Embed Size (px)

Citation preview

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act

2

Contents

I. Introduction 3

II. Meeting the “hedge or mitigate commercial risk” (“HMCR”) criteria 4Qualifies as a bona fide hedge (BFH) under the Commodity Exchange Act (CEA) Rules 6Qualifies for hedge accounting treatment under ASC 815/GASB 53 8Economically appropriate to the reduction of risks in the conduct and management of a commercial enterprise 10

III. Application framework 14

IV. Conclusion 15

Appendix A: Referenced rules and statutory language 16Note 1 16Note 2 16Note 3 17

Contacts 19

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 3

The Dodd-Frank Act (“the Act”) was the primary federal policy response to the financial disruption that affected the world economy in 2008. The Act was passed in July 2010, and included in its many provisions was Title VII, which addressed derivative activity. The energy industry, which uses derivatives to manage commodity price risk, is impacted by the provisions within Title VII.

The Act authorizes and directs the Commodity Futures Trading Commission (“CFTC”) to extend its regulatory oversight to over-the-counter derivatives and swaps. For more than two years, the CFTC has worked to build a regulatory framework to oversee derivative/swap trading and regulate the entities subject to the Act once this law is implemented.

The purpose of this whitepaper is:

• Toprovideanorganizeddiscussionoftherelevantpotentialimplicationsofhavingswapsactivitiesmeetthevariousdefinitions of hedging activity

• ToexplorethetypesofactivitiesthatentitiesmayassertarehedgingactivitieswithintherulespublishedbytheCFTC1

This paper proposes a framework for consideration in implementing the hedging-related rules established by the CFTC (“our framework”), and discusses relevant potential implications and practical applications of specific rules approved or proposed by the CFTC addressing hedging. The paper primarily focuses on the concept of hedging or mitigation of commercial risk (“HMCR”) activity, which is a term used to determine certain entity-level definitions and qualification of individual transactions for the end-user exception to clearing.

Within the discussion of the application of HMCR, we address three separate methods by which an entity can determine that an activity is hedging or mitigating commercial risk according to CFTC guidance. These methods are:

• Bonafidehedges(BFH)fordeterminingtheclassificationofanentityandtakinganend-userexception• HedgesthatqualifyforhedgeaccountingunderUnitedStatesGenerallyAcceptedAccountingPrinciples(“GAAP”)• Transactions/hedgesthatare“economicallyappropriate”tothemitigationofcommercialrisk

1 The final CFTC rule concerning position limit reporting has been ruled invalid by the judicial courts and must be revisited by the CFTC. Because of that decision, the impact from the position limit reporting rules will not be discussed herein.

I. Introduction

4

The CFTC Dodd-Frank rules include two specific rule making areas in which HMCR is an important component for compliance:

(1) Entity classification2 – the final entity classification rule allows transactions for hedging or mitigating commercial risk to be excluded from the notional value calculation used to determine if an entity is classified as either an swap dealer (SD) ormajorswapparticipant(MSP)

(2) End-user exception3 – a swap that qualifies for this exception is not required to be centrally cleared. This exception is notavailabletofinancialentities,whichincludesbothSDsandMSPs4. Additionally, the CFTC rules state that there is adifferenceinwhathedgingactivitymaybeexcludedintheSDandMSPentityclassificationcalculationsversuswhathedging activity may qualify for the end-user exception

A transaction may qualify for HMCR treatment by meeting any one of the following criteria5 6:

• QualifiesasaBFHunderCommodityExchangeAct(“CEA”)rules• QualifiesforhedgeaccountingtreatmentunderASC815/GASB537

• “Iseconomicallyappropriatetothereductionofrisksintheconductandmanagementofacommercialenterprise”8

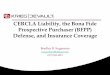

The graphic on the opposite page presents a framework to analyze individual transactions under the HMCR criteria, and the corresponding impact to the entity classification calculations and end-user exemption analysis. Due to swap dealers and major swap participants not being able to claim the end-user exception to clearing, an entity must know its entity classificationbeforeitcanappropriatelyclaimtheexception.Priortoperformingthecalculationsrequiredtoconcludeonitsentity classification, an entity must understand the impact of individual transactions. As such, this framework begins with a transaction level analysis.

• Process1addressesconsiderationastowhetherindividualswaptransactionswillqualifyasHMCRaseitheraBFH,anASC 815 hedge, or an economically appropriate hedge. A transaction may meet more than one HMCR criterion, but at least one must be met for the transaction to be considered HMCR.

• Process2demonstratestheimpactofatransactionconsideredHMCRvs.notconsideredHMCRontheentityclassification analyses.

• Process3demonstrateshowtheelectiontoapplytheend-userexemptiontoclearingisdependentupontheresultsoftheHMCRanalysisperformedinProcess1andtheentityclassificationresultsofProcess2.Finally,properdocumentationisrequiredfortheelectiontobeeffective.UnliketheHMCRanalysisinwhichonlyonecriterionmustbemet,theend-useranalysisrequiresthatallthreecriterionswithinProcess3bemetbeforetheend-userexceptionmaybeclaimed.

