Embed Size (px)

Citation preview

STRICTLY PRIVATE AND CONFIDENTIAL

For conference attendees of

Invest‟11 only

© NomuraSeptember 2011

Alternative Investments –

Trends in Strategies & Structures

Sandy Rattray

Chief Investment Officer

Man Systematic Strategies

DISCLAIMER

Important notes

This material is communicated by Man Investments AG (the „Company‟), which is regulated and authorised by the Swiss Financia l Market Supervisory Authority (FINMA).

This material is for educational purposes only and should not be relied upon for any other purpose. This material includes facts, views and opinions of global economic markets

deemed of interest.

This material is only to be communicated to investment professionals and professional clients only and should not be relied upon by any other person.

The information is submitted on a confidential basis to the attendees only and may not be reproduced to anyone else other than the attendees.

This material is proprietary information of the Company and its affiliates and may not be reproduced or otherwise disseminated in whole or in part without prior written consent

from the Company. The Company believes its data and text services to be reliable, but accuracy is not warranted or guaranteed. We do not assume any liability in the case of

incorrectly reported or incomplete information.

Information contained herein is provided from the Man database except where otherwise stated. Please be aware that investment products involve investment risks, including

the possible loss of the principal amount invested. Alternative investments can involve significant risks and the value of an investment may go down as well as up. Returns may

increase or decrease as a result of currency fluctuations. The data used herein constitutes the latest data available at the time of production.

The Company and/or any of its affiliates may have an investment in the described investment products.

Benchmarks and financial indices are shown only for illustrative purposes. There are inherent limitations in any comparison between a managed portfolio and a passive index.

Each index is unmanaged and does not incur management fees, transaction costs and other expenses associated with a managed portfolio.

In preparing this material, we have relied upon and assumed, without independent verification, the accuracy and completeness of all information available from public sources

or which was provided to us or otherwise reviewed by us. Some statements contained in these materials concerning goals, strategies, outlook or other non-historical matters

may be “forward-looking statements” and are based on current indicators and expectations. These forward-looking statements speak only as of the date on which they are

made, and The Company undertakes no obligation to update or revise any forward-looking statements. These forward-looking statements are subject to risks and uncertainties

that may cause actual results to differ materially from those contained in the statements.

This material is not suitable for US persons.

www.maninvestments.com

Source: Man database.

1. As at 30 June 2011 (Unaudited final figures).

2. As at 30 June 2011 (permanent employees).

3. As at 30 June 2011.

An independent alternative asset manager able to draw on the backing of a robust balance sheet

Offering a comprehensive range of transparent trading strategies across the liquidity spectrum, with US$71.0bn

under management1

Benefits from an extensive pool of talented professionals, with approximately 1,600 employees2 worldwide

Serves a highly-diversified and global client base through a powerful distribution network

A constituent of the FTSE 100 Index (UK: EMG) with a market capitalisation of US$7.0bn3

Strength through size, capital position, independence and global presence

Introduction to Man

2

1. Please note that Nephila is Man affiliated manager but is not wholly owned by Man Group.

Integrating world-leading investment talent in a single asset management entity

Introduction to Man

AHL GLG Multi-managerSingle manager

platform

Quantitative managed

futures manager

Multi-strategy global

alternative investment

specialist

Credit and convertibles

Long-only funds

FoHFs

Structured products

Managed accounts

Advisory solutions

Convertible bonds

Man Systematic Strategies

Nephila¹

Regulated in 17 jurisdictions worldwide

US

Cayman Is.

UKUAESwitzerlandNetherlands Singapore

Guernsey Hong Kong Ireland

LuxembourgJapan

Australia

Uruguay

ItalyCanadaBermuda

3

HF industry recovery from financial crisis

Investors’ search for transparency and liquidity

Success through innovation in systematic strategies

Source: HFR Global Hedge Fund Industry Report Q2 2011.

Industry AuM January 01, 1990 – June 30, 2011

HF industry recovery from financial crisis

0

200,000

400,000

600,000

800,000

1,000,000

1,200,000

1,400,000

1,600,000

1,800,000

2,000,000

2,200,000

1990 1991 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 Q1 2011

Q2 2011

Hedge fund industry AuM (USD million)

4

HF industry recovery from financial crisis

Source: Bloomberg.

