Embed Size (px)

Citation preview

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006

September 1, 2006 To: Our valued clients, friends and overseas affiliates

BUDGET 2007 Summary & Comments

We are proud once again this year to present our own BUDGET 2007 : Summary & Comments, a summary and synopsis of the 2007 Budget proposals. Our focus in this summary has been on matters, which we reckoned to be important and useful to the reader with useful information to assist them in proper planning and decision making for year ahead. For ease of reference and reading, the summary has been arranged into eight sections as follows:

Disclaimer: This publication is distributed gratuitously and without liability. AljeffriDean, Chartered Accountants and its associates, partners and employees disclaim all and any liability and responsibility to any person whosoever in respect of anything and of the consequences of anything done or omitted to be done by any such person in reliance wholly or partly upon the whole or any part of the contents of this publication.

Section Page

A Commentary

1

B Highlights

3

C Summary of Amendments to Direct Taxation

6

D Summary of Amendments to Indirect Taxation

25

E Summary of Business Opportunities and Other Incentives

31

F Synopsis and Comparison

43

G Summary of Revenues and Allocations

83

H Tax Rates & Relief 86

AljeffriDean

1 Friday. September 1, 2006

SECTION A

COMMENTARY

Malaysian National Budget 2007 presented by our Prime Minister and Finance Minister YAB Dato' Seri Abdullah Badawi today has special significant in that it is an indicator as to how the nation implements the national mission in achieving the national vision to achieve a developed status by year 2020.

These can be seen from the number of new initiatives proposed in Budget 2007. Focus has been made on areas that Malaysia has an economic edge particularly in Agriculture, Biotechnology and Islamic Banking.

Many incentives has been proposed to make Malaysia the leading player in Islamic banking in the global arena. Particular attention has also been given to make Malaysia competitive in attracting the setting up of an investment in the Real Estate Investment Trust which will have a positive impact on the real property sectors and derivative market.

We hope the introduction of the very attractive Bionexus Status Tax Incentive will be successful in attracting Foreign Direct Investments just like the Pioneer Status for the manufacturing industry and the MSC Status for the ICT industry for the years prior to this.

The economic development initiatives have been well thought out to place the various Greenfield projects appropriately spread out throughout the country. This includes the proposed locations for: (i) The Bio Innovation Centre in Nilai, Negri Sembilan, (ii) The Beef Valley Project in Gemas, Negri Sembilan, (iii) The Halal Parks in Pasir Mas, Kelantan; Gambang, Pahang; Chendering, Trengganu

and Padang Besar, Perlis, and; (iv) The Ornamental Fish Cluster Project in Penang. Regional specialisation is also being proposed as can be seen from the plan for the Northern Economic Corridor, the South Johor Economic Region and the East Coast Corridor. AljeffriDean hopes that details of the business opportunities such as matching grants, the form of financing through the special funds will be finalised and made available to entrepreneurs and business consultants soonest possible. The reduction of one percentage point for corporate tax, each in 2007 and 2008 although fail to meet the expectation of the corporate taxpayers is nonetheless a reflection of the Government's recognition that the corporate tax rate has to be lower than the current 28% to create a competitive business environment in the region. In this respect, the directive for the introduction of advance rulings in Income Tax Administration and to make available an improved tax audit guide and the framework for tax investigation are most welcome. We hope the initiative will create certainty for the taxpayers to plan and manage their businesses and take comfort that the tax administration in future will be very transparent where there will be uniformity in the process and systems of tax audits and investigations that will not overburden the taxpayers.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 2

The special treatment proposed for the property developers has removed the unwarranted difficulty faced by this industry till now which is not adequately dealt with by the present legislation. We hope this is an indication that the Government listened to the views of the Rakyat and is prepared to response positively to peculiar cases in specific industries. Although the 2007 Budget does not contain spectacular goodies for the general public in the short term, it does provide the dosages to instill confidence in the economic growth of Malaysia in the long term. Good luck Malaysia as we begin to activate the Ninth Malaysia Plan from now till the year 2020.

AljeffriDean Kuala Lumpur September 1, 2006

AljeffriDean

3 Friday. September 1, 2006

SECTION B

HIGHLIGHTS

THE PROSPECT OF MALAYSIAN ECONOMY

• The Gross Domestic Product (GDP) is projected to increase by 6 % for next year.

• Private investment is expected to increase by 10.5% while public investment will continue to grow of 8%.

• It is anticipated that the following sector will recorded growth expected as follow:

• The manufacturing sector - increase by 6.8%

• The service sector (including ICT, tourism and education) - increase by 6%.

• The agriculture sector - increase by 4.7%.

• The construction sector - increase by 3.7%.

• The budget deficit is expected to be reduced to a level 3.4% of GDP in 2007. BUDGET 2007

To Move The Economy Up The Value Chain

• The corporate tax rate will be reduced to 27% in the year assessment 2007 and further reduce 26% for the year assessment 2008.

• The government allocated RM3.6 billion for agriculture sector.

• Khazanah Nasional will establish an agriculture fund of RM200 million.

• RM210 million is allocated for development of the biotechnology sector.

• RM50 million is allocated to set up halal parks.

• The RM500 tax rebate for the incentive to purchase of a computer will be replaced with a tax relief of RM3,000 once in every three years.

• Income tax exemption for 10 years be given to all Islamic Banking and Takaful entities that conduct their business in foreign currencies.

• Income tax exemption for 10 years be given to fund managers, who manage Islamic funds for foreign investors.

• Dividends received by individual investors and local unit trust from listed Real Estate Investment Trust (REITs) be taxed at a rate of 15% while foreign institutional investors at 20%.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 4

• RM100 million of Overseas Investment Fund (OIF) will be established to provide soft loans to domestic companies.

• RM149 million is allocated for Visit Malaysia Year 2007.

• To promote tourism, income tax exemption for eligible tour operators is extended for five years.

• RM27.5 billion is allocated for the construction of road, quarters and other infrastructure facilities.

To Raise The Capacity For The Knowledge And Innovation And Nurture ‘First Class Mentality’

• Tax relief on the purchase of books be increased from RM700 to RM1,000 per year.

• For early cancer detection, RM50 subsidy for every mammogram done in approved private clinics and hospitals.

• RM721 million is provided to implement various youth and sports programmes.

To Address Persistent Socio-Economic Inequalities Constructively And Productively

• Perlis will be declared a promoted area in which designated projects will be eligible for a higher level of income tax exemption.

• Development allocation of RM2.3 billion has been provided for Johor, especially for Southern Johor Economic Region (SJER).

• RM3.4 billion is allocated for implementation of various rural development projects and programmes.

• RM578 million is allocated to accelerate the implementation of poverty eradication programmes and projects.

To Improve The Standard And Sustainability Of Quality Of Life

• Examination fees for UPSR, PMR, SPM, as well as STPM abolished in all Government schools, beginning with 2007 school session.

• RM302 million is allocated for programmes to improve the less fortunate groups welfare.

• RM10 billion is allocated for the provision of health facilities and equipment, services of specialists and training programmes.

AljeffriDean

5 Friday. September 1, 2006

• Excise duty on cigarettes up by one sen per stick and duty on liquor with alcohol content of more than 40% up by RM5 per litre.

• RM1 billion is provided for programmes to preserve ecological balance and splendour.

• RM685 million is allocated for the development and management of arts, promotion of culture and heritage activities.

To Strengthen The Institutional And Implementation Capacity

• RM200 million is allocated to The Public Transport Development Fund to assist taxi and bus operators to acquire new vehicles.

• Civil servants earning up to RM750 a month will be paid two month bonus and those earning more than RM750 a month will be paid one month bonus subject to a minimum of RM1,500.

• One-off payment ranging from RM200 to RM400 will be paid by the Government to the pensioners.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 6

SECTION C

SUMMARY OF AMENDMENTS TO DIRECT TAXATION REVIEW OF COMPANY INCOME TAX RATE PRESENT Company income tax rate is 28%. This rate also applies to the

following entities:

i) A trust body; ii) An executor of an estate of an individual who was

domiciled outside Malaysia at the time of his death; and

iii) A receiver appointed by the court. Small and medium scale companies (SMEs) with paid up capital not exceeding RM2.5 million are taxed at 20% on chargeable income up to RM500,000 and the remaining amount at 28%.

PROPOSED The company income tax rate be reduced in stages by 2

percentage points. The rate will be 27% for the year of assessment 2007 and 26% for the year of assessment 2008 his new rate also applies to the following entities:

i) A trust body; ii) An executor of an estate of an individual who was

domiciled outside Malaysia at the time of his death; and iii) A receiver appointed by the court.

Small and medium scale companies (SMEs) with paid up capital not exceeding RM2.5 million are taxed at 20% on chargeable income up to RM500,000 and the remaining amount The rate will be 27% for the year of assessment 2007 and 26% for the year of assessment 2008.

