Embed Size (px)

DESCRIPTION

Akuntansi Sektor Publik 1

Citation preview

Finantin1 Accountability 63 Management, 12(3), August 1996,0267-4424

DECENTRALIZATION, ACCOUNTING CONTROLS AND PERFORMANCE OF GOVERNMENT ORGANIZATIONS: A

NEW ZEALAND EMPIRICAL STUDY

N.Z. MIAH AND L. MIA*

INTRODUCTION

Both organization structure and accounting control systems have received considerable attention in the contemporary literature on organization theory and accounting systems. While organization theory researchers have been primarily concerned with identifying factors influencing the design of organization structure (see Pugh et al., 1969), accounting researchers have focused more on ascertaining the nature and extent of accounting-based controls in organizations that promote effective planning and decision making (see, for example, Bromwich, 1990; and Swieringa and Weick, 1987).

A review of the literature indicates that the findings of previous studies are inconsistent and thus it is difficult to integrate their results or to draw consistent conclusions about the issues. For example, while Gordon and Narayanan (1 984) found no relationship between the usefulness ofaccounting information and organization structure, this finding was inconsistent with the Chenhall and Morris (1986) study. A possible explanation for the inconsistency in the results is the level of managerial positions held by participants in these two studies. In the Gordon and Narayanan (GN) study, the participants were the Company President, Vice-president, or Controller of Finance, executives who would assume a high degree of authority and responsibility in their organization’s formal hierarchy. Consequently, there might not have been enough variation in the participants’ perception of the organic/mechanistic character of their organization’s structure which would explain the lack of a perceived association between structure and usefulness of accounting systems in the study. O n the other hand, the participants in Chenhall and Morris (CM) study held ‘middle and upper level’ positions (i.e., relatively lower level positions in their organization’s hierarchy

The authors are respectively, Lecturer at the University of Western Sydney; and Professor of Accounting at Grifith University. They acknowledge the helpful comments by A. Dunk, M. Aiken, R. Ma, R. Chenhall, L. Gordon and E. Iselin, on earlier drafts of this paper. Comments by the participants of the seminars on the paper at the 1994 British Accounting Association Conference, the 1994 European Accounting Association Conference, the University of Western Sydney, Grifith University and La Trobe University are acknowledged. They also acknowledge the helpful comments of the editor and two anonymous referees.

Address for correspoadene: Lokrnan Mia, Professor of Accounting, Faculty of Business and Hotel Management, Grifith University Gold Coast Campus, PMB 50, Cold Coast Mail Centre, Queensland 4217, Australia.

OBlackwell Publishers Ltd. 1996, 108 Cowley Road, Oxford OX4 IJF, UK and 238 Main Street, Cambridge, MA 02142, USA. 173

174 MIAH AND MIA

compared with those in GN’s study). These participants were in charge of subunits within their organizations. Because of the relatively lower level positions held by these participants, their perception of the level of authority and responsibility delegated by top management to them (the managers) might have varied from one another. Possible reasons for this variation in the managers’ perception are characteristics of the local environment they face, the size of the departmentlsubunit they manage, or their personality characteristics. The expected variation in these managers’ perception of their organization’s structure (centralization/decentralization) may explain why C M found the relationship between structure and usefulness of accounting systems in their study. Explanations for the association between structure and usefulness of accounting systems in organizations are provided in both GN’s and CM’s study.

Based on CM’s results, we predict that there is a positive and significant association between organization structure and perceived usefulness of accounting systems in the case of managers holding relatively lower level positions in the organization hierarchy. One of the objectives of the current study was to empirically test this proposition using a sample of department managers. This was done by testing the association between decentralization (the delegation of authority and responsibility) by a government department head office to its district offices and the managerial use of accounting control systems (ACS) in those district offices (see hypothesis 1 in the next section). In the government departments examined, district offices are the lowest managerial level in the formal organization structure. We consider that managers’ use of the ACS indicates the usefulness ofsuch information to them.

Another indication from the literature review is that previous studies on organization theory and on the design and use of accounting systems have ignored the issue of organizational performance. Since improving organizational performance is one of the ultimate objectives of management controls, ignoring this outcome (dependent) variable in previous research is a grievous omission in the research. The three studies most relevant to the current study are GN, CM and Mia and Chenhall (1994). None of these studies has looked into organizational performance. The current study attempts to address this issue by incorporating organizational performance in the model (Figure 1 ) . This was done by investigating (a) the relationship between the use of ACS in district offices and district office performance, and (b) the relationship between decentralization and district office performance. For purposes of this study, district office performance was defined in terms of the extent to which the goals set for the offices were achieved. As indicated in the abstract, managers’ perception of their district office’s (unit’s) performance was used to assess the performance.

The study was conducted in five departments of the Central Government in New Zealand. These departments provide services like education, welfare, law and order, health, and transport. The extant literature suggests that

Q Blackwell Publishers Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS: NEW ZEALAND 175

relevant previous studies concerning design and use of accounting systems have been conducted in profit-oriented private manufacturing firms. Mia and Goyal (1991) argue that generalization of results reported in studies on private profit-oriented organizations to not-for-profit organizations such as government departments is problematic for a number of reasons. Three of these reasons relevant to the current study are given below.

First, government organizations aim to maximise benefits to the public and minimise costs while private commercial organizations aim to maximise profit which may or may not involve cost minimization. For example, Martin ( 1 994) argues that government or public sector organizations are owned by the taxpayers and unlike private sector organizations, which have in common the profit motive, the objectives of these enterprises are generally to efficiently and effectively provide services that, for a variety of reasons, would not be provided at an acceptable price, quantity or quality without government intervention. Examples of government organizations’ objectives include equity, growth, stability, social welfare, and educations. Martin defines efficiency as the ability to achieve a given output or objective with minimum input (cost). Following Martin, this study argues that government organizations are likely to emphasize cost control. For cost control, managers usually need information (such as comparison of actual costs with budgets or standards) which could be provided from sources mainly internal to the organization. O n the contrary, profit maximisation involves sales/revenue planning (with or without cost control) which requires information from sources mainly external to the organization (see also GN, and CM). Consequently, the usefulness of accounting information as perceived by managers in private commercial organizations may be different from the usefulness of such information as perceived by managers in government organizations.