There is no guarantee of trading performance and past or projected performance is not a reliable indicator of future performance. Please note that the HFRI data over the last four months may be subject to change.

Hedge funds: HFRI Fund Weighted Composite Index. World stocks: MSCI World (USD, NDTR) Hedged. World bonds: Citigroup World Government Bond Index hedged to USD (Total return).

The core proposition of hedge funds reinforced

5

January 01, 1994 – January 31, 2011

0

1,000

2,000

3,000

4,000

5,000

6,000

1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Index value (US$)

End value

US$2,532

End value

US$4,882

End value

US$2,824

HFRI fund weighted composite index World stocks World bonds

(600)

(400)

(200)

0

200

400

600

1,300

1,400

1,500

1,600

1,700

1,800

1,900

2,000

2,100

2006 2007 2008 2009 2010 Q1 2011

Net flow Net performance Estimated assets

HF industry recovery from financial crisis

As at March 31, 2011.

Source: HFR, Q1 2011 report.

Flows dominated by $1bn+ firms, but still

a place for niche

Part of broader 2011 move across assets

into risk, out of low yield/cash

2011 industry flows show healthy demand for liquid alternatives

2006 – Q1 2011 Hedge fund industry flows trajectory

6

Industry rebuilds

through performanceFlow pick

up

(AUM US$bn) Net asset

increase

HF industry recovery from financial crisis

Investors’ search for transparency and liquiditySuccess through innovation in systematic strategies

Source: SEI Knowledge Partnership and Greenwich Associates, „The Era of the Investor: New Rules of Institutional Hedge Fund Investing‟, January 2011.

Investors’ search for transparency and liquidity

0 5 10 15 20 25

Educating board

Headline risk/bad press

Manager selection

Understanding risk

Earning non-correlated returns

Liquidity

Fees/value for money

Meeting performance expectations

Transparency

Respondents (%)

7

Single most important challenge faced, respondents (%)

What kind of portfolio information will you require from hedge fund managers?

Investors’ search for transparency and liquidity/2

2009 Deutsche Bank Alternative Investment Survey. Source: Deutsche Bank.

0

10

20

30

40

50

60

70

80

90

100

Performance Risk exposures Asset classes Regional breakdown Industry breakdown Largest positions Full position transparency

Respondents (%)

2008 2009

Even though with fewer importance than other aspects of transparency, investors‟ interest in full position transparency has increased

the most

8

Investors’ search for transparency and liquidity

Performance paramount, but confidence and understanding the key to rebuilding trust

Investor preferences Industry outcomes

Provide me with controlled, transparent and

flexible investment outcomes

Deliver my investment in formats I

know and trust

Re-assure me that the investment manager’s

business model is sustainable

Liquid strategies, un-benchmark constrained, with low

correlations to traditional allocations

MACs

Standalone allocations, completion portfolios, overlay

strategies

UCITS

Daily pricing, detailed reporting

Asset flow to managers demonstrating

– Financial and regulatory strength

– Transparency

– Resources to invest in people, systems and research

9

Do you use managed accounts?

Investors’ search for transparency and liquidity

2009 Deutsche Bank Alternative Investment Survey. Source: Deutsche Bank.

0

10

20

30

40

50

60

70

2004 2005 2008 2009

Respondents (%)

Yes No N/A

Managed accounts offer considerable transparency, liquidity and reporting benefits

10

Appetite for managed account investments has increased steadily

Investors’ search for transparency and liquidity

Regulatory trends taking greater shape

Enhanced manager regulation

Changing capital requirements for banks

Trading increasingly centralised and on-

exchange

Workable outcomes for scale managers

Depth of resources and breadth of offering key

Less crowded trading

Opportunities to capture spin-out teams

Increasing opportunity and efficiency

Premium on operational capability

11

Regulatory trends across the world

Investors’ search for transparency and liquidity

Cost to comply estimated at €5bn in Europe alone

Migration from consultation

to implementation

Different speeds and approaches

Deep regulatory expertise and

relationships a must have

Global themes

New regulatory architecture

AIFM Directive reached workable

compromise, detail to come

UCITS IV and V

OTC derivative trading review

and more…

Europe

Dodd-Frank: Challenge of

rule-making

OTC derivatives trading reform: US

6–12 months ahead of Europe

Volcker rule and spin out of hedge

teams and prop desks

US

Focus on selling process

and understanding

Product key information sheets and

enhanced risk disclosure

Classification of derivative products

Asia-Pacific

12

HF industry recovery from financial crisis

Investors’ search for transparency and liquidity

Success through innovation in systematic strategies

Equity hedged (%) Relative value (%) Event driven (%) Global macro (%) Managed futures (%)

