Embed Size (px)

DESCRIPTION

An Early Agent-Based Stock Market: Replication & Participation. L á szl ó Guly á s ( [email protected] ) Computer and Automation Research Institute Hungarian Academy of Sciences Ba lá zs Adamcsek AITIA, Inc. Budapest, Hungary - PowerPoint PPT Presentation

Citation preview

May 29, 2003. NEU2003, Venice, Italy 1

An Early Agent-Based Stock Market:

Replication & Participation

László Gulyás ([email protected])Computer and Automation Research Institute Hungarian Academy of Sciences

Balázs AdamcsekAITIA, Inc. Budapest, Hungary

Árpád KissAITIA, Inc. Budapest, HungaryLoránd Eötvös University, Budapest

May 29, 2003. NEU2003, Venice, Italy 2

Overview Motivation for…

Agent-Based Modeling Experimental Economics Participatory Simulation

The Early Santa Fe Artificial Stock Market Results:

Replication Participatory Experiments

May 29, 2003. NEU2003, Venice, Italy 3

Agent-Based Modeling (ABM) A form of computational modeling. Aiming at creating complex (social)

behavior “from the bottom up”. Complex interactions of A high number of (Complex) individuals.

A generative and mostly theoretical approach: Computational “thought experiments”, Existence proofs, etc.

May 29, 2003. NEU2003, Venice, Italy 4

Experimental Economics Controlled laboratory experiments with

human subjects. The effect of human cognition on economic

behavior. Learning and adaptation. Social traps, etc.

Typical tools: Observation (Videotaping) Questionnaires, etc.

An experimental approach.

May 29, 2003. NEU2003, Venice, Italy 5

Participatory Simulation (PS) A computer simulation, in which human

subjects also take part. Agent-based simulations are well suited:

Individuals are explicitly modeled, with Strict Agent-Environment and Agent-Agent

boundaries. Bridges the theoretical and experimental

approaches. Can help both of them: Testing assumptions and results of an ABM. Generating specific scenarios (e.g., crowd

behavior) for laboratory experiments.

May 29, 2003. NEU2003, Venice, Italy 6

Summary of the project Replication of a famous ABM in finance.

Replication of results is a most important step in science!

Conversion to a PS. Partly as a demonstration of our General-Purpose

Participatory Architecture for RePast (GPPAR).

Initial Experiments, testing: Original results’ sensitivity to human trading strategies. Human versus computational economic performance. The effect of human learning between runs.

May 29, 2003. NEU2003, Venice, Italy 7

The Santa Fe Artificial Stock Market 1/2 A prominent model of agent-based finance

(Arthur, Holland, LeBaron, Palmer and Tayler, 1994.) A minimalist model of two assets:

“Money”: fixed, risk-free, infinite supply, fixed interest. “Stock”: unknown, risky behavior, finite supply, varying

dividend.

Artificial traders Developing trading strategies. In an attempt to maximize their wealth.

May 29, 2003. NEU2003, Venice, Italy 8

The Santa Fe Artificial Stock Market 2/2 Two distinct behavioral regimes:

One:• Consistent with Rational Expectations Equilibrium.• Price follows fundamental value of stock.• Trading volume is low.

The other:• “Chaotic” market behavior.• “Crashes” and “bubbles”: price oscillates around

fundamental value.• Trading volume shows wild oscillations.• Appears to be “in accordance” with actual market

behavior.

May 29, 2003. NEU2003, Venice, Italy 9

The Early SFI-ASM 1/4 The most known version of the SFI-

ASM was published in 1997, after several years of work.

However, a first, simpler design was published in 1994. It has Less realistic market mechanisms. Simpler trading strategies for agents.

We were working with the early version.

May 29, 2003. NEU2003, Venice, Italy 10

The Early SFI-ASM 2/4 Dividend:

A stochastic (Ohrnstein-Uhlenbeck) process. Possible Actions:

Selling/Buying one share, Or holding.

Market Clearing: A rationing scheme (agents may only get a

fraction of their bids). May yield fractional shares.

May 29, 2003. NEU2003, Venice, Italy 11

The Early SFI-ASM 3/4 Agents:

60 ‘trading rules’:• Specifying actions (buy, sell, hold) based on market

indicators:• Price > Fundamental Value, or• Price < 100-period Moving Average, etc.