2 Refer to Appendix A, Note 3 3 Refer to Appendix A, Note 1 4 NotethattheCFTCrulesstatethatthereisadifferenceinwhathedgingactivitymaybeexcludedintheSDandMSPentityclassification

calculations vs. what hedging activity may qualify for the end-user exception.5 Refer to Appendix A, Note 26 Federal Register/Volume 77, pg. 307507 Accounting Standards Codification (www.fasb.org) and Government Accounting Standards Board (http://www.gasb.org/st/summary/gstsm53.html)8 Federal Register/Volume 77, pg. 30750

II. Meeting the “hedge or mitigate commercial risk” (“HMCR”) criteria

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 5

Note1:SwapswhichcanbeexcludedfromtheSDdefinitionaredifferentthanthosethatcanbeexcludedfromtheMSPdefinition(asshownabove). One interpretation would be that swaps which can be excluded from the SD definition would encompass all swaps meeting the BFH definition, and all swaps that would otherwise meet the bona fide hedge definition had they not exceeded the 12 month time horizon9.

9 See CFTC discussion of swaps that should be excluded from the SD calculation in Federal Register Volume 77, pg. 30612.

Process 2:Financial entity definition{Entity-specific analysis}

Process 3: End-user exemption to clearing

Exclude fromMSP analysis

Is Swap contract HMCR?

Is Swap contracta bona fide hedge?

2(a): MSP analysis

2(b): SD analysis

Include inMSP analysis

No

Yes

Yes

Yes

No

No

Include inSD analysis

Exclude fromSD analysis

Notify SD/MSP/SDR ofelection to apply end use

exemption to clearing

Considertransactioneligibility**

Eligible For qualifying swaps,prepare HMCRdocumentation

Exclude fromSD analysis

Does Swap contract fail to meet bona fide hedgingdue to a tenor exceeding

12 months? (note 1)

HMCR**Yes

Yes

Yes

No

Not HMCR

Economically appropriateto hedge or mitigate

commercial risk?

No

Qualifies for hedgeaccounting under

ASC 815/GASB 53?

No

Qualifies as a “bona fide”hedge under Commodity

Exchange Act (CEA)?

Considerentity eligibility*

Eligible

Transaction level process flow for entity-level classification and end-user analysis

*Note that SD & MSP are not eligible for end-user exemption (refer to process 2)**Note that only transactions that meet one of the HMCR criteria above (refer to process 1) are eligible for the end-user exemption

**Impacts entity-level analysis (refer to process 2) and end user exemption to clearing (refer to process 3)

Process 1:HMCR

{Transaction-specific analysis}

6

Qualifies as a bona fide hedge (BFH) under the Commodity Exchange Act (CEA) rulesBona fide hedging has several differing definitions within the CFTC rulemaking areas. This section of the paper focuses on the bona fide hedge definition per the Commodity Exchange Act (“CEA”) as applied in the entity classification and end-user exception rules. Section § 1.3 [Revised] of the CEA requires that “transactions and positions for excluded commodities” be included within the definition of a bona fide hedge.

A three prong test can determine if a transaction meets the definition of a BFH (all three prongs must be answered in the affirmative for the transaction to qualify as a BFH):

1. The transaction represents a substitute for a physical position typically made or forecasted to be made2. The transaction is economically appropriate to the reduction of risks 3. The transaction qualifies as an “enumerated” hedge, as defined below (entities wishing to use “non-enumerated”

hedges must request approval from the CFTC)

Given the strict guidelines concerning the definition of a BFH, it is important to understand the explicit limitations expressed within the CEA. The final rule defines BFHs as “… any agreement, contract or transaction…, where such transaction or position normally represents:

• Asubstitutefortransactionstobemadeorpositionstobetakenatalatertimeinaphysicalmarketingchannel• Andwheretheyareeconomicallyappropriatetothereductionofrisksintheconductandmanagementofa

commercial enterprise • Andwheretheyarisefrom:

– (i) The potential change in the value of assets which a person owns, produces, manufactures, processes, or merchandises or anticipates owning, producing, manufacturing, processing, or merchandising,

– (ii) The potential change in the value of liabilities which a person owns or anticipates incurring, or – (iii) The potential change in value of services which a person provides, purchases, or anticipates providing or

purchasing. – (iv) Notwithstanding the foregoing, no transaction or position shall be classified as bona fide hedging unless their

purpose is to offset price risks incidental to commercial cash or spot operations and such positions are established and liquidated in an orderly manner in accordance with sound commercial practices and, for transactions or positions on contract markets subject to trading and position limits in effect pursuant to section 4a of the Act…”10

The CFTC addresses the overlap of BFHs versus economic mitigation of risks by making BFHs more difficult to achieve (because in addition to being economically appropriate, a BFH must meet the other two criterions above).

The CFTC rules and commentary illustrate what could qualify as a BFH based on the definition above. The table on the opposite page lists the five specific types of transacting activities specifically allowed for under the rules (referred to as enumerated hedges within the rules) and an example that could be interpreted from the language of each activity:

10 Federal Register Volume 76, pg. 71683

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 7

CFTC Enumerated Hedges11 Example

1) Sales in quantities not to exceed owned or fixed price purchased assets, and up to 12 months unsold anticipated production of a commodity as long as it is not entered within the last five trading days of the month.

Financial hedges of forecasted sales of production or forecasted sales of assets expected to be purchased at a fixed price within 12 months. For example, forecasted sales from a power generation facility within the next 12 months.

2) Purchasesinquantitiesnottoexceedfixedpricesales of cash products or by-products of the same commodity, up to 12 months unfilled requirements of the commodity for processing or manufacturing as long as it is not entered within the last five days of the month.

Financial hedges of forecasted purchases used in production or forecasted purchases of assets for a fixed priced sale within 12 months. For example, forecasted gas purchases for a gas fired power generation facility within the next 12 months or forecasted power purchases to serve fixed price retail load blocks won at auction.

