Embed Size (px)

DESCRIPTION

AlphaRx Inc.

Citation preview

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 1

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

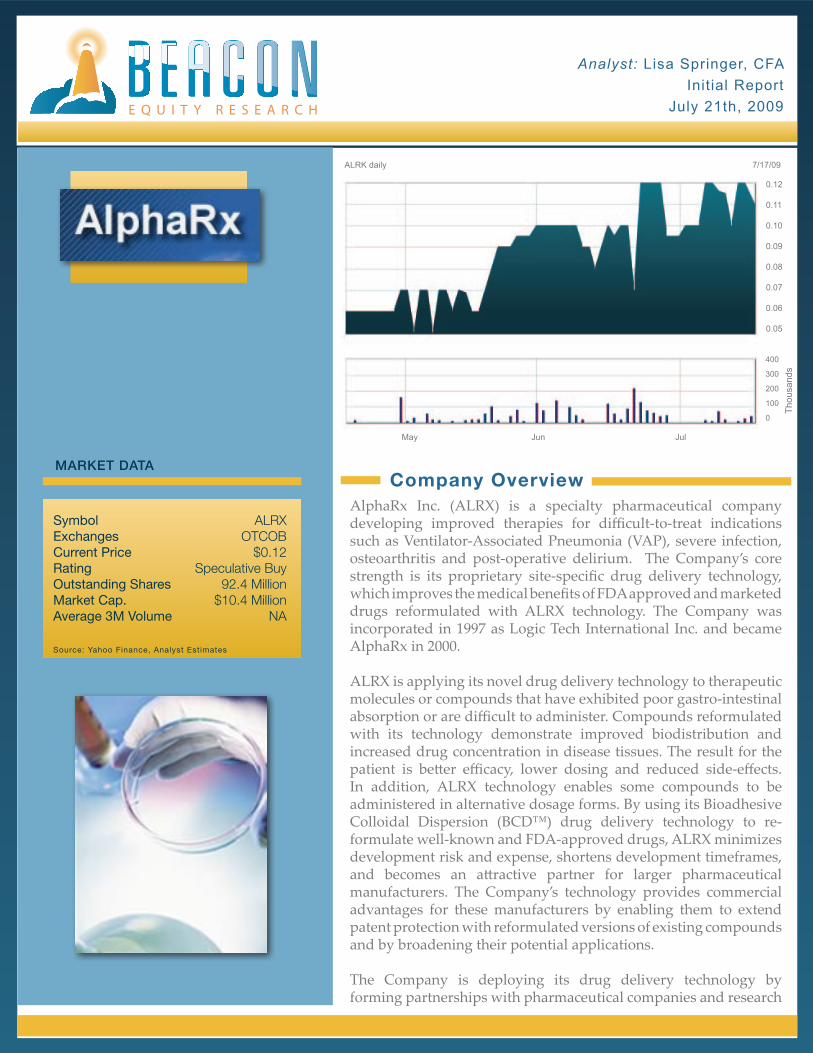

Company Overview MARKET DATA

SymbolExchangesCurrent PriceRatingOutstanding SharesMarket Cap.Average 3M Volume

Source: Yahoo Finance, Analyst Estimates

ALRXOTCOB

$0.12Speculative Buy

92.4 Million$10.4 Million

NA

AlphaRx Inc. (ALRX) is a specialty pharmaceutical company developing improved therapies for difficult-to-treat indications such as Ventilator-Associated Pneumonia (VAP), severe infection, osteoarthritis and post-operative delirium. The Company’s core strength is its proprietary site-specific drug delivery technology, which improves the medical benefits of FDA approved and marketed drugs reformulated with ALRX technology. The Company was incorporated in 1997 as Logic Tech International Inc. and became AlphaRx in 2000.

ALRX is applying its novel drug delivery technology to therapeutic molecules or compounds that have exhibited poor gastro-intestinal absorption or are difficult to administer. Compounds reformulated with its technology demonstrate improved biodistribution and increased drug concentration in disease tissues. The result for the patient is better efficacy, lower dosing and reduced side-effects. In addition, ALRX technology enables some compounds to be administered in alternative dosage forms. By using its Bioadhesive Colloidal Dispersion (BCD™) drug delivery technology to re-formulate well-known and FDA-approved drugs, ALRX minimizes development risk and expense, shortens development timeframes, and becomes an attractive partner for larger pharmaceutical manufacturers. The Company’s technology provides commercial advantages for these manufacturers by enabling them to extend patent protection with reformulated versions of existing compounds and by broadening their potential applications.

The Company is deploying its drug delivery technology by forming partnerships with pharmaceutical companies and research

7/17/09

volume

0.12

0.11

0.10

0.09

0.08

0.07

0.06

0.05

400

300

200

100

0

© BigCharts.com

ALRK daily

May Jun Jul

Thou

sand

s

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 2

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 2

institutions. ALRX has already completed phase II Proof of Concept studies of a topical NSAID targeting osteoarthritis, which it has licensed to Cypress Bioscience, and has six in-house compounds in pre-clinical development that address major market opportunities. In addition, ALRX is already generating modest revenues from formulation services and royalties, has partnerships that could result in milestone payments exceeding $160 million and a multi-million dollar, long-term royalty income stream; it has also begun marketing two OTC products in Hong Kong and an Rx product in Mexico, with three additional OTC products scheduled to launch in Mexico in 2009.

ALRX’s lead product candidate Zysolin™ is a polymeric, nanoparticlulate formulation of the antibiotic Tobramycin, used to treat Cystic Fibrosis and Gram-negative pneumonia in intubated and mechanically ventilated patients. Pneumonia is the second most frequent hospital-acquired infection, with approximately 300,000 cases annually in the U.S., and treatment costs exceeding $1.7 billion. ALRX has completed extensive animal studies of Zysolin™ in acute pneumonia and is ready to commence a low-risk clinical program. The Company is establishing protocols for phase I/II human trials, has secured the services of a GMP manufacturer, and anticipates completing the clinical development program through phase IIb within 24 months. ALRX is also advancing clinical development of GAI-122, an investigational, injectable nano-emulsion that has the potential to prevent post-operative delirium and treat acute hepatitis. About 10%-30% of post-operative patients over the age of 65 develop delirium after surgery. Current treatments for post-operative delirium have serious side-effects. At present, there is no preventive therapy. The worldwide market for an effective chronic hepatitis treatment is a multi-billion dollar opportunity. It is estimated that at least 350 million people worldwide are afflicted with chronic hepatitis B, a potentially life-threatening condition; millions more suffer from hepatitis C. ALRX estimates a potential U.S. market for GAI-122 exceeding $6.0 billion. The Company is conducting pre-IND toxicity studies of GAI-122 for applications in treating post-operative delirium and acute hepatitis. ALRX will receive funding for clinical development from its licensing partner, Gaia BioPharma. In addition, ALRX may receive more than $50 million in milestone payments for GAI-122 as well as royalty income on product sales.

$131 billion drug delivery market

Demand for pharmaceuticals is growing as a result of an aging population in the developed countries, which is increasing the incidence of medical conditions requiring drug therapy. Demand for drug delivery systems (including the value of delivered drugs) in the U.S. has grown 12.4% annually since 2002 to $80.2 billion in 2007. Approximately 28% of pharmaceutical demand reflects medicines adapted to specialized delivery formulations or devices, up from 21.7% in 1997. Demand is forecast to rise 10% annually to $131 billion by 2012. ALRX has compounds in development that address multiple disease indications and estimates that multi-billion market opportunities are available for its high-value drug delivery platform.

Proprietary drug delivery technology

The Company owns a proprietary, site-specific nano drug delivery technology called Bioadhesive Colloidal Dispersion (BCD™), which can be used to improve the efficacy and solubility of well-known and approved drugs. The technology uses site-specific nanoparticles that change the biodistribution of the drug in the human body, therby resulting in superior efficacy, fewer side-effects and lower treatment costs.

