Embed Size (px)

Citation preview

AKUNTANSI MANAJEMEN

SESI 7: Analisis Cost Volume Profit (CVP) *

Achmad Zaky,MSA.,Ak.,SAS.,CMA.,CA

* Slide ini di sadur dari Slide Resmi Hansen-Mowen 8Th Edition

2

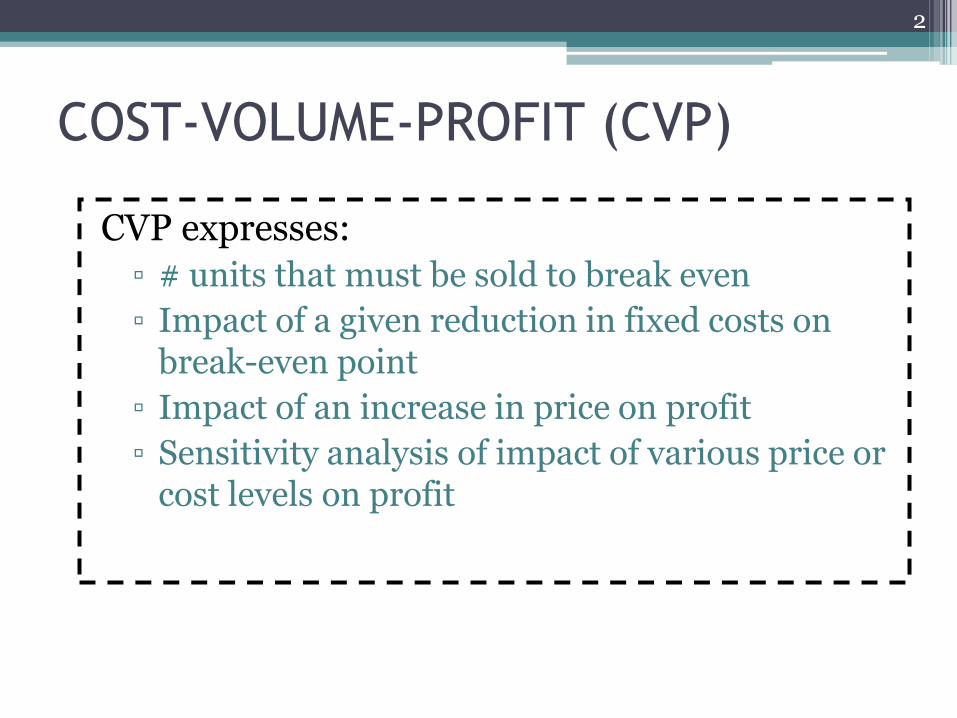

COST-VOLUME-PROFIT (CVP)

CVP expresses:

▫ # units that must be sold to break even

▫ Impact of a given reduction in fixed costs on break-even point

▫ Impact of an increase in price on profit

▫ Sensitivity analysis of impact of various price or cost levels on profit

3

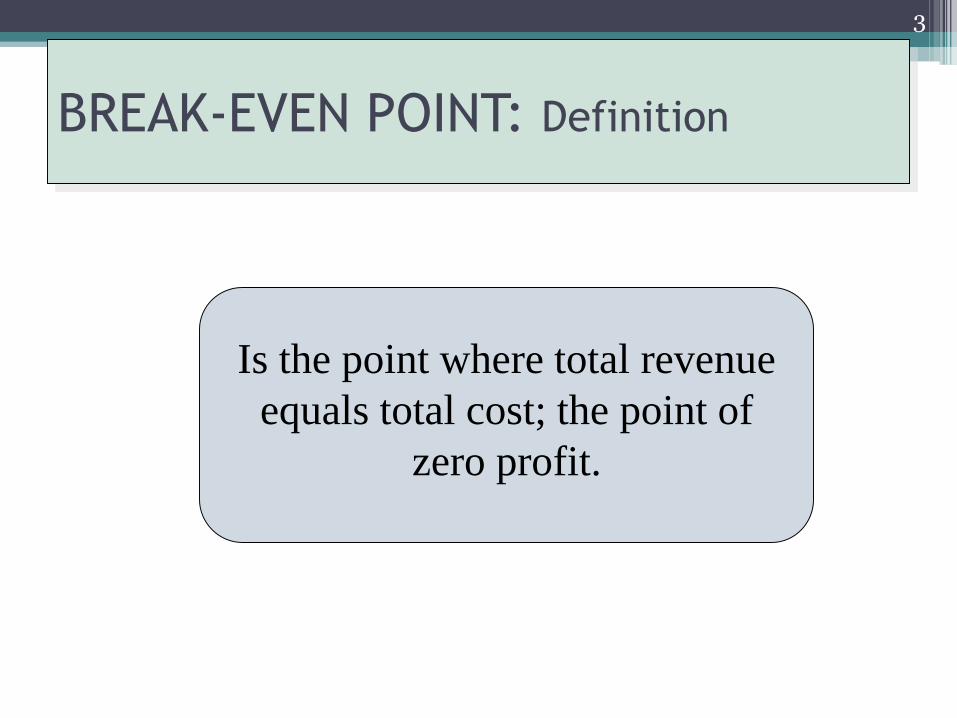

BREAK-EVEN POINT: Definition

Is the point where total revenue

equals total cost; the point of

zero profit.

4

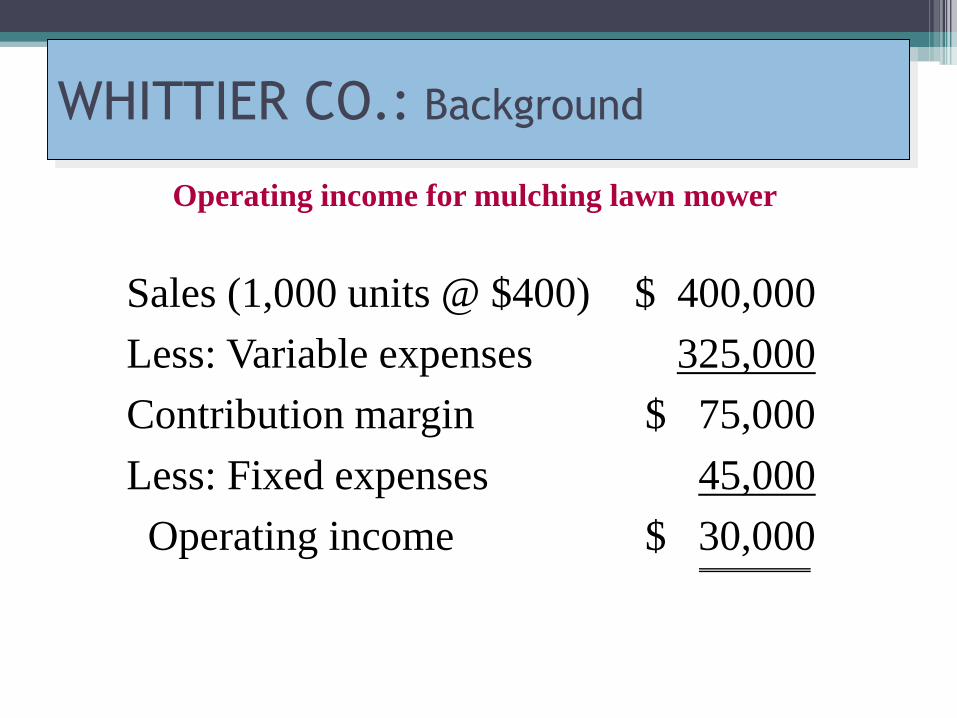

WHITTIER CO.: Background

Sales (1,000 units @ $400) $ 400,000

Less: Variable expenses 325,000

Contribution margin $ 75,000

Less: Fixed expenses 45,000

Operating income $ 30,000

Operating income for mulching lawn mower

5

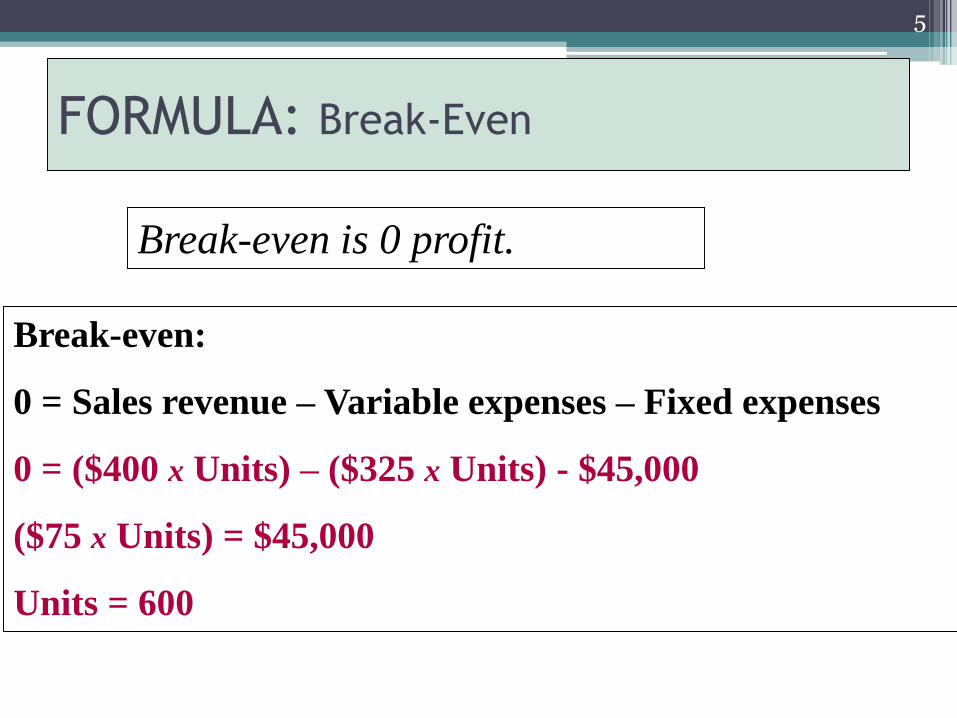

Break-even is 0 profit.

Break-even:

0 = Sales revenue – Variable expenses – Fixed expenses

0 = ($400 x Units) – ($325 x Units) - $45,000

($75 x Units) = $45,000

Units = 600

FORMULA: Break-Even

6

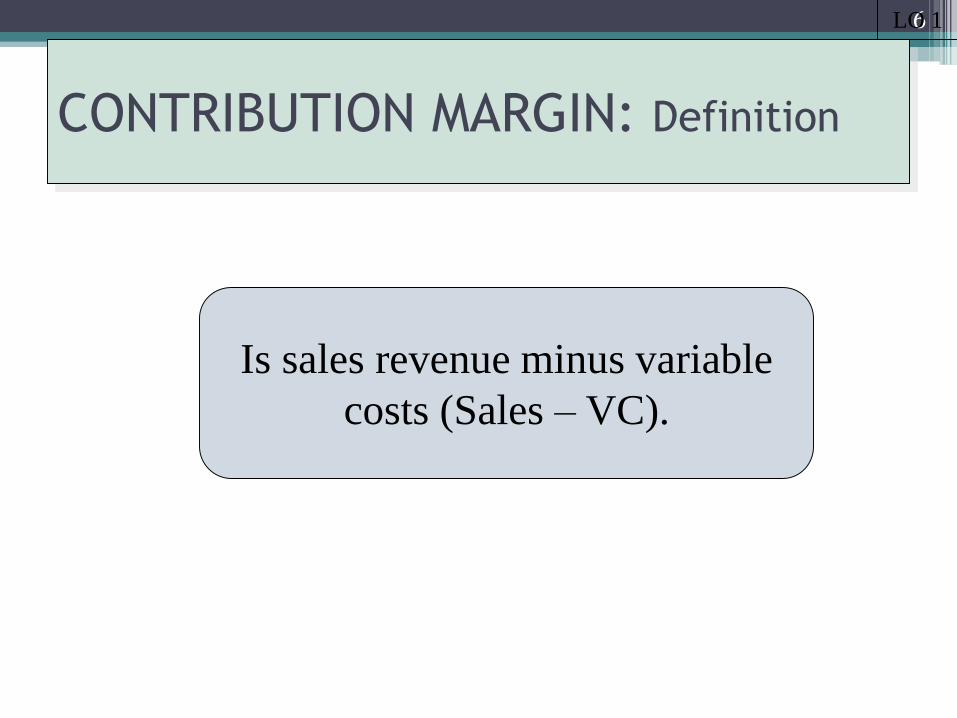

CONTRIBUTION MARGIN: Definition

Is sales revenue minus variable

costs (Sales – VC).

