Embed Size (px)

Citation preview

September 2016

An Emerging Precious Metal & Polymetallic Developer and Mine Operator in South America

This presentation contains forward-looking statements and factual information that are current as of the date the presentation was originally delivered. Prism Resources Inc and Miranda Gold Corp. disclaims any intention or obligation to update or revise any forward-looking statements, whether as a result of new information, future events or otherwise.

Forward-looking statements include, but are not limited to, statements with respect to the timing

and amount of estimated future exploration, success of exploration activities, expenditures, permitting, and requirements for additional capital and access to data.

Forward looking statements involve known and unknown risks, uncertainties, and other factors

which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by the forward looking statements. Such factors include, among others, risks related to actual results of current exploration activities; changes in project parameters as plans continue to be refined; the ability to enter into joint ventures or to acquire or dispose of properties; future prices of mineral resources; accidents, labor disputes and other risks of the mining industry; ability to obtain financing; and delays in obtaining governmental approvals of financing.

The information in this presentation has been obtained by Miranda from its own records and from

Prism Resources Inc other sources deemed reliable. However, no representation or warranty is made as to its accuracy or completeness.

Forward Looking Statement

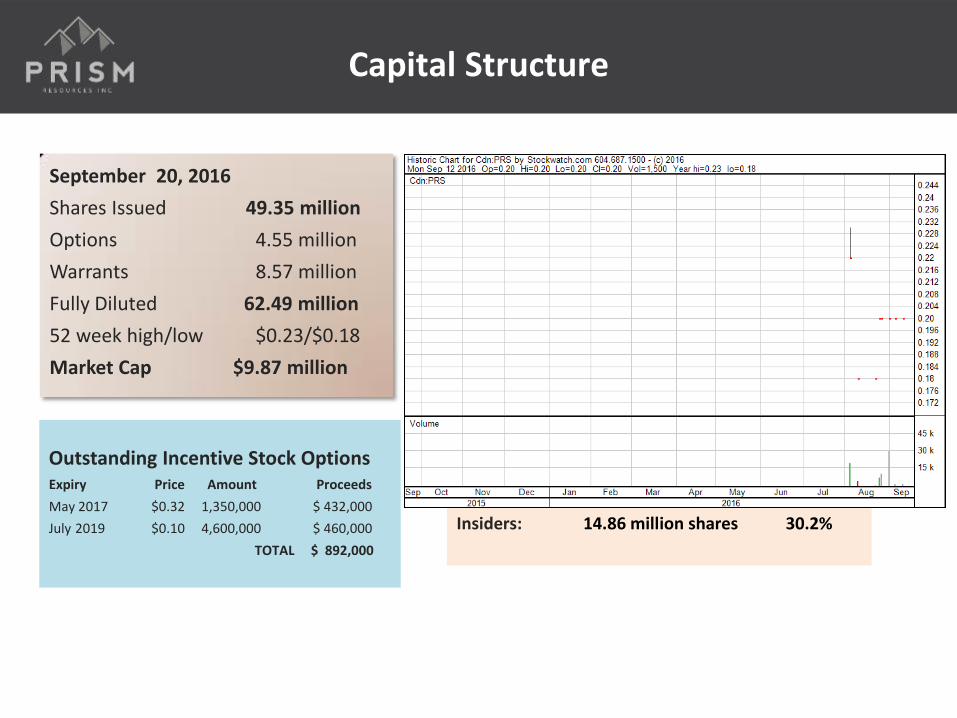

Capital Structure September 20, 2016

Shares Issued 49.35 million

Options 4.55 million

Warrants 8.57 million

Fully Diluted 62.49 million

52 week high/low $0.23/$0.18

Market Cap $9.87 million

Outstanding Incentive Stock Options Expiry Price Amount Proceeds

May 2017 $0.32 1,350,000 $ 432,000

July 2019 $0.10 4,600,000 $ 460,000

TOTAL $ 892,000

Insiders: 14.86 million shares 30.2%

Capital Structure

Officers

BOB BAXTER President & CEO

Mr. Baxter brings over 25 years of experience principally in Latin America, in the mining industry. Mr Baxter has held a number of important positions in

Latin America . In recent times Mr. Baxter was a Director of Chariot Resources Ltd.; until September 2010, Chairman of the Board of Marobre S.A.C.,

a 100% owned subsidiary of China Sci Tech; a Director of Petaquilla Minerals until November 2009; and President, Director and Chief Operating

Officer of Norsemont Mining until March 2011 when the company was acquired by Hudbay Minerals. Mr Baxter is presently a Director of Pan Global

Resources Inc. and is the General Manager of Baxter Consulting Engineering

RICHARD DUFRESNE Vice-President of Exploration

Mr. Dufresne brings to Prism more than 25 years of experience in the mineral exploration and development industry. He has held senior positions with

major mining companies including Anglo American Exploration (Canada) and Falconbridge (which was subsequently acquired by Xstrata/Glencore).

More recently, he was a senior geologist for Balmoral Resources in northern Quebec and prior to this role between 2009 and 2014 he held the position

VP Exploration for Camino Minerals in Mexico.

Mr. Dufresne has considerable international exploration experience in Peru, Mexico, Dominican Republic and the Ivory Coast. He has participated in

several new discoveries in the Raglan district of northern Quebec and the central lead-zinc-silver belt in Peru, where one discovery was recognized as

the Mining Prospect of the Year by the Peruvian Mining Merit Awards Committee in 2002. Mr. Dufresne graduated from the University of Montreal with

a B.Sc. in geology and is a member of the Association of Professional Engineers and Geoscientists of British Columbia (APEGBC) and of Ordre des

Géologues du Québec (OGQ).

OSCAR RUIZ FRANCO CFO

Mr Ruiz has 20 years of accounting, administration and finance experience in Peru and Canada in the mining, pharmaceutical and administration

support industries and holds a Bachelor of Accounting from Federico Villarreal National University, Lima, Peru.

SCOTT ROSS Corporate Secretary

Mr. Ross has many years of experience working with public and private companies. From 1988 to 1999 he served as Manager, Development for

Canlan Investment Corporation, a public real estate development company specializing in the construction and management of recreational ice rink

facilities across North America and golf course residential development in British Columbia. Since 2001 he has served as Vice-President and Director

of Rosstree Capital Corporation, a private investment holding company and he is currently a Director and President and Chief Executive Officer of

Bearclaw Capital Corp., a reporting issuer on the TSXV. He has a Bachelor of Arts (Hons) from Queen’s University, Kingston, Ontario.

Independent Directors

BOB PARSONS CPA, CA

Mr. Parsons is a Chartered Professional Accountant (CPA, CA) and retired PricewaterhouseCoopers (PwC) partner where his career spanned 34 years. At PwC, Bob headed up the firm’s global mining practice. Following retirement from PwC, as an independent consultant Bob has advised more than twenty governments around the world on mineral policy matters, and has served on the board of directors of nine listed mineral exploration companies. Bob is currently a director of Kennady Diamonds Inc., Indico Resources Ltd., and Pan Global Resources Inc. He has served on the boards of the PDAC (1985-2003), the Indonesian Mining Association, the Canada Indonesia Chamber of Commerce, the World Mines Ministries Forum, the Canadian Minerals Industry Federation, the Advisory Council of the Centre for Resource Studies at Queens University, and the Professional Advisory Board of the Government of Canada's Petroleum Monitoring Agency. In 2005, the PDAC presented Bob with their Distinguished Services Award, and in 2013 the Government of Canada awarded him the Queen Elizabeth II Diamond Jubilee Medal for his contribution to Canada’s mining industry. Mr. Parsons is a graduate of McGill University (B.Com, 1968) and a resident of British Columbia.

