Embed Size (px)

DESCRIPTION

A selection of pages from the July 2016 issue of AM – Automotive Management magazine.

Citation preview

2024 One in five new cars

sold can function autonomously

AUTOMOTIVE MANAGEMENT

www.am-online.com

July 2016 £8.00M C L A R E N 5 7 0 G T / P 7 8

Will it help McLaren to sell 4,000 supercars a year?

MOTOR RETAIL IN

2025Shrinking networks, soaring property costs and virtual showrooms – we offer dealers a vision of their future

S U Z U K I / P 2 2

There’s more to success than just numbers, says sales director Dale Wyatt

V I D E O / P 7 2

How video can build trust with your customers

A C Q U I S I T I O N / P 7

Marshall’s takeover of Ridgeway will require careful integration

2019Premium brands have stores in 25 shopping centres

2017Six car brands now offer online ordering to consumers

2020 Electric or hybrid powertrains available in all mainstream car ranges

2022 Recession speeds a 17% reduction in UK franchised networks

2023 14 UK cities have banned diesel cars from their roads

e

X

2018Virtual reality equipment is standard in premium brand franchises

>

PA G E S 2 7- 47

Be a part of the sharing community

www.am-online.com/eventsEvents

Date Event Venue

September 6 2016 AM Digital Dealer Conference Midlands

September 9 2016 AM Executive Breakfast Club Simpson’s in the Strand, London

November 11 2016 AM Executive Breakfast Club Simpson’s in the Strand, London

November 16 2016 Automotive Management Live Arena:MK, Milton Keynes

February 9 2017 AM Awards ICC, Birmingham

I N T H I S I S S U E

“As a result of changing technology

and the drive for

manufacturer brand equity,

there are likely to

be fewer, but larger

dealerships”Jim Saker – P39

“The ‘pay to drive’ rather than ‘pay to purchase’ ownership

model is achieving dominance”

Philip Nothard – P47

“There’s no other retail model in existence which can survive on

such limited footfall”Paul Gordon,

Autotorq – P34

am-online.com July 2016 3

Franchised dealers need

to find a retail model fit

for tomorrow’s world

WELCOME

[email protected] am-online.com/ami/am-online.com/linkedinam-online.com @amchatter facebook.com/automotivemanagementUK

f you have ever said to your teams the phrase “If you’re standing still, you’re also going backwards” then you should understand what the ‘Motor Retail in 2025’ theme of this issue of AM stands for. Business, consumer habits and certainly technology do not stay the same for long, and it is foolish to put all your focus on today, because all too quickly it will become yesterday.In 1885, Carl Benz completed the world’s first car, the Benz Patent

Motor Car. By 1910, Ford Motor Company was producing the world’s first mass production car, the Model T, in 93 minutes, making motorised transport affordable for the world’s middle classes. That same year, Henry Ford met UK entrepreneurs involved in bicycle sales and repair, and horse and carriage hire, and encouraged them to adapt to the new mobility revolution.

Today, the car brands you represent will already have their next-generation models hidden away in a design studio somewhere, likely accompanied by top-secret sketches and scale clay models of the cars to come even after that. Their research and development (R&D) programmes force them to predict what the consumer may want six, seven or more years ahead.

But what about the retail side of the automotive industry? The industry observers to whom AM has spoken agree that important changes to motor retail are just two five-year business plans away. Even more dramatic change could be coming another 10 years after that. Technology is empowering consumers with greater choice, and automotive managers must adapt and cater for that choice.

So are you ready?

I

Tim RoseEditor

27

34

4 July 2016 am-online.com

ASE ......................................................................17, 28

Auto Trader .......................................................11, 36

Automotive Property Consultancy .................34

AutosOnShow.........................................................72

Autotorq .....................................................28, 34, 36

BCA .............................................................................19

Black Horse .............................................................17

Bluesky Interactive .......................................37, 72

BMW .............................................................................8

Cambria Automobiles .........................................75

Carwow .......................................................................8

CDK Global ..............................................................36

CitNow ......................................................................72

Close Brothers Motor Finance .........................17

FCA ...............................................................................8

FLA ............................................................................15

Frost & Sullivan ....................................................34

Hendy Group ..........................................................10

Honda ........................................................................81

ICDP ....................................................................28, 36

J Edgar & Sons.........................................................8

Jaguar Land Rover ..............................................10

Jardine Motors Group .....................................8, 75

JCT600 .......................................................................11

Lifestyle Europe ....................................................10

Lookers ....................................................................10

Manheim ...................................................................19

Marshall Motor Holdings ......................................7

Mazda........................................................................82

McLaren Automotive ...........................................78

MTBN ........................................................................28

NFDA ..........................................................................17

Peter Vardy .............................................................10

Rapleys .....................................................................34

Redspy ......................................................................28

Ridgeway Garages ..................................................7

Robert Stephens & Co ........................................34

Ron Brooks ................................................................8

SMMT ..................................................................13, 16

Suzuki .......................................................................22

Toyota ...........................................................................8

TrustFord .................................................................10

Vertu Motors ..........................................................10

Visualise ...................................................................38

Volkswagen .............................................................13

Volvo ...................................................................10, 38

D E A L E R S A N D S U P P L I E R S I N T H I S I S S U E :

In this issue July 2016

MOTOR RETAIL IN 2025AM TAKES A LOOK AT WHAT’S COMING DOWN THE ROAD IN AUTOMOTIVE RETAIL

PROPERTY: WHAT’S NEXT FOR THE BRICKS-AND-MORTAR DEALERSHIP?

78

22

am-online.com July 2016 5

For the latest motor retail industry news, visit am-online.comSign up to get AM news daily by email: am-online.com/newsletter

YOUR NEWS7 News insight Marshall Motor Holdings will tread

“slowly and carefully” to integrate Ridgeway Garages, following its £106.9 million takeover.

8 News digest Carwow takes action against BMW

over dealer listing ban; JCT600 posts 12% sales increase in its 70th year; Franchised dealers ‘charge 65% more for parts than the independent sector’.

MARKET INTELLIGENCE

15 Asians grow market share Despite slowdown by Mitsubishi and

Nissan, Japanese and Korean brands gain ground over European rivals.

16 New car registrations Fleet props up rise in monthly figures

as retail registrations fall for second month running.

16 Finance offers Volkswagen offers heavy discounts on

Q1 finance offers to offset post-dieselgate registrations decline.

19 Used cars Manheim’s average selling price for

ex-fleet vehicles dropped for the fourth straight month in May.

INSIGHT22 Suzuki Suzuki GB sales and marketing

director Dale Wyatt is looking beyond the numbers for his brand’s growth.

27 Motor retail in 2025 What will franchised dealer networks

look like in the middle of the next decade?

34 Property speculation Digital consumer habits and soaring

prices will change how automotive retailers view dealership property.

36 Showroom technology Self-service, virtual reality and smooth

digital-to-physical transitions loom large in the showroom of the future.

39 Prof Jim Saker’s view from the business school

Over the next decade, carmaker power will grow and independents will suffer, predicts Jim Saker.

47 ‘iPhonification’ and the motor trade

Philip Nothard looks at the future impact of data and digital devices.

