-

8/13/2019 Altaf Internship Report

1/37

-

8/13/2019 Altaf Internship Report

2/37

AACCKKNNOOWWLLEEDDGGEEMMEENNTT

First of all I am thankful to "ALMIGHTY ALLAH" Who gave me the

strength, patience,

courage and enthusiasm needed to write and complete this report,

and countless salutations to

upon the Holy Prophet Muhammad (PBUH), the sea of knowledge who

has guided His

Ummah to seek knowledge from cradle to grave.

Then to my Supervisor Mam Noreen Afzal who assisted me to

accomplish this assignment. I

have a debt of gratitude to all my teachers who taught me

throughout my academic career.

The preparation of this report was a massive undertaking but the

highly competent and

experienced management of Askari Bank provided me with all

assistance, information,

advice and suggestions that I needed which contributed

importantly to this report.

Altaf Hussain

11111111111

-

8/13/2019 Altaf Internship Report

3/37

11..EEXXEECCUUTTIIVVEESSUUMMMMAARRYY

As per the requirements for the degree of MBA at University of

Education Lahore, Okara

campus, I got an opportunity to get six weeks internship

exposure. Askari Bank, katchary Road

Branch Depalpur provides me the chance to have this experience.

During my internship I was

rotated in the various departments in order to get in depth idea

of how the bank functions. This

report thoroughly outlines and explains my observations,

findings and analysis and my

knowledge of the banking sector in general and Askari Bank in

particular.

In this report, there is an introduction of Askari Bank. In

introduction, there is history of Askari

Bank, strong commitment and loyal service, highly trained

professionals, and credit rating. The

report also includes the details of the products offered by

Askari Bank

Subsequent to it this report contains five years financial

anaylsis and also SWOTS of Askari

Bank. With the help of these methods I have some suggestions and

recommendations to improve

the performance of the Bank, which also mentioned in this

report. By following these

suggestions bank can improve their product market and can easily

gain the attraction and

satisfaction of customers. Not only the customers, bank also can

improve the satisfaction and

performance level of its employees by these suggestions.

-

8/13/2019 Altaf Internship Report

4/37

22..OOBBJJEECCTTIIVVEESSOOFFSSTTUUDDYYIINNGGTTHHEEOORRGGAANNIIZZAATTIIOONN

OverviewAfter the completion of degree MBA (Finance) I want to

enter and check the practical work

according to my specialization. For that purpose I selected the

banking sector because I have

done specialization in finance.

Second and next main objective of studying organization; I want

to enter in practical field and

want to learn that which discipline is required for leading a

successful future life. I think I am

very lucky person that I selected Askari Bank as my learning

organization.

Objectives that I want to achieveObjectives that I want to

achieve by studying the organization are as follows:

First of all I want to check the practical work according to my

degree specialization.

During my internship in Askari Bank I have learnt that how to

use the knowledge in

practical field.

Secondly I want to learn that how to mange an organization and

how to mange the

finance for a financial organization, as my degree is related to

Financial Management.

Customers dealing is another major objective that I want to

achieve. During my

internship I learnt that how to deal with customer.

Financial institution is a place where every type of businessmen

visits, so during my

internship in AKBL I met with many businessmen and learnt that

how different

businesses run.

And another main objective that I want to achieve that how an

organization consist with

different departments and how different functions are done in

different departments of an

organization.

-

8/13/2019 Altaf Internship Report

5/37

Brief History Of The OrganizationAskari Bank Limited was

incorporated on October 9, 1991, as a Public Limited

Company, and is listed on Karachi, Lahore and Islamabad Stock

Exchanges. The

Bank obtained business commencement certificate on February 26,

1992 and

started operations from April 1, 1992. Askari Bank is scheduled

Commercial Bankand is principally engaged in the business of

Banking as defined in the Banking

Companies Ordinance 1962.Askari Bank Limited continues to scale

new heights in all areas of its operations.

The safety and security of depositors funds, high productivity

and optimum use of

technology are the hallmarks of its corporate strength.

