Embed Size (px)

Citation preview

CORPORATE PRESENTATION MARCH 2015

CORPORATE PRESENTATION

CORPORATE PRESENTATION MARCH 2015

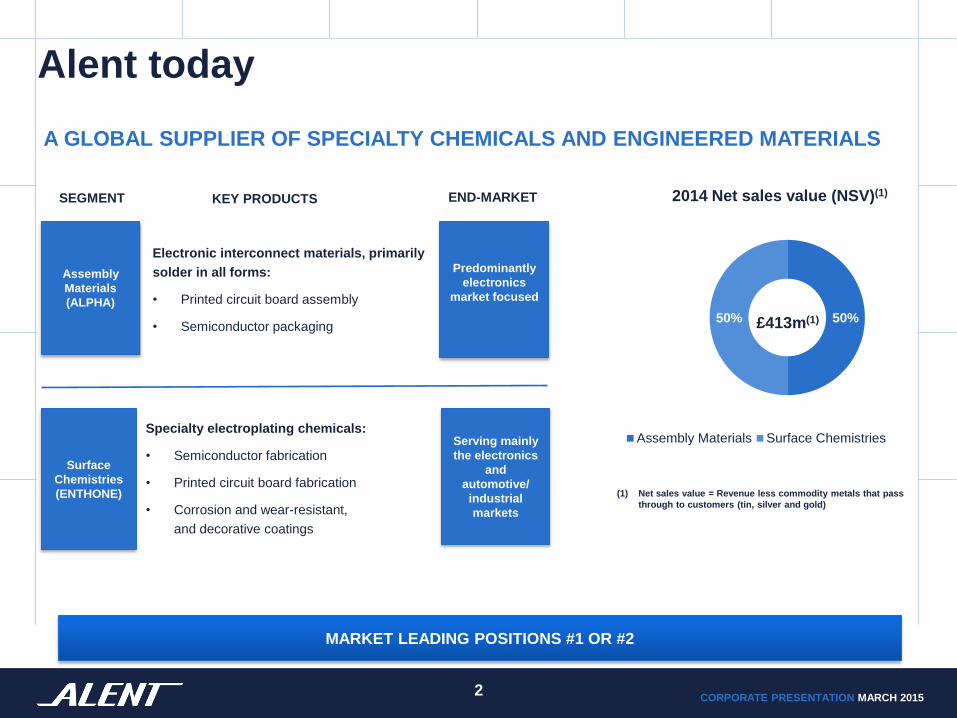

Alent today

Assembly

Materials

(ALPHA)

SEGMENT KEY PRODUCTS

Electronic interconnect materials, primarily

solder in all forms:

• Printed circuit board assembly

• Semiconductor packaging

Surface

Chemistries

(ENTHONE)

Specialty electroplating chemicals:

• Semiconductor fabrication

• Printed circuit board fabrication

• Corrosion and wear-resistant,

and decorative coatings

Serving mainly

the electronics

and

automotive/

industrial

markets

£413m(1)

2014 Net sales value (NSV)(1)

50% 50%

Assembly Materials Surface Chemistries

Predominantly

electronics

market focused

(1) Net sales value = Revenue less commodity metals that pass

through to customers (tin, silver and gold)

MARKET LEADING POSITIONS #1 OR #2

END-MARKET

2

A GLOBAL SUPPLIER OF SPECIALTY CHEMICALS AND ENGINEERED MATERIALS

CORPORATE PRESENTATION MARCH 2015

Alent products

Solder paste

Bar Solder

EVERYTHING WITH AN ON/OFF SWITCH – EVERY DAY, EVERYWHERE

3

Chemistry

Wire Solder

Copper Damascene Preforms

ASSEMBLY MATERIALS SURFACE CHEMISTRIES

CORPORATE PRESENTATION MARCH 2015

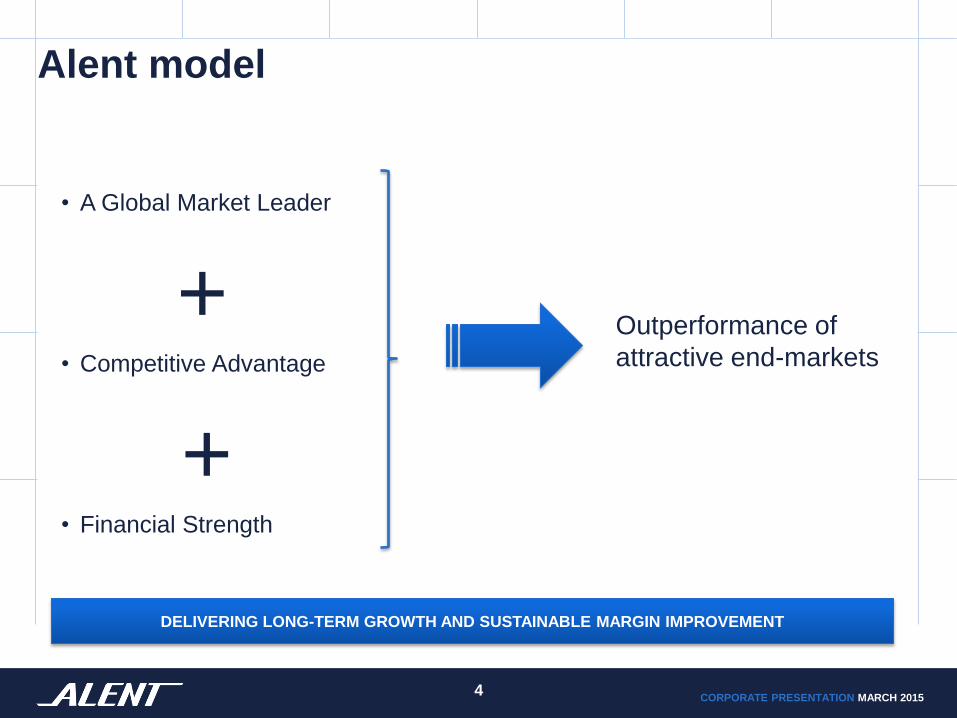

Alent model

• A Global Market Leader

+ • Competitive Advantage

+ • Financial Strength

Outperformance of

attractive end-markets

DELIVERING LONG-TERM GROWTH AND SUSTAINABLE MARGIN IMPROVEMENT

4

CORPORATE PRESENTATION MARCH 2015

A global market leader: Competitive landscape

Alent (Alpha)

Senju (Japan/Private)

Tamura (Japan/Public)

Indium (US/Private)

Kester (ITW - US/Listed)

Henkel (Europe/Listed)

Shenmao (Taiwan/Private)

Surface Chemistries Assembly Materials

Atotech (Total)

Alent (Enthone)

MacDermid (Platform)

Dow (Rohm & Haas)

OMG (US/Listed)

Coventya (Europe/Private)

Umicore (Europe/Listed)

MARKET LEADING POSITIONS #1 AND #2

5

Top 7 suppliers =

80% of the Market

Top 7 suppliers =

65% of the Market

CORPORATE PRESENTATION MARCH 2015

Strong global presence

2014 NSV by geography 2014 revenue by geography

28%

33%

39%

Americas Europe Asia

28%

29%

43%

Americas Europe Asia

£413.0m £644.8m

6

“Just in time” supply chain Present in over 100 countries Recent investments in high

