Embed Size (px)

Citation preview

Altius AssociatesDecember 8, 2010

Page 2Altius Associates| December 2010 Page 2

Topics for discussion

• What is the current state of global timberland investments – who, where, how?

• Where are the major centers of timber production and what is the demand outlook for paper and wood products?

• What regions do we believe offer compelling investment opportunities?

• Q & A

Page 3Altius Associates| December 2010 Page 3

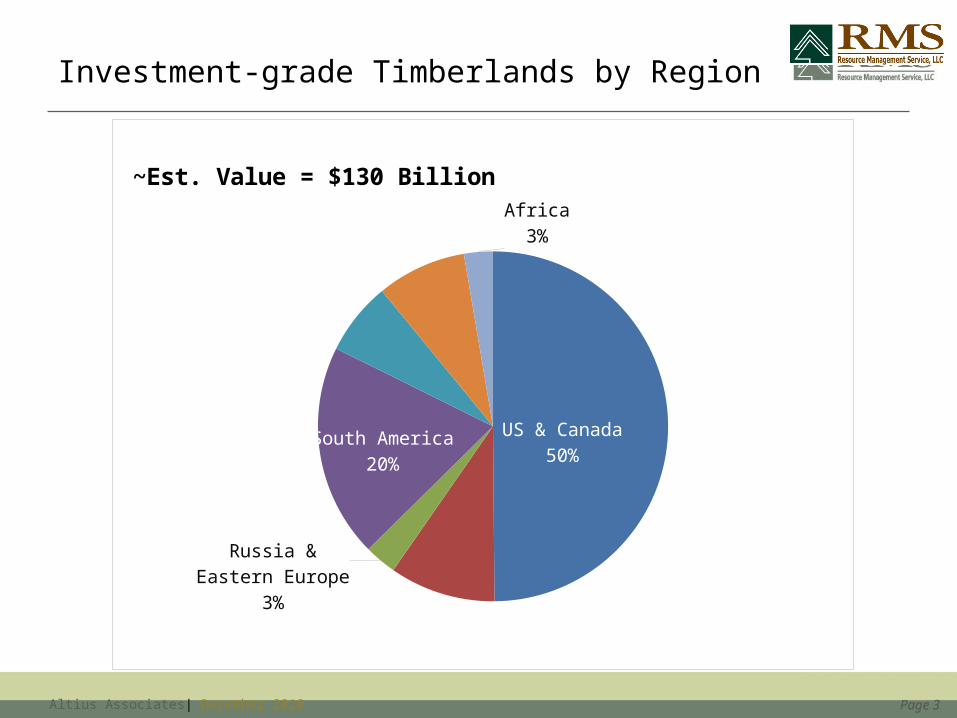

Investment-grade Timberlands by Region

US & Canada50%

Western Europe10%

Russia & Eastern Europe

3%

South America20%

Asia7%

Oceania8%

Africa3%

~Est. Value = $130 Billion

Page 4Altius Associates| December 2010

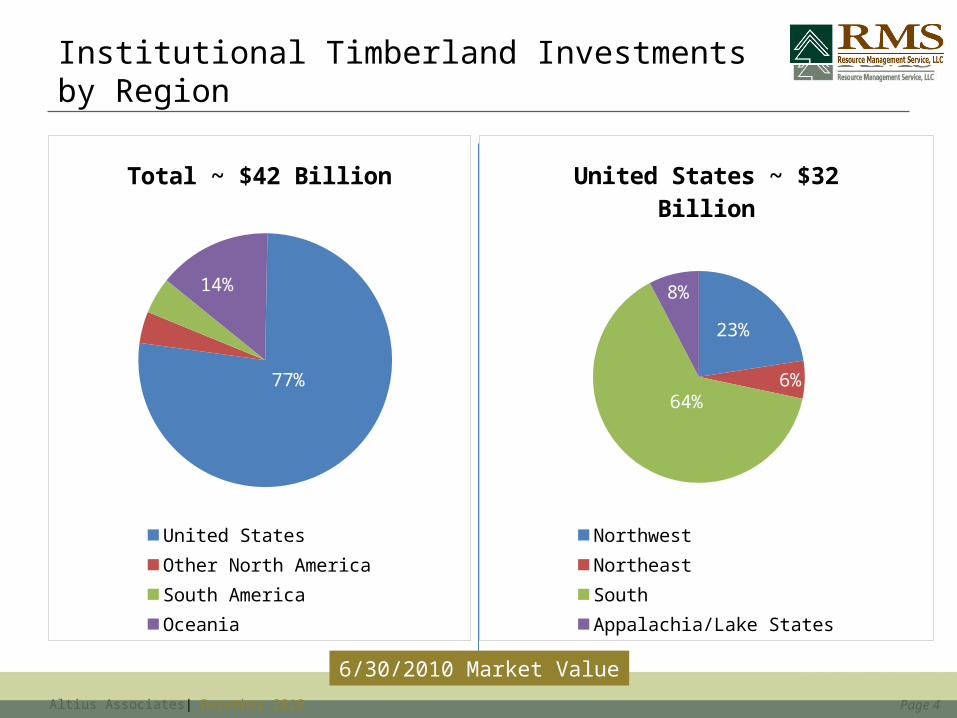

Institutional Timberland Investments by Region

77%

4%

5%

14%

Total ~ $42 Billion

United States Other North AmericaSouth America Oceania

23%

6%

64%

8%

United States ~ $32 Billion

Northwest NortheastSouth Appalachia/Lake States

6/30/2010 Market Value

Page 5Altius Associates| December 2010

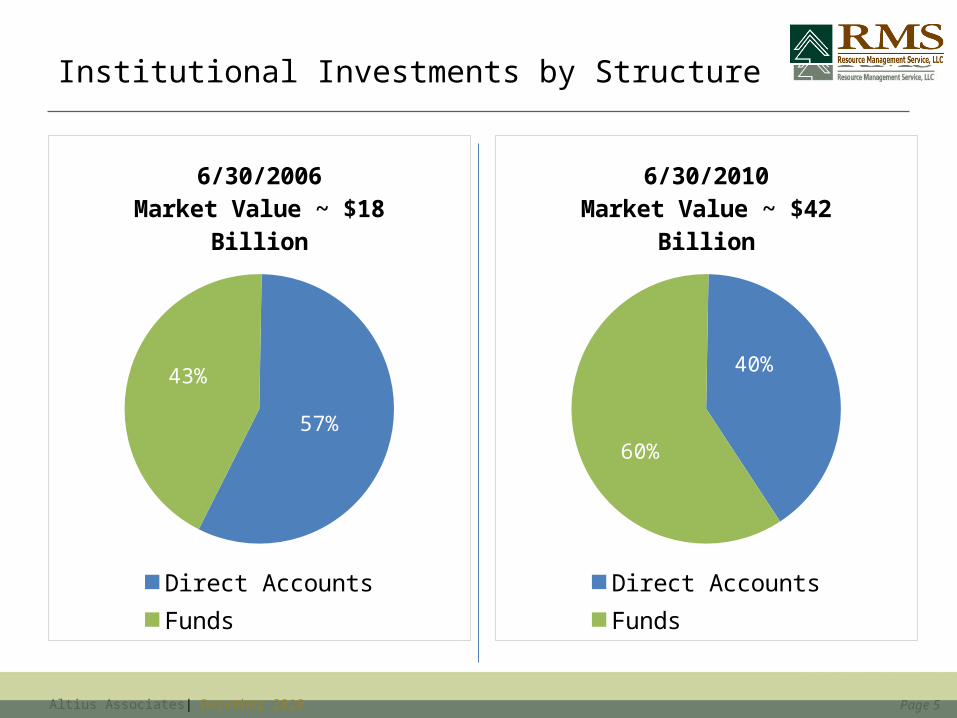

