Embed Size (px)

DESCRIPTION

An Examination of Inflated Bank Capital and Credit Risks in China

Citation preview

Electronic copy available at: http://ssrn.com/abstract=2184082

An examination of inflated bank capital and credit risks in China

Yishu Fu

Business School, University of Adelaide

Email: [email protected]

Shih-Cheng Lee

Faculty of Finance, Yuan Ze University and Business School, University of Adelaide

Email: [email protected]

Lei Xu*

Business School, University of Adelaide

Email: [email protected]

Ralf Zurbruegg

Business School, University of Adelaide

Email: [email protected]

Abstract

Since the historical capital regulation by China Banking Regulatory Commission (CBRC) in

2004, Chinese banks have reported remarkable capital growth in their statements. This study

examines the impacts of heavily issued and cross-held subordinate debt (SD) towards inflated

capital adequacy ratios (CARs) and the credit risks of Chinese banks when they meet regulatory

requirements between 2004 and 2009. Our findings suggest that mandatory capital regulations in

China have significantly improved bank capital levels despite the widespread window-dressing

practice. In addition, the well-capitalised Chinese banks have lowered their credit risks in our

sample period. However, the undercapitalised banks may require more strict regulations.

Key words Subordinate debts, bank capital, risks, regulation, China

JEL Codes G21 G28

* Corresponding author. Postal address: Business School, University of Adelaide, 10 Pulteney

Street, Adelaide, SA 5005, Australia Tel: 61-8-83137272 Fax: 61-8-82234782

Electronic copy available at: http://ssrn.com/abstract=2184082

1. Introduction

Repeated banking crises during the past decades have pushed governments to attend closely the

capital and behaviour of banks. Prior to 1988, regulators across the world tend to set the

minimum ratio between capital and total assets in the hope that capital requirements could

enhance the stability of banking systems. One milestone is Basel I (1988) which develops a risk-

weighted framework and defines Tier 1 and Tier 2 capital. The world-wide adoption of Basel I

has resulted in Basel II (2004) in an attempt to set risks and management requirements in an

international background. The recent global financial crisis (GFC) in 2007 has brought renewed

attention to banking regulation and refined the regulatory benchmarks through Basel III (2010),

which focuses on the benchmarks over capital quality, risk coverage and liquidity.

However, despite continuously tightened regulatory requirements, banks may have exploited the

risk-weighted framework in Basel Accords. One example can be the innovative usage of

subordinate debts by Chinese banks. The effective capital level of Chinese banks diminishes

when they have cross subordinate debt holdings to seemingly increase individual bank‟s capital

cover. This widespread bank behaviour also increases the systematic instability of the system.

Through the improved capital quality requirement, Basel III has excluded such practice with

subordinate debts from effective Tier 2 capital. However, banks can still seek new

unconventional practice to circumvent the tightened regulations.

The growing importance of China in the new financial map after the GFC requires more study

over its banks. The banks control over 90% of aggregate financial resources in the second largest

world economy. More interestingly, the banks seem unaffected by worldwide financial crises

during the past decades. A literature review suggests that there are scarce of studies over bank

capital and risks in this country. Existing studies have focused on the non-performing loans

(NPLs) among Chinese banks (such as Bonin and Huang, 2001; Huang, 2002; Nanto and Sinha,

2002; Gamble, 2003; Gordon, 2003; Kwong and Lee, 2005; Xiao, 2006; Dobson and Kashyap,

2006; Ma, 2006; Xu and Lin, 2007; García-Herrero et al., 2009). A few studies have extend the

discussion to the operational risks, bank efficiency and state ownership reforms of Chinese banks

Electronic copy available at: http://ssrn.com/abstract=2184082

(such as Heilmann, 2005; Xie, 1999; Allen et al., 2005; Ferri, 2009; García-Herrero et al., 2009;

Fu and Heffernan, 2009; Matthews and Zhang, 2010; Shan and Xu, 2012; Ariff and Can, 2012;

Allen et al., 2012). In comparison to the considerable literature that examines the effects of

capital requirements among developed countries, little is known about the behaviour of Chinese

banks in response to mandatory capital requirements and their true capital levels.

The examination of Chinese banks‟ capital and risk behaviour may be of interest in several

aspects. First, this paper provides initiative empirical evidence on banking behaviour in today‟s

second largest economy in response to its historical capital regulation in the country. Second, this

study seeks to find reliable measurements of real capital status of Chinese banks. Due to the

limited size and scope of the capital markets in China, banks may have relied heavily on issuing

and cross-holding each other‟s subordinated debts so as to meet the regulatory capital

requirements. Although this window-dressing technique boost reported CARs, banks may have

not solved the fundamental problem of capital inadequacy at least to certain extent. Furthermore,

this banking practice increases the systemic risks. Third, this study may provide initial evidence

to explain a puzzle that despite the remarkable capital ratios reported by Chinese banks their

thirst for additional capital seems unquenched. Even when banks report CARs well above the

mandatory benchmarks, they still take all possible means to raise additional capital, such as

world-record IPOs, additional shares and rights, bringing noticeable impacts over stock markets

in the country. Fourth, this study over bank capital and risks may lead to further studies over

listed companies in China. Nowadays Chinese banks weigh over half of the market capitalisation

in the stock market and contribute to around 70% of total profits of all listed companies. We can

see more studies over the performance of Chinese listed companies in recent years, such as

Wang (2005) and Kao et al. (2009). However, most of these studies are focused on non-finance

companies by excluding the banks from their samples. Fifth, Chinese banks may differ from US

banks in their ability to adjust capital and risk. The regulatory pressure implied by capital

requirements may be stronger in China since it is the only country seemingly immune from the

recent GFC. In the meantime, most public-listed banks in China are either directly or indirectly

state-owned banks (SOB) and consequently have access to such government supports as capital

injections or bailouts. Sixth, effectiveness of capital regulation in the country can be examined.

Only after joining the World Trade Organization (WTO) has China started imposing

international standards over domestic institutions. Allen and Carletti (2008) suggest reducing the

amount of non-performing loans among the major banks to normal levels is the most important

task for the reform of financial system in the short run while the further development of China‟s

financial market is the most critical task in the long run. Berger et al. (2009) believe that

minority foreign ownership shows the significantly improved efficiency in banks‟ performance.

However, there has been a surprising lack of study in evaluating the effectiveness of government

regulations over its banks. Therefore, the important implications of this initial study may start

similar discussions for forthcoming researches.

In this study, we advance the concept of capital ratios to real capital ratios by eliminating the

effects of cross-holding SD among Chinese banks. Moreover, based on the simultaneous

equations model established by Shrieves and Dahl (1992), Rime (2001), and Van Roy (2008), we

analyse the corresponding adjustments in capital and risk by Chinese banks as they approach the

minimum regulatory capital level. Interestingly we find that mandatory capital regulations in

China have significantly improved bank capital levels despite the widespread window-dressing

practice. The well-capitalised Chinese banks have additionally lowered their credit risks in our

sample period when they meet regulatory capital requirements. However, the undercapitalised

Chinese banks may require more strict regulations.

This paper is structured as follows. Section 2 reviews the theoretical, empirical and latest

literature about bank capital requirements. Section 3 summarises the developments of capital

requirements in China, describes the information about SD issuance among Chinese commercial

banks and introduces the concept about the real capital ratio. Section 4 presents data and

methodology. Section 5 provides the empirical results. Section 6 concludes the paper.

2. Capital requirements and bank behaviour: Review of Literature

2.1 Mean-variance framework and option model

There have been two strands of literature on banks‟ risk levels. One strand focuses on the utility-

maximizing banks and investigates the impacts of higher mandatory capital ratios on banks‟

portfolio risks while the other strand explores the value-maximizing banks and reaches the

opposite conclusions.

The strand of literature focusing on utility-maximizing banks uses the portfolio approach in a

mean-variance framework (Pyle, 1971; Hart and Jaffee, 1974). Within this framework, Koehn

and Santomero (1980) examine the impacts on banks‟ portfolio risk when the regulator increases

the minimum capital to asset ratio. They find that the introduction of mandatory capital ratios

lead banks to shift their portfolio into riskier assets. In addition, this reshuffling effect may

become larger for banks that initially have more risky assets per unit of capital.

However, Furlong & Keeley (1989) and Keeley & Furlong (1990) challenge the above

conclusions. Their studies examine the impacts of more stringent capital regulation on bank asset

portfolio risk for value-maximizing banks based on an option model. Their results indicate that

incentives for value-maximizing banks to increase asset risk decline as the capital increases.

Their studies also suggest that the mean-variance framework is inappropriate because it does not

adequately explain the bank‟s investment opportunity set by ignoring the option value of deposit

insurance and the possibility of bank failure.

Unfortunately there are few studies providing non-US evidence over the changes of bank capital

and risks. Using confidential UK data, Ediz et al. (1998) find that banks adjust their capital levels

more than the difference between the current and the target level, implying that banks overset

their targets each year. Rime (2001) focuses on Swiss banks and provides a simultaneous

measurement over non-US banks. Heid et al. (2004) examine the relationship between capital

and risk levels by investigating German banks over 1993 to 2000. Their results suggest that

banks with low capital buffers tend to rebuild a sufficient capital buffer by decreasing risks and

increasing capital simultaneously. By contrast, banks with high capital may try to maintain their

capital buffer by increasing risk when capital increases. From the option-pricing perspective,

Sheldon (1996) examines the risk effects of capital rules within G-10 countries and figures out

that Basel I does not have risk-increasing impact on banks portfolio. However, very small banks

are selected to represent the sample from certain countries.

In short, economic theories are ambiguous on whether imposing tightened capital leads banks to

hold riskier asset in their portfolio. Existing studies additionally indicate that the market

discipline may also have impacts on the banks‟ response of capital and credit risks to the capital

regulations (Basel Committee on Banking Supervision 1999).

