Embed Size (px)

Citation preview

American International Group IncAmerican International Group, Inc.Fourth Quarter 2011 Results

Conference Call PresentationConference Call Presentation

February 24, 2012

Cautionary Statement Regarding Projections and Cautionary Statement Regarding Projections and Other Information About Future EventsThis document and the remarks made within this presentation may include projections, goals, assumptions and statements that may constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. These projections, goals, assumptions and statements are not historical facts but instead represent only AIG’s belief p j , g , p p yregarding future events, many of which, by their nature, are inherently uncertain and outside AIG’s control. These projections, goals, assumptions and statements include statements preceded by, followed by or including words such as “believe”, “anticipate”, “expect”, “intend”, “plan”, “view”, “target”, or “estimate”. It is possible that AIG’s actual results and financial condition will differ, possibly materially, from the results and financial condition indicated in these projections, goals, assumptions and statements. Factors that could cause AIG’s actual results to differ, possibly materially, from those in the specific projections, goals, assumptions and statements include actions by credit rating agencies; changes in market p p j g p y g g gconditions; the occurrence of catastrophic events; significant legal proceedings; concentrations in AIG’s investment portfolios, including its municipal bond portfolio; judgments concerning casualty insurance underwriting and reserves; judgments concerning deferred policy acquisition costs recoverability; judgments concerning the recognition of deferred tax assets; judgments concerning the recoverability of aircraft values in ILFC’s fleet; and such other factors as discussed throughout Part I, Item 1A. Risk Factors and in Part II, Item 7. Management's Discussion and Analysis of Financial Condition and Results of Operations in AIG’s Annual Report on Form 10-K for the year ended December 31, 2011.

AIG is not under any obligation (and expressly disclaims any obligation) to update or alter any projections, goals, assumptions or other statements, whether written or oral, that may be made from time to time, whether as a result of new information, future events or otherwise. This document and the remarks made orally may also contain certain non-GAAP financial measures. The reconciliation of such measures to the most comparable GAAP measures in accordance with Regulation G is included in the Fourth Quarter 2011 Financial Supplement available in the Investor Information section of AIG's corporate website www aig comAIG s corporate website, www.aig.com .

IRS Circular 230 Disclosure: To ensure compliance with requirements imposed by the IRS, we inform you that (i) any U.S. tax advice contained in this communication (including any attachments) is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties under the Internal Revenue Code; (ii) any such tax advice is written in connection with the promotion or marketing of the matters addressed; and (iii) if you are not the original addressee of this communication, you should seek advice based on your particular circumstances from an independent advisor.

2

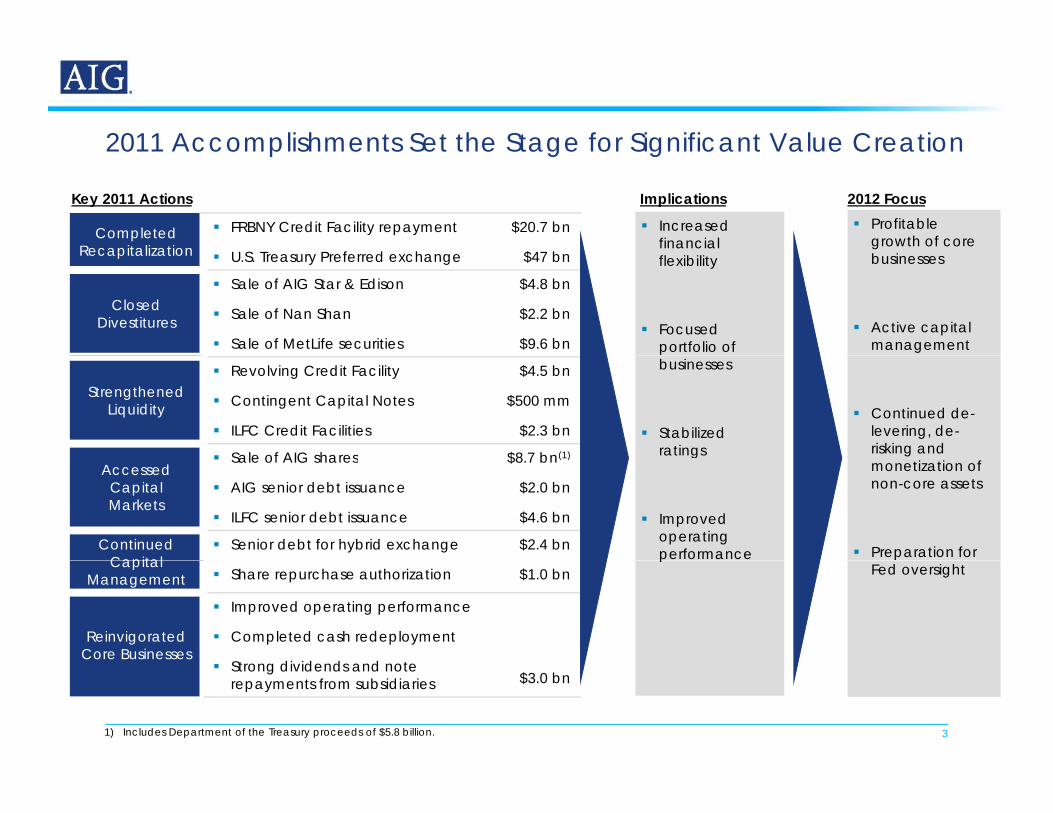

2011 Accomplishments Set the Stage for Significant Value Creation2011 Accomplishments Set the Stage for Significant Value Creation

Completed Recapitalization

FRBNY Credit Facility repayment

U S T P f d h

$20.7 bn

$47 b

Key 2011 Actions Profitable

growth of core i

2012 Focus

Increased financial

Implications

Recapitalization U.S. Treasury Preferred exchange $47 bn

Closed Divestitures

Sale of AIG Star & Edison

Sale of Nan Shan

Sale of MetLife securities

$4.8 bn

$2.2 bn

$9.6 bn

businesses

Active capital management

flexibility

Focused portfolio of

Strengthened Liquidity

Revolving Credit Facility

Contingent Capital Notes

ILFC Credit Facilities

$4.5 bn

$500 mm

$2.3 bn

Sale of AIG shares $8 7 bn(1)

Continued de-levering, de-risking and

businesses

Stabilized ratings

Accessed Capital Markets

Sale of AIG shares

AIG senior debt issuance

ILFC senior debt issuance

$8.7 bn(1)

$2.0 bn

$4.6 bn

Continued Capital

Senior debt for hybrid exchange $2.4 bn

monetization of non-core assets

Preparation for

g

Improved operating performanceCapital

Management Share repurchase authorization $1.0 bn

Reinvigorated Core Businesses

Improved operating performance

Completed cash redeployment

St di id d d t

Fed oversightp

3

Strong dividends and note repayments from subsidiaries $3.0 bn

1) Includes Department of the Treasury proceeds of $5.8 billion.

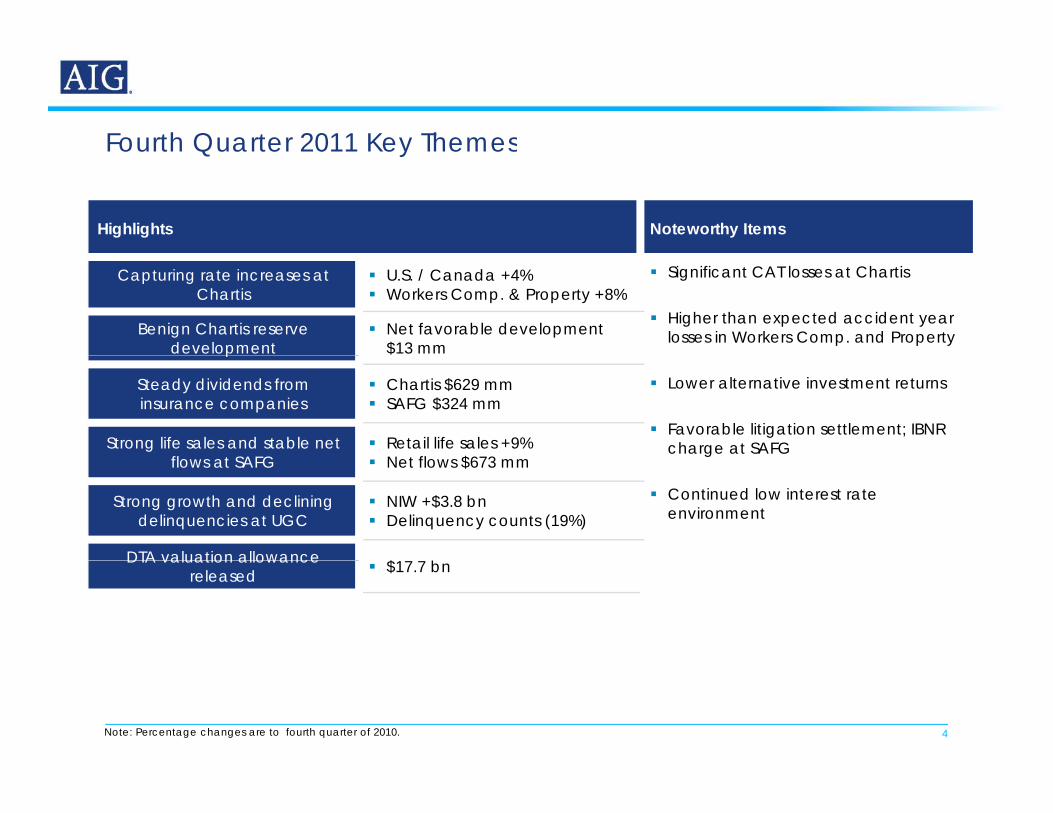

Fourth Quarter 2011 Key ThemesFourth Quarter 2011 Key Themes

Highlights Noteworthy Items

Capturing rate increases at Chartis

U.S. / Canada +4% Workers Comp. & Property +8%

Significant CAT losses at Chartis

Higher than expected accident year losses in Workers Comp. and PropertyBenign Chartis reserve

development Net favorable development

$13 mm

Lower alternative investment returns

Favorable litigation settlement; IBNR charge at SAFG

p $

Steady dividends from insurance companies

Chartis $629 mm SAFG $324 mm

Strong life sales and stable net fl t SAFG

Retail life sales +9%N t fl $673

Continued low interest rate environment

flows at SAFG Net flows $673 mm

Strong growth and declining delinquencies at UGC

NIW +$3.8 bn Delinquency counts (19%)

DTA valuation allowance $ bDTA valuation allowance released $17.7 bn

4Note: Percentage changes are to fourth quarter of 2010.

