Embed Size (px)

DESCRIPTION

Deals with the better method of measuring the corporate performance through determination of EVA.

Citation preview

Measuring Corporate Measuring Corporate Performance – An EVA Performance – An EVA ApproachApproach

Dr Sarbesh MishraDr Sarbesh MishraFinance Area, NICMAR, HyderabadFinance Area, NICMAR, Hyderabad..

BackdropBackdrop““If we don’ t know where If we don’ t know where we’re going, it doesn’t matter we’re going, it doesn’t matter how we get there” (Attitude = how we get there” (Attitude = 100%)100%)

Recent Buzzword in IndustryRecent Buzzword in Industry:: TransparencyTransparency AccountabilityAccountability Business EthicsBusiness Ethics Social ResponsibilitySocial Responsibility Shareholder’s interest protectionShareholder’s interest protection

Necessity of Corporate Necessity of Corporate GovernanceGovernance

1.1. Too much of power with few individual.Too much of power with few individual.2.2. Large scale diversion of funds to Large scale diversion of funds to

associated companies & risky associated companies & risky ventures.ventures.

3.3. Unfocussed business decisions leading Unfocussed business decisions leading to losses.to losses.

4.4. Preferential allotment of sweat equity Preferential allotment of sweat equity at low prices.at low prices.

5.5. Spinning off profitable business Spinning off profitable business operations to subsidiary companies.operations to subsidiary companies.

Recent HappeningsRecent HappeningsWorld ComWorld Com – Improper accounting of – Improper accounting of

$3.9bn in expenses leading to $3.9bn in expenses leading to bankruptcy.bankruptcy.

Enron Enron – Off balance sheet deals used – Off balance sheet deals used to hide the debt.to hide the debt.

AOL WarnerAOL Warner – AOL division accused of – AOL division accused of improperly accounted for some improperly accounted for some advertising revenues.advertising revenues.

XEROXXEROX – Financial Fraud. – Financial Fraud.UTIUTI – Indiscriminate investment by UTI. – Indiscriminate investment by UTI.

OriginOriginThe Sarbanes – Oxley Act, 2002, a The Sarbanes – Oxley Act, 2002, a recent enactment in USA which recent enactment in USA which deals with the Corporate deals with the Corporate Governance & Corporate Social Governance & Corporate Social Responsibilities has emphasized Responsibilities has emphasized audit functions & financial audit functions & financial disclosures. (Mandatory as per disclosures. (Mandatory as per NYSE listing Norms)NYSE listing Norms)(Benchmark practices in this regard is (Benchmark practices in this regard is calculation of EVA apart from Annual calculation of EVA apart from Annual Accounts)Accounts)

Indian ContextIndian Context

Kumara Mangalam Birla Committee Kumara Mangalam Birla Committee on Corporate Governance (2000) on Corporate Governance (2000) (SEBI (SEBI Sponsored)Sponsored)

Naresh Chandra Committee on Naresh Chandra Committee on Corporate Governance (2002)Corporate Governance (2002)

Narayana Murthy Committee on Narayana Murthy Committee on Corporate GovernanceCorporate Governance

What is EVA?What is EVA?New York based financial advisory New York based financial advisory Stern Stern Stewart & Co.Stewart & Co. postulated the very concept postulated the very concept of Economic Value Added (EVA) in 1990.of Economic Value Added (EVA) in 1990.

EVAEVA: Maximum amount which the : Maximum amount which the business is capable of distributing to business is capable of distributing to its shareholders while remaining in its shareholders while remaining in the same position at the end of the the same position at the end of the period as it was at the beginning with period as it was at the beginning with fair practices.fair practices.

EVA FormulaEVA Formula

EVA = NOPAT - Cost of Capital

1.1. NOPAT = Net operating Profit after TaxNOPAT = Net operating Profit after Tax

2.2. The The project’s cost of capitalproject’s cost of capital is the is the minimum required rate of return on funds minimum required rate of return on funds committed to the project, which depends on committed to the project, which depends on the riskiness of its cash flows.the riskiness of its cash flows.

The firm’s cost of capitalThe firm’s cost of capital will be the overall will be the overall (WACC), or average, required rate of return on (WACC), or average, required rate of return on the aggregate of investment projectsthe aggregate of investment projects..