2.2 Adjustment cost and buffer theory

Provided with rigidities and adjustment costs, banks would never hold more capital than that

required by the regulators or by the market. However, banks may not be able to adjust capital or

risk instantaneously because of the adjustment costs or illiquid markets. In the case of

asymmetric information, raising additional equity could transmit a negative signal to the market

(Myers and Majluf, 1984), rendering banks unable or reluctant to react to negative capital shocks

instantaneously. Nevertheless, a breach of the regulation could trigger costly supervisory actions,

or even the bank‟s closure. Consequently banks have incentives to hold a “buffer” of excess

capital as an insurance against a violation of mandatory minimum capital requirement, especially

if the bank‟s capital ratio is quite volatile. Since raising capital is relatively costly compared to

raising insured deposits, this trade-off determines the optimum capital buffer (Milne and

Whalley, 2001). According to the buffer theory, banks would try to maintain a capital buffer in

excess of the regulatory minimum so as to avoid a breach of the minimum capital requirements.

Therefore, banks with high capital buffers would aim at holding their capital buffers while banks

with low capital buffers would aim at rebuilding an appropriate capital buffer.

2.3 Recent studies about the bank capital regulation

Apart from the increased capital and banks‟ risk-taking behaviour, recent studies have taken into

account other factors, such as the banks‟ financial performance, profitability and efficiency, in

the examination of capital regulation impacts. Lin et al. (2005) examine the relationship between

capital adequacy ratio, insolvency risk index and financial performances. Altunbas et al. (2007)

analyze the relationship between capital, risk and efficiency for European banks. Ngo (2008)

explores the relationship between banks‟ capital-risk decisions and their profitability. Deelchand

and Padgett (2009) discuss the performance and capital of cooperative banks in Japan. Fiordelisi

et al. (2011) analyze the inter-temporal relationships among banks‟ efficiency, capital and risk-

taking behaviour in the European Union countries.

Bank capital cover is also considered cyclical in nature. The macro-economic impacts brought

about by the increased capital standards are discussed in some recent studies. For example,

Nachane et al. (2006) suggest that whether monetary policy can be more or less effective in

influencing bank lending depends on a number of factors, such as whether banks are constrained

under the revised Basel Accord, the quality of bank loans and the liquidity of banks‟ balance

sheets. Heid (2007) examines the issues of capital-induced lending cycles and the pro-cyclical

effects on the macro-economy. Jokipii and Milne (2008) find that capital buffers co-move

negatively with the business cycle for banks in the EU but co-move positively for banks in the

accession countries.

3. CBRC Capital regulation and SD issuance in China

Capital requirement is a main banking supervisory instrument in China. For undercapitalised

banks, the CBRC has the authority to require the commercial bank to suspend all but low-risk

activities, suspend the building of new branches, and stop introducing new products or services.

For significantly undercapitalised banks, the CBRC can require removal of their senior

management, take over or even close the banks.

3.1 Recent developments in the capital regulation over Chinese banks

The capital inadequacy of Chinese banks has been subject to criticism for decades (such as Xie,

1999; Dobson and Kashyap, 2006; Xu and Lin, 2007). In 1994, the People‟s Banks of China

(PBC)1 set assessments to commercial banks including capital ratios. These capital ratios were

later covered by the Commercial Bank Law (1995). In the following years the PBC even worked

out more details on capital ratios allocating risk weights to various assets. However, these capital

ratios were introduced as reference to Chinese banks rather than mandatory regulation. Few

banks treated seriously the capital ratios as important financial indicators. It was lack of

1 Before the establishment of CBRC in 2003, PBC took charge of the supervision of Chinese banks.

mandatory regulation that resulted in the poor capital ratios when China joined the WTO in 2001.

China established the CBRC in 2003 to strengthen its finance industry and to avoid similar bank

failures in surrounding countries during the Asian Financial Crisis. The CBRC historically

introduced mandatory regulations over bank capital in the country in 2004. Based on both Basle I

and II, the CBRC bank capital regulations are curtailed for the Chinese banking sector.

According to the CBRC capital rules2, the measurement of bank capital adequacy ratios in China

can be shown as:

Capital adequacy ratio (CAR)

= (total capital – deductions) / (risk-weighted assets + 12.5 * capital charge for market risk)

= (total capital – deductions) / (credit risk-weighted assets + market risk-weighted assets)

= (total capital – deductions) / Total risk-weighted assets (1)

Core capital adequacy ratio (CCAR)

= (core capital – deductions) / (risk-weighted assets + 12.5 * capital charge for market risk)

= (core capital – deductions) / (credit risk-weighted assets + market risk-weighted assets)

= (core capital – deductions) / Total risk-weighted assets (2)

It is worth mentioning that in these equations, risk-weighted assets literally represent credit risk-

weighted assets. Chinese banks only disclose credit risk-weighted assets, market risk capital and

total risk-weighted assets (the sum of credit risk-weighted assets and market risk-weighted assets)

in their financial reports without reporting operational risk-weighted assets. In other words, the

total risk-weighted assets of Chinese banks do not include operational risk-weighted assets under

CBRC regulations.

Through various regulatory decrees and documents, such as the Regulation Rules over Foreign

Banks in China (2004)3 , the Provisional Rules over Risk Evaluation of Joint-Stock Commercial

2 CBRC 2004 No.2 Decree, Regulation Governing Capital Adequacy of Commercial Banks, February 23, 2004. 3 CBRC 2004 No. 4 Decree, Regulation Rules over Foreign Banks in China, July 26, 2004, Article 17

Banks (2004)4, the Guide of Corporate Governance and Relevant Regulation over State-Owned

Commercial Banks (2006)5 , and the Notice of Capital Adequacy Information Disclosure by

Commercial Banks (2009)6, the CBRC further strengthens capital adequacy requirements. In the

meantime, the CBRC capital requirements seem stricter than Basel Accords. In December 2009,

minimum CAR of 11% is imposed onto the largest Chinese banks7, and 10% for the small-and-

medium-sized banks.

In response to the tightened capital regulations, Chinese banks have since reported sharp

increased CARs. The CBRC statistics disclose the average CAR of -2.98%8 in 2003 (with 8

small-sized banks or 0.6% of all banks in the country meet Basel I capital requirement).

However, by 2009 all 239 commercial banks in the country have met CBRC minimum capital

requirements when their average CAR reach 11.4%, well above Basel I & II threshold. By 2010

all commercial banks in China have reported the average 12.2% CAR and 10.1% Core CAR9.

3.2 SD issuance in China

Provided with limited size and scope of capital markets in China, it is doubtful that Chinese

banks could achieve such remarkable capital improvements from negative level to above 10%

under tightened regulations. Although traditional approaches (such as capital injection or bailouts

by the government, issuing shares or convertible bonds, and offloading NPLs) do not bring much

controversy to bank capital, Chinese banks may have inventively issued SD above and beyond

reasonable amount to window-dress their capital ratios.

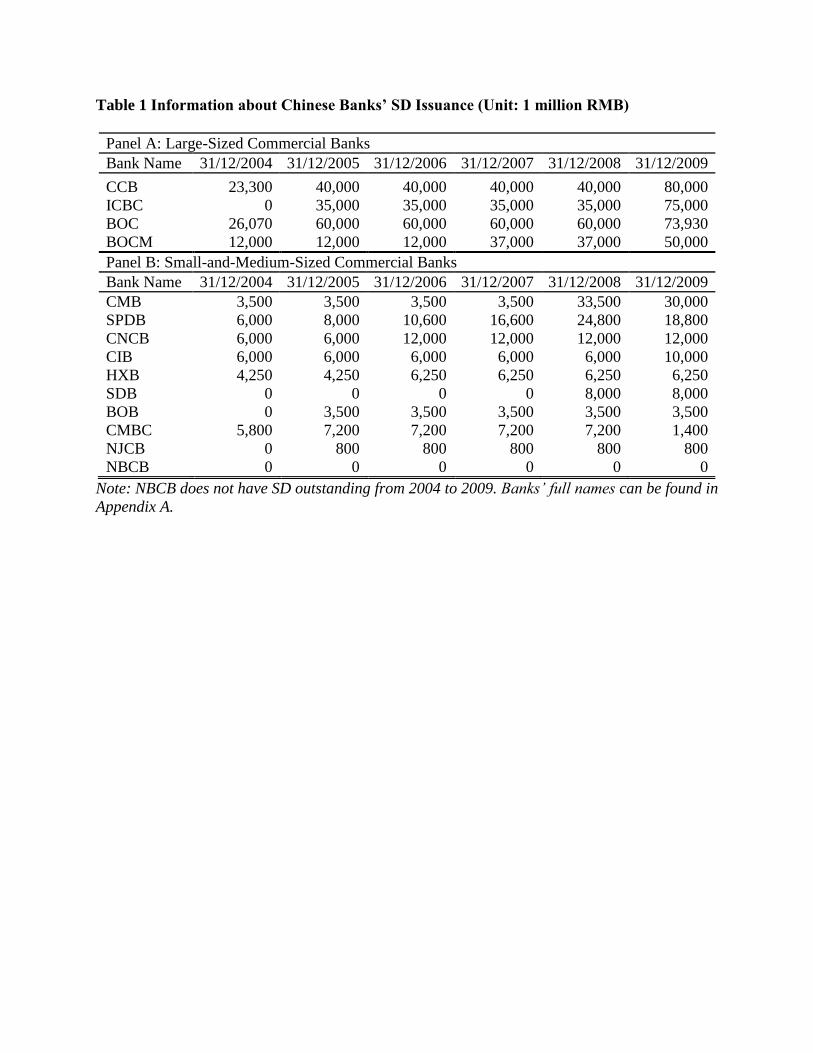

Table 1 summarises the SDs issued by Chinese banks between 2004 and 2009. We can see that

the large Chinese banks are the major issuers of SD in the interbank market. By comparison, the

aggregate SDs issued by small-and-medium-sized banks is less than half that of the four large

4 CBRC 2004 No. 3 Document, Provisional Rules over Risk Evaluation of Joint-Stock Commercial Banks, February 22, 2004 5 CBRC 2006 No. 22 Document, Guide of Corporate Governance and Relevant Regulation over State-owned Commercial Banks,

April 24, 2006, Article 20 & 23 6 CBRC 2009 No. 97 Document, Notice of Capital Adequacy Information Disclosure by Commercial Banks, November 7, 2009 7 They are the Industrial and Commercial Bank of China (ICBC), the Agricultural Bank of China (ABC), the Bank of China

(BOC), the China Construction Bank (CCB) and the Bank of Communications (BOCM). The ABC is listed in 2010 and therefore

not included in this study. 8 This happens when the difference between the capital and its‟ corresponding deduction, namely net capital, is less than zero. 9 Banking Capital Statistics, February 18th, 2011, CBRC Website

sized banks. As shown by Panel A, CCB ranks the top among the large banks in the amount of

SD outstanding. SD among all the listed banks increases sharply across the 2004-2009 sample

period. Panel B shows SD balance of small-and-medium-sized commercial banks. In 2009,

CMB10

and SPDB11

reduced their SD outstanding due to SD expiration while CMBC12

lowered

its SD balance because of redemption. Although NBCB does not issue SD during the sample

period, it is included in our sample because it holds around 800 million RMB SD of other banks

based on estimation by China International Capital Corporation Limited (CICC)13

.