In 1994, AKBL earned international recognition as Asia Money

Award and thetitle of

Best Commercial Bank of Pakistan for the year 1994, while Euro

moneydeclared the Bank as best domestic Bank of Pakistan for the

year 1995.

Askari Bank has since expanded into a network of 261 branches /

sub branches,including 34 dedicated Islamic banking branches, and a

wholesale bank branch in

Bahrain.A shared network of 5,903 online ATMs covering all major

cities in Pakistan

supports the delivery channels for customer service. As at

December 31,2012, the Bank had equity of Rs. 19.7 billion and total

assets of Rs. 353 billion,

with 907,984 banking customers, serviced by our 5,597

employees.Askari Investment Management Limited and Askari

Securities Limited are

subsidiaries of Askari Bank engaged in managing mutual funds and

share

brokerage, respectively.

-

8/13/2019 Altaf Internship Report

6/37

-

8/13/2019 Altaf Internship Report

7/37

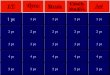

Organization Business Volum

The business volum of Askari B ank is expanding day by day. As

below table isshowing the business volum of Askari Bank of the last

five years.

Years 2008 2009 2010 2011 2012

Total Assets 206,191 254,327 314,744 343,756 353,056

Shareholder' Equity 12,971 14,949 16,004 17,776 19,688

Number of Branches 226 235 245 261

Number of Employees 6,159 6,442 5,994 5,597

Number of Customers 984,485 885,764 919,096 907,984

Source: AKBL Annual Reports from 2008-2012

Interpretation of Business VolumThe business volum ofAKBL in

terms of Total Assets, Share-holders Equity and the No. ofBrnches

incresd with the passage of time. Number of Employees working at

AKBL has shown

downward trend and the tolat number of customers does not show a

particular trend.

-

8/13/2019 Altaf Internship Report

8/37

Product Lines & Services

Agriculture

Products

Branch

Banking Consumer

BankingIslamic

BankingAlternate

Delivery

Channels

-

8/13/2019 Altaf Internship Report

9/37

1.Agriculture Product

1.1KISSAN EVER GREEN FINANCE

Features Details

Product Type: Profit Earning Account.

Eligibility: Pakistani Resident (Individuals).Security:

Mortgaged charge on agri land through Zari Pass Book.

Profit Amount: Profit on credit balances will be paid on half

yearly basis as

declared by the bank on PLS savings accounts.

Tenor: Yearly Basis.

Markup: The mark-up is charged for the actual days the finance

isutilized.

Benefits: 1. A special cheque book is issued to the farmer.

2. Automatic renewal upon adjustment of entire Principal

amount with mark-up once in a year.

3. The account is farmer friendly which benefits the farmersboth

ways. If the account is in credit, it earns profit, otherwise

it

provides instant finance, to the farmer for his agriculture

needs.

-

8/13/2019 Altaf Internship Report

10/37

1.2KISSAN AABPASHI FINANCE

Features Details

Product Type: To finance installation of Tube-Wells (electric,

diesel and solarenergy units) water management equipments and water

channel

development etc.Eligibility: Pakistani Resident (owner of

farmers).

Benefits: 1. Help farmers to make optimum use of limited water

resources.

2. To facilitate the farmer, to overcome the scarcity of

water.3. To develop mechanical water resources, sprinkler and

dripsystem etc.

4. To avoid traditional inefficient modes of irrigation and

wasteof available water.

5. To manage natural available resources through watermanagement

practices.

-

8/13/2019 Altaf Internship Report

11/37

1.3 KISSAN LIVESTOCK DEVELOPMENT FINANCE

Features Details

Product Type: To purchase Milch Animals, Goats, Sheep, Poultry

andFisheries without incurring extra expenditure because of

availability at his farm.Eligibility: Pakistani Resident (Owner

Farmers).

Benefits: The program will provide regular day to day income to

thefarmer to meet his own consumption and surplus to be

marketed.

