Embed Size (px)

Citation preview

All information sources cited in this presentation are available upon request.

Presented by: Martin H. Ruby, FSAStonewood Financial Solutions

The New Rules of Saving For Your Future

Why You Need a New Set of Rules

1985 vs.

2015

Meet Jim

Things That Were Popular in 1985

Things That Are Popular in 2015

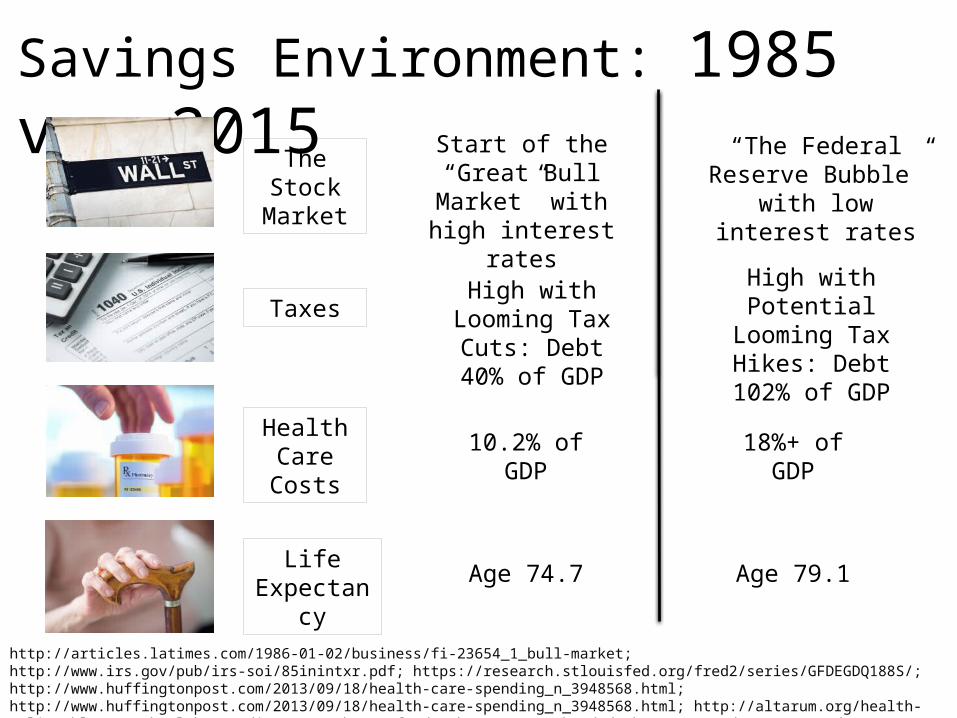

Savings Environment: 1985 vs. 2015

http://articles.latimes.com/1986-01-02/business/fi-23654_1_bull-market; http://www.irs.gov/pub/irs-soi/85inintxr.pdf; https://research.stlouisfed.org/fred2/series/GFDEGDQ188S/; http://www.huffingtonpost.com/2013/09/18/health-care-spending_n_3948568.html; http://www.huffingtonpost.com/2013/09/18/health-care-spending_n_3948568.html; http://altarum.org/health-policy-blog/u-s-health-spending-as-a-share-of-gdp-where-are-we-headed; http://www.data360.org/dsg.aspx?Data_Set_Group_Id=195

The Stock Market

Start of the “Great Bull Market” with high interest rates

“The Federal Reserve Bubble” with low

interest rates

TaxesHigh with

Looming Tax Cuts: Debt 40% of GDP

High with Potential Looming

Tax Hikes: Debt 102% of GDP

Health Care Costs

Life Expectancy

10.2% of GDP 18%+ of GDP

Age 74.7 Age 79.1

Accumulati

on (Sav

ing Years)

Deccumulation (Spending Years)

Retirement

1985: What We Thought Retirement Planning Would Be

Accumulation (S

aving Ye

ars)Deccumulation (Spending Years)

Retirement

2015: What We Know Retirement Planning To Be

RisksRisks

Assessing Your Risks

Buckets of Funds in RetirementLiving Expenses(Base Income)

Lifestyle Expenses (Additional Income)

• Pension• 401(k)/ IRA• Social

Security

• 401(k)• IRA• CD Savings• Annuities• Savings

Account

Emergency Savings(Rainy Day Fund)

• Savings Account

• LTC Insurance

• 401(k)• Savings

Account• Life

Insurance

Legacy Savings(Inheritance)The Market

Taxes

Health Expenses

Lifespan

THE MARKETGetting Your

Funds to Grow

http://articles.latimes.com/1986-01-02/business/fi-23654_1_bull-market

What worked:

Putting your funds in the market.