Table1 here

3.3 Definition of real capital

In order to approximate the real capital level of Chinese banks, we apply the capital calculation

proposed by CBRC in August 200914

and exclude proportions of cross-held SD from Tier 2 bank

capital. This prudential measurement is strict against the banks‟ SD window-dressing tool but

unfortunately not carried out by CBRC in its mandatory regulations15

. Where data about SD

issuance and holdings are available, we would apply the CBRC method (the 2009 Enquiry) to

calculate real CAR. However, due to the scarce data source of SD holdings, we are forced to

discount banks‟ tier 2 capital and investments in securities simultaneously in this study.

According to CBRC, 51% of SD has been cross-held by other banks in the country by 2009 and

only 49% of SD could be regarded as qualified Tier 2 capital following the prudential

measurement. Therefore, each bank‟s real capital can be recalculated as:

(3)

10 CMB‟s 3,500 million RMB SD issued between March 31st and June 10th 2004 went expired in 2009. 11 SPDB‟s 6,000 million RMB SD issued on the June 9th 2004 went expired on the 8th July in 2009. 12 CMBC‟s 5,800 million RMB SD issued in 2004 was redeemed in advance in 2009. 13 NBCB‟s public announcement on September 28th 2009 indicated that 2,500 million RMB SD would be issued soon to

supplement its Tier 2 capital. 14 CBRC, 2009, Notice of Improving Commercial Banks‟ Capital Raising Mechanisms (Enquiry), August 18th 2009. This

Document does not acknowledge the wide-spread practice of cross-holding subordinate debts among Chinese banks. 15 CBRC, 2009, Notice of Improving Commercial Banks‟ Capital Raising Mechanisms, No. 90 Document. This Document

allows Chinese banks to adjust slowly capital ratios inflated by subordinate debts but prohibits banks to start new SD issuing and

cross-holding practice after 2009.

Since we have to adjust banks‟ capital and assets simultaneously, each bank‟s real capital

adequacy ratio (RCAR) can be recalculated by following equation16:

(4)

Similarly, each bank‟s real capital to total assets ratio (RCAP) can be recalculated as follows:

(5)

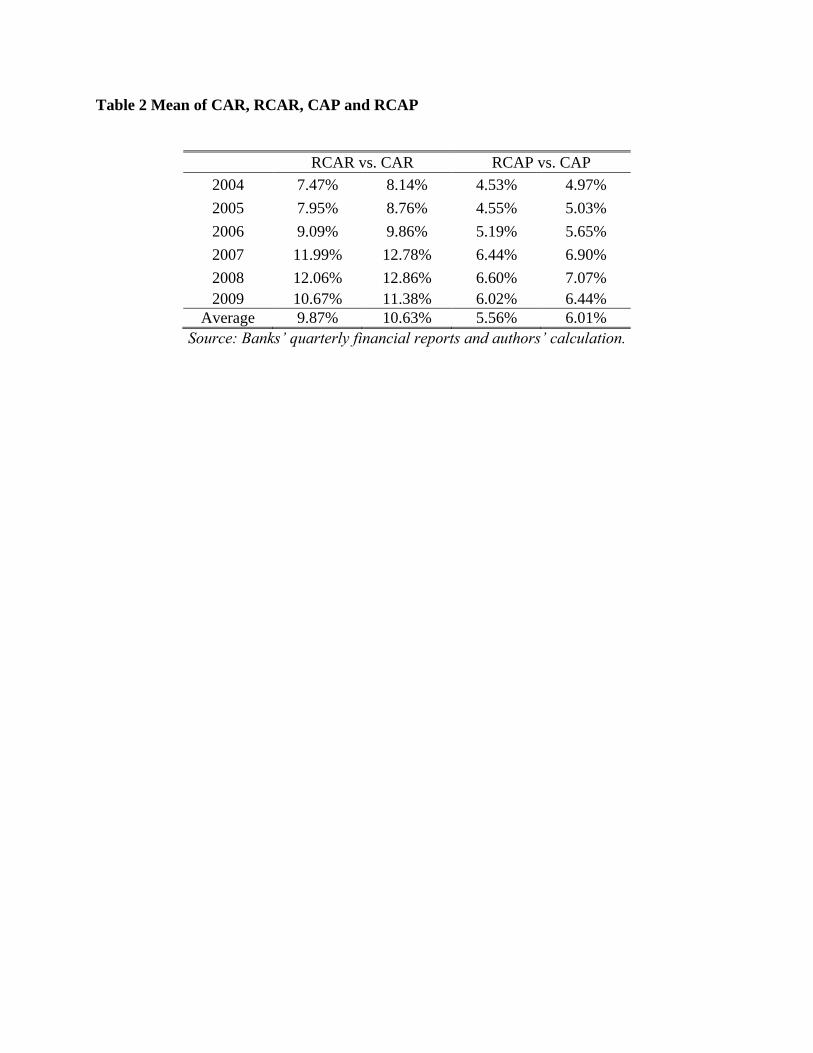

Comparisons between banks‟ real CAR and inflated CAR, and real CAP and inflated CAP are

provided by Table 2. The average banks‟ RCAR is 9.87%, which is almost 1% less than average

inflated CAR (10.63%). Similarly, the average RCAP from 2004 to 2009 is 5.66%, around 0.5%

less than the average inflated CAP (6.01%). Therefore, we can tell that Chinese banks do

substantially improve their reported CARs by commonly applying the window-dressing

technique through SD.

Table2 here

4. Data and Methodology

4.1 Data

Our sample covers all public-listed banks, including four large-sized and ten small-and-medium-

sized banks, in China between 2004 and 2009 with a total of 172 observations. All data are

manually collected from each bank‟s financial reports. Changes in capital and risk are measured

on quarterly basis, representing the highest frequency for which data is systematically available.

In our sample period, the listed banks are required by China Securities Regulatory Commission

16 CBRC, 2007, Decision of China Banking Regulatory Commission on Revising the Measures for the Management

of Capital Adequacy Ratios of Commercial Banks, No. 11 Document. This Document regulates 100% risk weight for SD.

(CSRC) to announce dual-audited financial reports17

. In addition, a few banks such as CCB and

ICBC are listed in our sample period.

4.2 Methodology

4.2.1 Simultaneous equations with partial adjustment framework

Considering that capital and risk decisions are determined concurrently, we use the simultaneous

model suggested by Shrieves and Dahl (1992), Rime (2001), and Van Roy (2008) to analyse

Chinese commercial banks‟ behavior in response to tightened capital regulation.

(6)

(7)

where and are the observed changes in capital and risk levels respectively for

bank i in period t; and are the discretionary adjustments in capital and risk

respectively; and are exogenously determined factors.

Since banks may not adjust their target capital ratio and risk levels instantaneously, we assume

that and follow a partial adjustment framework. Equation (6) and (7) suggest

that the discretionary changes in capital and changes in risk are proportional to the difference

between the target level in period t and the observed level in period t-1:

(8)

(9)

17 On November 14th 2000, CSRC regulated that listed banks shall have two accounting firms (at least one accounting firm must

be international) to audit their financial reports to avoid discrepancies in auditing practices. This regulation is no longer imposed

by CSRC since 2010.

where and

are bank i‟s target capital and risk levels, respectively.

Substituting equation (8) and (9) into equation (6) and (7), we can express the observed changes

in capital and risk as follows:

(10)

(11)

Therefore, the target capital and risk levels, the lagged capital and risk levels, as well as the

random exogenous shocks determine the adjustments in capital and risk.

4.2.2 Definitions of banks‟ capital and risk

We use two definitions of banks‟ capital: the total capital to assets ratio (CAP) and the total

capital to risk-weighted assets ratio (CAR). The former definition has been applied by Shrieves

and Dahl (1992). The latter has become more popular and many studies have employed CAR to

measure banks‟ capital since the application of risk-weighted capital standards (such as Jacques

and Nigro, 1997; Aggarwal and Jacques, 1998; Ediz et al., 1998; Cannata and Quagliariello,

2006; Saadaoui, 2011).

Academic literatures seem to cover various measurements over bank risks, most of which are

subject to criticisms over weaknesses. In this study, we measure bank risk-taking (RISK) with

credit risk ratio, the ratio of risk-weighted assets (RWA) to total assets (TA). This measurement is

first proposed by Shrieves and Dahl (1992) and subsequently used by Jacques and Nigro (1997),

Aggarwal and Jacques (1998), Rime (2001), Cannata and Quagliariello (2006), Van Roy (2008),

and Saadaoui (2011).

