Embed Size (px)

Citation preview

Allocation & ApportionmentTx 8300

Learning Objectives

1. Explain the __________ of allocation and apportionment rules,

2. Apply _______ allocation and apportionment rules,

3. Apportion _________ deductions, and

4. Apportion ____ deductions

You should be able to:

Purpose of Apportionment

• ____ taxpayers claim the foreign tax credit for foreign ______ tax paid or accrued.

• However, the FTC is limited to the following result:

Purpose: FTC Example

Domco earns $____ U.S. taxable income and $____ foreign taxable income. The U.S. and foreign tax rates are 35% and ___%, respectively. What is Domco’s foreign tax credit?

Purpose of Apportionment

• The U.S. taxes foreign persons on two categories of income:– Effectively _________ income– U.S. ______ investment income

Initial Remarks

• Sourcing income– Identify ____ of income– Apply appropriate source rule

• Allocating and apportioning deductions– Allocate deductions to _____ income ________– Apportion deductions to FSI or USSI

• Most rules appear in Reg. §1.861-__ to -__.

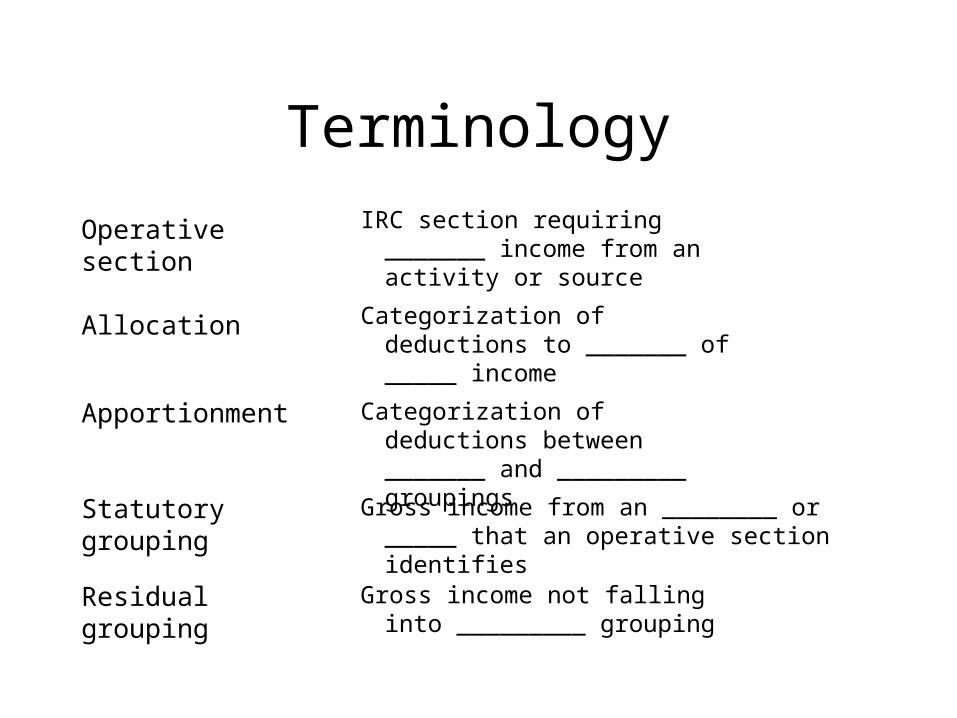

Terminology

Operative section IRC section requiring _______ income from an activity or source

Allocation

Apportionment

Statutory grouping

Categorization of deductions to _______ of _____ income

Categorization of deductions between _______ and _________ groupings

Gross income from an ________ or _____ that an operative section identifies

Residual grouping Gross income not falling into _________ grouping

Allocation Rules

• Allocate deductions to gross income classes when they _________ ______

• Allocate deductions to ___ gross income classes when they definitely ______

• Do not allocate deductions _________ to any gross income class

• Do not ________ personal and dependency exemptions

Allocation: U.S. Person

Domco sells and leases construction equipment, deriving $500 gross profit from sales and $300 rental income. It incurs the following deductions:

Sales commissions

Rental expensesAdministrative expenses

How should Domco allocate these deductions?

