Embed Size (px)

Citation preview

Alternative Energy and Agriculture:Perspectives on Cellulosic Feedstock and

Cellulosic Biorefineries

Francis Epplin

Department of Agricultural Economics

Oklahoma State University

Southern Association of Agricultural Sciences - Atlanta, GA

February 1 – 4, 2009

Collaborators

Plant & Soil SciencesCharles Taliaferro (Retired) – grass breeding Yanqi Wu – feedstock development

Biosystems & Agricultural EngineeringRay Huhnke – biomass harvest and storageDani Bellmer - gasificationTim Bowser - gasificationMark Wilkins - bioconversion

Chemical EngineeringA.J. Johannes – process engineeringRandy Lewis (BYU) – bioreactor, bioconversion

MicrobiologyRalph Tanner (OU) – microbial catalyst development

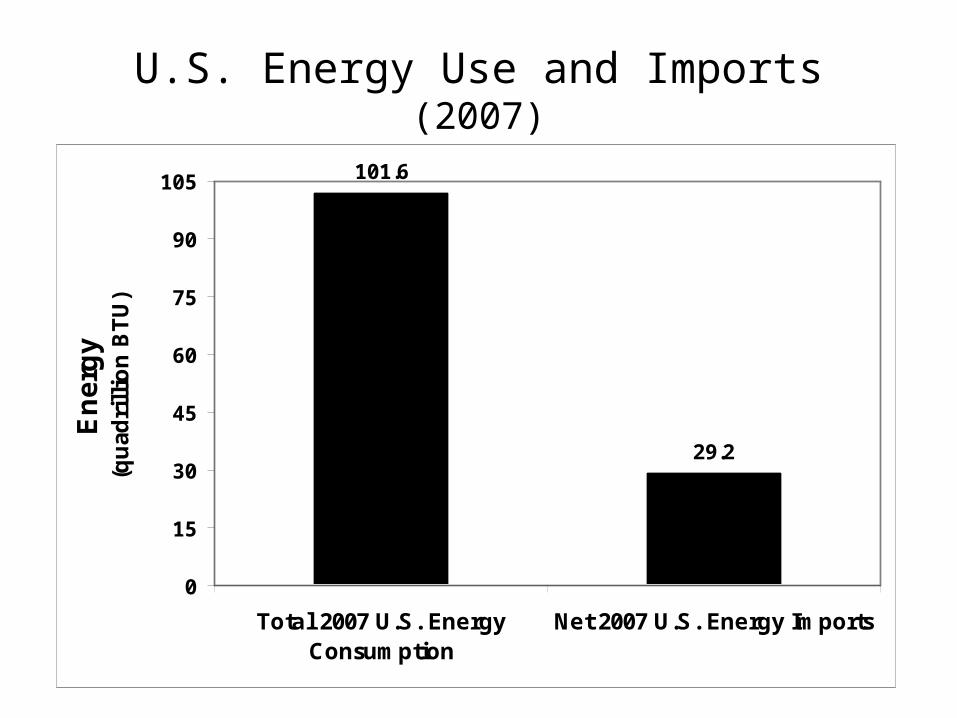

U.S. Energy Use and Imports (2007)

101.6

29.2

0

15

30

45

60

75

90

105

Total 2007 U.S. EnergyConsumption

Net 2007 U.S. Energy Imports

En

erg

y(q

uad

rill

ion

BT

U)

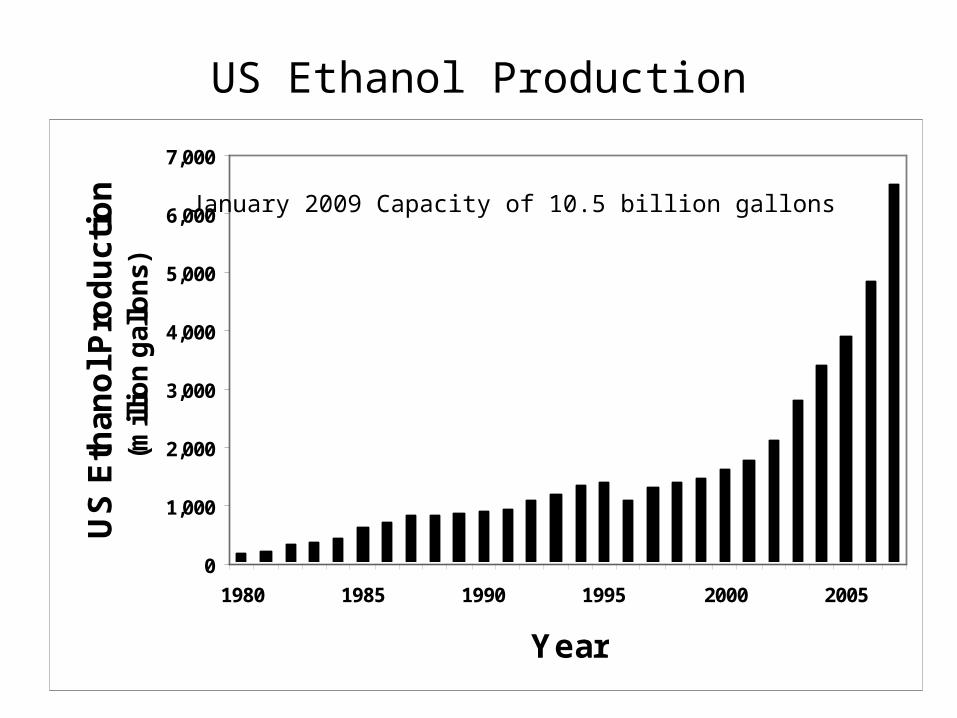

US Ethanol Production

0

1,000

2,000

3,000

4,000

5,000

6,000

7,000

1980 1985 1990 1995 2000 2005

Year

US

Eth

ano

l Pro

du

ctio

n(m

illio

n g

allo

ns)

January 2009 Capacity of 10.5 billion gallons

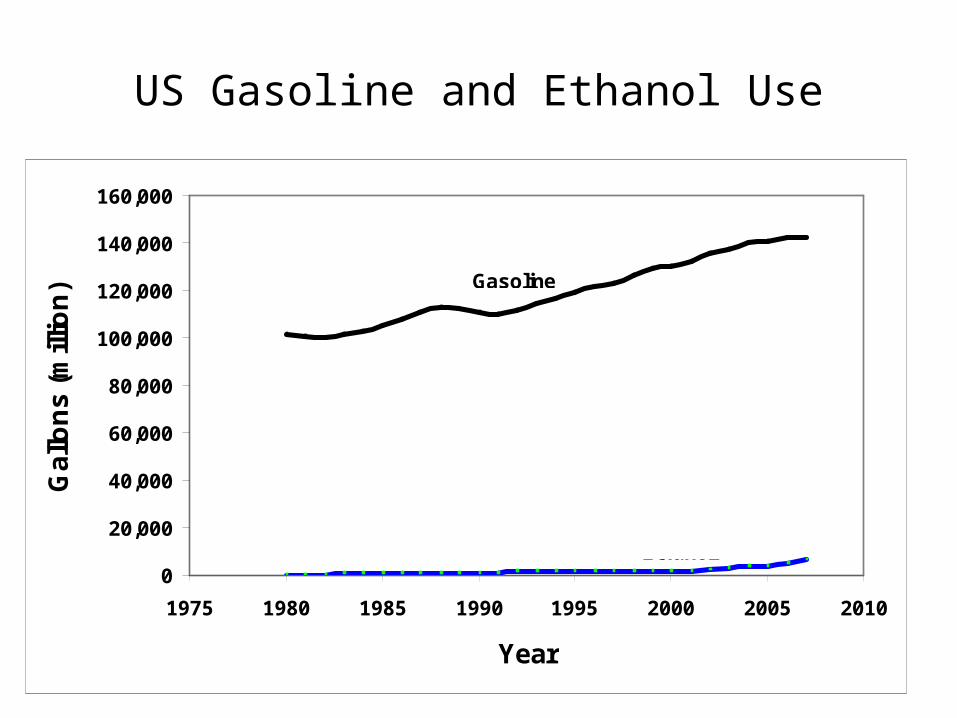

US Gasoline and Ethanol Use

0

20,000

40,000

60,000

80,000

100,000

120,000

140,000

160,000

1975 1980 1985 1990 1995 2000 2005 2010

Year

Ga

llon

s (

mill

ion

) Gasoline

Ethanol

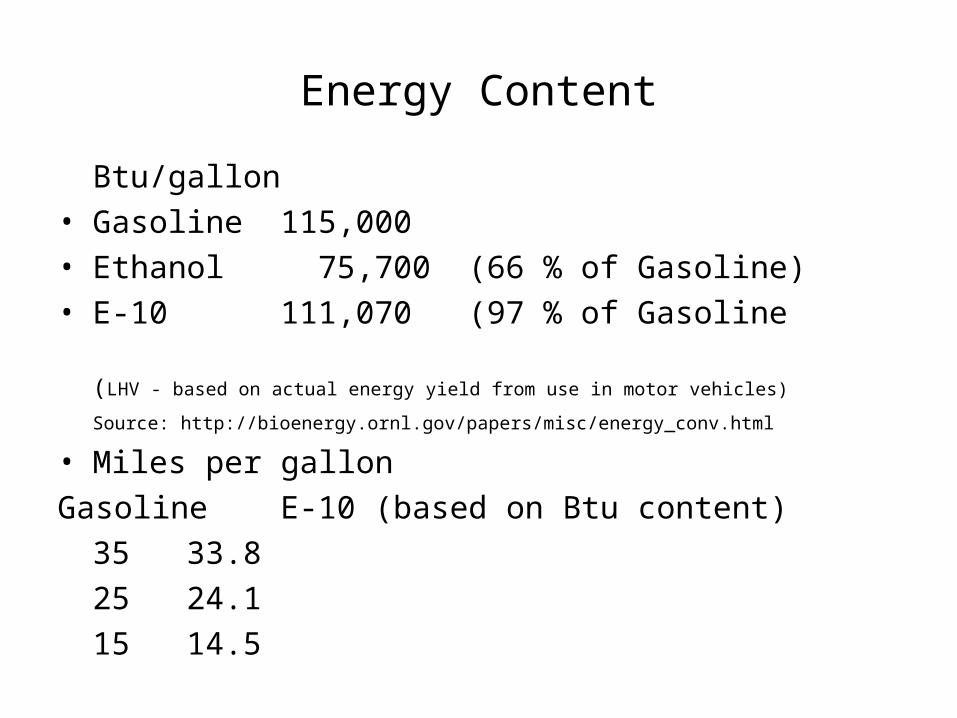

Energy Content

Btu/gallon• Gasoline 115,000 • Ethanol 75,700 (66 % of Gasoline)• E-10 111,070 (97 % of Gasoline