4.2.3 Variables affecting changes in capital and risk

Although it is not easy to observe directly the target capital and risk levels of a bank in equations

(10) and (11), these targets should depend on some sets of observable variables which describe

the bank‟s financial condition and the state of Chinese economy. We use the bank size (SIZE),

profitability (ROA), asset quality (LLOSS), changes in the credit risk ratio ( ), the degrees

of regulatory pressure (CARLOW and CARHIGH) and year dummies (YEAR) to approximate

the target capital to assets ratio ( . Besides, we employ SIZE, LLOSS, changes in the

capital to assets ratio ( ), CARLOW, CARHIGH, and YEAR to proxy the target credit risk

ratio ( ). Shrieves and Dahl (1992) use all these variables, except ROA which is emphasized

by Aggarwal and Jacqures (1998), and the regulatory pressure variables (RPL and RPG) which

are proposed by Aggarwal and Jacques (1998 & 2001), Godlewski (2005), Jacques and Nigro

(1997), Rime (2001) and Van Roy (2008).

Size

Bank size, measured by the natural log of total assets, is related to both bank‟s target capital and

risk. Size can affect target capital and risk level due to its relationship with risk diversification,

investment opportunities and access to equity capital markets.

Current profits

Current profits, measured by ROA, can affect the bank‟s target capital if the bank chooses to

increase capital through retained earnings rather than share offering. In the existence of

information asymmetry, equity issues could transmit negative signal about the bank‟s value to

the market.

Asset quality

Asset quality can affect the bank‟s target risk. This study uses the ratio of loan loss reserve to

total assets (LLOSS) to measure asset quality. LLOSS represents capital that the bank sets to

cover bad loans. Since increases in LLOSS lead to decreases in the risk-weighted assets, LLOSS

has negative effects in the risk equation.

Regulatory pressure

Previous studies use several ways to evaluate regulatory pressure. For example, Ediz et al. (1998)

apply a probabilistic approach with the dummy variable, which equals to one when the capital

adequacy ratio falls below the risk-based capital requirement plus one bank-specific standard

deviation of that bank‟s capital adequacy ratio series, and zero otherwise. However, their method

is not suitable for our study as the following two reasons. First, this study‟s sample data are

unbalanced. We need to use a different number of observations for each bank to calculate the

standard deviation of capital adequacy ratio, which is not appropriate. Second, this definition

implies that regulatory pressure is endogenous since bank behavior has influence on the

regulatory pressure (Van Roy, 2008).

Since Chinese banks with CARs above or below the regulatory requirement may react differently,

we partition regulatory pressure into two variables, CARLOW and CARHIGH, which can

recognise the nonlinear relationship between the regulatory capital standards and the changes

either in portfolio risk or capital ratios for both the undercapitalised and the adequately-

capitalised banks (Aggarwal and Jacques, 1998 & 2001; Godlewski, 2005; Jacques and Nigro,

1997; Rime, 2001).

The first regulatory pressure variable, CARLOW, equals to ( )

for banks with CAR below the regulatory RBC requirements and 0 otherwise. We use this

variable to study the reactions of undercapitalised banks to the increased capital standards. Banks

with positive CARLOW are subject to the regulatory pressure to enhance their capital ratios

because they fail to meet the minimum CBRC regulatory risk-based capital ratio. Thus, we

expect that CARLOW should have a positive effect on capital ratios and a negative effect on

portfolio risks, because banks may either increase capital or reduce risk-weighted assets to meet

the regulatory minimum risk-based standards.

Another regulatory pressure variable, CARHIGH, equals to (1/ -1/ ) for

banks with CAR above the peer market average and 0 otherwise. This variable is introduced to

examine the behaviour of the adequately-capitalised banks facing the binding capital

requirements. Although banks with CARs in excess of binding requirements are not explicitly

constrained by regulation, capital standards can still significantly influence banks‟ capital ratios

or risks in their portfolio of assets, banks may decrease their capital ratios or increase their

portfolio risk. Alternatively, these banks may choose to improve their capital ratios or reduce

risks to accumulate more buffers against shocks to equity in the future. By doing so, they can

signal to both the market and bank regulators so as to seek reduction in regulatory costs.

Simultaneous changes in risk and changes in capital

Since banks‟ capital and risk choices are interdependent, this study uses the simultaneous

equations to estimate them concurrently. Shrieves and Dahl (1992) claim that the relative

importance of the marginal benefits and marginal costs of asset risk and leverage will decide

whether changes in bank risk have a positive or negative relationship with the changes in bank

capital. When the bank‟s exploitation of the deposit insurance subsidy dominates the bank‟s

behaviour, we should observe a negative relationship between changes in risk and capital, and a

lasting trend toward lower capital and higher risk levels. However, some combination of

leverage and risk related cost factors would result in a positive relationship between the changes

in risk and the changes in capital.

Year dummy variables

In order to measure the effects of macroeconomic and regulatory shocks in any given year, the

simultaneous equations include dummy variables for each year, except 2004 to avoid perfect

multicollinearity.

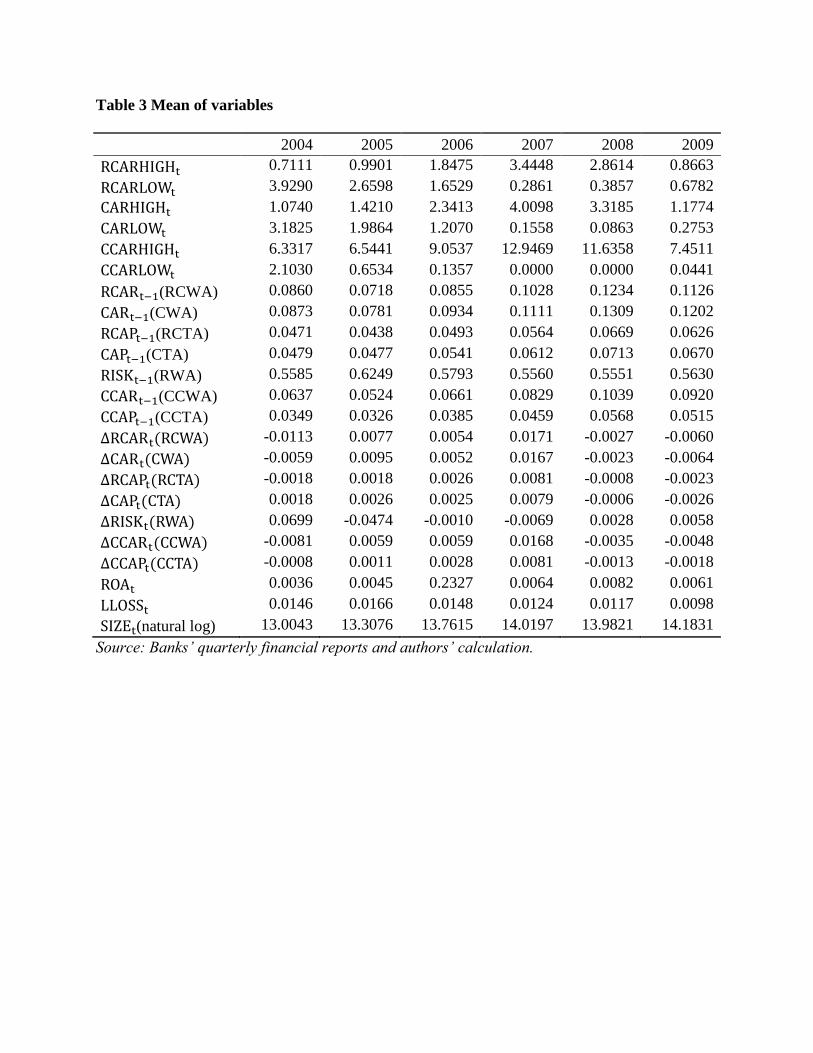

Table 3 shows the mean values of above important variables for each of the six sub-periods. We

notice that Chinese banks have relatively high capital adequacy ratios either measured by RCAR

or CAR and very low ROA in our sample period. However, the RCARs and the CARs indicate

different regulatory pressure over banks while banks are under constant pressure to adjust their

capital levels. In the meantime, despite rapid expansion in banks sizes, Chinese banks have

lowered their loan loss provisions as another means to boost their capital ratios. In other words,

Chinese banks may have lowered their asset quality when they report historically high CARs.

Table 3 here

4.2.4 Empirical specification

With the analysis of above variables, the model defined by equations (10) and (11) can be

written as:

(12)

(13)

where i is a bank index (i=1,…,14)

t is a time index (t=2005,…,2009)

~IID (0, )

~IID (0 )

The emphasis of this study is on the regulatory pressure variables, denoted by CARHIGH and

CARLOW. Moreover, and test the overall relationship between changes in capital and risk.

We pool the cross-sectional data over the research period and use the three-stage least squares

(Jacques and Nigro, 1997; Aggarwal and Jacques, 1998; Rime, 2001; Van Roy, 2008) to estimate

the simultaneous equations (12) and (13). In short, this methodology can take into account the

simultaneity of banks adjustments in capital and risk and obtain asymptotically more efficient

estimates than the two-stage least squares.