• Reinforced if their ‘advice’ would have yielded profit. A Genetic Algorithm

• Activated in Poisson-distributed intervals (individually for each agent).

• Replaces 10-20% of weakest the rules.

May 29, 2003. NEU2003, Venice, Italy 12

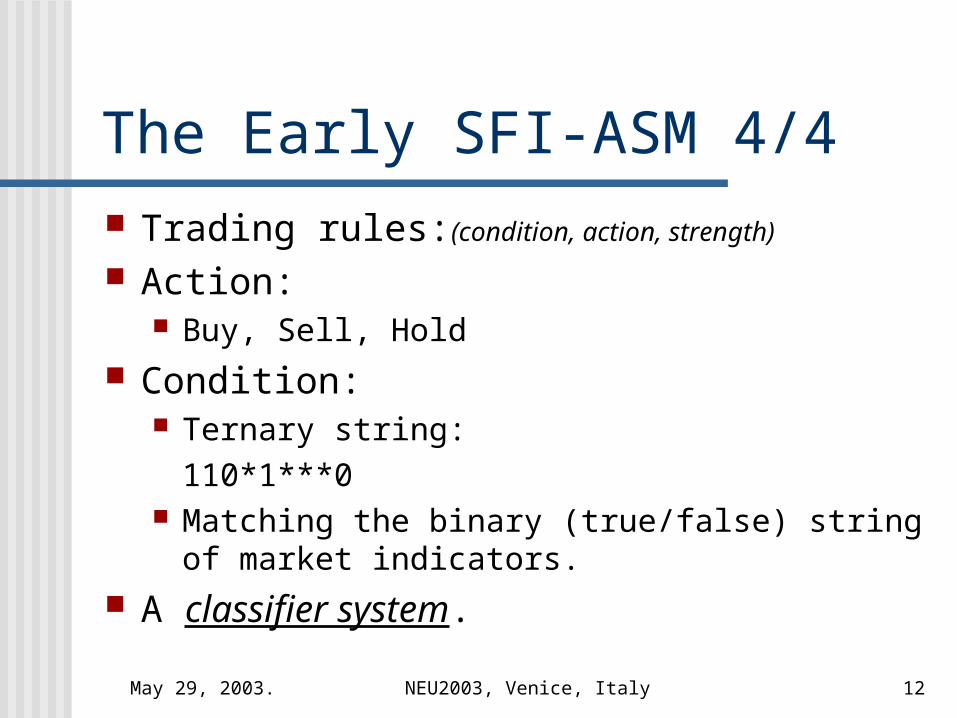

The Early SFI-ASM 4/4 Trading rules:(condition, action, strength)

Action: Buy, Sell, Hold

Condition: Ternary string:

110*1***0 Matching the binary (true/false) string of

market indicators. A classifier system.