1994 2.61 4.00 6.00 (4.30) (6.13)

1995 31.04 15.66 25.11 29.32 16.23

1996 21.75 14.49 24.84 9.32 18.18

1997 23.41 15.93 21.23 18.82 16.37

1998 15.98 2.81 1.70 6.19 12.94

1999 44.22 14.73 24.33 17.62 (4.37)

2000 9.09 13.41 6.74 1.97 7.20

2001 0.40 8.92 12.18 6.87 3.97

2002 (4.71) 5.44 (4.30) 7.44 26.67

2003 20.54 9.72 25.33 21.42 16.93

2004 7.68 5.58 15.01 4.63 3.39

2005 10.60 6.02 7.29 6.79 (1.95)

2006 11.71 12.37 15.33 8.15 6.20

2007 10.48 8.94 6.61 11.11 5.68

2008 (26.65) (18.04) (21.82) 4.83 17.45

2009 24.57 25.81 25.04 4.34 (7.55)

2010 10.45 11.43 11.86 8.06 13.27

Rank Best 2 3 4 5

Different hedge fund styles perform well in different time periods

Success through innovation in systematic strategies

13

Equity hedged: HFRI Equity Hedge (Total) Index. Relative value: HFRI Relative Value (Total) Index. Event driven: HFRI Event-Driven (Total) Index. Global macro: HFRI Macro (Total) Index. Managed futures: Stark 300 Trader Index.

The Stark 300 Trader index is 1.7 times levered to reflect Man‟s investment approach to managed futures.

Please note that the HFRI index data over the past 4 months may be subject to change.

Source: Bloomberg & Stark & Co, Inc.

Success through innovation in systematic strategies

Source: Article «What Happened To The Quants In August 2007?» written by Amir E. Khandani and Andrew W Lo.

A number of quantitative long/short equity hedge funds experienced unprecedented losses during the week of August 6, 2007

Hypothesis: Losses initiated by the rapid “unwind” of one or more sizeable quantitative equity-market neutral portfolios

Likely the result of a forced liquidation by a multi-strategy fund or a proprietary trading desk

Initial losses put further pressure on broader set of equity portfolios, causing further losses by triggering stop/loss and

de-leveraging policies

Significant rebound in these strategies on August 10th

What happened to the quants in August 2007? (A. E. Khandani and A. Lo)

14

-15%

-10%

-5%

0%

5%

10%

15%

20%

25%

08/06/07 08/07/07 08/08/07 08/09/07 08/10/07 08/13/07 08/14/07 08/15/07

Leveraged Contrarian Strategy S&P 500 S&P 600 (Small Cap) Lehman Corp-Gov

Unique factors

Innovative models

Long run experience

Solution

Performance of GLG broker ideas vs. ALL analyst recommendations from ALL brokers in Europe

Success through innovation in systematic strategies

Buy ideas provided to GLG by brokers have outperformed the market consistently

Ideas provided to GLG generally perform better than the average of all broker recommendations in the market

GLG specifically requests medium-term (60–90 day) ideas

0.0

0.5

1.0

1.5

2.0

0 10 20 30 40 50 60 70Business days after announcement day close

GLG buy recommendations IBES buy recommendations

Outperformance vs. market (%)

GLG

alpha

GLG typically reacts here

Long-only manager typically reacts here

Long-only

manager

alpha

Recommendation alpha slows

Performance of GLG broker ideas vs. ALL analyst recommendations from ALL brokers in Europe

15

Source: Source: GLG Partners LP, data as at Q4 2010

We have shown excess performance to the market, using the D J STOXX Large, Mid or Small cap index depending on the market cap of the stock. Performance is set at zero on the close of the day the recommendation is made.