growth Asia region

CORPORATE PRESENTATION MARCH 2015

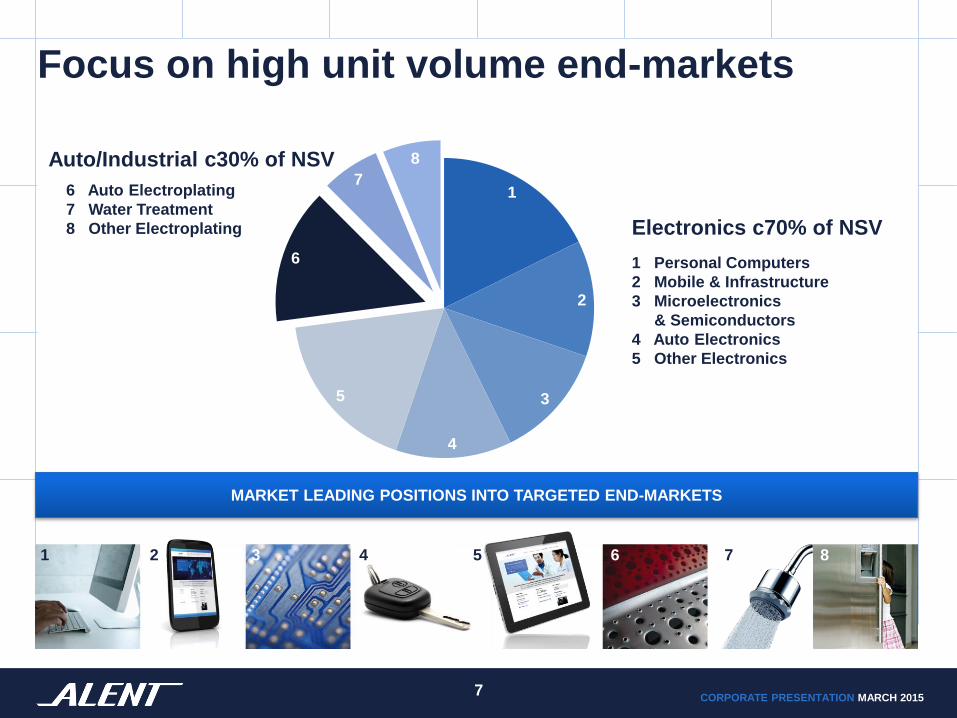

Focus on high unit volume end-markets

MARKET LEADING POSITIONS INTO TARGETED END-MARKETS

1 Personal Computers

2 Mobile & Infrastructure

3 Microelectronics

& Semiconductors

4 Auto Electronics

5 Other Electronics

6 Auto Electroplating

7 Water Treatment

8 Other Electroplating

7

1

2

3

4

5

6

7

8

Electronics c70% of NSV

Auto/Industrial c30% of NSV

1 2 3 4 5 6 7 8

CORPORATE PRESENTATION MARCH 2015

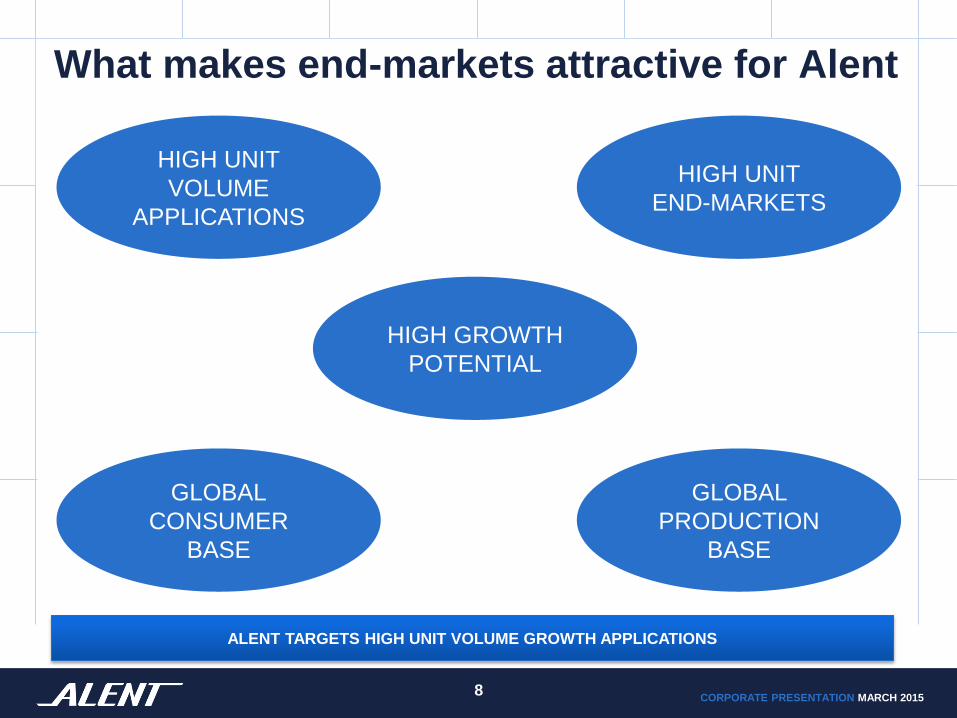

What makes end-markets attractive for Alent

ALENT TARGETS HIGH UNIT VOLUME GROWTH APPLICATIONS

8

HIGH UNIT

VOLUME

APPLICATIONS

GLOBAL

PRODUCTION

BASE

HIGH GROWTH

POTENTIAL

HIGH UNIT

END-MARKETS

GLOBAL

CONSUMER

BASE

CORPORATE PRESENTATION MARCH 2015

Alent’s competitive advantage

9

• Differentiated OEM customer model

• Customer-driven, “fast cycle” R&D

• Technical services

• Global footprint

DELIVERING LONG-TERM GROWTH AND SUSTAINABLE MARGIN IMPROVEMENT

CORPORATE PRESENTATION MARCH 2015

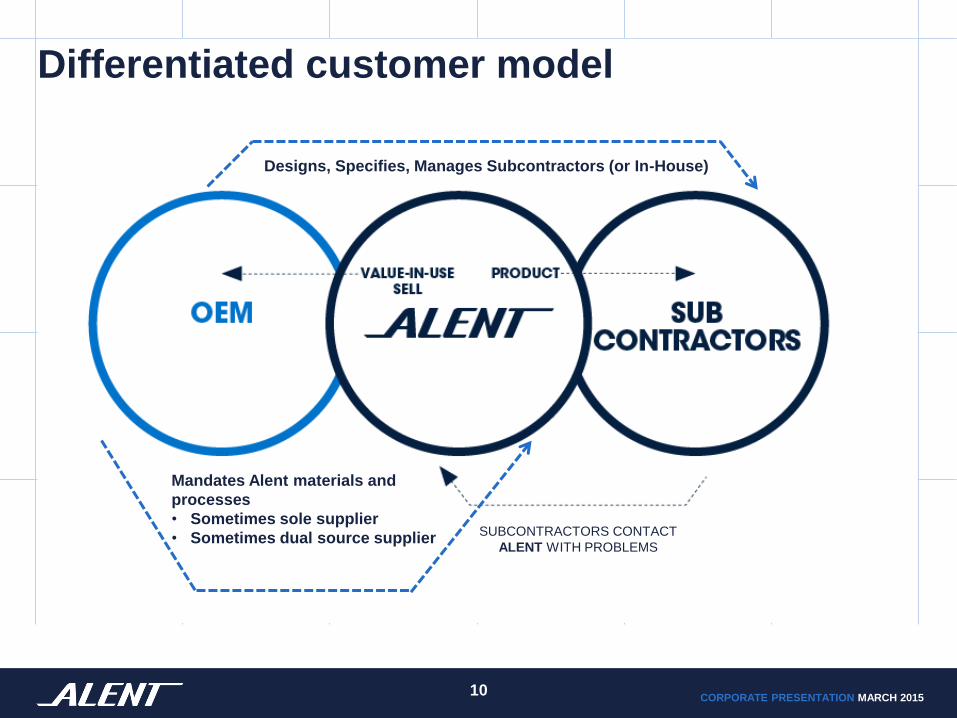

Differentiated customer model

10

Mandates Alent materials and

processes

• Sometimes sole supplier

• Sometimes dual source supplier

Designs, Specifies, Manages Subcontractors (or In-House)

SUBCONTRACTORS CONTACT

ALENT WITH PROBLEMS

CORPORATE PRESENTATION MARCH 2015

Alent OEM competitive advantage

• Market leadership and globally recognised brands gets us to the table

• Global team of value-in-use technical sales personnel

• Customer-driven, “fast cycle” R&D, enabling innovation and new

product pipeline

• R&D facilities to model customer processes and generate data to

demonstrate increased efficiencies and yield

• Value-in-use strategy ensures long-term relationship and price stability

• Strategic proximity to subcontractors (“customers”)

EXCELLENT EXECUTION PROVIDES HIGH BARRIERS TO ENTRY

11

CORPORATE PRESENTATION MARCH 2015

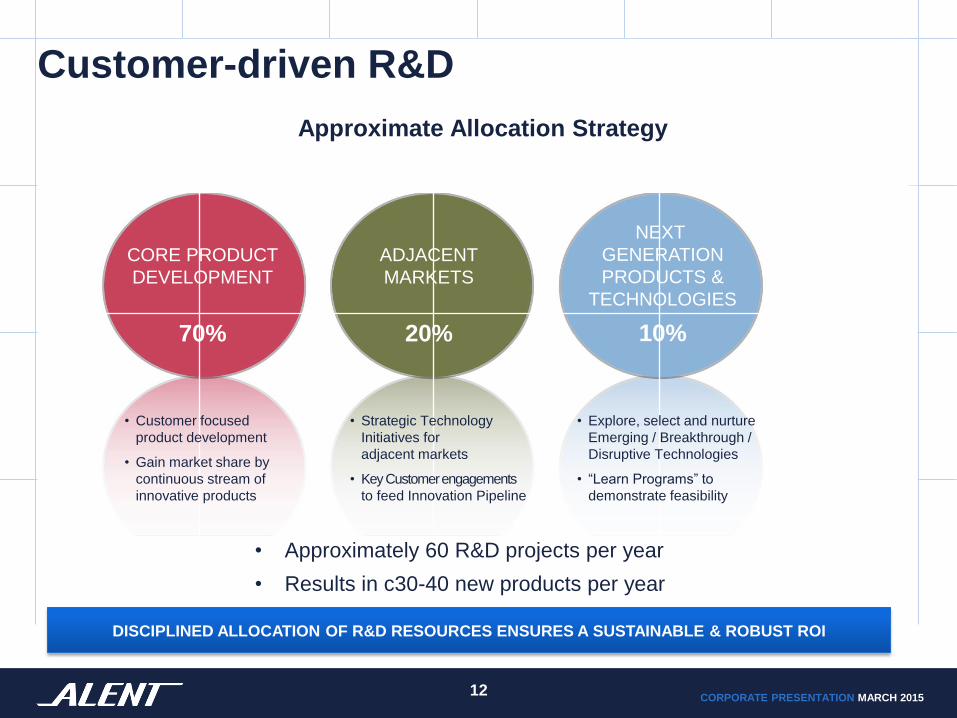

Customer-driven R&D

Approximate Allocation Strategy

DISCIPLINED ALLOCATION OF R&D RESOURCES ENSURES A SUSTAINABLE & ROBUST ROI

12

• Approximately 60 R&D projects per year

• Results in c30-40 new products per year

CORE PRODUCT

DEVELOPMENT

70%

ADJACENT

MARKETS

20%

NEXT

GENERATION

PRODUCTS &

TECHNOLOGIES

10%

• Customer focused

product development

• Gain market share by

continuous stream of

innovative products

• Strategic Technology

Initiatives for

adjacent markets

• Key Customer engagements

to feed Innovation Pipeline

• Explore, select and nurture

Emerging / Breakthrough /

Disruptive Technologies

• “Learn Programs” to

demonstrate feasibility

CORPORATE PRESENTATION MARCH 2015

“Fast cycle” R&D

• Mobile requires rapid/continuous development

• In only months Alent technology can reach volume manufacturing

• Automotive requires intensive material characterisation to demanding

segment specific reliability testing

• Greater than a year for Alent technology to reach volume manufacturing

Fast/long cycle

ABILITY TO SERVE BOTH MODELS DEMONSTRATES THE STRENGTH OF OUR INTEGRATED OEM/VOC

R&D STRATEGY

13

YEARS 1 2 3 4 5 6 7 8

Mobile

Automotive

Product approval

Product lifecycle

CORPORATE PRESENTATION MARCH 2015

Technical services

14

ON THE FRONT LINE, SOLVING PROBLEMS

• Global team of experienced engineers

• Deep understanding of customers’ processes

• Walking the floor, solving problems in real time

• Not every problem requires a new product

• “Fast cycle” R&D – develop, test and improve

CORPORATE PRESENTATION MARCH 2015

Global footprint

15 15

GLOBAL PRESENCE WITH CLOSE PROXIMITY TO OUR GLOBAL CUSTOMERS’ LOCAL SITES

• Global presence, enabling access to all key growth markets

• Strategically positioned manufacturing and R&D presence close to industry defining customers