AM BEST PRACTICE

NEW AND

USED

CARS

72 Video Video can boost service work, profits

and engagement, but experts say its key benefit is the trust it generates.

SHOWROOM78 McLaren 570GT The £154,000 super coupé is central

to McLaren’s plan to triple sales.

81 Honda HR-V Honda has made a series of films to

showcase the features of the HR-V.

82 Mazda2 Despite hiccups with its online offers,

Mazda2 registrations are soaring.

COMING SOON86 In August’s issue –

published July 22 Steven Eagell tells how a trio of

acquisitions puts his dealer group in a stronger position for growth; how to ensure suppliers live up to your expectations; reports from the AM/IMI People Conference; and the Suzuki Baleno reviewed.

MCLAREN 570GTA SUPERCAR FOR DRIVING EVERY DAY

SUZUKI‘MARKET SHARE IS NOT THE BE ALL AND END ALL’

NEWS INSIGHT S E N D U S Y O U R N E W S : n e w s d e s k @ a m . c o . u k

By Tim Rosearshall Motor Holdings has a delicate integration task on its hands after its acquisition of Ridgeway Garages.

Yet there is no reason to rush. Industry executives regard Ridgeway as a strong-performing business

with a respected workforce. One management source said Marshall is aware how highly Ridgeway’s staff regarded their energetic and charismatic leaders, chief executive John O’Hanlon and chairman David Newman, who stepped down after the sale. The source said Marshall would tread “slowly and carefully”.

Marshall has only recently integrated SG Smith, bought last November.

At a cost of £106.9 million, the Ridgeway takeover is the highest cost deal since 2010. There are clear geographical and brand considerations behind it. Ridgeway bridges the gap from Marshall’s heartland in East Anglia and East Midlands to its outlying dealerships in the West Country.AM understands Ridgeway chairman David Newman was

approached informally by another prospective buyer, which led Marshall to prepare its own bid. Marshall chief executive Daksh Gupta knows the Newbury-based premium brand dealer group well. He was briefly its managing director in 2008, before joining Marshall. After that, Gupta retained a non-executive role on Ridgeway’s board.

He stepped down from that role before beginning negotiations to buy Ridgeway.

Gupta said: “David Newman and his team have built an excellent business with fantastic senior management, great staff, strong performance and a similar culture to MMH.”

It is believed to be the fourth-biggest acquisition ever, behind the £504.2m paid by Pendragon to take over top 10 AM100 rival Reg Vardy in 2006, Inchcape’s £262.9m purchase of European Motor Holdings in 2007, and the £231.5m paid by Pendragon for CD Bramall in 2004.

Marshall funded the Ridgeway deal from its existing balance sheet capabilities, through releases of equity in stock and its leasing book, and expects it to create a significant uplift in profits.

The expected benefits include the additional choice that Marshall can offer customers, and increased career development opportunities for staff.

“Lots of what Ridgeway does is first-class, such as its social media presence. We will take what each party does best and roll them out across the new expanded business,” Gupta added.

The Ridgeway name will be retained until Marshall branding is introduced to the acquired sites in 2017/2018.

Marshall chief financial officer Mark Raban said: “This is massively significant in its earnings-per-share potential since we’re adding a business that, from a profitability perspective, is not that far off Marshalls. Last year, we made £23m EBITDA, Ridgeway just over £20m. So, it is almost doubling our earnings. It is transformational in terms of shareholder benefit.”

The positive outlook on performance, he said, was based on Ridgeway as a respected brand, in “great” locations, with more than 2% return on sales.

An industry analyst told AM that Marshall can now claim almost

am-online.com July 2016 7

Marshall will ‘tread carefully’ with Ridgeway integrationGeography and brand variety may bring post-acquisition management challenges

M

national coverage, which brings with it the challenges of complexity and maintaining effective management across a wide variety of brands and geography.

He added: “Over the past few years, there has been a slow, but steady, improvement in profitability, albeit from a low base.”

For four years out of the past 10, Marshall has had a return on sales (RoS) figure of near 0%. However, from breakeven in 2011, profits have climbed steadily to an RoS figure of 1.2% in 2015, despite its acquisitions being either neutral – Crystal Motor Group made an RoS of 1.3% in 2013, or challenging – Silver Street lost money prior to acquisition.

The analyst said: “Ridgeway, by contrast, has occasionally turned in an RoS at or above the fabled 2%. For the last three years, RoS has been around 1.5%, better than Marshall.

“In terms of franchise fit and geography, profitability and management resource, Ridgeway will undoubtedly be good for Marshall. Whether Marshall will be good for Ridgeway depends on the new combined management coping with the increase in complexity and developing the synergies that are available.”

Marshall has already announced new roles for some Ridgeway executives: operations director John Head becomes commercial director, and finance director Dan Taylor keeps the same role at Marshall, reporting to Raban.

Taking into account the amount of capital on its balance sheet, following its IPO, Marshall’s return on capital employed was just under 10%. In 2017, Raban said it will be more than 20%.

■ 2015 financials: £722.6m turnover, £20.2m EBITDA, 2.1% RoS■ Franchises: Audi (2), BMW/Mini (3), Jaguar (1), Land Rover (1), Maserati (1), Mercedes-Benz Cars (4), Mercedes-Benz Commercials (4), Škoda (3), Smart (3), Volkswagen Passenger Cars (4) and Volkswagen Commercial Vehicles (2).■ Other businesses: Ridgeway Select used car centres (5), TPS trade parts depots (2), bodyshops (2), standalone PDI centre.■ Founded in 1997 by David Newman with a single Volkswagen outlet on the carmaker’s sponsored retailer programme.

R I D G E W AY

M M H P R E - A C Q U I S I T I O N R I D G E W AY S I T E S A D D E D

“We will take what each

party does best and roll them out across the new expanded

business”Daksh Gupta, Marshall

8 July 2016 am-online.com

F O R D A I LY N E W S , V I S I T: a m - o n l i n e . c o m

S E N D U S Y O U R N E W S : n e w s d e s k @ a m . c o . u k

F O L L O W A M O N T W I T T E R : @ a m c h a t t e r

NEWS DIGEST11 Parts prices

Franchised dealers charge 65% more for parts than the independent sector, a report into the UK aftermarket shows.

JCT600 JCT600 celebrated double-digit growth in turnover for its 70th year in business, as sales rose 12% to £1.145bn.

13

T H E N E W S Y O U C A N ’ T A F F O R D T O H A V E M I S S E D

I N B R I E F

Carwow takes action against BMW over dealer listing ban

Carwow has appointed legal representa-tives in an attempt to lift a BMW UK ban on its franchised dealers using the online marketplace’s services.

Carwow chief executive James Hind said it had called in “specialists in competition law” as a last resort after talks with the manufacturer collapsed, leaving its retailers without the option of using the online platform.

The German brand has already been reported to the Competition and Markets Authority as part of the action.

Hind said: “Over some time, we have had talks with BMW retailers about their use of Carwow and it is an apparent source of frustration that BMW will not

allow them to use our service.“Due to BMW’s stance they simply cannot,

and it is them, and the customer, that is losing out.”

Asked whether BMW’s stance may be an effort to promote its own online marketing strategy – the brand will trial a used cars version of its AM Award-winning BMW Online Retail offering later this year – Hind said: “That could be the case.”

