Embed Size (px)

Citation preview

O l k f C l fO l k f C l fAn Outlook for California An Outlook for California Specialty CropsSpecialty Crops in the Global in the Global

EEp y pp y p

EconomyEconomy

March 1, 2010March 1, 2010

William A. MatthewsU i i f C lif i A i l l I C dUniversity of California Agricultural Issues Center and

Agricultural and Resource Economics, UC, Davis

Export of California agriculture.p g

Current and future projections ofCurrent and future projections of the global economy.

Future trade potential for pCalifornia agriculture.

Value of California Exports

Destination for Exports

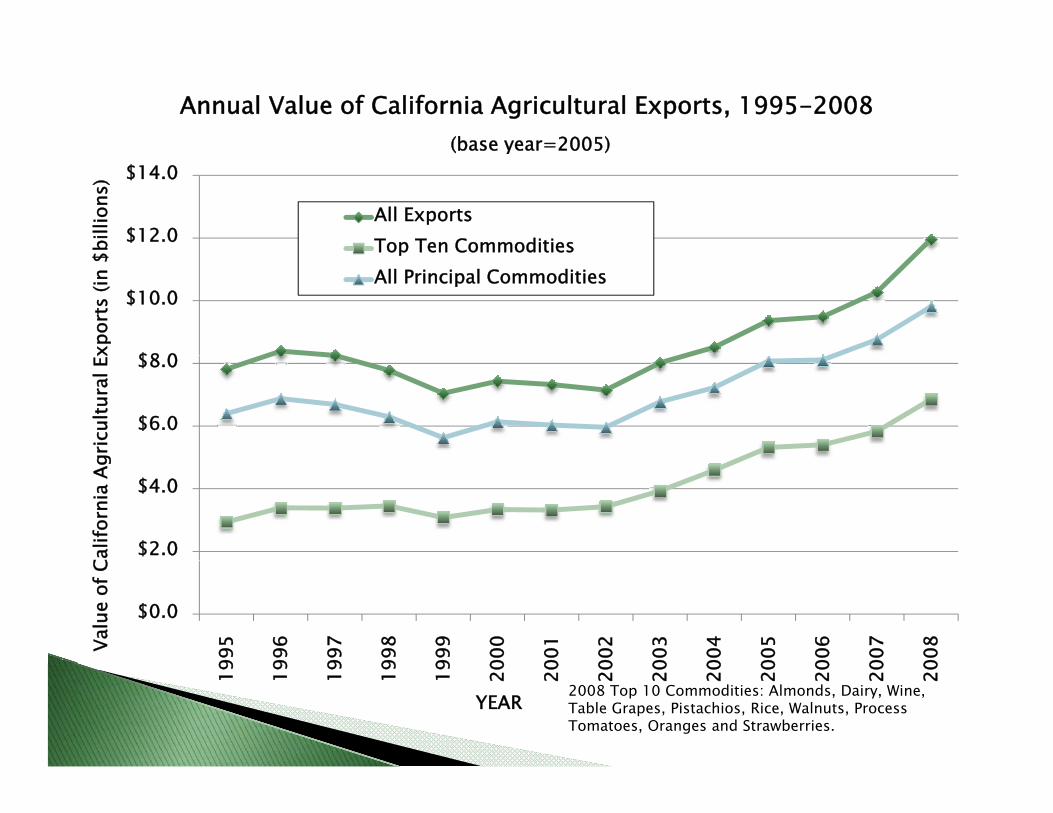

Annual Value of California Agricultural Exports, 1995-2008 (base year=2005)

$12.0

$14.0

billi

ons)

(base year 2005)

All ExportsTop Ten Commodities

$8 0

$10.0

xpor

ts (i

n $ p

All Principal Commodities

$6.0

$8.0

gric

ultu

ral E

x

$2.0

$4.0

Calif

orni

a Ag

$0.0

995

996

997

998

999

000

001

002

003

004

005

006

007

008Va

lue

of C

19 19 19 19 19 20 20 20 20 20 20 20 20 20

YEAR 2008 Top 10 Commodities: Almonds, Dairy, Wine, Table Grapes, Pistachios, Rice, Walnuts, Process Tomatoes, Oranges and Strawberries.

