Embed Size (px)

Citation preview

An Integrated Speciality Steel

&

Global Wire Rope Company

STRENGTH THROUGH INTEGRATION

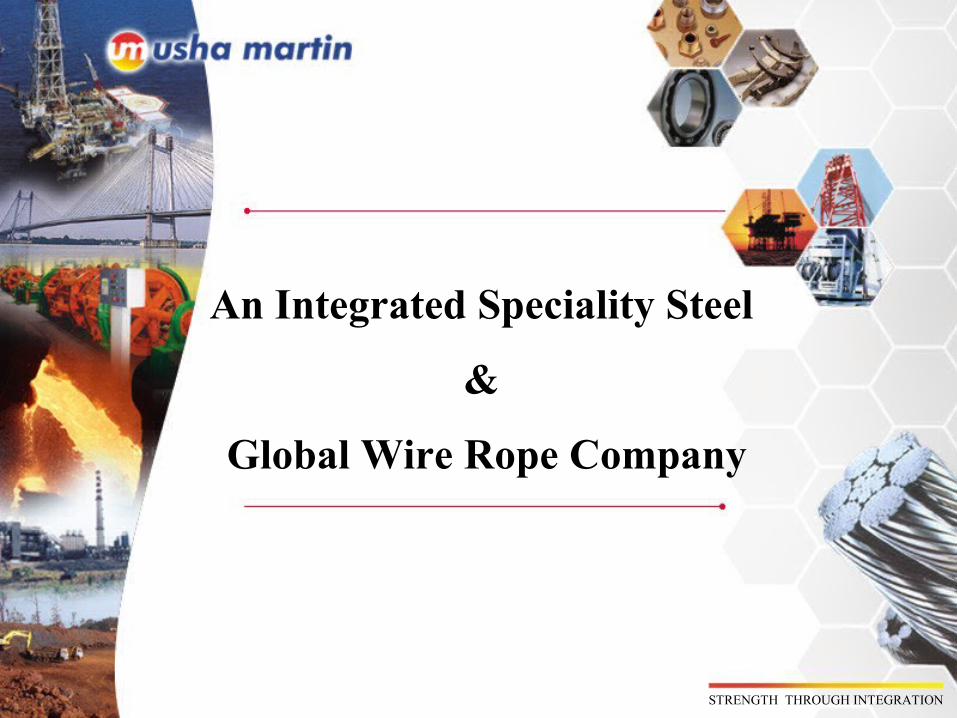

Business Profile – FY09

SPECIALITY STEEL & VALUE ADDED STEEL PRODUCTS

SERVICES

Rs 4,499Cr (USD 967 MN) TURNOVER WITH GLOBAL OPERATION

DISTRIBUTIONUMLSTAND ALONE

Rs. 238CR (USD 51 MN) – 5%Rs. 4,261 CR (USD 916 MN) – 95%

TELECOMMUNICATION

CABLE

Rs.3,085 CR (USD 663 MN)

OVERSEAS MANUFACTURING

Rs.445 CR (USD 96 MN)

Rs. 476CR (USD 102 MN)

Rs. 255 CR (USD 55 MN)

STEEL

Rs. 1807 CR (USD 388 MN)

VALUE ADDDED PRODUCTS

Rs. 1278 CR (USD 275 MN)

UML Stand alone - Rs 3,085 CrUML Stand alone - Rs 3,085 Cr

Subsidiaries – Rs 1,414 CrSubsidiaries – Rs 1,414 Cr

Note: Turnover reported above represents Gross level of activities and are without adjusting inter unit/company sales