(LHV - based on actual energy yield from use in motor vehicles)

Source: http://bioenergy.ornl.gov/papers/misc/energy_conv.html

• Miles per gallon Gasoline E-10 (based on Btu content)

35 33.825 24.115 14.5

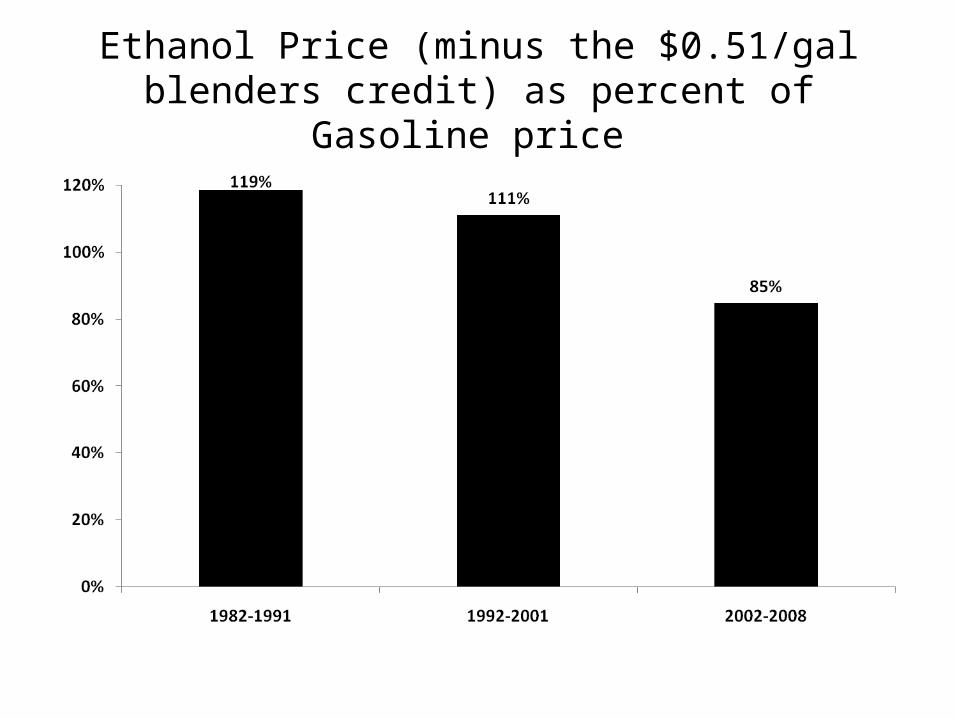

Ethanol Price (minus the $0.51/gal blenders credit) as percent of Gasoline price

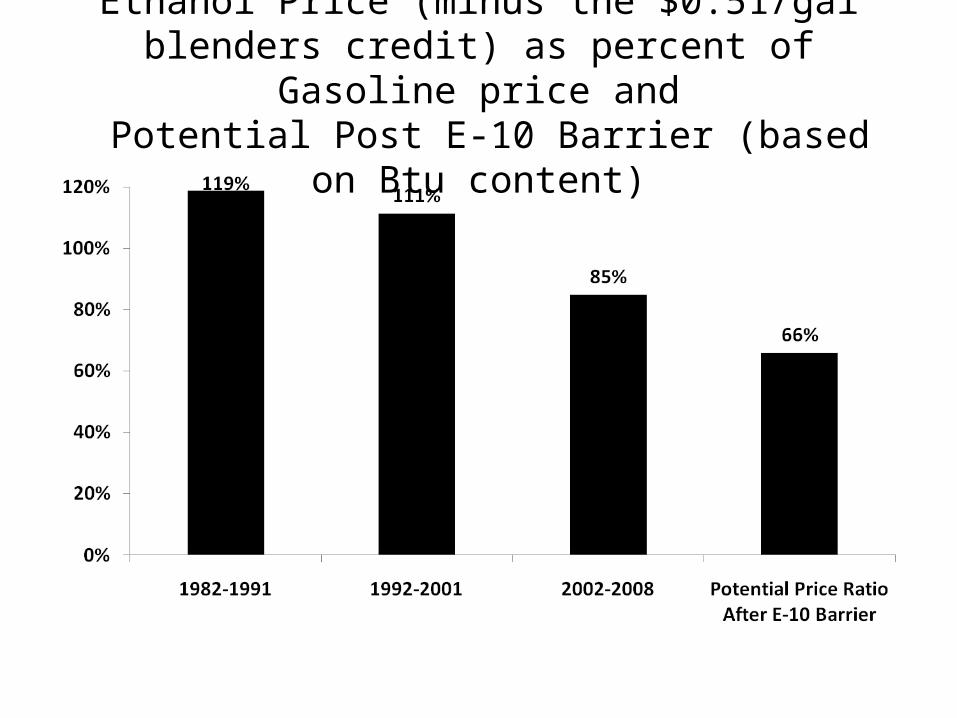

Ethanol Price (minus the $0.51/gal blenders credit) as percent of Gasoline price and

Potential Post E-10 Barrier (based on Btu content)

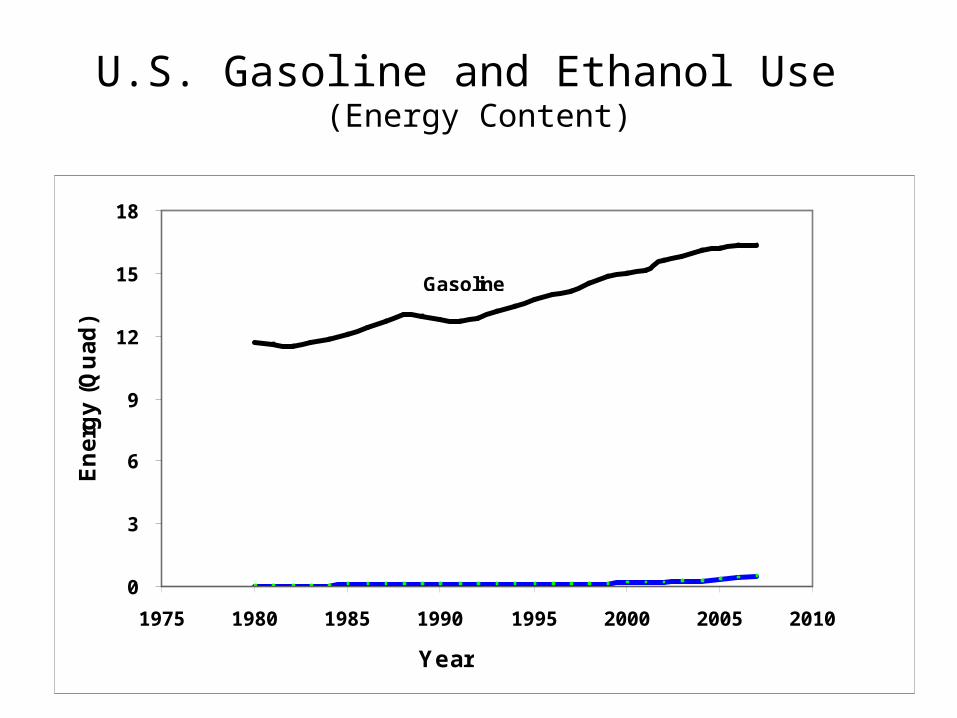

U.S. Gasoline and Ethanol Use (Energy Content)

0

3

6

9

12

15

18

1975 1980 1985 1990 1995 2000 2005 2010

Year

En

erg

y (

Qu

ad

)

