Embed Size (px)

Citation preview

Allianz Global Corporate & Specialty AGAnnual Report 2012

Allianz Global Corporate & Specialty

2012

Allianz ö

Foreword 3

AGCS Global Structure 4

AGCS Global by Line of Business 5

Supervisory Board, Board of Management 6

Report of the Supervisory Board 7

Management Report 8

Annual Financial Statements 21

Balance Sheet 22

Income Statement 24

Notes to the Financial Statements 26

Auditor’s Report 44

Supplementary information to the Management Report 45

Advisory council 46

Important addresses 47

2

Contents

Contents

3

Foreword

For the global economy, 2012 was a year of stagnation:The sovereign debt crisis continued to hold the Eurozone tightly in its grasp, most regions and sectorsrecorded weak growth at best, and capital markets sawno end in sight for low interest rates. In this challengingenvironment, Allianz Global Corporate & Specialty(AGCS) was able to draw on its previous success againin the seventh year of its existence.

We pressed forward on our growth path and cleared animportant symbolic hurdle last year: AGCS companiesworldwide – into which Allianz Risk Transfer has nowbeen fully integrated – generated more than € 5 billionin premium income for the first time. Totaling € 5.314billion, the premium volume increased by almost € 400million over last year. But natural disasters like HurricaneSandy, which hit the eastern coast of the United Statesin October, as well as a few major industrial losses lefttheir marks, and the combined ratio rose to 96 percent.Nevertheless, AGCS managed to produce an operatingprofit of € 420 million.

Despite the ongoing financial market crisis, AGCS wasable to reaffirm its financially sound position. Our verycompetitive ratings demonstrate the strength of ourcapital base. Thanks to our long-term, broadly diversifiedinvestment strategy, we were able to generate a totalinvestment result of € 387 million.

We continue to generate most of our premium incomein our key markets in Europe and the United States.They will also represent an important pillar of ourbusiness in the future. At the same time, it is our statedgoal to continue the geographic diversification of ourportfolio: By 2015, one-third of our premium income isto come from emerging economies in Asia, SouthAmerica, Africa and Eastern Europe.

We made huge strides toward this ambitious goal in2012: Our new branches in Hong Kong and Singaporebegan operations. We established a special team forindustrial risks within Allianz Russia. We startedbundling our activities in South Africa and the Sub-

Saharan region with a new regional headquarters inJohannesburg. And at the end of the year, we receivedapproval to operate a local reinsurance company inBrazil: AGCS Brazil opened in two new locations, one inRio de Janeiro and one in Sao Paulo. The company willbecome the hub of our expansion in South America overthe mid term.

Though local business practices may vary from countryto country, we globally apply our principle of profitablegrowth to build a sustainable long term business. Wefocus on disciplined underwriting and prudent costmanagement. In addition, we want to increasingly focuson those industry segments that appreciate ourparticular strengths: a distinct global network, profoundexpertise in technical risk assessment and underwriting,and financial stability.

Within our organization, we are laying the foundationfor the globalization of our business by decisivelymoving forward with our multi-year change programthat will standardize procedures and platforms acrossall AGCS sites. We want to respond more quickly to ourclients’ dynamic risk landscape by offering innovative,holistic insurance solutions which have been developedacross individual lines of business. The several industryawards we received last year from leading insurancemagazines speak to the fact that our coverage solutionsalready hold their own against the best solutions on themarket.

Though demanding tasks lie ahead, we expect to remainon the path of growth. What we have achieved and whatwe can still achieve, has first and foremost been theresult of our employees’ efforts. And with those words,I would like to take this opportunity to thank them fortheir unwavering commitment and their impressiveperformance over the past year.

Axel Theis, CEO Allianz Global Corporate & Specialty AG

Foreword

Allianz IARD, ParisAllianz of America Inc.,Wilmington / USA

Allianz SE, Munich

AGR US, Burbank / USACanada Branch

100%

AGCS MarineInsurance Company,

Chicago

100 %

100 %

89 % 11%

100 %

Allianz GlobalCorporate &

Specialty (France),Paris

Allianz Global Corporate & Specialty AG, Munich including:Austria Branch Belgium Branch French Branch Hong Kong Branch Italy Branch

AllianzRisk Transfer AG,

Zurich

AGCSParticipaçoes

Ltda.,Rio de Janeiro

100 %100 % 100 %

Allianz Fire andMarine InsuranceJapan Ltd., Tokyo

Netherland Branch

100 %

Nordic Branch Spain Branch Singapore Branch UK Branch

Allianz GlobalCorporate & SpecialtySouth Africa Ltd.,

Johannesburg

100 %(indirectparticipation)

profit and loss transfer agreement

AllianzRisk ConsultingGmbH, Munich

99 %(indirectparticipation)

4

AGCS Global Structure

AGCS Global Structure

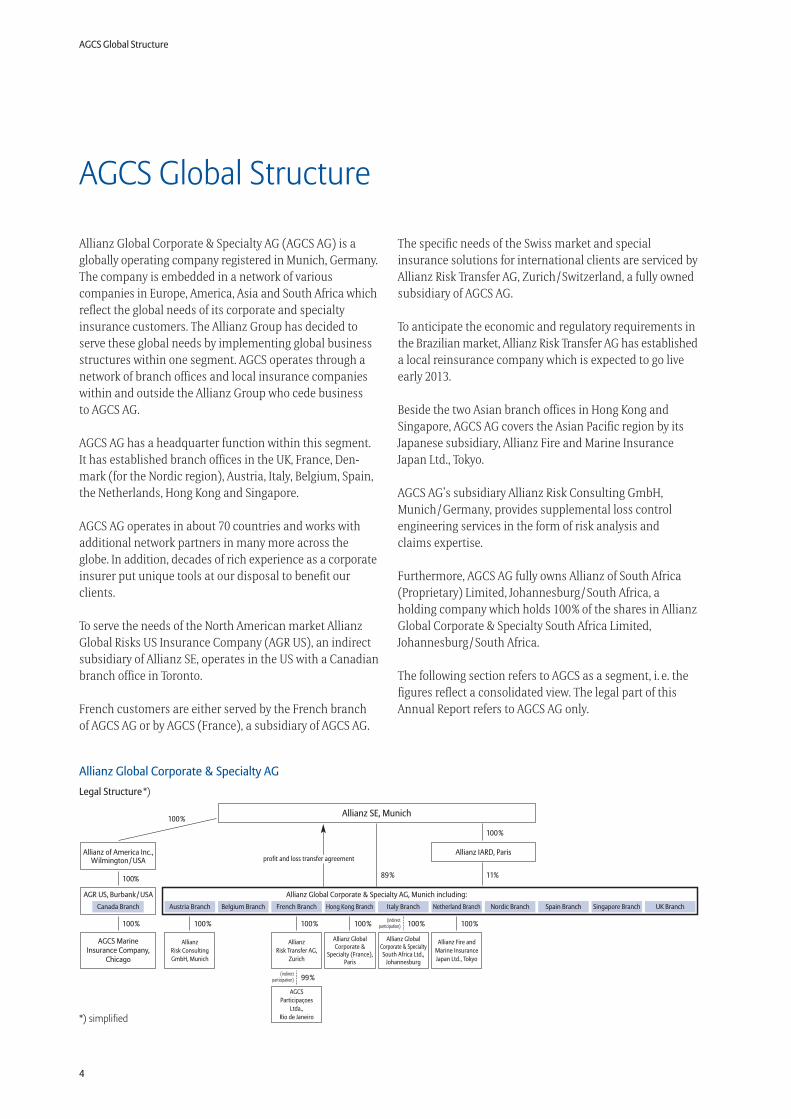

Allianz Global Corporate & Specialty AGLegal Structure *)

*) simplified

Allianz Global Corporate & Specialty AG (AGCS AG) is aglobally operating company registered in Munich, Germany.The company is embedded in a network of variouscompanies in Europe, America, Asia and South Africa whichreflect the global needs of its corporate and specialtyinsurance customers. The Allianz Group has decided toserve these global needs by implementing global businessstructures within one segment. AGCS operates through anetwork of branch offices and local insurance companieswithin and outside the Allianz Group who cede businessto AGCS AG.

AGCS AG has a headquarter function within this segment.It has established branch offices in the UK, France, Den-mark (for the Nordic region), Austria, Italy, Belgium, Spain,the Netherlands, Hong Kong and Singapore.

AGCS AG operates in about 70 countries and works withadditional network partners in many more across theglobe. In addition, decades of rich experience as a corporateinsurer put unique tools at our disposal to benefit ourclients.

To serve the needs of the North American market AllianzGlobal Risks US Insurance Company (AGR US), an indirectsubsidiary of Allianz SE, operates in the US with a Canadianbranch office in Toronto.

French customers are either served by the French branchof AGCS AG or by AGCS (France), a subsidiary of AGCS AG.

The specific needs of the Swiss market and specialinsurance solutions for international clients are serviced byAllianz Risk Transfer AG, Zurich/Switzerland, a fully ownedsubsidiary of AGCS AG.

To anticipate the economic and regulatory requirements inthe Brazilian market, Allianz Risk Transfer AG has establisheda local reinsurance company which is expected to go liveearly 2013.

Beside the two Asian branch offices in Hong Kong andSingapore, AGCS AG covers the Asian Pacific region by itsJapanese subsidiary, Allianz Fire and Marine InsuranceJapan Ltd., Tokyo.

AGCS AG’s subsidiary Allianz Risk Consulting GmbH,Munich/Germany, provides supplemental loss controlengineering services in the form of risk analysis andclaims expertise.

Furthermore, AGCS AG fully owns Allianz of South Africa(Proprietary) Limited, Johannesburg/South Africa, aholding company which holds 100% of the shares in AllianzGlobal Corporate & Specialty South Africa Limited,Johannesburg/South Africa.

The following section refers to AGCS as a segment, i. e. thefigures reflect a consolidated view. The legal part of thisAnnual Report refers to AGCS AG only.

1 includes LoB ART results also for 2011 to allow for comparability 5

AGCS Global by Line of Business

AGCS Global by Line of Business

AGCS global business consists of various legal entities that areunder AGCS management responsibility. Total global grossconsolidated premiums written amount to € 5,314.3 million,and represent an 8% growth relative to 2011 (€ 4,918.2 million1).Gross figures per Line of Business (LoB) are shown on a non-consolidated basis and include for the first time LoB ART(Allianz Risk Transfer ART is a center of competence for alter-native risk transfer within the Allianz Group and providestailored insurance, reinsurance and other non-traditional riskmanagement solutions). Overall, the consolidation effect ofgross premiums written amounts to € 731.5 million.

Gross premiums written for Aviation amounted to € 721.5(693.1) million which is 4.0% above prior year mainly driven bypositive FX effects and additional launches of communicationsatellites in the sub-product line Space that more thancompensated the current competitive market environmentaffected by favorable loss experience leading to overcapacityand pressure on rates. The calendar year loss ratio of 54.3%showed significant improvement relative to last year (64.2%)reflecting positive claims run-off and continued low Airlinesclaims. The combined ratio declined to 78.7% (89.2%).

Gross premiums written for Energy amounted to € 238.4(189.4) million, a 25.9% increase compared to last year, alsobenefiting from positive FX effect. The growth shows thatthe plans to expand and diversify the portfolio have beenimplemented successfully, with particularly encouraging newbusiness opportunities generated in North America onshoreand Asia offshore. In 2012, despite being less severe than theprevious year, Energy was again impacted by several largelosses. However, the calendar year loss ratio decreased to55.5% (96.9%) as the increased size of the book as well aspositive run-off supported strong profitability, resulting in acombined ratio of 73.4% (119.1%).

Gross premiums written for Engineering amounted to € 537.9(510.5) million, an increase compared to prior year of 5.3%.Despite difficult economic conditions in many marketsaccompanied by lower investment activity in projects andlapses driven by profitability initiatives, the portfolio could beexpanded, especially in Germany and the US. In 2012, negativeimpact from Storm Sandy could largely be shouldered bybenign claims development in non-cat segments as well asfavourable prior year loss movements resulting in a calendaryear loss ratio of 66.9% (67.7%). Due to one-off alignments oncommissions deferrals, the expense ratio eroded compared to2011 and the combined ratio ended up at 96.0% (89.7%).

Given the very challenging market environment, FinancialLines showed a satisfactory growth of 4.4% in gross premiumswritten and reached € 303.1 (290.1) million. AGCS couldachieve further growth in the UK mainly for professionalindemnity as well as seize growth opportunities in Switzer-land, Nordics and Canada. For 2012 the loss experienceremained as expected resulting in a loss ratio similar to prior

year levels at 56.9% (55.1%). The combined ratio of 83.2%(79.5%) was further impacted by one-off alignments on com-missions deferrals as well as higher broker charges in selectedcountries.

In 2012, gross premiums written in Liability increased to€ 938.4 (845.3) million due to higher volume of fronting busi-ness coupled with growth realized for General Liability busi-ness in US and Germany as well as higher business volume forPharmChem in UK. Whilst in 2011 the calendar year loss ratioof 58.0% was positively impacted by an exceptional run-offprofit from prior years, in 2012 Liability claims experienceremained in line with long term expectations at 63.8%. Thecombined ratio increased slightly yet remained a majorcontributor to overall AGCS results with 84.7% (78.7%).