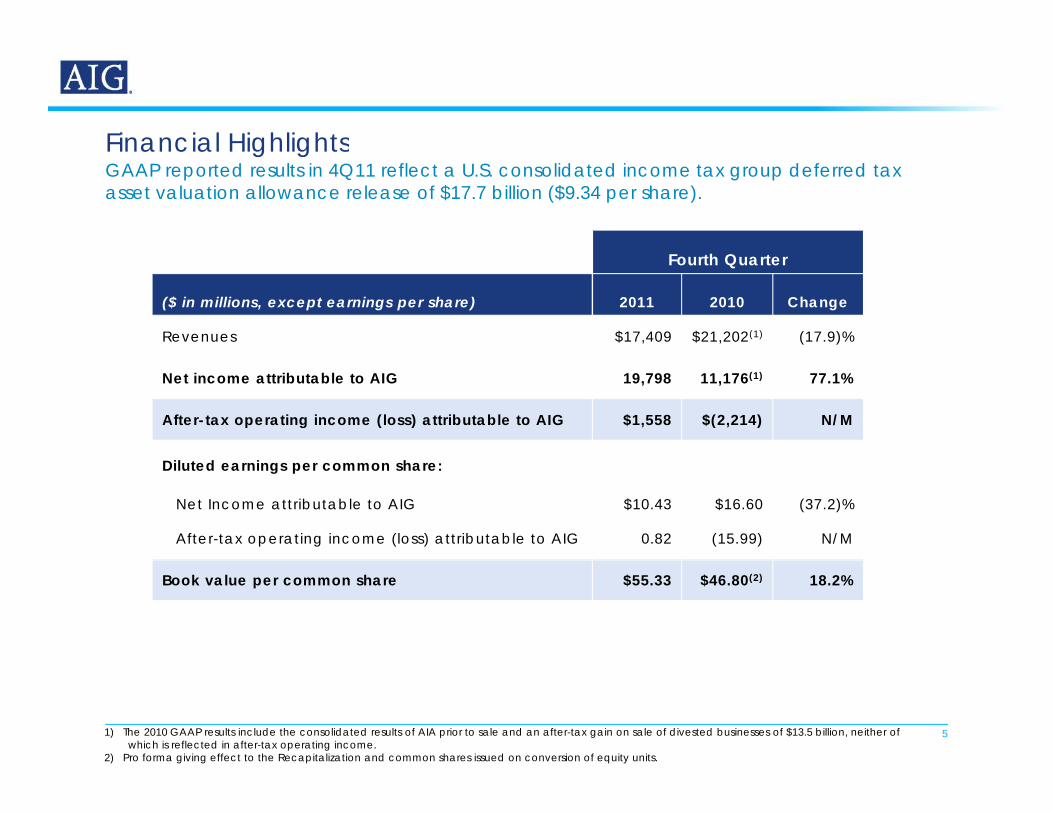

Financial HighlightsFinancial HighlightsGAAP reported results in 4Q11 reflect a U.S. consolidated income tax group deferred tax asset valuation allowance release of $17.7 billion ($9.34 per share).

Fourth Quarter

($ in millions, except earnings per share) 2011 2010 Change

Revenues $17,409 $21,202(1) (17.9)%

Net income attributable to AIG 19,798 11,176(1) 77.1%

After-tax operating income (loss) attributable to AIG $1,558 $(2,214) N/M

Diluted earnings per common share:

Net Income attributable to AIG $10.43 $16.60 (37.2)%

After-tax operating income (loss) attributable to AIG 0.82 (15.99) N/M

Book value per common share $55.33 $46.80(2) 18.2%

51) The 2010 GAAP results include the consolidated results of AIA prior to sale and an after-tax gain on sale of divested businesses of $13.5 billion, neither of which is reflected in after-tax operating income.

2) Pro forma giving effect to the Recapitalization and common shares issued on conversion of equity units.

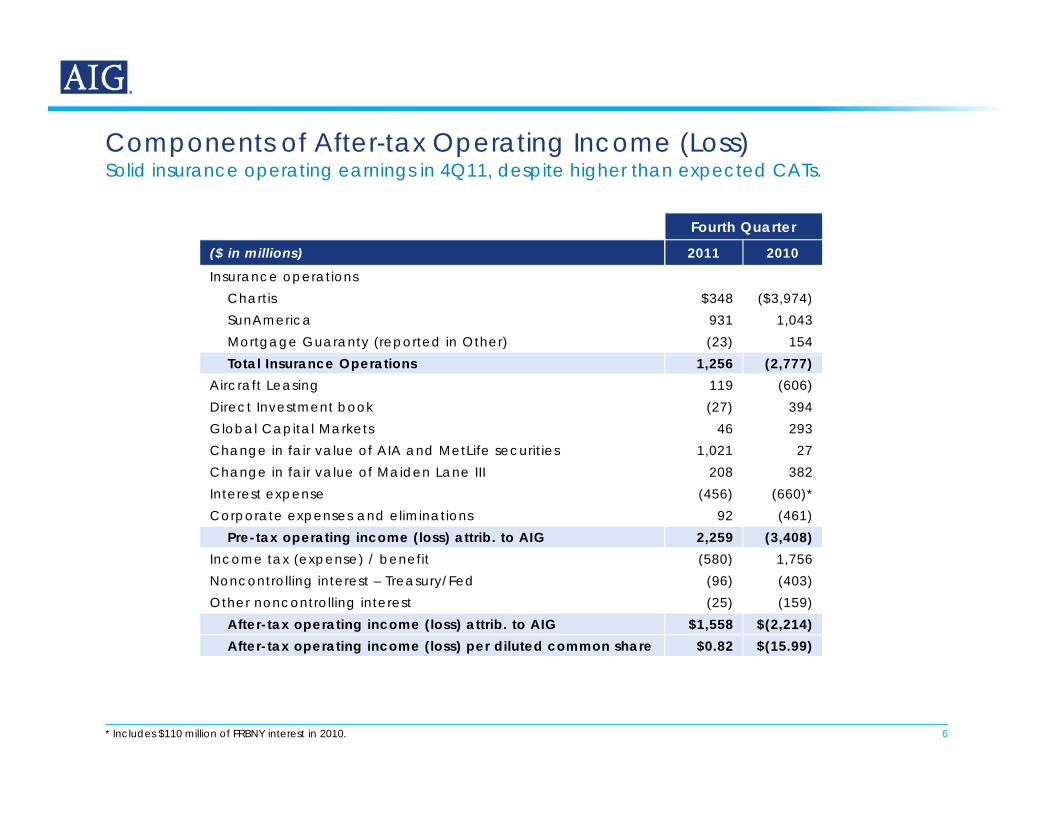

Components of After-tax Operating Income (Loss)Solid insurance operating earnings in 4Q11, despite higher than expected CATs.Components of After tax Operating Income (Loss)

Fourth Quarter

($ in millions) 2011 2010($ in millions) 2011 2010Insurance operations

Chartis $348 ($3,974)SunAmerica 931 1,043Mortgage Guaranty (reported in Other) (23) 154Total Insurance Operations 1,256 (2,777)

Aircraft Leasing 119 (606)Direct Investment book (27) 394Global Capital Markets 46 293Change in fair value of AIA and MetLife securities 1,021 27Change in fair value of Maiden Lane III 208 382Interest expense (456) (660)*Corporate expenses and eliminations 92 (461)

Pre-tax operating income (loss) attrib. to AIG 2,259 (3,408)Income tax (expense) / benefit (580) 1 756Income tax (expense) / benefit (580) 1,756Noncontrolling interest – Treasury/Fed (96) (403)Other noncontrolling interest (25) (159)

After-tax operating income (loss) attrib. to AIG $1,558 $(2,214)After-tax operating income (loss) per diluted common share $0.82 $(15.99)

6* Includes $110 million of FRBNY interest in 2010.