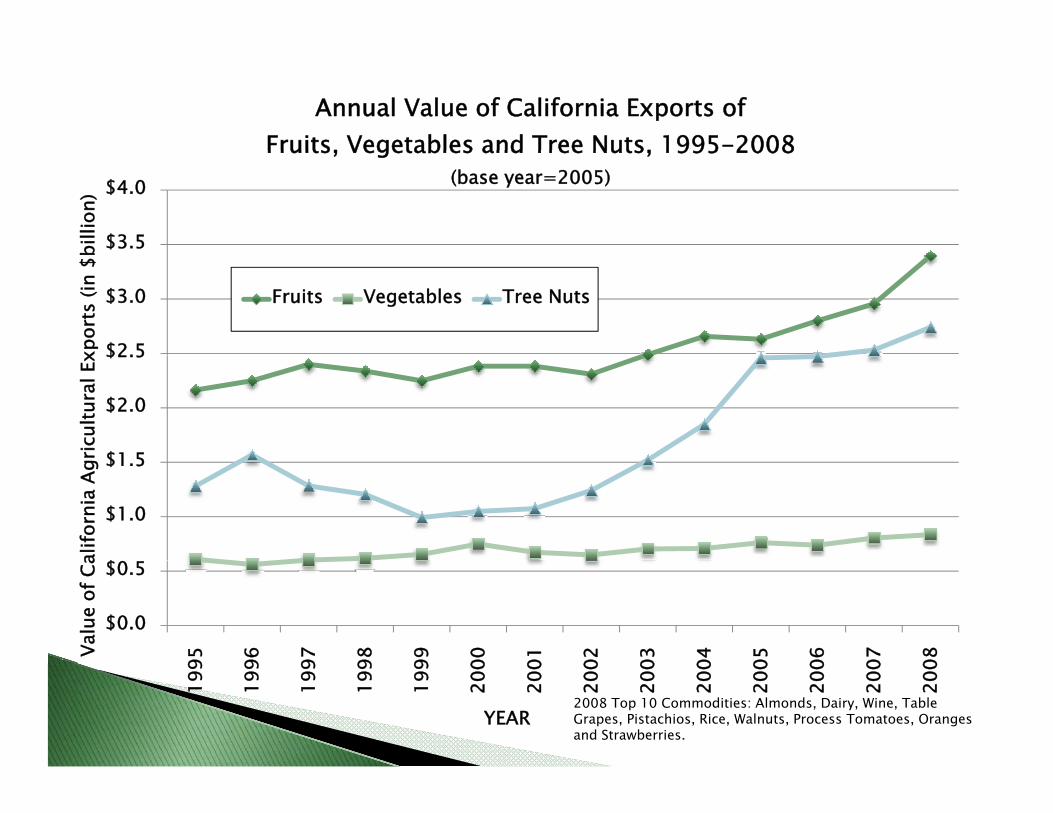

Annual Value of California Exports of Fruits, Vegetables and Tree Nuts, 1995-2008

$3.5

$4.0

billi

on)

Fruits, Vegetables and Tree Nuts, 1995 2008 (base year=2005)

$2.5

$3.0

xpor

ts (i

n $b

Fruits Vegetables Tree Nuts

$1 5

$2.0

$2.5

ricul

tura

l Ex

$

$1.0

$1.5

alifo

rnia

Ag

$0.0

$0.5

95 96 97 98 99 00 01 02 03 04 05 06 07 08

Valu

e of

Ca

199

199

199

199

199

200

200

200

200

200

200

200

200

200

YEAR2008 Top 10 Commodities: Almonds, Dairy, Wine, Table Grapes, Pistachios, Rice, Walnuts, Process Tomatoes, Oranges and Strawberries.

