Embed Size (px)

Citation preview

AmIslamic Master

30 September 2017

AmIttikalAmBon IslamAmAl-AminAmIslamic BalancedAmIslamic GrowthAmOasis Global Islamic Equity

Annual Reportfor Islamic Funds

AmInvest Islamic Master

TRUST DIRECTORY

Manager

AmFunds Management Berhad 9th & 10th Floor, Bangunan AmBank Group

55, Jalan Raja Chulan 50200 Kuala Lumpur

Board of Directors Raja Teh Maimunah Raja Abdul Aziz

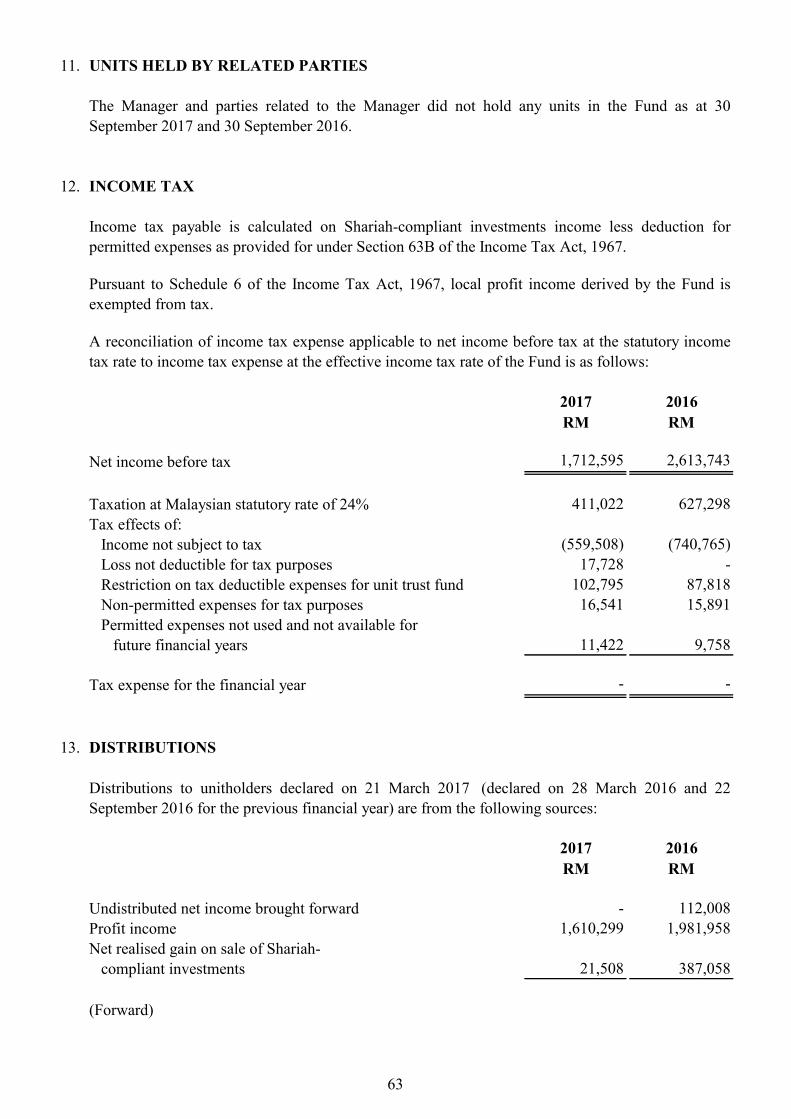

Mustafa Mohd Nor Tai Terk Lin

Goh Wee Peng Sum Leng Kuang

Investment Committee Sum Leng Kuang

Tai Terk Lin Mustafa Mohd Nor

Zainal Abidin Mohd Kassim

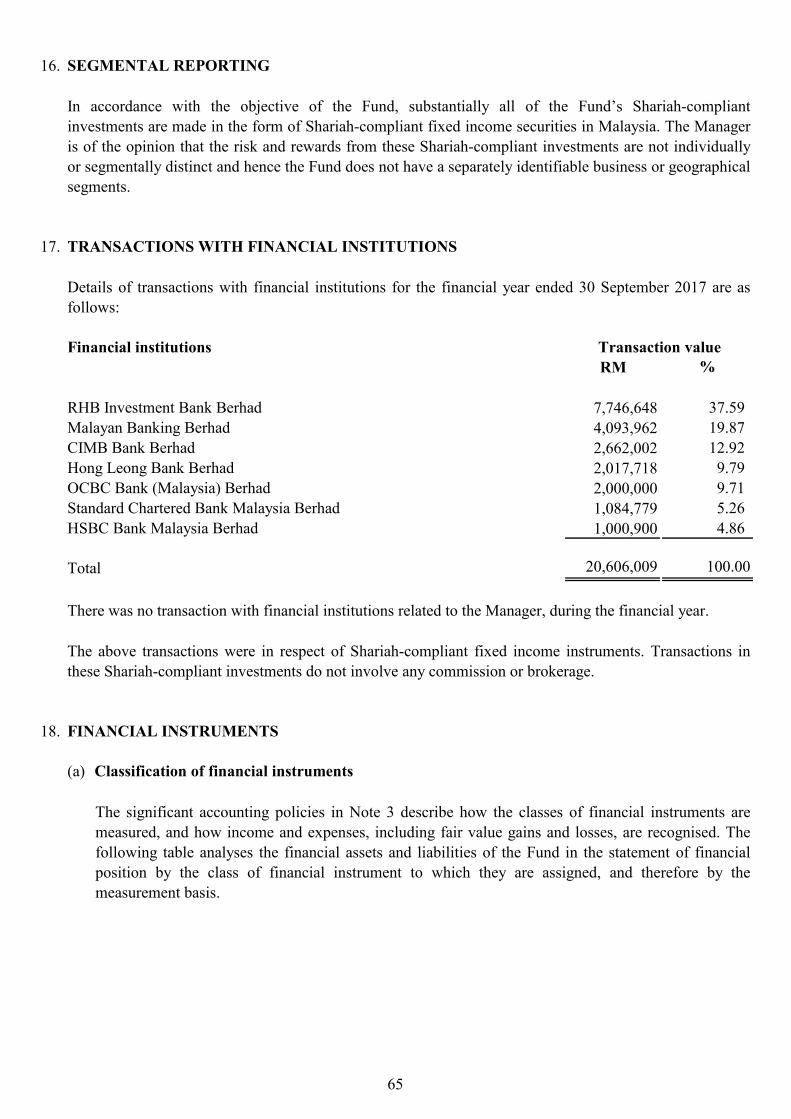

Shariah Adviser Amanie Advisors Sdn Bhd

Investment Manager AmIslamic Funds Management Sdn Bhd

Trustee AmanahRaya Trustees Berhad

Auditors and Reporting Accountants Ernst &Young

Taxation Adviser Deloitte Tax Services Sdn Bhd

AmInvest Islamic Master

CONTENTS AmIttikal AmIslamic Balanced

1 Manager’s Report 114 Manager’s Report

10 Independent Auditor’s Report to the Unitholders

124 Independent Auditor’s Report to the Unitholders

13 Statement of Financial Position 127 Statement of Financial Position 14 Statement of Comprehensive Income 128 Statement of Comprehensive Income 15 Statement of Changes in Equity 129 Statement of Changes in Equity 16 Statement of Cash Flows 130 Statement of Cash Flows 17 Notes to the Financial Statements 131 Notes to the Financial Statements 36 Statement by the Manager 154 Statement by the Manager 37 Trustee’s Report 155 Trustee’s Report

AmBon Islam AmIslamic Growth 38 Manager’s Report 156 Manager’s Report 45 Independent Auditor’s Report to the

Unitholders 165 Independent Auditor’s Report to the

Unitholders 48 Statement of Financial Position 168 Statement of Financial Position 49 Statement of Comprehensive Income 169 Statement of Comprehensive Income 50 Statement of Changes in Equity 170 Statement of Changes in Equity 51 Statement of Cash Flows 171 Statement of Cash Flows 52 Notes to the Financial Statements 172 Notes to the Financial Statements 73 Statement by the Manager 191 Statement by the Manager 74 Trustee’s Report 192 Trustee’s Report

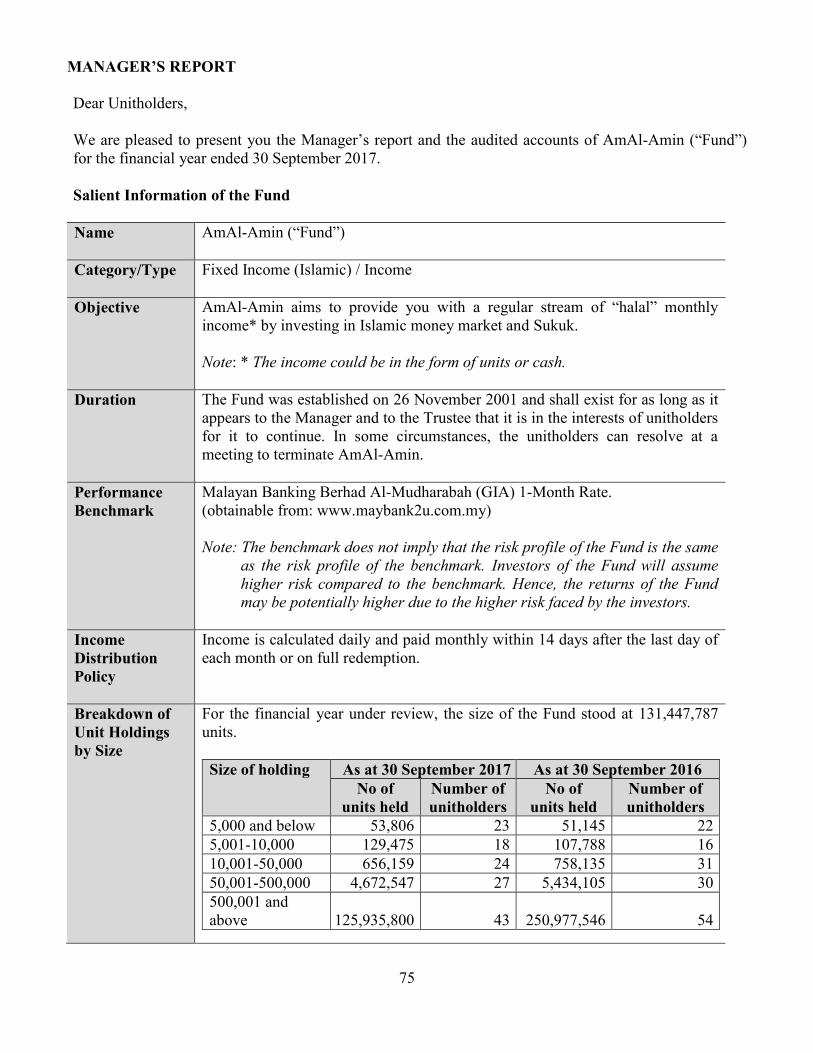

AmAl-Amin AmOasis Global Islamic Equity

75 Manager’s Report 193 Manager’s Report 83 Independent Auditor’s Report to the

Unitholders 201 Independent Auditor’s Report to the

Unitholders 86 Statement of Financial Position 204 Statement of Financial Position 87 Statement of Comprehensive Income 205 Statement of Comprehensive Income 89 Statement of Changes in Equity 207 Statement of Changes in Equity 90 Statement of Cash Flows 208 Statement of Cash Flows 91 Notes to the Financial Statements 209 Notes to the Financial Statements 112 Statement by the Manager 227 Statement by the Manager 113 Trustee’s Report 228 Trustee’s Report 229 Report of the Shariah Adviser to

Unitholders 230 Directory

1

MANAGER’S REPORT Dear Unitholders, We are pleased to present you the Manager’s report and the audited accounts of AmIttikal (“Fund”) for the financial year ended 30 September 2017. Salient Information of the Fund Name AmIttikal (“Fund”)

Category/Type

Equity (Islamic) / Income and to a lesser extent growth.

Objective Amlttikal is designed as a medium to long-term investment with an objective of producing “halal” income* and to a lesser extent capital growth. Note: *The income could be in the form of units or cash.

