Embed Size (px)

Citation preview

Strategic Management JournalStrat. Mgmt. J., 35: 1903–1929 (2014)

Published online EarlyView 21 November 2013 in Wiley Online Library (wileyonlinelibrary.com) DOI: 10.1002/smj.2195

Received 2 March 2012 ; Final revision received 18 September 2013

AMBIDEXTERITY UNDER SCRUTINY: EXPLORATIONAND EXPLOITATION VIA INTERNAL ORGANIZATION,ALLIANCES, AND ACQUISITIONS

URIEL STETTNER1 and DOVEV LAVIE2*1 Faculty of Management, Recanati Business School, Tel Aviv University, Tel Aviv,Israel2 Faculty of Industrial Engineering and Management, Technion—Israel Institute ofTechnology, Haifa, Israel

Prior research on ambidexterity has limited its concern to balancing exploration and exploitationvia particular modes of operation. Acknowledging the interplay of tendencies to explore versusexploit via the internal organization, alliance, and acquisition modes, we claim that balancingthese tendencies within each mode undermines firm performance because of conflicting routines,negative transfer, and limited specialization. Nevertheless, by exploring in one mode andexploiting in another, i.e., balancing across modes, a firm can avoid some of these impediments.Thus, we advance ambidexterity research by asserting that balance across modes enhancesperformance more than balance within modes. Our analysis of 190 U.S.-based software firmsfurther reveals that exploring via externally oriented modes such as acquisitions or alliances,while exploiting via internal organization, enhances these firms’ performance. Copyright ©2013 John Wiley & Sons, Ltd.

INTRODUCTION

The existing exploration-exploitation paradigmhas received much attention in managementresearch. Exploration involves developing newknowledge whereas exploitation refers to refin-ing knowledge (Levinthal and March, 1993).Exploration and exploitation entail distinct skills,so firms often debate whether to support oneactivity at the expense of the other. March (1991)conjectured that a balanced approach of pursuingboth activities, i.e., ambidexterity, is essential forperformance. Whereas most studies reveal positive

Keywords: exploration and exploitation; internal organi-zation; alliance; acquisition; firm performance; softwareindustry*Correspondence to: Dovev Lavie, Faculty of Industrial Engi-neering and Management, Technion—Israel Institute of Tech-nology, Technion, Haifa 32000, Israel. E-mail: [email protected]

Copyright © 2013 John Wiley & Sons, Ltd.

performance effects of balance (He and Wong,2004; Jansen, Van den Bosch, and Volberda, 2006;Lin, Yang, and Demirkan, 2007; Sidhu, Comman-deur, and Volberda, 2007), some find insignificant(Venkatraman, Lee, and Iyer, 2007) or negativeeffects (Lavie, Kang, and Rosenkopf, 2011). Theseinconsistencies can be ascribed, in part, to therestricted focus of prior research on explorationand exploitation via particular modes of operation,such as internal organization, alliances, or acqui-sitions, while disregarding the tendency to simul-taneously explore and exploit via multiple modes.

Scholars have debated the means by whichfirms strive for balance (Lavie, Stettner, and Tush-man, 2010). Some suggest that a firm can bal-ance exploration and exploitation within a singleorganizational unit by nurturing discipline, sup-port, and trust (Gibson and Birkinshaw, 2004),yet most scholars call for separating explo-ration from exploitation. One approach involves

1904 U. Stettner and D. Lavie

temporal separation by which a firm managestransitions between exploration and exploitationover time (Eisenhardt and Brown, 1997). Anotherapproach involves simultaneous exploration andexploitation by means of organizational separa-tion (Benner and Tushman, 2003), which enables afirm to maintain distinct activities while engagingin internally consistent tasks within separate orga-nizational units dedicated to either exploration orexploitation (O’Reilly and Tushman, 2008; Smithand Tushman, 2005). A third approach suggeststhat firms can separate exploration from exploita-tion across distinct domains, e.g., engaging inupstream activities of the value chain via recurrentalliances with the same partners, thus combiningstructural exploitation with functional exploration(Lavie and Rosenkopf, 2006).

Common to all aforementioned approaches istheir narrow application within a single modeof operation. Although some studies focus onexploring and exploiting via alliances (e.g., Lavieet al., 2011) or acquisitions (Hayward, 2002),the majority focus on the internal organizationof these activities (e.g., He and Wong, 2004;Jansen et al., 2006; Sidhu et al., 2007; Tushmanand O’Reilly, 1996). In so doing, they disregardthe firm’s tendencies to simultaneously exploreand exploit via alternative modes of operation.This leaves open questions: To what extent dothe benefits of exploring via alliances vary withthe tendency to explore via internal organiza-tion or acquisitions? Will a firm be better offexploring via acquisitions while exploiting via itsinternal organization, or vice versa? Answeringsuch questions is vital for identifying the desir-able approach for gaining from balance. Sincefirms engage simultaneously in internal organiza-tion, alliances, and acquisitions, restricting one’sconcern to a particular mode precludes accurateassessment of the balance between exploration andexploitation.

Some recent studies have begun juxtaposingalliances and internal organization (Hess andRothaermel, 2011; Hoang and Rothaermel, 2010;Rothaermel and Alexandre, 2009; Russo andVurro, 2010) but have not focused on the impli-cations of balancing exploration and exploitationwithin versus across these modes of operation.For instance, Russo and Vurro (2010) study theinterdependence between internal exploration andexternal exploration via alliances, yet they neitherexamine the performance effects of balance within

either mode, nor do they compare them to thoseof balance across these modes. Rothaermel andAlexandre (2009) consider internal and externalsources of technology in the internal organiza-tion mode, but don’t study these activities in othermodes. We extend Hoang and Rothaermel’s (2010)study by shifting focus from the project level to thefirm level and by considering the current configu-ration of exploration and exploitation as opposedto prior experience with these activities. Moreover,we extend Hess and Rothaermel’s (2011) work,which shows how downstream alliances comple-ment the contribution of star scientists, by account-ing also for acquisitions and explaining how thefirm can benefit from exploring externally whileexploiting internally.

We contribute to research on ambidexterity bystudying the interplay of a firm’s exploration andexploitation activities across distinct modes, thusaccounting for various means by which the firmbalances these activities. We depart from priorresearch that underscored the benefits of balancewithin the internal organization, alliance, or acqui-sition modes by positing that conflicting organi-zational routines, negative transfer, and limitedability to specialize undermine these benefits. Inturn, we suggest that firms can benefit by balancingexploration and exploitation across these modes.Furthermore, we contribute by identifying the mostbeneficial mode for pursuing exploration versusexploitation, yet our primary contribution is touncover the merits of exploring in one mode whileexploiting in another, as opposed to pursuing bothactivities within particular modes. Finally, whereasprior research has focused on the internal organi-zation of exploration, we suggest that firms thatexplore via an externally oriented mode such asacquisitions or alliances while exploiting internallycan improve their performance. We find supportfor our conjectures using a comprehensive datasetcovering all product introductions, alliances, andacquisitions of 190 prepackaged software firmsfrom 1990 to 2001. Hence, our study promotesa new approach for balancing exploration andexploitation.

THEORY AND HYPOTHESES

Exploration and exploitation can be pursued viainternal organization (e.g., He and Wong, 2004;Jansen et al., 2006; Sidhu et al., 2007; Tushman

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1905

and O’Reilly, 1996), alliances (e.g., Lavie andRosenkopf, 2006), or acquisitions (Hayward,2002). These are considered alternative modes ofoperation in the strategy literature (Dyer, Kale,and Singh, 2004; Hagedoorn and Wang, 2012;Harzing, 2002; Weilei and Prescott, 2012). Inparticular, given our focus on knowledge-basedexploration and exploitation, acquisitions thatincorporate external knowledge are distinctfrom the internal organization, which enablesthe firm to develop and leverage its internalknowledge, and differ from alliances that com-bine internal and external knowledge (Dyerand Singh, 1998). Knowledge spillovers acrossmodes may occur over time, but our focus is onthe immediate implications of exploration andexploitation rather than on subsequent knowledgetransfer.1

To fully understand the performance implica-tions of balancing exploration and exploitation, weconsider the various modes via which a firm pur-sues these activities. We assume that the tendencyto explore versus exploit is not inherently relatedto the choice of mode, which can serve for bothexploration and exploitation. Specifically, in theinternal organization mode, the firm can rely onits newly developed knowledge in order to offeroriginal products (exploration) as well as lever-age its existing knowledge in order to refine itsexisting products (exploitation) (Cao, Gedajlovic,and Zhang, 2009; Danneels, 2002; Danneels andSethi, 2011; Greve, 2007; He and Wong, 2004;Jansen et al., 2006; Voss, Sirdeshmukh, and Voss,2008). Introducing new products that are distinctfrom previous product generations entails technol-ogy development and innovation, which are con-sistent with Levinthal and March’s (1993) notionof exploration. In turn, versions of existing prod-ucts that represent mere improvements using thefirm’s existing technologies or competencies cor-respond to their notion of exploitation. In thealliance mode, a firm can develop and access newknowledge by collaborating with alliance part-ners in upstream activities of the value chain(exploration) as well as commercialize and mar-ket products based on its existing knowledge when

1 One may consider additional modes of operation and alter-native domains via which a firm can pursue exploration andexploitation. Although our theory can apply to different modes,we focus on the primary modes identified in the literature. Inauxiliary analyses, we demonstrate that our conclusions remainvalid in various domains.

jointly pursing downstream activities with alliancepartners (exploitation) (Koza and Lewin, 1998;Lavie and Rosenkopf, 2006; Park, Chen, and Gal-lagher, 2002; Rothaermel, 2001; Rothaermel andDeeds, 2004). Finally, in the acquisition mode,the firm can extend its knowledge base by tak-ing ownership of another firm with a remotelyrelated business (exploration) as well as leverageits established knowledge by acquiring a firm witha closely related business (exploitation) (Ahuja andKatila, 2001; Anand and Singh, 1997; Haleblianand Finkelstein, 1999; Seth, 1990; Vermeulen andBarkema, 2001). We expect a firm’s performanceto vary with the configuration of exploration andexploitation within and across the internal organi-zation, alliance, and acquisition modes. Because ofthe distinct natures of exploration and exploitation,firms often fail to a priori assess their net bene-fits, which is even more challenging when simul-taneously exploring and exploiting in multiplemodes.