IMPACT Enhance the nation's competitiveness. EFFECTIVE DATE Year of assessment 2007 REFERENCE Part I, Schedule I Income Tax Act, 1967

AljeffriDean

7 Friday. September 1, 2006

ENHANCING INCENTIVE FOR VENTURE CAPITAL INDUSTRY PRESENT

Venture capital companies (VCCs) have the option to choose between the following incentives:

i) Income tax exemption for 10 years for investing at least 70% of its investment funds in venture companies (VCs) in the form of seed capital, start-up or early stage financing; or

ii) Deduction for income tax purposes equivalent to the

value of investment made in VCs. PROPOSED VCCs investing at least 50% of its investment funds in VCs in

the form of seed capital be given income tax exemption for 10 years.

IMPACT Increase funding in seed capital. EFFECTIVE DATE Year of assessment 2007 REVIEW OF PENALTY ON WITHHOLDING TAX PRESENT Payment made to a non-resident such as interest, royalty, rental

and technical fees is subject to withholding tax. In respect of withholding tax not paid, a penalty of 10% is imposed on the total payment made to a non-resident.

PROPOSED

The 10% penalty on withholding tax be imposed on the amount of unpaid tax.

IMPACT To reduce the cost of doing business. EFFECTIVE DATE September 2, 2006 REFERENCE Section 107A(2), 109, 109B, 109D Income Tax Act, 1967 TAX TREATMENT ON ZAKAT PAID BY COOPERATIVES AND TRUST BODIES PRESENT Zakat paid by companies to Islamic Religious Authorities is

allowed as a deduction under the Income Tax Act 1967 subject to a maximum of 2.5% of the aggregate income. This deduction was effective from year of assessment 2005.

PROPOSED

The above deduction is extended to cooperatives and trust bodies.

IMPACT Accord equal tax treatment between companies, cooperatives

and trust bodies. EFFECTIVE DATE Year of assessment 2007 REFERENCE Section 44C(11A) Income Tax Act, 1967

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 8

INTRODUCTION OF ADVANCE RULINGS IN INCOME TAX ADMINISTRATION PRESENT No specific provision for the issuance of advance ruling in the

Income Tax Act 1967. The Inland Revenue Board (IRB) issues Public Rulings to make known the Director General's interpretation of provisions of the Act that have general applications. If a taxpayer does not agree with the interpretation, he may request for a private ruling. Since Malaysia is on a full self assessment system, it is only appropriate that IRB extends its services to the issuance of advance ruling.

PROPOSED

Specific provision be introduced under the Income Tax Act 1967, to allow a taxpayer to request for an advance ruling. An advance ruling is a written statement given by the Director General on the tax treatment of an arrangement to be undertaken by the taxpayer. The salient features of the advance ruling system to be introduced are as follows:

i) Application to be made in a prescribed form; ii) Fees to be charged on the application for advance

ruling;

iii) The ruling is only applicable to the applicant;

iv) The ruling can only be issued based on actual facts and not based on assumptions; and

v) The advance ruling issued by IRB is not applicable if the

facts used in making the advance ruling are incorrect or different.

IMPACT Promote clarity and certainty in the interpretation and

application of the tax law. EFFECTIVE DATE January 1, 2007 REFERENCE Section 138A, 138B Income Tax Act, 1967

AljeffriDean

9 Friday. September 1, 2006

FRAMEWORK FOR TAX AUDIT AND INVESTIGATION BY INLAND REVENUE BOARD PRESENT Tax audit is the primary activity of the Inland Revenue Board

(IRB) to enhance voluntary compliance. Currently, information on tax audit can be obtained from the "IRB Guide on Tax Audit". Tax investigation is an enforcement activity carried out by the investigation centres of IRB to curb tax evasion. No guideline on investigation has so far been issued by IRB.

PROPOSED

The existing Guide on tax audit be updated and the framework for tax investigation be issued by the IRB. The main areas to be covered in the guideline/framework are as follows:

i) Criteria for audit and investigation selection; ii) Tax audit and investigation methodology;

iii) Rights and responsibilities of taxpayers and tax agents,

audit and investigation officers;

iv) Settlement upon completion of an audit or investigation; and

v) Offences and penalties.

IMPACT Maintain and enhance public confidence in the tax

administration. EFFECTIVE DATE January 1, 2007 REVIEW OF INCENTIVES FOR BIOTECHNOLOGY INDUSTRY PRESENT Companies involved in the biotechnology industry are eligible

for the following tax incentives: 1. A company undertaking biotechnology activity and has been

approved with bionexus status by the Malaysian Biotechnology Corporation Sdn. Bhd. is eligible for the following incentives:

i) 100% income tax exemption for 10 years commencing

from the date of commencement of commercial production OR Investment Tax Allowance of 100% on the qualifying capital expenditure incurred within a period of 5 years;

ii) Tax exemption on dividends distributed by a bionexus

company;

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 10

iii) Exemption of import duty and sales tax on raw materials/components and machinery/equipment;

iv) Double deduction on expenditure incurred for R&D; and

v) Double deduction on expenditure incurred for the

promotion of exports; AND

2. A company that invests in its subsidiary, which is a bionexus

status company, is granted tax deduction equivalent to the amount of investment made in that subsidiary provided that the investing company owns at least 70% of that subsidiary.

PROPOSED

1. The existing incentive in Para l (i) be enhanced by amending the commencement date of the exemption period from the date of commercial production to the first year the company derives profit;

2. New incentives be introduced as follows:

i) A bionexus company be given a concessionary tax rate of 20% on income from qualifying activities for 10 years upon the expiry of the tax exemption period;

ii) A company or an individual investing in a bionexus

company be given a tax deduction equivalent to total investment made in seed capital and early stage financing;

iii) A bionexus company undertaking merger and acquisition

with a biotechnology company be given exemption of stamp duty and real property gains tax within a period of 5 years until 31 December 2011; and

iv) Buildings used solely for the purpose of biotechnology

research activities be given Industrial Building Allowance over a period of 10 years

Applications for these incentives will be evaluated by a Committee under the Malaysian Biotechnology Corporation Sdn. Bhd. and recommended for approval by the Minister of Finance.

IMPACT Further enhance the biotechnology industry. EFFECTIVE DATE September 2, 2006

AljeffriDean

11 Friday. September 1, 2006

REVIEW OF TAX INCENTIVE FOR THE PURCHASE OF COMPUTER PRESENT Individual taxpayers are eligible for a tax rebate of RM500 for

the purchase of a computer. The rebate is given once in 5 years per household.

PROPOSED

i) The rebate of RM500 be amended to a tax relief of up to RM3,000;

ii) The relief be given once in 3 years (instead of once in 5 years);

iii) In the case of separate assessment, each taxpayer is eligible

to claim the relief (instead of on a per household basis); and

iv) In the case of combined assessment, such expense is

deemed incurred by the spouse who pays income tax.

IMPACT Encourage individual ownership of computers. EFFECTIVE DATE Year of assessment 2007 REFERENCE Section 46(1)(j) Income Tax Act, 1967; Section 6A(3A) Income

Tax Act, 1967 ENHANCING THE INCENTIVE FOR PROMOTION OF MALAYSIAN BRAND NAME PRESENT A company that incurs advertising expenditure in the promotion

of Malaysian brand name locally is eligible to claim double deduction. This incentive is given to a company that fulfils the following criteria:

i) The company is incorporated in Malaysia and at least 70% of its equity is owned by Malaysian;

ii) The company is the registered proprietor of the

Malaysian brand name used in the advertisement; and

iii) The Malaysian brand name goods are of export quality.

iv) As such, a company in the same group that is not the owner of the brand name but has incurred advertising expenditure is not eligible for the deduction.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 12

PROPOSED

Double deduction on expenses incurred on advertising Malaysian brand names be extended to a company within the same group that has incurred the advertising expenditure, subject to the following conditions:

i) The company must be owned more than 50% by the registered proprietor of the Malaysian brand name; and

ii) The deduction can only be claimed by one company in a

year of assessment. As such, a company in the same group that is not the owner of the brand name but has incurred advertising expenditure is not eligible for the deduction.

IMPACT Continuous effort to promote Malaysian brand names. EFFECTIVE DATE Year of assessment 2007 INCOME TAX EXEMPTION FOR ISLAMIC BANKING AND TAKAFUL BUSINESS PRESENT The Government allows Islamic Banking and Takaful Business

transacted in international currencies to be conducted anywhere in Malaysia. However, such activities are currently not given any tax incentives.

PROPOSED

Full tax exemption for 10 years under the Income Tax Act 1967 be given to:

i) Islamic banks and Islamic banking units licensed under the Islamic Banking Act 1983 on income derived from Islamic banking business conducted in international currencies including transactions with Malaysian residents; and

ii) Takaful companies and Takaful units licensed under the

Takaful Act 1984 on income derived from Takaful business conducted in international currencies including transactions with Malaysian residents.

IMPACT To widen inter-linkages in the global Islamic financial markets

through the enhancement of Islamic banking and Takaful business.

EFFECTIVE DATE From year of assessment 2007 until year of assessment 2016.

