Embed Size (px)

Citation preview

Alternative Investments

Alternative Investments is an investment that is not one of the three traditional asset types (stocks, bonds and cash). Many alternative investments also have high minimum investments and fee structures compared to mutual funds and ETFs. While they are subject to less regulation, they also have less opportunity to publish verifiable performance data and advertise to potential investors.

Alternative investments are favored mainly because their returns have a low correlation with those of standard asset classes. Because of this, many large institutional funds such as pensions and private endowments have begun to allocate a small portion (typically less than 10%) of their portfolios to alternative investments such as hedge funds.

Hedge Funds

An aggressively managed portfolio of investments that uses advanced investment strategies such as

leveraged, long, short and derivative positions in both domestic and international markets with the goal

of generating high returns (either in an absolute sense or over a specified market benchmark).

Legally, hedge funds are most often set up as private investment partnerships that are open to a limited

number of investors and require a very large initial minimum investment. Investments in hedge funds

are illiquid as they often require investors keep their money in the fund for at least one year.

Both mutual funds and hedge funds are managed portfolios. This means that a manager (or a group of managers) picks securities that he or she feels will perform well and groups them into a single portfolio. Portions of the fund are then sold to investors who can participate in the gains/losses of the holdings. The main advantage to investors is that they get instant diversification andprofessional management of their money.

Just like a mutual fund, a hedge fund is a pooled investment vehicle that makes investments in equities, bonds, options and a variety of other securities.

Hedge funds are managed much more aggressively than their mutual fund counterparts. They are able to take speculative positions in derivative securities such as options and have the ability to short sell stocks. This will typically increase the leverage - and thus the risk - of the fund. This also means that it's possible for hedge funds to make money when the market is falling. Mutual funds, on the other hand, are not permitted to take these highly leveraged positions and are typically safer as a result.

Another key difference between these two types of funds is their availability. Hedge funds are only available to a specific group of sophisticated investors with high net worth. The U.S. government deems them as "accredited investors", and the criteria for becoming one are lengthy and restrictive. This isn't the case for mutual funds, which are very easy to purchase with minimal amounts of money.

For starters, hedge funds are not regulated. There are limits to what they can do, such as the number of investors they can have, or the fact they cannot advertise to the general public, but they are not regulated by theSEC per se. The implications of this are that an investor should be properly informed about a hedge fund, its strategy and the character of the principals before investing.

Hedge Funds: Risks

Standard DeviationThe most common risk measure used in both hedge fund and mutual fund evaluations is standard deviation. Standard deviation in this case is the level of volatility of returns measured in percentage terms, and usually provided on an annual basis. Standard deviation gives a good indication of the variability of annual returns and makes it easy to compare to other funds when combined with annual return data. For example, if comparing two funds with identical annualized returns, the fund with a lower standard deviation would normally be more attractive, if all else is equal.

Unfortunately, and particularly when related to hedge funds, standard deviation does not capture the total risk picture of returns. This is because most hedge funds do not have normally distributed returns, and standard deviation assumes a bell-shaped distribution, which assumes the same probability of returns being above the mean as below the mean.

Downside Capture

In relation to hedge funds, and in particular those that claim absolute return objectives, the measure

of downside capture can indicate how correlated a fund is to a market when the market declines. The

lower the downside capture, the better the fund preserves wealth during market downturns. This metric

is figured by calculating the cumulative return of the fund for each month that the market/benchmark

was down, and dividing it by the cumulative return of the market/benchmark in the same time frame.

Perfect correlation with the market will equate to a 100% downside capture and typically is only

possible when comparing the benchmark to itself.

DrawdownAnother measure of a fund's risk is maximum drawdown. Maximum drawdown measures the percentage drop in cumulative return from a previously reached high. This metric is good for identifying funds that preserve wealth by minimizing drawdowns throughout up/down cycles, and gives an analyst a good indication of the possible losses that this fund can experience at any given point in time. Months to recover, on the other hand, gives a good indication of how quickly a fund can recuperate losses. Take the case where a hedge fund has a maximum drawdown of 4%, for example. If it took three months to reach that maximum drawdown, as investors, we would want to know if the returns could be recovered in three months or less. In some cases where the drawdown was sharp, it should take longer to recover. The key is to understand the speed and depth of a drawdown with the time it takes to recover these losses. Do they make sense given the strategy?

LeverageFinally, leverage is a measure that often gets overlooked, yet is one of the main reasons why hedge funds incur huge losses. As leverage increases, any negative effect in returns gets magnified and worse, and causes the fund to sell assets at steep discounts to cover margin calls. Leverage has been the primary reason why hedge funds like LTCM and Amaranth have gone out of business. Each of these funds may have had huge losses due to the investments made, but chances are these funds could have survived had it not been for the impact of leverage and the effect it had on the liquidation process.

Hedge Funds: Why Choose Hedge Funds?

Risk Reduction

In any case, a hedge fund that provides consistent returns increases the level of portfolio stability when

traditional investments are underperforming or, at most, are highly unpredictable. There are many

hedge fund strategies that generate attractive returns with fixed-income-like volatility. The difference

between a hedge fund and traditional fixed income, however, is that during times of low interest rates,

fixed income may provide stable returns, but those are typically very low and may not even keep up

with inflation.

Hedge funds, on the other hand, can use their more flexible mandates and creativity to generate bond-

like returns that outpace inflation on a more consistent basis. The drawback, as previously mentioned, is

that hedge funds have certain terms that limit liquidity and are highly opaque. That said, a carefully

analyzed hedge fund can be a good way to reduce the risk of a portfolio, but we stress again the

importance of proper due diligence. ( Learn more in Due Diligence In 10 Easy Steps.)

Return Enhancement

The other primary reason for adding hedge funds to a portfolio is the ability of some hedge funds to

enhance the overall returns of a portfolio. This objective can be considered in two ways. The first way is

to maintain a low-risk portfolio but to try to squeeze out some additional returns through the use of a

low-volatility hedge fund, as described in the previous section. By adding a hedge fund strategy that

substitutes for an otherwise anemic fixed-income return, the returns on a portfolio can be increased

slightly without any increase in volatility.

The second way, which is much more exciting, is to add a hedge fund with a high-return strategy to boost overall returns. Some strategies, such as global macro, or commodity trading advisors, can generate some very high returns. These funds generally take directional positions based on their forecast of future prices on stocks, bonds, currencies, and/or commodities and can also invest using derivative instruments. But buyer beware that although these strategies are not correlated to traditional investments, they often exhibit high levels of volatility. The result, when properly allocated, can be a nice boost in returns without a proportional increase in portfolio volatility. (Learn more in Macroeconomic Analysis.)

Allocation ConsiderationsAdding hedge funds to a portfolio, however, should not be taken lightly. Even a low-volatility hedge fund can explode, as we saw in late 2007, when thesubprime mortgage market dried up and even securities that were paying as planned were written down to pennies on the dollar, as investors bid down their prices for fear of foreclosures. (Learn more in The Fuel That Fed The Subprime Meltdown.)

The allocation to hedge funds should consider the overall risk/return objectives of the portfolio, and proper analysis should be conducted to determine how and whether a particular hedge fund fits into the asset mix. A portfolio manager should not only consider the weighting given to any particular investment, but should also evaluate the level of concentration of the overall portfolio, and the correlation of each position relative to each other. For example, in a very concentrated portfolio, it is even more important that each position is less correlated to others, and one must also make sure that positions do not have similar performance drivers.

Yet another consideration when adding hedge funds to a portfolio is the level of gross and net exposure of the overall portfolio. With traditional investments, for example, gross and net exposure will always be the same and will never exceed 100% unless the portfolio adds its own leverage to its positions. With hedge funds, however, many of them employ leverage and in many cases, their net exposure is influenced by their long and short positions.

Therefore, a larger allocation to hedge funds will directly affect the total exposures of an entire portfolio. To use a highly leveraged fund as an example, assume a 10% position in a fund that is 10-times levered. If all other portfolio positions maintain a 100% exposure, the addition of a 10-times levered hedge fund will increase the gross exposure of the entire portfolio to 190%. The implications of this change can be dramatic depending on the strategy being used by the hedge fund.

MANAGED FUTURES

- The term managed futures describes an industry comprised of professional money managers known as commodity trading advisors (CTAs). These trading advisors manage client assets on a discretionary basis using global futures markets as an investment medium. Trading advisors take positions based on expected profit potential.