BRIAN KERZNER

Mr. Kerzner has over 23 years of experience as a successful entrepreneur in retailing and real estate. Mr. Kerzner is the Founder and President of Rocky Mountain Chocolate Factory Canada Inc., which operates retail chocolate stores from coast to coast in Canada. He has also founded several other private companies that have completed extensive residential and commercial development in Toronto, Phoenix, Whistler and Vancouver. Mr Kerzner has been extensively involved in providing seed capital for many successful public and private companies in the resources, environmental and technology sectors. Mr. Kerzner is an Honours graduate of the University of Toronto Bachelor of Commerce (B.Com) program and was a Director of Norsemont Mining Inc. He is also a member of the BC Children’s Hospital Circle of Care and is actively involved in many other charitable organizations.

DR. MARK CRUISE

Base metal deposit specialist with over 20-years project experience from grass-roots exploration through resource definition to permitting and production in Europe and the America’s on behalf of Pasminco Exploration, Anglo American and TSX-listed companies. Completed Geology Ph.D. on the Irish zinc-lead orefield and was a member of Anglo American’s Lisheen Zinc-Lead Mine feasibility/technical team in Ireland. Co-founded Trevali in 2007 to position the Company to take advantage of anticipated global Zn deficits.

Independent Directors

JULIAN BAVIN

Mr. Bavin has 30 years of technical, operational and commercial experience in mineral exploration gained from work in a wide range of commodities, jurisdictions and cultures most of which was spent with the Rio Tinto Group in South America, Australia, Indonesia and Europe. From 2000 to 2001 he was the Business Development Executive for the Industrial Minerals Group in Rio Tinto progressing opportunities in Europe and South America and from 2001 to 2009 he was the Exploration Director for the Rio Tinto Group in South America and responsible for the teams which identified the potential in a range of projects now in various stages of feasibility including the Rio Colorado potash and Alter copper/gold projects in Argentina, the Mina Justa, Constancia and La Granja copper projects in Peru, and the Amargosa bauxite project in Brazil. After South America he moved to London as Rio Tinto’s Exploration Director responsible for Africa, Europe, the Middle East and the FSU with a brief that included the Jadar lithium-borates discovery in Serbia (now in feasibility or FS). Mr Bavin is President and CEO of Pan Global Resources Inc and a non-executive Director of Estrella Resources and Exeter Resource Corp.

Mr. Bavin has a Bachelor of Science from the University of Leicester, a Master of Science from Imperial College in London, and is a graduate of the Senior Executive Programme at the London Business School.

TIM MOODY

Tim Moody has had over 30 years of experience in the mining industry. This includes mineral exploration, resource assessment, business development, strategy and government relations. Twenty-Four of those years have been spent with Rio Tinto.

Mr. Moody has an impressive track record in the discovery of mineral resources and completing commercial transactions in Australia, Asia, Latin America, Africa, Europe and North America. He has led teams in the identification and exploration of several projects now in feasibili ty and/or production status. These include Mina Justa, Constancia, La Granja, Corani and Ollachea.

Rio Tinto

During 2005-2010, Mr. Moody served as Exploration Director for the Project Generation Group, Asia Region. From 2010 to 2015, he was Vice President and Director for Business Development.

As Director of Business Development at Rio Tinto, his responsibilities included corporate strategy, M&A and public market transactions. His recent achievements include the takeover of Hathor Exploration Ltd. and leading the divestment of the Northparkes Mine. His work in the international arena has provided him with the opportunity to build an impressive network of business and government contacts.

Mr. Moody has a Bachelor of Science with Honours from the University of New England. He is a graduate of the Senior Leadership Program from the London Business School, a graduate of the Business Leadership Development Program from the Australian Graduate School of Management, and is a Fellow of the Society of Economic Geologists.

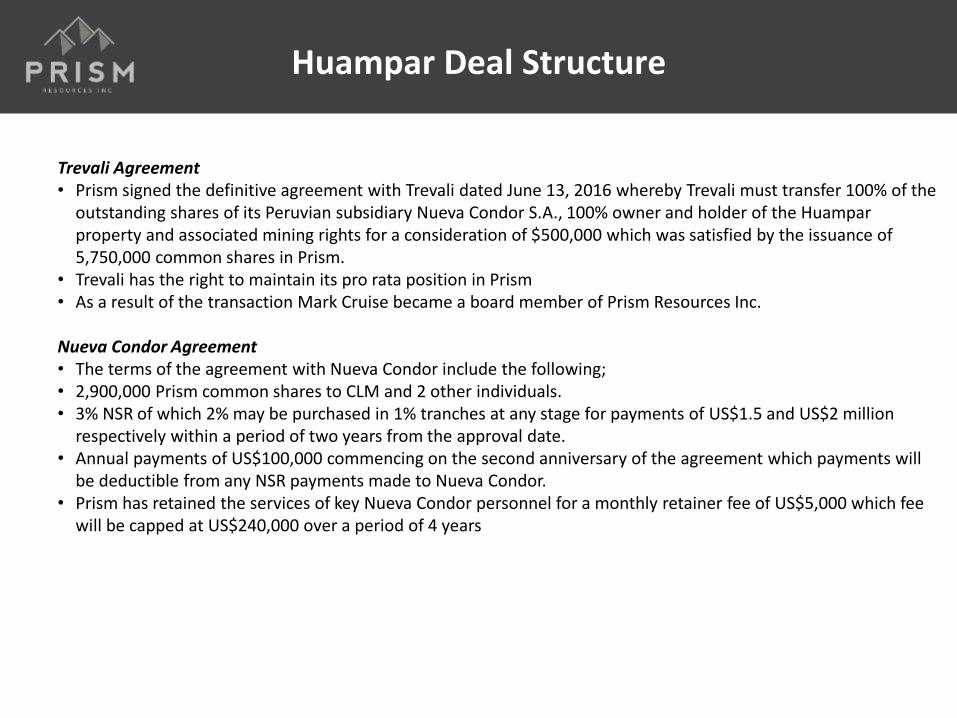

Huampar Deal Structure

Trevali Agreement • Prism signed the definitive agreement with Trevali dated June 13, 2016 whereby Trevali must transfer 100% of the

outstanding shares of its Peruvian subsidiary Nueva Condor S.A., 100% owner and holder of the Huampar property and associated mining rights for a consideration of $500,000 which was satisfied by the issuance of 5,750,000 common shares in Prism.

• Trevali has the right to maintain its pro rata position in Prism • As a result of the transaction Mark Cruise became a board member of Prism Resources Inc. Nueva Condor Agreement • The terms of the agreement with Nueva Condor include the following; • 2,900,000 Prism common shares to CLM and 2 other individuals. • 3% NSR of which 2% may be purchased in 1% tranches at any stage for payments of US$1.5 and US$2 million

respectively within a period of two years from the approval date. • Annual payments of US$100,000 commencing on the second anniversary of the agreement which payments will

be deductible from any NSR payments made to Nueva Condor. • Prism has retained the services of key Nueva Condor personnel for a monthly retainer fee of US$5,000 which fee