Duration The Fund was established on 12 January 1993 and shall exist for as long as it appears to the Manager and the Trustee that it is in the interests of the unitholders for it to continue. In some circumstances, the unitholders can resolve at a meeting to terminate AmIttikal.

Performance Benchmark

Malayan Banking Berhad 12-month Islamic General Investment Account plus 3% spread. (obtainable from: www.maybank2u.com.my) Note: The benchmark does not imply that the risk profile of the Fund is the same as the risk profile of the benchmark. Investors of the Fund will assume a higher risk compared to the benchmark. Hence, the returns of the Fund may be potentially higher due to the higher risk faced by the investors.

Income Distribution Policy

Income distribution (if any) is paid at least once every year.

Breakdown of Unit Holdings by Size

For the financial year under review, the size of the Fund stood at 238,025,628 units. Size of holding As at 30 September 2017 As at 30 September 2016

No of units held

Number of unitholders

No of units held

Number of unitholders

5,000 and below 2,783,942 898 5,207,996 1,823 5,001-10,000 5,499,391 742 1,1042,461 1,492 10,001-50,000 31,609,470 1,471 76,447,103 3,389 50,001-500,000 29,822,599 299 100,319,601 955 500,001 and above 168,310,226 11 108,970,396 31

2

Fund Performance Data Portfolio Composition

Details of portfolio composition of the Fund for the financial years as at 30 September are as follows: FY

2017 %

FY 2016 %

FY 2015 %

Construction 12.27 13.06 9.37 Consumer products 1.26 2.26 - Finance 4.26 4.20 3.53 Industrial products 12.54 8.53 18.13 Infrastructure 5.40 7.91 5.98 Plantation 4.19 5.49 7.09 Properties 2.64 6.26 1.28 Technology 2.70 2.16 - Trading/Services 32.70 30.01 43.34 Cash and others 22.04 20.12 11.28 Total 100.00 100.00 100.00

Note: The abovementioned percentages are calculated based on total net asset value.

Performance Details

Performance details of the Fund for the financial years ended 30 September are as follows: FY

2017 FY

2016 FY

2015 Net asset value (RM)* 151,309,309 192,201,158 222,717,078 Units in circulation* 238,025,628 301,987,557 345,696,067 Net asset value per unit (RM)* 0.6357 0.6365 0.6443 Highest net asset value per unit

(RM)* 0.6767

0.6758 0.7234 Lowest net asset value per unit

(RM)* 0.6193

0.6190 0.6008 Benchmark performance (%) 6.42 6.93 6.48 Total return (%)(1) 4.07 5.01 -5.04 - Capital growth (%) -0.12 -1.20 -9.27 - Income distribution (%) 4.19 6.21 4.23 Gross distribution (sen per unit) 2.67 4.00 3.00 Net distribution (sen per unit) 2.67 4.00 3.00 Management expense ratio

(%)(2) 1.65

1.51 2.05 Portfolio turnover ratio

(times)(3) 1.09

1.21 0.69

* Above prices and net asset value per unit are shown as ex-distribution. Note: (1) Total return is the actual return of the Fund for the respective financial

years computed based on the net asset value per unit and net of all fees.

3

(2) Management expense ratio (“MER”) is calculated based on the total fees and expenses incurred by the Fund divided by the average fund size calculated on a daily basis. The MER increased by 0.14% as compared to 1.51% per annum for the financial year ended 30 September 2016 mainly due to decrease in average fund size.

(3) Portfolio turnover ratio (“PTR”) is calculated based on the average of the total acquisitions and total disposals of investment securities of the Fund divided by the average fund size calculated on a daily basis. The PTR decreased by 0.12 times (9.9%) as compared to 1.21 times for the financial year ended 30 September 2016 mainly due to decrease in investing activities.

Average Total Return (as at 30 September 2017)

AmIttikal(a) %

MBB(b) %

One year 4.07 6.42 Three years 1.24 6.60 Five years 5.39 6.44 Ten years 5.22 6.26

Annual Total Return

Financial Years Ended (30 September)

AmIttikal(a) %

MBB(b) %

2017 4.07 6.42 2016 5.01 6.93 2015 -5.04 6.48 2014 10.71 6.22 2013 13.15 6.18

(a) Source: Novagni Analytics and Advisory Sdn Bhd. (b) Malayan Banking Berhad 12-months Islamic General Investment Accounts

plus 3% Spread (“MBB”) (Obtainable from: www.maybank2u.com.my). The Fund performance is calculated based on the net asset value per unit of the Fund. Average total return of the Fund and its benchmark for a period is computed based on the absolute return for that period annualised over one year. Note: Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up.

Fund Performance

For the financial year ending 30 September 2017, the NAV per unit of the Fund decreased by 0.13% from RM0.6365 to RM0.6357, while units in circulation decreased by 21.18% from 301,987,557 units as at 30 September 2016 to 238,025,628 units as at 30 September 2017. The Fund registered a return of 4.07% for the financial year ended 30 September 2017, comprising of negative 0.12% capital and 4.19% income distribution. Comparatively, for the same period, the benchmark, Malayan Banking Berhad twelve (12) months Islamic General Investment Accounts plus 3% spread registered a return of 6.42%. As such the Fund underperformed the benchmark by 2.35%.

4

The line chart below shows comparison between the annual performance of AmIttikal and its benchmark, MBB, for the financial years ended 30 September.

Note: Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up.

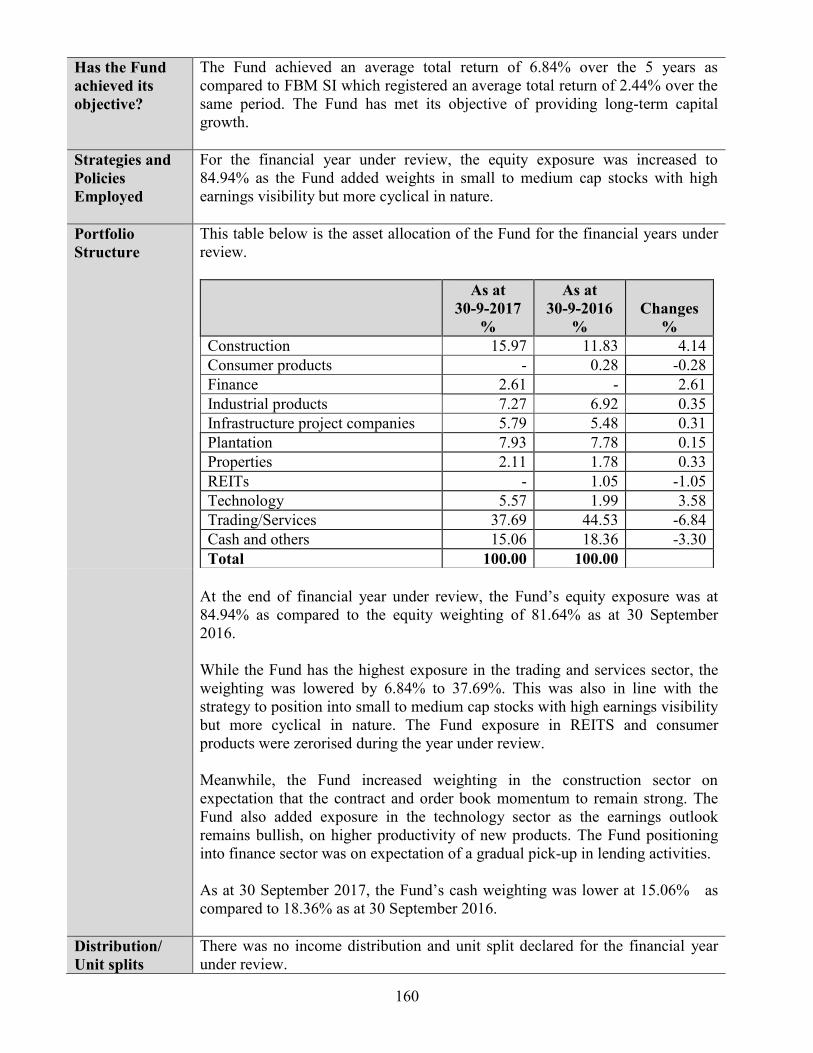

Has the Fund achieved its objective?

The Fund has achieved its objective over the medium to long term investment time frame in producing “halal” income* and to a lesser extent capital growth. For the year under review, the Fund has declared a dividend of 2.67 sen per unit translating to income distribution of 4.19%, meeting the objective of the Fund to meet halal income distribution. However, telecommunication and plantation sectors were a drag to the Fund’s performance, causing it to underperformed the benchmark.

Strategies and Policies Employed

For the financial year under review, the Fund’s strategy was to invest mainly in big cap stocks that were backed with strong balance sheets, cash flow and consistent dividend payments. The Fund also had high exposure in big cap stocks. While the blue chips anchored the portfolio, a smaller exposure to small to medium cap stocks with high earnings visibility but more cyclical in nature helped to contribute to the capital growth of the Fund.

5

Portfolio Structure

This table below is the asset allocation of the Fund for the financial years under review. As at

30-9-2017 %

As at 30-9-2016

%

Changes

% Construction 12.27 13.06 -0.79 Consumer products 1.26 2.26 -1.00 Finance 4.26 4.20 0.06 Industrial products 12.54 8.53 4.01 Infrastructure 5.40 7.91 -2.51 Plantation 4.19 5.49 -1.30 Properties 2.64 6.26 -3.62 Technology 2.70 2.16 0.54 Trading/Services 32.70 30.01 2.69 Cash and others 22.04 20.12 1.92 Total 100.00 100.00

The Fund’s equity exposure for the financial year under review was 77.96% as compared to 79.88% as at 30 September 2016 mainly to realize profits. The big changes were in the Industrial Products, Properties and Trading/Services sectors. The Industrial Products sector saw the most increase in weight of 4% as the Fund was increasingly optimistic on the global economy on the back of positive GDP growth from US and turnaround in China. The Fund took profits from Top Glove and VS Industry but plough the money back into Heveaboard, Petron and Wellcall. Meanwhile, the exposure in the properties sector came down by 3.6% due to profit takings on Eastern Oriental, SP Setia, Sunway and UOA Development. The Trading/Services exposure increased by 2.7% as the fund added Bermaz Auto, Dialog Group, MyEg, Pos and Uzma while zerorising Tiong Nam Logistic.

Distribution/ Unit splits

During the financial year under review, the Fund declared income distributions, detailed as follows: 2.67 sen per unit income distribution

Change in the unit price prior and

subsequent to the income distribution

Before income distribution on

29 September 2017 (RM)

After income distribution on

29 September 2017 (RM)

Net asset value per unit 0.6624 0.6357 There was no unit split declared for the financial year under review.

State of Affairs

There has been neither significant changes to the state of affairs of the Fund nor any circumstances that materially affect any interests of the unitholders during the financial year under review.

Rebates and Soft Commission

It is our policy to pay all rebates to the Fund. Soft commission received from brokers/dealers are retained by the Manager only if the goods and services provided are of demonstrable benefit to unitholders of the Fund. During the financial year under review, the Manager had received on behalf of the Fund, soft commissions in the form of fundamental database, financial wire

6

services, technical analysis software and stock quotation system incidental to investment management of the Fund. These soft commissions received by the Manager are deem to be beneficial to the unitholders of the Fund.