- is a type of alternative investment in which trading in the futures markets is managed by another person or entity, rather than the fund's owner.

- Managed futures are futures positions entered into by professional money managers, known

as commodity trading advisors, on behalf of investors. Managers invest in energy, agriculture

and currency markets (among others) using futures contracts and determine their positions

based on expected profit potential.

A futures contract is a financial contract obligating the buyer to purchase an asset (or the seller to sell

an asset), such as a physical commodity or a financial instrument, at a predetermined future date and

price. Futures contracts detail the quality and quantity of the underlying asset and are standardized to

facilitate trading on a futures exchange.

Managed futures as Alternative Investment

1. Broad diversification opportunities2. Potential to lower overall portfolio risk3. Opportunity to enhance overall portfolio returns4. Opportunity to profit in a variety of economic environments5. Limited losses due to a combination of flexibility and discipline

Commodity

Commodity is a marketable item produced to satisfy wants or needs. Economic commodities comprise goods and services. The exact definition of the term commodity is specifically used to describe a class of goods for which there is demand, but which is supplied without qualitative differentiation across a market.

How do we earn profit in Commodities: Hedge Against Inflation Performance/Return Enhanced Diversification

REAL ESTATE

Real estate is any land plus anything permanently fixed to it, including buildings, sheds and other items attached to the structure. Although, media often refers to the "real estate market"

from the perspective of residential living, real estate can be grouped into three broad categories based on its use: residential, commercial and industrial. Examples of real estate include undeveloped land, houses, condominiums, townhomes, office buildings, retail store buildings and factories.

It is a tangible asset. It is an immovable asset. Each real estate asset is a unique investment because of the property

and buildings that can be built on it. Real estate can be very illiquid if the land and buildings are purchased outright. On the other

hand, investors can enjoy higher liquidity if the same asset (either land or buildings) is purchased through a fund or some other vehicle.

It can be divided among a pool of investors, and can be categorized by the way the property is used by the owners or tenants.

Can be owned in various forms such as public, private or financed through equity of debt.

Characteristics of a Real Estate1. Produces relatively consistent total returns that are hybrid of income and capital growth - real

estate has a coupon-paying bond-like component in that it pays a regular, steady income stream, and it has a stock-like component in that its value has a propensity to fluctuate. And, like all securities that you have a long position in, you would prefer the value to go up more often than it goes down!

2. Capital appreciation of a property is determined by having the property appraised - If the appraiser thinks your property would sell for more than you bought it for, then you've achieved a positive capital return. Because the appraiser uses past transactions in judging values, capital returns are directly linked to the performance of the investment sales market. The investment sales market is affected largely by the supply and demand of investment product.

3. No fixed maturity - Unlike a bond which has a fixed maturity date, an equity real estate investment does not normally mature. In Europe, it is not uncommon for investors to hold property for over 100 years. This attribute of real estate allows an owner to buy a property, execute a business plan, then dispose of the property whenever appropriate. An exception to this characteristic is an investment in fixed-term debt; by definition a mortgage would have a fixed maturity.

4. Tangible - Real estate is, well, real! You can visit your investment, speak with your tenants, and show it off to your family and friends. You can see it and touch it. A result of this attribute is that you have a certain degree of physical control over the investment - if something is wrong with it, you can try fixing it. You can't do that with a stock or bond.

5. Requires Management - Because real estate is tangible, it needs to be managed in a hands-on manner. Tenant complaints must be addressed. Landscaping must be handled. And, when the building starts to age, it needs to be renovated.

6. Inefficient Markets - An inefficient market is not necessarily a bad thing. It just means that information asymmetry exists among participants in the market, allowing greater profits to be made by those with special information, expertise or resources. In contrast, public stock markets are much more efficient - information is efficiently disseminated among market participants, and those with material non-public information are not permitted to trade upon the information. In the real estate markets, information is king, and can allow an investor to see profit opportunities that might otherwise not have presented themselves.

7. High Transaction Costs - Private market real estate has high purchase costs and sale costs. On purchases, there are real-estate-agent-related commissions, lawyers' fees, engineers' fees and many other costs that can raise the effective purchase price well beyond the price the seller will actually receive. On sales, a substantial brokerage fee is usually required for the property to be properly exposed to the market. Because of the high costs of "trading" real estate, longer holding periods are common and speculative trading is rarer than for stocks.

8. Lower Liquidity - With the exception of real estate securities, no public exchange exists for the trading of real estate. This makes real estate more difficult to sell because deals must be privately brokered. There can be a substantial lag between the time you decide to sell a property and when it actually is sold - usually a couple months at least.

9. Underlying Tenant Quality - When assessing an income-producing property, an important consideration is the quality of the underlying tenancy. This is important because when you purchase the property, you're buying two things: the physical real estate, and the income stream from the tenants. If the tenants are likely to default on their monthly obligation, the risk of the investment is greater.

10. Variability among Regions - While it sounds cliché, location is one of the important aspects of real estate investments; a piece of real estate can perform very differently among countries, regions, cities and even within the same city. These regional differences need to be considered when making an investment, because your selection of which market to invest in has as large an impact on your eventual returns as your choice of property within the market.

How to gain from Real Estate1. Appreciation - The most common source for real estate profit is the appreciation - the increase in the value - of the property in question. This is achieved in different ways for different types of real estate. And, most importantly, it is only realized through selling or refinancing.

Raw Land - The most obvious source of appreciation for undeveloped land is, of course, developing it. As cities expand, land outside the limits becomes more and more valuable because of the potential for it to be purchased by developers. Then developers build houses that raise that value even further. Appreciation in land can also come from discoveries of

valuable minerals or materials, provided that the buyer holds the rights. An extreme example of this would be striking oil, but appreciation can also come from gravel deposits, trees and so on.

Residential Property - When looking at residential properties, location is often the biggest factor in appreciation. As the neighborhood around a home evolves, adding transit routes, schools, shopping centers, playgrounds and so on, the value climbs. Of course, this trend can also work in reverse, with home values falling as a neighborhood decays. Home improvements can also spur appreciation, and this is something a property owner can directly control. Putting in a new bathroom, upgrading to a heated garage and remodeling to an open concept kitchen are just some of the ways a property owner may try to increase the value of a home. Many of these techniques have been refined to high-return fixes by property flippers who specialize in adding value to a home in a short time.

Commercial Property - Commercial property gains value for the exact same reasons as the previous two types: location, development and improvements. The best commercial properties are in demand, and that drives the price up on them.

2. Income - Generally referred to as rent, income - or regular payments - from real estate can come in many forms.

Raw Land Income - Depending on your rights to the land, companies may pay you royalties for any discoveries or regular payments for any structures they add. These include pump jacks, pipelines, gravel pits, access roads, cell towers and so on. Raw land can also be rented for production, usually agricultural production.

Residential Property Income - Although it is possible that you may earn income from the installation of a cell tower or other structure, the vast majority of residential property income comes in the form of basic rent. Your tenants pay a fixed amount per month - and this will go up with inflation and demand - and you take out your costs from it and claim the remaining portion as rental income. While it is true that you will get an insurance payout if your tenants burn down the place, the payout only covers the cost of replacing what is lost and is not income in a real sense.

Commercial Property Income - Commercial properties can produce income from the aforementioned sources - with basic rent again being the most common - but can also add one more in the form of option income. Many commercial tenants will pay fees for contractual options like the right of first refusal on the office next door. These are essentially options that tenants pay a premium to hold, whether they exercise them or not. Options income is sometimes used for raw land and even residential property, but they are far from common.

3. REITs or MICs - Real estate investment trusts (REIT) and Mortgage Investment Corporations (MIC) are generally considered to be great ways of getting income from real estate. This is true, but only in the sense that real estate is the underlying security. With a REIT, the owner of multiple commercial properties sells shares to investors - usually to fund the purchase of more properties - and then passes on the rental income in the form of distribution. The REIT is the landlord for the tenants (who pay rent), but the owners of the REIT get the income once the expenses of running the buildings and the REIT are

taken out. MICs are even a further step removed, as they invest in private mortgages rather than the underlying properties. MICs are different from MBSs in that they hold entire mortgages and pass on the interest from payments to investors, rather than securitizing the interest streams independent of the original mortgage. Still, they are not so much real estate investments as they are debt investments, and thus outside of our area of interest.

