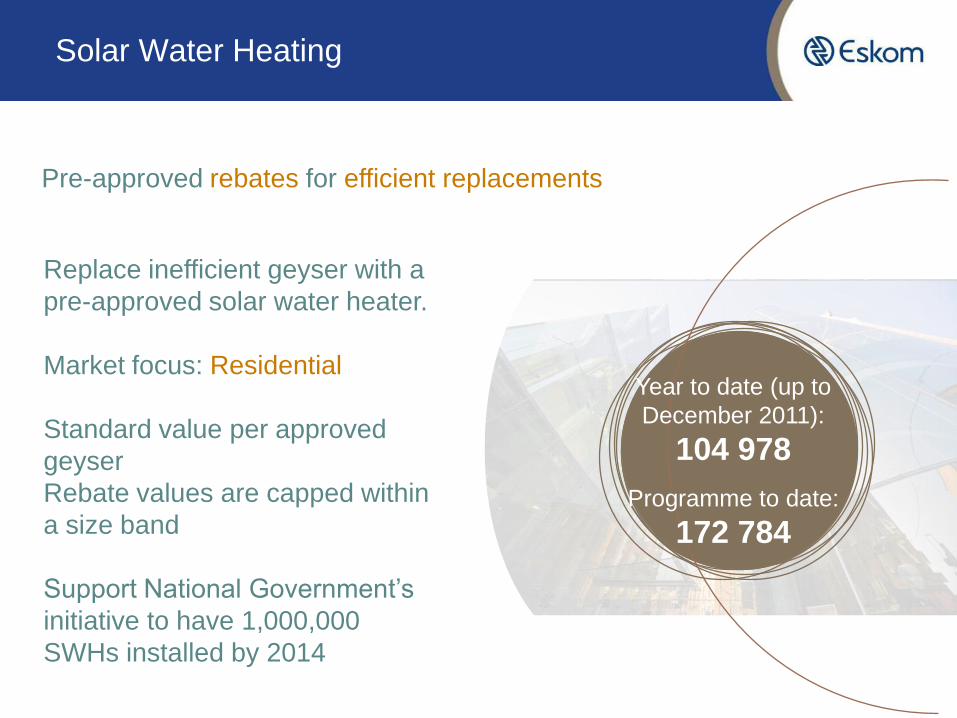

Solar Water Heating

Pre-approved rebates for efficient replacements

Replace inefficient geyser with a

pre-approved solar water heater.

Market focus: Residential

Standard value per approved

geyser

Rebate values are capped within

a size band

Support National Government’s

initiative to have 1,000,000

SWHs installed by 2014

Year to date (up to

December 2011):

104 978

Programme to date:

172 784

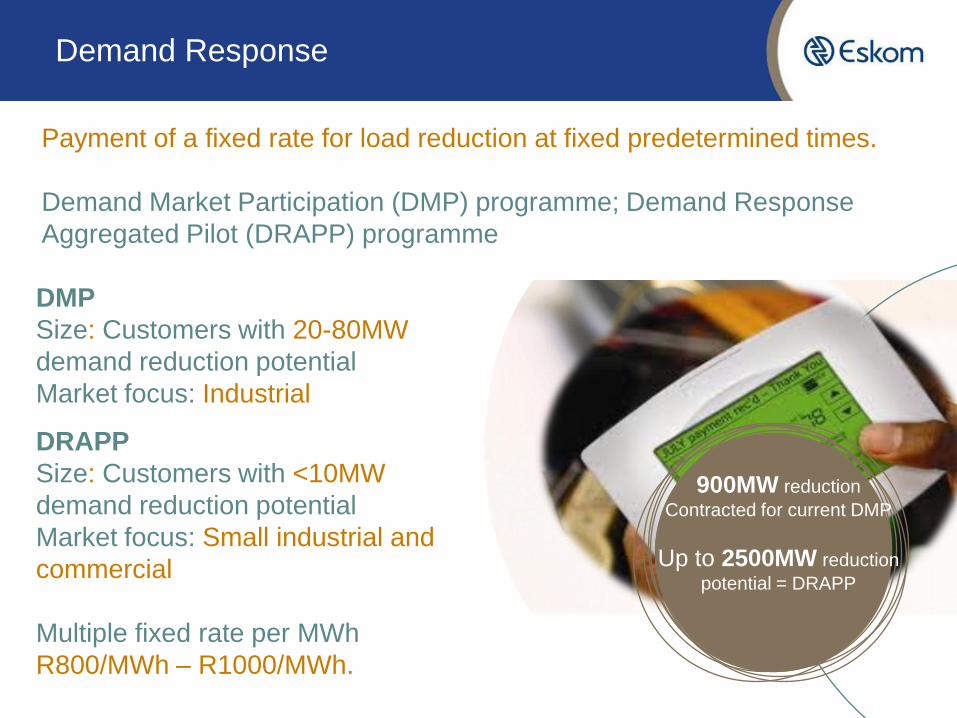

Demand Response

900MW reduction

Contracted for current DMP

Up to 2500MW reduction

potential = DRAPP

Payment of a fixed rate for load reduction at fixed predetermined times.

Demand Market Participation (DMP) programme; Demand Response

Aggregated Pilot (DRAPP) programme

DMP

Size: Customers with 20-80MW

demand reduction potential

Market focus: Industrial

DRAPP

Size: Customers with <10MW

demand reduction potential

Market focus: Small industrial and

commercial

Multiple fixed rate per MWh

R800/MWh – R1000/MWh.

Industrial Commercial / Agricultural Residential

ESCO

Performance Contracting

Standard Offer

Standard Product

Downlighters Mass

Roll-out

Residential Mass Roll-out

SWH / HP Rebate

Other Mass Rollout

Current Solutions

TECHNOLOGY

KEY:

PRIORITY 1PRIORITY 2Priority 3

Compressed Air, Ventilation, Lighting, Shower Heads,

Heat Pumps, SWH, etc.

Process Optimisation, Lighting

Heat Pumps, HVAC etc.

Energy

Solutions

Demand

Solutions

Lighting, Hot Water Systems,

Solar , Process Optimisation

Lighting, Shower Heads,

Industrial Heat Pumps

LED Downlighters, & CFL

downlighters

HP & LP Solar Water

Heaters, Heat Pumps

CFL Sustainability and

Fill-ins

Focus on Industrial Market,

catering for individual projects with

unique requirements

Target industrial, large

capital projects to increase

commitment and reduce risk

of non-delivery

• Extend into industrial

market

• Adjust pricing to

increase uptake

Incorporate into SO

to rationalise

solutions in

Commercial market

Residential “Mixed

Bag” of technologies

LESSONS LEARNED

Some observations and thing we need to improve on

Lessons learned notes

• Legislative, Policy and Regulatory Issues

– Unpredictability of timing/outcome results in high risk to solutions where these processes

are key dependencies

– Potential misalignment of anticipated legislative and policy environment with evolving

incentive structures

– NERSA 2004 policy focuses mainly on a demand related problem, rather than the current

energy shortage

– Challenges to amend Eskom’s NERSA mandate to include key market opportunities such

as small scale renewables, greenfields projects, waste heat recovery and fuel switching

– Complexities in national government governance framework (Policy Department,

“Shareholder” and Treasury)

– Lack of clarity on the role of Eskom with respect to EEDSM impacts the ability to enter

into long term financial commitment beyond the MYPD2 period

– Industry structure and implication to municipal finances

• Strategy

– Insufficient strategic framework due to speed of implementation

– Too many incentive options resulting in movement of customer uptake between offerings,

resulting in implications to ESCO’s

– Challenges to ensure uniqueness of marketing offers, with effective pricing structures and

levels

Lessons learned notes

• Operational

– Sound, project managed, multi-functional implementation approach required

– Need for optimisation and automation of business processes, systems and controls,

specifically in the transition to focus more on the Commercial and Residential markets

– Training of staff and advisors on complexities of multiples incentives essential

• ESCO Related issue

– Slow transformation in the ability to contract on performance basis

– Challenges to raise capital for performance based projects

– Small number of large ESCOs gain from lucrative opportunities

– Large number of small, mostly inactive ESCOs will require unique solutions to support

ESCO development

– Government and Eskom requirements in terms of SD&L, BBBEE, cidb, LOA’s etc.