will be capped at US$240,000 over a period of 4 years

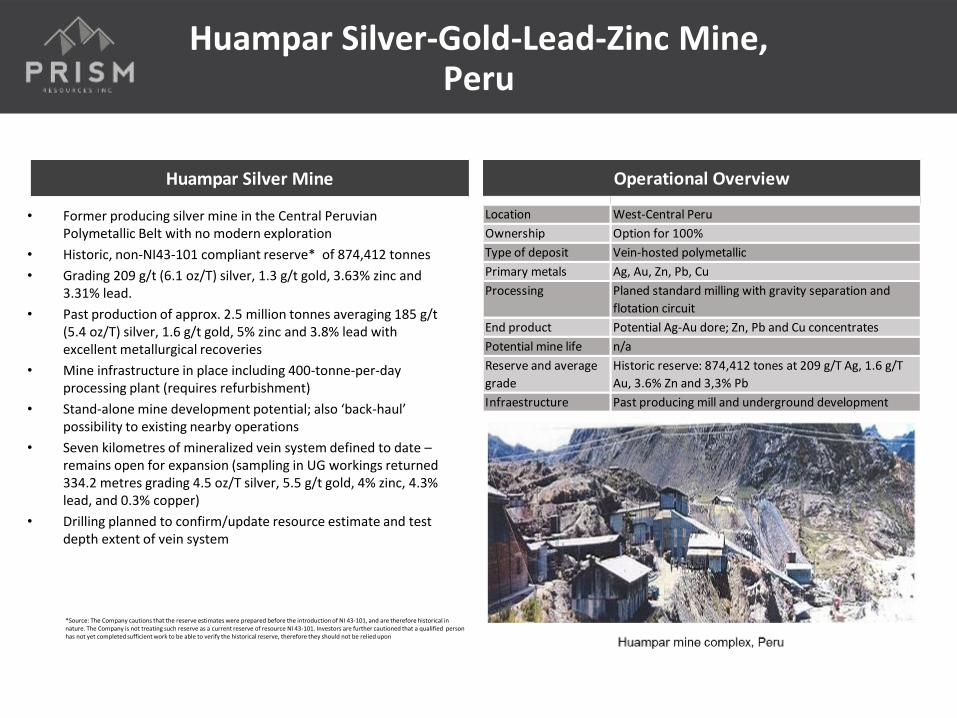

Location West-Central Peru

Ownership Option for 100%

Type of deposit Vein-hosted polymetallic

Primary metals Ag, Au, Zn, Pb, Cu

Processing Planed standard milling with gravity separation and

flotation circuit

End product Potential Ag-Au dore; Zn, Pb and Cu concentrates

Potential mine life n/a

Reserve and average

grade

Historic reserve: 874,412 tones at 209 g/T Ag, 1.6 g/T

Au, 3.6% Zn and 3,3% Pb

Infraestructure Past producing mill and underground development

Operational Overview

Huampar Silver-Gold-Lead-Zinc Mine, Peru

• Former producing silver mine in the Central Peruvian Polymetallic Belt with no modern exploration

• Historic, non-NI43-101 compliant reserve* of 874,412 tonnes

• Grading 209 g/t (6.1 oz/T) silver, 1.3 g/t gold, 3.63% zinc and 3.31% lead.

• Past production of approx. 2.5 million tonnes averaging 185 g/t (5.4 oz/T) silver, 1.6 g/t gold, 5% zinc and 3.8% lead with excellent metallurgical recoveries

• Mine infrastructure in place including 400-tonne-per-day processing plant (requires refurbishment)

• Stand-alone mine development potential; also ‘back-haul’ possibility to existing nearby operations

• Seven kilometres of mineralized vein system defined to date – remains open for expansion (sampling in UG workings returned 334.2 metres grading 4.5 oz/T silver, 5.5 g/t gold, 4% zinc, 4.3% lead, and 0.3% copper)

• Drilling planned to confirm/update resource estimate and test depth extent of vein system

*Source: The Company cautions that the reserve estimates were prepared before the introduction of NI 43-101, and are therefore historical in nature. The Company is not treating such reserve as a current reserve of resource NI 43-101. Investors are further cautioned that a qualified person has not yet completed sufficient work to be able to verify the historical reserve, therefore they should not be relied upon

Huampar Silver Mine

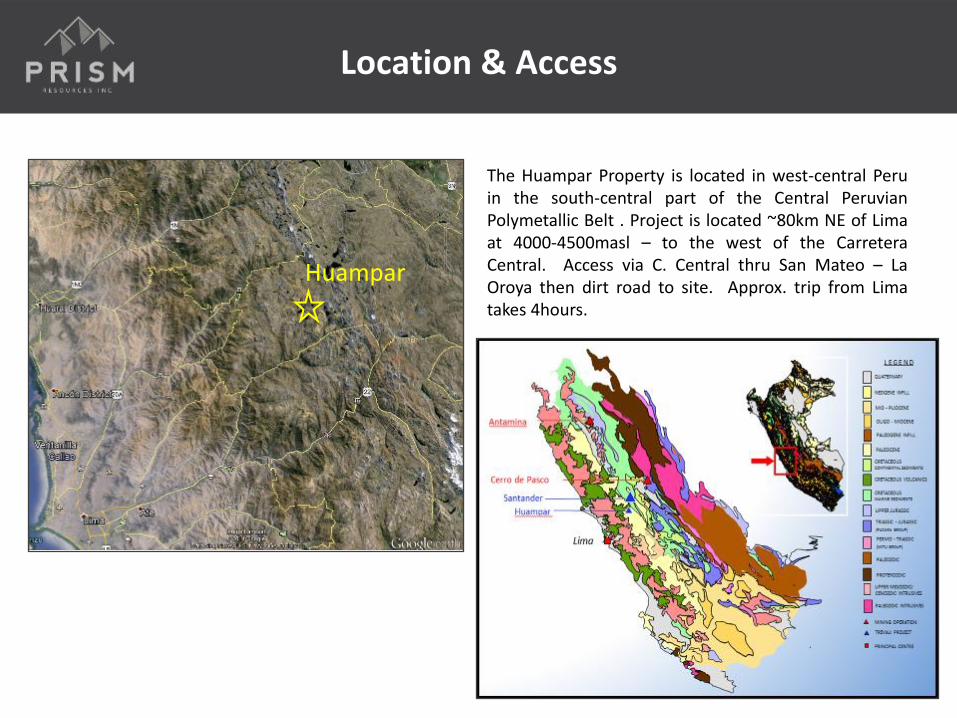

Location & Access

The Huampar Property is located in west-central Peru in the south-central part of the Central Peruvian Polymetallic Belt . Project is located ~80km NE of Lima at 4000-4500masl – to the west of the Carretera Central. Access via C. Central thru San Mateo – La Oroya then dirt road to site. Approx. trip from Lima takes 4hours.

Huampar

Status and Claims

• The overlying owner, Nueva Condor is presently in Chapter 11 proceedings

• Advanced project with near term production potential. Former producing mine from late 1950s to 1991 at ~250tpd. From 1997 – 2000/01 at 350-400tpd.

• The property is comprised of approximately 46 concessions for an approximate total of 2,000ha. All claims are in good standing. Annual associated payments total approx. US$35,000.

