Embed Size (px)

Citation preview

Featured Articles

• Why Audit Fleet Inventory?

• A Focus on the Fundamentals

• Audit of Metropolitan Nashville's Fuel Management Program

• Risks for Fleet Services

• Kansas City Streetcar's Public-Private Partnership

• Denver International Airport Fleet Management Program Audit

• King County Transit Audits

Local Government Auditing QuarterlyThe Journal of Local Government Auditing | Fall 2016

algaonline.org

Auditing Fleets

From the Editor

Welcome to the Fall 2016 issue of the LGAQ, Auditing Fleets. Much like our Summer issue, we have a lot of articles for you relating directly to the issue theme, but we have just as much content that does not directly relate to the theme of fleet operations. This is part of what I value about the Quarterly: providing something for everyone. Not

interested in fuel management or vehicle inventory? Never fear. Your interest is likely to be piqued by one of our other features, which address topics as wide ranging as mentorship, quality assurance, leadership, GASB, and fraud.

This is why we decided to start splitting out our feature articles into two sections: (Issue Theme) Features and Other Features. We will continue to have a dedicated theme for every issue but always welcome articles on other topics of interest to ALGA’s membership. This subtle change reflects more accurately how the LGAQ has been delivering content to our readers.

A not-so-subtle change that will affect the Quarterly is our upcoming change in leadership! Justin Anderson will be stepping down after three years as Chair of the Publications Committee. Justin has been a dedicated and thoughtful Chair, keeping things humming along and helping us bring exciting ideas to fruition. As the Editor of the LGAQ, I couldn’t have asked for a more supportive partner. I will miss his advice, encouragement, and perspective. Lucky for us, we will be in the very capable hands of Lisa Callas, who has been a member of the Publications Committee since 2014. Lisa’s familiarity with all things publications will be an asset to what I expect to be a seamless transition.

Fall isn’t typically thought of as a time of renewal—unless you are renewed by the arrival of football season—but I love this quote from The Great Gatsby by F. Scott Fitzgerald: “Life starts all over again when it gets crisp in the fall.” So, here’s to fresh starts, crisp weather, and football.

--Emily Jacobson

LGAQ: VOLUME 30, NUMBER 1

About the Quarterly

The Local Government Auditing Quarterly (LGAQ) is published

four times a year – in September, December, March, and June – by the Association of Local Government Auditors (ALGA)

Association of Local Government Auditors

499 Lewis Hargett Circle Suite 290

Lexington, KY 40503(859) 279-0686

Opinions expressed in the Local Government Auditing Quarterly are those of individual authors,

and they may differ from ALGA’s policies, official statements of

ALGA committees, or those of an author’s employer.

LGAQ Editor

Emily JacobsonCity and County of Denver, CO

LGAQ Assistant Editor

Kristine Adams-WannbergCity of Portland, OR

Social Media

Follow ALGA at algaonline.org

Follow ALGA on Twitter at twitter.com/ALGA_Gov

LGAQ Fall 2016 | Page i

TABLE OF CONTENTS

UPCOMING EVENTS

2Training Opportunities

2016 ANNUAL CONFERENCE

3Highlights

COLUMNS

7Opportunities for ImprovementGary Blackmer

FLEET FEATURES

12Why Audit Fleet Inventory?Nia Young

16A Focus on the FundamentalsJim Williamson

19Audit of Metropolitan Nashville’s Fuel Management ProgramSeth Hatfield

23Risks for Fleet ServicesJanine Mryglod, Queena Dong & Edwin Ryl

27Kansas City Streetcar’s Public-Private PartnershipJonathan Lecuyer

31Denver International Airport Fleet Management Program AuditSonia Montano

35King County Transit AuditsSean DeBlieck

OTHER FEATURES

38Reflections on Becoming a Mentor: Minions, Karma, and Everything In BetweenEric Spivak

41Q&A About QAOlga Ovcharenko

46Principles in Action: Reflections From a New CAEShanda Miller

51Do We Need a Universal Accounting Model for Leases?Khaled Abdel Ghany

57Preventing Fraud and Detecting Collections Fraud in CountiesJohn DuPree

SUBMISSIONS

62Submitting Abstracts, Articles, and Member News

LGAQ Fall 2016 | Page 1

TRAINING OPPORTUNITIES

WEBINAR

Oct 11 — Webinar: Stratified Random Sampling: Common Uses in Performance Audits

ANNUAL CONFERENCE

2017 ALGA Annual ConferenceMay 22-23, 2017Atlanta, Georgia

Pre-conference workshops will be held on May 21; post-conference workshops will be held on May 24.

EVENT REGISTRATION AND MEMBERSHIP MANAGEMENT PORTAL

ALGA’s event registration site can be found at alga.membershipsoftware.org.

At this site you can:

• Register for any ALGA event• Update your contact information and

renew your membership• Access ALGA’s online directory• Access ALGA’s members-only online

training resources

Questions about the event registration and membership management portal may be directed to ALGA Member Services at (859) 276-0608.

ARCHIVED WEBINARS & FREE TRAINING VIDEOS

Miss a webinar that you really wanted to participate in? You can access ALGA’s archived webinars on the membership management portal at alga.membershipsoftware.org!

Most of the webinars cost $50 and are worth one credit of self-study CPE (not NASBA-certified). There are also several free archived webinars.

ALGA members may view several free training videos in the portal. Videos in the following areas are available:

• Managing Audit Engagements• Risk Assessment• Fraud• Information Technology• Public Safety• Public Works• More!

You must be a current member of ALGA to view the archived webinars or to access the free training videos.

LGAQ Fall 2016 | Page 2

Exemplary Award Winner (Extra Small Shop) - City of College Station, TX

Distinguished Award Winner (Extra Small Shop) - Deschutes County, OR

Exemplary Award Winner (Small Shop) - Clark County, WA Distinguished Award Winner (Small Shop) - Sacramento City Auditor's Office

Exemplary Award Winner (Medium Shop) - City of Palo Alto, CA Distinguished Award Winner (Medium Shop) - City of Scottsdale, AZ

2016 ANNUAL CONFERENCE HIGHLIGHTS

LGAQ Fall 2016 | Page 3

Distinguished Award Winner (Medium Shop) - City of Seattle, WA

Exemplary Award Winner (Large Shop) - King County, WA

Distinguished Award Winner (Large Shop) - City of Long Beach, CA

Exemplary Award Winner (Extra Large Shop) - City and County of Denver, CO

Distinguished Award Winner (Extra Large Shop) - City of San Diego, CA

Distinguished Award Winner (Extra Large Shop) - City of San Francisco, CA

2016 ANNUAL CONFERENCE HIGHLIGHTS

LGAQ Fall 2016 | Page 4

Lifetime Achievement Award Winners - Jerry Shaubel, Jerry Heer, and Alan Ash

Outstanding Contribution to the Quarterly - Minh Dan Vuong, City of San Jose, CA

Mark Funkhauser presents at a General Session Peer Review Committee members in discussion

Listening to a General Session

2016 ANNUAL CONFERENCE HIGHLIGHTS

Evening social activities

LGAQ Fall 2016 | Page 5

Kymber Waltmunson receiving the President Award Incoming Board Members

Member Services Evening social activities

Evening social activities Evening social activities

2016 ANNUAL CONFERENCE HIGHLIGHTS

LGAQ Fall 2016 | Page 6

OPPORTUNITIES FOR IMPROVEMENT

WHAT I LEARNED WITHOUT TRAINING

Throughout my 30 years of auditing in three entirely different work environments– city, county, and state–I was always learning things that were never taught to me. I’m not criticizing continuing professional education at all; there is just so much to be learned, more than I acquired in all those classes, conferences, and webinars.

I also learned that some topics should be taught but aren’t, while others simply can’t be taught except through experience.

EVIDENCE

Evaluation of evidence should be taught. I have sought out practical audit training on evidence but it simply doesn’t exist. Oh sure, you can look at the Yellow Book but the definition of sufficiency is vague and circular. In part, there isn’t and can’t be a specific standard because sufficiency is related to the context of the audit statement being supported. It seems that such a key concept should be better explained in the Yellow Book, which could guide some training.

Without training, every audit shop seems to send rookie auditors out to gather evidence and expect on-the-job-training to establish some concept of sufficiency. When I was a rookie my first assignment was to perform quality control on an audit. I was challenged to think about what was persuasive evidence and it helped me see the kinds of expectations I needed to meet for evidence. I also saw how audits were assembled, which helped immensely when I started gathering and organizing needed evidence.

Ironically, many audit shops are pushed by the ‘supervision’ word in the Yellow Book to think only an experienced auditor understands sufficiency to perform this function. Everyone needs to understand sufficiency. The most important unmet training need is a conceptual structure and language to allow auditors to discuss the various considerations that comprise sufficiency.