Investment Appeals

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 3

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 3

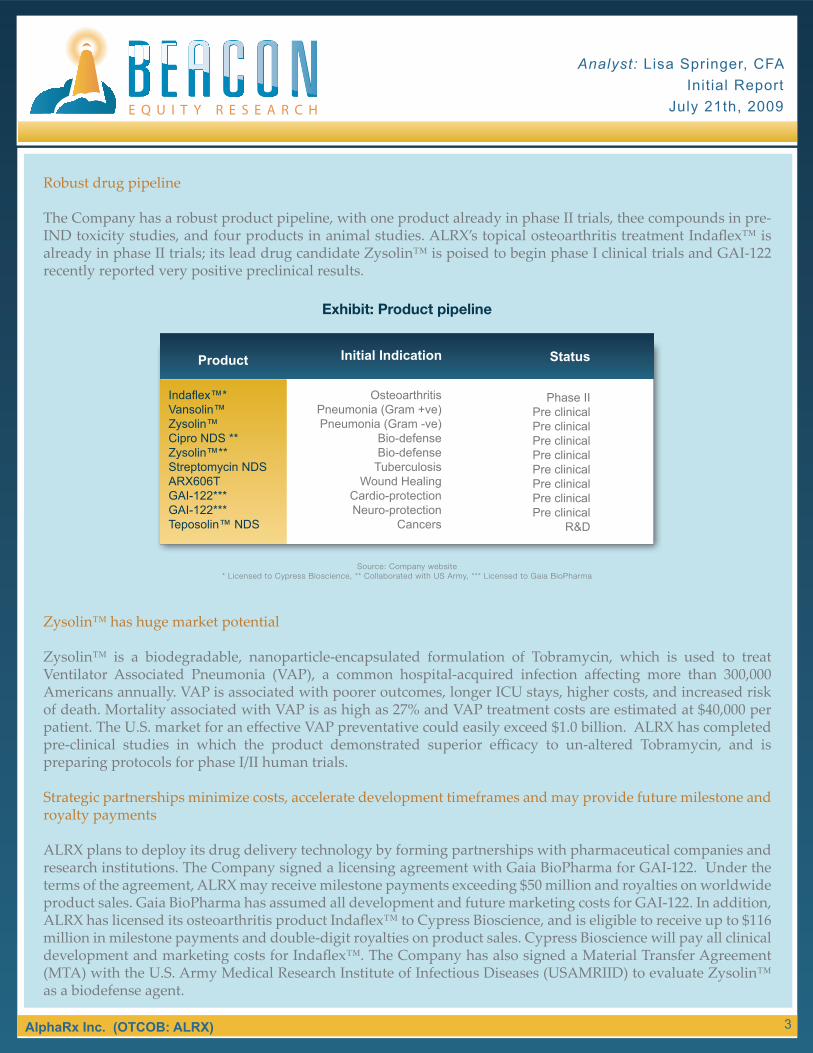

Robust drug pipeline

The Company has a robust product pipeline, with one product already in phase II trials, thee compounds in pre-IND toxicity studies, and four products in animal studies. ALRX’s topical osteoarthritis treatment Indaflex™ is already in phase II trials; its lead drug candidate Zysolin™ is poised to begin phase I clinical trials and GAI-122 recently reported very positive preclinical results.

Zysolin™ has huge market potential

Zysolin™ is a biodegradable, nanoparticle-encapsulated formulation of Tobramycin, which is used to treat Ventilator Associated Pneumonia (VAP), a common hospital-acquired infection affecting more than 300,000 Americans annually. VAP is associated with poorer outcomes, longer ICU stays, higher costs, and increased risk of death. Mortality associated with VAP is as high as 27% and VAP treatment costs are estimated at $40,000 per patient. The U.S. market for an effective VAP preventative could easily exceed $1.0 billion. ALRX has completed pre-clinical studies in which the product demonstrated superior efficacy to un-altered Tobramycin, and is preparing protocols for phase I/II human trials.

Strategic partnerships minimize costs, accelerate development timeframes and may provide future milestone and royalty payments

ALRX plans to deploy its drug delivery technology by forming partnerships with pharmaceutical companies and research institutions. The Company signed a licensing agreement with Gaia BioPharma for GAI-122. Under the terms of the agreement, ALRX may receive milestone payments exceeding $50 million and royalties on worldwide product sales. Gaia BioPharma has assumed all development and future marketing costs for GAI-122. In addition, ALRX has licensed its osteoarthritis product Indaflex™ to Cypress Bioscience, and is eligible to receive up to $116 million in milestone payments and double-digit royalties on product sales. Cypress Bioscience will pay all clinical development and marketing costs for Indaflex™. The Company has also signed a Material Transfer Agreement (MTA) with the U.S. Army Medical Research Institute of Infectious Diseases (USAMRIID) to evaluate Zysolin™ as a biodefense agent.

Indaflex™*Vansolin™Zysolin™Cipro NDS **Zysolin™**Streptomycin NDSARX606TGAI-122***GAI-122***Teposolin™ NDS

OsteoarthritisPneumonia (Gram +ve)Pneumonia (Gram -ve)

Bio-defenseBio-defense

TuberculosisWound Healing

Cardio-protectionNeuro-protection

Cancers

Phase IIPre clinicalPre clinicalPre clinicalPre clinicalPre clinicalPre clinicalPre clinicalPre clinical

R&D

Product Initial Indication Status

Source: Company website* Licensed to Cypress Bioscience, ** Collaborated with US Army, *** Licensed to Gaia BioPharma

Exhibit: Product pipeline

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 4

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 4

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 4

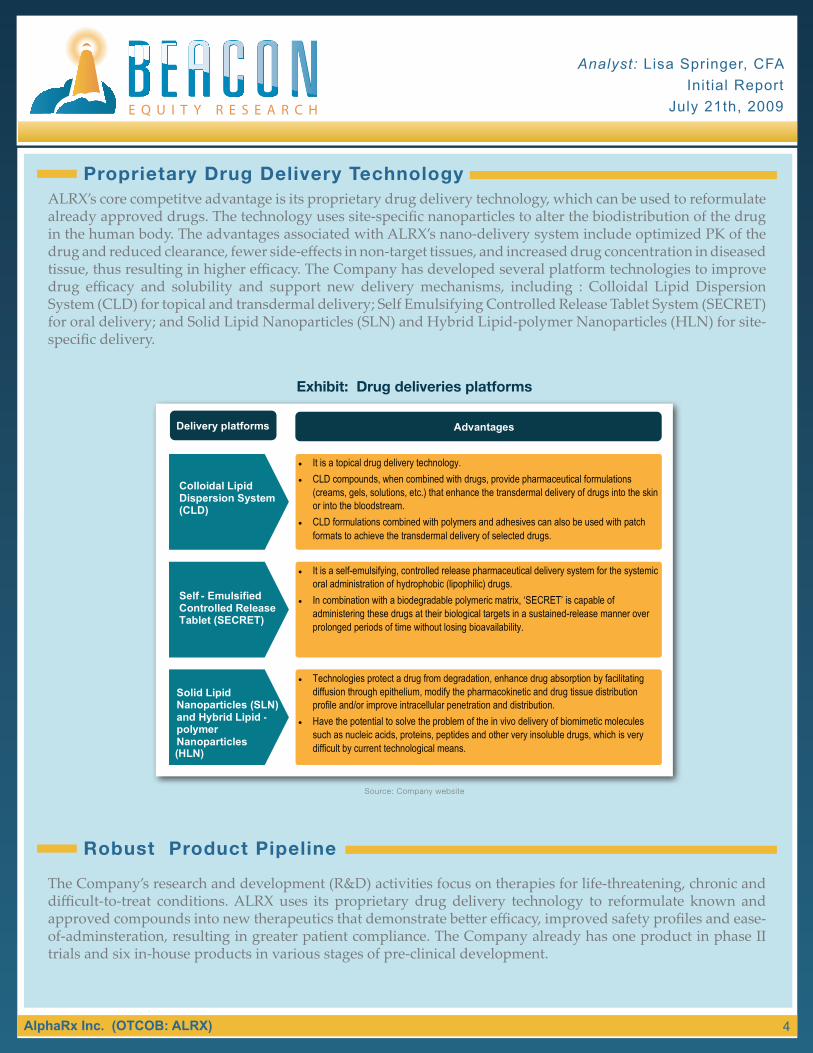

ALRX’s core competitve advantage is its proprietary drug delivery technology, which can be used to reformulate already approved drugs. The technology uses site-specific nanoparticles to alter the biodistribution of the drug in the human body. The advantages associated with ALRX’s nano-delivery system include optimized PK of the drug and reduced clearance, fewer side-effects in non-target tissues, and increased drug concentration in diseased tissue, thus resulting in higher efficacy. The Company has developed several platform technologies to improve drug efficacy and solubility and support new delivery mechanisms, including : Colloidal Lipid Dispersion System (CLD) for topical and transdermal delivery; Self Emulsifying Controlled Release Tablet System (SECRET) for oral delivery; and Solid Lipid Nanoparticles (SLN) and Hybrid Lipid-polymer Nanoparticles (HLN) for site-specific delivery.