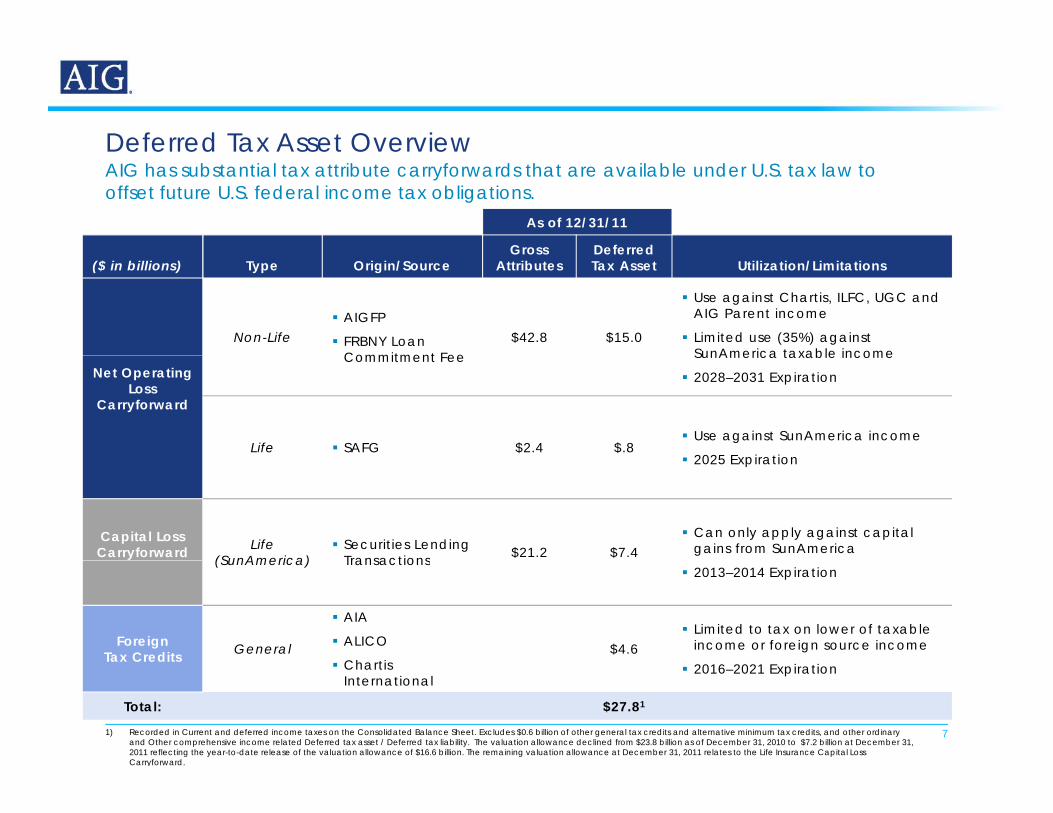

Deferred Tax Asset OverviewAIG has substantial tax attribute carryforwards that are available under U.S. tax law to offset future U.S. federal income tax obligations.

Deferred Tax Asset Overview

As of 12/31/11

Gross Deferred ($ in billions) Type Origin/Source

Gross Attributes

Deferred Tax Asset Utilization/Limitations

Non-Life AIGFP

FRBNY Loan Commitment Fee

$42.8 $15.0

Use against Chartis, ILFC, UGC and AIG Parent income

Limited use (35%) against SunAmerica taxable income

Net Operating Loss

Carryforward

Commitment Fee SunAmerica taxable income

2028–2031 Expiration

Life SAFG $2.4 $.8 Use against SunAmerica income

2025 Expiration 2025 Expiration

Capital LossCarryforward Life

(SunAmerica) Securities Lending

Transactions $21.2 $7.4 Can only apply against capital

gains from SunAmerica(SunAmerica) Transactions

2013–2014 Expiration

Foreign Tax Credits General

AIA

ALICO

Chartis $4.6

Limited to tax on lower of taxable income or foreign source income

71) Recorded in Current and deferred income taxes on the Consolidated Balance Sheet. Excludes $0.6 billion of other general tax credits and alternative minimum tax credits, and other ordinary and Other comprehensive income related Deferred tax asset / Deferred tax liability. The valuation allowance declined from $23.8 billion as of December 31, 2010 to $7.2 billion at December 31, 2011 reflecting the year-to-date release of the valuation allowance of $16.6 billion. The remaining valuation allowance at December 31, 2011 relates to the Life Insurance Capital Loss Carryforward.

Chartis International

2016–2021 Expiration

Total: $27.81

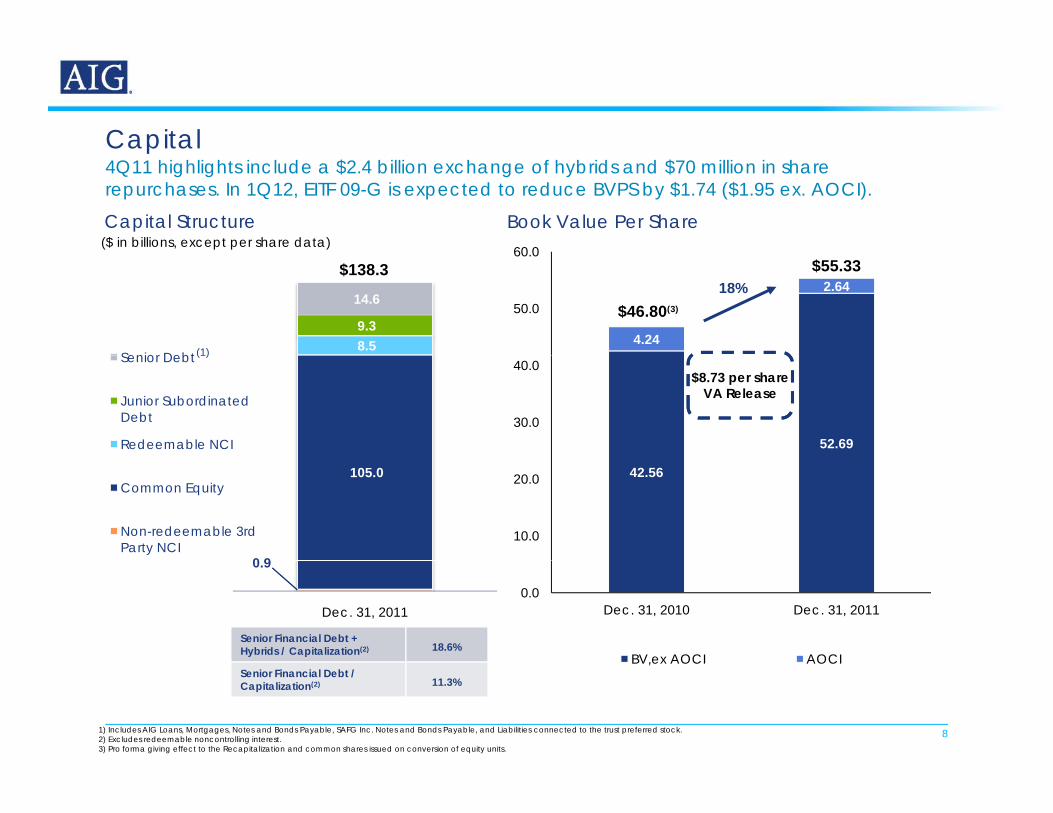

Capital

60 0

Book Value Per Share

p4Q11 highlights include a $2.4 billion exchange of hybrids and $70 million in share repurchases. In 1Q12, EITF 09-G is expected to reduce BVPS by $1.74 ($1.95 ex. AOCI).

Capital Structure($ in billions, except per share data)

4.24

2.6450.0

60.0$55.33

$46.80(3)

18%

8.5 9.3

14.6

Senior Debt

$138.3

(1)

52.6930.0

40.0Senior Debt

Junior Subordinated Debt

Redeemable NCI

(1)

$8.73 per shareVA Release

42.56

10.0

20.0

0 9

105.0 Common Equity

Non-redeemable 3rd Party NCI

0.0Dec. 31, 2010 Dec. 31, 2011

BV,ex AOCI AOCI

0.9

Dec. 31, 2011

Senior Financial Debt +Hybrids / Capitalization(2) 18.6%

8

BV,ex AOCI AOCI

1) Includes AIG Loans, Mortgages, Notes and Bonds Payable, SAFG Inc. Notes and Bonds Payable, and Liabilities connected to the trust preferred stock.2) Excludes redeemable noncontrolling interest. 3) Pro forma giving effect to the Recapitalization and common shares issued on conversion of equity units.