5. Results

5.1 Results on RCAR and CAR

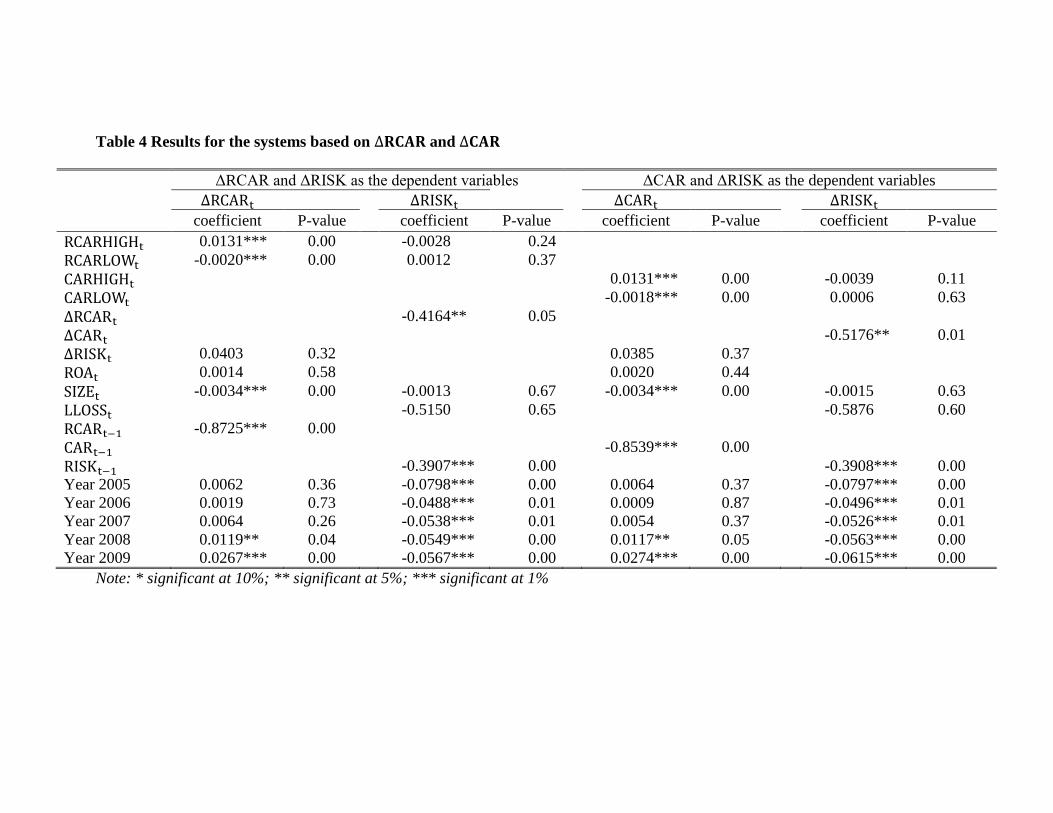

Table 4 provides the results of the simultaneous equations when we use the ratio of banks‟

capital (both real and inflated capital) to RWA and the ratio of RWA to total assets as dependent

variables. The left-hand part of Table 4 shows the results for the ratio of the real capital to RWA.

In the real capital equation, regulatory variables for adequately-capitalised banks (RCARHIGH)

has a significantly positive impact on the ratio of real total capital to RWA, which is consistent

with the findings by Haubrich and Wachtel (1993) in arguing the desire of well-capitalised banks

to signal both the market and bank regulators that they not only meet but clearly exceed the

minimum regulatory capital standards. Ceteris paribus, adequately-capitalised banks increase

their real capital ratio by 1.31 percents more than other banks, suggesting that CBRC risk-based

capital standard is effective in raising capital ratios among banks which are already incompliance

with the minimum risk-based standards. However, regulatory variable for undercapitalised banks

(RCARLOW) shows a negative and significant effect on banks‟ real capital level. Ceteris paribus,

undercapitalised banks decrease their real capital ratio by 0.2 percent more than other banks.

This result is not against the notion that risk-based capital has an impact on undercapitalised

banks. In fact, it indicates that mildly undercapitalised banks would experience relatively large

increases in their capital ratio either by raising capital or reducing risk-weighted assets, while the

most severely undercapitalised banks may experience relatively small increases in their capital

ratio. One possible explanation for this is that because constrained banks have the low ROA and

high expense of raising capital from external sources, severely undercapitalised banks may have

the extremely limited ability to meet the risk-based standards by raising capital, while mildly

undercapitalised banks may have been relatively more successful in raising their capital ratio. In

additions, most of Chinese banks are state-owned banks although they are undergoing the

process of partial privatization. The central government bailout and the almost zero possibility of

going bankruptcy give the capital-insufficient banks incentives to operate without actively

improving their poor capital positions. This result is consistent with the findings by Jacques and

Nigro (1997) that commercial banks which are deficient in risk-based capital, regulation have the

negative and significant effects on their capital ratios. In the controlling variables, SIZE has a

significantly negative impact, indicating that large Chinese banks increase the ratio of their

capital to RWA less than other banks. One plausible reason is that large banks can get access to

capital markets easily so that they can operate with lower capital. The Too-Big-to-Fail effect also

suggests that large banks feel less pressure to increase their capital ratio. The parameter on the

lagged capital is negative and significant, indicating that Chinese banks have adjusted their

capital ratios fast to desired levels since 2004.

In the risk equation, both regulatory variables RCARHIGH and RCARLOW have no significant

impact on banks‟ risk, suggesting that adequately-capitalised banks and undercapitalised banks

neither increased nor decreased the share of risk-weighted assets in their portfolio. The parameter

on lagged risk is negative and significant, indicating that Chinese banks were adjusting their risk

to desired levels fast from 2004 to 2009. All the time dummies in the equation are

significantly negative when RCAR is employed as the dependent variable. This result provides

evidence that banks in China decrease credit risk at the beginning of 2004, ceteris paribus.

Similarly, the right-hand part of Table 4 presents the results for the ratio of the inflated total

capital to RWA. All the variables in the system display the same sign and level of significance as

the measurement on banks‟ real capital ratio. Ceteris paribus, undercapitalised banks decrease

their capital ratio by 0.18 percent more than other banks while adequately-capitalised banks

increase their capital ratio by 1.31 percents more than other banks.

According to Table 4, changes in capital and credit risk are negatively and significantly related.

Specifically, Chinese banks adjust risk when capital changes but they do not adjust capital when

risk changes. In the case of relationship between RCAR and RISK, an increase of 1 percent in

the real capital ratio decreases the credit risk ratio by about 0.42 percent. This result indicates

that CBRC regulation is effective to limit adequately-capitalised banks‟ risk-taking behaviour.

However, this negative relationship between the changes in the real capital ratio and the changes

in the credit risk implicitly suggest that, binding capital requirements could cause the increase in

the portfolio risk for the under-capitalised banks. Comparisons with the previous empirical

studies, this discovery of negative relationship between the changes in the capital and risk is

consistent with the findings of Gunther and Robinson (1990), McManus and Rosen (1991),

Berger (1995), Jacques and Nigro (1997), Aggarwal and Jacques (1998), and Van Roy (2008).

The results from Aggrawal and Jacques (1998) indicate that an increase of 1% in the capital ratio

of banks causes a decrease of 0.058% in their credit risk in 1992 while an increase of 1% in the

credit risk ratio leads to a decrease of 0.476% in capital ratio, when the ratio of non-performing

loans to total assets is employed to measure the risk. The results on Japanese banks of Van Roy

(2008) suggest that an increase of 1% in the core capital-to-assets ratio of banks leads to a

decrease of 2.83% in the credit-risk ratio, assuming all other factors being equal. In other words,

Van Roy (2008) discovers that Japanese banks improve their tier one capital ratio by increasing

their tier 1 ratio and lowering their credit risk simultaneously. Shrieves and Dahl (1992) argue

that a negative correlation may result from the mispricing of deposit insurance. Jacques and

Nigro (1997) further argue that methodological flaws in the risk-based capital standards could

account for a negative relationship between risk and capital.

Table 4 here

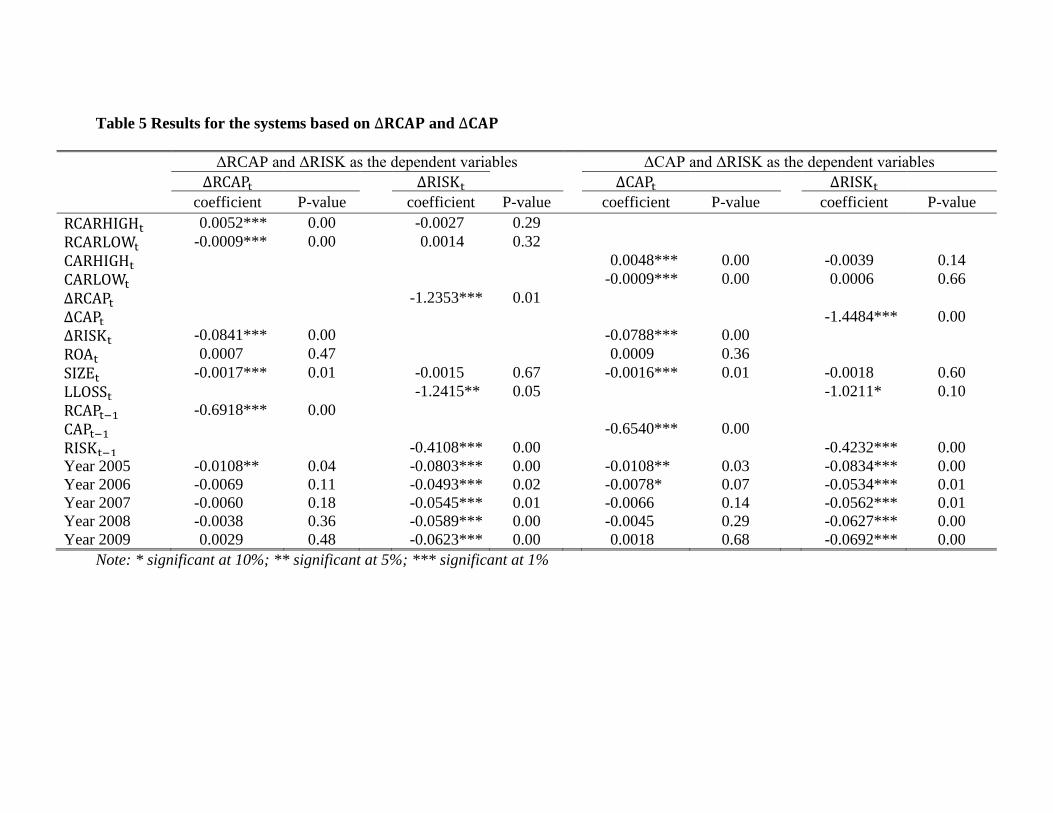

5.2 Results on RCAP and CAP

Table 5 shows the results of the simultaneous equations when the ratio of banks‟ capital (both

real and inflated capital) to total assets and the ratio of RWA to total assets are used as dependent

variables. The left-hand part of Table 5 presents the result for RCAP. One of the regulatory

pressure variables, RCARHIGH has a significantly positive effect on capital but no impact on

risk. Ceteris paribus, adequately-capitalised banks increase their real capital by 0.52 percent

more than other banks. The other regulatory pressure variable RCARLOW has a significantly

negative impact on the ratio of real total capital to RWA but no impact on risk. Ceteris paribus,

undercapitalised banks decrease their real capital ratio by 0.09 percent more than other banks. In

the controlling variables, both SIZE and LLOSS have significant impacts with expected signs. In

the capital equation, SIZE has a significantly negative impact, indicating that large Chinese

banks increase the ratio of their capital to RWA less than other banks. In the risk equation,

LLOSS has a significant and negative impact on credit risk, reflecting banks‟ increased capital

for covering bad loans. The right-hand part shows the estimates for CAP. Similarly, CARHIGH

has a significantly positive impact on the banks‟ inflated capital level for adequately-capitalised

banks. Specifically, these banks increase the total inflated capital ratio by 0.48 percent more than

other banks.