Balancing exploration and exploitation withinmodes

Prior research has underscored the complemen-tary benefits of exploration and exploitation (Heand Wong, 2004; Hess and Rothaermel, 2011;Lin et al., 2007), with less regard to the impedi-ments associated with their balance. This researchhas suggested that generating new knowledgeenables a firm to avoid obsolescence and remaincompetitive, whereas leveraging existing knowl-edge is essential for gaining efficiency and secur-ing the firm’s market position (March, 1991).Accordingly, a firm that engages in both explo-ration and exploitation is expected to maintainboth productivity and innovation, achieving reli-ability while enabling organizational renewal andthus enjoying enhanced performance. Neverthe-less, organizational challenges have been observedwhen balancing exploration and exploitation viainternal organization (Abernathy, 1978; Bennerand Tushman, 2003) and may manifest in othermodes as well. While acknowledging the meritsof balance within particular modes, we seek touncover some impediments associated with the useof conflicting routines, negative transfer, and lim-ited specialization, which can offset the benefits ofbalance.

Exploration and exploitation are fundamen-tally different activities that rely on distinctive

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1906 U. Stettner and D. Lavie

organizational routines (Dosi, Nelson, andWinter, 2000). Routines associated with exploita-tion leverage the firm’s existing knowledge, thusfacilitating consistency, stability, and control (Ben-ner and Tushman, 2003). In contrast, explorationroutines involve a search for new knowledge,thus facilitating experimentation, flexibility, andrisk taking (McGrath, 2001). A firm that balancesexploration and exploitation within a modesimultaneously relies on both types of routines,which induces organizational tension, complexity,and coordination challenges that can undermineperformance (Benner and Tushman, 2003). Forinstance, in the internal organization mode, a firmthat exploits by refining its existing knowledgerelies on routines for local search that can enhancethe efficiency of product development. In contrast,exploration routines are designed for boundaryspanning, experimentation with emerging tech-nologies, and discovery of novel product features(Sidhu et al., 2007). Employing both routinessimultaneously impairs product development,since the firm’s expertise with established knowl-edge conflicts with practices for discovering newknowledge. Similarly, in the alliance mode, explo-ration routines enable the firm to seek, assess,and incorporate its partners’ knowledge, whereasexploitation routines involve integrating, applying,and fine-tuning the firm’s own knowledge (Lavieet al., 2011). In each mode, a firm that pursuesboth exploration and exploitation cannot followpersistent patterns of behavior that are essentialfor effective use of its routines. The inconsistencybetween exploration and exploitation routines islikely to persist because of the self-reinforcingnature of these activities (Levinthal and March,1993). The success and failure traps suggestthat exploitation routines drive out exploration,whereas risky exploration leads to further changesand search for new knowledge. As a result, thefirm would face difficulties in furnishing resourcesto both activities and supporting an intermediateposition on the exploration-exploitation continuum(Simsek et al., 2009).

Moreover, a firm that balances explorationand exploitation within a mode may misapplyknowledge or practices that are suitable for oneactivity when performing the other, thus encoun-tering negative learning effects (Novick, 1988;O’Grady and Lane, 1996). Misapplication ofknowledge can occur when managers overlooksubtle yet critical differences between activities.

For example, in the acquisition mode, a firmthat explores by acquiring businesses beyond itsindustry boundaries can learn how to assess unfa-miliar knowledge under uncertainty and informa-tion asymmetry. Once acquired, these businessesoften require loose coordination, since the firmlacks expertise in unrelated knowledge domains(Datta, 1991). In contrast, a firm that exploitsby acquiring closely related businesses relies onits familiarity with these businesses and leveragesits established industry knowledge to proactivelyintegrate the acquired firms’ assets (Puranam,Singh, and Chaudhuri, 2009). Thus, a firm thatengages simultaneously in both types of acquisi-tions is unlikely to nurture consistent acquisitionpractices and may experience negative learningeffects when applying practices that were learnedin acquisitions of related businesses in its acquisi-tions of remotely related businesses (Haleblian andFinkelstein, 1999).

In addition, a firm that balances explorationand exploitation within a particular mode for-goes the benefits of specialization. It relin-quishes some of its ability to develop special-ized resources and foster core competencies inexploration or exploitation (Madhok, 1997). Thedistinctive natures of exploration and exploitationconstrain the resources that can be allocated toeither activity. These resources cannot be mobi-lized across activities, i.e., restored from one activ-ity and redeployed to the other (Anand and Singh,1997; Mishina, Pollock, and Porac, 2004). Forexample, in the internal organization mode, per-sonnel dedicated to refining existing technologiesmay not be qualified to experiment with new tech-nologies (Lepak and Snell, 1999). Consequently, afirm that simultaneously invests in developing newknowledge and refining its existing knowledgemay be unable to share development costs acrossproduct lines. Similarly, in the acquisition mode,a firm that simultaneously explores and exploitsby acquiring firms with various degrees of busi-ness relatedness undermines its ability to developspecialized skills for engaging in distinct types ofacquisitions. Inability to gain expertise in targetselection and due diligence can hinder the firm’sability to identify acquisition targets and gener-ate synergies (Haleblian and Finkelstein, 1999).Thus, by simultaneously exploring and exploitingin a certain mode, the firm may fail to gain scaleand scope economies otherwise attainable whenconcentrating on either exploration or exploitation

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1907

in that mode.2 For example, in 2005 Delta Air-lines decided to discontinue its innovative low-fare service, which was added to its efficient fullservice in 2003. This “Delta Song” service suf-fered from Delta’s cost structure and its inabil-ity to make independent pricing and schedulingdecisions:

‘Delta’s chief operating officer, James M.Whitehurst, said the cost of running the mainDelta brand and maintaining Song was veryexpensive. Delta’s chief marketing officer,Paul G. Matsen, added that the airline hadto be careful not to overlap the operationsof Delta and Song, especially in cities likeNew York and Los Angeles, which wereserved by both airlines. Beyond the expenseof supporting two brands, Delta faced acompelling need to add the Song planes to itsmain fleet. With Song going away, Delta canuse its Boeing 757’s on those routes. And,with the former Song planes being outfittedwith 26 first class seats apiece, Delta can

2 A firm may apply managerial techniques to cope with thechallenges of balance within modes. For instance, it may relyon separate organizational units exclusively dedicated to eitherexploration or exploitation (Tushman and O’Reilly, 1996). Suchambidextrous structure enables the firm to pursue consistentroutines in each unit and supports specialization. Nevertheless,it creates operational redundancy and integration challengesfor the top management team (Jansen et al., 2008; Mom, Vanden Bosch, and Volberda, 2007; Smith and Tushman, 2005).It calls for tight coordination and monitoring (Gibson andBirkinshaw, 2004) that may lead to failure because of managers’cognitive constraints (Gupta, Smith, and Shalley, 2006; O’Reillyand Tushman, 2008). Thus, even when conflicting routinesare avoided and specialization is maintained, the firm mayface organizational challenges and forego some economies ofscale and scope. Furthermore, organizational separation withinthe internal organization mode is not typical of small andyoung firms (Lubatkin et al., 2006; Tushman and O’Reilly,1996). In the alliance mode, a firm may institute a dedicatedalliance function that does not separate the managing ofupstream alliances from that of downstream alliances (Dyer,Kale, and Singh, 2001; Schreiner, Kale, and Corsten, 2009).Similarly, in the acquisition mode, a business development unitcan be put in charge of searching for targets and managingboth related and unrelated acquisitions (Chauduri and Tabrizi,1999). Hence, we do not expect organizational separation tobe prevalent in our setting, but if adopted, it can improve theperformance of balance within modes, so our study offers aconservative test of Hypothesis 1. In sum, although managerialtechniques can mitigate some caveats of balance within modes,they are not without costs, and most firms are unlikely toemploy them effectively in various modes. Whereas managerialtechniques enable firms to cope with challenges and managetrade-offs, balance across modes enables firms to circumventthese challenges.

potentially make more money than it did onSong flights.’ (New York Times , October 28,2005)

The organizational impediments that arise whena firm seeks to simultaneously explore and exploitin a particular mode are likely to outweigh thebenefits of balancing these activities or to preventthe firm from realizing such benefits in thefirst place, thus diminishing its performance. Wepredict the following:

Hypothesis 1: Balancing exploration andexploitation within a mode of operation (inter-nal organization, alliances, or acquisitions) willundermine firm performance relative to concen-trating on either exploration or exploitation inthat mode.

Balancing exploration and exploitation acrossmodes

A firm that balances exploration and exploitationacross distinct modes, i.e., explores in one modewhile exploiting in another, can enjoy the com-plementary benefits of exploration and exploita-tion, thus improving productivity while ensuringadaptability. In particular, balance across modesmay entail inhouse development of innovative newproducts (exploration) while leveraging existingknowledge via horizontal acquisitions (exploita-tion) or marketing alliances (exploitation). Alter-natively, a firm may infuse new knowledge viaR&D alliances (exploration) and acquire distinctbusinesses (exploration) while leveraging its estab-lished knowledge to refine its product design(exploitation). For example, Cisco has relied onalliances to tap into emerging technologies andidentify prospective acquisition targets that canbroaden its product portfolio. Its internal orga-nization has focused on marketing and servicingestablished products, while the product develop-ment teams of the acquired firms continued tooperate from their local offices.