AljeffriDean

13 Friday. September 1, 2006

STAMP DUTY EXEMPTION ON ISLAMIC FINANCIAL INSTRUMENTS PRESENT The additional instruments that are required to be executed in

accordance with Islamic principles have been given stamp duty exemption.

PROPOSED

The 20% stamp duty exemption be given on instruments used in Islamic financing for a period of 3 years. This exemption be given after the stamp duty is exempted for purpose of tax neutrality. This incentive is subject to the condition that the Islamic financial products are approved by the Bank Negara Malaysia Syariah Advisory Council or Securities Commission Syariah Advisory Council.

IMPACT Further encourage the development of Islamic financial sector. EFFECTIVE DATE September 2, 2006 until December 31, 2009 TAX EXEMPTION FOR COMPANIES MANAGING FOREIGN ISLAMIC FUNDS PRESENT Local and foreign companies licensed by the Securities

Commission under the Approved Foreign Fund Management Status to manage foreign investors' fund are subject to income tax at a concessionary rate of 10% on the management fees received from foreign investors.

PROPOSED

Local and foreign companies managing funds of foreign investors established under the Syariah principles be given full income tax exemption on the management fees for 10 years. The Securities Commission must approve such funds.

IMPACT Further promote foreign Islamic fund management activities. EFFECTIVE DATE From year of assessment 2007 until year of assessment 2016.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 14

EXTENDING THE SCOPE OF INDIVIDUAL TAX INCENTIVE FOR FURTHER EDUCATION PRESENT An individual tax payer pursuing courses at local institutions of

higher education in the fields of science, technical, vocational, industrial skills development, information and communication technology, accountancy and law is eligible for relief not exceeding RM5.000 per annum on the fees for such courses.

PROPOSED

The relief for individuals on study fees be extended to courses in Islamic finance approved by Bank Negara Malaysia or Securities Commission at local institutions of higher education including at the International Centre for Education in Islamic Finance (INCEIF).

IMPACT Increase the number of experts in the field of Islamic finance. EFFECTIVE DATE Year of assessment 2007 REFERENCE Section 46(1)(f) Income Tax Act, 1967 DEDUCTION ON EXPENSES TO ESTABLISH ISLAMIC STOCK BROKING COMPANY PRESENT The expenses incurred prior to the commencement of a

business including a stock broking company are not allowed as a deduction, whereas capital expenditure incurred for the purchase of assets to be used in the business is deemed incurred upon the commencement of the business and allowed as capital allowance.

PROPOSED

The expenses incurred prior to the commencement of an Islamic stock broking business be allowed as a deduction. This incentive is subject to the condition that the company must commence its business within a period of 2 years from the date of approval by the Securities Commission.

IMPACT Support the National Agenda to make Malaysia an Islamic

financial hub. EFFECTIVE DATE Applications received by the Securities Commission from

September 2, 2006 until December 31, 2009.

AljeffriDean

15 Friday. September 1, 2006

EXTENSION OF TAX INCENTIVE FOR ISSUANCE OF ISLAMIC SECURITIES PRESENT The expenses incurred on the issuance of Islamic securities

based on leasing (Ijarah), progressive sales (Istisna’), profit sharing (Mudharabah) and profit and loss sharing (Musyarakah) are allowed as deduction. This incentive will expire in the year of assessment 2007.

PROPOSED

Deduction on the expenses incurred on the issuance of Islamic securities based on Ijarah, Istisna', Mudharabah and Musyarakah be extended another 3 years. This incentive be also given to all Islamic securities products approved by the Securities Commission.

IMPACT Ensure Islamic securities are more competitive. EFFECTIVE DATE From year of assessment 2008 until year of assessment 2010.

EXTENDING THE SCOPE OF TAX INCENTIVE FOR FINANCIAL INSTITUTIONS PRESENT Interest income received by non-residents from banking and

financial institutions established under the Banking and Financial Institutions Act 1989 is exempted from tax. However, profits or interest income received by non residents from banking and financial institutions established under the Islamic Banking Act 1983 or other financial institutions are subject to tax.

PROPOSED Profits or interest income received by non-residents from

financial institutions established under the Islamic Banking Act 1983, and other financial institutions approved by the Minister of Finance be exempted from tax.

IMPACT Attract more foreign funds and streamline tax treatment on

profits or interest income received from all financial institutions EFFECTIVE DATE September 2, 2006 REFERENCE Para 33 Schedule 6 Income Tax Act, 1967 REVIEW OF INCENTIVES FOR REAL ESTATE INVESTMENT TRUSTS

PRESENT Tax incentives related to Real Estate Investment Trusts (REITs) as follows:

i) Exemption of real property gains tax on gains from disposal of real properties by individuals or companies to REITs;

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 16

ii) Exemption of stamp duty on instruments of transfer of real property from individuals or companies to REITs;

iii) Income tax exemption on total income of REITs

distributed to unit holders;

iv) Imposition of tax on unit holders at their respective tax rates on income distributed by REITs. For non-resident unit holders, the tax rate imposed is at 28% and such tax is paid by REITs through the withholding tax mechanism;

v) Tax credit is given to unit holders on the

accumulated income of REITs which was subjected to tax and subsequently distributed to unit holders; and

vi) Deduction on expenditure incurred on fees for

consultancy, legal and valuation services incurred in the establishment of REITs.

PROPOSED It is proposed that:

i) Non-corporate investors especially resident and non-

resident individuals and other local entities that receive dividends from REITs listed on the Bursa Malaysia be subject to a final withholding tax of 15% for 5 years;

ii) Foreign institutional investors especially pension

funds and collective investment funds that receive dividends from REITs listed on the Bursa Malaysia be subject to a final withholding tax of 20% for 5 years;

iii) Local and foreign corporate investors be subject to

existing tax treatment and tax rates;

iv) REITs be exempted from tax on all income provided that at least 90% of their total income is distributed to the investors; and

v) If the 90% distribution condition is not complied with,

REITs will then be subject to income tax, while all their investors are eligible to claim tax credit.

IMPACT Further enhance the development of REITs and attract investment especially funds from west Asia.

EFFECTIVE DATE Proposals (i) and (ii) - January 1, 2007 Proposals (iv) and (v) - Year assessment 2007

AljeffriDean

17 Friday. September 1, 2006

INCENTIVE FOR BANK TO SET UP OPERATIONS OVERSEAS PRESENT Bank is taxed on world income scope. As such, income derived

from its overseas branch or remittance from its subsidiary abroad is subject to income tax in Malaysia. However, such tax borne by that branch or subsidiary is eligible for double taxation relief.

PROPOSED The profits of newly established branches overseas or

remittances of new overseas subsidiaries be given income tax exemption for 5 years. This incentive is subject to the condition that such branch or subsidiary must commence operations within a period of 2 years from the date of approval by Bank Negara Malaysia.

IMPACT Encourage Malaysian owned banks to expand their operations

abroad. EFFECTIVE DATE From 2 September 2006 until 31 December 2009 EXTENSION OF INCENTIVE PERIOD FOR TOUR OPERATORS

PRESENT Tour operators are given the following incentives:

i) Tax exemption on income derived from the business of operating domestic tour packages participated by at least 500 inbound tourists per year; and/or

ii) Tax exemption on income derived from the business

of operating domestic tour packages participated by at least 1,200 local tourists per year.

These incentives are effective until year of assessment 2006.

PROPOSED Income tax exemption for tour operators on income derived from

the business of operating domestic tour packages participated by at least 500 inbound tourists per year or 1,200 local tourists per year be extended for another 5 years until year of assessment 2011.

IMPACT Further encourage the tourism industry.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 18

ENHANCING TAX TREATMENT ON LOCAL LEAVE PASSAGE PRESENT Benefits in kind received by an employee are treated as income

and subject to tax. Such benefits include expenses on leave passage for the employee and his immediate family members. Expenses on fares for vacations up to 3 times per year within the country and once per year overseas are given income tax exemption. However, expenses on meals and accommodation are not exempted.

PROPOSED Tax exemption on local leave passage currently given only on expenses for fares be extended to expenses on meals and accommodation.

IMPACT Further encourage domestic tourism. EFFECTIVE DATE Year of assessment 2007 REFERENCE Section 13(1)(b)(ii)(A) Income Tax Act, 1967 SPECIAL TAX TREATMENT FOR THE PROPERTY DEVELOPMENT AND CONSTRUCTION CONTRACT BUSINESS PRESENT The gross income and adjusted income from property

development and construction contract business are ascertained on the percentage of completion method based on the directions given by the Director General in accordance with the general provisions of the Income Tax Act 1967. Such directions are provided in Public Ruling No. 3/2006.