• Longstanding and collaborative customer relationships

• Leading position in innovation and product development

• Strong presence in Asia, particularly China

CORPORATE PRESENTATION MARCH 2015

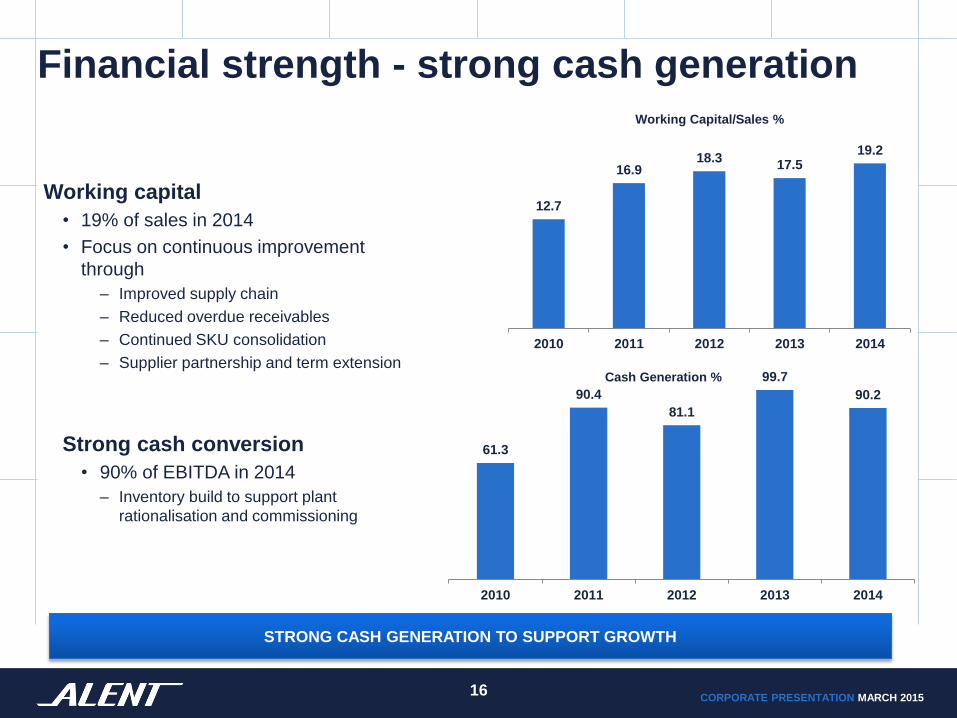

Financial strength - strong cash generation

12.7

16.9 18.3

17.5 19.2

2010 2011 2012 2013 2014

Working Capital/Sales %

Working capital

• 19% of sales in 2014

• Focus on continuous improvement

through

– Improved supply chain

– Reduced overdue receivables

– Continued SKU consolidation

– Supplier partnership and term extension

Strong cash conversion

• 90% of EBITDA in 2014

– Inventory build to support plant

rationalisation and commissioning

61.3

90.4

81.1

99.7

90.2

2010 2011 2012 2013 2014

Cash Generation %

STRONG CASH GENERATION TO SUPPORT GROWTH

16

CORPORATE PRESENTATION MARCH 2015

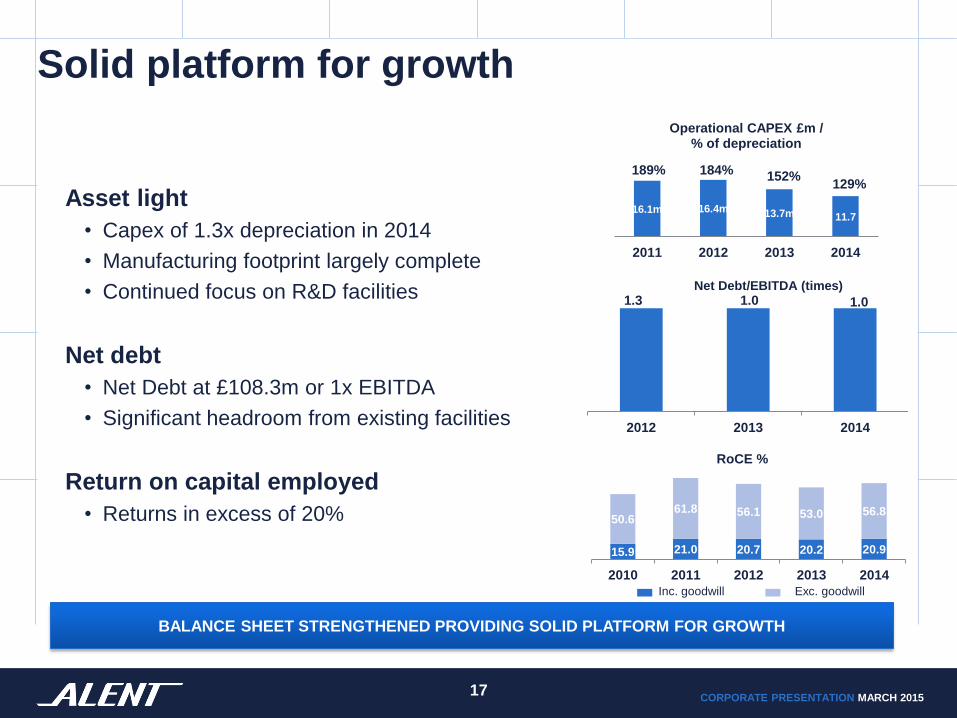

Solid platform for growth

15.9 21.0 20.7 20.2 20.9

50.6 61.8 56.1 53.0 56.8

2010 2011 2012 2013 2014

RoCE %

1.3 1.0 1.0

2012 2013 2014

Net Debt/EBITDA (times)

Asset light

• Capex of 1.3x depreciation in 2014

• Manufacturing footprint largely complete

• Continued focus on R&D facilities

Net debt

• Net Debt at £108.3m or 1x EBITDA

• Significant headroom from existing facilities

Return on capital employed

• Returns in excess of 20%

BALANCE SHEET STRENGTHENED PROVIDING SOLID PLATFORM FOR GROWTH

17

16.1m 16.4m 13.7m 11.7

2011 2012 2013 2014

Operational CAPEX £m / % of depreciation

189% 184% 152%

Inc. goodwill Exc. goodwill

129%

CORPORATE PRESENTATION MARCH 2015

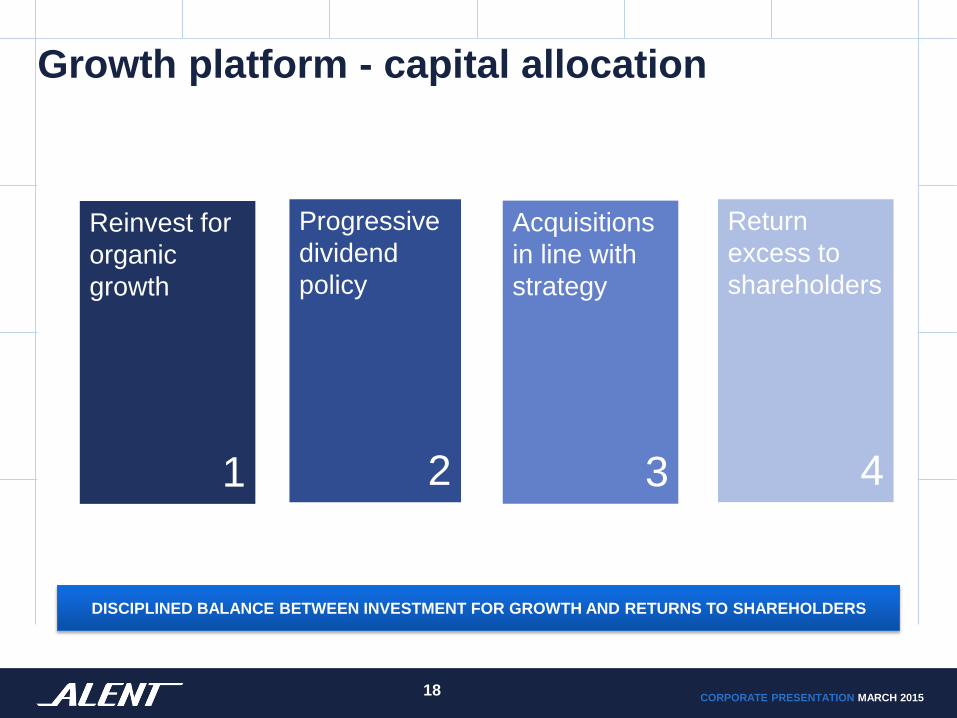

Growth platform - capital allocation

18 18

DISCIPLINED BALANCE BETWEEN INVESTMENT FOR GROWTH AND RETURNS TO SHAREHOLDERS

Progressive

dividend

policy

2

Reinvest for

organic

growth

1

Acquisitions

in line with

strategy

3

Return

excess to

shareholders

4

CORPORATE PRESENTATION MARCH 2015

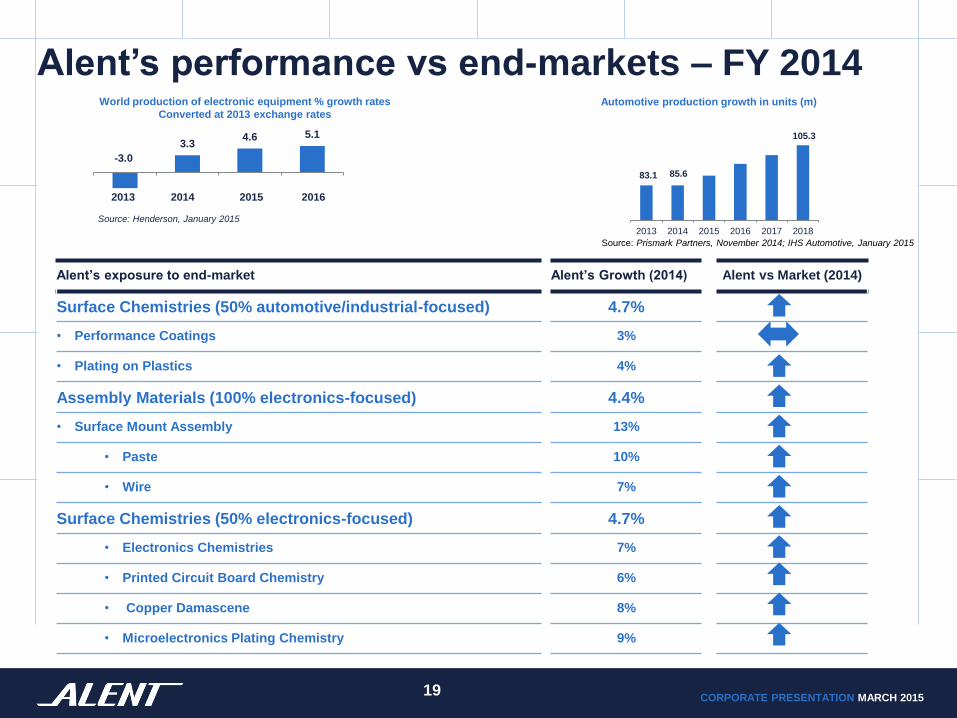

Alent’s performance vs end-markets – FY 2014

19

Alent’s exposure to end-market Alent’s Growth (2014) Alent vs Market (2014)

