Embed Size (px)

Citation preview

ALFI implementation project

Reporting to investors and annual reports under the AIFMD

ALFI guidance

Issue 1

Luxembourg, 3 October 2014

2 | P a g e

Important

This document was prepared by ALFI's working group for reporting under the Directive on Alternative Investment Fund Managers (AIFMD). The working group comprises representatives of asset managers, management companies, securities service firms, audit firms, law firms, and document and information management firms.

This document represents the view from a group of market participants which may not necessarily be definitive nor suitable for every circumstance. This guidance note has not been validated by any regulator. It does not diminish the management company's or the investment company's responsibility to comply with Directive 2011/61/EU, related delegated or implementing regulations, ESMA’s related guidelines and technical advice papers and any other European or national law or regulation. This document must not be relied upon as advice and is provided without any warranty of any kind and neither ALFI nor its members who contributed to this document accept any liability whatsoever for any action taken in reliance upon it.

This document may be amended without prior notice to incorporate new material and to amend previously published material where the working group considers it appropriate. ALFI will publish amended copies of this document to its members, showing marked-up changes from the immediately preceding copy.

ALFI's members are welcome to submit a question to the working group, which will review it and consider whether to include it in a future copy of this document. Please send your questions to [email protected]. We will acknowledge receipt of each question but we regret that we may be unable to reply individually to each one.

© ALFI 2014

3 | P a g e

Key documents for reporting to investors under AIFMD

Directive 2011/61/EU (“AIFMD”)

Directive 2011/61/EU of the European Parliament and of the Council of 8 June 2011 on Alternative Investment Fund Managers

EU Regulation 231/2013 (“AIFMD-CDR”)

Commission Delegated Regulation (EU) No 231/2013 of 19 December 2012 supplementing Directive 2011/61/EU of the European Parliament and of the Council with regard to exemptions, general operating conditions, depositaries, leverage, transparency and supervision

Luxembourg law of 12 July 2013 (“AIFMD law”)

Luxembourg law of 12 July 2013 on Alternative Investment Fund Managers

Luxembourg law of 17 December 2010 (“UCI law”)

Luxembourg law of 17 December 2010 on Undertaking for collective investments

Luxembourg law of 13 February 2007 (“SIF law”)

Luxembourg law of 13 February 2007 on Specialised Investment Funds

Luxembourg law of 19 December 2002 (“Annual accounts law”)

Luxembourg law on trade register and annual accounts of commercial companies

ESMA/2011/379 (“ESMA technical advice”)

ESMA’s technical advice to the European Commission on possible implementing measures of the Alternative Investment Fund Managers Directive

ESMA/2013/232 and ESMA/2013/201 (“Guidelines on remuneration”)

Guidelines on sound remuneration policies under the AIFMD

4 | P a g e

ESMA/2014/868 (“ESMA Q&A”)

Questions and Answers – Application of AIFMD – Revised on 21 July 2014

CSSF FAQ Document (“CSSF FAQ”)

CSSF Frequently Asked Questions concerning the Luxembourg Law of 12 July 2013 on alternative investment fund managers as well as the Commission Delegated Regulation (EU) No 231/2013 of 19 December 2012 supplementing Directive 2011/61/EU of the European Parliament and of the Council with regard to exemptions, general operating conditions, depositaries, leverage transparency and supervision (version published on 18 July 2014, regularly updated)

5 | P a g e

AIFMD: Reporting to investors

1. Scope and general consideration

Scope of this document The purpose of this document is to provide guidance in preparation of Luxembourg annual report of regulated AIFs (mainly UCI Part II and SIFs) under the AIFMD. As many configurations exist, we have focused on the particular case of a Luxembourg AIFM managing Luxembourg AIFs (Part II and SIFs). For non-regulated Luxembourg AIFs, references to Luxembourg law will have to be adapted in order to take into consideration requirements applicable to commercial companies in Luxembourg (Luxembourg law of 19 December 2002). For Luxembourg AIFs managed by an AIFM established in another Member State (“MS”), the AIFM will also have to consider whether specific requirements derive from the other MS’s transposition law or regulations. Specific cases of non-EU AIFMs and non-EU AIFs have not been specifically addressed in this paper. Practitioners are encouraged to refer to the CSSF’s FAQ document for further guidance in this regard. This document also focuses on the annual report to investors pursuant to article 20 of the AIFMD law as well as the periodic disclosure to investors (article 21 para. 4 and article 21 para. 5). It does not address the information to be included in the prospectus or offering documents (article 21 para. 1 to 3) nor the reporting to the regulator (article 22) that is specifically addressed in a separate ALFI document.

Accounting framework This document has been prepared on the basis of the two most common accounting frameworks used in Luxembourg: Luxembourg GAAP and IFRS. This does not preclude the use of other accounting frameworks, such as US GAAP, in particular in the context of foreign AIFs managed or marketed by Luxembourg AIFMs.

Responsibility for the preparation of the annual report Whilst article 20 imposes to the AIFM the responsibility to make available an annual report as well as periodic disclosures to investors in accordance with the AIFMD, the preparation of the annual report in line with applicable laws, regulations and the respective accounting framework remains with those in charge of the AIF governance, who might not be the AIFM, i.e. the Board of Directors of an AIF incorporated under a company form or the management company of an FCP. Determining relevant responsibilities in case an annual report is not made available to investors or is not compliant with AIFMD will depend on each AIF structure and is not addressed in this paper.

6 | P a g e

Make available to investors versus publication As developed in this paper, the AIFMD requires certain information to be made available to investors. For instance the Directive requires that the annual report that is made available to investors includes remuneration disclosure as well as material changes to offering information. Such information might not be currently required by the existing Luxembourg laws on annual accounts. The working group believes that, as developed further in the document, that such information shall not necessarily be included in the published annual accounts (as publication is required for Luxembourg AIFs incorporated in the form of companies) provided that the AIFM ensures that such information is being made available to existing investors and, where relevant in accordance with article 21 para. 1 of the AIFMD law, to prospective investors as well as to regulators. Therefore, we believe that including such information in the annual report by reference to a source of information available to investors meets such requirement. Both the AIF’s rules and the annual report shall indicate that such information is made available to investors as well as where to obtain such additional information.

Periodic disclosure to investors Information such as arrangements for managing liquidity of the AIF, leverage employed, risk profile and risk management system shall be periodically disclosed to investors and at least as the same time as the annual report is made available. This implies that the AIF may opt to include such information in tis annual report or to send a separate periodic statement to its investors.

Material and materiality concepts In the context of the annual report and disclosure to investors, the AIFMD refers several time to the concept of material and materiality. Materiality shall be assessed under the requirements of the accounting framework adopted (article 104 para. 5 of the AIFMD-CDR). As this concept of materiality shall be applied in the context of investor disclosure, it might differ from the concept of materiality applied to NAV errors (as the end objective might differ). It might be recommended that each AIF defines its principles to determine materiality in the context of the annual report, taking into consideration the AIF’s specificities (investment policy, open or closed-end,…). The AIFMD-CDR provides a specific definition of materiality in the context of material changes to information provided to investors upon investments (the AIF’s rules, articles, prospectus, offering documents). Article 106 defines material changes as “if there is a substantial likelihood that a reasonable investor, becoming aware of such information, would reconsider its investment in the AIF, including because such information could impact an investor’s ability to exercise its rights in relation to its investment, or otherwise prejudice the interests of one or more investors in the AIF.”

7 | P a g e

We therefore recommend that each AIF defines a specific materiality (or the principles to assess such materiality) for each of the three following purposes (as this could lead to a different tolerance level): -1- preparation of the annual report and related disclosure (materiality could differ depending on the nature of the information: asset class, Profit/Loss or disclosure), -2- material changes to the offering information, -3- NAV calculation error.

8 | P a g e

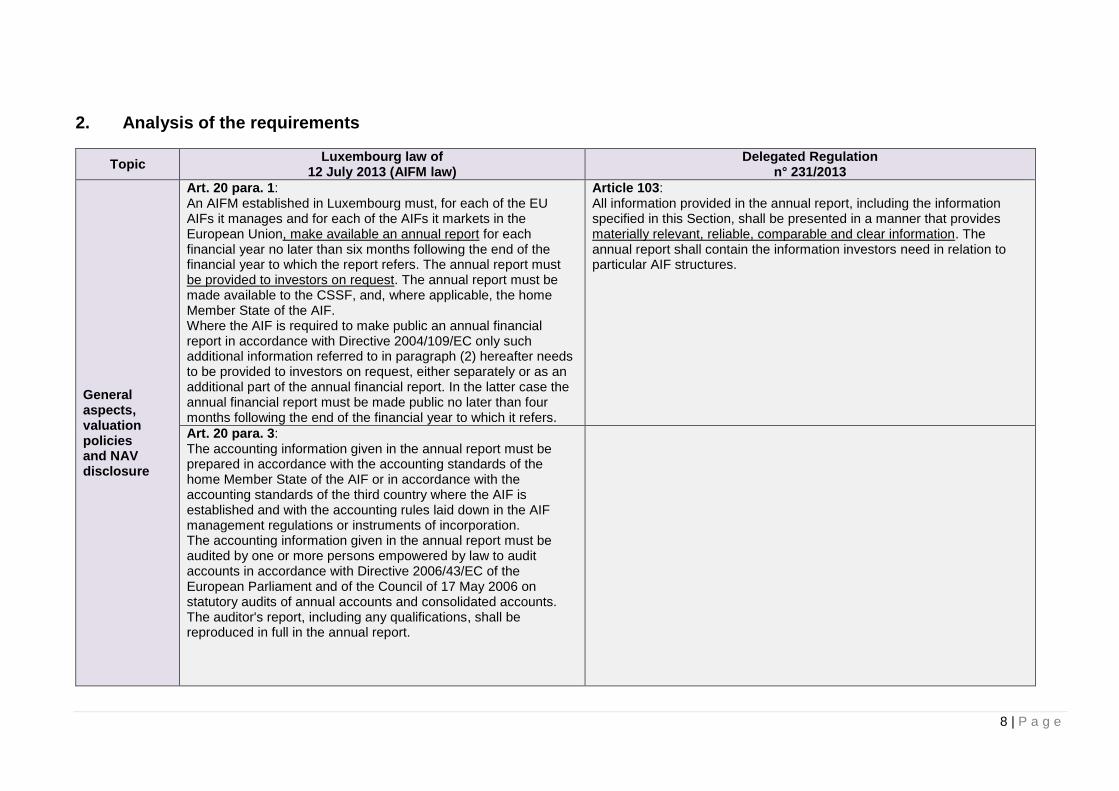

2. Analysis of the requirements

Topic Luxembourg law of

12 July 2013 (AIFM law) Delegated Regulation

n° 231/2013

General aspects, valuation policies and NAV disclosure

Art. 20 para. 1: An AIFM established in Luxembourg must, for each of the EU AIFs it manages and for each of the AIFs it markets in the European Union, make available an annual report for each financial year no later than six months following the end of the financial year to which the report refers. The annual report must be provided to investors on request. The annual report must be made available to the CSSF, and, where applicable, the home Member State of the AIF. Where the AIF is required to make public an annual financial report in accordance with Directive 2004/109/EC only such additional information referred to in paragraph (2) hereafter needs to be provided to investors on request, either separately or as an additional part of the annual financial report. In the latter case the annual financial report must be made public no later than four months following the end of the financial year to which it refers.