Hind said representatives from Carwow had held talks with officials from BMW UK, but he said they were “unwilling to move”.

A spokesman for BMW UK told AM the brand was aware of the legal situation.

“Carwow does not have any substance in European law in making their claim,” the spokesman said.

C A R W O W

J A R D I N E

Jardine Motors Group has acquired the bulk of Colliers Motor Group as part of a deal said to be driven by Land Rover’s “drive for a common ownership model”.

The purchase of Colliers’ single Land Rover, Honda and Mazda dealerships in Erdington as well as its Jaguar Tamworth site, means Jardine’s portfolio includes five Land Rover, six Jaguar, four Honda and its first Mazda franchise. Colliers will retain its one Nissan site.

Neil Williamson, Jardine Motors Group chief executive, said: “This new business will help drive forward our ambitious growth plans for 2016.”

Work has already started on a multi-million-pound development for Land Rover in Wolverhampton and the group is on a recruitment drive in the Midlands, creating more than 70 jobs across all levels and departments.

Jardine then did a sale and leaseback deal with Knight Frank for the former Colliers properties and rased £17 million.

It is the first new-generation Land Rover facility to be traded in the investment market.

R O N B R O O K SRon Brooks Group has opened a new eight-car Mansfield Suzuki showroom following seven months of building. The dealership, on Oak Tree Lane, continued trading from tempo-rary accommodation at the site during construction.

F C AThe Financial Conduct Authority (FCA) has announced that a full representative example and APR is no longer needed in an advertisement where there are no credit charges and the APR is 0%. The new rule applies to all 0% finance offers.

J E D G A R & S O NNissan dealer J Edgar & Son has completed the extension and refurbishment of its showroom at Rowrah, Cumbria, adding 80 square metres of space, to take the facility to a total of 450 sq m.

T O Y O TAToyota is considering legal action against the Vote Leave campaign after it used a Toyota logo on an EU Referendum flyer. Toyota said the flyer “could mislead the reader into thinking Toyota endorses the Vote Leave campaign” and added: “We offer no such endorsement and further we are considering a formal legal complaint.”

‘ C H AV C H A R I O T ’A car dealer listed a BMW as a ‘rusty chav chariot’ in an online ad. Richard Harris, sales manager at Classic Cars of Wirral, was so shocked at the condition of the 1998 BMW 318, he wrote: “If in doubt, please presume all parts of the car are either broken, rusty, or covered in some kind of dubious residue.”

It attracted more than 30 bids.

10 July 2016 am-online.com

NEWS DIGEST

wP E O P L E N E W S

A NDR E W S T EP HEN S O N

Lookers has appointed Andrew Stephenson as group human resources and

customer director.

J O N WA K EFIEL DVolvo Car UK has appointed Jon Wakefield as its acting managing director. Wakefield

succeeds Nick Connor, who will become chief executive of Polestar on July 1.

C A MERO N WA DEFormer Peter Vardy commercial director Cameron Wade has been appointed as managing director of

the AM100 group’s motor division.

PAU L L O W D O NPaul Lowdon has officially taken up his new post as general manager of Vertu Group Fleet

following the retirement of David Jewell last in April. Jewell retired after nine years of service and 48 years in the motor industry.

J O N HE A DMarshall appointed Jon Head as commercial director following its £106.9 million acquisition of Ridgeway. Head, formerly Ridgeway’s operations director, assumes responsibility for aftersales development, F&I, CRM, marketing and purchasing.

PAULINE ANN BESTFormer Specsavers and Vodafone director Pauline Ann Best has joined the board of Vertu

Motors. Best joined on June 1 as a non-executive director, and will sit as a member of Vertu’s nominations committee and remuneration committee.

TrustFord has brought together its two former operations in Epsom in a £4 million new FordStore in the town.

The new site is on the Longmead Industrial Estate and replaces the previous TrustFord Epsom dealerships at Kiln Lane and East Street.

A dedicated Transit Centre is included within the facility, which carries the complete range of 22 Ford vehicles – both car and commercial. It also features a further 100 display spaces for used vehicles.

The FordStore features an 18-vehicle showroom, interactive displays, colour walls and a customer seating zone with free Wi-Fi and USB connectivity.

Supported by a team of 50 specialists, the 17-bay workshop has extended opening hours, from 7am to 7pm, designed to allow customers to drop off and collect their vehicles before and after work.

Vertu Motors has bought the five-site Gordon Lamb Group and gained its first Toyota dealership.

The £18.7 million takeover of the family-run group also adds Vertu’s sixth Land Rover dealership, plus the Toyota site and additional Nissan and Škoda businesses, all in Chesterfield, and a Škoda outlet in Derby.

Gordon Lamb has traded in Derbyshire for more than 60 years, and recorded £85.8m turnover in 2015. Vertu said the acquisition progresses its strategic goal of growing its range of franchises.

The transaction includes goodwill of £8.3m and freehold properties valued at £7.5m.

Robert Forrester, Vertu Motors chief executive, said: “Gordon Lamb is a much respected and well established business operating in Derbyshire, a core territory of ours. It is a business we have long admired and I am delighted to welcome them to the Vertu group. I see a very clear cultural, strategic and business fit.”

Vertu said the new additions will be earnings-enhancing – in 2015 Gordon Lamb achieved adjusted EBITDA of £2.9m and adjusted PBT of £2.7m.

Jaguar Land Rover said it has “delivered everything it said it would deliver” to its retail network after achieving an 84% rise in fleet sales during Q1.

Jaguar’s fleet sales grew by 194% and Land Rover’s by 53% compared with the same period in 2015 as the brands benefited from new models such as the XE saloon and F-Pace SUV and the popularity of its sub-100g/km CO2 2.0-litre Ingenium turbodiesel engine.

JLR managing director Jeremy Hicks told AM the growth was the result of a retail plan that put greater emphasis on 50 UK-wide fleet specialists to grow sales.

“We sat down three years ago and developed our growth plan. It was set in stone. That drove the require-ment for 50 fleet specialists.

“It’s not about saying ‘I can sell them’, it’s about an ability to store, repair and deliver them.

“I can stand in front of the retailers now and say everything we said we’d deliver we have delivered.”

Land Rover’s Q1 retail registra-tions grew 10.8% year-on-year; with Jaguar rising 17.4%.

H E N D Y A U T O

Hendy Automotive Group has acquired Lifestyle Motor Group, which should see the newly formed Hendy Automotive Limited achieve a turnover of £600 million, placing it in the top 25 of the AM100.

The Lifestyle Motor Group, formed in 2001, operates Ford, Mazda, Kia, Renault, Dacia, Seat, Suzuki and Isuzu franchises in the South East.

Lifestyle Europe chairman Marc Matthew said: “We have built up a strong, profitable and successful business in Kent, Sussex and Surrey and believe this growth will continue with Hendy’s.”

Hendy recorded a turnover of £357m in 2015 and Lifestyle £187m. The new company has 12 motor franchises at 25 locations in Surrey, Sussex, Kent, Hampshire, and Devon.

The group employs about 1,000 staff and is expected to sell more than 40,000 vehicles a year from its dealerships and two used car stores.