PROPOSED Special regulations be formulated and published in the Gazette with the purpose of bringing the property development and construction contract business within the ambit of paragraph 36(a)(iv) of the Income Tax Act 1967. The salient features of the regulations are as follows:

i) Recognition of income

The gross income from a property development or construction contract business for a basis period for a year of assessment shall be determined using the percentage of completion method;

ii) Date of commencement of business

The specific date determined to be the date of commencement of a property development or construction contract business including a date based on such specific circumstances and facts acceptable to the Director General;

AljeffriDean

19 Friday. September 1, 2006

iii) Date of completion of a project or contract

A property development project is deemed completed upon the date on which the Temporary Certificate of Fitness for Occupation is issued or the date on which the Certificate of Fitness for Occupation is issued, whichever is applicable. In the case of construction contract, a contract is deemed completed upon the date on which the Certificate of Practical Completion is issued or where no such Certificate is issued, the date upon which the contract work is substantially completed, whichever is the earlier;

iv) Revision of estimates

Revision of estimates of gross profit from a property development project or construction contract can be allowed where there is an increase in development or construction costs due to escalating cost of materials, a reduction in selling price or contract sum or other commercial reasons acceptable to the Director General

v) Deductibility of expenses incurred during the defect liability or warranty period

Expenses incurred during the defect liability or warranty period shall be allowed against the income of the year of assessment in which the expenses are incurred or shall be carried forward to the following years of assessment. However, the property developer or construction contractor may elect to carry back the expenses to the basis period for the year of assessment in which the project or contract is completed. Where the income in the year of completion of the project or contract is insufficient to set off the expenses incurred, the excess of the expenses is allowed to be carried back further to be deducted from the income for the immediately preceding years of assessment for the duration of the project or contract. The option to elect is available to the property developer or construction contractor for each year of assessment for the duration of the defect liability or warranty period; and

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 20

vi) Final accounts

On submission of the final accounts upon the completion of the project or contract: a. Any income from the project or contract not

previously included in the gross income shall be included in the gross income for the basis period for the year of assessment in which the project or contract is completed;

b. Any losses ascertained may be apportioned to

each year of assessment for the duration of the project or contract using the percentage of completion method; and

c. Where the actual gross profit is less than the total

estimated gross profit, the property developer or construction contractor may review the assessment for the immediate preceding year of assessment prior to the year of completion of the project or contract. However, the property developer or construction contractor may elect to review all relevant assessments by apportioning the actual gross profit to each year of assessment for the duration of the project or contract using the percentage of completion method.

IMPACT Provide certainty in the tax treatment with respect to the

computation of the gross income and adjusted income from the property development and construction contract business.

EFFECTIVE DATE Year of assessment 2006 REVIEW OF TAX RELIEF FOR THE PURCHASE OF BOOKS PRESENT An individual taxpayer is eligible for a tax relief on the purchase

of books of up to RM700 per year. PROPOSED

The tax relief on the purchase of books be increased from RM700 to RM 1,000 per year.

IMPACT Further inculcate a reading culture and promote lifelong

learning. EFFECTIVE DATE Year of assessment 2007 REFERENCE Section 46(1)(i) Income Tax Act, 1967

AljeffriDean

21 Friday. September 1, 2006

EXTENDING THE SCOPE OF INCENTIVE FOR THE CAPITAL MARKET GRADUATE TRAINING SCHEME PRESENT Companies listed on the Bursa Malaysia are eligible for double

deduction on allowances paid to participants in the Securities Commission (SC) Capital Market Graduate Training Scheme, commencing from 1 October 2005 until 31 December 2008. The deduction is given for a period of 3 years from the date the scheme commences.

PROPOSED

The double deduction given on allowances paid to participants of the SC Capital Market Graduate Training Scheme be extended to unlisted companies under the supervision of the SC. Companies, both listed and unlisted, under the supervision of SC, will also be eligible for the double deduction incentive for their own in-house training schemes for graduates, which have been certified by the SC. These incentives commence from 2 September 2006 until 31 December 2008 and the deduction be given for a period of 3 years from the date the scheme commences.

IMPACT Further encourage the private sector to assist in enhancing the

employability of unemployed graduates. EFFECTIVE DATE September 2, 2006 EXTENDING THE PROMOTED AREAS PRESENT Promoted areas are the Eastern Corridor of Peninsular

Malaysia, which includes Kelantan, Terengganu, Pahang and district of Mersing in Johor as well as Sabah and Sarawak. Companies located in promoted areas are eligible for the following:

i) Pioneer Status with tax exemption of 100% of statutory income for a period of 5 years; or

ii) Investment Tax Allowance of 100% on the qualifying

capita! expenditure incurred within a period of 5 years. The allowance can be set-off against 100% of statutory income for each year of assessment:

provided the companies carry on promoted activities or promoted products;

iii) Infrastructure Allowance of 100% of qualifying capital

expenditure for companies incurring expenditure on infrastructure such as bridges, roads and ports. The allowance can be set-off against 100% of statutory income for each year of assessment; and

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 22

iv) Reinvestment Allwance of 60% of qualifying capital expenditure given to manufacturing and selected agriculture projects. The allowance can be set-off against 100% of statutory income for each year of assessment.

PROPOSED

Perlis be declared as a promoted area. Companies located in that state and undertaking promoted activities or producing promoted products be eligible for enhanced incentives presently given to the promoted areas.

IMPACT Improve the investment climate in the state of Perlis. EFFECTIVE DATE Applications received by the Malaysian Industrial Development

Authority (MIDA) from 2 September 2006. INCREASING THE LIMIT AND WIDENING THE SCOPE OF DEDUCTION ON DONATION FOR CHARITABLE ACTIVITIES PRESENT Companies which contribute cash donations to an approved

institution, organization or fund for charitable purposes are eligible for a deduction of up to 5% of their aggregate income under Section 44(6), Income Tax Act 1967. However, similar contributions made by companies towards sports activities are not given a deduction.

PROPOSED The current limit on deduction given to companies on

contributions for charitable activities be increased from 5% to 7% of the aggregate income. In addition, to support the Government's efforts to enhance attainment in sports, it is proposed that such deduction be extended to contributions made by companies towards sports activities approved by the Minister of Finance and sports bodies approved by the Commissioner of Sports. The deduction be subject to the condition that the sum of the 2 types of contributions does not exceed 7% of the companies' aggregate income.

IMPACT Encourage companies to be involved in corporate social

responsibility programmes. EFFECTIVE DATE Year of assessment 2007 REFERENCE Section 46(6), 44(11B) Income Tax Act, 1967

AljeffriDean

23 Friday. September 1, 2006

TAX TREATMENT ON PERQUISITE PRESENT Perquisite or benefits in cash or in kind such as long service

award and excellent service award received by an employee from an employer are considered as income and subject to tax.

PROPOSED Tax exemption on service awards received by employees be given on contribution in cash or in kind not exceeding RM1,000 a year. Examples of such awards are long service award, safety award and excellent service award. For awards exceeding RM1,000, only the balance will be subject to tax. For the purpose of this exemption, service award:

i) Cannot be a disguised wage;

ii) Must be awarded as part of a meaningful contribution to the organisation; and

iii) Is not provided frequently to the same employee.

Given to employee's who have served at least 10 years with the same employer.

IMPACT Encourage for long services.

EFFECTIVE DATE Year of assessment 2007

REFERENCE Para 25C Section 6 Income Tax Act, 1967 ENHANCING INCENTIVE FOR SPONSORING ARTS AND CULTURAL PERFORMANCES PRESENT A company that sponsors local and foreign arts and cultural

performances approved by the Ministry of Culture, Arts and Heritage is allowed a deduction up to RM300,000 per year. However, the deduction allowed for foreign performances should not exceed RM200.000 of the total annual deduction allowed.

PROPOSED The deduction on expenditure incurred in sponsoring such

performances and shows be increased to RM500.000 per year. However, the ceiling for deductions allowed on foreign performances and shows remains at RM200.000 per year.

IMPACT Further encourage the private sector to sponsor local arts, cultural and heritage performances and shows.

EFFECTIVE DATE Year of assessment 2007

REFERENCE Section 34(6)(K) Income Tax Act, 1967

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 24

TAX TREATMENT ON PAYMENT FOR RENTAL OF SHIP PRESENT Rental payment made to a non-resident under an agreement for

participation in a pool, by a resident shipping company in Malaysia engaged in the business of transporting passenger or cargo is exempted from income tax.

PROPOSED Rental payment of ships under voyage charter, time charter or

bare boat charter to a non-resident by a resident company in Malaysia be exempted from income tax.

IMPACT Further enhance the growth of the national shipping industry. EFFECTIVE DATE September 2, 2006 INCOME TAX EXEMPTION FOR SEAFARERS WORKING ON BOARD A FOREIGN SHIP PRESENT The income of a seafarer who works on board a Malaysian ship

is exempted from tax. In this context, a "Malaysian ship" means a seagoing ship registered under the Merchant Shipping Ordinance 1952, other than a ferry, barge, tug-boat, supply vessel, crew boat, lighter, dredger, fishing boat or other similar vessel. However, the income of a seafarer employed by a Malaysian shipping company on board a foreign ship is not given tax exemption.

PROPOSED

The income of a seafarer who is employed by a Malaysian shipping company on board a foreign ship chartered by the employer be given tax exemption.