3) Offsetting sales and purchases of the same commodity that do not exceed the volumetric quantity bought and sold at unfixed prices basis different delivery months as long as it is not in the last five days of the month.

Financial hedging of price risks associated with contracted physical index purchases and sales for different months. For example, assume an entity executes a crude purchase and sale agreement whereby an entity will purchase crude at the prevailing market rate in June and sell crude at the prevailing market rate in November. Swaps executed to economically hedge the purchase price in June and the sale price in November would meet this exception.

4) Purchasesandsalesenteredbyanagentinwhichthe agent has an agreement in place with the person who owns the asset being hedged.

Agents who both manage the physical scheduling of a commodity and the execution of hedges for another entity. For example, a power co-op managing physical price risk that schedules and executes transactions with the market on behalf of its member end-users.

5) Hedging of the items in (1)-(4) above as long as they are not in the same quantity and commodity provided that the change in fair value of the hedge substantially relates to the change in fair value of the item being hedged.

Cross commodity hedges that are economically appropriate to the price risk an entity is exposed to. For example, executing a natural gas swap to hedge a power exposure or executing a crude oil swap to hedge a natural gas liquids exposure.

Non-Enumerated hedges not included within the enumerated section of the standard above must be submitted to the CFTC for review and approval12.

Within the energy industry, the most common types of transactions likely to qualify as BFHs as defined by the CEA would be up to 12 months of anticipated purchases or sales as explained in 1 and 2 above. However, it is common within the industry to have contracts that surpass 12 months of anticipated purchases or sales. Based on a strict reading of the rules, these would not qualify as a BFH under the CEA’s definition. As such, when determining an entity’s classification and the applicability of the end-user exception, contracts settling greater than 12 months from inception would not meet the definition of a BFH and would not qualify for the end-user exception (unless the contracts met the

11 Federal Register Volume 76, pg. 7168412 Federal Register Volume 76, No.223 pg. 71684

8

definition of one of the other two exceptions defined below). If the only characteristic preventing the trade from meeting the BFH definition per the CEA is that the tenor of the trade exceeds the 12 month time horizon, it appears the transaction could be excluded from the SD analysis.

Qualifies for hedge accounting treatment under ASC 815/GASB 53 ASC815(previouslySFAS133)providestherequirementsforhedgeaccountingwithinU.S.GAAP.GASB53provideshedgeaccounting requirements, which are similar to ASC 815, for government entities. As such, ASC 815 will be referred to for the remainder of this document.

HedgeaccountingisanelectionwithinU.S.GAAPthatallowsfortherecognitionofincome/expenseassociatedwithaderivative instrument to more closely match the economics of the relationship between the hedge instrument and the hedged item. This election is allowed to be made only if certain criteria are met.

Criteria to elect to apply hedge accountingEach type of hedge accounting that can be elected under ASC 815 Derivatives and Hedging requires that all of the following criteria be met:

• Hedge Accounting/Risk Policy: The entity must have an overall hedge accounting and risk policy that details the circumstances under which hedge accounting will be applied and how it will be applied. While hedge accounting guidance requires specific calculations, the manner in which the calculation is performed is often flexible to the needs of the hedge relationship.

• Hedge Documentation: As hedge accounting is an election, contemporaneous documentation of the election is required prior to applying hedge accounting. In addition to documentation, cash flow hedges need to be supported by the representation that a forecasted transaction is probable of occurring. Commonly, a test is used to determine the probability of the hedged item occurrence by comparing actual hedged item results to forecasted hedge item results. This analysis supports an entity’s ability to adequately forecast that the hedged item is probable of occurring.

• Hedge Assessment: A hedge assessment is a calculation that must be measured against certain standards. This calculation tests if the hedge relationship has been effective in offsetting changes in fair value/cash flow of the hedged item and is expected to be effective in the future. The calculation results in determining whether hedge accounting can be applied or hedge accounting cannot be applied. This assessment is required to be performed at the inception of the hedge relationship and at least quarterly during the life of the hedge relationship.

• Hedge Measurement: The hedge measurement calculation determines the actual dollar amount of ineffectiveness in the hedge relationship and is recorded as an adjustment to current earnings.

Given these eligibility, documentation, and ongoing assessment requirements, the term “qualifies for hedge accounting” raises several questions.

“Qualifies”The term used within the CFTC rules is “qualifies”13. This term raises a question as to if the transaction only needs to meet the requirements for hedge accounting, not necessarily to be actually receiving hedge accounting in the financial statements. A reasonable interpretation of the “qualifies” language could be that a transaction only needs to meet the requirements for hedge accounting, not actually be in an active hedge relationship for financial statement purposes.

13 Federal Register Volume 77 No. 139, pg. 42590

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 9

While ASC 815 requires each of the items mentioned above to apply hedge accounting, a reasonable interpretation could be that all items are required to meet the “qualifies” criterion. We note that the CFTC comments in the final rules concerningtheMSPdefinition14 (and by corollary, the end-user exception) do not explicitly require hedge assessments or documentation15. However, that commentary was in reference to the overall HMCR exception, and not specifically addressing to the ASC 815 criteria. To meet the “qualifies for ASC 815” criterion within the HMCR exception, a reasonable interpretation could be that the following items would be needed:

• Hedge Accounting/Risk Policy: As hedge accounting is an election, so too is the HMCR exception. As such, contemporaneous hedge accounting/risk policy documentation is required.