This will revive / accelerate and supplement the income

generating capacity.It will enhance the repayment capacity of

the farmer.

-

8/13/2019 Altaf Internship Report

12/37

1.4 KISSAN FARM MECHANIZATION FINANCE

Features Details

Product Type: Finance for farm equipment, trailer, thresher,

drills & rotavatorsetc

Eligibility: Pakistani Resident (Individuals).Benefits: 1.Under

this program the farmer will get benefit of use of

modern agricultural tools, implements and equipments whichare

cost and time effective.

2.Improves per acre yield of agri crops and quality of

agriculture produce to get good price in the market3.Helps to

match / compete with international standards forexportable

agriculture produce.

-

8/13/2019 Altaf Internship Report

13/37

-

8/13/2019 Altaf Internship Report

14/37

2. Branch Banking products

2.1 VALUE PLUS CURRENT ACCOUNTFOR INDIVIDUALS

Features Details

Opening BalanceRequirements: Rs. 25,000/-

Minimum Monthly Rs. 25,000/-*

Average Balance

Requirements: (In case of short fall in the minimum balance

requirement, service charges for free services beingoffered will

be charged as per prevailing Schedule ofCharges.)

FREE FACILITIES: . Issuance of Visa Debit Card. Annual and

replacement feewould apply.

ATM Cash Withdrawal Insurance coverage upto dailycash witdrawal

limit of the debit card from Askari Bank

coverage to Debit Card / Visa Debit Card Holders. Rs.500,000/-

and Rs. 700,000/- for Classic and Gold Visa

Debit Cards respectively

24 hours world-wide Accidental Death & Permanent

Disability insurance coverage. The sum insured per

account holder shall be equivalent to four times of the

http://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdf

-

8/13/2019 Altaf Internship Report

15/37

average balance completed in the last six months

maximum upto Rs. 2 Million

On-line fund transfer facility

i-Net Banking facility

SMS Alerts of ATM Cash withdrawal to Visa Debit Cardholders.

Issuance of Pay orders / Demand drafts

Issuance of 2 Supplementary Visa Debit Cards. Annual

and replacement fee would apply

Issuance of Cheque Books

Duplicate account statements

VALUE PLUS CURRENT ACCOUNT

FOR BUSINESS

Features Details

Opening Balance

Requirements: Rs. 100,000/-Minimum Monthly

Average BalanceRequirements: Rs. 100,000/-*

(In case of short fall in the minimum balance

requirement, service charges for free services being

offered will be charged as per prevailing Schedule of

Charges.)UNIQUEFEATURE: If any organization opens Value Plus

Current Account

for Business, then its employees will be eligible to open

Value Plus Saving Account with an initial Deposit of Rs.5,000/-

only.

FACILITIES: On-line funds transfer facility

Issuance of Cheque Books

Issuance of Pay orders / Demand drafts Duplicate account

statements Statement of Account through email (Once a month)

http://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdf

-

8/13/2019 Altaf Internship Report

16/37

2.2 ASKARI PAISHGI MUNAFA TERM DEPOSIT

Features Details

Product Type: Term Deposit.

Eligibility: Pakistani Resident (Individuals).

Minimum Amount: Rs. 100,000/- or in multiples of Rs.

100,000/-.Profit Amount: Rs. 9,375/- on a deposit amount of Rs.

100,000/-

(expected rate of return 7.5 % p.a)Tenure: 15 Months.

Benefits: 1. Financing Facility up to 80% of Principal

amount.

2. Free Visa Debit Card issuance.3. No Minimum Balance

requirement in checkingaccount.

4. 2 Free Pay Orders in a month (Withholding Tax andother

Government charges will be applicable as per

Law).5. No maximum limit for investment.

-

8/13/2019 Altaf Internship Report

17/37

2.3 ASKARI BACHAT ACCOUNT

Features Details

Product Type: Term Deposit.Eligibility: Pakistani Resident

(Individuals Only).Balance Requirement: Minimum balance of Rs.