By Gary Blackmer

LGAQ Fall 2016 | Page 7

OPPORTUNITIES FOR IMPROVEMENT

Beyond the lack of clarity, there are efficiencies to be gained if auditors can distinguish sufficient from superfluous evidence. Gathering unnecessary evidence can eat a lot of audit hours. Consistent training will help the new hire develop, improve everyone’s efficiency while assuring compliance with standards, and reduce problems during quality control reviews.

We developed some training in Oregon to describe the aspects of sufficiency, which was presented at the ALGA conference in San Diego, and it is the first I’ve seen.

WRITING

Until I watched a journalist craft an audit report, I didn’t realize how badly I wrote, and we all wrote. In that audit, the narrative flowed, the findings were accessible, and the agency’s story was alive. In contrast, my sentences were cumbersome. My writing contained stale phrases with no spark of humanity. I still don’t write as well as I wished, but the much higher standard keeps me humble.

This storytelling skill is in us, but we seem to smother it in jargon. At our internal meetings on audit progress, we talk about our findings in clear and compelling ways. Then we write as if it were a technical manual for a nuclear spectroscope. Here’s my scientific explanation: our brains are closer to our mouths, and much farther from our fingers on a keyboard. The message degrades in the transmission.

I probably had at least 240 hours of training in my career to write better and it never made a lasting impression. Stan Stenersen’s training was the exception. He taught auditors how to translate complex findings into accessible concepts, which was a big leap. He also covered the second big step toward improving audit writing: incorporating the entire organization in addressing its collective writing and editing behavior. Senseless editing will puree the best sentences to a flavorless pulp.

The last step, expanding the vocabulary to enliven the narrative, wasn’t covered. We need good training, but organizations must empower our auditors to write stories for the public in an incisive language.

AUDIT PROCEDURES

There are two perspectives needed here. Managers need to be exposed to various ways that audits can be performed and staff need to be trained on the particular procedures chosen by their agency managers.

Anyone who thinks there is only one way to conduct an audit hasn’t been on a peer review. A common challenge for new peer reviewers is to accept that their way of conducting an audit is not the only way. Once they’ve overcome that mindset they will be surprised at how much they can learn about different ways to conduct audits and still comply with audit standards.

Until I watched a

journalist craft an

audit report, I didn’t

realize how badly

I wrote, and we all

wrote.

LGAQ Fall 2016 | Page 8

OPPORTUNITIES FOR IMPROVEMENT

There are multiple approaches to produce audits but these are not being taught. Even if they were, whole management teams need to be trained on the alternatives to help them agree upon the best steps for their organization. Once decided and documented, the rest of the staff need to be trained. Developing this training is important for new hires because the organization will benefit from a shorter learning curve, improved performance, and greater impact audits. You may think experienced auditors would need less training but I’ve also seen ‘generations’ of auditors, and managers, who each cling to the habits and precepts of their particular brand of early training. Engaging the whole organization in continual career learning is what we would ask of our auditees and we should commit to the same standard ourselves.

FACILITATION

One of the most valued classes I took many years ago taught meeting facilitation for applying a COSO framework. Most of the time was spent on skills and tools for leading discussions, with an emphasis on the responsibility of a facilitator to promote open discussion and reach a decision, without influencing it. It was not taught by an auditor, but by a facilitator.

The role of a facilitator was the big takeaway for me. Of course in exit interviews, I never declared I would play the ‘facilitator’ but I applied the skills. Watching the discussion from an observer’s standpoint, rather than a participant, gave me new insights, especially when I saw the unspoken body language. What was most valuable to me was the ability to switch from facilitator to decision-maker when needed. All managers and staff auditors could benefit from this training.

FINDING FINDINGS

I have said this before in many different ways, but we need to ensure that our audits address actual recurring problems more than theoretical risks. Identifying the biggest problems should be the first step of an audit.

Sure, we can train and apply the COSO model or other risk analyses to identify many things that might go wrong in an organization. Those are good textbook fundamentals, but we should also train auditors to spot the problems that impede the agency’s mission, using methods such as contacting staff, stakeholders, and peers of the auditee. Reality is much richer than any deductive or theoretical framework. (Trust me on this. I have a degree in philosophy.)

Yellow Book standards are silent on methods for audit topic selection. They are written as if setting the scope and objective was the first step of the audit, then developing findings within that framework. It's like your family doctor deciding, without even talking to you, that this visit will be about your spleen, just because there might be something wrong with it.

I have said this

before in many

different ways,

but we need to

ensure that our

audits address

actual recurring

problems more than

theoretical risks.

Identifying the

biggest problems

should be the first

step of an audit.

LGAQ Fall 2016 | Page 8 LGAQ Fall 2016 | Page 9

OPPORTUNITIES FOR IMPROVEMENT

Using a more inductive audit approach is not recognized in the Yellow Book, though it is not prohibited in any way. We need guidance on spotting and choosing potential audit findings, as well as training to compensate for this omission.

ORGANIZATIONAL DYNAMICS

The root causes of findings are spring from the organization. Employees may not have the supervision necessary for complex tasks. Leadership may not be hearing what is actually happening on the front lines. Resources may not match the workload in various parts of the organization. Or line staff may not be hearing clear direction from leadership.

Here is a sad truism that we have all seen: organizations dominated by frustrated and unhappy employees are less likely to provide good services. Talking to managers and line staff can reveal these problems to auditors who can then follow the causal chain on to their adverse effects on public services. I know there are public administration classes that teach how to organize people and resources to achieve an objective, which can be great criteria, and guide recommendations. A class on common dysfunctions in organizations could also help auditors more quickly spot the deficiencies.

UNTRAINABLE TOPICS

One of my phrases to auditors has been, “This is not your typical audit, but no audit is typical.” In reality, auditing is really more like jazz, not sheet music.

Over the years I learned that each audit follows its own path through the landscape of an organization and its mission, to use another metaphor.

Practice, Practice, Practice ─ A new hire sees that landscape as if it were a maze. The maze is a combination of audit standards and procedures, the finding, the relationship with the auditee, and many other factors. The movement within the maze seems haphazard, without an understanding of distance or overall direction. Afterward, the path taken and the structure of the maze can be better understood, as if seen from above. Yet the next audit is likely to be a different maze, with some factors altered.

Rote training produces unrealistic expectations for auditors. By unrealistic I mean impractical and unsuccessful when automatically applied. Auditors need to find the underlying and undiscovered themes that impede an organization, then draw the managers onto the path to improvement. And surprises will happen that the best laid plans will never anticipate.

No training can replace the experience gained from multiple audits, and the experience gained from the departures in subtle and important ways from a ‘standard’ path.

LGAQ Fall 2016 | Page 10

One of my phrases

to auditors has been,

“This is not your

typical audit, but no

audit is typical.” In

reality, auditing is

really more like jazz,

not sheet music.

LGAQ Fall 2016 | Page 11

OPPORTUNITIES FOR IMPROVEMENT

And multiple audits can instill an understanding of the role and conduct of an auditor in the course of an audit. We can talk about attitude and ethics and objectivity and many other important expectations, but again, the situations add that other layer of complexity, sometimes called real life.

Position of the Auditor ─ Training can’t address the unique ‘contexts’ of an audit organization or the organization being audited. The attitude toward the audit organization within the jurisdiction is one determinant of the auditor’s role. The relationship with elected officials is delicate and complex, starting with the authority of the auditor, either legislatively directed or independently elected. Some general principles can be set out in training, but the political context of the audit organization plays out in agency interactions and public perceptions of the auditors as they go about their work.

If the agencies respect or distrust or trivialize auditors, then each requires a different communications style that can’t be taught in a national seminar. Neither can training instill the correct behavior in an auditor who encounters angry auditees, an abused whistle blower, or the distraught victim of inappropriate agency ‘services’.

Good Coaching ─ There is no substitute for experience. And there is no substitute for a good mentor, on-the-job trainer, or communicative leader to offer guidance for new hires and experienced auditors. The field of performance auditing depends upon an apprenticeship period for its new auditors because there is so much that can’t be taught, or is particular to the audit organization’s working environment.

A performance auditor’s learning curve will truly span an entire career because we must never stop seeking ways to be better. And, continuous learning is one of the most satisfying elements of this profession.

ABOUT THE AUTHOR

Gary Blackmer has been conducting audits for 30 years and recently retired from his position as Director of the Oregon Audits Division. The Division conducts performance, financial, and information technology audits, monitors financial audits of local governments, and responds to hotline allegations. Previously, Blackmer served 10 years as the elected Portland City Auditor, eight years as elected Multnomah County Auditor, a management auditor, and analyst for a variety of state and local agencies. Blackmer is a past-Chair of the Pacific Northwest Intergovernmental Audit Forum, and past-President of the Association of Local Government Auditors. He received the ALGA Lifetime Achievement Award in 2015.

Training can’t

address the unique

‘contexts’ of an audit

organization or the

organization being

audited. The attitude

toward the audit

organization within

the jurisdiction is

one determinant of

the auditor’s role.

LGAQ Fall 2016 | Page 12

AUDITING FLEETS

WHY AUDIT FLEET INVENTORY?