The Company’s research and development (R&D) activities focus on therapies for life-threatening, chronic and difficult-to-treat conditions. ALRX uses its proprietary drug delivery technology to reformulate known and approved compounds into new therapeutics that demonstrate better efficacy, improved safety profiles and ease-of-adminsteration, resulting in greater patient compliance. The Company already has one product in phase II trials and six in-house products in various stages of pre-clinical development.

Proprietary Drug Delivery Technology

Robust Product Pipeline

Source: Company website

Exhibit: Drug deliveries platforms

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 5

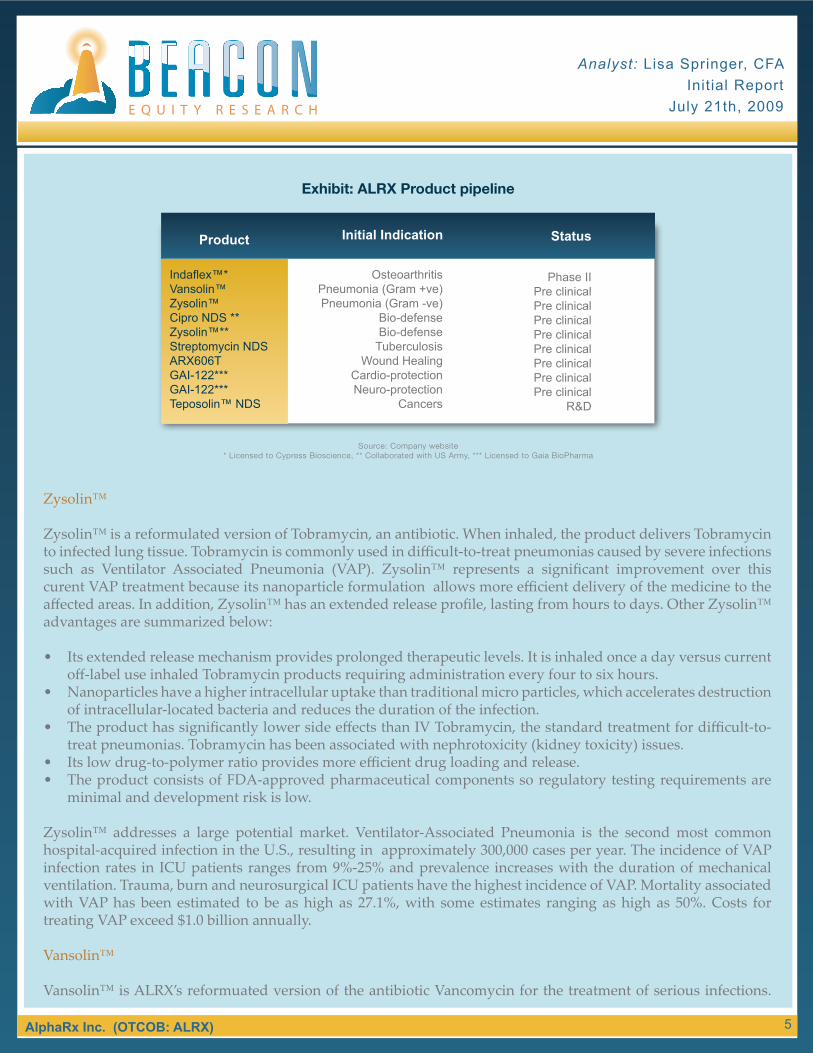

Zysolin™

Zysolin™ is a reformulated version of Tobramycin, an antibiotic. When inhaled, the product delivers Tobramycin to infected lung tissue. Tobramycin is commonly used in difficult-to-treat pneumonias caused by severe infections such as Ventilator Associated Pneumonia (VAP). Zysolin™ represents a significant improvement over this curent VAP treatment because its nanoparticle formulation allows more efficient delivery of the medicine to the affected areas. In addition, Zysolin™ has an extended release profile, lasting from hours to days. Other Zysolin™ advantages are summarized below:

• Its extended release mechanism provides prolonged therapeutic levels. It is inhaled once a day versus current off-label use inhaled Tobramycin products requiring administration every four to six hours.

• Nanoparticles have a higher intracellular uptake than traditional micro particles, which accelerates destruction of intracellular-located bacteria and reduces the duration of the infection.

• The product has significantly lower side effects than IV Tobramycin, the standard treatment for difficult-to-treat pneumonias. Tobramycin has been associated with nephrotoxicity (kidney toxicity) issues.

• Its low drug-to-polymer ratio provides more efficient drug loading and release. • The product consists of FDA-approved pharmaceutical components so regulatory testing requirements are

minimal and development risk is low.

Zysolin™ addresses a large potential market. Ventilator-Associated Pneumonia is the second most common hospital-acquired infection in the U.S., resulting in approximately 300,000 cases per year. The incidence of VAP infection rates in ICU patients ranges from 9%-25% and prevalence increases with the duration of mechanical ventilation. Trauma, burn and neurosurgical ICU patients have the highest incidence of VAP. Mortality associated with VAP has been estimated to be as high as 27.1%, with some estimates ranging as high as 50%. Costs for treating VAP exceed $1.0 billion annually.

Vansolin™

Vansolin™ is ALRX’s reformuated version of the antibiotic Vancomycin for the treatment of serious infections.

Indaflex™*Vansolin™Zysolin™Cipro NDS **Zysolin™**Streptomycin NDSARX606TGAI-122***GAI-122***Teposolin™ NDS

OsteoarthritisPneumonia (Gram +ve)Pneumonia (Gram -ve)

Bio-defenseBio-defense

TuberculosisWound Healing

Cardio-protectionNeuro-protection

Cancers

Phase IIPre clinicalPre clinicalPre clinicalPre clinicalPre clinicalPre clinicalPre clinicalPre clinical

R&D

Product Initial Indication Status

Source: Company website* Licensed to Cypress Bioscience, ** Collaborated with US Army, *** Licensed to Gaia BioPharma

Exhibit: ALRX Product pipeline

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 6

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 6

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 6

Vansolin™ enables site-specific delivery of the drug to infected lung tissue, resulting in improved efficacy (including MRSA- methicillin resistant staphylococcus aureus), lower dosing, and shorter treatment times. The current Vancomycin market is estimated to exceed $1.0 billion annually. ALRX will evaluate results from pre-clinical studies and determine in the second half of 2009 whether it will advance Vansolin™ development to the next stage.

Indaflex™

Indaflex™ is a reformulated verion of a well-known NSAID for the treatment of osteoarthritis. ALRX licensed this product to Proprius Pharma in return for potential milestone payments totaling $116 million, double-digit royalties, and worldwide marketing rights (with the exception of Asia and Mexico). Proprius Pharma will pay all clincial development costs and future marketing costs for this product, which has already advanced to phase II clinical trials. Proprius was recently acquired by publicly-traded Cypress Bioscience.

