Embed Size (px)

DESCRIPTION

Altrisk's quick guide to life

Citation preview

Altrisk’s quick guide to life Dare to get to know us

www.altrisk.co.za

Altrisk39862 FA.indd 1-2 2010/04/28 4:24 PM

Altrisk is not your ordinary life insurance provider. In fact, far from it.

We dare to be differentby offering life, critical illness and disability cover through our commitment to simplicity, accessibility and unique underwriting solutions.

It’s how we make it easier for you to do business with us.

What’s more, we are solutions driven, which means we don’t like to overlook those with a so-called high-risk profile. After all, a certain amount of risk makes life worth living. And life is our speciality.

SpecialisedrisksolutionsDeferred Life Cover:Because we believe that everyone should be able to apply for cover, our Deferred Life Cover benefit is available to those who would normally be declined for medical reasons.

A standard three-year waiting period applies to all policies, and during this period only accidental death is covered. But, after the waiting period is complete, all causes of death are covered.

HIV Positive Applications:This specialist Altrisk application offers life cover and selected accelerator benefits to people who are living with HIV. The only difference being an inclusion of Disease Management Compliance Endorsement in the policy document.

For a full description of any of the product benefits, please do not hesitate to contact us on 011 329 7000 or visit www.altrisk.co.za

Value-addedbenefitsGuaranteed Insurability Benefit: As unforeseen events can happen, it’s natural that people would want more security. This benefit therefore allows the policyholder to increase their life, critical illness, disability and impairment cover, with minimal evidence of health status. Future increases in cover can be taken as either an increase to the base policy or as a new stand-alone policy – it’s your client’s choice.

Flexible Cover: This benefit is available on either a personal or a business basis.

Personal:

This gives the policy owner the option to increase the life, disability, impairment and critical illness cover on their policy at any time in the future, with limited further underwriting. Existing cover can also be ‘banked’ in the facility, to be utilised at a later stage. Changes in cover can only be exercised on lump sum benefits.

Business:

This also gives the policy owner the option to increase the life, disability, impairment and critical illness cover on his/her policy at any time in the future, with limited further underwriting. This is provided simply to meet the changing financial needs of the business.

Female Protector:This benefit provides for the specific needs of a woman and her children in the case of unforeseen events. These could include cancer, pregnancy complications or a child’s impairment.

Altrisk39862 FA.indd 3-4 2010/04/28 4:24 PM

Altrisk is not your ordinary life insurance provider. In fact, far from it.

We dare to be differentby offering life, critical illness and disability cover through our commitment to simplicity, accessibility and unique underwriting solutions.

It’s how we make it easier for you to do business with us.

What’s more, we are solutions driven, which means we don’t like to overlook those with a so-called high-risk profile. After all, a certain amount of risk makes life worth living. And life is our speciality.

SpecialisedrisksolutionsDeferred Life Cover:Because we believe that everyone should be able to apply for cover, our Deferred Life Cover benefit is available to those who would normally be declined for medical reasons.

A standard three-year waiting period applies to all policies, and during this period only accidental death is covered. But, after the waiting period is complete, all causes of death are covered.

HIV Positive Applications:This specialist Altrisk application offers life cover and selected accelerator benefits to people who are living with HIV. The only difference being an inclusion of Disease Management Compliance Endorsement in the policy document.

For a full description of any of the product benefits, please do not hesitate to contact us on 011 329 7000 or visit www.altrisk.co.za

Value-addedbenefitsGuaranteed Insurability Benefit: As unforeseen events can happen, it’s natural that people would want more security. This benefit therefore allows the policyholder to increase their life, critical illness, disability and impairment cover, with minimal evidence of health status. Future increases in cover can be taken as either an increase to the base policy or as a new stand-alone policy – it’s your client’s choice.

Flexible Cover: This benefit is available on either a personal or a business basis.

Personal:

This gives the policy owner the option to increase the life, disability, impairment and critical illness cover on their policy at any time in the future, with limited further underwriting. Existing cover can also be ‘banked’ in the facility, to be utilised at a later stage. Changes in cover can only be exercised on lump sum benefits.

Business:

This also gives the policy owner the option to increase the life, disability, impairment and critical illness cover on his/her policy at any time in the future, with limited further underwriting. This is provided simply to meet the changing financial needs of the business.