Gross Profitfrom Sales

Sales commissions

Rental deductions

Administrative deductions

Rental Income

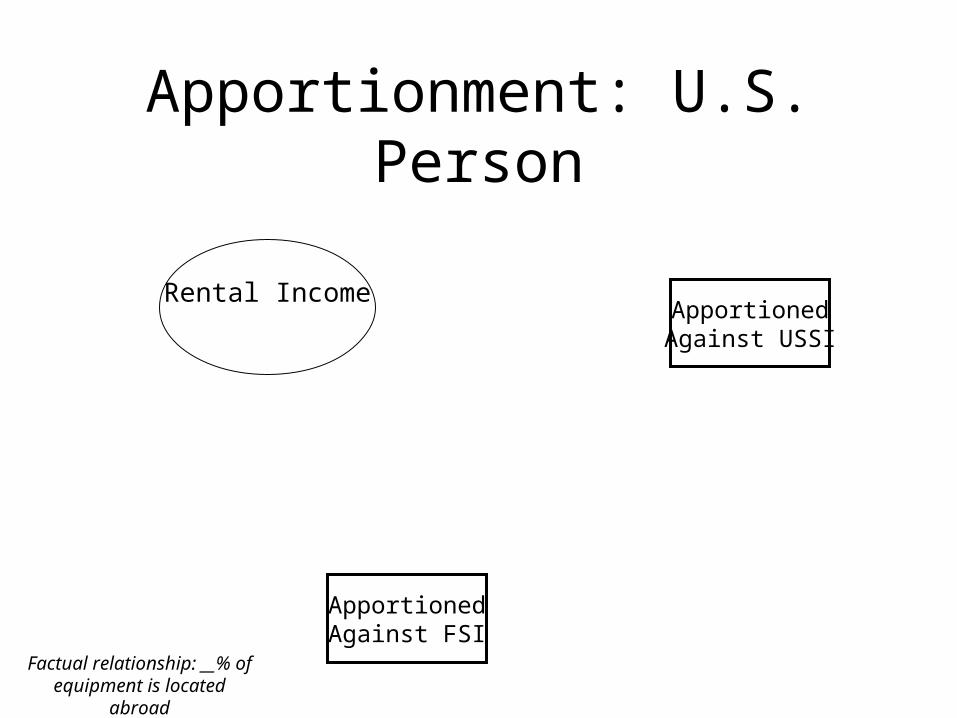

Allocation: U.S. Person

Apportionment Rules

• When deductions definitely relate to one or more gross income classes, apportion based on _______ relationship

• When deductions do not definitely relate to gross income classes, apportion based on _____ income

• Do not _________ personal and dependency exemptions

Assume that ___% of Domco’s sales occur abroad and apportion sales deduction on this basis.

Assume that ___% of Domco’s rental equipment is located abroad and apportion rental deductions on this basis.