GAI-122

GAI-122 is an injectible nanoemulsion containing proven safe pharmaceutical ingredients with an excellent safety profile. ALRX is developing GAI-122 as a treatment for acute hepatitis and post-operative delirium. The Company has licensed this compound to Gaia BioPharma, in return for potential milestone payments of up to $50 million and single-digit royalties on product sales. Gaia BioPharma has assumed all clinical development and marketing costs. ALRX notes that this product addresses a $6.0+ billion market and anticipates introducing GAI-122 in the Chinese market for indications in chronic hepatitis over the next three to five years. China was chosen because of that country’s huge population of chronic hepatitis sufferer; 34% of the world’s chronic hepatitis B patients and 24% of the world’s chronic hepatitis C patients live in China. Additional products ALRX is developing include a reformulated version of Streptomycin for TB, Cipro for biodefense, and Teposolin for treating various cancers; these products are all in early pre-clinical stage of development. Antibiotics are the third-largest pharmaceutical market worldwide, generating $35 billion in annually sales, including U.S. sales of $9.0 billion. The global cancer market is forecast to reach $53.1 billion in 2009.

Growing demand for improved drug delivery systems

Rapid technology advancement and pharmaceutical industry demand for delivery systems that can extend the patentable life of drugs nearing their expiration date are key growth drivers in the drug delivery systems market. The pharmaceutical industry (particularly the U.S.) has seen many new drug delivery systems introduced in recent years, including monoclonal antibodies, nanoparticle medicines and drug-eluting stents. Growing competition from generic drugs has prompted the large pharmaceutical companies to help fund the development of new delivery technologies, which can be used to modify formulations of widely prescribed medicines and extend market exclusivity. Between 2002 and 2007, demand for drug delivery systems (including the value of delivered drugs) expanded 12.4% annually to $80.2 billion. By 2007, approximately 28% of pharmaceutical demand was coming from medicines adapted to specialized delivery formulations or devices, up from 21.7% in 1997.

Drug Delivery System Market

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 7

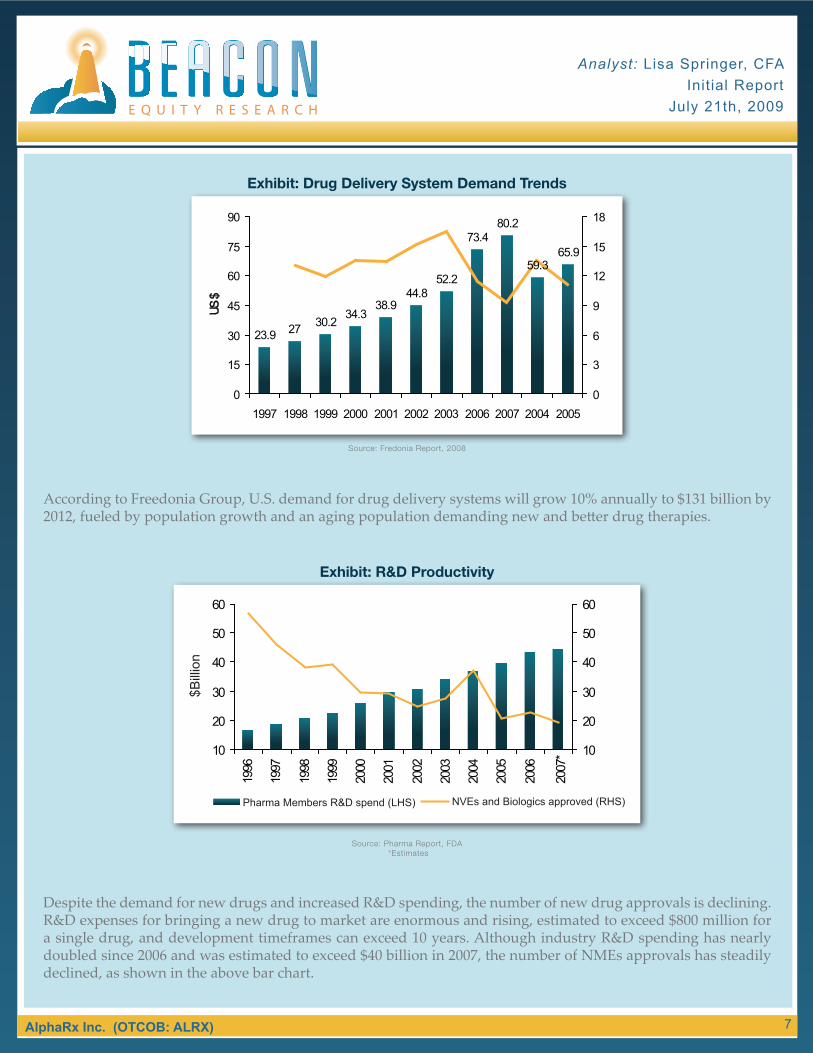

According to Freedonia Group, U.S. demand for drug delivery systems will grow 10% annually to $131 billion by 2012, fueled by population growth and an aging population demanding new and better drug therapies.

Despite the demand for new drugs and increased R&D spending, the number of new drug approvals is declining. R&D expenses for bringing a new drug to market are enormous and rising, estimated to exceed $800 million for a single drug, and development timeframes can exceed 10 years. Although industry R&D spending has nearly doubled since 2006 and was estimated to exceed $40 billion in 2007, the number of NMEs approvals has steadily declined, as shown in the above bar chart.

Source: Fredonia Report, 2008

Exhibit: Drug Delivery System Demand Trends

Source: Pharma Report, FDA *Estimates

Exhibit: R&D Productivity

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 8

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 8

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 8

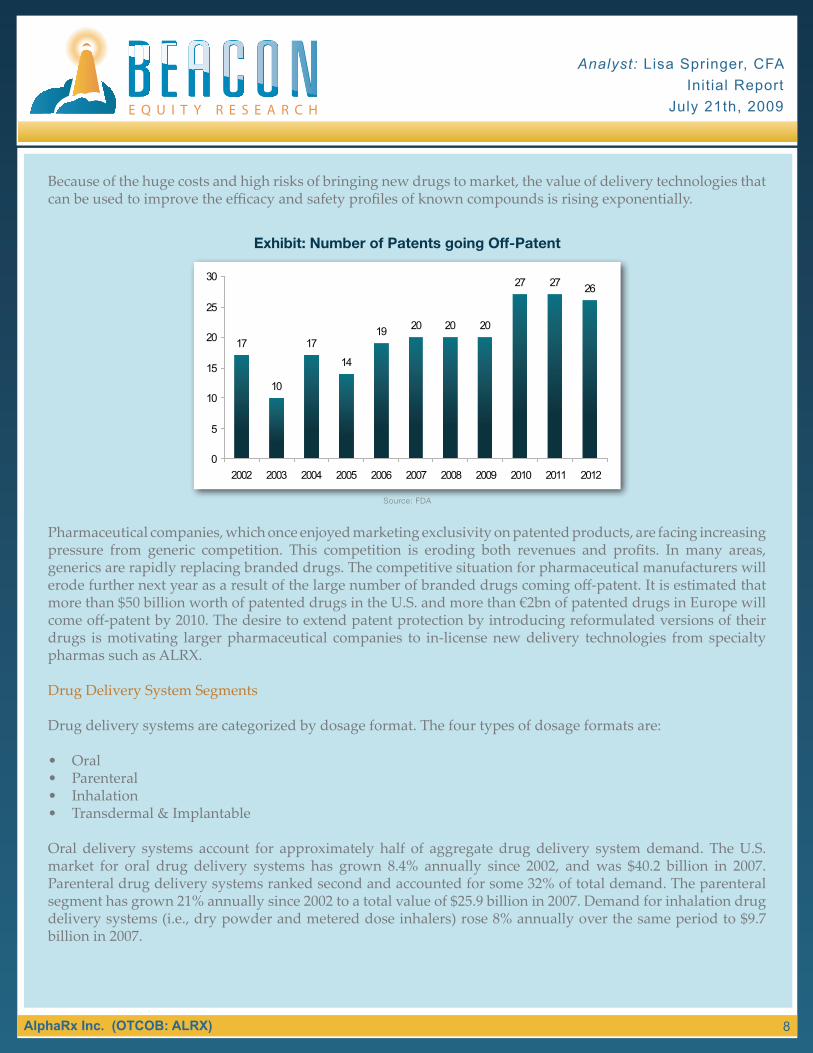

Because of the huge costs and high risks of bringing new drugs to market, the value of delivery technologies that can be used to improve the efficacy and safety profiles of known compounds is rising exponentially.