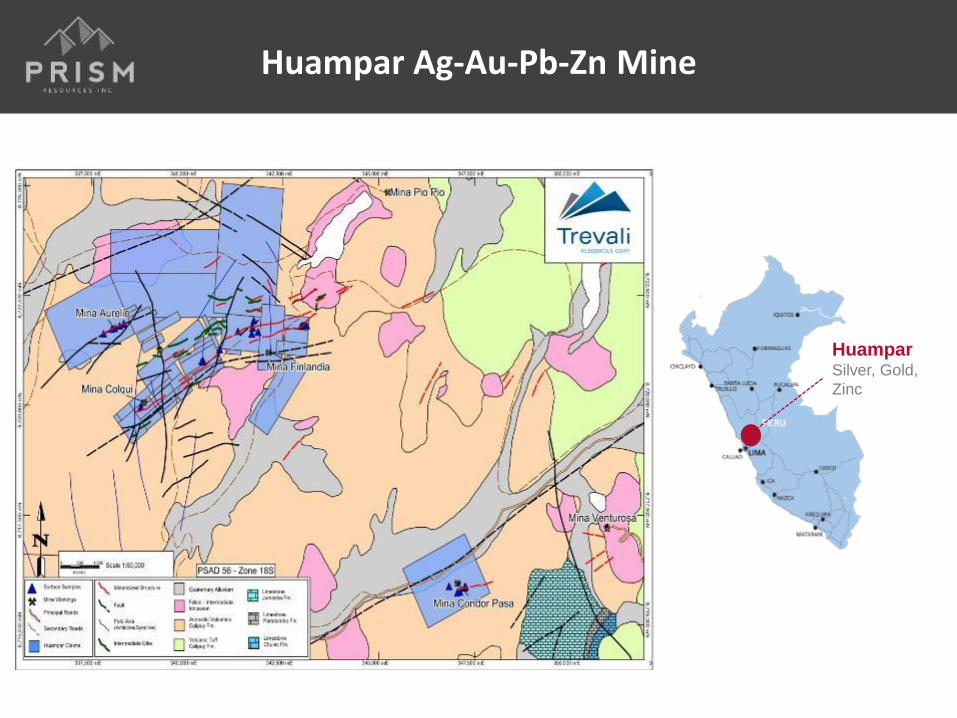

Huampar Ag-Au-Pb-Zn Mine

Huampar Silver, Gold,

Zinc

Company / Year Resource / Reserves

Tecnologia Minera

(Tecmin) SA – 1995

Proven – 214,500t @ 1.57g/t Au, 119 g/t Ag, 2.67% Pb & 3.74% Zn

Probable – 774,300t @ 0.8 g/t Au, 157 g/t Ag, 2.24% Pb, 1.12% Zn & 0.3% Cu

TOTAL – 958,000t @ 1g/t Au, 147g/t Ag, 2.34% Pb, 2.48% Zn & 0.23% Cu

Nueva Condor SA – 1998

Finlandia Mine – 509,000t @ 1.81g/t Au,154g/t Ag, 3.58% Pb & 4.43% Zn

Condora Pasa – 239,000t @ 0.9g/t Au, 215g/t Ag, 2.99% Pb & 2.97% Zn

Other - 183,000t @ 1.5 g/t Au, 255g/t Ag, 2.81% Pb & 1.96% Zn

TOTAL – 930,000t @ 1.18g/t Au, 191g/t Ag, 3.28% Pb & 3.57% Zn

Roscoe Postle Assoc.

(RPA) Canada Inc – 1997

Finlandia Vein M&I – 650,000t @ 0.84g/t Au, 103g/t Ag, 2.16% Pb, 2.96% Zn

& 0.22% Cu

Developed Ore – 214,500t @ 1.73g/t Au, 130g/t Ag, 2.94% Pb & 4.11% Zn

Undeveloped Ore – 744,300t @ 0.9g/t Au, 171g/t Ag, 2.46% Pb & 2.33% Zn

TOTAL – 958,800t @ 1g/t Au, 163g/t Ag, 2.57% Pb & 2.73% Zn

Tailings – c. 1Mt @ 1.2g/t Au, 34g/t Ag & 1.15% Zn (no data provided)

MRDI Canada – 1999

Finlandia Mine – 439,230t @ 1.3g/t Au, 171g/t Ag, 3.83% Pb & 4.73% Zn

Condor Pasa – 247,806t @ 0.9 g/t, 225g/t Ag, 3.06% Pb & 3.05% Zn

Other – 187,376t @ 1.7g/t Au, 274g/t Ag, 3.31% Pb & 3.63% Zn

TOTAL – 874,412t @ 1.3g/t Au, 209g/t Ag, 3.31% Pb & 3.63% Zn

GLOBAL AVERAGE 836,971t @ 1.12g/t Au, 173g/t Ag, 2.99% Pb & 3.35% Zn

Resources / Reserves

• Resource / Reserve estimates based on UG sampling of

drifts, cross-cuts and raises along the mineralized veins – sectional / polygonal methods.

• Reconciliation and check sampling by RPA (n=403) indicates that Tecmin calculations underestimating grades by ~10%. MRDI noted that 1997 to 1998 NSR Block values realized based on then prevailing metal prices, plant recoveries, and concentrate sales terms ranged from 14 to 168% higher than values based on the reserve grades

• Mineralization remains open at depth – no drilling, no modern exploration. Further exploration can easily define additional +1Mt at above grades.

Historic only, however most recent estimates were by reputable consulting companies and 3rd parties.

Geology and Exploration History

• The Huampar property is located in the south-central portion of the Central Peruvian Polymetallic Belt and is underlain by a moderately folded, 200-metre-to-1-kilometre thick package of lower Oligocene-to-Middle Miocene, subaerial, andesitic volcanic rocks of the Calipuy formation. Underlying the volcanics is an approximately 1-km thick package of strongly folded and faulted carbonates and clastic sediments. Included in this package are the Jumasha, Chulec and Santa Formation limestones, proven host sequences throughout Peru, including Trevali’s Santander Zn-Pb-Ag mine as well as many mines within the greater Huampar district (Felicidad and Poderosa mines). On regional scale the area contains numerous styles of mineralization, including high-grade polymetallic Ag-Au vein systems (Huampar, Constancia-Coricancha, Casapalca, Morococha), polymetallic carbonate replacement and skarn deposits (Poderosa, Felicidad, Casapalca, Morococha) and copper porphyries (Toromocho).

• Landsat indicates that the property is transected by a large scale ENE trending fracture zone. All mineralization discovered to date is hosted in ENE trending structures of very significant strike length (+1km) and presumably with considerable depth potential.

• Previous exploration was limited to drifting on exposed veins and underground cross-cuts designed to test for (successfully) and intersect sub-parallel structures. No exploration in the modern sense, no geophysics, no drilling etc.

Mineralization

• Polymetallic mineralization is hosted in laterally and vertically extensive vein systems.

The principal Finlandia system is comprised of at least 5 ‘major’ veins of variable widths ranging from 0.2 to 2m and averaging approximately 0.8 to 1m thick for an aggregate distance of 5km strike. The Condor Pasa system, located some 6km S of Finlandia is traceable for 2km strike. Veins are sub-vertical to steeply dipping 70-85° to south. All veins remain open along strike and at depth.

• Similar polymetallic mines in the district contain economic mineralization over vertical intervals of 500 to 1000m.

• Typical intermediate to low-sulphidation style veins showing multiple stages of mineralization with variable sulphide mineral assemblages and gangue textures (coliform to coarse euhedral quartz). Principle minerals include coarse crystalline galena and sphalerite ± chalcopyrite and tetrahedrite. Gangue minerals are dominantly quartz ± pyrite, siderite with lesser amounts of barite, muscovite and cinnabar. Gold occurs as fine disseminations of free gold within both sulphides and quartz. Examination of assay data indicates that grades range are 0.5 to 3-5g/t Au, 15 – 410g/t Ag, 0.5 - +10% Pb-Zn and traces to 1% Cu.

• It is considered likely that thicker – higher grade intervals represent ore-shoots, however there is presently insufficient data to ascertain as to whether they are predictable or not.

Vein Assays

Suecia Vein Level 450 – 747NE 2.15m @ 0.84 g/t Au, 244g/t Ag, 9% Pb & 9.85% Zn

Finlandia Vein Level 416 – 602NE 0.16m @ 1.54g/t Au, 541g/t Ag, 9.18% Pb & 7.72% Zn

Mining

Conventional cut-and-fill (well suited to narrow vein mining due to flexibility to follow changes in strike and dip of vein) was successfully used from late 1950s to 1999/2000. It is estimated that approximately 2.5-3Mt of ore was mined during this period. From 1983 to 1991 c. 750,000t was mined (see table below). Finally monthly production for September 1999 totaled 63,000t at 1.76g/t Au, 100g/t Ag, 2.68% Pb & 3.79% Zn.

Finlandia Mine is accessed on several levels and is essentially worked out above the main haulage on 412 Level. Below 412 Level a lower level was developed via a c.70-80m deep shaft but is currently flooded. Historically dilution varied averaged approximately 20% and varied from 35-40% to 15%. The subjacent Condor Pasa Mine has enjoyed less extensive exploitation and was mined via shrinkage-stoping (lower opex but requires good to excellent ground conditions). The Finlandia system could sustain an 800 to 1000tpd operation.