50,000/- with no upper limit.

Tenure: 1 Year.

Profit Payment: Monthly1st of every month.

Expected Rate of Return: 8.5% p.aFinancing Limits: Up to 90% of

the principal amount

Servicing: Available at all Askari Bank branches.Free

Facilities: 1- VISA DEBIT CARD (For the CASA account)

2- INSURANCE COVERAGE3- On-line fund transfer facility.

4- I-Net Banking facility5- Issuance of Cheque Books.

6- Duplicate account statements.7- Free Pay Orders.

-

8/13/2019 Altaf Internship Report

18/37

2.4 RUPEE TRAVELERS CHEQUES

Features Details

Eligibility: Any Literate individual customer (Account is

not

mandatory).

Denominations: Rs. 10,000/-.Validity: Until encashed.Processing:

Issuance

Desirous customer will submit the Application Form(duly filled/

signed) in any branch of Askari Bank

Limited.After verification, branch will forward the form to

Investment Products Unit.IPU will keep the record of the

customer and system will

automatically update that customers transaction.Encashment

Original purchaser will approach the nearest branch.Purchaser

will sign RTC on the face and branch will

verify his signatures with the signature mentioned on

CNIC before encashment of the same.

Charges: Refund processing charges are Rs. 1,000/-

andIssuance/Encashment are free.

-

8/13/2019 Altaf Internship Report

19/37

-

8/13/2019 Altaf Internship Report

20/37

4. PTCL Bill or Utility bill relevant with the address

mentioned on application.5. Post dated cheques.

6. One Year bank statement.

7. Specimen Signature card verified by the bank.8. Undertaking

on signature if signature differs from

CNIC.9. Latest Salary slip.

10. Proof of business & other income.11. NTN certificate

(optional).

12. Bank letter for proprietorship.

13.Wealth statement required in case of financing of 1.5M &

above.

14. Partnership deed (if applicable).

15. Verified CNIC of the guarantor.16. Guarantor Net worth

Statement (optional).

Documentation:

1. Standard Finance Documents.

2. Other Mandatory Documents.3. 15 Report (Police Clearance

Report).

4. Evaluation Report by approved surveyors.

5. Fresh Vehicle ownership certificate from ETO prior totransfer

in the name of AKBL.

-

8/13/2019 Altaf Internship Report

21/37

3.2 MORTGAGE FINANCE

Features Details

Purpose of Loan: Purchase of Plot + Construction.

Construction on Existing Plot.

Purchase of House/ Apartment.Renovation of House/

ApartmentBalance Transfer Facility.

3.3 PERSONAL FINANCE

Features Details

Applicant/ Borrower: Pakistani Resident (SEB/SEP cases are not

entertainedcurrently).

Age: Salaried: 21-61 years

Salary/ Income: Rs. 30,000/-per month.

Employment Status: 1 Year.Debt Burden: Maximum 50% of the net

disposable income.Credit Limit: Up to Maximum of Rs. 500,000/-

(Subject to maximum

of 50% DBR & Industry benchmark is maximum Rs.1.000 M).

Tenure: 1 - 5 years.Mark up: Secured Salaried: 19% p.a.

-

8/13/2019 Altaf Internship Report

22/37

Mark up: Unsecured Salaried: 21% p.a & Contract Employees

24.2% p.a

Reference: Two (2) references with complete details (one should

berelative).

Processing / Others Charges: As per "Schedule of Bank

Charges".

Documentation: 1. Application Form duly filled & Signed by

theapplicant in his/her own handwriting.

2. Clear copy of valid CNIC.3. Two passport size latest

photographs.

4. Last two month original salary slip or attestedphotocopy

required.

5. Last 6 month bank statement of salary account.

he latest paid utility bill received at the residentialaddress

in case of salaried individual.

he latest bill received at the business address &

residential address, in case of SEB/SEP.8. BBFS, DDA,

Undertaking CF-1, undertakingregarding other credit facilities.