Gross premiums written in Marine amounted to € 1,159.3(1,004.5) million. The 15.4% improvement versus prior year isexplained by positive FX effects and an increased premiumvolume for Cargo business based on German, US and Frenchexporting companies as well as new opportunities in Brazil.The calendar year loss ratio of 77.6% (75.4%) was significantlyimpacted by CAT losses, including Storm Sandy and Tornadoesin North America as well as the large Costa Concordia loss inEurope. Therefore in total the combined ratio ended up at108.2% (105.0%).

AGCS’ largest line, Property, generated gross premiumswritten of € 1,314.5 (1,291.5) million mainly driven by highervolume of fronting business as well as up-sells in Germanypartially offset by a portfolio reduction in a number ofcountries driven by profitability initiatives focused onpremium adequacy. Similar to the last 2 years, loss experiencein 2012 was again impacted by an extraordinary number ofnatural catastrophes events of which the Storm Sandy, ItalianEarthquake and US Tornadoes earlier in the year are the majorones. In contrast to 2011, when the higher than average claimsactivity was fully counterbalanced by exceptional one-timerun-off results, for 2012 the severe CAT events as well as somelarge losses have eroded the calendar year loss ratio by 27.8%-pto 88.0% (60.2%). The total combined ratio for Property in 2012is 114.9% (87.7%).

Gross premiums written for Allianz Risk Transfer (LoB ART)amounted to € 767.1 (642.4) million. The 19.4% growth relativeto prior year is mainly driven by higher Insurance LinkedMarkets (ILM) and fronting business. Compared to prior year,combined ratio at 68.8% (77.6%) has benefited from signi-ficantly better claims ratio relative to 2011 when CAT lossessuch as the Thailand Flood and New Zealand Earthquakeimpacted results more severely than in 2012 (Storm Sandy).

The gross premiums written of Other Lines that includesprimarily non-core corporate insurance business amountedto € 65.8 (101.2) million. The main driver of this decrease isthe discontinuation of motor business in Asia.

6

Supervisory Board

Clement BoothMember of the Board ofManagement, Allianz SEChairman

Oliver BäteMember of the Board ofManagement, Allianz SEDeputy Chairman

Jacques RichierChairman of the Board ofManagement,Allianz France SA

Jay RalphMember of the Board ofManagement, Allianz SEuntil December 31, 2012

Dr. Hermann JörissenFormer member of the Boardof Management, AGCS AGas of January 1, 2013

Bernadette ZieglerPersonnel OfficerEmployee representative

Senol SabahIT specialistEmployee representative

Board ofManagement

General Managers

Dr. Axel TheisCEOChairman

Andreas BergerCRMO

Sinéad BrowneCPRSOuntil December 31, 2012COOas of January 1, 2013

Chris Fischer HirsCFO

Dr. Hermann JörissenCUO Corporateuntil December 31, 2012

Hartmut MaiCUO Corporatesince January 01, 2012

Arthur MoossmannCUO Specialty

William ScaldaferriCUO Allianz Risk Transferand Reinsurancesince January 01, 2012

Robert TartagliaCOOuntil December 31, 2012

Branch Office United Kingdom

Carsten ScheffelChief Executive

Branch Office France

Gilles MareuseChief Executive

Branch Office Austria

Thomas GonserChief Executive

Branch Office Nordic Region

Stig JensenChief Executive

Branch Office Italy

Giorgio BidoliChief Executive

Branch Office Belgium

Eric PaniChief Executive

Branch Office Spain

Agustin Martin MartinChief Executive

Branch Office Netherlands

Nicolien KetelaarChief Executive

Singapore Branch Officesince January 01, 2012

Kevin LeongChief Executive

Hong Kong Branch Officesince January 01, 2012

Kevin NorthcottChief Executive

Supervisory Board, Board of Management

7

We continually monitored the Board of Management’s conduct of business on the basis of regular reports and weinformed ourselves about the state of affairs in several meetings. We have examined the Annual Financial State-ments and the Management Report and we concur with the findings of KPMG AG Wirtschaftsprüfungsgesellschaft,Munich, which issued an unqualified auditor’s certificate for the Annual Financial Statements for fiscal 2012 andthe Management Report presented to it. In its meeting on May 08, 2013, the Supervisory Board approved the AnnualFinancial Statements prepared by the Board of Management, which are herby confirmed.

Effective January 1, 2012, the Supervisory Board appointed Mrs. Sinéad Browne, Mr. Hartmut Mai and Mr. WilliamScaldaferri to the Board of Management. Mrs. Browne is responsible for Human Resources, Cat Management andDiscontinued Business. Mr. Mai, together with Dr. Jörissen, is responsible for Underwriting Corporate andMr. Scaldaferri is responsible for Underwriting Allianz Risk Transfer and Reinsurance. Effective December 31, 2012,Dr. Hermann Jörissen resigned from his position as member of the Board of Management and went into retirement.The company’s General Shareholders’ Meeting appointed Dr. Jörrisen to the Supervisory Board, effective January 1,2013, after Mr. Jay Ralph resigned from his mandate as a member of the Supervisory Board, effective December 31,2012.

Effective December 31, 2012, Mr. Robert Tartaglia resigned from his position as member of the Board of Managementwith the consent of the Supervisory Board. Mr. Tartaglia will take on different responsibilities within the AllianzGroup in the future.

We thank Dr. Jörrisen and Mr. Tartaglia for their contribution to the work of the Board of Management.

Based on the results of his examination, the responsible actuary granted unqualified actuarial certification asprovided for by section 11e in conjunction with section 11a 3 (2) of the German Insurance Supervision Law (VAG).

Munich, May 08, 2013

For the Supervisory Board

Clement Booth

Report of the Supervisory Board

Report of the Supervisory Board

The strength of the business model of Allianz Global Corporate & Specialty AG, which is the worldwide under-writing of international industrial insurance as well as aviation and marine risks was proven once again in 2012. Ina difficult market context the company succeeded in achieving a new profit record.

Gross premiums written reached a new record in the reporting year, as did net premiums earned. Slightly higherclaims expenses due to a number of major losses as well as lower run-offs resulted in higher overall claimsexpenses in the reporting year. The decrease of losses assumed from natural catastrophes compared to the previousyear was not able to compensate the increase in major losses.

Investment income was up once again, mainly due to distributions from our investments funds as well as our Swisssubsidiary. Nonetheless, our investments still contain high valuation reserves. In the future, a decline is to beexpected, because distributions will not be able to compensate historically low re-investment interest rates.

The profit of € 308.9 million transferred by Allianz Global Corporate & Specialty AG to Allianz SE represents a newrecord for our company. Since the founding of the company in 2006, a total of more than € 1.6 billion has beentransferred to Allianz SE.

The global orientation of Allianz Global Corporate & Specialty AG was again pursued consistently and with goodresults in the reporting year. The new branch offices in Singapore and Hong Kong have been operating since 2012so that we now also write direct insurance business in these two countries. In view of the saturated markets inwestern countries, an initiative to open up promising growth markets (such as Asia, South America and Africa)was launched in the beginning of 2012 under the title "Second Curve".

8

Management Report

Management Reportof Allianz Global Corporate & Specialty AG

Development overview

The business of Allianz Global Corporate & Specialty AGincludes the German and International CorporateBusiness (ICB), as well as the specialty insurance linesMarine, Aviation and Energy, in both the direct and theindirect insurance business. The bundling of ouractivities and the further diversification of insurancerisks have also enabled us to strengthen our offer ofinsurance solutions for specific needs as well as ourcomprehensive service. In the past year, we continuedto invest in the global harmonization and optimizationof business processes in all business units within theframework of our projects.

In a market context characterized by competitivepressures, we steadfastly pursued our risk-adequate andselective underwriting and reinsurance policy. It shouldbe noted that our sales figures and underwriting results

are impacted by currency effects stemming primarilyfrom the US dollar and the British pound, which are notcommented individually.Premium income in the reporting year rose significantlyby € 293.7 million and reached a new record of € 3.0 (2.7)billion. Premium income in Property/Casualty Insuranceincreased by € 138.3 million to € 1.76 (1.62) million. Theincrease resulted primarily from the indirect insurancebusiness. The newly founded branch offices in Singaporeand Hong Kong were able to generate a premiumvolume of € 126.7 million. In the other branch offices,premium volume increased by € 28.7 million from € 1.11billion in the prior year to € 1.13 billion in the reportingyear, which was also primarily driven by indirectinsurance business. The UK branch office reported anincrease of € 31.5 million to € 644.6 (613.1) million, thebranch office in Denmark an increase by € 7.0 million to€ 46.2 (39.2) million, the branch office in Italy anincrease by € 6.0 million to € 126.0 (120.0) million and

9

Allianz Global Corporate & Specialty AG

the branch office in Belgium an increase of € 5.3 millionto € 62.1 (56.8) million. However, premium income in theNetherlands of € 77.3 (85.2) million, in Spain of € 120.9(126.7) million, in Austria of € 29.1 (34.8) million and inFrance of € 28.0 (29.7) million was below the prior yearlevel.

Gross premiums written rose significantly to € 2.96(2.59) billion. Despite higher reinsurance cessions of€ 1.11 (0.95) billion, net premiums earned of € 1.85 (1.64)billion were clearly above the prior-year figure.

Claims expenses due to natural catastrophes in thereporting years decreased by € 178 million from theprior year to € 207 (385) million gross, or € 64 (194)million net, and were mainly impacted by hurricane“Sandy” and the severe earthquake in Italy.

As a result, the gross loss ratio decreased from 77.3percent in the previous year to 71.9 percent in thereporting year. The run-off of prior-year claims reserveswas less favorable than in the previous year anddecreased by € 59.9 million to € 194.5 (254.4) million.Overall, gross claims expenses for insurance losses roseby € 188.7 billion over the previous year to a total of€ 1.94 (1.75) billion. With respect to the overall portfolio,the gross loss ratio decreased by 2.1 percent from 67.5percent in the previous year to 65.4 percent in thereporting year. Despite the increase of gross under-writing expenses by € 53.3 million to € 606.1 (552.8)million, the gross cost ratio also decreased to 20.5 (21.3)percent, due to the strong growth of gross premiumsearned.

The claims equalization and similar reserves, which bylaw must be recognized in the balance sheet, requiredtotal allocations of € 137.0 (74.5) million.

This led to a substantially improved underwriting resultfor own account of € 5.2 (– 63.9) million.

To be able to evaluate the development of our businesssegment, the International Corporate Business must beviewed in its totality, just as in previous years.The impact of the business model of Allianz GlobalCorporate & Specialty AG, which aims to be closer tothe client through direct underwriting by local offices,is characterized by the fact that insurance businessthat was previously written as reinsurance assumedand reported as indirect business has since 2007 beenincreasingly reported as direct business. But basically,this is still the same insurance business. This businesspolicy essentially results in a shift of premium incomefrom indirect to direct insurance business. However, inthe reporting year the decline in the indirect insurancebusiness, which should have been expected as a resultof this trend, was more than compensated by increasingbusiness volume in the growth regions South Americaand Asia as well as Australia. Gross premium incomefrom direct insurance increased by € 61.1 million to€ 1.56 (1.50) billion; at the same time, premiums inindirect insurance increased by € 232.6 million to € 1.46(1.23) billion.

The fiscal year’s loss ratio in direct insurancedeteriorated from 80.3 percent to 82.8 percent due tomajor losses, which was partially compensated byhigher run-off from prior-year losses of € 162.0 (87.8)million. Claims expenses in the indirect insurancebusiness in the reporting year were only slightly belowthe prior-year figure which was marked by losses fromnatural catastrophes. Due to positive premiumdevelopment, the loss ratio for the fiscal year improvedto 60.1 (73.7) percent. Taking into account the run-offof the prior-year claims reserve of € 32.5 (166.5) million,which was clearly below the prior-year figure, the grossloss ratio of reinsurance business assumed amountedto 57.9 (59.5) percent. The gross loss ratio in the directinsurance business was 72.3 (74.1) percent.

The following comments on the development of ourbusiness are based on gross sales figures, and theunderwriting results are stated for own account.

•

•

Direct insurance business

In Personal Accident Insurance, premium income thisyear rose by € 3.3 million to € 14.5 (11.2) million. Claimsexpenses of € 3.4 (2.3) million were higher than in theprevious year but resulted in a gross loss ratio of 25.5(24.0) percent. After an allocation to the equalizationreserve of € 0.3 (0.2) million, the underwriting profit of€ 5.9 (3.9) million was above the prior-year level.

In Liability Insurance, premium income in the reportingyear grew by € 66.1 million to € 565.1 (499.0) million,which is mainly due to a premium increase in GeneralLiability and Financial Loss Liability insurance. Thenewly created branch offices in Singapore and HongKong also contributed to the increase of premiumincome. Claims expenses rose by € 7.8 million to € 364.1(356.3) million, essentially due to the year’s developmentin General Liability and Financial Loss Liabilityinsurance. The loss ratio came to 67.0 (77.5) percent andwas thus below the prior-year level. After an allocationof € 4.1 (15.0) million to the equalization reserve, a profitof € 9.4 (12.4) million was posted, slightly below theprior-year level.

Premium income in the insurance branch groupsAutomotive Liability Insurance and Other AutomotiveInsurance amounted to € 14.1 million, which isessentially due to the newly created Hong Kong branchoffice. In the previous year, following a decision byAllianz Group to no longer write this type of insurance inAllianz Global Corporate & Specialty AG, these insurancebranch groups reported no business. Lower claimsexpenses of € 3.3 million resulted in a loss ratio of 30.0percent. In fiscal 2012, this insurance branch groupreported a profit of € 0.6 million.