Pharmaceutical companies, which once enjoyed marketing exclusivity on patented products, are facing increasing pressure from generic competition. This competition is eroding both revenues and profits. In many areas, generics are rapidly replacing branded drugs. The competitive situation for pharmaceutical manufacturers will erode further next year as a result of the large number of branded drugs coming off-patent. It is estimated that more than $50 billion worth of patented drugs in the U.S. and more than €2bn of patented drugs in Europe will come off-patent by 2010. The desire to extend patent protection by introducing reformulated versions of their drugs is motivating larger pharmaceutical companies to in-license new delivery technologies from specialty pharmas such as ALRX.

Drug Delivery System Segments

Drug delivery systems are categorized by dosage format. The four types of dosage formats are:

• Oral• Parenteral• Inhalation• Transdermal & Implantable

Oral delivery systems account for approximately half of aggregate drug delivery system demand. The U.S. market for oral drug delivery systems has grown 8.4% annually since 2002, and was $40.2 billion in 2007. Parenteral drug delivery systems ranked second and accounted for some 32% of total demand. The parenteral segment has grown 21% annually since 2002 to a total value of $25.9 billion in 2007. Demand for inhalation drug delivery systems (i.e., dry powder and metered dose inhalers) rose 8% annually over the same period to $9.7 billion in 2007.

Source: FDA

Exhibit: Number of Patents going Off-Patent

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 9

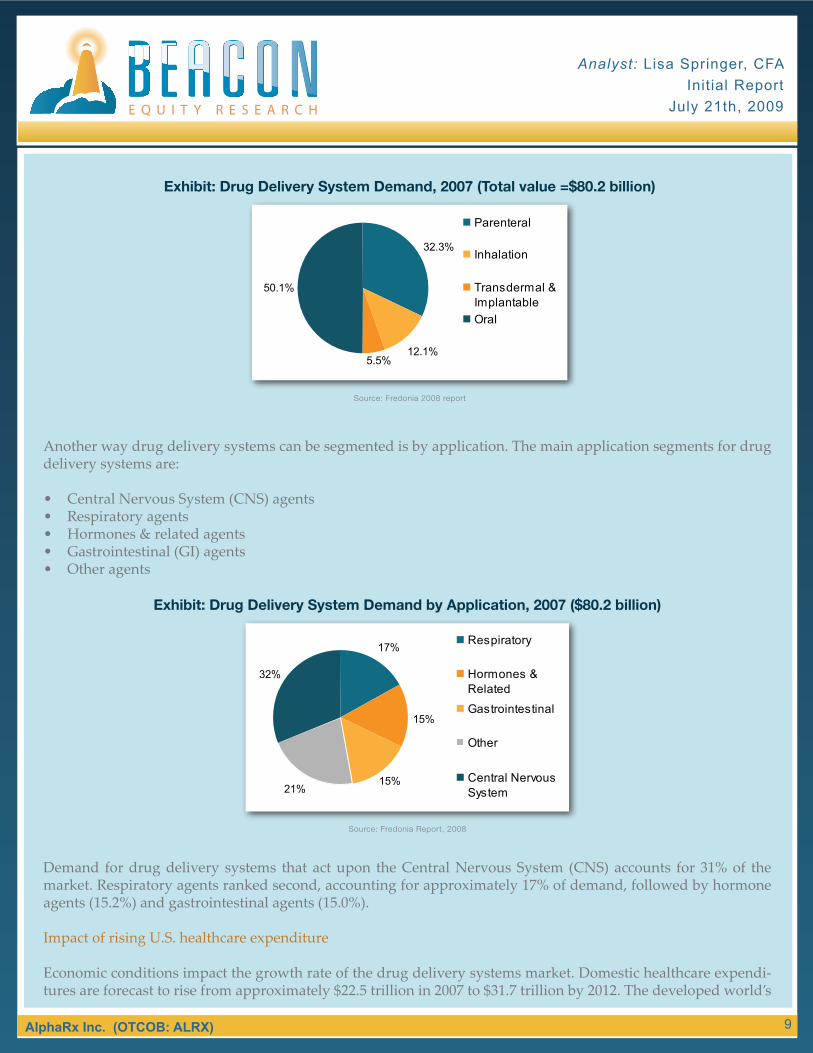

Another way drug delivery systems can be segmented is by application. The main application segments for drug delivery systems are:

• Central Nervous System (CNS) agents• Respiratory agents• Hormones & related agents• Gastrointestinal (GI) agents• Other agents

Demand for drug delivery systems that act upon the Central Nervous System (CNS) accounts for 31% of the market. Respiratory agents ranked second, accounting for approximately 17% of demand, followed by hormone agents (15.2%) and gastrointestinal agents (15.0%).

Impact of rising U.S. healthcare expenditure

Economic conditions impact the growth rate of the drug delivery systems market. Domestic healthcare expendi-tures are forecast to rise from approximately $22.5 trillion in 2007 to $31.7 trillion by 2012. The developed world’s

Source: Fredonia 2008 report

Exhibit: Drug Delivery System Demand, 2007 (Total value =$80.2 billion)

Source: Fredonia Report, 2008

Exhibit: Drug Delivery System Demand by Application, 2007 ($80.2 billion)

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 10

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 10

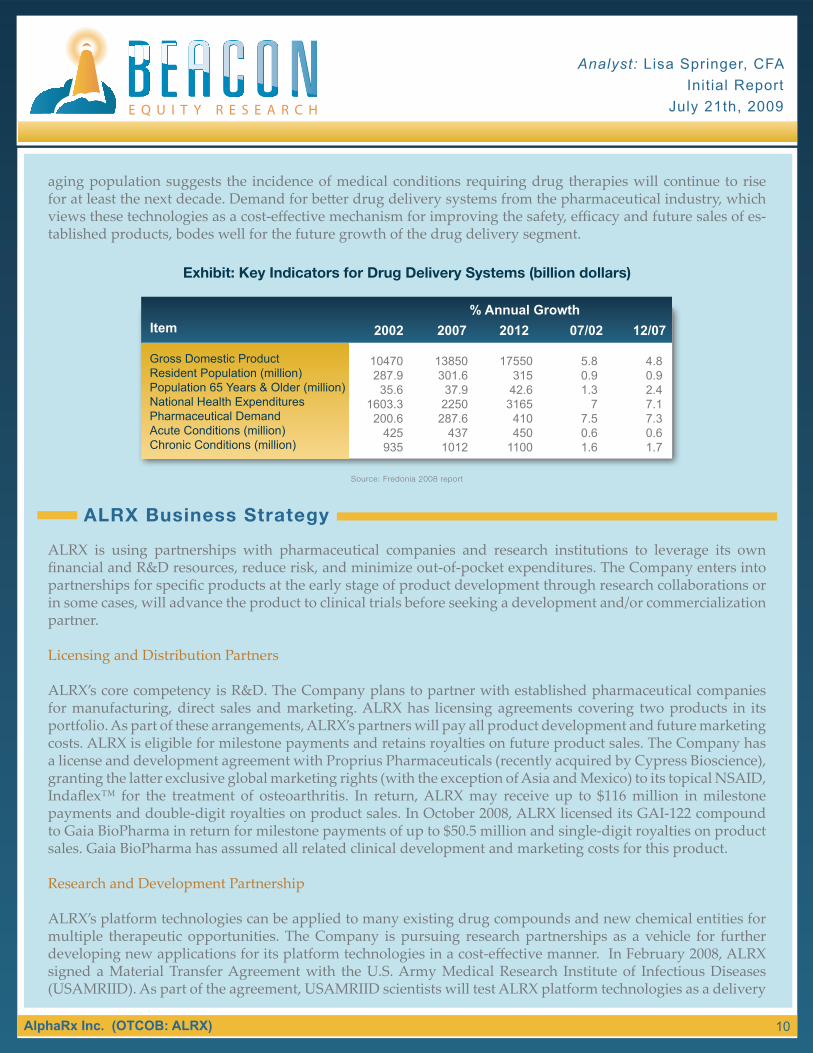

aging population suggests the incidence of medical conditions requiring drug therapies will continue to rise for at least the next decade. Demand for better drug delivery systems from the pharmaceutical industry, which views these technologies as a cost-effective mechanism for improving the safety, efficacy and future sales of es-tablished products, bodes well for the future growth of the drug delivery segment.