Surface Chemistries (50% automotive/industrial-focused) 4.7%

• Performance Coatings 3%

• Plating on Plastics 4%

Assembly Materials (100% electronics-focused) 4.4%

• Surface Mount Assembly 13%

• Paste 10%

• Wire 7%

Surface Chemistries (50% electronics-focused) 4.7%

• Electronics Chemistries 7%

• Printed Circuit Board Chemistry 6%

• Copper Damascene 8%

• Microelectronics Plating Chemistry 9%

-3.0

3.3 4.6 5.1

Source: Henderson, January 2015

World production of electronic equipment % growth rates

Converted at 2013 exchange rates Automotive production growth in units (m)

Source: Prismark Partners, November 2014; IHS Automotive, January 2015

2013 2014 2015 2016 2017 2018

105.3

83.1

2013 2014 2015 2016

85.6

CORPORATE PRESENTATION MARCH 2015

INVESTING FOR GROWTH

20

CORPORATE PRESENTATION MARCH 2015

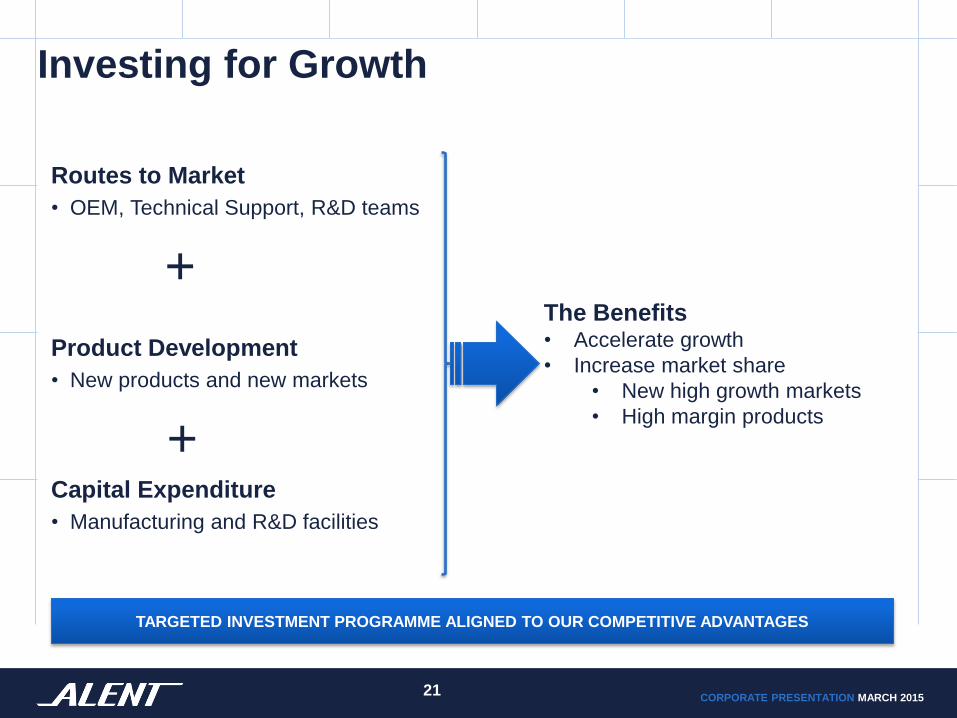

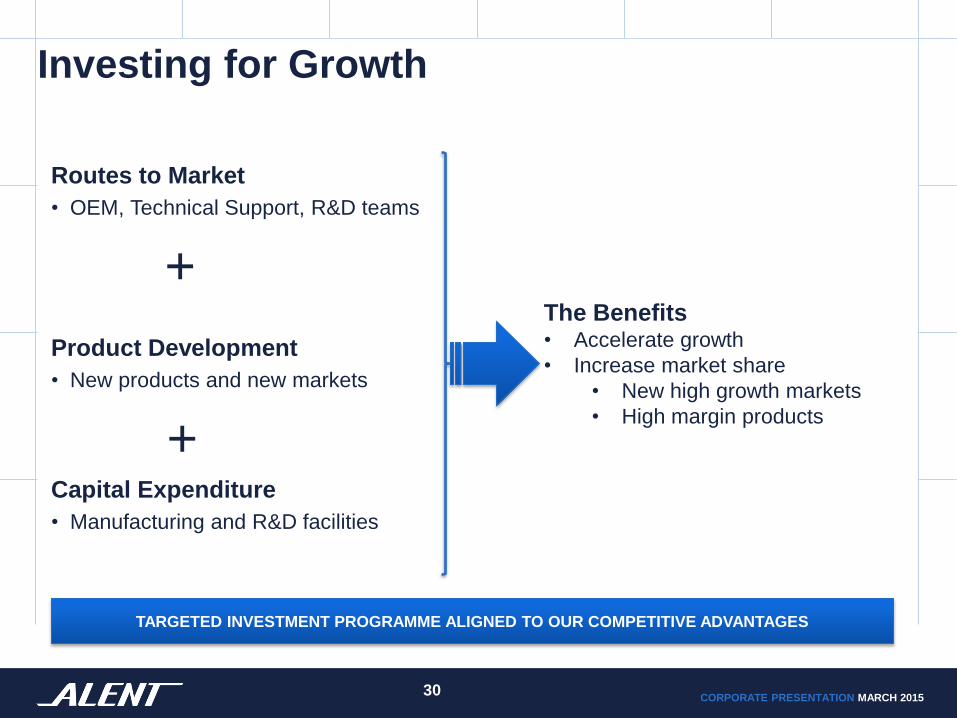

Investing for Growth

Routes to Market

• OEM, Technical Support, R&D teams

+

Product Development

• New products and new markets

+ Capital Expenditure

• Manufacturing and R&D facilities

The Benefits • Accelerate growth

• Increase market share

• New high growth markets

• High margin products

TARGETED INVESTMENT PROGRAMME ALIGNED TO OUR COMPETITIVE ADVANTAGES

21 21

CORPORATE PRESENTATION MARCH 2015

APPENDICES

22

CORPORATE PRESENTATION MARCH 2015

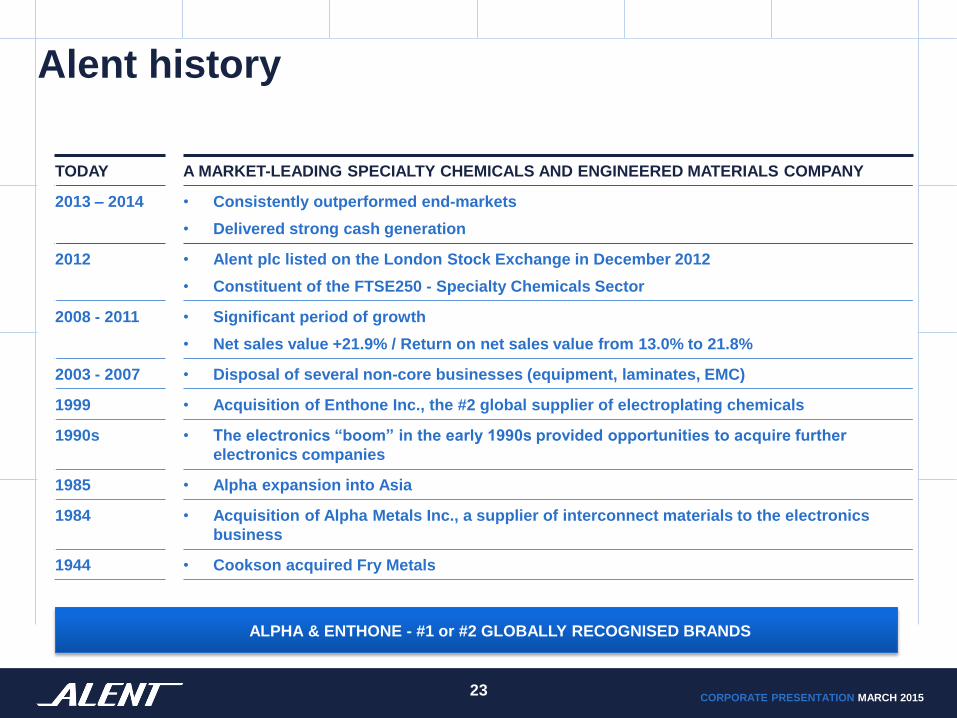

Alent history

TODAY A MARKET-LEADING SPECIALTY CHEMICALS AND ENGINEERED MATERIALS COMPANY

2013 – 2014 • Consistently outperformed end-markets

• Delivered strong cash generation

2012 • Alent plc listed on the London Stock Exchange in December 2012

• Constituent of the FTSE250 - Specialty Chemicals Sector

2008 - 2011 • Significant period of growth

• Net sales value +21.9% / Return on net sales value from 13.0% to 21.8%

2003 - 2007 • Disposal of several non-core businesses (equipment, laminates, EMC)

1999 • Acquisition of Enthone Inc., the #2 global supplier of electroplating chemicals

1990s • The electronics “boom” in the early 1990s provided opportunities to acquire further

electronics companies

1985 • Alpha expansion into Asia

1984 • Acquisition of Alpha Metals Inc., a supplier of interconnect materials to the electronics

business

1944 • Cookson acquired Fry Metals

ALPHA & ENTHONE - #1 or #2 GLOBALLY RECOGNISED BRANDS

23

CORPORATE PRESENTATION MARCH 2015

Assembly Materials – Product lines

Surface Mount Assembly – Products for use in electronic equipment

• Solder paste - Using a stencil to place small deposits of solder onto a printed circuit board