Senior Financial Debt / Capitalization(2) 11.3%

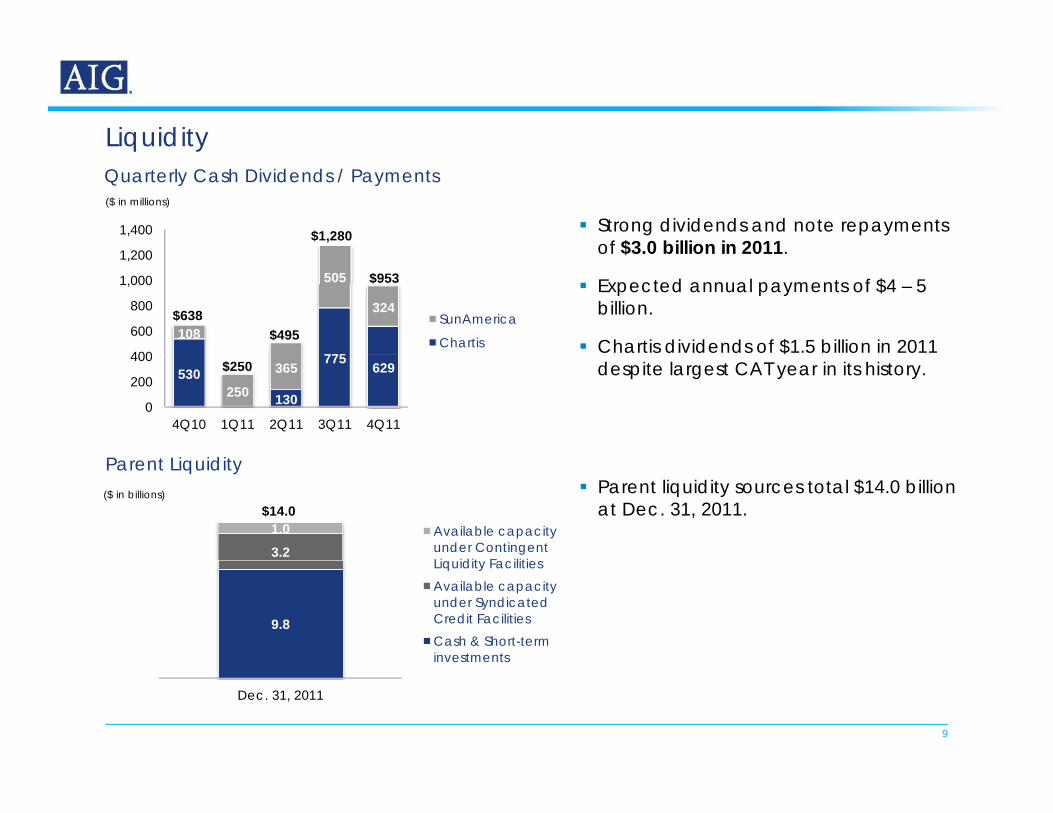

Liquidityq yQuarterly Cash Dividends / Payments

1 200

1,400

($ in millions)

$1,280 Strong dividends and note repayments of $3.0 billion in 2011.

775

108

505

324

400

600

800

1,000

1,200

SunAmerica

Chartis$495

$953

of $3.0 billion in 2011.

Expected annual payments of $4 – 5 billion.

Chartis dividends of $1.5 billion in 2011

$638

P t Li idit

530

130

775 629

250365

0

200

400

4Q10 1Q11 2Q11 3Q11 4Q11

$250$

despite largest CAT year in its history.

Parent liquidity sources total $14.0 billion at Dec. 31, 2011.

Parent Liquidity

3.21.0 Available capacity

under Contingent Li idit F iliti

($ in billions)$14.0

9.8

Liquidity FacilitiesAvailable capacity under Syndicated Credit FacilitiesCash & Short-term investments

9

Dec. 31, 2011

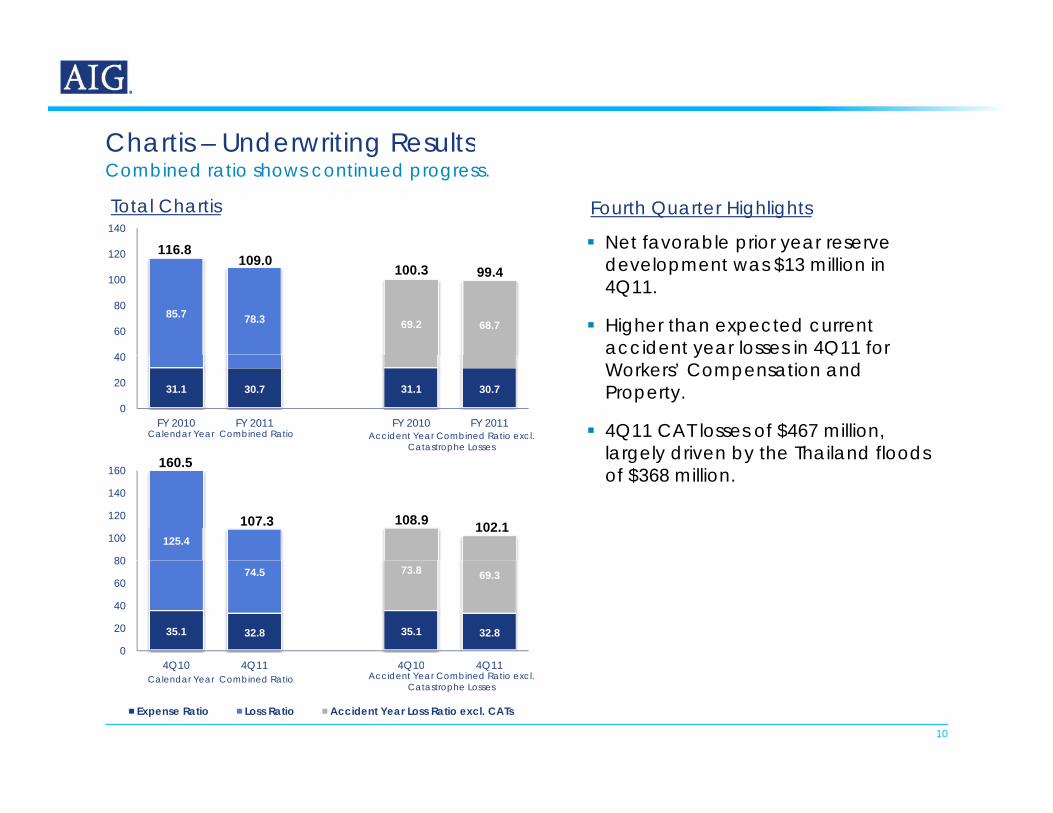

Chartis – Underwriting Results

120

140

Chartis Underwriting Results

Net favorable prior year reserve

Total Chartis

Combined ratio shows continued progress.

116.8

Fourth Quarter Highlights

85.7 78.3 69.2 68.7

40

60

80

100

120development was $13 million in 4Q11.

Higher than expected current accident year losses in 4Q11 for

116.8109.0

100.3 99.4

31.1 30.7 31.1 30.7

0

20

40

FY 2010 FY 2011 FY 2010 FY 2011

160 5

yWorkers’ Compensation and Property.

4Q11 CAT losses of $467 million, largely driven by the Thailand floods

Accident Year Combined Ratio excl.Catastrophe Losses

Calendar Year Combined Ratio

125.4

80

100

120

140

160 160.5

107.3 108.9 102.1

largely driven by the Thailand floods of $368 million.

35.1 32.8 35.1 32.8

74.5 73.8 69.3

0

20

40

60

80

4Q10 4Q11 4Q10 4Q11

10

4Q10 4Q11 4Q10 4Q11

Expense Ratio Loss Ratio Accident Year Loss Ratio excl. CATs

Calendar Year Combined Ratio Accident Year Combined Ratio excl.Catastrophe Losses

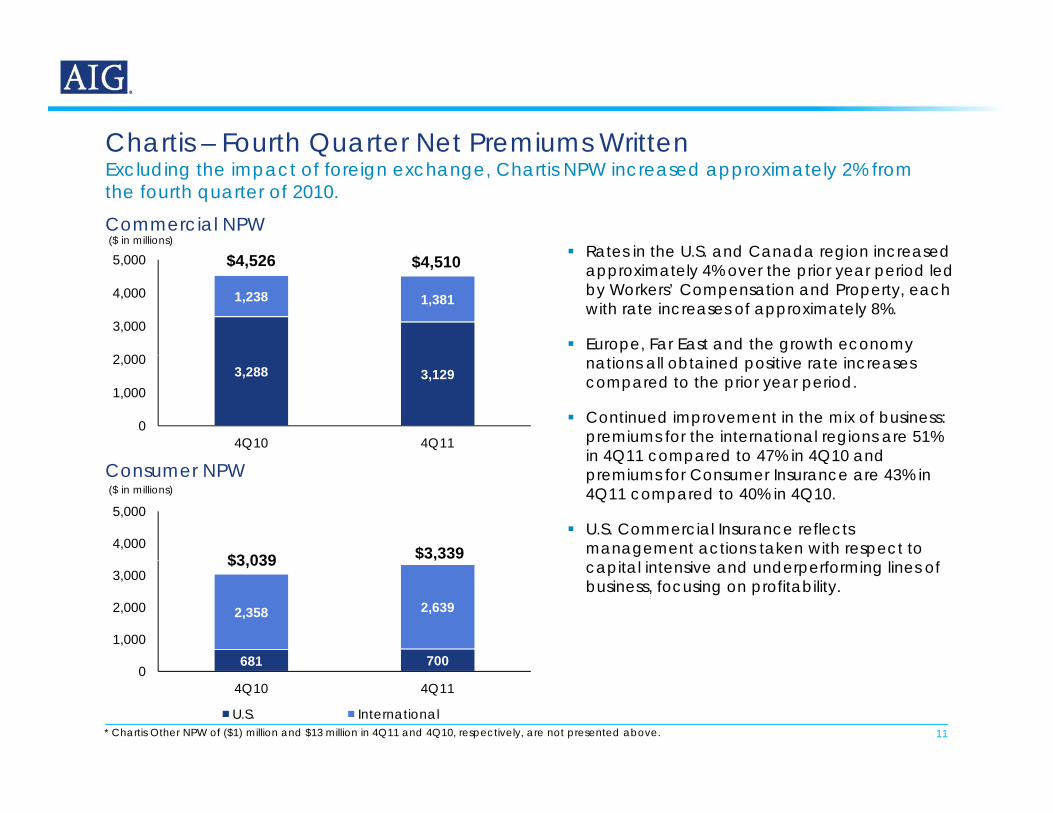

Chartis – Fourth Quarter Net Premiums Written

($ in millions)Commercial NPW

Rates in the U S and Canada region increased

Chartis Fourth Quarter Net Premiums WrittenExcluding the impact of foreign exchange, Chartis NPW increased approximately 2% from the fourth quarter of 2010.