Article 103: All information provided in the annual report, including the information specified in this Section, shall be presented in a manner that provides materially relevant, reliable, comparable and clear information. The annual report shall contain the information investors need in relation to particular AIF structures.

Art. 20 para. 3: The accounting information given in the annual report must be prepared in accordance with the accounting standards of the home Member State of the AIF or in accordance with the accounting standards of the third country where the AIF is established and with the accounting rules laid down in the AIF management regulations or instruments of incorporation. The accounting information given in the annual report must be audited by one or more persons empowered by law to audit accounts in accordance with Directive 2006/43/EC of the European Parliament and of the Council of 17 May 2006 on statutory audits of annual accounts and consolidated accounts. The auditor's report, including any qualifications, shall be reproduced in full in the annual report.

9 | P a g e

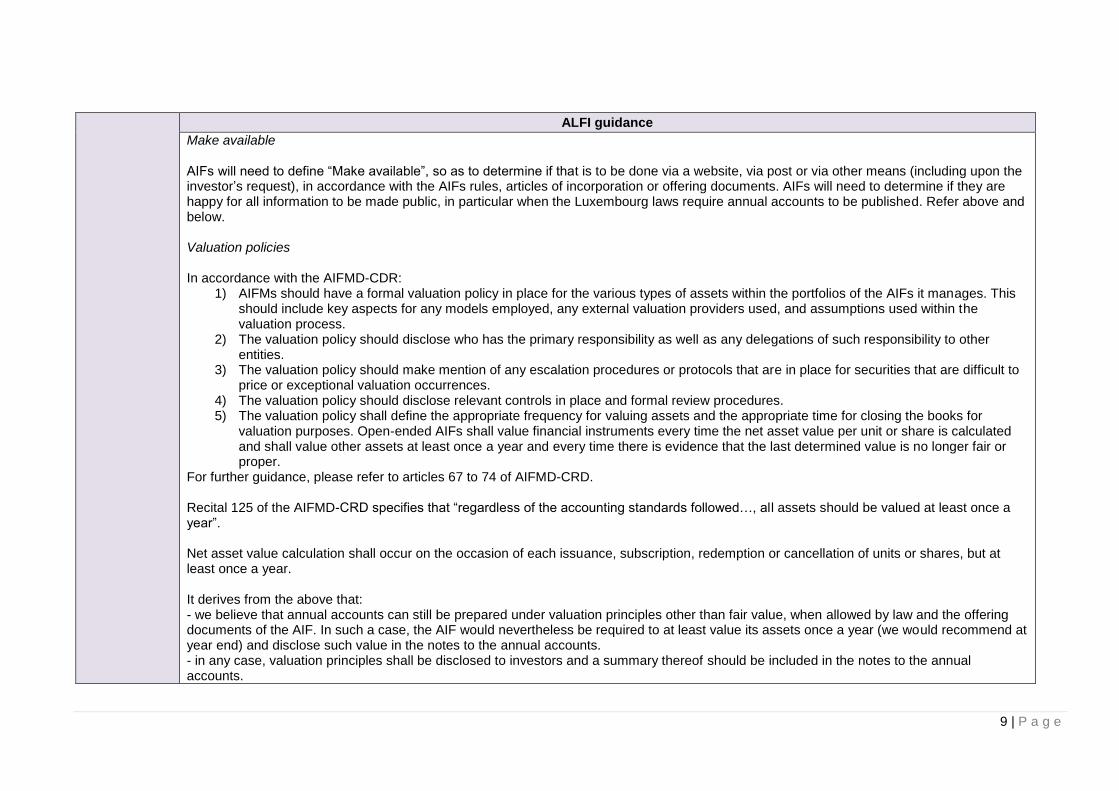

ALFI guidance

Make available AIFs will need to define “Make available”, so as to determine if that is to be done via a website, via post or via other means (including upon the investor’s request), in accordance with the AIFs rules, articles of incorporation or offering documents. AIFs will need to determine if they are happy for all information to be made public, in particular when the Luxembourg laws require annual accounts to be published. Refer above and below. Valuation policies

In accordance with the AIFMD-CDR:

1) AIFMs should have a formal valuation policy in place for the various types of assets within the portfolios of the AIFs it manages. This should include key aspects for any models employed, any external valuation providers used, and assumptions used within the valuation process.

2) The valuation policy should disclose who has the primary responsibility as well as any delegations of such responsibility to other entities.

3) The valuation policy should make mention of any escalation procedures or protocols that are in place for securities that are difficult to price or exceptional valuation occurrences.

4) The valuation policy should disclose relevant controls in place and formal review procedures. 5) The valuation policy shall define the appropriate frequency for valuing assets and the appropriate time for closing the books for

valuation purposes. Open-ended AIFs shall value financial instruments every time the net asset value per unit or share is calculated and shall value other assets at least once a year and every time there is evidence that the last determined value is no longer fair or proper.

For further guidance, please refer to articles 67 to 74 of AIFMD-CRD.

Recital 125 of the AIFMD-CRD specifies that “regardless of the accounting standards followed…, all assets should be valued at least once a year”.

Net asset value calculation shall occur on the occasion of each issuance, subscription, redemption or cancellation of units or shares, but at least once a year. It derives from the above that: - we believe that annual accounts can still be prepared under valuation principles other than fair value, when allowed by law and the offering documents of the AIF. In such a case, the AIF would nevertheless be required to at least value its assets once a year (we would recommend at year end) and disclose such value in the notes to the annual accounts. - in any case, valuation principles shall be disclosed to investors and a summary thereof should be included in the notes to the annual accounts.

10 | P a g e

Balance sheet and profit and loss

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

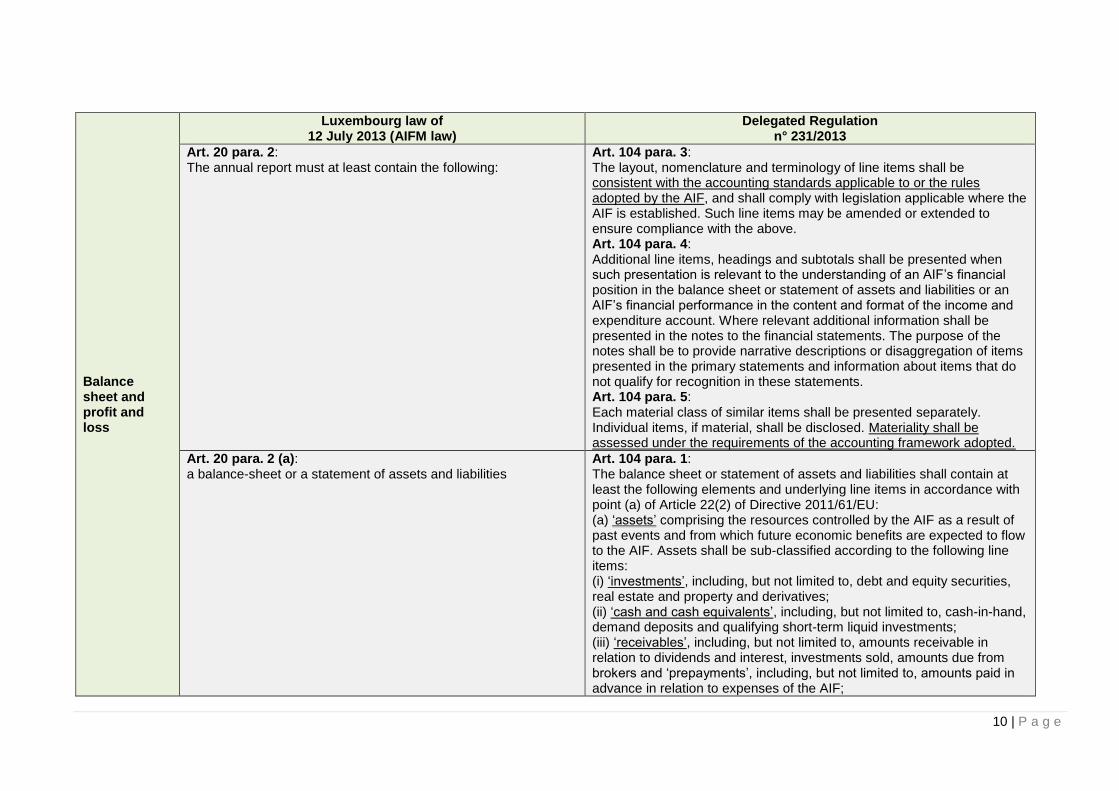

Art. 20 para. 2: The annual report must at least contain the following:

Art. 104 para. 3: The layout, nomenclature and terminology of line items shall be consistent with the accounting standards applicable to or the rules adopted by the AIF, and shall comply with legislation applicable where the AIF is established. Such line items may be amended or extended to ensure compliance with the above. Art. 104 para. 4: Additional line items, headings and subtotals shall be presented when such presentation is relevant to the understanding of an AIF’s financial position in the balance sheet or statement of assets and liabilities or an AIF’s financial performance in the content and format of the income and expenditure account. Where relevant additional information shall be presented in the notes to the financial statements. The purpose of the notes shall be to provide narrative descriptions or disaggregation of items presented in the primary statements and information about items that do not qualify for recognition in these statements. Art. 104 para. 5: Each material class of similar items shall be presented separately. Individual items, if material, shall be disclosed. Materiality shall be assessed under the requirements of the accounting framework adopted.