• Wire solder - Used in touch-up and rework applications

• Preforms - Solder components engineered into specific shapes/forms

• Stencils - Used to apply adhesive and solder paste onto a printed circuit board

Wave Solder Assembly – Products for use in electronic equipment

• Bar solder and flux – Used in mature wave soldering process

Microlectronics – Products for use in semiconductors

• Electronic polymers – Used for packaging, sealing and conductive adhesives

• Solder spheres – Used for integrated circuit and printed circuit board connections

• Die attach – Used to attach the semiconductor chip to the package

• PV ready ribbon – A pre-fluxed solder coated copper ribbon used for connecting solar cells within

a solar panel

Other

• Reclaim – Metal recycling business – reclaim of waste solder, reused in solder processes

• Water treatment – Produces chemicals for industrial end-markets

24

CORPORATE PRESENTATION MARCH 2015

Surface Chemistries – Product lines

Performance Coatings – Products for use in industrial/automotive end-markets

• Decorative coatings - Decorative electroplating chemistries developed to enable plating directly

onto plastic in industrial and automotive markets

• Wear resistant coatings - Chromium electroplating chemistries used in industrial applications and

for use on auto parts such as engine valves and shock absorber cylinders

• Corrosion resistant coatings - Zinc alloy electroplating chemistries used in industrial, building

and auto markets (e.g. on brake calipers and fasteners)

Electronics

• Copper damascene - Electroplating chemistry used to create the wires within a semiconductor

integrated circuit chip

• Wafer bumping chemistries - Electroplating for connections within the integrated circuit

• Interconnect materials - Electroplating chemistries for fabrication of printed circuit boards

25

CORPORATE PRESENTATION MARCH 2015

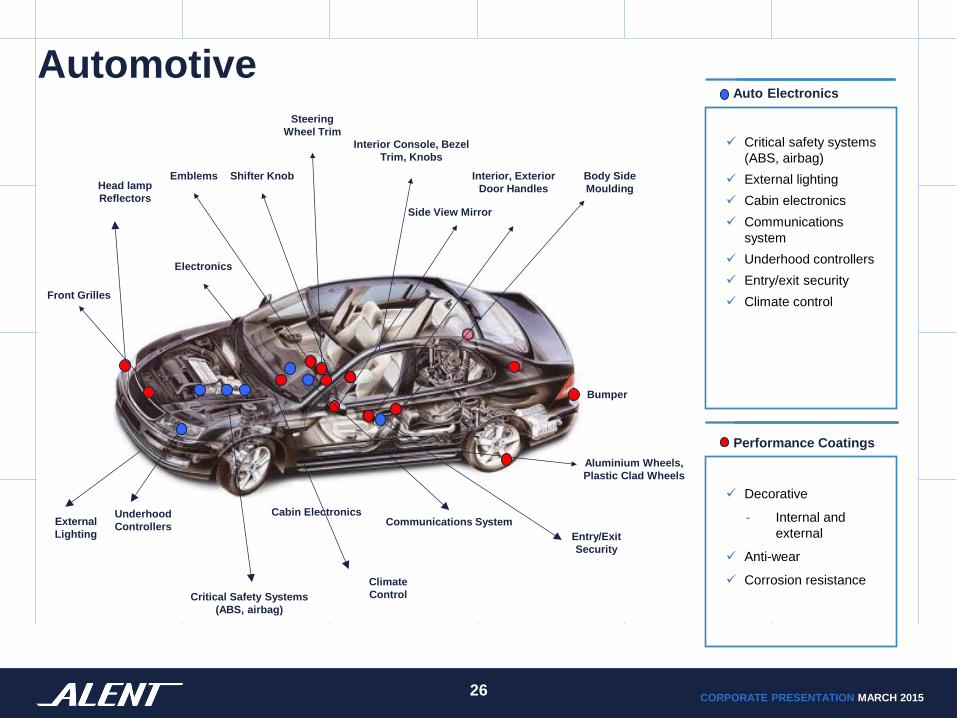

Automotive

Critical safety systems

(ABS, airbag)

External lighting

Cabin electronics

Communications

system

Underhood controllers

Entry/exit security

Climate control

Decorative

- Internal and

external

Anti-wear

Corrosion resistance

Performance Coatings

Auto Electronics

26

Head lamp

Reflectors

Front Grilles

Electronics

Emblems

Steering

Wheel Trim

Interior Console, Bezel

Trim, Knobs

Body Side

Moulding

Bumper

Aluminium Wheels,

Plastic Clad Wheels

Interior, Exterior

Door Handles

Side View Mirror

Shifter Knob

Critical Safety Systems

(ABS, airbag)

External

Lighting

Cabin Electronics Communications System

Underhood

Controllers Entry/Exit

Security

Climate

Control

CORPORATE PRESENTATION MARCH 2015

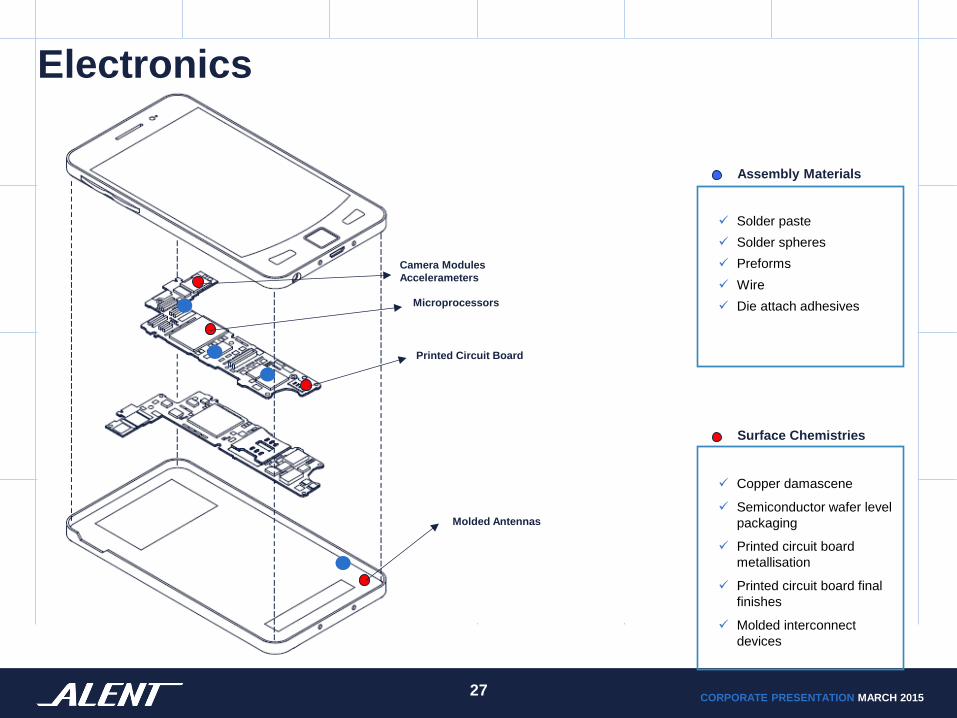

Electronics

27

Solder paste

Solder spheres

Preforms

Wire

Die attach adhesives

Copper damascene

Semiconductor wafer level

packaging

Printed circuit board

metallisation

Printed circuit board final

finishes

Molded interconnect

devices

Molded Antennas

Printed Circuit Board

Microprocessors

Camera Modules

Accelerameters

Surface Chemistries

Assembly Materials

CORPORATE PRESENTATION MARCH 2015

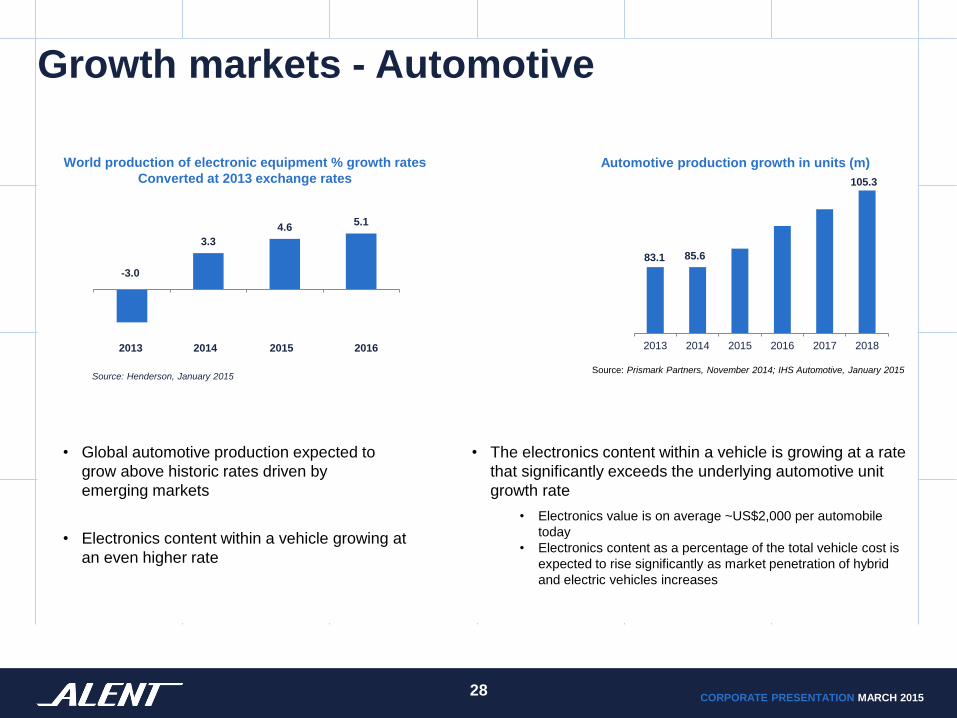

Growth markets - Automotive

28

• Global automotive production expected to

grow above historic rates driven by

emerging markets

• Electronics content within a vehicle growing at

an even higher rate

• The electronics content within a vehicle is growing at a rate

that significantly exceeds the underlying automotive unit

growth rate

• Electronics value is on average ~US$2,000 per automobile

today

• Electronics content as a percentage of the total vehicle cost is

expected to rise significantly as market penetration of hybrid

and electric vehicles increases

-3.0

3.3

4.6 5.1

Source: Henderson, January 2015

World production of electronic equipment % growth rates

Converted at 2013 exchange rates

Automotive production growth in units (m)