IBES is the Institutional Brokers‟ Estimate System which collects, analyses and redistributes broker forecast estimates and recommendations for companies across the globe and is publicly available

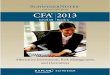

Intra-day volatility increased in week prior to Lehman

default

– Higher level compared to end August 2008 and beginning of

September 2008

September 2008 timeline

– Model forecast becomes higher than variance swap rates

– Trade initiated on September 11, 2008 when confirmation

received from implied volatility market

– Volatility increased significantly after announcement of

Lehman default (September 15)

Success through innovation in systematic strategies

Source: Man database and Bloomberg.

There is no guarantee of trading performance and past performance is no indication of current of future performance/results. Return data consists of the pro-forma profit and loss for the various strategies.

Neil Shephard and Kevin Sheppard (2010): “Realising the future: Forecasting with high-frequency-based volatility (HEAVY) models”, Journal of Applied Econometrics, vol. 25, pp 197-231.

Volatility spike detection through HEAVY models

0

20

40

60

80

25-Aug 30-Aug 04-Sep 09-Sep 14-Sep 19-Sep 24-Sep 29-Sep

Intraday volatility Model forecast 1m variance swap

Assessing volatility changes prior to/after Lehman default

(August 25, 2008 – September 30, 2008)

Lehman default (September 15)

Trade signal

16

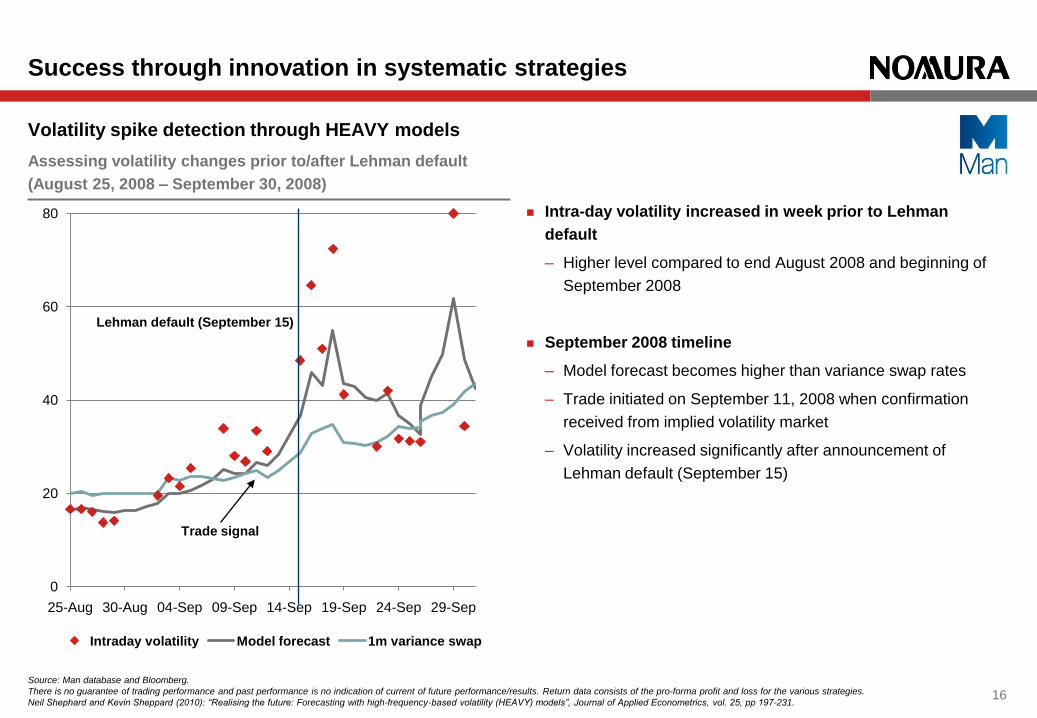

Value proposition

Central bank actions tend to be gradual, investor behaviour is

typically persistent short term interest rates often trend

Persistent slope of curve leads to a carry effect

Model characteristics

This model is based on momentum trading of the short end

Automatically detects the carry effect

It builds on AHL‟s core competency in futures

In the event of a regime shift, the model follows the move

(positive skew)

IRS markets are also attractive

Success through innovation in systematic strategies

Experience in short end rates trading

0.00

0.20

0.40

0.60

0.80

1.00

1.20

3m 6m 9m 12m 15m

Forward curve of interest rates

Forward curve of interest rates three months later

(%)

17Schematic illustration.