Accurate inventory data reduces the risk of loss or theft and provides information for the city to manage its inventory to maintain adequate stock for repairs. Data reliability was a key focus in two of our fleet-related audits. We conducted an audit in 2011 that evaluated controls and efficiency of fleet inventory operations, and in 2012 we evaluated controls over city fueling sites.

INACCURATE INVENTORY RECORDS MASKED LOSSES

We set out to match inventory recorded in the system to physical facility and found that out of a total value of $1.9 million recorded inventory, $500,000 was recorded with unknown location codes. Staff was unable to tell us where these 18,000 items were physically located, or whether they had ever been in the city’s custody or were recorded in error. We also tested stock levels for a random sample of 30 items to compare quantities recorded in inventory to quantities on hand. In eight instances, fewer items were on the shelf than were recorded in inventory. In one instance, one more item was on the shelf than was recorded in inventory. Both over and undercounts flag potential theft or billing problems. Inaccurate records of the quantity of parts on hand make it more difficult to detect theft or loss.

The Office of Fleet Services’ written policies required employees to conduct monthly counts of parts inventory, which we discovered had not occurred. Further, the office had no method to reconcile its fleet management system records with the city’s financial management system to ensure that all purchased items were recorded in inventory. Staff entered information into both systems, which weakened controls in each system that were intended to segregate incompatible duties and ensure items were accounted for when received. We identified discrepancies between purchases processed in Oracle and purchases recorded in the inventory system for the same period. In particular about 700 part purchases, totaling about $350,000 recorded in the inventory system over an 18-month period, had no corresponding record of receipt. These and other discrepancies and billing errors suggested that supervisory review and management approvals were not functioning as effective controls.

Nia Young

LGAQ Fall 2016 | Page 12 LGAQ Fall 2016 | Page 13

AUDITING FLEETS

INACCURATE INVENTORY RECORDS CONTRIBUTED TO OPERATIONAL INEFFICIENCY

Inaccurate inventory records also made it more difficult to establish and monitor reorder points to ensure that stock was available when needed. Of the 541 work orders open during our audit, 21% were waiting for parts that were supposed to be stock items. Almost 30% of the work orders had been open for more than 31 days. Longer turnaround times for maintenance and repairs increase the city’s operating costs. Inaccurate data also made it difficult to assess operations. Inventory turnover in 2010 was less than half of the industry standard, which could reflect bad data but could also indicate that the city was carrying obsolete parts, ordering incorrect parts, or failing to stock the parts that it needs. The turnover rate measures how often parts are used by calculating the ratio of parts billed to the average value of parts in inventory over a specified period.

We also noted that consolidating parts warehouses would improve operational efficiency and better safeguard inventory. Based on industry standards, the Office of Fleet Services didn’t have enough parts specialists to cover all shifts at all facilities. Inadequate staffing increased risk of theft and loss because incompatible duties were not segregated. To compensate for lack of parts specialists on duty, mechanic supervisors had keys to parts rooms. Further, we observed physical security risks, including poor lighting and unsecured access points, at five of the city’s seven locations.

MISUSE OF FUEL LIKELY COST THE CITY MORE THAN $300,000 PER YEAR

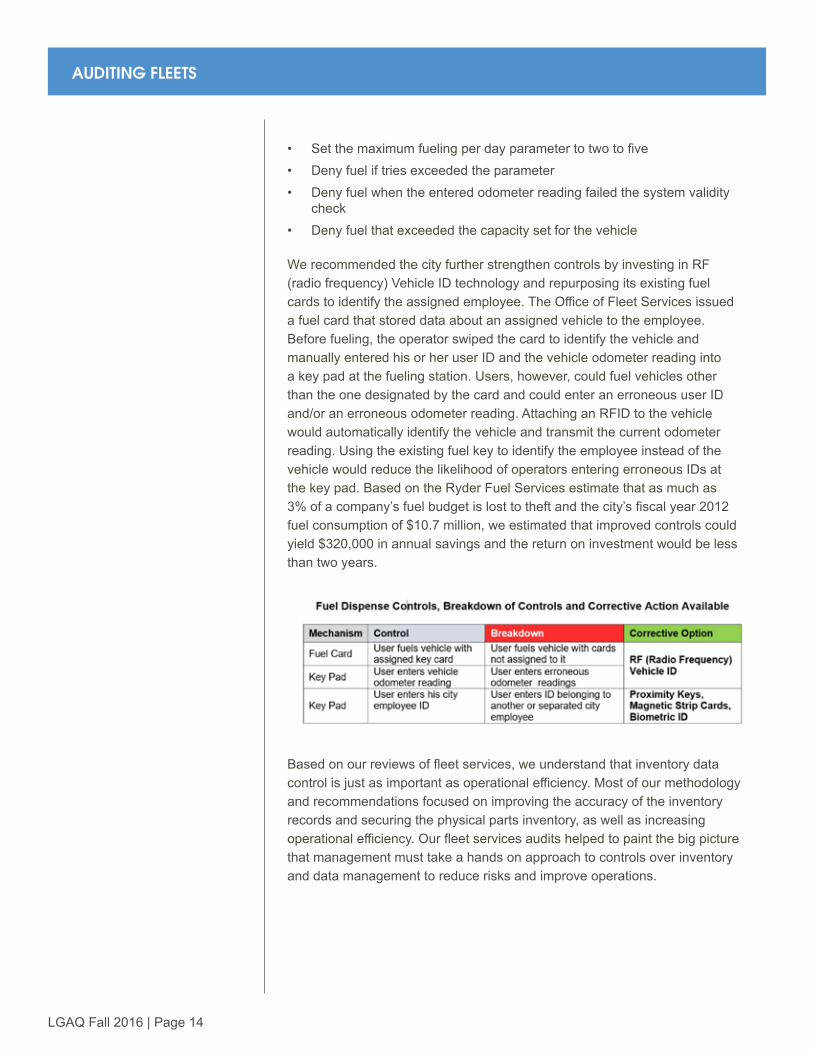

The Office of Fleet Services dispensed over 7 million gallons of fuel totaling $23 million in between March 2010 and June 2012. The office tracked departments’ fuel use with an automated fuel management system and billed departments monthly. Industry experts identify fuel as the second largest public sector fleet expense and some estimate that 3% of a company’s fuel budget is lost to theft. Our audit identified significant control deficiencies and an overall control environment inadequate to prevent or detect theft or misuse of fuel. The Office of Fleet Services failed to implement system settings to limit the amount of fuel pumped into vehicles/equipment. The system configuration allowed most vehicles/equipment to fuel up to 99 times per day, pump fuel after entering erroneous odometer readings, and even allowed users to dispense more fuel than the recorded capacity of the vehicle. Configuring the system with limits and to check the validity of data entered reduces the opportunity for theft and ensures that vehicle use data are accurate, which can allow fleet services management to identify underused equipment and to calculate miles per gallon per vehicle to flag potential problems. As a result of the audit, the fleet services director updated the system configuration to:

Inventory turnover

in 2010 was less

than half of the

industry standard,

which could reflect

bad data but could

also indicate that

the city was carrying

obsolete parts,

ordering incorrect

parts, or failing to

stock the parts that

it needs.

LGAQ Fall 2016 | Page 14

AUDITING FLEETS

• Set the maximum fueling per day parameter to two to five• Deny fuel if tries exceeded the parameter• Deny fuel when the entered odometer reading failed the system validity

check• Deny fuel that exceeded the capacity set for the vehicle

We recommended the city further strengthen controls by investing in RF (radio frequency) Vehicle ID technology and repurposing its existing fuel cards to identify the assigned employee. The Office of Fleet Services issued a fuel card that stored data about an assigned vehicle to the employee. Before fueling, the operator swiped the card to identify the vehicle and manually entered his or her user ID and the vehicle odometer reading into a key pad at the fueling station. Users, however, could fuel vehicles other than the one designated by the card and could enter an erroneous user ID and/or an erroneous odometer reading. Attaching an RFID to the vehicle would automatically identify the vehicle and transmit the current odometer reading. Using the existing fuel key to identify the employee instead of the vehicle would reduce the likelihood of operators entering erroneous IDs at the key pad. Based on the Ryder Fuel Services estimate that as much as 3% of a company’s fuel budget is lost to theft and the city’s fiscal year 2012 fuel consumption of $10.7 million, we estimated that improved controls could yield $320,000 in annual savings and the return on investment would be less than two years.

Based on our reviews of fleet services, we understand that inventory data control is just as important as operational efficiency. Most of our methodology and recommendations focused on improving the accuracy of the inventory records and securing the physical parts inventory, as well as increasing operational efficiency. Our fleet services audits helped to paint the big picture that management must take a hands on approach to controls over inventory and data management to reduce risks and improve operations.