While generating benefits from balance, thisapproach avoids some impediments associatedwith balance within modes. When balancingacross modes, the organizational and contractualboundaries of alternative modes of operation canbuffer exploration from exploitation by separat-ing new knowledge development from the lever-aging of established knowledge and by relying

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1908 U. Stettner and D. Lavie

on consistent organizational routines within eachmode. The underlying assumption is that per-sonnel, assets, and facilities allocated to explo-ration (exploitation) via the internal organizationbarely overlap with those assigned to exploita-tion (exploration) via alliances and acquisitions.In acquisitions, the acquired firm typically relieson its own organization for conducting said activ-ities, whereas in alliances, the collaborative agree-ment specifies which resources are assigned tothe alliance, thus separating them from internalresources (Lavie, 2006). Indeed, an employee oran asset can serve, in principle, for performingboth internal and external activities carried outby a partner or acquired firm, yet when balanc-ing across modes, this is unlikely given the dis-tinctive nature of assets and routines required forsupporting exploration versus exploitation (Bennerand Tushman, 2003). Unlike traditional approachesfor ambidexterity that require integration of theoutcomes of exploration and exploitation withinthe firm (Gibson and Birkinshaw, 2004; Jansenet al., 2009), balance across modes can circum-vent the need for such internal integration andthus alleviate some managerial burden. A firm canleverage internal knowledge for exploitation whilerelying on external knowledge of acquired firmsand alliance partners, thus avoiding integration.For instance, a firm can market its legacy softwareapplications while relying on an emerging tech-nology of its alliance partner to enter new appli-cation domains without internalizing this externaltechnology.

By decoupling exploration from exploitationacross modes, the firm can separately pursuethese activities, thus retaining the benefits of bal-ance and specialization, while mitigating negativetransfer and the tension between conflicting rou-tines. Specifically, when balancing exploration andexploitation across modes, a firm buffers conflict-ing routines while maintaining operational con-sistency in each mode, thus avoiding potentialtrade-offs. Employing routines for either explo-ration or exploitation in each mode enables thefirm to devise consistent rules and procedures,thus attenuating organizational tension, complex-ity, and coordination challenges as well as avoid-ing negative transfer of learning. For instance,Cisco has acquired a large number of start-upfirms in order to gain access to new technologiesand extend its product offering (external explo-ration). In turn, its internal organization provided

centralized marketing and customer support (inter-nal exploitation). Concentrating on new knowl-edge development via acquisitions enabled Ciscoto nurture separate and consistent routines forscreening targets based on their technology attrac-tiveness, product marketability, complementarity,and the qualifications of their managers and engi-neers. Relying on acquisitions for both explorationand exploitation would have prevented Cisco fromadopting consistent practices that enable routiniza-tion of the acquisition process and effective broad-ening of its product line.

Hence, a firm can both preserve a coherentlearning environment (Tsai, 2002) in which rou-tines become formalized and more efficient and atthe same time avoid procedural spillover acrossconflicting routines. By pursuing exploration inone mode and exploitation in another, the firmcan maintain consistency, control, productivity,and stability in certain modes, thereby enhanc-ing the efficiency of exploitation (Haleblian andFinkelstein, 1999). At the same time, it can facili-tate experimentation, flexibility, and risk taking insome other modes, and thus engage in effectivesearch and discovery of new knowledge. Whenthese activities are split across modes, the bound-aries of these modes become buffers that can effec-tively separate exploration from exploitation.3 Forexample, Cisco’s practices for screening acquisi-tion targets in emerging industries do not conflictwith its routines for refining its original productdesign.

Finally, by balancing exploration and exploita-tion across modes, a firm can develop spe-cialized resources, streamline capabilities, and

3 To the extent that firms rely on separate organizationalunits for managing their operations in each mode, they canfurther mitigate potential trade-offs between exploration andexploitation and prevent misapplication of knowledge acrossmodes. For instance, product development carried out by a firm’sinternal organization may be organizationally separated fromacquisitions that are executed by the firm’s business developmentunit or alliances that are coordinated by its dedicated alliancefunction (Kale, Dyer, and Singh, 2001). Unlike reliance onseparate organizational units for buffering exploration fromexploitation (Benner and Tushman, 2003), the dedicated alliancefunction or business development unit helps separate one modefrom another even though it can serve, in principle, for pursuingboth exploration and exploitation. A dedicated alliance functionor business development unit is desirable yet not necessaryin order for our predictions to hold. When balancing acrossmodes, the organizational boundaries of the firm (internalorganization versus alliances and acquisitions) buffer explorationfrom exploitation irrespective of whether the firm uses dedicatedunits for managing alliances and acquisitions.

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1909

enhance organizational processes in each mode.For instance, focusing on exploitation via market-ing alliances does not undermine the ability to gainfrom specialization in exploration via new productdevelopment or unrelated acquisitions. The firmcan gain efficiency and obtain scale and scopeeconomies by specializing in either explorationor exploitation in a particular mode. These gainsare ascribed to the firm’s skills or expertise forperforming the chosen activity in that mode. ForCisco, specializing in exploration via acquisitionsgenerated capabilities for identifying and assessingacquisition targets and for executing acquisitions.4

Investing dedicated resources in exploration viaone mode need not limit the pursuit of exploitationvia another mode. For example, a firm that concen-trates on experimenting with new technologies andinnovative product designs can effectively extendthe market reach of its established technologiesby forming marketing alliances. In fact, resourcesgarnered via exploitation in one mode can supportexploration in another mode (Rothaermel, 2001) orat least preserve their value when deployed in thesame mode (Vassolo, Anand, and Folta, 2004). Thebenefits of specialization are derived from main-taining a dominant type of activity within eachmode, so that vested resources do not need tobe shared across exploration and exploitation ineach mode. Concentrating on exploration in onemode, while focusing on exploitation in another,enhances performance by retaining the benefits ofbalance and specialization while avoiding negativetransfer and the adverse consequences of conflict-ing organizational routines. Our second hypothesisstates the following:

Hypothesis 2: Balancing exploration andexploitation across modes of operation willenhance firm performance relative to concen-trating on either exploration in both modes orexploitation in both modes .

We have thus far argued that balance acrossmodes is expected to be more beneficial thanengaging in either exploration or exploitationwithin these modes. Additionally, we asserted thatconcentrating on either exploration or exploita-tion within a particular mode should enhance

4 For further details on the Cisco example see Cisco Systems, Inc.and the Networking Equipment Industry by Sydney Finkelstein(Dartmouth College, 1998).

performance more than balancing these activitieswithin that mode. Consequently, we conclude thatbalancing exploration and exploitation across cer-tain modes of operation can enhance performancemore than balancing these activities within each ofthe corresponding modes.

For example, facing increased R&D expenses,shortened product-life cycles and intense compe-tition, Procter & Gamble (P&G) had witnessed35 percent decline in new product development,44 percent decline in market share, and $85 bil-lion loss of market value in 2000. Its incomingCEO, A.G. Lafley, abandoned P&G’s traditionof internal innovation, resorting instead to exter-nal innovation via acquisitions and alliances whileleveraging P&G’s marketing and manufacturinginfrastructure to exploit. P&G’s “Connect andDevelop” approach relied on its ability to recog-nize consumer trends while seeking external solu-tions to satisfy emerging customer needs. Insteadof internalizing knowledge by licensing intellec-tual property, P&G opted for acquisitions. Forinstance, in 2000, P&G declined a patent licens-ing deal and instead acquired SpinBrush fromDr. John. Shortly thereafter, P&G formed Pre-cision Diagnostics, a joint venture with Inver-ness Medical Innovations, to enter the consumerdiagnostics market. By 2006, 35 percent of P&G’sproducts had originated externally and 45 percentof its product development initiatives containedsubstantial external knowledge contributions. Thisled to increased productivity, reduced costs, anddoubling of P&G’s share price over these sixyears (Huston and Sakkab, 2006). This exampleillustrates how a firm can enhance its perfor-mance by shifting from balancing exploration andexploitation within its internal organization tobalancing these activities across modes. The under-lying reasoning is that decoupling exploration fromexploitation across modes can reduce the interde-pendence of these activities and circumvent theneed to maintain conflicting organizational rou-tines within each mode, while still enabling thefirm to benefit from simultaneous pursuit of explo-ration and exploitation. Thus, we propose:

Hypothesis 3: Balancing exploration andexploitation across modes of operation willenhance firm performance more than balanc-ing exploration and exploitation within thecorresponding modes of operation .

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1910 U. Stettner and D. Lavie

Configuring exploration and exploitationacross modes

A firm can pursue alternative configurations whenexploring in one mode and exploiting in another.This raises the question of which mode maximizesthe value of exploration and which offers greatervalue for exploitation. The inherent characteristicsof distinct modes may offer differential benefitsfor exploration versus exploitation. We posit thatexternally oriented modes that transcend a firm’sboundaries enable the firm to benefit from explo-ration, whereas internally oriented modes that con-fine operations to the firm’s boundaries increasethe value of exploitation. Hence, exploration ismost beneficial via acquisitions, which are moreexternally oriented than alliances. Alliances, inturn, are more externally oriented than internalorganization.

Exploration entails flexibility and ability to dis-lodge from inertial pressures (Hannan and Free-man, 1984). Moving away from a firm’s compe-tencies by minimizing reliance on prior knowledgedelays the formation of core rigidities that under-mine the value of exploration (Leonard-Barton,1992). Hence, exploration improves performanceas the firm distances itself from its core compe-tencies. Since knowledge that is nurtured withinthe firm’s boundaries is likely to be highly pathdependent, knowledge that spans these boundariescan better generate new opportunities (Rosenkopfand Nerkar, 2001). Although firms can changetheir knowledge bases over time, externally ori-ented modes such as alliances and acquisitionsoffer more immediate means to access new knowl-edge and skills. The value of exploitation, inturn, is associated with reliability and stabilitythat emerge when a firm leverages its estab-lished knowledge (March, 1991). Such knowledgesupports the refinement and application of corecompetencies. In turn, engaging in local searchenhances efficiency and enables the firm to con-sistently apply compatible skills and knowledge(Danneels, 2002). Exploitation thus increasinglyenhances performance as the firm moves closer tothe locus of its expertise.