Share of Annual California Tree Nut Export Values by Variety

80%

90%

100%

e

60%

70%

80%

Expo

rt V

alue

40%

50%

f Tre

e N

ut E

20%

30%

Perc

ent o

f

0%

10%

95 96 97 98 99 00 01 02 03 04 05 06 07 08

199

199

199

199

199

200

200

200

200

200

200

200

200

200

YEARAlmonds Pistachios Walnuts

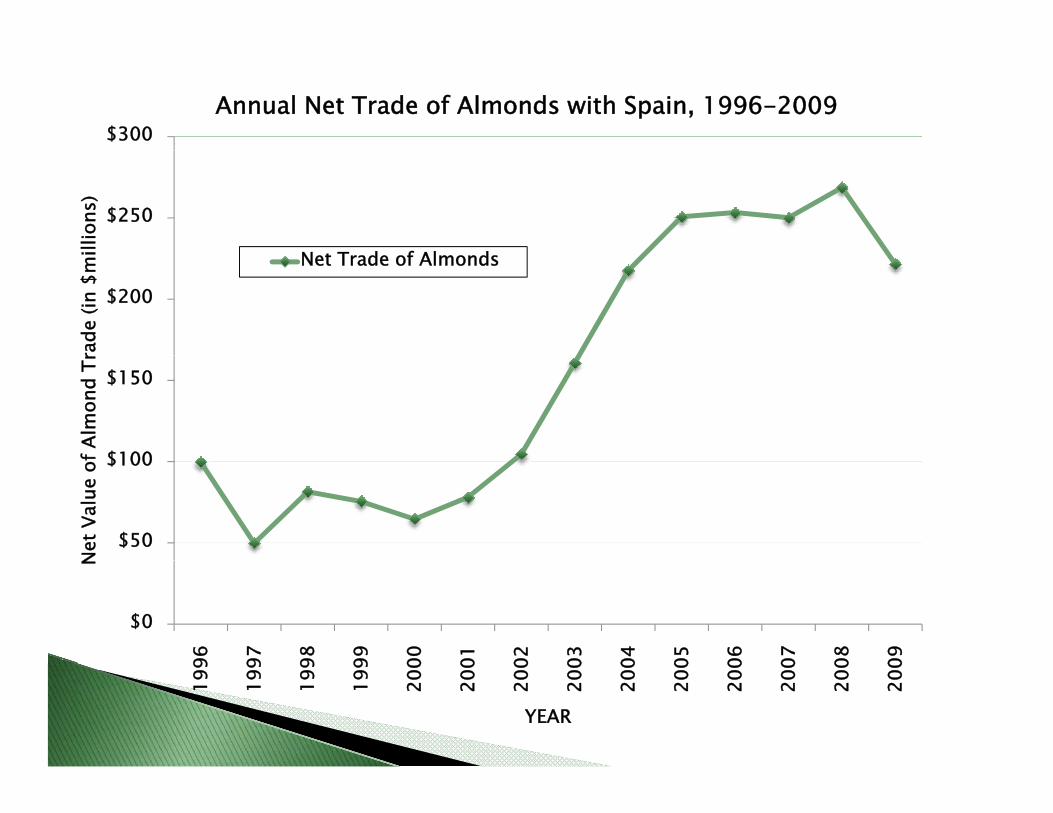

$300Annual Net Trade of Almonds with Spain, 1996-2009

$250

illio

ns)

N T d f Al d

$200

rade

(in

$mi Net Trade of Almonds

$100

$150

f Alm

ond

Tr

$50

$100

Net

Val

ue o

f

$0

96 97 98 99 00 01 02 03 04 05 06 07 08 09

N

199

199

199

199

200

200

200

200

200

200

200

200

200

200

YEAR

$900

Value of California Fruit Exports by Crop, 1995-2008 (base year=2005)

$

$800

$900

mill

ions

)

(base year 2005)