Institutional Investments by Structure

57%

43%

6/30/2006Market Value ~ $18 Billion

Direct Accounts Funds

40%

60%

6/30/2010Market Value ~ $42 Billion

Direct Accounts Funds

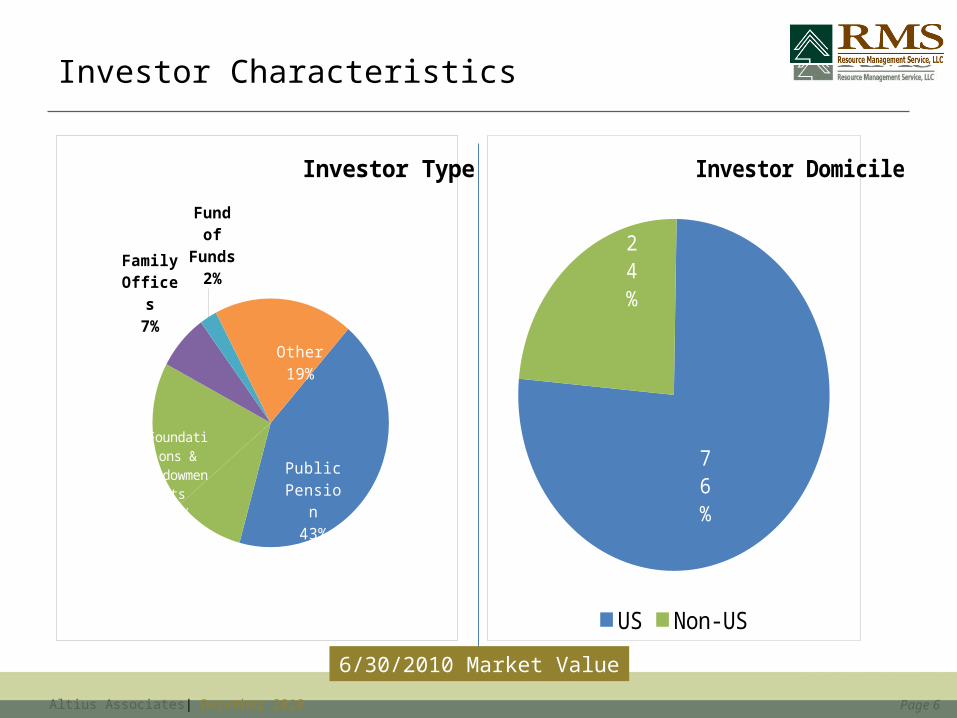

Page 6Altius Associates| December 2010

Investor Characteristics

76%

24%

Investor Domicile

US Non-US

Public Pension

43%

Corporate Pension

10%

Foundations & Endow-

ments19%

Family Of-fices7%

Fund of Funds

2%

Other19%

Investor Type

6/30/2010 Market Value

Page 7Altius Associates| December 2010 Page 7

Topics for discussion

• What is the current state of global timberland investments – who, where, how?

• Where are the major centers of timber production and what is the demand outlook for paper and wood products?

• What regions do we believe offer compelling investment opportunities?

• Q & A

Page 8Altius Associates| December 2010 Page 8

Timber Market OverviewPopulation = Demand

Page 9Altius Associates| December 2010 Page 9

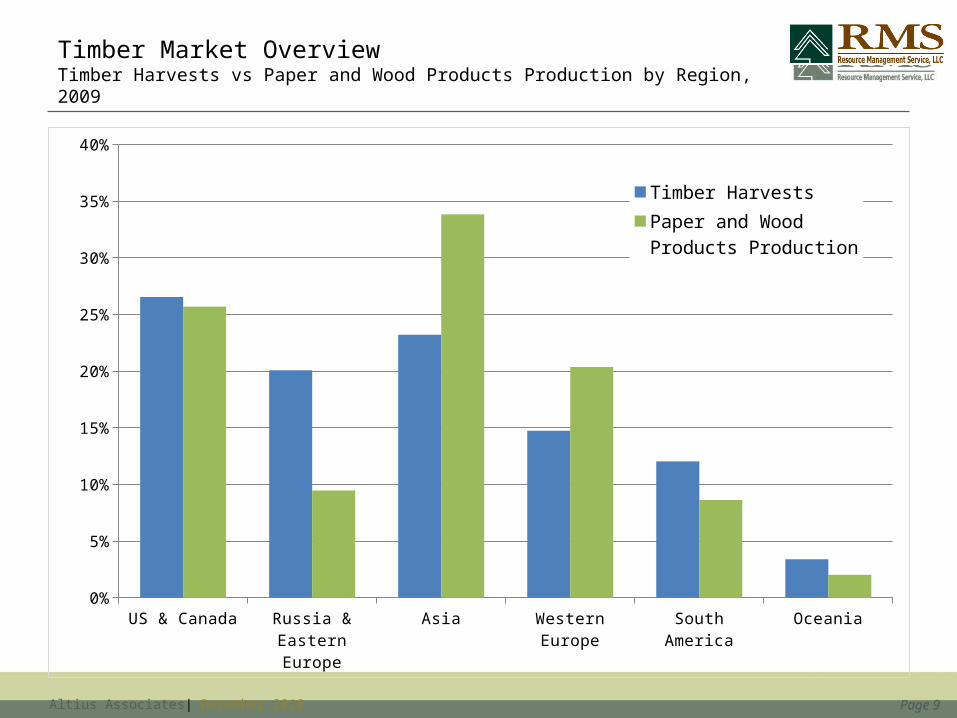

Timber Market OverviewTimber Harvests vs Paper and Wood Products Production by Region, 2009

US & Canada Russia & Eastern Europe

Asia Western Europe South America Oceania0%

5%

10%

15%

20%

25%

30%

35%

40%

Timber Harvests

Paper and Wood Products Production

Page 10Altius Associates| December 2010 Page 10

Timber Market OverviewUS Forest Production by Region

Page 11Altius Associates| December 2010 Page 11

Key Global DriverRecovery in US housing markets

Page 12Altius Associates| December 2010 Page 12

Changes in trade patterns

1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 20070

20

40

60

80

100

120

140

160

180

Timber Product Imports Pulp and Paper Imports

Million m3 Round Wood Equivalent

Sources: China Customs Data and Forest Trends Analysis 2007Note: As a benchmark, the total pine harvest in the

U.S. South in 2008 was ~180 million m3

Key Global DriverChina demand growth greatly exceeds domestic timber supplies

Page 13Altius Associates| December 2010 Page 13

Topography is challenging with high-cost cold winter logging & high logistics costs to market. Significant capital required for expansion.