Gross Profitfrom Sales

Rental Income

Apportionment: U.S. Person

Gross Profitfrom Sales

ApportionedAgainst FSI

ApportionedAgainst USSI

Apportionment: U.S. Person

Factual relationship: __% of sales occur abroad

ApportionedAgainst FSI

ApportionedAgainst USSI

Rental Income

Apportionment: U.S. Person

Factual relationship: __% of equipment is located abroad

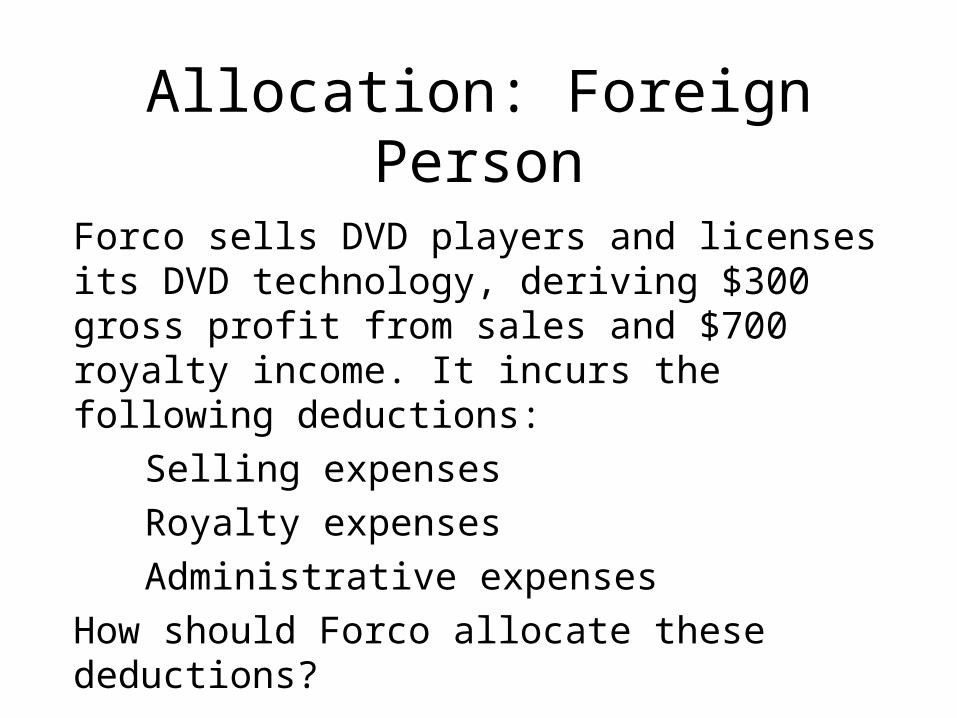

Allocation: Foreign Person

Forco sells DVD players and licenses its DVD technology, deriving $300 gross profit from sales and $700 royalty income. It incurs the following deductions:

Selling expenses

Royalty expenses

Administrative expenses

How should Forco allocate these deductions?