Source: Prismark Partners, November 2014; IHS Automotive, January 2015

2013 2014 2015 2016 2017 2018

105.3

83.1

2013 2014 2015 2016

85.6

CORPORATE PRESENTATION MARCH 2015

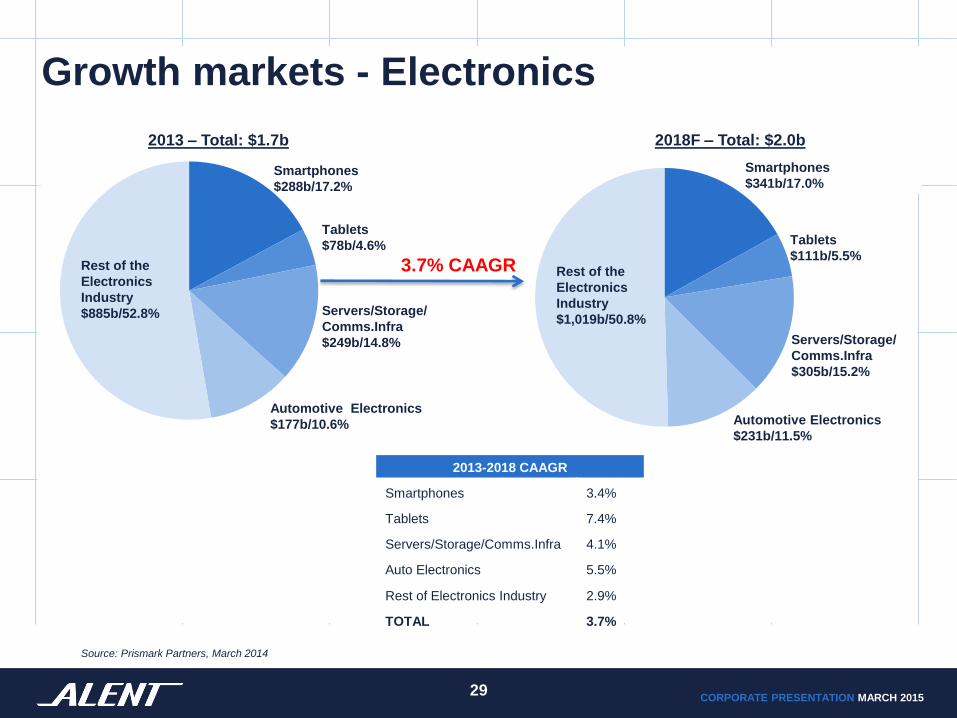

Growth markets - Electronics

2013-2018 CAAGR

Smartphones 3.4%

Tablets 7.4%

Servers/Storage/Comms.Infra 4.1%

Auto Electronics 5.5%

Rest of Electronics Industry 2.9%

TOTAL 3.7%

3.7% CAAGR

Smartphones

$288b/17.2%

Tablets

$78b/4.6%

Servers/Storage/

Comms.Infra

$249b/14.8%

Rest of the

Electronics

Industry

$885b/52.8%

Automotive Electronics

$177b/10.6%

Rest of the

Electronics

Industry

$1,019b/50.8%

Smartphones

$341b/17.0%

Tablets

$111b/5.5%

Automotive Electronics

$231b/11.5%

Servers/Storage/

Comms.Infra

$305b/15.2%

Source: Prismark Partners, March 2014

2013 – Total: $1.7b 2018F – Total: $2.0b

29

CORPORATE PRESENTATION MARCH 2015

Investing for Growth

Routes to Market

• OEM, Technical Support, R&D teams

+

Product Development

• New products and new markets

+ Capital Expenditure

• Manufacturing and R&D facilities

The Benefits • Accelerate growth

• Increase market share

• New high growth markets

• High margin products

TARGETED INVESTMENT PROGRAMME ALIGNED TO OUR COMPETITIVE ADVANTAGES

30 30

CORPORATE PRESENTATION MARCH 2015

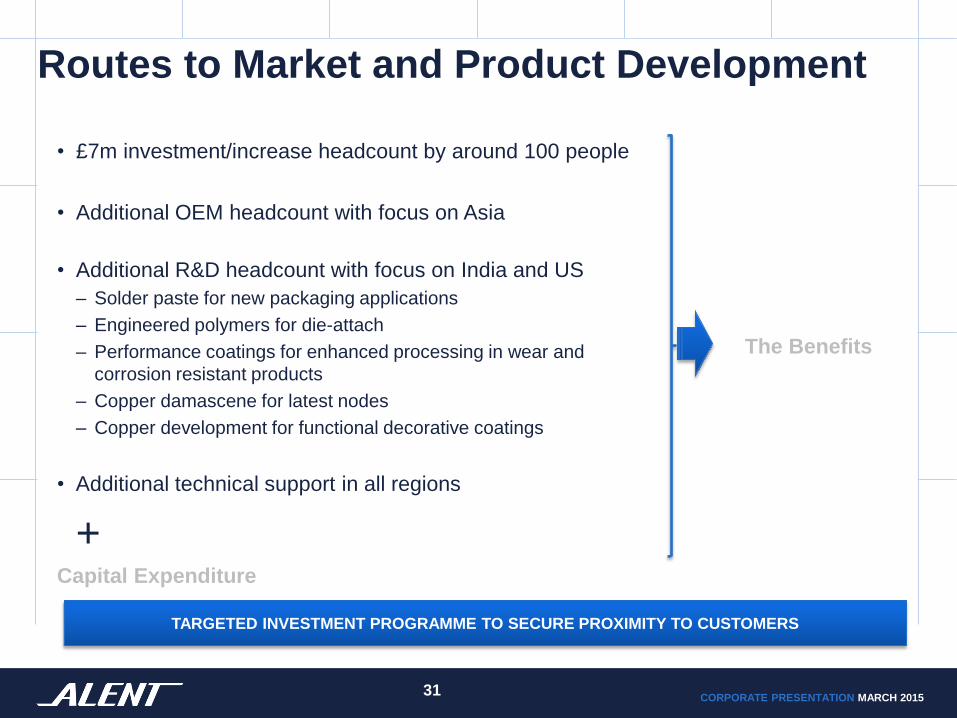

Routes to Market and Product Development

• £7m investment/increase headcount by around 100 people

• Additional OEM headcount with focus on Asia

• Additional R&D headcount with focus on India and US

– Solder paste for new packaging applications

– Engineered polymers for die-attach

– Performance coatings for enhanced processing in wear and

corrosion resistant products

– Copper damascene for latest nodes

– Copper development for functional decorative coatings

• Additional technical support in all regions

+ Capital Expenditure

31 31

TARGETED INVESTMENT PROGRAMME TO SECURE PROXIMITY TO CUSTOMERS

The Benefits

CORPORATE PRESENTATION MARCH 2015

Capital Expenditure

• 2015 CAPEX of 1.5 – 1.8x depreciation

• Invest in manufacturing capability

– US

• Wafer level packaging

• Copper damascene process line

– Asia

• Powder manufacturing capability

• Invest in R&D equipment with a focus on high margin products

– Die-attach, LED and nano silver in India

– Wafer fabrication research in the US

– Coating development equipment in Europe

+ Routes to Market and Product Development

The Benefits

TARGETED INVESTMENT PROGRAMME ALIGNED TO OUR COMPETITIVE ADVANTAGES

32 32

CORPORATE PRESENTATION MARCH 2015

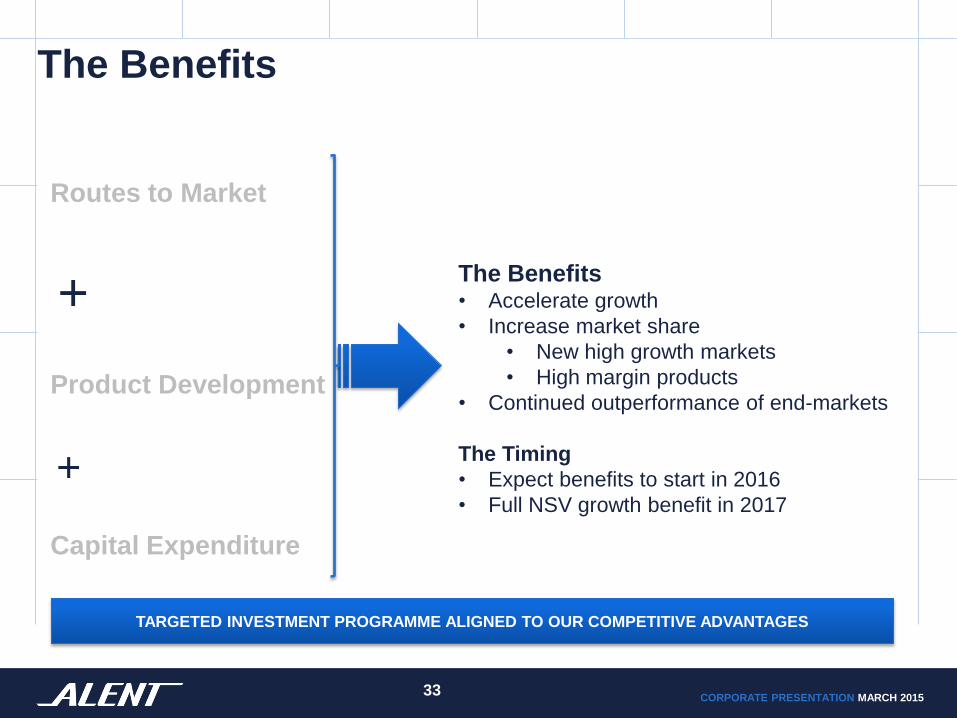

The Benefits

Routes to Market

+

Product Development

+

Capital Expenditure

TARGETED INVESTMENT PROGRAMME ALIGNED TO OUR COMPETITIVE ADVANTAGES

33 33

The Benefits • Accelerate growth

• Increase market share

• New high growth markets