Gasoline

Ethanol

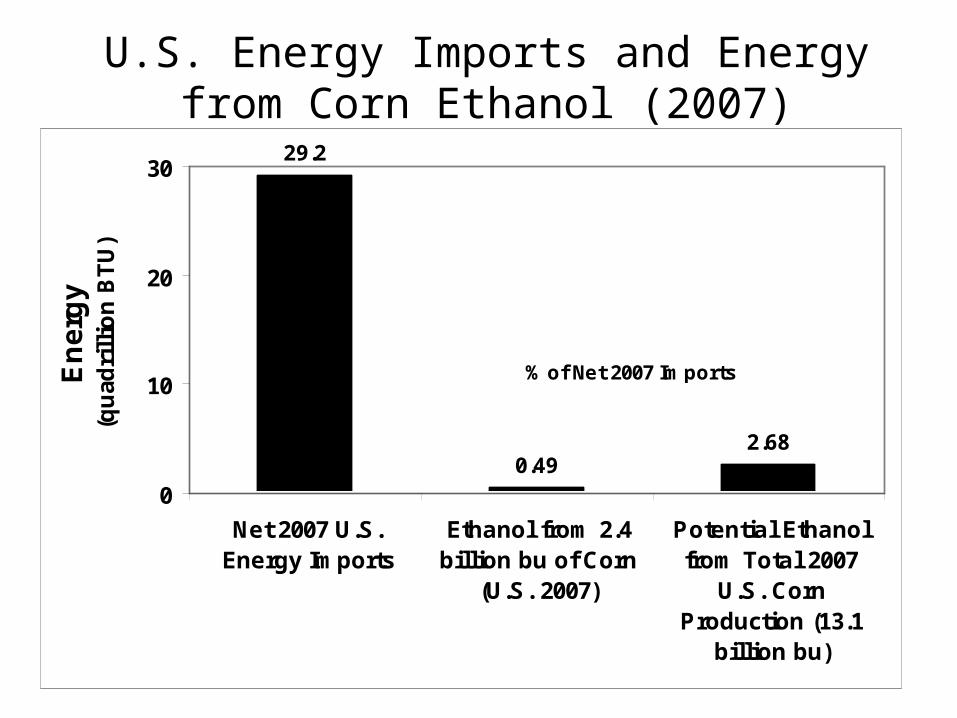

U.S. Energy Imports and Energy from Corn Ethanol (2007)

29.2

0.492.68

0

10

20

30

Net 2007 U.S.Energy Imports

Ethanol from 2.4billion bu of Corn

(U.S. 2007)

Potential Ethanolfrom Total 2007

U.S. CornProduction (13.1

billion bu)

En

erg

y(q

uad

rill

ion

BT

U)

% of Net 2007 Imports

1.7% 9.2%

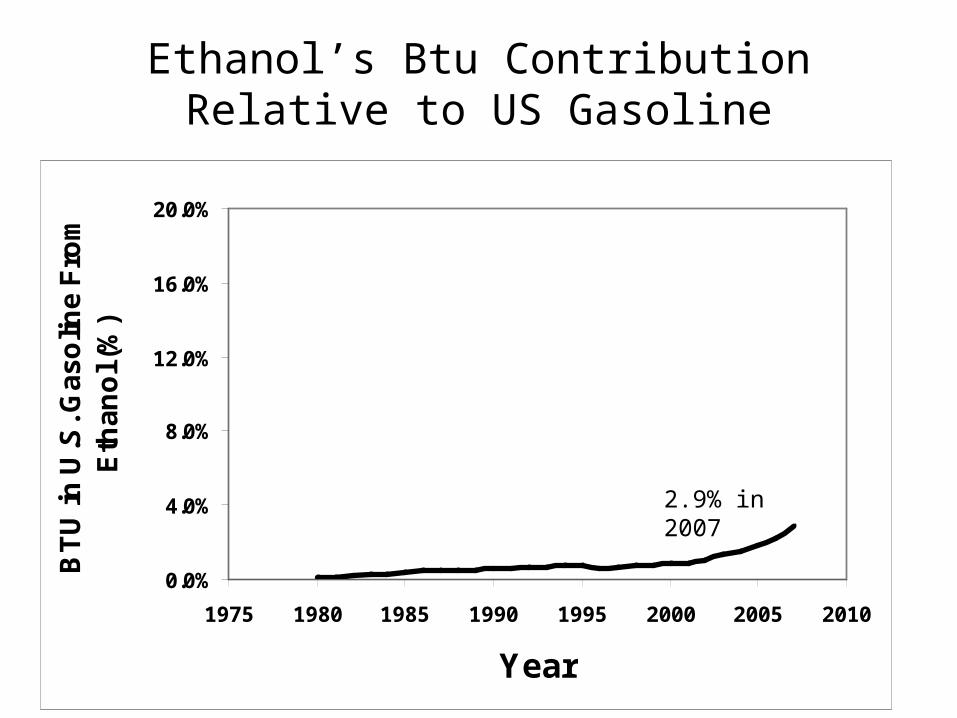

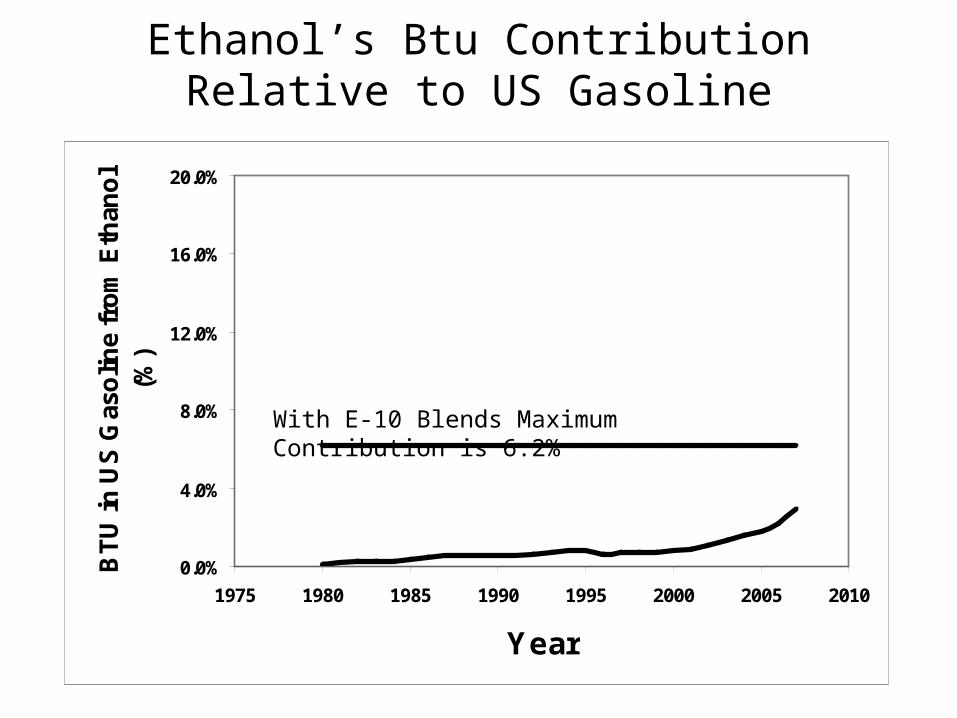

Ethanol’s Btu Contribution Relative to US Gasoline

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

1975 1980 1985 1990 1995 2000 2005 2010

Year

BT

U in

U.S

. Ga

so

line

Fro

m

Eth

an

ol (

%)

2.9% in 2007

0.0%

4.0%

8.0%

12.0%

16.0%

20.0%

1975 1980 1985 1990 1995 2000 2005 2010

Year

BT

U in

US

Gas

olin

e fr

om

Eth

ano

l (%

)

Ethanol’s Btu Contribution Relative to US Gasoline

With E-10 Blends Maximum Contribution is 6.2%

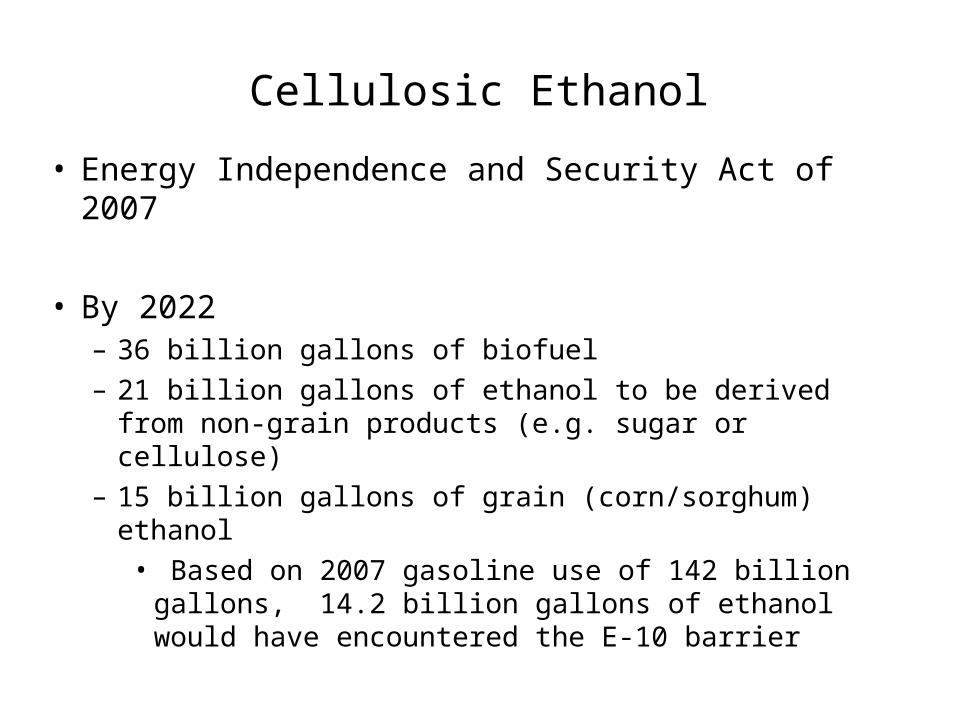

Cellulosic Ethanol

• Energy Independence and Security Act of 2007

• By 2022 – 36 billion gallons of biofuel– 21 billion gallons of ethanol to be derived from non-

grain products (e.g. sugar or cellulose)– 15 billion gallons of grain (corn/sorghum) ethanol