Internal organization

The value of exploration in the internal organi-zation mode depends on a firm’s ability to inno-vate using its internal knowledge. The more reliant

the firm is on its core competencies, the morelikely it is to develop path dependence in itsoperations (Danneels, 2002). This, in turn, facil-itates local search rather than boundary spanning,thus restricting the accessibility of novel solu-tions (Rosenkopf and Nerkar, 2001) and mak-ing it difficult to dislodge from current solutions.As the firm attempts to reach beyond the scopeof its current knowledge base, inevitable relianceon core competencies fosters organizational iner-tia and core rigidities (Leonard-Barton, 1992) thatdelay exploration and can impair performance.However, refining existing products based on inter-nally available knowledge is possible under suchconditions (Burgelman, 2002), since incremen-tal improvements support organizational reliabilityand productivity, which characterize exploitation(March, 1991). Thus, the proximity of knowl-edge search within the firm’s boundaries andthe restrictive application of internal knowledgeimpair the value of exploration while enhancingexploitation benefits in this mode.

Alliances

Interfirm collaboration enables a firm to extend itssearch and engage in boundary spanning by com-bining its own knowledge with the complementaryknowledge of partners (Dyer and Singh, 1998). Bypartially relying on internal, path-dependent skillsand established knowledge, however, explorationis somewhat restricted, since alliances cannot becompletely disconnected from the firm’s currentknowledge base and value chain activities. At thesame time, alliances do not enable the firm tofully leverage its established skills and idiosyn-cratic knowledge because they may be incompat-ible with or inapplicable when deployed in com-bination with the partners’ knowledge (Das andTeng, 2000). Hence, by engaging in boundary-spanning activities via alliances, the firm can effec-tively leverage external knowledge and distanceitself from its own knowledge base (Rosenkopfand Almeida, 2003), but search and discoveryof new knowledge are confined by the scope ofalliance agreements. Consequently, the benefits ofexploration are likely to be moderate, althoughalliances offer a more effective mode for explo-ration than internal organization. In turn, the ben-efits of exploitation depend on whether the firmcan leverage its established knowledge and applyits competencies in familiar domains. Exploitation

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1911

via alliances cannot rely exclusively on the firm’sestablished knowledge, instead requiring adjust-ment of its internal processes (Dyer and Singh,1998) and development of partner-specific rela-tional routines (Zollo, Reuer, and Singh, 2002)that support knowledge exchange or combination.This limits the firm’s ability to fully benefit fromthe reliability, stability, and productivity associ-ated with its established knowledge. Consequently,compared to internal organization, alliances dimin-ish the value of exploitation.

Acquisitions

Acquisitions enable a firm to gain immediate con-trol of knowledge that is entirely different fromits internal knowledge without calling for relat-edness, resemblance, or combination of knowl-edge (Harrison et al., 1991; Kim and Finkelstein,2009). Specifically, boundary-spanning search viaacquisitions enables the firm to seek new knowl-edge that is unrelated to its current knowledge(Vermeulen and Barkema, 2001). In contrast toalliances, which entail combining complementaryknowledge and coordinating activities in a waythat enables the firm to retain some knowledgethat is unshared with its partners (Lavie, 2006),acquisitions may require more challenging inte-gration of the acquired firm’s knowledge. Theacquiring firm’s ability to leverage its establishedknowledge and skills in its acquisitions is limitedwhen the acquired firm’s knowledge is remotelyrelated to its own (Puranam et al., 2009). Hence,acquisitions relieve the firm of the need to deployinternal knowledge when engaging in explorationand increase the scope of search for opportunitiesbeyond those available via alliances, as the latterstill require substantial reliance on internal knowl-edge. In turn, the more different an acquired firmfrom the acquirer, the more difficult it becomesto effectively integrate its knowledge with theacquirer’s own knowledge in order to maintainreliability and stability throughout their operations(Finkelstein, 1997; Larsson and Finkelstein, 1999).Therefore, when the firm exploits via an internallyoriented mode and explores via acquisitions, it isless likely to fully integrate acquired firms whosebusinesses are remotely related to its own (Datta,1991), thus avoiding integration challenges andreinforcing the value of exploration. Consequently,acquisitions maximize the value of explorationbeyond that achieved via alliances and internal

organization, yet limit the value of exploitation rel-ative to these modes of operation. Thus, we wouldexpect the following:

Hypothesis 4: When exploration and exploita-tion are balanced across modes of operation,exploration will enhance firm performance morevia an externally oriented mode than via aninternally oriented mode; likewise, exploitationwill enhance firm performance more via aninternally oriented mode than via an externallyoriented mode

METHODS

Research setting and sample

We tested our hypotheses with panel data onU.S.-based publicly traded firms operating in theprepackaged software industry (SIC 7372) dur-ing 1990–2001. This context is suitable giventhe extensive use of various modes for pursuingexploration and exploitation. Software firms fre-quently innovate with new products (Campbell-Kelly, 2003), acquire firms (Gaughan, 2002),and form alliances (Hagedoorn, 1993; Lavie andRosenkopf, 2006). Also, the software industry hasbeen dominated by U.S.-based firms (Mowery andNelson, 1999), making the sample highly represen-tative. Finally, a high proportion of public firmsare young and small, thus ensuring the availabilityof financial information and limiting sensitivity toage- and size-related biases.

We gathered data on product introductions,alliances, and acquisitions since 1985 to mea-sure experience during the preceding five years.After excluding 53 multibusiness firms, the sampleincluded 190 firms that operate in various mar-ket segments of the software industry but whoseperformance is almost insensitive to non-softwarebusinesses.5 We integrate four data sources. Finan-cial information included Compustat data onfirms’ assets, revenues, long-term debt, cash, R&Dexpenses, and net income. We extracted dataon outstanding shares and stock prices from theCompustat-CRSP (Center for Research in Secu-rity Prices) database. We gathered data on new

5 Of the 190 firms, 88.89 percent had only a primary SIC code(7372), 5.82 percent had one secondary SIC code, 4.76 percenthad two secondary SIC codes, and 0.53 percent had more thantwo secondary SIC codes.

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1912 U. Stettner and D. Lavie

software products and releases of subsequent ver-sions from press items published in LexisNexisand Thompson’s Dialog New Product Announce-ments databases. These press items were care-fully read by trained coders with extensive indus-try experience, who identified the functionality ofeach product, its introduction date, and whether itwas a new product based on recently developedknowledge or a version of a previously introducedproduct. Each product was coded by two coderswho followed meticulous guidelines. The pretrain-ing interrater reliability reached 84.57 percent. Weresolved coder disagreements via deliberation. Intotal, the 190 firms introduced 8,961 softwareproducts during 1985–2001. We transformed theserecords to 2,503 firm-year observations by pool-ing the data for all products introduced by eachfirm in a given year. After discarding records withmissing data or those referring to the first andonly product (defined as exploration by default),we retained 1,952 firm-year observations during1990–2001.

We compiled acquisition records from Thom-son’s SDC database. For acquisition targets witha primary business in the prepackaged softwareindustry (SIC 7372), we used the target’s busi-ness description to classify its software productsto relevant categories using a typology that wasdeveloped with the help of industry experts. Thetypology includes 464 distinct product functions in54 market segments of four product classes: per-sonal applications, system infrastructure, verticalapplications, and business applications. We clas-sified acquisition targets outside the prepackagedsoftware industry using the SIC system. In total,the 190 firms engaged in 435 acquisitions during1985–2001. We transformed the acquisition datato 240 firm-year observations during 1990–2001by pooling across all acquisitions made by a firmin a given year.

We obtained alliance records from an exist-ing database (Lavie, 2007) that integrates datafrom SDC and Factiva databases, corporate web-sites, and Edgar SEC (Securities and ExchangeCommission) filings. It documents the partners’identities, the alliance announcement date, andtypes of agreements: R&D, production, market-ing and service, original equipment manufactur-ing, value-added resale, licensing, royalties, orsupply. In total, the 190 sampled firms formed10,993 alliances during 1985–2001. By poolingacross all alliances in a firm’s portfolio in a given

year, we transformed the data into 1,515 firm-yearobservations during 1990–2001, after discardingrecords with missing data and records that reportthe first and only alliance (defined as explorationby default).

Dependent variable

We measured firm performance with a functionof market value that represents investors’ ex anteexpectations about a firm’s future performance,thus capturing the outcomes of exploration andexploitation via alternative modes of operation.This measure is in line with prior research that hasdemonstrated that the firm’s market value effec-tively captures the performance effects of nuancedaspects of publicly announced product intro-ductions (Chaney, Devinney, and Winer, 1991;Uotila et al., 2009), alliances (Chan et al., 1997;Lavie, 2007; Lavie et al., 2011), and acquisitions(Hayward, 2002; Kim and Finkelstein, 2009). Inparticular, prior research has demonstrated thatabnormal stock market returns effectively predictalliances performance (Kale, Dyer, and Singh,2002) and post-acquisition performance severalyears following the announcement (Choi andHarmatuck, 2006).6 We modeled performanceusing a logarithmic growth function, controllingfor market value at the prior year: ln(MV i ,t+1) =α

ln(MV i ,t ) + π’xi ,t + ei ,t . This function maintainsdesirable statistical properties under the linearity,homoskedasticity, and independence assumptions(Stuart, 2000). The annual market value MV i ,t+1is computed by multiplying the firm’s stock price

6 Market value is preferred to accounting measures, sincefirms follow different accounting standards (Chakravarthy, 1986;Lubatkin and Shrieves, 1986). Accounting measures are alsonot sufficiently robust to capture the expected proceeds fromexploration and from certain modes of operation such asupstream alliances (Gulati, 1998). In turn, the firm’s marketvalue effectively captures the expected proceeds from internallydeveloped products, alliances, and acquisitions irrespective ofdifferences in the timing of their accrual. To reduce thetime differential across modes of operation, we refer to thetime of product introduction rather than to the initiation ofproduct development in the internal organization mode. Firmsdisclose information about their products in the course of theirdevelopment and during their introduction to the market, thusenabling investors to assess their prospects. Such informationis made available in press releases of publicly traded firms anddistinguishes new products from versions of existing products,identifies the value chain functions of alliances, and clarifies howdistinct the firm’s business is from those of its acquisition targets.Such information typically identifies the sources of knowledgeused in products, alliances, and acquisitions as well as the firm’smotivations for undertaking these modes of operation.