impacting ESCO participation

• Market – Need for effective marketing and communication of incentives

– Fixed pricing more successful than tendering

– Need to manage the unintended consequences if an increasingly volatile market

• Never underestimate the bureaucracy

FUTUREEmerging and Future Focus

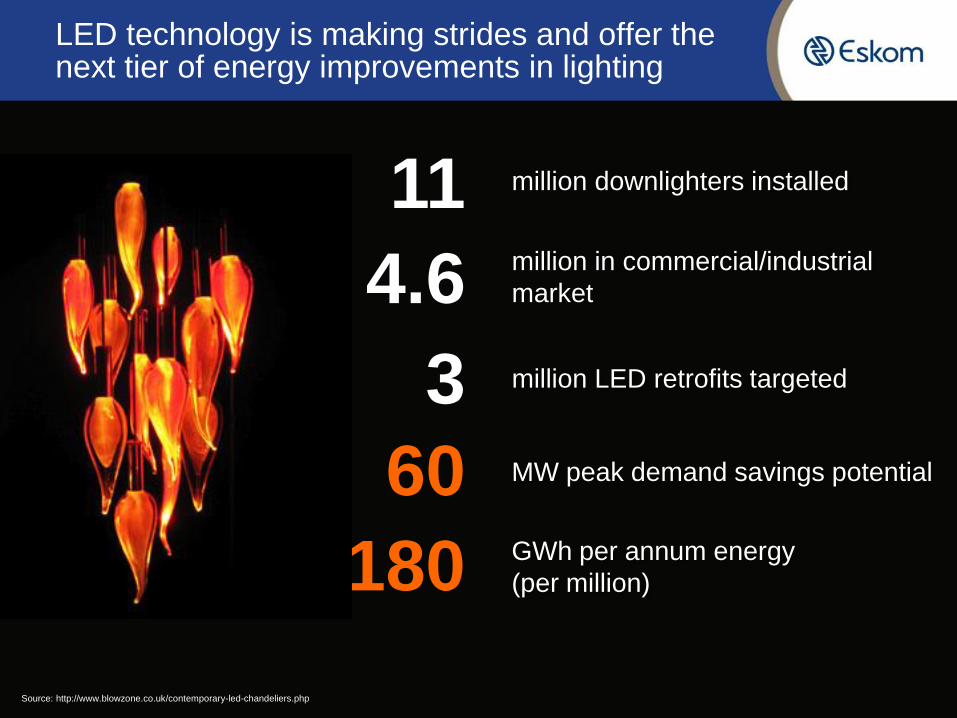

LED technology is making strides and offer the next tier of energy improvements in lighting

36

3

4.6

11

180

60

million downlighters installed

million in commercial/industrial

market

million LED retrofits targeted

MW peak demand savings potential

GWh per annum energy

(per million)