• Based on 2007 gasoline use of 142 billion gallons, 14.2 billion gallons of ethanol would have encountered the E-10 barrier

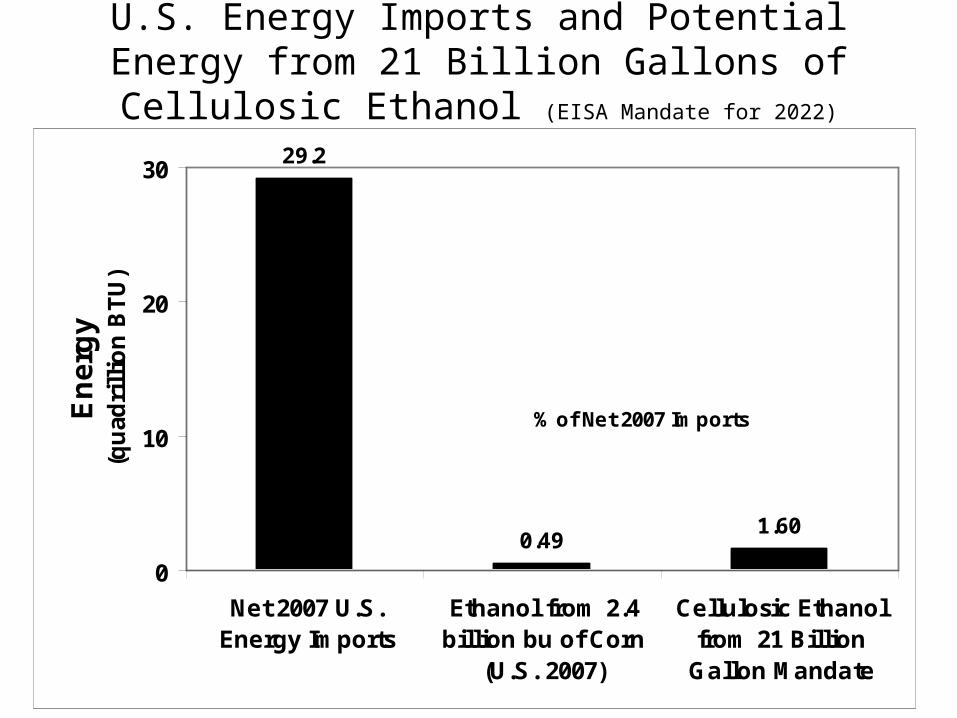

U.S. Energy Imports and Potential Energy from 21 Billion Gallons of Cellulosic Ethanol (EISA Mandate for 2022)

29.2

0.491.60

0

10

20

30

Net 2007 U.S.Energy Imports

Ethanol from 2.4billion bu of Corn

(U.S. 2007)

Cellulosic Ethanolfrom 21 Billion

Gallon Mandate

En

erg

y(q

uad

rill

ion

BT

U)

% of Net 2007 Imports

1.7% 5.5%

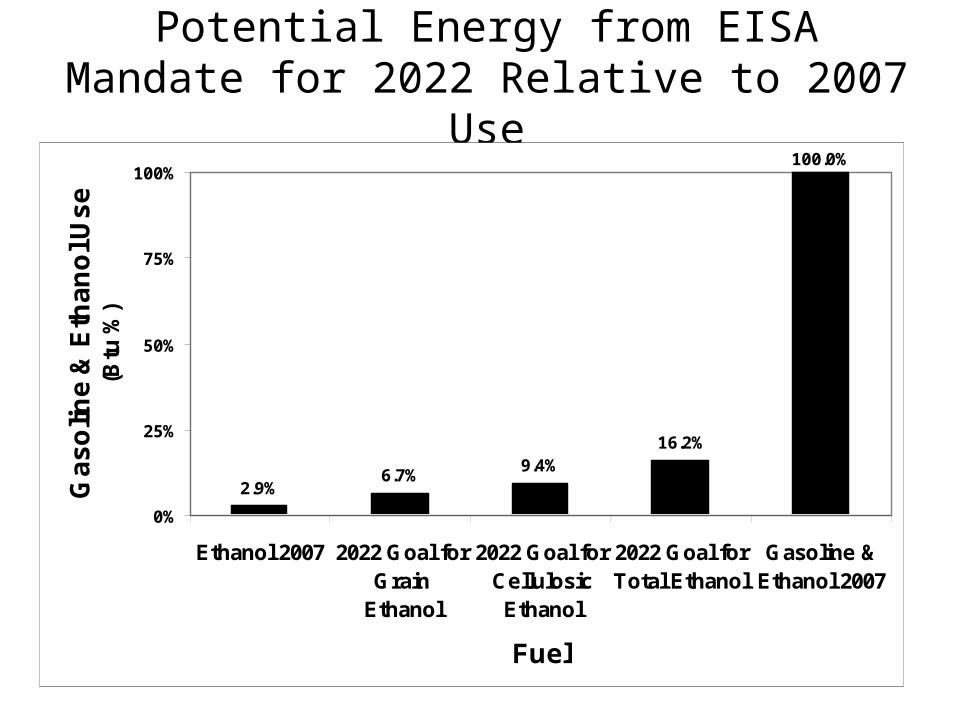

Potential Energy from EISA Mandate for 2022 Relative to 2007 Use

2.9%6.7%

9.4%16.2%

100.0%

0%

25%

50%

75%

100%

Ethanol 2007 2022 Goal forGrain

Ethanol

2022 Goal forCellulosicEthanol

2022 Goal forTotal Ethanol

Gasoline &Ethanol 2007

Fuel

Ga

so

line

& E

tha

no

l Us

e(B

tu %

)

Perspective

• 2022 goal of 36 billion gallons of ethanol would be equivalent to increasing fleet mileage by

– Four miles per gallon (e.g. 25 to 29 miles per gallon)

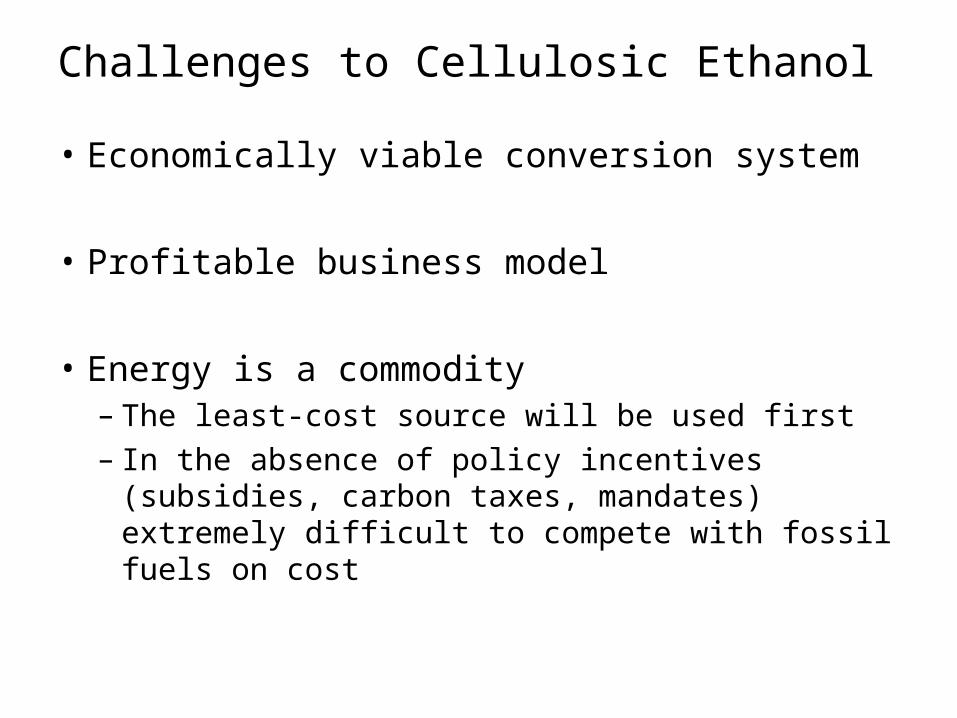

Challenges to Cellulosic Ethanol

• Economically viable conversion system

• Profitable business model

• Energy is a commodity– The least-cost source will be used first– In the absence of policy incentives (subsidies,