Table Grapes Oranges Strawberries Rasins WIne

$600

$700

port

s (in

$m

$400

$500

nia

Frui

t Exp

$200

$300

e of

Cal

iforn

$0

$100

5 6 7 8 9 0 1 2 3 4 5 6 7 8

Valu

e

199

199

199

199

199

200

200

200

200

200

200

200

200

200

YEAR

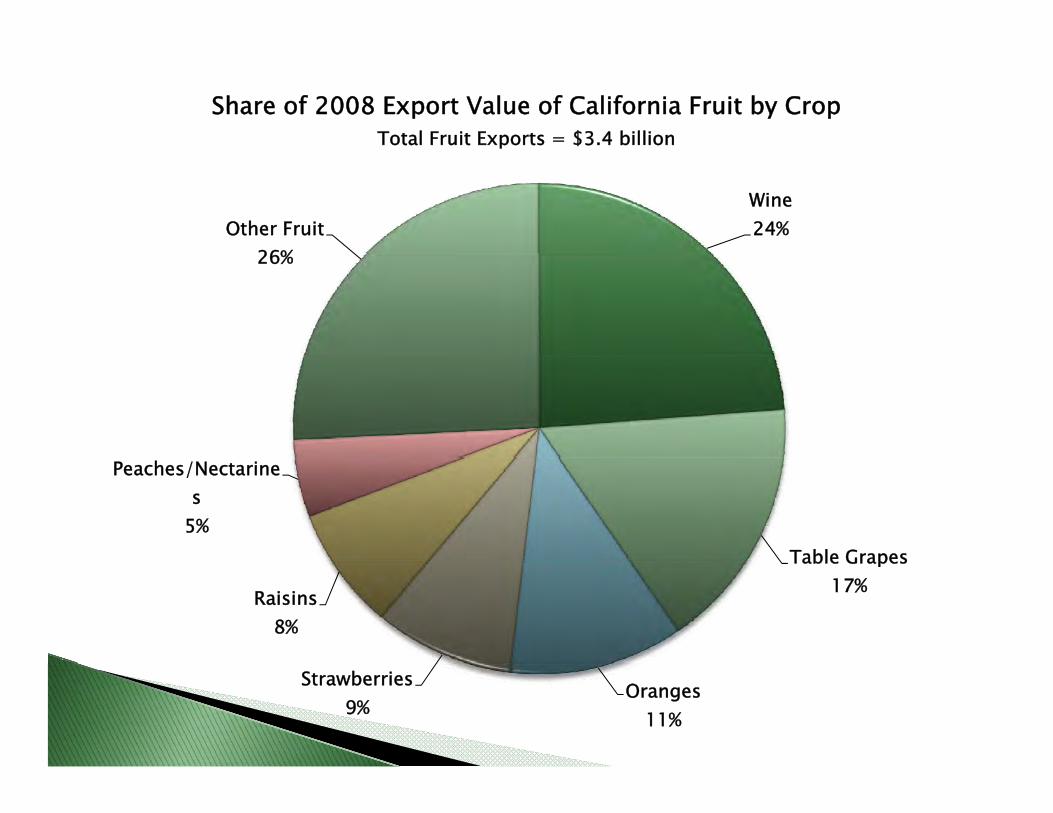

Share of 2008 Export Value of California Fruit by CropTotal Fruit Exports = $3.4 billion