Source: Man database.

Carry Rates

move

The mean reversion challenge

– Deviation from the mean: Bet on reversion

– Further deviation: Increase bet (bigger opportunity) or reduce bet (regime shift)?

Systematic risk reduction in mean reversion strategies

Success through innovation in systematic strategies

Solution

– Mean reversion is parameterised by volatility, σ, and strength of mean reversion, λ.

– Markowitz, Kelly, Control theory all argue for a bet proportional to λ/σ^2

– In a regime shift: σ typically increases; λ decreases so positions decrease and losses are capped

– Cap positions by expected sharpe of the position

Ra

te

Tenorwingbodywing

18Schematic illustration.

Source: Man database.

Simple carry strategy

– On average, investors get paid for holding EM currencies

– Flight to quality gives occasional deep drawdowns, negative skew

Making carry trading robust

Success through innovation in systematic strategies

Carry + regime detection

– Reduce/close/short carry positions during flight to quality

– Reduced drawdowns, small positive skew (5%)

15%

35%

55%

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

19

MSS FX active carry

Source: Man database.

The simulated past performance of the Man Systematic Fixed Income portfolio is based on the weighted returns of its constituting underlying funds, including estimated transaction costs but excluding management and performance

fees. Simulated past performance means performance that has been calculated for a period for which no actual performance information for the is available. Actual performance results may differ, and may differ substantially, from

such simulated past performance. The simulated past performance is for information purposes only.

A systematic fixed income product

Success through innovation in systematic strategies

(25)

25

75

125

175

225

2001 2002 2003 2004 2005 2006 2007 2008 2009 2010 2011

Cumulative returns

FX active carry Yield curve shape Short end rates Total return

20

Source: Man database.

The simulated past performance of the Man Systematic Fixed Income portfolio is based on the weighted returns of its constituting underlying funds, including estimated transaction costs but excluding management and performance

fees. Simulated past performance means performance that has been calculated for a period for which no actual performance information for the is available. Actual performance results may differ, and may differ substantially, from

such simulated past performance. The simulated past performance is for information purposes only.

STRICTLY PRIVATE AND CONFIDENTIAL

For conference attendees of

Invest‟11 only

© Nomura

This presentation has been prepared by Man Investments AG and Nomura takes no responsibility for the contents. Nomura International plc is authorised and regulated by UK Financial Services Authority (FSA). This presentation is

intended only for investors who are "eligible market counterparties" or "professional clients" as defined by FSA. This presentation is not intended for retail clients and should not be distributed as such. You may not without the prior written

consent of NIplc distribute, reproduce, in whole or in part, summarise, quote from or otherwise publicly refer to the contents of this presentation. This presentation is for discussion purposes only. This presentation does not constitute an offer

to sell, or the solicitation of an offer to purchase, any securities. All opinions and estimates included in this document constitute NIplc's judgment as of this date and are subject to change without notice. There can be no assurance, nor is

there any guarantee (implied or otherwise), that any opinions contained in this document related to any forecasts will be met. The information contained herein is believed to be accurate in all respects, but no representation or warranty,

expressed or implied, as to its accuracy or completeness is made by any party. Nothing contained herein should be relied upon as a promise or representation as to the future. Information contained in this presentation is not intended to

provide, and should not be relied upon for, accounting, legal, or tax advice or investment recommendations. It does not constitute a personal recommendation as defined by the FSA, or take into account the particular investment objectives,

financial situations, or needs of individual investors. You should consult your tax, legal and accounting advisers about the issues discussed herein and you shall be responsible for evaluating the risks and merits involved in any investment

described in this presentation. Information on any particular tax treatment may not be applicable to your individual circumstance and may be subject to change in the future. NIplc gives no assurance or guarantee that forecasts contained in

this presentation will be met. Figures presented in this document may refer to the past or simulated past performance. Past and simulated past performance is not a reliable indicator of future performance.