STRENGTH THROUGH INTEGRATION

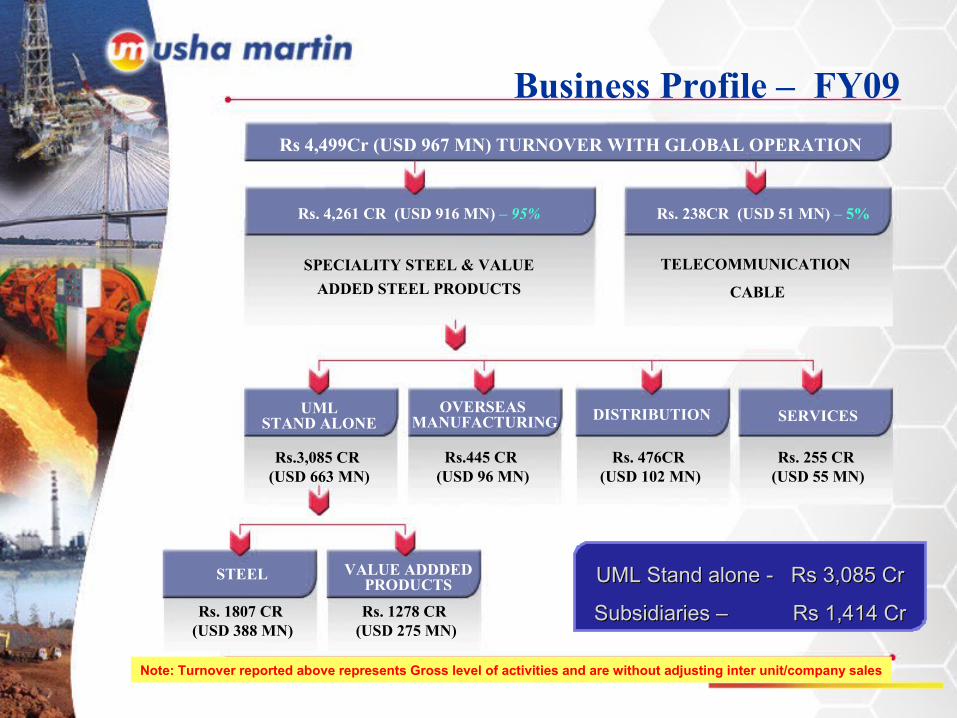

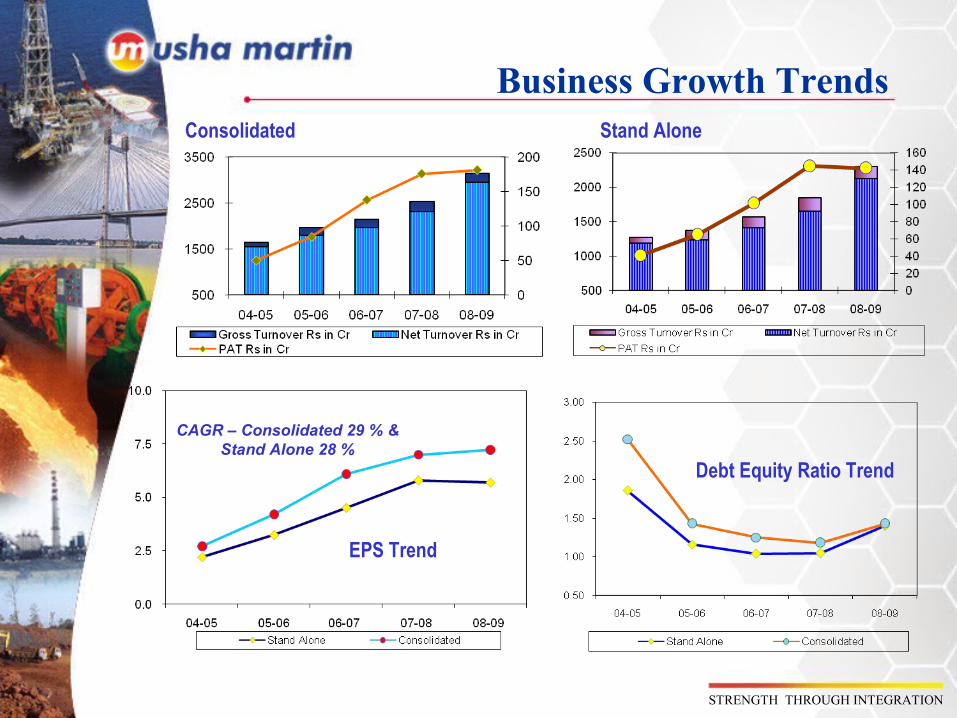

Consolidated Financial Performance Trends at a Glance

Rs in CrParticulars 03-04(A) 04-05(A) 05-06(A) 06-07(A) 07-08(A) 08-09 (A) CAGR %