carbon taxes, mandates) extremely difficult to compete with fossil fuels on cost

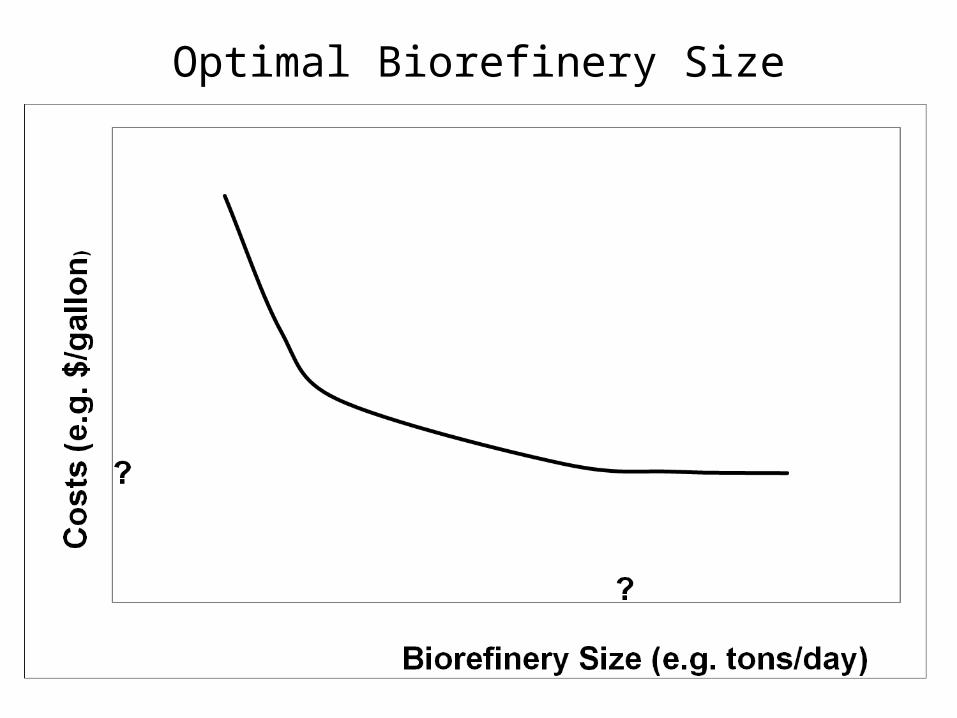

Optimal Biorefinery Size

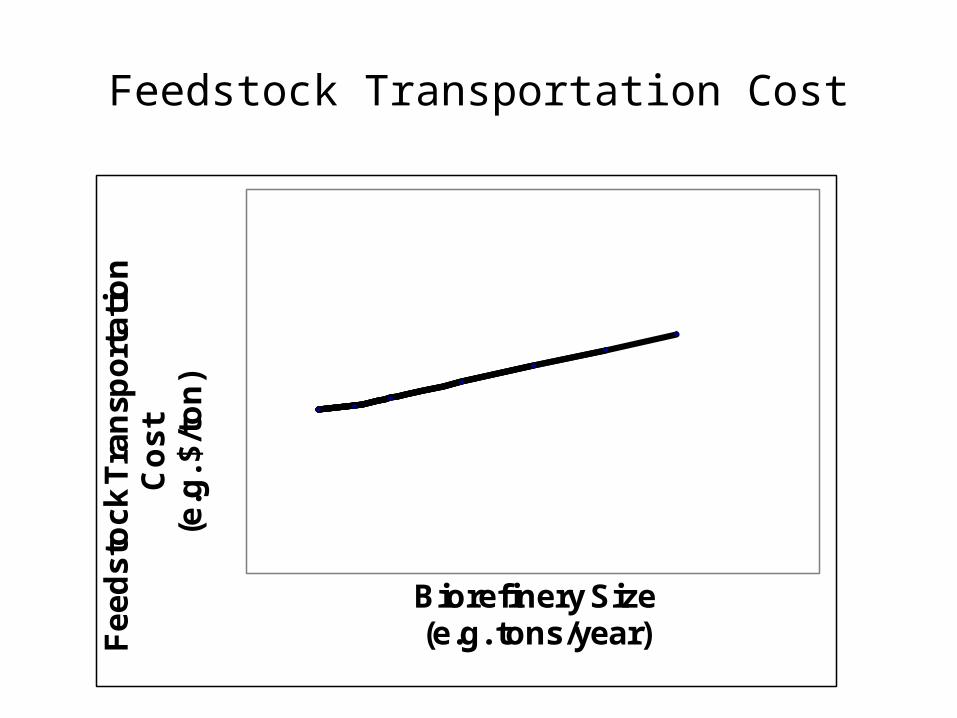

Feedstock Transportation CostF

ee

ds

toc

k T

ran

spo

rta

tio

n

Co

st

(e.g

. $/t

on

)

Biorefinery Size(e.g. tons/year)

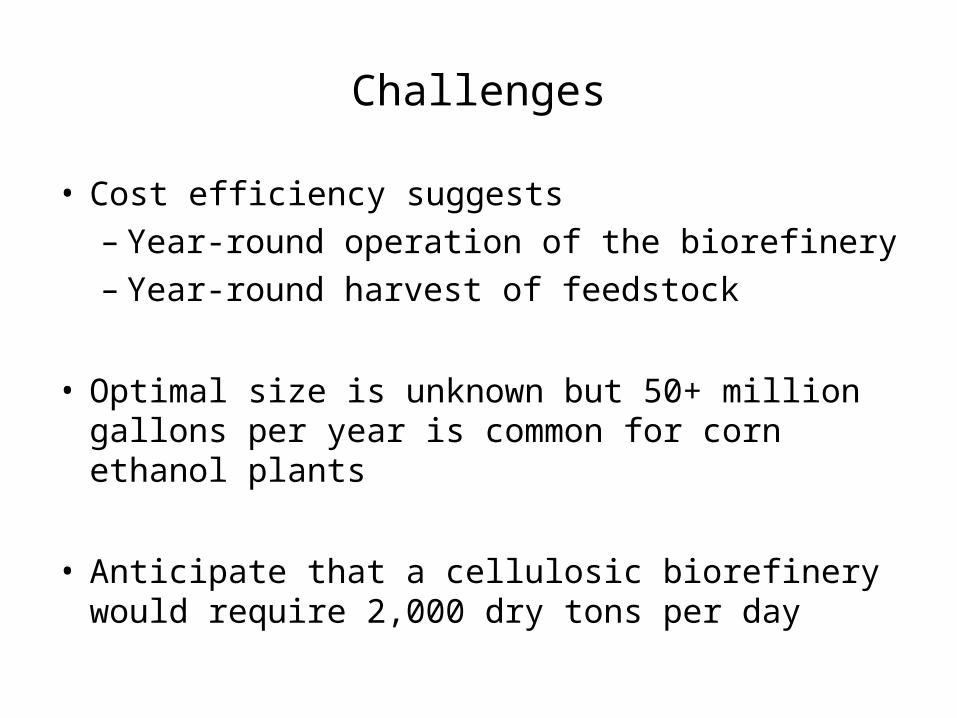

Challenges

• Cost efficiency suggests– Year-round operation of the biorefinery– Year-round harvest of feedstock

• Optimal size is unknown but 50+ million gallons per year is common for corn ethanol plants

• Anticipate that a cellulosic biorefinery would require 2,000 dry tons per day

Quantity of Feedstock Required for a2,000 tons per day Biorefinery

• 700,000 tons of biomass per year

• 350 days of operation per year

• 17 dry tons per truck

• 118 trucks per day

• 24 hours per day

• 4.9 trucks per hour

Can Agricultural Resources be Reallocated to Provide Feedstock for Cellulosic Ethanol?

Hypotheses

• Land suitable for economically producing continuous corn and corn-soybeans in rotation is too valuable for producing perennial grass for cellulosic feedstock

• “Corn lobby” will spend a great deal trying to make corn stover work as the base feedstock for cellulosic energy (ethanol business is concentrated in the corn belt)

• Corn stover is not likely to be an economical feedstock (but it won’t be for lack of trying and lack of research funds)

• If the subsidies/incentives are sufficiently great, stover “may work”

Trouble with StubbleFindings of a pilot corn stover collection project conducted near Harlan, Iowa• collection, storage, and transportation of a continuous flow of corn stover is

a “…logistical nightmare…”. • In the U.S. Corn Belt, stover harvest may be complicated by

– Rain– Mud– Snow– Narrow harvest window– Fire– Stalk moisture retention

• Dual collection combines, substantially more expensive, slow harvest, increase the risk of grain loss

Source: Schechinger, Tom. Current Corn Stover Collection Methods and the Future. October 24, 2000. Online. Available at http://www.afdc.doe.gov/pdfs/4922.pdf.

Trouble with Stubble

"Our main concern is $4-per-bushel corn (worth $750 to $800 an acre)," Johnson (a corn producer) said. “$30/acre for biomass is a minor concern for our operation.“

Source: Bill Hord, 27 March 2007, Omaha World-Herald

May require 350,000 acres of corn stover for a single biorefinery

contracts?

spot markets?

Will Perennial Grasses Work ?

Hypotheses• Not on land suitable for economical production

of continuous corn and/or of corn-soybeans rotation

• Perhaps on marginal cropland and cropland pasture (remains to be seen if pasture can be bid from livestock and converted to perennial grasses)

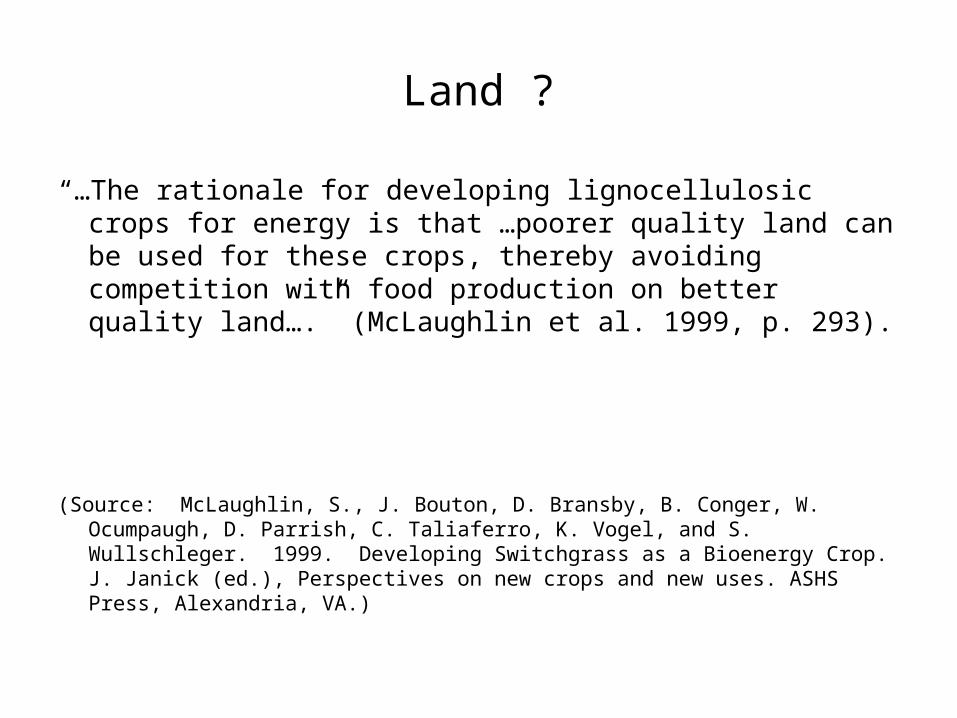

Land ?