Key Global DriverEconomic viability of Russian timber supplies

Page 14Altius Associates| December 2010 Page 14

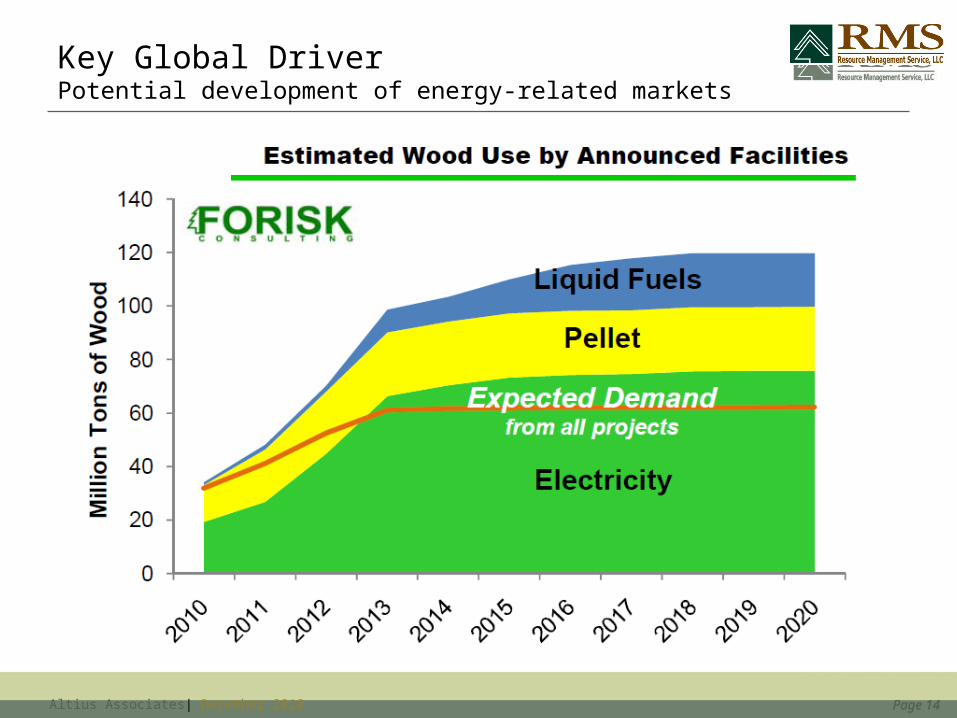

Key Global DriverPotential development of energy-related markets

Page 15Altius Associates| December 2010 Page 15

Topics for discussion

• What is the current state of global timberland investments – who, where, how?

• Where are the major centers of timber production and what is the demand outlook for paper and wood products?

• What regions do we believe offer compelling investment opportunities?