3.4 CREDIT CARD

Features Details

Eligibility: Pakistani Resident.

Card Types: 1.Silver Card (cash withdrawal limit per day

Rs=50,000)2. Gold Card (cash withdrawal limit per day

Rs=100,000)

http://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdfhttp://www.askaribank.com.pk/docs/SOCz.pdf

-

8/13/2019 Altaf Internship Report

23/37

4. Islamic Banking Products

4.1 ASKARI IJARAH BIS SAYYARAH(IJARAH CAR FINANCING)

Features Details

What is Ijarah? Ijarah is a rental agreement, under which the

usufructs of

an asset is transferred to the client on pre-agreed termsand

conditions. It is a Shariah Compliant mode of

finance, adopted by Askari Islamic Banking to meet theCar

Financing needs of its valued customers.

Key features: Prompt Processing Time.

Facility to acquire more than One VehicleFacility Income

Evaluation Plan

Low Security DepositCompetitive Profit Rates

Eligibility: A Pakistani National.Earning at least two times

more than your monthly Car

Ijarah rentalsBetween 21 to 60 years, (for salaried class) and

of age,

till the maturity of the lease periodEmployment experience of

minimum six months in a

permanent capacity in the current organizationBeing in business

for at least one year

DocumentsRequired: (For Business Person)

Copy of CNICTwo recent passport sizes colored photographs.

-

8/13/2019 Altaf Internship Report

24/37

-

8/13/2019 Altaf Internship Report

25/37

4.2ASKARI HOME MUSHARAKAH(MUSHARAKAH HOME FINANCE)

Features Details

Askari Home

Musharakah:Joint ownership is created in the property between

Bank &

Customer on the basis of the Musharakah Agreement. (This isbases

on the principles of Shirkat ul Milk).

Banks share is divided into units and is given to the client

onrent.

Client promises to purchase Banks share (units) over the

tenureof transaction.

Client purchases the units every month and will eventuallybecome

the owner of the property.

Rental amount will be adjusted according to the banks

share(units) remaining in the property.

Askari Home Musharakah has tailor made solutions to meetyour

needs

Askari Home

Musharakah

Purchase: Askari Islamic Banking offers a convenient and easy

way tobuy your own home, with a financing of 85% of the

property

cost, upto Rs. 50 Million.

-

8/13/2019 Altaf Internship Report

26/37

Askari Home Musharakah

Construction: You can simply build your home as you desire, with

halalIstisna/Musharakah Finance from Askari Islamic Banking,

specifically tailored to match your cash flows and needs.

Askari Home Musharakah

Improvement: If you want to renovate your home, let Askari

Islamic Bankingfacilitate you in making you home look even

better.

Askari Home Musharakah

Transfer: Just switch your existing interest based mortgage to

Askari

Islamic Banking by getting advantage of our Askari

HomeMusharakah Transfer Facility, with peace of mind of having

halal transaction.

Features andBenefits: Shariah compliant

Prompt processing.

Competitive rentals.

Clubbing-of family incomeMaximum financing limit: Up to Rs. 50

million.

Financing tenure: 3 to 20 years

Documentation/ legal/ valuation/ income estimation

charges:Atactual.

Eligibility: A Pakistani National.

Earning at least two time more than your monthly Car

Ijarahrentals.

Between 21 to 65 years.A permanent employment with at least six

months of service

with present employer

A self employed individual with at least 3 years of business

track record.Income verification / documents required.

-

8/13/2019 Altaf Internship Report

27/37

5. Alternate Delivery Channels

5.1VISA DEBIT CARD

Features Details

Product Type: Debit Card.

DistinctiveFeatures:

Classic: Cash withdrawal Limit is 50,000, Shopping Limit200,000

& Funds Transfer Limit 250,000.

Gold: Cash withdrawal Limit is 100,000, Shopping Limit250,000

& Funds Transfer Limit 300,000.