“…The rationale for developing lignocellulosic crops for energy is that …poorer quality land can be used for these crops, thereby avoiding competition with food production on better quality land….” (McLaughlin et al. 1999, p. 293).

(Source: McLaughlin, S., J. Bouton, D. Bransby, B. Conger, W. Ocumpaugh, D. Parrish, C. Taliaferro, K. Vogel, and S. Wullschleger. 1999. Developing Switchgrass as a Bioenergy Crop. J. Janick (ed.), Perspectives on new crops and new uses. ASHS Press, Alexandria, VA.)

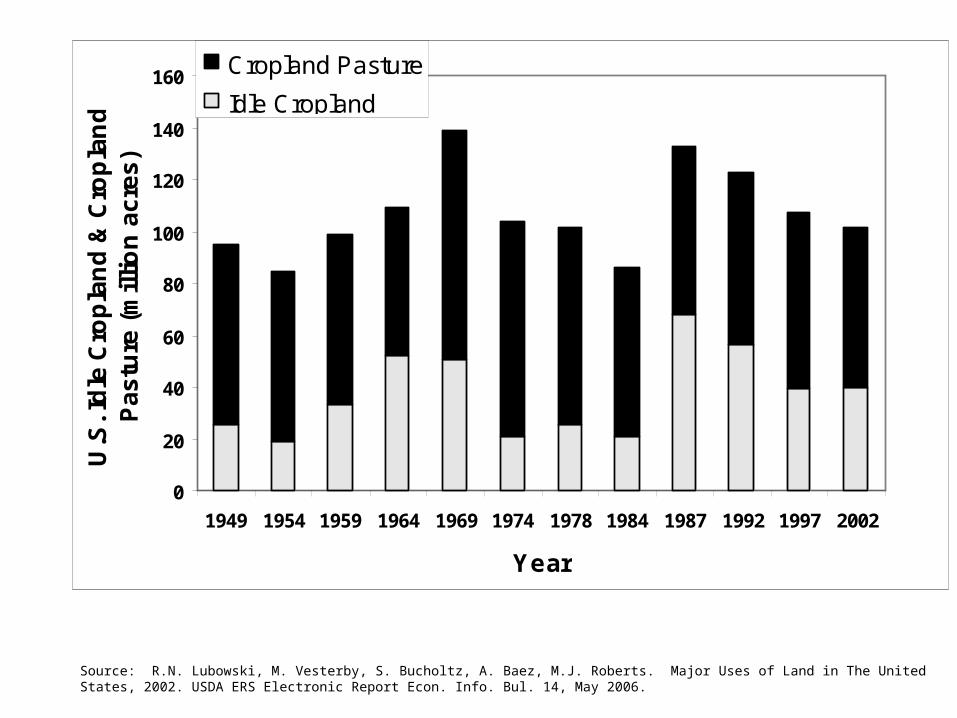

Source: R.N. Lubowski, M. Vesterby, S. Bucholtz, A. Baez, M.J. Roberts. Major Uses of Land in The United States, 2002. USDA ERS Electronic Report Econ. Info. Bul. 14, May 2006.

0

20

40

60

80

100

120

140

160

1949 1954 1959 1964 1969 1974 1978 1984 1987 1992 1997 2002

Year

U.S

. Id

le C

rop

lan

d &

Cro

pla

nd

P

as

ture

(m

illi

on

ac

res

)

Cropland Pasture

Idle Cropland

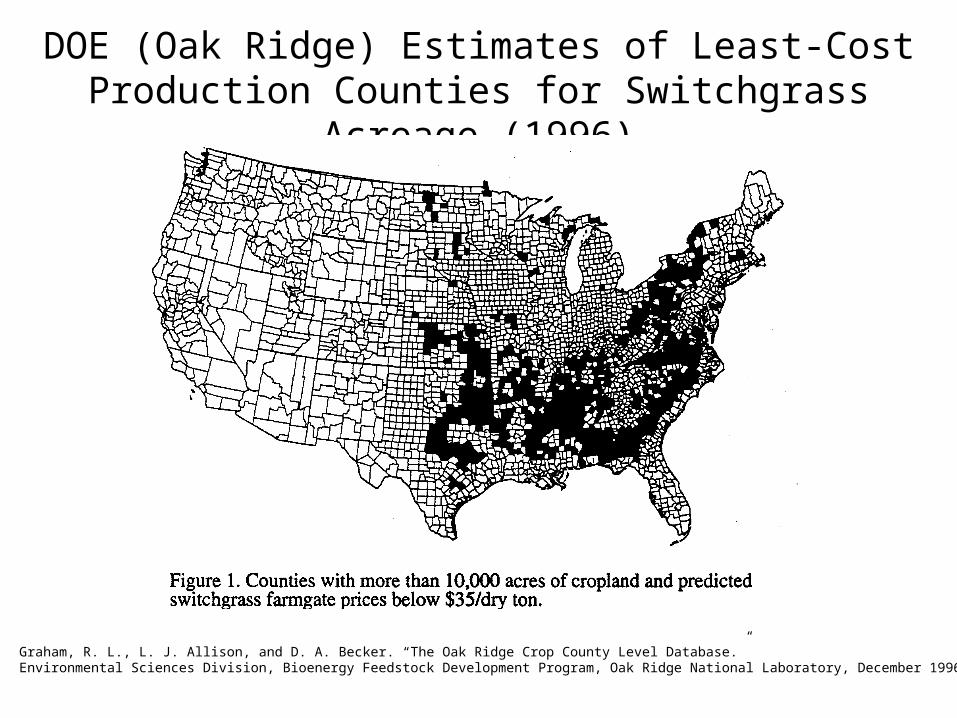

DOE (Oak Ridge) Estimates of Least-Cost Production Counties for Switchgrass Acreage (1996)

Graham, R. L., L. J. Allison, and D. A. Becker. “The Oak Ridge Crop County Level Database.” Environmental Sciences Division, Bioenergy Feedstock Development Program, Oak Ridge National Laboratory, December 1996.

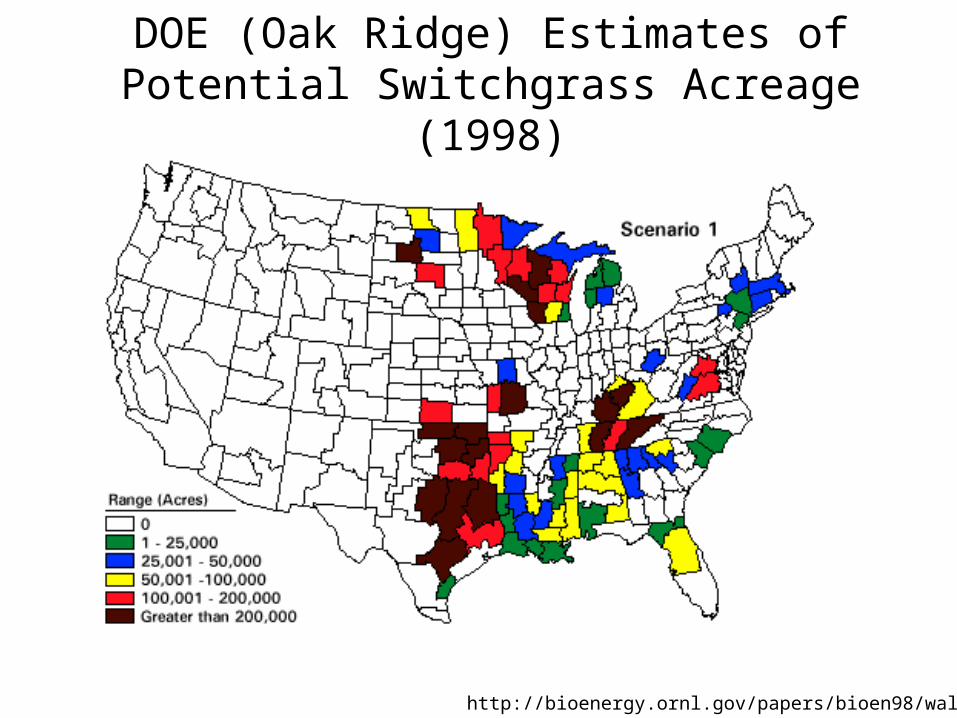

DOE (Oak Ridge) Estimates of Potential Switchgrass Acreage (1998)