• Q & A

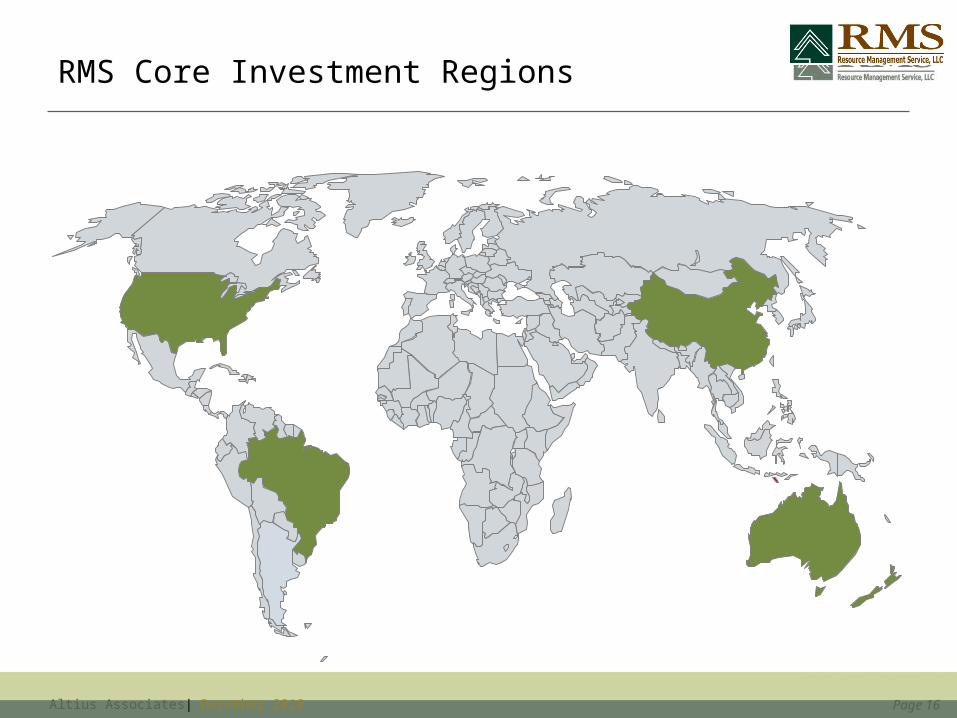

Page 16Altius Associates| December 2010

RMS Core Investment RegionsRMS Target Investment Regions

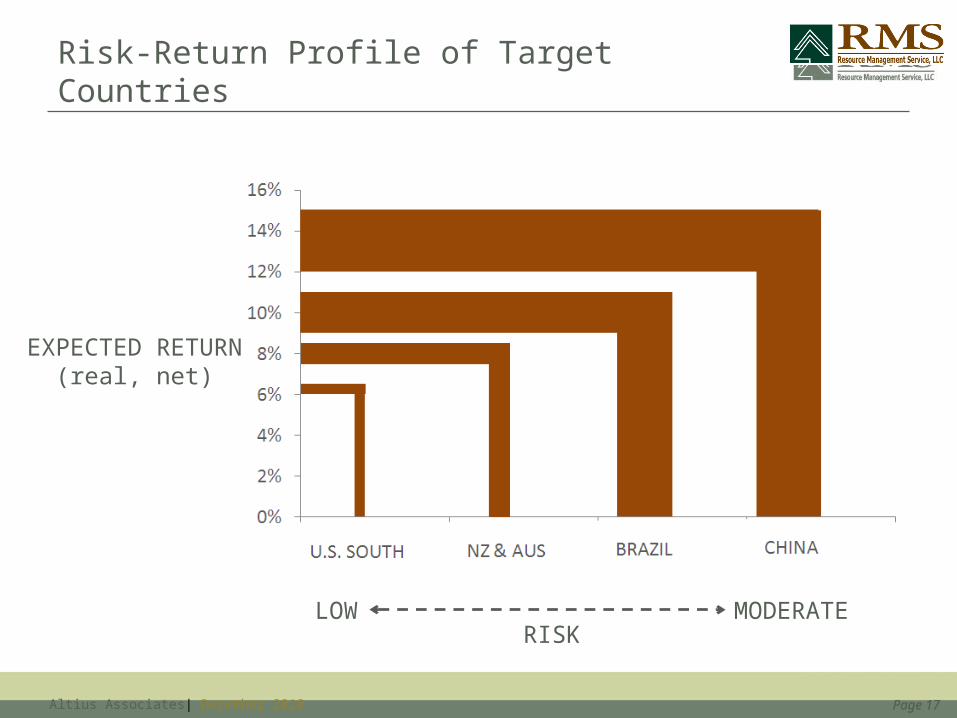

Page 17Altius Associates| December 2010 Page 17

Risk-Return Profile of Target Countries

EXPECTED RETURN(real, net)

LOW MODERATERISK

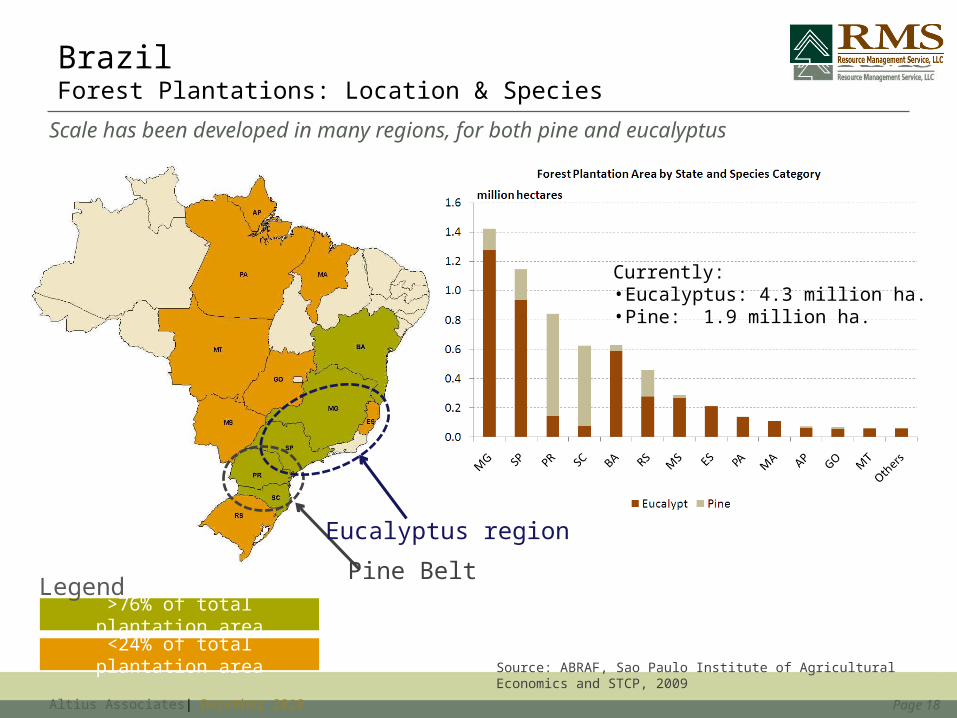

Page 18Altius Associates| December 2010

BrazilForest Plantations: Location & Species

Scale has been developed in many regions, for both pine and eucalyptus

Pine Belt

Source: ABRAF, Sao Paulo Institute of Agricultural Economics and STCP, 2009

Eucalyptus region

>76% of total plantation area

<24% of total plantation area

Legend

Currently:• Eucalyptus: 4.3 million ha.• Pine: 1.9 million ha.