• Hedge Documentation: As hedge accounting is an election, so too is the HMCR exception. As such, contemporaneous hedge documentation is required. This hedge documentation should provide support concerning the probability of the forecasted transaction actually occurring, which the individual financial instrument is hedging. As noted above, a reasonable interpretation could be that a transaction may “qualify” for hedge accounting for the Act, but not actually receive hedge accounting within the financial statements. As such, it will be critically important to distinguish in the hedge documentation the specific purpose of the documentation: qualification for hedge accounting under the Act, application of hedge accounting in the financial statements, or both.

• Hedge Assessment: An assessment calculation is required prior to the application of hedge accounting. By default, a transaction cannot qualify for hedge accounting unless a hedge assessment is performed prior to the election.

Note that the one item that a reasonable interpretation could determine to not be required is a hedge measurement calculation. The hedge measurement calculation is not performed at the inception of a hedge relationship, but is instead performed periodically after inception to measure the actual dollar amount of hedge accounting ineffectiveness in the relationship. Because it is not required to support the inception of hedge accounting relationship, a reasonable interpretation could be that it is required for purposes of HMCR qualification under the Act.

Inception vs. ongoing maintenanceA key question associated with meeting HMCR criterion via “qualifies” for hedge accounting method would be determining what would happen if hedge accounting would no longer be appropriate? This can happen within the energy industry for a variety of reasons, which may include the following:

• Commoditypricescandivergesuchthatpreviouslyassessedcommodityrelationshipsmeetingtherequirementsforhedge accounting no longer qualify

• Businessoperationsmaychangesuchthatforecastedtransactionspreviouslybelievedtobeprobable,nolongerare• Thepricingmechanismofthehedgeditemchangessuchthatthehedgeinstrumentisnolongerhighlyeffective

In these situations, traditional hedge accounting for these transactions must be discontinued.

We noted the following guidance within the CFTC rules and ASC 815 literature concerning ongoing monitoring and assessment:

• Transactionselectedfortheend-userexceptionmustbedocumentedatinception,howevertheCFTChascommentedthat documentation is not required for the HMCR exception for entity classification16.

14 As indicated previously, the SD definition does not specifically reference ASC 815 hedges.15 Federal Register Volume 77 No. 100, pg. 3067616 Federal Register Volume 77 No. 100, pg. 30676, and No. 139, pg. 42572

10

• TheCFTCindicatedthatongoingeffectivenesstestingisnotrequiredfortheHMCRexception17 within the entity classification rule or for qualifying for the end-user exception to clearing18. However, the CFTC did indicate that the economically appropriate designation should be continuously monitored to ensure reasonableness of the exception19.

• SDandMSPclassificationsmustbemonitoredonanongoingbasis(quarterly).• ASC815requiresbothcontemporaneoushedgedocumentationatinceptionofthehedgerelationshipandongoing

hedge assessments to support the continued application of hedge accounting.

Based on the above observations of the CFTC rules, a reasonable interpretation could be the following:

• ForMSPclassification,becausethereisanongoingmonitoringrequirementrelatedtodeterminingifentitieshavetripped the requirements of the rule, each transaction should continue to be monitored to ensure that it qualifies for economic appropriateness.

• ForMSPclassification,instrumentsmeetingtheHMCRexceptionunderthehedgeaccountingcriterionshouldcontinueto meet hedge accounting requirements. Hedge assessments would continue to be performed to support both the designation of new transactions and the continued designation of existing transactions.

• Theserequirementsdonotexistwithintheend-userexception.

Recent trendsThe Financial Accounting Standards Board (“FASB”) has recently released an exposure draft (a proposed change to accounting standards) to simplify hedge accounting20. This exposure draft has focused on many areas, but one of the most significant changes was the loosening of hedge accounting assessment requirements from “highly effective” as required in currentU.S.GAAPto“reasonablyeffective”intheproposedexposuredraft.“Reasonablyeffective”wasintentionallynotdefined within the exposure draft to allow for entities to qualitatively support hedging relationships. It is expected that only in rare circumstances would a quantitative analysis be required to support the assertion of “reasonably effective” hedge relationships.

This change could potentially allow for more relationships to qualify for hedge accounting under proposed amendments toU.S.GAAP.Consequently,moretransactionswouldqualifyfortheend-userexceptionforclearingandbeexcludedfromtheMSPnotionalvaluecalculation.ThischangewouldappeartoalignwiththethinkingoftheCFTC,asthedefinitionofHMCR has also been left intentionally undefined. As such, a reasonable interpretation would be that the proposed change in hedge accounting requirements would change the requirements of entities in applying the HMCR criteria although it has the potential to allow additional transactions to be excluded from the clearing requirement.

Economically appropriate to the reduction of risks in the conduct and management of a commercial enterpriseThis section will discuss swaps deemed to be economically appropriate to the hedging or mitigation of risk. This sub-category of HMCR encompasses a broader scope of transactions than those envisioned under bona fide hedging (which, for example has limits on the tenor for anticipatory hedges) or under ASC 815 (which has strict criteria in the assessment of the degree of offset as being “highly effective”21 and limits what types of risks may be identified and designated as being hedged). As noted in the CEA22, a swap is deemed to be HMCR when “such a position is economically appropriate to the reduction of risks that are associated with the conduct and management of a commercial enterprise.”