1,238 1,381

2 000

3,000

4,000

5,000 $4,510$4,526 Rates in the U.S. and Canada region increased approximately 4% over the prior year period led by Workers’ Compensation and Property, each with rate increases of approximately 8%.

Europe, Far East and the growth economy 3,288 3,129

0

1,000

2,000

4Q10 4Q11

nations all obtained positive rate increases compared to the prior year period.

Continued improvement in the mix of business: premiums for the international regions are 51% in 4Q11 compared to 47% in 4Q10 and

4,000

5,000($ in millions)Consumer NPW

$3,339$3 039

in 4Q11 compared to 47% in 4Q10 and premiums for Consumer Insurance are 43% in 4Q11 compared to 40% in 4Q10.

U.S. Commercial Insurance reflects management actions taken with respect to

681 700

2,358 2,639

1,000

2,000

3,000$$3,039 capital intensive and underperforming lines of

business, focusing on profitability.

11

681 7000

4Q10 4Q11

U.S. International* Chartis Other NPW of ($1) million and $13 million in 4Q11 and 4Q10, respectively, are not presented above.

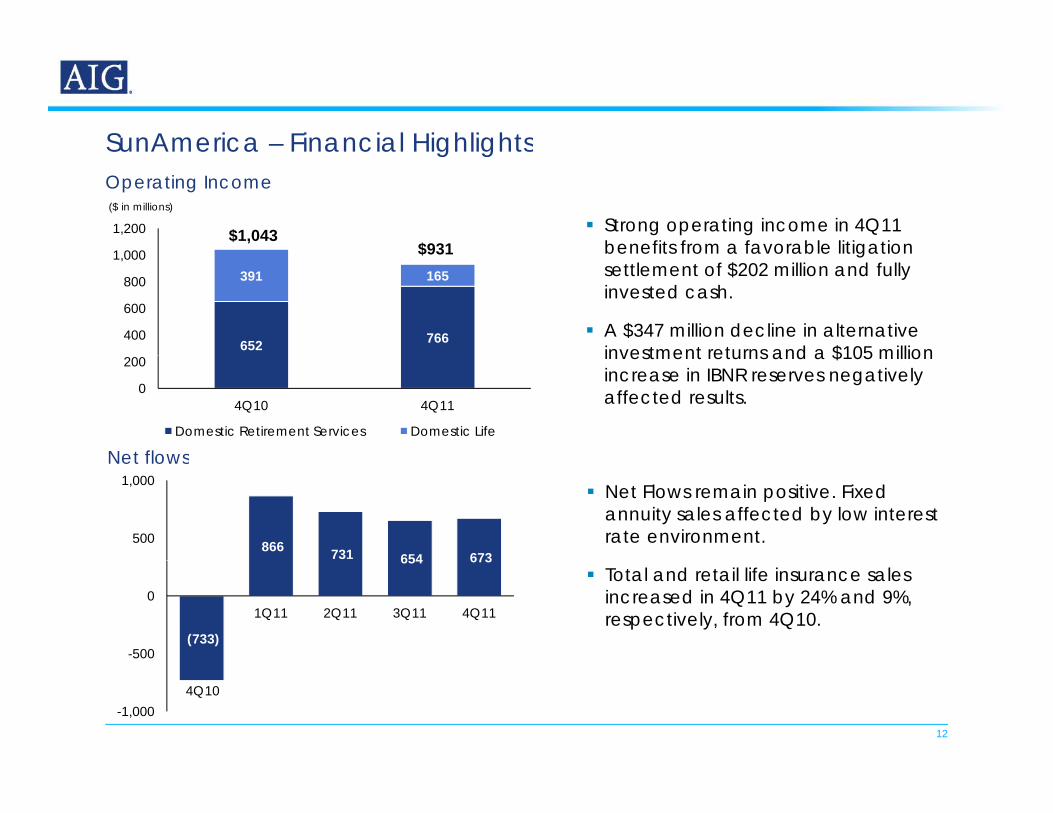

SunAmerica – Financial Highlights

1 000

1,200($ in millions)

Operating Income

$931$1,043 Strong operating income in 4Q11

benefits from a favorable litigation

SunAmerica Financial Highlights

652 766

391 165

400

600

800

1,000 $931 benefits from a favorable litigation settlement of $202 million and fully invested cash.

A $347 million decline in alternative investment returns and a $105 million

0

200

4Q10 4Q11

Domestic Retirement Services Domestic Life

investment returns and a $105 million increase in IBNR reserves negatively affected results.

Net flowsNet flows

866 731 654 673 500

1,000 Net Flows remain positive. Fixed

annuity sales affected by low interest rate environment.

(733)

654 673

-500

01Q11 2Q11 3Q11 4Q11

Total and retail life insurance sales increased in 4Q11 by 24% and 9%, respectively, from 4Q10.

12

-1,0004Q10

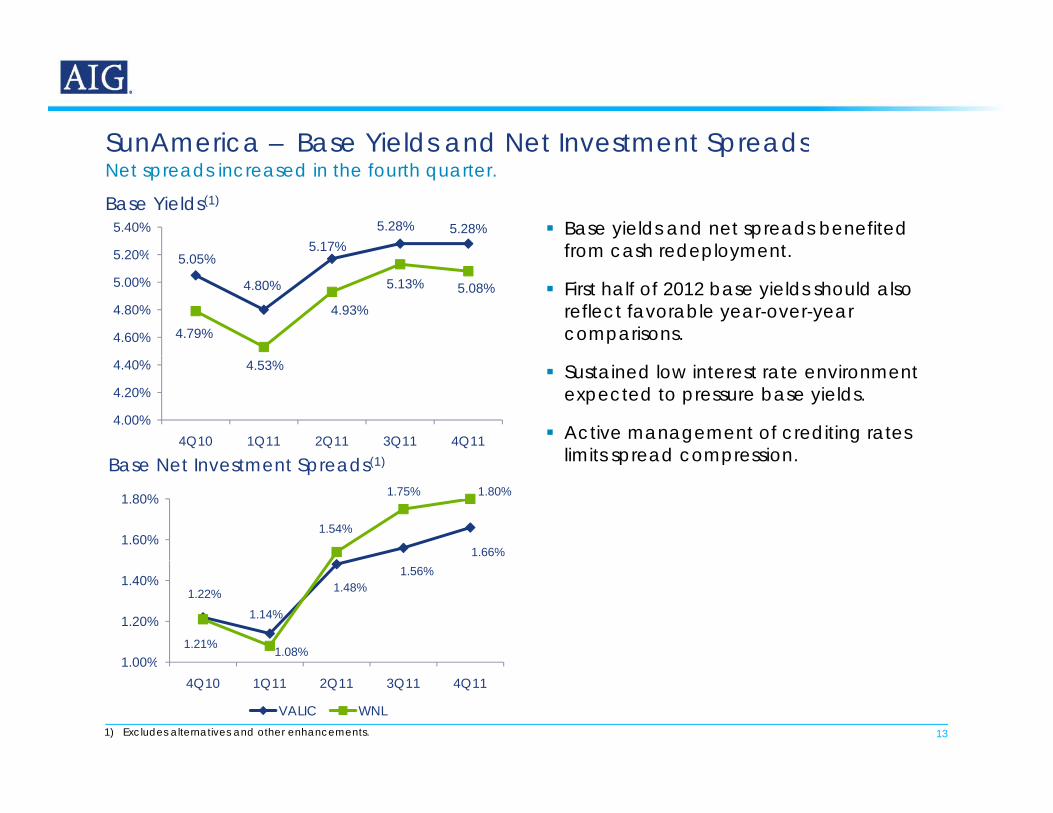

SunAmerica – Base Yields and Net Investment Spreads

Base yields and net spreads benefited from cash redeployment

Net spreads increased in the fourth quarter.SunAmerica Base Yields and Net Investment Spreads

5.17%5.28% 5.28%

5 20%

5.40%Base Yields(1)

from cash redeployment.

First half of 2012 base yields should also reflect favorable year-over-year comparisons.

5.05%

4.80%

4.79%

4.93%

5.13% 5.08%

4.60%

4.80%

5.00%

5.20%

Sustained low interest rate environment expected to pressure base yields.

Active management of crediting rates limits spread compression

4.53%

4.00%

4.20%

4.40%

4Q10 1Q11 2Q11 3Q11 4Q11

B N t I t t S d (1) limits spread compression.

1.66%

1.54%

1.75% 1.80%

1.60%

1.80%

Base Net Investment Spreads(1)

1.22%1.14%

1.48%1.56%

1.21% 1.08%1 00%

1.20%

1.40%

13

1.00%4Q10 1Q11 2Q11 3Q11 4Q11

VALIC WNL1) Excludes alternatives and other enhancements.