LO 1

7

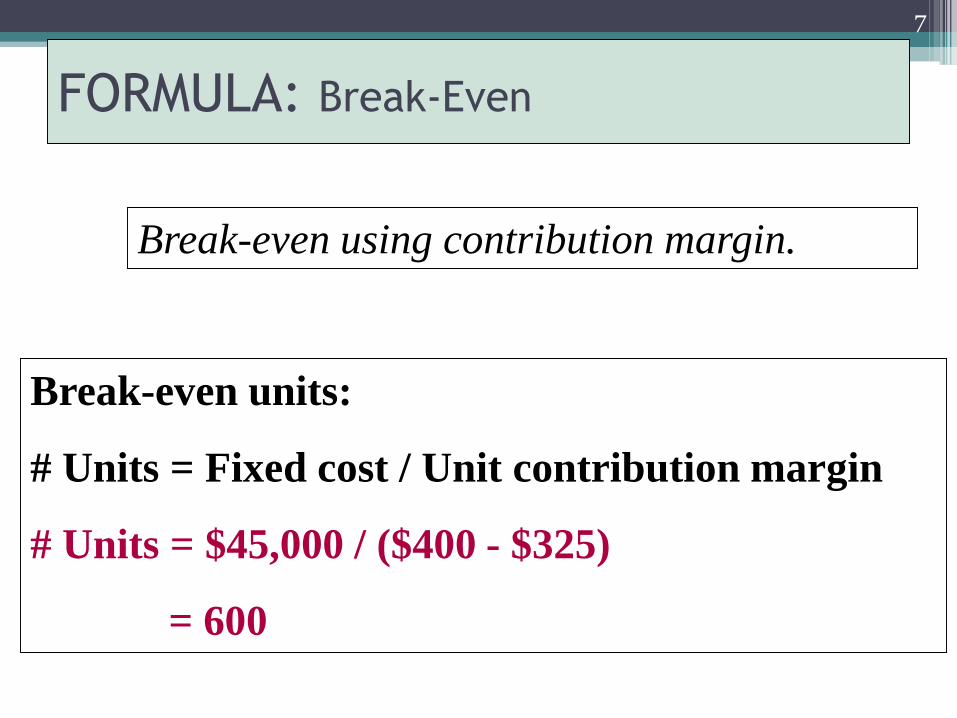

FORMULA: Break-Even

Break-even using contribution margin.

Break-even units:

# Units = Fixed cost / Unit contribution margin

# Units = $45,000 / ($400 - $325)

= 600

8

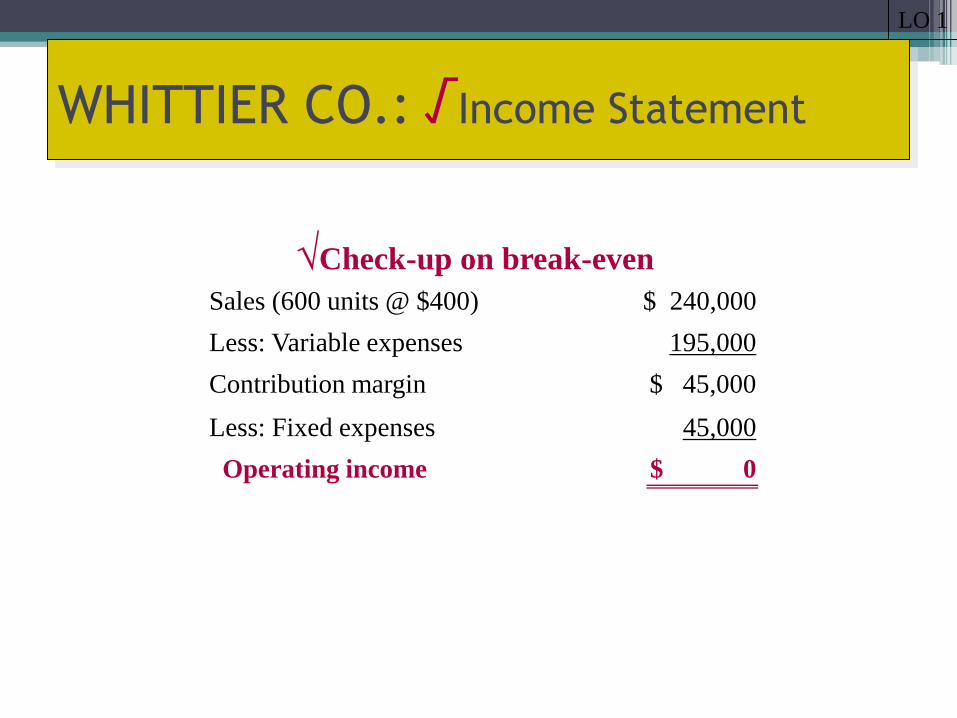

WHITTIER CO.: √Income Statement

LO 1

Sales (600 units @ $400) $ 240,000

Less: Variable expenses 195,000

Contribution margin $ 45,000

Less: Fixed expenses 45,000

Operating income $ 0

√Check-up on break-even

9

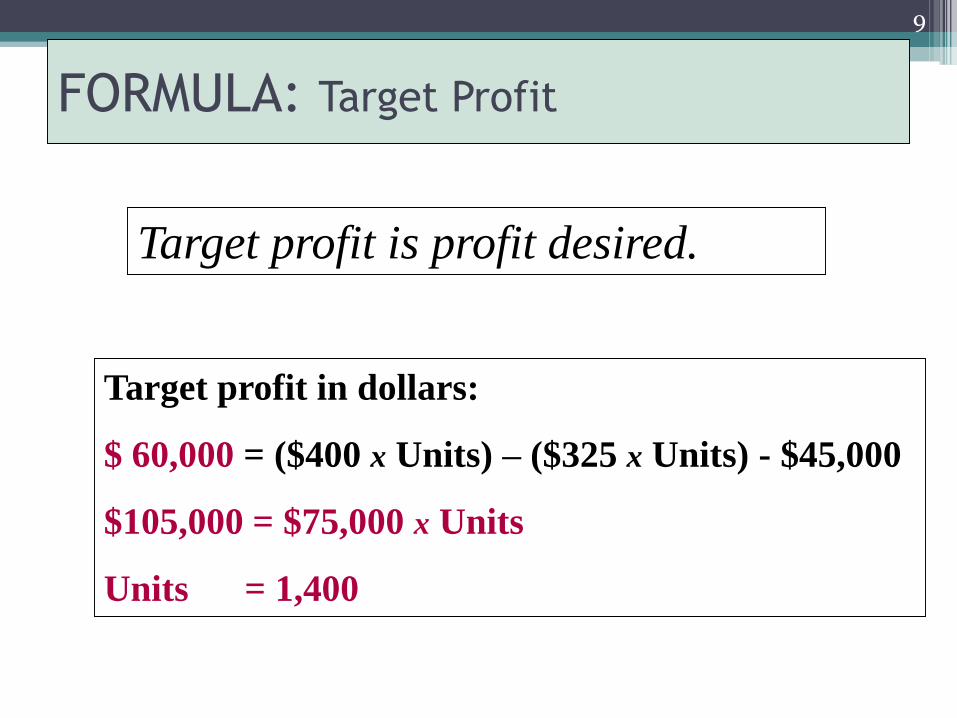

FORMULA: Target Profit

Target profit is profit desired.

Target profit in dollars:

$ 60,000 = ($400 x Units) – ($325 x Units) - $45,000

$105,000 = $75,000 x Units

Units = 1,400

10

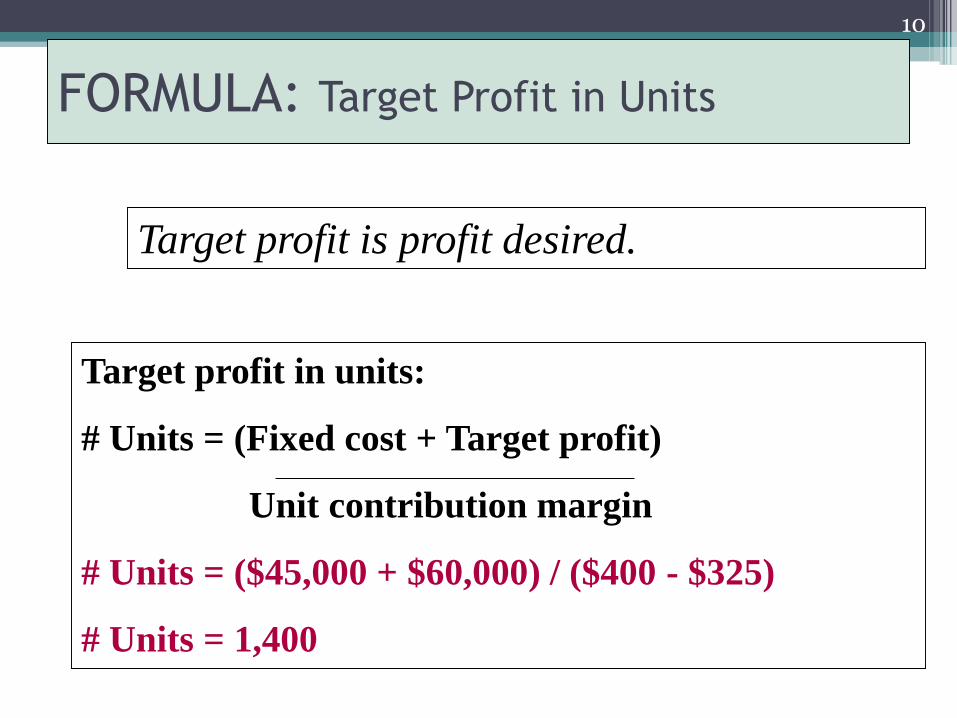

FORMULA: Target Profit in Units

Target profit is profit desired.