17 Federal Register Volume 77 No. 100, pg. 3068018 Federal Register Volume 77 No. 100, pg. 4527519 Federal Register Volume 77 No. 100, pg. 3068020 http://www.fasb.org/cs/ContentServer?c=FASBContent_C&pagename=FASB%2FFASBContent_C%2FProjectUpdatePage&cid=117580188965421 ASC 815-20-25-7522 See Appendix A, Note 2

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 11

This section will first consider the term “economically appropriate” and will then consider the following additional phrase used in the definition of HMCR23: “Such position is:

(1) Not held for a purpose that is in the nature of speculation or trading(2) Not held to mitigate the risk of another… swap position, unless that other position is itself held for the purpose of

hedging or mitigating commercial risk as defined by this section…”

Speculation vs. economically appropriate…Speculation or trading is often an arbitrary term within the energy transacting industry. Activities that are interpreted as economic optimization by some entities could be viewed as speculating by others. The CFTC has described speculation, investment or trading as activities involving swap positions “held primarily to take an outright view on market direction, including positions held for short term resale, or to obtain arbitrage profits”24. While the CFTC agrees that there is a fine line between speculating and economic hedging25, such a distinction must be made.

A reasonable interpretation would be that “economically appropriate” in this context is addressing the ability of the swap to offset the cash flow or fair value risk of some identified risk related to an entity’s business. Several examples of swaps were used by the CFTC within the position limit reporting final rule to incorporate considerations of “economically appropriate”26. In these examples, two factors are repeatedly considered: 1) from a volumetric perspective the quantity of swaps does not exceed the quantity of risk held by the entity; and 2) from a value perspective, the value change to the swap resulting from an underlying price movement is offsetting the value change in the risk driven by the same pricing change.

In the context of transacting a swap to offset a risk related to an entity’s operations, such as the output of a plant or facility operated by the entity, the consideration of quantities appears relatively straightforward when contrasted against the diverse number of discretely priced energy products or commodity grades are used in many entities’ risk mitigation programs.27 How an entity is to determine whether the swap achieves an acceptable degree of offset to the risk it is meant to hedge or mitigate is not specified in detail. A reasonable interpretation of such consideration would rely on qualitative understanding relevant to the markets, products and risks being used or hedged. If the CFTC had considered that an absolute threshold was necessary, appropriate, and relevant to all instances, a reasonable interpretation would be that one would have been incorporated into the rulemakings. Instead, the CFTC left the term undefined. A reasonable interpretation would be that a qualitative assessment would allow for consideration of facts and circumstances that are relative to each unique HMCR situation.

Challenges in applying “economically appropriate”There are gray areas that may warrant consideration in the application of the “economically appropriate” test. For example, one may view that the requirement that a swap mitigates commercial risk is a determination that is made in the context of whether a swap is more likely to mitigate the overall risks to a commercial enterprise or more likely to create overall risk to a commercial enterprise. A proponent of this view would likely deem a swap to qualify as “economically appropriate” if it were “more likely than not” to mitigate risks to the enterprise (i.e., a greater than 50% degree of offset).

Alternatively, one may consider the individual swap in the context of the identified risk that it is meant to hedge or mitigate and determine that the swap does address the risk in question (without regard for other risks brought about by the swap instrument). An example of this would be the use of a crude oil swap to mitigate the risk associated with a forecasted

23 Federal Register Volume 77 No. 139, pg. 4259124 Federal Register Volume 77 No. 100, pg. 3067625 Federal Register Volume 77 No. 139, pg. 4257326 Federal Register Volume 76 No. 223, pg. 7169627 Federal Register Volume 77 No. 100, pg. 30673

12

y-grade (economically representing a basket of natural gas liquids) purchase. Such a swap would have cash flows impacted by changes in the benchmark crude oil index. In the context of the identified risk being hedged (i.e., the basket of natural gas liquids), consideration would be given to the correlation between crude oil and natural gas liquids prices, such that crude oil may not be deemed an effective hedge for all natural gas liquids products at all times. Accordingly, in the context of overall risks to a commercial enterprise, one may view that the crude oil index risk created by the swap introduced risk (as no inherent crude oil risk was identified related to the entity’s business), but may have also mitigated a portion of an identified risk. With such a view, the example would require judgment from the entity applying the “economically appropriate” test.

Challenges in applying the hedge and mitigate commercial risk exceptionAs indicated by the lengthy comment process on the entity definitions and commentary by the CFTC, the application of the HMCR exception will likely be challenging. Even the hedge accounting prong of HMCR taken from ASC 815, which provides objective standards for the application of hedge accounting, contains items that could be considered subjective. We note the following areas as some of the challenges:

Application of ASC 815The application of ASC 815 would appear to be the most defendable prong in regards to the HMCR exception. It provides the most objective standards that have been established and recognized by existing regulatory and rule making entities (Securities and Exchange Commission, Financial Accounting Standards Board, Governmental Accounting Standards Board, etc.).

However, we expect that the ASC 815 prong will be the most onerous to meet due to the documentation requirements and effectiveness testing requirements. In addition, a reasonable interpretation would be that transactions should continue to be subject to ongoing effectiveness testing, which could threaten the ongoing use of HMCR.

Additionally, ASC 815 does not provide for a singular standard in regards to the application of hedge accounting. This flexibility appears intentionally written into ASC 815. Thus, transactions hedging the exact same risk may result in different ASC 815 accounting conclusions depending upon an individual entity’s derivative accounting policy documentation and hedge assessment methodology. In addition, speculative activities may qualify for hedge accounting in certain situations28. As speculative activities are specifically exempted from the HMCR exception, while likely to be a rare situation, this potential allowance of hedge accounting under ASC 815 would appear to contradict the intent of the CFTC.