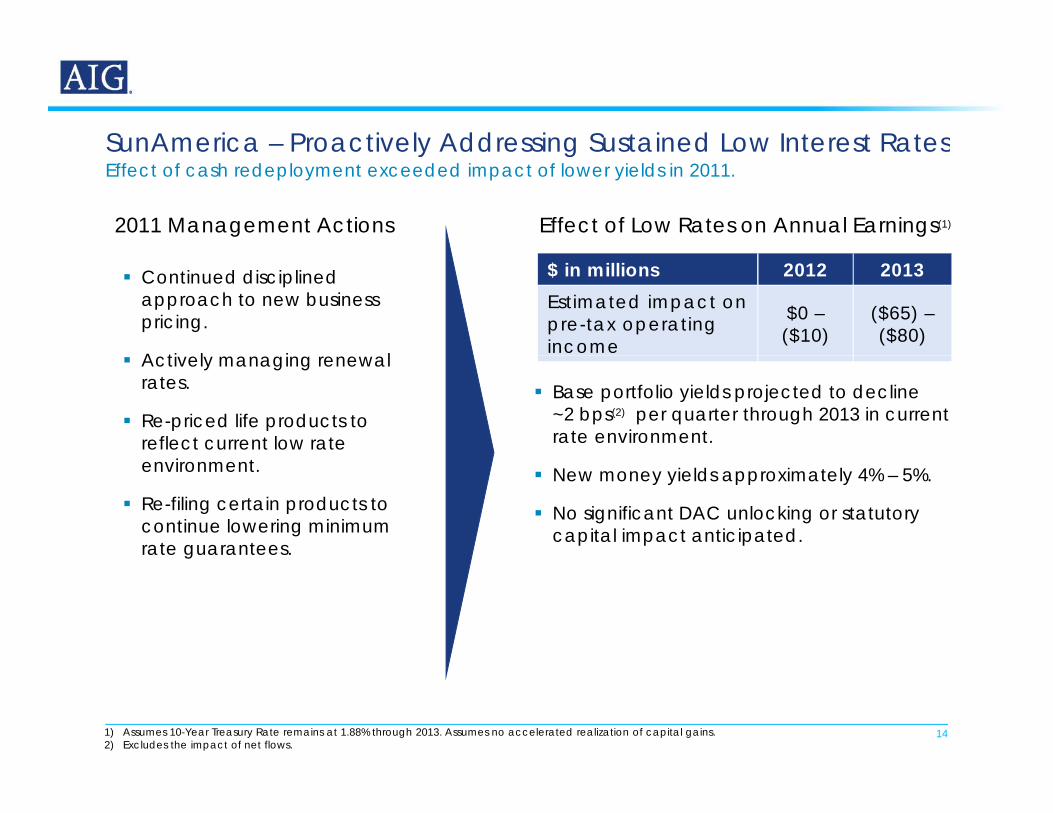

SunAmerica – Proactively Addressing Sustained Low Interest RatesEffect of cash redeployment exceeded impact of lower yields in 2011.SunAmerica Proactively Addressing Sustained Low Interest Rates

Effect of Low Rates on Annual Earnings(1)2011 Management Actions

$ in millions 2012 2013Estimated impact on pre-tax operating income

$0 –($10)

($65) –($80)

Continued disciplined approach to new business pricing.

A ti l i l Base portfolio yields projected to decline

~2 bps(2) per quarter through 2013 in current rate environment.

Actively managing renewal rates.

Re-priced life products to reflect current low rate

i New money yields approximately 4% – 5%.

No significant DAC unlocking or statutory capital impact anticipated.

environment.

Re-filing certain products to continue lowering minimum rate guarantees.

141) Assumes 10-Year Treasury Rate remains at 1.88% through 2013. Assumes no accelerated realization of capital gains.2) Excludes the impact of net flows.

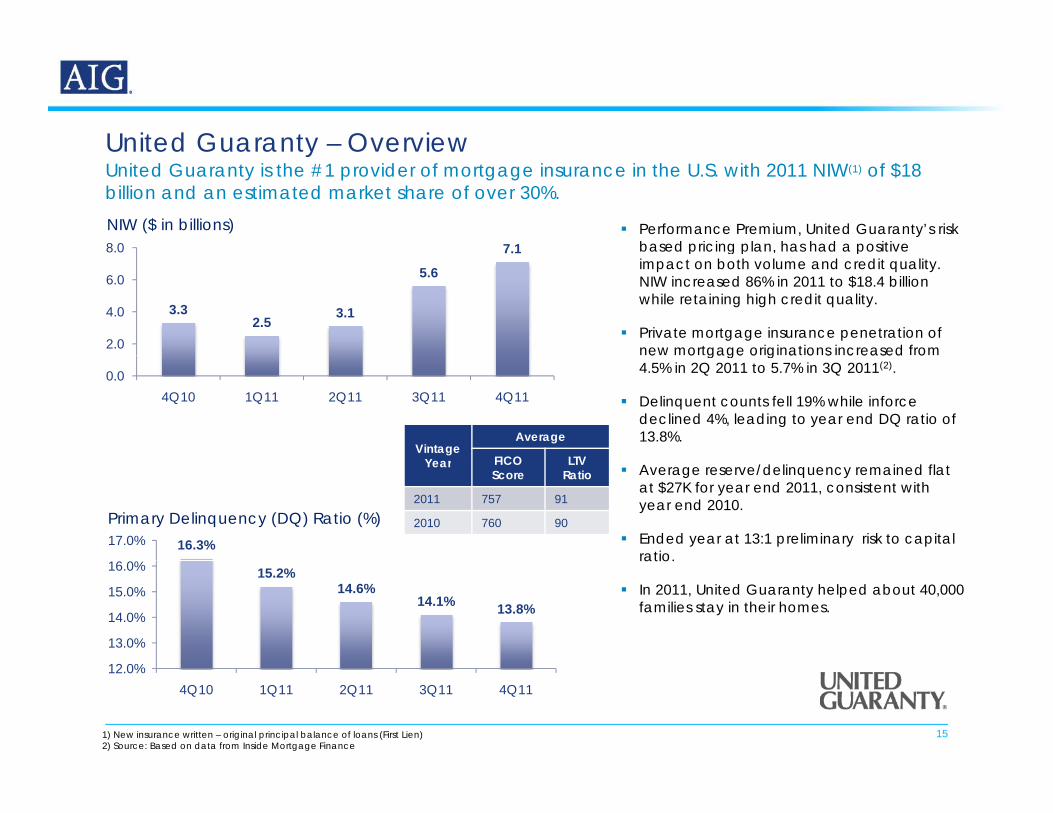

United Guaranty – OverviewUnited Guaranty OverviewUnited Guaranty is the #1 provider of mortgage insurance in the U.S. with 2011 NIW(1) of $18 billion and an estimated market share of over 30%.NIW ($ in billions)

7.18.0 Performance Premium, United Guaranty’s risk

based pricing plan, has had a positive

3.32.5

3.1

5.6

7.1

2.0

4.0

6.0

p g p pimpact on both volume and credit quality. NIW increased 86% in 2011 to $18.4 billion while retaining high credit quality.

Private mortgage insurance penetration of new mortgage originations increased from

VintageAverage

FICO LTV

0.04Q10 1Q11 2Q11 3Q11 4Q11

e o gage o g a o s c eased o 4.5% in 2Q 2011 to 5.7% in 3Q 2011(2).

Delinquent counts fell 19% while inforcedeclined 4%, leading to year end DQ ratio of 13.8%.

Year FICOScore

LTVRatio

2011 757 91

2010 760 90

16.3%17.0%Primary Delinquency (DQ) Ratio (%)

Average reserve/delinquency remained flat at $27K for year end 2011, consistent with year end 2010.

Ended year at 13:1 preliminary risk to capital ratio.

15.2%14.6%

14.1% 13.8%

13.0%

14.0%

15.0%

16.0%ratio.

In 2011, United Guaranty helped about 40,000 families stay in their homes.

151) New insurance written – original principal balance of loans (First Lien)2) Source: Based on data from Inside Mortgage Finance

12.0%4Q10 1Q11 2Q11 3Q11 4Q11

Appendix

16

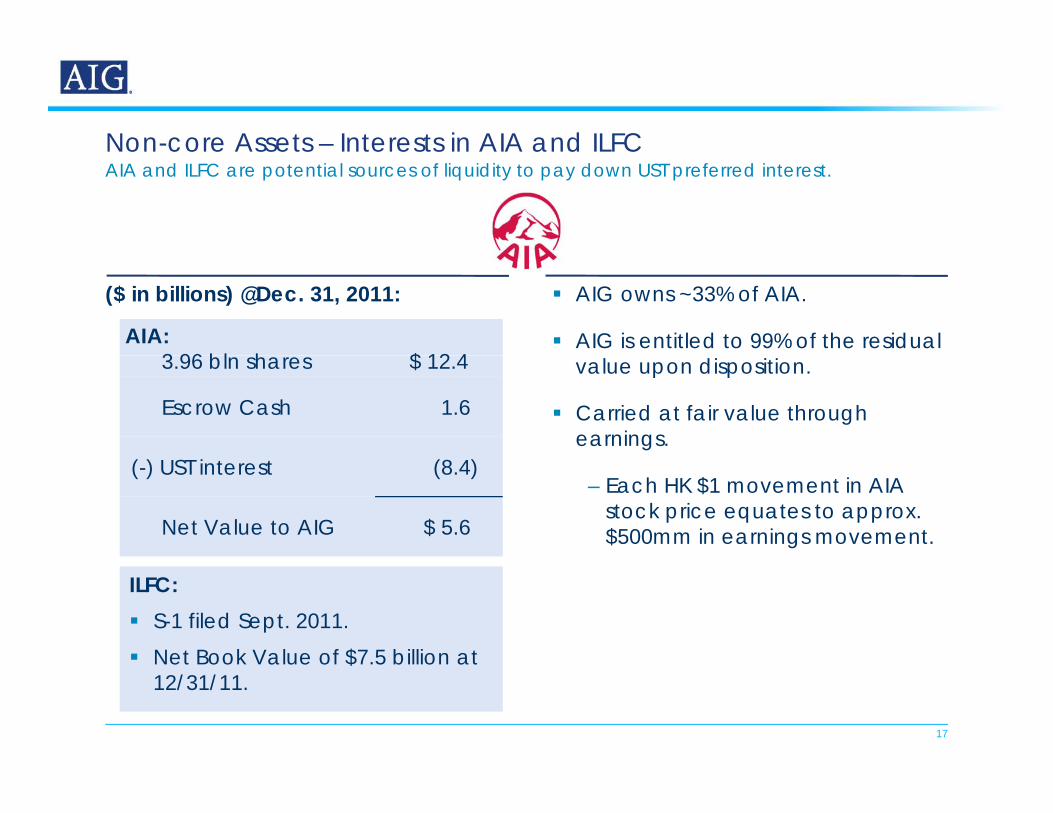

Non-core Assets – Interests in AIA and ILFCAIA and ILFC are potential sources of liquidity to pay down UST preferred interest.Non core Assets Interests in AIA and ILFC

AIG owns ~33% of AIA.