Target profit in units:

# Units = (Fixed cost + Target profit)

Unit contribution margin

# Units = ($45,000 + $60,000) / ($400 - $325)

# Units = 1,400

11

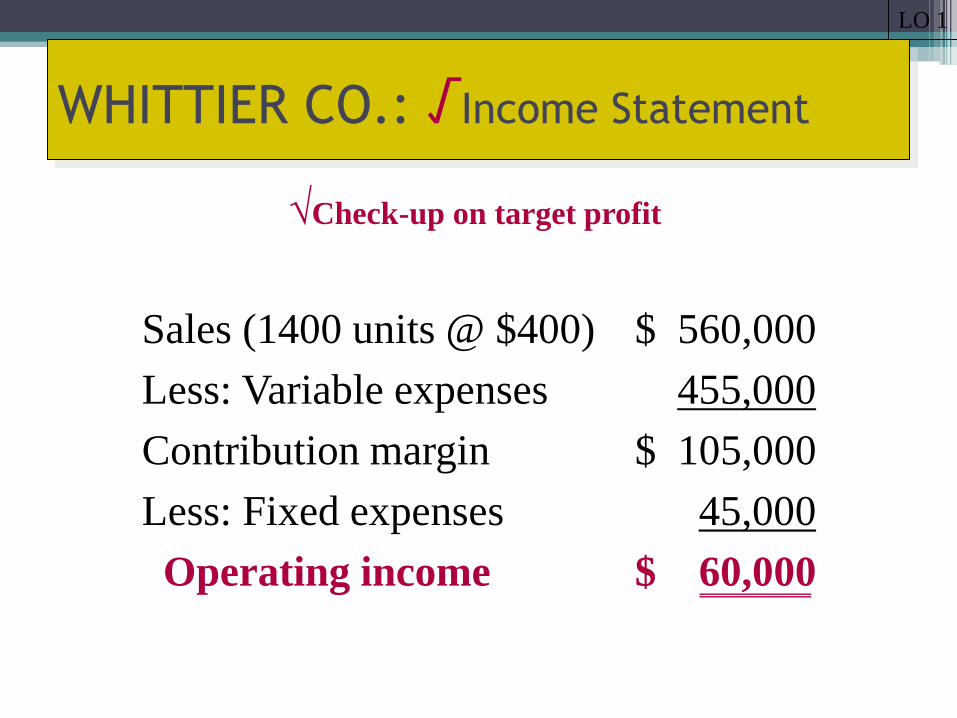

WHITTIER CO.: √Income Statement

LO 1

Sales (1400 units @ $400) $ 560,000

Less: Variable expenses 455,000

Contribution margin $ 105,000

Less: Fixed expenses 45,000

Operating income $ 60,000

√Check-up on target profit

12

FORMULA: Target Profit % Sales

Target profit can be calculated as % of

revenue.

Target profit as % of sales:

0.15 ($400 x Units) =

($400 x Units) – ($325 x Units) - $45,000

$60 x Units = ($75 x Units) - $45,000

# Units = 3,000

13

FORMULA: After-Tax Target Profit

If Whittier has a 35% tax rate & wants

Net income (after-tax profit) of $48,750.

LO 1

After-tax target profit:

Net income = Operating income (1 – Tax rate)

$48,750 = Operating income (1 – 0.35)

$75,000 = Operating income

14

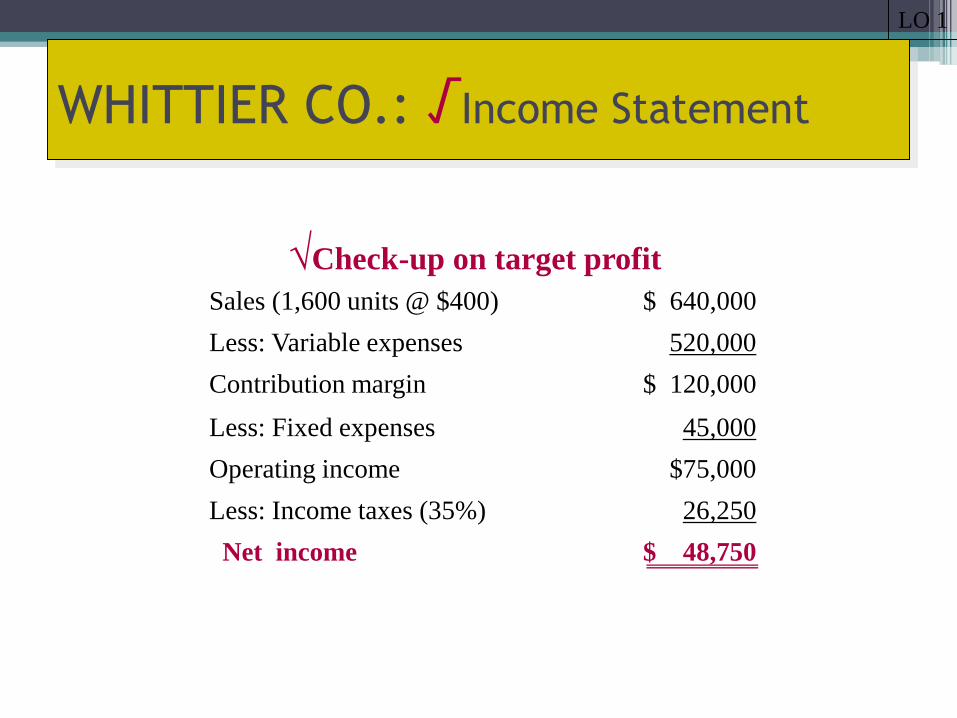

WHITTIER CO.: √Income Statement

LO 1

Sales (1,600 units @ $400) $ 640,000

Less: Variable expenses 520,000

Contribution margin $ 120,000

Less: Fixed expenses 45,000

Operating income $75,000

Less: Income taxes (35%) 26,250

Net income $ 48,750

√Check-up on target profit

15

VARIABLE COST RATIO: Definition

Is the proportion of each sales

dollar used to cover variable

costs.

16

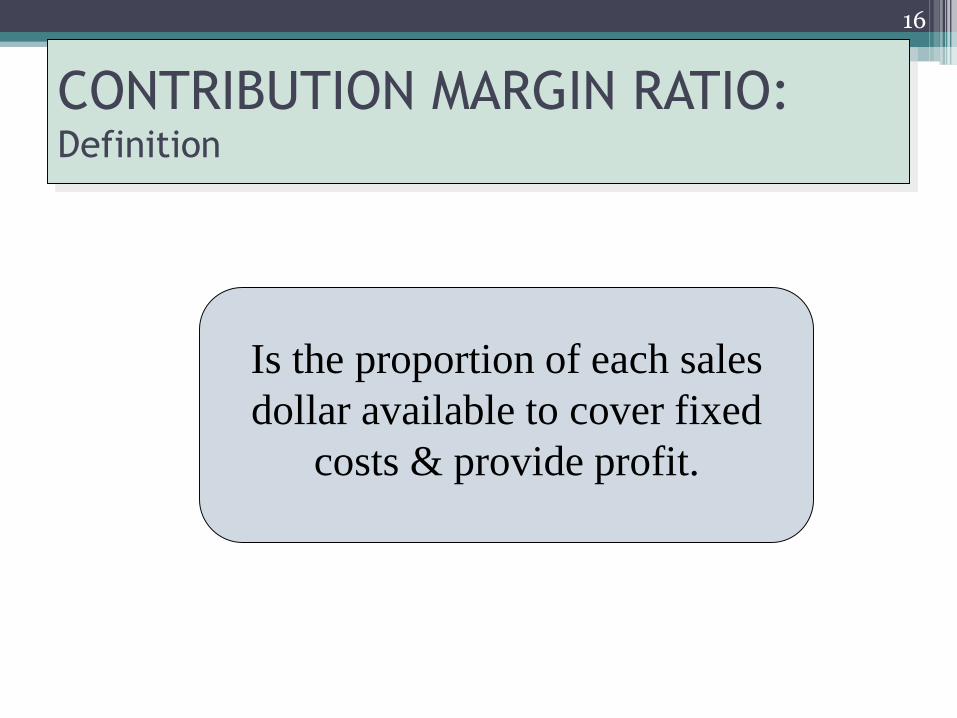

CONTRIBUTION MARGIN RATIO: Definition

Is the proportion of each sales

dollar available to cover fixed

costs & provide profit.

17

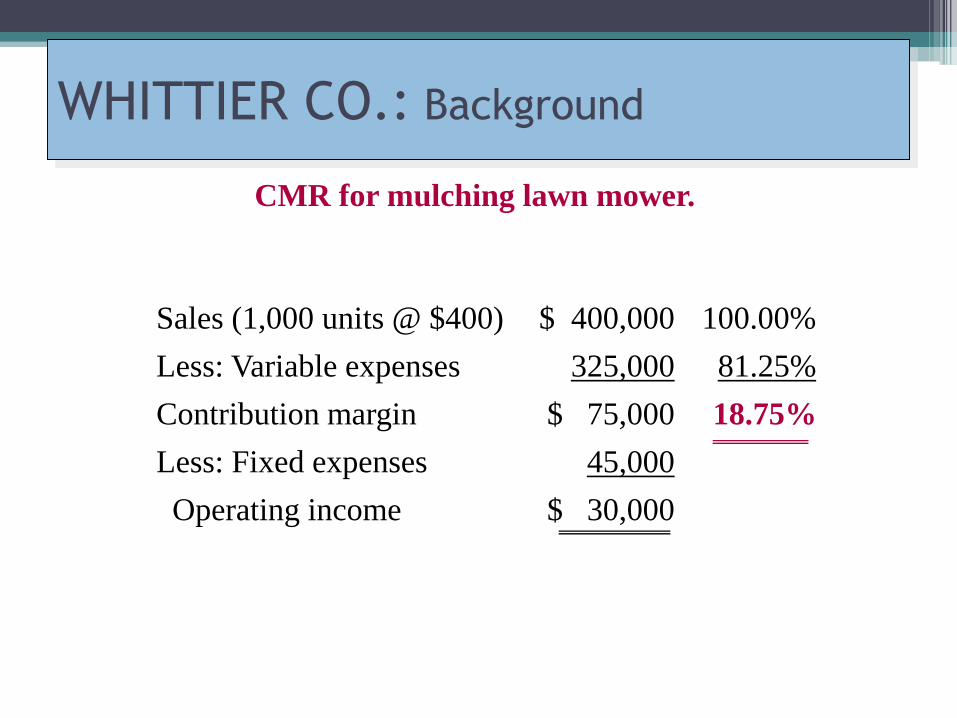

WHITTIER CO.: Background

Sales (1,000 units @ $400) $ 400,000 100.00%

Less: Variable expenses 325,000 81.25%

Contribution margin $ 75,000 18.75%

Less: Fixed expenses 45,000

Operating income $ 30,000

CMR for mulching lawn mower.

18

FORMULA: Break-Even CMR

Contribution margin ratio (CMR) makes

calculation easier.

LO 2

0 = Sales (1 – VC rate) – Fixed Costs

= Sales (1 – 0.8125) - $45,000

Sales = $240,000

OR

Break-even Sales = Fixed cost / CMR

$240,000 = $45,000 / 0.1875

19

Can we use CVP if

Whittier has more than 1

product?

Yes. But we have to add direct

fixed expenses into the

analysis.

LO 3

20

DIRECT FIXED EXPENSES: Definition

Are fixed costs that can be

traced to each product and

would be avoided if the product

did not exist.