Second, the relatively more extensive public scrutiny, which is generally imposed on government organizations, requires a greater compliance by these organizations of predetermined rules and regulations in record keeping for costs and expenses. This may encourage managers in government organizations to view internal and or historical information differently from managers in private organizations.

Third, government organizations generally operate in a monopolistic or quasi monopolistic market. Previous research (see Khandwalla, 1972) suggests that the level of market competition is a determining factor of managers’ use of information for decision making.

As mentioned earlier, this study was conducted in five New Zealand Central Government Departments which are large and complex organizations. These departments were created by the government primarily to facilitate public administration and to provide services to the public as defined in the Public Finance Act 1989 and the State Sector Act 1988. The underlying reason for choosing to conduct this study in the Government departments is that over

0 Blackwell Publishen Ltd 1996

176 MIAH AND MIA

recent years the New Zealand Government has taken several steps to improve performance in public sector entities. These steps include inter aha the reduction of centralized control through delegation of operational and financial responsibility to district office managers (The Treasury, 1982; and State Sector Act 1988). The lack of research on management controls in not- for-profit organizations prompted Wortman ( 1979) to identify such organizations as important areas for potential research.

THEORY DEVELOPMENT

Decentralization, Managerial Use of ACS and District 0 f f i c e Performance

The extent to which decision making in organizations should be delegated to lower management levels (an issue of organization structure) has received a great deal of attention in organization research. It has been shown that the amount of delegation depends on a variety of contextual and environmental variables (Pugh et al, 1969; and Negandhi and Reimann, 1973). For purposes of this study, delegation refers to the extent to which higher management allows lower management to make decisions independently (Heller and Yukl, 1969). Delegation provides lower management (subordinates) with authority in decision making along with responsibility for their actions. Authority is the discretionary right to carry out assignments, while responsibility is the obligation to accomplish such assignments (Hellriegel and Slocum, 1978).

The importance of decentralization as an element of the formal structural arrangements has long been stressed in the organization and management literature. Thompson ( 1967) outlined the need for ‘localised’ (decentralized) subunits as a structural response to deal with unpredictable environments. Gordon and Miller (1976) suggest that with the increase in administrative complexity, tasks and responsibilities should be delegated to lower levels of management to ease the burden of decision making at higher management levels. In a situation of decentralized decision making, subordinate managers assume the role of making decisions and implementing them (rather than just doing the latter) and they become responsible for the operations of their subunits. Such a situation leads to a greater use of information by subunit managers in decision making. Consequently, there is a greater need for the use of ACS. For example, Cushing and Romney (1994) argue that an organization’s choice of structure (e.g., degree of decentralization) has significant implications for accounting information systems as the systems must assist unit managers in making decisions and taking actions to achieve their unit goals (see also Gul et al., 1995; Emmanuel et al., 1990; and Caplan and Atkinson, 1989).

Decentralization is likely to accentuate the need for the use of ACS in another way. The greater the amount of authority and responsibility

0 Blackwell Publisherr Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS NEW ZEALAND 177

delegated by the top management to lower levels of management, the greater is the need for the control and evaluation of the lower management’s financial activities. For improved performance to result from the decentralization of operating decision making, the organization must also adopt the requisite controls (Hill, 1988). Bruns and Waterhouse ( 1975) suggest that organizations which delegate decision making authority develop means for maintaining control by utilizing procedures for measuring role performance.

Increased decentralization is observed in the New Zealand Government Departments in recent years. Under the State Sector Act 1988, a Government Department is given effectively the same authority to manage its affairs as ifit were aprivatesector organization. As McCulloch and Ball ( 1992, p. 9) observe:

Previously, departments were subject to detailed cash constraints and other controls. As a consequence ofchief executives becoming explicitly accountable for departments’ performance, they are now given much greater discretion over the acquisition, utilisation, disposal and mix of resources that they use to achieve their outputs. In addition, two key resources previously managed centrally, personnel and cash, have been put under the control ofchiefexecutives.The State Sector Act 1988 effectively gave chief executives the same powers ofemploying staff as in the private sector.

Along with the increased authority delegated to the department’s chief executives, they are also made more responsible for department performance. For example, the Public Finance Act 1989 requires each department to submit forecast financial statements stating expected financial position, expected cash flows, projected service performance, and expected revenue. Departments are also required to submit ex post financial statements including audited financial position, and cash flows, and a statement of production of goods and services that they had agreed to produce (see McCulloch and Ball, 1992 for details). The district offices, in turn, are required to submit similar statements and forecasts to the department Head Office (HO). We argue that the preparation of the above mentioned statements and forecasts in the district offices results in an increased managerial use of ACS in those offices. This relationship is named P21 in Figure 1. Hypothesis 1 summarizes the above discussions.

HI: An increased level of decentralization of decision making among district offices leads to a greater use of ACS in those offices.

The use of ACS may facilitate planning and control of organizational activities and thereby organizational performance. The recent literature on accounting information systems places increasing emphasis on the use of accounting information to improve the accuracy of organizational decision making. For example, Martin ( 1 994) suggests that the purpose of accounting information is to facilitate informed judgements and decisions by users of the information. Macintosh (1994) suggests that accounting systems are a very important part of the entire spectrum ofcontrol mechanisms used to motivate,

0 Bladwdl Publishen Ltd 1996

178 MIAH AND MIA

measure, and sanction the actions of managers and employees in the organizations. Similarly, Miah and Goyal (1990) argue that an effective accounting system is a pre-requisite to improved performance. They further argue that failure to use necessary accounting information contributes to ineffective resource management and a gradual decline in organizational performance (see also, Cushing and Romney, 1994). This implies that a greater managerial use of ACS may lead to improvements in organizational performance by facilitating better decision making and control of financial activities by managers.