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1913

by its number of common shares outstanding.Because of its volatility, we calculated MV i ,t+1by averaging the 12 end-of-month daily valuesof the relevant year (Lavie, 2007): 1

12

∑12m

(Stock Pricei,t+1,m × Outstanding Sharesi,t+1,m).All independent variables and controls werelagged by one year relative to the dependentvariable.

Independent variables

We operationalized exploration-exploitation witha set of continuous variables rather than withtwo separate measures, assuming that explorationinhibits exploitation and vice versa (Greve, 2007;Lavie and Rosenkopf, 2006; Sidhu et al., 2007;Simsek et al., 2009; Uotila et al., 2009). The tran-sition from exploration to exploitation is gradual,and the distinction between these activities is oftena matter of degree rather than of kind. Such tran-sitivity and relativity call for the conceptualizationof exploration and exploitation along a continuum(Lavie et al., 2010). Since a firm can introducemultiple products and engage in several acquisi-tions and alliances, within each mode its activitiesvary continuously between pure exploration andpure exploitation, with exploration incorporatingnew knowledge and exploitation leveraging exist-ing knowledge.

Specifically, in the internal organization mode,a firm exploits by relying on its established knowl-edge to introduce refined versions of existingproducts or instead explores by introducing com-pletely new products based on its new designs andrecently developed knowledge (Cao et al., 2009;Danneels, 2002; Greve, 2007; He and Wong, 2004;Jansen et al., 2006; Voss et al., 2008). A productthat draws on the firm’s established knowledge andcompetencies that served in developing its previ-ously introduced products is indicative of exploita-tion. For example, the following press releaseexcerpt refers to a new version of an existing prod-uct by Synopsys, a software firm offering synthe-sis, simulation, and test applications for designersof integrated circuits. This product clearly buildson established knowledge that served in priorversions:

‘Our team of world class synthesis expertshave been very busy developing the mostsignificant QoR and runtime improvements

in the past five years . . . [Synopsys will]introduce Design Compiler 1999.05 (DC99),the latest version of its flagship product. . . The new release promises significantrun-time and productivity enhancements.’(Electronic Engineering Times , March 8,1999)

In turn, a new product that is meaningfullydistinct from the firm’s prior products and thatdraws on knowledge and competencies that thefirm has not used in the past is indicative ofexploration (Danneels, 2002; Danneels and Sethi,2011), as illustrated in another product releasedby Synopsys:

‘Behavioral Compiler, a revolutionary syn-thesis tool that drastically simplifies inte-grated circuit (IC) design . . . raises the levelof design specification to a much higher levelthan logic synthesis . . . This is the type ofexploration designers have been looking for. . . our customers have been asking us forbehavioral synthesis for years . . . Finally,it’s here.’ (Business Wire, May 16, 1994)

Accordingly, for each of the firm’s products, anindicator received a value of 1 if the firm had notpreviously released a prior version of that productusing similar knowledge and 0 if a prior version ofthat product existed. We calculated exploration viainternal organization as the value of that indicatoraveraged across all products introduced by the firmin a given year.7

In the alliance mode, a firm can exploit byengaging in downstream value chain activities viamarketing alliances or instead explore by pursuingupstream activities via R&D alliances (Koza andLewin, 1998; Rothaermel, 2001). Downstreamalliances rely on the firm’s established knowledgeand the partners’ distribution channels to expandthe market reach of the firm’s existing products,

7 To avoid classifying a firm’s first product as exploration bydefault, we excluded eight observations relating to years inwhich firms released their first and only product. Productsoriginally developed by a recently acquired firm or jointlywith an alliance partner were also excluded. Nevertheless, weconsidered the firm’s introduction of new versions of productsoriginally developed by acquired firms as exploitation viainternal organization.

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1914 U. Stettner and D. Lavie

thus classified as exploitation, as illustrated by thefollowing example:

‘ . . . a multi-year agreement with Synopsys. . . to resell Synopsys FPGA and CPLDsynthesis technology . . . ‘This relationshipallows VeriBest to distribute and supportSynopsys’ leading edge technology . . . ’ (PRNewswire, January 27, 1997)

Upstream alliances in the software industryentail moving beyond the firm’s knowledge baseand developing new products that integrate its part-ners’ knowledge, thus representing exploration.Following is an example of such alliance formedby Synopsys:

‘ATE vendor Agilent Technologies Inc. andEDA provider Synopsys Inc. are joiningforces in a far-reaching partnership . . . thejoint work will likely start by embeddingSynopsys design-for-test (DFT) technologyonto a line of Agilent devices . . . Bothcompanies cited the advantage of internallyleveraged technologies, with Agilent’s largeIC design staff in-house . . . We see this asmuch broader and far-reaching in impact; theopportunity for creating solutions for differ-ent kinds of test problems . . . ’ (ElectronicEngineering Times , March 19, 2001)

Following Lavie and Rosenkopf (2006), anindicator denoted for each alliance whether itinvolved knowledge-generating upstream activitiessuch as joint R&D, coded 1; knowledge-leveragingdownstream activities such as joint marketing,resale, production, or supply, coded 0; or acombination of both activities, coded 0.5. We thencalculated alliance exploration as the average valueof this indicator across all alliances formed by thefirm in a given year.

Finally, we measured exploitation in the acquisi-tion mode, in which a firm can acquire targets thatoperate related businesses or businesses remotefrom its own business (Ahuja and Katila, 2001;Anand and Singh, 1997; Seth, 1990). The closerthe resemblance between the acquired business andthe firm’s current business, the greater the overlapin knowledge bases, thus indicative of exploitation.The following example reports such acquisition bySynopsys:

‘Synopsys pushed deeper into the physical-design realm by acquiring startup StanzaSystems . . . The Stanza team will be addedto the Epic Technology Group within Syn-opsys . . . ‘Stanza has technology that isfully complementary to what we’re doingin physical design.’ . . . Synopsys sees theStanza acquisition as a natural continuationof its purchase of Epic Design Technol-ogy two years ago.’ (Computergram Inter-national , June 25, 1999)

In turn, acquiring a business that is less relatedto the firm’s current business is indicative ofexploration because it expands the scope ofthe firm’s knowledge base and product offering(Vermeulen and Barkema, 2001), as illustrated bythe following example:

‘Synopsys Inc., the leading developer ofhigh-level design automation software, todayannounced that it will acquire Silicon Archi-tects, a private company that pioneered theStructured ASIC Methodology . . . We’vebeen working on enhancements to our basicsynthesis process for the past seven years.Libraries are an area that has been, for themost part, overlooked. . . . Since 1987, I’vebeen looking for a library that would allowsynthesis to realize its full potential for qual-ity of results. In Silicon Architects’ CBAlibrary, I’ve finally found it . . . This mergergives Synopsys another opportunity to addleading-edge technology to our portfolio . . . ’(Business Wire, April 17, 1995)

Based on the business descriptions of acquiredfirms and the product function typology, for eachacquisition within SIC 7372, an indicator receiveda value of 0 if the acquiring firm had previouslyoffered a similar product function, a value of 1if that function was not offered but the firm hadprior products in the same market segment, and avalue of 2 if that function was not offered but thefirm had prior products in the same applicationclass. For an acquired firm with a primary SICcode different from 7372, the indicator received avalue of 3 if the first three-digit SIC code equaled737, a value of 4 if the two-digit SIC code equaled73, a value of 5 if the one-digit SIC code equaled7, and a value of 6 if the acquired firm operated in

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1915

an entirely unrelated industry. For each firm-year,we calculated acquisition exploration as the valueof this indicator averaged across all acquisitions inthat year.

To facilitate interpretation and maintain consis-tency across all exploration variables, the threemeasures were transformed to range between 0 and1, with high values indicating exploration.

Control variables

We control for interindustry variation by samplingfirms in a single industry (SIC 7372). We con-trol for intertemporal trends with year dummies.Together with the lagged performance incorpo-rated in the growth function (Lavie, 2007; Rothaer-mel and Alexandre, 2009), the firm fixed effectsaccount for unobserved heterogeneity.

Additionally, we incorporated firm-level con-trols, including a firm’s size, R&D intensity,solvency, product life-cycle, organizational sepa-ration, hardware experience, and mode experience.Firm size can influence the firm’s innovative out-put and performance (Ahuja, Lampert, andTandon, 2008). It was measured with the value oftotal assets in the preceding year (DeCarolis andDeeds, 1999). R&D intensity reflects the extentto which the firm invests in new technologies(Christensen, 1997) and represents its absorptivecapacity (Cohen and Levinthal, 1990), which canenhance the value of internal exploration efforts.We measured it by dividing the firm’s R&Dexpenses by its total revenue in the precedingyear. A firm’s solvency captures the financialresources available to support exploration andexploitation activities. It represents organizationalslack, which may affect innovation and perfor-mance (Nohria and Gulati, 1996). We measuredfirm solvency with the log-transformed ratio ofcash to long-term debt in the preceding year. Wealso controlled for product life-cycle, given thatthe contribution of a product to firm performancemay vary over time, with maximum contributionexpected at an intermediate stage. We measuredit with the average number of years (up to three)since the introduction of software products to themarket (Harter, Krishnan, and Slaughter, 2000).