21

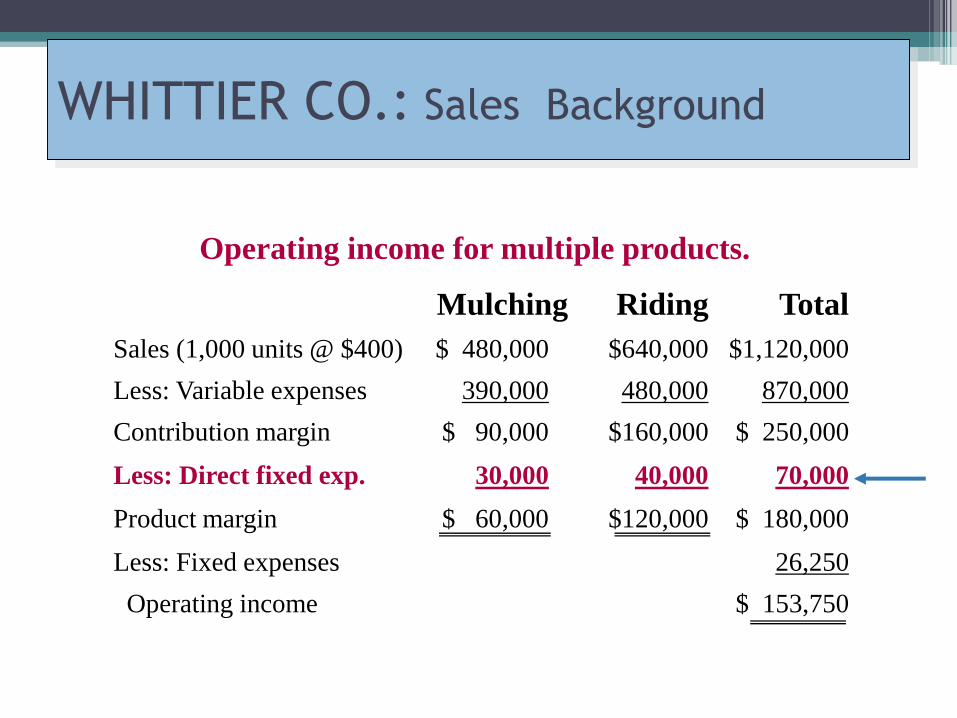

WHITTIER CO.: Sales Background

Mulching Riding Total

Sales (1,000 units @ $400) $ 480,000 $640,000 $1,120,000

Less: Variable expenses 390,000 480,000 870,000

Contribution margin $ 90,000 $160,000 $ 250,000

Less: Direct fixed exp. 30,000 40,000 70,000

Product margin $ 60,000 $120,000 $ 180,000

Less: Fixed expenses 26,250

Operating income $ 153,750

Operating income for multiple products.

22

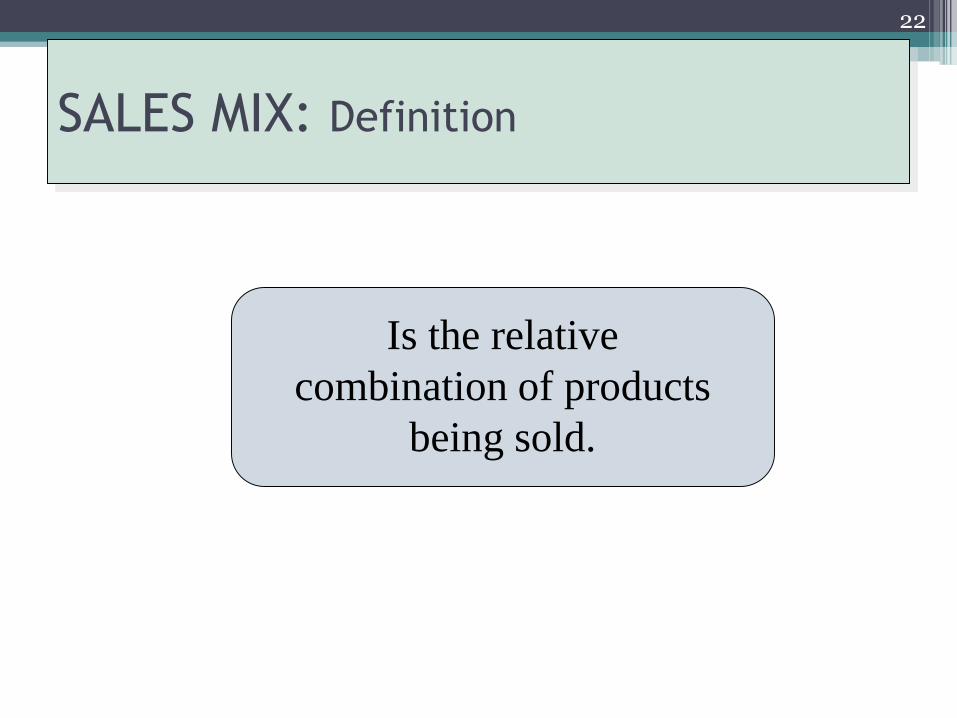

SALES MIX: Definition

Is the relative

combination of products

being sold.

23

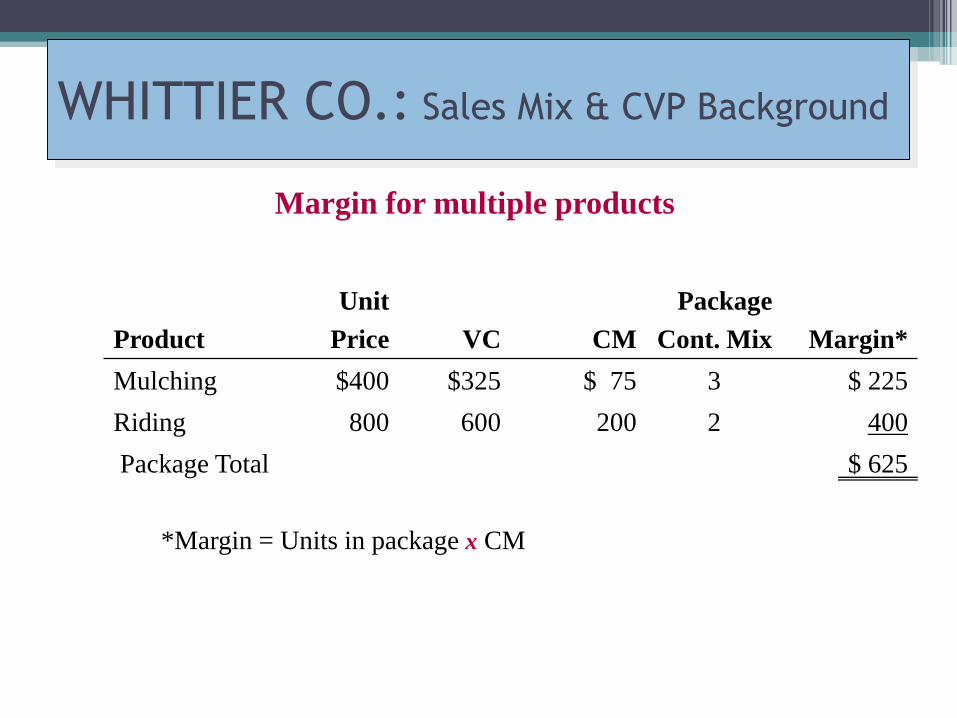

WHITTIER CO.: Sales Mix & CVP Background

Product

Unit

Price VC CM

Package

Cont. Mix Margin*

Mulching $400 $325 $ 75 3 $ 225

Riding 800 600 200 2 400

Package Total $ 625

Margin for multiple products

*Margin = Units in package x CM

24

FORMULA: Break-Even Multiple Products

If Whittier has 2 products, calculate

break-even separately.

Break-Even = Fixed costs / (Price – Unit VC)

Mulching mower = $30,000 / $75

= 400 units

Riding mower = $40,000 / $200

= 200 units

25

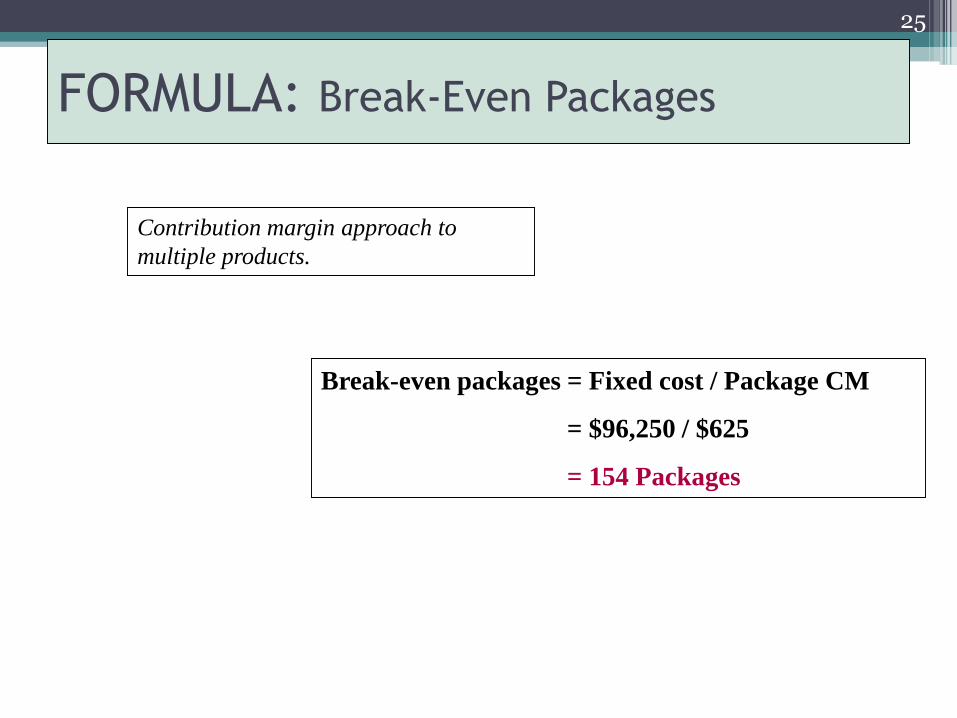

FORMULA: Break-Even Packages

Contribution margin approach to

multiple products.

Break-even packages = Fixed cost / Package CM

= $96,250 / $625

= 154 Packages

26

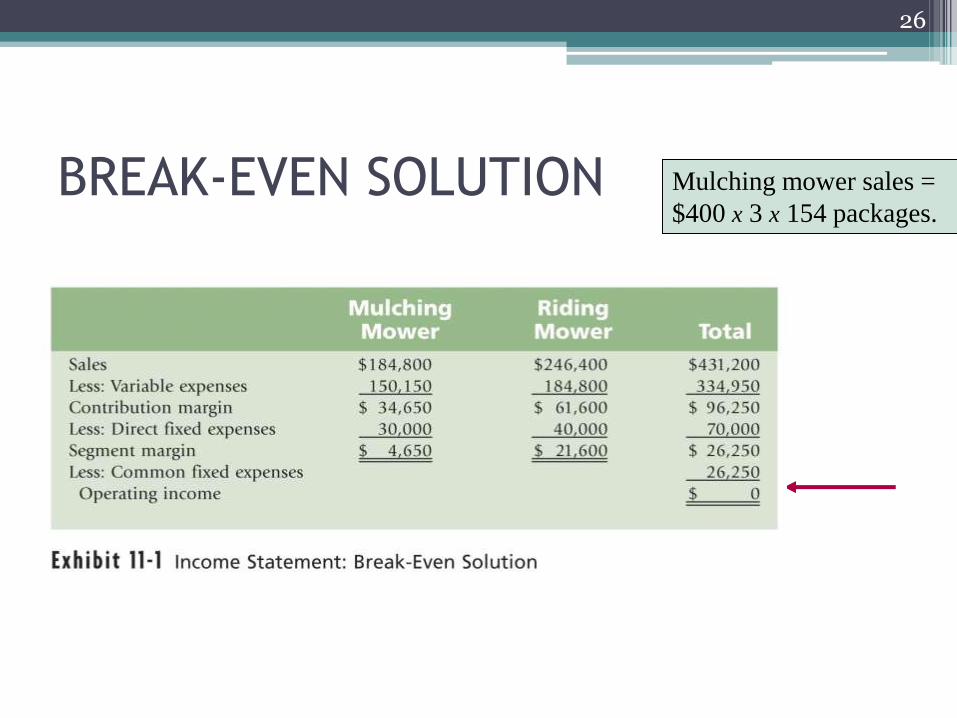

BREAK-EVEN SOLUTION Mulching mower sales =

$400 x 3 x 154 packages.

27

COST-PROFIT-VOLUME GRAPH

AKUNTANSI MANAJEMEN

SESI 8: Tactical Decision Making (TDM) *

Achmad Zaky,MSA.,Ak.,SAS.,CMA.,CA

* Slide ini di sadur dari Slide Resmi Hansen-Mowen 8Th Edition

29

Is there a difference

between tactical and

strategic decisions?