Gross premium income in the insurance branch groupsFire Insurance and other Property Insurance decreased by€ 33.1 million to € 391.2 (424.3) million.The decline of premium income in Fire Insurance by€ 33.2 million to € 157.3 (190.5) million is essentially dueto portfolio reductions and a more restrictive under-writing policy. Claims expenses of € 123.2 (136.2) millionwere below the prior-year level. The loss ratio for thefiscal year thus came to 72.4 (78.0) percent. After anallocation of € 8.0 (withdrawal of € 19.2) million to theequalization reserve an underwriting loss at the prior-year level of € 20.3 (loss of 20.2) was posted.Premium income from Other Property Insuranceremained at the prior-year level of € 233.9 (233.8) million.

Claims expenses increased by € 9.4 million over theprevious year to € 136.8 (127.4) million and resulted in alower loss ratio of 60.2 (58.2) percent. After a withdrawalfrom the equalization reserve of € 3.7 (3.2) million, OtherProperty Insurance posted a loss of € 45.9 (loss of 39.2)million.Overall, the insurance branch group Fire Insurance andother Property Insurance ended the year with an under-writing loss of € 66.2 (59.4) million. The withdrawal fromthe equalization reserve amounted to € 11.7 (withdrawalof 16.0) million.

Premium income in Marine and Aviation Insuranceincreased to € 477.8 (470.6) million in the reporting year.In Marine insurance, gross premium income increasedby € 1.3 million to € 248.2 (246.9) million. Due to almostunchanged claims expenses of € 185.6 (187.9) million,which were essentially attributable to losses incurred inthe course of the year, the gross loss ratio stayed at theprior-year level of 75.0 percent. Overall, this insuranceline reported an underwriting loss of € 23.0 (loss of 21.7)million after changes to the equalization reserve.Aviation Insurance recorded a decline in premiumincome by € 6.0 million to € 229.6 (223.6) million, whilegross claims expenses declined to € 140.4 (172.3)million. The loss ratio followed this development withan additional improvement of 16.2 percent to 60.4 (76.6)percent. After an allocation of € 40.6 (withdrawal of€ 1.4) million to the equalization reserve an under-writing profit of € 9.8 (loss of 16.0) was posted. Overall,the insurance branch group’s result improved by € 24.6million to a loss of € 13.1 (loss of 37.7) million afterallocations to the equalization reserve.

In the insurance branch Other Insurance, gross premiumincome of € 96.2 (92.9) million remained nearly at theprior-year level. However, gross claims expensesincreased by € 91.7 million to € 161.3 (69.6) million,which was essentially due to business interruptioninsurance. Accordingly, the loss ratio increased to 158.0(85.1) percent.After an allocation to the equalization reserve of € 0.5(withdrawal of 4.4) million, Other Property Insuranceposted a loss of € 74.2 (loss of 1.8) million.

•

•

•

•

10

Management Report

•

•

•

•

•

•

•

Reinsurance business assumed

Premium income in Property/Casualty Insurancedecreased by € 0.5 million to € 9.3 (9.8) million. Claimsexpenses rose by € 2.5 million to € 2.0 million (incomeof € 0.5 million). This insurance line ended the year withan underwriting profit of € 5.0 (8.0) million.

Gross premium income in Liability Insurance came to€ 307.1 (268.2) million in the reporting year, which was€ 38.9 million above the prior-year level. This isessentially attributable to an increase in general liabilityinsurance, which benefited to a great extent fromreinsurance business assumed by our Braziliansubsidiary. Gross claims expenses increased by € 56.8million to € 125.8 (69.0) million, mainly due to GeneralLiability Insurance business, which drove up the totalloss ratio to 42.4 (26.2) percent. € 31.1 (allocation of 16.2)million were allocated to the claims equalization reserve.After the positive development of business ceded, aprofit of € 84.0 (21.7) million was reported.

In Automotive Liability Insurance and Other AutomotiveInsurance, premium income in the reporting yeardeclined by € 16.7 million to € 5.9 (22.6) million. Withclaims expenses totaling € 10.8 (17.7) million, thesebranch groups ended the year with an underwriting lossof € 3.4 (profit of 8.1) million.

The insurance branch group Fire Insurance and OtherProperty Insurance posted an increase of gross premiumincome by € 99.4 million to € 631.9 (532.5) million. FireInsurance registered an increase in premium income to€ 358.5 (291.0) million, which was mainly attributableto the newly created Singapore Branch Office as well asreinsurance business assumed in Brazil and Australia.Gross claims expenses rose to € 135.4 (109.1) million.At 37.9 (37.7) percent, the loss ratio remained at nearlythe same level as in the prior year. After reinsurancecessions and allocation to the equalization reserve of€ 20.1 (withdrawal of 52.4) million, an underwritingprofit of € 23.7 (86.6) million was reported.

Gross premium income in Other Property Insuranceincreased by € 31.9 million over the prior year to € 273.4(241.5) million, which is essentially due to the positivedevelopment of reinsurance business assumed as wellas the opening of the branch office in Hong Kong. Theabsence of losses from natural catastrophes as well aslower major loss claims in this insurance line resulted ina decline of claims expenses by € 83.8 million to € 167.5(251.3) million. The previous year had been marked byclaims expenses from the earthquake in Japan and flooddamages in Australia. After a withdrawal from theequalization reserve of € 0.6 (allocation of 0.8) millionthis insurance line ended the year with an underwritingprofit of € 68.3 (loss of 46.3) million. After an allocationto the equalization reserve of € 19.5 (withdrawal of 51.6)million, this insurance line ended the year with anunderwriting profit of € 92.0 (loss of 40.3) million.

Marine and Aviation Insurance generated gross premiumincome of € 405.2 (320.1) million.In Marine Insurance, premiums rose € 81.2 million fromthe previous year and reached € 216.4 (135.2) million,which is to a great extent due to higher cessions fromBrazil. Losses increased by € 180.6 million, mainly dueto hurricane “Sandy”, and resulted in gross claimsexpenditures of € 242.8 (62.2) million. € 30.2 (allocationof 60.0) million were allocated to the claims equalizationreserve. The result was an underwriting loss of € 45 (lossof 39.9) million.In Aviation Insurance, gross premium income amountedto € 188.8 (184.8) million. Gross claims expensesincreased by € 10.9 million to € 83.4 (72.5) million andresulted in a higher loss ratio of 44.6 (39.4) percent.After an allocation of € 22.3 (allocation of € 56.5) millionto the equalization reserve, an underwriting profit of€ 3.9 (loss of 23.1) million was posted.Overall, the branch group ended the year with an under-writing loss of € 41.1 (loss of 63.1) million after changesto the equalization reserve.

Gross premiums written in Other insurance rose to€ 100.7 (74.4) million this year. Lower claims expensesof € 52.2 (115.8) million resulted in a loss ratio of 63.2(177.6) percent. Overall, the branch group closed theyear with an underwriting profit of € 6.3 (20.0) million.

11

Allianz Global Corporate & Specialty AG

Reinsurance business ceded

In the reporting year, the company once again ceded itsinsurance business in part to the various Groupcompanies and in part to external reinsurers. In keepingwith the reinsurance strategy pursued in the previousyears, non-proportional reinsurance contracts in theform of a global coverage program were concluded withthe reinsurers. With few exceptions, reinsurance cededcovers maximum risks and natural disasters to a limitedextent on a quota-share basis and selectively in mostinsurance lines. The largest part of the business cededto Group companies is assumed by Allianz ReinsuranceDublin Limited, while Munich Re (Münchener Rückver-sicherungs-Gesellschaft AG) in Munich is the leadingexternal reinsurer for Allianz Global Corporate &Specialty AG. Premiums ceded to reinsurers increasedby a total of € 180.7 million to € 1,148.4 (967.7) million,which is essentially due to higher facultative reinsurancecessions in the amount of € 706.9 (522.1) million.Despite higher cessions, passive reinsurance posted aresult of € 273.8 (273.3) million, nearly unchanged fromthe prior year. This was due to higher claims expenses ofthe reinsurers for losses in the direct insurance businessduring the reporting year.

Supplementary information to the Management Report

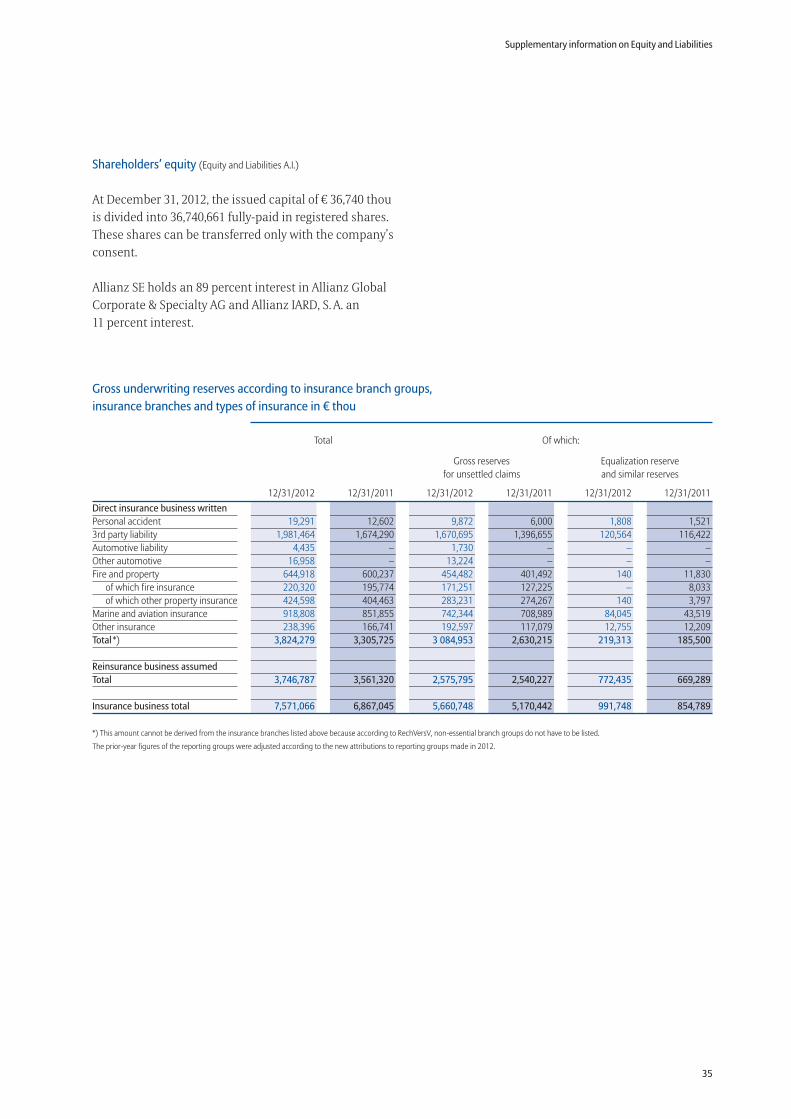

The various insurance lines and types offered arepresented in detail on page 45.

As part of the preparations for Solvency II, the individualproducts were subjected to a general examination withrespect to their hierarchical assignment to branchgroups. In certain cases this resulted in changes.These changes concern the reclassifications betweenLiability Insurance and Aviation Insurance as well asbetween Other Property Insurance and Other Insurance.The biggest reclassification in terms of premium incomeresults from the reclassification of Aviation LiabilityInsurance from the Liability Insurance branch group tothe branch group Marine and Aviation Insurance.The respective prior-year figures have been adjustedaccordingly in both the comments and the tables.

Developments in the capital markets and their impacton investments

Allianz Global Corporate & Specialty AG continued itssuccessful, safety-oriented investment strategy in 2012.Our objective is to generate as high a return as possiblewhile limiting our risk. For reasons of safety we mix andspread our investments over many different investmentsegments. As in previous years, this helped to cushionthe effects of the persisting high uncertainty in thecapital markets as well historically low interest rates.

Due to our financial obligations from the insurancebusiness, the by far greatest part of our portfolio isinvested in fixed-interest securities. The averagematurity of the fixed-interest investments increasedslightly in the course of the reporting year.

Our fixed-income investments continue to be focusedon German mortgage bonds, supplemented by Germanand European government bonds. Mortgage bonds arebacked by valuable securities such as communal loansor senior mortgage loans, which makes them highlysecure investments. In government bonds we continuedto concentrate on the Euro zone core countries. Due tothe high ratings of German issuers, we slightly reducedour investments in other Euro zone countries duringthe year. At the end of 2012, 0.8 (0.4) percent of ourinvestments were in Italian government bonds. Ourholdings in government bonds from Greece, Ireland,Portugal and Spain were already completely divested in2010. The share of investments held in foreign currenciesas matching cover for underwriting liabilities, inparticular in US dollars, Australian dollars and BritishPounds remained nearly constant and in a year-to-yearcomparison, the currencies registered relatively smallfluctuations.

We assess the risk situation with respect to our capitalbase as well as the coverage of our financial obligationswith qualified investments from two perspectives: Forboth areas we use stress test models as well as an earlywarning system and a risk capital model. These testsare performed on an ongoing basis and our investmentspassed all of them without exception in the reportingyear.