V E R T U

J L RT R U S T F O R D

am-online.com July 2016 15

MARKET INTELLIGENCE T H E N E W S I N D E P T H

16New cars

Fleet props up rise in monthly figures as retail registrations fall for second month running.

16Finance

Volkswagen offers heavy discounts on Q1 finance offers to offset post-dieselgate registrations decline.

Sponsored by

Asian brands slowly eating share from European rivalsNissan and Mitsubishi hinder Japanese brands’ growth as Koreans gain ground

17Dealer profits

Average dealer made £9,000 profit in April, up from £6,000 a year earlier.

he brands from the Far East are slowly eating into the share of the UK new car market that was traditionally held by

mainstream European carmakers.The nine Japanese and three

South Korean carmakers operating in the UK have taken a combined 23.5% share of the UK’s new car registrations so far in 2016. That is a 2.6ppt gain over the past five years – for the first five months of 2011, their combined share was 20.9%.

However, SMMT data shows that declines by Nissan and Mitsubishi this year, after record performances in 2015, seem to be threatening the Japanese brands’ trend of growth. This is despite Honda and Suzuki increasing sales thanks to better product supply, marketing activity and stronger finance offers.

At the end of May, the Japanese brands held a 16.6% year-to-date share, their second-highest this decade, but down 0.2ppts on the same period in 2015. The star performers in the Japanese camp so far this year are Honda and Mazda, although both are still clawing their way back to the level they enjoyed at the turn of the decade.

The Korean brands, however, are

T

Showroom finance for new cars rose 12% in April, according to the Finance & Leasing Association (FLA).

By value, the finance provided was 17% ahead of April 2015.

Penetration continues to rise, fuelled by PCP and PCH offers. The percentage of private new car sales financed by FLA members through the point of sale (POS) reached 83.6% in the 12 months to April, up from 82.7% in the 12 months to March.

The POS consumer used car finance market also reported further new business growth in April of 9% by value and 8% by volume.

Geraldine Kilkelly, head of research and chief economist at the FLA, said: “Growth in new business volumes reported by the POS consumer car finance market was relatively steady in April and in line with the industry’s expectations of achieving solid single-digit growth in 2016 as a whole.”

F I N A N C E S TAT S

A S I A N B R A N D S ’ M A R K E T S H A R E ( % ) – Y E A R T O M AY 3 1

A P R I L M O T O R F I N A N C E M A R K E T: N E W C A R S

New cars bought on finance by consumers through dealerships

Apr 2016 Change on 3 months Change on 12 months Change on previous year to Apr 2016 previous year to Apr 2016 previous year

Value of advances (£m) 1,456 +17% 5,460 +18% 17,215 +18%

Number of cars 85,436 +12% 321,189 +12% 1,026,978 +12%

New cars bought on finance by businesses through dealerships

Number of cars 51,182 -3% 140,755 +4% 513,931 +3%

Source: FLA

slowly gaining ground again. Together, Hyundai, Kia and SsangYong account for a 6.8% slice of 2016’s new car market to date, with 0.2ppts of growth after three years flatlining around the 6.6% mark.

Among the South Korean brands, Hyundai’s performance is flat, although the activity it is under-taking as a sponsor of the Euro 2016 tournament may restart growth in the months ahead. Nevertheless, Kia is in growth thanks largely to the new Sportage, and niche 4x4

specialist SsangYong has doubled its share now its award-winning Tivoli small crossover is in the market.

The march of the Asian brands is likely to continue. Toyota and Kia both have B-segment SUVs – badged C-HR and Niro respectively – waiting in the wings and ready to compete in a growing market segment. Toyota also has an MPV version of the Proace on the way, Hyundai has a hybrid Ioniq, and in 2017 Honda launches a new Civic while Nissan will revise its segment-leading Qashqai.

JAPANESE 2016 2015 2014 2013 2012 2011 2010

Honda 2.34 2.08 2.37 2.61 2.51 2.68 3.13

Infiniti 0.09 0.05 0.02 0.02 0.03 0.02 0.00

Lexus 0.52 0.51 0.43 0.36 0.45 0.42 0.33

Mazda 1.92 1.79 1.62 1.39 1.49 1.67 2.28

Mitsubishi 0.80 0.99 0.45 0.49 0.36 0.61 0.49

Nissan 5.56 6.05 5.42 5.38 4.97 4.71 3.85

Subaru 0.13 0.13 0.10 0.10 0.13 0.17 0.20

Suzuki 1.42 1.30 1.55 1.48 1.22 1.05 1.08

Toyota 3.83 3.94 3.99 4.10 4.40 3.86 4.47

KOREANS 2016 2015 2014 2013 2012 2011 2010

Hyundai 3.42 3.44 3.36 3.37 3.20 3.10 3.79

Kia 3.26 3.09 3.17 3.21 3.17 2.62 3.29

SsangYong 0.17 0.09 0.06 0.03 0.04 0.00 0.02

18 July 2016 am-online.com

MARKET INTELLIGENCE

Growth appears to be slowing. Last month, there were still two brands with more than 100% year-on-year growth: Infiniti and SsangYong. This month there are none.

With its new XE, XF and now F-Pace in showrooms, Jaguar’s registrations are 5,993 units ahead year-on-year and it is gaining market share fast. A strong May has also pushed its sister brand Land Rover into the top 10 – the SUV specialist is 5,770 registrations ahead.

Between them, volume brands Volkswagen, Vauxhall, Peugeot and Nissan have lost 15,252 sales so far this year.

R I S E R S & F A L L E R S

10

10

TOP

BOTTOM

10-year market trends available: www.am-online.com/amiN E W C A R R E G I S T R AT I O N S

*Citroën’s monthly registrations included DS until May 2015. As the Citroën result for May 2015 is for both brands, please combine the Citroën and DS registrations for May 2016 when comparing year-on-year.