ALRX is using partnerships with pharmaceutical companies and research institutions to leverage its own financial and R&D resources, reduce risk, and minimize out-of-pocket expenditures. The Company enters into partnerships for specific products at the early stage of product development through research collaborations or in some cases, will advance the product to clinical trials before seeking a development and/or commercialization partner.

Licensing and Distribution Partners

ALRX’s core competency is R&D. The Company plans to partner with established pharmaceutical companies for manufacturing, direct sales and marketing. ALRX has licensing agreements covering two products in its portfolio. As part of these arrangements, ALRX’s partners will pay all product development and future marketing costs. ALRX is eligible for milestone payments and retains royalties on future product sales. The Company has a license and development agreement with Proprius Pharmaceuticals (recently acquired by Cypress Bioscience), granting the latter exclusive global marketing rights (with the exception of Asia and Mexico) to its topical NSAID, Indaflex™ for the treatment of osteoarthritis. In return, ALRX may receive up to $116 million in milestone payments and double-digit royalties on product sales. In October 2008, ALRX licensed its GAI-122 compound to Gaia BioPharma in return for milestone payments of up to $50.5 million and single-digit royalties on product sales. Gaia BioPharma has assumed all related clinical development and marketing costs for this product.

Research and Development Partnership

ALRX’s platform technologies can be applied to many existing drug compounds and new chemical entities for multiple therapeutic opportunities. The Company is pursuing research partnerships as a vehicle for further developing new applications for its platform technologies in a cost-effective manner. In February 2008, ALRX signed a Material Transfer Agreement with the U.S. Army Medical Research Institute of Infectious Diseases (USAMRIID). As part of the agreement, USAMRIID scientists will test ALRX platform technologies as a delivery

Gross Domestic ProductResident Population (million)Population 65 Years & Older (million)National Health ExpendituresPharmaceutical DemandAcute Conditions (million)Chronic Conditions (million)

10470287.9

35.61603.3

200.6425935

13850301.6

37.92250287.6

4371012

1755031542.6

3165410450

1100

5.80.91.3

77.50.61.6

4.80.92.47.17.30.61.7

Item 2002 2007 2012 07/02 12/07% Annual Growth

Source: Fredonia 2008 report

Exhibit: Key Indicators for Drug Delivery Systems (billion dollars)

ALRX Business Strategy

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 11

mechanism for biodefense agents. Compounds reformulated with ALRX technology will be studied in severe intracellular bacterial infections in animal models.

Competition within the drug delivery systems segment is intense. Several competitors have developed novel oral drug delivery technologies that compete with ALRX’s proprietary platform. The Company’s competitors include large, established players such as Novartis AG and Gilead Sciences, as well as fast-growing start-ups such as Nektar Therapeutics and Paladin Labs. Its small size and proprietary technology could make ALRX an attractive acquisition candidate for a larger pharmaceutical company. The Company’s signed licensing agreements indicate that larger players are already recognizing the value of its technology.

Novartis AG (NVS)

Switzerland-based Novartis AG develops, manufactures and markets medicines, preventive vaccines, diagnostic tools, generic pharmaceuticals and consumer health products. Through a subsidiary, it has well-established operations in the U.S. drug delivery market. Novartis’ TOBI product has been submitted for FDA approval as a treatment for Cystic Fibrosis (CF), and an inhalable Tobramycin formulation is being developed that will compete directly with ALRX’s Zysolin™ product. Novartis recorded revenues of $42.6 billion and operating profits of $8.9 billion last year.

Gilead Sciences Inc. (GLID)

U.S.-based Gilead Sciences develops and commercializes therapeutics in areas of unmet medical need. Gilead’s inhalable Aztreonam lysine product has completed clinical trials but is not yet FDA approved. This product competes with ALRX’s Zysolin™ product. Gilead Sciences generated 2008 revenues of $5.3 billion and operating profits of $2.7 billion.

Nektar Therapeutics (NKTR)

Nektar Therapeutics is developing drug candidates based on its PEGylation and advanced polymer conjugate technologies. Nektar is developing products with applications in oncology, pain management, anti-infectives, anti-viral and immunology. The Company reported revenues of $90.2 million in 2008 and posted a $32.3 million operating loss.

Paladin Labs Inc. (PLB)

Canada-based Paladin Labs developed and markets Metadol, an analgesic for acute cancer pain, palliative care and chronic pain disorders, and Pennsaid, a lotion for the treatment of osteoarthritis. Its Pennsaid product competes with ALRX’s Indaflex™ product. Paladin reported revenues of $82.7 million in fiscal 2008 and earnings before interest, taxes, depreciation and amortization of $29.0 million.

Competitors

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 12

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 12

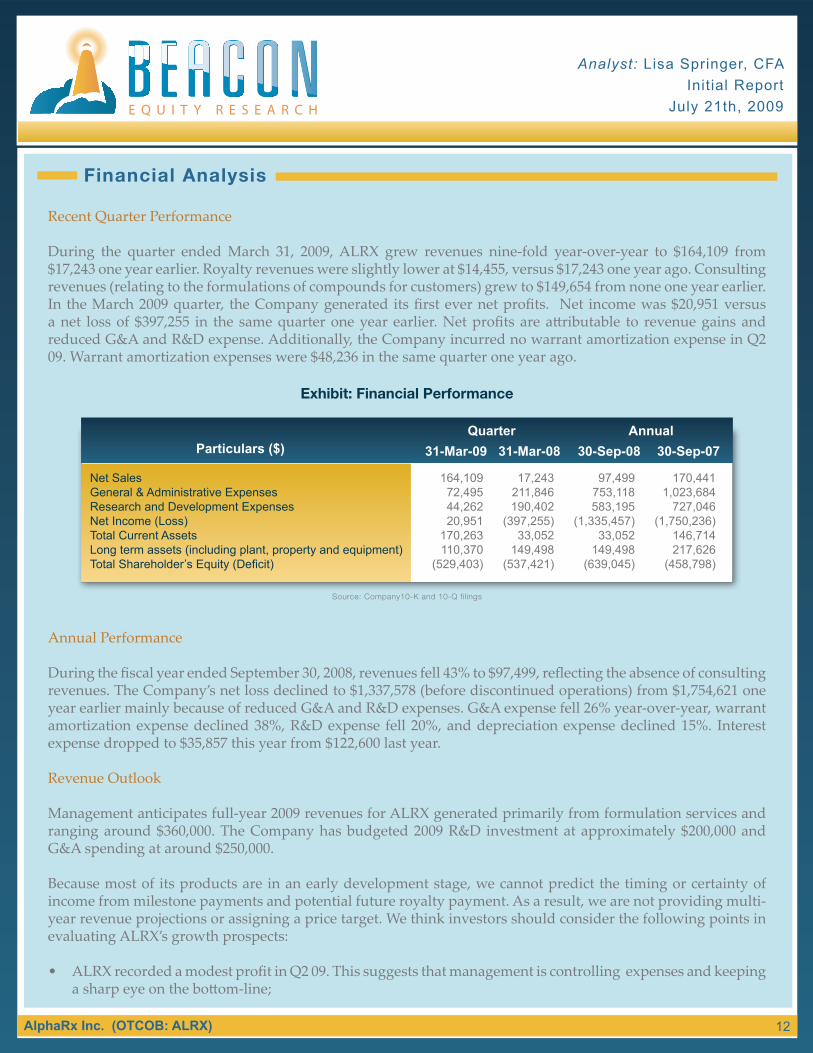

Recent Quarter Performance

During the quarter ended March 31, 2009, ALRX grew revenues nine-fold year-over-year to $164,109 from $17,243 one year earlier. Royalty revenues were slightly lower at $14,455, versus $17,243 one year ago. Consulting revenues (relating to the formulations of compounds for customers) grew to $149,654 from none one year earlier. In the March 2009 quarter, the Company generated its first ever net profits. Net income was $20,951 versus a net loss of $397,255 in the same quarter one year earlier. Net profits are attributable to revenue gains and reduced G&A and R&D expense. Additionally, the Company incurred no warrant amortization expense in Q2 09. Warrant amortization expenses were $48,236 in the same quarter one year ago.