IMPACT Streamline the tax treatment. EFFECTIVE DATE Year of assessment 2007 REFERENCE Para 34(1) Section 6 Income Tax Act, 1967

AljeffriDean

25 Friday. September 1, 2006

SECTION D

SUMMARY OF AMENDMENTS TO INDIRECT TAXATION

ESTABLISHMENT OF CUSTOMS APPEAL TRIBUNAL

PRESENT Disputes pertaining to technical and administrative decisions by the Royal Malaysian Customs may be appealed to the Minister of Finance. These disputes are mostly related to classification and valuation of goods and taxable services.

PROPOSED An independent Customs Appeal Tribunal (CAT) be established to

decide on appeals against the decisions of the Director General of Customs pertaining to matters under the Customs Act 1967, Sales Tax Act 1972, Service Tax Act 1975 and Excise Act 1976. The main features of CAT are as follows: i. the Tribunal shall consist of not less than three (3) members

of which the Chairman shall be from the judicial and legal service and other members with experience in taxation or custom matters.

ii. appeal against the decision of the Director General of Customs shall be made within 30 days from the date of notification of that decision; and

iii. the decision of the Tribunal shall be final except on such cases where there shall be further right of appeal to the High Court or Federal Court.

IMPACT To further enhance transparency in tax administration. EFFECTIVE DATE 1 March 2007

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 26

INTRODUCTION OF CUSTOMS RULING

PRESENT Any person can apply to the Royal Malaysian Customs (RMC) in respect of the classification or valuation of goods or services in order to determine the class and duty of such goods or the tax treatment of such services. These rulings are issued on an ad hoc basis and their applications are not comprehensive which have caused inconsistencies in their implementation.

PROPOSED Customs Ruling be introduced under the Customs Act 1967, Sales

Tax Act 1972, Service Tax Act 1975 and Excise Act 1976. The Ruling issued by the RMC and agreed by the applicant shall be legally binding between both parties for a specific period of time. The main features of Customs Ruling to be introduced are as follows:

i. application for Customs Ruling can be made with respect to classification of goods, determination of taxable services and the principles of determination of value of goods and services.

ii. application to be made in writing together with sufficient facts and a prescribed fee;

iii. application may be made before the goods are imported or the services are provided upon which RMC will issue an advance ruling;

iv. the Customs Ruling is only applicable to the applicant; and

v. the Director General of Customs may amend, modify or revoke a Ruling if there is any error in the Ruling due to typing or wrong reference or if the Ruling is based on an error of fact as in the case of the use of incomplete analysis done on a product or if there is a change in law which can result in a new tariff structure.

IMPACT To provide the business sector with the elements of certainty and

predictability in planning their business activities. EFFECTIVE DATE 1 January 2007

AljeffriDean

27 Friday. September 1, 2006

REVIEW OF ELIGIBILITY PERIOD TO CLAIM REFUND OF SALES TAX AND SERVICE TAX RELATED TO BAD DEBTS

PRESENT Sales tax and service tax paid by the licensee could be refunded if the debts becomes bad provided the following conditions are met :

i) the licensee is unable to collect the debt from the client after a period of 12 months from the date of payment of the tax; or

ii) the debtor had been adjudged a bankrupt under Bankruptcy Act 1967; or

iii) the debtor had been placed under receivership or official assignee; or

iv) the debtor had been ordered by the court to wind up; or v) the licensee had filed a claim in court to recover the tax

or the licensee had initiated action for the client to be adjudged a bankrupt; and

vi) payments for goods sold have been written off as bad debts in the account of the licensee.

PROPOSED It is proposed that eligibility to refund of sales tax and service tax

related to bad debts be shortened from 12 months to 6 months from the date the tax is paid. The amendments on the above criteria (i) and (vi) are as follows:

a) criterion (i) – the period to be shortened from 12 months to 6 months

b) criterion (vi) – introduce a new condition where doubtful debts have been provided in the accounts of the licensee as an alternative to the existing condition of writing off the bad debts

IMPACT To strengthen company’s cash flow position and to reduce cost of

doing business EFFECTIVE DATE 1 January 2007

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 28

REVIEW OF COMPOUND OR FINE FOR UNDER DECLARATION AND SMUGGLING OF HIGH DUTY GOODS

PRESENT Offences of under declaration of the value of goods and smuggling are punishable as follows:

i) compound of not more than 10 times of the duty or value of the goods; or

ii) a fine if charged in court and convicted, other than

imprisonment sentence, can be imposed as follows:

a. in the case of dutiable goods: i. for the first offence, a fine of not less than 10 times the amount of duty or RM50,000, whichever is the lesser amount and not more than 20 times the amount of the duty or RM100,000, whichever is the greater amount; and

ii. for the second or any subsequent offence, a fine of not less than 10 times the amount of duty or RM100,000, whichever is the lesser amount and not more than 40 times the amount of the duty or RM500,000, whichever is the greater amount.

b. in the case of prohibited goods:

i. for the first offence, a fine of not less than 10 times the value of the goods or RM50,000, whichever is the lesser amount and not more than 20 times the value of the goods or RM100,000, whichever is the greater amount; and

ii. for the second or any subsequent offence, a fine of not less than 10 times the value of the goods or RM100,000, whichever is the lesser amount and not more than 40 times the value of the goods or RM500,000, whichever is the greater amount.

PROPOSED The punishments are as follows:

i) the minimum compound imposed be 5 times of the total duty; and

ii) the fine imposed be in line with the maximum compound

and updated as follows:

a. in the case of dutiable goods: i. for the first offence, a fine of not less than 10 times the amount of duty and not more than 20 times the amount of duty; and

ii. for a second or any subsequent offence, a fine of not less than 20 times the amount of

AljeffriDean

29 Friday. September 1, 2006

duty and not more than 40 times the amount of duty.

b. in the case of prohibited goods:

i. for the first offence, a fine of not less than 10 times the value of the goods and not more than 20 times the value of the goods; and

ii. for a second or any subsequent offence, a fine of not less than 20 times the value of the goods and not more than 40 times the value of the goods.

IMPACT To overcome the problem of under declaration of the value of

goods and smuggling of high duty goods particularly cars, cigarettes and liquor.

EFFECTIVE DATE 1 January 2007

ADDITIONAL INCENTIVE FOR TOUR OPERATORS

PRESENT Tour operators are given full excise duty exemption on national cars used as hire and drive cars.

PROPOSED Tour operators are given 50% excise duty exemption on locally

assembled 4WD vehicles. IMPACT To enable tourists to explore challenging destinations. EFFECTIVE DATE 2 September 2006

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 30

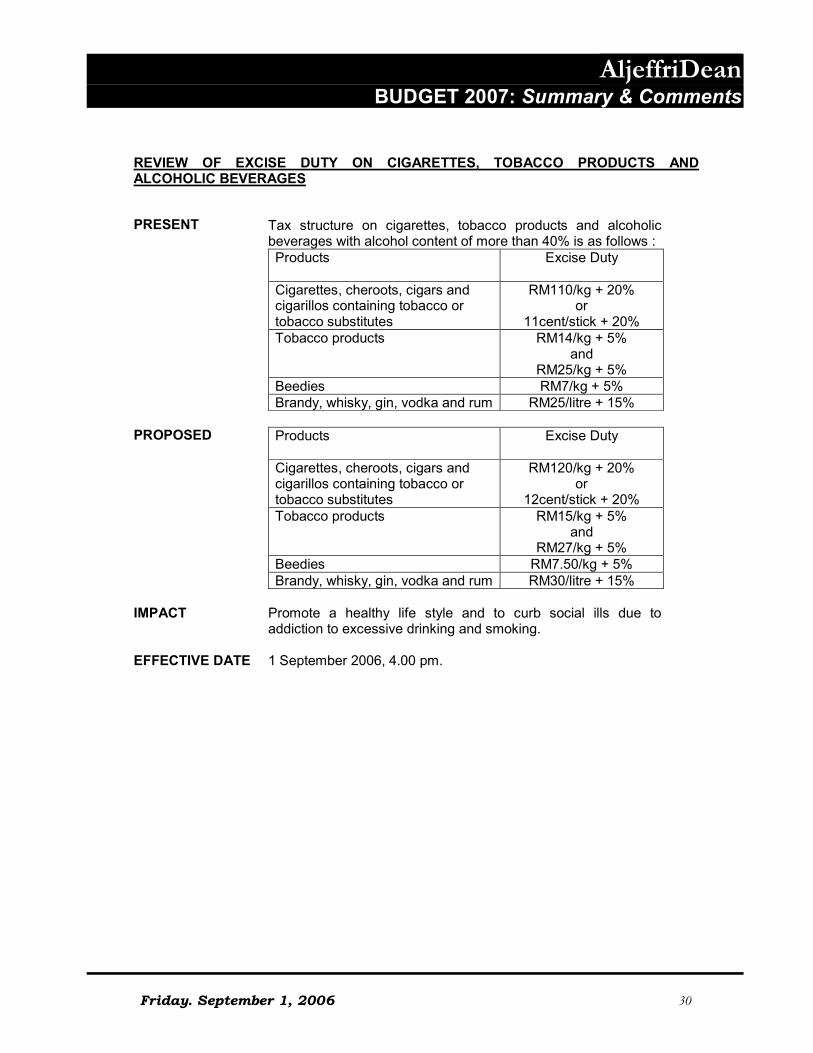

REVIEW OF EXCISE DUTY ON CIGARETTES, TOBACCO PRODUCTS AND ALCOHOLIC BEVERAGES

PRESENT Tax structure on cigarettes, tobacco products and alcoholic beverages with alcohol content of more than 40% is as follows :

Products Excise Duty

Cigarettes, cheroots, cigars and cigarillos containing tobacco or tobacco substitutes

RM110/kg + 20% or

11cent/stick + 20%

Tobacco products RM14/kg + 5% and

RM25/kg + 5%

Beedies RM7/kg + 5%

Brandy, whisky, gin, vodka and rum RM25/litre + 15% PROPOSED Products Excise Duty

Cigarettes, cheroots, cigars and cigarillos containing tobacco or tobacco substitutes

RM120/kg + 20% or

12cent/stick + 20%

Tobacco products RM15/kg + 5% and

RM27/kg + 5%

Beedies RM7.50/kg + 5%

Brandy, whisky, gin, vodka and rum RM30/litre + 15% IMPACT Promote a healthy life style and to curb social ills due to

addiction to excessive drinking and smoking. EFFECTIVE DATE 1 September 2006, 4.00 pm.