In the public sector context, the delegation ofauthority and responsibility by the HO of a government department to its district offices can have two consequences. First, due to the delegation the district office managers are required to make an increasing number of operating decisions, thus becoming more accountable to the HO for their district office performance (henceforth, performance). This situation requires an increased amount of information for decision making and control at the district office level which results in an increased use of ACS. Second, the increased use of ACS enables the district office managers to make better decisions and control operations more effectively, therefore, to improve performance. These consequences may be illustrated by the following example. Consider that the Department of Road Transport wants to reduce accidents on roads, and asks its district offices to come up with a plan to achieve the objectives in their respective localities. Depending on the causes for road accidents in areas under respective district offices, the plan may involve implementing all or a combination of steps, such as road patrols, vehicle safety checks, road maintenance, speed control, and breath tests. Since the causes ofaccidents may bedifferent in different localities, relevant district offices rather than the Department HO are in a better position to identify thecauses ofaccidents and effectively deal withsuchcauses. This will require the respective district offices to develop different plans taking into account the estimated costs and expected success (benefits) in dealing with the relevant causes. The use of ACS can assist the district office managers in estimating costs and probability of success of specific plans and selecting the best alternative in each case, thus improving performance (see Figure 1, relationship P32). The above discussion leads to the formulation ofhypothesis 2.

H2: The greater the use of ACS in district offices the better is the performance.

DECENTRALIZATION AND PERFORMANCE

Williamson ( 1970 and 1975)suggests that decentralization of decision making has far-reaching performance implications for the organization as a whole. Recently CM argue that decentralization of decision making among managers is aimed at improving their performance by encouraging them to

0 Blackwell Publishen Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS NEW ZEALAND 179

develop distinctive competences for dealing with uncertain local conditions. Mukhi et al. (1988) suggest that decentralization allows managers to effectively deal with events, act without delay and improve quality ofdecisions leading to better performance. Davis and Newstrom (1985) also support the role of decentralization in improving managerial performance. In a decentralized decision making environment, HO can hold managers responsible for the performance of operations under their control. Managers in such environments are likely to have a greater incentive to improve efficiency because they can develop their own goals and management styles to deal with local needs. In the case of government departments, an appropriate degree of decentralization of district offices is likely to enable district office managers to respond-timely to local situations, thereby making the process of government adaptable and responsive to changes in community needs. Williamson (as stated by Hill, 1988) further argues that the operating autonomy given to managers creates an internal organizational environment which is conducive to fostering cost minimizing behaviour. In government organizations, cost minimizing behaviour is particularly important for the cost effective provision of services to the public.

Based on the above discussion, we argue that performance is likely to improve with increased decentralization of decision making at the district office level. Figure 1 presents this relationship as P31. This argument is consistent with Hill’s ( 1988) suggestion that decentralization leads to improved performance in large complex organizations. This argument leads to the formulation of hypothesis 3.

HS: An increased decentralization of decision making at district office level is associated with improved performance in those ofices.

The discussions leading to hypotheses 1 and 2 can be used to argue that the use of ACS plays an intervening role in the relationship between decentralization and performance. The use of ACS plays an intervening role in the sense that an increased decentralization at district office level is associated with a greater use of ACS which, in turn, is associated with improved performance. In combination, these relationships illustrated in Figure 1 are expected to explain at least partly the bi-variate relationship between decentralization and performance (see Chenhall and Brownell, 1988). For purposes of this study, the intervening role of the use of ACS is supported if both hypotheses 1 and 2 are significant and in the positive direction, therefore, explaining at least partly the relationship between decentralization and performance.

METHOD

Data for the study were collected from the district offices offive New Zealand Central Government departments located throughout the country. These

8 Blackwell Publishers Ltd 1996

180 MIAH AND MIA

departments provide services like education, welfare, law and order, health, and transport. The data were collected from 95 district office managers. For this purpose, the study used a mailed questionnaire which was completed by the managers. These district offices were selected a t random from a list of all district ofices of the five departments participating in the study. The questionnaire and a self-addressed stamped envelope were attached to a cover letter explaining the purpose of the study and assuring confidentiality of the information provided. The letter was addressed to each of the participants (district office managers) who were in charge of the district offices. These managers are the ‘front-line’ officers (lowest managerial level) who interpret and enforce various government rules and policies and deal with local problems (complex problems, however, are referred to the regional or head office for consideration and action). Fifty nine useable questionnaires were returned resulting in a response rate of 62 per cent.

Measurement of Variables

The questionnaire contained three sets of items assessing the extent of decentralization, the extent of managerial use of ACS, and performance respectively. To ensure clarity and relevance of the measures to the government departments, the qucstionnaire was pre-tested with five district office mangers (one from each of the five departments selected for the study) located in a large city. A personal interview with each of these live managers (who are not included in the final sample of 59) indicated that the government had an accounting control system in place in each of the live departments.

Decentralization

The extent of decentralization of decision making at the district office level was assessed by the district office mangers using a five items instrument adapted from GN. An example of the items is: ‘To what extent has your office got authority and responsibility for making decision on financial matters?’. Appendix A presents the items in the measure. The measure uses a five point Likert scale ranging from 1 (almost no delegation) to 5 (complete delegation). A factor analysis of the items in the measure produced a single factor which means the measure is unidimensional. Appendix A presents the factor loadings, the eigenvalue and the percentage of the variance explained. Also, a Cronbach (1951) alpha of 0.79 indicated a satisfactory internal validity of the measure. The ratings on these items are averaged to arrive at a single index for decentralization.

Managerial Use of Accounting Control Systems

The extent ofthe use ofACS in district offices was assessed by the district office managers using a six items instrument adapted from Khandwalla (1972) and

8 Blackwell Publirhcn Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS: NEW ZEALAND 181

later used by McPherson (1986) in studying the control system of New Zealand Inland Revenue Department district offices. An example of items in the measure is the extent to which sampling or other statistical techniques are used in controlling quality of operations. Appendix B presents the specific items in the measure. The measure uses a five point Likert scale ranging from 1 (never used) to 5 (always used). The interviews with the five managers in the pilot study indicated that the specific items used in the measure were subject to the control of the district office managers. The manager’s ratings on these items were averaged to arrive at a single index for ACS use. A factor analysis of the items in the measure produced a single factor which means the measure is unidimensional. Appendix B presents the factor loadings, the eigenvalue and the percentage of the variance explained. Again, a Cronbach alpha of 0.75 indicated a satisfactory internal reliability of the measure.