Wine24%Other Fruit

26%26%

Table Grapes

Peaches/Nectarines

5%Table Grapes

17%Raisins8%

Oranges11%

Strawberries9%

$350

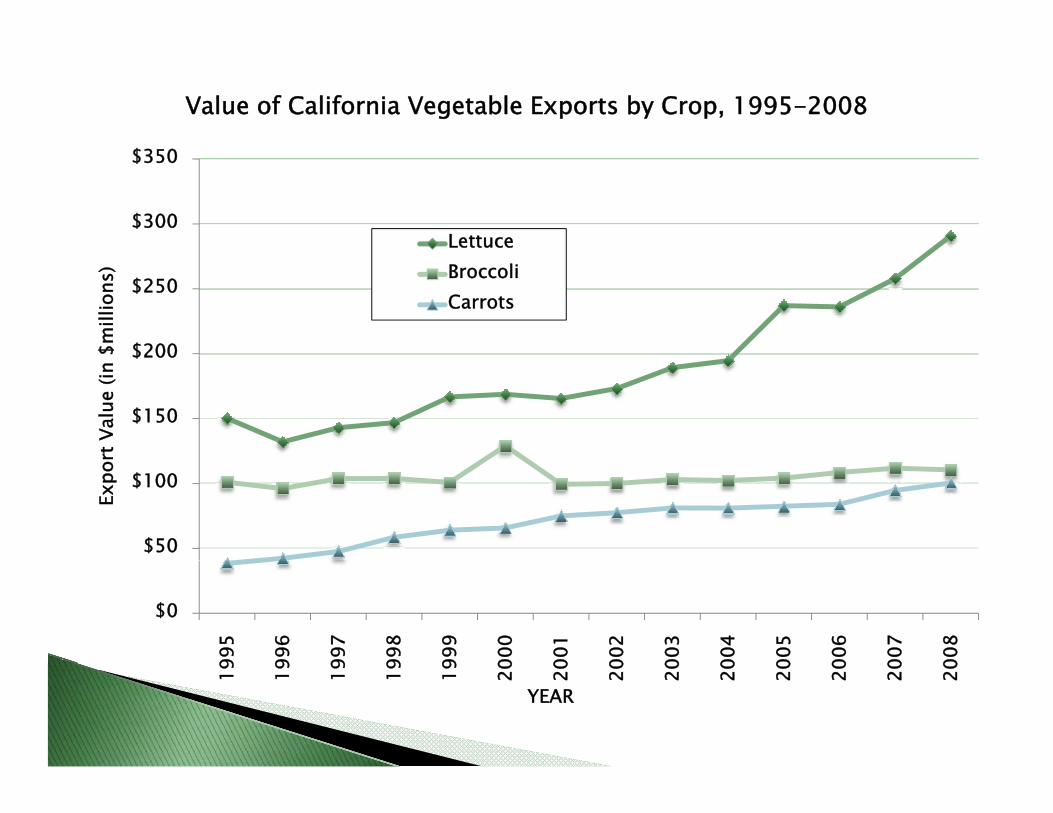

Value of California Vegetable Exports by Crop, 1995-2008

$300

$350

Lettuce

$200

$250

$mill

ions

) BroccoliCarrots

$150

$200

rt V

alue

(in

$50

$100

Expo

r

$0

995

996

997

998

999

000

001

002

003

004

005

006

007

008

19 19 19 19 19 20 20 20 20 20 20 20 20 20

YEAR

Share of 2008 Export Value of California Vegetables by CropTotal Vegetable Exports = $835 million