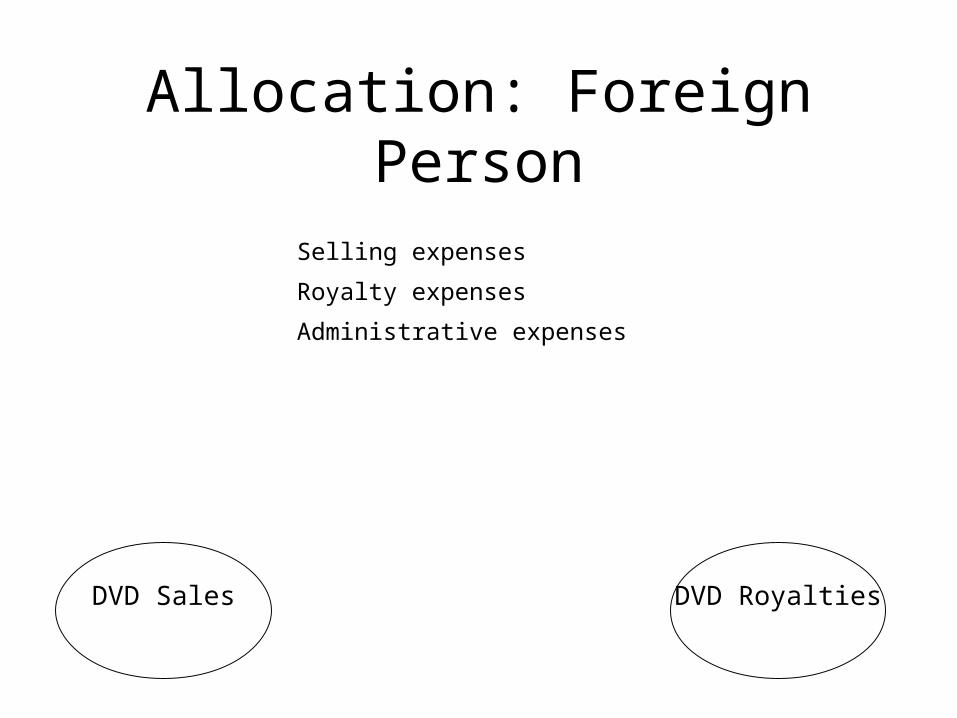

DVD Sales

Selling expenses

Royalty expenses

Administrative expenses

DVD Royalties

Allocation: Foreign Person

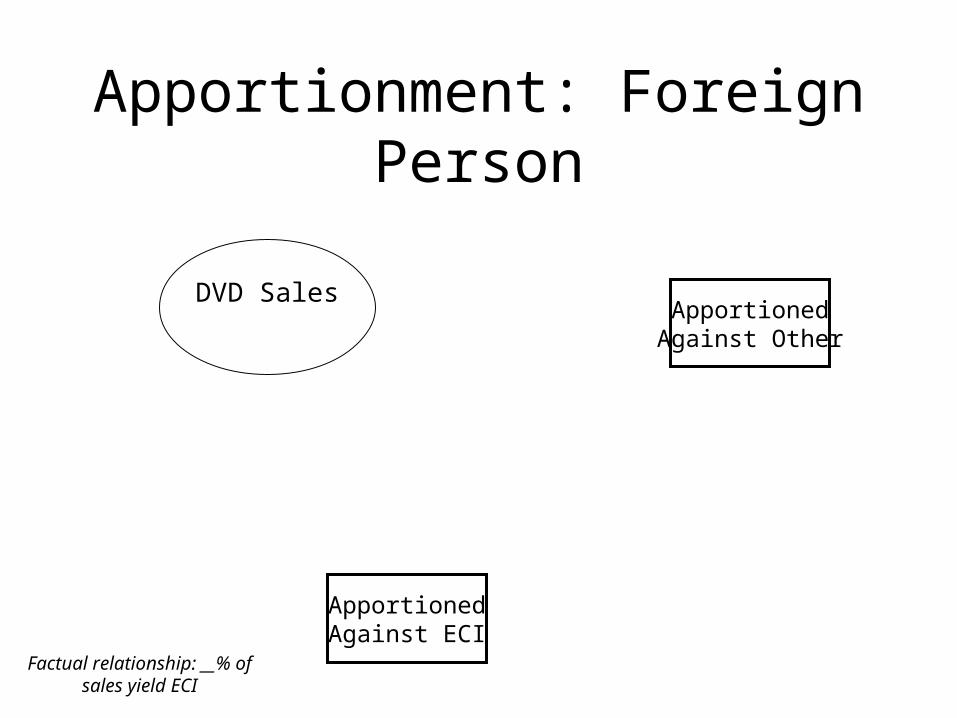

• Assume that 40% of Forco’s sales result in ECI and apportion selling expenses on this basis.