District Office Performance

The district office managers were asked to indicate, on a 9 point Likert scale ranging from 1 (not at all satisfactory) to 9 (outstanding), the recent overall performance of their office in view of the set goals.

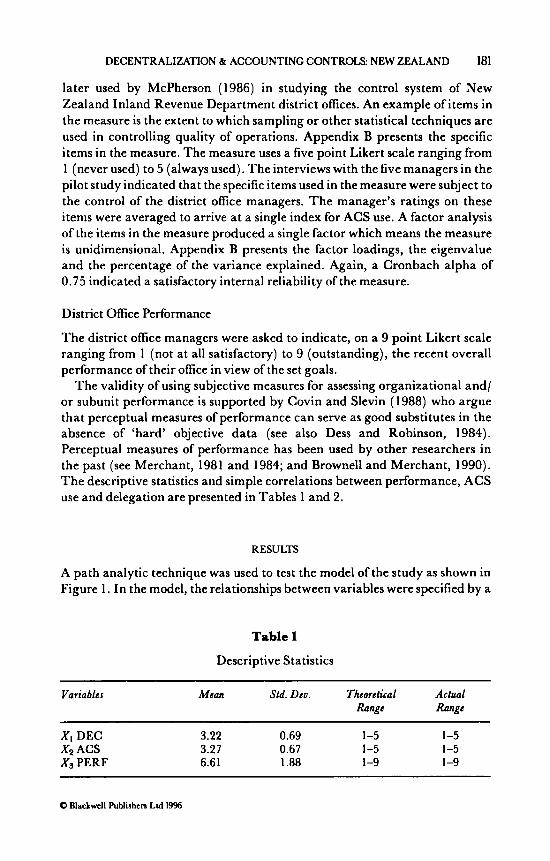

The validity of using subjective measures for assessing organizational and/ or subunit performance is supported by Covin and Slevin (1988) who argue that perceptual measures of performance can serve as good substitutes in the absence of ‘hard’ objective data (see also Dess and Robinson, 1984). Perceptual measures of performance has been used by other researchers in the past (see Merchant, 1981 and 1984; and Brownell and Merchant, 1990). The descriptive statistics and simple correlations between performance, ACS use and delegation are presented in Tables 1 and 2.

RESULTS

A path analytic technique was used to test the model of the study as shown in Figure 1. In the model, the relationships between variables were specified by a

Table 1

Descriptive Statistics

Variables Mean Std. Dev. Theoretical Actual Range Range

Xi DEC Xz ACS Xs PERF

3.22 0.69 1-5 1-5 3.27 0.67 1-5 1-5 6.61 1.88 1-9 1 -9

0 Blackwell Publishen Ltd 1996

182 MIAH AND MIA

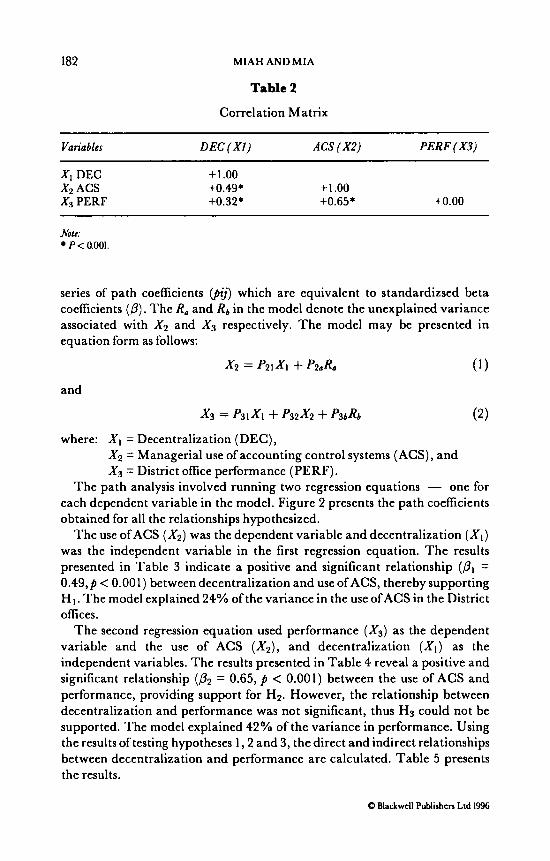

Table 2

Correlation Matrix

Variables DEC(X1) ACS ( X 2 ) PERF ( X 3 )

Xi DEC Xz ACS X , PERF

+ 1 .oo +0.49* + 1 .oo +0.32* +0.65* +o.oo

Note: P < 0.001.

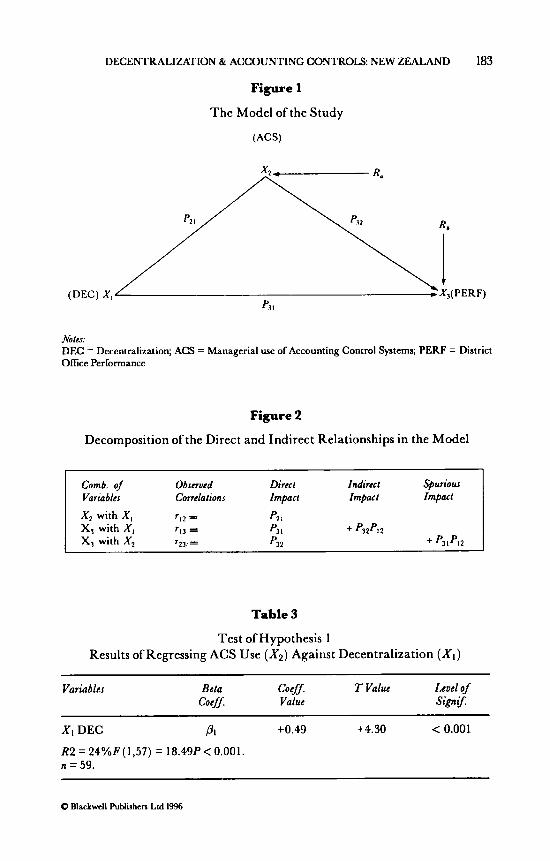

series of path coefficients (pij) which are equivalent to standardizsed beta coefficients (p) . The R, and Rb in the model denote the unexplained variance associated with X2 and X , respectively. The model may be presented in equation form as follows:

X2 = p21X1 + P 2 A (1)

(2)

and

x3 = ~ I X I + p32x2 + hbRb

X , = Managerial use of accounting control systems (ACS), and X 3 = District office performance (PERF).