Yes! Tactical & strategic

decisions differ on the time

period affected.

30

TACTICAL DECISION MAKING: Definition

Consists of choosing among

alternatives with an immediate

or limited end in view.

31

STRATEGIC DECISION MAKING: Definition

Is selecting among alternative

strategies so that long term

competitive advantage is

established.

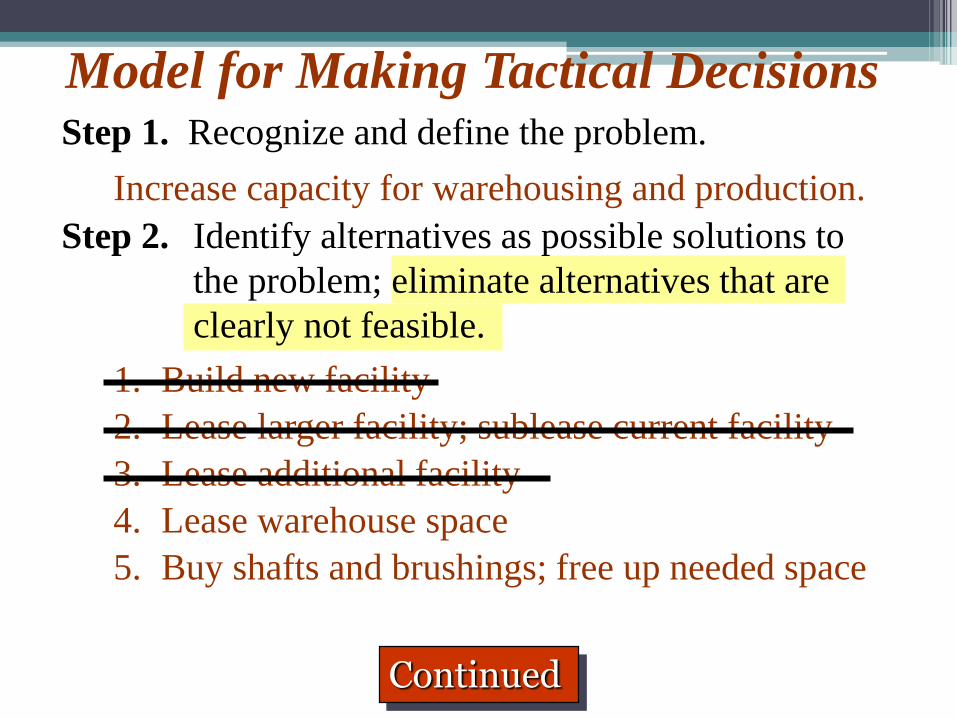

Model for Making Tactical DecisionsStep 1. Recognize and define the problem.

Continued

Increase capacity for warehousing and production.

Step 2. Identify alternatives as possible solutions to

the problem; eliminate alternatives that are

clearly not feasible.

1. Build new facility

2. Lease larger facility; sublease current facility

3. Lease additional facility

4. Lease warehouse space

5. Buy shafts and brushings; free up needed space

Model for Making Tactical Decisions

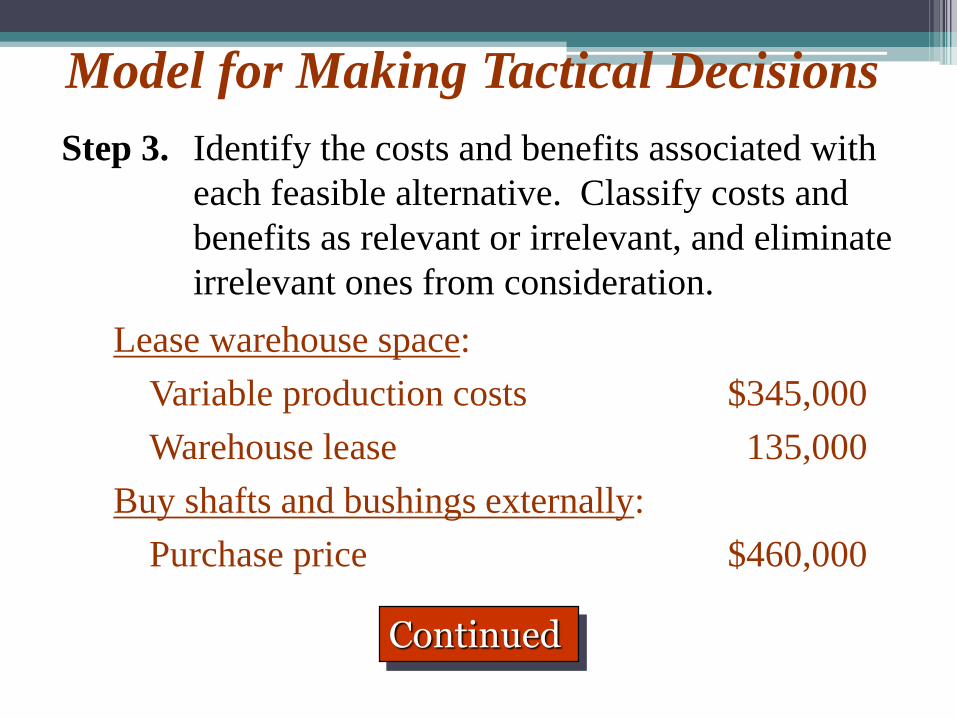

Lease warehouse space:

Variable production costs $345,000

Warehouse lease 135,000

Buy shafts and bushings externally:

Purchase price $460,000

Step 3. Identify the costs and benefits associated with

each feasible alternative. Classify costs and

benefits as relevant or irrelevant, and eliminate

irrelevant ones from consideration.

Continued

Model for Making Tactical Decisions

Step 4. Total the relevant costs and benefits for each

alternative.

Continued

Lease warehouse space:

Variable production costs $345,000

Warehouse lease 135,000

Total $480,000

Buy shafts and bushings externally:

Purchase price $460,000

Differential cost $ 20,000

Model for Making Tactical Decisions

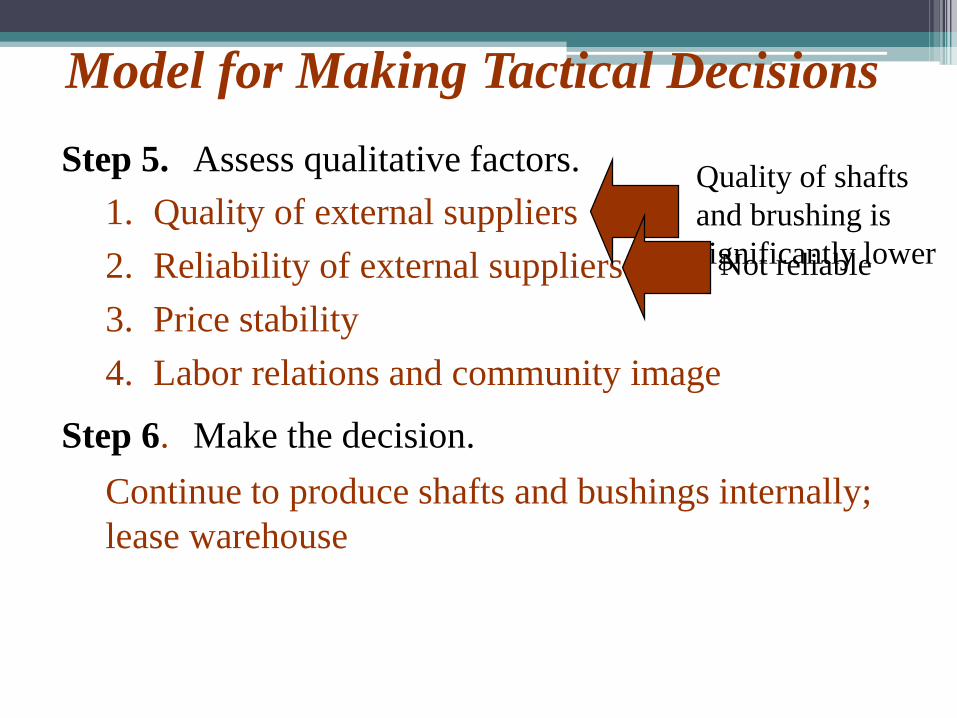

Step 5. Assess qualitative factors.

1. Quality of external suppliers

2. Reliability of external suppliers

3. Price stability

4. Labor relations and community image

Step 6. Make the decision.

Quality of shafts

and brushing is

significantly lowerNot reliable

Continue to produce shafts and bushings internally;

lease warehouse

Relevant Costs Defined

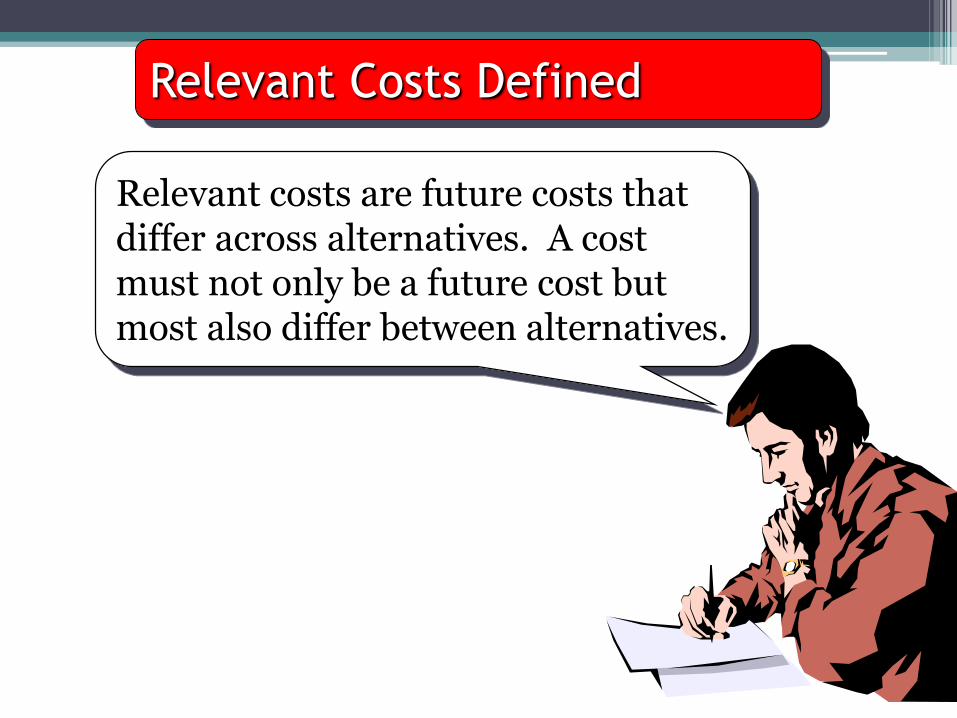

Relevant costs are future costs that differ across alternatives. A cost must not only be a future cost but most also differ between alternatives.