4. Smoke and Mirrors - Similar to securities with real estate underlying the investment, most of the alternative "blow your mind with super fantastic return" methods are merely a layer on top of these two basic steams of income.For example, there are informal residential real estate options where you pay a fee to have the right to buy a house at a given time, say after a month, for an agreed upon price. Then, you find investors who will pay more than your option price for the property. In this case, the premium you get is essentially a finder's fee for matching a person looking for an investment with a person looking to sell - no different than a real estate agent. Although this is income, it doesn't come from buying (i.e. holding the deed to) a piece of real estate. Similarly, no money down or OPM deals are simply the financing aspect of the deal - it doesn't change how the buyer is planning to make money in the long run.

UITF

What are the risks of investing in a UITF?

A client investing in a UITF product should be prepared to absorb the following potential risks: (a) interest rate risk – the potential for an investor to experience losses due to changes in interest rates; (b) market/price risk – the potential for an investor to experience losses due to changes in the market prices of securities (e.g. bonds and equities); (c) liquidity risk – the inability to sell or convert assets into cash quickly or where conversion to cash is possible but at a loss; and (d) credit risk – the risk of loss due to a borrower or issuer’s failure to repay principal and/or interest on securities issued.

Because the assets of the UITF are valued based on the prevailing market prices, yields and potential yields cannot be guaranteed. There is a possibility of incurring losses in the UITF if the client withdraws in a scenario of generally declining market prices, even if the fund is invested in government securities. It should be noted that investments in government securities, although considered credit risk free in the domestic market are also subject to interest rate risk, market risk and under extreme volatile conditions, to liquidity risk. Should this situation arise, clients may, however, opt to defer their withdrawals until market conditions become more favorable.

Being a trust product, there is no guaranty on the principal and income of the investments and losses, if any, shall be for the risk of the UITF investors. UITFs are governed by BSP regulations but are not deposit products, hence are not covered by the Philippine Deposit Insurance Corporation (PDIC). Historical performance of a fund may be used for reference purposes only and do not guarantee similar future results.

UNIT INVESTMENT TRUST FUND

Unit Investment Trust Fund (UITF) is an open-pooled trust fund denominated in pesos or any acceptable currency, which is operated and administered by a trust entity and made available by participation. It is a collective investment idea offered by banks wherein money from various investors are pooled together into one fund to achieve a specific investment objective. UITFs are very good investment vehicles for people who have no time or expertise to do actual stock or bond trading since professional investment managers are the ones managing the fund.In UITF, you buy units of participation in the Trust Fund therefore prices are expressed and reported in NAVPU (Net Asset Value per Unit).

Net Asset Value represents a fund's per share/unit market value. This is the price at which investors buy ("bid price") fund shares from a fund company and sell them ("redemption price") to a fund company. It is derived by dividing the total value of all the cash and securities in a fund's portfolio, less any liabilities, by the number of shares outstanding.

Parties involved:

Unit Holder- the investor who’s holding a certain number of unitsFund Manager- responsible for the day-to-day running of the trust and for investing the fundsThe Trustee- who is governed by the Trust Companies Act 1967, their role is to monitor the manager's performance against the trust's deed

Types of UITF’s

UITFs are established and managed based on a set of investment objectives and strategies, and these have varying levels of risks and returns. UITFs may be denominated in Philippine Pesos, US Dollars and acceptable third currencies. Following are the four general major types of UITFs listed according to ascending levels of risk, return and investment time horizon:

a. Money Market Funds - These funds are invested principally in short term, fixed income deposits and securities with a portfolio duration of one year or less.

b. Bond Funds - The mandate of these funds is to invest in a portfolio of bonds and other similar fixed income securities with portfolio duration which may exceed one year. These may further be classified into Intermediate Funds (where the fund mandate limits the duration up to 3 years), Medium Term Funds (where the fund mandate allows a duration of up to 5 years) and Long Term Funds (where the fund mandate allows a duration of greater than 5 years).

c. Balanced Funds - The mandate of these funds is to invest in a diversified portfolio of bonds and stocks where investments in stocks shall be up to a maximum of 40% to 60% of the fund, with the balance invested in fixed income securities.

d. Equity Funds - The mandate of these funds is to invest substantially in equities. Cash may be kept for liquidity and portfolio re-balancing purposes.

What are the benefits of investing in a UITF?

Investors in UITFs can avail of the following benefits:

•Diversification. By participating in a UITF, risks are spread out across the various investments held by the pooled trust fund. Diversification comes in the form of various types of investments, issuers and tenors. UITFs are required to observe its exposure in a single entity and its related parties to 15% of the market value of the fund, except in the case of government securities.

•Liquidity. While it is advisable to stay invested in the UITF for a longer period of time, clients can redeem units of participation at any time. The fund will not have difficulty redeeming such units of participation because UITF investments are limited to marketable or tradable securities.

•Affordability. UITFs generally have low minimum investment requirements. Additional investments may be made in tranches as funds become available to the client.

•Better earnings potential. Greater earnings potential is achieved without having to invest large sums of money. There are opportunities for potentially higher returns due to possible marked-to-market gains on top of accrued income from investments. UITFs provide access to financial instruments not readily available to retail investors.

•Exempt from reserve requirements. UITFs are not subject to reserve requirements imposed on bank deposits and CTFs.

•Professional fund management. Participating in a UITF allows clients to gain access to the expertise and services of seasoned fund managers who are able to actively monitor the markets for possible investment opportunities.

•Transparency. Trust entities are required to publish the UITF NAVPUs at least weekly, allowing investors to compare investment performance of various fund managers. Each UITF is subject to a separate annual audit by an independent auditor acceptable to the BSP, the results of which may be made available to investors. In addition, each UITF is required to have a BSP accredited third party custodian, who is tasked with safekeeping the securities of the UITF and performing independent marking-to-market of such securities.

•Regulated product. The management and administration of UITFs are governed by the BSP.

How much will an investor get when the UITF investment is redeemed?

The investor can calculate the proceeds of his UITF investment by simply multiplying the number of units being redeemed by the applicable NAVPU for the day. Generally, the NAVPU is already net of the trust fees, taxes and qualified charges. However, there may be additional charges to the client such as

early withdrawal charges in cases where the client redeems his UITF investment prior to the completion of the minimum holding period required by the trustee.

How does a participant determine how much he earned from the UITF?

The difference between the value of the units of participation at the time of purchase and the value at the time the units are redeemed determines how much an investor earned (or the loss incurred) from the UITF investment. As the fund value increases, each participant earns more. Ideally, the longer a client stays invested in the fund, the better his chances of earning more since the underlying investment outlets become less prone to market volatility over time.

How does an investor determine the return on the UITF investment?

The client’s return on investment can be determined using the following formula:

Return on Investment = [ (Proceeds of investment – Initial investment) / (Initial investment) ] *100

Where: Proceeds of investment = Applicable NAVPU x number of units of participation (less early withdrawal charges, if any)

Initial investment = Amount invested.

Derivatives

A derivative is a contract that derives its value from the performance of an underlying entity. This underlying entity can be an asset, index, or interest rate, and is often called the "underlying". Derivatives can be used for a number of purposes including insuring against price movements (hedging), increasing exposure to price movements for speculation or getting access to otherwise hard to trade assets or markets. Some of the more common derivatives include forwards, futures, options, and swaps.

Trading Markets

In broad terms, there are two groups of derivative contracts, which are distinguished by the way they are traded in the market:

Over-the-counter (OTC) derivatives are contracts that are traded (and privately negotiated) directly between two parties, without going through an exchange or other intermediary. The OTC derivative market is the largest market for derivatives, and is largely unregulated with respect to disclosure of information between the parties, since the OTC market is made up of banks and other highly sophisticated parties, such as hedge funds. Reporting of OTC amounts is difficult because trades can occur in private, without activity being visible on any exchange. Because OTC derivatives are not traded on an exchange, there is no central counter-party. Therefore, they are subject to counterparty risk, like an ordinary contract, since each counter-party relies on the other to perform.

Exchange Traded Derivatives (ETD) are those derivatives instruments that are traded via specialized derivatives exchanges or other exchanges. A derivatives exchange is a market where individuals trade standardized contracts that have been defined by the exchange. A derivatives exchange acts as an intermediary to all related transactions, and takes initial margin from both sides of the trade to act as a guarantee.

Forward Contract

• A contract between two parties to buy or sell an asset at a specified price on a future date.• It can be used for hedging or speculation• It can be customized to any commodity, amount and delivery date• Forward contracts do not trade on a centralized exchange and are therefore regarded as over-

the-counter (OTC) instruments.