The path analysis involved running two regression equations - one for each dependent variable in the model. Figure 2 presents the path coefficients obtained for all the relationships hypothesized.

The use ofACS ( X 2 ) was the dependent variable and decentralization ( X I ) was the independent variable in the first regression equation. The results presented in Table 3 indicate a positive and significant relationship (PI = 0.49,p < 0.001) between decentralization and use of ACS, thereby supporting H I . The model explained 24% of the variance in the use ofACS in the District offices.

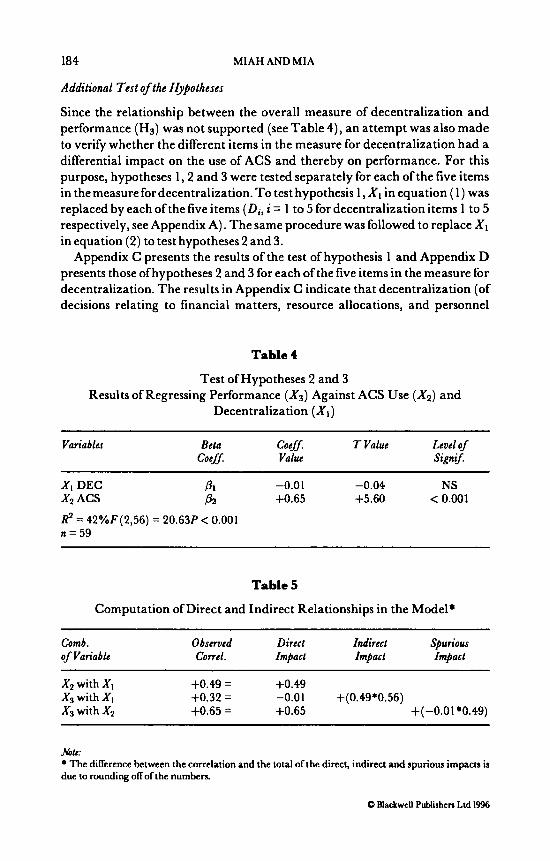

The second regression equation used performance ( X s ) as the dependent variable and the use of ACS (&), and decentralization ( X I ) as the independent variables. The results presented in Table 4 reveal a positive and significant relationship ( P 2 = 0.65, p < 0.001) between the use of ACS and performance, providing support for H 2 . However, the relationship between decentralization and performance was not significant, thus H3 could not be supported. The model explained 42% of the variance in performance. Using the results of testing hypotheses 1,2 and 3, the direct and indirect relationships between decentralization and performance are calculated. Table 5 presents the results.

where: XI = Decentralization (DEC),

0 Blackwell Publishen Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS NEW ZEALAND

Figure 1

The Model of the Study

183

(ACS)

Notes: DEC = Decentralization; ACS = Managerial use of Accounting Control Systems; PERF = District Office Performance

Figure 2

Decomposition of the Direct and Indirect Relationships in the Model

Comb. o j Observed Direct Indirect spuriour

X 2 with X , r12 = p2 I

Variables Correlations Impact Impact Impact

X3 with X , r13 = ‘3 I -+ p32p12 X7 with X , 7 7 7 . = P77 4- p31p12

Table 3

Test of Hypothesis 1 Results of Regressing ACS Use (X , ) Against Decentralization ( X I )

Variables Beta cog-.- T Value Level OJ cot fJ Value Sign$

~

XI DEC P1 +0.49 +4.30 < 0.001 R2 = 24%F(1,57) = 18.49P< 0,001 n = 59.