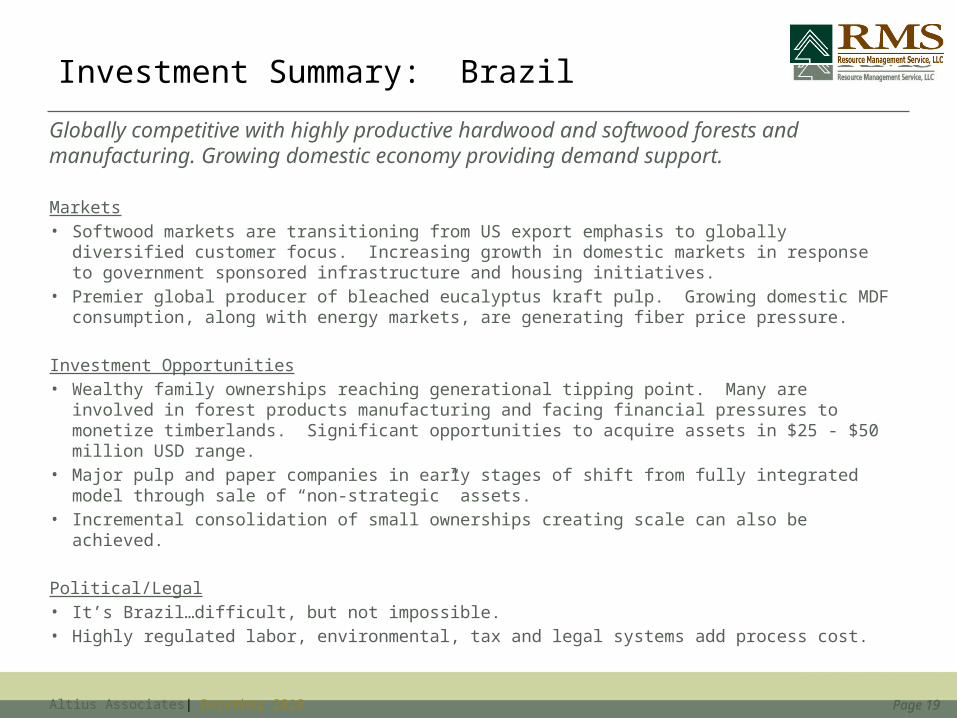

Page 19Altius Associates| December 2010 Page 19

Investment Summary: Brazil

Markets• Softwood markets are transitioning from US export emphasis to globally diversified customer focus.

Increasing growth in domestic markets in response to government sponsored infrastructure and housing initiatives.

• Premier global producer of bleached eucalyptus kraft pulp. Growing domestic MDF consumption, along with energy markets, are generating fiber price pressure.

Investment Opportunities• Wealthy family ownerships reaching generational tipping point. Many are involved in forest products

manufacturing and facing financial pressures to monetize timberlands. Significant opportunities to acquire assets in $25 - $50 million USD range.

• Major pulp and paper companies in early stages of shift from fully integrated model through sale of “non-strategic” assets.

• Incremental consolidation of small ownerships creating scale can also be achieved.

Political/Legal• It’s Brazil…difficult, but not impossible.• Highly regulated labor, environmental, tax and legal systems add process cost.

Globally competitive with highly productive hardwood and softwood forests and manufacturing. Growing domestic economy providing demand support.

Page 20Altius Associates| December 2010

New ZealandForest Plantations: Location & Species

New Zealand’s forest resource is dominated by radiata pine.

Source: MAF National Exotic Forest Description, 2008

Currently:• Radiata Pine: 1.57 million ha.• Other: 0.18 million ha.