LGAQ Fall 2016 | Page 15

AUDITING FLEETS

ABOUT THE AUTHOR

Nia Young is a Senior Performance Auditor for City of Atlanta. Previously, she was a government operations consultant with the Department of Education in Florida, with additional experience in higher education organizations in program management and evaluation. Nia earned her Masters of Public Administration degree from Southern University in 2012.

LGAQ Fall 2016 | Page 16

AUDITING FLEETS

A FOCUS ON THE FUNDAMENTALS

It’s easy to get enchanted with innovative ways of doing things and forget about the fundamentals of the task. In football, you often see an infatuation with new offenses like the “air raid” or “mobile quarterbacks;” but in the end, most games turn on which team has the best fundamentals. Blocking, tackling, footwork, positioning: these are the important fundamentals that successful coaches never forget. In our profession, using data analysis to develop value-added recommendations to improve operating efficiency and program outcomes is now common. More reader friendly reporting styles are developing to enhance communication of our audit results. Technology is becoming integrated into almost every aspect of our work. This type of innovation and change is important to auditors’ continued relevance and success. But, like successful football coaches, we shouldn’t forget our fundamentals: analytics, assessing internal controls, and verifying that control procedures are carried out effectively. A recent audit in Oklahoma City illustrates this point.

THE GAME PLAN

Oklahoma City hires a contractor to operate five parking garages and six surface lots. The contractor collects and remits $7.5 million in annual operating revenue by depositing collected revenue directly into a City bank account. The City reimburses the contractor $2.4 million for annual operating costs and pays the contractor a $100,000 management fee. We included an audit of this contract in our audit plan based on the amount of cash handled in the operation and previous lapses in contractor oversight by the City’s Parking Division staff.

SCANNING THE FIELD

Our initial step in the audit was a comparison of reported monthly revenue to bank deposits for our fiscal year audit period. This simple comparison revealed a $190,000 cash shortfall. Initial inquiries with the contractor’s Accounting Manager, a 15-year employee assigned as our audit contact, were fruitless. The Accounting Manager’s explanation was that “it must be some sort of timing difference.”

Jim Williamson

LGAQ Fall 2016 | Page 17

AUDITING FLEETS

Her apparent apathy about the issue was disconcerting. The City’s Parking Division staff were also no help as we discovered they didn’t perform basic reconciliations of the contractor’s monthly revenue reports to the bank account. Their oversight was limited to comparing daily cashier reports to corresponding bank deposits. They had adopted the approach that, “if the daily deposits match, then the monthly revenue amounts must be accurate.” Knowing that we had a typical assessment and testing of the contractor’s internal controls ahead of us, we postponed further investigation of the discrepancy in hopes that our fieldwork would help us better understand the subject.

BLITZING

Our control assessment revealed no obvious weaknesses and this seemed to be confirmed during our walk-through. However, in testing, we quickly identified missing cashier deposits from the daily revenue collections. We elevated our discussion of the discrepancies to the contractor’s Controller who, after not being able to explain the missing funds, proceeded to call the Accounting Manager into her office. The Accounting Manager reiterated that “it must be some sort of timing difference.” At this point we informed the Controller that we believed the missing cashier deposits were the reason for the $190,000 cash shortfall discovered in our initial analysis. The Controller responded by saying, “What $190,000 shortfall?” The Accounting Manager had not informed the Controller of our earlier inquiry. Later that day, when the Accounting Manager didn’t return from lunch, the Controller contacted us to say she was afraid there was a problem.

THE FAKE

As our investigation progressed we discovered that, contrary to contractor policy, the Accounting Manager often took the daily revenue collections to the bank. Given the Accounting Manager’s revenue responsibilities, this violated the basic segregation of duties principle. Separate deposits were made for each cashier. During a trip to the bank, the Accounting Manager would open the sealed bank bag, remove a cashier deposit, and then seal the remaining cashier deposits in another bank bag to which she had access. Upon returning to her office, the Accounting Manager would simply omit the stolen funds’ daily cashier report from those sent to the City’s Parking Division. She hid her embezzlement from City staff, but she did not have the ability to change daily deposit summaries required by the contractor’s corporate office.

To hide her theft from corporate staff, she included the stolen cashier deposit amounts on a calculator tape, obviously not supported by receipted deposit slips, but nicely matching the daily revenue reports. She emailed the packet to the contractor’s corporate office where, as she had hoped, employees relied on the calculator tape rather than receipted deposit slips confirming the daily revenue total. The Accounting Manager carried out this scheme from May 2012 through November 2015, embezzling almost $420,000.

LGAQ Fall 2016 | Page 18

AUDITING FLEETS

SACKING THE QUARTERBACK

Due to the magnitude of the fraud and the fact that grant funds are involved in financing the City’s Transportation and Parking Department, the Police Department referred the case to an Interagency Task Force comprised of local, state, and federal agency representatives, including the IRS. We provided evidence of the embezzlement to the Task Force and assisted them in developing the case. The Task Force presented the case to the US Attorney General’s Office who filed charges against the Accounting Manager.

During sentencing, the Accounting Manager admitted embezzling to “cover up a gambling addiction.” She was convicted in federal court of wire fraud (emailing false revenue reports) and tax fraud (failing to declare income from her embezzlement). The Accounting Manager was ordered to pay $500,000 in restitution, spend 5 years on probation, and serve 216 days in jail on weekends. The City’s agreement with the contractor stipulates that the contractor is responsible for the operating revenue until it is deposited in the City’s bank account. The contractor remitted all of the missing revenue to the City. The contractor’s insurance company and the IRS will receive most of the restitution payments.

WINNING THE GAME

Our detection of this fraud was a good reminder to focus on the fundamentals; it was perpetrated without segregated duties, concealed with falsified documents, and undetected by management due to control procedures not being carried out effectively. It was detected through basic analytics, control assessment, and compliance testing. We auditors should continue to strive to be innovative and forward thinking but, like successful football coaches, we can’t afford to forget our fundamentals.

ABOUT THE AUTHOR

Jim Williamson joined the Office of the City Auditor in 1988, was appointed City Auditor in 2008, and has over 32 years of auditing experience. Jim has held several positions with ALGA including President and Peer Review Committee Chair as well as several positions with the IIA’s Oklahoma City Chapter including President. He serves as Past-Chair on the Peer Review Oversight Committee for the Oklahoma Accountancy Board. Jim is also an AICPA, OSCPA, ACFE and AGA member.

Our detection of this

fraud was a good

reminder to focus on

the fundamentals;

it was perpetrated

without segregated

duties, concealed

with falsified

documents, and

undetected by

management due to

control procedures

not being carried out

effectively.

LGAQ Fall 2016 | Page 19

AUDITING FLEETS

AUDIT OF METROPOLITAN NASHVILLE’S FUEL MANAGEMENT PROGRAM

INTRODUCTION

In September 2008, rumors spread that Nashville would run out of gasoline due to recent hurricanes along the gulf coast. The rumors caused a run on gas stations and left the majority of them dry. Two years later, a 1,000-year flood brought Nashville to a standstill and caused extensive damage to Nashville’s businesses, homes, and infrastructure. The Metropolitan Nashville police cruisers, fire trucks, and public works vehicles were able to keep operating during these extraordinary situations due to the effective fuel management practice of maintaining internal fuel sites. This highlights how important an effective fuel management program can be for your city. In 2012, our office conducted a performance audit of the government’s motor fuel usage. The purpose of this article is to highlight the objectives, testing, and recommendations from our audit.

BACKGROUND

In 2004, Transportation Consultants, Incorporated conducted a review of the Metropolitan Nashville and Davidson County fuel program. The recommendations from that report helped shape the current structure of the government’s fuel management program. One recommendation was the creation of the Office of Fleet Management with the goal that it would be the principal entity for procurement, dispensing, accounting, and billing for fuel. This was accomplished by Mayor Karl Dean’s Executive Order Number 31, which established the Office of Fleet Management in hopes to centralize the fuel management function. The Office of Fleet Management is comprised of five programs: Contracts and Assets, Parts, Repair Shops, Special Operations, and Fuel and Assets Financials.

OBJECTIVES

Our audit primarily focused around the fuel management within the Fuel and Assets Financials Program: billing for fuel usage, internal fuel sites, and fuel cards. For fuel usage billings, we wanted to determine if billings were complete

Seth Hatfield

LGAQ Fall 2016 | Page 20

AUDITING FLEETS

and accurate. With the internal fuel sites, we wanted assurance that fuel purchased, received, and pumped was being tracked, and the sites were physically protected. For the fuel card program, our objective was to determine that payments made were for authorized transactions.

FUEL USAGE BILLINGS

The Office of Fleet Management uses either allocated billings or direct billings to recover the costs of fuel and preventative maintenance. Allocated billings are used for vehicles purchased through the Office of Fleet Management reserve fund, and direct billings are used for vehicles purchased through grants, forfeitures, and other fleet additions.

The specific department’s previous years’ fuel consumption is the basis for the allocated billings. Once an approved budget was in place, the department’s allocation percentage was multiplied by the budget to determine the amount of the billing.