May Year-to-date

Marque 2016 % market share

2015 % market share

% change

2016 % market share

2015 % market share

% change

Ford 23,740 11.66 24,273 12.22 -2.20 140,948 12.10 144,095 12.88 -2.18

Vauxhall 16,300 8.01 20,698 10.42 -21.25 107,369 9.22 112,412 10.05 -4.49

Volkswagen 16,050 7.88 17,316 8.71 -7.31 90,370 7.76 96,394 8.61 -6.25

BMW 15,423 7.58 12,206 6.14 26.36 72,898 6.26 63,121 5.64 15.49

Audi 13,970 6.86 13,802 6.95 1.22 75,018 6.44 71,985 6.43 4.21

Mercedes-Benz 13,721 6.74 11,355 5.71 20.84 73,037 6.27 61,748 5.52 18.28

Nissan 10,925 5.37 11,561 5.82 -5.50 64,797 5.56 67,652 6.05 -4.22

Peugeot 8,208 4.03 6,922 3.48 18.58 46,003 3.95 47,333 4.23 -2.81

Hyundai 7,232 3.55 7,045 3.55 2.65 39,783 3.42 38,539 3.44 3.23

Toyota 7,144 3.51 7,300 3.67 -2.14 44,576 3.83 44,144 3.94 0.98

Kia 6,912 3.40 6,133 3.09 12.70 37,940 3.26 34,541 3.09 9.84

Land Rover 6,290 3.09 4,966 2.50 26.66 36,890 3.17 31,120 2.78 18.54

Renault 6,259 3.07 5,453 2.74 14.78 35,414 3.04 30,186 2.70 17.32

Škoda 6,159 3.03 5,914 2.98 4.14 33,198 2.85 31,333 2.80 5.95

Citroën* 5,783 2.84 6,301 3.17 -8.22 31,776 2.73 38,017 3.40 -16.42

Mini 5,073 2.49 5,239 2.64 -3.17 25,245 2.17 24,138 2.16 4.59

Fiat 4,327 2.13 4,370 2.20 -0.98 26,882 2.31 26,114 2.33 2.94

Honda 4,243 2.08 3,624 1.82 17.08 27,305 2.34 23,259 2.08 17.40

Seat 3,499 1.72 4,595 2.31 -23.85 20,389 1.75 22,278 1.99 -8.48

Volvo 2,973 1.46 3,192 1.61 -6.86 17,805 1.53 16,839 1.50 5.74

Mazda 2,862 1.41 2,718 1.37 5.30 22,367 1.92 20,062 1.79 11.49

Suzuki 2,738 1.34 2,589 1.30 5.76 16,586 1.42 14,598 1.30 13.62

Jaguar 2,590 1.27 1,579 0.79 64.03 13,675 1.17 7,682 0.69 78.01

Dacia 2,137 1.05 2,046 1.03 4.45 11,488 0.99 11,895 1.06 -3.42

DS* 1,478 0.73 26 0.01 5,584.62 7,664 0.66 26 0.00 29,376.92

Mitsubishi 1,310 0.64 1,608 0.81 -18.53 9,287 0.80 11,048 0.99 -15.94

Jeep 1,078 0.53 1,109 0.56 -2.80 6,127 0.53 4,436 0.40 38.12

Porsche 1,023 0.50 1,136 0.57 -9.95 5,710 0.49 5,188 0.46 10.06

Smart 1,001 0.49 705 0.35 41.99 4,738 0.41 2,716 0.24 74.45

Lexus 874 0.43 959 0.48 -8.86 6,046 0.52 5,689 0.51 6.28

Alfa Romeo 337 0.17 447 0.22 -24.61 2,290 0.20 2,184 0.20 4.85

SsangYong 310 0.15 189 0.10 64.02 1,950 0.17 976 0.09 99.80

MG 296 0.15 269 0.14 10.04 1,560 0.13 1,436 0.13 8.64

Abarth 282 0.14 181 0.09 55.80 1,596 0.14 868 0.08 83.87

Subaru 246 0.12 249 0.13 -1.20 1,503 0.13 1,422 0.13 5.70

Infiniti 137 0.07 98 0.05 39.80 996 0.09 505 0.05 97.23

Maserati 129 0.06 122 0.06 5.74 550 0.05 645 0.06 -14.73

Bentley 120 0.06 74 0.04 62.16 773 0.07 584 0.05 32.36

Aston Martin 67 0.03 68 0.03 -1.47 382 0.03 403 0.04 -5.21

Lotus 20 0.01 18 0.01 11.11 131 0.01 153 0.01 -14.38

Other British 98 0.05 62 0.03 58.06 347 0.03 323 0.03 7.43

Other Imports 221 0.11 184 0.09 20.11 1,458 0.13 872 0.08 67.20

Total 203,585 198,706 2.46 1,164,870 1,119,072 4.09

SsangYong 99.80%

Infiniti 97.23%

Abarth 83.87%

Jaguar 78.01%

Smart 74.45%

Jeep 38.12%

Bentley 32.36%

Land Rover 18.54%

Mercedes-Benz 18.28%

Honda 17.40%

Peugeot -2.81%

Dacia -3.42%

Nissan -4.22%

Vauxhall -4.49%

Aston Martin -5.21%

Volkswagen -6.25%

Seat -8.48%

Lotus -14.38%

Maserati -14.73%

Mitsubishi -15.94%

Maserati -14.73%

Mitsubishi -15.94%

am-online.com July 2016 19

Sponsored by

E C O N O M I C I N D I C AT O R S

+2.3%Average regular pay, excluding bonuses, was £470 a week before tax and other deduc-tions between February and April, up 2.3% on a year earlier. Average total pay, including bonuses, was £503 per week, up 2% on a year earlier.

➡

PAY

The unemployment rate was 5%, the lowest since August to October 2005, 0.1ppts down on January to March.

-0.1PPTS

➡ UNEMPLOYMENT

The Council of Mortgage Lenders reported that first-time buyers borrowed £3.9bn in April, down 11% on March, but up 15% on April last year. This totalled 25,100 loans, down 9% month-on-month but up 7% year-on-year.

+15%➡

MORTGAGES

There were 217 million purchases in April, with a total value of £12.2 billion, said the British Banking Association. That was down from March’s 223m purchases, worth £12.6bn.

-3.2%➡CREDIT CARD BORROWING

As of April 2016, the average house price in the UK is £209,054. Property prices have risen by 0.6% compared with the previous month and are 8.2% higher than April 2015.

+8.2%➡

HOUSE PRICES

Used cars bought on finance by consumers through dealerships

Apr 2016 Change on 3 months to Change on 12 months to Change on previous year Apr 2016 previous year Apr 2016 previous year