AljeffriDean

31 Friday. September 1, 2006

SECTION E

SUMMARY OF BUSINESS OPPORTUNITIES AND OTHER INCENTIVES

I. FUNDS AND SCHEMES UNDER MINISTRIES AND AGENCIES

Ministry of Entrepreneur and Co-operative Development 1. Franchise Development Assistance Scheme

Purpose To assist and provide incentive to individual entrepreneurs and Malaysian companies to franchise its product or business locally or overseas.

Ministry of Science, Technology and innovations 2. Industry Research And Development Grant Scheme (IGS)

Purpose To encourage Malaysian companies to be more innovative in using and adapting to the existing technologies and creating new technologies, products and processes, as well as promoting closer cooperation between private and public sector. The scheme would facilitate Malaysian companies to establish strategic global and regional linkages in R & D to enhance indigenous technology development.

Ministry of Youth and Sport 3. Trust Fund for Youth Development

Purpose To assist youth to undertake business venture

Bank Negara Malaysia 4. New Entrepreneurs Fund 2

Purpose To help stimulate the growth of small and medium-sized Bumiputera enterprises

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 32

5. Fund for Small and Medium Industries 2

Purpose To promote SME activities in the export and domestic oriented sectors

6. Fund for Food

Purpose To increase of food production in Malaysia

7. Bumiputera Entrepreneurs Project Fund

Purpose To provide financing to Bumiputera entrepreneurs who have been awarded contracts/projects by the Government, Government-related agencies, statutory bodies and reputable private/public companies

8. Rehabilitation Fund for Small Businesses

Purpose To assist viable SMEs that are constrained by non performing loans (NPLs) through Small Debt Restructuring Scheme (SDRS) by facilitating their request for loan restructuring and arranging for new financial institutions.

Small and Medium Industries Development Corporation (SMIDEC) 9. Special Assistance Scheme for Women Entrepreneurs

Purpose To allow greater access to financing for women entrepreneurs This scheme is more flexible and accessible to women entrepreneurs

10. Industrial Technical Assistance Fund 1 (Business planning, technology and

market development scheme)

Purpose To assist small and medium enterprises for :

• Market feasibility studies

• Technology feasibility studies

• Business planning

• Domestic and export market strategy

AljeffriDean

33 Friday. September 1, 2006

11. Industrial Technical Assistance Fund 2 (Improving and upgrading existing product, product design and processes scheme)

Purpose Financing SMEs for :

• Improvement and upgrading of existing product

• Improvement and upgrading existing product design

• Improvement and upgrading of existing process

12. Industrial Technical Assistance Fund 3 (Productivity and quality improvement and

to achieve international quality standards and certification scheme)

Purpose Financing SMEs for :

• Productivity and quality improvement

• Productivity and quality improvement based on customer’s requirement

• Quality Development System (5S, Quality Control Circle (QCC), Total Preventive maintenance (TPM))

• Productivity and quality system certification

• Quality series

• Occupational and safety measures

• HACCP, HALAL and other product quality certification

13. Soft Loan Package for Small and Medium Enterprises

Purpose The package offers assistance to small and medium enterprises in modernizing and automating their manufacturing operations

14. Soft Loan for Factory Relocation

Purpose To assist small and medium entrepreneurs to relocate their premises from operating in an unlicensed factories to an approved industrial site as well as to acquire assets that will enhance their capabilities to obtain other financial assistance

Bank Perusahaan Kecil Dan Sederhana Malaysia Berhad (SME Bank) 15. Seed Capital Scheme (Batik and Craft)

Purpose To promote Malaysian Batik and craft industry by providing financing to Bumiputera batik and craft operator

16. Fiction Film Financing Scheme

Purpose To encourage Malaysian film company to produce successful fiction film for local or international market

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 34

17. Rural Economy Financing Scheme

Purpose To assist Bumiputera entrepreneurs operating in rural areas

18. Rural Economy Financing Scheme for Indian Community

Purpose To assist rural Indian community entrepreneurs involves in pottery business to obtain financing

19. Graduate Entrepreneur Fund

Purpose To encourage graduates to participate and venture into business with potential to expand

20. Special Fund for Tourism 2

Purpose To support Government efforts to develop tourism industry

21. Terengganu State Entrepreneurs Fund

Purpose To develop entrepreneurs in the state of Terengganu

22. Tanmiah Scheme 1

Purpose To assist bumiputera’s company to enhance their status in manufacturing and services industry

23. Tanmiah Scheme 2 (Strategic industry scheme)

Purpose To enhance the viability of the factory project undertaken by increasing Bumiputera’s participation in wholesale and distribution activities in domestic and international market

Bank Industri & Teknologi Malaysia Berhad 24. New Shipping Fund

Purpose To stimulate the growth of shipping industry and shipyard

25. High Technology Fund

Purpose To support the development of high technology industry

AljeffriDean

35 Friday. September 1, 2006

26. Tourism Infrastructure Fund

Purpose To support Government efforts to develop tourism industry

Bank Pertanian Malaysia 27. Financing Scheme for Bumiputera Trade & Industry Community

Purpose To encourage the creation pf bumiputera entrepreneurs in agriculture sector, particularly in production of food crop, processing and marketing of agriculture products except rubber, oil palm, tobacco, cocoa, pepper, forestry, drinks and vegetable oil

28. Financing Scheme for Agricultural Mechanism & Automation

Purpose To modernize and commercialise agricultural sector through the usage of machinery and automation tools in production, processing and marketing of agricultural products except for rubber, palm oil, tobacco, cocoa, pepper, forestry, soft drink and vegetable oil.

Perbadanan Nasional Berhad 29. PNS Equity Investment Scheme

Purpose To develop and increase the number of medium class Bumiputera entrepreneurs through financial assistance or SME equity financing

30. PNS Franchise Investment Scheme

Purpose To develop and increase the number of Middle-Level Bumiputera Enterpreneurs (MLBE) in franchise businesses through PNS equity investment scheme

31. PNS Franchisee Financing Scheme

Purpose To develop and increase the number of Middle-Level Bumiputera Entrepreneurs (MLBE) in franchise businesses through financial assistance for purposes of business expansion and starting-up franchise companies

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 36

Perbadanan Usahawan Nasional Berhad (PUNB) 32. Bumiputera Entrepreneurs Retail Project Fund

Purpose To increase and upgrade Bumiputera entrepreneurs participation in the retail business. PUNB provides capital up to 30% or loan up to 90% of total project cost based on Islamic financing

Majlis Amanah Rakyat (MARA) 33. MARA Business Financing Scheme

Purpose To increase the participation of Bumiputera entrepreneurs in the small and medium industries

Malaysian Technology Development Corporation (MTDC) 34. Technology Acquisition Fund for Women

Purpose To provide greater access to financing for women entrepreneurs involve in the technology industry. The financing is in the form of grant

35. Commercialisation of R&D Fund (Phase 1) (market survey and research)

Purpose To provide assistance in evaluating the market potential of certain proposed product / process for purpose of commercialisation

36. Commercialisation of R&D Fund (Phase 2) (product / process design and

development)

Purpose To facilitate the design and physical development of prototypes into products / processes

37. Commercialisation of R&D Fund (Phase 3) (standards and regulatory compliance

and intellectual property protection)

Purpose To facilitate commercialization of products / processes through testing for compliance with standards and regulations as well as intellectual property protection

AljeffriDean

37 Friday. September 1, 2006

38. Commercialisation of R&D Fund (Phase 4) (Demonstrations of technology)

Purpose To provide exposure for indigenous technology to potential market and to expedite technology roll-out by drawing interest from potential investors.