Q Blackwell Publishers Ltd 1996

184 MIAH AND MIA

Additional Test of the Hypotheses

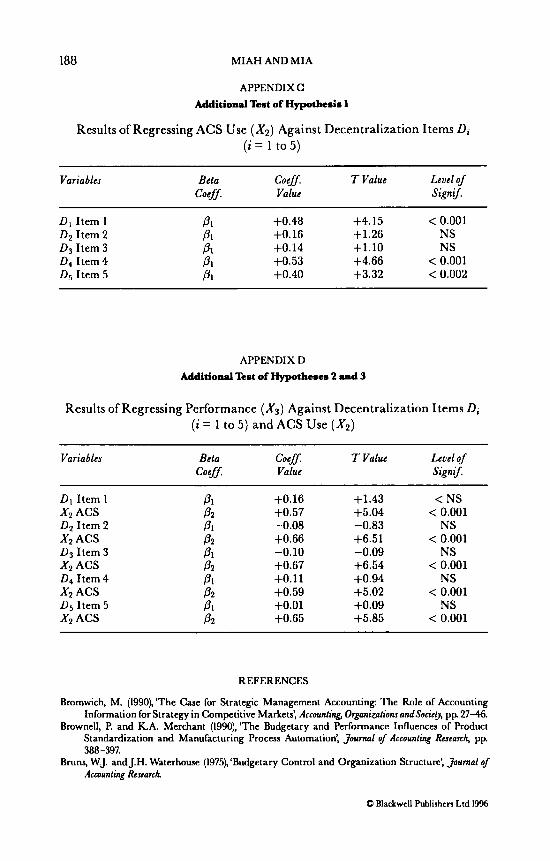

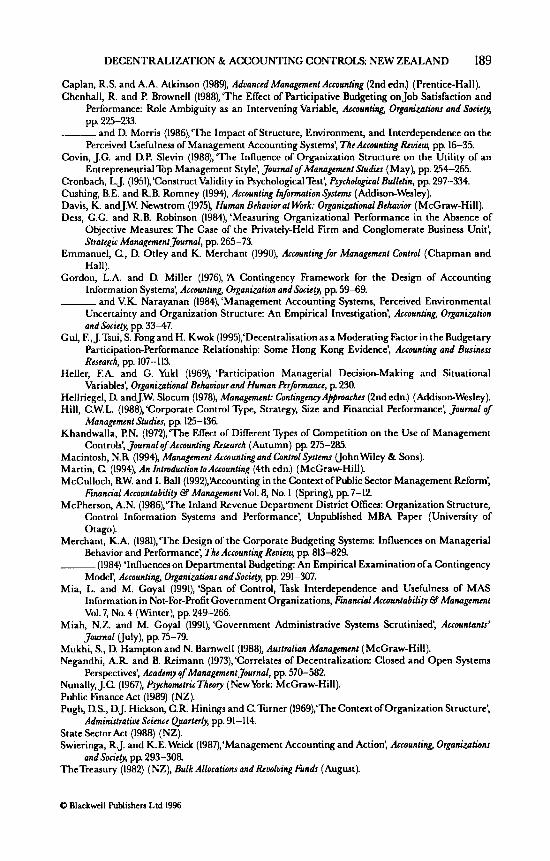

Since the relationship between the overall measure of decentralization and performance (H3) was not supported (see Table 4), an attempt was also made to verify whether the different items in the measure for decentralization had a differential impact on the use of ACS and thereby on performance. For this purpose, hypotheses 1 , 2 and 3 were tested separately for each of the five items in the measure for decentralization. To test hypothesis 1 , X I in equation ( 1) was replaced by each of the five items (Di, i = 1 to 5 for decentralization items 1 to 5 respectively, see Appendix A). The same procedure was followed to replace X I in equation (2) to test hypotheses 2 and 3.

Appendix C presents the results of the test of hypothesis 1 and Appendix D presents those ofhypotheses 2 and 3 for each of the five items in the measure for decentralization. The results in Appendix C indicate that decentralization (of decisions relating to financial matters, resource allocations, and personnel

Table 4

Test of Hypotheses 2 and 3 Results of Regressing Performance ( X , ) Against ACS Use (&) and

Decentralization ( X I )

Variables Beta coeff. I Value Level of cot fJ Value Sign$

XI DEC 81 -0.01 -0.04 NS

R2 = 42%F(2,56) = 20.63P < 0.001 n=59

X2 ACS Pz +0.65 +5.60 < 0.001

Table 5

Computation of Direct and Indirect Relationships in the Model*

Comb. Observed Direct Indirect spuriour of Variable COrrLl. Impact Impact Impact

X2 with XI +0.49 = +0.49 X3 with XI +0.32 = -0.01 +(0.49*0.56) X3 with X2 +0.65 = +0.65 +(-0.01'0.49)

Note: The diKerence between the correlation and the total of the direct, indirect and spurious irnpacu is

due to rounding off of the numbers.

0 Blackwell Publishers Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS: NEW ZEALAND 185

management at the district office level) was positively associated with the use of ACS in those offices.

The results presented in Appendix D indicate that none of the five items in the decentralization measure had a direct relationship with performance. Thus, the results presented in Table 4 may be considered stable.

DISCUSSION, LIMITATIONS AND CONCLUSIONS

The results of the study indicate that the use of ACS acts as a mediator in the relationship between decentralization of decision making and performance of government department district offices. The results reveal that an increased level of decentralization is associated with an increased use of ACS which, in turn, is associated with improved performance in the district offices. However, no direct association could be found between decentralization and the district office performance. An explanation for the above results is that simply more decentralization of decision making at lower level management does not improve performance of the management. For this purpose, the decentralization may be complemented by a suitable accounting control system. This is because, in a decentralized decision making environment, managers need adequate information, rules and procedures for running their operations. Decentralization of decision making a t the district office level without a provision for adequate information, rules and procedures does not enable the district offices to carry out their duties and responsibilities efficiently. The ACS in place provide necessary information, prescribed rules and procedures. Thus, the relationship between decentralization and the district office performance exists via the use of the accounting control systems. None of the previous studies (e.g. GN and CM) investigated this relationship.

This study reconciles the results reported by GN and CM. While GN could not find a relationship between structure and usefulness of accounting information, CM did. The results ofthe current study are consistent with those reported by CM and support the argument made earlier in the paper. The argument is that at a lower level of formal organization hierarchy, decentralization of decision making is likely to be associated with the use (therefore, usefulness) of accounting control systems. The current study supports the argument empirically.

There are at least four limitations to the study. First, out ofvarious Central Government Departments in New Zealand, only five departments participated in the study. Therefore, caution is required in generalizing the results to other departments. Second, the relationships investigated in this study may be influenced by other factors such as district office size, personality of district ofice managers, leadership style of departmental heads or other senior executives, and superior-subordinate relationships within the

0 Blackwell Publishen Ltd 1996

186 MIAH AND MIA

department. Third, this study considers the influence of decentralization of decision making on use of accounting control systems within the government departments in the sample. There are other important factors such as change in government funding, legislative requirements, and introduction of competition may also have impact on the use of accounting control systems in the departments. Future research would benefit from incorporating these factors into research models investigating use of accounting control systems in government organizations. Fourth, all the variables in the study are assessed subjectively using perception of the district office managers. Incorporating an objective measure (if available) along with the subjective measure for some of the variables such as the district office performance would have allowed a comparison between the two measures in the study. Note that there was no objective measure of performance available for the district offices in the study at the time of the study.

Implications for Public Policy

Despite the above limitations, the results have at least the following two implications for the development and implementation of public policies. First, the accounting control system can facilitate improvement in performance at the lower level of government organizations. The results reveal that decentralization of decision making at the government district office level coupled with an accounting control system facilitates improvements in the district office performance. This relationship is evident particularly in the case of decentralization of decisions relating to financial matters, allocation of resources and personnel matters at the district office level. We argue that the district office managers’ use of an accounting control system facilitates the efficiency that results from their improved decisions on these matters. Thus, it follows that the accounting control system can facilitate success of the government’s policy of decentralizing public administration at the lower organizational level.