Page 21Altius Associates| December 2010 Page 21

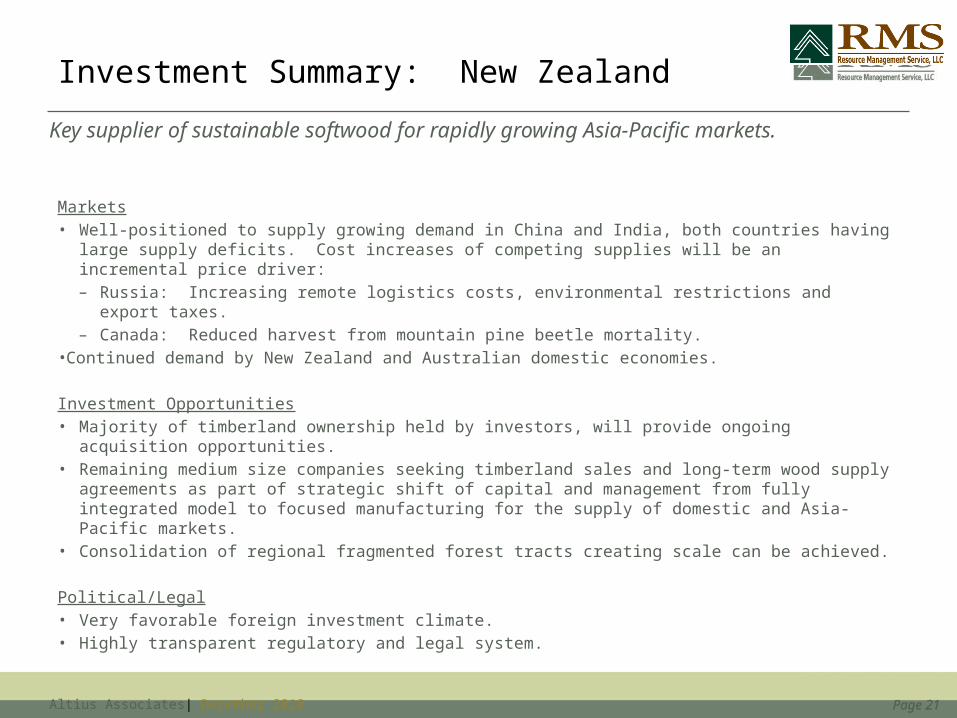

Investment Summary: New Zealand

Markets• Well-positioned to supply growing demand in China and India, both countries having large supply deficits.

Cost increases of competing supplies will be an incremental price driver:– Russia: Increasing remote logistics costs, environmental restrictions and export taxes.– Canada: Reduced harvest from mountain pine beetle mortality.

•Continued demand by New Zealand and Australian domestic economies.

Investment Opportunities• Majority of timberland ownership held by investors, will provide ongoing acquisition opportunities.• Remaining medium size companies seeking timberland sales and long-term wood supply agreements as part

of strategic shift of capital and management from fully integrated model to focused manufacturing for the supply of domestic and Asia-Pacific markets.

• Consolidation of regional fragmented forest tracts creating scale can be achieved.

Political/Legal• Very favorable foreign investment climate.• Highly transparent regulatory and legal system.

Key supplier of sustainable softwood for rapidly growing Asia-Pacific markets.

Page 22Altius Associates| December 2010

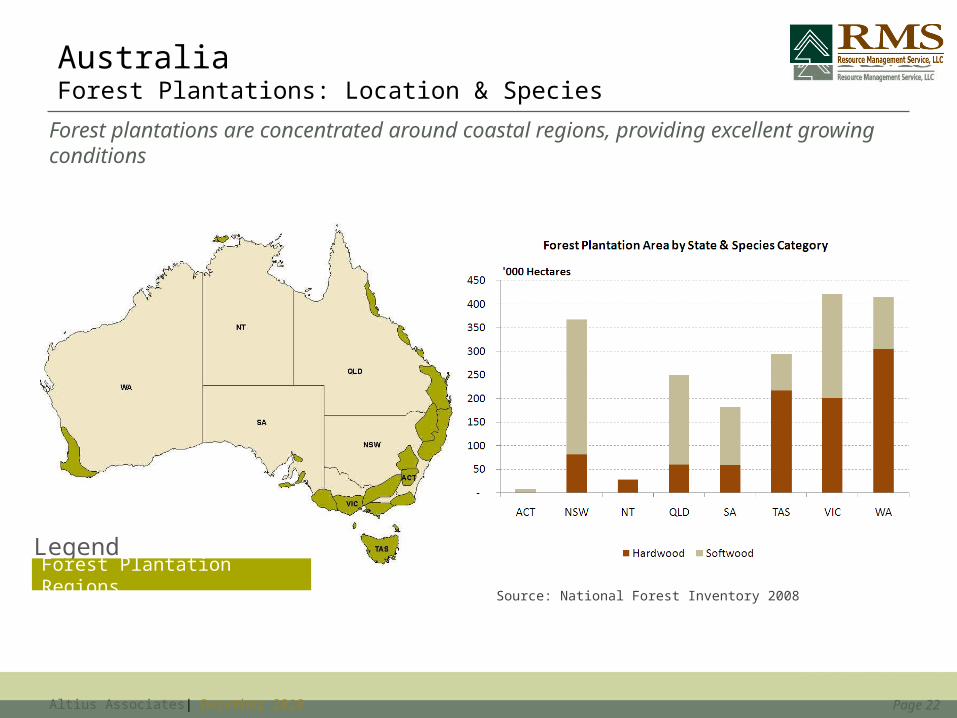

AustraliaForest Plantations: Location & Species

Forest plantations are concentrated around coastal regions, providing excellent growing conditions

Source: National Forest Inventory 2008

LegendForest Plantation Regions

Page 23Altius Associates| December 2010 Page 23

Investment Summary: Australia

Markets• Strong softwood markets driven by domestic consumption for construction, outdoor and appearance

products. Inadequate domestic supply supplemented by imports, mainly from New Zealand. • Largest supplier of hardwood chips to rapidly growing Asia-Pacific markets.