•

http://bioenergy.ornl.gov/papers/bioen98/walsh.html

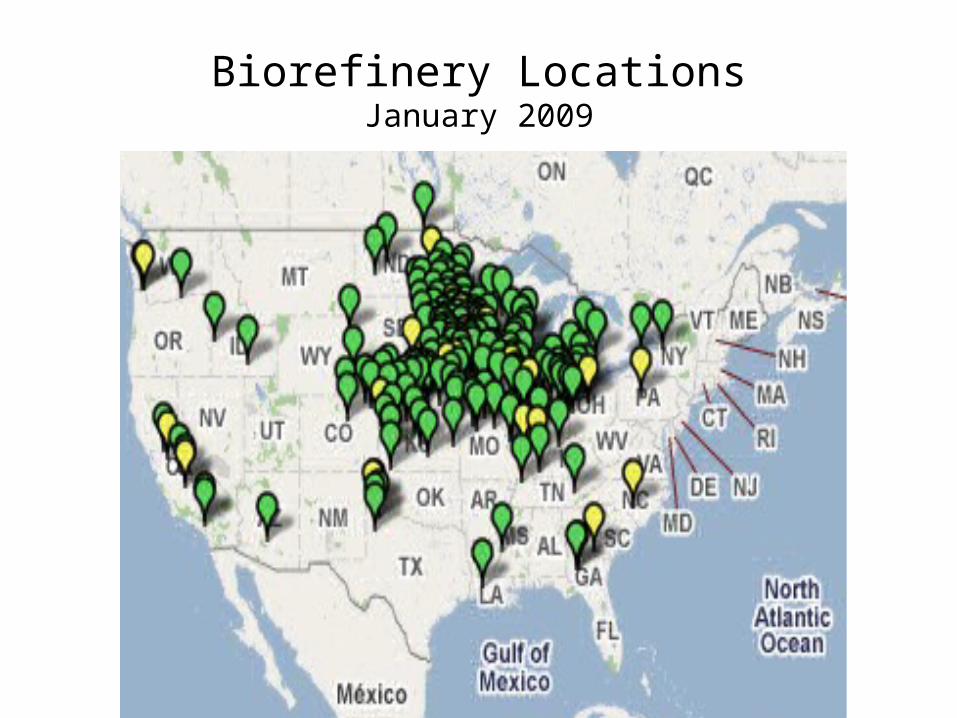

Biorefinery LocationsJanuary 2009

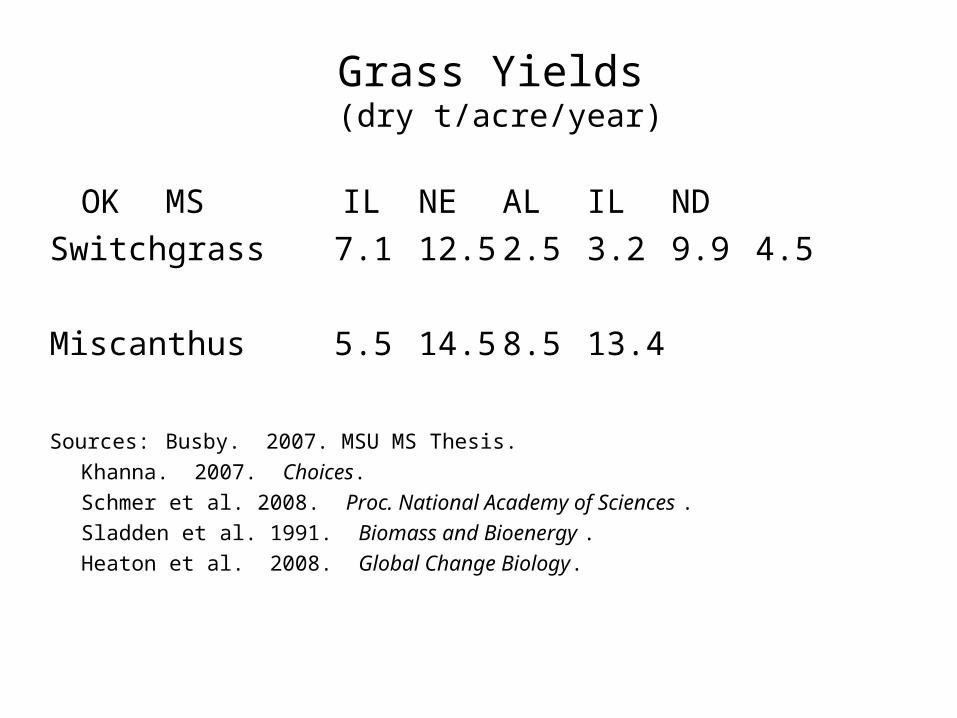

Grass Yields (dry t/acre/year)

OK MS IL NE AL ILND

Switchgrass 7.1 12.5 2.5 3.2 9.9 4.5

Miscanthus 5.5 14.5 8.5 13.4

Sources: Busby. 2007. MSU MS Thesis.Khanna. 2007. Choices. Schmer et al. 2008. Proc. National Academy of Sciences .Sladden et al. 1991. Biomass and Bioenergy . Heaton et al. 2008. Global Change Biology.

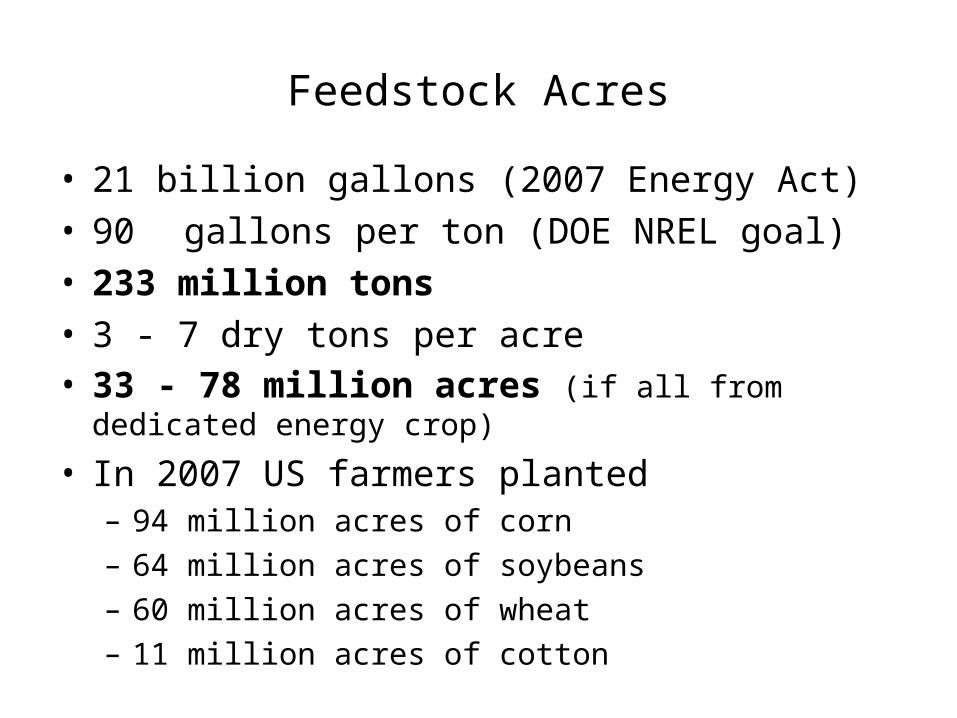

Feedstock Acres

• 21 billion gallons (2007 Energy Act)• 90 gallons per ton (DOE NREL goal)• 233 million tons• 3 - 7 dry tons per acre • 33 - 78 million acres (if all from dedicated energy crop)

• In 2007 US farmers planted – 94 million acres of corn – 64 million acres of soybeans– 60 million acres of wheat– 11 million acres of cotton

Business Model

• Is the most efficient switchgrass-biorefinery business model likely to resemble the corn-ethanol business model?

– Perhaps in distillation and post-distillation

– Not in feedstock procurement

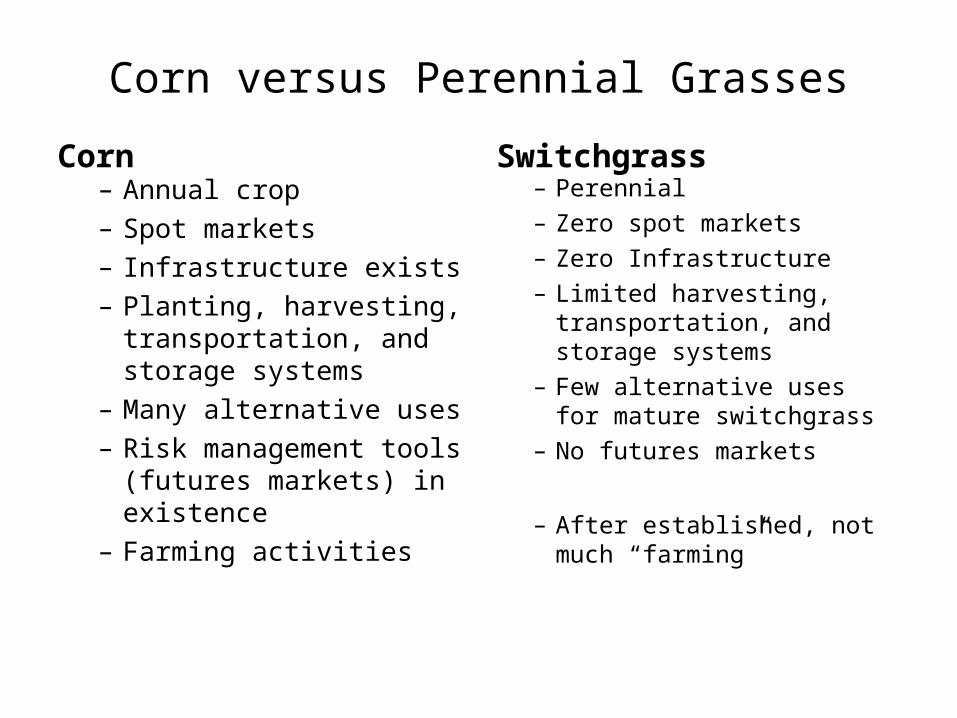

Corn versus Perennial Grasses

Corn– Annual crop– Spot markets– Infrastructure exists– Planting, harvesting,

transportation, and storage systems

– Many alternative uses– Risk management tools

(futures markets) in existence

– Farming activities

Switchgrass– Perennial– Zero spot markets– Zero Infrastructure– Limited harvesting,

transportation, and storage systems

– Few alternative uses for mature switchgrass

– No futures markets

– After established, not much “farming”