Market Review

The market started the period under review on a positive note. The Government announced its Budget 2017 with Gross Domestic Product (“GDP”) growth is forecasted to be within 4%-5%. 2017 Budget includes plans to set up small to mid-cap research Public Listed Companies (“PLC”) and allocation of a special fund of up to RM3bn to fund managers to invest in small to mid-cap PLC. The ringgit ended higher against the US dollar following the tabling of Budget 2017 which lifted foreign investors' confidence, thus creating a better demand for the local currency. In November 2016, market underwent heavy selling pressure due to surge in US Treasury yields and the measure of its full impact to emerging markets currencies. This was on the back of the outcomes of the recent US presidential election. The Ringgit weakened 6% and 10Y MGS yield spiked up to 4.35% on fears of Fed rate hike. The external negative sentiments outweigh better than expected 3Q2016 GDP numbers of 4.3%. Malaysia's economy grew 4.3 per cent in the third quarter from year-ago levels, accelerating after five straight quarters of decline. The growth was stronger than the median forecast of 4.1 per cent and better than the 4.0 per cent growth posted in the second quarter. Sentiment recovered in December 2016, following Organization of the Petroleum Exporting Countries (“OPEC”) agreeing to reduce production by c1.2 million barrels per day (“mbd”) bringing its output ceiling to 32.5mbd. The duration of the cut is 6 months effective 1 Jan 2017, with a possibility to extend for another 6 months, sending oil prices from the level of USD50/barrel to almost USD54/barrel at the peak in the month of December. BNM introduced six measures to enhance the liquidity and depth of the onshore market effective 5 Dec. But, in the month, we still saw the ringgit weakening against the USD moving from RM4.45/USD to RM4.49/USD as foreigners kept selling out of the Malaysian bond and equity market. It also did not help that the 3Q16 results performance came in weaker than expected. We saw negative revisions to earnings but believe that the pace of downward revisions has slowed. The Federal Reserve increased its key interest rate by 0.25% on 14 Dec 2016 which led to the weakening of all EM currencies including the ringgit. But, as we approached the end of the year, we saw some window dressing activities taking place. Year 2017 started on a positive note, spurred by foreign inflow on the back of an improving ringgit from 4.48RM/USD to 4.43RM/USD, and stabilizing oil prices at USD50-55/bbl. The market was also be boosted by some repositioning and reallocation of funds at the start of the year. Improving sentiment on local banks, and M&A news flow on major GLCs such as Sime Darby and UMW further boosted the buoyant mood on local equities. Apart from that, deferment of punitive regulations (i.e. levy for foreign workers) until 2018 helped to recover investor confidence on less downside risk to future earnings.

7

The month of February 2017 started off with another round of rallies in equities, supported by further net foreign inflows of c. RM1 bil (YTD 2017:RM1.5 bil), with oil prices hovering within the USD52-55/bbl band and ringgit averaging 4.44RM/USD. We saw trading interest on all fronts i.e. big to small cap stocks. The index peaked above 1700 towards the end of February, but ended the month slightly lower at 1694 on profit taking. Post the February result season (for 4Q 2016 results), data shows that 21% of companies recorded results above our expectations - the best quarter so far in the past one year. MSCI Malaysia 2017 earnings were revised lower by -0.1% mom in February. However more significantly, it shows a bottoming of 2017 earnings expectation as this was the lowest negative revision since January 2016. Most upgrades came from Materials, Energy and Consumers sectors, whilst downgrades were from Real Estate, Telco and Utilities. In March 2017, the global and regional equity markets continued their rallies. For the local bourse, trading interest shifted to mid and small-cap stocks and on property and technology stocks. Highlight of the month was the announcement of the Digital Free Trade Zone by the PM during Jack Ma’s visit in KL. Maybank and CIMB also announced partnership with Ant Financial Services Group to enable the Alipay mobile wallet in Malaysia. Furthermore, Malaysian Digital Economy Corp announced that Multimedia Super Corridor companies have recorded new investments of RM16.3 bil in 2016.

The upward momentum continued in April 2017, as sentiment was supported by a stronger ringgit, improving outlook for corporate earnings and strong inflow of foreign funds. The broader market outperformed the KLCI, with the FBM EMAS up 2.2% mom to 12,631pts. However, average daily value traded on Bursa in April fell by 8% mom to RM2.8bn. The finance, technology and energy sectors outperformed the market. The energy sector outperformed, on the back of continued optimism about Saudi Aramco’s potential USD7 bil investment in RAPID. The financial sector outperformed, presumably on reflation trade. Materials were a major underperformer, led by Lafarge and PChem, on a weaker pricing environment. Consumer staples underperformed on lower CPO prices, while defensive utilities continued to underperform. After a strong performance in the first 4 months of 2017, the market paused its uptrend in May 2017. News of the Bandar Malaysia deal cancellation by the Malaysian government caused dampened sentiment on fears of reversal of capital inflows from China; these were subsequently eased when Malaysia signed more MoUs with China at the One Belt One Road Initiative (“OBOR”) conference one week later. Stronger-than-expected GDP growth for 1Q17 was offset by an earnings season that did not see much surprise on the upside due to high expectations. In June, the market started the month trending higher but failed to hold on to its gain as profit-taking sets in due to concerns over valuations. The results release for the period of April-June saw substantial downgrades in consensus estimates in telcos, utilities, consumer discretionary & staples, whilst substantial upgrades were on technology, healthcare and energy.

8

The market was range bound in the month of July, with a lack of catalysts to drive the market. Invest Malaysia saw a higher turnout however, indicating renewed investor interest in Malaysia. As usual, the government announced several measures at the event, including (1) the Leading Entrepreneur Accelerator Platform (“LEAP”) market (2) a single regulator for the property sector. The listing of Lotte Chemical Titan, the largest IPO since 2012, turned out terribly for investors as the stock dropped 23% in a single day on 31 July after it announced a headline 67% QoQ and 72% YoY drop in 2Q17 net profit. Adjusted for exceptionals, the decline was more moderate at 17% QoQ and 36% YoY. However, due to the ineffective guidance by management, the damage to the stock’s marketability has been substantial. The lackluster performance continued in the month of August. After seven consecutive months of net buy, foreign investors turned marginal net sellers of Malaysia equities at RM0.3 bil. This brought the eight months cumulative foreign buy to RM10.9 bil. This was consistent with their retracement in the other ASEAN emerging markets. For the month of August, the key attraction to the market development was the 2Q17 corporate results reporting season, where corporate results have been lackluster in general. Although 2Q17 corporate earnings report card has been somewhat subdued and unexciting, we believe that 2H17 earnings should be stronger due to 1) 2Q17 5.8% GDP growth is the strongest in the past 2 years; 2) Ringgit has been stabilising; 3) improving labour market coupled with continued wage growth and moderating inflation will support and spur domestic economy and 4) government's continuous effort in the ongoing roll-out of infrastructure projects. In September, foreign outflows continue, with net outflow of RM0.8 bil (Aug: -RM0.3 bil), bringing down the Year-to-Date (“YTD”) cumulative foreign buy to RM10.0 bil. Crude oil price spiked 13.0% m.o.m to US$58/bbl, leading to outperformance in the Energy sector. The oil price were driven by hurricanes in US which have disrupted some oil logistics; Geopolitical issue in middle-east where Turkey is threatening to stop oil flow from Iraq’s Kurdish area which will affect up to 1.5% of global oil supply; Opec’s rhetoric to extend production cut to Dec18 from Mac18. Telco and Material sectors were outperformers too. For the period under review, FBM Shariah Index (FBMS) ended at 12,797.37 points, a gain of 3.64%.

Market Outlook

The key focus for the local market in October was the Budget 2018, which is also known as the pre-election budget. The continuous BR1M handout and income tax reduction is expected to lift private consumption, hence further strengthened our overweight call on the consumer sector. Furthermore, we view that the local consumer spending is poised to recover since the implementation of GST more than 2 years ago. In the budget, the government reiterated its commitment towards the main stream transportation-led projects which will continue to drive the construction sector. On top of this, the special end-financing scheme for PR1MA buyers has now been extended to private

9

developers as well, with the aim of helping first-time home buyers to obtain loans. This will benefit the banks as loan approvals are expected to escalate going forward. The GDP growth forecast for this year has also been raised to 5.2-5.7% during the budget, up from 4.3-4.8%. Authority expects growth to remain sanguine, albeit slightly lower at 5.0-5.5% in 2018. Overall, we believe that the Budget 2018 is positive to most of the sectors that we previously favored and continue to favor such as financial, consumer, construction/infrastructure, technology and export players. Going forward, we believe the market will refocus on external developments, namely 1) US-North Korea conflicts; 2) US tax reform; 3) Fed rate hike and 4) Middle Eastern tensions while on the local front, we are watchful on 1) the upcoming 3Q17 reporting season and 2) election developments.

Additional Information

Following the renewal of the Master Prospectus effective from 10 September 2017, the “Counterparty Credit Risk” has been included on page 43 as the inclusion in the Fund explicitly describes the risk in counterparty dealing instead of issuer/obligor credit. The insertion of this risk is for clarity purposes. Counterparty Credit Risk Counterparty credit risk is the risk arising from the possibility that the counterparty may default or not able to fulfill a trade settlement prior or on the settlement date of the trade. This could adversely affect the value of the Fund. For more details, kindly refer to the Master Prospectus dates 10 September 2017.

Kuala Lumpur, Malaysia AmFunds Management Berhad 7 November 2017

Independent auditors’ report to the unitholders of AmIttikal

Report on the audit of the financial statements

Opinion

Basis for opinion

Independence and other ethical responsibilities

Information other than the financial statements and auditors’ report thereon

We have audited the financial statements of AmIttikal (“the Fund”), which comprise the statementof financial position as at 30 September 2017, and the statement of comprehensive income,statement of changes in equity and statement of cash flows for the year then ended, and notes to thefinancial statements, including a summary of significant accounting policies, as set out on pages 13to 35.

In our opinion, the accompanying financial statements give a true and fair view of the financialposition of the Fund as at 30 September 2017 and of its financial performance and its cash flows forthe year then ended in accordance with Malaysian Financial Reporting Standards and InternationalFinancial Reporting Standards.

We conducted our audit in accordance with approved standards on auditing in Malaysia andInternational Standards on Auditing. Our responsibilities under those standards are further describedin the Auditor’s Responsibilities for the Audit of the Financial Statements section of our report. Webelieve that the audit evidence we have obtained is sufficient and appropriate to provide a basis forour opinion.

We are independent of the Fund in accordance with the By-Laws (on Professional Ethics, Conductand Practice) of the Malaysian Institute of Accountants (“By-Laws”) and the International EthicsStandards Board for Accountants’ Code of Ethics for Professional Accountants (“IESBA Code”),and we have fulfilled our other ethical responsibilities in accordance with the By-Laws and theIESBA Code.

The Manager is responsible for the other information. The other information comprises informationin the Annual Report, but does not include the financial statements of the Fund and our auditors’report thereon.

Our opinion on the financial statements of the Fund does not cover the other information and we donot express any form of assurance conclusion thereon.

In connection with our audit of the financial statements of the Fund, our responsibility is to read theother information and, in doing so, consider whether the other information is materially inconsistentwith the financial statements of the Fund or our knowledge obtained in the audit or otherwiseappears to be materially misstated.

10

Independent auditors’ report to the unitholders of AmIttikal (cont’d.)

Responsibilities of the Manager and the Trustees for the financial statements

Auditor’s responsibilities for the audit of the financial statements

Our objectives are to obtain reasonable assurance about whether the financial statements of theFund, as a whole are free from material misstatement, whether due to fraud or error, and to issue anauditors’ report that includes our opinion. Reasonable assurance is a high level of assurance, but isnot a guarantee that an audit conducted in accordance approved standards on auditing in Malaysiaand International Standards on Auditing will always detect a material misstatement when it exists.Misstatements can arise from fraud or error and are considered material if, individually or in theaggregate, they could reasonably be expected to influence the economic decisions of users taken onthe basis of these financial statements.

If based on the work we have performed, we conclude that there is a material misstatement of thisother information, we are required to report that fact. We have nothing to report in this regard.

The Manager is responsible for the preparation of the financial statements of the Fund that give atrue and fair view in accordance with Malaysian Financial Reporting Standards and InternationalFinancial Reporting Standards. The Manager is also responsible for such internal control as theManager determines is necessary to enable the preparation of financial statements of the Fund thatare free from material misstatement, whether due to fraud or error.

In preparing the financial statements of the Fund, the Manager is responsible for assessing theFund’s ability to continue as a going concern, disclosing, as applicable, matters related to goingconcern and using the going concern basis of accounting unless the Manager either intends toliquidate the Fund or to cease operations, or has no realistic alternative to do so.

The Trustee is responsible for ensuring that the Manager maintains proper accounting and otherrecords as are necessary to enable true and fair presentation of these financial statements.

