Embed Size (px)

Citation preview

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

An Open Economy

Christina Zauner

Department of Economics, University of Vienna

June 8th, 2011

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Introduction

I For simplicity, we have so far assumed that theeconomy under consideration is closed, i.e. there are nointeractions with the rest of the world

I Now we relax this assumption, in particular we willassume that consumers can buy domestic or foreigngoods and investors can buy domestic or foreign assets

I This openness has important implications for thedomestic economy, in particular on output and thesavings-investment relation

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

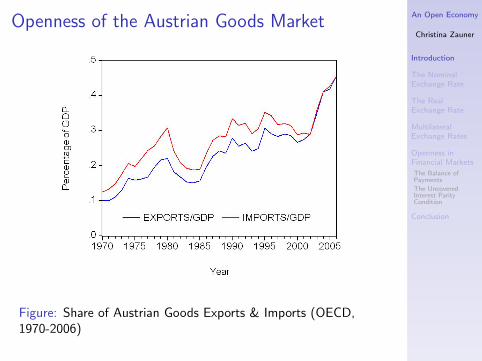

Openness of the Austrian Goods Market

Figure: Share of Austrian Goods Exports & Imports (OECD,1970-2006)

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Openness in Goods Market

I In an open economy consumers face aconsumption-savings decision AND they have to decidewhether to buy domestic or foreign goods (or both)

I Their decision has important implications: e.g. if theybuy more foreign goods, foreign output, instead ofdomestic output, increases

I The decision is mainly based on the price of domesticgoods in terms of foreign goods, i.e. the real exchangerate

I The latter is not directly observable but we canconstruct it from the nominal exchange rate

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Nominal Exchange RateQuotation

There are two ways to quote the nominal exchange rate E

I the price of domestic currency in terms of foreigncurrency (e.g. price of one Euro in terms of U.S.Dollars; USD/EUR)

I the price of foreign currency in terms of domesticcurrency (e.g. price of one U.S. Dollar in terms ofEuros; EUR/USD)

We will always use the first definition: A nominal exchangerate between the USD and the Euro of E = 1.2644 impliesthat you have to give up 1.2644 U.S. Dollars to buy one Euro

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Nominal Exchange RateAppreciation and Depreciation

I Appreciation: an increase in the price of domesticcurrency in terms of foreign currency (E ↑), i.e. moreforeign currency is needed to buy one unit of thedomestic currency

I Depreciation: a decrease in the price of domesticcurrency in terms of foreign currency (E ↓), i.e. lessforeign currency is needed to buy one unit of thedomestic currency

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

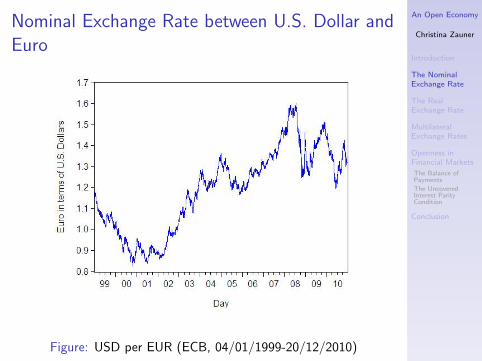

Nominal Exchange Rate between U.S. Dollar andEuro

Figure: USD per EUR (ECB, 04/01/1999-20/12/2010)

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Real Exchange RateMotivation

I The nominal exchange rate only tells the consumer howmany units of foreign currency he gets for domesticcurrency

I It does not tell him how many goods he can buy withthe foreign currency compared to how many goods hecan buy with the domestic currency

I Therefore consumers also have to take into accountdomestic and foreign prices

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Real Exchange RateCalculation

I An Austrian consumer wants to buy a “basket ofgoods” (either in Austria or from the U.S.)