There are two parties in forward contracts: Short - the party that has the obligation to sell the underlying asset Long - the party who has an obligation to buy the underlying asset

Counterparty Risk• A risk to each party of a contract that the counterparty will not live up to its contractual

obligations. • A risk to both parties and should be considered when evaluating a contract.

Futures• A financial contract obligating the buyer to purchase an asset (or the seller to sell an asset), such

as a physical commodity or a financial instrument, at a predetermined future date and price. • Also called as “standardized forward contracts”• Futures contracts detail the quality and quantity of the underlying asset• They are standardized to facilitate trading on a futures exchange. • Some futures contracts may call for physical delivery of the asset, while others are settled in

cash.

Futures Exchange Usually owned by its members, determines what contracts will be traded, what the terms of the

contracts will be, the trading hours, and how and when futures can be traded. The exchange also is the main regulator of the futures business conducted at the exchange. It houses the trading floor for floor trading, and the computers used for electronic trading.

Clearinghouse

A department of the exchange whose main function is the settling of and marking to market of the exchange members' accounts, guarantees the other side of all futures trades, and oversees contract performance.

Future Commission Merchant• The intermediary between the exchanges and the public investor, acting as a broker for the

buying and selling of futures, and as the custodian of the customers funds.

Margin• It is a margin to minimize credit risk to the exchange; traders must post a margin or a

performance bond, typically 5%-15% of the contract’s value. To minimize counterparty risk to traders, trades executed on regulated exchanges are guaranteed by a clearing house.

ClearingMargin• Clearing margin are financial safeguards to ensure that companies or corporations perform on

their customers ‘open futures and options contracts. • Clearing margins are distinct from customer margins that individual buyers and sellers of futures

contracts are required to deposit with brokers.

Costumer Margin• Customer margin within the futures industry, financial guarantees required of both buyers and

sellers of futures contracts to ensure fulfillment of contract obligations. • Futures Commission Merchants are responsible for overseeing customer margin accounts.

Margins are determined on the basis of market risk and contract value.•

Initial Margin• Initial margin is the equity required to initiate a futures position. The maximum exposure is not

limited to the amount of the initial margin; however the initial margin requirement is calculated based on the maximum estimated change in contract value within a trading day.

• Initial margin is set by the exchange.

Settlement – physical vs. cash-settled futuresPhysical delivery

• The amount specified of the underlying asset of the contract is delivered by the seller of the contract to the exchange, and by the exchange to the buyers of the contract.

• Physical delivery is common with commodities and bonds. Cash settled futures

• The parties settle by paying/receiving the loss/gain related to the contract in cash when the contract expires.

• Cash settled futures are those that, as a practical matter, could not be settled by delivery of the referenced item

Options

An option is a contract which gives the buyer (the owner) the right, but not the obligation, to buy or sell an underlying asset or instrument at a specified strike price on or before a specified date. The seller has the corresponding obligation to fulfill the transaction – that is to sell or buy – if the buyer (owner) "exercises" the option. The buyer pays a premium to the seller for this right. An option that conveys to the owner the right to buy something at a specific price is referred to as a call; an option that conveys the right of the owner to sell something at a specific price is referred to as a put.

Owners of put and call options have no voting rights, no privileges of ownership, and no interest or dividend income. They are created by individual investors, not by the organizations that issue the underlying financial asset.

According to the option right:

Call options give you the right but not the obligation, to buy something at a specific price for a specific time period.

Put options give you the right but not the obligation, to sell something at a specific price for a specific time period.

According to the underlying assets

Equity option Bond option Future option Index option Commodity option Currency Option

According to the trading markets

Exchange-traded options (also called "listed options") are a class of exchange-traded derivatives. Exchange traded options have standardized contracts, and are settled through a clearing house with fulfillment guaranteed by the Options Clearing Corporation (OCC). Since the

contracts are standardized, accurate pricing models are often available. Exchange-traded options include:

-stock options

-bond options and other interest rate options

-stock market index options or, simply, index options and

-options on futures contracts

callable bull/bear contract

Over-the-counter options (OTC options, also called "dealer options") are traded between two private parties, and are not listed on an exchange. The terms of an OTC option are unrestricted and may be individually tailored to meet any business need. In general, at least one of the counterparties to an OTC option is a well-capitalized institution. Option types commonly traded over the counter include:

-interest rate options

-currency cross rate options, and

-options on swaps or swaptions

Swaps

A swap is a derivative in which two counter-parties exchange cash flows of one party's financial instrument for those of the other party's financial instrument. The benefits in question depend on the type of financial instruments involved.

Swaps can be used to hedge certain risks such as interest rate risk, or to speculate on changes in the expected direction of underlying prices.

Types of swaps

Interest rate swaps Currency swaps Commodity swaps Credit default swaps Subordinated risk swaps Other variations

Interest rate swaps

The most common type of swap is a "plain Vanilla" interest rate swap. It is the exchange of a fixed rate loan to a floating rate loan. The life of the swap can range from 2 years to over 15 years.

The reason for this exchange is to take benefit from comparative advantage. Some companies may have comparative advantage in fixed rate markets, while other companies have a comparative advantage in floating rate markets. When companies want to borrow, they look for cheap borrowing, i.e. from the market where they have comparative advantage. However, this may lead to a company borrowing fixed when it wants floating or borrowing floating when it wants fixed. This is where a swap comes in. A swap has the effect of transforming a fixed rate loan into a floating rate loan or vice versa.

Currency Swaps

A currency swap involves exchanging principal and fixed rate interest payments on a loan in one currency for principal and fixed rate interest payments on an equal loan in another currency. Just like interest rate swaps, the currency swaps are also motivated by comparative advantage. Currency swaps entail swapping both principal and interest between the parties, with the cashflows in one direction being in a different currency than those in the opposite direction. It is also a very crucial uniform pattern in individuals and customers.

Commodity swaps

A commodity swap is an agreement whereby a floating (or market or spot) price is exchanged for a fixed price over a specified period. The vast majority of commodity swaps involve crude oil.

Credit default swaps

A credit default swap (CDS) is a contract in which the buyer of the CDS makes a series of payments to the seller and, in exchange, receives a payoff if an instrument, typically a bond or loan, goes into default (fails to pay). Less commonly, the credit event that triggers the payoff can be a company undergoing restructuring, bankruptcy or even just having its credit rating downgraded. CDS contracts have been compared with insurance, because the buyer pays a premium and, in return, receives a sum of money if one of the events specified in the contract occur. Unlike an actual insurance contract the buyer is allowed to profit from the contract and may also cover an asset to which the buyer has no direct exposure.

Subordinated risk swaps

A subordinated risk swap (SRS), or equity risk swap, is a contract in which the buyer (or equity holder) pays a premium to the seller (or silent holder) for the option to transfer certain risks. These can include any form of equity, management or legal risk of the underlying (for example a company). Through execution the equity holder can (for example) transfer shares, management responsibilities or else. Thus, general and special entrepreneurial risks can be managed, assigned or prematurely hedged. Those instruments are traded over-the-counter (OTC) and there are only a few specialized investors worldwide.

Valuation

The value of a swap is the net present value (NPV) of all estimated future cash flows. A swap is worth zero when it is first initiated, however after this time its value may become positive or negative. There are two ways to value swaps: in terms of bond prices, or as a portfolio of forward contracts.