As part of an audit in accordance with the approved standards on auditing in Malaysia andInternational Standards on Auditing, we exercise professional judgment and maintain professionalskepticism throughout the planning and performance of the audit. We also:

Identify and assess the risks of material misstatement of the financial statements of the Fund,whether due to fraud or error, design and perform audit procedures responsive to those risks,and obtain audit evidence that is sufficient and appropriate to provide a basis for our opinion.The risk of not detecting a material misstatement resulting from fraud is higher than for oneresulting from error, as fraud may involve collusion, forgery, intentional omissions,misrepresentations, or the override of internal control.

Obtain an understanding of internal control relevant to the audit in order to design auditprocedures that are appropriate in the circumstances, but not for the purpose of expressing anopinion on the effectiveness of the Fund’s internal control.

11

Independent auditors’ report to the unitholders of AmIttikal (cont’d.)

Other matters

Ernst & Young Wan Daneena Liza Bt Wan Abdul RahmanAF: 0039 No. 2978/03/18(J)Chartered Accountants Chartered Accountant

Kuala Lumpur, Malaysia7 November 2017

We communicate with the Manager regarding, among other matters, the planned scope and timingof the audit and significant audit findings, including any significant deficiencies in internal controlthat we identify during our audit.

This report is made solely to the unitholders of the Fund, as a body, and for no other purpose. We donot assume responsibility to any other person for the content of this report.

Evaluate the appropriateness of accounting policies used and the reasonableness of accountingestimates and related disclosures made by the Manager.

Conclude on the appropriateness of the Manager’s use of the going concern basis ofaccounting and, based on the audit evidence obtained, whether a material uncertainty existsrelated to events or conditions that may cast significant doubt on the Fund’s ability to continue as a going concern. If we conclude that a material uncertainty exists, we are required to drawattention in our auditors’ report to the related disclosures in the financial statements or, if suchdisclosures are inadequate, to modify our opinion. Our conclusions are based on the auditevidence obtained up to the date of our auditors’ report. However, future events or conditionsmay cause the Fund to cease to continue as a going concern.

Evaluate the overall presentation, structure and content of the financial statements of theFund, including the disclosures, and whether the financial statements of the Fund representthe underlying transactions and events in a manner that achieves fair presentation.

12

AmIttikal

STATEMENT OF FINANCIAL POSITIONAS AT 30 SEPTEMBER 2017

2017 2016Note RM RM

ASSETSShariah-compliant investments 4 117,959,881 153,522,563Deposits with financial institutions 5 30,002,795 4,000,329 Dividends receivable 145,347 282,076Sundry receivables 6 900,120 532,131Cash at banks 12,812,482 37,217,316

TOTAL ASSETS 161,820,625 195,554,415

LIABILITIESNet amount due to Manager 7 2,760,110 3,146,024Amount due to Trustee 8 9,334 12,333 Distribution payable and to be reinvested 6,355,284 - Sundry payables and accrued expenses 6 1,386,588 194,900

TOTAL LIABILITIES 10,511,316 3,353,257

EQUITYUnitholders’ capital 11(a) 306,601,066 348,325,358 Accumulated losses 11(b)(c) (155,291,757) (156,124,200)

TOTAL EQUITY 11 151,309,309 192,201,158

TOTAL EQUITY AND LIABILITIES 161,820,625 195,554,415

UNITS IN CIRCULATION 11(a) 238,025,628 301,987,557

NET ASSET VALUE PER UNIT 63.57 sen 63.65 sen

The accompanying notes form an integral part of the financial statements.

13

AmIttikal

STATEMENT OF COMPREHENSIVE INCOMEFOR THE FINANCIAL YEAR ENDED 30 SEPTEMBER 2017

2017 2016Note RM RM

SHARIAH-COMPLIANT INVESTMENT INCOMEGross dividend income 3,897,457 4,331,084Profit income 771,092 1,354,292Net gain fromShariah-compliant investments:− Financial assets at fair value through profit or loss (“FVTPL”) 9 5,416,842 7,883,207

Gross Income 10,085,391 13,568,583

EXPENDITUREManager’s profit 7 (2,507,698) (2,709,334) Trustee’s fee 8 (122,678) (147,121) Auditors’ remuneration (7,000) (7,000) Tax agent’s fee (5,000) (5,000) Custodian’s fee (3,944) - Other expenses 10 (251,344) (297,939)

Total Expenditure (2,897,664) (3,166,394)

NET INCOME BEFORE TAX 7,187,727 10,402,189 LESS: INCOME TAX 13 - -

NET INCOME AFTER TAX 7,187,727 10,402,189

OTHER COMPREHENSIVE INCOME - -

TOTAL COMPREHENSIVE INCOME FOR THE FINANCIAL YEAR 7,187,727 10,402,189

Total comprehensive income comprises the following: Realised income 9,880,331 10,673,387 Unrealised loss (2,692,604) (271,198)

7,187,727 10,402,189

Distributions for the financial year:Net distributions 14 6,355,284 13,143,085

Gross/net distributions per unit (sen) 14 2.67 4.00

The accompanying notes form an integral part of the financial statements.

14

AmIttikal

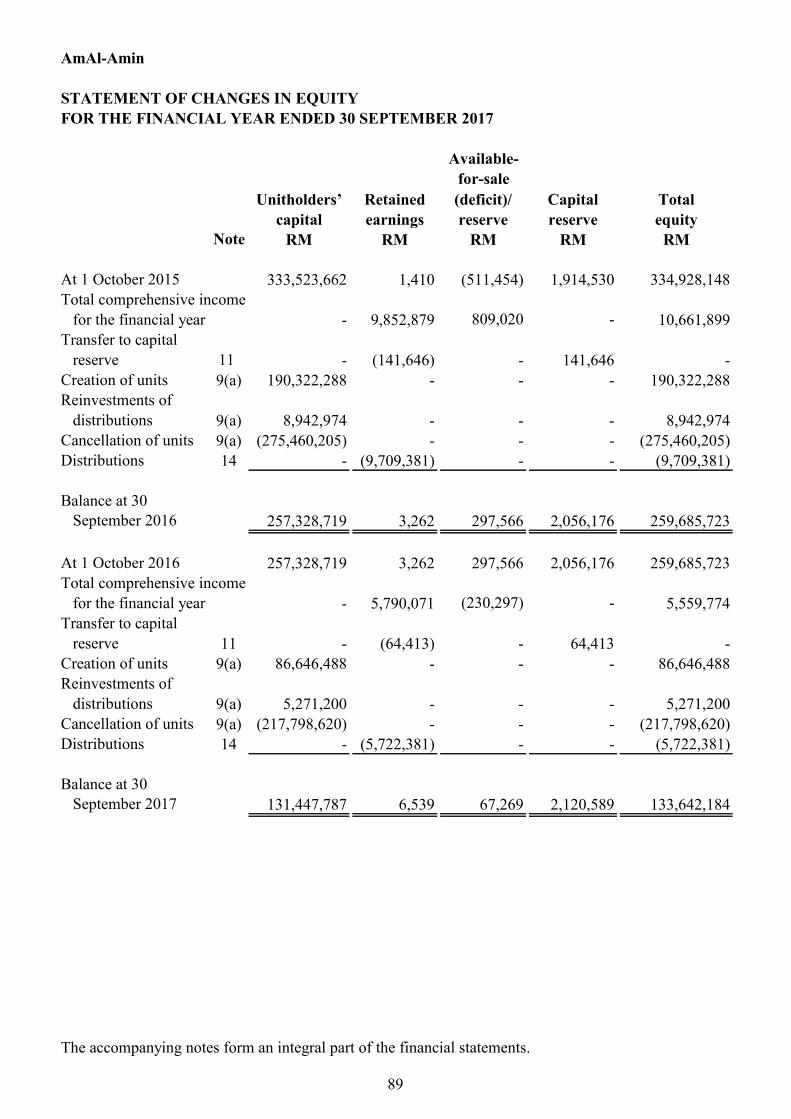

STATEMENT OF CHANGES IN EQUITYFOR THE FINANCIAL YEAR ENDED 30 SEPTEMBER 2017

Unitholders’ Accumulated Total capital losses equity

Note RM RM RM

At 1 October 2015 376,100,382 (153,383,304) 222,717,078 Total comprehensive income for the

financial year - 10,402,189 10,402,189 Creation of units 11(a) 15,580,034 - 15,580,034 Reinvestments of distributions 11(a),14 10,166,338 - 10,166,338 Cancellation of units 11(a) (53,521,396) - (53,521,396)Distributions 14 - (13,143,085) (13,143,085)

Balance at 30 September 2016 348,325,358 (156,124,200) 192,201,158

At 1 October 2016 348,325,358 (156,124,200) 192,201,158 Total comprehensive income for the

financial year - 7,187,727 7,187,727 Creation of units 11(a) 55,696,164 - 55,696,164 Cancellation of units 11(a) (97,420,456) - (97,420,456) Distributions 14 - (6,355,284) (6,355,284)

Balance at 30 September 2017 306,601,066 (155,291,757) 151,309,309

The accompanying notes form an integral part of the financial statements.

15

AmIttikal

STATEMENT OF CASH FLOWSFOR THE FINANCIAL YEAR ENDED 30 SEPTEMBER 2017

2017 2016Note RM RM

CASH FLOWS FROM OPERATING ANDINVESTING ACTIVITIES

Proceeds from sale of Shariah-compliant investments 211,898,167 280,986,467 Dividends received 4,034,186 4,486,859 Profit received 771,092 1,354,292 Tax refunded - 22,951 Manager’s profit paid (2,709,334) (4,526,434)Trustee’s fee paid (125,677) (148,748)Tax agent’s fee paid (5,000) (5,000)Custodian’s fee paid (3,944) - Payments for other expenses (261,787) (277,620)Purchase of Shariah-compliant investments (170,091,501) (228,455,717)

Net cash generated from operating and investing activities 43,506,202 53,437,050

CASH FLOWS FROM FINANCING ACTIVITIESProceeds from creation of units 55,715,094 15,561,104 Payments for cancellation of units (97,623,664) (53,267,122)Distributions paid - (2,976,747)

Net cash used in financing activities (41,908,570) (40,682,765)

NET INCREASE IN CASH AND CASH EQUIVALENTS 1,597,632 12,754,285

CASH AND CASH EQUIVALENTS AT BEGINNING OF FINANCIAL YEAR 41,217,645 28,463,360

CASH AND CASH EQUIVALENTS AT END OF FINANCIAL YEAR 42,815,277 41,217,645

Cash and cash equivalents comprise:Deposits with financial institutions 5 30,002,795 4,000,329 Cash at banks 12,812,482 37,217,316

42,815,277 41,217,645

The accompanying notes form an integral part of the financial statements.

16

AmIttikal

NOTES TO THE FINANCIAL STATEMENTS

1. GENERAL INFORMATION

2. BASIS OF PREPARATION OF FINANCIAL STATEMENTS

Standards effective during the financial year

Standards issued but not yet effective

Effective for financial periods

beginning on or after

MFRS 9: Financial InstrumentsMFRS 15: Revenue From Contracts With Customers

The Fund plans to adopt the above pronouncements when they become effective in the respectivefinancial periods. These pronouncements are expected to have no significant impact to the financialstatements of the Fund upon their initial application except as described below:

1 January 20181 January 2018

AmIttikal (“the Fund”) was established pursuant to a Deed dated 19 October 1992 as amended byDeeds Supplemental thereto (“the Deed”), between AmFunds Management Berhad as the Manager,AmanahRaya Trustees Berhad as the Trustee and all unitholders.

As at the date of authorisation of these financial statements, the following Standards, which arerelevant to the Fund, have been issued by MASB but are not yet effective and have not beenadopted by the Fund.

The Fund was set up with the objective of providing investors with a means to pool and invest theirfunds in a professionally managed portfolio of Shariah-compliant equities and other non-interestbearing securities. The Fund aims to provide an investment alternative where profits earned are inaccordance with Principles of Shariah. The Fund is managed based on the concept of Al-Mudharabah. As provided in the Deed, the “accrual period” or the financial year shall end on 30September and the units in the Fund were first offered for sale on 18 December 1992.

The financial statements of the Fund have been prepared in accordance with Malaysian FinancialReporting Standards (“MFRS”) as issued by the Malaysian Accounting Standards Board(“MASB”) and are in compliance with International Financial Reporting Standards.