With the respect of the overall relationship either between CAP and RISK or between CAP

and RISK, we observe a negative and significant relationship between changes in capital and

changes in risk. In the case of relationship between RCAP and RISK, an increase of 1 percent

in the real capital to assets ratio decrease the credit risk by about 1.24 percents while a same

increase in the credit risk ratio causes a decrease in RCAP by about 0.08 percent.

To sum up, CBRC capital regulations have a positive effect on the improvement of Chinese

banks‟ capital adequacy (both real and inflated capital) and the decrease in their risk-taking

behaviour for adequately-capitalised banks regardless of the effect of cross-holding SD.

However, our results are less conclusive about the impacts of the capital requirements on the

capital constrained banks.

Table 5 here

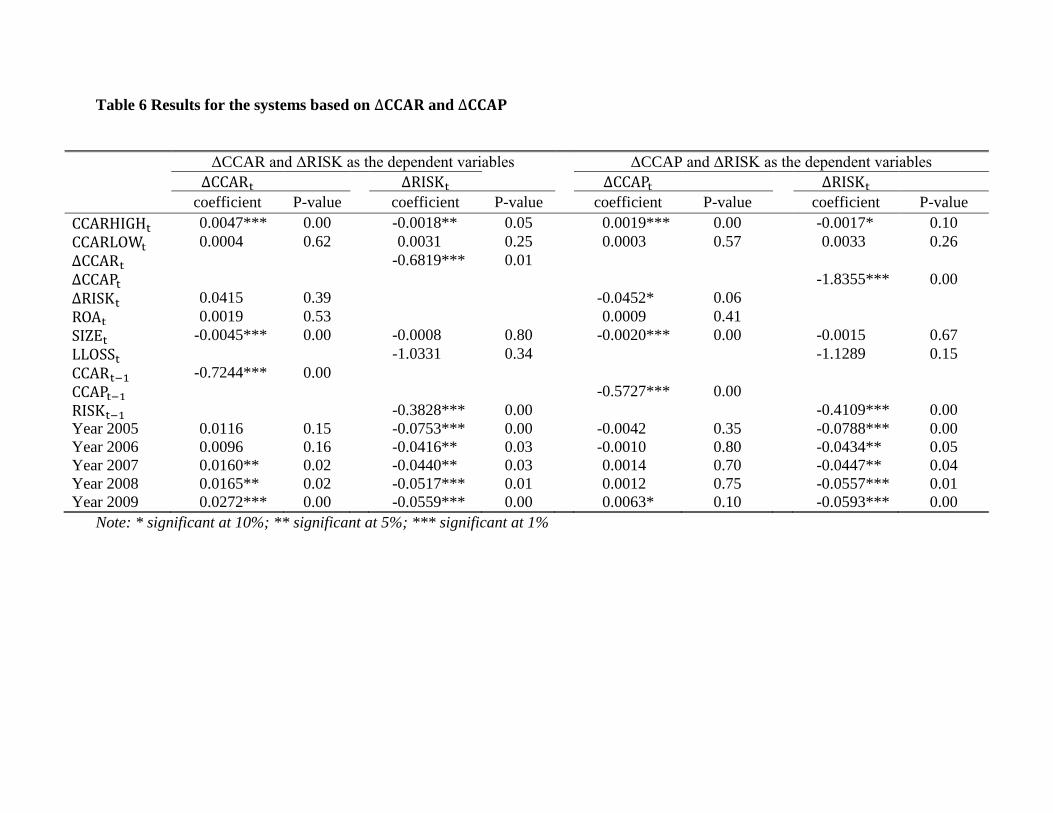

5.3 Robustness

In Sections 5.1 and 5.2, we examine the impacts of CBRC regulation on both real and inflated

capital ratios. In this section, core capital ratios are used for robustness check. Using the three-

stage least squares, we find that our estimation of the coefficients and the relationship between

the changes in the capital ratios and the changes in the credit risk level for Chinese banks, is

robust to alternative specifications.

Table 6 provides the results of the simultaneous equations when the ratio of banks‟ core capital

ratios and credit risk ratios are used as dependent variables. As noted, this alternative

specification yields similar estimations for Chinese banks. The left-hand part suggests that

CBRC regulation CCARHIGH has a positive effect on the capital ratios and the risk-taking

behaviour for adequately-capitalised banks. As for the undercapitalised banks, the regulation

pressure CCARLOW has no significant effect on both banks‟ capital ratio and credit risk-taking

behaviour. Regarding the overall relationship between the changes in capital ratios and that in

credit risk levels, a negative impact can be identified on the changes of capital ratios.

Specifically, Chinese banks adjust risk when their capital changes but they do not adjust capital

when risk changes. All other things being equal, an increase of 1 percent in bank‟s leads

to a decrease of 0.68 percent in the banks‟ . In the capital equation, most of the time

dummies, except that for 2005 and 2006, have significant positive effects on capital level,

suggesting that Chinese banks increase their target capital levels at the beginning of 2004.

Similarly, the right-hand part of Table 6 presents the results for the ratio of the core capital to

total assets. Most of the variables in the system display the same sign and level of significance as

the measurement on the ratio of core capital to RWA except for the changes in in the

capital equation, which shows a negative and significant effect on banks‟ core capital level as

well. Ceteris paribus, an increase of 1 percent in bank‟s leads to a decrease of around 0.06

percent in .

Table 6 here

6. Conclusion

This study initiatively explores the notion of real capital ratio by considering the cross-holding

portion of SDs and uses simultaneous measurements to examine how Chinese banks respond to

the regulatory capital regulations during the period 2004-2009. Our findings can be summarised

as follows. First, Chinese banks do improve their capital ratios by substantially cross-holding

other banks‟ SDs. Second, CBRC regulatory pressure has significant positive impacts on the

ratio of bank‟s capital to risk-weighted assets and the ratio of capital to total assets regardless of

the banks‟ window-dressing technique, without influencing bank‟s risk. This finding suggests

that Chinese banks may choose to increase the required capital through retained earnings or

equity issues, rather than adjusting the risk of their portfolio of assets. Third, our finding could

suggest the desire of adequately-capitalised banks to maintain larger buffers of capital and to

signal both regulators and market that they can clearly exceed the regulatory capital standards.

Fourth, changes in banks‟ credit risk and changes in capital ratios are significantly negatively

related, indicating that CBRC capital regulations are not only useful to improve capital level but

also helpful to limit risk-taking behaviour for adequately-capitalised banks. However, results for

the undercapitalised banks are not satisfying. More regulation should be implemented for the

undercapitalised banks.

In short, we can conclude that CBRC capital regulations are effective in increasing the capital

buffers for adequately-capitalised banks and in controlling their credit risk despite the window-

dressing through SDs. Our findings have rather important policy implications for that the capital

regulations have achieved to a large extent the desired effects on banks‟ capital and risk-taking

behaviour. This is consistent with the traditional view that Chinese regulators maintain rather

strict control over its financial institutions. However, the regulators‟ control has been weakened

by the common window-dressing practice and the risk-taking behaviour of undercapitalised

banks in the country.

References

Aggarwal, R. and K. Jacques. 1998. Assessing the impact of prompt corrective action on bank

capital and risk. Federal Reserve Bank of New York Policy Review 4: 23–31.

Aggarwal, R. and K. Jacques. 2001. The impact of FDICIA and prompt corrective action on

bank capital and risk: Estimates using a simultaneous equations model. Journal of Banking

and Finance 25: 1139-1160.

Altunbas, Y., S. Carbo, EPM. Gardener, and P. Molyneux. 2007. Examining the relationships

between capital, risk and efficiency in European banking. European Financial

Management 13: 49–70.

Allen, F., J. Qian, and M. Qian. 2005. Law, finance, and economic growth in China,

Journal of Financial Economics 77: 57-116.

Allen, F., and E. Carletti. 2008. Mark-to-market accounting and liquidity pricing, Journal of

Accounting and Economics 45: 358-378.

Allen, F., J. Qian, C. Shan, and M. Zhao. Forthcoming. The IPO of Industrial and Commercial

Bank of China and the „Chinese Model‟ of Privatizing Large Financial Institutions,

European Journal of Finance

Ariff, M. and L. Can. 2012. Cost and profit efficiency of Chinese banks: a non-parametric

analysis. China Economic Review 19: 260-273.

Basel Committee on Banking Supervision. 1999. Capital requirements and bank behaviour: The

impact of the Basel Accord. BIS Working Paper No. 1.

Berger, A.N. 1995. The Relationship between capital and earnings in banking. Journal of Money,

Credit, and Banking 27: 432-56.