I The price of the Austrian goods basket is EUR P; a(comparable) U.S. basket costs USD P∗; the nominalexchange rate is E

I The product EP gives the price of the Austrian goodsbasket in terms of U.S. Dollars

I Dividing this product by P∗ yields the price of theAustrian goods basket in terms of U.S. goods baskets,i.e. the real exchange rate:

ε ≡ EP

P∗

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Real Exchange RateExample

I The real exchange rate is equal to ε

I The Euro appreciates by 2%, so the new nominalexchange rate is given by E

′= 1.02 · E

I Furthermore, the price of Austrian goods increases by2%, i.e. P

′= 1.02 · P, while the price of U.S. goods

increases by 5%, i.e. P∗′= 1.05 · P∗

I For one Euro a consumer now gets 2% more U.S.Dollars, but the inflation rate in Austria is smaller thanin the U.S.; should the consumer now buy Austriangoods or U.S. goods.?

I The new real exchange rate is given by ε′

= 0.99 · εI The price of Austrian goods in terms of U.S. goods has

decreased by 1%, i.e. the former are now relativelycheaper

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Real Exchange RateRemarks

I For the construction of the real exchange rate weusually use GDP deflators (cp. Chapter 2)

I Since the latter are mere index numbers, the level of thereal exchange rate is uninformative

I However, as illustrated in the previous example, the rateof change of the real exchange rate is instructive

I An increase in the real exchange rate is called realappreciation, while a decrease is called real depreciation

I A real appreciation/depreciation not necessarily dependson E , but can also be caused by a change in P or P∗

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

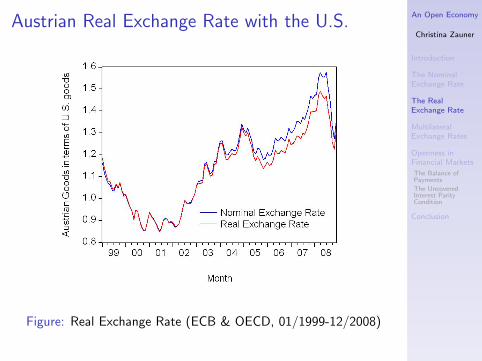

Austrian Real Exchange Rate with the U.S.

Figure: Real Exchange Rate (ECB & OECD, 01/1999-12/2008)

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Multilateral Exchange Rate

I The real exchange rate is the price of domestic goods interms of the goods of one particular foreign country

I If we want to know the price of domestic goods interms of foreign goods in general we have to look at theso-called multilateral exchange rate

I The latter is a weighted sum of real exchange rateswhere the shares of trade with different foreigncountries are used as weights

I The multirateral exchange rate (or effective exchangerate) can be used to analyze the competitiveness of acountry and its goods respectively

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

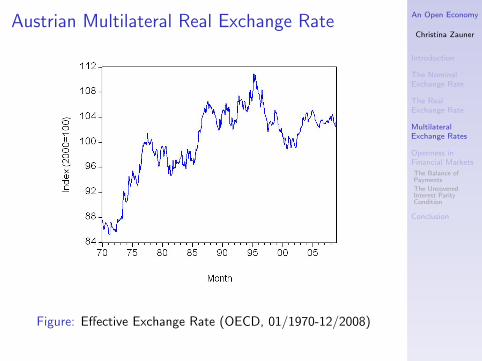

Austrian Multilateral Real Exchange Rate

Figure: Effective Exchange Rate (OECD, 01/1970-12/2008)

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Openness in Financial Markets

I Open financial markets allow investors to hold bothdomestic and foreign assets and they facilitate trade

I Furthermore, open financial markets allow a country torun a trade deficit (or a trade surplus)

I For instance, by borrowing from the rest of the world acountry can finance its trade deficit, i.e. the differencethat arises if the country is buying more from the rest ofthe world than it is selling to the rest of the world

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

The Balance of PaymentsCurrent Account

I The transactions of an economy with the rest of theworld are summarised in the balance of payments(BOP), which consists of the current account (CA) andthe financial account (FA)

I The current account records all payments to and fromthe rest of the world:

1. exports (+) and imports (-) of goods and services2. investment income received (+) and paid (-) (e.g.

dividends on shares, interests on bonds)3. transfers received (+) and paid (-) (e.g. foreign aid)