Summary of DefinitionSummary of Definition

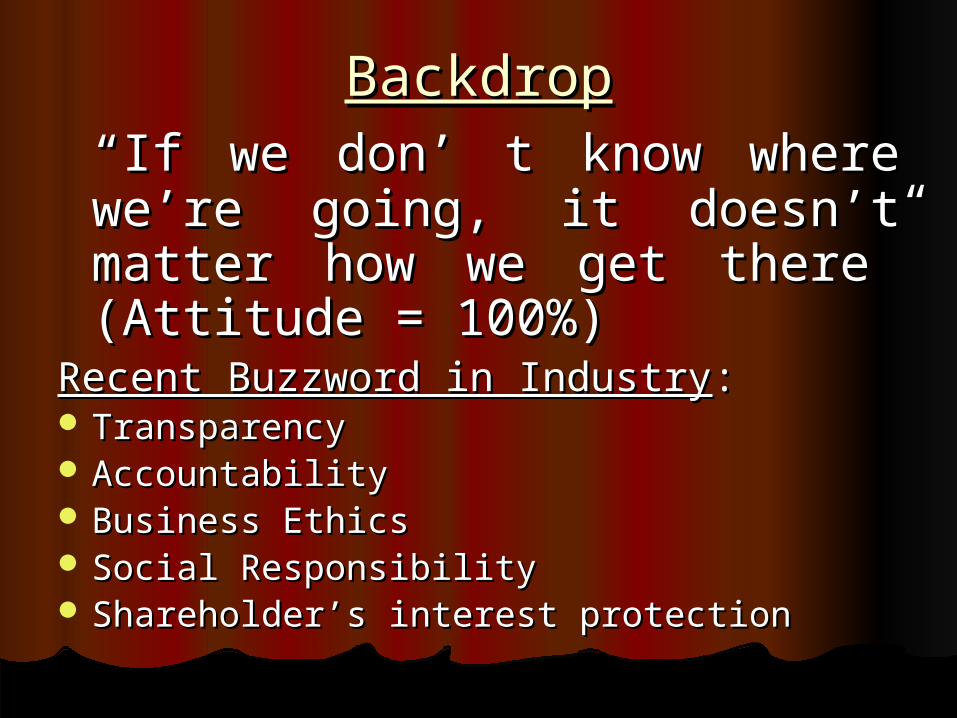

Thus EVA measures the Operating Thus EVA measures the Operating Profit, which should be fair enough to Profit, which should be fair enough to meet the cost of capital. So excess of meet the cost of capital. So excess of returns over cost of capital is returns over cost of capital is otherwise referred as EVA.otherwise referred as EVA.

If EVA is If EVA is

+Ve+Ve = Firm is creating shareholder’s wealth = Firm is creating shareholder’s wealth

-Ve-Ve = Firm is destroying shareholder’s = Firm is destroying shareholder’s wealthwealth

Computation of NOPATComputation of NOPAT

Profit after tax but before InterestProfit after tax but before Interest

+ Increase to Deferred Taxes+ Increase to Deferred Taxes

+ Goodwill Amortized in Current year+ Goodwill Amortized in Current year

+ Increase to Net Capitalized + Increase to Net Capitalized IntangiblesIntangibles

+/- Unusual loss or (Gains) net of tax+/- Unusual loss or (Gains) net of taxN. B: Some 144 adjustments are thereN. B: Some 144 adjustments are there

Implementation of EVAImplementation of EVA

MeasurementMeasurementManagement SystemManagement SystemMotivationMotivationMindsetMindset

Key Strategies to Enhance Key Strategies to Enhance EVAEVA

Operate: Set targets to Improve ROCE.

Build: Invest capital only when return exceeds the cost of the capital.

Divest: Divest capital when return fail to achieve cost of capital.

Optimise: Restructure capital to reduce the cost of the Capital.