Berger, A.N., I. Hasan, and M. Zhou. 2009. Bank ownership and efficiency in China: what will

happen in the world's largest nation? Journal of Banking and Finance 33: 113-130.

Bonin, J.P. and Y. Huang. 2001. Dealing with the bad loans of the Chinese banks.

Journal of Asian Economics 12: 197-214

Cannata, F. and M. Quagliariello. 2006. Capital and risk in Italian banks: A simultaneous

equation approach. Journal of Banking Regulation 7: 283-297.

Deelchand, T. and C. Padgett. 2009. The Relationship between risk, capital and efficiency:

evidence from Japanese cooperative banks. ICMA Centre Discussion Paper. DP 2009-12.

Dobson, W. and A.K. Kashyap. 2006. The contradiction in China's gradualist banking

reforms. Brookings Papers on Economic Activity 37: 103-148

Ediz, T., I. Michael, and W. Perraudin. 1998. Capital regulation and UK banks‟ behaviour.

Financial Stability Review 5, Bank of England.

Ferri, G. 2009. Are new tigers supplanting old mammoths in China's banking system? Evidence

from a sample of city commercial banks. Journal of Banking and Finance 33: 131-140.

Fiordelisi, F., D. Marques-Ibanez, and P. Molyneux. 2011. Efficiency and risk-taking in

European banking. Journal of Banking and Finance 35: 1315-1326

Fu, X. and S. Heffernan. 2009. The effects of reform on China's bank structure and performance.

Journal of Banking and Finance 33: 39-52

Furlong, F.T. and M.C. Keeley. 1989. Capital regulation and bank risk-taking: a note. Journal of

Banking and Finance 13: 883-891.

Gamble, W. 2003. Going Bust, Harvard International Review 25:54-57

García-Herrero, A., S. Gavilá, and D. Santabárbara. 2009. What explains the low profitability of

Chinese banks? Journal of Banking and Finance 33: 2080-2092.

Godlewski, C.J. 2005. Capital regulation and credit risk taking in emerging market economics.

Journal of Banking Regulation 6: 128-145.

Gordon, M.J. 2003. Is China's financial system threatened by its policy loans debt?

Journal of Asian Economics 14: 181-188

Gunther, J.W. and K.J. Robinson. 1990. Moral hazard and Texas banking in the 1980s: Was

there a connection? Federal Reserve Bank of Dallas Financial Industry Studies: 1-8.

Hart, O.D. and D.M. Jaffee. 1974. On the application of portfolio theory to depository financial

intermediaries. Review of Economic Studies 41: 129–47.

Haubrich, J.G. and P. Watchel. 1993. Capital requirements and shifts in commercial bank

portfolios. Economic Review, Federal Reserve Bank of Cleveland 29: 2-15.

Heid, F., D. Porath, and S. Stolz. 2004. Does capital regulation matter for bank behaviour?

Evidence for German savings banks. Discussion paper No. 03/2004, Deutsche Bundesbank.

Heid, F. 2007. The cyclical effects of the Basel II capital requirements. Journal of Banking and

Finance 31: 3885–3900.

Heilmann, S. 2005. Regulatory innovation by Leninist means: communist party supervision in

China's financial industry. China Quarterly 181: 1-21.

Huang, Y. 2002, Is meltdown of the Chinese banks inevitable? China Economic Review 13: 382-

387.

Jacques, K. and P. Nigro. 1997. Risk-based capital, portfolio risk, and bank capital: A

simultaneous equations approach. Journal of Economics and Business 49: 533-547.

Jokipii, T. and A. Milne. 2008. The cyclical behaviour of European bank capital buffers. Journal

of Banking and Finance 32: 1440–1451.

Kao, J.L., D.H. Wu, and Z.F. Yang. 2009. Regulations, earnings management, and post-IPO

performance: the Chinese evidence. Journal of Banking and Finance 33: 63-76.

Keeley, M.C. and F.T. Furlong. 1990. A re-examination of the mean-variance analysis of bank

capital regulation. Journal of Banking and Finance 14: 69-84.

Koehn, M. and A.M. Santomero. 1980. Regulation of bank capital and portfolio risk. Journal of

Finance 35: 1235-1244.

Kwong, C.C.L. and P.K. Lee. 2005. Bad loans versus sluggish rural industrial growth: a dilemma

of China‟s banking reform. Journal of the Asia Pacific Economy 10: 1-25.

Lin, S.L., J.H. Penm, S.C. Garg, and C.S. Chang. 2005. Risk based capital adequacy in assessing

on insolvency-risk and financial performances in Taiwan‟s banking industry. Research in

International Business and Finance 19: 111–153.

Ma, G. (2006), Who pays China‟s bank restructuring bill? CEPII Working Paper No. 2006–04.

McManus, D., and R. Rosen. 1991. Risk and capitalization in banking. In Rebuilding Banking,

Proceedings of the 27th Conference on Bank Structure and Competition, Federal Reserve

Bank of Chicago, 296-321.

Matthews, K. and X. Zhang. 2010. Bank productivity in China 1997–2007: measurement and

convergence. China Economic Review 21: 617-628.

Milne, A. and E. Whalley. 2001. Bank capital regulation and incentives for risk-taking. Mimeo.

City University Business School, London.

Myers, S.C. and N.C. Majluf. 1984. Corporate financing and investment decisions when firms

have information that investors do not have. Journal of Financial Economics 13: 187-221.

Nanto, D.K. and R. Sinha. 2002. China's banking reform, Post-Communist Economies 14: 469-

493

Nachane, D.M., S. Ghosh, and P. Ray. 2006. Basel II and bank lending behavior: some likely

implications for monetary policy. Economic and Political Weekly 41: 1053-1058

Ngo, PTH. 2008. Capital-Risk decisions and profitability in banking: Regulatory versus

economic capital. 21st Australasian Finance and Banking Conference 2008, Working

Paper Series.

Pyle, D.H. 1971. On the theory of financial intermediation. Journal of Finance 26: 737–47.

Rime, B. 2001. Capital requirements and bank behavior: Empirical evidence for Switzerland.

Journal of Banking and Finance 25: 789-805.

Saadaoui, Z. 2011. Risk-based capital standards and bank behavior in emerging and developed

countries. Journal of Banking Regulation 12: 180-191.

Shan, G. and L. Xu, 2012, Do Internal Governance Mechanisms Impact on Firm Performance?

Empirical Evidence from Financial Sector in China. Journal of Asia-Pacific Business 13:

114-142.

Sheldon, G. 1996. Capital adequacy rules requirements and the risk-seeking behaviour of banks:

a firm-level analysis. Swiss Journal of Economics and Statistics 132: 709-734

Shrieves, R.E. and D. Dahl. 1992. The relationship between risk and capital in commercial banks.

Journal of Banking and Finance 16: 439-457.

Wang, J. 2010. A comparison of shareholder identity and governance mechanisms in the

monitoring of CEOs of listed companies in China. China Economic Review 21: 24-37.

Xiao, G. 2006. Nonperforming debts in Chinese enterprises: patterns, causes, and implications

for banking reform. Asian Economic Papers 4: 61-113.

Xie, P. 1999. Bank restructuring in China. BIS Policy Papers 6, August: 124–129.

Xu, L. and C.T. Lin. 2007. Can Chinese banks compete after accession to WTO? Journal of

Asian Economics 18: 883-903

Van Roy, P. 2008. Capital requirements and bank behaviour in the early 1990: Cross-country

evidence. International Journal of Central Banking 4: 29–60.

Appendix A: List of Abbreviations

PBOC The People‟s Bank of China

CBRC China Banking Regulatory Commission

CICC China International Capital Corporation Limited

ICBC Industrial and Commercial Bank of China Limited

BOCM Bank of Communication

CCB China Construction Bank

BOC Bank of China

BOB Bank of Beijing

NJCB Bank of Nanjing

CMBC China Minsheng Banking Corporate.Ltd

NBCB Bank of Ningbo

SPDB Shanghai Pudong Development Bank

HXB Huaxia Bank

CNCB China Citic Bank

CMB China Merchants Bank

SDB Shenzhen Development Bank

CIB Industrial Bank Co.Ltd

Appendix B: Definition of Variables

RCAR: The ratio of calculated real total capital to risk-weighted assets.

CAR: The ratio of inflated total capital to risk-weighted assets.

RCAP: The ratio of calculated real total capital to total assets.

CAP: The ratio of inflated total capital to total assets.

RISK: The ratio of risk-weighted assets to total assets.

CCAR: The ratio of total core capital to risk-weighted assets.

CCAP: The ratio of total core capital to total assets.

ΔRCAR: The difference between the current and the lagged RCAR.

ΔCAR: The difference between the current and the lagged CAR.

ΔRCAP: The difference between the current and the lagged RCAP.

ΔCAP: The difference between the current and the lagged CAP.

ΔRISK: The difference between the current and the lagged RISK.

ΔCCAR: The difference between the current and the lagged CCAR.

ΔCCAP: The difference between the current and the lagged CCAP.

RCARHIGH: The difference between the inverse of the regulatory minimum risk-based capital

ratio (RBC) and the inverse of bank i‟s real risk-based capital ratio; RCARHIGH equals to

(1/ 1/ for banks with RCAR greater than the capital ratio requirement

and 0 otherwise.

RCARLOW: The difference between the inverse of bank i‟s real risk-based capital ratio and the

inverse of the regulatory minimum risk-based capital ratio (RBC); RCARLOW equals to

(1/ 1/ for banks with RCAR less than the capital ratio requirements

and 0 otherwise.

CARHIGH: The difference between the inverse of the regulatory minimum risk-based capital

ratio (RBC) and the inverse of bank i‟s inflated risk-based capital ratio; CARHIGH equals to

(1/ 1/ for banks with CAR greater than the capital ratio requirement

and 0 otherwise.