Female Protector:This benefit provides for the specific needs of a woman and her children in the case of unforeseen events. These could include cancer, pregnancy complications or a child’s impairment.

Altrisk39862 FA.indd 3-4 2010/04/28 4:24 PM

Altrisk is not your ordinary life insurance provider. In fact, far from it.

We dare to be differentby offering life, critical illness and disability cover through our commitment to simplicity, accessibility and unique underwriting solutions.

It’s how we make it easier for you to do business with us.

What’s more, we are solutions driven, which means we don’t like to overlook those with a so-called high-risk profile. After all, a certain amount of risk makes life worth living. And life is our speciality.

SpecialisedrisksolutionsDeferred Life Cover:Because we believe that everyone should be able to apply for cover, our Deferred Life Cover benefit is available to those who would normally be declined for medical reasons.

A standard three-year waiting period applies to all policies, and during this period only accidental

death is covered. But, after the waiting period is complete, all causes of death are covered.

Value-addedbenefitsGuaranteed Insurability Benefit: As unforeseen events can happen, it’s natural that people would want more security. This benefit therefore allows the policyholder to increase their life, critical illness, disability and impairment cover, with minimal evidence of health status. Future increases in cover can be taken as either an increase to the base policy or as a new stand-alone policy – it’s your client’s choice.

Flexible Cover: This benefit is available on either a personal or a business basis.

Personal:

This gives the policy owner the option to increase the life, disability, impairment and critical illness cover on their policy at any time in the future, with limited further underwriting. Existing cover can also be ‘banked’ in the facility, to be utilised at a later stage. Changes in cover can only be exercised on lump sum benefits.

Business:

This also gives the policy owner the option to increase the life, disability, impairment and critical illness cover on his/her policy at any time in the future, with limited further underwriting. This is provided simply to meet the changing financial needs of the business.

Female Protector:This benefit provides for the specific needs of a woman and her children in the case of unforeseen events. These could include cancer, pregnancy complications or a child’s impairment.

Altrisk39862 FA.indd 5-6 2010/04/28 4:24 PM

Altrisk is not your ordinary life insurance provider. In fact, far from it.

We dare to be differentby offering life, critical illness and disability cover through our commitment to simplicity, accessibility and unique underwriting solutions.

It’s how we make it easier for you to do business with us.

What’s more, we are solutions driven, which means we don’t like to overlook those with a so-called high-risk profile. After all, a certain amount of risk makes life worth living. And life is our speciality.

SpecialisedrisksolutionsDeferred Life Cover:Because we believe that everyone should be able to apply for cover, our Deferred Life Cover benefit is available to those who would normally be declined for medical reasons.

A standard three-year waiting period applies to all policies, and during this period only accidental

death is covered. But, after the waiting period is complete, all causes of death are covered.

Value-addedbenefitsGuaranteed Insurability Benefit: As unforeseen events can happen, it’s natural that people would want more security. This benefit therefore allows the policyholder to increase their life, critical illness, disability and impairment cover, with minimal evidence of health status. Future increases in cover can be taken as either an increase to the base policy or as a new stand-alone policy – it’s your client’s choice.

Flexible Cover: This benefit is available on either a personal or a business basis.

Personal:

This gives the policy owner the option to increase the life, disability, impairment and critical illness cover on their policy at any time in the future, with limited further underwriting. Existing cover can also be ‘banked’ in the facility, to be utilised at a later stage. Changes in cover can only be exercised on lump sum benefits.

Business:

This also gives the policy owner the option to increase the life, disability, impairment and critical illness cover on his/her policy at any time in the future, with limited further underwriting. This is provided simply to meet the changing financial needs of the business.

Female Protector:This benefit provides for the specific needs of a woman and her children in the case of unforeseen events. These could include cancer, pregnancy complications or a child’s impairment.

Altrisk39862 FA.indd 5-6 2010/04/28 4:24 PM

IncomeReplacementPlan:

This is designed to pay a monthly benefit to the insured after the expiry of the selected waiting period, should he/she become temporarily disabled and unable to perform their occupation.

Not forgetting those who are self-employed, we also offer the Business Overhead Protector benefit.

DisabilityPremiumWaiver:

To prevent a client’s policy from lapsing should they become disabled and unable to perform their occupation, this benefit pays the monthly premium due, after the expiry of the one-month waiting period. Just one less thing for a client to worry about in these circumstances.