Art. 20 para. 2 (a): a balance-sheet or a statement of assets and liabilities

Art. 104 para. 1: The balance sheet or statement of assets and liabilities shall contain at least the following elements and underlying line items in accordance with point (a) of Article 22(2) of Directive 2011/61/EU: (a) ‘assets’ comprising the resources controlled by the AIF as a result of past events and from which future economic benefits are expected to flow to the AIF. Assets shall be sub-classified according to the following line items: (i) ‘investments’, including, but not limited to, debt and equity securities, real estate and property and derivatives; (ii) ‘cash and cash equivalents’, including, but not limited to, cash-in-hand, demand deposits and qualifying short-term liquid investments; (iii) ‘receivables’, including, but not limited to, amounts receivable in relation to dividends and interest, investments sold, amounts due from brokers and ‘prepayments’, including, but not limited to, amounts paid in advance in relation to expenses of the AIF;

11 | P a g e

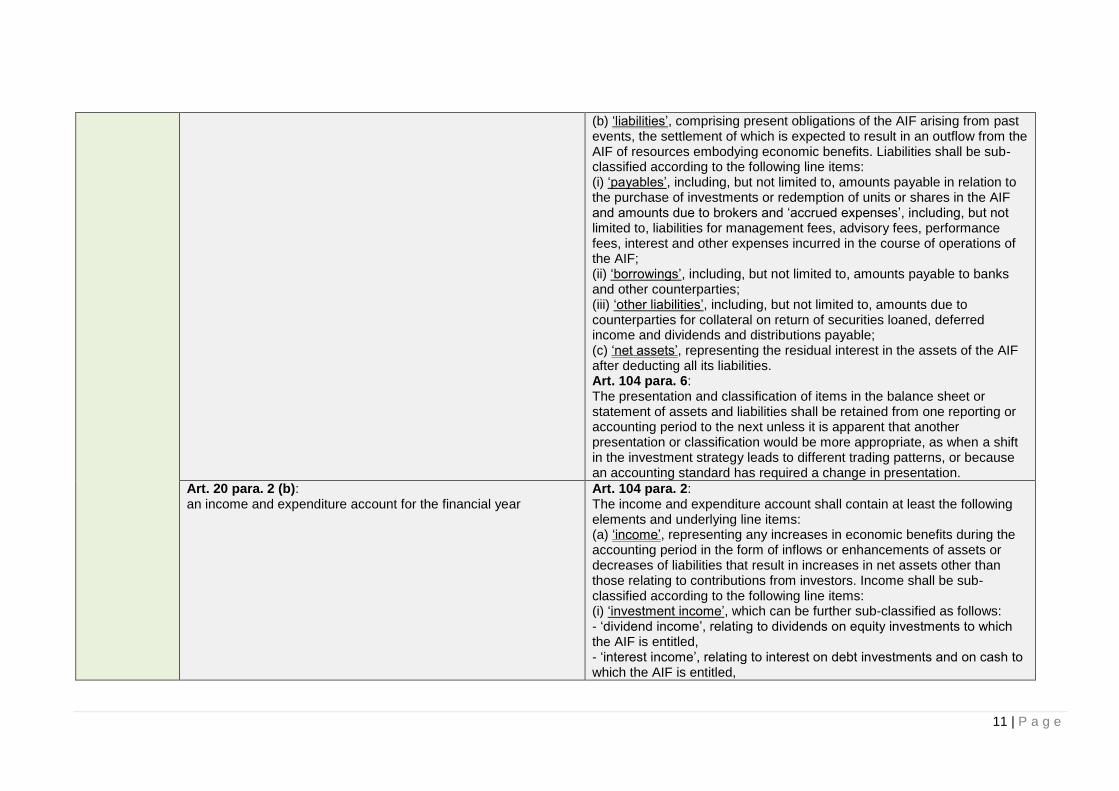

(b) ‘liabilities’, comprising present obligations of the AIF arising from past events, the settlement of which is expected to result in an outflow from the AIF of resources embodying economic benefits. Liabilities shall be sub-classified according to the following line items: (i) ‘payables’, including, but not limited to, amounts payable in relation to the purchase of investments or redemption of units or shares in the AIF and amounts due to brokers and ‘accrued expenses’, including, but not limited to, liabilities for management fees, advisory fees, performance fees, interest and other expenses incurred in the course of operations of the AIF; (ii) ‘borrowings’, including, but not limited to, amounts payable to banks and other counterparties; (iii) ‘other liabilities’, including, but not limited to, amounts due to counterparties for collateral on return of securities loaned, deferred income and dividends and distributions payable; (c) ‘net assets’, representing the residual interest in the assets of the AIF after deducting all its liabilities. Art. 104 para. 6: The presentation and classification of items in the balance sheet or statement of assets and liabilities shall be retained from one reporting or accounting period to the next unless it is apparent that another presentation or classification would be more appropriate, as when a shift in the investment strategy leads to different trading patterns, or because an accounting standard has required a change in presentation.

Art. 20 para. 2 (b): an income and expenditure account for the financial year

Art. 104 para. 2: The income and expenditure account shall contain at least the following elements and underlying line items: (a) ‘income’, representing any increases in economic benefits during the accounting period in the form of inflows or enhancements of assets or decreases of liabilities that result in increases in net assets other than those relating to contributions from investors. Income shall be sub-classified according to the following line items: (i) ‘investment income’, which can be further sub-classified as follows: - ‘dividend income’, relating to dividends on equity investments to which the AIF is entitled, - ‘interest income’, relating to interest on debt investments and on cash to which the AIF is entitled,

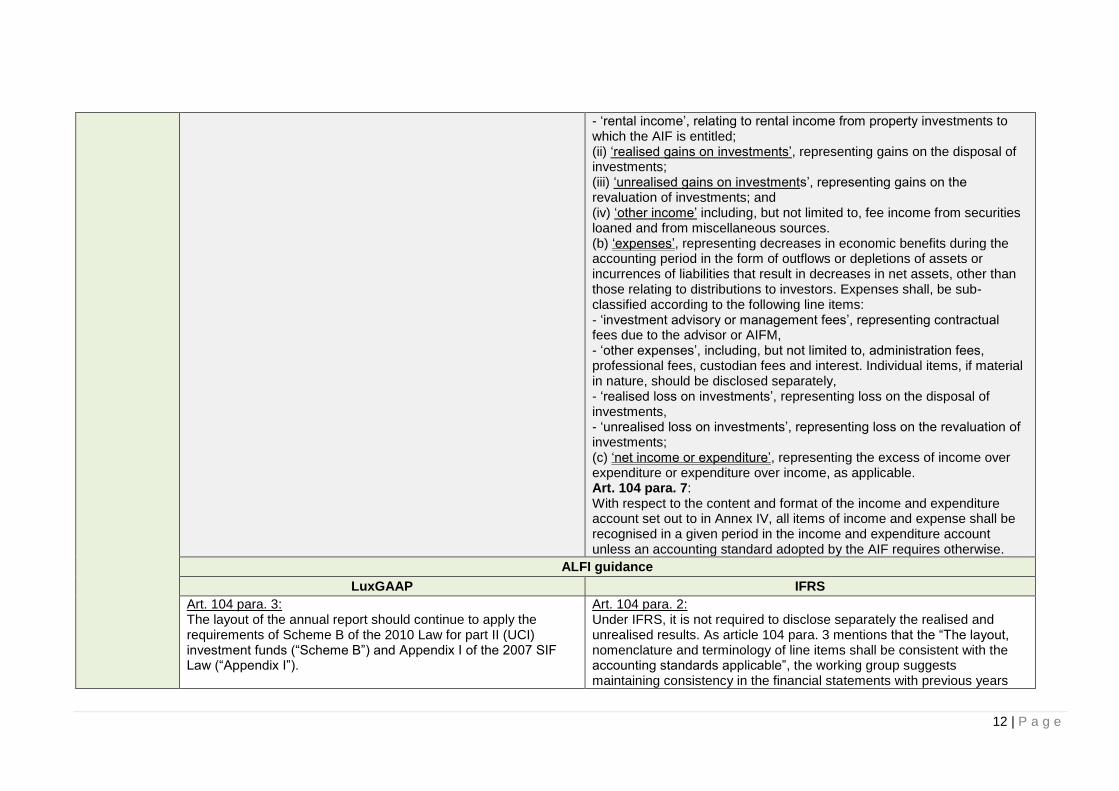

12 | P a g e

- ‘rental income’, relating to rental income from property investments to which the AIF is entitled; (ii) ‘realised gains on investments’, representing gains on the disposal of investments; (iii) ‘unrealised gains on investments’, representing gains on the revaluation of investments; and (iv) ‘other income’ including, but not limited to, fee income from securities loaned and from miscellaneous sources. (b) ‘expenses’, representing decreases in economic benefits during the accounting period in the form of outflows or depletions of assets or incurrences of liabilities that result in decreases in net assets, other than those relating to distributions to investors. Expenses shall, be sub-classified according to the following line items: - ‘investment advisory or management fees’, representing contractual fees due to the advisor or AIFM, - ‘other expenses’, including, but not limited to, administration fees, professional fees, custodian fees and interest. Individual items, if material in nature, should be disclosed separately, - ‘realised loss on investments’, representing loss on the disposal of investments, - ‘unrealised loss on investments’, representing loss on the revaluation of investments; (c) ‘net income or expenditure’, representing the excess of income over expenditure or expenditure over income, as applicable. Art. 104 para. 7: With respect to the content and format of the income and expenditure account set out to in Annex IV, all items of income and expense shall be recognised in a given period in the income and expenditure account unless an accounting standard adopted by the AIF requires otherwise.

ALFI guidance

LuxGAAP IFRS

Art. 104 para. 3: The layout of the annual report should continue to apply the requirements of Scheme B of the 2010 Law for part II (UCI) investment funds (“Scheme B”) and Appendix I of the 2007 SIF Law (“Appendix I”).