To isolate the effect of balancing explorationand exploitation from the firm’s use of managerialtechniques such as organizational separation, weaccounted for organizational separation betweenunits responsible for internal development and

dedicated units for managing alliances andacquisitions. Such organizational separation mayenable the firm to allocate specialized resourcesand more effectively manage its alliances andacquisitions (Kale et al., 2000). We gathereddata on the firm’s dedicated alliance functionand business development unit responsible foracquisitions in a particular year from LexisNexispress releases and listings of relevant managerialpositions in the Corporate Affiliations database.Organizational separation received a value of0 if no dedicated organizational unit was usedfor managing alliances or acquisitions, a valueof 1 if a dedicated unit served for managingeither alliances or acquisitions, and a value of 2if two units were used for separately managingalliances and acquisitions. High levels of thiscontrol variable are expected to improve the firm’sability to effectively separate exploration fromexploitation across different modes of operation.

In addition, we controlled for the firm’s expe-rience with hardware products, which may tradeoff against its focus on software, measuring thenumber of hardware products introduced in thepreceding five years. Finally, we accounted formode experience, which may enable the firm toenhance specialization and consistency of routines.This set of measures also controls for the firm’sabsolute level of exploration. We measured thefirm’s experience with each mode by countingthe number of corresponding corporate events thatoccurred in the preceding five years (Haleblianand Finkelstein, 1999; Wang and Zajac, 2007).Thus, the firm’s internal organization experiencewas measured with the total number of products,alliance experience was measured with the num-ber of alliances formed, and acquisition experiencewas measured with the number of firms acquiredin the preceding five years. Experience was mod-eled to be preserved at 90 percent per year, usingthe formula

∑St=1 Et−1 × (1 − r)t−1, where Et

represents the firm’s exploration in a particularmode in a given year and r represents the decayrate of 10 percent. In auxiliary analyses, we veri-fied that our findings were insensitive to alternativememory decay rates.

Analysis

We account for endogeneity in a firm’s tenden-cies to operate via particular modes with two-stage analysis (Hamilton and Nickerson, 2003;

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1916 U. Stettner and D. Lavie

Shaver, 1998). A firm’s decision to engage in aparticular mode such as alliance or acquisition maybe influenced by the inherent benefits of that mode,such as accessibility of external knowledge andtime to market, as well as by costs such as poten-tial opportunistic behavior or acquisition premium.These mode-specific considerations apply irrespec-tive of the tendency to explore versus exploit inthat mode, yet influence the firm’s propensity toengage in that mode. Following Heckman (1979),we used three probit first-stage models to estimatewhether the firm used a particular mode in a givenyear. We regressed the probability of using a par-ticular mode on the firm’s size as captured by itstotal sales, its available cash, long-term debt, R&Dinvestment, prior experience with hardware devel-opment, and experience with particular modes ascaptured by indicators that receive a value of 0 ifthe firm did not have any prior experience in thecorresponding mode and a value of 1 if the firmhad prior experience in that mode. The first-stagemodel accounted for the panel data structure withfirm and year fixed effects. The predicted valuesfrom the first-stage models were used to calculatethe inverse Mills ratios (λ), which were then incor-porated as additional controls in the second stageto account for self-selection bias in engaging inparticular modes.

The second-stage models served for testingthe hypotheses, incorporating panel data withfirm fixed affects to explain within-firm varia-tion in performance over time. Hausman testssuggested that the fixed effects models are supe-rior or equivalent to random effects models(Hausman, 1978). The analysis of panel dataraises concerns about serial correlation of errorswithin cross-sections, which may deflate stan-dard errors and inflate significance levels. Wetested for autocorrelation of errors within cross-sections (Baltagi and Wu, 1999) and incorpo-rated first-order autoregressive errors to accountfor an AR(1) process. Thus, the tested mod-els took the form: Y i ,t+1 =α +βx i ,t + ui + εi,t ,where εi,t = ρεi ,t-1 +μi ,t and −1 <ρ < 1, withui representing the firm fixed effects and ρ theautoregressive AR(1) parameter, which has a 0mean, homoskedastic, and serially uncorrelatederror term μi,t. We estimated the models usingmaximum likelihood with missing values subjectto listwise deletion. Model fit was evaluated withlog likelihood ratio tests comparing each modelto its baseline model. The second-stage models

incorporated Mills ratios from the first-stage mod-els (results available from the authors). The λ

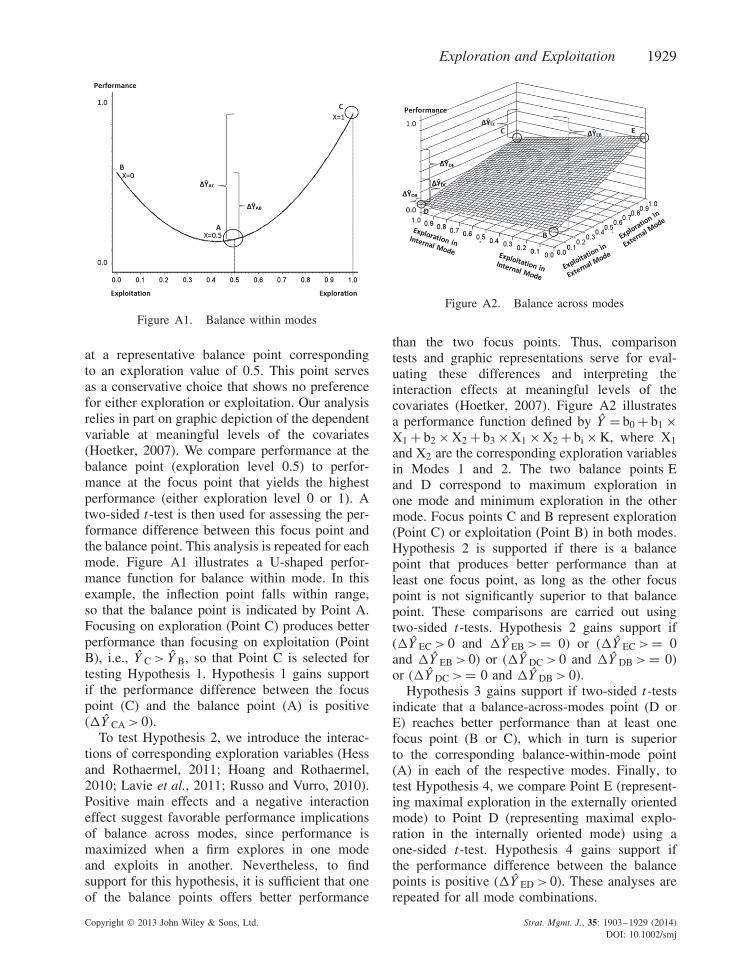

parameters are insignificant in models estimatingbalance within modes, so the ability to balanceexploration and exploitation in a particular modeis unaffected by the inclination to use that mode.When balancing across modes, some λ parame-ters are significant, so the propensity to engage ininternal organization and alliances affect the abilityto effectively balance exploration and exploitationacross these modes. An elaborate explanation ofthe procedures used for testing our hypotheses isprovided in the Appendix.