Gross Turnover 1,145 1,648 1,969 2,148 2,528 3,147 22%

Net Turnover 1,063 1,550 1,802 1,965 2,309 2,950 23%

Profit Before Tax 26 71 126 183 247 281 62%

PAT 16 50 84 137 175 185 63%

Capial Employed (Excl CWIP) 1,529 1,535 1,545 1,698 1,767 1,773

ROCE 7.4% 10.2% 14.1% 16.2% 19.7% 23.8%

RONW 4.3% 13.1% 20.3% 22.3% 21.6% 19.2%

Total Debt Equity Ratio 2.96 2.52 1.43 1.25 1.18 1.43

EPS - Fully Diluted (FV Rs 1/-) 0.88 2.71 3.36 5.48 7.01 7.41 53%

Interest Cover 2.2 2.8 3.4 4.0 4.4 3.8

STRENGTH THROUGH INTEGRATION

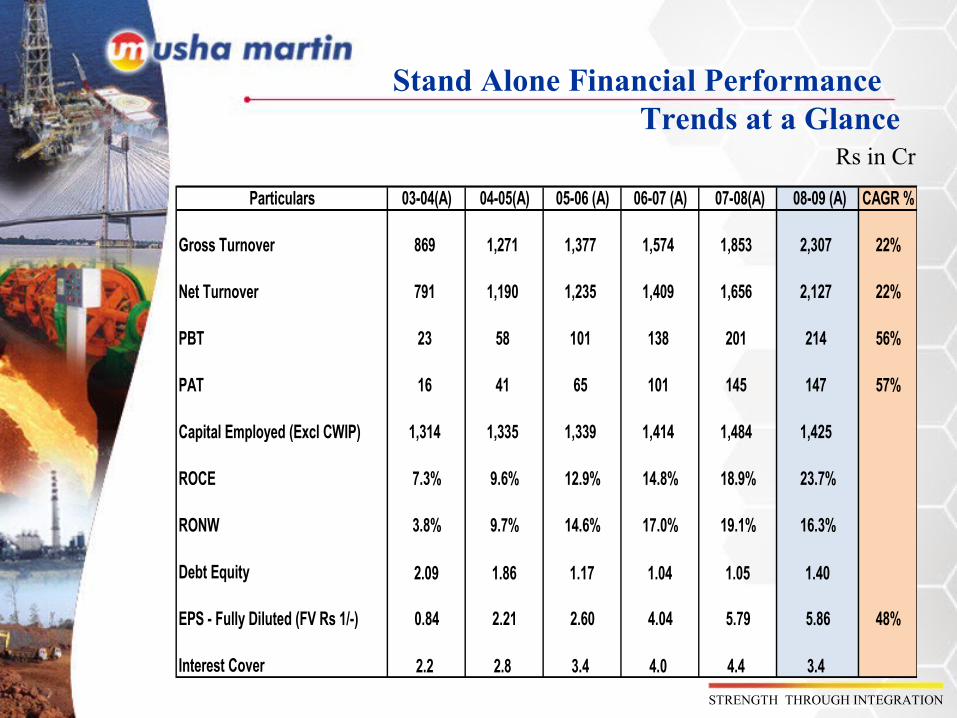

Stand Alone Financial Performance Trends at a Glance

Rs in Cr

Particulars 03-04(A) 04-05(A) 05-06 (A) 06-07 (A) 07-08(A) 08-09 (A) CAGR %

Gross Turnover 869 1,271 1,377 1,574 1,853 2,307 22%

Net Turnover 791 1,190 1,235 1,409 1,656 2,127 22%

PBT 23 58 101 138 201 214 56%

PAT 16 41 65 101 145 147 57%

Capital Employed (Excl CWIP) 1,314 1,335 1,339 1,414 1,484 1,425

ROCE 7.3% 9.6% 12.9% 14.8% 18.9% 23.7%

RONW 3.8% 9.7% 14.6% 17.0% 19.1% 16.3%

Debt Equity 2.09 1.86 1.17 1.04 1.05 1.40

EPS - Fully Diluted (FV Rs 1/-) 0.84 2.21 2.60 4.04 5.79 5.86 48%

Interest Cover 2.2 2.8 3.4 4.0 4.4 3.4

STRENGTH THROUGH INTEGRATION

Consolidated

EPS Trend

Debt Equity Ratio Trend

Stand Alone

CAGR – Consolidated 29 % & Stand Alone 28 %

Business Growth Trends

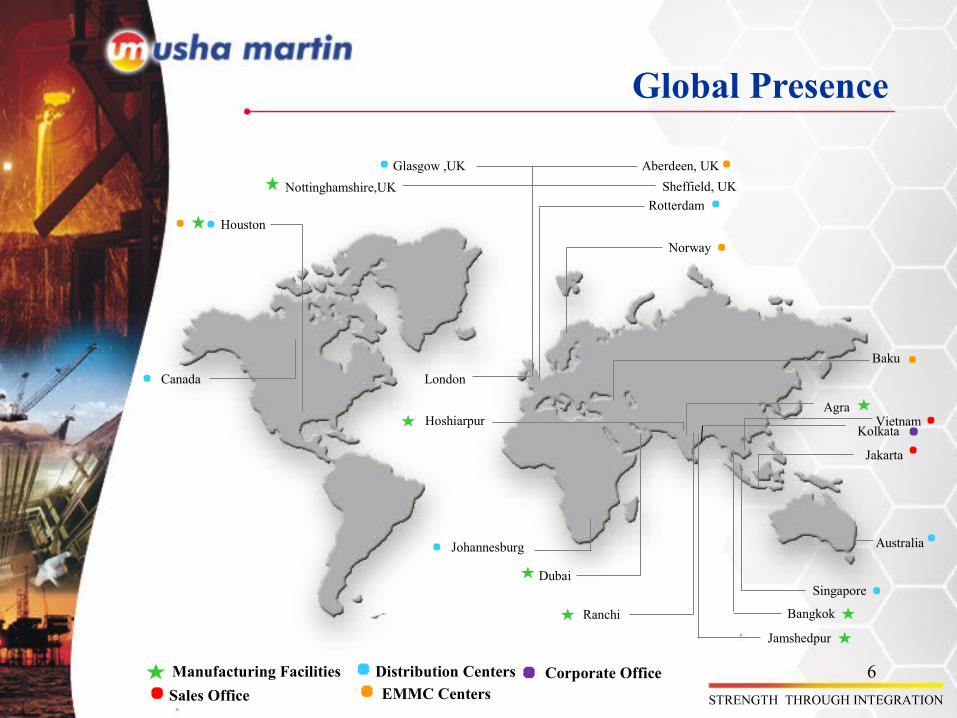

Global Presence

Aberdeen, UKGlasgow ,UK

Norway

Baku

Houston

Dubai

Jamshedpur

Bangkok

Johannesburg

Singapore

Sales Office EMMC CentersManufacturing Facilities Distribution Centers

Nottinghamshire,UK

Vietnam

Ranchi

Australia

STRENGTH THROUGH INTEGRATION

Canada

Hoshiarpur

Jakarta

RotterdamSheffield, UK

Agra

Kolkata

Corporate Office

London

6

STRENGTH THROUGH INTEGRATION

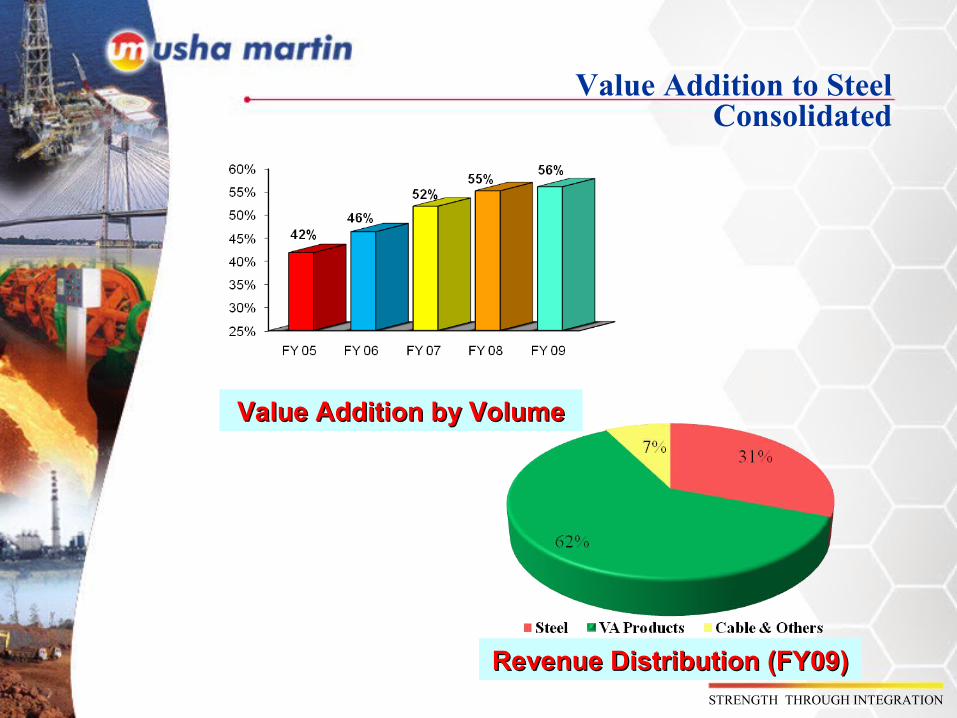

Value Addition to Steel Consolidated

Value Addition by VolumeValue Addition by Volume

Revenue Distribution (FY09)Revenue Distribution (FY09)