12

Management Report

Investments

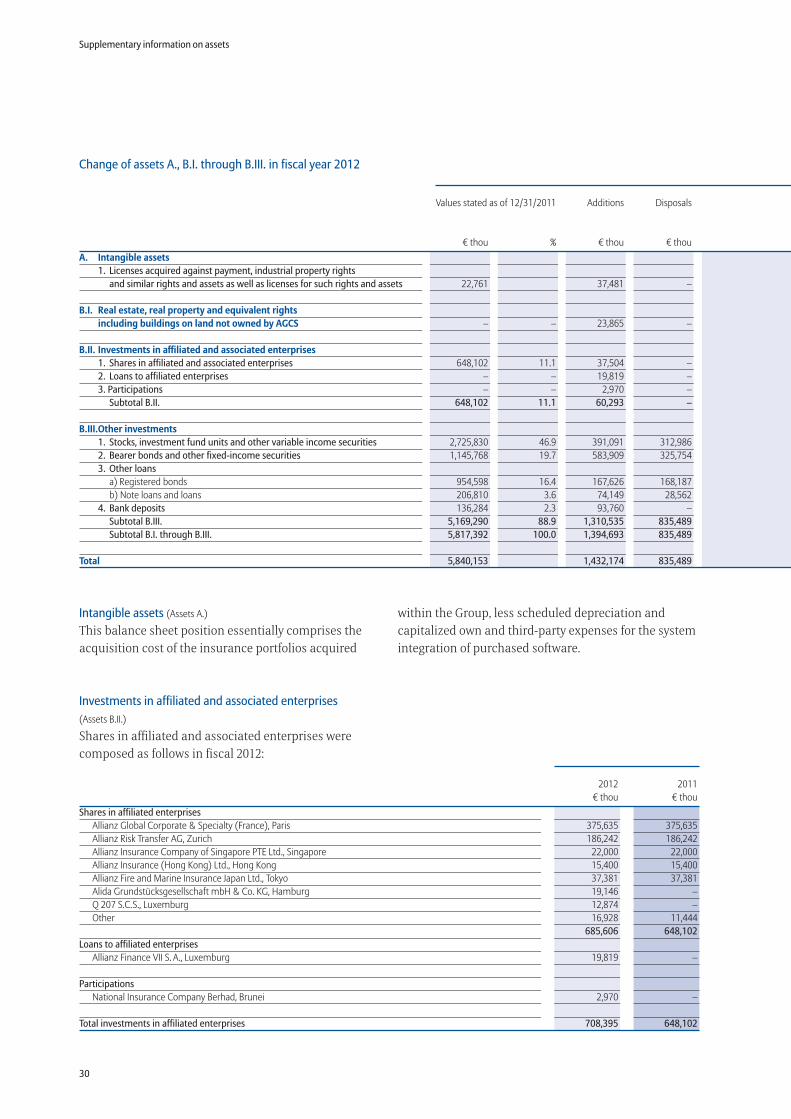

The book value of investments grew by a solid 9.0 percentto € 6,417.9 (5,887.0) million in the reporting year.

Investments in affiliated enterprises and participationsrose to € 708.4 (648.1) million. This increase is mainlydue to investments in real estate investment funds.

The book value of shares, investment certificates andother variable-income securities amounted to € 2,803.9(2,725.8) million at the end of the year. The increase isdue to allocations of investment certificates in annuitieswhile our stock portfolios were completely divested.

The book value of bearer bonds grew substantially to€ 1,399.0 (1,145.8) million; other loans also increased to€ 1,206.4 (1,161.4) million.

Bank deposits amounted to € 230.0 (136.3) million,while funds held by others came to € 46.5 (69.6) millionat the end of the year.

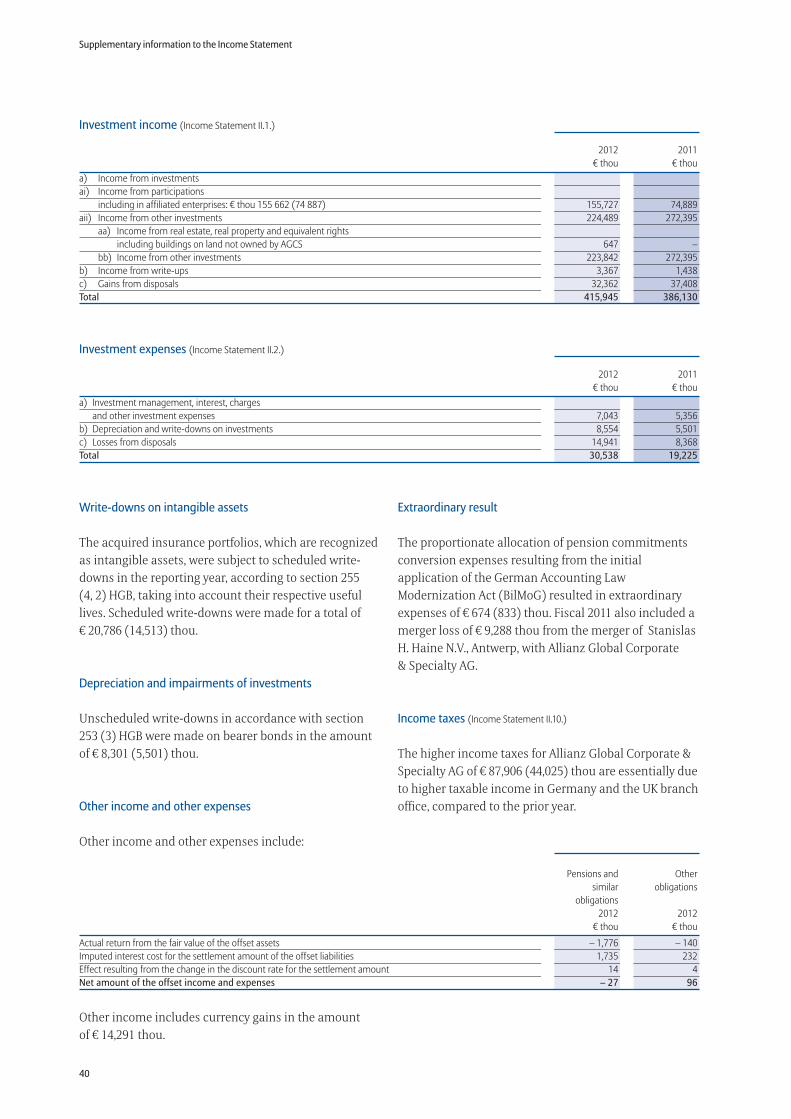

Investment income

Current income from investments was up from theprior year and amounted to € 380.2 (347.3) million.Higher dividend distributions of the affiliated enter-prises effectively compensated for lower distributionsfrom investment funds.

The disposal of investments produced income of € 32.4(37.4) million. The gains were mainly generated fromthe sale of investment fund shares and bearer bonds.Gains from write-ups in 2012 amounted to € 3.4 (1.4)million. These were entirely attributable to bearer bonds.The sale of investments resulted in losses of € 14.9 (8.4)million, which were also completely attributable toinvestment fund shares and bearer bonds.

Depreciation and impairments of investments in thereporting year amounted to € 8.6 (5.5) million, of which€ 0.3 million were attributable to scheduled write-downsand € 8.3 million to bearer bonds.

Investment management and interest expensesamounted to € 7.0 (5.4) million.

Total investment income of € 385.4 (366.9) million onceagain surpassed the already very high prior-year figure.

Valuation reserves on investments increased to a total of€ 1,128.3 (943.4) million. Of this amount, € 614.4 (563.1)million are related to shares in affiliated and associatedenterprises. The valuation reserves on investmentcertificates clearly increased to € 300.8 (229.8) million.The valuation reserves on investment certificates roseto € 97.1 (73.9) million. For other loans, the valuationreserves amounted to € 115.5 (76.5) million.

The reserve ratio, i.e. the percentage of valuation reservesin relation to the book value of total investments, stoodat 17.6 (16.0) percent at the end of the year.

Other non-underwriting business

Other non-underwriting business produced a profit of€ 7.2 (loss of 61.4) million, which was primarily due tocurrency exchange gains.

The overall result of the non-underwriting business thusamounted to € 392.6 (305.4) million.

Extraordinary result

The proportionate allocation of pension commitmentsconversion expenses resulting from the initial applicationof the German Accounting Law Modernization Act(BilMoG) resulted in extraordinary expenses of € 0.7(10.1) million.

Overall result

Tax charges for the reporting year (including intra-groupcharges) came to € 88.2 (44.2) million.

The overall result after taxes was a profit of € 308.9(187.2) million. Under the terms of the existingmanagement control and transfer-of-profit agreement,this profit was transferred to Allianz SE.

13

Allianz Global Corporate & Specialty AG

14

Management Report

Corporate agreements

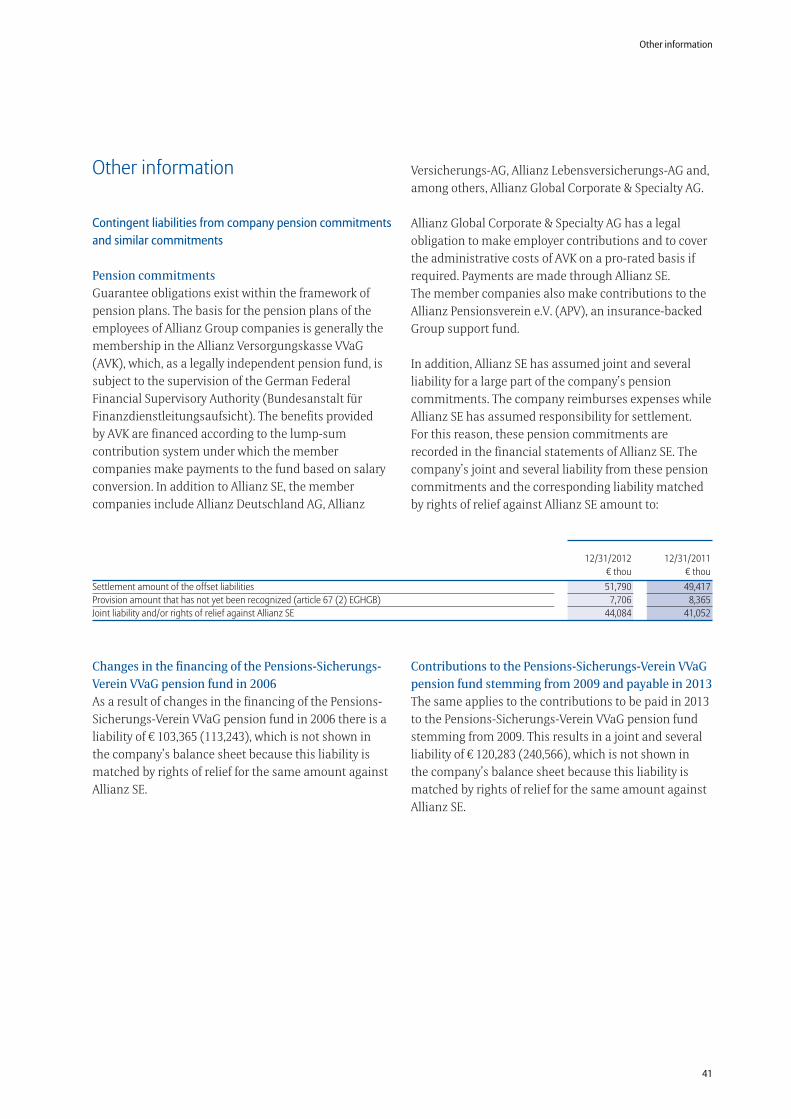

The shareholders of Allianz Global Corporate & SpecialtyAG are Allianz SE and Allianz IARD S.A.Allianz SE and Allianz Global Corporate & Specialty AGare linked by a management control and transfer-of-profit agreement.

Branch offices

Allianz Global Corporate & Specialty AG maintainsbranch offices in London (UK), Paris (France), Vienna(Austria), Copenhagen (Denmark), Milan (Italy),Antwerp (Belgium), Madrid (Spain), Rotterdam(Netherlands), Singapore and Hong Kong (China).

Outsourcing of functions

Transfer of responsibilities

Accounting and collection functions are provided tothe company by the CFO - Accounting units in Munichand Hamburg. The accounting functions of the foreignaffiliates are in part handled locally and in part centrallyin Munich or the London branch office. For the Italianbranch office this service is provided by the local Allianzcompany.

Investments and asset management

On the basis of group-internal service contracts,investments and asset management are handled byAllianz Deutschland AG, Munich, Allianz InvestmentManagement SE, Munich, and for partial areas by PIMCODeutschland GmbH Munich, Allianz Global InvestorsKapitalanlagegesellschaft mbH, Frankfurt/Main andAllianz Real Estate GmbH, Munich.

Information Technology

Computing center services as well as printing andIT services are provided to Allianz Global Corporate &Specialty AG by Allianz Managed Operations & ServicesSE, Munich.