The financial statements of the Fund have been prepared under the historical cost convention,unless otherwise stated in the accounting policies.

The adoption of MFRS which have been effective during the financial year did not have anymaterial financial impact to the financial statements.

17

MFRS 9 Financial Instruments

3. SIGNIFICANT ACCOUNTING POLICIES

Income recognition

Income tax

Functional and presentation currency

Statement of cash flows

Distribution

Current tax assets and liabilities are measured at the amount expected to be recovered from or paidto the tax authorities. The tax rates and tax laws used to compute the amount are those that areenacted or substantively enacted at the reporting date.

Current taxes are recognised in profit or loss except to the extent that the tax relates to itemsrecognised outside profit or loss, either in other comprehensive income or directly in equity.

Functional currency is the currency of the primary economic environment in which the Fundoperates that most faithfully represents the economic effects of the underlying transactions. Thefunctional currency of the Fund is Ringgit Malaysia which reflects the currency in which the Fundcompetes for funds, issues and redeems units. The Fund has also adopted Ringgit Malaysia as itspresentation currency.

The Fund adopts the direct method in the preparation of the statement of cash flows.

Cash equivalents are short-term, highly liquid Shariah-compliant investments that are readilyconvertible to cash with insignificant risk of changes in value.

Distributions are at the discretion of the Fund. A distribution to the Fund’s unitholders is accountedfor as a deduction from realised reserves. A proposed distribution is recognised as a liability in theperiod in which it is approved.

MFRS 9 reflects International Accounting Standards Board’s (“IASB”) work on the replacement ofMFRS 139 Financial Instruments: Recognition and Measurement (“MFRS 139”). MFRS 9 will beeffective for financial year beginning on or after 1 January 2018. The Fund is in the process ofquantifying the impact of the first adoption of MFRS 9.

Income is recognised to the extent that it is probable that the economic benefits will flow to theFund and the income can be reliably measured. Income is measured at the fair value ofconsideration received or receivable.

Dividend income is recognised when the Fund’s right to receive payment is established. Profitincome on Islamic short-term deposits is recognised on an accrual basis using the effective profitmethod.

18

Unitholders’ capital

Financial assets

(i) Financial assets at FVTPL

(ii) Receivables

Subsequent to initial recognition, receivables are measured at amortised cost using the effectiveprofit method. Gains and losses are recognised in profit or loss when the receivables arederecognised or impaired, and through the amortisation process.

For Shariah-compliant investments in quoted securities, market value is determined based onthe closing price quoted on Bursa Malaysia Securities Berhad. Unrealised gains or lossesrecognised in profit or loss are not distributable in nature.

On disposal of Shariah-compliant investments, the net realised gain or loss on disposal ismeasured as the difference between the net disposal proceeds and the carrying amount of theShariah-compliant investments. The net realised gain or loss is recognised in profit or loss.

Financial assets with fixed or determinable payments that are not quoted in an active market areclassified as receivables.

Financial assets are recognised in the statement of financial position when, and only when, theFund becomes a party to the contractual provisions of the financial instrument.

When financial assets are recognised initially, they are measured at fair value, plus, in the case offinancial assets not at fair value through profit or loss, directly attributable transaction costs.

The Fund determines the classification of its financial assets at initial recognition, and thecategories applicable to the Fund include financial assets at fair value through profit or loss(“FVTPL”) and receivables.

Financial assets are classified as financial assets at FVTPL if they are held for trading or aredesignated as such upon initial recognition. Financial assets held for trading by the Fundinclude Shariah-compliant equity securities acquired principally for the purpose of selling inthe near term.

Subsequent to initial recognition, financial assets at FVTPL are measured at fair value.Changes in the fair value of those financial instruments are recorded in ‘Net gain or loss onfinancial assets at fair value through profit or loss’. Dividend revenue and profit earnedelements of such instruments are recorded separately in ‘Gross dividend income’ and ‘Profitincome’ respectively.

The unitholders’ capital of the Fund meets the definition of puttable instruments and is classified asequity instruments under MFRS 132 Financial Instruments: Presentation (“MFRS 132”).

19

Impairment of financial assets

(i) Receivables carried at amortised cost

Financial liabilities

Classification of realised and unrealised gains and losses

The Fund assesses at each reporting date whether there is any objective evidence that a financialasset is impaired.

To determine whether there is objective evidence that an impairment loss on financial assetshas been incurred, the Fund considers factors such as the probability of insolvency orsignificant financial difficulties of the debtor and default or significant delay in payments.

If any such evidence exists, the amount of impairment loss is measured as the differencebetween the asset’s carrying amount and the present value of estimated future cash flowsdiscounted at the financial asset’s original effective profit rate. The impairment loss isrecognised in profit or loss.

The carrying amount of the financial asset is reduced through the use of an allowance account.When a receivable become uncollectible, it is written off against the allowance account.

If in a subsequent period, the amount of the impairment loss decreases and the decrease can berelated objectively to an event occurring after the impairment was recognised, the previouslyrecognised impairment loss is reversed to the extent that the carrying amount of the asset doesnot exceed its amortised cost at the reversal date. The amount of reversal is recognised in profitor loss.

The Fund’s financial liabilities are recognised initially at fair value plus directly attributabletransaction costs and subsequently measured at amortised cost using the effective profit method.

Financial liabilities are classified according to the substance of the contractual arrangementsentered into and the definitions of a financial liability.

Financial liabilities, within the scope of MFRS 139, are recognised in the statement of financialposition when, and only when, the Fund becomes a party to the contractual provisions of thefinancial instrument.

Unrealised gains and losses comprise changes in the fair value of financial instruments for theperiod and from reversal of prior period’s unrealised gains and losses for financial instrumentswhich were realised (i.e. sold, redeemed or matured) during the reporting period.

A financial liability is derecognised when the obligation under the liability is extinguished. Gainsand losses are recognised in profit or loss when the liabilities are derecognised, and through theamortisation process.

20

Significant accounting estimates and judgments

4. SHARIAH-COMPLIANT INVESTMENTS2017 2016RM RM

Financial assets at FVTPL

Quoted Shariah-compliant equity securities in Malaysia 117,959,881 153,522,563

Details of Shariah-compliant investments as at 30 September 2017 are as follows:Market

value as a percentage of

Number of Market Purchase net assetName of company shares value cost value

RM RM %

Quoted Shariah-compliant equity securities in Malaysia

ConstructionGadang Holdings Berhad 2,648,400 3,257,532 3,375,860 2.15Gamuda Berhad 1,062,700 5,611,056 5,448,233 3.71IJM Corporation Berhad 968,800 3,197,040 3,240,390 2.11Kerjaya Prospek Group Berhad 446,300 1,633,458 1,637,735 1.08Sunway Construction

Group Berhad 1,112,000 2,535,360 2,601,944 1.68WCT Holdings Berhad 1,331,993 2,330,988 2,629,435 1.54

7,570,193 18,565,434 18,933,597 12.27

(Forward)

The preparation of the Fund’s financial statements requires the Manager to make judgments,estimates and assumptions that affect the reported amounts of revenues, expenses, assets andliabilities, and the disclosure of contingent liabilities at the reporting date. However, uncertaintyabout these assumptions and estimates could result in outcomes that could require a materialadjustment to the carrying amount of the asset or liability in the future.

The Fund classifies its Shariah-compliant investments as financial assets at FVTPL as the Fundmay sell its Shariah-compliant investments in the short-term for profit-taking or to meetunitholders’ cancellation of units.

No major judgments have been made by the Manager in applying the Fund’s accounting policies.There are no key assumptions concerning the future and other key sources of estimation uncertaintyat the reporting date, that have a significant risk of causing a material adjustment to the carryingamounts of assets and liabilities within the next financial year.

Realised gains and losses on disposals of financial instruments classified at fair value through profitor loss are calculated using the weighted average method. They represent the difference between aninstrument’s initial carrying amount and disposal amount.

21

Marketvalue as a

percentage ofNumber of Market Purchase net asset

Name of company shares value cost valueRM RM %

Quoted Shariah-compliant equity securities in Malaysia

ConsumerHong Leong Industries Berhad 202,600 1,904,440 1,892,774 1.26

FinanceBIMB Holdings Berhad 723,100 3,174,409 2,997,410 2.10Syarikat Takaful Malaysia

Berhad 860,400 3,269,520 3,503,491 2.16

1,583,500 6,443,929 6,500,901 4.26

Industrial productsDRB-Hicom Berhad 969,900 1,580,937 2,647,479 1.05Heveaboard Berhad 961,200 1,528,308 1,635,137 1.01Petron Malaysia Refining &

Marketing Bhd 320,700 3,303,210 3,279,032 2.18PETRONAS Gas Berhad 222,400 3,980,960 4,812,221 2.63SKP Resources Bhd 2,109,400 3,164,100 3,140,440 2.09Thong Guan Industries Berhad 776,300 3,128,489 3,391,571 2.07Wellcall Holdings Berhad 1,775,200 2,290,008 2,472,269 1.51

7,135,100 18,976,012 21,378,149 12.54

Infrastructure projectsDiGi.Com Berhad 1,032,200 5,057,780 5,561,900 3.34TIME dotCom Berhad 350,800 3,115,104 3,266,921 2.06

1,383,000 8,172,884 8,828,821 5.40

PlantationGenting Plantations Berhad 234,700 2,417,410 2,540,090 1.60IJM Plantations Berhad 1,065,600 3,079,584 3,855,994 2.03IOI Corporation Berhad 186,900 848,526 836,090 0.56

1,487,200 6,345,520 7,232,174 4.19

PropertiesEco World Development

Group Berhad 1,549,700 2,402,035 2,431,413 1.59Mah Sing Group Berhad 1,070,900 1,595,641 1,610,083 1.05

2,620,600 3,997,676 4,041,496 2.64

(Forward)

22

Marketvalue as a

percentage ofNumber of Market Purchase net asset

Name of company shares value cost valueRM RM %

Quoted Shariah-compliant equity securities in Malaysia

TechnologyGlobetronics Technology Berhad 258,600 1,590,390 1,481,704 1.05Malaysian Pacific Industries

Berhad 186,800 2,499,384 2,628,417 1.65

445,400 4,089,774 4,110,121 2.70

Trading/ServicesAxiata Group Berhad 1,628,600 8,533,864 9,989,196 5.64Bermaz Auto Berhad 869,100 1,833,801 1,949,277 1.21Dayang Enterprise Holdings

Berhad 913,000 903,870 2,325,850 0.60Dialog Group Berhad 2,465,700 4,931,400 4,835,532 3.27IHH Healthcare Berhad 859,100 4,939,825 5,704,032 3.26Maxis Berhad 679,900 3,943,420 4,752,690 2.61My E.G. Services Berhad 1,250,600 2,563,730 2,629,963 1.69Pos Malaysia Berhad 295,800 1,552,950 1,414,456 1.03Sime Darby Berhad 1,590,400 14,345,408 14,192,353 9.48Telekom Malaysia Berhad 633,200 4,115,800 3,912,631 2.72Uzma Berhad 1,250,100 1,800,144 1,819,702 1.19

12,435,500 49,464,212 53,525,682 32.70

Total financial assets at FVTPL 34,863,093 117,959,881 126,443,715 77.96

Shortfall of market value over cost (8,483,834)