EVA Determination – A Case EVA Determination – A Case StudyStudy

Calculation of EVA Calculation of EVA for NTPC in FY for NTPC in FY 2005-062005-06

Calculation of EVA for NTPCCalculation of EVA for NTPC

1.1. EVA= NOPAT- Cost of CapitalEVA= NOPAT- Cost of Capital = PAT+ Interest paid – WACC = PAT+ Interest paid – WACC ( Average Capital)( Average Capital)

Calculation for NTPC for FY 2004-05Calculation for NTPC for FY 2004-05

= (5,500cr+1,000cr) - WACC = (5,500cr+1,000cr) - WACC 1/2(Capital at the beginning of the 1/2(Capital at the beginning of the year + Capital at the end of the year)year + Capital at the end of the year)

WorkingsWorkings

WACC = Ke* W1 +Kd* W2WACC = Ke* W1 +Kd* W2 Debt : EquityDebt : Equity

= 0.14 * 0.7 + 0.8(1- Tax) * 0.3 = 0.14 * 0.7 + 0.8(1- Tax) * 0.3 30 : 30 : 7070

= 0.98 + 0.3 * (0.8 * 0.65)= 0.98 + 0.3 * (0.8 * 0.65) W2 : W1W2 : W1

= 0.98 + 0.3 * 0.52= 0.98 + 0.3 * 0.52 Ke = 14% as Ke = 14% as per govt. normsper govt. norms

= 0.098 + 0.15= 0.098 + 0.15 Kd = Int. paid/Loan Kd = Int. paid/Loan Taken Taken = 0. 254= 0. 254 Tax= 35% Tax= 35%

Calculation of Cost of EquityCalculation of Cost of Equity

Cost of Equity can also be calculated taking Cost of Equity can also be calculated taking CAPM modelCAPM model

Ke Ke =Rf + =Rf + B B (Rm – Rf)(Rm – Rf) Rf = Risk Free Rate of ReturnRf = Risk Free Rate of Return

= = 0.08 + 0.8 (0.14 – 0.08 ) 0.08 + 0.8 (0.14 – 0.08 ) Rm = Market Rate of Rm = Market Rate of ReturnReturn

= 0.08 + 0.8 * 0.06= 0.08 + 0.8 * 0.06 BB = Beta Coefficient for = Beta Coefficient for NTPCNTPC = 0.134= 0.134

BB = = Covariance of Rm & RfCovariance of Rm & Rf

Variance of RmVariance of Rm

EVA of NTPCEVA of NTPC

EVA EVA = 6,500 – 0.254 ( 20,000 )= 6,500 – 0.254 ( 20,000 )

= 6,500 - 5080= 6,500 - 5080

= Rs 1420 Cr EVA= Rs 1420 Cr EVA

A positive EVA indicates that A positive EVA indicates that this company creates value. It this company creates value. It helps managers to create value helps managers to create value for share holders.for share holders.

Strategies for increasing EVAStrategies for increasing EVA

Increase the return on existing project.Increase the return on existing project. Invest in new projects that have a Invest in new projects that have a

return greater than the cost of capital..return greater than the cost of capital..Use less capital to achieve the same Use less capital to achieve the same

return.return.Reduce the cost of capital.Reduce the cost of capital.Curtail further investment in sub-Curtail further investment in sub-

standard operations where inadequate standard operations where inadequate returns are being earned.returns are being earned.

EVA DeficiencyEVA DeficiencyNot easy to use (for calculation of Not easy to use (for calculation of

PAT, some 144 adjustments are PAT, some 144 adjustments are there) too complicated for small there) too complicated for small business.business.

Recommends inexpensive debts in Recommends inexpensive debts in order to reduce cost of capital (COC), order to reduce cost of capital (COC), is a very questionable strategy for is a very questionable strategy for small business.small business.

A passive accounting tool : measures A passive accounting tool : measures past performance.past performance.

InferenceInference

Thus, A company must strive Thus, A company must strive continuously to increase not only continuously to increase not only profitability but also the EVA.profitability but also the EVA.

EVA reflects high net worth of the EVA reflects high net worth of the company, thus it’s credibility company, thus it’s credibility increases.increases.

In India, Companies like Dr. Reddy’s In India, Companies like Dr. Reddy’s Lab, WIPRO, INFOSYS are coming up Lab, WIPRO, INFOSYS are coming up with their respective EVAs along with with their respective EVAs along with their Annual Report.their Annual Report.