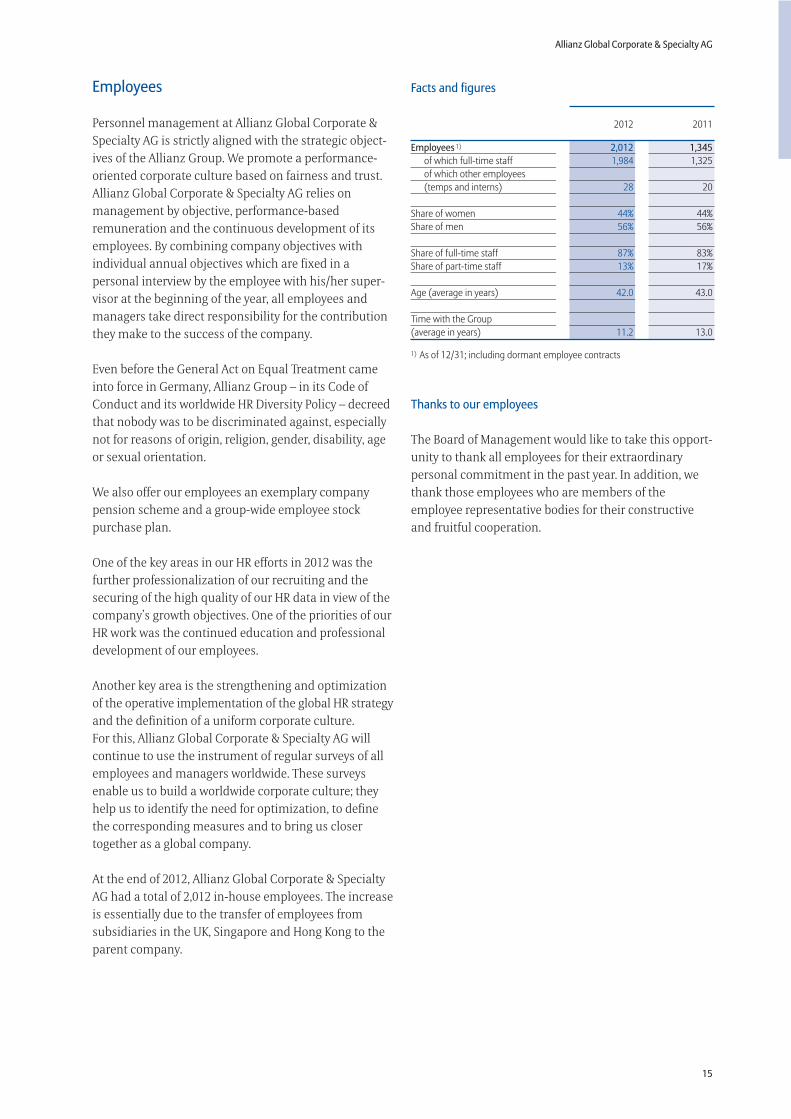

Facts and figures

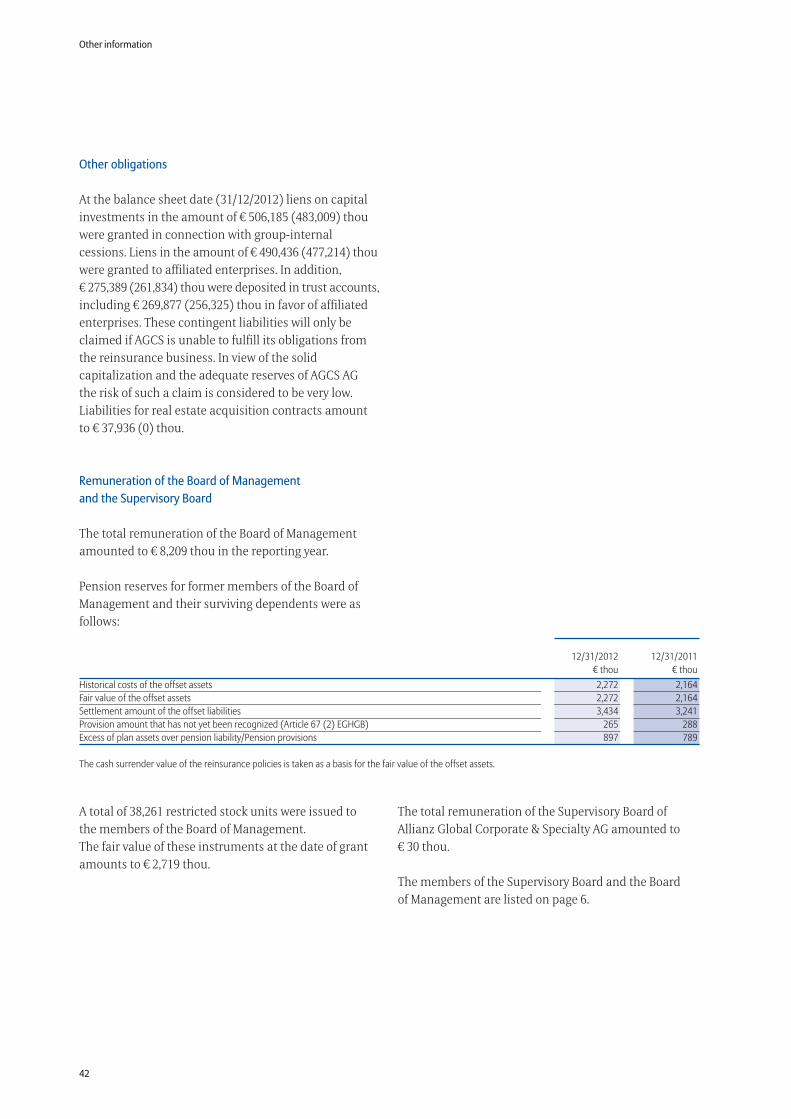

Thanks to our employees

The Board of Management would like to take this opport-unity to thank all employees for their extraordinarypersonal commitment in the past year. In addition, wethank those employees who are members of theemployee representative bodies for their constructiveand fruitful cooperation.

15

Allianz Global Corporate & Specialty AG

Employees

Personnel management at Allianz Global Corporate &Specialty AG is strictly aligned with the strategic object-ives of the Allianz Group. We promote a performance-oriented corporate culture based on fairness and trust.Allianz Global Corporate & Specialty AG relies onmanagement by objective, performance-basedremuneration and the continuous development of itsemployees. By combining company objectives withindividual annual objectives which are fixed in apersonal interview by the employee with his/her super-visor at the beginning of the year, all employees andmanagers take direct responsibility for the contributionthey make to the success of the company.

Even before the General Act on Equal Treatment cameinto force in Germany, Allianz Group – in its Code ofConduct and its worldwide HR Diversity Policy – decreedthat nobody was to be discriminated against, especiallynot for reasons of origin, religion, gender, disability, ageor sexual orientation.

We also offer our employees an exemplary companypension scheme and a group-wide employee stockpurchase plan.

One of the key areas in our HR efforts in 2012 was thefurther professionalization of our recruiting and thesecuring of the high quality of our HR data in view of thecompany’s growth objectives. One of the priorities of ourHR work was the continued education and professionaldevelopment of our employees.

Another key area is the strengthening and optimizationof the operative implementation of the global HR strategyand the definition of a uniform corporate culture.For this, Allianz Global Corporate & Specialty AG willcontinue to use the instrument of regular surveys of allemployees and managers worldwide. These surveysenable us to build a worldwide corporate culture; theyhelp us to identify the need for optimization, to definethe corresponding measures and to bring us closertogether as a global company.

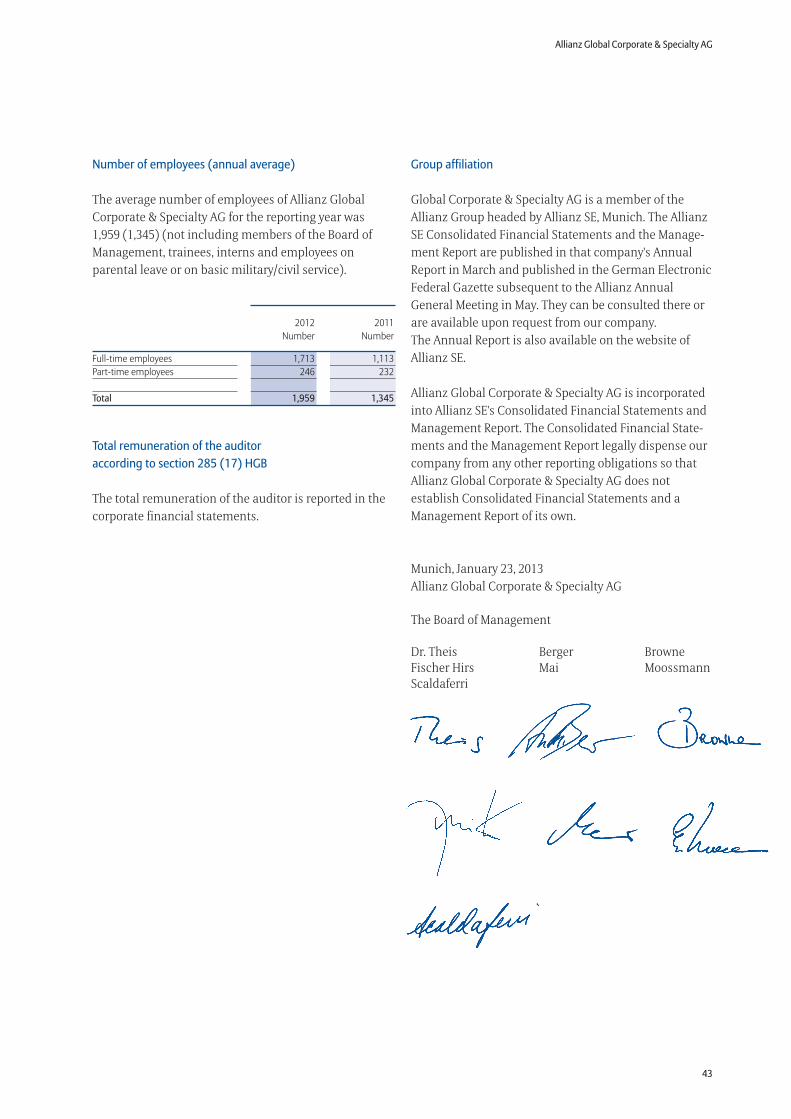

At the end of 2012, Allianz Global Corporate & SpecialtyAG had a total of 2,012 in-house employees. The increaseis essentially due to the transfer of employees fromsubsidiaries in the UK, Singapore and Hong Kong to theparent company.

2011 2012

Employees 1) 2,012 1,345of which full-time staff 1,984 1,325of which other employees(temps and interns) 28 20

Share of women 44% 44%Share of men 56% 56%

Share of full-time staff 87% 83%Share of part-time staff 13% 17%

Age (average in years) 42.0 43.0

Time with the Group(average in years) 11.2 13.0

1) As of 12/31; including dormant employee contracts

16

Management Report

Risk Report

Assuming and managing risk is part of the businessmodel of Allianz Global Corporate & Specialty AG. Welldeveloped risk awareness and the weighing of chancesand risks are therefore an integral part of our businessprocesses. The key elements of our risk management are:

A strong risk management culture, promoted by a solidrisk organization and effective risk governance.Comprehensive risk capital calculations with theobjective of protecting our capital base and supportingeffective capital management.The integration of capital needs and risk considerationsinto the decision-making and management process.

This comprehensive approach makes sure that risksare adequately identified, analyzed and evaluated.Our risk propensity is described by a clear risk strategyand a system of limits. Strict risk control and thecorresponding reports enable us to detect early on anypossible deviations from our risk tolerance.

Risk Organization

The responsibility for risk management within the Boardof Management lies with the Chief Financial Officer(CFO). The Chief Risk Officer, who is reporting to theCFO, monitors the risks assumed and regularly informsthe Board of Management of Allianz Global Corporate &Specialty AG about risk-relevant developments, thecurrent risk profile and capital adequacy. In addition, theChief Risk Officer makes sure that appropriate measuresare taken, for instance in cases where the reduction oravoidance of a risk position is required, and he isresponsible for the continued development of the riskmanagement processes.

As an independent risk control function, the RiskManagement Department systematically monitorsidentified risks by means of qualitative and quantitativerisk analysis and evaluations and ensures the regularor – in case of need – spontaneous reporting of essentialrisks to the Board of Management and to Allianz SE.

Headed by the Chief Financial Officer, the AGCS RiskCommittee examines all relevant risks on a quarterlybasis and agrees on measures for risk mitigation andthe continued development of our risk managementprocesses. The Chief Executive Officer, Chief FinancialOfficer, Chief Underwriting Officer Corporate, ChiefOperating Officer, Chief Personnel & Risk Services Officer

as well as the Chief Underwriting Officer Allianz RiskTransfer, who are members of the Board of Management,are also members of the AGCS Risk Committee, whichensures close cooperation and interaction between riskcontrol and the Board as a whole. The Chief Risk Officeris a member of all of the company’s key committees:the Reinsurance Committee, Loss Reserve Committee,Underwriting Committee and Finance Committee.

The risk management of Allianz Global Corporate &Specialty AG is tied into the risk control system ofAllianz SE. Its binding guidelines are the Group RiskStrategy and the Group Risk Policy set by Allianz SE aswell as additional directives for risk management andthe modeling of internal risk capital. The controllingbody for the risk management of Allianz GlobalCorporate & Specialty AG is the Group Risk unit ofAllianz SE. Other internal and external control functionsare vested in the Supervisory Board, Legal & Complianceas well as Internal Audit.

Risk strategy and risk reporting

The risk strategy defines the core risks of Allianz GlobalCorporate & Specialty AG, the risk bearing capacity ofthe company as well as the risk tolerance of the AGCSBoard of Management. The current risk profile iscontrolled by means of the risk report. It providesindicators with specified fixed threshold values and issubmitted to the Risk Committee on a quarterly basis.The Risk Committee decides on the implementation ofrisk mitigation measures.

Risk categories and control measures

In its circular 3/2009, the German Federal FinancialSupervisory Authority (Bundesanstalt für Finanzdienst-leistungsaufsicht – BaFin) set mandatory MinimumRequirements for Risk Management in Insurance Under-takings (MA Risk [VA]). For grouping its risks, AllianzGlobal Corporate & Specialty AG uses internal categorieswhich are comparable to those of MaRisk guidelines.In particular, we monitor:

Underwriting risk: Premium risk from insufficientpremiums charged and reserve risk from insufficientreserves.Concentration risks: Risk from natural catastrophesand other highly correlated risks with significant lossexposure or default potential.

