Embed Size (px)

Citation preview

An Industry and Economy in Transition:

Overview and Outlook for theP/C Insurance Markets/Midwest State Focus

2012 Commercial Cornerstone MeetingLa Jolla, CAMay 30, 2012

Download at www.iii.org/presentationsRobert P. Hartwig, Ph.D., CPCU, President & Economist

Insurance Information Institute 110 William Street New York, NY 10038Tel: 212.346.5520 Cell: 917.453.1885 [email protected] www.iii.org

3

Economics 2012:

The World Is Changing2012 Is the First Year Since 2005 Where Economic Perceptions and Reality in the US Will Be Positive

Potentially Enormous Benefits for P/C Insurers

3

5

P/C Insurance Exposures Grow Robustly Personal and commercial exposure growth is certain in 2012; Strongest since 2004 But restoration of destroyed exposure will take until mid-decade

P/C Industry Growth in 2012 Will Be Strongest Since 2004 Growth likely to exceed A.M. Best projection of +3.8% for 2012 No traditional “hard market” emerges in 2012

Underwriting Fundamentals Deteriorate Modestly Some pressure from claim frequency, in some severity in key lines

Increasing Private Sector Hiring Will Drive Payrolls/WC Exposures Wage growth is also positive and could modestly accelerate WC will prove to be tough to fix from an underwriting perspective

Increase in Demand for Commercial Insurance Will Accelerate in 2012 Includes workers comp, property, marine, many liability coverages Laggards: inland marine, aviation, commercial auto, surety Personal Lines: Auto leads, homeowners lags (though HO leads in NPW growth due to rates)

Investment Environment Is/Remains Much More Favorable Return of realized capital gains as a profit driver Interest rates remain low; Some upward pressured if economic strength surprises

Industry Capacity Hits a New Record by Year-End 2012 (Barring Mega-CAT)

Insurance Industry Predictions for 2012

The Strength of the Economy Will Influence P/C Insurer

Growth Opportunities

6

Growth Will Expand Workers Comp Payroll Exposure Base

6

America’s Manufacturing Renaissance?Construction Activity Still Depressed?

7

US Real GDP Growth*

* Estimates/Forecasts from Blue Chip Economic Indicators.Source: US Department of Commerce, Blue Economic Indicators 5/12; Insurance Information Institute.

2.7

%0

.9%

3.2

%2

.3%

2.9

%-0

.7%

0.6

%-4

.0%

-6.8

% -4.9

%-0

.7%

1.6

%5

.0%

3.9

%3

.8%

2.5

%2

.3%

0.4

%1

.3%

1.8

% 3.0

%2

.2%

2.2

%2

.4%

2.6

%2

.2%

2.6

%2

.9%

3.0

%4.1

%1

.1%

1.8

%2

.5% 3.6

%3

.1%

-8%

-6%

-4%

-2%

0%

2%

4%

6%

2

00

0

2

00

1

2

00

2

2

00

3

2

00

4

2

00

5

2

00

6

07

:1Q

07

:2Q

07

:3Q

07

:4Q

08

:1Q

08

:2Q

08

:3Q

08

:4Q

09

:1Q

09

:2Q

09

:3Q

09

:4Q

10

:1Q

10

:2Q

10

:3Q

10

:4Q

11

:1Q

11

:2Q

11

:3Q

11

:4Q

12

:1Q

12

:2Q

12

:3Q

12

:4Q

13

:1Q

13

:2Q

13

:3Q

13

:4Q

Demand for Insurance Continues To Be Impacted by Sluggish Economic Conditions, but the Benefits of Even Slow Growth Will Compound and

Gradually Benefit the Economy Broadly

Real GDP Growth (%)

Recession began in Dec. 2007. Economic toll of credit crunch, housing

slump, labor market contraction has been

severe but modest recovery is underway

The Q4:2008 decline was the steepest since the Q1:1982 drop of 6.8%

2012 is expected to see a modest but choppy

acceleration in growth continuing into 2013

74

.4

73

.6

73

.6

72

.2

73

.6 76

67

.8

68

.9

68

.2

67

.7 71

.6 74

.5

74

.2 77

.5

67

.5 69

.8

74

.3

71

.5

63

.7

55

.7 59

.4

60

.9 64

.1

69

.9

75

.0

75

.3

76

.2

76

.4

77

.8

40

45

50

55

60

65

70

75

80

85

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-

10

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

Ma

y-1

2

Consumer Sentiment Survey (1966 = 100)

January 2010 through May 2012

Consumer confidence has been low for years amid high unemployment, falling home prices and other factors adversely impact

consumers, but improved substantially in late 2011 and early 2012

Source: University of Michigan; Insurance Information Institute

Optimism among consumers is recovering, in part due to an

improving jobs outlook, after plunging amid the debt debate debacle and S&P downgrade

8

9

16.9

16.5

16.1

13.2

10.4

11.6 12

.7

14.5 14

.9

14.7 15

.1

15.4

15.5

15.4

16.9

16.617

.117.5

17.8

17.4

9

10

11

12

13

14

15

16

17

18

19

99 00 01 02 03 04 05 06 07 08 09 10 11 12F 13F 14F 15F 16F 17F 18-22F

(Millions of Units)

Auto/Light Truck Sales, 1999-2022F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (10/11 and 5/12); Insurance Information Institute.

Car/Light Truck Sales Will Continue to Recover from the 2009 Low Point, Bolstering the Auto Insurer Growth and the Manufacturing Sector.

New auto/light truck sales fell to the lowest level since the late 1960s. Forecast for 2012-13 is

still far below 1999-2007 average of 17 million units, but a recovery is underway.

Job growth and improved credit market conditions will boost auto sales in

2012 and beyond

10

(Millions of Units)

New Private Housing Starts, 1990-2022F

1.4

8

1.4

7 1.6

2

1.6

4

1.5

7

1.6

0 1.7

1 1.8

5 1.9

6 2.0

7

1.8

0

1.3

6

0.9

1

0.5

5

0.5

9

0.6

1 0.7

3 0.8

7

1.3

4

1.2

3

1.3

2

1.3

81

.42

1.3

51.4

6

1.2

9

1.2

0

1.0

11.1

9

0.3

0.5

0.7

0.9

1.1

1.3

1.5

1.7

1.9

2.1

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12F13F14F15F16F17F 18-22F

Source: U.S. Department of Commerce; Blue Chip Economic Indicators (10/11 and 5/12); Insurance Information Institute.

Little Exposure Growth Likely for Homeowners Insurers Until at least 2014. Also Affects Commercial Insurers with Construction Risk Exposure, Surety

New home starts plunged

72% from 2005-2009; A

net annual decline of 1.49 million units, lowest since

records began in 1959

The plunge and lack of recovery in homebuilding and in construction in general

is holding back payroll exposure growth

Job growth, improved credit

market conditions and demographics

will eventually boost home construction

11

Construction Employment,Jan. 2010—Apr. 2012*

*Seasonally adjustedSources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

5,59

3

5,52

9 5,55

2

5,55

9

5,51

8

5,50

7

5,49

1 5,51

1

5,49

2

5,49

9

5,48

8

5,47

7

5,45

6

5,48

9

5,49

6

5,49

5

5,49

8

5,49

5

5,50

8

5,49

8

5,52

8

5,51

9

5,52

0 5,54

6 5,56

4

5,56

3

5,56

0

5,55

8

5,400

5,450

5,500

5,550

5,600

5,650

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

2/30

/210

2

Mar

-12

Apr

-12

Construction employment is still below where it was in

Jan. 2010. In a normal recovery, construction employment would be

growing robustly

(Thousands)

12

Value of Construction Put in Place, Mar. 2012 vs. Mar. 2011*

-3.2%

-17.0%

-2.8%

6.0%

11.5%

7.4%

15.2%

-20%

-15%

-10%

-5%

0%

5%

10%

15%

20%

TotalConstruction

Total PrivateConstruction

Residential--Private

Non-Residential--

Private

Total PublicConstruction

Residential-Public

Non-Residential--

Public

Overall Construction Activity is Up, But Growth Is Entirely in the Private Sector as State/Local Government Budget Woes Continue

Growth (%)

Private sector construction activity is up in both the residential and nonresidential segments

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

Private: +11.5% Public: -3.2%

Public sector construction activity remains depressed

13

Value of Private Construction Put in Place, by Segment, Mar. 2012 vs. Mar. 2011*

9.5%7.0%

17.7%

-6.8%

9.4% 7.5%

-2.5%

22.1%

38.5%

11.5%7.4%

15.2%

2.9%8.6%

-10%-5%0%5%

10%15%20%25%30%35%40%45%

To

tal

Pri

vate

Co

nst

ruct

ion

Res

iden

tial

To

tal

No

nre

sid

enti

al

Lo

dg

ing

Off

ice

Co

mm

erci

al

Hea

lth

Car

e

Ed

uca

tio

nal

Rel

igio

us

Am

use

men

t &

Rec

.

Tra

nsp

ort

atio

n

Co

mm

un

icat

ion

Po

wer

Man

ufa

ctu

rin

g

Private Construction Activity is Up in Most Segments, Including Residential Construction

Growth (%) Private sector construction activity is up by double

digits in many segments after plunging during the

“Great Recession”

*seasonally adjustedSource: U.S. Census Bureau, http://www.census.gov/construction/c30/c30index.html ; Insurance Information Institute.