Art. 104 para. 2: Under IFRS, it is not required to disclose separately the realised and unrealised results. As article 104 para. 3 mentions that the “The layout, nomenclature and terminology of line items shall be consistent with the accounting standards applicable”, the working group suggests maintaining consistency in the financial statements with previous years

13 | P a g e

Financial statements under Lux GAAP do not require figures comparable to the balance sheet and profit and loss accounts. The AIFMD does not provide any change in this regard. Art. 104 para. 5: Depending on the materiality threshold chosen (see above), AIFs will need to determine whether items should be presented separately or combined with other similar items, in accordance with the accounting framework adopted. Art. 104 para. 1: The minimum disclosure of balance sheets or statements of assets and liabilities does not deviate from Scheme B of the UCI law and of Appendix I of the SIF law, but it is nevertheless more specific as regards terminology and breakdown. It should be adapted and detailed according to the accounting principles and the investor’s needs. Whilst no significant changes are expected in the presentation of the statement of net assets, AIFs will need to assess whether their current presentation will result in a re-classification of items which complies with the descriptions of these headings as per AIFMD. Accounting policies adopted should be applied consistently from one period to the next unless a different presentation is considered more appropriate. Art. 104 para. 2: Same comment as Art. 104 para.1. “Other expenses”, if material, shall be disclosed separately in the income and expenditure account. However, AIFs should consider consistency with disclosure of the previous year. Additionally, where previous accounting policy choices or material judgments have been influenced by the fact that other expenses were shown at an aggregated level, such assessments may need to be revisited. AIFs may also elect to present such information in the notes to the annual accounts. Please also note that AIFs established under Part II of the UCI law are now required to disclose separately “transaction costs” (amendment to Schedule B of Annex I of UCI law). Transaction

and adding details in a separate note in order to disclose the breakout of the four separate captions: - income – realised gain - income – unrealised gain - expense – realised loss - expense – unrealised loss

14 | P a g e

costs, as defined in question 16 of CSSF FAQ, include all the costs incurred by a UCI in connection with transactions on its portfolio, including those charged by the custodian bank for the execution of the UCI’s transactions and can be disclosed either under a specific heading “transaction costs” of the profit and loss account or in the notes to the accounts.

15 | P a g e

Report of activities

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

Art. 20 para. 2 (c): a report on the activities of the financial year

Art. 105 para. 1: The report on activities of the financial year shall include at least: (a) an overview of investment activities during the year or period, and an overview of the AIF’s portfolio at year-end or period end; (b) an overview of AIF performance over the year or period; (c) material changes as defined below in the information listed in Article 23 of Directive 2011/61/EU not already present in the financial statements. Art. 105 para. 2: The report shall include a fair and balanced review of the activities and performance of the AIF, containing also a description of the principal risks and investment or economic uncertainties that the AIF might face. Art. 105 para. 3: To the extent necessary for an understanding of the AIF’s investment activities or its performance, the analysis shall include both financial and non-financial key performance indicators relevant to that AIF. The information provided in the report shall be consistent with national rules where the AIF is established. Art. 105 para. 4: The information in the report on the activities of the financial year shall form part of the directors or investment managers report in so far as this is usually presented alongside the financial statements of the AIF.

ALFI guidance

LuxGAAP IFRS

Activities, risks and uncertainties disclosure It shall be noted that recital 126 of the AIFMD-CDR foresees that “the report shall include a fair and balanced review of the activities of the AIF with a description of the principal risks and investments or economic uncertainties that it faces. That disclosure shall not result in the publication of proprietary information of the AIF that would be to the detriment of the AIF and its investors. Therefore, if the publication of a particular proprietary information would have such effect, it could be aggregated to a level that would avoid the detrimental effect and would not need to capture, for example, the performance or statistics of an individual portfolio company or investment that could lead to the disclosure of proprietary information of the AIF.”

16 | P a g e

Performance disclosure Each AIF shall determine the most appropriate way to disclose its performance, for instance depending on its investment policy. It shall be a combination of quantitative and qualitative criteria. We recommend to explain the methodology chosen and to apply it consistently from one period to another. Regarding comments on the performance of the AIF, in addition to any commentary traditionally made in the managers/directors report regarding the performance of the AIF, additional financial and non-financial key performance indicators (“KPIs”, in real estate, this may include commentary on capital expenditure items, impact of regulatory and oversight changes on operations and structuring, vacancy/rollover risk due to market conditions) should be disclosed in order to enable any current or future investors to accurately assess the constitution and performance, and future issues of the portfolio/investment. As many of these items will be qualitative in nature, they will be in the managers’ report/commentary as opposed to the audited financial statements of the annual report. In the case of real estate funds, the INREV disclosures will already meet substantially these disclosure requirements. Many items will be further highlighted by the new risk management disclosure requirements, particularly concerning the remediation/mitigation to risk exposure items. This will give current and prospective investors more insight to the issues and how it is planned to deal with them. We would suggest that, depending on the type of assets under management, these details could be disclosed to investors as a separate document outside the audited annual report, particularly if the corporate form of the AIF requires the publication of annual accounts in the trade register, in order to avoid that commercially sensitive or portfolio specific items are disclosed to the public.

17 | P a g e

Luxembourg law of

12 July 2013 (AIFM law) Delegated Regulation

n° 231/2013

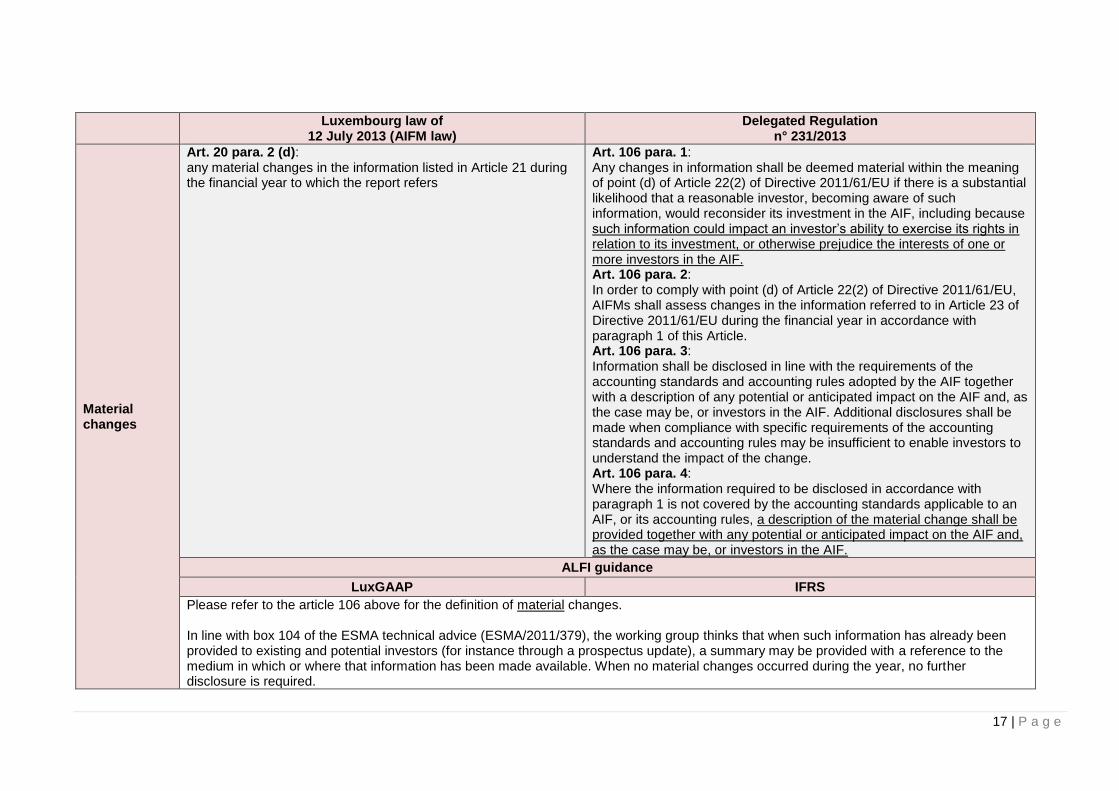

Material changes

Art. 20 para. 2 (d): any material changes in the information listed in Article 21 during the financial year to which the report refers

Art. 106 para. 1: Any changes in information shall be deemed material within the meaning of point (d) of Article 22(2) of Directive 2011/61/EU if there is a substantial likelihood that a reasonable investor, becoming aware of such information, would reconsider its investment in the AIF, including because such information could impact an investor’s ability to exercise its rights in relation to its investment, or otherwise prejudice the interests of one or more investors in the AIF. Art. 106 para. 2: In order to comply with point (d) of Article 22(2) of Directive 2011/61/EU, AIFMs shall assess changes in the information referred to in Article 23 of Directive 2011/61/EU during the financial year in accordance with paragraph 1 of this Article. Art. 106 para. 3: Information shall be disclosed in line with the requirements of the accounting standards and accounting rules adopted by the AIF together with a description of any potential or anticipated impact on the AIF and, as the case may be, or investors in the AIF. Additional disclosures shall be made when compliance with specific requirements of the accounting standards and accounting rules may be insufficient to enable investors to understand the impact of the change. Art. 106 para. 4: Where the information required to be disclosed in accordance with paragraph 1 is not covered by the accounting standards applicable to an AIF, or its accounting rules, a description of the material change shall be provided together with any potential or anticipated impact on the AIF and, as the case may be, or investors in the AIF.

ALFI guidance

LuxGAAP IFRS

Please refer to the article 106 above for the definition of material changes. In line with box 104 of the ESMA technical advice (ESMA/2011/379), the working group thinks that when such information has already been provided to existing and potential investors (for instance through a prospectus update), a summary may be provided with a reference to the medium in which or where that information has been made available. When no material changes occurred during the year, no further disclosure is required.