Example of cut and fill mining

Note Gold was not routinely assayed in 1991 – zero value assigned where no data

YEAR Tonnes Au g/t Ag g/t Pb% Zn% Cu%

1983 37,782 2.7 229 2.07 2.33 0.31

1984 112,496 1.02 135 2.59 2.75 0.28

1985 109,696 1.4 163 2.85 2.93 0.4

1986 101,616 2.28 147 2.78 3.11 0.21

1987 97,848 1.89 130 2.62 3.11 0.21

1988 74,410 2.27 153 2.49 2.84 0.16

1989 90,710 2.44 123 1.87 2.24 0.15

1990 79,270 2.66 110 2.19 2.34 Na

1991 44,820 0.17 128 2.19 2.75 Na

TOTAL 748,649 1.87 142 2.44 2.73 0.21

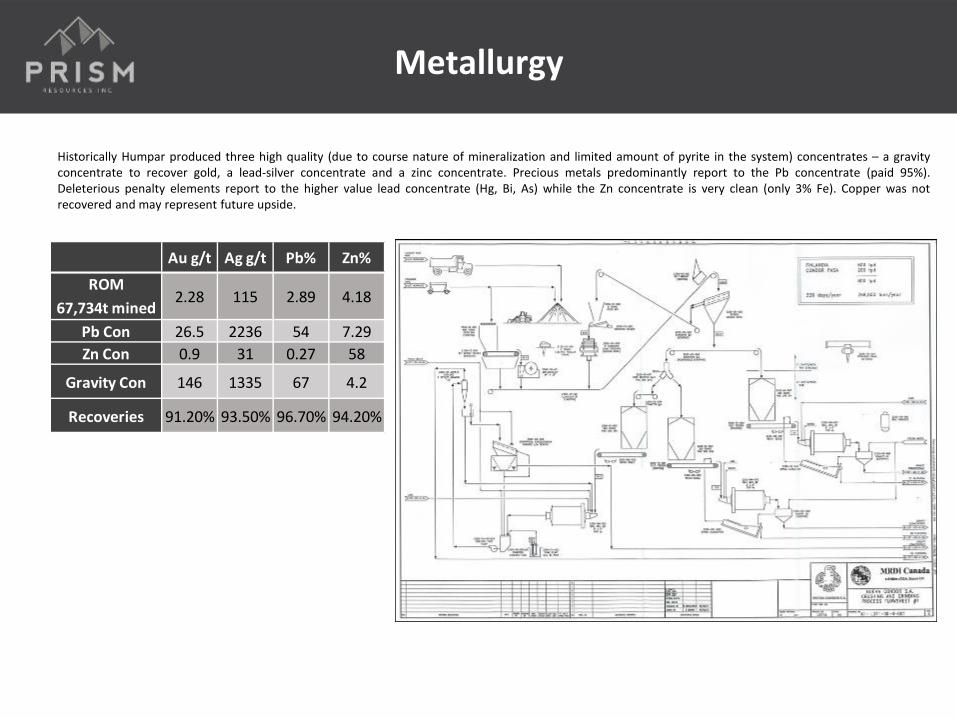

Metallurgy

Historically Humpar produced three high quality (due to course nature of mineralization and limited amount of pyrite in the system) concentrates – a gravity concentrate to recover gold, a lead-silver concentrate and a zinc concentrate. Precious metals predominantly report to the Pb concentrate (paid 95%). Deleterious penalty elements report to the higher value lead concentrate (Hg, Bi, As) while the Zn concentrate is very clean (only 3% Fe). Copper was not recovered and may represent future upside.

Au g/t Ag g/t Pb% Zn%

ROM

67,734t mined

Pb Con 26.5 2236 54 7.29

Zn Con 0.9 31 0.27 58

Gravity Con 146 1335 67 4.2

Recoveries 91.20% 93.50% 96.70% 94.20%

2.28 115 2.89 4.18

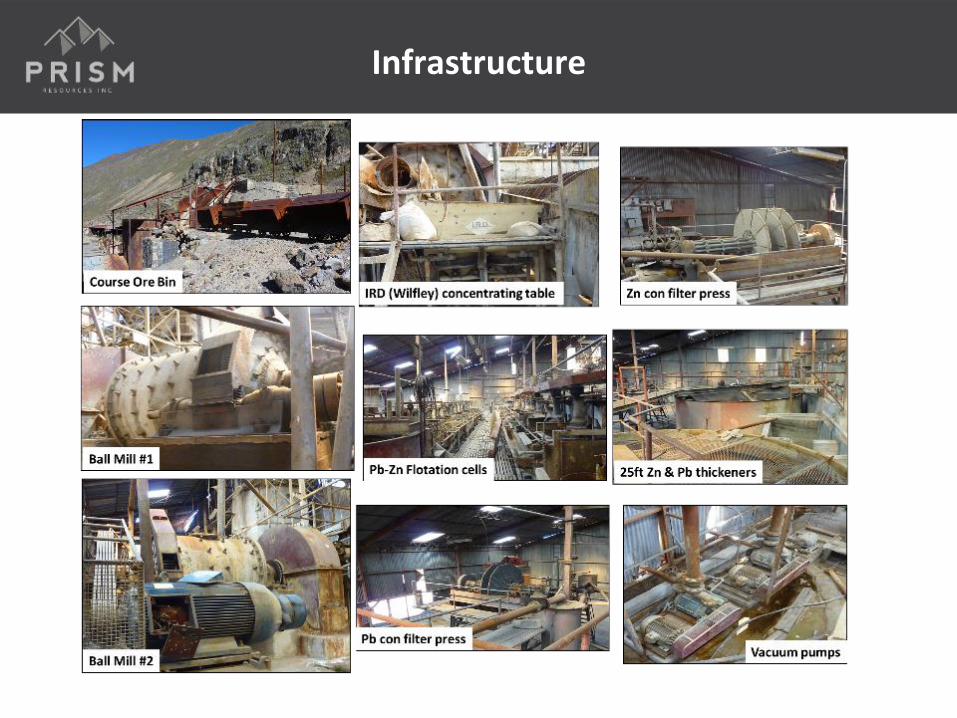

Infrastructure

• Site – large site encompassing several valleys with sufficient room for expansion

• Camp (600-man up to 1991 then 200-man most recently) with offices / shops

• Roads – site and access roads are in poor condition and will require improvements. It is estimated that roads are suitable for 20t concentrate trucks following rehabilitation

• Power – pylons to the main-grid exist however wire is missing – 30km required. GyM just completed construction of hydro-electric plant subjacent to Huampar – this would significantly de-risk the project

• Plant – the current 350-400tpd plant is in workable condition, however major rebuild / over-haul would be required to expand to 800-1000tpd

• Tailings – the current tailings is not to code – a new tailings impoundment is required. Substantial basic engineering study by Kilborn – SVS has located several suitable sites with sufficient capacity to store 17-years production base on 800tpd operation

• Initial CAPEX would be relatively modest on the order of $10-15M to commence operations at 800-1000tpd.

Infrastructure

Exploration Potential

Exploration potential is considered very good – all veins remain open at depth and predominantly along strike. Near-term upside includes depth extensions of all the major veins and structural targeting of thicker, high-grade ore-shoots in particular the Finlandia and Suecia veins as well as the Condor Pasa mine to the South.

Potentially every 100m vertical depth extension assuming a 2km vein strike and average vein width of 0.8m (Finlandia system = 5km) would add approximately ~500,000t of reserves or ~2-years of production for a 800tpd operation. Even if we assume depth potential as 25% of strike length this would suggest over 1,000m additional depth potential on the main Finlandia system.