“Economically appropriate”The application of the “economically appropriate” criterion appears to be a subjective prong to meeting the HMCR criterion, and thus could be challenged by regulators and auditors. As noted above and by the CFTC, there is a fine line between speculation and “economically appropriate” hedging activities. As noted in the final published rule on entity classification, the CFTC intentionally left judgment29 within the “economically appropriate” definition. While these risks are limited to the six risks defined by the CFTC within the hedge or mitigate risk definition, these risks are broadly defined such that most commercial risks will be covered.

We note the certain transacting strategies common to the industry may cause concern. While many entities may execute a single transaction to hedge forecasted purchases or sales, many other entities employ a dynamic strategy that results in an

28 PerEITF02-03“Aderivativeheldfortradingpurposesmaybedesignatedasahedginginstrument,prospectively,ifalloftheapplicablecriteriain Statement 133 have been met.”

29 Federal Register Volume 77, No 139, pg. 42572

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 13

entity transacting multiple times based on their “view of the market.” Different individual strategies may exist, but each is associated with replacing a single executed hedge with a subsequent offsetting hedge and a new hedge, often referred to as optimization.

The following examples illustrate different scenarios within the energy industry that may be considered “economically appropriate” mitigation of risk by certain entities or speculation by others:

• Arefiningoperationanticipatesfuturepurchasesof10,000barrelsofoilinDecember.InJanuary,therefinertransactsaswap to purchase 10,000 barrels of crude for December delivery at a fixed price. In February, the refiner decides to re-expose its operations to crude oil price risk and executes an offsetting swap for 10,000 barrels of crude for December delivery. Further assume that in March the refiner chooses to re-hedge its December exposure and enters into a third swap; again to fix the price of 10,000 barrels of crude for December delivery.

• Arefiningoperationproducesjetfuel.Therefineranticipatestheproductionandsaleofjetfuelinthreeyears’time;however no such contract readily exists that allows the refiner to fix the future price of jet fuel. Instead the refiner enters into a crude oil swap and determines that such a swap is “economically appropriate” to the mitigation of its future sale of jet fuel because jet fuel is a product made from the refining of oil. Consider further that subsequent to the transaction, a jet fuel product becomes available in the financial markets. With the intention of identifying a swap better suited for its risks, the refiner enters into an offsetting crude swap and also executes a swap to fix its future sales price of jet fuel.

• Anelectricitygeneratorseekstomitigatepowerpricerisksrelatedtotheanticipatedproductionandsaleof100megawatt hours (“MWH”) of power in 2015. The only readily available electricity products in the market would be “calendar strip” transactions (those that call for an equal amount of power to be delivered throughout the calendar year, at the same fixed price); therefore the generator transacts a swap for 100MWH at a fixed price, for delivery in 2015. In the year 2014, the market now has products readily available for each month or quarter of the year 2015. The generator enters into a second “calendar strip” swap for 100MWH to offset its initial swap. The generator then executes several additional swaps for varying quantities in each month or quarter in 2015. The purpose of each swap is to more closely match the executed hedge instrument to the load profile against which the entity must deliver power.

• Anelectricitygeneratorseekstomitigatepowerpricerisksrelatedtotheanticipatedproductionandsaleof100megawatt hours of power in 2013. Due to the relatively near term of the forecast, the market has products available for each month of 2013, and thus the generator executes individual monthly financial contracts to hedge forecasted production for each month. Due to a forecasted decline in generation due to demand reduction, the generator executes offsetting contracts to lower the amount of net financially hedged forecasted generation. This net position is then adjusted subsequently based on forecasted generation shifts.

Each potential scenario had an original instrument to mitigate a risk, a second offsetting instrument to re-open the risk, and a third instrument to re-mitigate the risk. However, each scenario was different as to the reasons each instrument was executed. Questions that these scenarios raise include: Do all of these transactions meet the “economically appropriate” threshold? Does only the original transaction meet the threshold? Do only the first two meet the threshold? Do subsequent transactions undo prior designations?

While the rule states that the volume of the hedge instrument must always remain “economically appropriate,” understanding where to draw the line between speculation and “economically appropriate” hedging activity may be a challenge for entities wishing to apply the HMCR exception. Although not required, documentation concerning how an entity is meeting the “economically appropriate” threshold should be considered as a means to archive decision making. Additionally, entities should consider the involvement of external counsel in documenting and supporting assertions made concerning the “economically appropriate” criterion.

14

Earlier in this paper we discussed the implications of hedge activity to various CFTC rules which drive reporting requirements. Any framework adopted by an entity to comply with the rules under the Act should help ensure compliance with the rules while also properly applying exemptions within the Act. For example, an entity may consider that based on the quantitative nature of its activity, it is a major swap participant when the true nature of that activity conforms to certain end-user exemptions which may impact that entity’s conclusion about its entity classification.

The CFTC has not required documentation as it relates to the use of the HMCR exception for entity classification purposes. However,theend-userexceptiondoesrequiredocumentationandthecriteriafordetermininghedgesfortheMSPdefinition and the end-user exception are nearly identical. As such, it may be expected that in application, documentation of the HMCR exception for entity classification will in effect be required for those entities wishing to exclude transactions from clearing.

The documentation required by the end-user rule is on a transaction by transaction basis and must support the assertion that a swap was executed for purposes of hedging or mitigating commercial risk. To put that in practice, an entity should think strategically when designing a process that accurately reflects the nature of risks present in its business and best leverages current processes around deal capture and authorization.

At a minimum, an entity will be expected to have a document that links entity-wide strategies and risks (including considering those publicly disclosed) to specific business units or assets that give rise to risks, coupled with designation at the individual swap level on conformance of the swap with that stated strategy.