May 29, 2003. NEU2003, Venice, Italy 13

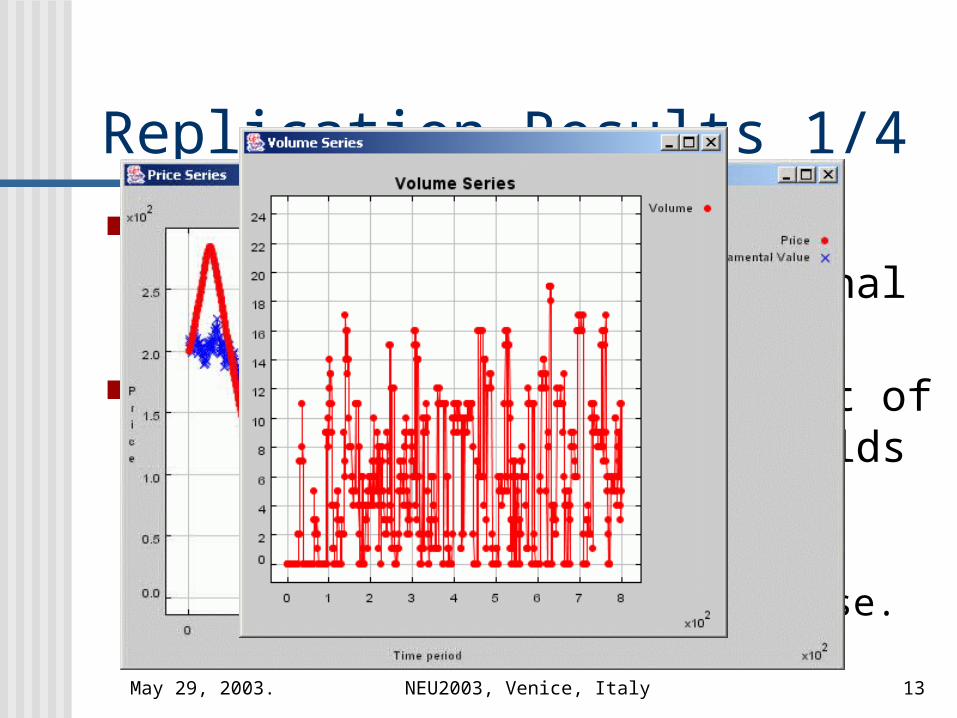

Replication Results 1/4 Our implementation confirms those

reported in the original publication. The interesting case is that of a

complex system, which yields Market volatility and high volume. Agents’ strategies grow diverse.

May 29, 2003. NEU2003, Venice, Italy 14

Replication Results 2/4 High trading volume suggest

diverse agents. A good measure of this is the

wealth distribution of the agents.

May 29, 2003. NEU2003, Venice, Italy 15

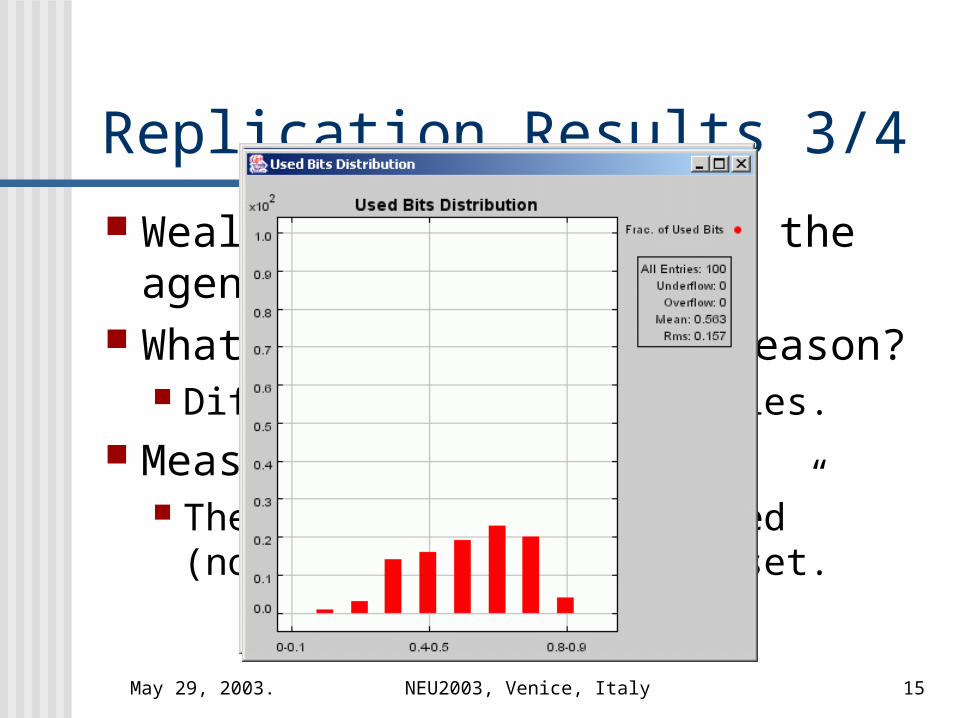

Replication Results 3/4 Wealth is only a sign of the agents’

heterogeneity. What is the underlying reason?

Different trading strategies. Measure:

The average number of “used” (non-*) bits in the rule set.

May 29, 2003. NEU2003, Venice, Italy 16

Replication Results 4/4 Concluding remarks:

The agent community learned to ‘manipulate’ price in such a way that it follows FV.(Subject to a certain range of error.)

Agents “self-organize” (i.e., mutually adapt) to achieve this.

However, heterogeneity suggests that some learned to be smart, while others learned to “sacrifice” their wealth.

May 29, 2003. NEU2003, Venice, Italy 17

Participatory ASM: Questions Can agents adapt to external trading strategies,

just as well as they did to those developed by fellow agents?