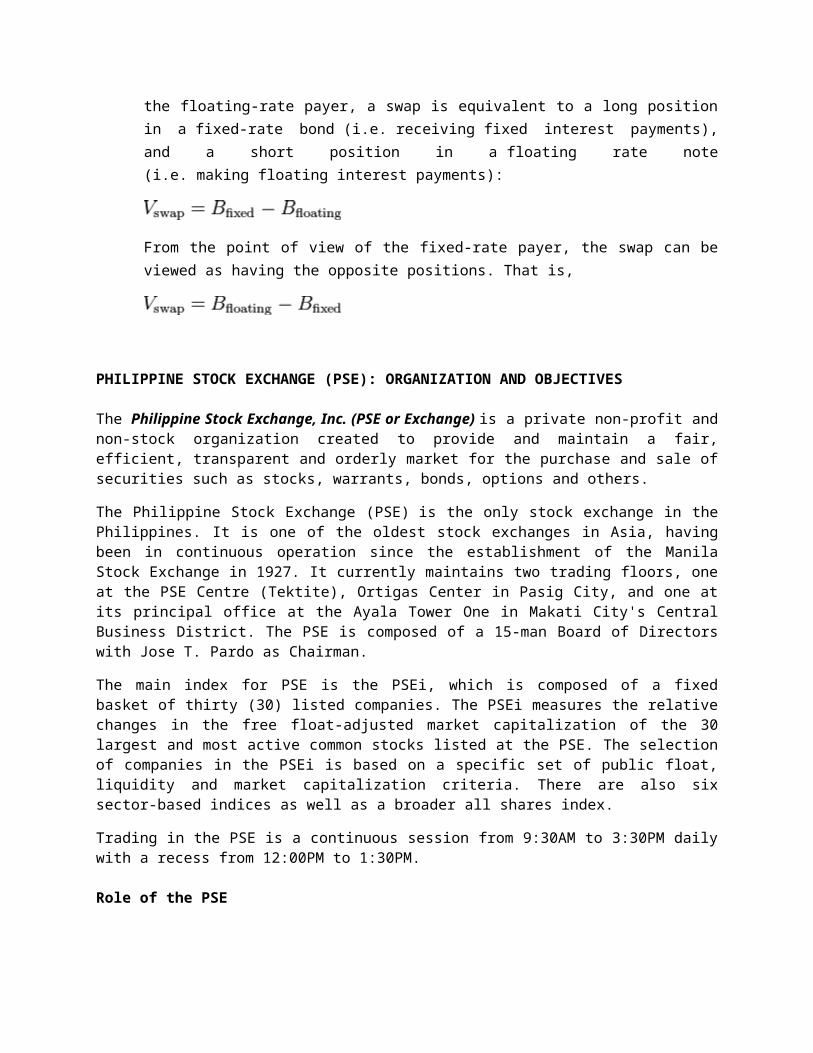

Using bond prices

While principal payments are not exchanged in an interest rate swap, assuming that these are received and paid at the end of the swap does not change its value. Thus, from the point of view of the floating-rate payer, a swap is equivalent to a long position in a fixed-rate bond (i.e. receiving fixed interest payments), and a short position in a floating rate note (i.e. making floating interest payments):

From the point of view of the fixed-rate payer, the swap can be viewed as having the opposite positions. That is,

PHILIPPINE STOCK EXCHANGE (PSE): ORGANIZATION AND OBJECTIVES

The Philippine Stock Exchange, Inc. (PSE or Exchange) is a private non-profit and non-stock organization created to provide and maintain a fair, efficient, transparent and orderly market for the purchase and sale of securities such as stocks, warrants, bonds, options and others.

The Philippine Stock Exchange (PSE) is the only stock exchange in the Philippines. It is one of the oldest stock exchanges in Asia, having been in continuous operation since the establishment of the Manila Stock Exchange in 1927. It currently maintains two trading floors, one at the PSE Centre (Tektite), Ortigas Center in Pasig City, and one at its principal office at the Ayala Tower One in Makati City's Central Business District. The PSE is composed of a 15-man Board of Directors with Jose T. Pardo as Chairman.

The main index for PSE is the PSEi, which is composed of a fixed basket of thirty (30) listed companies. The PSEi measures the relative changes in the free float-adjusted market capitalization of the 30 largest and most active common stocks listed at the PSE. The selection of companies in the PSEi is based on a specific set of public float, liquidity and market capitalization criteria. There are also six sector-based indices as well as a broader all shares index.

Trading in the PSE is a continuous session from 9:30AM to 3:30PM daily with a recess from 12:00PM to 1:30PM.

Role of the PSE

The PSE bring together companies which aim to raise capital through the issue of new securities.Through the listing of their share in the stock exchange, companies can have easier access to funds. Raising new capital through an additional public offering is easier and less expensive when the company is already listed in the Exchange. Therefore, the PSE plays a vital role in the financing of productive enterprises that use the funds for growth and expansion of new jobs. It is therefore essential to the growth of the Philippine economy.

Furthermore, the PSE facilitates the selling and buying of the issued stocks and warrants. It provides a suitable market for the trading of securities to individuals and organizations seeking to invest their saving or excess funds through the purchase of securities.

Apart from these functions, the PSE has committed itself to (a) protecting the interest of the investing public; and (b) developing and maintaining an efficient, fair, orderly and transparent market.

Efficient.This means that orders are executed and transactions are settled in the fastest possible way. Some reforms have been instituted or are being carried out by the PSE to make the market more efficient, such as:

· installation of fully automated trading system;· installation of computer trading terminals in cities outside Metro Manila to

encourage the entry of provincial investors; and creation of a central cleaning and depository system to mobilized stock certificates and allow transfer of shares and funds by book entry.

Fair. This means that the PSE assures that no investor will have an undue advantage over another, market player in trading by manipulating prices and engaging into insider trading. Insider trading is the act of buying or selling a particular stock based on certain privileged information which is not available to the public. As such it is considered as illegal and prohibited by the PSE.

Market Transparency.Transparency proceeds from the assumption that the investor can only make informed and intelligent information about the particular sock he wants to buy. The PSE requires listed companies to disclose timely, complete and accurate material information to the Exchange and the public on a regular basis. Such information would include stock price information, corporate conditions and developments which tend to affect stock prices like dividend, mergers and joint ventures, and the like.

PSE ORGANIZATION

The PSE”S organizational structure holds five (5) groups, namely: Listings & Disclosure Group, Compliance & Surveillance Group, Operations/Automated Trading Group, Finance and Investment Group and Business Development & Information Group along with the Office of the General Counsel, Membership Department and Human Resources Management Department, which reports directly to the Office of the President.

The functional responsibilities of each department are as follows:

Listings and Disclosure Group.This group is composed of the following departments: Listing Processing, Legal Advisory and Corporate Disclosure. It processes and evaluates listing applications, conducts legal due diligence, and monitors compliance to continuing listing requirements including disclosure of listed companies. It also coordinates IPO (initial public offering) distribution.

Compliance and Surveillance Group.This group acts as the police of the Exchange. It is composed of the Compliance Audit Department, Special Investigation Department, Market Surveillance Department and Legal Section. The group conducts legal audit and review aside from auditing of member-brokers books and operations. It also monitors the member’s compliance to set rules and regulations and enforces appropriate sanctions to violators or erring member-brokers. It takes responsibility in the operation of the surveillance activity, to ascertain that there are no illegal postings and dealings made in any of the issues listed in the Exchange.

Operations/Automated Trading Group.Placed under this group are the Computer Operations Unit, Systems Development Unit and Systems Integration and technical Support Unit along with the Trading & Settlement Department, Administration Department and PSE Plaza Operations Department to function as one group. It is considered as one of the most critical responsibility areas in the organization since it handles the operation of the automated trading and clearing and settlement activities for stock operations.

The Automated Trading Group examines and controls the monitoring, logging and analysis of computer system resource utilization; the maintenance of network connections of all workstations at the trading floor and remote offices; managing of database of off-floor installed sites; and the implementation and integration of the different components of the trading and office systems.

On the other hand, the Trading and Settlement Department monitors compliance of member-brokers to the clearing and settlement requirements of the settlement banks and central depository. It coordinates with these agencies and the custodian banks, both local and foreign, any trading discrepancies, irregularities or settlement concerns of the member-brokers and investing public.

The Administration Department and the PSE Plaza Operations Department handles the building maintenance, security and administration as well as the procurement management and utilization of supplies and equipment including the daily administrative requirements of the Exchange. It is also responsible for the daily dissemination of all the listed companies’ corporate announcements along with the foreign quotation report.

Finance and Investment Group.The group is responsible for the management of the company’s financial resources. It is composed of the Accounting Department, Treasury Department, Payroll and Budget Section and Investments Monitoring Section which handles the maintenance of book of accounts, preparation of financial statements and budget, management and placement of PSE funds, monitoring of accounts receivables and billing of accounts.

Business Development and Information Group.This group is comprised of the following: Product Development Department, Market Development Department, Research and Public Information Department, Corporate communications Department, PSE Training Institute and PSE Rule Book/Task Force Quality Unit.

The Product Development Department is in charge of the expansion, development and packaging of domestic and foreign financial products, equity-related securities, debt-related securities and other

forms of securities and derivatives. It coordinates with private businesses, government agencies and associations in the overall development and packaging of the securities, derivatives and trading facilities.