58

.3

57

.1

60

.4

59

.6

57

.8

55

.3

55

.1

55

.2

55

.3 56

.9 58

.2

58

.5 60

.8

61

.4

59

.7

59

.7

54

.2 55

.8

51

.4 52

.5

52

.5

51

.8

52

.2 53

.1 54

.1

52

.4 53

.4 54

.8

40

45

50

55

60

65

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-

10

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

ISM Manufacturing Index(Values > 50 Indicate Expansion)

January 2010 through April 2012

The manufacturing sector has been expanding and adding jobs. The question is whether this will continue.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/mfgrob.cfm; Insurance Information Institute.

Optimism among manufacturers was

increasing in late 2011 and into early 2012

15

16

$200,000

$300,000

$400,000

$500,000

Dollar Value* of Manufacturers’ Shipments Monthly, Jan. 1992—Mar. 2012

*seasonally adjustedSource: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Monthly shipments are nearly back to peak (in July 2008, 8 months into the recession). Trough in May 2009. Growth from trough to March 2012 was 31%. This

growth leads to gains in many commercial exposures: WC, Commercial Auto, Marine, Property and Various Liability Coverages

The value of Manufacturing Shipments in Mar. 2012 was up 31% to $466B from its May 2009 trough.

Dec. figure is only 3.9% below its previous record high in July 2008.

$ Millions

16

17

Manufacturing Growth for Selected Sectors, 2012 vs. 2011*

7.2%

12.7%

6.1%4.5%

13.5%

4.0%

9.0%5.8%

9.8% 11.4%

7.1%

31.4%

13.5%

0%

5%

10%

15%

20%

25%

30%

35%

All

Ma

nu

fact

uri

ng

Du

rab

le M

fg.

Wo

od

Pro

du

cts

Pri

ma

ryM

eta

ls

Ma

chin

ery

Ele

ctri

cal

Eq

uip

.

Tra

nsp

ort

atio

nE

qu

ip.

No

n-D

ura

ble

Mfg

.

Fo

od

Pro

du

cts

Pe

tro

leu

m &

Co

al

Ch

em

ica

l

Pla

stic

s &

Ru

bb

er

Te

xtile

Pro

du

cts

Manufacturing Is Expanding Across a Wide Range of Sectors that Will Contribute to Growth in Insurable Exposures Including: WC, Commercial

Property, Commercial Auto and Many Liability Coverages

Growth (%)

Manufacturing of durable goods has been

especially strong

*Seasonally adjusted; Date are YTD comparing data through March 2012 to the same period in 2011.Source: U.S. Census Bureau, Full Report on Manufacturers’ Shipments, Inventories, and Orders, http://www.census.gov/manufacturing/m3/

Durables: +11.4% Non-Durables: +8.5%

19

Manufacturing Employment,Jan. 2010—Apr. 2012*

11,4

58

11,4

62

11,4

70

11,5

02

11,5

36

11,5

46

11,5

66

11,5

49

11,5

51

11,5

51

11,5

60

11,5

75

11,6

27

11,6

64

11,6

90

11,7

18

11,7

26

11,7

38

11,7

68

11,7

71

11,7

68

11,7

77

11,7

80

11,8

08

11,8

60

11,8

90

11,9

31

11,9

47

11,000

11,200

11,400

11,600

11,800

12,000

12,200

12,400

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

2/30

/210

2

Mar

-12

Apr

-12

Manufacturing employment is up by nearly 500,000 or 4.3% since Jan. 2010—a

surprising source of strength in the economy

*Seasonally adjustedSources: US Bureau of Labor Statistics at http://data.bls.gov; Insurance Information Institute.

(Thousands)

50

.7 52

.7 54

.1

54

.6

54

.8

53

.5

53

.7

52

.8 53

.9

54

.6 56 5

7.1 5

9.4

59

.7

56

.3

54

.4

53

.3

53

.4

53

.8

52

.6

52

.6

52

.6

52

.6

53

.0

56

.8

57

.3

56

.0

53

.5

40

45

50

55

60

65

Jan

-10

Fe

b-1

0

Ma

r-1

0

Ap

r-1

0

Ma

y-1

0

Jun

-10

Jul-

10

Au

g-1

0

Se

p-1

0

Oct

-10

No

v-1

0

De

c-1

0

Jan

-11

Fe

b-1

1

Ma

r-1

1

Ap

r-1

1

Ma

y-1

1

Jun

-11

Jul-

11

Au

g-1

1

Se

p-1

1

Oct

-11

No

v-1

1

De

c-1

1

Jan

-12

Fe

b-1

2

Ma

r-1

2

Ap

r-1

2

ISM Non-Manufacturing Index(Values > 50 Indicate Expansion)

January 2010 through April 2012

Non-manufacturing industries have been expanding and adding jobs. The question is whether this will continue.

Source: Institute for Supply Management at http://www.ism.ws/ismreport/nonmfgrob.cfm; Insurance Information Institute.

Optimism among non-manufacturers was

stable in late 2011 and increased in early 2012

20

21

43,6

9448

,125

69,3

0062

,436

64,0

04 71,2

77 81,2

3582

,446

63,8

5363

,235

64,8

5371

,549

70,6

4362

,304

52,3

7451

,959

53,5

4954

,027

44,3

6737

,884

35,4

7240

,099

38,5

4035

,037

34,3

1739

,201

19,6

95 28,3

2243

,546

60,8

3756

,282

47,8

0610

,998

0

10,000

20,000

30,000

40,000

50,000

60,000

70,000

80,000

90,000

80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 1112

:Q1

Business Bankruptcy Filings,1980-2012: Q1

Sources: American Bankruptcy Institute at http://www.abiworld.org/AM/AMTemplate.cfm?Section=Home&TEMPLATE=/CM/ContentDisplay.cfm&CONTENTID=61633; Insurance Information Institute

Significant Exposure Implications for All Commercial Lines as Business Bankruptcies Begin to Decline

2011 bankruptcies totaled 47,806, down 15.1% from 56,282 in 2010—the second consecutive year of decline. Business bankruptcies more

than tripled during the financial crisis. Through Q1:2012, filings are down 11.1% vs. Q1:2011

% Change Surrounding Recessions

1980-82 58.6%1980-87 88.7%1990-91 10.3%2000-01 13.0%2006-09 208.9%*

21

22

Private Sector Business Starts, 1993:Q2 – 2011:Q3*

175

186

174

180

186

192

188

187 18

918

6 190 19

419

119

9 204

202

195

196

196

206

206

201

192

198

206

206

203

211

205

212

200 20

520

420

419

720

320

920

119

219

219

320

1 204

202

210 21

220

921

6 220 22

322

022

021

022

121

220

421

820

920

720

719

919

1 193

172 17

616

918

417

5 179

188

200

183 18

7 191

203

150

160

170

180

190

200

210

220

230

93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11

Business Starts Were Down Nearly 20% in the Recession, Holding Back Most Types of Commercial Insurance Exposure, But

Are Recovering Slowly* Data through June 30, 2011 are the latest available as of May 21, 2012; Seasonally adjusted. **Annualized based on data through Q3:2011.Source: Bureau of Labor Statistics, http://www.bls.gov/news.release/cewbd.t08.htm.

(Thousands)

Business starts were up 3.5% to 561,000 in the first 9 months of 2011 vs. first 9

months of 2011. 722,000 new business starts were recorded in 2010, up 3.6% from

697,000 in 2009, which was the slowest year for new business starts since 1993

Business Starts2006: 872,0002007: 843,0002008: 790,0002009: 697,000 2010: 722,000 2011: 748,000**

22

NFIB Small Business Optimism Index

January 1985 through April 2012

Source: National Federation of Independent Business at http://www.advisorperspectives.com/dshort/charts/indicators/Sentiment.html?NFIB-optimism-index.gif ; Insurance Information Institute. 23

Small business optimism has increased but is still only at

the level it was when the Financial Crisis began

24

12 Industries for the Next 10 Years: Insurance Solutions Needed

Export-Oriented Industries

Health Sciences

Health Care

Energy (Traditional)

Alternative Energy

Petrochemical

Agriculture

Natural Resources

Technology (incl. Biotechnology)

Light Manufacturing

Insourced Manufacturing

Many industries are

poised for growth, though

insurers’ ability to

capitalize on these

industries varies widely

Shipping (Rail, Marine, Trucking)

25

Presidential Politics & the P/C Insurance Industry

How Is Profitability Affected by the President’s Political Party?