Would the apparently complex market behavior appear so to human players? Or would they easily learn to control the market?

Will computational agents outperform humans, particularly in a fast game?

What effect would human learning between sessions play on the outcome?

May 29, 2003. NEU2003, Venice, Italy 18

Participatory ASM:Implementation, Design The illusion of a ‘real market’:

A fast, ‘real-time’ game. Based on the General-Purpose Participatory

Architecture for RePast (GPPAR). Can be used to transform arbitrary

ABMs to participatory simulation. Networked execution. Extensive logging: the possibility of

“replay”.

May 29, 2003. NEU2003, Venice, Italy 19

Participatory ASM:Experimental Settings Inexperienced subjects (CS students

and office workers). Not allowed to communicate. “Open-ended” runs, stopped by the

experimenter without prior notice. 3-4 runs per person. Questionnaire after the session.

May 29, 2003. NEU2003, Venice, Italy 20

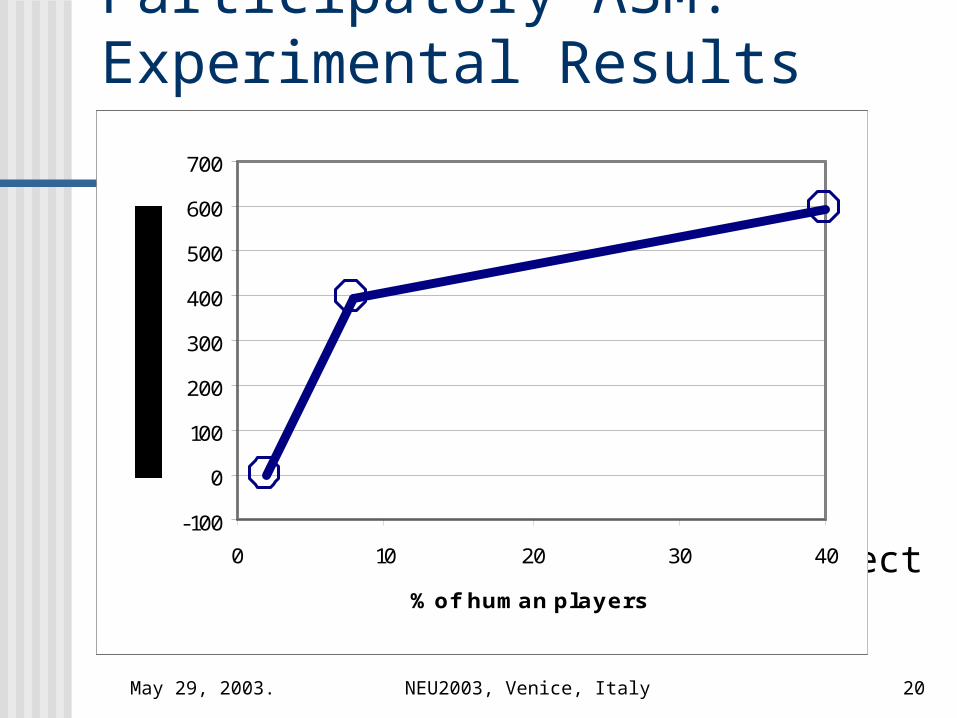

Participatory ASM:Experimental Results 1/4 The presence of human traders increased

market volatility. The higher percentage of the population

was human, the higher the difference was w.r.t. the performance of the fully computational population.

However, this may also be an effect of human learning.