Value of advances (£m) 1,163 +9% 3,530 +13% 12,663 +13%

Number of cars 109,821 +8% 332,188 +10% 1,189,649 +10%

Used cars bought on finance by businesses through dealerships

Number of cars 2,983 -6% 9,516 -10% 37,312 -8%

Source: FLA

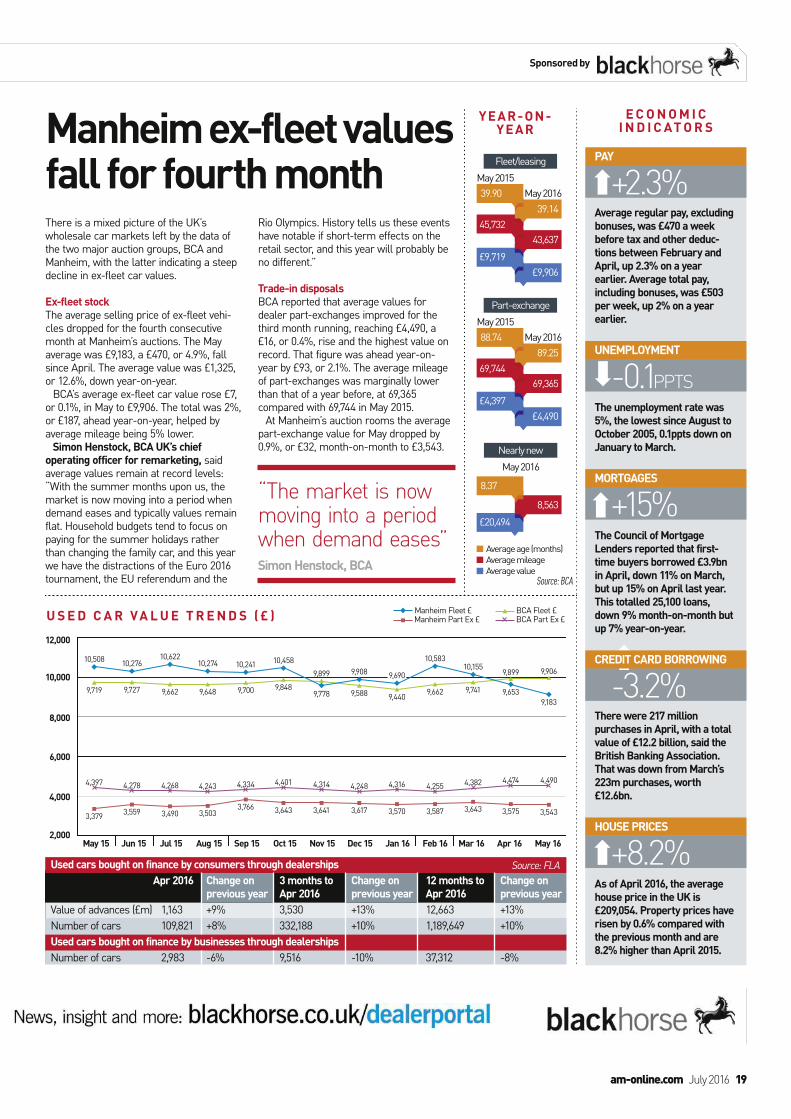

Manheim ex-fleet values fall for fourth monthThere is a mixed picture of the UK’s wholesale car markets left by the data of the two major auction groups, BCA and Manheim, with the latter indicating a steep decline in ex-fleet car values.

Ex-fleet stockThe average selling price of ex-fleet vehi-cles dropped for the fourth consecutive month at Manheim’s auctions. The May average was £9,183, a £470, or 4.9%, fall since April. The average value was £1,325, or 12.6%, down year-on-year.

BCA’s average ex-fleet car value rose £7, or 0.1%, in May to £9,906. The total was 2%, or £187, ahead year-on-year, helped by average mileage being 5% lower.

Simon Henstock, BCA UK’s chief operating officer for remarketing, said average values remain at record levels: “With the summer months upon us, the market is now moving into a period when demand eases and typically values remain flat. Household budgets tend to focus on paying for the summer holidays rather than changing the family car, and this year we have the distractions of the Euro 2016 tournament, the EU referendum and the

Rio Olympics. History tells us these events have notable if short-term effects on the retail sector, and this year will probably be no different.”

Trade-in disposalsBCA reported that average values for dealer part-exchanges improved for the third month running, reaching £4,490, a £16, or 0.4%, rise and the highest value on record. That figure was ahead year-on-year by £93, or 2.1%. The average mileage of part-exchanges was marginally lower than that of a year before, at 69,365 compared with 69,744 in May 2015.

At Manheim’s auction rooms the average part-exchange value for May dropped by 0.9%, or £32, month-on-month to £3,543.

“The market is now moving into a period when demand eases”Simon Henstock, BCA

YEAR-ON- YEAR

May 2015

May 2016

£9,906

£9,719

Fleet/leasing

45,732

43,637

39.90

39.14

Average age (months)Average mileageAverage value

May 2015

May 2016

£4,490

£4,397

Part-exchange

69,744

69,365

88.74

89.25

May 2016

£20,494

Nearly new

8,563

8.37

BCA Fleet £ BCA Part Ex £

Manheim Fleet £ Manheim Part Ex £

2,000

4,000

6,000

8,000

10,000

12,000

Apr 16 May 16Sep 15 Oct 15 Nov 15 Dec 15 Jan 16May 15 Feb 16 Mar 16Jun 15 Jul 15 Aug 15

U S E D C A R VA L U E T R E N D S ( £ )

3,3793,559 3,490 3,503

3,766 3,643 3,641 3,617 3,570 3,587 3,643 3,575 3,543

4,397 4,278 4,268 4,243 4,334 4,401 4,314 4,248 4,316 4,255 4,382 4,474 4,490

10,50810,276

10,62210,274 10,241

10,458

9,908

10,58310,155

9,6539,183

9,690

9,7789,719 9,727 9,662 9,648 9,700 9,8489,588 9,440

9,662 9,741

9,899 9,9069,899

Source: BCA

utomotive Management Live is a day-long exhibition packed with innovative ideas, best-practice advice and the latest products for used car retailers and franchised dealers, who are invited to attend for free.

Taking place across 2,800 square metres of floor space at the Arena MK, Milton Keynes, the expo will also feature product launches, grand prize draws and business-boosting drop-in clinics, as well as legal and regulatory updates to help bring all of your industry knowledge up to date.

Stephen Briers, editor-in-chief of AM, said: “We’re really excited to be launching this new event for the UK’s motor retail industry in 2016. We expect it to become one of our flagship events, alongside the AM Awards and AM100 Dinner, because the quality and breadth of information will be essential for people employed in motor retail at any level.”

Sue Robinson, director of the NFDA, said: “We are delighted be part of this important event for the motor industry and would encourage all dealers to participate from all sectors of their business.”

Demand is strong, so visit automotivemanagementlive.co.uk now to register and we look forward to seeing you on November 16.

Find out more and register (dealers go FREE) at: automotivemanagementliv

AM is pleased to bring you its biggest daytime motor industry event yet

A

6 July 2016 am-online.com

*SO FAR...

16 November 2016

Milton Keynes Arena

01733 468325

automotive-management-live.am-online.com

61 EXHIBITORS*

38 SECTORS*

15 SPEAKERS8 MASTERCLASSES1 INSPIRING EVENTNOVEMBER 16, 2016, ARENA MK, MILTON KEYNES

*SO FAR...

REGISTRATION

NOW OPEN!

ntlive.co.uk. Tweet us on @AMLive2016 if you are attending #AMLive

The F&I Theatre The F&I Theatre will be your place to learn the latest on Financial Conduct Authority (FCA ) regulation in an engaging, interactive way.

Best-practice masterclassesAs part of AM’s Best Practice Programme, industry experts will share their most effective working methods and crucial advice in a dedicated masterclass area throughout the day.

CitNOW: How video is forging customer relationships, sales and retentionThe opportunity to use video throughout the customer lifecycle is huge. CitNOW will explain video relationship marketing (VRM) and show how manufacturers and dealers have adopted this.

Cooper Solutions: The modern auction as part of the new and used car strategyExploring the role of both physical and online auctions and the appraisal process as vital elements of the dealership’s new and used car strategy.

eDynamix: Boosting customer loyalty via aftersalesThis session discusses how aftersales can maximise the dealership’s customer retention capability, confronts issues such as migration to the independent sector and explores wider opportunities.

GForces: The continually evolving digital landscapeGForces will highlight how the fast-paced digital environment continually develops and evolves and outlines some of the best practices currently in operation.

iVendi: Understanding consumer online finance behaviouriVendi draws on its data and detailed analysis to show how finance and the availability of information online can sway the car-buyer’s decision to visit a dealership and other insights into the car-buyer’s online behaviour.

JudgeService: From purchase to retention, the customer review cycleThis session underlines the hugely influential role fellow consumers play in a customer’s decision to buy. It will encourage dealers to think holistically about the entire purchase journey including how consumers research their next vehicle, the purchase experience, customer reviews, retention and repurchase.