Critical Illness Cover:This provides the insured with cover for a range of specified diseases, which are an unfortunate fact of life.

There are three variations from which to choose, split into the Basic, Core and Comprehensive benefits.

The Basic Critical Illness benefit covers cancer, heart attack, stroke and Coronary Artery By-pass Graft (CABG) only. Our definitions of these conditions are in line with SCIDEP (Standardised Critical Illness Definitions Project) as implemented by ASISA. Interestingly, these conditions make up between 75% and 90% of all critical illness claims. But for those who would like more peace of mind, the Core Critical Illness and Comprehensive Critical Illness benefits cover a total 26 and 45 conditions respectively.

Value-addedbenefits

Whyus?There are many reasons to do business with us. But just to give you a taste, here are a few:

• We’reowner-managedwithacorefocusontheriskmarket. We do what we do well!

• Ourquotessystemmakeslifeeasier.Thanks to simple navigation, resulting quotations are easy to read and understand.

• Wehavethesimplestapplicationforminthebusiness. Only eight pages long, including the RPAR.

• Wehavethefewestgeneralexclusionsinthemarket.Just one on our disability and impairment benefits: self-inflicted injuries.

• Weprovideaflexiblecoverfacility, which allows a reduction in premiums until it’s convenient to increase them again.

• Ourincomereplacementbenefitsareflexible,cost-effectiveandcaterforolderpeople. Almost all components of our income replacement can be taken as freestanding benefits to suit individual needs and budgets. And, we have the highest entry age for income replacement, age 65.

• Ourdeathincomebenefitispractical, providing a monthly income to the beneficiary for either 12 or 24 months after the life insured’s death. The 24-month benefit can be extended to what would have been the life insured’s expiry age (60, 65 or 70).

• Wehavethebest,solutions-orientatedunderwritingteaminthebusiness, with almost 150 years’ collective direct insurance and reinsurance experience!

Ourheadstart

Since our humble beginnings, we have achieved a number of firsts in our field. It’s all part of our quest to be recognised as the best risk provider in our chosen market, in a very competitive industry - and to offer you the best possible solutions for your clients, of course.

First to regularly cover people with severe medical impairments – those who tra-ditionally couldn’t get cover in the marketplace.

First to offer new-generation life cover to people living with HIV.

First to regularly cover people working in high-risk countries.

First to introduce a suicide exclusion that recognises previous periods of life cover.

First to adopt standardised critical illness definitions.

First to do away with irrelevant general exclusions.

Altrisk39862 FA.indd 7-8 2010/04/28 4:24 PM

IncomeReplacementPlan:

This is designed to pay a monthly benefit to the insured after the expiry of the selected waiting period, should he/she become temporarily disabled and unable to perform their occupation.

Not forgetting those who are self-employed, we also offer the Business Overhead Protector benefit.

DisabilityPremiumWaiver:

To prevent a client’s policy from lapsing should they become disabled and unable to perform their occupation, this benefit pays the monthly premium due, after the expiry of the one-month waiting period. Just one less thing for a client to worry about in these circumstances.

Critical Illness Cover:This provides the insured with cover for a range of specified diseases, which are an unfortunate fact of life.

There are three variations from which to choose, split into the Basic, Core and Comprehensive benefits.

The Basic Critical Illness benefit covers cancer, heart attack, stroke and Coronary Artery By-pass Graft (CABG) only. Our definitions of these conditions are in line with SCIDEP (Standardised Critical Illness Definitions Project) as implemented by ASISA. Interestingly, these conditions make up between 75% and 90% of all critical illness claims. But for those who would like more peace of mind, the Core Critical Illness and Comprehensive Critical Illness benefits cover a total 26 and 45 conditions respectively.

Value-addedbenefits

Whyus?There are many reasons to do business with us. But just to give you a taste, here are a few:

• We’reowner-managedwithacorefocusontheriskmarket. We do what we do well!

• Ourquotessystemmakeslifeeasier.Thanks to simple navigation, resulting quotations are easy to read and understand.

• Wehavethesimplestapplicationforminthebusiness. Only eight pages long, including the RPAR.

• Wehavethefewestgeneralexclusionsinthemarket.Just one on our disability and impairment benefits: self-inflicted injuries.