Other Vegetables25%

Lettuce35%

25%

Celery7%

Tomatoes, Fresh8%

Broccoli13%

Carrots12%

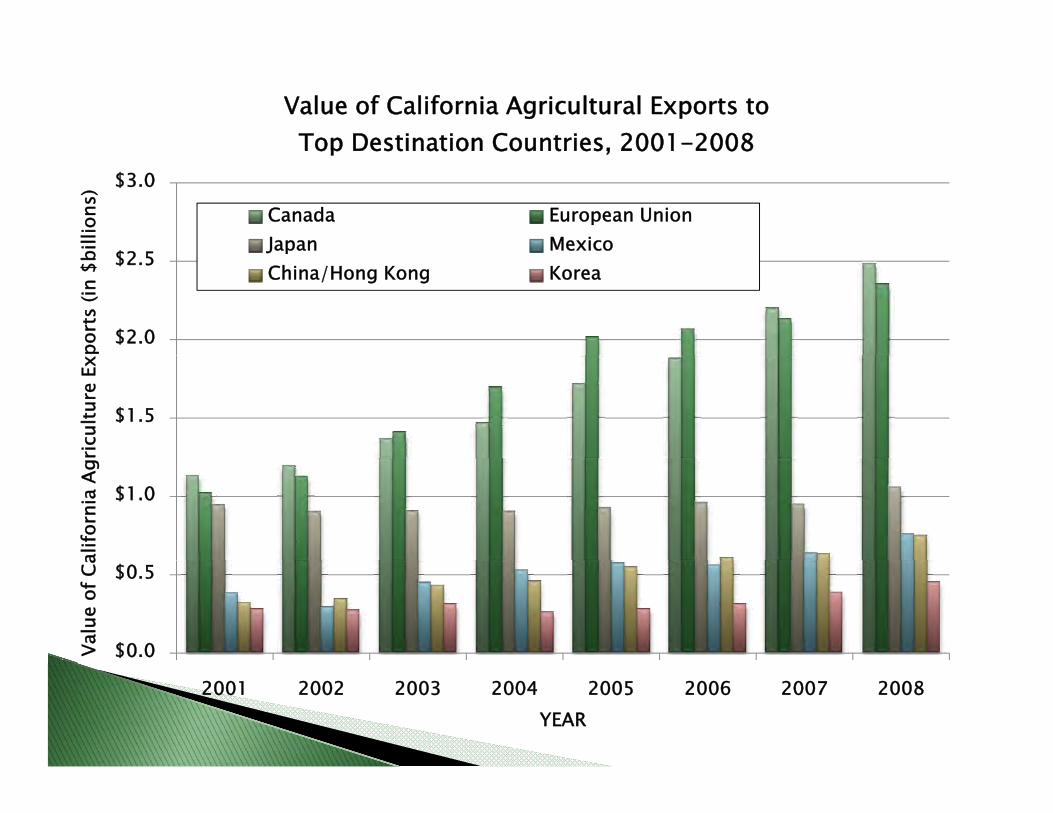

Value of California Agricultural Exports to Top Destination Countries, 2001-2008

$2 5

$3.0

billi

ons)

Top Destination Countries, 2001 2008

Canada European UnionJapan Mexico

$2.0

$2.5

port

s (in

$b J p

China/Hong Kong Korea

$1.5

ricul

ture

Ex

$1.0

alifo

rnia

Ag

$0.0

$0.5

Valu

e of

Ca

2001 2002 2003 2004 2005 2006 2007 2008YEAR

2007Product Category

European Union Canada JapanValue

($million)% Value

($million)% Value

($million)%

Animal Products $50.51 2.4% $115.29 5.2% $90.57 9.5%Field Crops $54.73 2.6% $196.31 8.8% $260.78 27.2%Fruits $213.42 10.0% $864.99 38.9% $308.17 32.2%Tree Nuts $1366.61 64.0% $199.36 9.0% $181.87 19.0%$ $ $Vegetables $15.71 0.7% $640.88 28.8% $58.80 6.1%Flowers and Nursery $9.20 0.4% $22.54 1.0% $1.90 0.2%Wine $423.90 19.9% $182.14 8.2% $55.12 5.8%

2008Product Category

European Union Canada JapanValue

($million)% Value

($million)% Value

($million)%

Animal Products $49.9 2.1% $140.6 5.6% $127.9 12.0%

Field Crops $127.9 5.4% $256.7 10.3% $330.5 31.0%

Fruits $303.4 12.9% $988.6 39.7% $317.5 29.8%

Tree Nuts $1,414.5 60.0% $196.1 7.9% $173.8 16.3%

Vegetables $14.4 0.6% $677.5 27.2% $57.6 5.4%

Flowers and Nursery $7.9 0.3% $24.1 1.0% $3.2 0.3%

Wine $437.6 18.6% $206.9 8.3% $54.6 5.1%

2008 2009 2010 projection 2011 projection

World 3 ‐0.8 3.9 4.3

Developed economies 0.5 ‐3.2 2.1 2.4

United States 0.4 ‐2.5 2.7 2.4

Euro area 0.6 ‐3.9 1 1.6

Japan ‐1.2 ‐5.3 1.7 2.2

Developing economies 6.1 2.1 6 6.3

Source: International Monetary Fund World Economic Outlook database, January 2010.