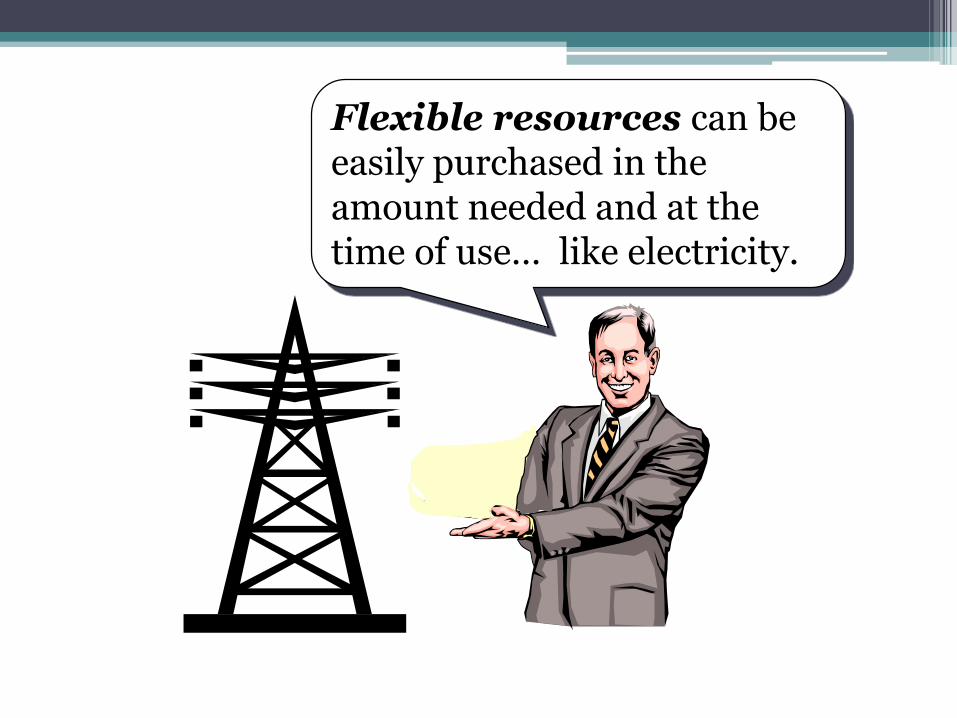

Flexible resources can be easily purchased in the amount needed and at the time of use… like electricity.

Committed resources are purchased before they are used, such as salaried employees.

Important: Short-term Perspective

Illustrative Examples of

Relevant Cost Applications

Make or Buy

Keep or Drop

Special Order

Sell or Process Further

Product Mix

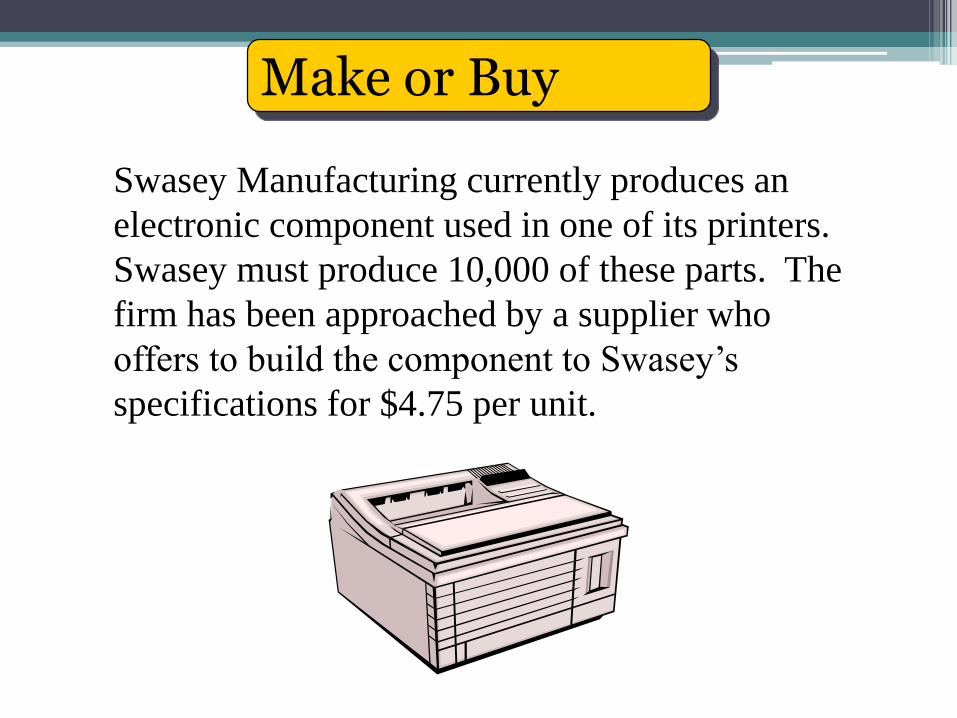

Make or Buy

Swasey Manufacturing currently produces an

electronic component used in one of its printers.

Swasey must produce 10,000 of these parts. The

firm has been approached by a supplier who

offers to build the component to Swasey’s

specifications for $4.75 per unit.

Make or Buy

Total Cost Unit Cost

Rental of equipment $12,000 $1.20

Equipment depreciation 2,000 0.20

Direct materials 10,000 1.00

Direct labor 20,000 2.00

Variable overhead 8,000 0.80

General fixed overhead 30,000 3.00

Total $82,000 $8.20

The full absorption cost for the 10,000 parts is

computed as follows:

Enough material is on hand to make 5,000 parts.

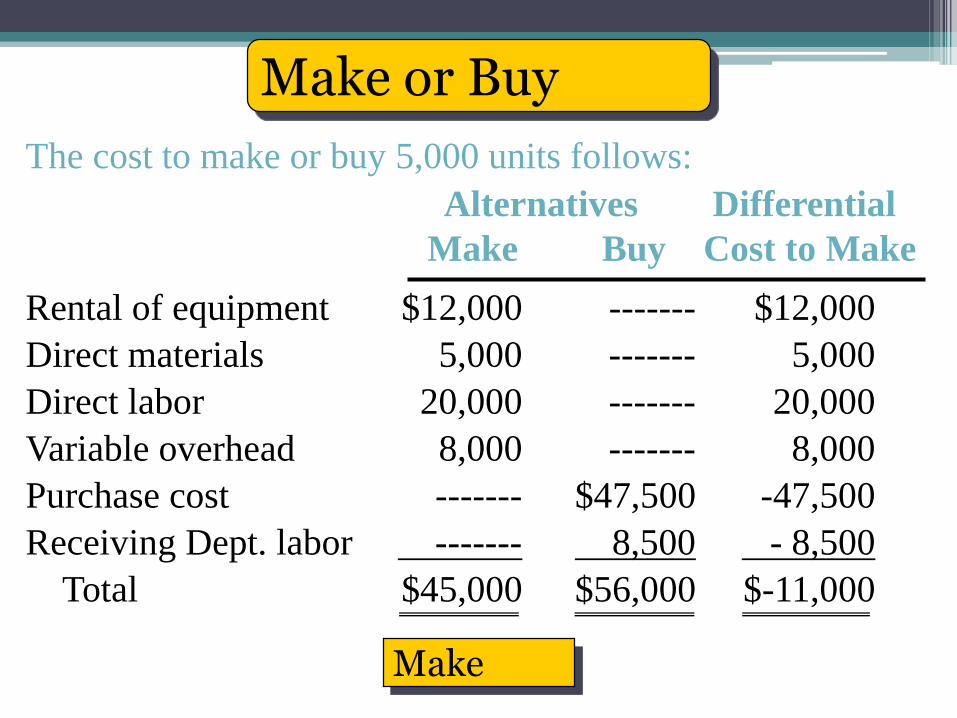

Make or Buy

Alternatives Differential

Make Buy Cost to Make

Rental of equipment $12,000 ------- $12,000

Direct materials 5,000 ------- 5,000

Direct labor 20,000 ------- 20,000

Variable overhead 8,000 ------- 8,000

Purchase cost ------- $47,500 -47,500

Receiving Dept. labor ------- 8,500 - 8,500

Total $45,000 $56,000 $-11,000

The cost to make or buy 5,000 units follows:

Make

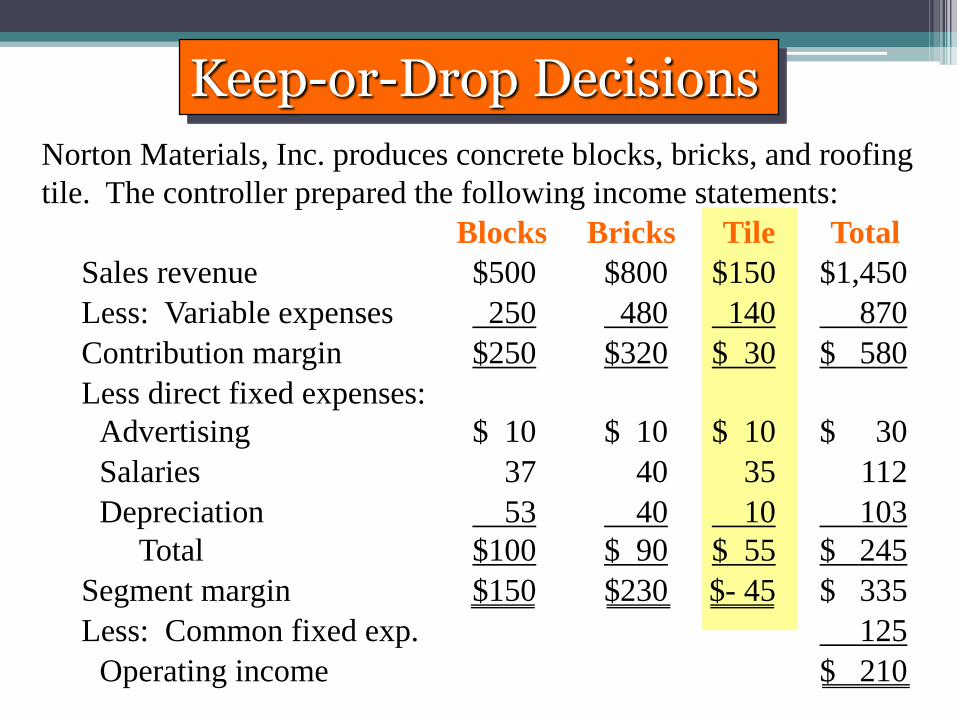

Norton Materials, Inc. produces concrete blocks, bricks, and roofing

tile. The controller prepared the following income statements:

Keep-or-Drop Decisions

Blocks Bricks Tile Total

Sales revenue $500 $800 $150 $1,450

Less: Variable expenses 250 480 140 870

Contribution margin $250 $320 $ 30 $ 580

Less direct fixed expenses:

Advertising $ 10 $ 10 $ 10 $ 30

Salaries 37 40 35 112

Depreciation 53 40 10 103

Total $100 $ 90 $ 55 $ 245

Segment margin $150 $230 $- 45 $ 335

Less: Common fixed exp. 125

Operating income $ 210

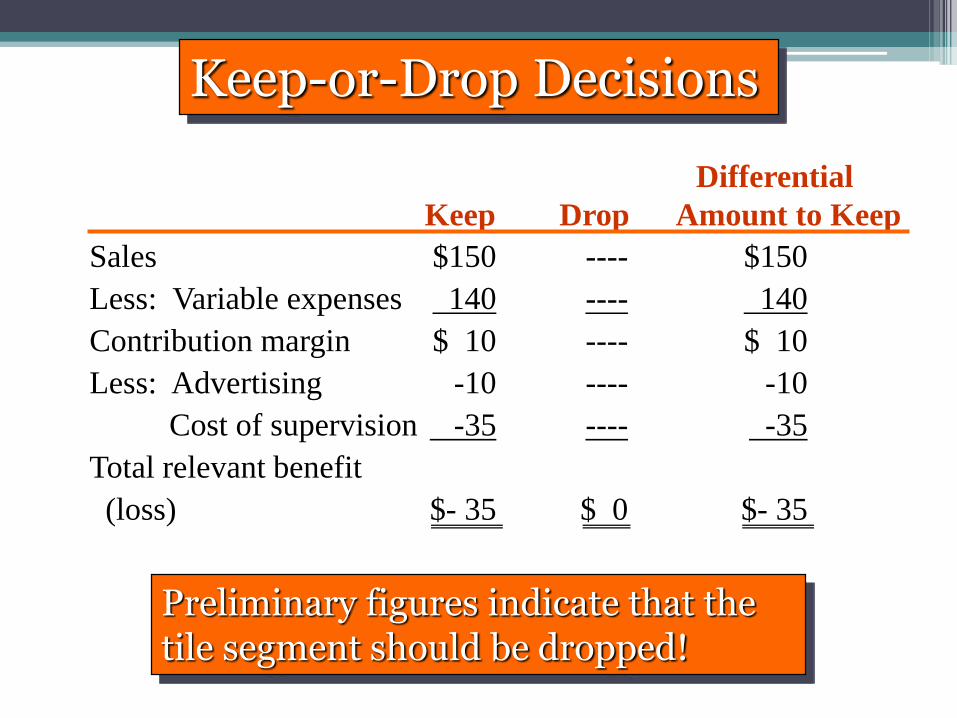

Keep-or-Drop Decisions

Differential

Keep Drop Amount to Keep

Sales $150 ---- $150

Less: Variable expenses 140 ---- 140

Contribution margin $ 10 ---- $ 10

Less: Advertising -10 ---- -10

Cost of supervision -35 ---- -35

Total relevant benefit

(loss) $- 35 $ 0 $- 35

Preliminary figures indicate that the tile segment should be dropped!

