Embed Size (px)

Citation preview

1

Compliance with Canada’s Amended

AML and ATF Legislation

Matthew McGuire MNP LLP

2

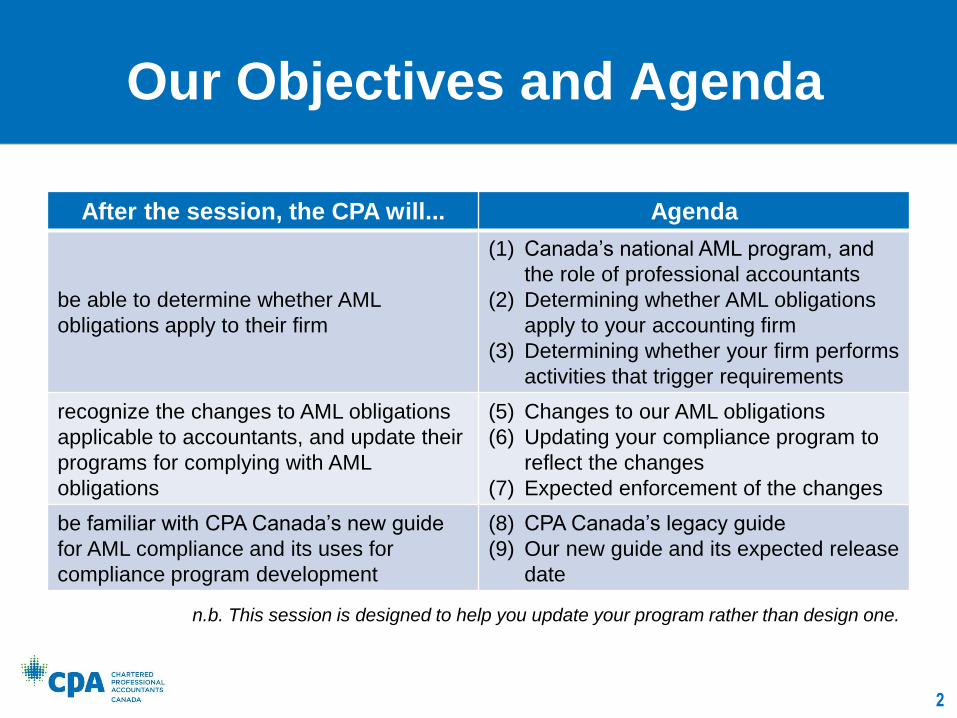

Our Objectives and Agenda

After the session, the CPA will... Agenda

be able to determine whether AML

obligations apply to their firm

(1) Canada’s national AML program, and

the role of professional accountants

(2) Determining whether AML obligations

apply to your accounting firm

(3) Determining whether your firm performs

activities that trigger requirements

recognize the changes to AML obligations

applicable to accountants, and update their

programs for complying with AML

obligations

(5) Changes to our AML obligations

(6) Updating your compliance program to

reflect the changes

(7) Expected enforcement of the changes

be familiar with CPA Canada’s new guide

for AML compliance and its uses for

compliance program development

(8) CPA Canada’s legacy guide

(9) Our new guide and its expected release

date

n.b. This session is designed to help you update your program rather than design one.