25

15.10%

9.40%

8.93%

8.65%

8.35%

7.98%

7.68%

6.98%

6.97%

6.65%

5.43%

5.03%

4.83%

4.43%

3.55%

16.43%

0% 2% 4% 6% 8% 10% 12% 14% 16% 18%

Carter

Reagan II

G.W. Bush II

Nixon

Clinton I

G.H.W. Bush

Clinton II

Reagan I

Nixon/Ford

Truman

Obama

Eisenhower I

Eisenhower II

G.W. Bush I

Johnson

Kennedy/Johnson

*Truman administration ROE of 6.97% based on 3 years only, 1950-52; ROEs for the years 2008 forward exclude mortgage and financial guaranty segments.Estimated ROE for 2012 = 7.0%. Source: Insurance Information Institute

OVERALL RECORD: 1950-2012*

Democrats 7.67%Republicans 7.97%

Party of President has marginal bearing on profitability of P/C insurance industry

P/C Insurance Industry ROE by Presidential Administration, 1950- 2012*

-5%

0%

5%

10%

15%

20%

25%

50

52

54

56

58

60

62

64

66

68

70

72

74

76

78

80

82

84

86

88

90

92

94

96

98

00

02

04

06

08

10

12

E

BLUE = Democratic President RED = Republican President

Tru

man Nixon/Ford

Ken

ned

y/

Joh

nso

n

Eis

enh

ow

er

Car

ter

Reagan/Bush I Clinton Bush II

P/C insurance Industry ROE by Presidential Party Affiliation, 1950- 2012*

*ROEs for the years 2008 forward exclude mortgage and financial guaranty segments; Estimated 2012 ROE = 7.0%Source: Insurance Information Institute

Ob

ama

28

Labor Market Trends

Massive Job Losses Sapped the Economy and Commercial/Personal

Lines Exposure, But Trend is Improving

28

29

Unemployment and Underemployment Rates: Stubbornly High in 2012, But Falling

2

4

6

8

10

12

14

16

18

Jan00

Jan01

Jan02

Jan03

Jan04

Jan05

Jan06

Jan07

Jan08

Jan09

Jan10

Jan11

Jan12

Traditional Unemployment Rate U-3

Unemployment + Underemployment Rate U-6

Unemployment stood at 8.1% in

April 2012

Unemployment peaked at 10.1% in October 2009, highest monthly rate since 1983.

Peak rate in the last 30 years:

10.8% in November -

December 1982

Source: US Bureau of Labor Statistics; Insurance Information Institute.

U-6 went from 8.0% in March

2007 to 17.5% in October 2009; Stood at 14.5%

in Apr. 2012

January 2000 through April 2012, Seasonally Adjusted (%)

Recession ended in

November 2001

Unemployment kept rising for

19 more months

Recession began in

December 2007

Stubbornly high unemployment and underemployment constrain overall economic growth, but the job market is now clearly improving

29

Apr 12

186

7921

365

127

42 15-1

09-1

465

9723

-12

-85 -58

-161

-253 -230

-257

-347

-456

-547

-734 -6

67-8

06-7

07-7

44-6

49-3

34-4

52-2

97-2

15 -186

-262

75-8

316

62

229

51 6111

714

311

2 193

128 16

711

925

726

126

410

810

2 175

5221

613

9 178 23

4 277

254

166

130

144

(1,000)

(800)

(600)

(400)

(200)

0

200

400

Jan-

07F

eb-0

7M

ar-0

7A

pr-0

7M

ay-0

7Ju

n-07

Jul-0

7A

ug-0

7S

ep-0

7O

ct-0

7N

ov-0

7D

ec-0

7Ja

n-08

Feb

-08

Mar

-08

Apr

-08

May

-08

Jun-

08Ju

l-08

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09F

eb-0

9M

ar-0

9A

pr-0

9M

ay-0

9Ju

n-09

Jul-0

9A

ug-0

9S

ep-0

9O

ct-0

9N

ov-0

9D

ec-0

9Ja

n-10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10Ju

l-10

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11F

eb-1

1M

ar-1

1A

pr-1

1M

ay-1

1Ju

n-11

Jul-1

1A

ug-1

1S

ep-1

1O

ct-1

1N

ov-1

1D

ec-1

1Ja

n-12

Feb

-12

Mar

-12

Apr

-12

Monthly Change in Private Employment

January 2008 through April 2012* (Thousands)

Private Employers Added 4.159 million Jobs Since Jan. 2010 After Having Shed 4.66 Million Jobs in 2009 and 3.81 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Monthly Losses in Dec. 08–Mar. 09 Were

the Largest in the Post-WW II Period

130,000 private sector jobs were created in April

30

0.02

30.

011

-0.0

74-0

.132

-0.2

93-0

.546

-0.7

76-1

.033

-1.3

80-1

.836

-2.3

83-3

.117

-3.7

84-4

.590

-5.2

97-6

.041

-6.6

90-7

.024

-7.4

76-7

.773

-7.9

88-8

.174

-8.4

36-8

.361

-8.4

44-8

.428

-8.3

66-8

.222

-7.9

93-7

.942

-7.8

81-7

.764

-7.6

21-7

.509

-7.3

16-7

.188

-7.0

21-6

.902 -6.3

84-6

.120

-6.0

12-5

.910

-5.7

35-5

.683

-5.4

67-5

.328

-5.1

50-4

.916

-4.6

39-4

.406

-4.2

85-4

.089

-6.6

45

-10

-8

-6

-4

-2

0

2

Dec

-07

Jan-

08F

eb-0

8M

ar-0

8A

pr-0

8M

ay-

Jun-

08Ju

l-08

Aug

-08

Sep

-08

Oct

-08

Nov

-08

Dec

-08

Jan-

09F

eb-0

9M

ar-0

9A

pr-0

9M

ay-

Jun-

09Ju

l-09

Aug

-09

Sep

-09

Oct

-09

Nov

-09

Dec

-09

Jan-

10F

eb-1

0M

ar-1

0A

pr-1

0M

ay-

Jun-

10Ju

l-10

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11F

eb-1

1M

ar-1

1A

pr-1

1M

ay-

Jun-

11Ju

l-11

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12F

eb-1

2M

ar-1

2A

pr-1

2

Mill

ion

sCumulative Change in Private Employment: Dec. 2007—Apr. 2012

December 2007 through April 2012* (Millions)

Source: US Bureau of Labor Statistics: http://www.bls.gov/ces/home.htm; Insurance Information Institute

Cumulative job losses peaked at 8.444 million

in December 2009

Cumulative job losses as of Apr. 2012 totaled

4.089 million

31

All of the jobs “lost” since President

Obama took office in Jan. 2009 have

been recouped

Private Employers Added 4.36 million Jobs Since Jan. 2010 After Having Shed 4.66 Million Jobs in 2009 and 3.81 Million in 2008 (State and Local Governments Have Shed Hundreds of Thousands of Jobs)

0

-8

40

86

518

259

109

-70

-212 -188

-201

-221

-230

-267

-282

-295

-349

-367

-446 -4

13

-427

-454

-475

-486

-488

-483

-495

-510

-600

-400

-200

0

200

400

600

Jan-

10

Feb

-10

Mar

-10

Apr

-10

May

-10

Jun-

10

Jul-1

0

Aug

-10

Sep

-10

Oct

-10

Nov

-10

Dec

-10

Jan-

11

Feb

-11

Mar

-11

Apr

-11

May

-11

Jun-

11

Jul-1

1

Aug

-11

Sep

-11

Oct

-11

Nov

-11

Dec

-11

Jan-

12

Feb

-12

Mar

-12

Apr

-12

Cumulative Change in Government Employment: Jan. 2010—Apr. 2012

January 2010 through April 2012* (Millions)

Source: US Bureau of Labor Statistics http://www.bls.gov/data/#employment; Insurance Information Institute

Cumulative job losses through Apr. 2012 totaled 510,000

33

Governments at All Levels are Under Severe Fiscal Strain As Tax Receipts Plunged and Pension Obligations Soared During the

Financial Crisis, Causing Them to Reduce Staff

Government at all levels has shed more than a half

million jobs since Jan. 2010 even as private employers created 4.36 million jobs.

Temporary Census hiring distorted 2010

figures

35

Unemployment Rates by State, April 2012:Highest 25 States*

11

.7

11

.2

10

.9

9.5

9.4

9.1

8.9

8.8

8.7

8.7

8.7

8.5

8.5

8.3

8.3

8.2

8.1

8.1

7.9

7.9

7.8

7.7

7.7

7.4

7.4

7.3

0

2

4

6

8

10

12

14

NV RI CA DC NC NJ GA SC FL IL MS NY OR KY MI AZ US WA CO IN TN CT ID OH PA MO

Un

em

plo

ym

en

t R

ate

(%

)

*Provisional figures for April 2012, seasonally adjusted.

Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In April, 37 states and the District of Columbia reported over-the-month

unemployment rate decreases, 5 had increases, and 8 had no change.

36

7.2

7.2

7.2

7.1

6.9

6.9

6.9

6.8

6.7

6.7

6.7

6.3

6.3

6.1

6.1

6.0

5.6

5.6

5.3

5.1

5.0

5.0

4.6

4.3

3.9

3.0

0

2

4

6

8

AL AR ME LA AK NM TX DE MD WV WI HI MA KS MT UT MN VA WY IA NH OK VT SD NE ND

Un

em

plo

ym

en

t R

ate

(%

)

Unemployment Rates By State, April 2012: Lowest 25 States*

*Provisional figures for April 2012, seasonally adjusted.Sources: US Bureau of Labor Statistics; Insurance Information Institute.

In April, 37 states and the District of Columbia reported over-the-month

unemployment rate decreases, 5 had increases, and 8 had no change.