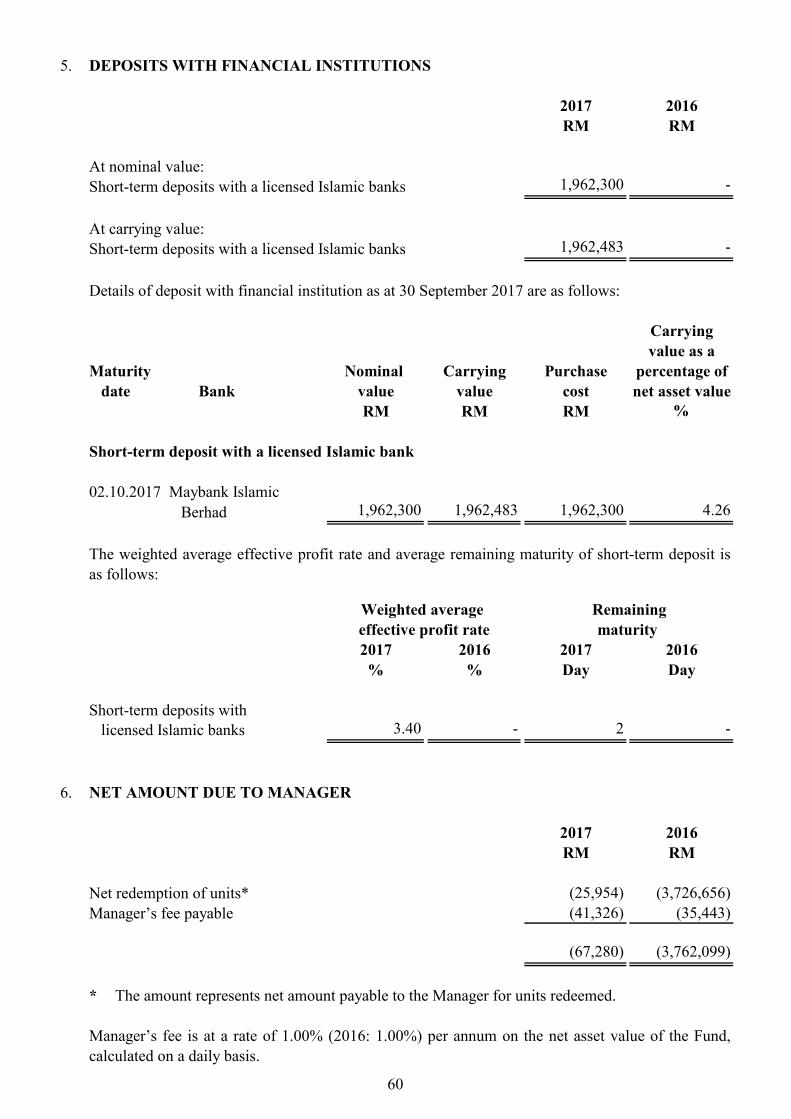

5. DEPOSITS WITH FINANCIAL INSTITUTIONS

2017 2016RM RM

At nominal value:Short-term deposits with licensed Islamic banks 30,000,000 4,000,000

At carrying value:Short-term deposits with licensed Islamic banks 30,002,795 4,000,329

23

Details of deposit with financial institution as at 30 September 2017 are as follows:

Carryingvalue as a

percentage of Maturity Nominal Carrying Purchase net asset

date Bank value value cost valueRM RM RM %

Short-term deposit with a licensed Islamic bank

Maybank Islamic Berhad 30,000,000 30,002,795 30,000,000 19.83

Weighted average effective Remaining profit rate maturity

2017 2016 2017 2016% % Days Days

Short-term deposits with licensed Islamic banks 3.40 3.00 2 4

6. SUNDRY RECEIVABLES/PAYABLES AND ACCRUED EXPENSES

2017 2016RM RM

Amounts owing from financial institutions 900,120 532,131 Amounts owing to brokers/financial institutions (1,195,131) -

The normal trade credit period is three business days.

7. NET AMOUNT DUE TO MANAGER2017 2016RM RM

Net redemption of units* (252,412) (436,690)Manager’s profit payable (2,507,698) (2,709,334)

(2,760,110) (3,146,024)

*

Manager’s profit is up to 20% of the net realised profits.

02.10.2017

The amount represents net amount payable to the Manager for units redeemed.

Included in sundry receivables/payables and accrued expenses were amounts owing from/tobrokers/financial institutions for outstanding contracts where settlement were not due as follows:

The weighted average effective profit rate and average remaining maturity of short-term depositsare as follows:

24

8. AMOUNT DUE TO TRUSTEE

9. NET GAIN FROM SHARIAH-COMPLIANT INVESTMENTS

2017 2016RM RM

Net gain on financial assets at FVTPL comprised:− Net realised gain on sale of Shariah-compliant investments 8,109,446 8,154,405 − Net unrealised loss on changes in fair values of

Shariah-compliant investments (2,692,604) (271,198)

5,416,842 7,883,207

10. OTHER EXPENSES

11. TOTAL EQUITY

Total equity is represented by:

2017 2016Note RM RM

Unitholders’ capital (a) 306,601,066 348,325,358Accumulated losses- Realised loss (b) (146,807,923) (150,332,970)- Unrealised loss (c) (8,483,834) (5,791,230)

151,309,309 192,201,158

Included in other expenses is Goods and Services Tax incurred by the Fund during the financialyear amounting to RM164,506 (2016: RM172,778).

The normal credit period in the previous and current financial years for Trustee’s fee payable is onemonth.

Trustee’s fee is at a rate of 0.07% (2016: 0.07%) per annum on the net asset value of the Fund,calculated on a daily basis.

The normal credit period in the previous and current financial years for creation and redemption ofunits is three business days.

The normal credit period in the previous and current financial years for Manager’s profit payable isone month.

25

(a) UNITHOLDERS’ CAPITAL/UNITS IN CIRCULATION

Number of Number of units RM units RM

At beginning of the financial year 301,987,557 348,325,358 345,696,067 376,100,382Creation during the financial year 84,047,148 55,696,164 23,826,330 15,580,034Distributions reinvested (Note 14) - - 15,627,507 10,166,338Cancellation during the financial year (148,009,077) (97,420,456) (83,162,347) (53,521,396)

At end of the financial year 238,025,628 306,601,066 301,987,557 348,325,358

(b) REALISED – DISTRIBUTABLE

2017 2016RM RM

At beginning of the financial year (150,332,970) (147,863,272)

Total comprehensive income for the financial year 7,187,727 10,402,189 Net unrealised loss attributable to Shariah-compliant

investments held transferred to unrealised reserve[Note 11(c)] 2,692,604 271,198

Distributions out of realised reserve (Note 14) (6,355,284) (13,143,085)

Net increase/(decrease) in realised reserve for the financial year 3,525,047 (2,469,698)

At end of the financial year (146,807,923) (150,332,970)

(c) UNREALISED – NON-DISTRIBUTABLE

2017 2016RM RM

At beginning of the financial year (5,791,230) (5,520,032)Net unrealised loss attributable to Shariah-compliant

investments held transferred from realised reserve[Note 11(b)] (2,692,604) (271,198)

At end of the financial year (8,483,834) (5,791,230)

12. UNITS HELD BY RELATED PARTIES

20162017

The Manager and parties related to the Manager did not hold any units in the Fund as at 30September 2017 and 30 September 2016.

26

13. INCOME TAX

2017 2016RM RM

Net income before tax 7,187,727 10,402,189

Taxation at Malaysian statutory rate of 24% 1,725,054 2,496,500Tax effects of:

Income not subject to tax (3,066,719) (3,321,500)Loss not deductible for tax purposes 646,225 65,100Restriction on tax deductible expenses for unit trust fund 561,555 611,300Non-permitted expenses for tax purposes 71,490 80,700Permitted expenses not used and not available for future financial years 62,395 67,900

Tax expense for the financial year - -

14. DISTRIBUTIONS

2017 2016RM RM

Undistributed net income brought forward - 2,469,698Gross dividend income 2,822,271 4,331,084Profit income 558,372 1,354,292Net realised gain on sale of Shariah-compliant investments 5,872,305 8,154,405

9,252,948 16,309,479Less: Expenses (2,897,664) (3,166,394)

Total amount of distributions 6,355,284 13,143,085

Gross/net distributions per unit (sen) 2.67 4.00

Distributions made out of:- Realised reserve [Note 11(b)] 6,355,284 13,143,085

(Forward)

Distributions to unitholders declared on 29 September 2017 (28 October 2015, 7 January 2016, 8April 2016 and 29 August 2016 for the previous financial year) are from the following sources:

Pursuant to Schedule 6 of the Income Tax Act, 1967, local profit income derived by the Fund isexempted from tax.

A reconciliation of income tax expense applicable to net income before tax at the statutory incometax rate to income tax expense at the effective income tax rate of the Fund is as follows:

Income tax payable is calculated on Shariah-compliant investment income less deduction forpermitted expenses as provided for under Section 63B of the Income Tax Act, 1967.

27

2017 2016RM RM

Comprising:Distributions reinvested [Note 11(a)] - 10,166,338Distribution payable and to be reinvested 6,355,284 - Cash distributions - 2,976,747

6,355,284 13,143,085

15. MANAGEMENT EXPENSE RATIO (“MER”)

2017 2016% p.a. % p.a.

Manager’s fee 1.43 1.29Trustee’s fee 0.07 0.07Fund’s other expenses 0.15 0.15

Total MER 1.65 1.51

16. PORTFOLIO TURNOVER RATIO (“PTR”)

17. SEGMENTAL REPORTING

− A portfolio of Shariah-compliant equity instruments; and− A portfolio of Shariah-compliant fixed income instruments, including deposit with financial

institution.

Included in the distributions for the financial year ended 30 September 2016 was RM2,469,698distributed from previous financial years’ realised income.

The above distributions for the financial year ended 30 September 2017 have been proposed beforetaking into account the net unrealised loss of RM8,483,834 (2016: RM5,791,230) which are carriedforward to the next financial year.

The Fund’s MER is as follows:

The MER of the Fund is the ratio of the sum of annualised fees and expenses incurred by the Fund tothe average net asset value of the Fund calculated on a daily basis.

The PTR of the Fund, which is the ratio of average total acquisitions and disposals of Shariah-compliant investments to the average net asset value of the Fund calculated on a daily basis, is 1.09times (2016: 1.21 times).

The Manager and Investment Committee of the Fund are responsible for allocating resources availableto the Fund in accordance with the overall investment strategies as set out in the Investment Guidelinesof the Fund. The Fund is managed by two segments:

28

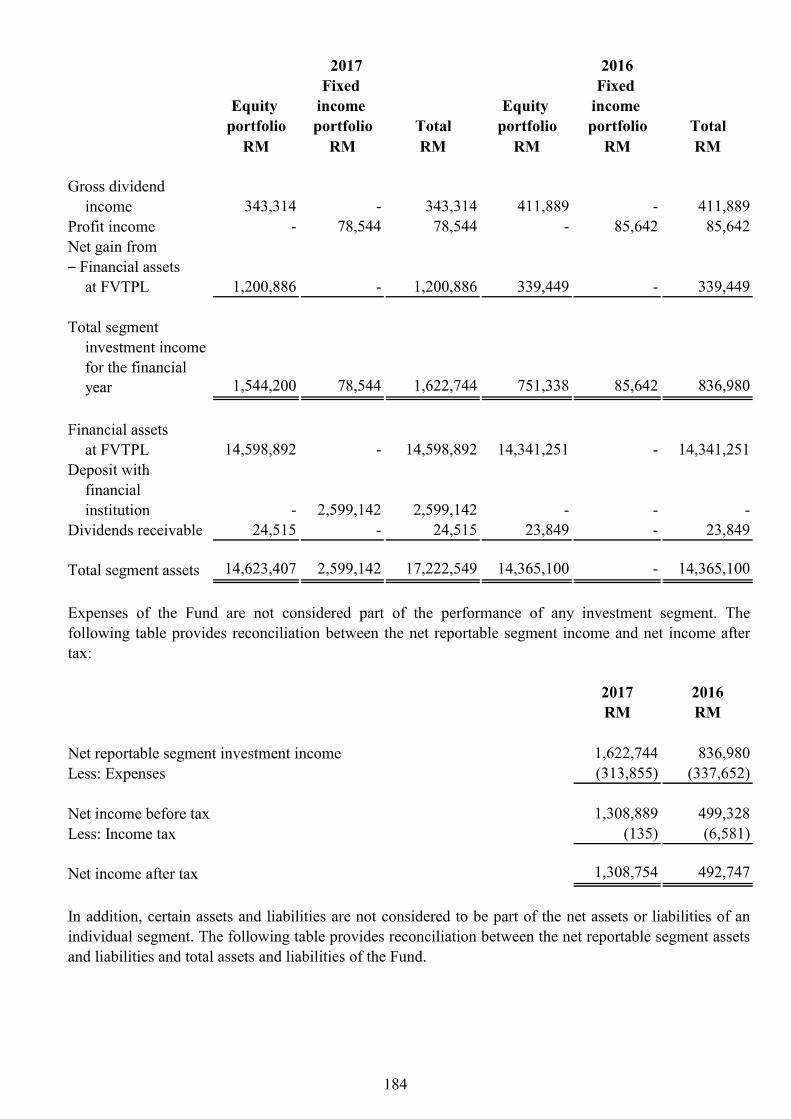

Fixed Fixed Equity income Equity income

portfolio portfolio Total portfolio portfolio TotalRM RM RM RM RM RM

Gross dividend income 3,897,457 - 3,897,457 4,331,084 - 4,331,084

income - 771,092 771,092 - 1,354,292 1,354,292

Shariah-compliant investments:

‒ Financialassetsat FVTPL 5,416,842 - 5,416,842 7,883,207 - 7,883,207

Total segment investment income forthe financial year 9,314,299 771,092 10,085,391 12,214,291 1,354,292 13,568,583

Financial assets at FVTPL 117,959,881 - 117,959,881 153,522,563 - 153,522,563

Deposits with financial institutions - 30,002,795 30,002,795 - 4,000,329 4,000,329

Dividends receivable 145,347 - 145,347 282,076 - 282,076

Amount owing from broker 900,120 - 900,120 532,131 - 532,131

Total segment assets -119,005,348 30,002,795 149,008,143 154,336,770 4,000,329 158,337,099

Amount owing tobroker 1,195,131 - 1,195,131 - - -

Total segment liabilities 1,195,131 - 1,195,131 - - -

2017 2016

The investment objective of each segment is to achieve consistent returns from the Shariah-compliantinvestments in each segment while safeguarding capital by investing in diversified portfolios. Therehave been no changes in reportable segments in the current financial year. The segment informationprovided is presented to the Manager and Investment Committee of the Fund.