For direct billing vehicles, the actual usage is directly billed to the department. The Metropolitan Nashville owned fuel sites have a Fuel Master system which requires a “prokee” to obtain fuel. All transactions from Fuel Master and the fuel card vendor, Wright Express, are recorded, downloaded once a month, and directly billed to departments. The Office of Fleet Management uses a Microsoft Access database to capture the billing information and to create invoices to the departments. A journal entry is then performed to move funds from the department back to the Office of Fleet Management. Our office reconciled the billing invoices back to the original data pulled from the Fuel Master system and found that 56 percent of invoices were incorrect. Another 27 percent of invoices did not have payment detail, indicating that payment may never have been received. Some of our recommendations around billing included ensuring the direct bill download matched the original information from Fuel Master and Wright Express, updating the Access database to include a field for check numbers so payment reconciliations could be completed, and periodically running reports to determine if a billing journal entry or check number is missing indicating that payment was not received.

INTERNAL FUELING SITES

The Metropolitan Nashville government has a total of 21 fuel sites. Six are operated by the Office of Fleet Management, six are operated by the Parks and Recreation Department, and another nine are operated by the Fire Department. Our office selected three sites and performed a quarterly inventory. The reconciliations found variances ranging between negative 4,157 gallons and positive 767 gallons. The Office of Fleet Management personnel stated that the veeder root probes, the gauges measuring the fuel, were not regularly calibrated. The calibrations were not required by Tennessee State law because the fuel was not being sold to the public.

Our office reconciled

the billing invoices

back to the original

data pulled from the

Fuel Master system

and found that 56

percent of invoices

were incorrect.

Another 27 percent

of invoices did not

have payment detail,

indicating that

payment may never

have been received.

LGAQ Fall 2016 | Page 21

AUDITING FLEETS

The veeder root probes were only calibrated when a problem caused an operational error or alarm. Additionally, the mechanical pulsars could stick, count too fast/slow, and can create metering errors causing the gallon count to be off in the Fuel Master system. The American Petroleum Institute recommends daily and monthly inventory reconciliations as a good practice and that operational practices should be carefully examined when variances exceed five gallons per every 1,000 gallons. Our office recommended veeder root equipment be calibrated per equipment guidelines, quarterly calibrations tests be completed and documented for pumps and meters, and daily and monthly reconciliations be completed.

Purchasing motor fuel at a competitive price is an important area to review when auditing a fuel program. Daily quotes received by the Office of Fleet Management for 45 days were compared to Oil Price Information Service historical rack prices for the Nashville market as part of the audit procedures. No material pricing differences were observed.

Physical and internal protection of fuel sites is necessary to prevent unauthorized access from the general public. Our auditors visited fuel sites around the city and found most sites to have adequate protection. The fuel sites operated by the Office of Fleet management had the protection of the Fuel Master “prokee” which is necessary to pump fuel. The fuel sites operated by Parks and Recreations had fences and padlocks to protect their pumps. The only issues were with the diesel pumps located at fire stations which had no protection against unauthorized use. However, the proximity to the fire stations acted as a thief deterrent factor. It was evident that with three different entities operating fuel sites, the government was not achieving a centralized fuel management program as recommended by Mayor Dean’s Executive Order 31. We recommended that the Office of Fleet Management coordinate with the Office of the Mayor to determine if the current operating practices were aligned with the intent of the Metro-wide fuel management system.

FUEL CARDS

Fuel cards are used by Metropolitan Nashville vehicles when access to internal fuel sites may not be possible or convenient. We wanted to determine if fuel cards were being used for authorized purchases and that no duplicate payments existed. An administrative order specifies fuel and car washes to be the only acceptable purchases with a fuel card. Specifically, only 87 Octane gasoline, E85 Ethanol, and #2 diesel fuel purchases were allowed for fuel. We requested all purchases from Wright Express during the audit period and uploaded them into ACL Analytics for analysis.

The “Look for Duplicates” function was used to locate any duplicate charges that would have been paid. This test pinpointed 66 duplicate payments between January 1, 2010, and December 31, 2011. To locate unauthorized transactions, any product description that did not match an authorized

We recommended

that the Office of

Fleet Management

coordinate with

the Office of the

Mayor to determine

if the current

operating practices

were aligned with

the intent of the

Metro-wide fuel

management

system.

LGAQ Fall 2016 | Page 22

AUDITING FLEETS

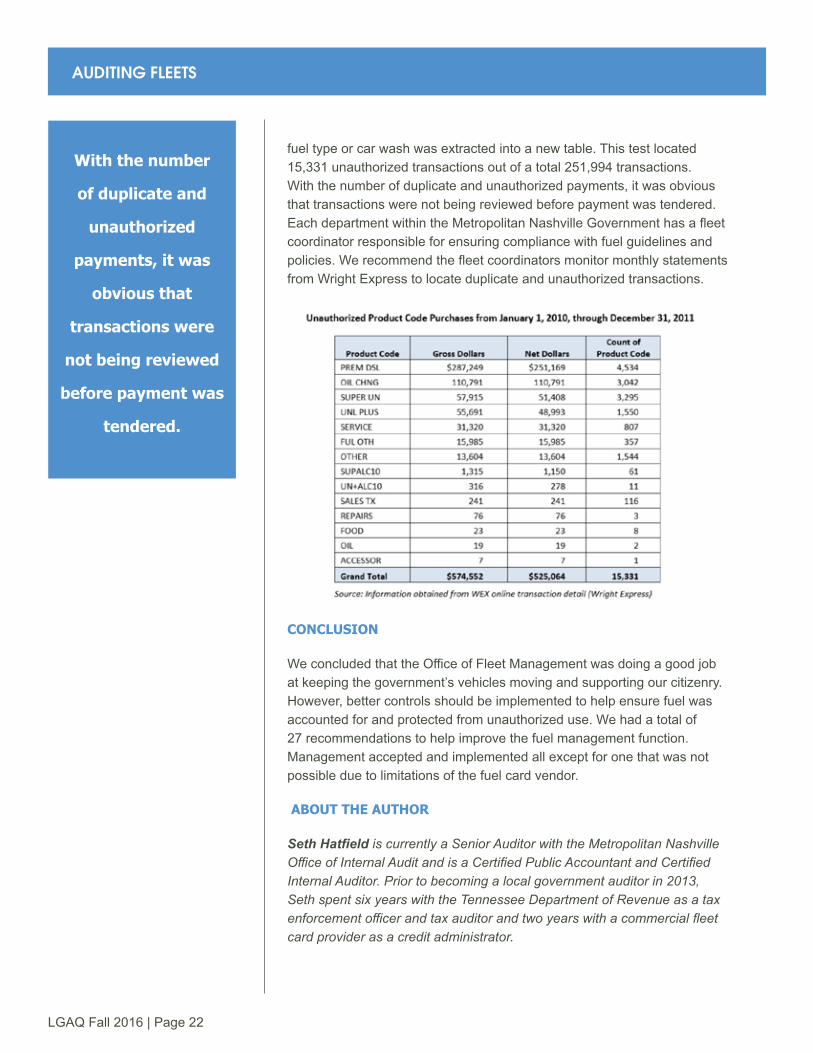

fuel type or car wash was extracted into a new table. This test located 15,331 unauthorized transactions out of a total 251,994 transactions. With the number of duplicate and unauthorized payments, it was obvious that transactions were not being reviewed before payment was tendered. Each department within the Metropolitan Nashville Government has a fleet coordinator responsible for ensuring compliance with fuel guidelines and policies. We recommend the fleet coordinators monitor monthly statements from Wright Express to locate duplicate and unauthorized transactions.

CONCLUSION

We concluded that the Office of Fleet Management was doing a good job at keeping the government’s vehicles moving and supporting our citizenry. However, better controls should be implemented to help ensure fuel was accounted for and protected from unauthorized use. We had a total of 27 recommendations to help improve the fuel management function. Management accepted and implemented all except for one that was not possible due to limitations of the fuel card vendor.

ABOUT THE AUTHOR

Seth Hatfield is currently a Senior Auditor with the Metropolitan Nashville Office of Internal Audit and is a Certified Public Accountant and Certified Internal Auditor. Prior to becoming a local government auditor in 2013, Seth spent six years with the Tennessee Department of Revenue as a tax enforcement officer and tax auditor and two years with a commercial fleet card provider as a credit administrator.

With the number

of duplicate and

unauthorized

payments, it was

obvious that

transactions were

not being reviewed

before payment was

tendered.

LGAQ Fall 2016 | Page 23

AUDITING FLEETS

RISKS FOR FLEET SERVICES

Since 2007, the Office of the City Auditor for the City of Edmonton has conducted three audits of Fleet Services. This article summarizes some of the key risk areas and procedures that we used in these audits. The intent is to provide a resource for other auditors who may be considering, or actively planning, their own fleet services audits.