18 | P a g e

Remuneration

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

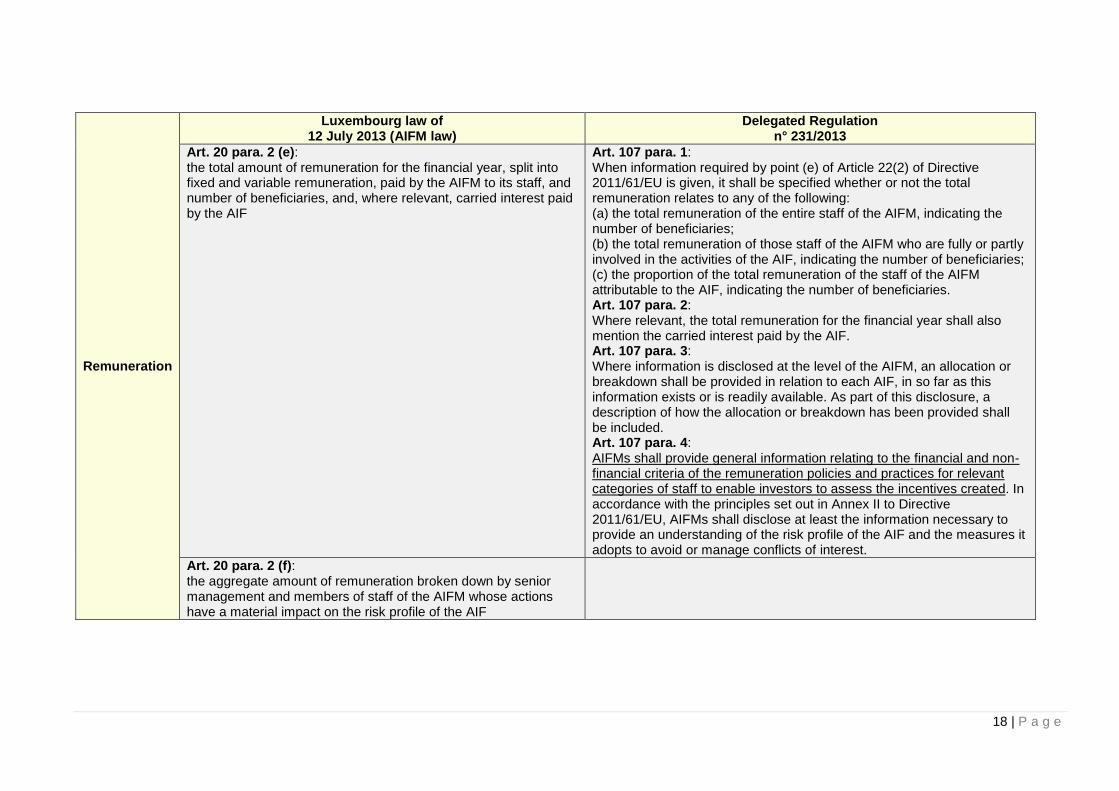

Art. 20 para. 2 (e): the total amount of remuneration for the financial year, split into fixed and variable remuneration, paid by the AIFM to its staff, and number of beneficiaries, and, where relevant, carried interest paid by the AIF

Art. 107 para. 1: When information required by point (e) of Article 22(2) of Directive 2011/61/EU is given, it shall be specified whether or not the total remuneration relates to any of the following: (a) the total remuneration of the entire staff of the AIFM, indicating the number of beneficiaries; (b) the total remuneration of those staff of the AIFM who are fully or partly involved in the activities of the AIF, indicating the number of beneficiaries; (c) the proportion of the total remuneration of the staff of the AIFM attributable to the AIF, indicating the number of beneficiaries. Art. 107 para. 2: Where relevant, the total remuneration for the financial year shall also mention the carried interest paid by the AIF. Art. 107 para. 3: Where information is disclosed at the level of the AIFM, an allocation or breakdown shall be provided in relation to each AIF, in so far as this information exists or is readily available. As part of this disclosure, a description of how the allocation or breakdown has been provided shall be included. Art. 107 para. 4: AIFMs shall provide general information relating to the financial and non-financial criteria of the remuneration policies and practices for relevant categories of staff to enable investors to assess the incentives created. In accordance with the principles set out in Annex II to Directive 2011/61/EU, AIFMs shall disclose at least the information necessary to provide an understanding of the risk profile of the AIF and the measures it adopts to avoid or manage conflicts of interest.

Art. 20 para. 2 (f): the aggregate amount of remuneration broken down by senior management and members of staff of the AIFM whose actions have a material impact on the risk profile of the AIF

19 | P a g e

ALFI guidance

LuxGAAP IFRS

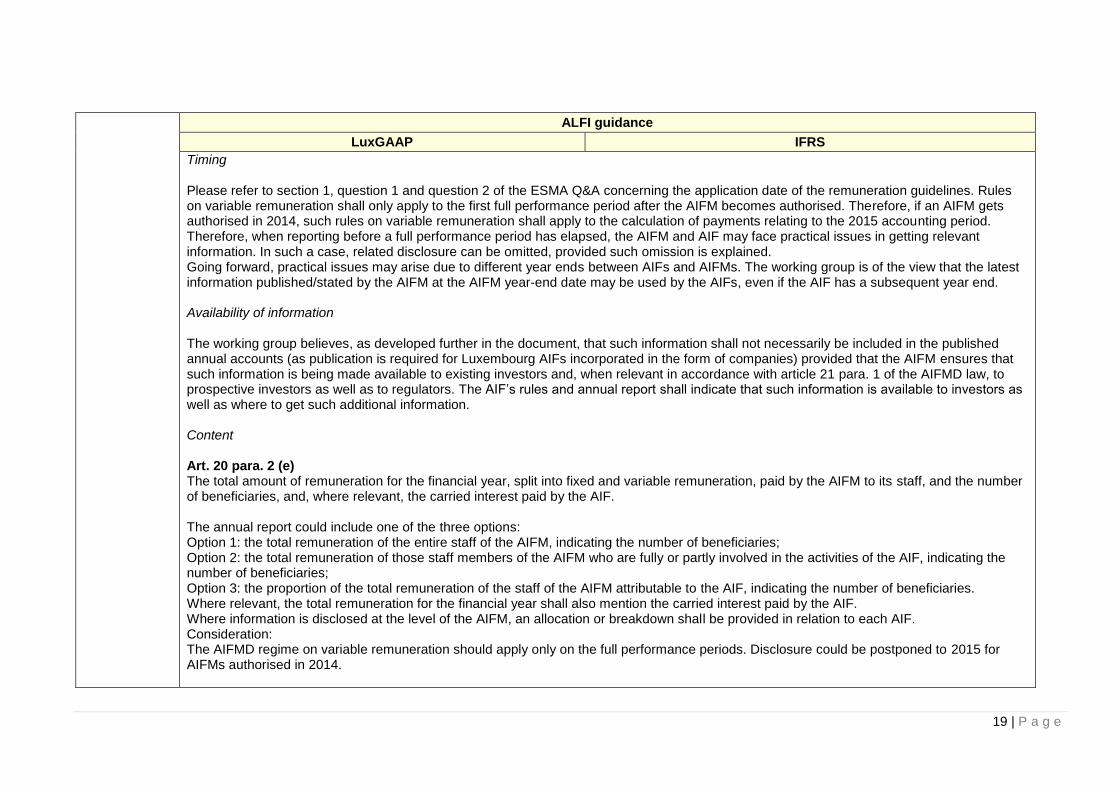

Timing Please refer to section 1, question 1 and question 2 of the ESMA Q&A concerning the application date of the remuneration guidelines. Rules on variable remuneration shall only apply to the first full performance period after the AIFM becomes authorised. Therefore, if an AIFM gets authorised in 2014, such rules on variable remuneration shall apply to the calculation of payments relating to the 2015 accounting period. Therefore, when reporting before a full performance period has elapsed, the AIFM and AIF may face practical issues in getting relevant information. In such a case, related disclosure can be omitted, provided such omission is explained. Going forward, practical issues may arise due to different year ends between AIFs and AIFMs. The working group is of the view that the latest information published/stated by the AIFM at the AIFM year-end date may be used by the AIFs, even if the AIF has a subsequent year end. Availability of information The working group believes, as developed further in the document, that such information shall not necessarily be included in the published annual accounts (as publication is required for Luxembourg AIFs incorporated in the form of companies) provided that the AIFM ensures that such information is being made available to existing investors and, when relevant in accordance with article 21 para. 1 of the AIFMD law, to prospective investors as well as to regulators. The AIF’s rules and annual report shall indicate that such information is available to investors as well as where to get such additional information. Content Art. 20 para. 2 (e) The total amount of remuneration for the financial year, split into fixed and variable remuneration, paid by the AIFM to its staff, and the number of beneficiaries, and, where relevant, the carried interest paid by the AIF. The annual report could include one of the three options: Option 1: the total remuneration of the entire staff of the AIFM, indicating the number of beneficiaries; Option 2: the total remuneration of those staff members of the AIFM who are fully or partly involved in the activities of the AIF, indicating the number of beneficiaries; Option 3: the proportion of the total remuneration of the staff of the AIFM attributable to the AIF, indicating the number of beneficiaries. Where relevant, the total remuneration for the financial year shall also mention the carried interest paid by the AIF. Where information is disclosed at the level of the AIFM, an allocation or breakdown shall be provided in relation to each AIF. Consideration: The AIFMD regime on variable remuneration should apply only on the full performance periods. Disclosure could be postponed to 2015 for AIFMs authorised in 2014.