I The sum of net payments is called current accountbalance; if it is positive (negative), the country isrunning a current account surplus (deficit)

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

The Balance of PaymentsFinancial Account

I A current account deficit implies that a country has toborrow from the rest of the world

I Borrowing in this respect means that foreign holdings ofdomestic assets are larger than domestic holdings offoreign assets, i.e. net capital flows to the country arepositive

I The financial account describes these asset holdings

I Positive (negative) net capital flows are called financialaccount surplus (deficit)

I The current and the financial account balance should inprinciple be the same (with different signs); in realitythere is a statistical discrepancy (due to different datasources)

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Domestic vs. Foreign AssetsMotivation

I In an open economy, investors face the decision whetherto buy domestic or foreign interest-paying assets

I If the investor decides to invest in foreign assets he firsthas to get foreign currency to buy the assets and thenhas to exchange the returns on the asset (which arepaid out in the foreign currency) back into his domesticcurrency

I Therefore, his decision in which asset to invest will notonly be influenced by the respective interest rates butalso by the nominal exchange rate at the time of thepurchase and the expected exchange rate at thematurity date of the asset

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Domestic vs. Foreign AssetsExample

I An Austrian investor wants to invest one Euro, either inone year Austrian bonds or one year U.S. bonds

I If the nominal interest rate on Austrian bonds in year tequals it then in t + 1 the investor gets (1 + it) Euros

I If the investor buys U.S. bonds he first has to buy U.S.Dollars; for one Euro he gets Et U.S. Dollars

I If the nominal interest rate on U.S. bonds in year tequals i∗t then in t + 1 the investor gets Et(1 + i∗t ) U.S.Dollars

I The investor then has to convert these U.S. Dollars intoEuros; if the expected nominal exchange rate equalsE e

t+1, his expected return is [Et(1 + i∗t )]/E et+1 Euros

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

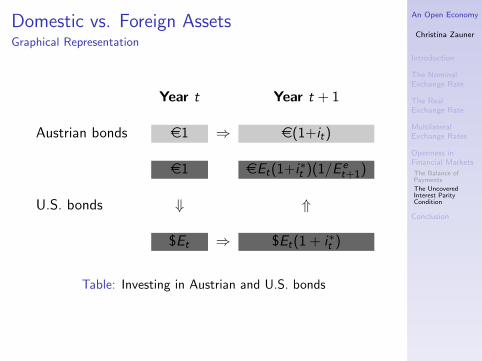

Domestic vs. Foreign AssetsGraphical Representation

Year t Year t + 1

Austrian bonds e1 ⇒ e(1+it)

e1 eEt(1+i∗t )(1/E et+1)

U.S. bonds ⇓ ⇑

$Et ⇒ $Et(1 + i∗t )

Table: Investing in Austrian and U.S. bonds

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

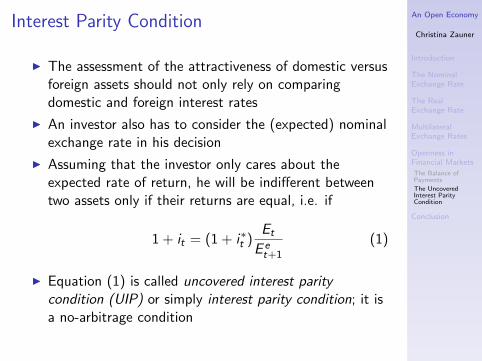

Interest Parity Condition

I The assessment of the attractiveness of domestic versusforeign assets should not only rely on comparingdomestic and foreign interest rates

I An investor also has to consider the (expected) nominalexchange rate in his decision

I Assuming that the investor only cares about theexpected rate of return, he will be indifferent betweentwo assets only if their returns are equal, i.e. if

1 + it = (1 + i∗t )Et

E et+1

(1)

I Equation (1) is called uncovered interest paritycondition (UIP) or simply interest parity condition; it isa no-arbitrage condition

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

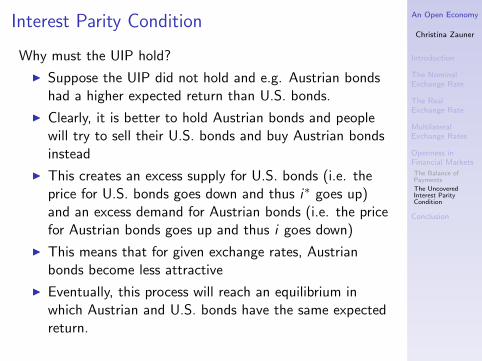

Interest Parity Condition

Why must the UIP hold?