The Market Development Department handles the expansion, development and monitoring of the investor base for both domestic and foreign market on an individual and institutional level. It looks at the PSE trading operation’s presence and positioning in the domestic, regional, and international markets including the expansion and development of market intermediation services and facilities covering secondary, over-the-counter (OTC) and third markets.

The research and Public Information Department is composed of the Research Services Sections, Information and Publications Section and the Public Information and Assistance Center (PIAC). It conceptualizes, processes, consolidates and handles multi-media dissemination of statistical and analytical information and studies related to the business requirements of members. It conducts research and provides information support to the expansion and development of the Exchange trading operations and its markets. It also maintains, develops and disseminates information through manual or electronic libraries and documentation. The department produces regular publications – Weekly Report, Monthly Reports, and Fact Book – that provide market users with a review of the market’s performance along with historical and current data on stock trading activities and listed companies. The Department also acts as the liaison of the Exchange through the sharing of data and information with foreign individuals, organizations and institutions.

Under the Research and Public Information Department is PIAC which implement the Exchange’s continual public assistance program by covering information promotion and facilitation along with complaints mediation in the physical center at the principal offices of the PSE. It also manages the operation of the PSE Souvenir Shop.

The Corporate Communications Department manages all forms of media and public relation through press releases, information and educational campaigns. It is in charge of managing and developing business promotional and marketing exposure requirements of the PSE including the production and dissemination of corporate internal bulletin and other forms of information materials.

The PSE Training Institute is responsible for the development of programs/curricula along with providing lectures, trainings and seminars about securities market participants. Aside from in-house seminars, it conducts road shows to investors in the provinces. The Institute also provides logistics support to all training-related activities of the departments in the PSE. In the future, the Institute plans to conduct activities such as the Certified Securities Representative (CSR) seminars and the technical and fundamental analysis seminars in the coordination with other intuitions.

The PSE Rile Book/Task Force Quality is responsible for the codification and the manualization of the PSE’s rules, guidelines, procedures and other legislative materials coming from government agencies, into a consolidated and comprehensive Manual of Rules of the Exchange.

The PSE Rule Book consists of five (5) volumes which are: (1) Corporate Rules, (2) Membership Rules, (3) Listing and Disclosure Rules, (4) Trading and Settlement Rules, and (5) Compliance and Surveillance Rules.

Membership Department.This department manages, implements and coordinates members’ requirements, planned activities and projects with the end in view of assisting PSE management in the expansion, consolidation and development of its membership. It also processes membership applications and various corporate changes of member-brokers for approval by the Membership

Committee. It is in charge of circular preparations concerning membership, and the monitoring of financial statements of brokers and SEC licenses of its stock traders. In coordination with the Membership Committee, it facilitates membership’s arbitration. Further, the Membership Department organizes and prepares social activities for all members.

Human Resources Management Department.This department, under the Office of the President, handles employee career management, administration of employee compensation and benefits, management of corporate culture and organization development, implementation of the company’s performance management system and formulation and enforcement of company policies. To ensure continuing organization and employee development, this department integrates the organizational structure/processes and workforce issues into the business equation and evaluates group processes and dynamics to tailor-fit results with a corporate staff training and management development program.

Office of the General Counsel.The Office of the General Counsel renders corporate legal services and serves as the primary legal advisor to the Board of Governors, the President, and the Chief Operating Officer, the various departments, officers and employees of the Exchange. It also coordinates with the external legal consultants on matters referred by the exchange; represents the Exchange before judicial and administrative/quasi-judicial bodies; and, attend legislative and administrative hearings or meeting as well as draft position papers and/or comments to pending legislation and administrative issuances.

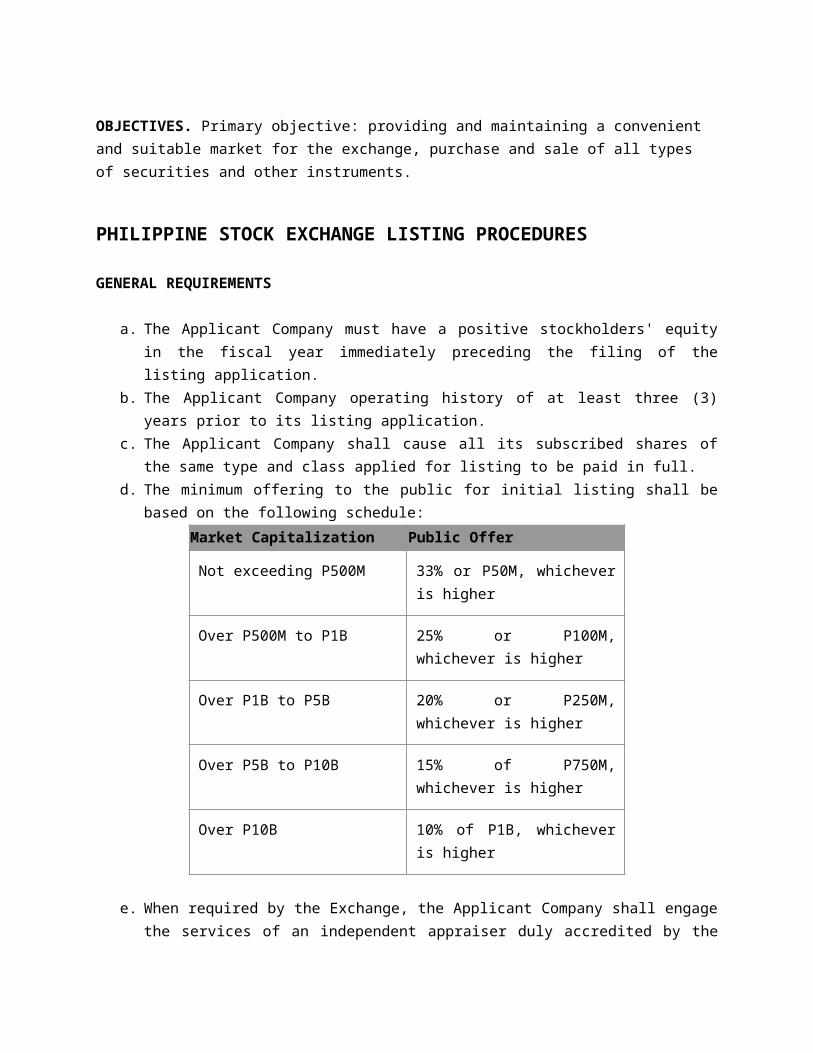

OBJECTIVES. Primary objective: providing and maintaining a convenient and suitable market for the exchange, purchase and sale of all types of securities and other instruments.

PHILIPPINE STOCK EXCHANGE LISTING PROCEDURES

GENERAL REQUIREMENTS

a. The Applicant Company must have a positive stockholders' equity in the fiscal year immediately preceding the filing of the listing application.

b. The Applicant Company operating history of at least three (3) years prior to its listing application.

c. The Applicant Company shall cause all its subscribed shares of the same type and class applied for listing to be paid in full.

d. The minimum offering to the public for initial listing shall be based on the following schedule:

Market Capitalization Public Offer

Not exceeding P500M 33% or P50M, whichever is higher

Over P500M to P1B 25% or P100M, whichever is higher

Market Capitalization Public Offer

Over P1B to P5B 20% or P250M, whichever is higher

Over P5B to P10B 15% of P750M, whichever is higher

Over P10B 10% of P1B, whichever is higher

e. When required by the Exchange, the Applicant Company shall engage the services of an independent appraiser duly accredited by the Exchange and the Securities and Exchange Commission ("SEC") in determining the value of their assets.

f. The Applicant Company shall have an investor relation program to ensure that information affecting the company are communicated effectively to investors. Such program shall include, at the minimum, a corporate website that contains, at the minimum, the following information:

i. Company information - organizational structure, board of directors, and management team

ii. Company news - analyst briefing report, latest news, press releases, newsletter (if any)iii. Financial report - annual and quarterly reports, at least for the past two (2) yearsiv. Disclosures - recent disclosures to PSE and SEC for the past two (2) yearsv. Investor FAQs - commonly asked questions of stockholders

vi. Investor Contact - email address for feedback/ comments, shareholder assistance and service

vii. Stock Information - key figures, dividends, and stock information

MAIN BOARD

TRACK RECORD REQUIREMENTSa. A cumulative consolidated earnings before interest, taxes, depreciation and amortization

(EBITDA), excluding non-recurring items, of at least P50 Million for three (3) full fiscal years immediately preceding the application for listing;

b. A minimum EBITDA of P10 Million for each of the three (3) fiscal years; andc. The applicant company must be engaged in materially the same business(es) and must have a

proven track record of management throughout the last three (3) years prior to the filing of the application.