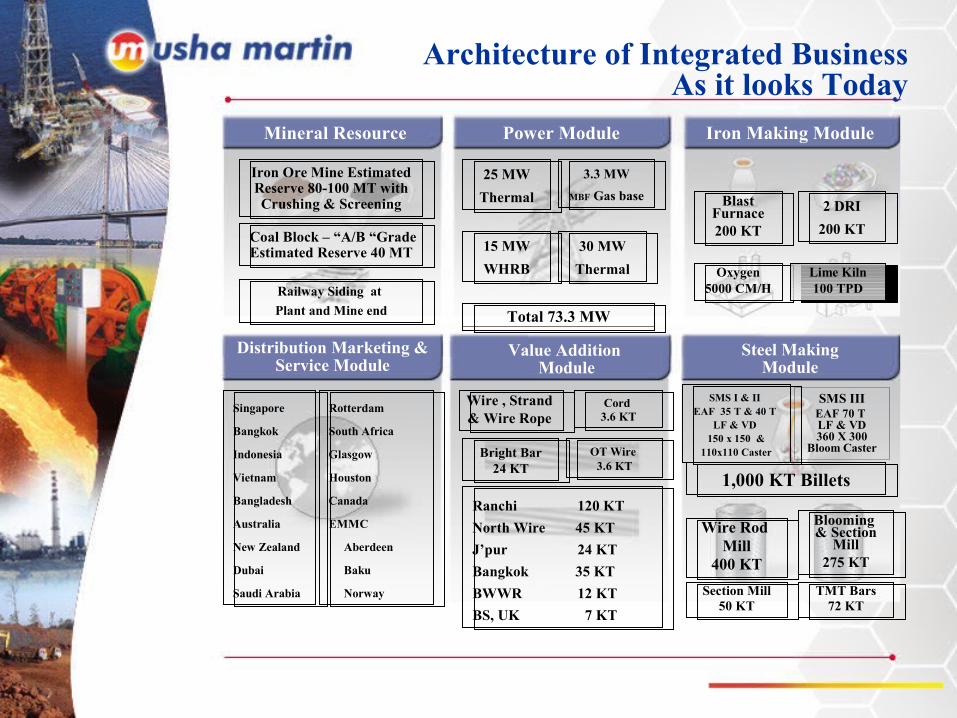

Architecture of Integrated Business As it looks Today

Mineral Resource Power Module Iron Making Module

Distribution Marketing & Service Module

Value Addition Module

Steel MakingModule

Wire , Strand & Wire Rope

Blooming & Section

Mill275 KT

Cord 3.6 KT

Ranchi 120 KTNorth Wire 45 KTJ’pur 24 KTBangkok 35 KTBWWR 12 KTBS, UK 7 KT

Bright Bar24 KT

OT Wire 3.6 KT

Iron Ore Mine Estimated Reserve 80-100 MT with Crushing & Screening

25 MWThermal

3.3 MWMBF Gas base

15 MWWHRB

Singapore

Bangkok

Indonesia

Vietnam

Bangladesh

Australia

New Zealand

Dubai

Saudi Arabia

Rotterdam

South Africa

Glasgow

Houston

Canada

EMMC

Aberdeen

Baku

Norway

30 MWThermal

Total 73.3 MW

Blast Furnace200 KT

2 DRI200 KT

1,000 KT Billets

Wire Rod Mill

400 KTSection Mill

50 KTTMT Bars

72 KT

Oxygen5000 CM/H