I Suppose the UIP did not hold and e.g. Austrian bondshad a higher expected return than U.S. bonds.

I Clearly, it is better to hold Austrian bonds and peoplewill try to sell their U.S. bonds and buy Austrian bondsinstead

I This creates an excess supply for U.S. bonds (i.e. theprice for U.S. bonds goes down and thus i∗ goes up)and an excess demand for Austrian bonds (i.e. the pricefor Austrian bonds goes up and thus i goes down)

I This means that for given exchange rates, Austrianbonds become less attractive

I Eventually, this process will reach an equilibrium inwhich Austrian and U.S. bonds have the same expectedreturn.

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

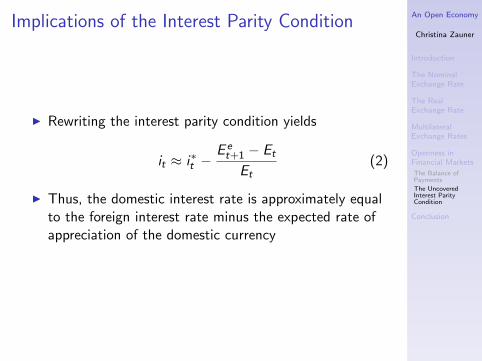

Implications of the Interest Parity Condition

I Rewriting the interest parity condition yields

it ≈ i∗t −E e

t+1 − Et

Et(2)

I Thus, the domestic interest rate is approximately equalto the foreign interest rate minus the expected rate ofappreciation of the domestic currency

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

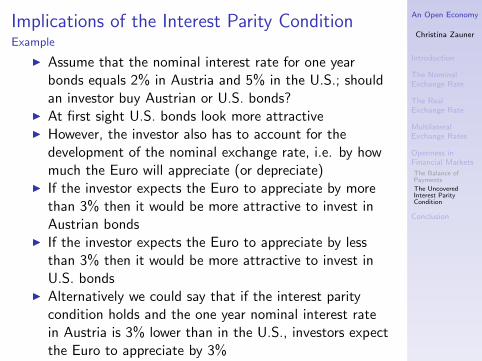

Implications of the Interest Parity ConditionExample

I Assume that the nominal interest rate for one yearbonds equals 2% in Austria and 5% in the U.S.; shouldan investor buy Austrian or U.S. bonds?

I At first sight U.S. bonds look more attractiveI However, the investor also has to account for the

development of the nominal exchange rate, i.e. by howmuch the Euro will appreciate (or depreciate)

I If the investor expects the Euro to appreciate by morethan 3% then it would be more attractive to invest inAustrian bonds

I If the investor expects the Euro to appreciate by lessthan 3% then it would be more attractive to invest inU.S. bonds

I Alternatively we could say that if the interest paritycondition holds and the one year nominal interest ratein Austria is 3% lower than in the U.S., investors expectthe Euro to appreciate by 3%

An Open Economy

Christina Zauner

Introduction

The NominalExchange Rate

The RealExchange Rate

MultilateralExchange Rates

Openness inFinancial Markets

The Balance ofPayments

The UncoveredInterest ParityCondition

Conclusion

Summary

I Openness in goods markets allows consumers to choosebetween domestic and foreign goods

I Their choice primarily depends on the real exchangerate, i.e. the price of domestic goods in terms of foreigngoods

I Openness in financial markets allows investors to choosebetween domestic and foreign assets

I Their choice primarily depends on the expected rates ofreturn of these assets, which depend on domestic andforeign interest rates as well as on the current and theexpected nominal exchange rate