7/29/2019 Alan Reynolds Links E-p Ratio to Bond Yield, March 21,

1991

1/2

Alan Reynolds AssociatesThe Stock Market Likes Bonds

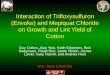

Th e graph _presents an in t r iguingpuzz le . Shaded bars show

the r a t i oof earnings to s tock pr ices . [Thisi s the inverse

of the pr ice/earningr a t io - a low bar means s tock pricesare

high , r e l a t i ve to earnings.] The

The graph 's main puzzle i s t ha t thes tock mult ip le of ten

seems to improvebefore bond y ie lds f a l l - look a t1975,

1979-80 and 1989-90. There i sonly one year on th e graph t h a t

looksout of place - 1987 - s ince stock

10-Year U.S. Treasury Bond Yieldand the Earnings/Price Ratio of

Stocks

{S&P 500 )

- - 10 yr bond + core inflation (PPI)percent (bond yie ld &

inflation)+

15 -

D earnings/s tock pricee /p ratio (s tocks)

15

I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I I

I60 65 70 75 80 85 91

1991 is forecas tcore inflation is PPI Dec-lo -D ec(less food

and energy after 1973 )

dark l ine shows the y ie ld on 10-yearTreasury bonds. Stock

mult ip les areobviously qui te c lose ly re la ted tobond yie lds

.At f i r s t glance, th i s may seemobvious. As i n t e r e s t r

a tes f a l l , thepresen t value of fu ture earnings i sworth

more, because it i s discounteda t a lower i n t e r e s t r a t e

.

prices were high r e l a t i ve to earnings( for the year as a

whole), y e t bondyie lds were high too . However, th i sanomaly

was "f ixed" in October oft ha t year , as s tock pr ices col

lapsedand bond pr ices rose . Today, highs tock pr ices , r e l a t

i ve to lo wearnings , are simply not consis tentwith a bond y ie

ld as high as 8%.Something has to give . Th e c r i t i c a l

8605 Allisonville Road, Suite 105, Indianapolis, IN

46250Affiliated with Keane Securities - Member New York Stock

Exchange

SO Broadway, New York, NY, 212-422-1255; Trading, 212-422-1002

and 800-221-1920The information, opinions and recommendations

herein cont ained represent a study or report for the use of our

customers solely for advisory andmformati_ve purposes. Such

mformation has been obtained from company reports, standard

reference manuals, trade publications or elsewhere. Themformat1on

may have been obtamed from none or all of the above sources wh ich

we believe to be reliable but we do not guarantee its accuracy.

7/29/2019 Alan Reynolds Links E-p Ratio to Bond Yield, March 21,

1991

2/2

quest ion, o f course, i s whether t ha tmeans s tock pr ices

must f a l l , or t ha tbond pr ices wi l l r i se . With the

soleexception of l a t e 1987 (a periodd i f f e r en t in many

ways from today) ,t h i s evidence suggests tha t bonds areoverdue

fo r a s igni f icant r a l ly .To bring s tock mult iples into l

inewith bond yie lds , some combination ofthe following has to

happen: ( l)stock pr ices have to f a l l , (2 )earnings have to r

i se , and/or (3 )bond pr ices have to r i s e . As can beseen in

the graph, my forecas t for1991 puts most of the adjustment onbond

yie lds , which remain below 7.5%,on average, for t h i s en t i r

e year .Earnings and s tock pr ices both r iseover the course of

the year . For1991 as a whole, though, earnings

still look low re la t ive to stockpr ices . The market i s

buyingimproved prospects for futureearnings , not ju s t the

currentdividend.Inves tors may expect the stockmarket to fol low

bond r a l l i e s , notlead them. But the idea of stocksmoving f i

r s t i s not rea l ly s t range,ju s t unfamil ia r . Fi r s t of

a l l , it i scommon to expla in a r a l ly in stocksof u t i l i t

i e s or banks, for example,as a bet on a bond r a l ly tha t has

notyet appeared. This i s no di f ferentthan seeing s tocks of o i

l companieschange in an t i c ipa t ion of a change ino i l pr ices

tha t i s l ikewise not yet

vis ib le . In te res t - sens i t ive s tocks,in par t icu la r

, may thus be seen as ameasure of expectat ions about bonds.Second,

a b ig ra l ly in stocksreduces the dividend yie ld , makingthe

coupon on bonds begin to lookre la t ive ly a t t rac t ive to

marginalinves tors . A marginal por t fo l ios h i f t in to bonds

i s par t icu la r lyl ike ly when long-term yie lds are wellabove

shor t - te rm, as they are now.Rick Mishkin 's extensive research

onyie ld curves reveals tha t "when thespread i s high th e long ra

te wil l

f a l l . 1Third, and most s igni f icant , therei s a common

force a t work tha ta f f ec t s both s tock mult iples and bondyie

lds - namely, expected in f la t ion .The graph shows producer pr

icein f la t ion , l es s food and energy,which I expect to be well

below 3%(down from 3.5% l a s t year) . Robert

Shi l le r of Yale f inds tha t s tockpr ices are more sens i t

ive toinf la t ion than bonds, which i sconsis tent with the view

tha t bondinves tors have something to learnfrom s tocks . 2In

contras t to the Keynesian view,

our expecta t ion of lower in f la t ion i sa both consequence

and cause ofincreased r ea l ac t iv i ty . Lowerpr ices of homes,

fo r example, helps e l l houses. Higher growth ofproduction an d

product ivi ty helpskeep costs and pr ices down. Lowerin f la t ion

also improves the qual i tyof prof i ts , and reduces the ef fec t

ivetax ra te on rea l pr o f i t s an d cap i t a lgains . That i s

one reason why s tockpr ices s tay high r e la t ive toearnings.

And the inflow into . u.s .markets associa ted with a t t r ac t

ivestocks and bonds keeps the dol la rs t rong, fur ther contr ibut

ing to a lowin f la t ion environment.An important impl ica t ion

of t h i sanalys is i s to avoid the herdi n s t i nc t to s e l l

bonds on news ofst ronger r ea l ac t iv i ty . Anotherrecent

National Bureau studydemonstrates t ha t "news of

higherthan-expected rea l ac t iv i ty when theeconomy i s al ready

s t rong r e su l t s inlower s tock pr ices , whereas the

samesurpr ise in a weak economy i s

a s s o c i a t ~ d with higher s tockpr ices . " Going back to

the graph,good news i s thus l ike ly to drivestock pr ices up more

promptly than itdoes earnings. And when theearnings/pr ice r a t io

f a l l s , tha t hasalways been associa ted with lower,not higher

, long-term in te r e s t r a t e s .

What i s good new for s tocks i s nowgood news fo r bonds

too.Alan ReynoldsMarch 21, 1991

====================================1. Fredric s. Mishkin,

"Yield Curve" NBER WorkingPaper No. 3550, Dec. 19902. Robert J .

Shiller & Andrea E. Beltratti, "StockPrices and Bond Yields . .

. " NBER Working Paper No.3454, Oct. 1990.

3. Grant McQueen & V. Vance Roley, "Stock Prices,News, and

Business Conditions" NBER Working PaperNo. 3520, Nov. 1990.