0

0.01

0.02

0.03

0.04

0.05

0.06

0.07

0.08

1 1001

Time period

8%

0%

-100

0

100

200

300

400

500

600

700

0 10 20 30 40

% of human players

May 29, 2003. NEU2003, Venice, Italy 21

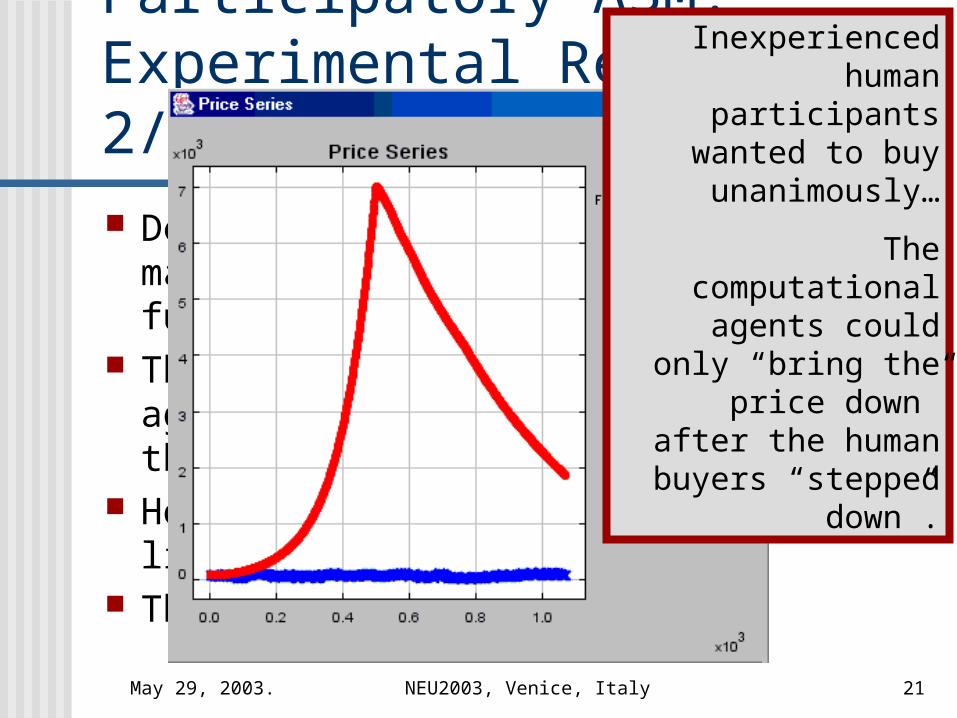

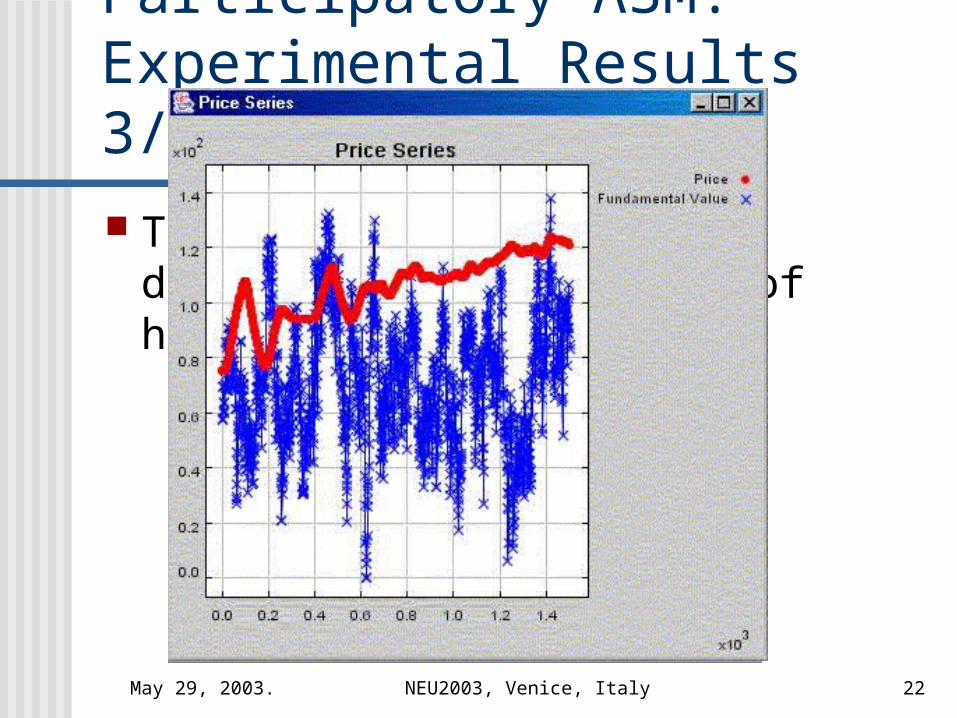

Participatory ASM:Experimental Results 2/4 Despite the increased level of market

deviations, price followed fundamental value.

This suggests that computational agents are able to adapt and ‘keep’ the market in balance.