• Weprovideaflexiblecoverfacility, which allows a reduction in premiums until it’s convenient to increase them again.

• Ourincomereplacementbenefitsareflexible,cost-effectiveandcaterforolderpeople. Almost all components of our income replacement can be taken as freestanding benefits to suit individual needs and budgets. And, we have the highest entry age for income replacement, age 65.

• Ourdeathincomebenefitispractical, providing a monthly income to the beneficiary for either 12 or 24 months after the life insured’s death. The 24-month benefit can be extended to what would have been the life insured’s expiry age (60, 65 or 70).

• Wehavethebest,solutions-orientatedunderwritingteaminthebusiness, with almost 150 years’ collective direct insurance and reinsurance experience!

Ourheadstart

Since our humble beginnings, we have achieved a number of firsts in our field. It’s all part of our quest to be recognised as the best risk provider in our chosen market, in a very competitive industry - and to offer you the best possible solutions for your clients, of course.

First to regularly cover people with severe medical impairments – those who tra-ditionally couldn’t get cover in the marketplace.

First to offer new-generation life cover to people living with HIV.

First to regularly cover people working in high-risk countries.

First to introduce a suicide exclusion that recognises previous periods of life cover.

First to adopt standardised critical illness definitions.

First to do away with irrelevant general exclusions.

Altrisk39862 FA.indd 7-8 2010/04/28 4:24 PM

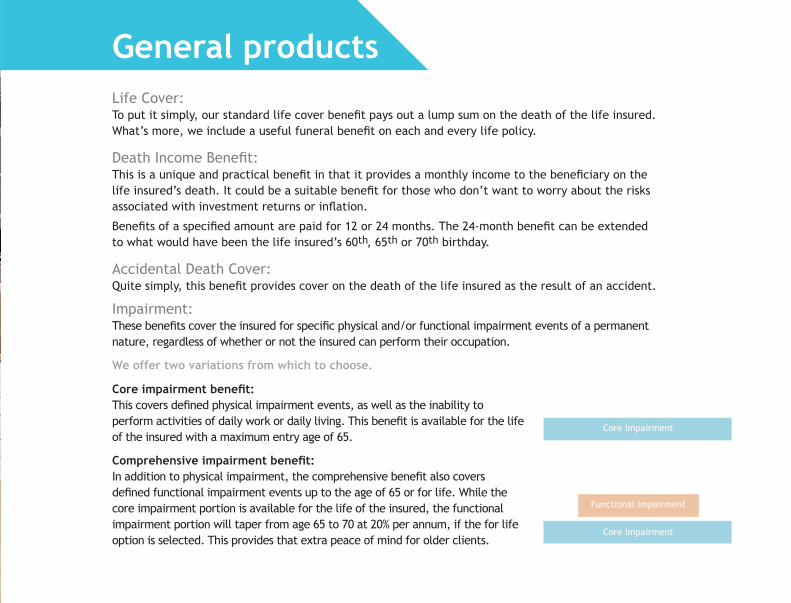

GeneralproductsLife Cover: To put it simply, our standard life cover benefit pays out a lump sum on the death of the life insured. What’s more, we include a useful funeral benefit on each and every life policy.

Death Income Benefit:This is a unique and practical benefit in that it provides a monthly income to the beneficiary on the life insured’s death. It could be a suitable benefit for those who don’t want to worry about the risks associated with investment returns or inflation.

Benefits of a specified amount are paid for 12 or 24 months. The 24-month benefit can be extended to what would have been the life insured’s 60th, 65th or 70th birthday.

Accidental Death Cover:Quite simply, this benefit provides cover on the death of the life insured as the result of an accident.

Impairment:These benefits cover the insured for specific physical and/or functional impairment events of a permanent nature, regardless of whether or not the insured can perform their occupation.

Weoffertwovariationsfromwhichtochoose.

Coreimpairmentbenefit:This covers defined physical impairment events, as well as the inability to perform activities of daily work or daily living. This benefit is available for the life of the insured with a maximum entry age of 65.

Comprehensiveimpairmentbenefit:In addition to physical impairment, the comprehensive benefit also covers defined functional impairment events up to the age of 65 or for life. While the core impairment portion is available for the life of the insured, the functional impairment portion will taper from age 65 to 70 at 20% per annum, if the for life option is selected. This provides that extra peace of mind for older clients.