Source: http://www.blowzone.co.uk/contemporary-led-chandeliers.php

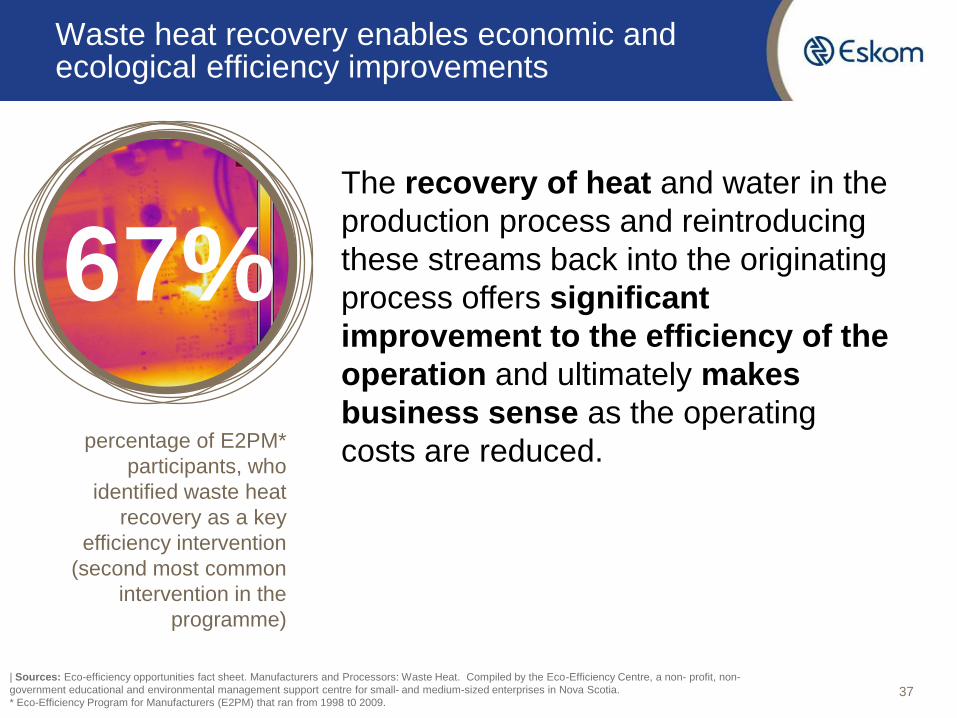

Waste heat recovery enables economic and ecological efficiency improvements

37

67%The recovery of heat and water in the

production process and reintroducing

these streams back into the originating

process offers significant

improvement to the efficiency of the

operation and ultimately makes

business sense as the operating

costs are reduced.

| Sources: Eco-efficiency opportunities fact sheet. Manufacturers and Processors: Waste Heat. Compiled by the Eco-Efficiency Centre, a non- profit, non-

government educational and environmental management support centre for small- and medium-sized enterprises in Nova Scotia.

* Eco-Efficiency Program for Manufacturers (E2PM) that ran from 1998 t0 2009.

percentage of E2PM*

participants, who

identified waste heat

recovery as a key

efficiency intervention

(second most common

intervention in the

programme)

Energy efficiency and renewable energy are key components of zero energy facilities

38

Formal commitments are being

made globally to pursue zero

energy goals.

This requires a combination of

energy efficiency and small-scale

renewable energy interventions.

Accordingly several initiatives,

including India’s Ministry of Power

and Canada’s Clean Air Partnership,

have broadened their definitions of

DSM to incorporate

green/renewable energy.

Eskom IDM, in consultation with

NERSA, is hoping to follow suit.

Supplier development & localisationA development imperative in South Africa

http://bee.thedti.gov.za/

http://www.eskom.co.za/c/61/eskom-purchasing-

policies/

http://www.eskom.co.za/c/63/supplier-criteria/

The South African Government is committed to job creation, economic

development (with specific priority to the development of green industry) and

aims to promote economic transformation in order to enable meaningful

participation of black South Africans in the economy. It is important to note that

these priorities have been incorporated into the procurement policies for the

country. Details area available from:

40

Government’s large scale renewable energy procurement programme

41

The South Africa’s Integrated Resource Plan (IRP) for electricity envisages

that independent power producers (IPPs) and State utility Eskom will build a

combined renewables base of 17,800 MW by 2030.

During August 2011, the South African Government took the first step in this

multidecade clean-energy investment programme by inviting tenders for

3,725 MW of renewable capacity to be developed by independent power

producers.

53 bids, representing some 2,100 MW of potential capacity, were received by

the DoE during this first bidding window. On 7 December 2011 the DOE

announced the first 28 successful renewable bidders for a total of 1,415.5

MW capacity. The preferred bidders named included 18 solar photovoltaic

(PV) projects, eight onshore wind projects and two concentrated solar power

(CSP) projects.

This round of tenders was the first of potentially 5 bidding windows. The

second bidding window is currently due to close on March 5, 2012.

Energy Efficiency Tax Incentive

42

The Department of Energy published draft regulations on the allowance for

energy efficiency savings* for public comment on 16 September 2011.

The Regulation is currently being revised to incorporate comments and recent

changes in the energy policy landscape (most notably the cancellation of the

REFIT which formed the basis for the calculation of the energy efficiency

allowance).

An ambitious target date for the revised Regulations to be published and

implemented has been set for April 2012.

Under section 19 of the National Energy Act, 2008 (Act No. 34 of 2008), read with section 12L of the Income Tax Act, 1962 (Act No. 58 of 1962)*