• High margin products

• Continued outperformance of end-markets

The Timing

• Expect benefits to start in 2016

• Full NSV growth benefit in 2017

CORPORATE PRESENTATION MARCH 2015

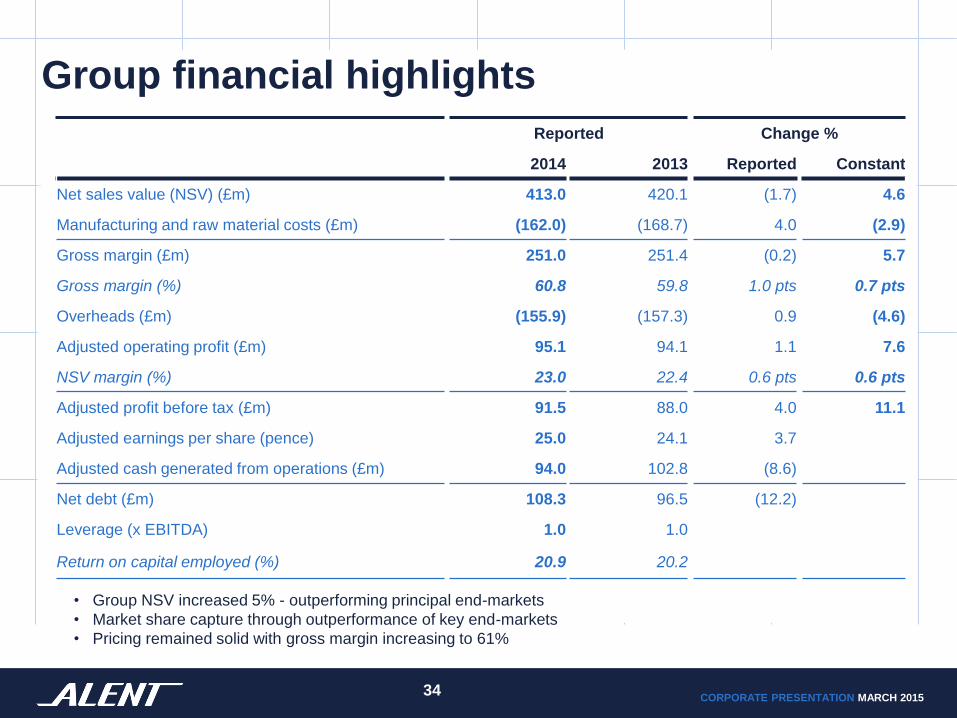

Group financial highlights

34 34

Reported Change %

2014 2013 Reported Constant

Net sales value (NSV) (£m) 413.0 420.1 (1.7) 4.6

Manufacturing and raw material costs (£m) (162.0) (168.7) 4.0 (2.9)

Gross margin (£m) 251.0 251.4 (0.2) 5.7

Gross margin (%) 60.8 59.8 1.0 pts 0.7 pts

Overheads (£m) (155.9) (157.3) 0.9 (4.6)

Adjusted operating profit (£m) 95.1 94.1 1.1 7.6

NSV margin (%) 23.0 22.4 0.6 pts 0.6 pts

Adjusted profit before tax (£m) 91.5 88.0 4.0 11.1

Adjusted earnings per share (pence) 25.0 24.1 3.7

Adjusted cash generated from operations (£m) 94.0 102.8 (8.6)

Net debt (£m) 108.3 96.5 (12.2)

Leverage (x EBITDA) 1.0 1.0

Return on capital employed (%) 20.9 20.2

• Group NSV increased 5% - outperforming principal end-markets

• Market share capture through outperformance of key end-markets

• Pricing remained solid with gross margin increasing to 61%

CORPORATE PRESENTATION MARCH 2015

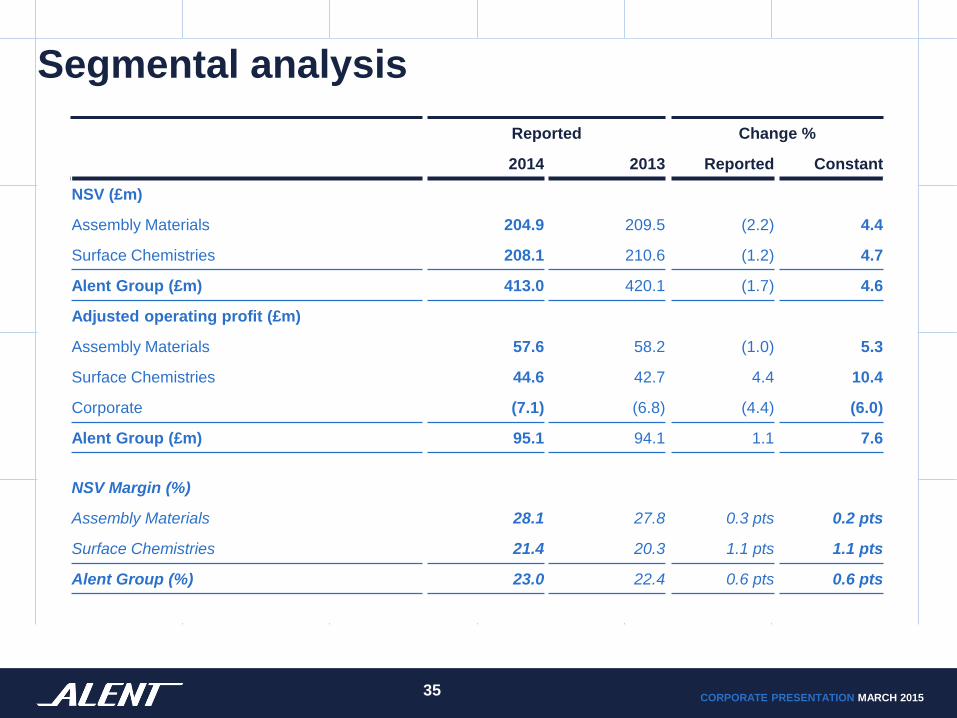

Segmental analysis

35 35

Reported Change %

2014 2013 Reported Constant

NSV (£m)

Assembly Materials 204.9 209.5 (2.2) 4.4

Surface Chemistries 208.1 210.6 (1.2) 4.7

Alent Group (£m) 413.0 420.1 (1.7) 4.6

Adjusted operating profit (£m)

Assembly Materials 57.6 58.2 (1.0) 5.3

Surface Chemistries 44.6 42.7 4.4 10.4

Corporate (7.1) (6.8) (4.4) (6.0)

Alent Group (£m) 95.1 94.1 1.1 7.6

NSV Margin (%)

Assembly Materials 28.1 27.8 0.3 pts 0.2 pts

Surface Chemistries 21.4 20.3 1.1 pts 1.1 pts

Alent Group (%) 23.0 22.4 0.6 pts 0.6 pts

CORPORATE PRESENTATION MARCH 2015

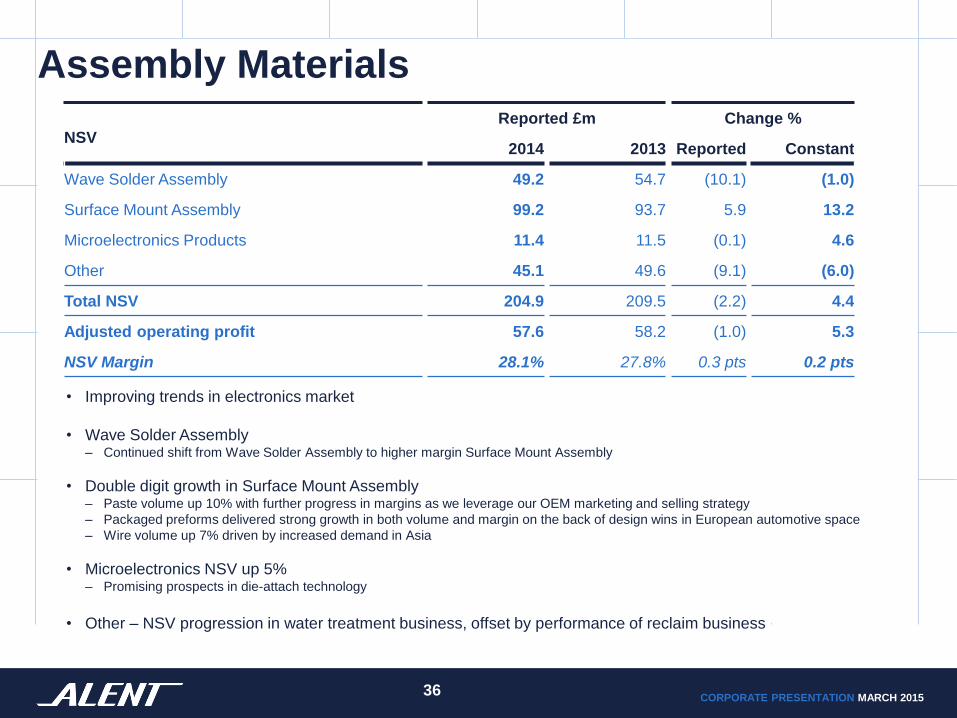

Assembly Materials

36 36

NSV

Reported £m Change %

2014 2013 Reported Constant

Wave Solder Assembly 49.2 54.7 (10.1) (1.0)

Surface Mount Assembly 99.2 93.7 5.9 13.2

Microelectronics Products 11.4 11.5 (0.1) 4.6

Other 45.1 49.6 (9.1) (6.0)

Total NSV 204.9 209.5 (2.2) 4.4

Adjusted operating profit 57.6 58.2 (1.0) 5.3

NSV Margin 28.1% 27.8% 0.3 pts 0.2 pts

• Improving trends in electronics market

• Wave Solder Assembly – Continued shift from Wave Solder Assembly to higher margin Surface Mount Assembly

• Double digit growth in Surface Mount Assembly – Paste volume up 10% with further progress in margins as we leverage our OEM marketing and selling strategy

– Packaged preforms delivered strong growth in both volume and margin on the back of design wins in European automotive space

– Wire volume up 7% driven by increased demand in Asia

• Microelectronics NSV up 5% – Promising prospects in die-attach technology

• Other – NSV progression in water treatment business, offset by performance of reclaim business

