Embed Size (px)

Citation preview

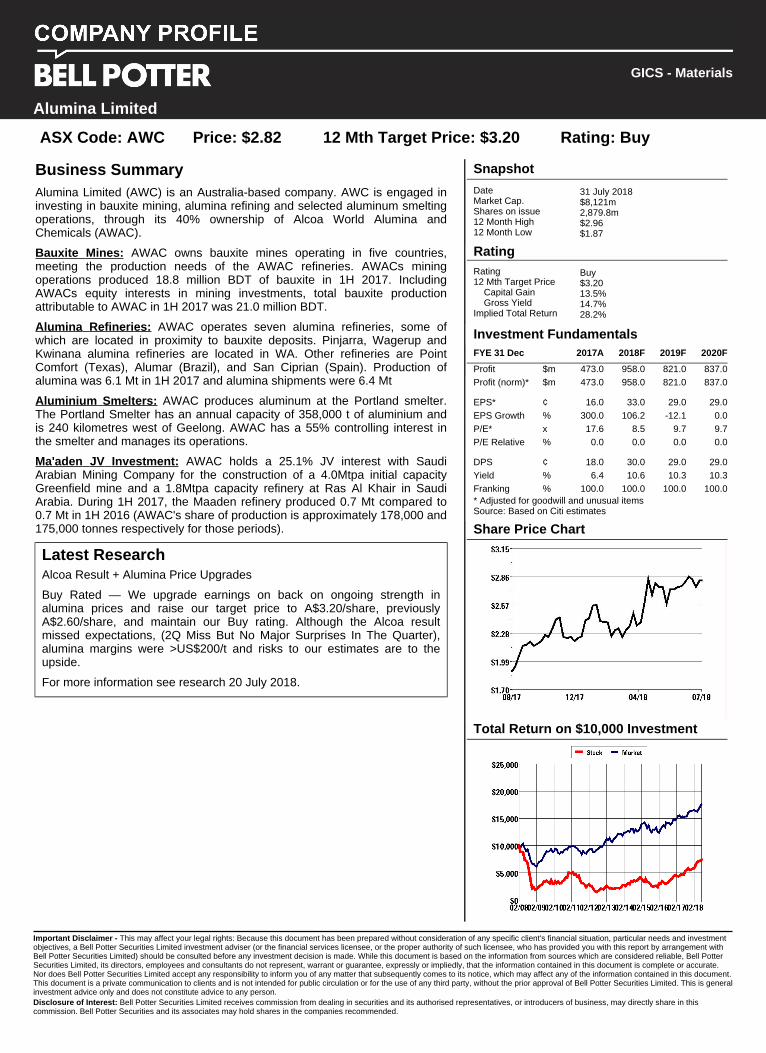

Business SummaryAlumina Limited (AWC) is an Australia-based company. AWC is engaged ininvesting in bauxite mining, alumina refining and selected aluminum smeltingoperations, through its 40% ownership of Alcoa World Alumina andChemicals (AWAC).

Bauxite Mines: AWAC owns bauxite mines operating in five countries,meeting the production needs of the AWAC refineries. AWACs miningoperations produced 18.8 million BDT of bauxite in 1H 2017. IncludingAWACs equity interests in mining investments, total bauxite productionattributable to AWAC in 1H 2017 was 21.0 million BDT.

Alumina Refineries: AWAC operates seven alumina refineries, some ofwhich are located in proximity to bauxite deposits. Pinjarra, Wagerup andKwinana alumina refineries are located in WA. Other refineries are PointComfort (Texas), Alumar (Brazil), and San Ciprian (Spain). Production ofalumina was 6.1 Mt in 1H 2017 and alumina shipments were 6.4 Mt

Aluminium Smelters: AWAC produces aluminum at the Portland smelter.The Portland Smelter has an annual capacity of 358,000 t of aluminium andis 240 kilometres west of Geelong. AWAC has a 55% controlling interest inthe smelter and manages its operations.

Ma'aden JV Investment: AWAC holds a 25.1% JV interest with SaudiArabian Mining Company for the construction of a 4.0Mtpa initial capacityGreenfield mine and a 1.8Mtpa capacity refinery at Ras Al Khair in SaudiArabia. During 1H 2017, the Maaden refinery produced 0.7 Mt compared to0.7 Mt in 1H 2016 (AWAC's share of production is approximately 178,000 and175,000 tonnes respectively for those periods).

Latest ResearchAlcoa Result + Alumina Price Upgrades

Buy Rated — We upgrade earnings on back on ongoing strength inalumina prices and raise our target price to A$3.20/share, previouslyA$2.60/share, and maintain our Buy rating. Although the Alcoa resultmissed expectations, (2Q Miss But No Major Surprises In The Quarter),alumina margins were >US$200/t and risks to our estimates are to theupside.

For more information see research 20 July 2018.