•

•

•

•

•

Allianz Global Corporate & Specialty AG

17

•

•

•

•

•

Market risks: The risk of potential losses in the portfoliovalue of fixed-income investments or stocks as well asthe foreign currency and interest risk. In this context wealso monitor the liquidity risk in order to ensure ourability to meet our financial obligations whenever theybecome due.Credit risks (including country risks): The risk arisingfrom the insolvency or liquidity shortages of reinsurers,policy holders, insurance brokers and security issuers,as well as reliability risks due to losses stemming fromdebtors’ impaired creditworthiness.Operational risk: Risk that arises from inadequate orfailed internal processes and controls. It may be causedby technology, employees, the organization or byexternal influences and legal risks.

Other, non-quantifiable risks are monitored by meansof structured identification and evaluation processes.These risks are:

Strategic risk: Risk resulting from strategic businessdecisions. This includes risks caused by businessdecisions that are not adapted to a changed economicenvironment.Reputational risk: The risk that arises from possibledamage to an undertaking’s reputation as a consequenceof negative public perception.

Premium risks are controlled primarily with the helpof actuarial models used to calculate premiums andmonitor claim patterns. In addition, we issue guidelinesfor concluding insurance contracts and underwritinginsurance risks. In pricing the risks we underwrite wealso aim to control the combined ratio within clearlydefined limits. We continually test our expectations forthe development of the combined ratio by means ofregular analysis of the claims development.

We control reserve risks by constantly monitoring theprovisions for insurance claims that have been sub-mitted but not yet settled and by amending theseprovisions if necessary. For this we use various actuarialmethods. In business lines with a comparably shorterclaims history, such as financial lines, we have developedfactor-based approaches that enable us to continuallymonitor the adequacy of the provisions made.

Concentration risks occur in connection with naturalcatastrophes such as earthquakes, storms and floodsand represent a special challenge for risk management.In order to manage such risks and to better estimatethe potential effects of natural disasters, we use specialmodeling techniques based on probability. These involvethe correlation of information on our portfolios – forexample the geographic distribution of the amountscovered – with simulated natural disaster scenarios toestimate potential damages. This approach makes itpossible to determine the possible effects andconcentration of these events. Where such models donot exist, for example for the storm risk in Asia, we usescenario-based deterministic approaches. We controlour exposure to natural catastrophes by means of alimit system and the monthly monitoring of possibledamages caused. The insights gained this way are usedto limit the risks we underwrite and to calculate thecapital efficiency of a risk transfer toward the reinsurancemarket.

Market risks. The investments of Allianz GlobalCorporate & Specialty AG are centrally managed by thespecialists of Allianz Investment Management SE (AIMSE). The investment strategy is aligned with the needsof the asset-liability management of Allianz GlobalCorporate & Specialty AG. The investment strategy isimplemented by AIM SE within the framework of aninvestment risk and limit system established by AllianzGlobal Corporate & Specialty AG. This risk and limitsystem is adjusted annually and adopted by the AGCSRisk Committee and the Finance Committee.The efficient implementation of the investment strategyalso involves the use of derivatives and structuredproducts.

Our investments are broadly diversified according totype of investment (shareholdings, stocks, fixed-incomesecurities), solvency and geographic location.A continuous risk analysis is performed by our invest-ment management. Allianz Global Corporate & SpecialtyAG holds a conservative investment portfolio. At the endof the year, the portfolio contained no stocks (except forparticipations). By means of various stress scenarios weregularly monitor the sensitivity of the portfolio withrespect to market changes such as falling stock prices oryield curve shifts.Market risks from derivatives are assessed and controlledby means of up-to-date value-at-risk calculations, stresstests and the setting of limits.

Due to the international orientation of the business ofAllianz Global Corporate & Specialty, large parts of thereserves are constituted in foreign currencies.Overall, the share of foreign currencies of the insurancereserves including unearned premiums amounts toapproximately 41 percent. Our primary exposures arein USD (24 percent) and GBP (9 percent). Allianz GlobalCorporate & Specialty AG actively controls the currencyrisks resulting from this situation. This process takesinto account all balance sheet items subject to currencyconversion. In addition to provisions, this also includesall receivables and liabilities as well as investments inforeign currencies. To hedge our currency exposure wealso use FX derivatives within precisely defined limits toobtain an effective and timely minimization of currencyrisks. The monthly control of currency risks is based onmonthly data.

In fiscal 2012, the current premium and investmentincome of Allianz Global Corporate & Specialty AGexceeded claims payouts and expenses. To be able tocope with possible liquidity risks that might arise none-theless, a large part of our investments are in highlyliquid government bonds, and our insurance commit-ments are to the greatest extent backed by funds withmatching maturities. Constant surveillance is ensuredthrough rolling wave planning of short, medium andlong-term liquidities and by continuous liquidity andcash flow analyses.

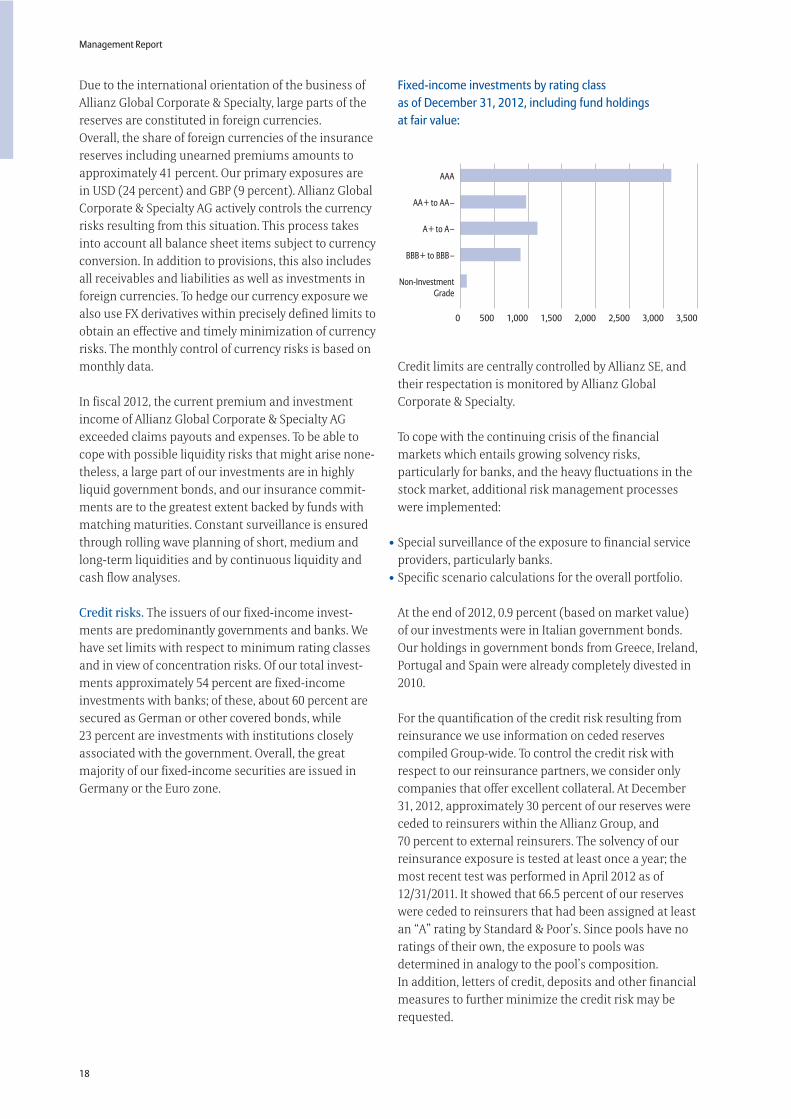

Credit risks. The issuers of our fixed-income invest-ments are predominantly governments and banks. Wehave set limits with respect to minimum rating classesand in view of concentration risks. Of our total invest-ments approximately 54 percent are fixed-incomeinvestments with banks; of these, about 60 percent aresecured as German or other covered bonds, while23 percent are investments with institutions closelyassociated with the government. Overall, the greatmajority of our fixed-income securities are issued inGermany or the Euro zone.

Fixed-income investments by rating classas of December 31, 2012, including fund holdingsat fair value:

Credit limits are centrally controlled by Allianz SE, andtheir respectation is monitored by Allianz GlobalCorporate & Specialty.

To cope with the continuing crisis of the financialmarkets which entails growing solvency risks,particularly for banks, and the heavy fluctuations in thestock market, additional risk management processeswere implemented:

Special surveillance of the exposure to financial serviceproviders, particularly banks.Specific scenario calculations for the overall portfolio.

At the end of 2012, 0.9 percent (based on market value)of our investments were in Italian government bonds.Our holdings in government bonds from Greece, Ireland,Portugal and Spain were already completely divested in2010.

For the quantification of the credit risk resulting fromreinsurance we use information on ceded reservescompiled Group-wide. To control the credit risk withrespect to our reinsurance partners, we consider onlycompanies that offer excellent collateral. At December31, 2012, approximately 30 percent of our reserves wereceded to reinsurers within the Allianz Group, and70 percent to external reinsurers. The solvency of ourreinsurance exposure is tested at least once a year; themost recent test was performed in April 2012 as of12/31/2011. It showed that 66.5 percent of our reserveswere ceded to reinsurers that had been assigned at leastan “A” rating by Standard & Poor’s. Since pools have noratings of their own, the exposure to pools wasdetermined in analogy to the pool’s composition.In addition, letters of credit, deposits and other financialmeasures to further minimize the credit risk may berequested.

18

Management Report

3,000 3,5002,5002,0001,5001,0005000

AAA

AA + to AA –

A + to A –

BBB + to BBB –

Non-InvestmentGrade

•

•

Allianz Global Corporate & Specialty AG

19

At December 31, 2012, total third-party receivables withdue dates exceeding 90 days amounted to € 38.2 million(not including write-offs for impairment). The averagedefault rate for the past three years was 1 percent.

Operational risks refer to losses which arise becausebusiness processes, employees or systems areinappropriate and entail unfavorable developments,because external events such as power failures orflooding cause a business interruption, because lossesare incurred through employee fraud or because thecompany loses a law suit. Operational risks arecontrolled by a comprehensive system of internalsecurity measures and checks as well as a multitude oftechnical and organizational measures. Among others,these include IT safety such as backup systems and fire-walls, as well as internal control systems (for examplethe four-eye principle). The independent Internal Auditregularly examines our internal control processes.In particular, all processes that can have an impact onfinancial reporting are documented and examined.Possible risks are minimized by controls. The imple-mentation and internal testing of the correspondingcontrols was applied to the full fiscal year 2012.Following a structured approach, we regularly examinescenarios representing possible operational risks.We meet the requirements of our expanding businessas an industrial insurer by continually integrating andupgrading our IT system landscape, for example throughthe introduction of Global Genius, a system for theworldwide uniform administration of our insurancecontracts.

Limiting our legal risks is an essential task that iscarried out by our legal department with the support ofthe other specialized departments. The objective is toensure that laws are observed, to react appropriately toall impending legislative changes or new court rulings,attend to legal disputes and litigation, and providelegally suitable solutions for transactions and businessprocesses. Other, non quantifiable risks such as strategicand reputational risks are assessed and evaluated inqualitative terms as part of a Top Risk Assessment atleast once a year. Special attention was given to risksarising from the current macro-economic situation inthe European economic area. In addition to monitoringrisks stemming from the present economic context, itwas also made sure that strategic business decisionswere effectively implemented.

Reputational risks are controlled by including allpotentially concerned functions such as investments,underwriting, human resources, communication andthe legal department. To avoid risks resulting from apossible damage to the company’s reputation becauseof the negative public perception of our actions, certaincritical decisions are subject to a rigorous review processthat actively involves the communication departmentas well as risk management, if required.

Risk bearing capacity

The solvency test in the fourth quarter of 2012 waspassed with 293 percent. In addition, the stress testsrequired by the German Federal Financial SupervisoryAuthority were passed with a wide safety margin. Dueto our systematic planning and implementation of therequirements of the European Solvency II Project we arealso well prepared for future regulatory requirements.The actual risk situation, which, with the help of stresstests, also tests the risk of future developments, thusremains largely within the company’s risk bearingcapacity.

In planning the future development of the company,AGCS takes into account a three-year time horizon.The current planning for the time horizon 2013 to 2015,with a focus on 2013, is based on the assumption thatour business results will continue their positivedevelopment.

Outlook

For 2013, Allianz Global Corporate & Specialty AGexpects only slight premium growth. The main driverwill be the planned expansion in the so-called growthmarkets, primarily in selected countries in Asia, LatinAmerica and Africa. Depending on our positioning inthe respective markets, growth will be achieved mainlyin direct business, e.g. in Asia, where Allianz GlobalCorporate & Specialty AG operates its own branch officesin Singapore and Hong Kong, or mostly in the indirect,reinsured business, particularly in those countries,where other units of the Allianz Group sign business forAllianz Global Corporate & Specialty AG. Due to thecreation of a separate reinsurance company in Brazil asa subsidiary of Allianz Risk Transfer AG, Zurich, at theend of 2012, the Brazilian reinsurance business ofAllianz Global Corporate & Specialty AG is likely todecline in 2013. The by far greatest growth in 2013 isexpected to come from Financial Lines and Energy, dueto special initiatives in these areas.In addition, it is planned to merge AGCS (France), Paris,with Allianz Global Corporate & Specialty AG in 2013. Inthis context, Allianz Global Corporate & Specialty AG isto be transformed into a Societas Europaea (SE). In 2012,AGCS (France) reported a gross premium volume of€ 607.8 million. At December 31, 2012, the investmentsof AGCS (France) amounted to € 1,367.5 million and itsunderwriting reserves to € 1,005.3 million. In the courseof the intended merger, the existing reinsurance relationsbetween the two companies (€ 43.6 gross premiumswritten in 2012) will be terminated.