CORPORATE PRESENTATION MARCH 2015

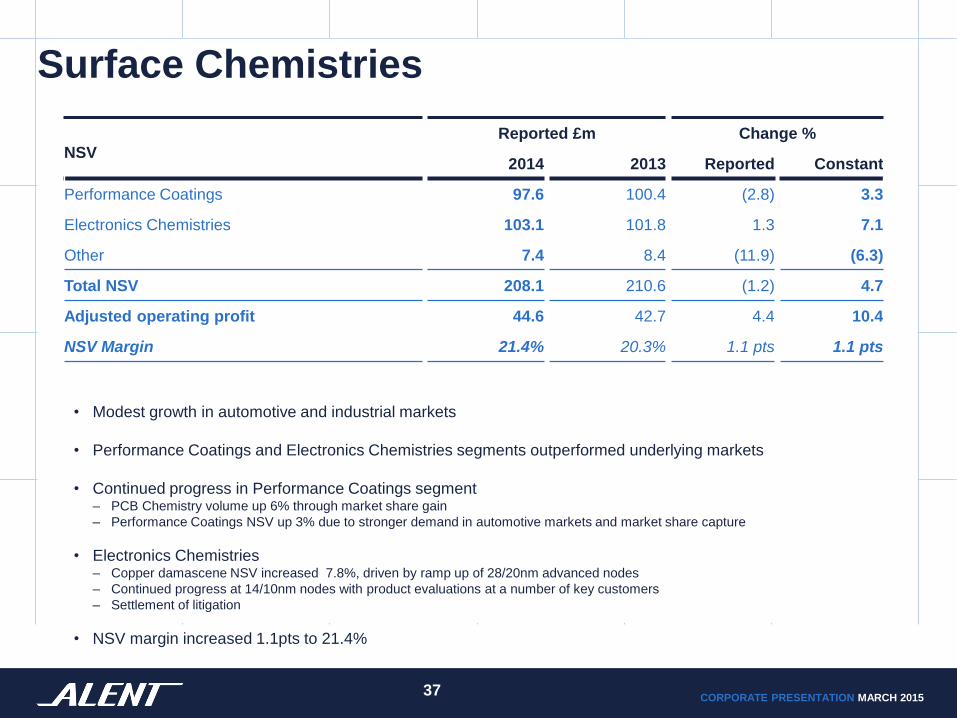

Surface Chemistries

37 37

NSV

Reported £m Change %

2014 2013 Reported Constant

Performance Coatings 97.6 100.4 (2.8) 3.3

Electronics Chemistries 103.1 101.8 1.3 7.1

Other 7.4 8.4 (11.9) (6.3)

Total NSV 208.1 210.6 (1.2) 4.7

Adjusted operating profit 44.6 42.7 4.4 10.4

NSV Margin 21.4% 20.3% 1.1 pts 1.1 pts

• Modest growth in automotive and industrial markets

• Performance Coatings and Electronics Chemistries segments outperformed underlying markets

• Continued progress in Performance Coatings segment – PCB Chemistry volume up 6% through market share gain

– Performance Coatings NSV up 3% due to stronger demand in automotive markets and market share capture

• Electronics Chemistries – Copper damascene NSV increased 7.8%, driven by ramp up of 28/20nm advanced nodes

– Continued progress at 14/10nm nodes with product evaluations at a number of key customers

– Settlement of litigation

• NSV margin increased 1.1pts to 21.4%

CORPORATE PRESENTATION MARCH 2015

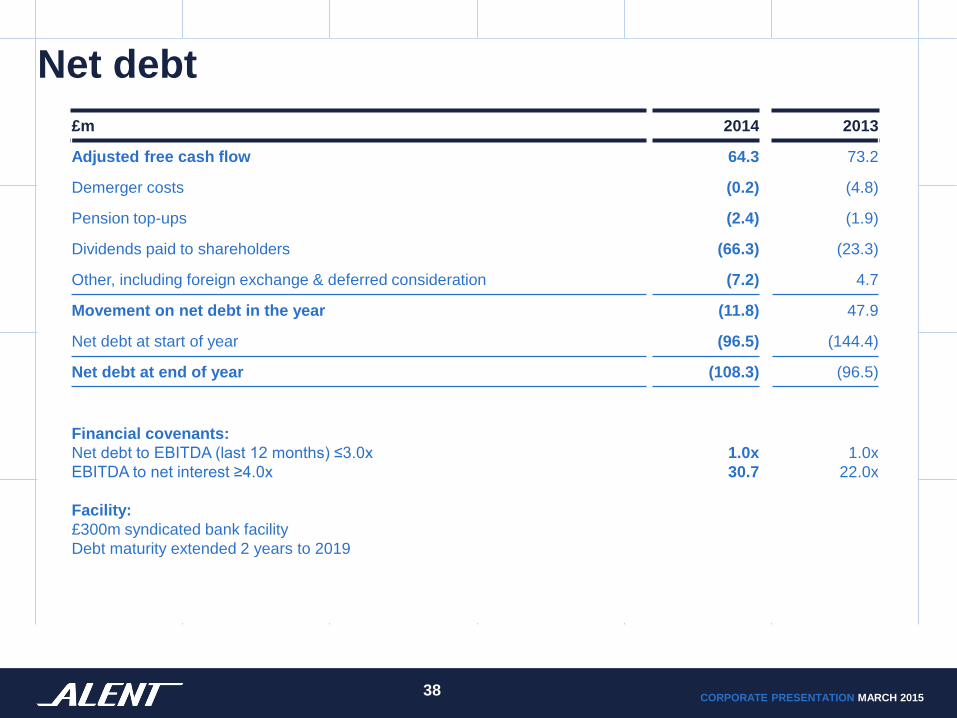

Net debt

38 38

£m 2014 2013

Adjusted free cash flow 64.3 73.2

Demerger costs (0.2) (4.8)

Pension top-ups (2.4) (1.9)

Dividends paid to shareholders (66.3) (23.3)

Other, including foreign exchange & deferred consideration (7.2) 4.7

Movement on net debt in the year (11.8) 47.9

Net debt at start of year (96.5) (144.4)

Net debt at end of year (108.3) (96.5)

Financial covenants:

Net debt to EBITDA (last 12 months) ≤3.0x

EBITDA to net interest ≥4.0x

Facility:

£300m syndicated bank facility

Debt maturity extended 2 years to 2019

1.0x

30.7

1.0x

22.0x

CORPORATE PRESENTATION MARCH 2015

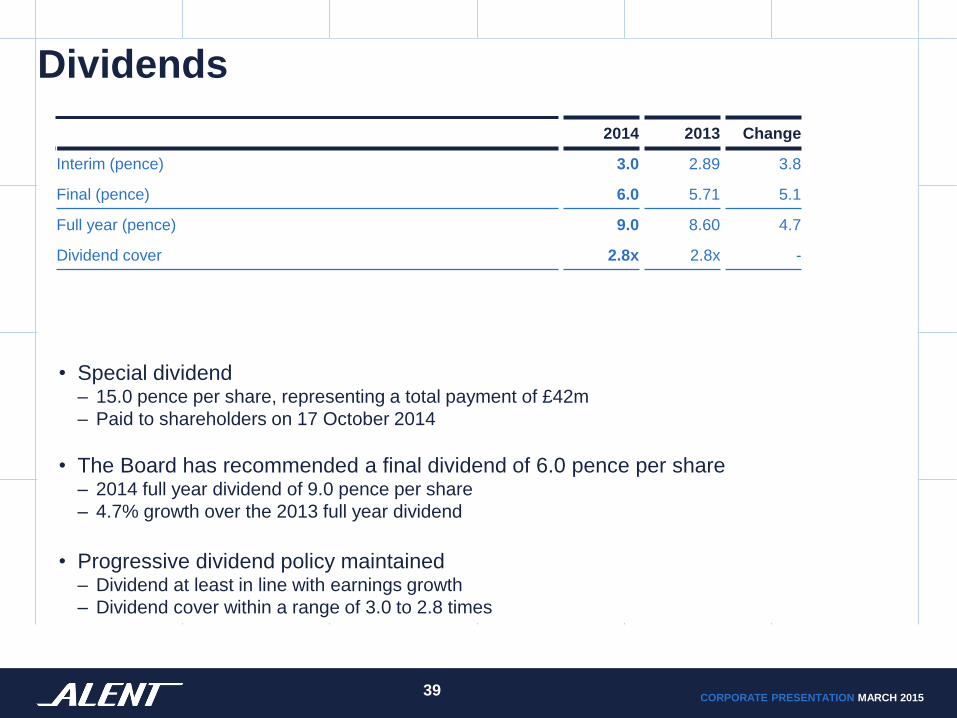

Dividends

39 39

2014 2013 Change

Interim (pence) 3.0 2.89 3.8

Final (pence) 6.0 5.71 5.1

Full year (pence) 9.0 8.60 4.7

Dividend cover 2.8x 2.8x -

• Special dividend – 15.0 pence per share, representing a total payment of £42m

– Paid to shareholders on 17 October 2014

• The Board has recommended a final dividend of 6.0 pence per share – 2014 full year dividend of 9.0 pence per share

– 4.7% growth over the 2013 full year dividend

• Progressive dividend policy maintained – Dividend at least in line with earnings growth

– Dividend cover within a range of 3.0 to 2.8 times

CORPORATE PRESENTATION MARCH 2015

Definitions

40 40

The following are referred to throughout this presentation:-

• NSV is revenue less commodity metals (tin, silver, gold).

• Adjusted operating profit, adjusted profit before tax, adjusted profit for the year and adjusted earnings per share are,

where appropriate, each stated before: exceptional items; amortisation of acquired intangible assets; deferred tax on

acquired intangible assets and goodwill; utilisation of deferred tax assets (where initial recognition was as an

exceptional item); acquisition costs; the impact arising from the fair valuing of financial instruments; and profits or

losses arising on business disposals.

• Adjusted cash generated from operations is cash generated from operations after adding back £0.2m (2013: £4.8m)

for demerger cash costs.

• Free cash flow is defined as net cash from operating activities after net outlays for the purchase and sale of property,

plant and equipment and dividends from joint ventures but before additional funding contributions to Group pension

plans.

![pcw 2011 Cut off - 58 - talentacademy.co.in · PSC- L.D ¢m¿°v ap≥h¿j tNmZy-t]-∏-dp-Iƒ Talent Academy hnP-b-tcJ {]kn-≤o-I-cWw TT T ALENT ALENT ALENT 57. Im°-\m-S≥ F∂](https://img.pdfslide.us/doc/110x75/5c9c7e1f09d3f23b2a8c0f6b/pcw-2011-cut-off-58-psc-ld-mv-aphj-tnmzy-t-dp-if-talent.jpg)