Eligibility: 1. Literate individual customer.2. Having Pak Rupee

checking account under the category of

Current, Saving, ASDA, Value Plus Accounts (Current &Saving)

Basic Banking Account and Smart Cash etc., with

credit balance and 'normal' status, may apply.

3. No minimum balance requirements for issuance or retention

of the VISA debit card. An eligible customer may apply for anyof

the debit cards i.e. Classic or Gold.

4. Joint account holders, with the authority to operate

theaccount singly, may be issued supplementary card(s). The

supplementary Card(s) may be issued to only those jointaccount

holders who can operate the account singly with either

or survivor option.5. A customer/staff is allowed to retain as

many cards as

number of accounts and is allowed to link multiple accountswith

single debit card.

6. Multiple accounts of same customer, maintained at

different

-

8/13/2019 Altaf Internship Report

28/37

branches of Askari Bank, may also be linked with single VISA

Debit Card. If the customer has an account with otherbranch(es),

the application receiving branch must verify &

confirm the following either through online system or from

the

concerned branch(es).Validity: Five (05) Years. (New card will

only be issued on customers

written request).Activation/

De-activation: Through our Call Centre by calling at our toll

free number0800-00078.

5.2 INTERNET BANKING SERVICES

Features Details

ImportantFeatures: Payment of Utility Bills

Payment of Mobile PaymentsPurchase of Mobile Air Time

Account Statements

Payments' Details

Online registrationFund transfer to any account within Askari

Bank

Inter-bank fund transfer (IBFT)Askari Master Card details

Askari Master Card bill paymentEmail alerts

Enhanced security

-

8/13/2019 Altaf Internship Report

29/37

5.3Call Center

Askari Bank has been one of the leading banks in the country for

over a number of

years now and has constantly come up with new services for its

valued customers;being one of the first to start ATM and Internet

Banking services. Striving for

further customer satisfaction Askari Bank launched its Call

Centre which becamean efficient and effective medium to put

information at their customer's fingertips.

The Call Center provides a single point of contact for all of

its customers, yet offerunique and individualized services on real

time information for its time-conscious

customers, as it will be available anytime-day or night.

Following are the services available at Call Center:

1. Balance Inquiries, Account Statements ( read out and fax)2.

Complaint handling for all sorts of complaints related to the

bank.

3. Funds transfer from one account to the other.4. Utility Bill

payments for all utility companies listed with the Bank.

Credit Card related queries and information

For further queries please call: 0800-00078Or

Email at: [email protected]

mailto:[email protected]:[email protected]:[email protected]

-

8/13/2019 Altaf Internship Report

30/37

-

8/13/2019 Altaf Internship Report

31/37

Organizational Structure of Branch

-

8/13/2019 Altaf Internship Report

32/37

-

8/13/2019 Altaf Internship Report

33/37

a) CASH DEPARTMENTAll the physical movements of cash in the bank

are made through this department.

Normally cash department performs following functions;

Receipts

Payments

Transfer of funds from one account to another account

Handling of ATM

Posting

Verification of signatures

b)CLEARING DEPARTMENTAll the bank which are the member of

clearing house maintain accounts with State Bank of

Pakistan by debit and credit to which the clearing settlements

are made. If on a particular day, a

bank delivers cheques and other negotiable instruments worth

more than the total amount of

Cheque received by it that banks accounts with State Bank of

Pakistan will be credited with the

differential amount. If on the other hand the total amount of

cheques and other negotiable

instruments draw on a certain bank by other bank is more than

the total amount receivable by it

from other banks, then this banks account will be debited on

that day. The cheque delivered to

the representatives of other banks for clearing are called

outward clearing, whereas cheques

received from the representatives of other banks for payment are

called inward clearing.

c) Remittance DepartmentThe Remittance Department issues drafts,

payment orders, traveler cheques etc.

Remittance means transfer of funds from one place to another

place. Drafts are issued for other

cities while payment orders are issued for within a city

purpose.

d)Lockers DepartmentLockers provide services of safe keeping the

previous object of public. Locker holders pay

annual rent. One key of the locker is kept by the bank other is

given to the client.

e) Credit DepartmentIt provides loans to various clients and has

a major contribution in the bank's profit and assets.