Profit

Net gain from

29

2017 2016RM RM

Net reportable segment investment income 10,085,391 13,568,583Less: Expenses (2,897,664) (3,166,394)

Net income before tax 7,187,727 10,402,189Less: Income tax - -

Net income after tax 7,187,727 10,402,189

2017 2016RM RM

Total segment assets 149,008,143 158,337,099Cash at banks 12,812,482 37,217,316

Total assets of the Fund 161,820,625 195,554,415

Total segment liabilities 1,195,131 -Net amount due to Manager 2,760,110 3,146,024Amount due to Trustee 9,334 12,333 Distribution payable and to be reinvested 6,355,284 - Sundry payables and accrued expenses 191,457 194,900

Total liabilities of the Fund 10,511,316 3,353,257

18. TRANSACTIONS WITH BROKERS AND FINANCIAL INSTITUTIONS

Brokerage fee, stampBrokers/Financial institutions Transaction value duty and clearing fee

RM % RM %

AmInvestment Bank Berhad* 96,003,031 25.03 310,238 23.61 Affin Investment Bank Berhad 29,510,873 7.69 117,810 8.97 Maybank Investment Bank Berhad 28,129,455 7.33 115,045 8.76 CIMB Investment Bank Berhad 25,727,111 6.71 95,264 7.25 Citigroup Global Markets Malaysia

Sdn Bhd 21,232,763 5.54 67,090 5.11 KAF Seagroatt & Campbell Securities

Sdn Bhd 20,364,845 5.31 64,351 4.90 CLSA Securities Sdn Bhd 19,431,633 5.07 61,377 4.67

(Forward)

Details of transactions with brokers and financial institutions for the financial year ended 30September 2017 are as follows:

In addition, certain assets and liabilities are not considered to be part of the net assets or liabilities ofan individual segment. The following table provides reconciliation between the net reportable segmentassets and liabilities and total assets and liabilities of the Fund.

Expenses of the Fund are not considered part of the performance of any investment segment. Thefollowing table provides reconciliation between the net reportable segment income and net incomeafter tax:

30

Brokerage fee, stampBrokers/Financial institutions Transaction value duty and clearing fee

RM % RM %

Macquarie Capital Securities (M) Sdn Bhd 17,495,505 4.56 57,140 4.35 RHB Investment Bank Berhad 16,472,172 4.29 62,215 4.74 Public Investment Bank Berhad 15,674,616 4.09 51,281 3.90 Other brokers and financial institutions 93,510,784 24.38 311,869 23.74

Total 383,552,788 100.00 1,313,680 100.00

*

19. FINANCIAL INSTRUMENTS

(a) Classification of financial instruments

Financial Financial Receivables liabilities at

assets at amortised amortisedat FVTPL cost cost Total

RM RM RM RM

AssetsShariah-compliant investments 117,959,881 - - 117,959,881Deposits with financial institutions - 30,002,795 - 30,002,795Dividends receivable - 145,347 - 145,347Sundry receivables - 900,120 - 900,120Cash at banks - 12,812,482 - 12,812,482

Total financial assets 117,959,881 43,860,744 - 161,820,625

LiabilitiesNet amount due to Manager - - 2,760,110 2,760,110Amount due to Trustee - - 9,334 9,334Distribution payable and to be

reinvested - - 6,355,284 6,355,284Sundry payables and accrued

expenses - - 1,386,588 1,386,588

Total financial liabilities - - 10,511,316 10,511,316

(Forward)

2017

A financial institution related to the Manager. The Manager and the Trustee are of the opinionthat the above transactions have been entered in the normal course of business and have beenestablished under terms that are no less favourable than those arranged with independent thirdparties.

The above transactions were in respect of Shariah-compliant listed securities.

The significant accounting policies in Note 3 describe how the classes of financial instruments aremeasured, and how income and expenses, including fair value gains and losses, are recognised.The following table analyses the financial assets and liabilities of the Fund in the statement offinancial position by the class of financial instrument to which they are assigned, and therefore bythe measurement basis.

31

Financial Financial Receivables liabilities at

assets at amortised amortisedat FVTPL cost cost Total

RM RM RM RM

AssetsShariah-compliant investments 153,522,563 - - 153,522,563 Deposits with financial institutions - 4,000,329 - 4,000,329 Dividends receivable - 282,076 - 282,076 Sundry receivables - 532,131 - 532,131 Cash at banks - 37,217,316 - 37,217,316

Total financial assets 153,522,563 42,031,852 - 195,554,415

LiabilitiesNet amount due to Manager - - 3,146,024 3,146,024 Amount due to Trustee - - 12,333 12,333 Sundry payables and accrued

expenses - - 194,900 194,900

Total financial liabilities - - 3,353,257 3,353,257

Income, expense, gainsand losses

2017 2016RM RM

Net gain from financial assets at FVTPL 5,416,842 7,883,207 Income, of which derived from:– Gross dividend income from financial assets at FVTPL 3,897,457 4,331,084- Profit income from receivables 771,092 1,354,292

(b) Financial instruments that are carried at fair value

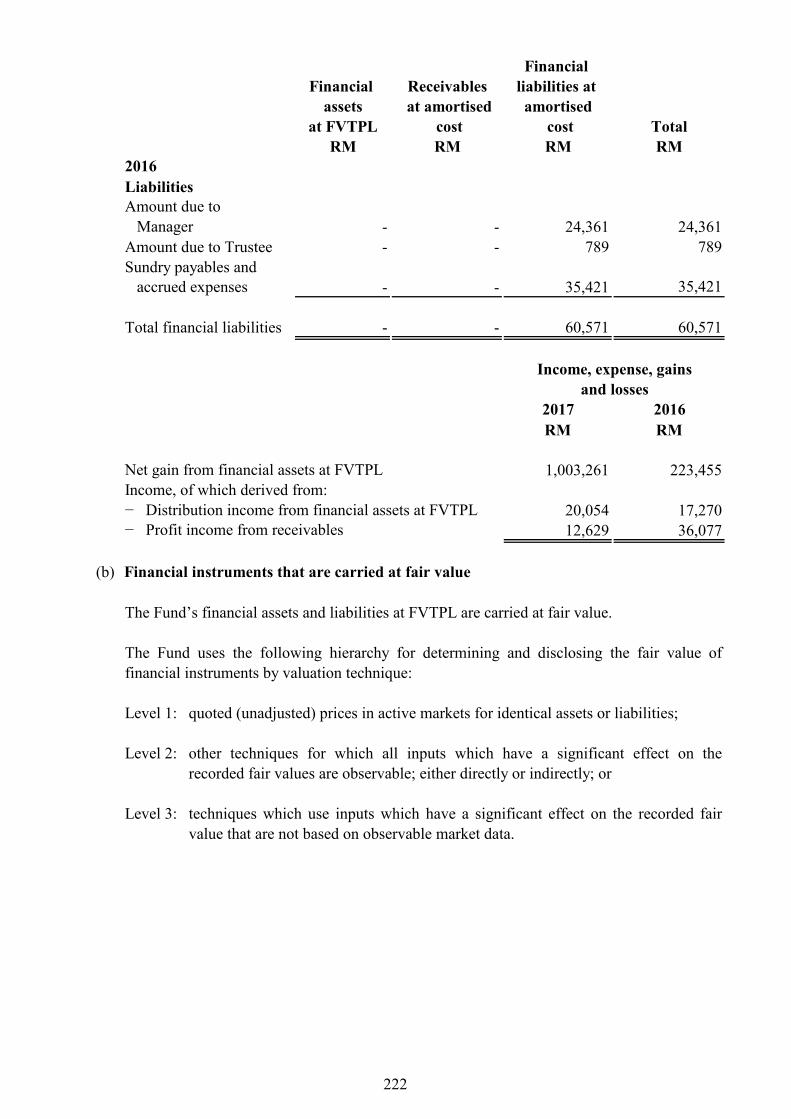

Level 1: quoted (unadjusted) prices in active markets for identical assets or liabilities;

Level 2:

Level 3:

The following table shows an analysis of financial instruments recorded at fair value by the levelof the fair value hierarchy:

techniques which use inputs which have a significant effect on the recorded fair valuethat are not based on observable market data.

The Fund’s financial assets and liabilities at FVTPL are carried at fair value.

other techniques for which all inputs which have a significant effect on the recordedfair values are observable; either directly or indirectly; or

2016

The Fund uses the following hierarchy for determining and disclosing the fair value of financialinstruments by valuation technique:

32

Level 1 Level 2 Level 3 TotalRM RM RM RM

117,959,881 - - 117,959,881

153,522,563 - - 153,522,563

(c)

Deposits with financial institutions Dividends receivable Sundry receivables Cash at banks Net amount due to Manager Amount due to Trustee Distribution payable and to be reinvested Sundry payables and accrued expenses

20. RISK MANAGEMENT POLICIES

Market risk

Financial assets at FVTPL

Financial instruments that are not carried at fair value and whose carrying amounts arereasonable approximation of fair value

The Fund is exposed to a variety of risks that include market risk, credit risk, liquidity risk, singleissuer risk, regulatory risk, management risk and non-compliance/Shariah non-compliance risk.

Risk management is carried out by closely monitoring, measuring and mitigating the above said risks,careful selection of Shariah-compliant investments coupled with stringent compliance to Shariah-compliant investment restrictions as stipulated by the Capital Market and Services Act 2007, SecuritiesCommission’s Guidelines on Unit Trust Funds and the Deed as the backbone of risk management ofthe Fund.

Market risk, in general, is the risk that the value of a portfolio would decrease due to changes in marketrisk factors such as equity prices, foreign exchange rates, rate of return (yield curve) and commodityprices.

The following are classes of financial instruments that are not carried at fair value and whosecarrying amounts are reasonable approximation of fair value due to their short period to maturityor short credit period:

2016Financial assets at FVTPL

There are no financial instruments which are not carried at fair values and whose carrying amountsare not reasonable approximation of their respective fair values.

2017

33

(i) Price risk

Percentage movements in price by: 2017 2016

RM RM

-5.00% (5,897,944) (7,676,128)+5.00% 5,897,994 7,676,128

(ii) Profit rate risk

Parallel shift in yield curve by: 2017 2016

RM RM

+100 bps (2,373) (424)-100 bps 2,397 428

Credit risk

Domestic profit rate on deposits and placements with licensed financial institutions are determinedbased on prevailing market rates.