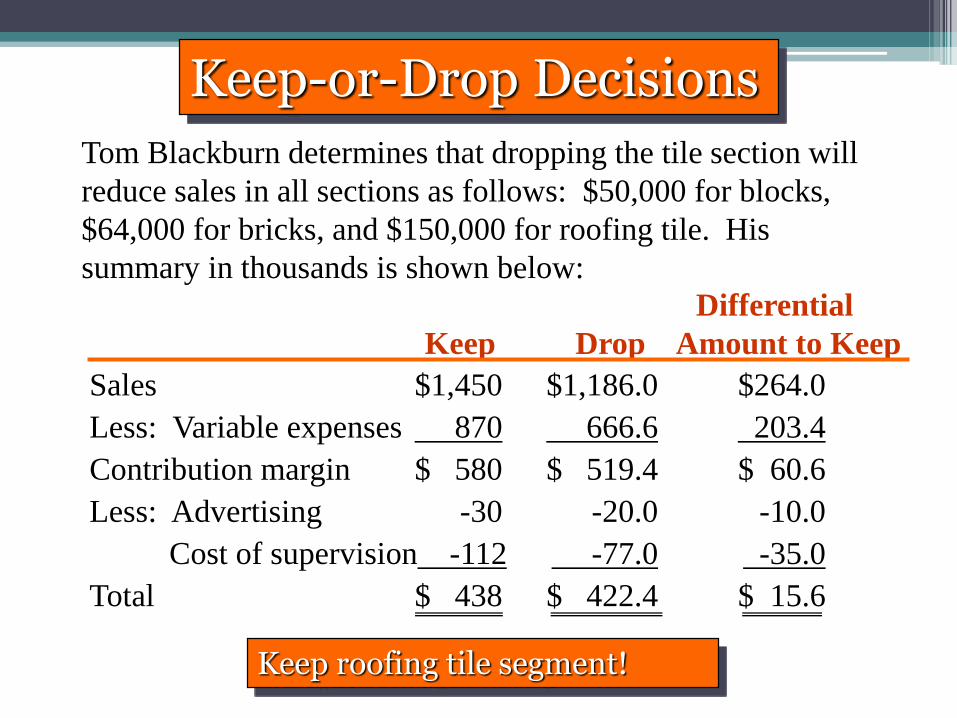

Keep-or-Drop Decisions

Tom Blackburn determines that dropping the tile section will

reduce sales in all sections as follows: $50,000 for blocks,

$64,000 for bricks, and $150,000 for roofing tile. His

summary in thousands is shown below:

Sales $1,450 $1,186.0 $264.0

Less: Variable expenses 870 666.6 203.4

Contribution margin $ 580 $ 519.4 $ 60.6

Less: Advertising -30 -20.0 -10.0

Cost of supervision -112 -77.0 -35.0

Total $ 438 $ 422.4 $ 15.6

Differential

Keep Drop Amount to Keep

Keep roofing tile segment!

Keep-or-Drop Decisions

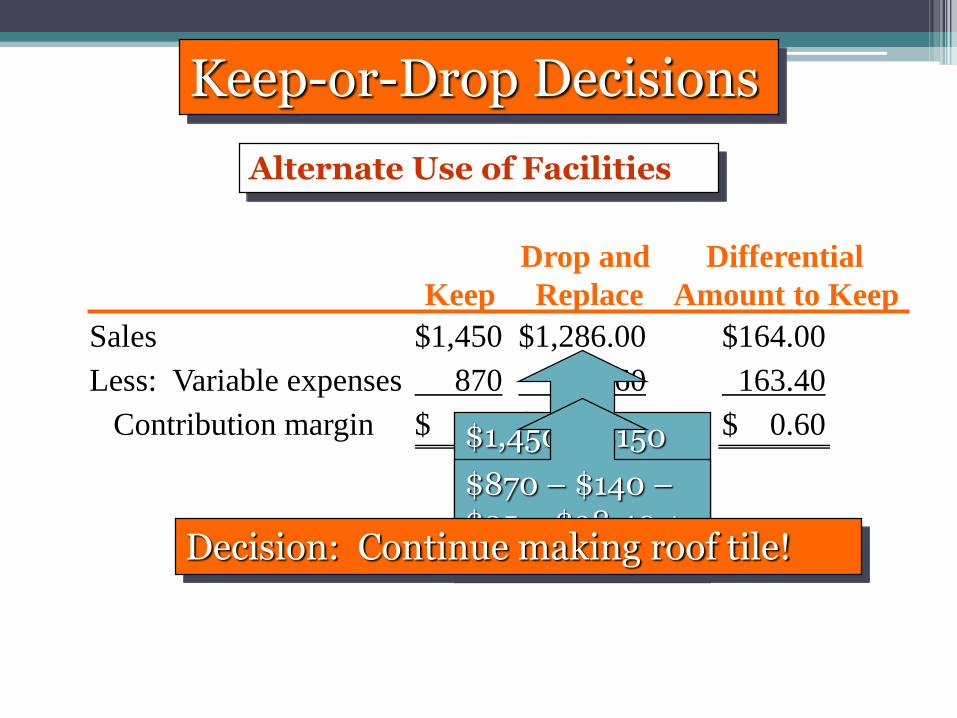

The marketing manager sees the market for floor tile as

stronger and less competitive than roof tile. He submits the

following figures for floor tile sales:

Alternate Use of Facilities

Sales $100,000

Less: Variable expenses 40,000

Contribution margin $ 60,000

Less: Direct fixed expenses 55,000

Segment margin $ 5,000

Keep-or-Drop Decisions

Alternate Use of Facilities

Drop and Differential

Keep Replace Amount to Keep

Sales $1,450 $1,286.00 $164.00

Less: Variable expenses 870 706.60 163.40

Contribution margin $ 580 $ 579.40 $ 0.60$1,450 – $150 –$50 – $64 + $100$870 – $140 –$25 – $38.40 + $40Decision: Continue making roof tile!

Special-Order Decisions

An ice cream company is

operating at 80 percent of its

productive capacity (20 million

half gallon units). The unit costs

associated with producing and

selling 16 million units are shown

on the next slide.

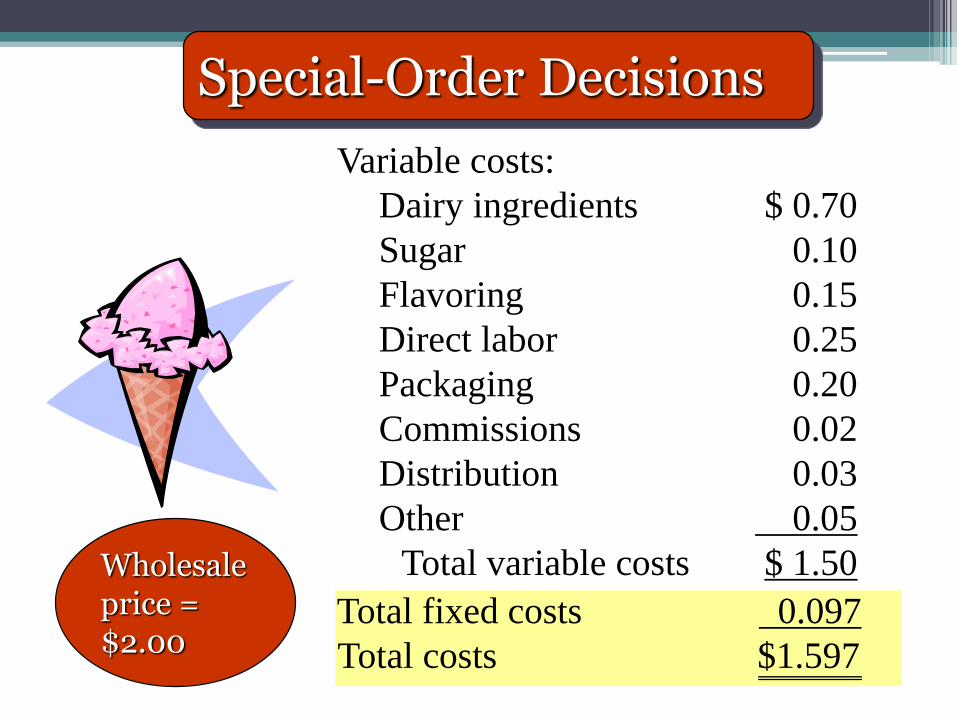

Special-Order Decisions

Variable costs:

Dairy ingredients $ 0.70

Sugar 0.10

Flavoring 0.15

Direct labor 0.25

Packaging 0.20

Commissions 0.02

Distribution 0.03

Other 0.05

Total variable costs $ 1.50Wholesale price = $2.00

Total fixed costs 0.097

Total costs $1.597

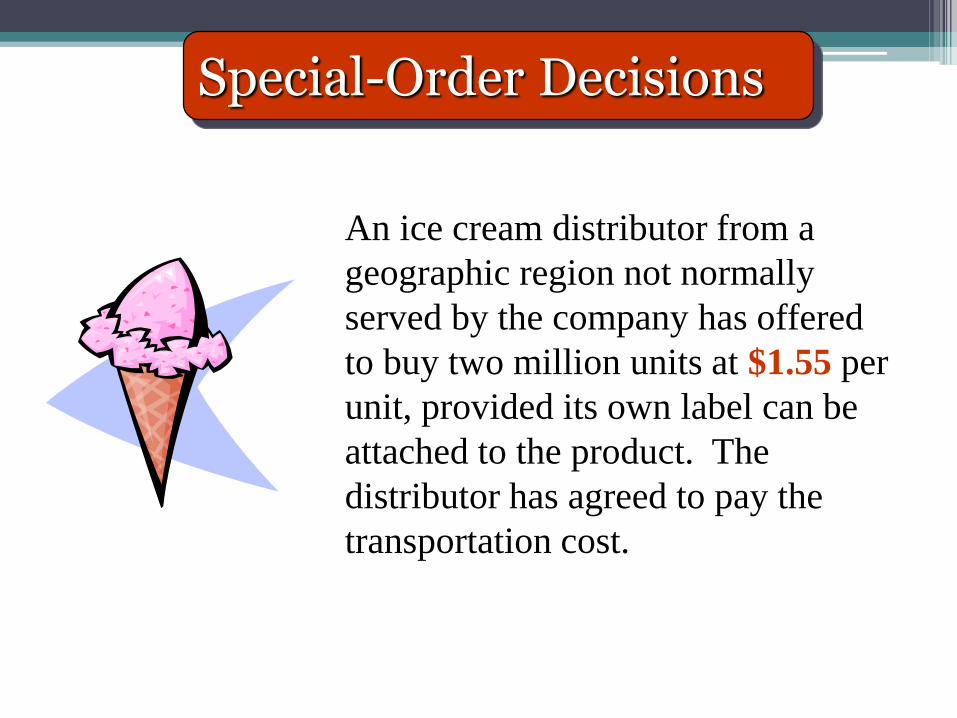

Special-Order Decisions

An ice cream distributor from a

geographic region not normally

served by the company has offered

to buy two million units at $1.55 per

unit, provided its own label can be

attached to the product. The

distributor has agreed to pay the

transportation cost.