20 | P a g e

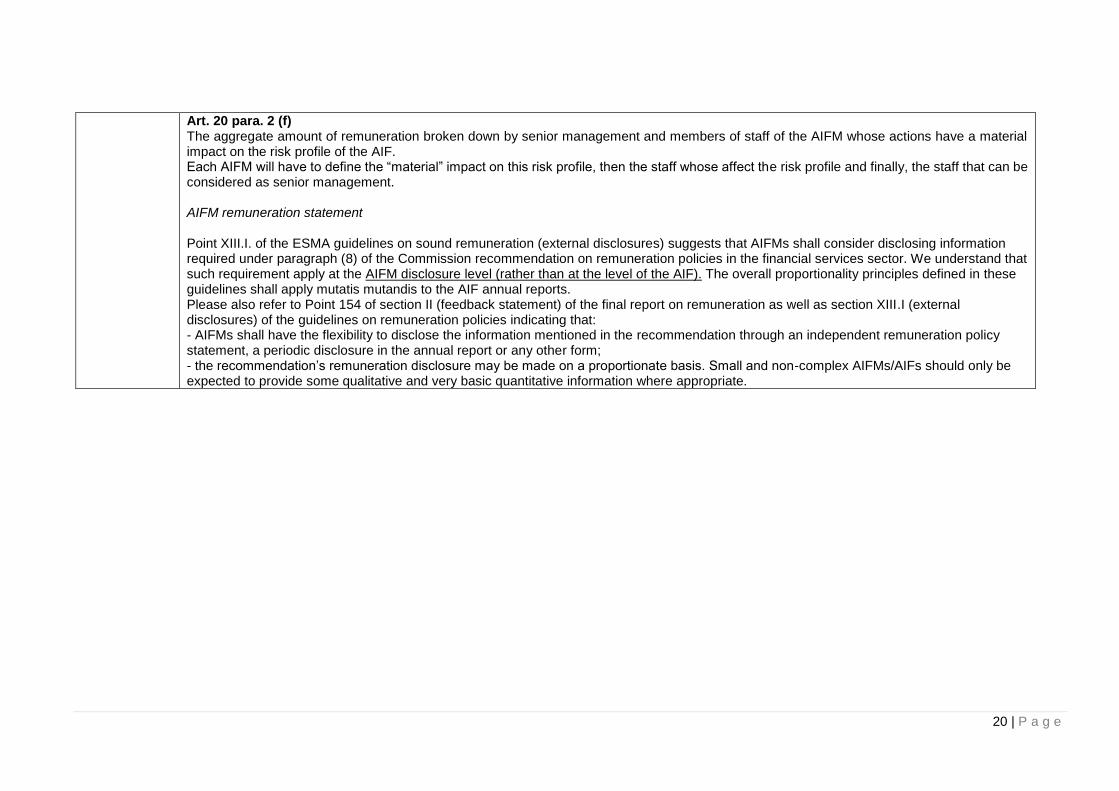

Art. 20 para. 2 (f) The aggregate amount of remuneration broken down by senior management and members of staff of the AIFM whose actions have a material impact on the risk profile of the AIF. Each AIFM will have to define the “material” impact on this risk profile, then the staff whose affect the risk profile and finally, the staff that can be considered as senior management. AIFM remuneration statement Point XIII.I. of the ESMA guidelines on sound remuneration (external disclosures) suggests that AIFMs shall consider disclosing information required under paragraph (8) of the Commission recommendation on remuneration policies in the financial services sector. We understand that such requirement apply at the AIFM disclosure level (rather than at the level of the AIF). The overall proportionality principles defined in these guidelines shall apply mutatis mutandis to the AIF annual reports. Please also refer to Point 154 of section II (feedback statement) of the final report on remuneration as well as section XIII.I (external disclosures) of the guidelines on remuneration policies indicating that: - AIFMs shall have the flexibility to disclose the information mentioned in the recommendation through an independent remuneration policy statement, a periodic disclosure in the annual report or any other form; - the recommendation’s remuneration disclosure may be made on a proportionate basis. Small and non-complex AIFMs/AIFs should only be expected to provide some qualitative and very basic quantitative information where appropriate.

21 | P a g e

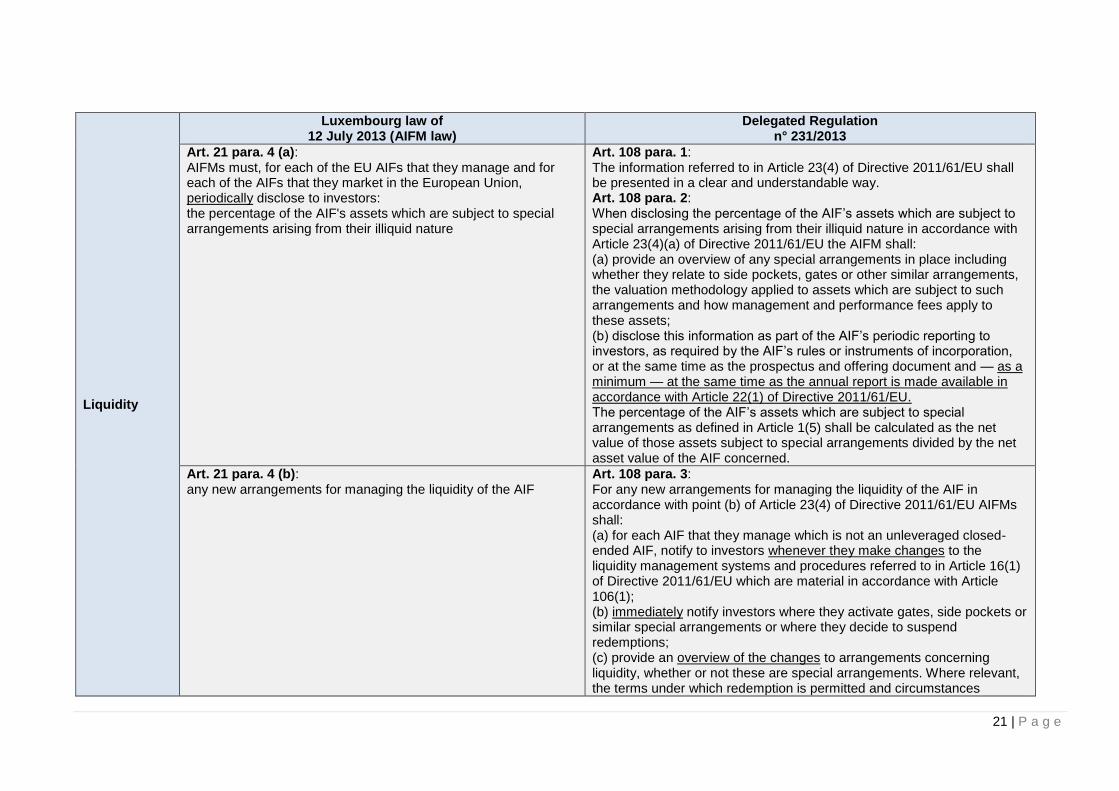

Liquidity

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

Art. 21 para. 4 (a): AIFMs must, for each of the EU AIFs that they manage and for each of the AIFs that they market in the European Union, periodically disclose to investors: the percentage of the AIF's assets which are subject to special arrangements arising from their illiquid nature

Art. 108 para. 1: The information referred to in Article 23(4) of Directive 2011/61/EU shall be presented in a clear and understandable way. Art. 108 para. 2: When disclosing the percentage of the AIF’s assets which are subject to special arrangements arising from their illiquid nature in accordance with Article 23(4)(a) of Directive 2011/61/EU the AIFM shall: (a) provide an overview of any special arrangements in place including whether they relate to side pockets, gates or other similar arrangements, the valuation methodology applied to assets which are subject to such arrangements and how management and performance fees apply to these assets; (b) disclose this information as part of the AIF’s periodic reporting to investors, as required by the AIF’s rules or instruments of incorporation, or at the same time as the prospectus and offering document and — as a minimum — at the same time as the annual report is made available in accordance with Article 22(1) of Directive 2011/61/EU. The percentage of the AIF’s assets which are subject to special arrangements as defined in Article 1(5) shall be calculated as the net value of those assets subject to special arrangements divided by the net asset value of the AIF concerned.

Art. 21 para. 4 (b): any new arrangements for managing the liquidity of the AIF

Art. 108 para. 3: For any new arrangements for managing the liquidity of the AIF in accordance with point (b) of Article 23(4) of Directive 2011/61/EU AIFMs shall: (a) for each AIF that they manage which is not an unleveraged closed-ended AIF, notify to investors whenever they make changes to the liquidity management systems and procedures referred to in Article 16(1) of Directive 2011/61/EU which are material in accordance with Article 106(1); (b) immediately notify investors where they activate gates, side pockets or similar special arrangements or where they decide to suspend redemptions; (c) provide an overview of the changes to arrangements concerning liquidity, whether or not these are special arrangements. Where relevant, the terms under which redemption is permitted and circumstances

22 | P a g e

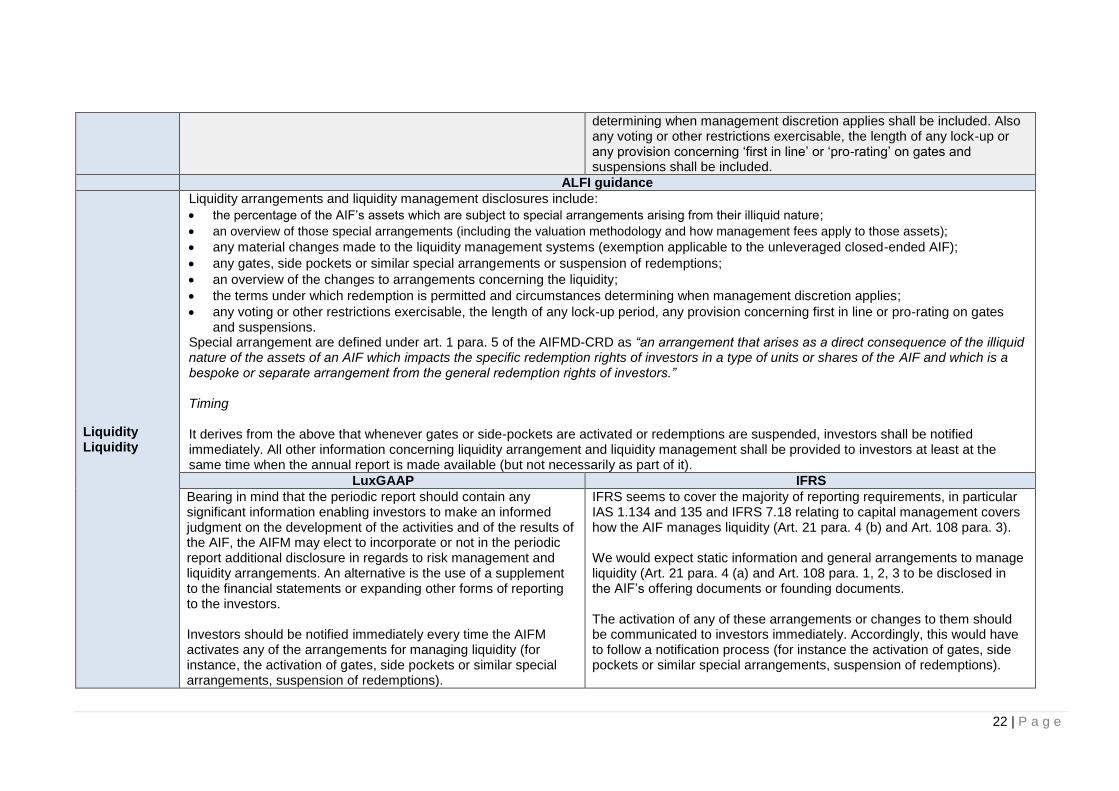

determining when management discretion applies shall be included. Also any voting or other restrictions exercisable, the length of any lock-up or any provision concerning ‘first in line’ or ‘pro-rating’ on gates and suspensions shall be included.