MoreaboutusandwhatwedoAltrisk started out over a decade ago, specialising in life, disability and critical illness cover for impaired lives. We founded our business on a philosophy of simplicity and a moral code based on ‘doing the right thing’.

Soon, Altrisk entered the standard life market. With our unique underwriting skills, we were able to provide individual assessments, supporting our purpose of being in the business of paying claims. And we haven’t looked back.

Today, our offerings not only include conventional life, disability and critical illness benefits, but also cover for clients who traditionally would have been declined, like those living with HIV or other serious medical impairments. All our benefits remain uncomplicated and competitively priced.

Core impairment

Core impairment

Functional impairment

GeneralproductsLife Cover: To put it simply, our standard life cover benefit pays out a lump sum on the death of the life insured. What’s more, we include a useful funeral benefit on each and every life policy.

Death Income Benefit:This is a unique and practical benefit in that it provides a monthly income to the beneficiary on the life insured’s death. It could be a suitable benefit for those who don’t want to worry about the risks associated with investment returns or inflation.

Benefits of a specified amount are paid for 12 or 24 months. The 24-month benefit can be extended to what would have been the life insured’s 60th, 65th or 70th birthday.

Accidental Death Cover:Quite simply, this benefit provides cover on the death of the life insured as the result of an accident.

Impairment:These benefits cover the insured for specific physical and/or functional impairment events of a permanent nature, regardless of whether or not the insured can perform their occupation.

Weoffertwovariationsfromwhichtochoose.

Coreimpairmentbenefit:This covers defined physical impairment events, as well as the inability to perform activities of daily work or daily living. This benefit is available for the life of the insured with a maximum entry age of 65.

Comprehensiveimpairmentbenefit:In addition to physical impairment, the comprehensive benefit also covers defined functional impairment events up to the age of 65 or for life. While the core impairment portion is available for the life of the insured, the functional impairment portion will taper from age 65 to 70 at 20% per annum, if the for life option is selected. This provides that extra peace of mind for older clients.

MoreaboutusandwhatwedoAltrisk started out over a decade ago, specialising in life, disability and critical illness cover for impaired lives. We founded our business on a philosophy of simplicity and a moral code based on ‘doing the right thing’.

Soon, Altrisk entered the standard life market. With our unique underwriting skills, we were able to provide individual assessments, supporting our purpose of being in the business of paying claims. And we haven’t looked back.

Today, our offerings not only include conventional life, disability and critical illness benefits, but also cover for clients who traditionally would have been declined, like those living with HIV or other serious medical impairments. All our benefits remain uncomplicated and competitively priced.

Core impairment

Core impairment

Functional impairment

Altrisk39862 FA.indd 9-10 2010/04/28 4:24 PM

GeneralproductsLife Cover: To put it simply, our standard life cover benefit pays out a lump sum on the death of the life insured. What’s more, we include a useful funeral benefit on each and every life policy.

Death Income Benefit:This is a unique and practical benefit in that it provides a monthly income to the beneficiary on the life insured’s death. It could be a suitable benefit for those who don’t want to worry about the risks associated with investment returns or inflation.

Benefits of a specified amount are paid for 12 or 24 months. The 24-month benefit can be extended to what would have been the life insured’s 60th, 65th or 70th birthday.

Accidental Death Cover:Quite simply, this benefit provides cover on the death of the life insured as the result of an accident.

Impairment:These benefits cover the insured for specific physical and/or functional impairment events of a permanent nature, regardless of whether or not the insured can perform their occupation.

Weoffertwovariationsfromwhichtochoose.

Coreimpairmentbenefit:This covers defined physical impairment events, as well as the inability to perform activities of daily work or daily living. This benefit is available for the life of the insured with a maximum entry age of 65.

Comprehensiveimpairmentbenefit:In addition to physical impairment, the comprehensive benefit also covers defined functional impairment events up to the age of 65 or for life. While the core impairment portion is available for the life of the insured, the functional impairment portion will taper from age 65 to 70 at 20% per annum, if the for life option is selected. This provides that extra peace of mind for older clients.

MoreaboutusandwhatwedoAltrisk started out over a decade ago, specialising in life, disability and critical illness cover for impaired lives. We founded our business on a philosophy of simplicity and a moral code based on ‘doing the right thing’.