The imminent slow-down of global economic growthand the recession in the Euro zone as well as increasingcompetition and overcapacities give no reason to expecta general recovery of rates across all regions andinsurance segments. If at all, isolated positive pricedevelopments may be achievable in certain markets.

Our focus on profitability remains unchanged. For 2013,we are aiming for a combined ratio of about 95 percent.Due to the required investments for the establishmentor expansion of our operations in growth markets, weexpect a slight increase of the cost ratio in 2013.

The existing reinsurance concept of Allianz GlobalCorporate & Specialty AG will be continued essentiallyunchanged in 2013. In some segments such as Aviation,Natural Catastrophes and Liability, coverage wasextended to meet increasing capacity demands.In Marine insurance, however, coverage limitations hadto be accepted since the reinsurance market as a resultof various market events only offers lower coverageamounts than in the past.

Management Report

20

Allianz Global Corporate & Specialty AG is going topursue its safety-oriented investment strategy in thefuture. In this respect the company will continue to relyon the Allianz Group’s wealth of experience with invest-ments in Germany and other counties. To reduce thedependence on developments in the capital marketsand to further diversify the investment portfolio ofAllianz Global Corporate & Specialty AG we are planninginvestments in real estate and inflation-proof debtsecurities. These plans are based on the assumptionthat the capital markets will be stable. Safety-orientedinvestments in conjunction with the interest ratedevelopments of the past years lead us to expect adecline of interest income in the coming years. For thisreason we assume that the overall result before transferof profit will be at a lower level in the next two years.Because of the persistent insecurity with respect tofuture developments in the capital markets, the comingyears may have a corresponding negative or, conversely,positive impact on the market value and investmentresults of Allianz Global Corporate & Specialty AG.

The above statements are subject to the proviso thatnatural disasters, adverse developments in the capitalmarkets or other factors may undermine the validityof our forecasts to a greater or lesser extent.

Munich, February 28, 2013Allianz Global Corporate & Specialty AG

The Board of Management

Dr. Theis Berger Browne Fischer Hirs Mai MoossmannScaldaferri

21

Annual Financial Statementsof Allianz Global Corporate & Specialty AG

Annual Financial Statements

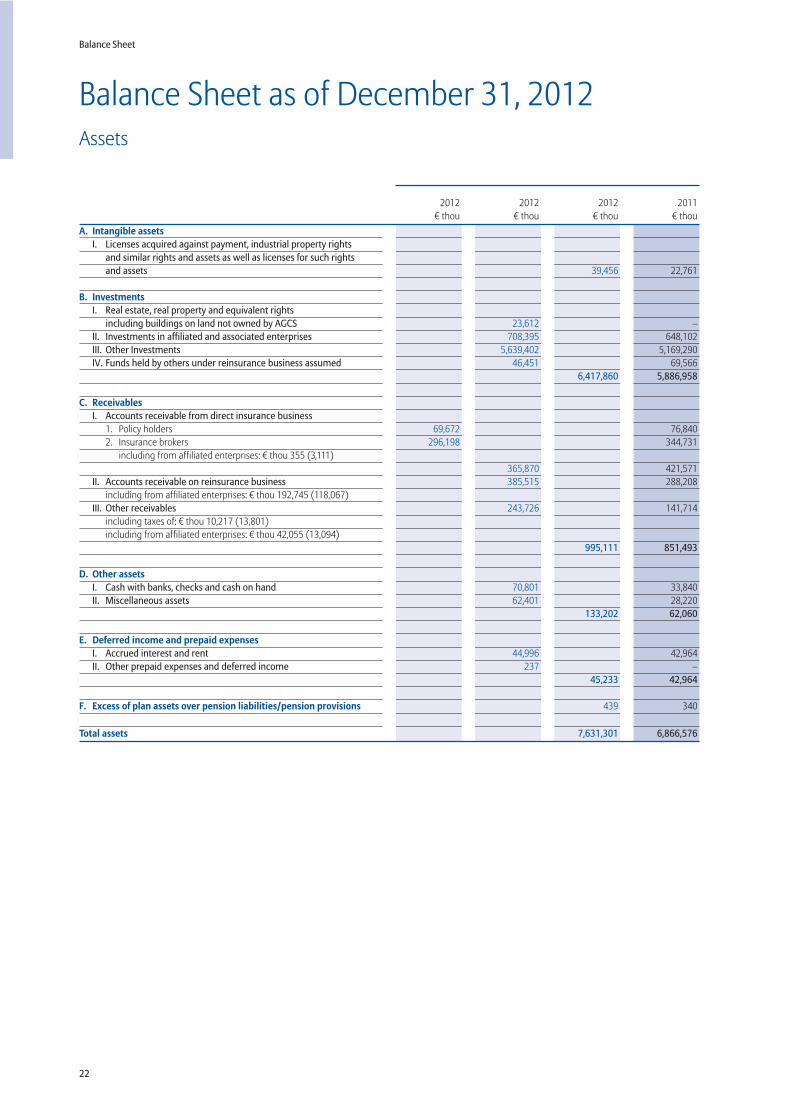

Balance Sheet as of December 31, 2012Assets

22

Balance Sheet

2011€ thou

2012€ thou

2012€ thou

2012€ thou

A. Intangible assetsI. Licenses acquired against payment, industrial property rights

and similar rights and assets as well as licenses for such rightsand assets 39,456 22,761

B. InvestmentsI. Real estate, real property and equivalent rights

including buildings on land not owned by AGCS 23,612 –II. Investments in affiliated and associated enterprises 708,395 648,102III. Other Investments 5,639,402 5,169,290IV. Funds held by others under reinsurance business assumed 46,451 69,566

6,417,860 5,886,958

C. ReceivablesI. Accounts receivable from direct insurance business

1. Policy holders 69,672 76,8402. Insurance brokers 296,198 344,731

including from affiliated enterprises: € thou 355 (3,111)365,870 421,571

II. Accounts receivable on reinsurance business 385,515 288,208including from affiliated enterprises: € thou 192,745 (118,067)

III. Other receivables 243,726 141,714including taxes of: € thou 10,217 (13,801)including from affiliated enterprises: € thou 42,055 (13,094)

995,111 851,493

D. Other assetsI. Cash with banks, checks and cash on hand 70,801 33,840II. Miscellaneous assets 62,401 28,220

133,202 62,060

E. Deferred income and prepaid expensesI. Accrued interest and rent 44,996 42,964II. Other prepaid expenses and deferred income 237 –

45,233 42,964

F. Excess of plan assets over pension liabilities/pension provisions 439 340

Total assets 7,631,301 6,866,576

23

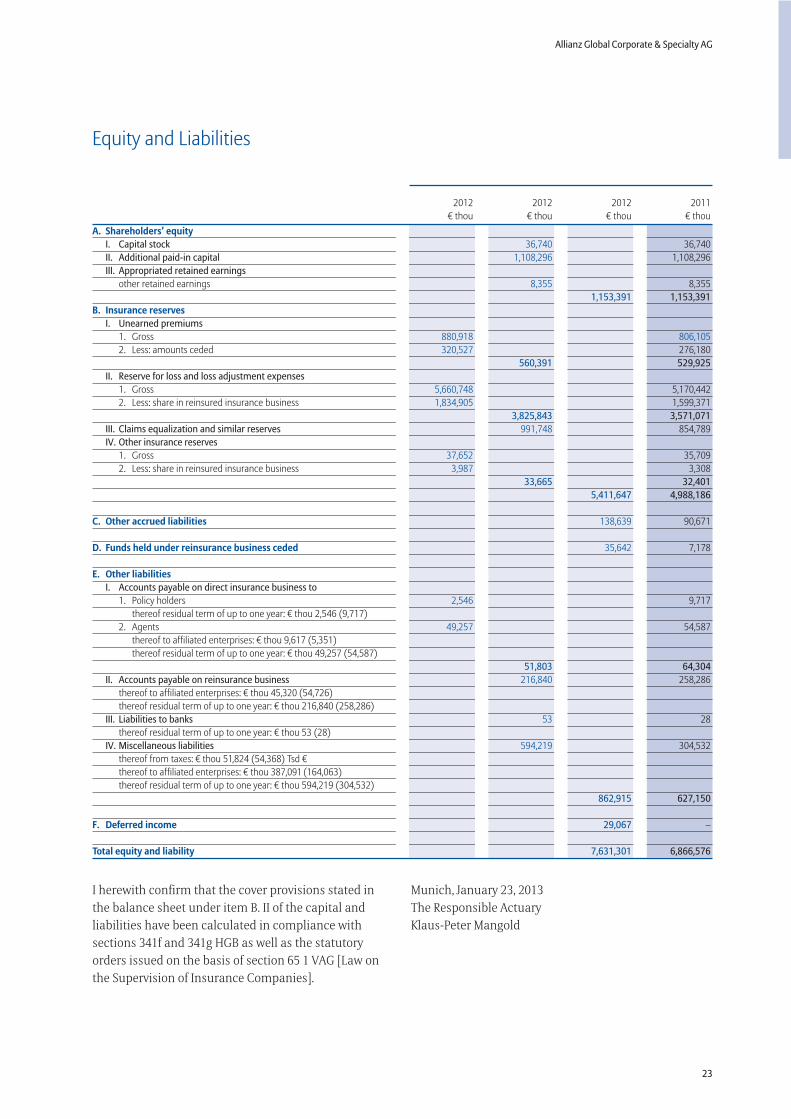

Allianz Global Corporate & Specialty AG

Equity and Liabilities

2011€ thou

2012€ thou

2012€ thou

2012€ thou

A. Shareholders’ equityI. Capital stock 36,740 36,740II. Additional paid-in capital 1,108,296 1,108,296III. Appropriated retained earnings

other retained earnings 8,355 8,3551,153,391 1,153,391

B. Insurance reservesI. Unearned premiums

1. Gross 880,918 806,1052. Less: amounts ceded 320,527 276,180

560,391 529,925II. Reserve for loss and loss adjustment expenses

1. Gross 5,660,748 5,170,4422. Less: share in reinsured insurance business 1,834,905 1,599,371

3,825,843 3,571,071III. Claims equalization and similar reserves 991,748 854,789IV. Other insurance reserves

1. Gross 37,652 35,7092. Less: share in reinsured insurance business 3,987 3,308

33,665 32,4015,411,647 4,988,186

C. Other accrued liabilities 138,639 90,671

D. Funds held under reinsurance business ceded 35,642 7,178

E. Other liabilitiesI. Accounts payable on direct insurance business to

1. Policy holders 2,546 9,717thereof residual term of up to one year: € thou 2,546 (9,717)

2. Agents 49,257 54,587thereof to affiliated enterprises: € thou 9,617 (5,351)thereof residual term of up to one year: € thou 49,257 (54,587)

51,803 64,304II. Accounts payable on reinsurance business 216,840 258,286

thereof to affiliated enterprises: € thou 45,320 (54,726)thereof residual term of up to one year: € thou 216,840 (258,286)

III. Liabilities to banks 53 28thereof residual term of up to one year: € thou 53 (28)

IV. Miscellaneous liabilities 594,219 304,532thereof from taxes: € thou 51,824 (54,368) Tsd €thereof to affiliated enterprises: € thou 387,091 (164,063)thereof residual term of up to one year: € thou 594,219 (304,532)

862,915 627,150

F. Deferred income 29,067 –

Total equity and liability 7,631,301 6,866,576

I herewith confirm that the cover provisions stated inthe balance sheet under item B. II of the capital andliabilities have been calculated in compliance withsections 341f and 341g HGB as well as the statutoryorders issued on the basis of section 65 1 VAG [Law onthe Supervision of Insurance Companies].