3

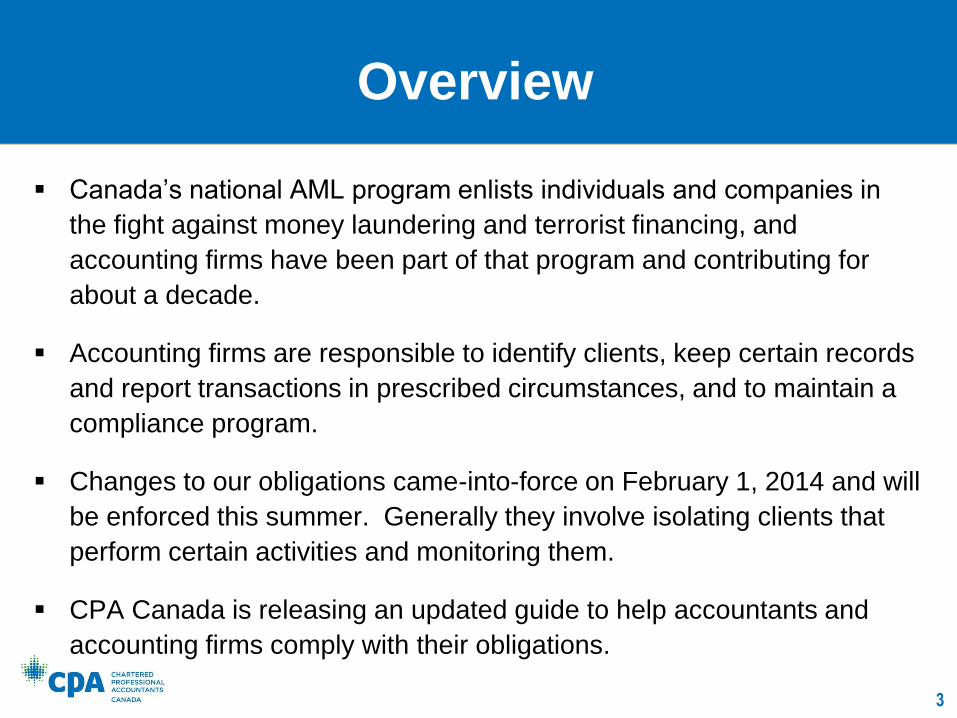

Overview

Canada’s national AML program enlists individuals and companies in

the fight against money laundering and terrorist financing, and

accounting firms have been part of that program and contributing for

about a decade.

Accounting firms are responsible to identify clients, keep certain records

and report transactions in prescribed circumstances, and to maintain a

compliance program.

Changes to our obligations came-into-force on February 1, 2014 and will

be enforced this summer. Generally they involve isolating clients that

perform certain activities and monitoring them.

CPA Canada is releasing an updated guide to help accountants and

accounting firms comply with their obligations.

4

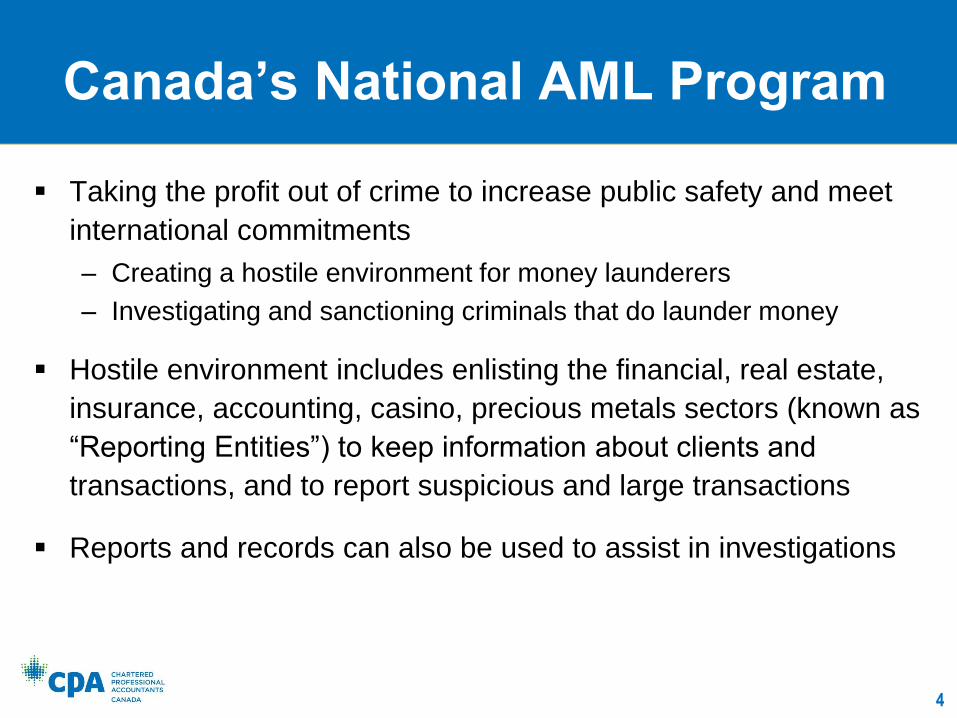

Canada’s National AML Program

Taking the profit out of crime to increase public safety and meet

international commitments

– Creating a hostile environment for money launderers

– Investigating and sanctioning criminals that do launder money

Hostile environment includes enlisting the financial, real estate,

insurance, accounting, casino, precious metals sectors (known as

“Reporting Entities”) to keep information about clients and

transactions, and to report suspicious and large transactions

Reports and records can also be used to assist in investigations

5

Canada’s National AML Program

The Financial Transaction Reports and Analysis Centre

(FINTRAC) is Canada’s Financial Intelligence Unit, and has

two roles

– Collecting, analyzing and disclosing money laundering and terrorist

financing intelligence to law enforcement, tax, and other intelligence

agencies

– Enforcing Reporting Entity compliance with their obligations

6

The Role of Accountants in AML

When AML requirements are applicable, Accountants and

Accounting Firms must:

(A) Perform certain responsibilities in their day-to-day activities

(B) Maintain a program to ensure that they comply with their

responsibilities

7

The Role of Accountants in AML

When AML requirements are applicable, Accountants and

Accounting Firms must:

(A) Perform certain responsibilities in their day-to-day activities

Circumstance

Re

ce

ipt

of

Fu

nd

s

Re

co

rd

Cli

en

t

Ide

nti

fic

ati

on

La

rge

Ca

sh

Tra

ns

ac

tio

n R

ep

ort

Th

ird

Pa

rty

De

term

ina

tio

n

Su

sp

icio

us

Tra

ns

ac

tio

n R

ep

ort

Te

rro

ris

t P

rop

ert

y

Re

po

rt

Receiving funds of $3,000 or more ● ●

Receiving $10,000 or more in cash ● ● ● ●

Suspicious activity or transaction ● ●

Knowledge of terrorist property ●

8

The Role of Accountants in AML

When AML requirements are applicable, Accountants and

Accounting Firms must

(B) Maintain a program to ensure that they comply with their

responsibilities

• A person designated to implement and maintain the program

(Chief Anti-Money Laundering Officer, or CAMLO)

• An assessment of AML risk and risk mitigation plan

• Policies and procedures

• A program to train all employees and agents

• A bi-annual effectiveness review

9

Applicability to Your Firm

There is a two part test, first:

(1) Does your firm qualify as an accounting firm?

(2) Does your firm conduct any triggering activities, that aren’t

otherwise exempted?

10

Applicability to Your Firm

There is a two part test, first:

(1) Does your firm qualify as an accounting firm?

• Does your firm provide accounting services to the public?

– Bankruptcy/Insolvency generally exempted

• At least of the entity’s partners, employees or administrators

is a professionally designated accountant?

11

Applicability to Your Firm

There is a two part test, first:

(2) Does your firm conduct or instruct any triggering activities on

behalf of a client?

• Receiving, paying or transferring funds

• Purchasing or selling real property, business assets, or

entities

• Purchasing, transferring or selling securities

Important considerations: (1) Instructions versus advice, and

assurance engagements

(2) Even one triggering activity obligates

your firm to have a program... It’s

important that you have one in place if

only to isolate triggering activities

12

Changes to Our Obligations

Legislation which came into force on February 1, 2014

obligates Accountants and Accounting Firms to track and

monitor “Business Relationships”

A “Business Relationship” is established for every client for

which two or more triggering activity transactions occur over

a five year period involving: a receipt of funds record; large

cash report, or suspicious transaction report

13

Changes to Our Obligations

Within 30 days of the inception of a “Business Relationship”,

the Accounting Firm must document the “Purpose and

Intended Nature of a Business Relationship”, which may be

described as:

– Transferring funds or securities

– Paying or receiving funds on behalf of a client

– Purchasing or selling assets or entities

That documentation may be maintained in your regular

records (e.g. An engagement letter).

14

Changes to Our Obligations

All Business Relationships must be subject to “Ongoing Monitoring” on a

risk-sensitive basis

Ongoing Monitoring consist of periodically:

– reviewing transactions to assess whether there are any suspicious

transactions, or those that are otherwise inconsistent with our expectations

of the client;

– Keeping client identification information up to date, such as their address,

principal business or occupation, and other information collected when you

identify them (but not necessarily re-identifying the client); and,

– Re-assessing the level of client risk.

All Ongoing Monitoring efforts must be documented

15

How to Update Your Program

Update your mechanism for identifying triggering activities to track all

triggering activity transactions by clients over time, together with a risk

rating/tracking system.

Design and Implement a program to document the client’s purpose and

intended nature of their business relationship on the second triggering

transaction, or by which routine documents will be referenced.

Design and implement a program to initiate and document reviews of

client identification information, transaction and risk, with greater

frequency for higher risk clients.

Change procedures to reflect the above.

Update training to reflect the above for impacted individuals.

16

Expected Enforcement

FINTRAC released guidance related to the new Business Relationship

requirements on January 31, 2014, the day before the related

regulations came-into-force (see below)

FINTRAC has signalled that, because of the delay in producing

guidance, examinations will begin addressing the new requirements

around August 2014

Policy and procedure deficiencies are subject to maximum penalties of

$100,000

Client identification information deficiencies are subject to maximum

penalties of $1,000 per client

English: http://www.fintrac.gc.ca/publications/guide/Guide6/6D-eng.asp

French: http://www.canafe.gc.ca/publications/guide/Guide6/6D-fra.asp

17

CPA Canada’s Legacy AML Guide

http://www.cica.ca/publications/list-of-publications/manual/item13720.pdf

18

CPA Canada’s New AML Guide

Expected publication in June/July 2014

Addresses all existing AML obligations

Contains guidance and sample forms related to:

– Determining the application of AML obligations

– Performing required tasks

– Designing and implementing a compliance program

– Dealing with FINTRAC examinations

– Addressing privacy concerns

19

Questions