Special-Order Decisions

Variable costs:

Dairy ingredients $0.70

Sugar 0.10

Flavoring 0.15

Direct labor 0.25

Packaging 0.20

Commissions 0.02

Distribution 0.03

Other 0.05

Total variable costs $1.50

Total fixed costs 0.097

Total costs $1.597

Which costs

are irrelevant?$1.45

$1.45

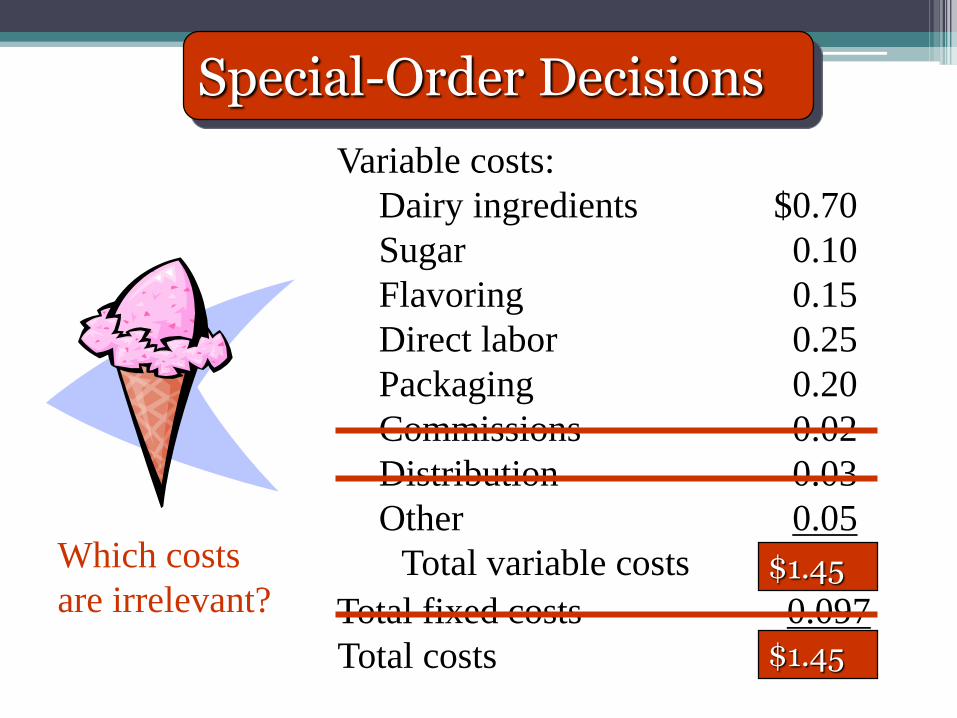

Special-Order Decisions

Variable costs:

Dairy ingredients $ 0.70

Sugar 0.10

Flavoring 0.15

Direct labor 0.25

Packaging 0.20

Commissions 0.02

Distribution 0.03

Other 0.05

Total variable costs $ 1.50

Total fixed costs 0.097

Total cost $1.597

Which costs

are irrelevant?$1.45

$1.45

Accept the offer ($0.10 x 2,000,000 = $200,000 more profit).

Sell or Further Process

Yield at Split-Off

Grade A800 lbSell for $0.40 lb

Grade B600 lb

Grade C600 lb

Joint Cost

$300

Bagged120 BagsCost $0.05/BagSell for $1.30/Bag

Applesauce500 16-oz CansCost $0.10/lbSell for $0.75 can

Further Processing

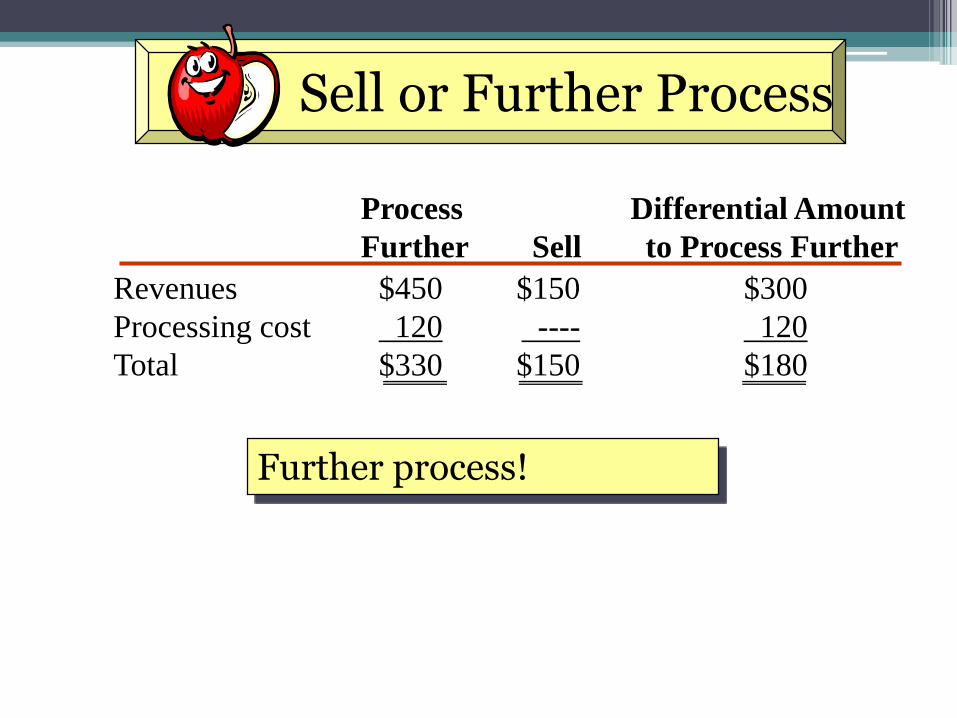

Sell or Further Process

Process Differential Amount

Further Sell to Process Further

Revenues $450 $150 $300

Processing cost 120 ---- 120

Total $330 $150 $180

Further process!

Two Approaches to Pricing

1. Cost-Based Pricing

2. Target Costing and Pricing

56

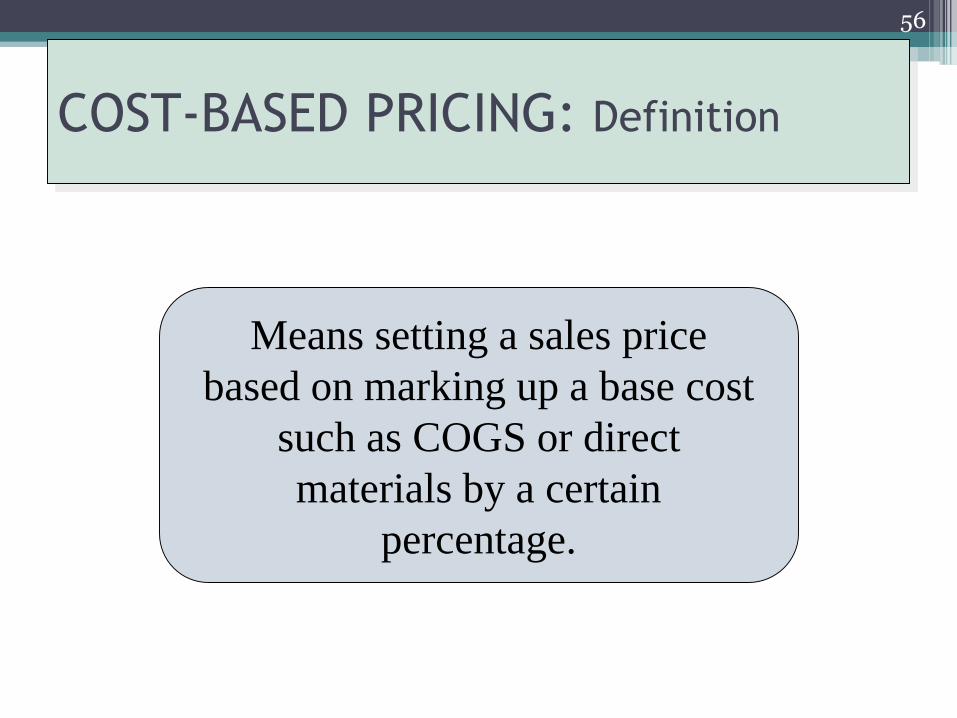

COST-BASED PRICING: Definition

Means setting a sales price

based on marking up a base cost

such as COGS or direct

materials by a certain

percentage.

Target Costing and Pricing

Target costing is a method of determining the cost of a product or service based on the price (target price) that customers are willing to pay.

This is referred to as price-driven costing.

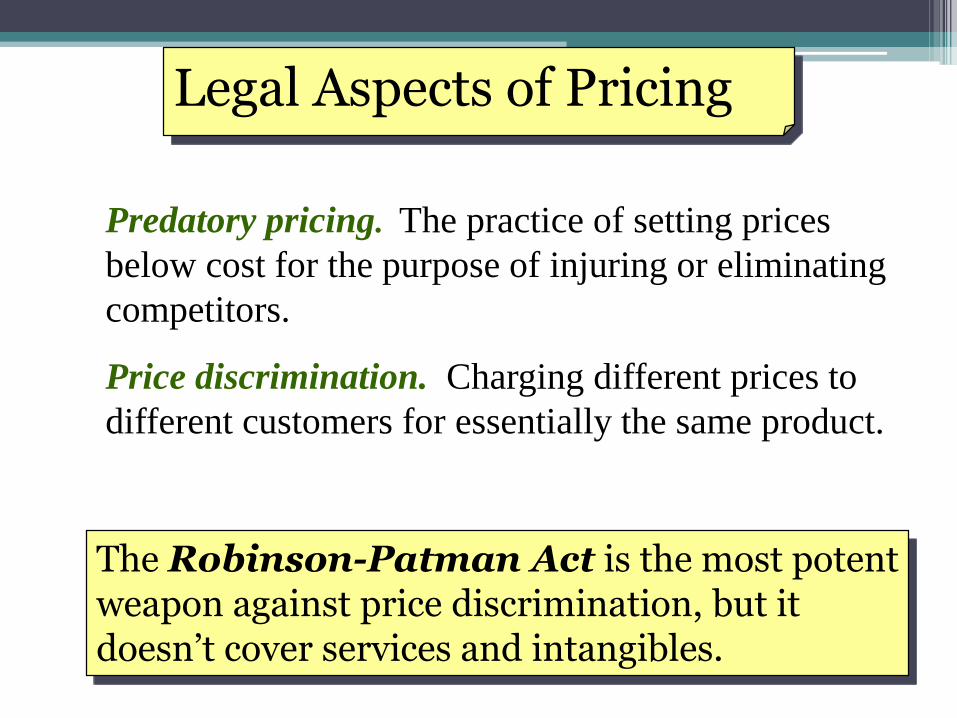

Legal Aspects of Pricing

Predatory pricing. The practice of setting prices

below cost for the purpose of injuring or eliminating

competitors.

Price discrimination. Charging different prices to

different customers for essentially the same product.

The Robinson-Patman Act is the most potent weapon against price discrimination, but it doesn’t cover services and intangibles.