Marketing Delivery: The maturing of social mediaTackling issues such as balancing organic and paid-for reach, local content, the dominance of mobile and relevant analytics, this session promises to bring you up-to-date with the latest thinking, trends and influences.

Supagard: Developing a sustainable new car strategyExploring the new car market and areas that require the dealer’s focus in order to maximise profitability and best prepare for the future.

am-online.com July 2016 7

ALPHERA Financial ServicesCreating a win-win approach to customer financeExploring the motor finance landscape in the context of increasing competition, evolving consumer demands and regulatory impacts, Alphera draws upon its decade of experience in the UK market to share knowledge and deliver skills-oriented workshops. These will feature practical ideas that can be implemented in dealerships, as well as some ‘must-do’ finance top tips.

Car Care PlanInsurance products, regulation, customer satisfaction and profitabilityStringent regulations under the FCA are creating a very different sales environment for insurance products. This session looks at the latest developments and how best practice has evolved since the introduction of new GAP rules. It also explores the increasing role of online in customer engagement and alternative methods of purchase to the traditional point of sale.

Legal advice clinicIndependent legal advisers to the automotive sector, Lawdata will be on hand to answer individual queries in the Automotive Management Live Legal Advice Clinic. Dealers will be able to raise any areas on which they would like a legal view. Lawdata expects questions on legal developments such as the Consumer Rights Act, employment law and compliance queries.

Exhibitors

So far, 61 exhibitors from 38 industry sectors – including website designers, legal experts, finance providers and remarketing firms – have signed up to appear.

AA Garage GuideAlphera Financial ServicesASEAutomotive ComplianceAutos on showAutoWeb DesignAutovoloBCABuyacarCall it Automotive Car Care PlancarwowCBW DesignCitNOWCodeweaversCooper Solutions

Dealer Management ServicesDiamondbriteDrive Development SolutionsDSG GroupDuraEDT AutomotiveEMaCeDynamixGardX InternationalGemini Computer SystemsGForcesHitachi Capital Consumer FinanceHowes PercivalIn-AutomotiveInsurethatiVendi

JudgeServiceLawdataManheim Remarketing Marketing DeliveryMoneypennyMotors.co.ukMovexNextgear CapitalNFDA Nick Stone MediaPentana SolutionsPerfect ChannelPremia SolutionsProduct PartnershipsQuid Car AdsRDS Global

Reef Business SystemsReynolds & ReynoldsRhino EventsRotary LiftSearch OpticsSpidersnetSupagardT Cards DirectTitan Dealer Management SolutionsTotal UKTRACS SolutionsVE InteractiveWMG

78 July 2016 am-online.com

On the fast track to 4,000 cars a yearThe £154,000 570GT is central to McLaren Automotive’s plan to double UK registrations and almost triple production

development, said the five-year-old manufacturer, which is poised to announce a third consecutive year of profitability, has high hopes for the new model.

Managing demand for the product is already a key priority, with a seven-month lead time for customers and impressive performance expected within the increasingly important McLaren Qualified approved used programme. Residual values for the 570GT (3yr/30,000 miles) are expected to be on par with the 570S’s 63% – some 18% better than a Porsche 911 Turbo S.

Grose said: “Our 80 retailers will soon be receiving their allocation of a showroom car and a demonstrator and the challenge for them will perhaps be persuading customers that they can’t have those cars and have to wait.

“McLaren is intent on maintaining its exclusivity, so we will never produce more than around 4,500 cars a year and that will make the job of managing lead times quite difficult.”

Although the 570GT is intended for everyday driving, it still

By Tom Sharpe

herever McLaren Automotive moves, it moves at speed and its Sports Series is about to usher in a period of growth that it says will see production grow from about 1,400 cars a year to more than 4,000.

Billed as an “everyday driver”, the £154,000 570GT is its most luxurious, refined and comfortable sports car yet, according to McLaren.

Unveiled at the Geneva Motor Show in March and now offi-cially heading into the UK’s five McLaren Automotive show-rooms (soon to be six, with the imminent opening of Rybrook Holdings’ facility at Bristol’s Cribbs Causeway), the Surrey-based brand’s latest creation could be its most important yet.

In 2015, McLaren produced a total of 1,654 vehicles, with UK registrations of 171 up from 121 in 2014, and the expectation is to double that figure this year.

Geoff Grose, McLaren Automotive head of vehicle

W

F I R S T D R I V E : M C L A R E N 5 7 0 G T

SHOWROOM T H E C A R S D R I V I N G Y O U R B U S I N E S S

Honda HR-VHonda has made a series of films to showcase the features of the HR-V.

Mazda2Despite a few hiccups with its online offers, registrations of the Mazda2 are soaring.

Read our interview with McLaren’s sales and marketing director, Jolyon Nash, from the February issue of AM, at am-online.com/mclaren-profile

81 82

SPECIFICATION

Price from £154,000

Engine 3.8-litre twin-turbocharged, 564bhp

Performance 0-62mph 3.4 seconds; top speed 204mph

Transmission 7sp automatic

Efficiency 26.6mpg, 249g/km CO2

RV 3yr/30k 63% (est)

Rivals Porsche 911 Turbo S, Audi R8

am-online.com July 2016 79

TOP GEARThe GT is elegant and understated. But there’s nothing under-stated about the way it lights your fire when you point it down a cursive road.

THE TELEGRAPHThe 570GT proves that by dialling back on the numbers, McLaren is learning to make a great road car as well as a track car.

EVOIt may be the most refined, luxurious and ‘long-trip’ McLaren ever made – but its DNA is still laced with sports car genes.

“The challenge for [retailers] will perhaps be persuading customers that they have to wait” Geoff Grose, McLaren

The 570GT’s doors now open more vertically,

improving access in tight parking spaces

The interior is the most plush of the

Sports Series range

WHAT YOUR CUSTOMERS WILL READ ABOUT THE MCLAREN

570GT

F O R M O R E R E V I E W S V I S I T: w w w . a m - o n l i n e . c o m / r o a d t e s t s

takes its performance credentials very seriously – it can accelerate to 62mph in a searing 3.4 seconds and on to a 204mph top speed. It is fitted with a 3.8-litre twin-turbo-charged V8, delivering 564bhp and 443lb-ft of torque.

Fuel efficiency claims of 26.6mpg on the combined cycle and CO2 emissions of 249g/km do not scream practicality, but with a design fundamentally changed from that of the more performance-focused £147,000 570S, the 570GT has introduced a side-opening rear glass hatch, underneath which lies a 220-litre luggage space. In addition to the 150 litres of space available under the bonnet, the result is a load space equivalent to that found in a BMW 1-Series.

A panoramic glass roof continues the theme set by that glass rear hatch, allowing light to flood into a leather-wrapped interior. This features prominent areas of the carbon-fibre trim that defines the look of many McLaren products, but the interior of the 570GT is more plush than anything found elsewhere in the comparatively pared back and driver-focused Sports Series range.

The glass roof uses McLaren’s Sound and Solar Film to cut down glare and deaden noise. McLaren has also worked with Pirelli to develop a set of P Zero tyres, which incorporate the French brand’s patented Pirelli Noise Cancelling tech-nology to deliver a more refined ride.