RESULTS

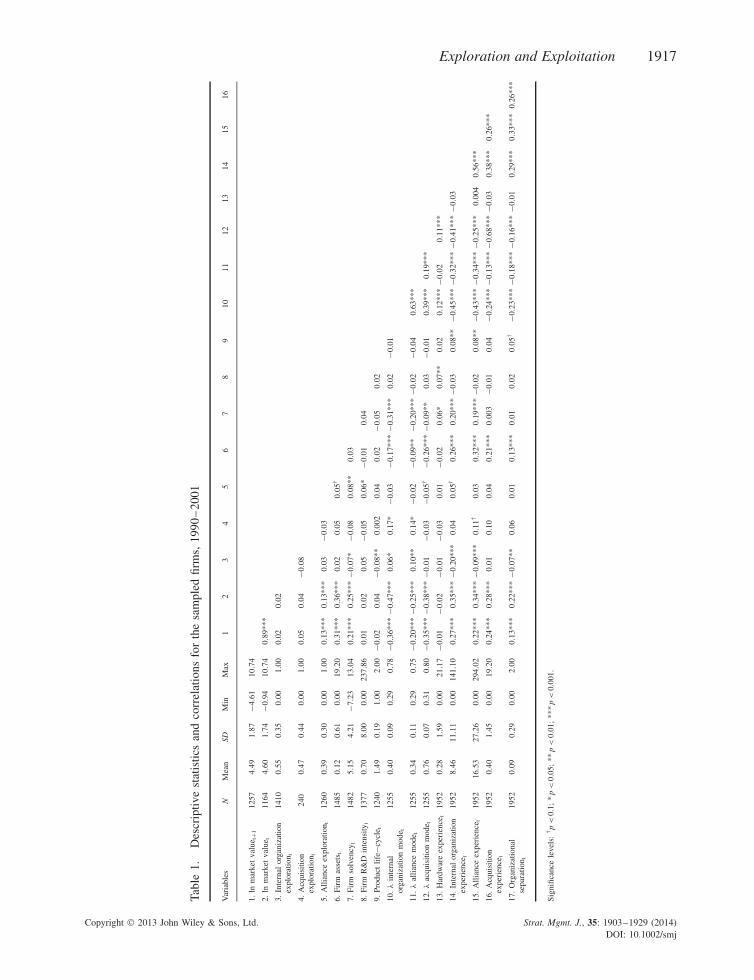

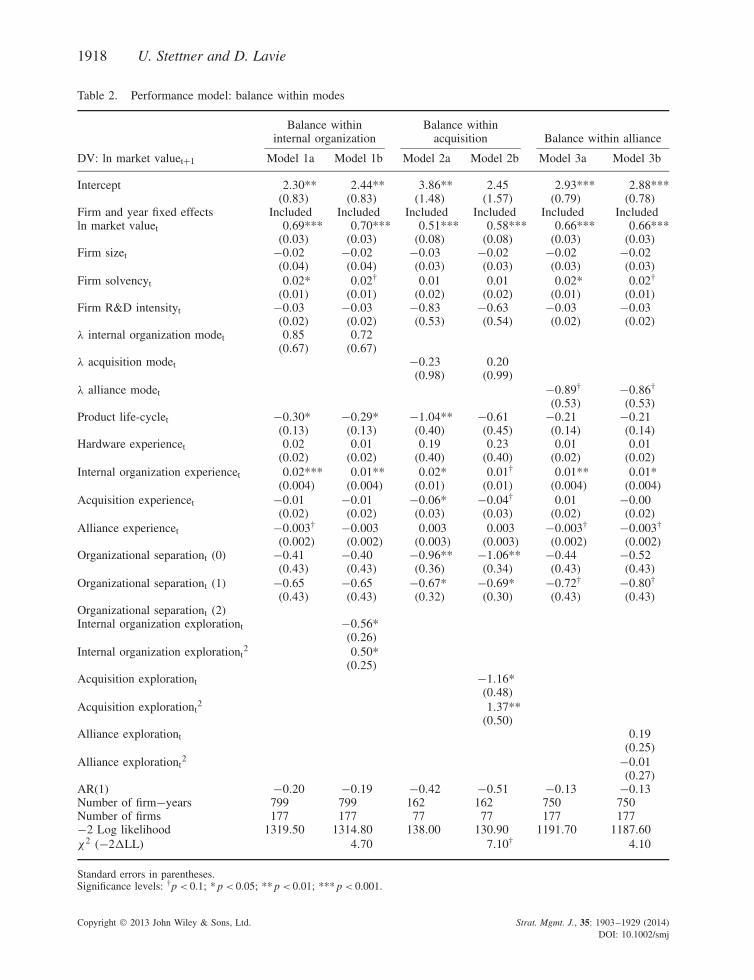

Table 1 reports descriptive statistics. The rel-atively low correlations of the three explo-ration variables suggest their independence, whichjustifies the operationalization of exploration-exploitation along separate modes. The highcorrelation between the tendency for internal orga-nization (λ internal organization) and tendency toform alliances (λ alliance) suggests that a firmthat develops more products also tends to collab-orate extensively. Models estimating the perfor-mance effects of balance within modes are reportedin Table 2. The baseline models show that, inthe internal organization mode (Model 1a), per-formance is positively related to firm solvencyand internal organization experience, yet declineswith product life-cycle and alliance experience.In the acquisition mode (Model 2a), performanceincreases with internal organization experience,yet declines with product life-cycle and acquisi-tion experience. In the alliance mode (Model 3a),performance increases with solvency and inter-nal organization experience, yet declines with thefirm’s inclination to form alliances and its allianceexperience (Table 3).

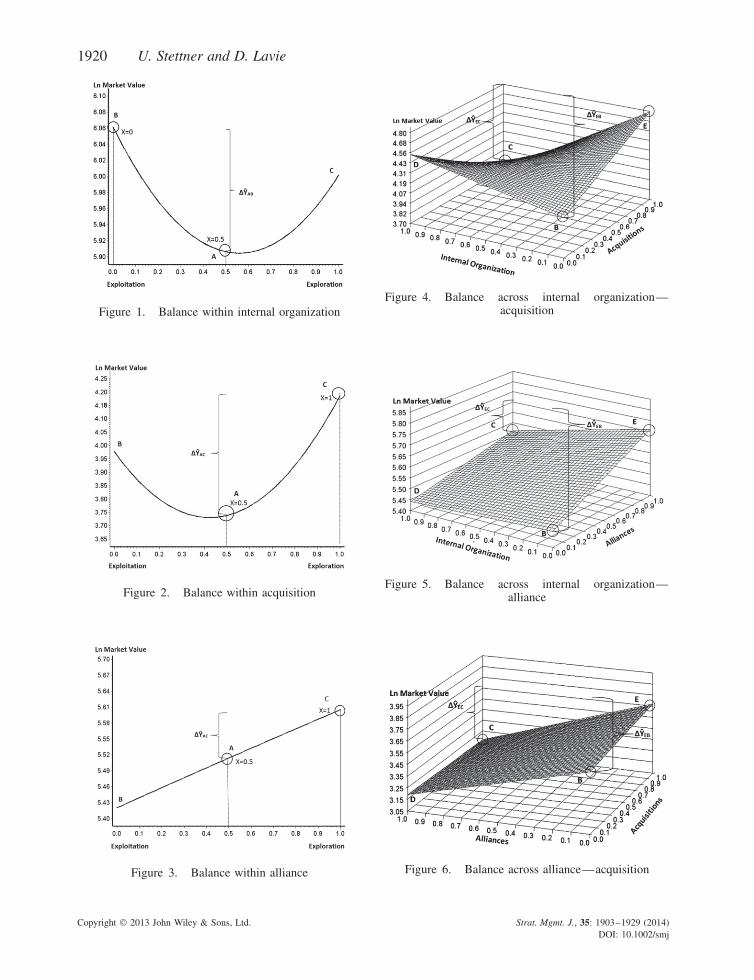

Table 4 reports t-tests for Hypothesis 1 basedon Models 1b–3b. Model 1b introduces the linearand quadratic terms of exploration in the internalorganization mode. The linear effect is negative(β = −0.56, p < 0.05), and the quadratic term ispositive (β = 0.50, p < 0.05). Maximum perfor-mance is reached when focusing on exploitation(X = 0). In support of Hypothesis 1, a two-sidedt-test shows significant improvement in perfor-mance for exploitation relative to the balancepoint (�Y = 0.65, p < 0.05). The performance

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1917

Tabl

e1.

Des

crip

tive

stat

istic

san

dco

rrel

atio

nsfo

rth

esa

mpl

edfir

ms,

1990

–20

01

Var

iabl

esN

Mea

nSD

Min

Max

12

34

56

78

910

1112

1314

1516

1.ln

mar

ket

valu

e t+1

1257

4.49

1.87

−4.6

110

.74

2.ln

mar

ket

valu

e t11

644.

601.

74−0

.94

10.7

40.

89**

*

3.In

tern

alor

gani

zatio

nex

plor

atio

n t14

100.

550.

350.

001.

000.

020.

02

4.A

cqui

sitio

nex

plor

atio

n t24

00.

470.

440.

001.

000.

050.

04−0

.08

5.A

llian

ceex

plor

atio

n t12

600.

390.

300.

001.

000.

13**

*0.

13**

*0.

03−0

.03

6.Fi

rmas

sets

t14

850.

120.

610.

0019

.20

0.31

***

0.36

***

0.02

0.05

0.05

†

7.Fi

rmso

lven

cyt

1482

5.15

4.21

−7.2

313

.04

0.21

***

0.25

***

−0.0

7*−0

.08

0.08

**0.

03

8.Fi

rmR

&D

inte

nsity

t13

770.

708.

000.

0023

7.86

0.01

0.02

0.05

−0.0

50.

06*

−0.0

10.

04

9.Pr

oduc

tlif

e−cy

cle t

1240

1.49

0.19

1.00

2.00

−0.0

20.

04−0

.08*

*0.

002

0.04

0.02

−0.0

50.

02

10.λ

inte

rnal

orga

niza

tion

mod

e t12

550.

400.

090.

290.

78−0

.36*

**−0

.47*

**0.

06*

0.17

*−0

.03

−0.1

7***

−0.3

1***

0.02

−0.0

1

11.λ

allia

nce

mod

e t12

550.

340.

110.

290.

75−0

.20*

**−0

.25*

**0.

10**

0.14

*−0

.02

−0.0

9**

−0.2

0***

−0.0

2−0

.04

0.63

***

12.λ

acqu

isiti

onm

ode t

1255

0.76

0.07

0.31

0.80

−0.3

5***

−0.3

8***

−0.0

1−0

.03

−0.0

5†−0

.26*

**−0

.09*

*0.

03−0

.01

0.39

***

0.19

***

13.

Har

dwar

eex

peri

ence

t19

520.

281.

590.

0021

.17

−0.0

1−0

.02

−0.0

1−0

.03

0.01

−0.0

20.

06*

0.07

**0.

020.

12**

*−0

.02

0.11

***

14.

Inte

rnal

orga

niza

tion

expe

rien

cet

1952

8.46

11.1

10.

0014

1.10

0.27

***

0.35

***

−0.2

0***

0.04

0.05

†0.

26**

*0.

20**

*−0

.03

0.08

**−0

.45*

**−0

.32*

**−0

.41*

**−0

.03

15.

Alli

ance

expe

rien

cet

1952

16.5

327

.26

0.00

294.

020.

22**

*0.

34**

*−0

.09*

**0.

11†

0.03

0.32

***

0.19

***

−0.0

20.

08**

−0.4

3***

−0.3

4***

−0.2

5***

0.00

40.

56**

*

16.

Acq

uisi

tion

expe

rien

cet

1952

0.40

1.45

0.00

19.2

00.

24**

*0.

28**

*0.

010.

100.

040.

21**

*0.

003

−0.0

10.

04−0

.24*

**−0

.13*

**−0

.68*

**−0

.03

0.38

***

0.26

***

17.

Org

aniz

atio

nal

sepa

ratio

n t19

520.

090.

290.

002.

000.

13**

*0.

22**

*−0

.07*

*0.

060.

010.

13**

*0.

010.

020.

05†

−0.2

3***

−0.1

8***

−0.1

6***

−0.0

10.

29**

*0.

33**

*0.

26**

*

Sign

ifica

nce

leve

ls:

†p

<0.

1;*

p<

0.05

;**

p<

0.01

;**

*p

<0.

001.