Annual GDP growth rates and projections for selected countries, 2003- 2011

4

6

GD

P

,

2

nsta

nt p

rice

2

0

2003

2004

2005

2006

2007

2008

2009

2010

2011

chan

ge, c

on

-4

-2

perc

enta

ge c

United States

Canada

Germany

-6

Annu

al p Japan

Mexico

-8Source: International Monetary Fund, World Economic Outlook Database, January 2010

Nominal exchange-rate indexes for largest trading partners, monthly January 2004 to February 2010

110

115

120monthly January 2004 to February 2010

100

105

110

00

90

95

Jan

2004

=1

75

80

85

J

Canada Eurozone Japan China

70

75

-04

-04

-05

-05

-06

-06

-07

-07

-08

-08

-09

-09

-10

Canada Eurozone Japan China

Jan- Jul-

Jan- Jul-

Jan- Jul-

Jan- Jul-

Jan- Jul-

Jan- Jul-

Jan-

Source: ERS

1.20Annual nominal and real exchange rates , 1990 - 2010

(Euro/$)

1.10

(Euro/$)

1.00

0.80

0.90

0.70Nominal exchange rate

0.60

990

992

994

996

998

000

002

004

006

008

010

Nominal exchange rate

19 19 19 19 19 20 20 20 20 20 20

Source: USDA ERS "Nominal Annual Country Exchange Rates" and "Real Annual Country Exchange Rates." Feb 17, 2010. http://www.ers.usda.gov/Data/ExchangeRates/Note: local currency per $US

Trade-weighted export exchange-rate indexes, monthly January 1999 to February 2010

120

130monthly January 1999 to February 2010

Almonds Grapes Lettuce

100

110

00

Almonds Grapes Lettuce

90

100

Jan-

99=

1

70

80

60

an-9

9pr

-99

ul-9

9ct

-99

an-0

0pr

-00

ul-0

0ct

-00

an-0

1pr

-01

ul-0

1ct

-01

an-0

2pr

-02

ul-0

2ct

-02

an-0

3pr

-03

ul-0

3ct

-03

an-0

4pr

-04

ul-0

4ct

-04

an-0

5pr

-05

ul-0

5ct

-05

an-0

6pr

-06

ul-0

6ct

-06

an-0

7pr

-07

ul-0

7ct

-07

an-0

8pr

-08

ul-0

8ct

-08

an-0

9pr

-09

ul-0

9ct

-09

an-1

0

Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja Ap Ju Oc Ja

Source: Export data from FAS, exchange-rate data from ERS

In 2 generations Korea’s economy went through changes that took 100 years in the U.S. and Europe.

In 1970 Korea Agriculture = 30% of Korea Economy In 2007 Agriculture = 3% KoreaEconomy. In 2007 Agriculture = 3% Korea Economy.

Source: Lee , H. and D.A. Sumner. 2007. The Prospective Free Trade Agreement with Korea: Background, Analysis and Perspectives for California Agriculture.

f Tar

iff

t Sha

re o

fPe

rcen

tLi

nes

T iff RTariff Rate BracketSource: Lee , H. and D.A. Sumner. 2007. The Prospective Free Trade Agreement with Korea:

Background, Analysis and Perspectives for California Agriculture.

Average Agricultural Tariff in Korea = 62%Average Agricultural Tariff applied by U.S. = 12%I i l i fIn many cases, potential imports from California agriculture face tariffs of more than 30 percent30 percent.◦ Table grapes, Almonds, Lettuce tariff rates = 45%-

50%

California Agricultural Exports to Korea 2001 2008

$450

$500

Exports to Korea, 2001-2008

All Agriculture Trade

$350

$400

$450

MIL

LIO

N) Fruits

$250

$300

PORT

S (IN

$

$100

$150

$200

ALUE

OF

EXP

$0

$50

$100

VA

2001 2002 2003 2004 2005 2006 2007 2008

YEAR

Commodity Rank Share of Export Value

Oranges 2 22%Grape Juice 2 41%Grapefruit 3 12%Grapefruit 3 12%Walnuts 4 9%Cherries 5 8%Lemons 5 5%Lemons 5 5%