39. Technology Acquisition Fund

Purpose To promote technology upgrading through the introduction and utilization of modern and efficient technology in the manufacturing and physical development of existing and new products or processes as well as to enhance the competitiveness level of firms to enable them to compete globally

Multimedia Development Corporation Sdn Bhd (MDC) 40. Multimedia Super Corridor Research and Development Grant Scheme

Purpose To assist local companies or joint venture companies in developing multimedia technologies and applications which would contribute to the overall development of Multimedia Super Corridor (MNC).

MIMOS Berhad 41. Demonstrator Application Grant Scheme

Purpose To develop the culture, social and economic progress of Malaysians through innovation use the information and communication technologies (ICT) and to build an integrated network of electronic community which utilized multimedia and ICT.

Bank Kerjasama Rakyat Malaysia Berhad 42. Rural Economy Financing Scheme

Purpose To assist Bumiputera entrepreneurs operating in rural areas.

Malaysian Venture Capital Management Berhad 43. Venture Capital Financing

Purpose To provide venture capital financing.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 38

Yayasan Tekun Nasional (YTN) 44. Fund for Economic Business Venture

Purpose To provide financing for additional capital for the small entrepreneurs.

Amanah Ikhtiar Malaysia (AIM) 45. Initiative Financing Scheme

Purpose To reduce the poverty rate in Malaysia by providing financing to poor household in rural area to undertake any viable economic activities which would increase their household income.

Credit Guarantee Corporation Malaysia Berhad (CGC) 46. Direct Access Guarantee Scheme

Purpose Enable entrepreneurs to obtain guarantee cover directly from CGC for the needed financing from banking institution.

47. Franchise Financing Scheme

Purpose Assist entrepreneurs to obtain financing in franchising business. 48. Small Entrepreneurs Guarantee Scheme

Purpose To facilitate small entrepreneur with viable business venture to obtain guarantee cover for credit.

49. New Principal Guarantee Scheme

Purpose To facilitate small entrepreneur with viable business venture to obtain guarantee cover for credit facility up to RM10 million.

50. Islamic Banking Guarantee Scheme

Purpose To provide guarantee for loans granted by commercial banks and finance companies under the Islamic banking principle for manufacturing and priority sector.

51. Flexi Guarantee Scheme

Purpose Guaranteeing loan under the Fund for Small and Medium Industries 2, New Entrepreneurs Fund 2 and Rehabilitation Fund for Small Businesses which fund are managed by Bank Negara Malaysia.

AljeffriDean

39 Friday. September 1, 2006

II. OTHER BUSINESS OPPORTUNITIES AND INCENTIVES (As proposed in Budget 2007)

• Private Sector

Purpose To stimulate private investment

Mechanism (i) By implementation of Private Financing initiatives (PFI)

(ii) Financial support to enhance viability of projects identified by private entities such as by providing land and basic infrastructures, sponsorship and, purchase and lease of property, to enhance viability.

RM20 billion and 5 billion fund is allocated for PFI and PFI Facilitation Fund, respectively.

Who will Benefit

Private companies, especially contractors

• Agriculture Sector

Purpose To transform agriculture sector into a modern, commercial and competitive.

Mechanism (i) by creation of RM3.6 billion comprising Fund for

Food, Non-Food Agriculture Scheme, livestock projects and aquaculture industries;

(ii) Encouraging business partnership between entrepreneur and Co-operatives; and

(iii) Venture capital financing in area of new technology intensive agriculture projects.

Who will Benefit

Private business entities and co-orperatives

• Bio-technology Sector

Purpose To put greater emphasis on bio-technology as a new source of growth

Mechanism (i) Allocation of fund amounting to RM210 million via Biotechnology Commercialisation Fund and R&D initiatives;

(ii) Establishment of Bio Innovation Centre for commercialization and bio-manufacturing activities

Who will Benefit

Private business entities which are involved in bio-technology.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 40

• Halal Industry

Purpose To promote Malaysian global halal industry

Mechanism (i) establishment of Halal Industry Development Corporation that will coordinate and ensure integration and comprehensive development;

(ii) setting up halal parks throughout Malaysia;

with a total of RM95 million Fund.

Who will Benefit

Private business entities.

• ICT Development

Purpose To act as a catalyst in the implementation of national economic development plans

Mechanism By promoting shared services and outsourcing (SSO) in logistics and financial services.

Who will Benefit

SSO-based private business entities

• Research & Development

Purpose To promote R&D and commercialisation of R&D findings

Mechanism (i) Establishment of Science and Techno Funds; (ii) MSC Grand Scheme

Who will Benefit

Research agencies and private business entities

• Investment Abroad

Purpose To encourage domestic companies to invest abroad

Mechanism (i) Facilities offered by EXIM Bank; (ii) Establishment of Overseas Investment Fund for

start-up costs

Who will Benefit

Private business entities and bankers.

AljeffriDean

41 Friday. September 1, 2006

• Tourism

Purpose To boost foreign tourists and further promoting tourism in Malaysia

Mechanism (i) organise Visit Malaysia Year 2007 with RM149

million fund allocation ; (ii) upgrade tourist facilities and develop new tourism

products

Who will Benefit

Tour operators and tourism-related business entities

• Construction Sector

Purpose To turnaround and accelerate growth in the construction sector Mechanism (i) Higher allocation i.e. RM2.75 billion through

construction of infrastructure facilities, housing and buildings, roads, quarters and other facilities;

(ii) Maintenance of existing infrastructures and public amenities

Who will Benefit

Private business entities which are involved in construction.

• Reducing Regional Disparity

Purpose To reduce growth imbalances between regions and between urban and rural areas

Mechanism (i) development of Northern Economic Corridor, East

Coast Corridor and Southern Johor Economic Region as business operation;

(ii) declaration of Perlis as promoted area

Who will Benefit

Private business entities relating to commercialised agriculture, petrochemicals, handicrafts, tourism, private higher education and healthcare.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 42

• Environmental Preservation

Purpose To promote environmental preservation Mechanism (i) By providing an allocation of RM179 million to

improve mini incinerators and upgrade present solid waste disposal sites;

(ii) Develop Bio-diesel Industry Fund amounting to RM500 million

Who will Benefit

Private business entities relating to solid waste management and bio-diesel.

• Arts, Culture and Heritage

Purpose To inculcate greater appreciation of the arts and culture Mechanism Establishment of Creative Industry Development Fund of

RM100 million

Who will Benefit

Private business entities relating to creative industry

AljeffriDean

43 Friday. September 1, 2006

SECTION F

SYNOPSIS AND COMPARISON

(Period under review 2000 to 2007)

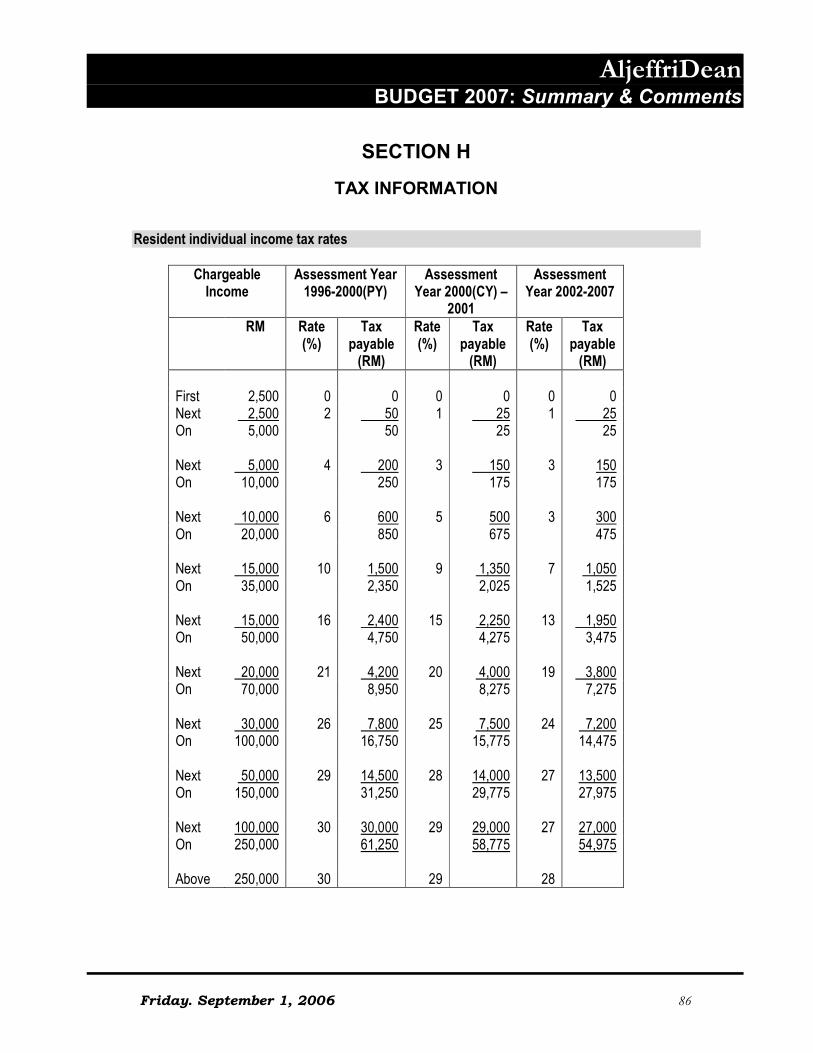

PERSONAL TAX

Tax Rate Income Tax i) Resident 2000-2001 Chargeable income < RM2,500=

0% Chargeable income > RM150,000 = 29% Other income group = 1% - 28%

2002-2006 Chargeable income < RM2,500= 0% Chargeable income > RM250,000 = 28% Other income group = 1% - 27%

2007 No changes ii) Non-resident 2000-2001 29% 2002-2006 28% 2007 No changes Personal relief a. Self relief 2000-2006 RM8,000 2007 No changes b. Husband relief (for husband with no

income) 2000

2001-2006 Nil RM3,000

2007 No changes c. Disabled person - Taxpayer

- Spouse

2000-2004 2005-2006

2007

2000-2004 2005-2006

2007

RM5,000 RM6,000 No changes RM2,500 RM3,500 No changes

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 44

d. Normal Children below 18 years old

2000-2003 2004-2006

2007

RM800 each RM1,000 each No changes

e.