Exploration Potential

Based on this initial very cursory examination the following first-pass low-risk targets present:

Nuruega Structure: Located immediately adjacent to Finlandia Alta and has seen limited underground exploration from the 2nd level. If geometry is similar to Finlandia and there is no reason presently to suggest that it is not then the upside between the main haulage at 412 level and upper 428 level is approximately +1 to 1.5Mt.

Finlandia – Colqui Mine extension. The former producing Colqui Mine (1972 production of 72,000t at 1.4g/t Au, 530g/t Ag, 5.5% Pb, 3.8% Zn and 0.2% Cu occurs 1200m along strike extension of the Finlandia – Suecia structure.

Colqui Mine – structure terminates to SW in a major fault zone which is currently interpreted to dip c. 50º to the S. Down-thrown extensions?

District-wise (c. 20km radius) to the immediate N, the W, S and E the exploration potential increases significantly– there are numerous Ag-rich prospects that could make attractive small high-grade satellite orebodies. Using a similar analogy to Santander which ever Co. builds and controls the infrastructure controls the District.

A logical exploration program would be rehabilitation of 300m section of principal 412 Level and construction of a new 80m cross-cut from which if required a series of short UG holes can be drilled to confirm vein(s) continuity to very modest depths (100m below current workings).

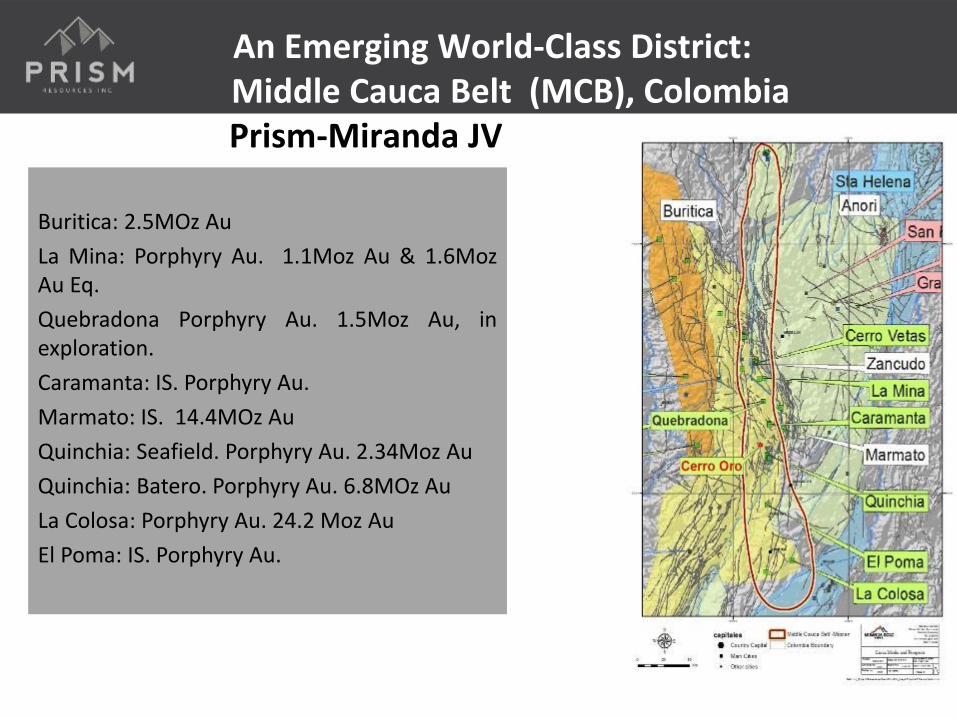

Buritica: 2.5MOz Au

La Mina: Porphyry Au. 1.1Moz Au & 1.6Moz Au Eq.

Quebradona Porphyry Au. 1.5Moz Au, in exploration.

Caramanta: IS. Porphyry Au.

Marmato: IS. 14.4MOz Au

Quinchia: Seafield. Porphyry Au. 2.34Moz Au

Quinchia: Batero. Porphyry Au. 6.8MOz Au

La Colosa: Porphyry Au. 24.2 Moz Au

El Poma: IS. Porphyry Au.

An Emerging World-Class District: Middle Cauca Belt (MCB), Colombia

Prism-Miranda JV

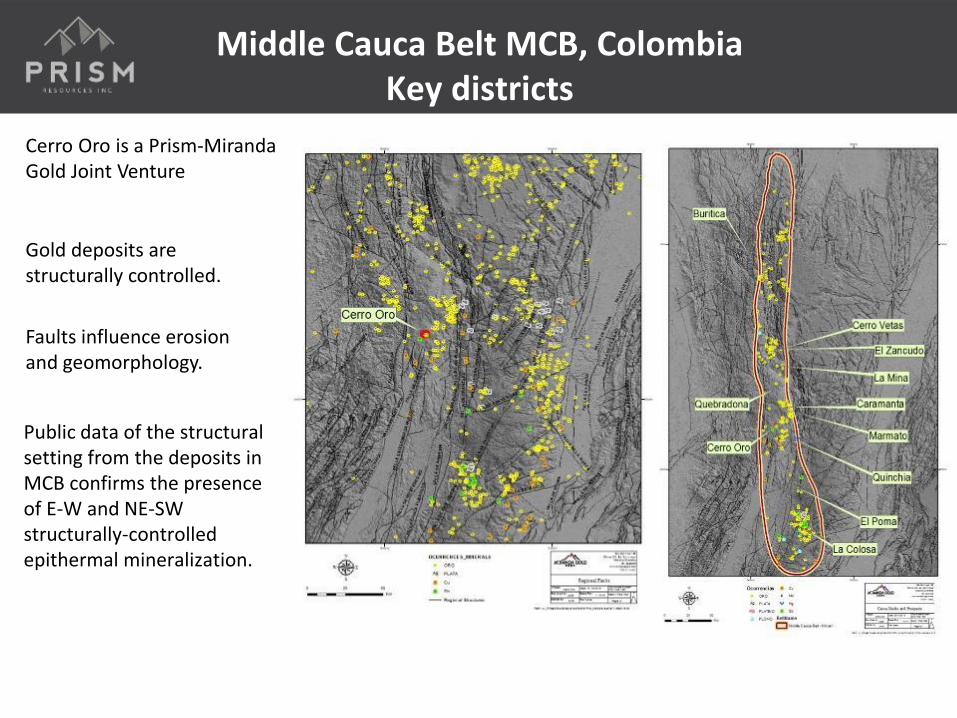

Gold deposits are structurally controlled.

Faults influence erosion and geomorphology.

Public data of the structural setting from the deposits in MCB confirms the presence of E-W and NE-SW structurally-controlled epithermal mineralization.