Lime Kiln100 TPDRailway Siding at

Plant and Mine end

Coal Block – “A/B “GradeEstimated Reserve 40 MT

SMS I & II EAF 35 T & 40 T

LF & VD 150 x 150 &

110x110 Caster

SMS IIIEAF 70 T LF & VD 360 X 300

Bloom Caster

STRENGTH THROUGH INTEGRATION

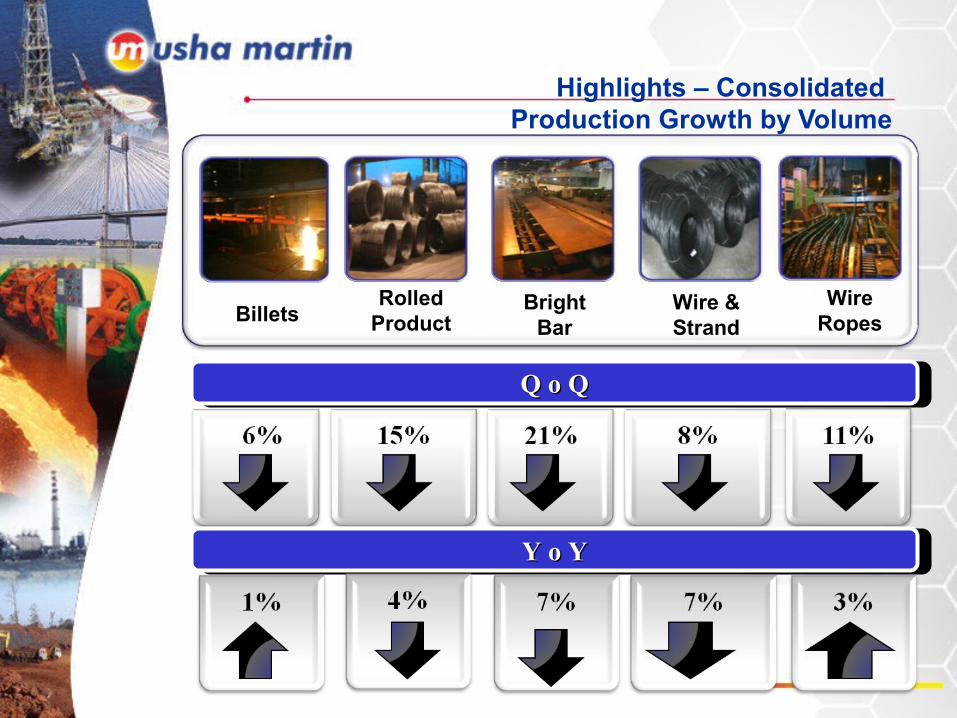

Highlights – Consolidated Production Growth by Volume

BilletsRolled

ProductBright

BarWire & Strand

Wire Ropes

Q o QQ o Q

Y o YY o Y

Highlights – Stand Alone Financials

8%

29%

52%

1%

STRENGTH THROUGH INTEGRATION

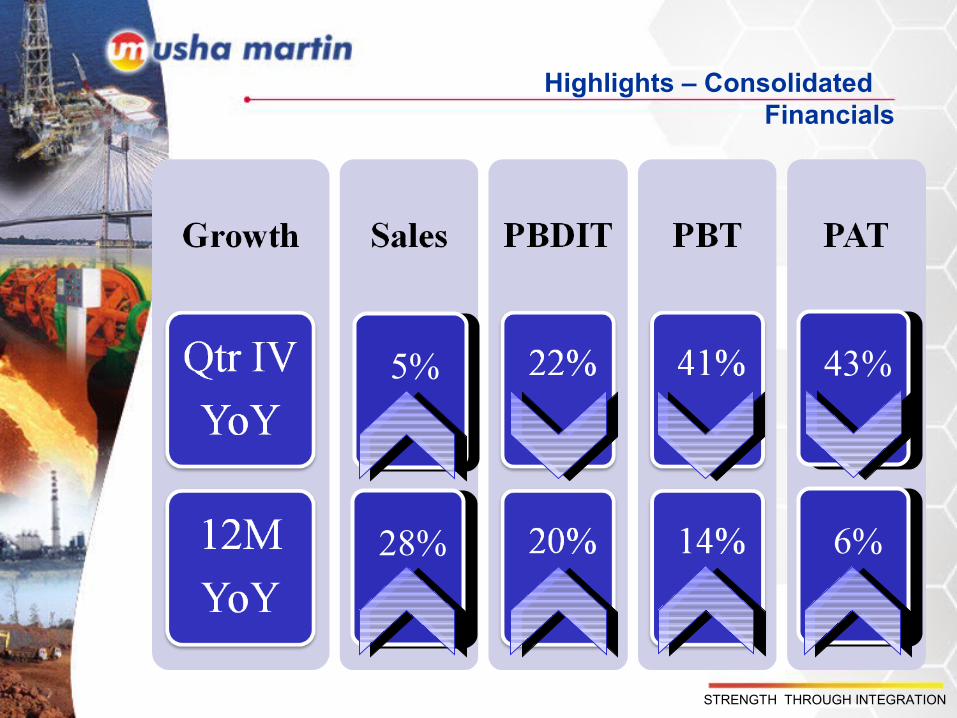

Highlights – Consolidated Financials

5%

28%

43%

6%

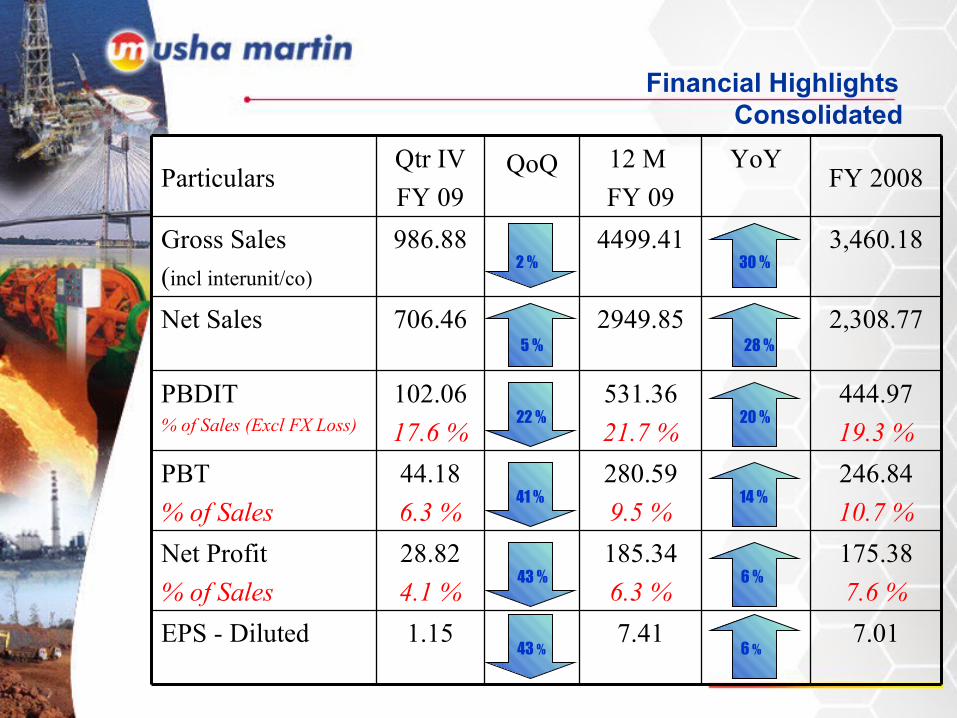

Financial Highlights Consolidated

ParticularsQtr IVFY 09

QoQ 12 M FY 09

YoYFY 2008

Gross Sales(incl interunit/co)

986.88 4499.41 3,460.18

Net Sales 706.46 2949.85 2,308.77

PBDIT% of Sales (Excl FX Loss)