The carbon-fibre tub that forms the lightweight (just 75kg) and rigid core of all McLaren Automotive products has been modified to be both lower and narrower at the front end of the door sill to allow easier access and the trademark dihe-dral doors now open more vertically, bringing improved access in tight parking spaces.

One area where retailers will be keen to see developments is in the McLaren Special Operations (MSO) division headed by executive director Paul Mackenzie.

Mackenzie told AM that MSO is becoming more and more involved in the early development of cars to come up with a range of personalised options.

He said: “The MSO products represent a huge and growing opportunity for retailers. We have seen that many are making great profits by really embracing the concept, while others are more apprehensive, but the benefits for them are obvious.

“Many of the bespoke parts on the newer cars have been

redesigned to allow them to be fitted by the retailer and that’s all part of the move we need to make as volumes grow and retailers gain the ability to realise greater profits.”

While desirable options will benefit dealers, the 570GT’s design, by chief designer Robert Melville, is described by the Yorkshireman as McLaren’s most “classically graceful”.

A rear spoiler – 10mm taller than the 570S – helps to reduce lift at speed and huge air intakes down each flank aid cooling on the turbocharged V8.

On the road, the 570GT – riding on conventional springs with damping some 15% softer than the 570S – provides a supple ride. At motorway speeds, a degree of roll can even become apparent.

The ability to affect both handling and drivetrain via two dials on the centre console means the driver can tune the car through Normal, Sport and Track settings.

In Normal, the car is relaxed and remarkably refined, albeit still hugely fast when called upon.

Sport tightens the ride up and sharpens the gear shifts of the seven-speed automatic gearbox which can be operated manually via a pair of F1-style, steering-wheel paddles.

Adjusting suspension, drivetrain and stability systems still further, Track is best preserved for circuit driving.

Whip-crack gear-changes and surging acceleration is a given in this supercar-quick slice of advanced British engineering.

The combination of performance and finesse is expected to see the 570GT account for 40% of all sales generated from the three-model Sports Series range made up by the 540C (£126,000), 570S and 570GT, which itself is anticipated to account for two thirds of all McLaren sales in the coming 12 months.

McLaren Automotive powertrain director, Richard Farquhar, said: “The reaction to the 570GT has been amazing.

“Everyone in the business has to step back and realise what we are all part of at the moment. From the designers to the engineers and the production teams and retailers: we are building what will hopefully be a truly iconic brand for decades to come.”

The Japanese brand launches new technology in this not-so-mini supermini.

First drive: Suzuki Baleno

86 July 2016 am-online.com

IN AUGUST’S ISSUE PUBLISHED JULY 22

A D V E R T I S E R S ’ I N D E X

Accident Exchange ...........................26

Aston Barclay .....................................80

Autoclenz ............................................76

Autotech Recruit ...............................83

Autotorq ...........................30, 31, 32-33

Autoweb Design ................................46

Barclaycard Loans .............................2

British Car Auctions ...................76, 85

Call It Automotive .............................83

Carwow .........................................48-49

Castrol .................................................24

CDK Global (UK) ..........................44-45

Chris Eastwood Automotive ..........85

Cooper Solutions .........................50-51

Dealer Management Services.......25

Dennis Buyacar ...........................52-53

Drive Group.........................................35

Enquiry Max ..........................54-55, 85

Exchange Enterprises .......................9

Gardx International ....................56-57

Hitachi Capital Consumer Finance ....

..........................................................58-59

Infomedia ...............................60-61, 88

Ivendi ..............................................12, 82

John W Groombridge .......................80

Karcher (UK) ......................................77

Lawdata ...............................................77

Lloyds Banking Group ...............14, 17

Mapfre Abraxas UK ....................62-63

Motonovo Finance ......................64-65

Perfect Channel ..........................66-67

Search Optics UK .........................68-69

Secure Valeting ...........................70-71

Steele-Dixon & Associates ............85

Symco Training ..................................42

Tootle ......................................................6

Trader Publishing ................40-41, 43

Trusted Dealers.................................13

Zype TV ....................................11, 73, 74

How dealers decide what to outsource, and how to ensure suppliers live up to your expectations.

Expert advice on getting the most from your employees.

Managing third- party relationships

AM/IMI People Conference Report

AM, Media House, Lynch Wood, Peterborough PE2 6EA Email: [email protected]

Editor-in-chief Stephen Briers 01733 468024 Editor Tim Rose 01733 468266News and features editor Tom Sharpe 01733 468343 Head of digital/associate editor Jeremy Bennett 01733 468261

AM productionHead of publishingLuke Neal 01733 468262Production editor Finbarr O’Reilly 01733 468267 Designer Erika Small 01733 468312

Contributors Debbie Kirlew, Chris Lowndes, Philip Nothard, Prof Jim Saker, Tom Seymour

AM advertising Commercial director Carlota Hudgell 01733 366466(maternity cover)Group advertisement managerSheryl Graham 01733 366467Head of project management Leanne Patterson 01733 468332Project managers Kerry Unwin 01733 468578Lucy Peacock 01733 468327Account managers Sara Donald 01733 366474Richard Kerr 01733 366473Kelly Crown 01733 366364Recruitment enquiriesRichard Kerr 01733 366473 AM eventsEvent director Chris LesterEvent managerLuke Clements 01733 468325Event plannerNicola Baxter 01733 468289 AM publishingManaging director Tim LucasOffice managerJane Hill 01733 468319Group managing director Rob Munro-HallChief executive officerPaul Keenan

Subscriptions 01635 588494. Annual UK subscription £99, two years £168, three years £238. Overseas one year/12 issues £149, two years £253, three years £358.

AM is published 12 times a year by Bauer Consumer Media Ltd, registered address Media House, Peterborough Business Park, Lynch Wood, Peterborough, PE2 6EA. Registered number 01176085.No part of the magazine may be reproduced in any form in whole or in part, without prior permission of the publisher. All material published remains the copyright of Bauer Consumer Media Ltd.We reserve the right to edit letters, copy or images submitted to the magazine without further consent. The submission of material to Bauer Media whether unsolicited or requested, is taken as permission to publish in the magazine, including any licensed editions throughout the world. Any fees paid in the UK include remuneration for any use in any other licensed editions.We cannot accept any responsibility for unsolicited manuscripts, images or materials lost or damaged in the post. Whilst every reasonable care is taken to ensure accuracy, the publisher is not respon-sible for any errors or omissions nor do we accept any liability for any loss or damage, howsoever caused, resulting from the use of the magazine.

Printing: Headley Brothers Ltd, Kent

Complaints: Bauer Consumer Media Limited is a

member of the Independent Press Standards Organisa-

tion (www.ipso.co.uk) and endeavours to respond to and

resolve your concerns quickly. Our Editorial Complaints

Policy (including full details of how to contact us about

editorial complaints and IPSO’s contact details) can be

found at www.bauermediacomplaints.co.uk. Our email

address for editorial complaints covered by the Editorial

Complaints Policy is [email protected].

C O N TA C T U S

Face to Face: Steven EagellSteven EagellHow a hat-trick of acquisitions is putting AM100 dealer

group Steven Eagell in a stronger position for growth with its sole brand partner, Toyota.