Investment Opportunities• Privatization of large public forests has begun and will provide significant opportunities to acquire quality

softwood assets.• Liquidation of overly leveraged MIS schemes may provide opportunities to acquire eucalyptus plantation

assets.

Political/Legal• Very favorable foreign investment climate.• Highly transparent regulatory and legal system.

Strong domestic softwood market and major hardwood chip exporter.

Page 24Altius Associates| December 2010 Page 24

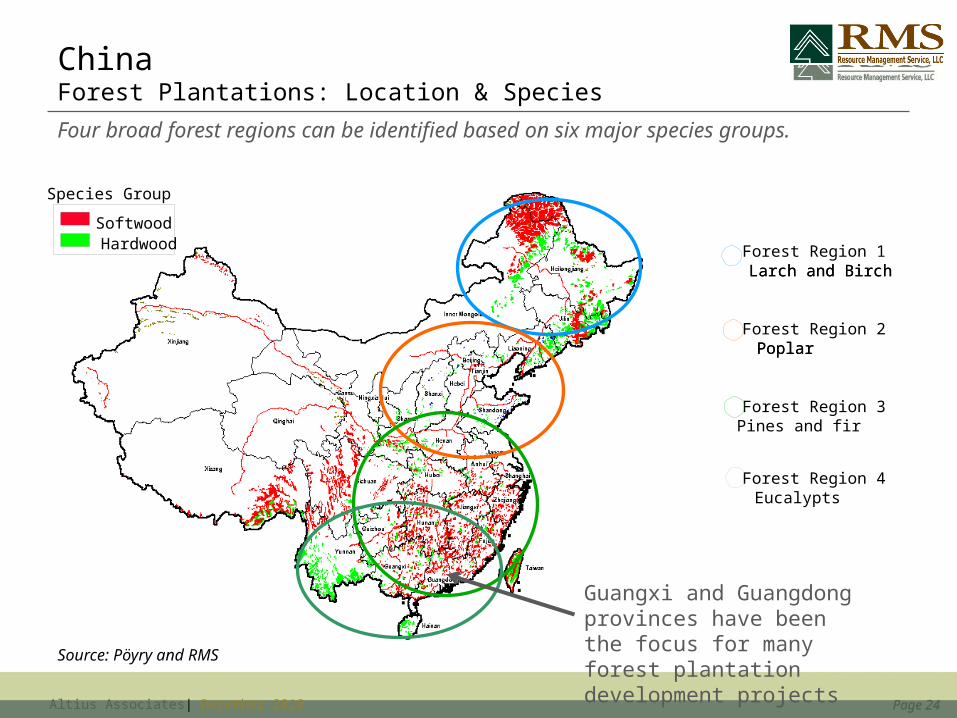

ChinaForest Plantations: Location & Species

Four broad forest regions can be identified based on six major species groups.

Source: Pöyry & RMS Analysis 2007

Masson pineChinese firSouthern pines

SprucePineFirHemlock

Larch

OakAshBirchAspen

Hardwood &Rainforest

Fibre

Masson pine Chinese firSpruce

PineFirHemlock

Larch

OakAshBirchAspen

Hardwood &Rainforest

Forest Region 1Larch and Birch

Forest Region 2Poplar

Forest Region 3Pines and fir

Forest Region 4

Masson pineChinese firSouthern pines

SprucePineFirHemlock

Larch

OakAshBirchAspen

Hardwood &Rainforest

Fibre

Masson pine Chinese firSpruce

PineFirHemlock

Larch

OakAshBirchAspen

Hardwood &Rainforest

Masson pineChinese firSouthern pines

SprucePineFirHemlock

Larch

OakAshBirchAspen

Hardwood &Rainforest

Softwood Hardwood

Species Group

Source: Pöyry and RMS

Larch and Birch

Poplar

Eucalypts

Guangxi and Guangdong provinces have been the focus for many forest plantation development projects

Page 25Altius Associates| December 2010 Page 25

Investment Summary: China

Markets• China’s strong demand growth is pulling increasing imports, equivalent to US Southern pine harvest.• Domestic sawlog and pulp log pricing is based on import parity.

Investment Opportunities• Estates accumulated by medium to large size companies to assure fiber supply are becoming

available as owners shift capital and management from a fully integrated model to leading edge manufacturing. These former owners will provide market stability as a major customer.

• Incremental consolidation with smaller acquisitions creating scale can also be achieved.

Political/Legal• Forests can be privately owned with long term leases and are transferable.• Sustainable commercial forests and associated rural manufacturing have strong political support.• Transparency of the tax and regulatory systems has substantially improved with WTO entry.• Legal protection, tax minimization and capital repatriation supported with Hong Kong structures.

Strongest growing global forest products market that is sustained by domestic growth with a perennially large and increasing fiber supply deficit.

Page 26Altius Associates| December 2010

Questions?