Second, based on the results we also argue that an accounting control system (by providing necessary information) would assist the managers to make appropriate decisions without waiting for clarification or explanations from the head office. This would (i) reduce the time taken in decision making at the district office level and (ii) reduce public expenditures (such as telephone, transportation and postage). Moreover, an appropriate accounting control system in place would promote an effective flow of information between the head office and district offices as well as among district offices. Such an information flow is likely to help in the formulation of departmental budgets, taking into account local needs and aspirations and, thereby, resulting in proper utilization and control of public resources. I t follows that the New Zealand Government, as part of its decentralization policy, ought to ensure that every department has an appropriate

0 Blackwell Publishen Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS: NEW ZEALAND 187

accounting control system in place to assist the district office managers’ decision making.

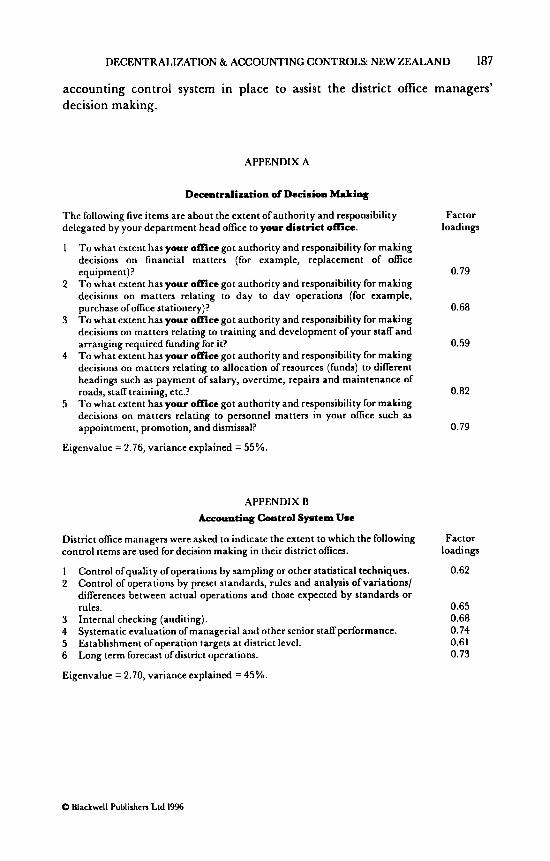

APPENDIX A

Decentralization of Decision Making

The following five items are about the extent ofauthority and responsibility delegated by your department head office to your district office.

I

Factor loadings

T o what extent has your office got authority and responsibility for making decisions on financial matters (for example, replacement of office equipment)? 0.79 T o what extent has your office got authority and responsibility for making decisions on matters relating to day to day operations (for example, purchase of office stationery)? 0.68 To what extent has your office got authority and responsibility for making decisions on matters relating to training and development of your staff and arranging required funding for it? T o what extent has your office got authority and responsibility for making decisions on matters relating to allocation of resources (funds) to different headings such as payment of salary, overtime, repairs and maintenance of roads, staff training, etc.? 0.82 To what extent has your office got authority and responsibility for making decisions on matters relating to personnel matters in your office such as appointment, promotion, and dismissal? 0.79

2

3

0.59 4

5

Eigenvalue = 2.76, variance explained = 55%.

APPENDIX B Amounting Control System Use

District office managers were asked to indicate the extent to which the following control items are used for decision making in their district oflices.

1 2

Control ofquality ofoperations by sampling or other statistical techniques. Control of operations by preset standards, rules and analysis ofvariationsl differences between actual operations and those expected by standards or rules.

3 Internal checking (auditing). 4 Systematic evaluation of managerial and other senior staff performance. 5 Establishment of operation targets a t district level. 6 Long term forecast ofdistrict operations.

Eigenvalue = 2.70, variance explained = 45%.

Factor loadings

0.62

0.65 0.68 0.74 0.61 0.73

Q Blackwcll Publishen Ltd 1996

188 MIAH AND MIA

APPENDIXC Additional Test of Hypothesis 1

Results of Regressing ACS Use ( X , ) Against Decentralization Items D, (i = 1 to 5)

Variables Beta COG fJ 7 Value Level of COdJ Value Sign$

D, Item 1 Dz Item 2 D3 Item 3 D4 I tern 4 D5 Item 5

P1 +0.48 +4.15 < 0.001

P1 +0.53 +4.66 < 0.001 P I +0.40 +3.32 < 0.002

P1 +0.16 +1.26 NS 81 +0.14 +1.10 NS

APPENDIX D Mditionnl Test of Hypotheses 2 md 3

Results of Regressing Performance ( X , ) Against Decentralization Items D , (I’ = 1 to 5) and ACS Use ( X , )

Variables Beta COG fJ 7 Value Level 0 f COG fJ Value Sign$

DI Item 1

0 2 Item 2

03 Item 3

D4 Item 4

0 5 Item 5

Xz ACS

Xz ACS

Xz ACS

Xz ACS

Xz ACS

P I

P2 P I

P2 P1 Pz P1 P2 P1 Pz

+0.16 +0.57 -0.08 +0.66 -0.10 +0.67 +o. 11 +0.59 +0.01 +0.65

+1.43 +5.04 -0.83 +6.51 -0.09 +6.54 +0.94 +5.02 +0.09 +5.85

< NS < 0.001

NS < 0.001

NS < 0.001

NS < 0.001

NS < 0.001

REFERENCES

Bmmwich, M. (1990), ‘The Case for Strategic Management Accounting: The Role of Accounting Information for Strategy in Competitive Markets’, Accounfiq, 0rganiwfion.s andSociep, pp 27-46.

Brownell, P. and ICA. Merchant (1990), ‘The Budgetary and Performance Influences of Product Standardization and Manufacturing Process Automation’, journal of Accounfing Research, pp 388-397.