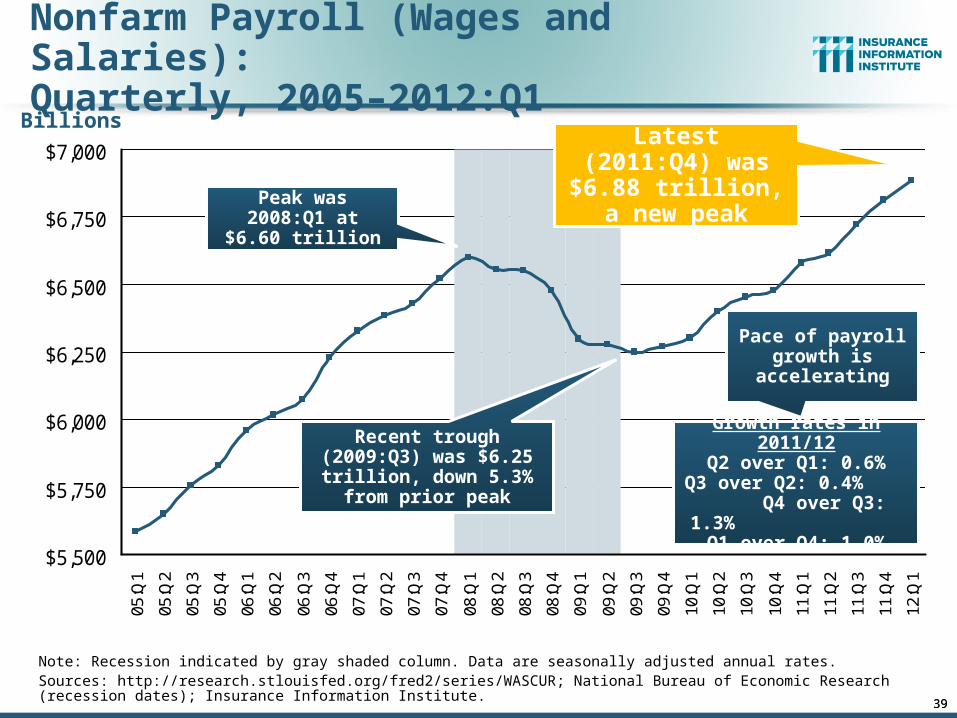

39

Nonfarm Payroll (Wages and Salaries):Quarterly, 2005–2012:Q1

Note: Recession indicated by gray shaded column. Data are seasonally adjusted annual rates.Sources: http://research.stlouisfed.org/fred2/series/WASCUR; National Bureau of Economic Research (recession dates); Insurance Information Institute.

Billions

$5,500

$5,750

$6,000

$6,250

$6,500

$6,750

$7,00005

:Q1

05:Q

2

05:Q

3

05:Q

4

06:Q

1

06:Q

2

06:Q

3

06:Q

4

07:Q

1

07:Q

2

07:Q

3

07:Q

4

08:Q

1

08:Q

2

08:Q

3

08:Q

4

09:Q

1

09:Q

2

09:Q

3

09:Q

4

10:Q

1

10:Q

2

10:Q

3

10:Q

4

11:Q

1

11:Q

2

11:Q

3

11:Q

4

12:Q

1

Peak was 2008:Q1 at $6.60 trillion

Latest (2011:Q4) was $6.88 trillion, a

new peak

Recent trough (2009:Q3) was $6.25 trillion, down

5.3% from prior peak

Growth rates in 2011/12Q2 over Q1: 0.6%

Q3 over Q2: 0.4% Q4 over Q3: 1.3%

Q1 over Q4: 1.0%

Pace of payroll growth is

accelerating

39

$2,000

$3,000

$4,000

$5,000

$6,000

$7,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*

$25

$30

$35

$40

$45

$50Wage & Salary DisbursementsWC NPW

40

Payroll Base* WC NWP

Payroll vs. Workers Comp Net Written Premiums, 1990-2011

*Private employment; Shaded areas indicate recessions. Payroll and WC premiums for 2011 is I.I.I. estimateSources: NBER (recessions); Federal Reserve Bank of St. Louis at http://research.stlouisfed.org/fred2/series/WASCUR ; NCCI; I.I.I.

Continued Payroll Growth and Rate Increases Suggest WC NWP Will Grow Again in 2012; +7.9% Growth in 2011 Was the First Gain Since 2005

7/90-3/91 3/01-11/0112/07-6/09

$Billions $Billions

WC premium volume dropped two years before

the recession began

WC net premiums written were down $14B or 29.3% to

$33.8B in 2010 after peaking at $47.8B

in 2005

+7.9% in 2011

51

P/C Insurance Industry Financial Overview

Profit Recovery Was Set Back in 2011 by High Catastrophe

Loss & Other Factors

51

P/C Net Income After Taxes1991–2011 ($ Millions)

$1

4,1

78

$5

,84

0

$1

9,3

16

$1

0,8

70

$2

0,5

98

$2

4,4

04 $

36

,81

9

$3

0,7

73

$2

1,8

65

$3

,04

6

$3

0,0

29

$6

2,4

96

$3

,04

3

$3

5,2

04

$1

9,1

50$2

8,6

72

-$6,970

$6

5,7

77

$4

4,1

55

$2

0,5

59

$3

8,5

01

-$10,000

$0

$10,000

$20,000

$30,000

$40,000

$50,000

$60,000

$70,000

$80,000

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*

2005 ROE*= 9.6% 2006 ROE = 12.7% 2007 ROE = 10.9% 2008 ROE = 0.1% 2009 ROE = 5.0% 2010 ROE = 6.6% 2011:Q3 ROAS1 = 3.5%

P-C Industry 2011 profits were down 46% to $19.2B vs. 2010, due

primarily to high catastrophe losses and as non-cat

underwriting results deteriorated

* ROE figures are GAAP; 1Return on avg. surplus. Excluding Mortgage & Financial Guaranty insurers yields a 4.6% ROAS for 2011, 7.6% for 2010 and 7.4% for 2009.Sources: A.M. Best, ISO, Insurance Information Institute

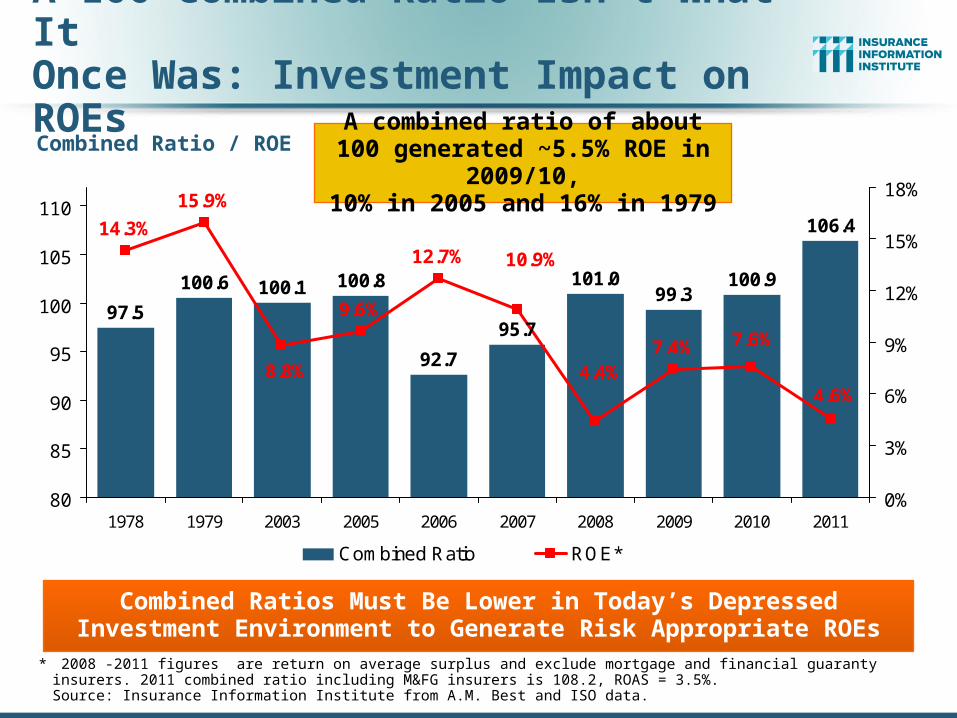

A 100 Combined Ratio Isn’t What ItOnce Was: Investment Impact on ROEs

Combined Ratio / ROE

* 2008 -2011 figures are return on average surplus and exclude mortgage and financial guaranty insurers. 2011 combined ratio including M&FG insurers is 108.2, ROAS = 3.5%. Source: Insurance Information Institute from A.M. Best and ISO data.

97.5

100.6 100.1 100.8

92.7

101.099.3

100.9

106.4

95.7

4.6%

7.6%7.4%4.4%

9.6%

15.9%

14.3%

12.7% 10.9%

8.8%

80

85

90

95

100

105

110

1978 1979 2003 2005 2006 2007 2008 2009 2010 20110%

3%

6%

9%

12%

15%

18%

Combined Ratio ROE*

Combined Ratios Must Be Lower in Today’s DepressedInvestment Environment to Generate Risk Appropriate ROEs

A combined ratio of about 100 generated ~5.5% ROE in 2009/10,

10% in 2005 and 16% in 1979

-5%

0%

5%

10%

15%

20%

25%

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

*

Profitability Peaks & Troughs in the P/C Insurance Industry, 1975 – 2011*

*Profitability = P/C insurer ROEs are I.I.I. estimates. 2011 figure is an estimate based on ROAS data. Note: Data for 2008-2011 exclude mortgage and financial guaranty insurers. For 2011:Q3 ROAS = 3.5% including M&FG.Source: Insurance Information Institute; NAIC, ISO, A.M. Best.

1977:19.0% 1987:17.3%

1997:11.6%2006:12.7%

1984: 1.8% 1992: 4.5% 2001: -1.2%

10 Years

10 Years9 Years

2011:4.6%*

History suggests next ROE peak will be in 2016-2017

ROE

1975: 2.4%

55

ROE: Property/Casualty Insurance vs. Fortune 500, 1987–2011*

* Excludes Mortgage & Financial Guarantee in 2008 - 2011; 2012 Fortune 500 figure is an III estimate.Sources: ISO, Fortune; Insurance Information Institute.