102.0617.6 %

531.3621.7 %

444.9719.3 %

PBT% of Sales

44.186.3 %

280.599.5 %

246.8410.7 %

Net Profit% of Sales

28.824.1 %

185.346.3 %

175.387.6 %

EPS - Diluted 1.15 7.41 7.01

5 %

22 %

41 %

43 %

43 %

2 %

28 %

20 %

14 %

6 %

6 %

30 %

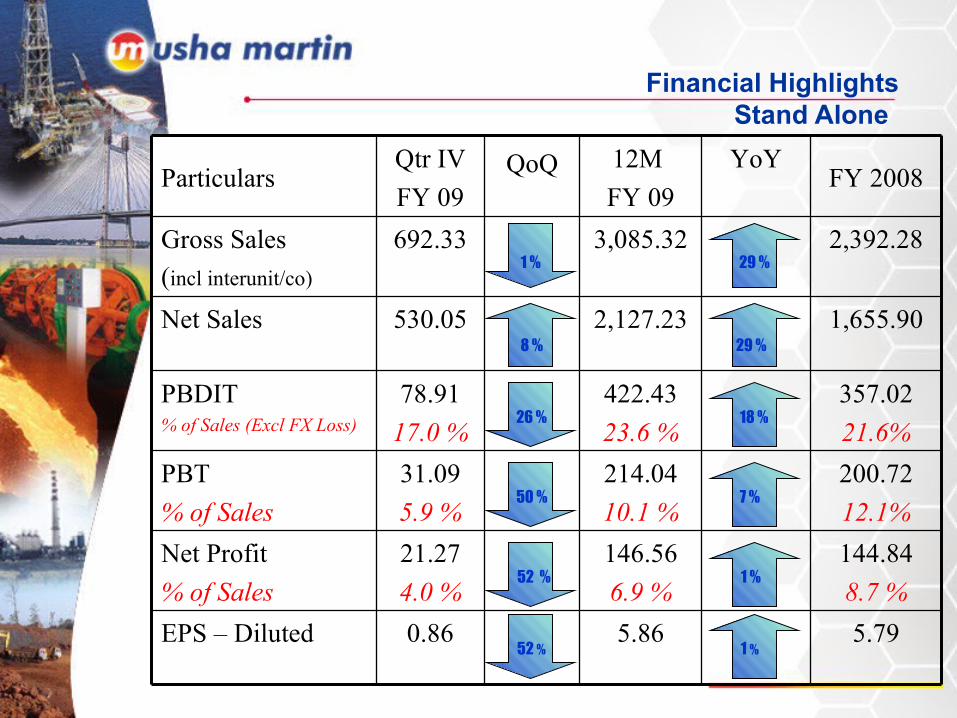

Financial Highlights Stand Alone

ParticularsQtr IVFY 09

QoQ 12M FY 09

YoYFY 2008

Gross Sales(incl interunit/co)

692.33 3,085.32 2,392.28

Net Sales 530.05 2,127.23 1,655.90

PBDIT% of Sales (Excl FX Loss)