Based on Deloitte’s experience, common industry practice is to maintain hedge documentation at a level that is higher than the individual transaction (portfolio level designation). This higher, portfolio level documentation is often done on a transacting book basis, or some other form of grouping within an entity’s listing of open transactions, such that any transaction within that book receives hedge accounting based upon the hedge documentation at the portfolio level. Providedtransactionswithinthebookmeettheattributerequirementsofthehedgedocumentation,theinstrumentisdesignated to have been elected to receive hedge accounting.

A reasonable interpretation could be that a similar level of documentation concerning HMCR could meet the intentions of the rules. The CFTC states it will require notification of the end-user exception on a transaction by transaction basis30. To support the assertion that the transaction “qualifies” for hedge accounting, the notification provided to the CFTC could reference HMCR documentation maintained at the book level to support the election.

30 Federal Register Volume 77, No. 139, pg. 42565

III. Application framework

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 15

Understandingtheterm“hedgeormitigatecommercialrisk”willbeofcentralimportanceasentitiesattempttounderstandand comply with the CFTC rule-making areas addressing entity classification and the end-user exception to clearing. CFTC rules addressing these activities are written to be applied transaction by transaction. Depending upon an individual entity’s strategy for complying with aspects of the Act (e.g., clearing via the end-user exception), entities should determine and document the hedging purpose of each financial transaction executed.

To meet the requirements of the hedge or mitigate commercial risk criteria, entities have three separate methods:

• BFHsfordeterminingtheclassificationofanentityandtakinganend-userexception• HedgesthatqualifyforhedgeaccountingunderU.S.GAAP• Transactions/hedgesthatare“economicallyappropriate”tothemitigationofcommercialrisk

The bona fide hedge criterion specified in the CFTC entity classification rules appears the most restrictive and difficult to meet. However, the CFTC has also provided the most commentary and objective standards to determine that this criterion is met. Additionally, transactions meeting the definition of a BFH per the CEA appear to have the widest application as these transactions may:

• Beexcludedfromentityclassificationcalculations• Applytomeetingtheend-userexceptiontoclearing

While transactions meeting the “qualifies for ASC 815” or “economically appropriate” criteria may not have as wide anapplication,meetingeitheroneofthesecriteriawillallowanentitytoexcludethetransactionfromtheMSPentityclassification and qualify for the end use exception. A reasonable interpretation could be that to the meet the “qualifies for ASC 815” criterion, an entity will be required to prepare the following:

• Hedgeaccounting/riskpolicy• Hedgedocumentation• Hedgeassessment

The “economically appropriate” criterion appears to be the most subjective of the three hedge or mitigate commercial risk prongs. A reasonable interpretation would be that “economically appropriate” in the context of the CFTC rules appears to address the ability of the swap to offset the cash flow or fair value risk of some identified risk related to an entity’s business, while also considering the volume level of the transaction.

As entities begin to apply and comply with the CFTC rules and implementing the Dodd-Frank Act, careful considerations should be made to how the hedge or mitigate commercial risk criteria will be applied. While the CFTC has indicated that documentation is not required for all aspects of the hedge or mitigate commercial risk criteria, documentation in some form could allow entities to objectively judge their transacting against these criteria and more appropriately comply with the individual rules.

IV. Conclusion

16

Note 1:End-user exception The end-user exception is provided for in Section 723(a)(3) of the Act. First, section 2h contains the requirement for clearing:

(h) CLEARING REQUIREMENT.—(1) IN GENERAL.—(A) STANDARD FOR CLEARING.—It shall be unlawful for any person to engage in a swap unless that person submits such swap for clearing to a derivatives clearing organization that is registered under this Act or a derivatives clearing organization that is exempt from registration under this Act if the swap is required to be cleared.

Within the same section, the exception to the clearing requirement is provided:

(7) The requirements of paragraph (1)(A) shall not apply to a swap if 1 of the counterparties to the swap—(i) Is not a financial entity;(ii) Is using swaps to hedge or mitigate commercial risk; and(iii) Notifies the Commission, in a manner set forth by the Commission, how it generally meets its financial obligations

associated with entering into non-cleared swaps.

Note 2:Definition of hedge or “mitigate commercial risk”For purposes of section 2(a)(7)(A)(ii) of the CEA and § 39.6(b)(4), a swap shall be deemed to be used to hedge or mitigate commercial risk when the swap is:

1) Economically appropriate to the reduction of risks in the conduct and management of a commercial enterprise, where the risks arise from:(A) The potential change in the value of assets that a person owns, produces, manufactures, processes, or

merchandises or reasonably anticipates owning, producing, manufacturing, processing, or merchandising in the ordinary course of business of the enterprise;

(B) The potential change in the value of liabilities that a person has incurred or reasonably anticipates incurring in the ordinary course of business of the enterprise; or

(C) The potential change in the value of services that a person provides, purchases, or reasonably anticipates providing or purchasing in the ordinary course of business of the enterprise;

(D) The potential change in the value of assets, services, inputs, products, or commodities that a person owns, produces, manufactures, processes, merchandises, leases, or sells, or reasonably anticipates owning producing, manufacturing, processing, merchandising, leasing, or selling in the ordinary course of business of the enterprise;

(E) Any potential change in value related to any of the foregoing arising from foreign exchange rate movements associated with such assets, liabilities, services, inputs, products, or commodities; or

(F) Any fluctuation in interest, currency, or foreign exchange rate exposures arising from a person’s current or anticipated assets or liabilities;

OR

2) Qualifies as bona fide hedging for purposes of an exemption from position limits under the Act;