Different types of loans are provided to the clients depending

on their needs and demands. Loan

against property (Saiban Scheme) and Loan against assets

(advance salary) etc is provided. Such

-

8/13/2019 Altaf Internship Report

34/37

loan is given keeping in view the total income as well as salary

being drawn per month by the

applicants.

Structure and Functions of the Accounts / Finance Department

Account Department of any branch of bank is a major department.

It performs all the activities of

accounting in bank. This department is responsible to maintain

the proper record of account

holders and other account of the branch.

Functions of Account Department

The main function of this department is to handle the cash,

record the cash

transaction, summarizes all the bank transaction daily and sends

the report to head

office.a) Branch Credit Committee.

b) Area / Regional Office Credit Committee

c) Head Office Credit Committee.

d) Executive Committee

e) Board of Directors.

Note: Each approved limit (BCC/AOCC/ROCC/HOCC/EC) will be

subject to Risk Asset

Review by Risk Management Division, Head Office, and

Rawalpindi.

Structure of the Finance Department

The finance department at head office reconciles the data

collected from the branches. The uses

this data to prepare the overall position of the banks in terms

of

Prepare Balance sheet

Income Statement

Sources and Uses of Funds

Cash Flow Statement

The department is also responsible to review the policies of

bank in terms of financial matters

and give feedback to policy makers. Their participation in

policy making is encouraged by the

bank management. In order to give suggestion in policy making

the department gathers feedback

from the branch level.

-

8/13/2019 Altaf Internship Report

35/37

The department is also responsible to publish the financial

position of bank in print and

electronic media as per the SBP policy. The information provided

by bank is very important for

investor because they very much rely on this information in

order to invest in the bank. The

depositors also feel secure if the position of bank is

positive.

Income and Expense

The department also needs to calculate the revenues and

expenses, control expenditure and

forecast profits every month.

Budget

Formulation of yearly budgets & targets in consultation with

the branch manager is also done by

the accounts department.

Activity Checking

Daily activity checking and monitoring is done by the accounts

department of the whole bank.

Storage of Records

Accounts Department also has the duty to store vouchers and

system generated reports.

Payments

The accounts department is responsible to pay vendors on behalf

of the bank with authorization

from the branch manager. It also has to amortize large payments

and calculate depreciation of

branch assets.

5.3 The role of financial managers in establishing

relationship

This is a senior role and the Relationship Manager will manage a

portfolio of complex borrowing

corporate clients as well as being the primary point of contact

for the banks relationships with the

Hedge Fund Sector. The role will report to the Head of Corporate

Banking.

The ideal candidate will maximize opportunities to strengthen

and leverage existing relationships

as well as continue to maintain and ensure high levels of

customer satisfaction and retention all

the while generating new recommendations. The successful

candidate will be experienced in

developing growth plans and expanding the divisions borrowing

and non-borrowing

relationships within the hedge fund sector.

-

8/13/2019 Altaf Internship Report

36/37

-

8/13/2019 Altaf Internship Report

37/37

Sources and Uses of Funds

Cash Flow Statement

The department is also responsible to review the policies of

bank in terms of financial matters

and give feedback to policy makers. Their participation in

policy making is encouraged by thebank management. In order to give

suggestion in policy making the department gathers feedback

from the branch level.

The department is also responsible to publish the financial

position of bank in print and

electronic media as per the SBP policy. The information provided

by bank is very important for

investor because they very much rely on this information in

order to invest in the bank. The

depositors also feel secure if the position of bank is

positive.

![[Internship Report] folder... · Web view[Internship Report] [Internship Report] 3 [Internship Report] Prince Mohammed Bin Fahd University College of Computer Engineering and Science](https://img.pdfslide.us/doc/110x75/5adbc5e37f8b9add658e5f6e/internship-report-folderweb-viewinternship-report-internship-report-3-internship.jpg)