Exceptions to the 3-year track record requirement:1. The Applicant Company has been operating for at least ten (10) years prior to the filing of the

application and has a cumulative EBITDA of at least P50 Million for at least two (2) of the three (3) fiscal years immediately preceding the filing of the listing application;2. The Applicant Company is a newly formed holding company which uses the operational track record of its subsidiary. However, the newly formed holding company is prohibited from divesting its shareholdings in the said subsidiary for a period of three (3) years from the listing of its securities. The prohibition shall not apply if a divestment plan is approved by majority of the Applicant Company's stockholders.

MINIMUM CAPITAL REQUIREMENTSMinimum authorized capital stock of P500M, of which, at least 25% is subscribed and fully paid.

At listing, the market capitalization of the Applicant Company must be at least P500M.

MINIMUM NUMBER OF STOCKHOLDERSUpon listing, at least 1,000 stockholders each owning stocks is equivalent to at least one (1)

board lot.

RESTRICTIONSa. No divestment of shares in operating subsidiary - A newly formed holding company which

invokes the operational track record of its subsidiary to qualify for the track record requirement of profitable operations, is prohibited from divesting its shareholdings in the said subsidiary for a period of three (3) years from the listing of its securities. The prohibition shall not apply if a divestment plan is approved by majority of the Applicant Company's stockholders.

b. No secondary offering for companies invoking exemption of track record and operating history requirements, such as mining, petroleum and renewable energy companies and newly formed holding companies during the initial public offering.

LOCK-UPAn Applicant Company shall cause it existing stockholders who own an equivalent of at least

10% of the issued and outstanding shares of stock of the company to refrain from selling, assigning or in any manner disposing of their shares for a period of:

1. One hundred eighty (180) days after the listing of said shares if the Applicant Company meets the track record requirements; or

2. Three hundred sixty-five (365) days after listing of said shares if the Applicant Company is exempt from the track record and operating history requirements.

If there is any issuance or transfer of shares (i.e., private placements, asset for shares swap or a similar transaction) or instruments which lead to issuance of shares (i.e., convertible bonds, warrants or a similar instrument) done and fully paid for within One hundred eighty (180) days prior to the start of the offering period, or, prior to listing date in case of companies listing by way of introduction, and the transaction price is lower than that of the offer price in the Initial Public Offering, or listing price for a

listing by way of introduction, all shares availed of shall be subject to a lock-up period of at least Three hundred sixty-five (365) days from full payment of the aforesaid shares.

The lock-up requirement shall be stated in the Articles of Incorporation of the Applicant Company.

SME (SMALL AND MEDIUM-SIZED ENTERPRISES) BOARD

TRACK RECORDS REQUIREMENTS

a. A cumulative earnings before interest, taxes, depreciation and amortization (EBITDA), excluding non-recurring items, of at least P15 Million for three (3) fiscal years immediately preceding the application for listing;

b. A positive EBITDA was generated in at least two (2) of the last three (3) fiscal years, including the fiscal year immediately preceding the filing of the application; and

c. The Applicant Company must be engaged in materially the same business and must have a proven track record of management throughout the last three (3) years prior to the filing of the application for listing.

The Applicant Company shall demonstrate its stable financial condition and prospects for continuing growth by providing a business plan indicating the steps that have been taken and to be undertaken in order to advance its business over a period of five (5) years.

As a general rule, financial projections are not required, but should there be references made in the business plan to future profits or losses, or any other item that would be construed to indicate forecasts, then the Applicant Company is required to include financial projections in the business plan duly reviewed by an independent accounting firm.

MINIMUM CAPITAL REQUIREMENTMinimum authorized capital stock of P100M, of which, at least 25% is subscribed and fully paid.

MINIMUM NUMBER OF SHAREHOLDERSUpon listing, at least 200 stockholders each owning stocks is equivalent to at least one (1) board

lot.

RESTRICTIONSa. No listing of holding, portfolio and passive income companies;b. No change in primary purpose and/or secondary purpose for a period of seven (7) years

following its listing; and

c. No offering of secondary securities for companies exempt from the track record and operating history requirements such as mining, petroleum and renewable energy companies.

LOCK-UPAn Applicant Company shall cause its existing stockholders to refrain from selling, assigning,

encumbering or in any manner disposing of their shares for a period of one (1) year after the listing of such shares.

If there is any issuance or transfer of shares (i.e., private placements, asset for shares swap or a similar transaction) or instruments which lead to issuance of shares (i.e., convertible bonds, warrants or a similar instrument) done and fully paid for within six (6) months prior to the start of the offering period, or, prior to listing date in case of companies listing by way of introduction, and the transaction price is lower than that of the offer price in the initial public offering, or listing price for listing by way of introduction, all shares subscribed or acquired shall be subject to a lock-up period of at least one (1) year from listing of the aforesaid shares.

The lock-up requirement shall be stated in the Articles of Incorporation of the Applicant Company.

Trading Rules and Regulation

Trading Day Scheduleo Trading Day and Non-Trading Day

Every day shall be a trading day except for Saturdays, Sundays, legal Holidays, special holidays, days when BangkoSentralngPilipinas(BSP) is closed and such other days as may otherwise be declared by the SEC or the Exchange, through its President or other duly authorized representative, to be Non-Trading Day

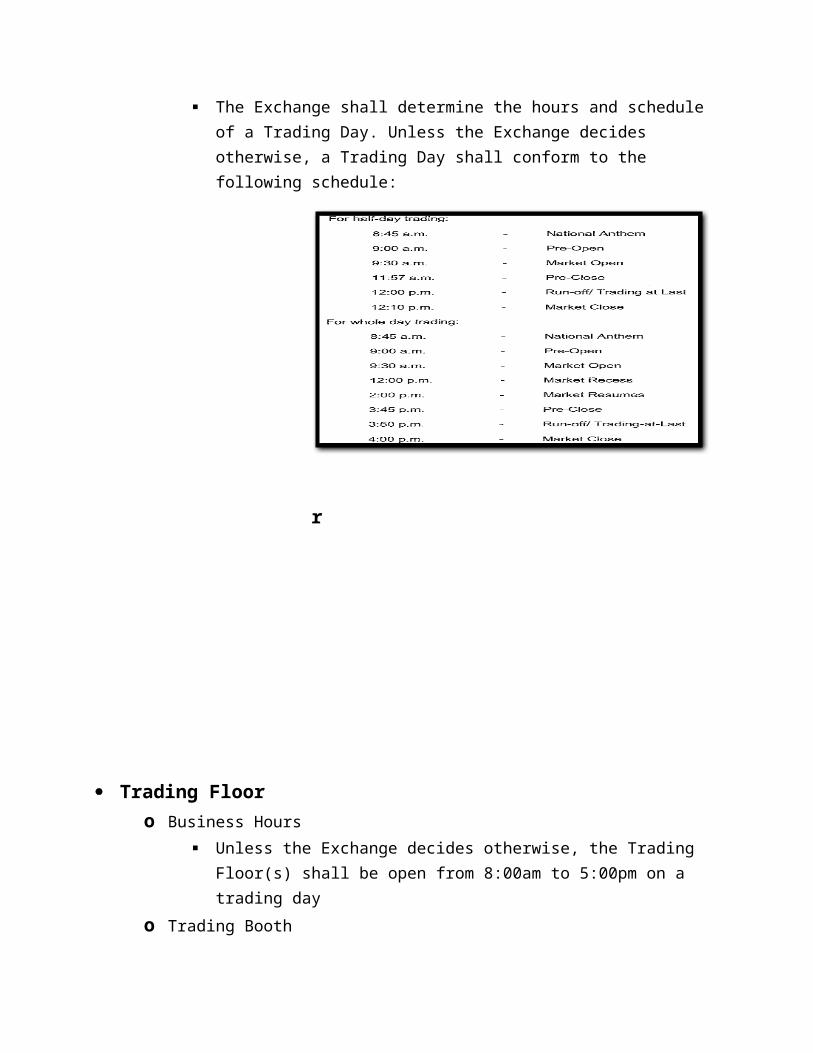

o Trading Hours The Exchange shall determine the hours and schedule of a Trading Day.