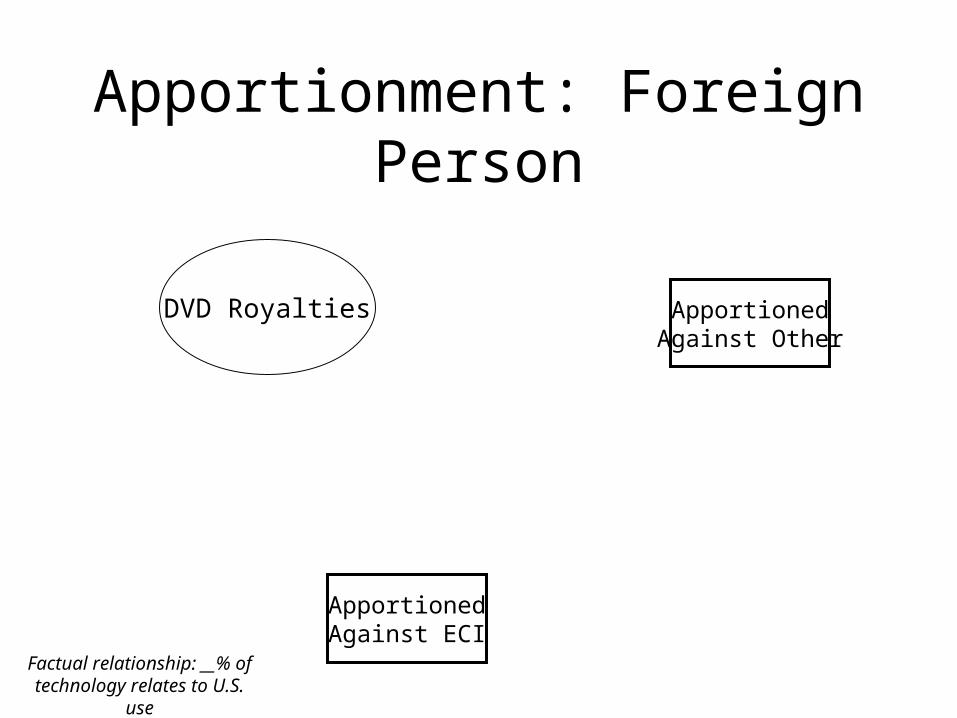

• Assume that Forco licenses 20% of its technology for U.S. use and apportion royalty deductions on this basis.

DVD Sales DVD Royalties

Apportionment: Foreign Person

DVD Sales

ApportionedAgainst ECI

ApportionedAgainst Other

Apportionment: Foreign Person

Factual relationship: __% of sales yield ECI

ApportionedAgainst ECI

ApportionedAgainst Other

DVD Royalties

Apportionment: Foreign Person

Factual relationship: __% of technology relates to U.S. use

Special Rules for Interest

• Procedures differ for U.S. and foreign persons

• Rules based on money’s _________ nature

• Cannot apportion based on gross income

• Must apportion based on _______

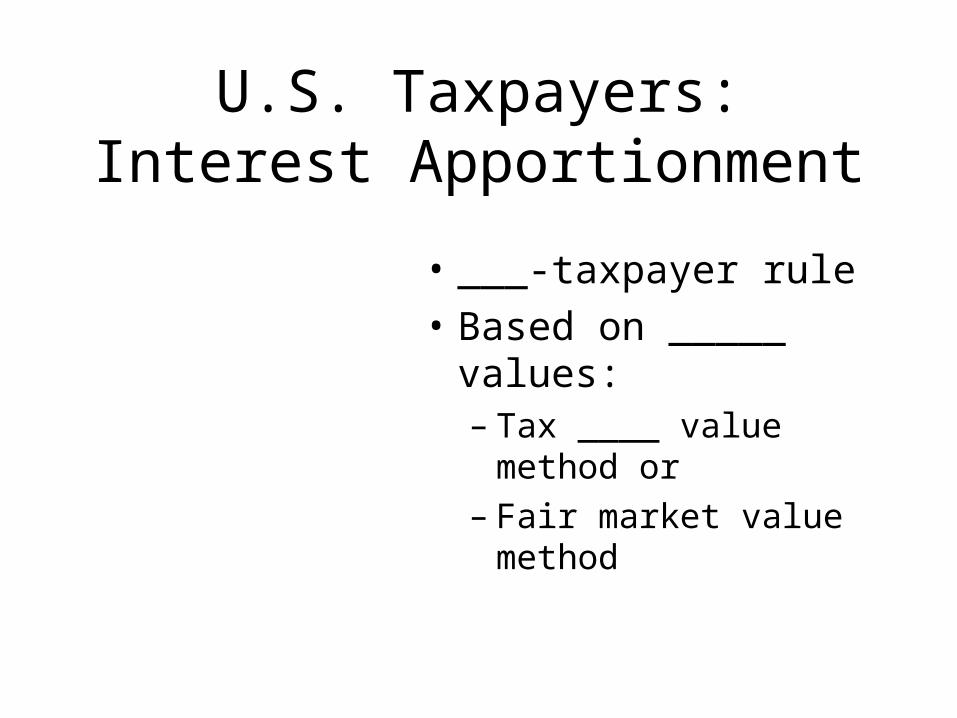

U.S. Taxpayers: Interest Apportionment

• ___-taxpayer rule

• Based on _____ values:– Tax ____ value method or– Fair market value method

Apportionment: Example

Domco incurs $__ interest expense, and its foreign subsidiary incurs $__. Apportion interest based on the following asset values:

U.S. Assets Foreign Assets

Domco $200 $100

Foreign sub 0 120

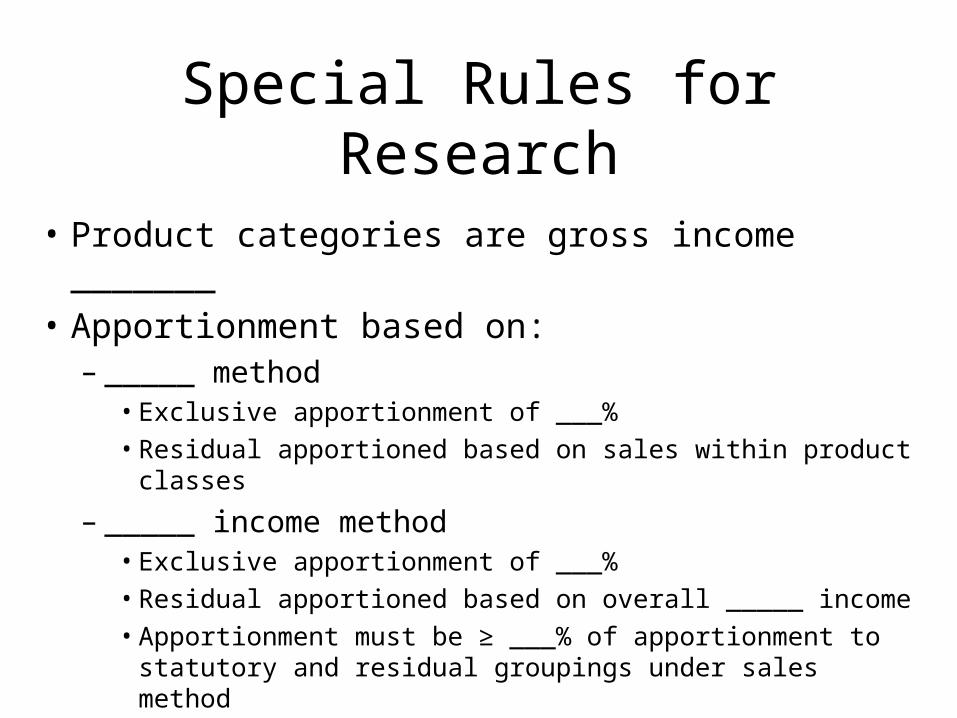

Special Rules for Research

• Product categories are gross income _______

• Apportionment based on:– _____ method

• Exclusive apportionment of ___%

• Residual apportioned based on sales within product classes

– _____ income method• Exclusive apportionment of ___%

• Residual apportioned based on overall _____ income

• Apportionment must be ≥ ___% of apportionment to statutory and residual groupings under sales method

Apportioning R&E: Example

Domco conducts research in Phoenix for products X and Y. Its R&E deduction is $400, ___% attributable to Product Y. Apportion R&E for Product X based on the information below:

U.S. Sales Foreign Sales

Product X 70% 30%

Allocation

Product X

Product Y

Product X Apportionment via Sales Method

USSI

FSI

Apportioning R&E: Example

Domco conducts research in Phoenix for products X and Y. Its R&E deduction is $400, ___% attributable to Product Y. Apportion R&E for Product Y based on the information below:

U.S. Sales Foreign Sales

Product Y 60% 40%

Allocation

Product X

Product Y

Product Y Apportionment via Sales Method

USSI

FSI

Apportioning R&E: Example

Domco conducts research in Phoenix for products X and Y. Its R&E deduction is $400, ___% attributable to Product Y. Apportion R&E using the gross income method. Assume that ___% of Domco’s gross income is from U.S. sources.

Gross Income Method Apportionment

USSI

FSI

Sales Method Apportionment

USSI

FSI R&E deduction