The result below summarised the profit rate sensitivity of the Fund’s NAV, or theoretical value(applicable to Islamic money market deposit) due to the parallel movement assumption of theyield curve by +100bps and -100bps respectively:

Credit risk is the risk that the counterparty to a financial instrument will cause a financial loss to theFund by failing to discharge an obligation. Credit risk applies to Islamic short-term deposits anddividends receivable. The issuer of such instruments may not be able to fulfill the required profitpayments or repay the principal invested or amount owing. These risks may cause the Fund’s Shariah-compliant investments to fluctuate in value.

For deposits with financial institutions, the Fund makes placements with financial institutions withsound rating of P1/MARC-1 and above. Cash at banks are held for liquidity purposes and are notexposed to significant credit risk.

Price risk refers to the uncertainty of an investment’s future prices. In the event of adverse pricemovements, the Fund might endure potential loss on its quoted Shariah-compliant investments. Inmanaging price risk, the Manager actively monitors the performance and risk profile of theinvestment portfolio.

The result below summarised the price risk sensitivity of the Fund’s NAV due to movements ofprice by -5.00% and +5.00% respectively:

Sensitivity of the Fund’s NAV

Sensitivity of the Fund’s NAV, or theoretical value

Profit rate risk will affect the value of the Fund’s Shariah-compliant investments, given the profitrate movements, which are influenced by regional and local economic developments as well aspolitical developments.

34

Liquidity risk

Single issuer risk

Regulatory risk

Management risk

Non-compliance/Shariah non-compliance risk

21. CAPITAL MANAGEMENT

No changes were made in the objective, policies or processes during the financial years ended 30September 2017 and 30 September 2016.

The primary objective of the Fund’s capital management is to ensure that it maximises unitholders’value by expanding its fund size to benefit from economies of scale and achieving growth in net assetvalue from the performance of its Shariah-compliant investments.

The Fund manages its capital structure and makes adjustments to it, in light of changes in economicconditions. To maintain or adjust the capital structure, the Fund may issue new or bonus units, makedistribution payment, or return capital to unitholders by way of redemption of units.

Poor management of the Fund may cause considerable losses to the Fund that in turn may affect the netasset value of the Fund.

This is the risk of the Manager, the Trustee or the Fund not complying with internal policies, the Deedof the Fund, securities law or guidelines issued by the regulators. In the case of an Islamic Fund, thisincludes the risk of the Fund not conforming to Shariah Investment Guidelines. Non-compliance riskmay adversely affect the Shariah-compliant investments of the Fund when the Fund is forced to rectifythe non-compliance.

Any changes in national policies and regulations may have effects on the capital market and the netasset value of the Fund.

Internal policy restricts the Fund from investing in securities issued by any issuer of not more than acertain percentage of its net asset value. Under such restriction, the risk exposure to the securities ofany single issuer is diversified and managed based on internal/external ratings.

The Fund maintains sufficient level of liquid assets, after consultation with the Trustee, to meetanticipated payments and cancellations of units by unitholders. Liquid assets comprise of deposits withlicensed financial institutions and other instruments, which are capable of being converted into cashwithin 5 to 7 days. The Fund’s policy is to always maintain a prudent level of liquid assets so as toreduce liquidity risk.

Liquidity risk is defined as the risk of being unable to raise funds or borrowings to meet paymentobligations as they fall due. This is also the risk of the Fund experiencing large redemptions, when theInvestment Manager could be forced to sell large volumes of its holdings at unfavourable prices tomeet redemption requirements.

35

AmIttikal

STATEMENT BY THE MANAGER

Kuala Lumpur, Malaysia

I, GOH WEE PENG, for and on behalf of the Manager, AmFunds Management Berhad, for

AmIttikal do hereby state that in the opinion of the Manager, the accompanying statement of

financial position, statement of comprehensive income, statement of changes in equity, statement of

cash flows and the accompanying notes are drawn up in accordance with Malaysian Financial

Reporting Standards and International Financial Reporting Standards so as to give a true and fair

view of the financial position of the Fund as at 30 September 2017 and the comprehensive income,

the changes in equity and cash flows of the Fund for the financial year then ended.

7 November 2017

GOH WEE PENGFor and on behalf of the ManagerAmFunds Management Berhad

36

37

TRUSTEE’S REPORT

38

MANAGER’S REPORT Dear Unitholders, We are pleased to present you the Manager’s report and the audited accounts of AmBon Islam (“Fund”) for the financial year ended 30 September 2017. Salient Information of the Fund Name AmBon Islam (“Fund”)

Category/ Type

Sukuk / Income

Objective AmBon Islam is a medium to long-term Sukuk fund that aims to provide a stream of halal income*. Note: *The income could be in the form of units or cash.

Duration The Fund was established on 26 November 2001 and shall exist for as long as it appears to the Manager and the Trustee that it is in the interests of the unitholders for it to continue. In some circumstances, the unitholders can resolve at a meeting to terminate AmBon Islam.

Performance Benchmark

BPAM Corporates (3 years to 7 years) Sukuk Index. (source: www.bpam.com.my/www.aminvest.com) Note: The risk profile of the Fund may not be the same as the risk profile of the performance benchmark.

Income Distribution Policy

Income distribution (if any) is paid at least twice every year.

Breakdown of Unit Holdings by Size

For the financial year under review, the size of the Fund stood at 36,501,065 units. Size of holding As at 30 September 2017 As at 30 September 2016

No of units held

Number of unitholders

No of units held

Number of unitholders

5,000 and below 109,913 52 185,677 89 5,001-10,000 34,205,919 10 862,283 46 10,001-50,000 658,354 32 2,183,365 22 50,001-500,000 199,961 28 27,128,276 11 500,001 and above 1,326,918 9 252,285 35

39

Fund Performance Data Portfolio Composition

Details of portfolio composition of the Fund for the financial years as at 30 September are as follows:

FY 2017 %

FY 2016 %

FY 2015 %

Corporate sukuk 95.95 89.88 66.32 Cash and others 4.05 10.12 33.68 Total 100.00 100.00 100.00

Note: The abovementioned percentages are calculated based on total net asset value.

Performance Details

Performance details of the Fund for the financial years ended 30 September are as follows: FY

2017 FY

2016 FY

2015 Net asset value (RM)* 46,019,117 38,093,654 40,072,623 Units in circulation* 36,501,065 30,611,886 32,794,231 Net asset value per unit (RM)* 1.2608 1.2444 1.2219 Highest net asset value per unit (RM)*

1.2609 1.2723 1.2518

Lowest net asset value per unit (RM)*

1.2305 1.2223 1.2185

Benchmark performance (%) 3.84 7.93 3.17 Total return (%)(1) 3.79 6.86 2.84 - Capital growth (%) 1.38 1.95 -0.81 - Income distribution (%) 2.41 4.91 3.65 Gross distribution (sen per unit) 3.00 6.00 4.50 Net distribution (sen per unit) 3.00 6.00 4.50 Management expense ratio (%)(2) 1.18 1.19 1.14 Portfolio turnover ratio (times)(3) 0.22 0.68 0.81

* Above price and net asset value per unit are shown as ex-distribution. Note: (1) Total return is the annualised return of the Fund for the respective financial

years computed based on the net asset value per unit and net of all fees. (2) Management expense ratio (“MER”) is calculated based on the total fees

and expenses incurred by the Fund divided by the average fund size calculated on a daily basis. The MER decreased by 0.01% as compared to 1.19% per annum for the financial year ended 30 September 2016 mainly due to increase in average fund size.

(3) Portfolio turnover ratio (“PTR”) is calculated based on the average of the total acquisitions and total disposals of investment securities of the Fund divided by the average fund size calculated on a daily basis. The PTR decreased by 0.46 times (67.6%) as compared to 0.68 times for the financial year ended 30 September 2016 mainly due to decrease in investing activities.

40

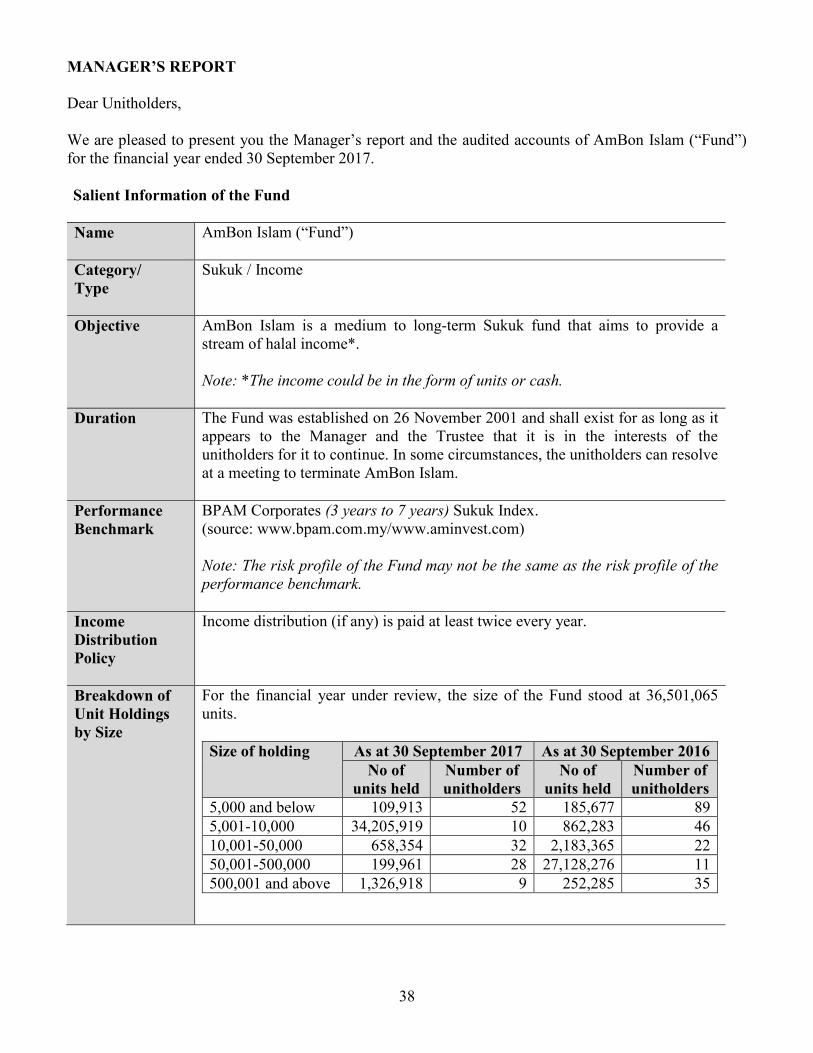

Average Total Return (as at 30 September 2017)

AmBon Islam(a)

%

BPAM 3Y – 7Y Sukuk

Index/MGII(b) %

One year 3.79 3.84 Three years 4.48 4.96 Five years 3.74 4.20 Ten years 4.43 4.63

Annual Total Return Financial Years Ended (30 September)

AmBon Islam(a)

%

BPAM 3Y – 7Y Sukuk

Index/MGII(b) %

2017 3.79 3.84 2016 6.86 7.93 2015 2.84 3.17 2014 3.28 3.43 2013 1.98 2.70

(a) Source: Novagni Analytics and Advisory Sdn Bhd. (b) Medium Government Investment Issues Index (“MGII”)

(Source: www.fundslogic.com). Performance benchmark has been changed to BPAM Corporates (3 years to 7 years) Sukuk Index with effect from 1 October 2016.

The Fund performance is calculated based on the net asset value per unit of the Fund. Average total return of the Fund and its benchmark for a period is computed on the absolute return for that period annualised over one year. Note: Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up.

Fund Performance

For the financial year under review, the Fund registered a return of 3.79% comprising of 1.38% capital growth and 2.41% income distribution. Thus, the Fund’s return of 3.79% has underperformed the benchmark’s return of 3.84% by 0.05%. As compared with the financial year ended 30 September 2016, the net asset value (“NAV”) per unit of the Fund increased by 1.32% from RM1.2444 to RM1.2608, while units in circulation decreased by 19.24% from 30,611,886 units to 36,501,065 units. The Line Chart below shows comparison between the annual performances of AmBon Islam and its benchmark, BPAM 3Y – 7Y Sukuk Index /MGII, for the

41

financial years ended 30 September.

Note: Past performance is not necessarily indicative of future performance and that unit prices and investment returns may go down, as well as up.