Bruns, W.J. andJ.H. Waterhouse (1975), ‘Budgetary Control and Organization Structure’, journal of Accounting Research.

8 Blackwell Publishers Ltd 1996

DECENTRALIZATION & ACCOUNTING CONTROLS NEW ZEALAND 189

Caplan, R.S. and A.A. Atkinson (1989), Aduanccd Managcmcnf Accounfing (2nd edn.) (Pztntice-Hall). Chenhall, R. and P. Bmwnell (1988),‘The Effect of Participative Budgeting on Job Satisfaction and

Performance: Role Ambiguity as an Intervening Variable, Accounting, Organizafionr and Socic& p p 225-233.

-and D. Morris (1986),‘The Impact of Structure, Environment, and Interdependence on the Perceived Usefulness of Management Accounting Systems’, The Accounting Reuicq p p 16-35.

Covin, J.G. and D.P. Slevin (1988), ‘The Influence of Organization Structure on the Utility of an EntrepreneurialTop Management Style’, 30urn0l ofManagcmcnf studies (May), pp. 254-265.

Cronbach, L.J. (1951),‘Construct Validity in PsychologicalTest’, fychological Bullcfin, p p 297-334. Cushing, B.E. and RB. Romney (1994), Accounfing InJormafion @sfems (Addison-Wesley). Davis, K. andJ.W. Newstrom (1975), Human Echauior af Work: Organizational Behavior (McGraw-Hill). Dess, G.G. and R.B. Robinson (1984), ‘Measuring Organizational Performance in the Absence of

Objective Measures: The Case of the Privately-Held Firm and Conglomerate Business Unit’, Sfratcgic Managnnmfjournal, pp. 265-73.

Emmanuel, C., D. Otley and K. Merchant (1990), Accounfing for Managcmcnf Confrol (Chapman and Hall).

Gordon, L.A. and D. Miller (1976), A Contingency Framework for the Design of Accounting Information Systems’, Accounfing, O r g a n i d o n and .Socie& p p 59-69. - and V.K. Narayanan (1984), ‘Management Accounting Systems, Perceived Environmental

Uncertainty and Organization Structure: An Empirical Investigation’, Accounfing, O r g a n b f i o n and SocicQ, pp. 3347.

Gul, F., J.Tsui, S. Fongand H. Kwok (1995),‘Decentralisation as a Moderating Factor in the Budgetary Participation-Performance Relationship: Some Hong Kong Evidence’, Accounting and Burinerr Research, pp. 107-113.

Heller, F.A. and G. Yukl (1969), ‘Participation Managerial Decision-Making and Situational Variables’, Organizational Behauiour and Human PcrJormancc, p. 230.

Hellriegel, D. andJ.W. Slocum (1978), Managcmcnf: Confingcncy Ajpmaches (2nd edn.) (Addison-Wesley). Hill, C.W.L. (1988), ‘Corporate Control Type, Strategy, Size and Financial Performance’, Journal of

Monagcmnf Sfudics, p p 125-136. Khandwalla, P.N. (1972),‘The Effect of DiKerent Types of Competition on the Use of Management

Controls’, journal ofAccounfing &search (Autumn) p p 275-285. Macintosh, N.B. (1994), Managcmcnf Acmunfing and Confml Sysfcms (John Wiley & Sons). Martin, C. (1994), An Infmducfion f o Accounfing (4th edn.) (McGraw-Hill). McCulloch, B.W. and I. Ball (1992),‘Accounting in the Context of Public Sector Management Reform’,

financial Accounfabilily B Managcmcnf Vol. 8, No. 1 (Spring), p p 7-12. McPherson, A.N. (1986),‘The Inland Revenue Department District Offices: Organization Structure,

Control Information Systems and Performance’, Unpublished MBA Paper (University of Otago).

Merchant, K.A. (1981),‘The Design of the Corporate Budgeting Systems: Influences on Managerial Behavior and Performance’, The Accounfing Rcuiny p p 813-829. - (1984) ‘Influences on Departmental Budgeting: An Empirical Examination ofa Contingency

Model’, Accounfing, Organizafions andSociely, pp. 291-307. Mia, L. and M. Goyal (1991), ‘Span of Control, Task Interdependence and Usefulness of MAS

Information in Not-For-Profit Government Organizations, FEnanticrl Accounfabilily B Managcmcnf Vol. 7, No. 4 (Winter), pp. 249-266.

Miah, N.Z. and M. Goyal (1991), ‘Government Administrative Systems Scrutinised’, Accounfanfs’ 30urn0l (July), pp. 75-79.

Mukhi, S., D. Hampton and N. Barnwell (1988), Ausfralian Managmunf (McCraw-Hill). Negandhi, A.R and B. Reimann (1973), ‘Correlates of Decentralization: Closed and Open Systems

Nunally, J.C. (1967), PsyhomcfricThcory (NewYork McGraw-Hill). Public Finance Act (1989) (NZ). Pugh, D.S., D.J. Hickson, C.R. Hinings and C.Turner (1969);The Context oforganization Structure’,

State Sector Act (1988) (NZ). Swieringa, R.J. and KE. Weick (1987),‘Management Accounting and Action’, Accounfing, Organizafionr

andSocie!y, pp 293-308. TheTreasury (1982) (NZ), Bulk Allocafions and huoluing Funk (August).

Perspectives’, Academy of Managcmcnfjournal, pp. 570-582.

Adminisfratiuc Science Quarfnb, pp. 91-114.

8 Blackwcll Publishers Ltd 1996

190 MIAH AND MIA

Thompson, J.D. (1970), Organbfionr in Action (McCraw-Hill). Williamson, O.E. (1970), Corporate Control andEusiness Eehauiour (Englewood Cliffs, NJ, Prentice-Hall). - (1975), Markets and Hicrarchies: Analynj and Anfifrusf Implications (New York, Free Press). Wortman, M.S. (1979), ‘Strategic Management: Not-for-Profit Organizations, in D.E. Schendel and

C.W. Hofer (eds.), Sfrafcgic Managcmcnt (Little, Brown and Company), p p 353-373.

8 Blackwell Publishen Ltd 1996