Annual Performance

During the fiscal year ended September 30, 2008, revenues fell 43% to $97,499, reflecting the absence of consulting revenues. The Company’s net loss declined to $1,337,578 (before discontinued operations) from $1,754,621 one year earlier mainly because of reduced G&A and R&D expenses. G&A expense fell 26% year-over-year, warrant amortization expense declined 38%, R&D expense fell 20%, and depreciation expense declined 15%. Interest expense dropped to $35,857 this year from $122,600 last year.

Revenue Outlook

Management anticipates full-year 2009 revenues for ALRX generated primarily from formulation services and ranging around $360,000. The Company has budgeted 2009 R&D investment at approximately $200,000 and G&A spending at around $250,000.

Because most of its products are in an early development stage, we cannot predict the timing or certainty of income from milestone payments and potential future royalty payment. As a result, we are not providing multi-year revenue projections or assigning a price target. We think investors should consider the following points in evaluating ALRX’s growth prospects:

• ALRX recorded a modest profit in Q2 09. This suggests that management is controlling expenses and keeping a sharp eye on the bottom-line;

Financial Analysis

Net SalesGeneral & Administrative ExpensesResearch and Development ExpensesNet Income (Loss)Total Current AssetsLong term assets (including plant, property and equipment)Total Shareholder’s Equity (Deficit)

164,10972,49544,26220,951

170,263110,370

(529,403)

17,243211,846190,402

(397,255)33,052

149,498(537,421)

97,499 753,118 583,195

(1,335,457) 33,052

149,498 (639,045)

170,441 1,023,684

727,046 (1,750,236)

146,714 217,626

(458,798)

Particulars ($) 31-Mar-09 31-Mar-08 30-Sep-08 30-Sep-07Quarter Annual

Source: Company10-K and 10-Q filings

Exhibit: Financial Performance

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 13

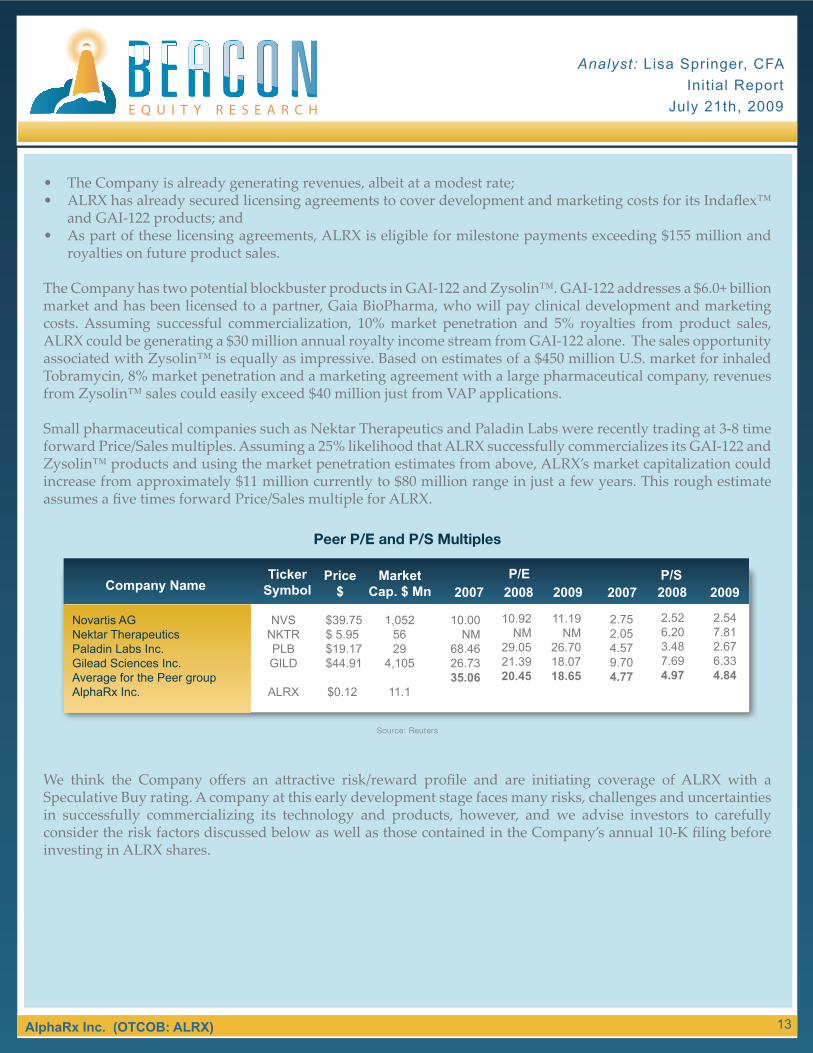

• The Company is already generating revenues, albeit at a modest rate;• ALRX has already secured licensing agreements to cover development and marketing costs for its Indaflex™

and GAI-122 products; and• As part of these licensing agreements, ALRX is eligible for milestone payments exceeding $155 million and

royalties on future product sales.

The Company has two potential blockbuster products in GAI-122 and Zysolin™. GAI-122 addresses a $6.0+ billion market and has been licensed to a partner, Gaia BioPharma, who will pay clinical development and marketing costs. Assuming successful commercialization, 10% market penetration and 5% royalties from product sales, ALRX could be generating a $30 million annual royalty income stream from GAI-122 alone. The sales opportunity associated with Zysolin™ is equally as impressive. Based on estimates of a $450 million U.S. market for inhaled Tobramycin, 8% market penetration and a marketing agreement with a large pharmaceutical company, revenues from Zysolin™ sales could easily exceed $40 million just from VAP applications.

Small pharmaceutical companies such as Nektar Therapeutics and Paladin Labs were recently trading at 3-8 time forward Price/Sales multiples. Assuming a 25% likelihood that ALRX successfully commercializes its GAI-122 and Zysolin™ products and using the market penetration estimates from above, ALRX’s market capitalization could increase from approximately $11 million currently to $80 million range in just a few years. This rough estimate assumes a five times forward Price/Sales multiple for ALRX.

We think the Company offers an attractive risk/reward profile and are initiating coverage of ALRX with a Speculative Buy rating. A company at this early development stage faces many risks, challenges and uncertainties in successfully commercializing its technology and products, however, and we advise investors to carefully consider the risk factors discussed below as well as those contained in the Company’s annual 10-K filing before investing in ALRX shares.

2008

Novartis AGNektar TherapeuticsPaladin Labs Inc.Gilead Sciences Inc.Average for the Peer groupAlphaRx Inc.

NVSNKTRPLBGILD

ALRX

1,0525629

4,105

11.1

$39.75 $ 5.95

$19.17 $44.91

$0.12

10.00 NM

68.46 26.73 35.06

2.75 2.05 4.57 9.70 4.77

10.92 NM

29.05 21.39 20.45

2.52 6.20 3.48 7.69 4.97

11.19 NM

26.70 18.07 18.65

2.54 7.81 2.67 6.33 4.84

Company NamePrice

$ Market

Cap. $ MnP/E P/S Ticker

Symbol 2007 2007 2008 2008 2009 2009

Source: Reuters

Peer P/E and P/S Multiples

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 14

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 14

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 14

History of operating losses

Since its inception through the quarter ended March 31, 2009, ALRX has accumulated a $17.6 million deficit. Although the Company is generating revenues and recorded its first ever net profit last quarter, revenues will likely be modest in 2009. The Company may be years away from achieving milestone payments and royalties on product sales, and there is no guarantee ALRX will ever commercialize any of its development-stage products. The Company is presently generating minimal revenues from formulation services and royalties on its Indaflex™ product, which is being marketed in Mexico through a collaborative partnership with Industria Farmaceutica Andromaco, S.A. de C.V.

Need for additional financing

The Company has minimal capital resources and a working capita deficit. To advance its products through the pipeline, ALRX must secure additional licensing arrangements and significant additional financing. Since its inception, the Company has raised approximately $15 million in capital. There is no guarantee that the Company will be able to secure new licensing agreements or raise additional capital in the future on favorable terms, if at all. ALRX may be forced to delay or even abandon clinical development of some of its products if it failures to secure partners and/or additional funding.