GICS - Materials

Alumina Limited

ASX Code: AWC Price: $2.82 12 Mth Target Price: $3.20 Rating: Buy

Important Disclaimer - This may affect your legal rights: Because this document has been prepared without consideration of any specific client's financial situation, particular needs and investmentobjectives, a Bell Potter Securities Limited investment adviser (or the financial services licensee, or the proper authority of such licensee, who has provided you with this report by arrangement withBell Potter Securities Limited) should be consulted before any investment decision is made. While this document is based on the information from sources which are considered reliable, Bell PotterSecurities Limited, its directors, employees and consultants do not represent, warrant or guarantee, expressly or impliedly, that the information contained in this document is complete or accurate.Nor does Bell Potter Securities Limited accept any responsibility to inform you of any matter that subsequently comes to its notice, which may affect any of the information contained in this document.This document is a private communication to clients and is not intended for public circulation or for the use of any third party, without the prior approval of Bell Potter Securities Limited. This is generalinvestment advice only and does not constitute advice to any person.Disclosure of Interest: Bell Potter Securities Limited receives commission from dealing in securities and its authorised representatives, or introducers of business, may directly share in thiscommission. Bell Potter Securities and its associates may hold shares in the companies recommended.

Snapshot

DateMarket Cap.Shares on issue12 Month High12 Month Low

31 July 2018$8,121m2,879.8m$2.96$1.87

RatingRating12 Mth Target Price

Capital GainGross Yield

Implied Total Return

Buy$3.2013.5%14.7%28.2%

Investment FundamentalsFYE 31 Dec 2017A 2018F 2019F 2020F

Profit $m 473.0 958.0 821.0 837.0Profit (norm)* $m 473.0 958.0 821.0 837.0

EPS* ¢ 16.0 33.0 29.0 29.0EPS Growth % 300.0 106.2 -12.1 0.0P/E* x 17.6 8.5 9.7 9.7P/E Relative % 0.0 0.0 0.0 0.0

DPS ¢ 18.0 30.0 29.0 29.0Yield % 6.4 10.6 10.3 10.3Franking % 100.0 100.0 100.0 100.0* Adjusted for goodwill and unusual itemsSource: Based on Citi estimates

Share Price Chart

Total Return on $10,000 Investment

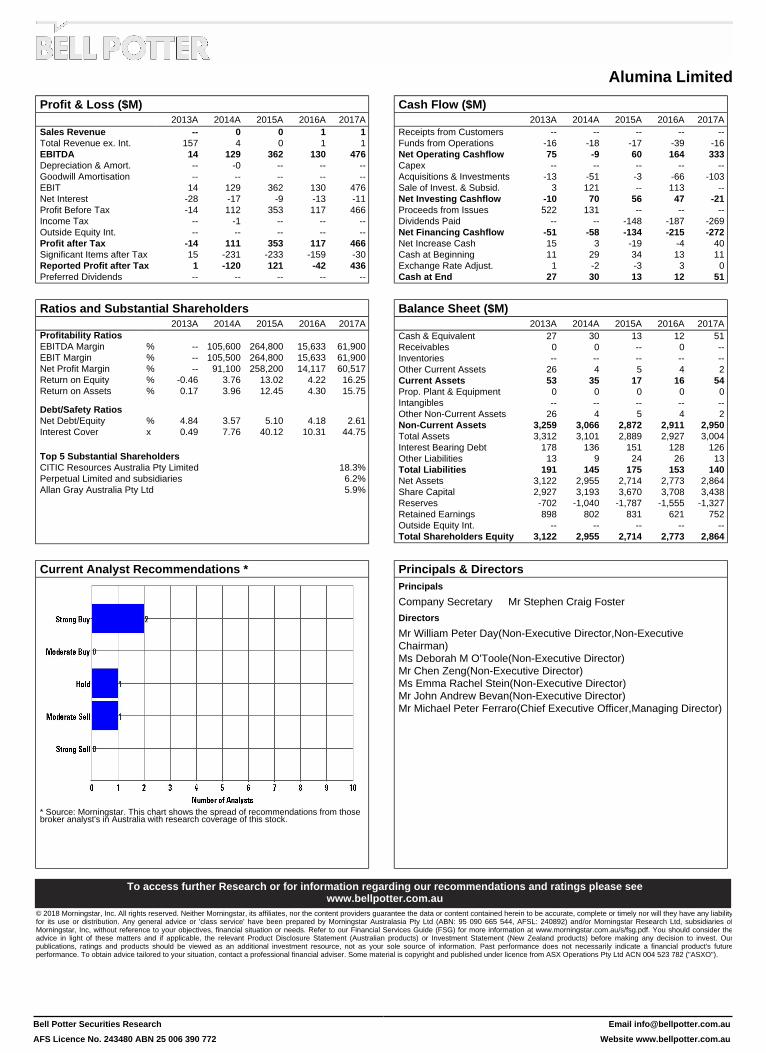

Profit & Loss ($M)2013A 2014A 2015A 2016A 2017A

Sales Revenue -- 0 0 1 1Total Revenue ex. Int. 157 4 0 1 1EBITDA 14 129 362 130 476Depreciation & Amort. -- -0 -- -- --Goodwill Amortisation -- -- -- -- --EBIT 14 129 362 130 476Net Interest -28 -17 -9 -13 -11Profit Before Tax -14 112 353 117 466Income Tax -- -1 -- -- --Outside Equity Int. -- -- -- -- --Profit after Tax -14 111 353 117 466Significant Items after Tax 15 -231 -233 -159 -30Reported Profit after Tax 1 -120 121 -42 436Preferred Dividends -- -- -- -- --