-5%

0%

5%

10%

15%

20%

87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*

P/C Profitability Is Both by Cyclicality and Ordinary Volatility

Hugo

Andrew

Northridge

Lowest CAT Losses in 15 Years

Sept. 11

Katrina, Rita, Wilma

4 Hurricanes

Financial Crisis*

(Percent)

56

ROE vs. Equity Cost of Capital:U.S. P/C Insurance:1991-2011*

* Return on average surplus in 2008-2011 excluding mortgage and financial guaranty insurers.Source: The Geneva Association, Insurance Information Institute

-2%

0%

2%

4%

6%

8%

10%

12%

14%

16%

18%

91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08* 09* 10* 11*

ROE Cost of Capital

-13

.2 p

ts +1

.7 p

ts

+2

.3 p

ts

-9.0

pts

-6.4

pts

-3.2

pts

The P/C Insurance Industry Fell WellShort of Its Cost of Capital Every Year Since 2008

US P/C Insurers Missed Their Cost of Capital by an Average 6.7 Points from 1991 to 2002, but on Target or Better

2003-07, Fell Short in 2008-2010

The Cost of Capital is the Rate of Return Insurers Need to

Attract and Retain Capital to the Business

(Percent)

-2.4

pts

-7.3

pts

58

Profitability and Growth in Illinois, Iowa, Kansas, Michigan, Minnesota,

Missouri, Nebraska, South Dakota and Wisconsin P/C Insurance Markets

Analysis by Line and Nearby State Comparisons

59

RNW All Lines: IL, IA, KS, MI, MN, MO, NE, SD, WI vs. U.S., 2001-2010

Sources: NAIC.

-40%

-20%

0%

20%

40%

01 02 03 04 05 06 07 08 09 10

US IL IA KS MI MN MO NE SD WI

(Percent)

All Lines: 10-Year Average RNW IL, IA, KS, MI, MN, MO, NE, SD, WI vs. U.S.

6.4%

7.1%7.7%

8.5%9.1%

10.1%

10.9%11.4%

5.6%

7.1%

0% 2% 4% 6% 8% 10% 12%

Iowa

Kansas

South Dakota

Nebraska

Wisconsin

Missouri

Minnesota

U.S.

Illinois

Michigan

Source: NAIC, Insurance Information Institute

2001-2010

Comm. Auto: 10-Year Average RNW IL, IA, KS, MI, MN, MO, NE, SD, WI vs. U.S.

8.9%

9.7%10.3%

12.8%13.0%

14.5%14.8%

15.4%

8.9%

9.2%

0% 5% 10% 15% 20%

Minnesota

South Dakota

Kansas

Iowa

Wisconsin

Nebraska

Illinois

U.S.

Missouri

Michigan

Source: NAIC, Insurance Information Institute

2001-2010

Comm. M-P: 10-Year Average RNW IL, IA, KS, MI, MN, MO, NE, SD, WI vs. U.S.

6.7%

8.3%8.8%

10.1%12.8%

13.7%

16.5%32.0%

3.0%

8.0%

0% 10% 20% 30% 40%

Illinois

South Dakota

Michigan

Wisconsin

Kansas

Nebraska

U.S.

Missouri

Iowa

Minnesota

Source: NAIC, Insurance Information Institute

2001-2010

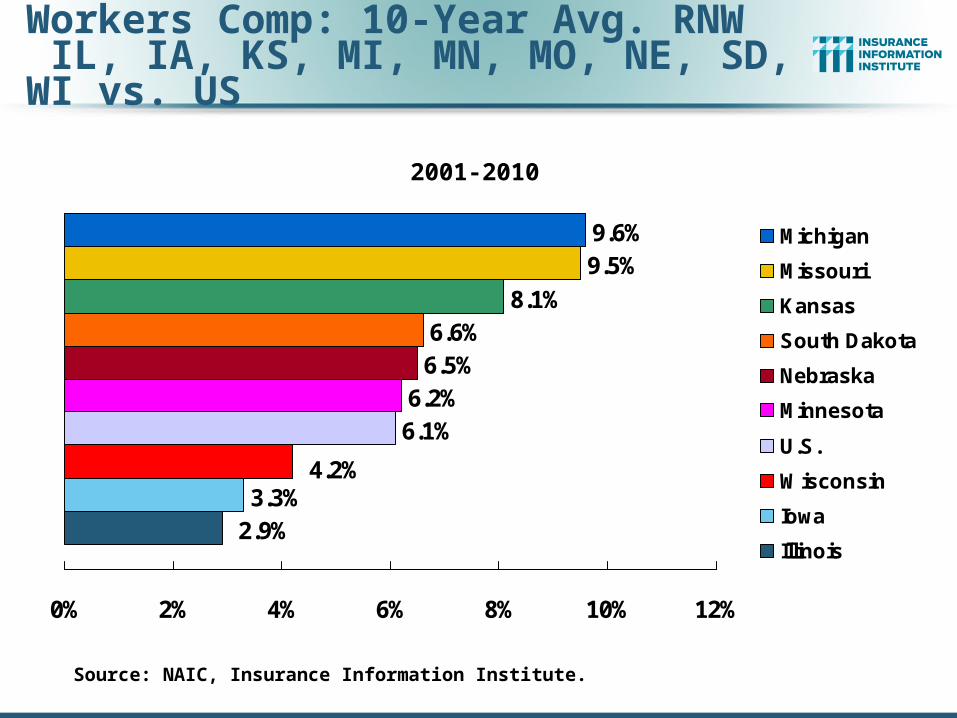

Workers Comp: 10-Year Avg. RNW IL, IA, KS, MI, MN, MO, NE, SD, WI vs. US

3.3%

6.1%6.2%

6.5%6.6%

8.1%

9.5%9.6%

2.9%

4.2%

0% 2% 4% 6% 8% 10% 12%

Michigan

Missouri

Kansas

South Dakota

Nebraska

Minnesota

U.S.

Wisconsin

Iowa

Illinois

Source: NAIC, Insurance Information Institute.

2001-2010

67

All Lines DWP Growth: IL, IA, KS, MI, MN, MO, NE, SD, WI vs. U.S., 2002-2011

Source: SNL Financial.

-10%

0%

10%

20%

02 03 04 05 06 07 08 09 10 11

US IL IA KS MI MN MO NE SD WI

(Percent)

Global Catastrophe Loss Developments and Trends

71

2011 Rewrote Catastrophe Loss and Insurance History

But Will Losses Turn the Market?

71

Geophysical events(earthquake, tsunami, volcanic activity)

Meteorological events (storm)

Hydrological events(flood, mass movement)

Selection of significant loss events (see table)

Natural catastrophes

Earthquake, tsunami Japan, 11 March

EarthquakeNew Zealand, 22 Feb.

Cyclone Yasi Australia, 2–7 Feb.

Landslides, flash floodsBrazil, 12/16 Jan.

Floods, flash floods Australia, Dec. 2010–Jan. 2011

Severe storms, tornadoesUSA, 22–28 April

Severe storms, tornadoesUSA, 20–27 May

WildfiresUSA, April/Sept.

EarthquakeNew Zealand, 13 June

FloodsUSA, April–May

Climatological events(extreme temperature, drought, wildfire)

Number of Events: 820Number of Events: 820

DroughtUSA, Oct. 2010– ongoing

Hurricane IreneUSA, Caribbean22 Aug.–2 Sept.

WildfiresCanada, 14–22 May

DroughtSomaliaOct. 2010–Sept. 2011

FloodsPakistanAug.–Sept.

FloodsThailandAug.–Nov.

Earthquake Turkey23 Oct.

Flash floods, floodsItaly, France, Spain4–9 Nov.

Floods, landslidesGuatemala, El Salvador11–19 Oct.

Tropical Storm WashiPhilippines, 16–18 Dec.

Winter Storm JoachimFrance, Switzerland, Germany, 15–17 Dec.

73Source: MR NatCatSERVICE

Natural Loss Events, 2011

World Map

82

U.S. Insured Catastrophe Loss Update

2011 Was One of the Most Expensive Years on Record

82

83

Top 14 Most Costly Disastersin U.S. History

(Insured Losses, 2011 Dollars, $ Billions)

*Losses will actually be broken down into several “events” as determined by PCS. Includes losses for the period April 1 – June 30.Sources: PCS; Insurance Information Institute inflation adjustments.