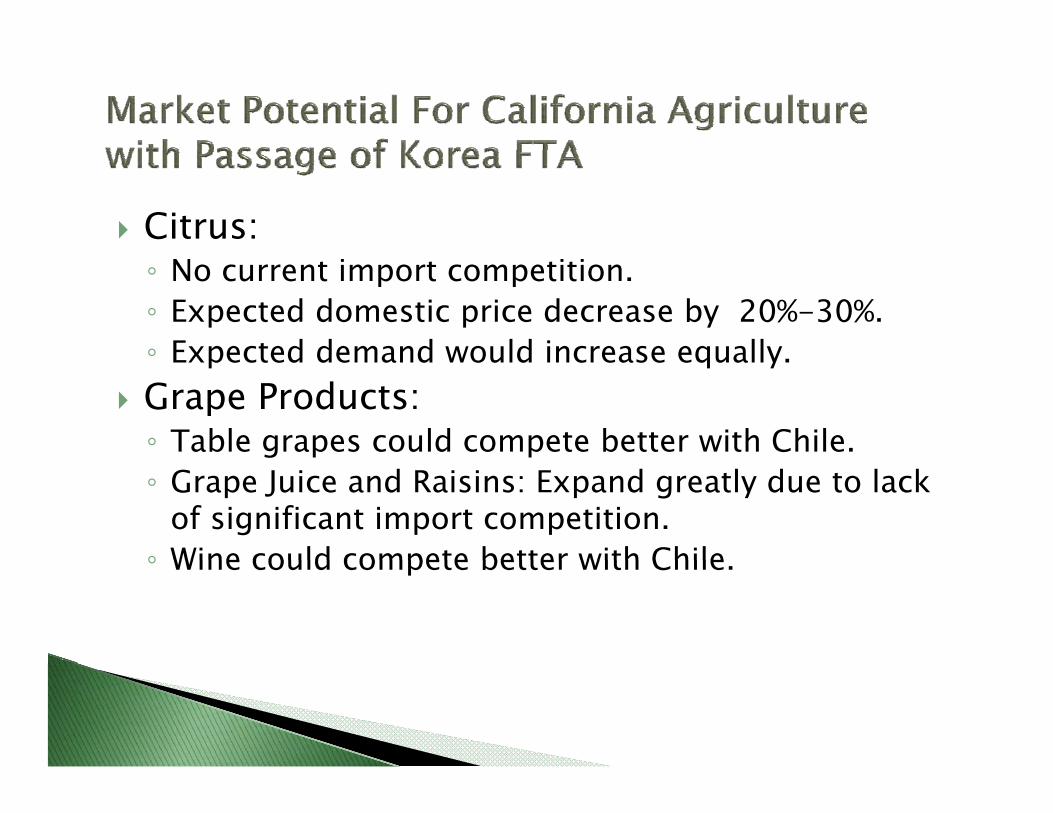

Citrus:◦ No current import competition. ◦ Expected domestic price decrease by 20%-30%.◦ Expected demand would increase equally◦ Expected demand would increase equally.Grape Products:◦ Table grapes could compete better with Chile.◦ Grape Juice and Raisins: Expand greatly due to lack

of significant import competition. ◦ Wine could compete better with Chile◦ Wine could compete better with Chile.

Fruits and Berries◦ Currently stone fruits and cherries are not a

significant part of Korean market.◦ Elimination of 24%-50% tariff would greatly expandElimination of 24% 50% tariff would greatly expand

market potential. Canned peaches are big part of Korean diet. Elimination of 50% tariff would allow CaliforniaElimination of 50% tariff would allow California peaches a significant price advantage over current imports from South Africa, Greece, and China. Same for PearsSame for Pears.

Vegetables◦ Even with 45% tariff Korea still imports Lettuce from

CaliforniaCalifornia.◦ Elimination of tariff could expand greatly the export

of lettuce and other leafy greens to Korean Market. Tree Nuts ◦ Already big presence in Korea market, could

potentially expand rapidly with elimination ofpotentially expand rapidly with elimination of tariffs.

“For agricultural products, the FTA would immediately eliminate or phase out tariffs and quotas on a broad range of products withquotas on a broad range of products, with almost two-thirds (by value) of Korea's agriculture imports from the United States becoming duty free upon entry into force.”

California continues to be competitive in international agricultural trade.

D i i i h fDespite recent economic issues, the future for California exports remains positive.

Ratification of Korea FTA could have significant economic impact for Californiasignificant economic impact for California agriculture.