Cash Flow ($M)2013A 2014A 2015A 2016A 2017A

Receipts from Customers -- -- -- -- --Funds from Operations -16 -18 -17 -39 -16Net Operating Cashflow 75 -9 60 164 333Capex -- -- -- -- --Acquisitions & Investments -13 -51 -3 -66 -103Sale of Invest. & Subsid. 3 121 -- 113 --Net Investing Cashflow -10 70 56 47 -21Proceeds from Issues 522 131 -- -- --Dividends Paid -- -- -148 -187 -269Net Financing Cashflow -51 -58 -134 -215 -272Net Increase Cash 15 3 -19 -4 40Cash at Beginning 11 29 34 13 11Exchange Rate Adjust. 1 -2 -3 3 0Cash at End 27 30 13 12 51

Ratios and Substantial Shareholders2013A 2014A 2015A 2016A 2017A

Profitability RatiosEBITDA Margin % -- 105,600 264,800 15,633 61,900EBIT Margin % -- 105,500 264,800 15,633 61,900Net Profit Margin % -- 91,100 258,200 14,117 60,517Return on Equity % -0.46 3.76 13.02 4.22 16.25Return on Assets % 0.17 3.96 12.45 4.30 15.75

Debt/Safety RatiosNet Debt/Equity % 4.84 3.57 5.10 4.18 2.61Interest Cover x 0.49 7.76 40.12 10.31 44.75

Top 5 Substantial ShareholdersCITIC Resources Australia Pty Limited 18.3%Perpetual Limited and subsidiaries 6.2%Allan Gray Australia Pty Ltd 5.9%

Balance Sheet ($M)2013A 2014A 2015A 2016A 2017A

Cash & Equivalent 27 30 13 12 51Receivables 0 0 -- 0 --Inventories -- -- -- -- --Other Current Assets 26 4 5 4 2Current Assets 53 35 17 16 54Prop. Plant & Equipment 0 0 0 0 0Intangibles -- -- -- -- --Other Non-Current Assets 26 4 5 4 2Non-Current Assets 3,259 3,066 2,872 2,911 2,950Total Assets 3,312 3,101 2,889 2,927 3,004Interest Bearing Debt 178 136 151 128 126Other Liabilities 13 9 24 26 13Total Liabilities 191 145 175 153 140Net Assets 3,122 2,955 2,714 2,773 2,864Share Capital 2,927 3,193 3,670 3,708 3,438Reserves -702 -1,040 -1,787 -1,555 -1,327Retained Earnings 898 802 831 621 752Outside Equity Int. -- -- -- -- --Total Shareholders Equity 3,122 2,955 2,714 2,773 2,864

Current Analyst Recommendations *

* Source: Morningstar. This chart shows the spread of recommendations from thosebroker analyst's in Australia with research coverage of this stock.

Principals & DirectorsPrincipals

Company Secretary Mr Stephen Craig Foster

Directors

Mr William Peter Day(Non-Executive Director,Non-ExecutiveChairman)Ms Deborah M O'Toole(Non-Executive Director)Mr Chen Zeng(Non-Executive Director)Ms Emma Rachel Stein(Non-Executive Director)Mr John Andrew Bevan(Non-Executive Director)Mr Michael Peter Ferraro(Chief Executive Officer,Managing Director)

To access further Research or for information regarding our recommendations and ratings please seewww.bellpotter.com.au

© 2018 Morningstar, Inc. All rights reserved. Neither Morningstar, its affiliates, nor the content providers guarantee the data or content contained herein to be accurate, complete or timely nor will they have any liabilityfor its use or distribution. Any general advice or 'class service' have been prepared by Morningstar Australasia Pty Ltd (ABN: 95 090 665 544, AFSL: 240892) and/or Morningstar Research Ltd, subsidiaries ofMorningstar, Inc, without reference to your objectives, financial situation or needs. Refer to our Financial Services Guide (FSG) for more information at www.morningstar.com.au/s/fsg.pdf. You should consider theadvice in light of these matters and if applicable, the relevant Product Disclosure Statement (Australian products) or Investment Statement (New Zealand products) before making any decision to invest. Ourpublications, ratings and products should be viewed as an additional investment resource, not as your sole source of information. Past performance does not necessarily indicate a financial product's futureperformance. To obtain advice tailored to your situation, contact a professional financial adviser. Some material is copyright and published under licence from ASX Operations Pty Ltd ACN 004 523 782 ("ASXO").

Alumina Limited

Bell Potter Securities Research

AFS Licence No. 243480 ABN 25 006 390 772

Email [email protected]

Website www.bellpotter.com.au