AIG is entitled to 99% of the residual

($ in billions) @Dec. 31, 2011:

AIA:3 96 bl h $ 12 4 value upon disposition.

Carried at fair value through earnings.

3.96 bln shares $ 12.4

Escrow Cash 1.6

– Each HK $1 movement in AIA stock price equates to approx. $500mm in earnings movement.

(-) UST interest (8.4)

Net Value to AIG $ 5.6

ILFC: S-1 filed Sept. 2011. Net Book Value of $7.5 billion at

17

Net Book Value of $7.5 billion at 12/31/11.

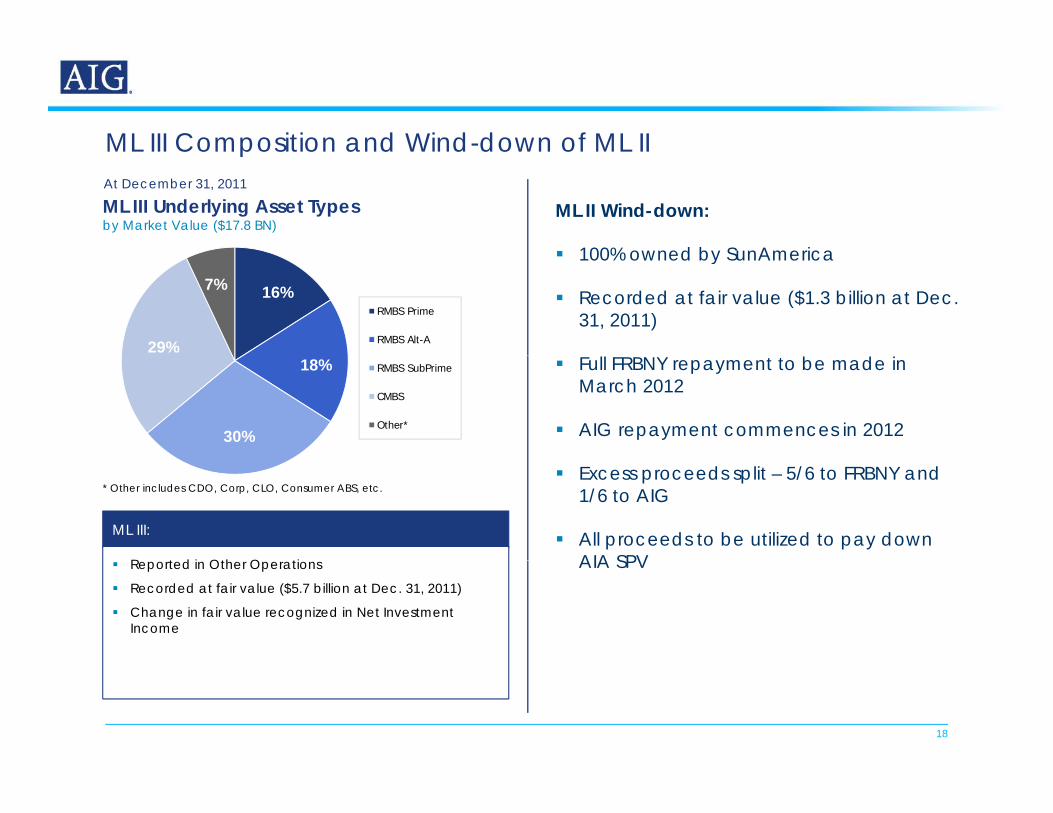

ML III Composition and Wind-down of ML IIML III Composition and Wind down of ML II

ML III Underlying Asset Types by Market Value ($17.8 BN)

At December 31, 2011

ML II Wind-down:

100% owned by SunAmerica

16%

29%

7%RMBS Prime

RMBS Alt-A

100% owned by SunAmerica

Recorded at fair value ($1.3 billion at Dec. 31, 2011)

18%

30%

RMBS SubPrime

CMBS

Other*

Full FRBNY repayment to be made in March 2012

AIG repayment commences in 2012

ML III:

R t d i Oth O ti

* Other includes CDO, Corp, CLO, Consumer ABS, etc. Excess proceeds split – 5/6 to FRBNY and

1/6 to AIG

All proceeds to be utilized to pay down AIA SPV Reported in Other Operations

Recorded at fair value ($5.7 billion at Dec. 31, 2011)

Change in fair value recognized in Net Investment Income

AIA SPV

18

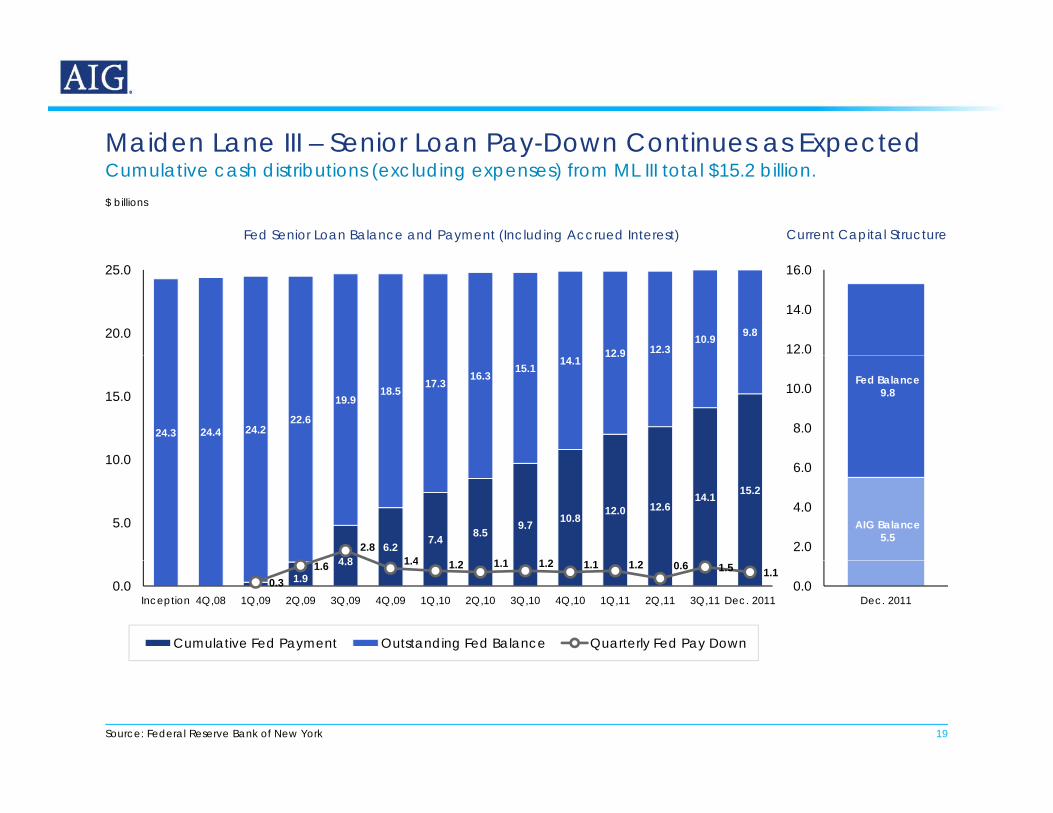

Maiden Lane III – Senior Loan Pay-Down Continues as ExpectedCumulative cash distributions (excluding expenses) from ML III total $15.2 billion.Maiden Lane III Senior Loan Pay Down Continues as Expected

$ billions

Current Capital StructureFed Senior Loan Balance and Payment (Including Accrued Interest)

12.9 12.310.9 9.820.0

25.0

12.0

14.0

16.0

24.3 24.4 24.222.6

19.918.5 17.3 16.3 15.1 14.1 12.9

10 0

15.0

8.0

10.0Fed Balance

9.8

4 86.2 7.4 8.5 9.7 10.8 12.0 12.6

14.1 15.2

2.81 4 2 1 1 1 2 2

5.0

10.0

2.0

4.0

6.0

AIG Balance5.5

1.94.8

0.31.6 1.4 1.2 1.1 1.2 1.1 1.2 0.6 1.5 1.1

0.0Inception 4Q,08 1Q,09 2Q,09 3Q,09 4Q,09 1Q,10 2Q,10 3Q,10 4Q,10 1Q,11 2Q,11 3Q,11 Dec. 2011