Earning meaningful returns on more secure vehicles

1985

00 01 02 03 04 05 06 07 08 09 10 11 12 13 14$40,000

$60,000

$80,000

$100,000

$120,000

$140,000

$160,000

$180,000

$200,000

$220,000

$240,000

$260,000

$280,000

-9.10% -11.89%

-22.10%

28.68%10.88%

4.91%

15.79%5.49%

-37.00%

26.46%

15.06% 2.11%

16.00%

32.39%

13.69%

Annual Total Return of the S&P 500

Total Return of the Stock Market (including dividends)

Data used to create this chart was obtained from: Yahoo Finance GSPC Historical Prices

This example is for illustrative purposes only and should not be deemed a representation of future results, and is no guarantee of return or future performance. This information is not intended to provide any tax, legal or investment advice or provide the basis for any financial decision. Be sure to speak with a qualified professional before making any decisions about your personal situation.

$186,428 4.2% average annual return

-1% average annual return

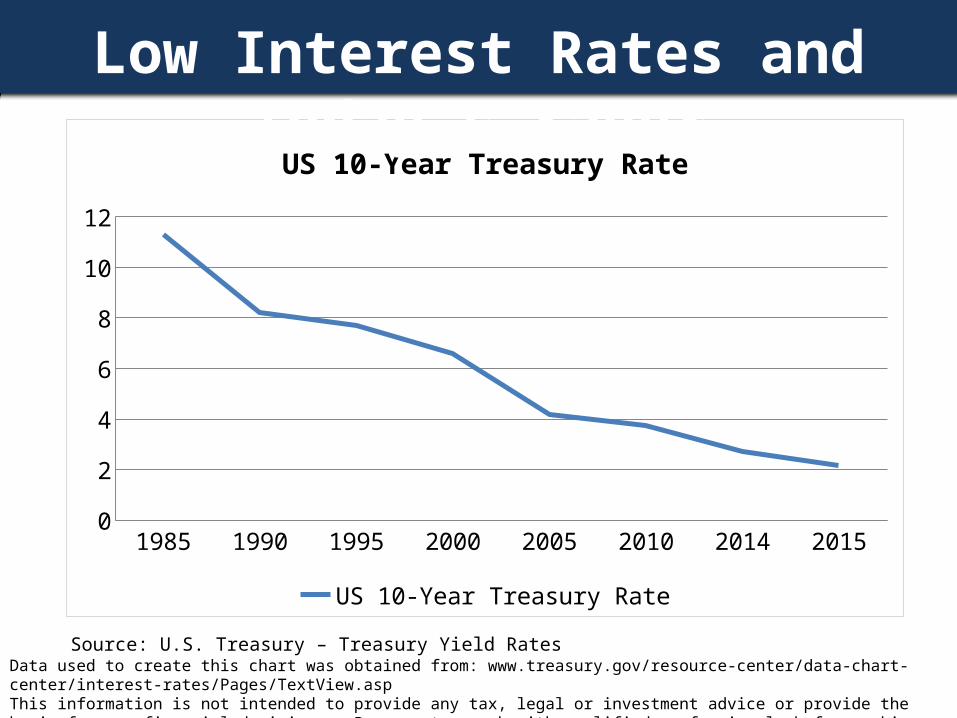

1985 1990 1995 2000 2005 2010 2014 20150

2

4

6

8

10

12

US 10-Year Treasury Rate

US 10-Year Treasury Rate

Source: U.S. Treasury – Treasury Yield RatesData used to create this chart was obtained from: www.treasury.gov/resource-center/data-chart-center/interest-rates/Pages/TextView.aspThis information is not intended to provide any tax, legal or investment advice or provide the basis for any financial decisions. Be sure to speak with qualified professionals before making any decisions about your personal situation.

Low Interest Rates and Today’s Saver

2015What works:

Finding ways to achieve meaningful growth while also protecting funds from market fluctuations.

TAXESHow Much You

Get to Keep

1985What worked:

Assuming you’d be in a lower tax bracket in the future.

Not worrying about future tax burden

This information is not intended to provide tax, legal or investment advice. Be sure to speak with qualified professionals before making any decisions about your personal situation.