Munich, January 23, 2013The Responsible ActuaryKlaus-Peter Mangold

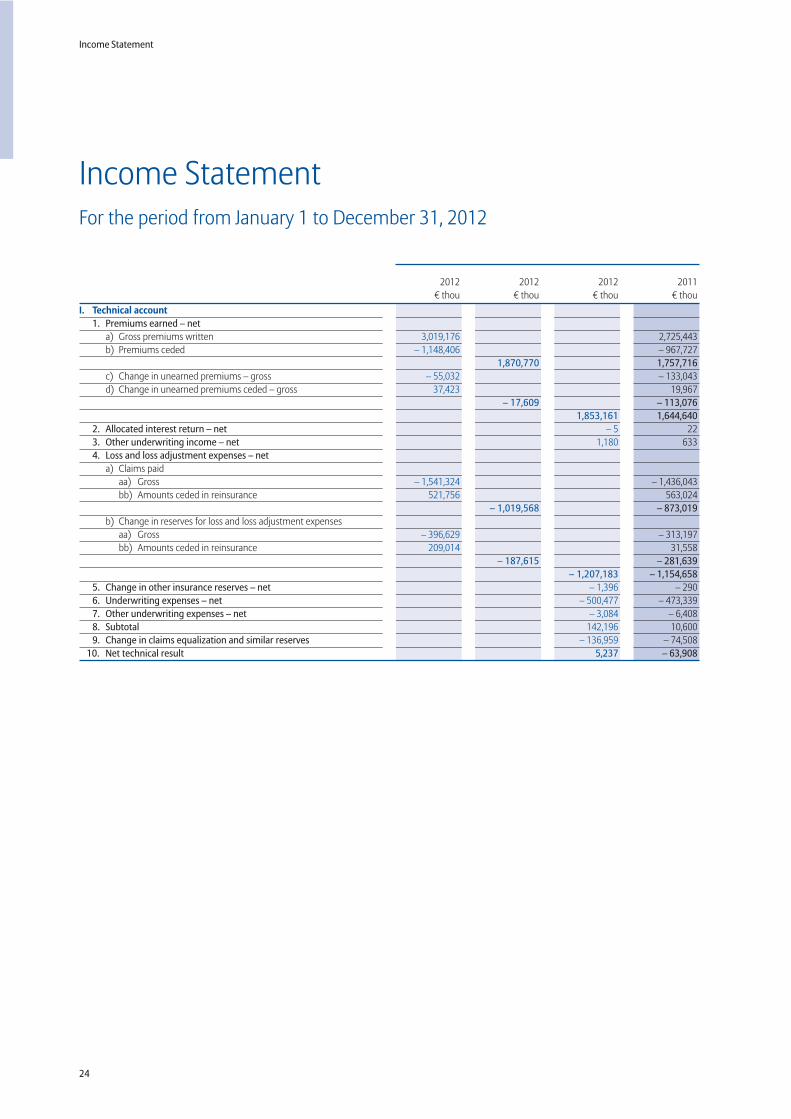

Income StatementFor the period from January 1 to December 31, 2012

24

Income Statement

2011€ thou

2012€ thou

2012€ thou

2012€ thou

I. Technical account1. Premiums earned – net

a) Gross premiums written 3,019,176 2,725,443b) Premiums ceded – 1,148,406 – 967,727

1,870,770 1,757,716c) Change in unearned premiums – gross – 55,032 – 133,043d) Change in unearned premiums ceded – gross 37,423 19,967

– 17,609 – 113,0761,853,161 1,644,640

2. Allocated interest return – net – 5 223. Other underwriting income – net 1,180 6334. Loss and loss adjustment expenses – net

a) Claims paidaa) Gross – 1,541,324 – 1,436,043bb) Amounts ceded in reinsurance 521,756 563,024

– 1,019,568 – 873,019b) Change in reserves for loss and loss adjustment expenses

aa) Gross – 396,629 – 313,197bb) Amounts ceded in reinsurance 209,014 31,558

– 187,615 – 281,639– 1,207,183 – 1,154,658

5. Change in other insurance reserves – net – 1,396 – 2906. Underwriting expenses – net – 500,477 – 473,3397. Other underwriting expenses – net – 3,084 – 6,4088. Subtotal 142,196 10,6009. Change in claims equalization and similar reserves – 136,959 – 74,508

10. Net technical result 5,237 – 63,908

25

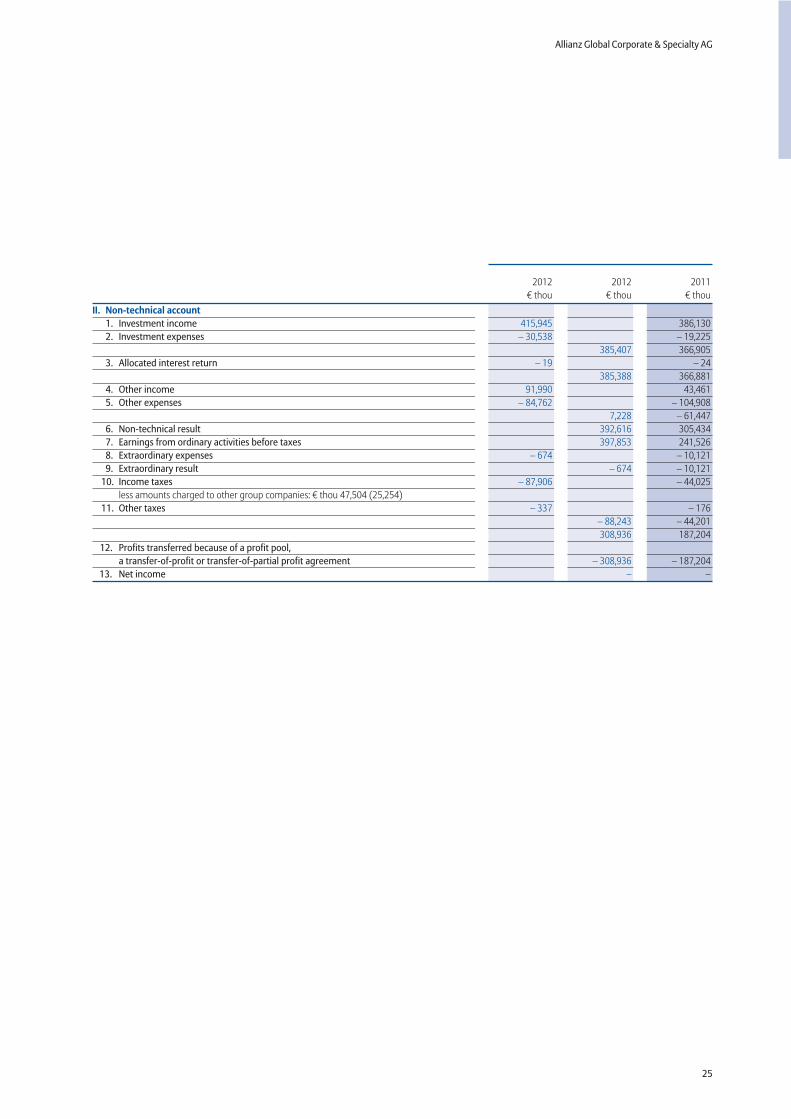

Allianz Global Corporate & Specialty AG

2011€ thou

2012€ thou

2012€ thou

II. Non-technical account1. Investment income 415,945 386,1302. Investment expenses – 30,538 – 19,225

385,407 366,9053. Allocated interest return – 19 – 24

385,388 366,8814. Other income 91,990 43,4615. Other expenses – 84,762 – 104,908

7,228 – 61,4476. Non-technical result 392,616 305,4347. Earnings from ordinary activities before taxes 397,853 241,5268. Extraordinary expenses – 674 – 10,1219. Extraordinary result – 674 – 10,121

10. Income taxes – 87,906 – 44,025less amounts charged to other group companies: € thou 47,504 (25,254)

11. Other taxes – 337 – 176– 88,243 – 44,201308,936 187,204

12. Profits transferred because of a profit pool,a transfer-of-profit or transfer-of-partial profit agreement – 308,936 – 187,204

13. Net income – –

26

Notes to the Financial Statements

Notes to the Financial Statements

Applicable legal regulations

The company’s Financial Statements and the Manage-ment Report are prepared in accordance with theregulations contained in the German Commercial Code(HGB), taking into account the Accounting LawModernization Act (“Bilanzrechtsmodernisierungs-gesetz, BilMoG”), the Corporation Law (AktG), the Lawon the Supervision of Insurance Enterprises (VAG), andthe Government Order on the External AccountingRequirements of Insurance Enterprises (RechVersV).The amounts in the financial statements are stated inEuro thousand (€ thou).

Accounting, valuationand calculation methods

Intangible assets

These are recorded at their acquisition cost lesstax-allowable depreciation.

Real estate, real property and equivalent rights includingbuildings on land not owned by AGCS

These items are recorded at cost less accumulatedscheduled and unscheduled depreciation. Scheduleddepreciation is measured according to ordinary usefullife. In case of probable permanent impairment, thevalues of these items are adjusted through unscheduledwrite-downs.

Shares in affiliated enterprises, loans to affiliatedenterprises, participations

These are valued according to the moderate lower-valueprinciple and carried at amortized cost or a lower long-term fair value.

Write-downs are made if the amortized cost ofacquisition at the balance sheet date is higher thanthe market value or the long-term fair value.

Other investments

Stocks, interests in funds, debt securities, and other fixedand variable income securities

Securities held as current assets according to section341b HGB in conjunction with section 253 (1), (4) and(5) HGB are valued in accordance with the strict lower-value principle and carried at average cost of acquisitionor the lower market value.

Investments recognized in accordance with the rulesapplicable to fixed assets are intended to serve thebusiness on a permanent basis. Their purpose isattributed at the time the investment is added. Theattribution is reviewed when changes in the investmentstrategy are made or a divestment is considered. Thesesecurities are valued in accordance with the moderatelower-value principle and reported at average acquisitioncosts or a lower long-term fair value. Permanent impair-ments are recognized in the Income Statement. Forimpairments deemed to be temporary there is a choicewith respect to their amortization. As in the previousfiscal year, AGCS in 2012 opted to not recognizetemporary impairments for economic reasons. Thisresults in undisclosed liabilities.

Registered bonds, debentures and loans

These are valued according to the moderate lower-valueprinciple and carried at amortized cost.

For registered bonds, debentures and loans thedifference between acquisition cost and redemptionamount is amortized over the remaining period basedon the effective interest method.

Write-downs are made if the amortized cost ofacquisition at the balance sheet date is higher thanthe market value or the long-term fair value.

Bank deposits

These are recorded at face value.

27

Allianz Global Corporate & Specialty AG

Requirement to reinstate original values and write-ups

The requirement to reinstate original values applies toassets that were written down to a lower market valuein past years. If their value at the balance sheet date ishigher than the book value, they must be written upagain. The write-up is made either up to amortized costor to a lower long-term or market value.

Funds held by others under reinsurance business assumed

In accordance with section 341c HGB these items arerecorded at face value.

Receivables and other assets

These include the following:a) accounts receivable on direct insurance businessb) accounts receivable on reinsurance businessc) other receivablesd) cash with banks, checks and cash on hande) other assets

These are recorded at face value less repayments.For accounts receivable from direct insurance business,general loss allowances are made to account for thecredit risk.

Other assets are carried at acquisition cost lesscumulated depreciation. Low-value assets worth up to€ 150 are written off immediately. A compound item fortax purposes was formed in accordance with section 6(2 a) of the German Income Tax Act (EStG) for assetsfrom € 150 to € 1,000. This item is released with profit-decreasing effect in the year of formation and in thesubsequent four years, by one fifth in each year.

Plan assets

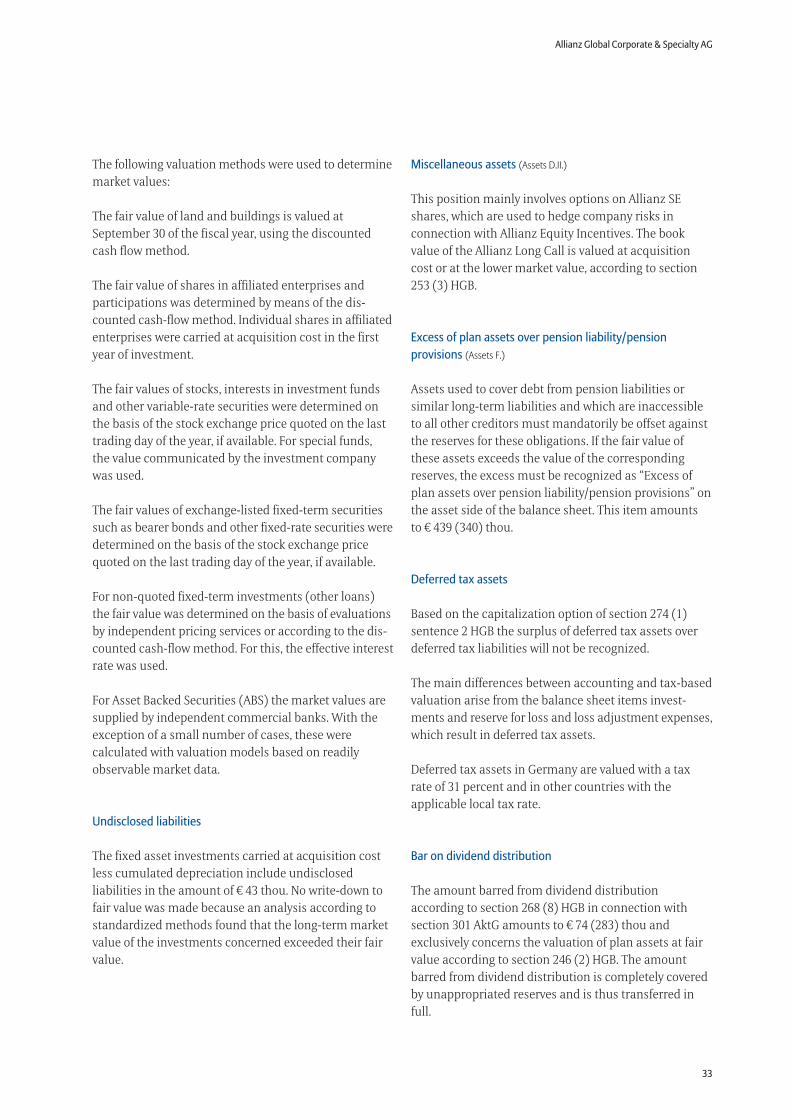

Securities to meet liabilities resulting from retirementprovision commitments are valued at fair value inaccordance with section 253 (1) HGB and offset againstthe liabilities in accordance with section 246 (2) HGB.

Deferred tax assets

The company does not use its capitalization optionaccording to section 274 (1) HGB to constitute a deferredtax asset on the temporary difference between theaccounting valuation of assets, liabilities and deferredincome/prepaid expenses and their tax-based valuation,if these differences will result in tax relief in the follow-ing years.

Insurance reserves