Soon, Altrisk entered the standard life market. With our unique underwriting skills, we were able to provide individual assessments, supporting our purpose of being in the business of paying claims. And we haven’t looked back.

Today, our offerings not only include conventional life, disability and critical illness benefits, but also cover for clients who traditionally would have been declined, like those living with HIV or other serious medical impairments. All our benefits remain uncomplicated and competitively priced.

Core impairment

Core impairment

Functional impairment

GeneralproductsLife Cover: To put it simply, our standard life cover benefit pays out a lump sum on the death of the life insured. What’s more, we include a useful funeral benefit on each and every life policy.

Death Income Benefit:This is a unique and practical benefit in that it provides a monthly income to the beneficiary on the life insured’s death. It could be a suitable benefit for those who don’t want to worry about the risks associated with investment returns or inflation.

Benefits of a specified amount are paid for 12 or 24 months. The 24-month benefit can be extended to what would have been the life insured’s 60th, 65th or 70th birthday.

Accidental Death Cover:Quite simply, this benefit provides cover on the death of the life insured as the result of an accident.

Impairment:These benefits cover the insured for specific physical and/or functional impairment events of a permanent nature, regardless of whether or not the insured can perform their occupation.

Weoffertwovariationsfromwhichtochoose.

Coreimpairmentbenefit:This covers defined physical impairment events, as well as the inability to perform activities of daily work or daily living. This benefit is available for the life of the insured with a maximum entry age of 65.

Comprehensiveimpairmentbenefit:In addition to physical impairment, the comprehensive benefit also covers defined functional impairment events up to the age of 65 or for life. While the core impairment portion is available for the life of the insured, the functional impairment portion will taper from age 65 to 70 at 20% per annum, if the for life option is selected. This provides that extra peace of mind for older clients.

MoreaboutusandwhatwedoAltrisk started out over a decade ago, specialising in life, disability and critical illness cover for impaired lives. We founded our business on a philosophy of simplicity and a moral code based on ‘doing the right thing’.

Soon, Altrisk entered the standard life market. With our unique underwriting skills, we were able to provide individual assessments, supporting our purpose of being in the business of paying claims. And we haven’t looked back.

Today, our offerings not only include conventional life, disability and critical illness benefits, but also cover for clients who traditionally would have been declined, like those living with HIV or other serious medical impairments. All our benefits remain uncomplicated and competitively priced.

Core impairment

Core impairment

Functional impairment

Altrisk39862 FA.indd 9-10 2010/04/28 4:24 PM

GeneralproductsDisability Cover:These benefits pay the insured a specified lump sum in the event of disability or impairment. Again, to cater for our clients’ unique circumstances, we have several variations from which to choose.

The following three options contain a core impairment portion. These benefits are available for life or to the age of 65. If the for life option is selected, the occupational disability, functional impairment and disability income benefit portions respectively, will taper from the age of 65 to 70 at 20% per annum.

Disability:

This benefit covers the insured in the event of permanent and total occupational disablement. For added certainty it is underpinned by a core impairment benefit.

ComprehensiveDisability:

In addition to the disability benefit, comprehensive disability also covers the insured for defined functional impairment events.

DisabilityPlus:

Disability Plus incorporates all the elements from core impairment through to comprehensive disability as well as a 24-month income benefit. The impairment income portion is available for the life of the insured.

Core impairment

Income benefit

Functional impairmentOccupational disability

Core impairment

Functional impairmentOccupational disability

Core impairment

Occupational disability

Whyus?There are many reasons to do business with us. But just to give you a taste, here are a few:

• We’reowner-managedwithacorefocusontheriskmarket. We do what we do well!

• Ourquotessystemmakeslifeeasier.Thanks to simple navigation, resulting quotations are easy to read and understand.

• Wehavethesimplestapplicationforminthebusiness. Only eight pages long, including the RPAR.

• Wehavethefewestgeneralexclusionsinthemarket.Just one on our disability and impairment benefits: self-inflicted injuries.

• Weprovideaflexiblecoverfacility, which allows a reduction in premiums until it’s convenient to increase them again.

• Ourincomereplacementbenefitsareflexible,cost-effectiveandcaterforolderpeople. Almost all components of our income replacement can be taken as freestanding benefits to suit individual needs and budgets. And, we have the highest entry age for income replacement, age 65.