$9.0$11.9 $13.1

$19.1$21.3

$24.0 $25.0

$47.6

$8.5$7.7$6.5$5.5$4.4$4.3

$0$5

$10$15$20$25$30$35$40$45$50

Irene(2011)

Jeanne(2004)

Frances(2004)

Rita (2005)

Hugo (1989)

Ivan (2004)

Charley(2004)

Wilma(2005)

Ike (2008)

Northridge(1994)

SpringTornadoes& Storms*

(2011)

9/11Attack(2001)

Andrew(1992)

Katrina(2005)

Taken as a single event, the Spring 2011 tornado and storm season are

is the 4th costliest event in US insurance history

Hurricane Irene became the 11th most expense

hurricane in US history

Nu

mb

er

Geophysical (earthquake, tsunami, volcanic activity)

Climatological (temperature extremes, drought, wildfire)

Meteorological (storm)

Hydrological (flood, mass movement)

Natural Disasters in the United States, 1980 – 2011Number of Events (Annual Totals 1980 – 2011)

Source: MR NatCatSERVICE 84

37

8

51

2

50

100

150

200

250

300

1980 1982 1984 1986 1988 1990 1992 1994 1996 1998 2000 2002 2004 2006 2008 2010

There were 117 natural disaster events in 2011

86

$1

2.3

$1

0.7

$3

.7 $1

4.0

$1

1.3

$6

.0

$3

3.9

$7

.4 $1

5.9 $

32

.9

$7

1.7

$1

0.3

$7

.3

$2

8.5

$1

1.2

$1

4.1

$3

2.3

$1

00

.0

$1

3.7

$4

.7

$7

.8

$3

6.9

$8

.6

$2

5.8

$0

$20

$40

$60

$80

$100

$120

89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*20??

US Insured Catastrophe Losses

*PCS figure as of April 6, 2012.Note: 2001 figure includes $20.3B for 9/11 losses reported through 12/31/01 ($25.9B 2011 dollars). Includes only business and personal property claims, business interruption and auto claims. Non-prop/BI losses = $12.2B ($15.6B in 2011 dollars.) Sources: Property Claims Service/ISO; Insurance Information Institute.

US CAT Losses in 2011 Were the 5th Highest in US History on An Inflation Adjusted Basis

$100 Billion CAT Year is Coming Eventually

Record Tornado Losses Caused

2011 CAT Losses to Surge

($ Billions, 2011 Dollars)

86

$500

$530

$830

$975

$980

$1,000

$1,200

$1,400

$1,510

$2,000

$5,000

$6,900

$7,300

$840

$0 $1,000 $2,000 $3,000 $4,000 $5,000 $6,000 $7,000

Flooding, April*

Wildfire, Sep. 4-19

Thunderstorms, Apr. 19-20

Thunderstorms, Aug. 18-19

Winter Storm, Jan. 31-Feb. 3

Thunderstorms, Jul. 10-14

Texas Drought, 2011*

Thunderstorms, Jun. 16-22

Thunderstorms, Apr. 14-16

Thunderstorms, Apr. 8-11

Thunderstorms, Apr. 3-5

Hurricane Irene, Aug. 26-28**

Thunderstorms, May 20-27

Thunderstorms, Apr. 22-26

**Includes $700 million in flood losses insured through the National Flood Insurance Program.Source: PCS except as noted by “*” which are sourced to Munich Re; Insurance Information Institute.

2011’s Most Expensive Catastrophes, Insured Losses

Includes $1.65B in AL, mostly in the Tuscaloosa

and Birmingham

areas

Includes approximately $2B in losses

for May 22 Joplin tornado

88

Claim Payments to Policyholders, by State, for the May 20-27 Storms (Joplin)

$2,160

$1,050$975

$485 $460$340

$255 $225$161 $155 $110 $75 $65 $54 $50 $50 $40 $35

$115

$0

$500

$1,000

$1,500

$2,000

$2,500

MO OH TX TN IN OK KS PA MN IL WI AR GA NC NE KY VA IA NY

Missouri Claim Payout Accounted for 32% of the $6.9 Billion US Total for the May 20-27 Tornado and Storm Event, Which Affected 19 States

89

At $2.16 billion, MO suffered, by far, the largest losses from

the May 20-27 storms

TOTAL = $6.9 BILLION

Sources: Catastrophe loss data is for Catastrophe Serial No. 48 (May 22 – 27, 2011) from PCS as of May 10, 2012; Insurance Information Institute .

($ Thousands)

Commercial, 7,000 , 11%

Vehicle, 28,000 , 46%

Home, 26,000 , 43%

Distribution of Number of Claims Paid to MO Policyholders for May 20-27 Storms

TOTAL = 61,000 CLAIMS PAID

Sources: Catastrophe loss data is for Catastrophe Serial No. 48 (May 20 – 27, 2011) from PCS as of May 10, 2012; Insurance Information Institute .

Commercial (business) claims

accounted for 64% of the claim dollars paid by insurers but just

11% of the actual number of claims

Commercial, $1,385 , 64%

Vehicle, $100 , 5%

Home, $675 , 31%

Commercial (business) claims

accounted for 64% of the claim dollars paid by insurers but just

11% of the actual number of claims

Distribution of Claim Dollars Paid to MO Policyholders for May 20-27 Storms ($ Mill)

Sources: Catastrophe loss data is for Catastrophe Serial No. 48 (May 20 – 27, 2011) from PCS as of May 10, 2012; Insurance Information Institute .

TOTAL = $2.160 BILLION

Claim Payments to Policyholders, by State, for the April 22-28 Storms (Tuscaloosa)

$2,925

$2,000

$590$435 $338 $305

$169 $112 $111 $90 $79 $66$80

$0

$500

$1,000

$1,500

$2,000

$2,500

$3,000

$3,500

AL TN TX GA AR MO MS KY OH VA LA IL OK

Alabama Claim Payout Accounted for 40% of the $7.3 Billion US Total for the April 22-28 Tornado and Storm Event, Which Affected 13 States

92Sources: Catastrophe loss data is for Catastrophe Serial No. 46 (April 22 – 28, 2011) from PCS as of April 13, 2012; Insurance Information Institute .

At $2.925 billion, AL suffered, by far, the largest losses from

the Apr. 22-28 storms

TOTAL = $7.3 BILLION

93

Combined Ratio Points Associated with Catastrophe Losses: 1960 – 2011*

*Insurance Information Institute estimates for 2010 and 2011 based on A.M. Best data.Notes: Private carrier losses only. Excludes loss adjustment expenses and reinsurance reinstatement premiums. Figures are adjusted for losses ultimately paid by foreign insurers and reinsurers.Source: ISO; Insurance Information Institute.

0.4

1.2

0.4 0.

8 1.3

0.3 0.4 0.

71.

51.

00.

40.

4 0.7

1.8

1.1

0.6

1.4 2.

01.

3 2.0

0.5

0.5 0.7

3.0

1.2

2.1

8.8

2.3

5.9

3.3

2.8

1.0

3.6

2.9

1.6

5.4

1.6

3.3

3.3

8.1

2.7

1.6

5.0

2.6

4.4

8.0

3.6

0.9

0.1

1.1

1.1

0.8

0

1

2

3

4

5

6

7

8

9

10

1960

1962

1964

1966

1968

1970

1972

1974

1976

1978

1980

1982

1984

1986

1988

1990

1992

1994

1996

1998

2000

2002

2004

2006

2008

2010

The Catastrophe Loss Component of Private Insurer Losses Has Increased Sharply in Recent Decades

Avg. CAT Loss Component of the Combined Ratio

by Decade

1960s: 1.04 1970s: 0.85 1980s: 1.31 1990s: 3.39 2000s: 3.52 2010s: 6.20*

Combined Ratio Points

U.S. Thunderstorm Loss Trends, 1980 – 2011

94Source: Property Claims Service, MR NatCatSERVICE

Average thunderstorm

losses are up more than 5 fold since the early 1980s

Hurricanes get all the headlines, but thunderstorms are consistent

producers of large scale loss. 2008-2011 are the most expensive

years on record.

Thunderstorm losses in 2011 totaled a record

$25.8 billion

Source: Property Claims Service, MR NatCatSERVICE

U.S. Winter Storm Loss Trends, 1980 – 2011

95

Insured winter storm losses in 2011 totaled $2.0 billion. Average winter storm losses have nearly doubled

since the early 1980s

Slide 95

Source: National Forest Service, MR NatCatSERVICE

U.S. Acreage Burned by Wildfires, 1980 – 2011

96

8.3 millions acres were burned by wildfires in 2011, one of the worst years on record, causing

$855 in insured losses

Slide 96

100

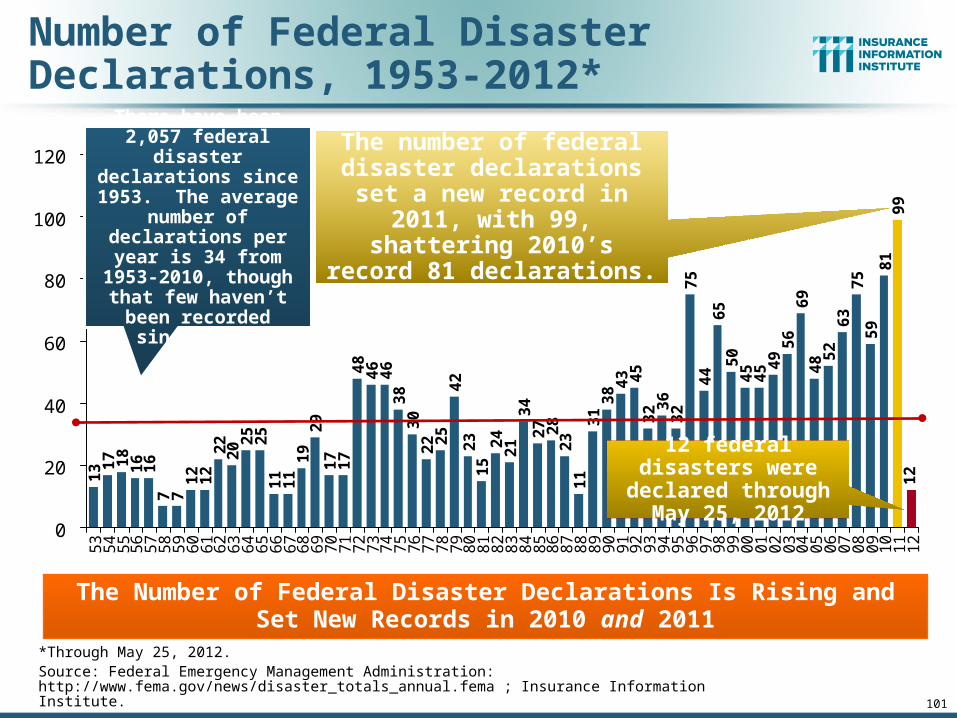

Federal Disaster Declarations Patterns:

1953-2012

100

Records Were Set for Federal Disaster Declarations in 2010 and

2011—Most Declarations Were Unrelated to Tropical Activity

Number of Federal Disaster Declarations, 1953-2012*

13 1

7 18

16

16

7 71

21

22

22

0 25

25

11

11

19

29

17

17

48

46

46

38

30

22 2

54

22

31

52

42

13

42

7 28

23

11

31

38

45

32 3

63

27

54

46

55

04

54

5 49

56

69

48 5

26

37

55

98

19

91

2

43

0

20

40

60

80

100

120

53

54

55

56

57

58

59

60

61

62

63

64

65

66

67

68

69

70

71

72

73

74

75

76

77

78

79

80

81

82

83

84

85

86

87

88

89

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

12

*Through May 25, 2012.Source: Federal Emergency Management Administration: http://www.fema.gov/news/disaster_totals_annual.fema ; Insurance Information Institute.

The Number of Federal Disaster Declarations Is Rising and Set New Records in 2010 and 2011

The number of federal disaster declarations set a

new record in 2011, with 99, shattering 2010’s record 81

declarations.

There have been 2,057 federal disaster

declarations since 1953. The average

number of declarations per year is 34 from

1953-2010, though that few haven’t been

recorded since 1995.

12 federal disasters were declared

through May 25, 2012

101

102

Federal Disasters Declarations by State, 1953 – 2012: Highest 25 States*

86

78

70

65

63

58

56

56

53

53

51

51

50

48

48

48

47

47

47

45

45

45

42

40

39

0

10

20

30

40

50

60

70

80

90

100

TX CA OK NY FL LA AL KY AR MO IL TN MS IA MN WV KS NE PA OH VA WA ND NC IN

Dis

as

ter

De

cla

rati

on

s

*Through May 25, 2012.

Source: FEMA: http://www.fema.gov/news/disaster_totals_annual.fema; Insurance Information Institute.

Over the past nearly 60 years,

Texas has had the highest number of Federal Disaster

Declarations

103

Federal Disasters Declarations by State, 1953 – 2012: Lowest 25 States*

39

39

37

36

35

33

33

28

28

27

26

26

25

24

24

23

22

20

17

17

16

15

14

11

10

9 9

0

10

20

30

40

50

ME SD AK GA WI VT NJ NH OR MA PR HI MI AZ NM ID MD MT NV CT CO SC DE DC UT RI WY

Dis

as

ter

De

cla

rati

on

s

*Through May 25, 2012. Includes Puerto Rico and the District of Columbia.

Source: FEMA: http://www.fema.gov/news/disaster_totals_annual.fema; Insurance Information Institute.

Over the past nearly 60 years, Utah and Rhode Island had the fewest

number of Federal Disaster Declarations

104

SPRING 2012 TORNADO & SEVERE STORM OUTBREAK

2012 Is Off to a Worrisome Start, But a Repeat of 2011 Is Unlikely

104

105

1,1

33

1,1

32 1

,29

7

1,1

73

1,0

82 1,2

34

1,1

73

1,1

48

1,4

24

1,3

45

1,0

71 1,2

16

94

1

1,3

76

1,2

64

1,1

03

1,0

98

1,6

92

1,1

46 1,2

82

71

1

1,819

1,6

91

553

0

200

400

600

800

1,000

1,200

1,400

1,600

1,800

2,000

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12*

Nu

mb

er

of

To

rna

do

es

0

100

200

300

400

500

600

Nu

mb

er o

f De

ath

s

Number of Tornadoes

Number of Deaths

*Through May 22, 2012.Source: U.S. Department of Commerce, Storm Prediction Center, National Weather Service at http://www.spc.noaa.gov/climo/online/monthly/newm.html

Number of Tornadoes and Related Deaths, 1990 – 2012*

Tornadoes claimed 553 lives in 2011, the most since 1925

711 tornadoes have been recorded so far

this year*

2012 Tornado Losses Is Off to a Ominous Beginning. First Half 2011 Insured Losses from Tornadoes and Thunderstorms Topped $21B.

U.S. Tornado Count, 2005-2012*

106

*Through May 20, 2012.Source: http://www.spc.noaa.gov/wcm/

2012 count is running well behind 2011

There were 1,897 tornadoes in the US in 2011 far above

average, but well below 2008’s record

Location of Tornadoes in the US, 2012*

*Through May 22, 2012.Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2012_annual_summary.html# 107

711 tornadoes killed 63 people through

May 16

Location of Large Hail Reports in the US, 2012*

109*Through May 22, 2012.Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2012_annual_summary.html#

There were 3,477 “Large Hail”

reports through May 22, 2012,

causing extensive damage to homes,

businesses and vehicles

Location of Wind Damage Reports in the US, 2012*

111*Through May 22, 2012.Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2012_annual_summary.html#

There were 2,783 “Wind Damage” reports through May 22, causing

extensive damage to homes and,

businesses

Severe Weather Reports, 2012*

113*Through May 22, 2012.Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2012_annual_summary.html#

There were already 6,970

severe weather reports through

May 22; including 711

tornadoes; 3,477 “Large Hail” reports

and 2,783 high wind events

Severe Weather Reports, 2011

114Source: NOAA Storm Prediction Center; http://www.spc.noaa.gov/climo/online/monthly/2011_annual_summary.html#

There were 29,996 severe

weather reports in 2011;

including 1,894 tornadoes;

9,417 “Large Hail” reports

and 18,685 high wind events

The BIG Question:When Will the Market Turn?

116

Are Catastrophes and Other Factors Pressuring Insurance Markets?

116

117

Criteria Necessary for a “Market Turn”:All Four Criteria Must Be Met

Criteria Status Comments

Sustained Period of

Large Underwriting

LossesEarly Stage,

Inevitable

•Apart from 2011 CAT losses, overall p/c underwriting losses remain modest•Combined ratios (ex-CATs) still in low 100s (vs. 110+ at onset of last hard market)•Prior-year reserve releases continue to reduce u/w losses, boost ROEs, though more modestly

Material Decline in Surplus/ Capacity

Entered 2011 At Record High; Only

Small Decline

•Surplus hit a record $565B as of 3/31/11•Fell just 1.6% through 12/31/11 from 12/31/10•Will likely see new record in 2012•Little excess capacity remains in reinsurance markets•Modest growth in demand for insurance is insufficient to absorb much excess capacity

Tight Reinsurance

MarketSomewhat in

Place

•Much of the global “excess capacity” was eroded by cats•Higher prices in Asia/Pacific•Modestly higher pricing for US risks

Renewed Underwriting

& Pricing Discipline

Some Firming esp. in

Property, WC

•Commercial lines pricing trends have turned from negative to flat and now positive, esp. Property & WC; •Competition remains intense as many seek to maintain market share

Sources: Barclays Capital; Insurance Information Institute.

1. UNDERWRITING

118

Have Underwriting Losses Been Large Enough for Long Enough to Turn the Market?

118

119

P/C Insurance Industry Combined Ratio, 2001–2011*

* Excludes Mortgage & Financial Guaranty insurers 2008--2011. Including M&FG, 2008=105.1, 2009=100.7, 2010=102.4, 2011=106.4 Sources: A.M. Best, ISO.

95.7

99.3100.8

106.4

101.0

92.6

100.898.4

100.1

107.5

115.8

90

100

110

120

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011*

Best Combined

Ratio Since 1949 (87.6)

As Recently as 2001, Insurers Paid Out

Nearly $1.16 for Every $1 in Earned

Premiums

Relatively Low CAT Losses, Reserve Releases

Cyclical Deterioration

Heavy Use of Reinsurance Lowered Net

Losses

Relatively Low CAT Losses, Reserve Releases

Avg. CAT Losses,

More Reserve Releases

Higher CAT

Losses, Shrinking Reserve

Releases, Toll of Soft

Market

Underwriting Gain (Loss)1975–2011E*

* Includes mortgage and financial guaranty insurers in all yearsSources: A.M. Best, ISO; Insurance Information Institute.

Large Underwriting Losses Are NOT Sustainable in Current Investment Environment

-$55

-$45

-$35

-$25

-$15

-$5

$5

$15

$25

$35

75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 1011*

Cumulative underwriting deficit from 1975 through

2011 is $479B

($ Billions) Underwriting losses in

2011 totaled $36.5B, the

largest since 2001

122

2

(2)

(8)

(3)

(7)(10) (10)

(4)

(0)

11

24

15

119

(5)

(9)

(14)

(10) (11)(7)

(5)(2)

-$20

-$15

-$10

-$5

$0

$5

$10

$15

$20

$25

$309

2

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

E

12

F

13

F

Pri

or

Yr.