PROFILE

Fleet Services at the City of Edmonton has a large set of responsibilities. They provide fleet repair, customized fabrication, and maintenance services for the City of Edmonton as well as select private sector clients. From 15 garages in various locations throughout the City, Fleet Services maintains:

• Construction and street maintenance vehicles and equipment• Turf and ice management vehicles and equipment

• Buses, police vehicles, fire vehicles and equipment, and ambulance units

Fleet Services is also heavily involved in the equipment lifecycle process including procurement. They are responsible for managing the fleet safety program, and advising on alternative fuels, emission standards, and legislative requirements. They also provide services related to equipment modifications, and failure and collision analysis. In short, if there is a vehicle or mobile equipment used by the City, Fleet Services will usually be involved.

AUDITS

2007 - The objective of this audit was to provide assurance that Fleet Services was providing economical, efficient, and effective services.

2014 - This audit assessed two aspects of fleet safety: driver training, and driver permit management.

Janine Mryglod, Queena Dong, and Edwin Ryl

LGAQ Fall 2016 | Page 24

AUDITING FLEETS

2015 - The objectives of this audit was to assess the efficiency and effectiveness of fleet maintenance; to determine if the training program for Transit and Municipal Fleet Maintenance staff was adequate and appropriate; and to determine if the procurement process was effective.

RISK/FOCUS AREAS

1. Staff productivity and training

As is the case with most service-based industries, wages tend to be one of the biggest expenses. As such, there is a significant financial risk and opportunity when it comes to fleet staff productivity. Staff training was identified as a risk because it can impact productivity, safety, and compliance with Occupational Health & Safety rules. To address these risks, we tested:

• If employees were doing the jobs that they were supposed to be doing.• If there was a reasonable split between productive and unproductive time

(usually referred to as ‘wrench time’).• If the ratio of buses to transit mechanics was reasonable.• If there were enough buses available to meet transit scheduling demand.• If the hours and topics of staff training were reasonable.• If training records were complete, accurate, timely, and accessible.

2. Operational efficiency/effectiveness

Operational efficiency and effectiveness were key risks because they impact both cost and quality of service. To assess these risks, we analyzed the results of operational performance measures, including:

• Fleet availability - This shows if vehicles and equipment were available to clients when they needed them.

• The amount of planned work versus the amount of unplanned work. Planned work uses staff more efficiently and effectively, and is more economical than unplanned work. This is particularly the case when the work is routine maintenance or non-urgent issues.

• Equipment downtime - This shows if vehicles and equipment were available when needed and determines if Fleet Services is completing repairs in a timely manner.

• Shop rates - to determine if the operational costs for the City’s fleet maintenance program were reasonably comparable to private industry and other public organizations.

As is the case

with most service-

based industries,

wages tend to be

one of the biggest

expenses. As such,

there is a significant

financial risk and

opportunity when it

comes to fleet staff

productivity.

LGAQ Fall 2016 | Page 25

AUDITING FLEETS

We also identified that one of the factors that reduced efficiency was the variety of vehicle manufacturers and models that Fleet Services was required to maintain. Variation means that mechanics and technicians require broader experience and training, and that a much larger inventory of parts is required to complete repairs. Reducing the variety of vehicles and equipment helps make the operations more efficient and reduces maintenance costs.

3. Operational economy and ‘best value’

Throughout the audits, when we assessed risks, we also identified possible opportunities to streamline operations, reduce costs, or increase value. These included:

• Compliance with the vehicle and equipment’s required maintenance schedule. This helps ensure that the asset achieves its full life-cycle. The City has a program where the cost to replace the vehicle is put aside in a reserve over the life-cycle of the vehicle. If the vehicle needs to be replaced before that life-cycle is complete, the funds may not be there to do it.

• Ensuring that the ongoing maintenance requirements are known before purchasing vehicles and equipment. This helps reduce the variation. If vehicles are procured without full understanding of what the maintenance requirements are, it increases the cost and complexity of maintenance.

• Negotiating fuel contracts on behalf of the City as a whole. This is a more economical approach as division of client departments meant that fuel purchases were managed in different ways.

• Tracking and managing vehicle warranty entitlements. Vehicles and equipment often come with warranties. If Fleet Services does not properly track and manage them, then it will incur repair costs rather than the manufacturer or seller.

4. Service, satisfaction, and safety

Much of the work related to fleets is service-oriented. As such, there are risks related to the delivery of service and the satisfaction of clients. We assessed service and satisfaction through a blend of objective and subjective measures, such as:

• Review of Service-Level-Agreement and service delivery targets. They define the expected service levels for the operation. The agreements can provide valid, accepted criteria for assessing the service in relation to the needs and expectations of the clients.

• Review of client satisfaction survey results. They are a good proxy measure for the reputation of the service. They also provide the business with the chance to identify opportunities for changes and continuous improvement.

Much of the work

related to fleets is

service-oriented.

As such, there are

risks related to the

delivery of service

and the satisfaction

of clients.

LGAQ Fall 2016 | Page 26

AUDITING FLEETS

Safety is always a risk. Since the City of Edmonton has an Occupational Health and Safety program which includes a comprehensive safety audit every three years, we focused on risks related to drivers. This includes:

• The effectiveness of the City’s driver permit process. City Driver Permits are issued to employees who operate City vehicles. When the permit process does not operate effectively, there is a risk that unqualified employees are operating City vehicles.

• The effectiveness of a driver safety program. We assessed this by reviewing safety performance measures.

• A review of traffic infractions obtained while operating City vehicles. We used this to identify safety risks for the operation of the fleet.

The majority of municipalities operate a fleet. They may differ in size and strategy, but it is likely that they all still share a set of common risks. We have attempted to provide an overview of the various risks and possible procedures that may apply to many municipal fleets and hope this is a helpful resource.

ABOUT THE AUTHORS

The Office of the City Auditor at the City of Edmonton, Alberta has a staff of 16 and conducts performance audits and investigations, and manages hotline complaints. As the lead auditors on these reports, Queena Dong, Janine Mryglod, and Edwin Ryl collectively hold one or more of CIA, P. Eng., MBA, CRMA, and CPA.

The majority of

municipalities

operate a fleet. They

may differ in size

and strategy, but it

is likely that they all

still share a set of

common risks.

LGAQ Fall 2016 | Page 27

AUDITING FLEETS

KANSAS CITY STREETCAR’S PUBLIC-PRIVATE PARTNERSHIP

More than 50 years after dismantling its citywide system, Kansas City opened a 2 mile starter streetcar line this past spring. The project was a high profile and highly controversial endeavor from the get go. During the entire construction phase, the local media provided daily coverage of every movement and decision made by the city related to the streetcar. At one point a local TV station did a live shot of a power substation being installed under a bridge. Thrilling TV! It was clear everything related to this project was a potential lightning rod. The addition of an audit to the ongoing project added to the overall pressures faced by city staff involved. Did I mention this was my first audit?

BACKGROUND

Kansas City tried to pass a variety of more expansive light rail plans for the past 20 years, but all would fail at the ballot box. The smaller scope of this project utilized the creation of a political subdivision known as a Transportation Development District to successfully secure the approval of a voter pool concentrated around the greater downtown area. To further secure backing for the streetcar from somewhat weary downtown interests, the city agreed to develop a non-profit corporation to assist in the management of the streetcar system. The Kansas City Streetcar Authority is governed by seven privately established directors and only six publicly appointed directors.

To govern this public-private partnership, the city entered into a tri-party agreement with the Transportation District and the Streetcar Authority. The Transportation District essentially became a silent funding mechanism with revenues flowing through the city while the Streetcar Authority took on a much bigger role once the operational phase began.

WHAT WE AUDITED AND WHY

The streetcar system is a city-owned asset with both physical infrastructure and a newly minted fleet of streetcars. Our audit’s objective was to determine whether

Jonathan Lecuyer

LGAQ Fall 2016 | Page 28

AUDITING FLEETS

the tri-party agreement protected the city’s interest in these assets. It was important to make sure the city retained enough control over the project in proportion to the risk it had assumed. We released the audit about nine months prior to the beginning of the streetcar’s operations.

Kansas City’s strategy to include a private non-profit in the governance of the streetcar was, in part, modeled after a similar agreement in Portland that had been in place for nearly 20 years. When we saw an audit released by the Portland Auditor’s Office that had findings and recommendations related to this type of partnership, it caught our attention.1 (If you’d like to know more about their audit, Tenzin Choephel wrote about Portland’s experience in the Spring 2015 Quarterly, I recommend you check it out.) We saw this as an opportunity to identify any potential issues and offer management recommendations to address these issues prior to any actual operation of the streetcar. Auditing for the future!

Public-private partnerships are increasingly becoming a common practice among local and state governments to provide a variety of services and capital projects. It is important to audit these types of agreements to ensure they adequately protect the public’s interest in these assets and programs. These projects exist on a continuum that, depending on their structure, shifts a portion of the control, funding, ownership, risk, and potential revenues towards a private entity. By giving up some control and revenue, a city is often able to undertake projects it could otherwise not afford or politically achieve on its own. It is crucial for an audit of public-private partnership to understand how each project is unique in its agreement, roles, context, structure, and intent. Though Kansas City’s agreement was initially modeled after Portland’s agreement, we quickly found out the actual structures were quite different.