Middle Cauca Belt MCB, Colombia Key districts

Cerro Oro is a Prism-Miranda Gold Joint Venture

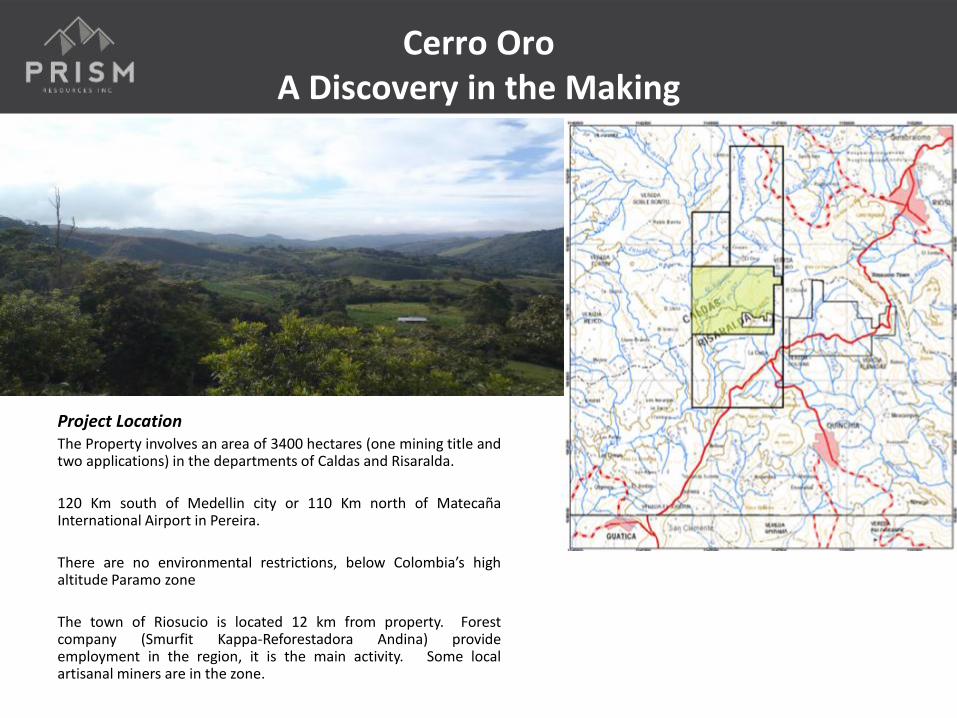

Cerro Oro A Discovery in the Making

Project Location The Property involves an area of 3400 hectares (one mining title and two applications) in the departments of Caldas and Risaralda.

120 Km south of Medellin city or 110 Km north of Matecaña International Airport in Pereira.

There are no environmental restrictions, below Colombia’s high altitude Paramo zone

The town of Riosucio is located 12 km from property. Forest company (Smurfit Kappa-Reforestadora Andina) provide employment in the region, it is the main activity. Some local artisanal miners are in the zone.

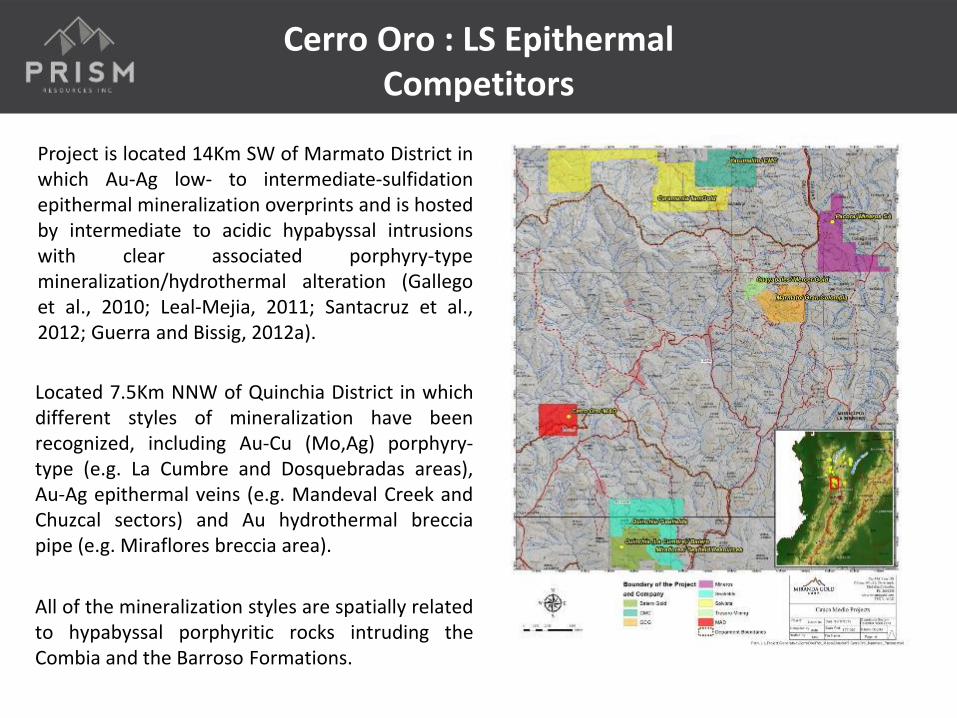

Project is located 14Km SW of Marmato District in which Au-Ag low- to intermediate-sulfidation epithermal mineralization overprints and is hosted by intermediate to acidic hypabyssal intrusions with clear associated porphyry-type mineralization/hydrothermal alteration (Gallego et al., 2010; Leal-Mejia, 2011; Santacruz et al., 2012; Guerra and Bissig, 2012a).

Located 7.5Km NNW of Quinchia District in which different styles of mineralization have been recognized, including Au-Cu (Mo,Ag) porphyry-type (e.g. La Cumbre and Dosquebradas areas), Au-Ag epithermal veins (e.g. Mandeval Creek and Chuzcal sectors) and Au hydrothermal breccia pipe (e.g. Miraflores breccia area).

All of the mineralization styles are spatially related to hypabyssal porphyritic rocks intruding the Combia and the Barroso Formations.

Cerro Oro : LS Epithermal Competitors

Cerro Oro: LS Epithermal Planned Drill Program

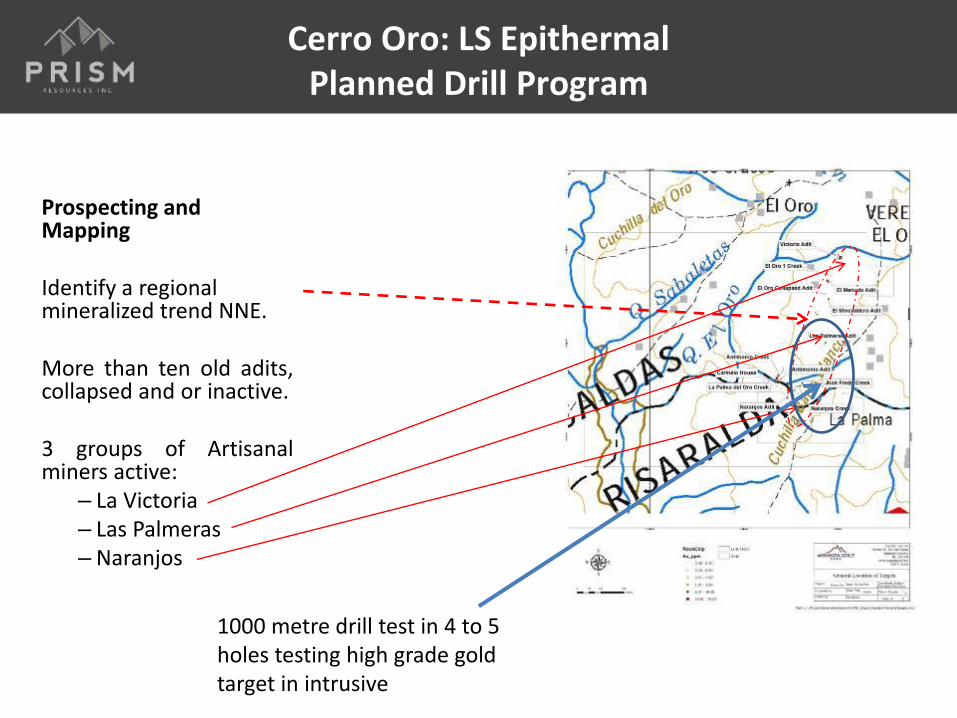

Prospecting and Mapping Identify a regional mineralized trend NNE. More than ten old adits, collapsed and or inactive. 3 groups of Artisanal miners active:

– La Victoria – Las Palmeras – Naranjos

1000 metre drill test in 4 to 5 holes testing high grade gold target in intrusive