Re

se

rve

Re

lea

se

($

B)

-6

-4

-2

0

2

4

6

8 Imp

ac

t on

Co

mb

ine

d R

atio

(Po

ints

)

Prior Yr. ReserveDevelopment ($B)

Impact onCombined Ratio(Points)

P/C Reserve Development, 1992–2013F

Reserve Releases Remained Strong in 2010 But Tapered Off in 2011. Releases Are Expected to

Further Diminish in 2012 and 2103Note: 2005 reserve development excludes a $6 billion loss portfolio transfer between American Re and Munich Re. Including this transaction, total prior year adverse development in 2005 was $7 billion. The data from 2000 and subsequent years excludes development from financial guaranty and mortgage insurance. Sources: Barclays Capital; A.M. Best.

Prior year reserve releases totaled $8.8

billion in the first half of 2010, up from

$7.1 billion in the first half of 2009

Financial Strength & Underwriting

125

Cyclical Pattern is P-C Impairment History is Directly Tied to

Underwriting, Reserving & Pricing

125

127

P/C Insurer Impairment Frequency vs. Combined Ratio, 1969-2011

90

95

100

105

110

115

1206

97

07

17

27

37

47

57

67

77

87

98

08

18

28

38

48

58

68

78

88

99

09

19

29

39

49

59

69

79

89

90

00

10

20

30

40

50

60

70

80

91

01

1

Co

mb

ine

d R

ati

o

0.0

0.2

0.4

0.6

0.8

1.0

1.2

1.4

1.6

1.8

2.0

Imp

airm

en

t Ra

te

Combined Ratio after Div P/C Impairment Frequency

Source: A.M. Best; Insurance Information Institute

2011 impairment rate was 0.91%, up from 0.67% in 2010; the rate is slightly higher than the 0.82% average since 1969

Impairment Rates Are Highly Correlated With Underwriting Performance and Reached Record Lows in 2007; Recent Increase Was Associated

Primarily With Mortgage and Financial Guaranty Insurers and Not Representative of the Industry Overall

128

Reasons for US P/C Insurer Impairments, 1969–2010

3.6%4.0%

8.6%

7.3%

7.8%

7.1%

7.8%13.6%

40.3%

Source: A.M. Best: 1969-2010 Impairment Review, Special Report, April 2011.

Historically, Deficient Loss Reserves and Inadequate Pricing AreBy Far the Leading Cause of P-C Insurer Impairments.

Investment and Catastrophe Losses Play a Much Smaller Role

Deficient Loss Reserves/Inadequate Pricing

Reinsurance Failure

Rapid GrowthAlleged Fraud

Catastrophe Losses

Affiliate Impairment

Investment Problems (Overstatement of Assets)

Misc.

Sig. Change in Business

131

Performance by Segment:Commercial Lines

131

109.4110.2

118.8

109.5

112.5

110.2

107.6

104.1

109.7 110.2

102.5

105.4

91.2

94.8

101.299.5

101.0

107.5

102.0102.0

111.1112.3

122.3

90

95

100

105

110

115

120

125

90

91

92

93

94

95

96

97

98

99

00

01

02

03

04

05

06

07

08

09

10

11

P

12

F

Co

mm

erc

ial L

ine

s C

om

bin

ed

Ra

tio

*2007-2012 figures exclude mortgage and financial guaranty segments.Source: A.M. Best; Insurance Information Institute

Commercial Lines Combined Ratio, 1990-2012F*

Commercial lines underwriting

performance in 2011 was the worst since 2002

133

Commercial Auto Combined Ratio: 1993–2012F

11

2.1

11

2.0

11

3.0

11

5.9

10

2.7

95

.2

92

.9

92

.1

92

.4 94

.3 96

.8 99

.4

98

.0 10

2.6

10

2.1

11

8.1

11

5.7

11

6.2

80

85

90

95

100

105

110

115

120

125

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11P 12F

Commercial Auto is Expected to Deteriorate as Loss Frequency and Severity Trends Deteriorate 2011-2012

Sources: A.M. Best Insurance Information Institute. 134

Commercial Multi-Peril Combined Ratio: 1995–2012F

119.

0

119.

8

108.

5

125.

0

116.

2

116.

1

104.

9

101.

9

105.

4

95.4 97

.7

94.2 96

.2100.

7

116.

8

113.

6

115.

3 122.

4

115.

0

117.

0

97.3

89.0

97.7

93.8

83.8

89.8

108.

4

98.6 10

2.5

113.

0

102.

1

113.

1

115.

0 121.

0

80

85

90

95

100105

110

115

120

125

130

95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11E* 12F

CMP-Liability CMP-Non-Liability

Commercial Multi-Peril Underwriting Performance is Expected to Improve in 2012 Assuming Normal

Catastrophe Loss Activity

*2012 figures are A.M. Best estimate/forecast for the combined liability and non-liability components.Sources: A.M. Best; Insurance Information Institute. 135

Workers Compensation Combined Ratio: 1994–2012F

10

2.0

97

.0 10

0.0

10

1.0

11

0.9

11

0.0

10

7.0

10

2.7

98

.4 10

3.6

10

4.4 1

10

.6 11

6.8

11

5.0

11

6.01

21

.7

10

7.0

11

5.3

11

8.2

80

85

90

95

100

105

110

115

120

125

130

94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11P 12F

Workers Comp Underwriting Results Are Deteriorating Markedly and the Worst They

Have Been in a DecadeSources: A.M. Best (1994-2010 all carriers); NCCI for 2011 (Private carriers only); 2012 (All Carriers) Insurance Information Institute. 139

2. SURPLUS/CAPITAL/CAPACITY

150

Have Large Global Losses Reduced Capacity in the Industry, Setting

the Stage for a Market Turn?

150

152

Policyholder Surplus, 2006:Q4–2011:Q4

Sources: ISO, A.M .Best.

($ Billions)

$487.1$496.6

$512.8$521.8

$478.5

$455.6

$437.1

$463.0

$490.8

$511.5

$540.7$530.5

$544.8

$559.2 $559.1

$538.6

$550.3

$564.7

$505.0$515.6$517.9

$420

$440

$460

$480

$500

$520

$540

$560

$580

06:Q4 07:Q1 07:Q2 07:Q3 07:Q4 08:Q1 08:Q2 08:Q3 08:Q4 09:Q1 09:Q2 09:Q3 09:Q4 10:Q1 10:Q2 10:Q3 10:Q4 11:Q1 11:Q2 11:Q3 11:Q4

2007:Q3Previous Surplus Peak

Quarterly Surplus Changes Since 2011:Q1 Peak

11:Q2: -$5.6B (-1.0%)11:Q3: -$26.1B (-4.6%)11:Q4: -$14.3B (-2.5%)

Surplus as of 12/31/11 was down 2.5% below its all

time record high of $564.7B set as of 3/31/11. A new record high in 2012 is

possible.

*Includes $22.5B of paid-in capital from a holding company parent for one insurer’s investment in a non-insurance business in early 2010.

The Industry now has $1 of surplus for every $0.80 of NPW, close to the strongest claims-

paying status in its history.

159

3. REINSURANCE MARKET CONDITIONS

Record Global Catastrophes Activity is

Pressuring Pricing

159

161

Global Property Catastrophe Rate on Line Index, 1990—2012 (as of Jan. 1)

15%

-3%

-13%

-8%

-20% -18% -1

1%

3%

14%

-11%

-6%

-9%

-16%

10%

-12%

-3%

8%

14%

76%

68%

25%

20%

0%

115

141

230

200184

147

123

152

255

233

195

235

184

199

133111

105

237

100

154

173

145

190

-40%

-20%

0%

20%

40%

60%

80%

100%

90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11 12

Ye

ar

Ov

er

Ye

ar

% C

ha

ng

e in

RO

L

0

50

100

150

200

250

300

Cu

mu

lativ

e R

ate

on

Lin

e (1

99

0=

10

0)

Year Over Year % Change

Cumulative Rate on Line Index

Sources: Guy Carpenter; Insurance Information Institute.

Property-Cat reinsurance pricing is up about 8% as of 1/1/12—modest relative

to the level CAT losses

4. RENEWED PRICING DISCIPLINE

163

Is There Evidence of a Broad and Sustained Shift in Pricing?

163

164

-5%

0%

5%

10%

15%

20%

25%

71 72 73 74 75 76 77 78 79 80 81 82 83 84 85 86 87 88 89 90 91 92 93 94 95 96 97 98 99 00 01 02 03 04 05 06 07 08 09 10 11*

Premium Growth Is Up Modestly: More in 2012?

(Percent)1975-78 1984-87 2000-03

Shaded areas denote “hard market” periodsSources: A.M. Best (historical and forecast), ISO, Insurance Information Institute.

Net Written Premiums Fell 0.7% in 2007 (First Decline

Since 1943) by 2.0% in 2008, and 4.2% in 2009, the First 3-Year Decline Since 1930-33.

NWP was up 0.9% in 2010

2011 growth

was +3.3%

165

Direct Premiums Written: All P/C Lines Percent Change by State, 2005-2010

44

.8

25

.4

19

.8

17

.3

16

.6

14

.2

13

.9

12

.4

12

.3

11

.9

9.1

8.1

8.1

7.1

6.8

5.4

5.2

4.7

3.8

3.7

3.1

3.0

1.5

1.2

1.1

0

5

10

15

20

25

30

35

40

45

ND

SD LA

WY

OK

WV

KS IA TX

MT

NE

DE

MS

NM SC