CARLOW: The difference between the inverse of bank i‟s inflated risk-based capital ratio and

the inverse of the regulatory minimum risk-based capital ratio (RBC); CARLOW equals to

(1/ 1/ for banks with CAR less than the capital ratio requirements and

0 otherwise.

CCARHIGH: The difference between the inverse of the regulatory minimum risk-based core

capital ratio (core RBC) and the inverse of bank i‟s risk-based core capital ratio; CCARHIGH

equals to (1/ 1/ for banks with CCAR greater than the core

capital ratio requirement and 0 otherwise.

CCARLOW: The difference between the inverse of bank i‟s risk-based core capital ratio and the

inverse of the regulatory minimum risk-based core capital ratio (core RBC); CCARLOW equals

to (1/ 1/ for banks with CCAR less than the core capital ratio

requirement and 0 otherwise.

ROA: The ratio of net income to total assets.

SIZE: The natural log of total assets.

LLOSS: The ratio of loan loss reserve to total assets.

Table 1 Information about Chinese Banks’ SD Issuance (Unit: 1 million RMB)

Panel A: Large-Sized Commercial Banks

Bank Name 31/12/2004 31/12/2005 31/12/2006 31/12/2007 31/12/2008 31/12/2009

CCB 23,300 40,000 40,000 40,000 40,000 80,000

ICBC 0 35,000 35,000 35,000 35,000 75,000

BOC 26,070 60,000 60,000 60,000 60,000 73,930

BOCM 12,000 12,000 12,000 37,000 37,000 50,000

Panel B: Small-and-Medium-Sized Commercial Banks

Bank Name 31/12/2004 31/12/2005 31/12/2006 31/12/2007 31/12/2008 31/12/2009

CMB 3,500 3,500 3,500 3,500 33,500 30,000

SPDB 6,000 8,000 10,600 16,600 24,800 18,800

CNCB 6,000 6,000 12,000 12,000 12,000 12,000

CIB 6,000 6,000 6,000 6,000 6,000 10,000

HXB 4,250 4,250 6,250 6,250 6,250 6,250

SDB 0 0 0 0 8,000 8,000

BOB 0 3,500 3,500 3,500 3,500 3,500

CMBC 5,800 7,200 7,200 7,200 7,200 1,400

NJCB 0 800 800 800 800 800

NBCB 0 0 0 0 0 0

Note: NBCB does not have SD outstanding from 2004 to 2009. Banks’ full names can be found in

Appendix A.

Table 2 Mean of CAR, RCAR, CAP and RCAP

RCAR vs. CAR RCAP vs. CAP

2004 7.47% 8.14% 4.53% 4.97%

2005 7.95% 8.76% 4.55% 5.03%

2006 9.09% 9.86% 5.19% 5.65%

2007 11.99% 12.78% 6.44% 6.90%

2008 12.06% 12.86% 6.60% 7.07%

2009 10.67% 11.38% 6.02% 6.44%

Average 9.87% 10.63% 5.56% 6.01%

Source: Banks’ quarterly financial reports and authors’ calculation.

Table 3 Mean of variables

2004 2005 2006 2007 2008 2009

0.7111 0.9901 1.8475 3.4448 2.8614 0.8663

3.9290 2.6598 1.6529 0.2861 0.3857 0.6782

1.0740 1.4210 2.3413 4.0098 3.3185 1.1774

3.1825 1.9864 1.2070 0.1558 0.0863 0.2753

6.3317 6.5441 9.0537 12.9469 11.6358 7.4511

2.1030 0.6534 0.1357 0.0000 0.0000 0.0441

(RCWA) 0.0860 0.0718 0.0855 0.1028 0.1234 0.1126

(CWA) 0.0873 0.0781 0.0934 0.1111 0.1309 0.1202

(RCTA) 0.0471 0.0438 0.0493 0.0564 0.0669 0.0626

(CTA) 0.0479 0.0477 0.0541 0.0612 0.0713 0.0670

(RWA) 0.5585 0.6249 0.5793 0.5560 0.5551 0.5630

(CCWA) 0.0637 0.0524 0.0661 0.0829 0.1039 0.0920

(CCTA) 0.0349 0.0326 0.0385 0.0459 0.0568 0.0515

-0.0113 0.0077 0.0054 0.0171 -0.0027 -0.0060

-0.0059 0.0095 0.0052 0.0167 -0.0023 -0.0064

-0.0018 0.0018 0.0026 0.0081 -0.0008 -0.0023

0.0018 0.0026 0.0025 0.0079 -0.0006 -0.0026

0.0699 -0.0474 -0.0010 -0.0069 0.0028 0.0058

-0.0081 0.0059 0.0059 0.0168 -0.0035 -0.0048

-0.0008 0.0011 0.0028 0.0081 -0.0013 -0.0018

0.0036 0.0045 0.2327 0.0064 0.0082 0.0061

0.0146 0.0166 0.0148 0.0124 0.0117 0.0098

(natural log) 13.0043 13.3076 13.7615 14.0197 13.9821 14.1831

Source: Banks’ quarterly financial reports and authors’ calculation.

Table 4 Results for the systems based on and

ΔRCAR and ΔRISK as the dependent variables ΔCAR and ΔRISK as the dependent variables

coefficient P-value coefficient P-value coefficient P-value coefficient P-value

0.0131*** 0.00 -0.0028 0.24

-0.0020*** 0.00 0.0012 0.37

0.0131*** 0.00 -0.0039 0.11

-0.0018*** 0.00 0.0006 0.63

-0.4164** 0.05

-0.5176** 0.01

0.0403 0.32 0.0385 0.37

0.0014 0.58 0.0020 0.44

-0.0034*** 0.00 -0.0013 0.67 -0.0034*** 0.00 -0.0015 0.63

-0.5150 0.65 -0.5876 0.60

-0.8725*** 0.00

-0.8539*** 0.00

-0.3907*** 0.00 -0.3908*** 0.00

Year 2005 0.0062 0.36 -0.0798*** 0.00 0.0064 0.37 -0.0797*** 0.00

Year 2006 0.0019 0.73 -0.0488*** 0.01 0.0009 0.87 -0.0496*** 0.01

Year 2007 0.0064 0.26 -0.0538*** 0.01 0.0054 0.37 -0.0526*** 0.01

Year 2008 0.0119** 0.04 -0.0549*** 0.00 0.0117** 0.05 -0.0563*** 0.00

Year 2009 0.0267*** 0.00 -0.0567*** 0.00 0.0274*** 0.00 -0.0615*** 0.00

Note: * significant at 10%; ** significant at 5%; *** significant at 1%

Table 5 Results for the systems based on and

ΔRCAP and ΔRISK as the dependent variables ΔCAP and ΔRISK as the dependent variables

coefficient P-value coefficient P-value coefficient P-value coefficient P-value

0.0052*** 0.00 -0.0027 0.29

-0.0009*** 0.00 0.0014 0.32

0.0048*** 0.00 -0.0039 0.14

-0.0009*** 0.00 0.0006 0.66

-1.2353*** 0.01

-1.4484*** 0.00

-0.0841*** 0.00 -0.0788*** 0.00

0.0007 0.47 0.0009 0.36

-0.0017*** 0.01 -0.0015 0.67 -0.0016*** 0.01 -0.0018 0.60

-1.2415** 0.05 -1.0211* 0.10

-0.6918*** 0.00

-0.6540*** 0.00

-0.4108*** 0.00 -0.4232*** 0.00

Year 2005 -0.0108** 0.04 -0.0803*** 0.00 -0.0108** 0.03 -0.0834*** 0.00

Year 2006 -0.0069 0.11 -0.0493*** 0.02 -0.0078* 0.07 -0.0534*** 0.01

Year 2007 -0.0060 0.18 -0.0545*** 0.01 -0.0066 0.14 -0.0562*** 0.01

Year 2008 -0.0038 0.36 -0.0589*** 0.00 -0.0045 0.29 -0.0627*** 0.00

Year 2009 0.0029 0.48 -0.0623*** 0.00 0.0018 0.68 -0.0692*** 0.00

Note: * significant at 10%; ** significant at 5%; *** significant at 1%

Table 6 Results for the systems based on and

ΔCCAR and ΔRISK as the dependent variables ΔCCAP and ΔRISK as the dependent variables

coefficient P-value coefficient P-value coefficient P-value coefficient P-value

0.0047*** 0.00 -0.0018** 0.05 0.0019*** 0.00 -0.0017* 0.10

0.0004 0.62 0.0031 0.25 0.0003 0.57 0.0033 0.26

-0.6819*** 0.01

-1.8355*** 0.00

0.0415 0.39 -0.0452* 0.06

0.0019 0.53 0.0009 0.41

-0.0045*** 0.00 -0.0008 0.80 -0.0020*** 0.00 -0.0015 0.67

-1.0331 0.34 -1.1289 0.15

-0.7244*** 0.00

-0.5727*** 0.00

-0.3828*** 0.00 -0.4109*** 0.00

Year 2005 0.0116 0.15 -0.0753*** 0.00 -0.0042 0.35 -0.0788*** 0.00

Year 2006 0.0096 0.16 -0.0416** 0.03 -0.0010 0.80 -0.0434** 0.05

Year 2007 0.0160** 0.02 -0.0440** 0.03 0.0014 0.70 -0.0447** 0.04

Year 2008 0.0165** 0.02 -0.0517*** 0.01 0.0012 0.75 -0.0557*** 0.01

Year 2009 0.0272*** 0.00 -0.0559*** 0.00 0.0063* 0.10 -0.0593*** 0.00

Note: * significant at 10%; ** significant at 5%; *** significant at 1%

![BAYESIAN INFERENCE FOR ZERO-INFLATED …scientificadvances.co.in/admin/img_data/562/images/[2] JSATA... · Keywords and phrases: Bayes, zero-inflated Poisson, regression analysis,](https://img.pdfslide.us/doc/110x75/5a78eb487f8b9ae6228ef3c1/bayesian-inference-for-zero-inflated-2-jsatakeywords-and-phrases-bayes.jpg)