However, their ability has its limitations… The lesson of the initial runs:

Inexperienced human participants

wanted to buy unanimously…

The computational agents could only

“bring the price down” after the

human buyers “stepped down”.

May 29, 2003. NEU2003, Venice, Italy 22

Participatory ASM:Experimental Results 3/4 This initial mishap also

demonstrates the effect of human learning.

May 29, 2003. NEU2003, Venice, Italy 23

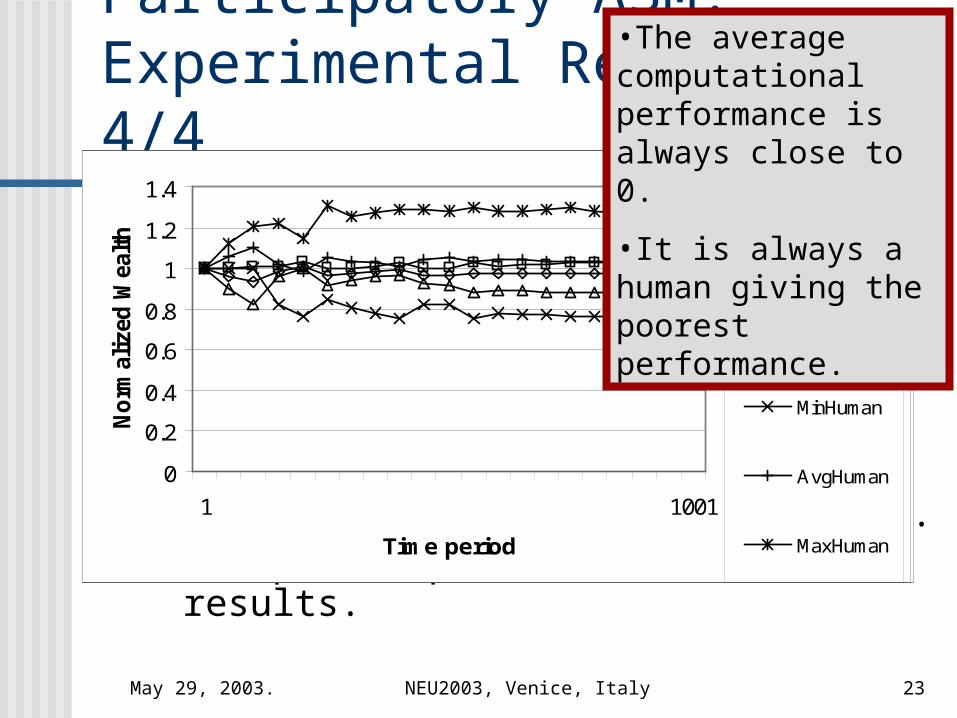

Participatory ASM:Experimental Results 4/4 Human learning is also obvious in

the relative performance of human participants and computational agents.

Notes: The notion of base wealth: the wealth

of an agent that did nothing. The path-dependent nature of the

results.

-1.5-1

-0.50

0.51

1.52

2.53

3.5

1 1001

Time period

No

rmal

ized

Wea

lth

MinComp

AvgComp

MaxComp

MinHuman

AvgHuman

MaxHuman

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1 1001

Time period

No

rmal

ized

Wea

lth

MinComp

AvgComp

MaxComp

MinHuman

AvgHuman

MaxHuman

•The average computational performance is always close to 0.

•It is always a human giving the poorest performance.

May 29, 2003. NEU2003, Venice, Italy 24

Participatory ASM:Trading Strategies

Humans initially applied technical trading strategies, but gradually discovered fundamental strategies. The winning human’s strategy was:

• Buy if price < FV, sell otherwise.

The experiments confirmed that technical trading leads to market deviations.

May 29, 2003. NEU2003, Venice, Italy 25

Conclusions We have introduced Agent-Based

Modeling and Participatory Simulation.

We have argued for the use of PS to test ABMs and to help setting up laboratory experiments.

We have demonstrated the applicability of the concept.

![Veeam Backup & Replication - Integra Group · Veeam Agent za fizičke servere [RTM] Veeam Agent for Microsoft Windows 2.0 • Free, Workstation and Server editions • Veeam Backup](https://img.pdfslide.us/doc/110x75/5ec8f4917e3eb61a633b269f/veeam-backup-replication-integra-group-veeam-agent-za-fizike-servere-rtm.jpg)