Unmarried child age above 18 & studying in higher learning institutions i. Overseas Institutions of higher learning

2000-2004 2005 2006

2007

2 x Normal rate Normal rate 4 x Normal rate at a recognised institution of higher learning abroad. No changes

ii. Local Institutions of higher learning 2000-2006

2007 4 x Normal rate No changes

f. Disabled child (unmarried) 2000-2005

2006

2007

RM5,000 Additional RM4,000 to disabled child studying in higher learning institutions at diploma level and above in Malaysia or at degree level and above outside Malaysia. No changes

g. Annuity purchased through EPF 2000-2006 Maximum RM1,000 2007 No changes h. Life insurance premiums/ Approved fund contributions - Taxpayer (max)

2000-2004 2005-2006

2007

RM5,000 RM6,000 No changes

i. Medical and Education Insurance 2000-2006 Increased to RM3,000 2007 No changes

j. Fee for education in scientific, technology or vocational fields in Malaysia

2000 Maximum RM2,000

2001-2005 Maximum RM5,000 and field extended to ICT

2006 Extended to professional courses, accountancy and law undertaken at recognised institutions. The eligible professional fields are to be approved by the Ministry of Finance.

2007 Extended to courses in Islamic finance approved by Bank Negara or Securities Commission.

k. Purchases of books, journals & magazines 2000 2001-2004

Nil Up to RM500

2005-2006 2007

Up to RM700 Up to RM1,000

l. Complete medical examination 2000 2001-2006

Nil Up to RM500

2007 No changes

m. Purchase of computer 2007 Up to RM3,000 once in 3 years per taxpayers.

AljeffriDean

45 Friday. September 1, 2006

Rebate a. Entitlement 2000

2001-2006 Chargeable income < RM10,000 Chargeable income < RM35,000

2007 No changes b. Tax payer 2000 RM110 2001-2006 RM350 2007 No changes c. Wife (Joint assessment) 2000 RM60 2001-2006 RM350 2007 No changes d. Husband (Joint assessment) 2000

2001-2006 Nil RM350

2007 No changes e. Tax rebate for personal computer (PC) 2000-2004 RM400 once in 5 years per family 2005-2006 RM500 once in 5 years per family 2007 Amended as tax relief Income exempted from income tax: a. Income from musical composition 2000-2006 Maximum RM20,000 2007 No changes

b.Income derived by non-residents performing in art and cultural shows, exhibitions, games and competitions held at the National Sports Complex, National Theatre, National Art Gallery and Petronas Philharmonic Hall

2000-2006 2007

Exempted No changes

c. Income derived by organisers of sports, cultural shows, art exhibition and carnivals involving foreign participation held at the National Sports Complex, National Theatre, National Art Gallery and Petronas Philharmonic Hall

2000-2006 2007

Tax exemption of 50% No changes

d.Income derived by drivers of “Formula One” and motor racing internationally recognised and held in Malaysia

2000-2006 2007

Exempted No changes

e. Income derived by organisers of “Formula

One” and motor racing internationally recognised and held in Malaysia

2000-2006 2007

50% of statutory income exempted No changes

f. Leave passage 2000-2006 Exemption for overseas trip is

restricted to RM3,000.

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 46

Allowable expenses: Fares. Non allowable expenses: Meals and accommodation.

2007 Exemption is extended to meals and accommodation.

g.Statutory income from provision of chartering services of luxury yacht departing from and ending at ports in Malaysia

2000-2001 2001-2006

2007

Taxable w.e.f. 20.10.2001 exempted for 5 years No changes

h. Computer given by employer 2000

2001-2003 Taxable Exempted

2004-2006 2007

Taxable No changes

i. Royalty received by non-resident franchisors from franchised education scheme approved by the Ministry of Education.

Royalty received by resident on royalty from art artisticistic works.

2000-2001 2002-2005

2006

2006

2007

Taxable Exempted w.e.f 20.10.2001. Tax exempted from withholding tax for a period of 5 years. Tax exemption on royalty to be increased to RM10,000 a year. No changes

j. Export of qualifying services by resident 2000-2001 Exemption equivalent to 10% of

increased in export value 2002-2006

Exemption equivalent to 50% of the increased in export value

2007 No changes

k. Rental of ISO containers received by non-residents from shipping companies in Malaysia

2000-2001 2002-2006

No exemption Exempted from income tax w.e.f 20.10.2001

2007 Exemptions included rental payment of ships under voyage charter, time charter and/or bare boat charter w.e.f 02.09.2006

l. Compensation for loss of employment 2000-2002 Exempted from income tax up to RM4,000 per complete year of service

2003-2006 Exemption limit increase to RM6,000

2007 No changes m. Fees or honorarium received by

lecturers/experts from LAN (not from official duties)

2000-2003 2004-2006

2007

Taxable Exempted No changes

n. Honorarium or royalty for researchers to commercialise research finding

2000-2003 2004-2006

2007

Taxable Exempted No changes

AljeffriDean

47 Friday. September 1, 2006

o. Interest from MERDEKA bond 2000-2003 Taxable 2004-2006 Exempted 2007 No changes p. Income from foreign source remitted by a resident

2000-2003 2004-2006

Taxable Exempted

2007 No changes q. Interest income derived by non-resident

companies from investments in islamic securities and debentures and Government Securities

2000-2004 2005-2006

2007

Taxable Exempted No changes

r. Chargeable income distributed to unit

holders of REIT or PTF approved by Securities Commisioner

2000-2004 2005-2006

2007

Taxable Exempted No changes

s. Retirement Gratuities at retirement age below 55

2000-2004 2005-2006

Taxable up to RM6,000 per complete year of service

2007 No changes t. Income from Islamic banking and takaful business

2000-2006 2007

Taxable Exempted (w.e.f YA 2007 until YA 2016)

u. Local and foreign companies managing

funds of foreign investors established under Shariah principles.

2000-2006 2007

Taxable Exempted (w.e.f YA 2007 until YA 2016)

v. Income tax exemption for seafarers working on board a foreign ship

2007 Tax exemption for income of a seafarer who is employed by a Malaysia shipping company on board a foreign ship chartered by the employer

w. Tax treatment for perquisite 2007 Tax exemption for award received

by employees in cash or in kind up to RM1,000

AljeffriDean BUDGET 2007: Summary & Comments

Friday. September 1, 2006 48

CORPORATE TAX Tax Rates Income tax 2000-2002 28% 2003 Companies with paid up capital not more

than RM2.5 million – Chargeable income of first RM100,000 = 20% and the balance is taxed at 28%

2004-2006 Chargeable Income up to RM500,000 is taxed at 20% and the balance is tax at 28%

2007 27% (normal tax rate) (YA 2008 will be reduced to 26%)

Assessment system 2000 Current year basis. 2001-2006 Self assessment system / Current year basis 2007 No changes Insurance Company Incentive for mergers 2000-2006 50% of accumulates losses of the acquired

companies be allowed as deduction in form of tax credit to be utilised within 2 years.

2007 No changes Stock broking firms Incentive for mergers 2000-2006 50% of accumulates losses of the acquired

companies be allowed as deduction in form of tax credit to be utilised within 2 years.

2007 No changes Banking industries

Interest on loan 2000 Exempted if achieve at least 10% growth in net lending

2001-2006 Taxable 2007 No changes

AljeffriDean

49 Friday. September 1, 2006

Deductible Expenses Donation to seriously ill person deposited into an account approved by IRB.

2000-2001 2002-2006

2007

Not deductible Deductible No changes

Donation to approved institution 2000 Fully deductible from aggregate income. 2001-2006 Deduction restricted to 5% of aggregate

income 2007 Deduction restricted to 7% of aggregate

income Sponsoring arts and cultural activities approved by Ministry of Cultural Arts performed in Malaysia

2000 2001-2003

No deduction Deductible up to RM 200,000