ALFI guidance

Liquidity Liquidity

Liquidity arrangements and liquidity management disclosures include:

the percentage of the AIF’s assets which are subject to special arrangements arising from their illiquid nature;

an overview of those special arrangements (including the valuation methodology and how management fees apply to those assets);

any material changes made to the liquidity management systems (exemption applicable to the unleveraged closed-ended AIF);

any gates, side pockets or similar special arrangements or suspension of redemptions;

an overview of the changes to arrangements concerning the liquidity;

the terms under which redemption is permitted and circumstances determining when management discretion applies;

any voting or other restrictions exercisable, the length of any lock-up period, any provision concerning first in line or pro-rating on gates and suspensions.

Special arrangement are defined under art. 1 para. 5 of the AIFMD-CRD as “an arrangement that arises as a direct consequence of the illiquid nature of the assets of an AIF which impacts the specific redemption rights of investors in a type of units or shares of the AIF and which is a bespoke or separate arrangement from the general redemption rights of investors.” Timing It derives from the above that whenever gates or side-pockets are activated or redemptions are suspended, investors shall be notified immediately. All other information concerning liquidity arrangement and liquidity management shall be provided to investors at least at the same time when the annual report is made available (but not necessarily as part of it).

LuxGAAP IFRS

Bearing in mind that the periodic report should contain any significant information enabling investors to make an informed judgment on the development of the activities and of the results of the AIF, the AIFM may elect to incorporate or not in the periodic report additional disclosure in regards to risk management and liquidity arrangements. An alternative is the use of a supplement to the financial statements or expanding other forms of reporting to the investors. Investors should be notified immediately every time the AIFM activates any of the arrangements for managing liquidity (for instance, the activation of gates, side pockets or similar special arrangements, suspension of redemptions).

IFRS seems to cover the majority of reporting requirements, in particular IAS 1.134 and 135 and IFRS 7.18 relating to capital management covers how the AIF manages liquidity (Art. 21 para. 4 (b) and Art. 108 para. 3). We would expect static information and general arrangements to manage liquidity (Art. 21 para. 4 (a) and Art. 108 para. 1, 2, 3 to be disclosed in the AIF’s offering documents or founding documents. The activation of any of these arrangements or changes to them should be communicated to investors immediately. Accordingly, this would have to follow a notification process (for instance the activation of gates, side pockets or similar special arrangements, suspension of redemptions).

23 | P a g e

If the changes to these arrangements are material to investors, they would have to be disclosed as well in the periodic report.

If the changes to these arrangements are material to investors they would have to be disclosed as well in the periodic report.

24 | P a g e

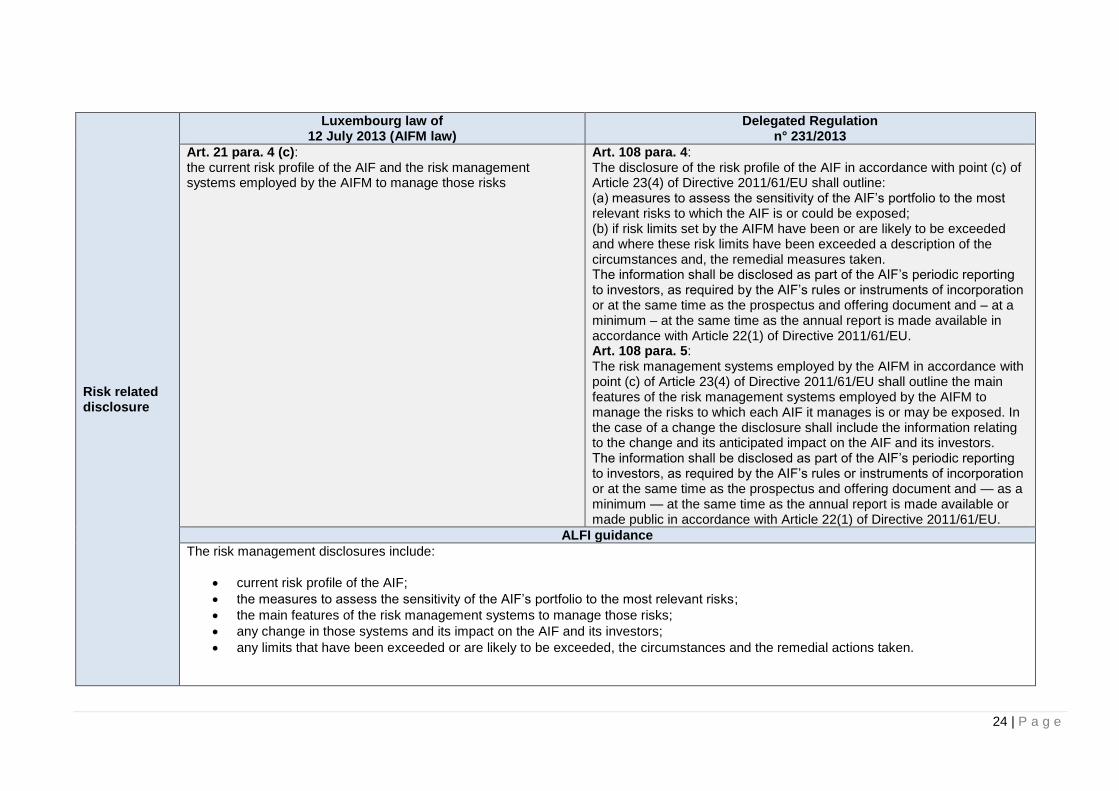

Risk related disclosure

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

Art. 21 para. 4 (c): the current risk profile of the AIF and the risk management systems employed by the AIFM to manage those risks

Art. 108 para. 4: The disclosure of the risk profile of the AIF in accordance with point (c) of Article 23(4) of Directive 2011/61/EU shall outline: (a) measures to assess the sensitivity of the AIF’s portfolio to the most relevant risks to which the AIF is or could be exposed; (b) if risk limits set by the AIFM have been or are likely to be exceeded and where these risk limits have been exceeded a description of the circumstances and, the remedial measures taken. The information shall be disclosed as part of the AIF’s periodic reporting to investors, as required by the AIF’s rules or instruments of incorporation or at the same time as the prospectus and offering document and – at a minimum – at the same time as the annual report is made available in accordance with Article 22(1) of Directive 2011/61/EU. Art. 108 para. 5: The risk management systems employed by the AIFM in accordance with point (c) of Article 23(4) of Directive 2011/61/EU shall outline the main features of the risk management systems employed by the AIFM to manage the risks to which each AIF it manages is or may be exposed. In the case of a change the disclosure shall include the information relating to the change and its anticipated impact on the AIF and its investors. The information shall be disclosed as part of the AIF’s periodic reporting to investors, as required by the AIF’s rules or instruments of incorporation or at the same time as the prospectus and offering document and — as a minimum — at the same time as the annual report is made available or made public in accordance with Article 22(1) of Directive 2011/61/EU.

ALFI guidance

The risk management disclosures include:

current risk profile of the AIF;

the measures to assess the sensitivity of the AIF’s portfolio to the most relevant risks;

the main features of the risk management systems to manage those risks;

any change in those systems and its impact on the AIF and its investors;

any limits that have been exceeded or are likely to be exceeded, the circumstances and the remedial actions taken.

25 | P a g e

Proposal for disclosure of risks that have been breached in the reporting period or are likely to be breached

Based upon the requirements of the AIFMD and the Delegated Regulations, the working group understands that only those breaches of limits have to be disclosed to investors where the limits are explicitly mentioned in binding documents which have been sent to the investor, or where breaches of these limits would lead to non-compliance with the fund’s strategy, asset universe as disclosed to investors, or any national rule applicable to the relevant fund. Internal soft regulations, triggers, which should mainly lead to internal discussions for clarification or improved analysis or risk management procedures or temporary limitations, which reflect the current market view of the investment committee or similar specifications, may be touched or even exceeded without disclosing them to the investor. Options for placing risk and liquidity reporting requirements

1. Integration in the financial statements; 2. Integration in a supplement or additional document to the financial statements; 3. Separate periodic reporting statement.

The supplement or additional document may comprise a risk summary, which includes all AIFMD risk related information and any other information deliberately given to the investor, regardless of whether they are already included somewhere else in the financial statements, and knowing that the annual report should already contain any significant information enabling investors to make an informed judgment about the development of activities and of the results of the AIF. Indeed, the AIFMD-CDR does not require information to be included in the annual report but to be made available to investors at the same time as the annual accounts.

LuxGAAP IFRS

Bearing in mind that the periodic report should contain any significant information enabling investors to make an informed judgment about the development of activities and of the results of the AIF, the AIFM may elect to incorporate or not in the periodic report additional disclosure in regards to risk management. An alternative is the use of a supplement to the financial statements or expanding other forms of reporting to investors.

IFRS seems to cover the majority of the reporting requirements, in particular:

IAS 1.134 and 135 and IFRS 7.18 related to capital management covers how the AIF manages liquidity (art. 21 para. 4 (b) and art. 108 para. 3);

IFRS 7 requires the AIF to disclose its financial risk management objectives and policies (art. 21 para. 4 (c) and art. 108 para. 5);

IFRS 13 requires a split of assets by fair value hierarchy, disclosures on the measurement of assets based on different risk profiles, sensitivity analysis on asset values to changes in unobservable inputs (art. 21 para. 4 (c) and art. 108 para.4);

26 | P a g e

collaterals and guarantees must as well be disclosed in the IFRS financial statement.

Being IFRS principle based, the additional information to be disclosed would depend on the extent of the disclosures already included in the financial statements of the AIF, nevertheless we would expect the following to be added:

changes to the maximum level of leverage calculated by the gross and commitment method, and current level of leverage and extended disclosures in relation to the nature of the rights granted for the reuse of collateral; the nature of guarantees granted; and details of changes in any service providers which relate to these items (art.21 para. 5 and art. 109 para. 2, 3); changes to the maximum level of leverage would as well require a change in the offering documents of the AIF (prior consent of investors);

whether the fund breached any restriction in the period, reasons thereto and mitigating actions taken (art. 108 para. 4);

any changes to the risk management systems in the period and its anticipated impact on the AIF and its investors (which we would expect to be any).