78.9117.0 %

422.4323.6 %

357.0221.6%

PBT% of Sales

31.095.9 %

214.0410.1 %

200.7212.1%

Net Profit% of Sales

21.274.0 %

146.566.9 %

144.848.7 %

EPS – Diluted 0.86 5.86 5.79

29 %

18 %

7 %

1 %

1 %

29 %

8 %

26 %

50 %

52 %

52 %

1 %

STRENGTH THROUGH INTEGRATION

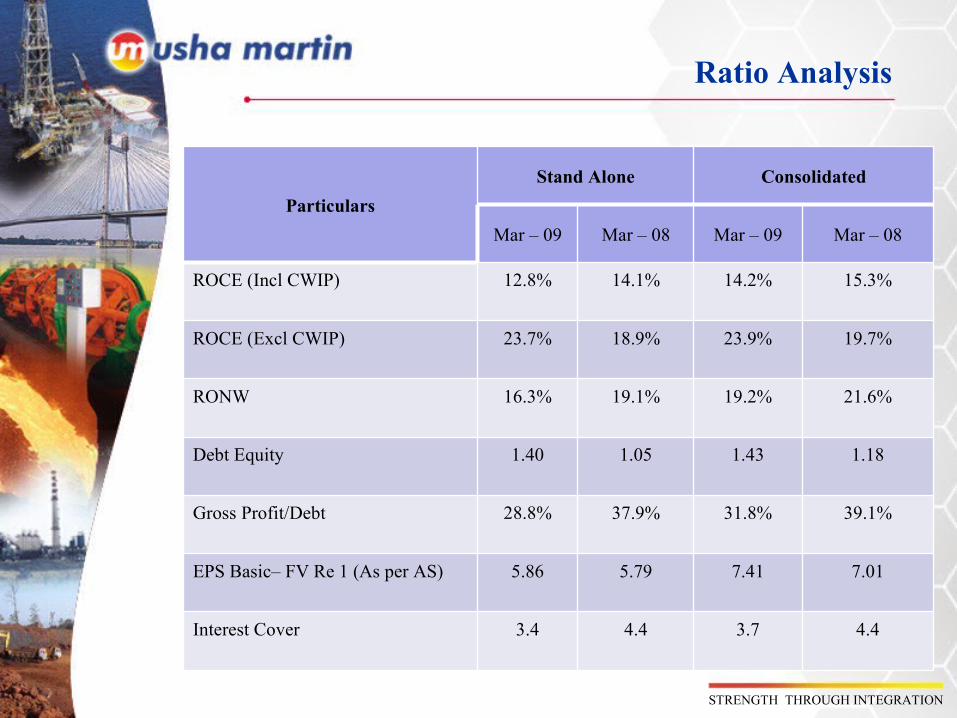

ParticularsStand Alone Consolidated

Mar – 09 Mar – 08 Mar – 09 Mar – 08

ROCE (Incl CWIP) 12.8% 14.1% 14.2% 15.3%

ROCE (Excl CWIP) 23.7% 18.9% 23.9% 19.7%

RONW 16.3% 19.1% 19.2% 21.6%

Debt Equity 1.40 1.05 1.43 1.18

Gross Profit/Debt 28.8% 37.9% 31.8% 39.1%

EPS Basic– FV Re 1 (As per AS) 5.86 5.79 7.41 7.01

Interest Cover 3.4 4.4 3.7 4.4

Ratio Analysis

STRENGTH THROUGH INTEGRATION

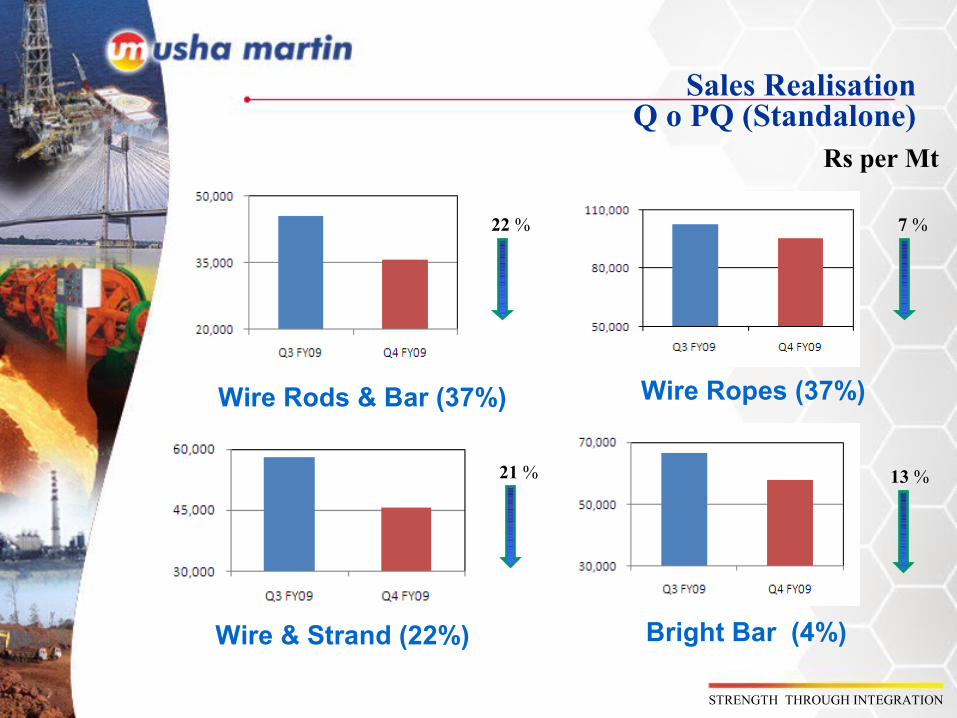

Sales RealisationQ o PQ (Standalone)

Rs per Mt

Wire Rods & Bar (37%)

Bright Bar (4%)Wire & Strand (22%)

Wire Ropes (37%)

21 % 13 %

7 %22 %

STRENGTH THROUGH INTEGRATION

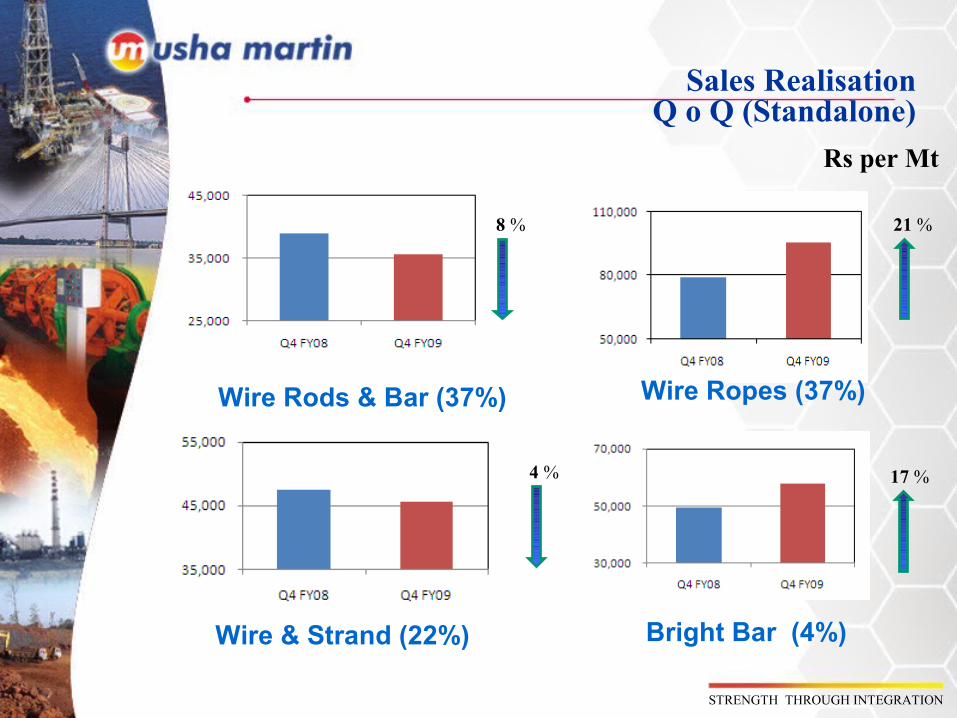

Sales RealisationQ o Q (Standalone)

Rs per Mt

Wire Rods & Bar (37%)

Bright Bar (4%)Wire & Strand (22%)

Wire Ropes (37%)