Unless the Exchange decides otherwise, a Trading Day shall conform to the following schedule:

r

Trading Flooro Business Hours

Unless the Exchange decides otherwise, the Trading Floor(s) shall be open from 8:00am to 5:00pm on a trading day

o Trading Booth The Exchange shall provide and make available to all the Trading Participants

a trading booth in the Trading Floor(s). The Exchange reserves the right to operate an electronic trading

environment without a Trading Floor.o Terminals and Equipment in the Trading Booth

Every Trading Participant and its Salesmen/Traders and other Trading Floor Personnel shall ensure that: a.) Computer terminals and equipment installed in the trading booths conform with the standards as set by the Exchange and, b.)Only duly authorized personnel of the Trading Participant have access thereto.

o Admission to the Trading Floor

Unless the Exchange authorizes otherwise, only the following persons shall allowed to access to the Trading Floor when open as provided:

a. Salesmen/Tradersb. Dealersc. Trading Floor Assistantd. Nomineese. Trainees for a one-time, non-extendible period of six (6) months and

subject to provisions of SRC Rule 28.1 (4) (a) and the following conditions:

i. A Salesman/Traders shall at all times must supervise the trainees.

ii. The Trainees shall not solicit clients or deal directly to the clients.

iii. The Trading Participant shall not pay the Trainees any form of commission , salary or other compensation, except for reasonable allowance

iv. The Trading Participant shall immediately inform in writing the Exchange of the hiring of the Trainees and shall comply with all orders or regulations of the Exchange in relation to such hiring.

o Conduct in the trading floor The following offenses are deemed to be detrimental to the interest of the

Exchange and are strictly prohibited in the Trading Floor:a. Bringing in food/drinksb. Horse-playingc. Bringing in animalsd. Non-compliance with the dress code as provided in this Rulee. Bringing in liquorf. Being in the influence of liquor/drugsg. Bringing in firecrackers, inflammable materials and other

pyrotechnicsh. Bringing in guns and other deadly weaponsi. Destroying and/ or vandalizing Exchange propertiesj. Disrespect to the flag, and member of the Board of Directors,

Nominees of the Trading Participants or Exchange Officersk. Engaging in disruptive behaviorl. Immoral conduct or indecent acts, including sexual harassment.m. Stealing

n. Gamblingo. Smokingp. Repetitive minor offensesq. Answering calls when the national anthem is being played.

Any personnel violating any of the above-mentioned acts shall be subject to the penalties imposed by the Exchange for such acts.

Any Trading Participant or its suly authorized representative has the duty to exercise due care in operating and using all equipment found at the Trading Participant’s booth inside the Trading Floor. The Exchange may impose a disciplinary sanction, provided it is reasonable and appropriate under the circumstances, if it is proven that the Trading Participant concerned or any of its authorized representatives caused the damage intentionally.

Acts deemed to be detrimental to the interests of the Exchange are not limited by the foregoing enumeration. The Exchange reserves the right to take action for other acts or omissions not stated above the impose penalties on the offender as may be appropriate under circumstances.

o Dress Code/Hairstyle Only accepted business attire such as suits, blazer,barong (long or short

sleeves) plain long-sleeved and short-sleeved shirt with tie, or Exchange uniform shall be allowed in the trading floor.

Wearing of sandals, shorts, sneakers, jeans, denims, shoes without socks for men, athletic jacket, t-shirts, plunging necklines, micro-mini skirts and other improper attire not suitable during business hours are not allowed in the Trading Floor.

Trading Participants’ Nominees are exempted from wearing the Exchange-designated uniform. However, the Nominees will be required to observe the above-mentioned acceptable business attire.

o Identification Accounts/Cards/Passes All trading Participants must use valid PSE Identification

Accounts/Cards/Passes (ID’s). A valid ID is one which has been issued officially by the PSE personnel connected with the Trading Participant.

Issuance of PAM Account IDs

The Exchange will only grant terminal account IDs to Trading Participants and Their Traders with Valid Licenses issued by the SEC and who have been duly certified by PSE to use the PAM.

Issuance of color –coded PSE IDsThe following PSE IDs/passes shall be observed:

a. For Salesman/Traders and Dealers, ID Color is Blueb. For Trading Floor Assistants, ID color is Yellowc. For Trainees, ID color is Greend. For guest, ID/Pass color is Black

IDs for new floor personnelA Trading Participant who hires new Trading Floor personnel must apply to the Exchange for the immediate issuance of a new PSE ID/pass to the employee prior to his assignment to the Trading Floor.

Unauthorized Use of ID Issued by the ExchangeAny person not connected with any Trading Participant but who gains access to the Trading Floor or to the Exchange Trading System by using the PSE ID issued to him under the name of his previous employee shall be banned permanently from the Exchange..

Entry of Guests/trainees to the Trading FloorA nominee may request for PSE ID/pass for purposes of allowing entry to the Trading Floor by submitting a letter-request to the MOD, whenever applicable, at least one (1) day prior to the actual date of entry to the Trading Floor.

Registration of Securities

1. All securities required to be registered under Subsection 8.1 shall be registered through the

filing by the issuer in the main office of the Commission, of a sworn registration statement with

respect to such securities, in such form and containing such information and documents as the

Commission shall prescribe.

2. In promulgating rules governing the content of any registration statement (including any

prospectus made a part thereof or annexed thereto), the Commission may require the

registration statement to contain such information or documents as it may, by rule, prescribe.

It may dispense with any such requirement, or may require additional information or

documents, including written information from an expert, depending on the necessity thereof

or their applicability to the class of securities sought to be registered.

3. The information required for the registration of any kind, and all securities, shall include,

among others, the effect of the securities issue on ownership, on the mix of ownership,

especially foreign and local ownership.

4. The registration statement shall be signed by the issuer’s executive officer, its principal

operating officer, its principal financial officer, its comptroller, principal accounting officer, its

corporate secretary or persons performing similar functions accompanied by a duly verified

resolution of the board of directors of the issuer corporation. The written consent of the

expert named as having certified any part of the registration statement or any document used

in connection therewith shall also be filed. Where the registration statement includes shares

to be sold by selling shareholders, a written certification by such selling shareholders as to the

accuracy of any part of the registration statement contributed to by such selling shareholders

shall also be filed.

4.a)Upon filing of the registration statement, the issuer shall pay to the Commission a fee of not

more than one-tenth (1/10) of one per centum (1%) of the maximum aggregate price at

which such securities are proposed to be offered. The Commission shall prescribe by rule

diminishing fees in inverse proportion to the value of the aggregate price of the offering.

4.b) Notice of the filing of the registration statement shall be immediately published by the issuer,

at its own expense, in two(2) newspapers of general circulation in the Philippines, once a

week for two (2) consecutive weeks, or in such other manner as the Commission by rule

shall prescribe, reciting that a registration statement for the sale of such security has been

filed, and that the aforesaid registration statement, as well as the papers attached thereto

are open to inspection at the Commission during business hours, and copies thereof,

photostatic or otherwise, shall be furnished to interested parties at such reasonable charge

as the Commission may prescribe.

5. Within forty-five (45) days after the date of filing of the registration statement, or by such

later date to which the issuer has consented, the Commission shall declare the registration

statement effective or rejected, unless the applicant is allowed to amend the registration

statement as provided in Section 14 hereof. The Commission shall enter an order declaring

the registration statement to be effective if it finds that the registration statement together

with all the other papers and documents attached thereto, is on its face complete and that

the requirements have been complied with. The Commission may impose such terms and

conditions as may be necessary or appropriate for the protection of the investors.

6.. Upon effectivity of the registration statement, the issuer shall state under oath in every

prospectus that all registration requirements have been met and that all information are true

and correct as represented by the issuer or the one making the statement. Any untrue

statement of fact or omission to state a material fact required to be stated therein or

necessary to make the statement therein not misleading shall constitute fraud.

Requirement in Registration of Securities

1. Securities shall not be sold or offered for sale or distribution within the Philippines, without a

registration statement duly filed with and approved by the Commission. Prior to such sale,

information on the securities, in such form and with such substance as the Commission may

prescribe, shall be made available to each prospective purchaser.

2. The Commission may conditionally approve the registration statement under such terms as it

may deem necessary.

3. The Commission may specify the terms and conditions under which any written

communication, including any summary prospectus, shall be deemed not to constitute an

offer for sale under this Section.

4. A record of the registration of securities shall be kept in a Register of Securities in which shall