• Ourdeathincomebenefitispractical, providing a monthly income to the beneficiary for either 12 or 24 months after the life insured’s death. The 24-month benefit can be extended to what would have been the life insured’s expiry age (60, 65 or 70).

• Wehavethebest,solutions-orientatedunderwritingteaminthebusiness, with almost 150 years’ collective direct insurance and reinsurance experience!

Ourheadstart

Since our humble beginnings, we have achieved a number of firsts in our field. It’s all part of our quest to be recognised as the best risk provider in our chosen market, in a very competitive industry - and to offer you the best possible solutions for your clients, of course.

First to regularly cover people with severe medical impairments – those who traditionally couldn’t get cover in the marketplace.

First to offer new-generation life cover to people living with HIV.

First to regularly cover people working in high-risk countries.

First to introduce a suicide exclusion that recognises previous periods of life cover.

First to adopt standardised critical illness definitions.

First to do away with irrelevant general exclusions.

CLIENT: AltriskJOB: Sales BrochureJOB NO.: 39862DATE: 3/25/10 11:16 AM

Altrisk39862 FA.indd 11-12 2010/04/28 4:24 PM

GeneralproductsDisability Cover:These benefits pay the insured a specified lump sum in the event of disability or impairment. Again, to cater for our clients’ unique circumstances, we have several variations from which to choose.

The following three options contain a core impairment portion. These benefits are available for life or to the age of 65. If the for life option is selected, the occupational disability, functional impairment and disability income benefit portions respectively, will taper from the age of 65 to 70 at 20% per annum.

Disability:

This benefit covers the insured in the event of permanent and total occupational disablement. For added certainty it is underpinned by a core impairment benefit.

ComprehensiveDisability:

In addition to the disability benefit, comprehensive disability also covers the insured for defined functional impairment events.

DisabilityPlus:

Disability Plus incorporates all the elements from core impairment through to comprehensive disability as well as a 24-month income benefit. The impairment income portion is available for the life of the insured.

Core impairment

Income benefit

Functional impairmentOccupational disability

Core impairment

Functional impairmentOccupational disability

Core impairment

Occupational disability

Whyus?There are many reasons to do business with us. But just to give you a taste, here are a few:

• We’reowner-managedwithacorefocusontheriskmarket. We do what we do well!

• Ourquotessystemmakeslifeeasier.Thanks to simple navigation, resulting quotations are easy to read and understand.

• Wehavethesimplestapplicationforminthebusiness. Only eight pages long, including the RPAR.

• Wehavethefewestgeneralexclusionsinthemarket.Just one on our disability and impairment benefits: self-inflicted injuries.

• Weprovideaflexiblecoverfacility, which allows a reduction in premiums until it’s convenient to increase them again.

• Ourincomereplacementbenefitsareflexible,cost-effectiveandcaterforolderpeople. Almost all components of our income replacement can be taken as freestanding benefits to suit individual needs and budgets. And, we have the highest entry age for income replacement, age 65.

• Ourdeathincomebenefitispractical, providing a monthly income to the beneficiary for either 12 or 24 months after the life insured’s death. The 24-month benefit can be extended to what would have been the life insured’s expiry age (60, 65 or 70).

• Wehavethebest,solutions-orientatedunderwritingteaminthebusiness, with almost 150 years’ collective direct insurance and reinsurance experience!

Ourheadstart

Since our humble beginnings, we have achieved a number of firsts in our field. It’s all part of our quest to be recognised as the best risk provider in our chosen market, in a very competitive industry - and to offer you the best possible solutions for your clients, of course.

First to regularly cover people with severe medical impairments – those who traditionally couldn’t get cover in the marketplace.

First to offer new-generation life cover to people living with HIV.

First to regularly cover people working in high-risk countries.

First to introduce a suicide exclusion that recognises previous periods of life cover.

First to adopt standardised critical illness definitions.

First to do away with irrelevant general exclusions.

CLIENT: AltriskJOB: Sales BrochureJOB NO.: 39862DATE: 3/25/10 11:16 AM

Altrisk39862 FA.indd 11-12 2010/04/28 4:24 PM

Altrisk’s quick guide to life Dare to get to know us

www.altrisk.co.za

Altrisk39862 FA.indd 1-2 2010/04/28 4:24 PM