FDA regulatory requirements

The clinical development of therapeutics has inherent clinical and regulatory risks. Of the thousands of new compounds developed each year, only a handful will advance into clinical trials, and only a tiny percentage of those will eventually secure FDA marketing approval. ALRX attempts to minimize development risk by reformulating well-known or approved drugs. Changes in FDA and European Union regulatory requirements, however, could increase the Company’s drug development costs and make its business unprofitable.

Generic competition

Some of the Company’s products compete with from lower cost generics. The over-the-counter healthcare market is characterized by frequent introductions of new products, including the migration of prescription drugs to the OTC market, often accompanied by costly advertising and promotional campaigns. In some product areas, ALRX may find it difficult to compete with larger competitors who can support their products with greater financial and marketing resources.

Reliance on partners for funding, manufacturing and marketing

The Company is highly dependent on funding from its collaborative partners for product development. Additionally, ALRX has no manufacturing or marketing capabilities and no plans to establish the necessary infrastructure.

Risk Factors

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 15

Prior to joining AlphaRx, Mr. Urbanc served as CFO of Oasis Technology Ltd. and Nelson Vending Tech-nology. He also held senior positions at Household Financial Corporation and Arthur Andersen. Mr. Ur-banc is a Chartered Accountant and holds business degrees from York University.

Marcel UrbancChief Financial Officer

Dr. Schwarz has extensive R&D experience in the area of controlled release drug delivery systems. His expertise includes colloidal and microcorpusculate drug delivery systems, submicron emulsions (SME) and transdermal delivery (topical and systemic). He has worked with some of the world’s leading research companies, including D-Pharma, Teva Pharmaceutical Industries, and the Biotechnology Research Insti-tute (Russia). Dr. Schwarz graduated from Tomsk State University in Russia, and completed his Ph.D. thesis on ‘Synthesis and properties of alpha-C-nitrogydrazones’ in 1980. He has published more than 40 articles in various scientific journals, and has more than 20 patents and patent applications.

Joseph SchwarzChief Scientist

Prior to joining AlphaRx, Dr. Weisspapir held a variety of research positions at the University of Tel Aviv and Rabin Medical Center in Israel, and the University Health Network at the University of Toronto. Dr. Weisspapir has extensive experience in interdisciplinary research and development in the areas of experi-mental pharmacology, immunopharmacology, toxicology, neuroscience, cancer research, radiobiology and radiotoxicology. His articles have been published in more than 20 leading scientific publications. He is a graduate of Chelyabinsk State Medical Institute in Russia, and completed his Ph.D. thesis on ‘Immuno-pharmacology of Mercaptobenzimidazole’ in 1985.

Michael WeisspapirChief Medical Officer

Management Team

Mr. Lee is ALRX’s founder, president and CEO. He has more than 15 years experience in the areas of high-tech development, marketing and corporate finance. He holds a Bachelor of Science in applied mathematics from the University of Western Ontario.

Michael LeePresident & Chief Executive Officer

Analyst: Lisa Springer, CFAInitial Report

July 21th, 2009

AlphaRx Inc. (OTCOB: ALRX) 16

Disclaimer

DO NOT BASE ANY INVESTMENT DECISION UPON ANY MATERIALS FOUND ON THIS REPORT. We are not registered as a securities broker-dealer or an investment adviser either with the U.S. Securities and Exchange Commission (the “SEC”) or with any state securities regulatory authority. We are neither licensed nor qualified to provide investment advice.

The information contained in our report should be viewed as commercial advertisement and is not intended to be investment advice. The report is not provided to any particular individual with a view toward their individual circumstances. The information contained in our report is not an offer to buy or sell securities. We distribute opinions, comments and information free of charge exclusively to individuals who wish to receive them.

Our newsletter and website have been prepared for informational purposes only and are not intended to be used as a complete source of information on any particular company. An individual should never invest in the securities of any of the companies profiled based solely on information contained in our report. Individuals should assume that all information contained in the report about profiled companies is not trustworthy unless verified by their own independent research.

Any individual who chooses to invest in any securities should do so with caution. Investing in securities is speculative and carries a high degree of risk; you may lose some or all of the money that is invested. Always research your own investments and consult with a registered investment advisor or licensed stock broker before investing.

The report is a service of BlueWave Advisors, LLC, a financial public relations firm that has been compensated by the companies profiled. All direct and third party compensation received has been disclosed within each individual profile in accordance with section 17(b) of the Securities Act of 1933. This compensa-tion constitutes a conflict of interest as to our ability to remain objective in our communication regarding the profiled companies. BlueWave Advisors, LLC, and/or its affiliated will hold, buy, and sell securities in the companies profiled. When compensated in shares, all readers should be aware that is our policy to liquidate all shares immediately. We reserve the right to buy or sell the shares of any the companies mentioned in any materials we produce at any time. This compensation constitutes a conflict of interest as to our ability to remain objective in our communication regarding the profiled companies. BeaconEquity is a Web site wholly owned by BlueWave Advisors, which has been compensated twenty five thousand dollars directly from ALRX as a marketing budget to man-age a comprehensive investor awareness program including the creation and distribution of this report as well as other investor relations efforts.

Information contained in our report will contain “forward looking statements” as defined under Section 27A of the Securities Act of 1933 and Section 21B of the Securities Exchange Act of 1934. Subscribers are cautioned not to place undue reliance upon these forward looking statements. These forward looking state-ments are subject to a number of known and unknown risks and uncertainties outside of our control that could cause actual operations or results to differ ma-terially from those anticipated. Factors that could affect performance include, but are not limited to, those factors that are discussed in each profiled company’s most recent reports or registration statements filed with the SEC. You should consider these factors in evaluating the forward looking statements included in the report and not place undue reliance upon such statements.

We are committed to providing factual information on the companies that are profiled. However, we do not provide any assurance as to the accuracy or com-pleteness of the information provided, including information regarding a profiled company’s plans or ability to effect any planned or proposed actions. We have no first-hand knowledge of any profiled company’s operations and therefore cannot comment on their capabilities, intent, resources, nor experience and we make no attempt to do so. Statistical information, dollar amounts, and market size data was provided by the subject company and related sources which we believe to be reliable.

To the fullest extent of the law, we will not be liable to any person or entity for the quality, accuracy, completeness, reliability, or timeliness of the information provided in the report, or for any direct, indirect, consequential, incidental, special or punitive damages that may arise out of the use of information we provide to any person or entity (including, but not limited to, lost profits, loss of opportunities, trading losses, and damages that may result from any inaccuracy or incompleteness of this information).

We encourage you to invest carefully and read investment information available at the websites of the SEC at http://www.sec.gov and FINRA at http://www.finra.org.

All decisions are made solely by the analyst and independent of outside parties or influence.

I, Lisa Springer, CFA, the author of this report, certify that the material and views presented herein represent my personal opinion regarding the content and se-curities included in this report. In no way has my opinion been influenced by outside parties, nor has my compensation been either directly or indirectly tied to the performance of any security listed. I certify that I do not currently own, nor will own and shares or securities in any of the companies featured in this report.

Lisa Springer, MBA, CFA - Senior Analyst Lisa serves Beacon Research Partners as a research analyst. She brings to the company over 15 years experience in equity research and investment marketing. Prior to joining Beacon, Lisa worked as an equity analyst for an independent research provider. She has also held positions as investor relations officer for a NYSE-listed company and director of financial analysis for a large consulting firm. Lisa earned an MBA from the University of Chicago and is a Chartered Financial Analyst (CFA).

![CSC231 - Assembly€¦ · inc reg32 inc mem8 inc mem16 inc mem32 alpha db 3 beta dw 4 x dd 0 inc al inc cx inc ebx inc word[beta] ;beta](https://img.pdfslide.us/doc/110x75/5f9dc2880a2ac3769365ee04/csc231-inc-reg32-inc-mem8-inc-mem16-inc-mem32-alpha-db-3-beta-dw-4-x-dd-0-inc.jpg)