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1918 U. Stettner and D. Lavie

Table 2. Performance model: balance within modes

Balance withininternal organization

Balance withinacquisition Balance within alliance

DV: ln market valuet+1 Model 1a Model 1b Model 2a Model 2b Model 3a Model 3b

Intercept 2.30** 2.44** 3.86** 2.45 2.93*** 2.88***(0.83) (0.83) (1.48) (1.57) (0.79) (0.78)

Firm and year fixed effects Included Included Included Included Included Includedln market valuet 0.69*** 0.70*** 0.51*** 0.58*** 0.66*** 0.66***

(0.03) (0.03) (0.08) (0.08) (0.03) (0.03)Firm sizet −0.02 −0.02 −0.03 −0.02 −0.02 −0.02

(0.04) (0.04) (0.03) (0.03) (0.03) (0.03)

Firm solvencyt 0.02* 0.02† 0.01 0.01 0.02* 0.02†

(0.01) (0.01) (0.02) (0.02) (0.01) (0.01)Firm R&D intensityt −0.03 −0.03 −0.83 −0.63 −0.03 −0.03

(0.02) (0.02) (0.53) (0.54) (0.02) (0.02)λ internal organization modet 0.85 0.72

(0.67) (0.67)λ acquisition modet −0.23 0.20

(0.98) (0.99)

λ alliance modet −0.89† −0.86†

(0.53) (0.53)Product life-cyclet −0.30* −0.29* −1.04** −0.61 −0.21 −0.21

(0.13) (0.13) (0.40) (0.45) (0.14) (0.14)Hardware experiencet 0.02 0.01 0.19 0.23 0.01 0.01

(0.02) (0.02) (0.40) (0.40) (0.02) (0.02)

Internal organization experiencet 0.02*** 0.01** 0.02* 0.01† 0.01** 0.01*(0.004) (0.004) (0.01) (0.01) (0.004) (0.004)

Acquisition experiencet −0.01 −0.01 −0.06* −0.04† 0.01 −0.00(0.02) (0.02) (0.03) (0.03) (0.02) (0.02)

Alliance experiencet −0.003† −0.003 0.003 0.003 −0.003† −0.003†

(0.002) (0.002) (0.003) (0.003) (0.002) (0.002)Organizational separationt (0) −0.41 −0.40 −0.96** −1.06** −0.44 −0.52

(0.43) (0.43) (0.36) (0.34) (0.43) (0.43)

Organizational separationt (1) −0.65 −0.65 −0.67* −0.69* −0.72† −0.80†

(0.43) (0.43) (0.32) (0.30) (0.43) (0.43)Organizational separationt (2)Internal organization explorationt −0.56*

(0.26)

Internal organization explorationt2 0.50*

(0.25)Acquisition explorationt −1.16*

(0.48)

Acquisition explorationt2 1.37**

(0.50)Alliance explorationt 0.19

(0.25)

Alliance explorationt2 −0.01

(0.27)AR(1) −0.20 −0.19 −0.42 −0.51 −0.13 −0.13Number of firm−years 799 799 162 162 750 750Number of firms 177 177 77 77 177 177−2 Log likelihood 1319.50 1314.80 138.00 130.90 1191.70 1187.60χ2 (−2�LL) 4.70 7.10† 4.10

Standard errors in parentheses.Significance levels: †p < 0.1; * p < 0.05; ** p < 0.01; *** p < 0.001.

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

Exploration and Exploitation 1919

Table 3. Balance within modes (Hypothesis 1)

DV: ln market valuet+1

Maximum performancedifference

Focus vs. balance inthe internalorganization mode

�YBA = 0.65* (0.31), t = 2.11

Focus vs. balance inthe acquisitionmode

�YCA = 1.61** (0.61), t = 2.64

Focus vs. balance inthe alliance mode

�YCA = 0.10 (0.32), t = 0.30

Standard errors in parentheses.Significance levels: †p < 0.1, * p < 0.05; ** p < 0.01;*** p < 0.001.

difference between the balance point and focus onexploration (X = 1) is also significant, in favor ofthe latter point. Hence, balance within the inter-nal organization mode undermines performance.Model 2b introduces the linear and quadratic termsof exploration in the acquisition mode. The lin-ear term of exploration is negative (β =−1.16,p < 0.05), while the quadratic term is positive(β = 1.37, p < 0.01). Per Hypothesis 1, maxi-mum performance achieved at exploration (X = 1)is significantly better than performance at bal-ance (�Y = 1.61, p < 0.01). Model 3b reveals nosignificant effects of exploration in the alliancemode. The predicted performance function reachesmaximum performance at the highest level ofexploration (X = 1). Accordingly, exploration issuperior to balance (X = 0.5) in the alliancemode, yet the corresponding performance differ-ence (�Y = 0.10) is insignificant.

The significant findings of negative performanceimplications of balance within the internal organi-zation and acquisition modes are obtained whilecontrolling for organizational separation. Table 2reveals that organizational separation enhances theperformance of balance within these modes as evi-dent by the negative coefficients of the 0 and 1levels of this variable relative to the baseline 2level. Evidently, a firm needs to operate both adedicated alliance unit and a business develop-ment unit to gain from organizational separationin the acquisition mode (�β02 = 1.06, p < 0.01)and alliance mode (�β12 = 0.80, p < 0.10).

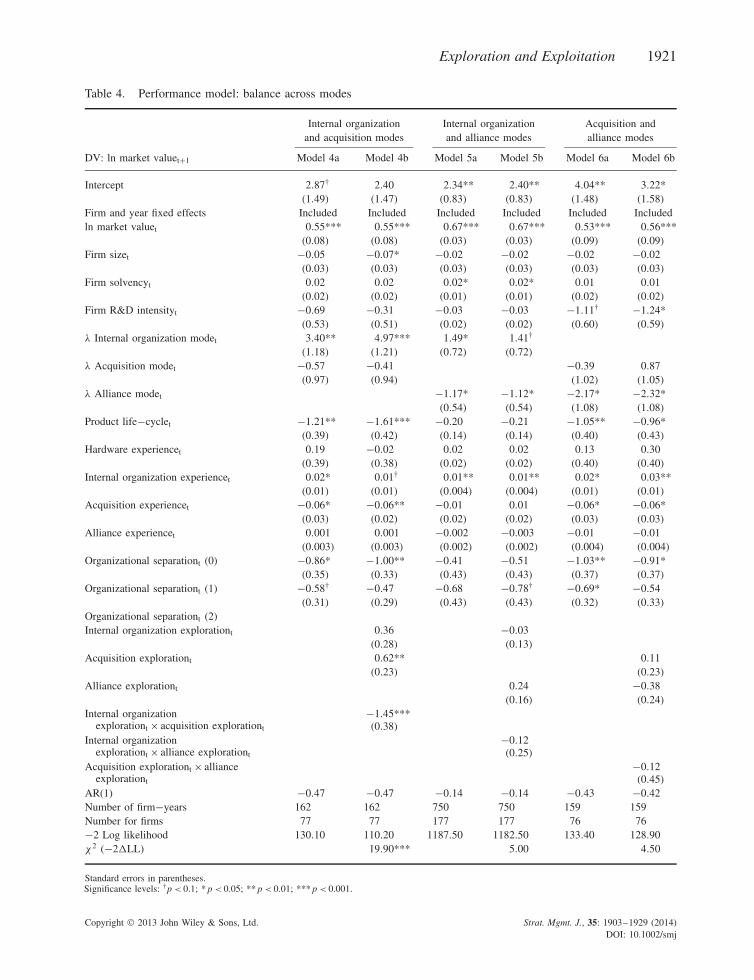

Table 4 estimates the performance effects ofbalance across the internal organization and acqui-sition modes (Model 4), the internal organizationand alliance modes (Model 5), and the acquisition

and alliance modes (Model 6). The baseline mod-els reveal that performance improves with inter-nal organization experience. When explorationand exploitation are balanced across the inter-nal organization and acquisition modes (Model4a), performance declines with product life-cycleand acquisition experience; when exploration andexploitation are balanced across the internal orga-nization and alliance modes (Model 5a), perfor-mance increases with solvency; and when they arebalanced across the acquisition and alliance modes(Model 6a), performance declines with prod-uct life-cycle, acquisition experience, and R&Dintensity.

Model 4b (Table 4) reveals that when explo-ration and exploitation are balanced across theinternal organization and acquisition modes,the interaction effect is negative (β =−1.45,p < 0.001), and the main effects are positive yetsignificant only for exploration in the acquisitionmode (β = 0.62, p < 0.01). The performancefunction indicates that exploring in the acquisitionmode while exploiting in the internal organizationmode (Point E) offers better performance thanfocusing on either exploration (Point C) orexploitation (Point B) in both modes. Table 5reports t-tests for Hypothesis 2. In support ofHypothesis 2, balance point E is superior tofocus points C (�Y = 1.09, p < 0.001) and B(�Y = 0.62, p < 0.05). When exploration andexploitation are balanced across the internalorganization and alliance modes (Model 5b), theinteraction effects are insignificant. Consistentwith Hypothesis 2, balance point E is superior tofocus points B (�Y = 0.24) and C (�Y = 0.16),although these differences are insignificant. Model6b is used for testing the performance effects ofbalancing exploration and exploitation across theacquisition and alliance modes. Per this model,the linear and interaction effects of explorationin these modes are insignificant. Consistent withHypothesis 2, balance point E is superior to focuspoint C (�Y = 0.50), although this differenceis insignificant. These findings hold while con-trolling for organizational separation, which alsoimproves performance. Specifically, when thefirm maintains both a dedicated unit for managingalliances and a business development unit incharge of acquisitions, its performance improveswhen balancing exploration and exploitationacross the internal organization and acquisitionmodes (�β02 = 1.00, p < 0.01), across the internal

Copyright © 2013 John Wiley & Sons, Ltd. Strat. Mgmt. J., 35: 1903–1929 (2014)DOI: 10.1002/smj

1920 U. Stettner and D. Lavie

Figure 1. Balance within internal organization

Figure 2. Balance within acquisition