4 % 17 %

21 %8 %

STRENGTH THROUGH INTEGRATION

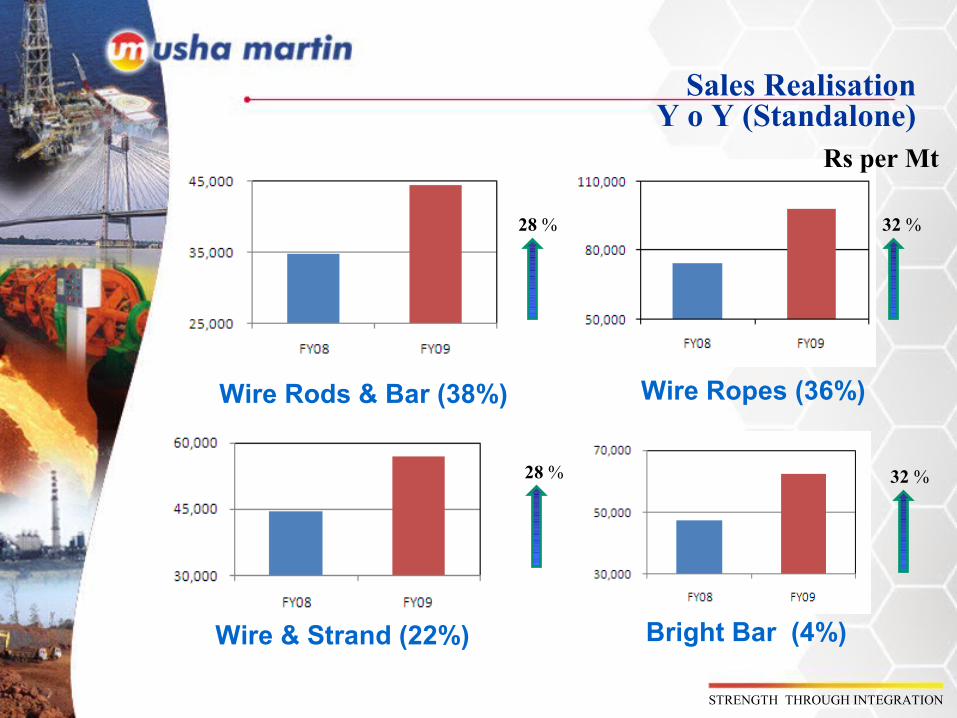

Sales RealisationY o Y (Standalone)

Rs per Mt

Wire Rods & Bar (38%)

Bright Bar (4%)Wire & Strand (22%)

Wire Ropes (36%)

28 % 32 %

32 %28 %

STRENGTH THROUGH INTEGRATION

Key Highlights

harp reduction in product and raw material prices in

second half of the financial year

olatility in foreign exchange – Loss of Rs 78.30 Cr in the

year against gain of Rs 20.33 Cr in the previous year

ull absorption of high cost inventory

ontinued focus on export market

roduct Mix diversification

igh cost of funds

ontinued focus on Value Addition

STRENGTH THROUGH INTEGRATION

STRENGTH THROUGH INTEGRATION

Strategic Growth Plan

Steel Capacity Expansion Steel capacity expansion to a million ton by FY’11. Market / Product diversification Full integration of iron ore and coal Metallic's integration Power capacity enhancement to 120 MW

Value Added Products – Maintain share at 50% Increasing Wire rope , LRPC and Bright bar production

significantly Strengthening global operation

Lime Kiln & Producer Gas

100 TPD

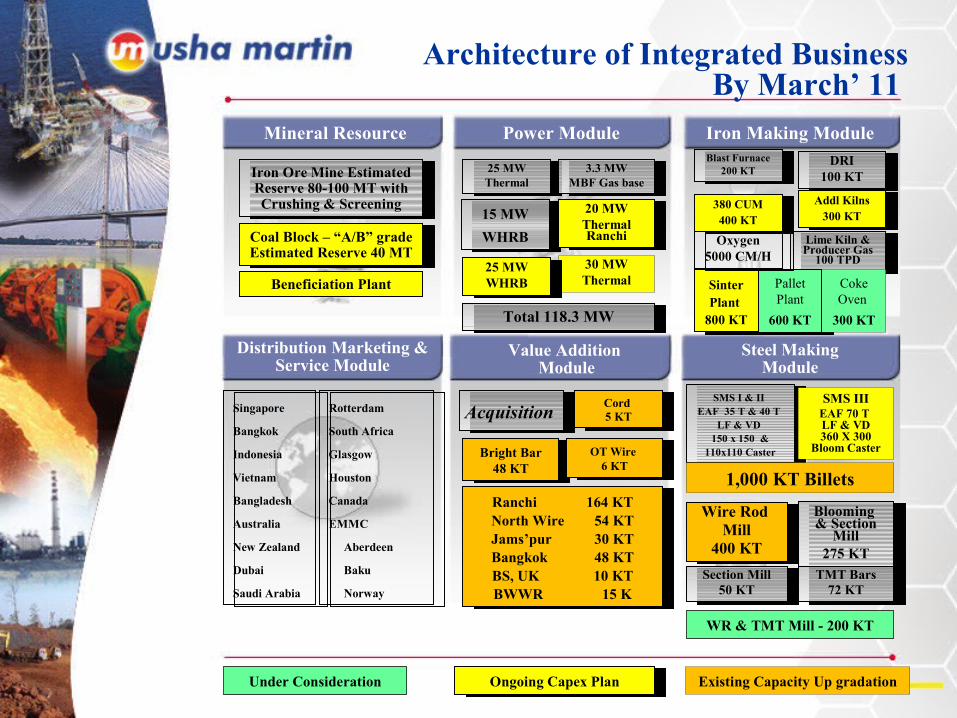

Architecture of Integrated BusinessBy March’ 11

Mineral Resource Power Module Iron Making Module

Distribution Marketing & Service Module

Value Addition Module

Steel MakingModule

Acquisition SMS I & II

EAF 35 T & 40 T LF & VD

150 x 150 & 110x110 Caster

SMS IIIEAF 70 T LF & VD 360 X 300

Bloom Caster

Existing Capacity Up gradation

Blooming & Section

Mill275 KT

Cord 5 KT

Ranchi 164 KTNorth Wire 54 KTJams’pur 30 KTBangkok 48 KTBS, UK 10 KTBWWR 15 K

Bright Bar48 KT

OT Wire 6 KT

Ongoing Capex Plan

Iron Ore Mine Estimated Reserve 80-100 MT with Crushing & Screening

25 MWThermal

3.3 MWMBF Gas base

15 MWWHRB

20 MWThermal Ranchi

Singapore

Bangkok

Indonesia

Vietnam

Bangladesh

Australia

New Zealand

Dubai

Saudi Arabia

Rotterdam

South Africa

Glasgow

Houston

Canada

EMMC

Aberdeen

Baku

Norway

30 MWThermal

Total 118.3 MW

25 MWWHRB

380 CUM400 KT

Addl Kilns300 KT

Blast Furnace200 KT

DRI100 KT

Sinter Plant

800 KT

Pallet Plant

600 KT

Coke Oven

300 KT

1,000 KT Billets

Wire Rod Mill

400 KTSection Mill

50 KTTMT Bars

72 KT

Beneficiation Plant

Coal Block – “A/B” gradeEstimated Reserve 40 MT

Under Consideration

WR & TMT Mill - 200 KT

Oxygen5000 CM/H