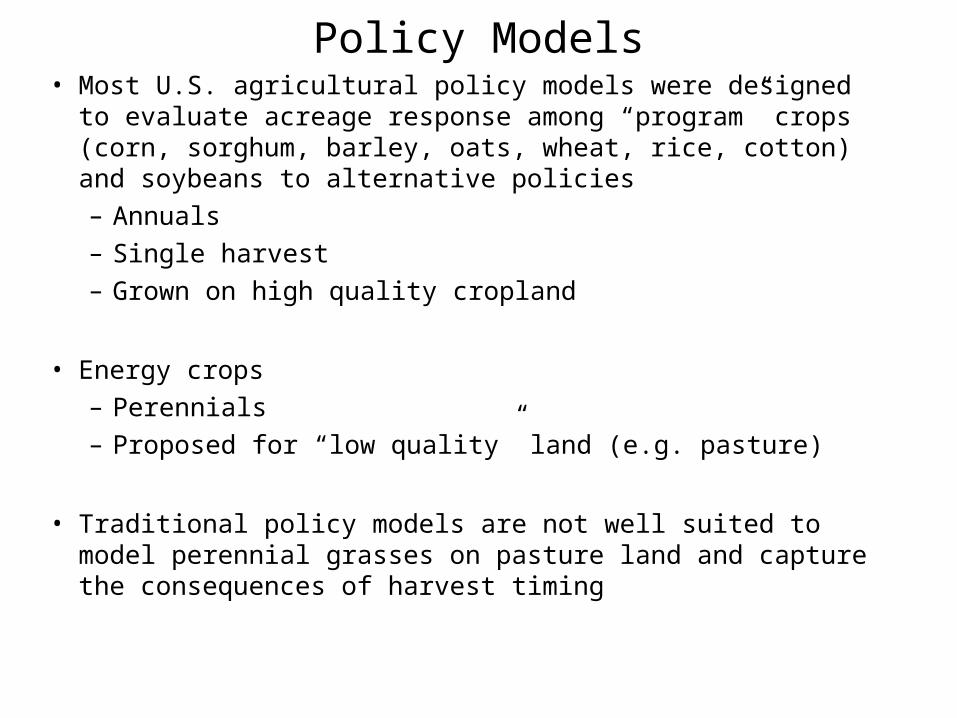

Policy Models• Most U.S. agricultural policy models were designed to evaluate

acreage response among “program” crops (corn, sorghum, barley, oats, wheat, rice, cotton) and soybeans to alternative policies– Annuals– Single harvest– Grown on high quality cropland

• Energy crops– Perennials – Proposed for “low quality” land (e.g. pasture)

• Traditional policy models are not well suited to model perennial grasses on pasture land and capture the consequences of harvest timing

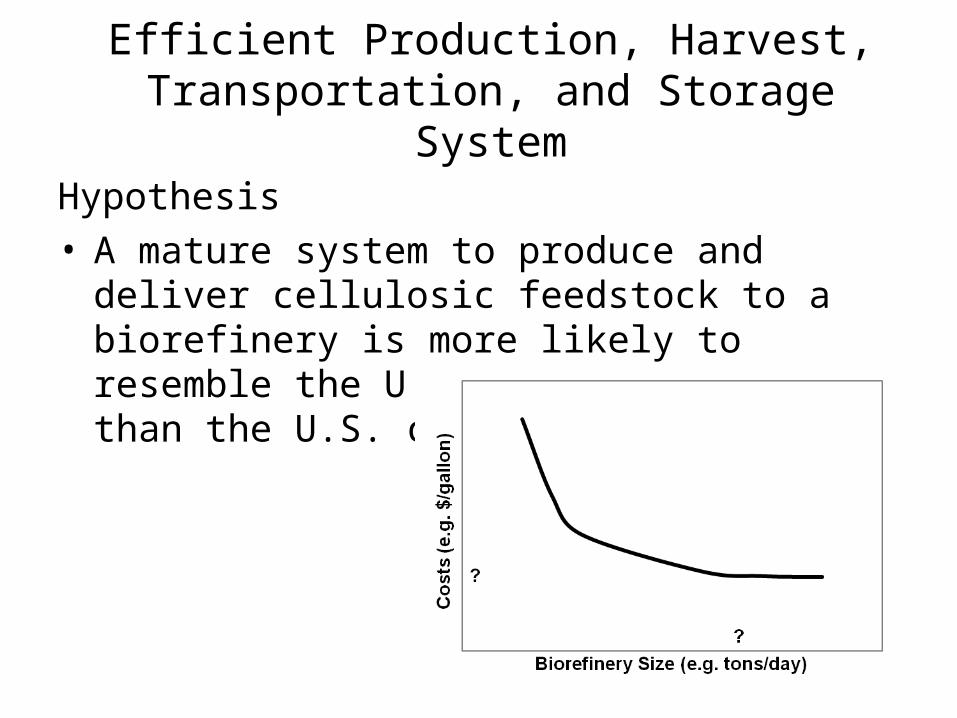

Efficient Production, Harvest, Transportation, and Storage System

Hypothesis• A mature system to produce and deliver

cellulosic feedstock to a biorefinery is more likely to resemble the U.S. timber industry than the U.S. corn industry

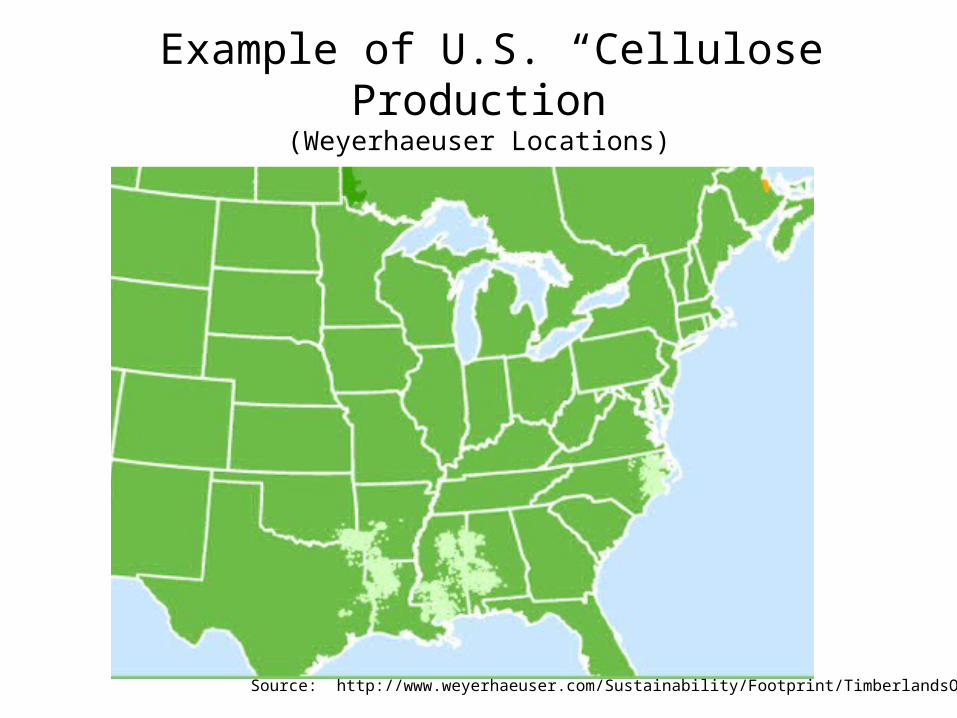

Example of U.S. “Cellulose” Production(Weyerhaeuser Locations)

Source: http://www.weyerhaeuser.com/Sustainability/Footprint/TimberlandsOwnership

South relative to Corn Belt for Producing Perennial Grasses

• Higher yields

• Less expensive land

• Longer harvest window

• Longer growing season

• History of large integrated “cellulosic” production and processing systems (timber)

Issues– Profitable business model

– Efficient method to acquire the long term services of millions of acres of land (contract acres or contract production; insurance for the land owner in the event of default by biorefinery)

– Sources for billions of dollars of investment capital

– Policy could be implemented that discriminates against integrated systems

Cellulosic Ethanol

• Potential market is huge

• Many challenges remain

Acknowledgements

• Oklahoma Agricultural Experiment Station• USDA/CSREES• USDA/IFAFS• Oklahoma Bioenergy Center• Sun Grant Initiative• Aventine

• Coskata (licensed technology)