OR

3) Qualifies for hedging treatment under Financial Accounting Standards Board Accounting Standards Codification Topic 815, Derivatives and Hedging (formerly known as Statement No. 133)

Appendix A: Referenced rules and statutory language

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 17

In addition to meeting one of the requirements from above, the swap must not be:

1) Used for a purpose that is in the nature of speculation, investing, or trading2) Used to hedge or mitigate the risk of another swap or securities-based swap, unless that other swap itself is used to

hedge or mitigate commercial risk as defined by this rule, or the equivalent definitional rule governing security-based swaps promulgated by the Securities and Exchange Commission under the Securities Exchange Act of 1934

Note 3:Entity definitionsSection 721 of the Act amended the CEA by adding the defined terms “swap dealer” and “major swap participants.” The Commodity Futures Trade Commission (“CFTC”) issued finalized definitions of swap dealer and major swap participant in April 201231, along with interpretive guidance concerning these definitions.

Swap dealerSection 721 of the Act provides the base definition of a swap dealer as any entity who:

• Holdsitselfoutasadealerinswaps• Makesamarketinswaps• Regularlyentersintoswapswithcounterpartiesasanordinarycourseofbusinessforitsownaccount• Engagesinactivitycausingitselftobecommonlyknowninthetradeasadealerormarketmakerinswaps32

This definition was further defined by the CFTC to contain a de minimis exception for a certain amount of swap dealing. Swap dealing below this threshold would not result in an entity meeting the swap dealer definition. The CFTC determined de minimis threshold is a gross notional amount of swaps executed over the prior twelve months not exceeding $3 billion. A phase in period would exist such that the threshold would begin at $8 billion and would be studied over a two and half year period to determine an appropriate threshold.

The CFTC further stated that entering into swaps in certain situations should not be considered swap dealing. Specifically, swaps executed for the following reasons may be excluded from the notional calculation of swap dealing:

• The price risks arise from the potential change in the value of assets that the person owns, produces, manufactures, processes, or merchandises, liabilities that the person owns or anticipates incurring, or services that the person provides or purchases

• Theswaprepresentsasubstitutefortransactionsorpositionsinaphysicalmarketingchannel• Theswapiseconomicallyappropriatetothereductionoftheperson’srisksintheconductandmanagementofa

commercial enterprise• Theswapisenteredintoinaccordancewithsoundcommercialpracticesandisnotstructuredtoevadedesignationas

a swap dealer33

31 http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/defs_factsheet.pdf32 Section 721 (49) of the Act33 http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/defs_factsheet.pdf

18

Major swap participantSection 721 of the Act provides the base definition of a major swap participant. Any entity who:

• “Maintains a substantial position in any of the major swap categories, excluding positions held for hedging or mitigating commercial risk

• Apersonwhoseoutstandingswapscreatesubstantialcounterpartyexposurethatcouldhaveseriousadverseeffectson the financial markets

• Anyfinancialentitythatishighlyleveragedrelativetotheamountofcapitalsuchentityholdsandthatisnotsubjecttocapital requirements established by the appropriate Federal banking agency and that maintains a substantial position in any of the major swap categories”34

The four major swap categories are defined as:

• Rateswaps(anyswapbasedonreferenceratessuchasinterestratesorcurrencyexchangerates)• Creditswaps(anyswapbasedoninstrumentsofindebtednessorrelatedindices)• Equityswaps(anyswapbasedonequitiesorequityindices)• Othercommodityswaps(anyswapnotincludedinthefirstthreecategories)35

A substantial position is determined to exist if either of two thresholds is met:

1) Uncollateralized exposure, after the impact of netting agreements: An entity with an uncollateralized exposure exceeding $1 billion in each of the credit, equity and other swap categories, and $3 billion in the rate category, would be determined to be a major swap participant.

2) Uncollateralized exposure plus potential future exposure: An entity with an uncollateralized exposure plus future potential exposure exceeding $2 billion in each of the credit, equity and other swap categories, and $6 billion in the rate category, would be determined to be a major swap participant. Future exposure would be determined by:

• Multiplyingthetotalnotionalprincipalamountoftheperson’sswappositionsbyspecifiedriskfactorpercentages(ranging from ½% to 15%)

• Discountingtheamountofpositionssubjecttomasternettingagreementsbyafactorrangingbetweenzeroand60%

• Iftheswapsareclearedorsubjecttodailymark-to-marketmargining,furtherdiscountingtheamountofthepositions by 80%36

34 Section 721 (33) of the Act35 http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/defs_factsheet.pdf36 http://www.cftc.gov/ucm/groups/public/@newsroom/documents/file/defs_factsheet.pdf

An interpretation of the “hedge or mitigate risk” criteria and the impact to compliance with the Dodd-Frank Act 19

Clint CarlinPartnerDeloitte&ToucheLLP+1 713 982 [email protected]

William HedermanDirector Deloitte&ToucheLLP+1 703 885 [email protected]

John BayneSenior ManagerDeloitte&ToucheLLP+1 713 982 [email protected]

Contacts

This document contains general information only and Deloitte is not, by means of this document, rendering accounting, business, financial, investment, legal, tax, or other professional advice or services. This document is not a substitute for such professional advice or services, nor should it be used as a basis for any decision or action that may affect your business. Before making any decision or taking any action that may affect your business, you should consult a qualified professional advisor. Deloitte, its affiliates, and related entities shall not be responsible for any loss sustained by any person who relies on this document.

Copyright © 2012 Deloitte Development LLC. All rights reserved.Member of Deloitte Touche Tohmatsu Limited