Taxable

• Stock accounts• Brokerage accounts• CDs• Money Market Funds• Savings Accounts• Social Security

This information is not intended to provide tax, legal or investment advice. Be sure to speak with qualified professionals before making any decisions about your personal situation.

Taxation as You Accumulate Funds

• 401(k)s• 403(b)s• Traditional IRAs• Tax-deferred

Annuities• Savings Bonds

• Roth 401(k)s • Roth IRAs• Life Insurance• Municipal Bonds

Tax Deferred Tax Free

Benefits of Your Tax Strategy

This hypothetical example does not consider every product or feature of tax-deferred accounts and is for illustrative purposes only. It should not be deemed a representation of past or future results, and is no guarantee of return or future performance. This information is not intended to provide tax, legal or investment advice. Be sure to speak with qualified professionals before making any decisions about your personal situation.

Tax Status Benefits Drawbacks

TaxableMay be the only way to access the kind of assets you want

You must pay taxes on your earnings every year

Tax DeferredNo annual taxes on earnings

When funds are withdrawn, you must pay taxes on earnings, and in some cases on contributions, too

Tax FreeNo taxes paid on earnings in the account

You must use after-tax dollars to fund these assets

Are Taxes Going Up or Down?

This information is not intended to provide tax, legal or investment advice. Be sure to speak with qualified professionals before making any decisions about your personal situation.

Four Ways You Can End Up Paying More Taxes Than Planned

Move Into a Higher

Tax Bracket

Raise All Tax Rates

Lose Tax Deductions

Enact “Stealth”

Taxes

This information is not intended to provide tax, legal or investment advice. Be sure to speak with qualified professionals before making any decisions about your personal situation.

2015What works:

Tax diversification Improving the tax

status of each of your assets.

HEALTHYour Medical Costs of Aging

1985What worked:

Relying on Medicare and Social Security for your healthcare needs.

65 year old healthy couple’s total healthcare costs in retirement:

55 year old healthy couple’s total healthcare costs in retirement (starting age 65):

2015 Retirement Health Care Cost Data Report, HealthView Insights, January 2015

55-year old couple who lives TWO YEARS beyond average life expectancy =

Health Costs In Retirement

$394,954

$463,849

additional $57,353

Percent of Social Security Income being used for medical expenses:

Assumptions: 66-year old couple with SSI primary insurance amount of $25,332. Future dollars based on 2% annual COLA Increase. Data obtained from 2015 Retirement Health Care Cost Data Report, HealthView Insights, January 2015

Cutting Into Your Social Security Benefit

AGE 80 AGE 87

68% 89%

https://www.genworth.com/corporate/about-genworth/industry-expertise/cost-of-care.htmlhttp://longtermcare.gov/the-basics/who-needs-care/

The Cost of Long-Term Care

Average cost for assisted living facility: $32,400 a year

Average cost for nursing home care: $67,525 a year

Chance of a 70-year old couple needing long-term care: 80%

2015What works:

Establishing additional resources for long-term care and medical costs.

LIFESPANHow Long Do Your Funds

Have to Last?

1985

What worked:

Planning to live 15 to 20 years in retirement

80 85 90 950%

10%

20%

30%

40%

50%

60%

70%

80%

90%

MaleFemale

Percentage of 65-year olds who will live to…

Data used to create this chart was sourced from: American Academy of Actuaries “Lifetime Income: Risks and Solutions,” Oct. 26, 2011. Based on 75% of Social Security Mortality in 2007.

https://www.fidelity.com/viewpoints/retirement/8X-retirement-savings

Why It Matters

8595

Live to Age

Live to Age

6.2 times your last working salary in savings

8.6 times your last working salary in savings

2015

What works:

Planning to live 20 to 30 years in retirement

New Savings Rules for 2015

Have a strategy to grow your funds AND protect them from market fluctuations

Improve the tax status of your assets

Establish additional funds to cover the medical cost of aging

Have a strategy to make your funds last as long as you do

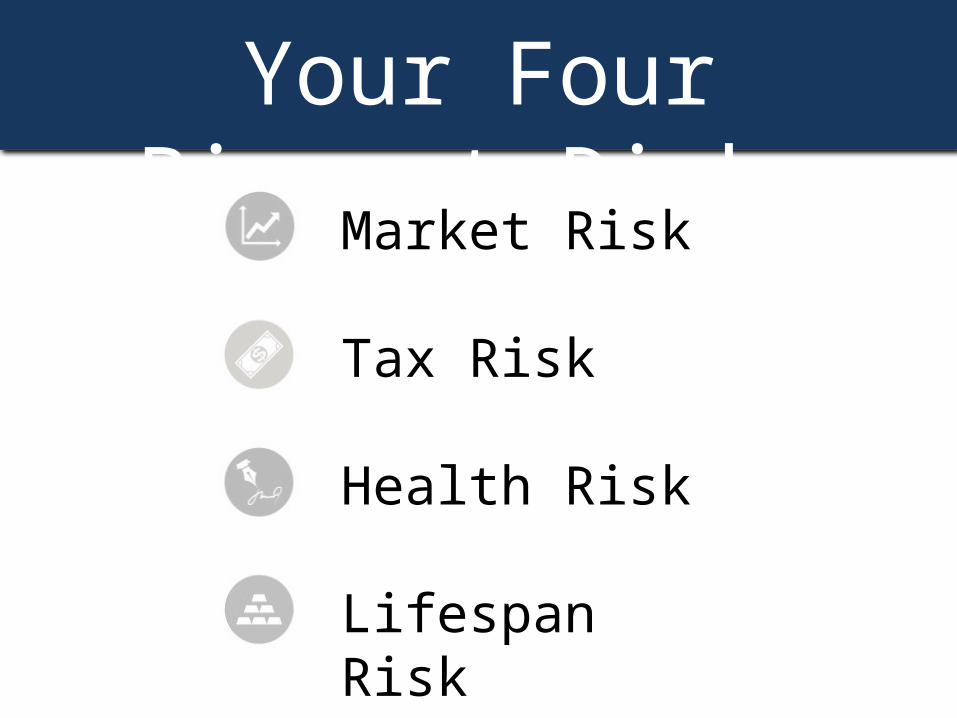

Addressing Your Risks

Your Four Biggest Risks

Market Risk

Tax Risk

Health Risk

Lifespan Risk

Are you concerned about these risks?

Are you prepared to handle them?

Accomplishing Your GoalsThere are financial strategies that can:

Allow you to participate in good markets while protecting you for down markets

Deliver additional funds for long-term care from savings assets

Completely eliminate the risk of outliving your assets

Improve the tax status of your funds

Helping JimJim had at $50,000 CD but was frustrated it was earning very little.

We created a strategy to help those funds:

- Grow, with meaningful rates of return

- Stay protected and secure

- Offer additional funds for long-term care needs

- Remain liquid should he need to access them

Helping Ann MarieAnne Marie had a 401(k), but she wasn’t sure how to make it last throughout her retirement.

We created a strategy to help those funds:

- Deliver guaranteed income for as long as she lived

- Continue growing

- Potentially offer benefits for her spouse

Helping Scott

Scott was very concerned with his tax liability on his retirement savings.

We created a strategy to help those funds:

- Grow tax-free

- Diversify his tax liability

- Offer additional funds for long-term care needs

This information is not intended to provide tax, legal or investment advice. Be sure to speak with qualified professionals before making any decisions about your personal situation.

Complimentary No-Obligation

Risk ReviewAnalyze your current approach

Identify areas of exposure or under performance

Recommend areas for improvement

All information sources cited in this presentation are available upon request. This presentation is for informational purposes only. It is not intended to provide legal, tax or investment advice. Be sure to consult a qualified professional about your individual situation. The presenter is licensed to sell insurance. By setting up a meeting with this advisor, you may be offered information about life insurance products. .

Stonewood Financial Solutions

(502) 588-7155StonewoodFinancial.com

![fsa imagery [Read-Only] · PDF fileObjectives of Presentation: ... FSA Imagery Requirements ... FSA Ortho Large Format FSA Ortho DOQs Small Format GIS Possible Yes Yes FAA](https://img.pdfslide.us/doc/110x75/5ab947c47f8b9ad5338dc355/fsa-imagery-read-only-of-presentation-fsa-imagery-requirements-fsa-ortho.jpg)

![Ruby on Rails [ Ruby On Rails.ppt ] - [Ruby - [Ruby-Doc.org](https://img.pdfslide.us/doc/110x75/5491e450b479597e6a8b57d5/ruby-on-rails-ruby-on-railsppt-ruby-ruby-docorg-.jpg)