Cerro Oro: LS Epithermal

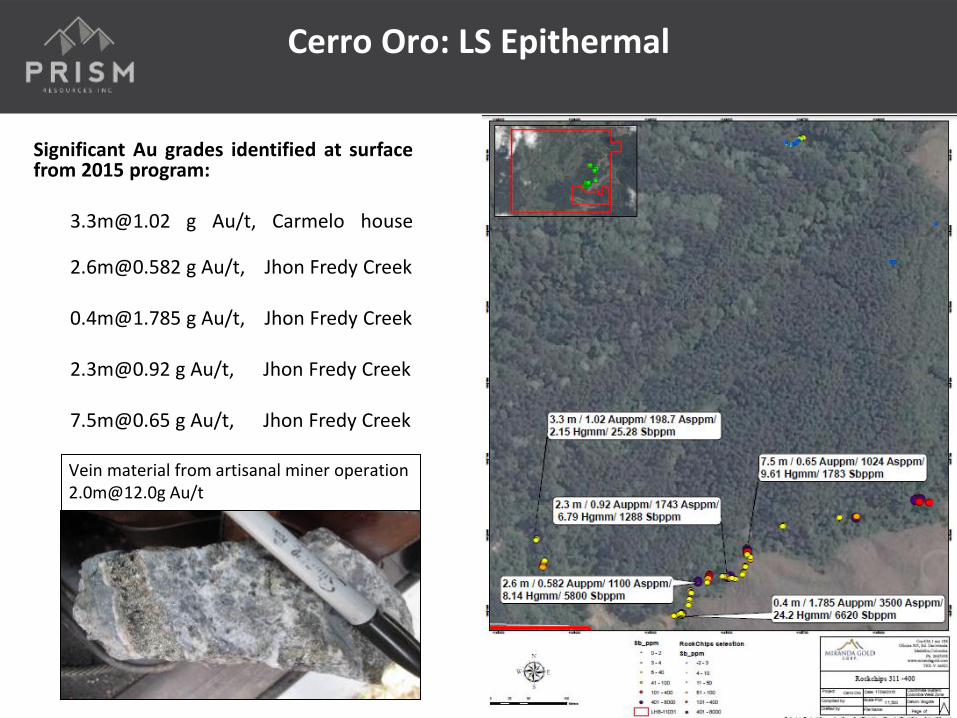

Significant Au grades identified at surface from 2015 program:

[email protected] g Au/t, Carmelo house [email protected] g Au/t, Jhon Fredy Creek [email protected] g Au/t, Jhon Fredy Creek [email protected] g Au/t, Jhon Fredy Creek [email protected] g Au/t, Jhon Fredy Creek

Vein material from artisanal miner operation [email protected] Au/t

Cerro Oro: LS Epithermal Typical outcrop

Geochemical Results for samples:

RIOS-401 to RIOS -443 Widths between 0.9m and

2.3m 65% are 2m width or more 100% are channel samples

Tupia Adit shows strong anomaly in As, Cu and Sb,

local gold values

RIOS-430. Tupia Adit, Basalt:

[email protected]/t-33.8ppmSb

RIOS-438. Tupia Adit, Basalt: [email protected]/t-

142ppmCu

RIOS-436. Tupia Adit, Basalt: [email protected]/t-

4070ppmSb-121.5ppmCu

RIOS-415. Road, Andesite

[email protected]/t RIOS-417. Road, Andesite:

Cerro Oro: LS Epithermal Typical Outcrop

Geochemical Results for samples:

RIOS-444 to RIOS -457. TRENCH No. 1

Sample widths 2.0m to 2.3m. 100% are channel samples

Trench 1 was 28m in length, 1.2m depth, 0.8m wide.

Results show anomalies in Au, Cd and Zn. Pb is consistent but low

Local values of up to [email protected]/t

RIOS-447. Trench No. 1, Andesite: [email protected]/t -

555ppmZn

RIOS-456. Trench No. 1, Andesite: [email protected]/t -

178ppmZn

RIOS-448. Trench No. 1, Andesite: [email protected]/t -

709ppmZn

RIOS-449. Trench No. 1, Andesite: [email protected]/t -

190ppmZn

RIOS-452. Trench No. 1, Andesite: [email protected]/t -

260ppmZn

Cerro Oro : LS Epithermal Exploration Plan

Planned exploration is straightforward, efficient and drill targets can be advanced quickly

Diamond drilling program started on August 21st, 2016 testing the high grade gold target and lower grade gold mineralisation in the upper volcanics.

A budget of $250K has been allocated for the test program

Overview and Investment JV Terms

• Earning up to 70% of a potential high grade vein and bulk disseminated gold project in

the Marmato district located 120km south of Medellin. 3400 hectares of exploration

licenses and applications.

• Miranda Gold as JV partners are operationally and technically competent.

• Prism is obligated to fund $4 million over 4 years to earn a 51% interest in the Cerro Oro project.

• Prism can earn an additional 19% in the project by completing a Feasibility Study for a total of 70%.

• To maintain the lease additional payments of US$525K are to be made over a 5 year period of which US$270 remains to be paid in 2017 and 2018 with annual payments of US$135K thereafter.

• The project is also subject to a 1.2% production royalty and a per ounce gold bonus for measured and indicated NI43-101 compliant resource.

• The Company completed a private placement raising a total of

CDN $1.585 million in July 2016

• Placing 15.854 million shares @ 10c per share with a half warrant at

13c

• Cerro Oro drilling $250K to test the high grade target and lower grade

upper volcanics in three to four holes.

• Huampar additonal property acquisition and data recompilation ahead

of further evaluation underground and/or by drilling. Minimum $400K

• Other property acquisition and project evaluation $350K.

Private Placement – Use of Proceeds

Lower Detour 7.5% NPI

Prism has a 7.5% NPI on the Lower Detour area where Detour Gold is currently exploring a high grade gold resource amenable to open cut and underground mining

Detour Gold has been actively exploring the Lower Detour Area which is located approximately 6 kilometres from its flagship Detour Lake gold mine. A system hosting two important gold mineralized zones was identified, Zone 58N and 75. Since 2013 a total of 112,879 metres was completed in 297 diamond drill holes (DGC news releases). The main target is Zone 58N which totalled 210 holes. The gold mineralized system (Zone 58N and 75) has been intersected over an east-west strike length of 450 metres, from surface to a depth of 800 metres. The mineralized system remains open at depth.

Zone 58 N – 2016 Significant Intercepts (uncut gold assay reported) 35.19 g/t over 5.2 m (DLD-16-190) 26.38 g/t over 13.0 m, including 79.40 g/t over 4.0 m (DLD-16-205) 26.97 g/t over 8.0 m (DLD-16-233A) 10.23 g/t over 22.0 m, including 18.91 g/t over 6.0 m (DLD-16-245) 14.75 g/t over 22.0 m, including 34.21 g/t over 9.0 m (DLD-16-248) 30.79 g/t over 10.0 m, including 75.60 g/t over 4.0 m (DLD-16-250) 15.46 g/t over 13.0 m (DLD-16-270) 18.93 g/t over 13.0 m, including 57.58 g/t over 4.0 m (DLD-16-273) 34.98 g/t over 23.2 m, including 95.58 g/t over 8.0 m (DLD-16-277) 21.95 g/t over 9.0 m (DLD-16-278A)

The surface and underground infrastructure scoping work has started for the development of an underground exploration program. The design, timeline and cost estimate are expected to be completed in the fourth quarter. Metallurgical testing at this time indicates that the mineralized material from Zone 58N is compatible with the current Detour Lake Plant flowsheet. (DGC, News Release July 28, 2016)

Contact Details

Principal Office

214-3540 W 41st Avenue

Vancouver, British Columbia

V6N 3E6

Scott Ross

Telephone: 1-604-803-4883

Facsimile: 1-604-682-0318

Lima Office

Bob Baxter

Telephone +51-1-243-1547

Lima Mobile +51-1-9935-26473

Canada Mobile +1-778-928-1864