Cumulative Fed Payment Outstanding Fed Balance Quarterly Fed Pay Down

0.0Dec. 2011

19Source: Federal Reserve Bank of New York

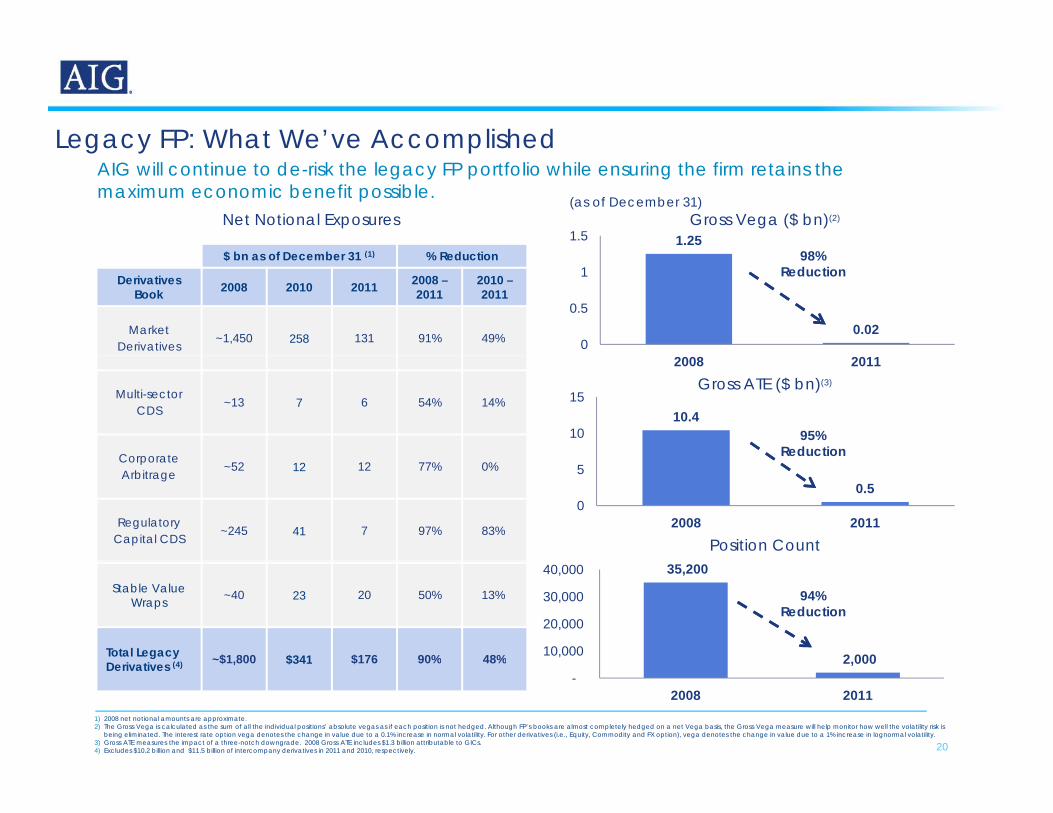

Legacy FP: What We’ve Accomplishedg y p

(1)

$ b f D b 31 (1) % R d ti

AIG will continue to de-risk the legacy FP portfolio while ensuring the firm retains the maximum economic benefit possible.

Net Notional Exposures1.251.5

98%

Gross Vega ($ bn)(2)(as of December 31)

$ bn as of December 31 (1) % Reduction

Derivatives Book 2008 2010 2011 2008 –

20112010 –2011

Market Derivatives

~1,450 258 131 91% 49%0.02

0

0.5

198%

Reduction

Multi-sector CDS

~13 7 6 54% 14%

Corporate

2008 2011

10.410

15

95% Reduction

Gross ATE ($ bn)(3)

Corporate Arbitrage

~52 12 12 77% 0%

Regulatory Capital CDS

~245 41 7 97% 83%

0.50

5

2008 2011Position Count

Stable Value Wraps ~40 23 20 50% 13%

Total Legacy D i ti (4) ~$1,800 $341 $176 90% 48%

35,200

2,000 10,000

20,000

30,000

40,000

94% Reduction

20

Derivatives (4) $1,800 $341 $176 90% 48%

1) 2008 net notional amounts are approximate. 2) The Gross Vega is calculated as the sum of all the individual positions’ absolute vegas as if each position is not hedged. Although FP’s books are almost completely hedged on a net Vega basis, the Gross Vega measure will help monitor how well the volatility risk is

being eliminated. The interest rate option vega denotes the change in value due to a 0.1% increase in normal volatility. For other derivatives (i.e., Equity, Commodity and FX option), vega denotes the change in value due to a 1% increase in lognormal volatility. 3) Gross ATE measures the impact of a three-notch downgrade. 2008 Gross ATE includes $1.3 billion attributable to GICs. 4) Excludes $10.2 billion and $11.5 billion of intercompany derivatives in 2011 and 2010, respectively.

2,000 -

2008 2011

20

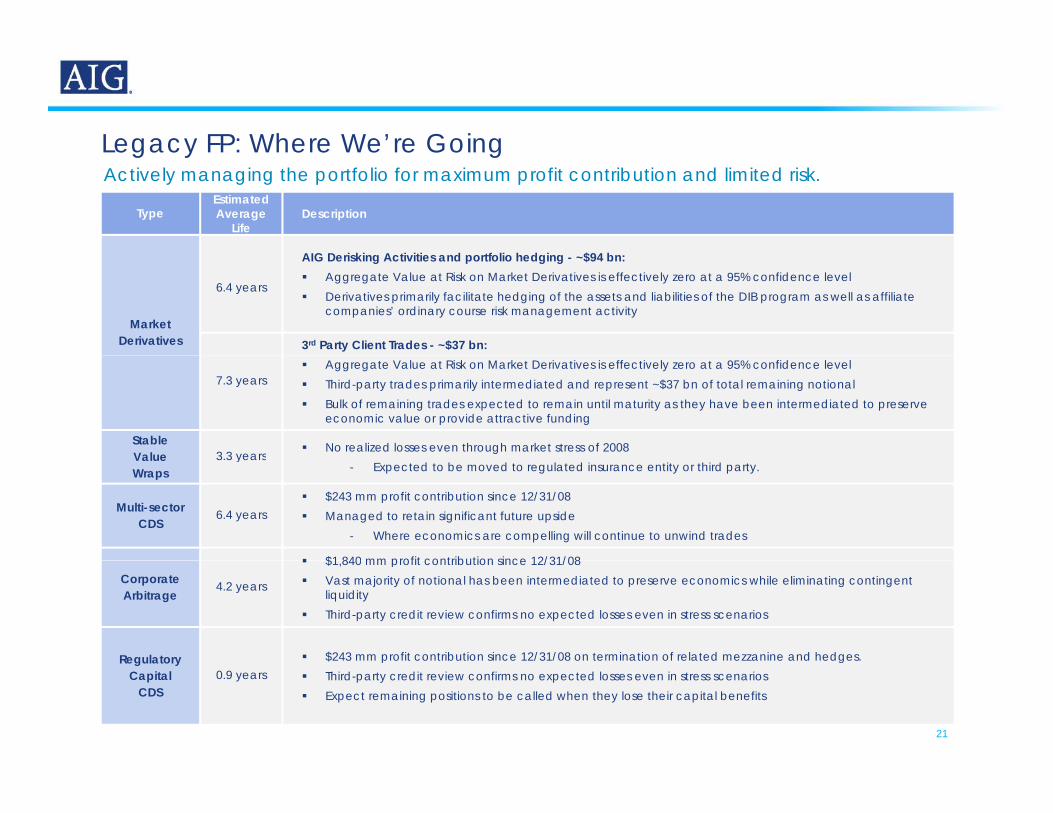

Legacy FP: Where We’re Going

(1)TypeEstimatedAverage

LifeDescription

AIG D i ki A ti iti d tf li h d i $94 b

Legacy FP: Where We re GoingActively managing the portfolio for maximum profit contribution and limited risk.

Market Derivatives

6.4 years

AIG Derisking Activities and portfolio hedging - ~$94 bn: Aggregate Value at Risk on Market Derivatives is effectively zero at a 95% confidence level Derivatives primarily facilitate hedging of the assets and liabilities of the DIB program as well as affiliate

companies’ ordinary course risk management activity

3rd Party Client Trades - ~$37 bn:

7.3 years Aggregate Value at Risk on Market Derivatives is effectively zero at a 95% confidence level Third-party trades primarily intermediated and represent ~$37 bn of total remaining notional Bulk of remaining trades expected to remain until maturity as they have been intermediated to preserve

economic value or provide attractive funding

StableValue 3 3 years

No realized losses even through market stress of 2008ValueWraps

3.3 years- Expected to be moved to regulated insurance entity or third party.

Multi-sector CDS

6.4 years $243 mm profit contribution since 12/31/08 Managed to retain significant future upside

- Where economics are compelling will continue to unwind trades

$1 840 mm profit contribution since 12/31/08Corporate Arbitrage

4.2 years

$1,840 mm profit contribution since 12/31/08 Vast majority of notional has been intermediated to preserve economics while eliminating contingent

liquidity Third-party credit review confirms no expected losses even in stress scenarios

Regulatory $243 mm profit contribution since 12/31/08 on termination of related mezzanine and hedges.

21

Regulatory Capital

CDS0.9 years Third-party credit review confirms no expected losses even in stress scenarios

Expect remaining positions to be called when they lose their capital benefits