27 | P a g e

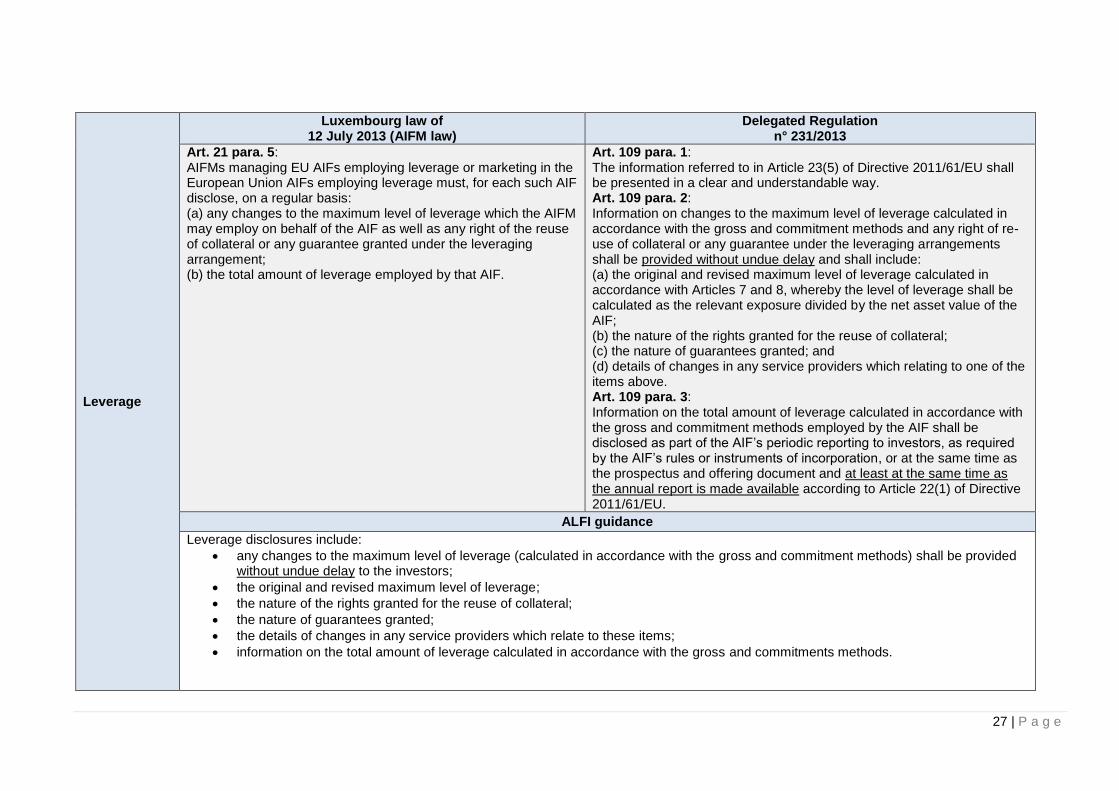

Leverage

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

Art. 21 para. 5: AIFMs managing EU AIFs employing leverage or marketing in the European Union AIFs employing leverage must, for each such AIF disclose, on a regular basis: (a) any changes to the maximum level of leverage which the AIFM may employ on behalf of the AIF as well as any right of the reuse of collateral or any guarantee granted under the leveraging arrangement; (b) the total amount of leverage employed by that AIF.

Art. 109 para. 1: The information referred to in Article 23(5) of Directive 2011/61/EU shall be presented in a clear and understandable way. Art. 109 para. 2: Information on changes to the maximum level of leverage calculated in accordance with the gross and commitment methods and any right of re-use of collateral or any guarantee under the leveraging arrangements shall be provided without undue delay and shall include: (a) the original and revised maximum level of leverage calculated in accordance with Articles 7 and 8, whereby the level of leverage shall be calculated as the relevant exposure divided by the net asset value of the AIF; (b) the nature of the rights granted for the reuse of collateral; (c) the nature of guarantees granted; and (d) details of changes in any service providers which relating to one of the items above. Art. 109 para. 3: Information on the total amount of leverage calculated in accordance with the gross and commitment methods employed by the AIF shall be disclosed as part of the AIF’s periodic reporting to investors, as required by the AIF’s rules or instruments of incorporation, or at the same time as the prospectus and offering document and at least at the same time as the annual report is made available according to Article 22(1) of Directive 2011/61/EU.

ALFI guidance

Leverage disclosures include:

any changes to the maximum level of leverage (calculated in accordance with the gross and commitment methods) shall be provided without undue delay to the investors;

the original and revised maximum level of leverage;

the nature of the rights granted for the reuse of collateral;

the nature of guarantees granted;

the details of changes in any service providers which relate to these items;

information on the total amount of leverage calculated in accordance with the gross and commitments methods.

28 | P a g e

Timing It derives from what is mentioned above that whenever changes occur to the maximum level of leverage, investors shall be notified without undue delay. All the other information concerning the total amount of leverage shall be provided to investors at least at the same time when the annual report is made available (but not necessarily as part of it). Format It derives from what is mentioned above that AIFs may elect to incorporate such information either in their annual report, as a supplement to it or in a separate periodic disclosure document provided to investors at the same time as the annual report.

29 | P a g e

Private Equity disclosure

Luxembourg law of 12 July 2013 (AIFM law)

Delegated Regulation n° 231/2013

Art. 27 para. 1: When an AIF acquires, individually or jointly, control of a non-listed company pursuant to Article 24(1), in conjunction with paragraph (5) of that Article, the AIFM managing such an AIF must either: (a) request and use its best efforts to ensure that the annual report of the non-listed company drawn up in accordance with paragraph (2) is made available by the board of directors of the company to the employees' representatives or, where there are none, to the employees themselves within the period such annual report has to be drawn up in accordance with the national applicable law; or (b) for each such AIF include in the annual report provided for in Article 20 the information referred to in paragraph (2) relating to the relevant non-listed company. Art. 27 para. 2: The additional information to be included in the annual report of the company or the AIF, in accordance with paragraph (1), must include at least a fair review of the development of the company's business representing the situation at the end of the period covered by the annual report. The report must also give an indication of: (a) any important events that have occurred since the end of the financial year; (b) the company's likely future development; and (c) the information concerning acquisitions of own shares prescribed by Article 22(2) of Council Directive 77/91/EEC. Art. 27 para. 3: The AIFM managing the relevant AIF must either: a) request and use its best efforts to ensure that the board of directors of the non-listed company makes available the information referred to in point (b) of paragraph (1) relating to the company concerned to the employees' representatives of the company concerned or, where there are none, to the employees themselves within the period referred to in Article 20(1); or

30 | P a g e

b) make available the information referred to in point (a) of paragraph (1) to the investors of the AIF, in so far as already available, within the period referred to in Article 20(1) and, in any event, no later than the date on which the annual report of the non-listed company is drawn up in accordance with the national applicable law.

ALFI guidance

LuxGAAP IFRS

Purpose of art. 27 on specific provisions regarding the annual report of AIFs exercising control of non-listed companies The main purpose is to ensure information that would typically be part of a MD&A (“Management Discussion and Analysis”), inter alia:

fair review of the development of the company’s business representing the situation at the end of the period covered by the annual report;

any important events that have occurred since the end of the financial year;

the company’s likely future development; and

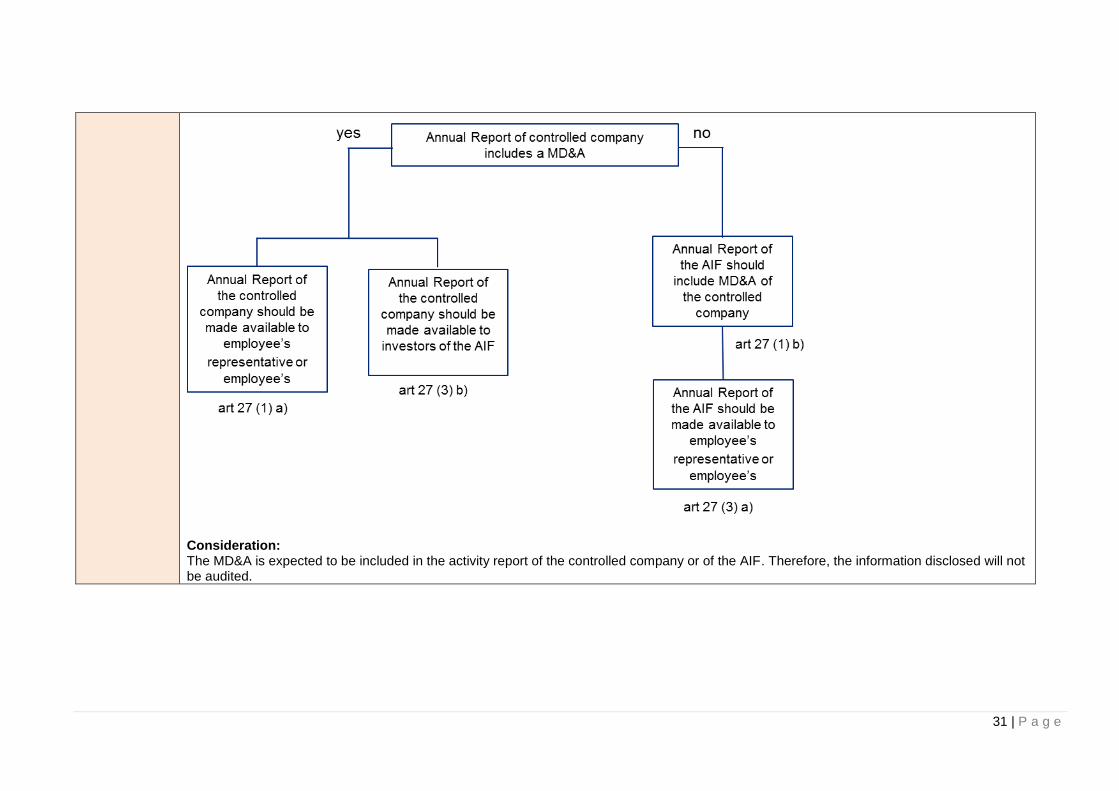

information concerning acquisitions of own shares prescribed by art. 22 para. 2 of Council Directive 77/91/EEC. This information should be available to the employees’ representative or the employees of the controlled company themselves, and to the investors of the AIF. Where should the MD&A of the controlled company be disclosed? See table on the next page.

31 | P a g e

Consideration: The MD&A is expected to be included in the activity report of the controlled company or of the AIF. Therefore, the information disclosed will not be audited.