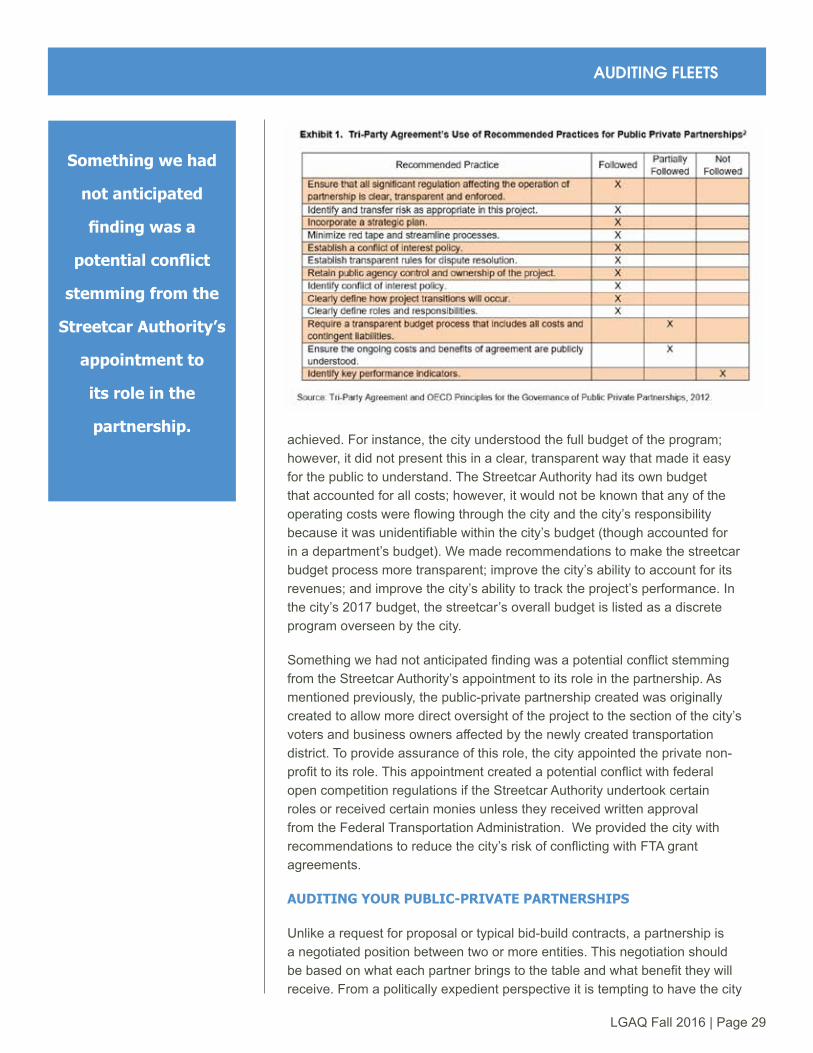

WHAT WE FOUND

Because our audit scope focused on the agreement itself, we created a framework to assess whether the agreement adequately addressed recommended practices for public-private partnerships. We were pleased to find that the agreement addressed a large portion of recommended practices. The three areas we found the agreement to be lacking centered on accountability and transparency during the ongoing operational phase of the streetcar.

Specifically, the agreement did not adequately define a transparent budget process that included all costs and contingent liabilities, it did not ensure that the ongoing costs and benefits of the agreement were publicly understood, and it did not include key performance indicators. As part of our framework outlined in Exhibit 1, we identify some of our audit findings as “partially followed” because while elements of the recommended practice may have been present, the overall intent of the recommended practice was not

Public-private

partnerships

are increasingly

becoming a common

practice among

local and state

governments to

provide a variety of

services and capital

projects.

LGAQ Fall 2016 | Page 29

AUDITING FLEETS

achieved. For instance, the city understood the full budget of the program; however, it did not present this in a clear, transparent way that made it easy for the public to understand. The Streetcar Authority had its own budget that accounted for all costs; however, it would not be known that any of the operating costs were flowing through the city and the city’s responsibility because it was unidentifiable within the city’s budget (though accounted for in a department’s budget). We made recommendations to make the streetcar budget process more transparent; improve the city’s ability to account for its revenues; and improve the city’s ability to track the project’s performance. In the city’s 2017 budget, the streetcar’s overall budget is listed as a discrete program overseen by the city.

Something we had not anticipated finding was a potential conflict stemming from the Streetcar Authority’s appointment to its role in the partnership. As mentioned previously, the public-private partnership created was originally created to allow more direct oversight of the project to the section of the city’s voters and business owners affected by the newly created transportation district. To provide assurance of this role, the city appointed the private non-profit to its role. This appointment created a potential conflict with federal open competition regulations if the Streetcar Authority undertook certain roles or received certain monies unless they received written approval from the Federal Transportation Administration. We provided the city with recommendations to reduce the city’s risk of conflicting with FTA grant agreements.

AUDITING YOUR PUBLIC-PRIVATE PARTNERSHIPS

Unlike a request for proposal or typical bid-build contracts, a partnership is a negotiated position between two or more entities. This negotiation should be based on what each partner brings to the table and what benefit they will receive. From a politically expedient perspective it is tempting to have the city

Something we had

not anticipated

finding was a

potential conflict

stemming from the

Streetcar Authority’s

appointment to

its role in the

partnership.

LGAQ Fall 2016 | Page 30

AUDITING FLEETS

assume financial, compliance, operational or other responsibilities without retaining the appropriate amount of oversight, control, or revenue shares. In order to “just get the project done” it can be easier to worry about the details later. What this can lead to is a situation where a city or other public entity bears the ongoing risks of a project without having the proper oversight and control necessary 15 to 20 years into a project. At that point the problem will likely not only be much bigger, but also more expensive to remedy.

Public-private partnerships present a great opportunity for an audit to ensure the public’s interest has been adequately addressed. These agreements exist on a wide spectrum of possibilities and can therefore be extremely complicated in their structure. Sprinkle in regulatory compliance needs and the details really start to matter. Because each partnership can be so unique, it is critical to identify where exactly on the public-private spectrum the partnership you are auditing lies. This process will allow you to define the roles, responsibilities, assumed risk, and constraints of each partner as well as external factors influencing the partnership that are necessary to know prior to assessing it against the framework you establish.

I think our audit helped the city recognize the ongoing risks and responsibilities it had assumed in the streetcar system’s operation and take necessary steps to mitigate those risks.

To see our full audit report, you can find it at: https://webfusion.kcmo.org/coldfusionapps/auditor/showrecord.cfm?ID=573

ABOUT THE AUTHOR

Jonathan Lecuyer has been an auditor with the city of Kansas City, Missouri since 2015. Prior to joining the office, Jonathan worked in the non-profit housing development field for six years creating housing communities for those in mental health services and managing grant compliance. This work was briefly punctuated by a two-year overseas stint to the Philippines with the US Peace Corps where he focused on program evaluation and development of youth programs. Jonathan completed a Master of Public Administration degree at the University of Kansas City, Missouri where he is also currently a candidate for a Master of Economics degree.

Public-private

partnerships

present a great

opportunity for an

audit to ensure the

public’s interest has

been adequately

addressed.

LGAQ Fall 2016 | Page 31

AUDITING FLEETS

DENVER INTERNATIONAL AIRPORT FLEET MANAGEMENT PROGRAM AUDIT

Denver International Airport (DIA) is one of the busiest airports in the United States and the largest in square miles. Ensuring that personnel can efficiently and safely navigate the property is important. The weather in Colorado can be unpredictable and large snow storms can have a significant impact on travel and safety for personnel as well as customers. Therefore, it is important to have a well maintained and reliable fleet of vehicles to clear snow and keep operations intact.

DIA’s Fleet Maintenance section (Fleet Maintenance) manages the airport’s fleet of more than 1,800 vehicles and units of equipment for all divisions throughout the airport, many of which provide specialized services. The equipment comprises a mix of light duty and heavy duty vehicles, as well as stationary and portable equipment such as generators, portable message signs, and hand-held push mowers. Much of DIA’s fleet is dedicated to snow removal and runway maintenance, including a majority of attachment pieces. The budget for fleet equipment derives from the Airport Enterprise Fund. From 2014 to 2016, DIA’s budget for all capital equipment expenditures was between approximately $4 million and $8 million per year.

PURPOSE OF THE AUDIT

Our audit assessed the effectiveness and efficiency of DIA’s fleet management program. The audit examined DIA’s fleet management practices on both the airside and landside of the facility. Methodologies for the audit included the following:

• Researching various regulations

• Interviewing personnel from various DIA divisions and sections that interface with the fleet management program

Sonia Montano

LGAQ Fall 2016 | Page 32

AUDITING EDUCATION

• Reviewing Fleet Maintenance policies and procedures and Standard Operating Procedures

• Assessing the primary systems used by Fleet Maintenance

• Verifying that fixed assets are properly inventoried and accounted for

• Reviewing data related to controls for take-home vehicles, fuel usage, and preventive maintenance

• Conducting benchmarking of fleet management practices and metrics at other airports

FINDINGS

The key finding of our audit was that DIA Management needed to strengthen oversight of and internal controls over the fleet management program. In July 2012, DIA hired a new Director of Fleet Maintenance, who had started to address a variety of operational issues, specifically concerning oversight and internal control weaknesses, many of which were observed during the course of our audit. The Director had also been granted approval to hire two new analyst positions to assist with management oversight and strengthening the internal control environment. These two positions were charged with improving communication within Fleet Maintenance as well as between Fleet Maintenance and other DIA departments and divisions. Communication is paramount due to the number of other DIA departments and divisions that the fleet affects operationally.

We found two major areas where the fleet management program could improve its operations, both of which the new Director recognized. Following are details about these areas.

INSUFFICIENT MANAGERIAL INVOLVEMENT IN AND CONTROL OVER FLEET ASSETS

Our audit found that Fleet Maintenance did not have sufficient involvement in and control over fleet assets. These issues could have resulted in unnecessary costs, an increased risk of misuse of assets, and unsafe vehicles or equipment. Following were specific areas of concern:

• Noncompliance with some policies governing the take-home vehicle program

• Inadequate oversight and internal controls governing fuel access

• Lack of a formal fleet utilization program

• Fixed assets not being consistently recorded or monitored

• Preventive maintenance not being consistently tracked and monitored

• Damage to fleet vehicles not being reported timely

The key finding of

our audit was that

DIA Management

needed to

strengthen oversight

of and internal

controls over the

fleet management

program.

LGAQ Fall 2016 | Page 33

AUDITING FLEETS

TAKE-HOME VEHICLE PROGRAM

The city authorizes the use of take-home vehicles for employees whose job duties include responding to emergencies or responding to non-scheduled work program service requests that require an emergency vehicle with specialized equipment outside of normal business hours. Examples of these kinds of duties include snow removal, street flooding, power outages, unsafe street conditions, and various public safety emergencies. At the time of the audit, DIA had approximately 50 assigned take-home vehicles for the purpose of responding to these instances. Employees authorized to take a vehicle home generally used the vehicles for personal use commuting to and from work. To compensate the city for this personal use, an employee was charged $1.50 for each trip to and from work, which amounted to approximately $90 per month. However, these employees enjoy the benefits of not having to pay for the costs associated with owning a personal vehicle, including monthly payments, maintenance costs, insurance premiums, and fuel expenses.

In assessing this practice, we determined that requirements surrounding take-home vehicle usage were not being consistently monitored or complied with. The city’s Fiscal Accountability Rule requires that the driver of a take-home vehicle reside within a 25-mile radius of his or her main or regular place of work. Our testing determined that 12 of the 53 individuals (23 percent) with take-home vehicles were identified as residing beyond the maximum 25-mile radius from DIA. The further a driver resides from the airport, the longer it will take to respond to an emergency outside of normal business hours, reducing the effectiveness of the take-home vehicle policy.

We determined that individuals with take-home vehicles who were residing beyond the 25-mile radius requirement were consuming more fuel, which was increasing overall fuel consumption and costs to DIA. Based on our audit work, take-home vehicle users who were residing outside of the 25-mile radius consumed twice as much fuel as those who lived within the 25-mile radius. Thus, non-compliance with the city’s Fiscal Accountability Rule results in additional costs to the city. In addition, another way the take-home vehicle program was not effectively serving its intended purpose was that a majority of the miles logged were for commuting to and from work, not for business use such as responding to emergencies. We determined that DIA Management would be able to reduce its number of authorized take-home vehicles without impacting public safety.

INADEQUATE OVERSIGHT & INTERNAL CONTROLS FOR FUEL ACCESS

In addition to monitoring and maintaining take-home vehicles, Fleet Maintenance also has fiscal responsibility for fuel use at DIA. Fleet Maintenance is responsible for monitoring fuel obtained through DIA’s fuel information system, Fuel Force, which is used to control access at fueling

We determined

that individuals

with take-home

vehicles who were

residing beyond

the 25-mile radius

requirement were

consuming more

fuel, which was

increasing overall

fuel consumption

and costs to DIA.

LGAQ Fall 2016 | Page 34

AUDITING FLEETS

locations throughout the airport. Anticipated budgeted costs related to the delivery, distribution, and review of fuel for 2012 was to exceed $3 million. Audit work identified four areas where fuel use controls were either not operating or were ineffective in design, creating a risk for misuse of fuel. We identified areas of concern related to fuel access activation and deactivation, exception resets, management oversight, and segregation of duties for those responsible for oversight.

MISSED OPPORTUNITIES RELATED TO OPERATING & CAPITAL COSTS

We identified several budget and supplemental funding opportunities that were not being diligently pursued by Fleet Maintenance management, which could help to offset increasing operating expenses. First, Fleet Maintenance was not requesting additional funding for preventive maintenance costs despite a growing fleet. Second, Fleet Maintenance was not fully documenting or taking advantage of possible supplemental funding available through grants. Third, DIA missed opportunities to reduce expenses by not recouping the cost of fuel consumption at DIA by other city agencies and third parties. With these three opportunities in mind, we found that Fleet Maintenance should better capture and communicate the costs associated with maintaining a growing fleet, develop and document processes undertaken to pursue grant funding, and monitor outside agencies and third-party vendors in relation to fuel use and invoice them for consumption.

AUDIT FOLLOW-UP RESULTS

We conducted the follow-up to our audit a few years later and found that DIA had implemented a majority of our audit findings and, as a result, have realized savings and efficiency improvements. Most notably, by re-designating 28 take-home vehicles to assigned vehicles, Fleet Maintenance has saved approximately $38,000 annually on fuel as well as over 345,000 miles of wear and tear on city vehicles. In addition, implementation of an accident/abuse policy now allows Fleet Maintenance to monitor and record vehicles and equipment that need repair from either an accident or abuse in a timely manner.

ABOUT THE AUTHOR

Sonia Montano is an audit supervisor in the Denver Auditor’s Office. She is a Certified Government Auditing Professional and has a Certification in Risk Management Assurance. She has a bachelor’s degree in Accounting and over 20 years of professional experience in the government sector.

LGAQ Fall 2016 | Page 35

AUDITING FLEETS

KING COUNTY TRANSIT AUDITS

WHAT IS THE KING COUNTY TRANSIT AUDIT FUNCTION?

In November 2014, the King County Auditor’s Office established an ongoing audit program focused on King County Metro Transit (Transit). This means that the office is conducting audits of Transit throughout the year.

HOW IS THIS DIFFERENT FROM WHAT THE AUDITOR’S OFFICE DID IN THE PAST?

In the past, our office would conduct audits of Transit, but not on a regular, ongoing basis.

WHY FOCUS ON TRANSIT?

King County Metro Transit is one of the largest transit agencies in the county, serving a population of over 2 million people. It has an annual budget of $700 million, and is one of the most visible services that the county provides. Given its size and services, there is a lot of interest in ensuring that it is operating efficiently and effectively. In addition, with rapid population growth in the region, people are more concerned about gridlock and being able to get to where they need to go. An audit by our office in 2009 found millions in potential savings, and there were issues in 2014 that prompted King County Council and public interest.

LIKE WHAT?

In early 2014, Transit reported a potential budget shortfall and the possibility of cutting services on over 150 routes. In the spring, county voters rejected a proposition that would have increased sales tax and car-tab fees to maintain those transit services, meaning that many routes were slated for substantial cuts. With a majority of urban voters voting for the failed King County proposition, the

Sean DeBlieck

LGAQ Fall 2016 | Page 36

AUDITING FLEETS

City of Seattle decided to put its own proposition to the voters to mitigate the impact of the cuts in the city. However, by early fall, sales tax revenues were more optimistic, showing that most cuts would not have to be made. Nevertheless, Seattle voters went on to vote to pay for transit services, the ‘buspacalypse’ didn’t occur—in fact, service increased with the better-than-expected tax revenue plus the funds from Seattle. As a result, there is renewed interest in looking more closely at the agency.

WHAT KINDS OF TRANSIT AUDITS HAS YOUR OFFICE COMPLETED SO FAR?

Our office did a comprehensive audit of the agency in 2009 where we looked at finances, procurement, capital projects, transit policing, and other areas. Our first item of business in 2015 was reviewing the status of the recommendations that were still listed as ‘in progress.’ We then conducted two new performance audits, one on capital maintenance projects and another on vehicle maintenance. Our current engagements are examining the paratransit program and IT projects. We are also following up on the recommendations we made last year.

WHY THESE PARTICULAR AUDIT TOPICS?