Embed Size (px)

Citation preview

1BRIGHT MARKET INSIGHT

No.1 Spring 2013

Greentech - the forest as a future resourceI N S I G H T

No.1 Spring 2013

I N D E X & R E P O R T O F T H E W O R L D B I O R E F I N E R Y I N D U S T R Y

I N S I G H T

No.1 Spring 2013

INDEX & REPORT for the GLOBAL PULP & BIOREFINERY INDUSTRY

I N S I G H T

VISCOSE THE COMEBACK

Major Capacity Increases Cause Volatility

GLOBAL McKinsey´s advice about the paradigM shift EurOpE frantic activity at sca ortviKen

LAtin AmEricA bright future despite rising costs cHinA tiMe for recovery

nOrtH AmEricA ford focuses on new cellulose Materials r&D&i the centre for world-leading research

prOFiLE Mats nordlander, head of stora enso renewable pacKaging

PAGE 47

Market TrendsFORECAST30 MONTHS

Market TrendsFORECAST30 MONTHS

2 BRIGHT MARKET INSIGHT

CONTENT

Peter Berg, McKinsey: Advice to the forest industry

Volatitlity in the viscose market

CHAPTER 1

6

9

GLOBAL

Frantic acitivity at SCA Ortviken

SCA R&D: Full focus on new materials

SCA Östrand: Equipped for the future

Interview with Ulf Larsson, President of SCA Forest Products

Aditya Birla Domsjö: Leading viscose manufacturer

CHAPTER 2

12

13

EUROPE

14

16

18

The hurricane Sandy gives Resolute a boost

Ford devlops new cellulose materials

CHAPTER 4

30

32

NORTH AMERICA

Pressure from rising costs

Five companies – five growth strategies

Fibria and Ensyn teams up to produce biofuels

Tres Lagoas – the world’s forest industrial metropolis

CHAPTER 5

34

35

LATIN AMERICA

36

39

FSCN – The centre of worldleading research

Bonanza for the mills

Focus on energy efficiency

Fourth generation paper

CHAPTER 6

40

41

42

43

R&D&I

Chinas import boost the pulp price

CHAPTER 7

44

CHRONICLE

A strong market 2013 and 2014

CHAPTER 8

47

INDEX

INDEX PAGE 47

VISCOSE PAGE 9

STORA ENSO fOCuSES ON CHINA PAGE 24

Lumber demand: Time for recovery

New emission standards

Merger in Taiwan

Stora Enso invests EUR 1,6 billion in Guangxi

Interview with Mats Nordlander, Stora Enso Renewable Packaging

Russia and the Angara paper project

CHAPTER 3

20

22

CHINA & ASIA

23

24

26

28

EDitOr–in–cHEiF

EDitOriAL StAFF

DESiGn

puBLiSHEr

SALES

WEBSitE

ADDrESS

pHOnE

carl Johard per aronsson, henriK brandÃo Jönsson, leonard Johard, Jan höKerberg, MiKael Jåfs, nils lindstrand, lennart pehrson

JoaKiM Karlsson (art director) & terÉse lind, sweet williaMs and pop

caleJo future intelligence ab

håKan freudenthal, sales director

www.brightMarKetinsight.coM

strandgatan 4, 85231 sundsvall, sweden

+46 60159090

3BRIGHT MARKET INSIGHT

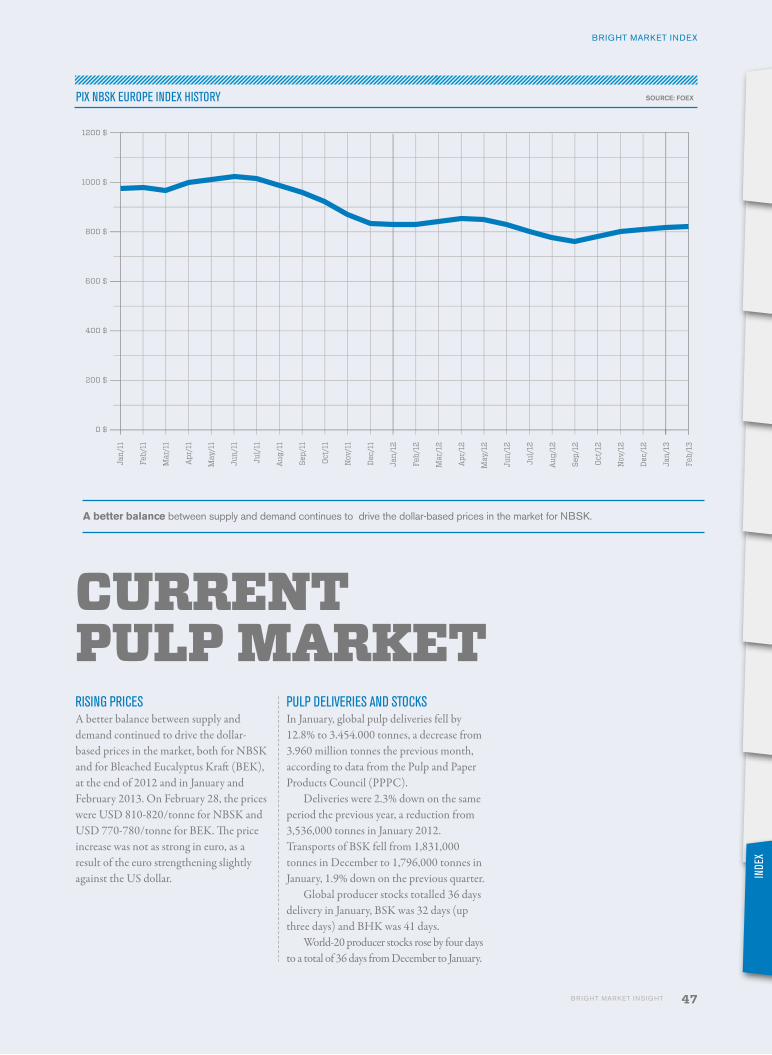

Bright Market Insight is an exclusive, qualitative quarterly market report with coverage, interviews, news and analyses from the international markets in Europe, North America, Latin America, China and the rest of Asia and Oceania. It is published four times a year with an exclusive and up-to-date report on news and trends in the international biorefinery and pulp market as well as a unique long-term forecast (Bright Market Index) of pulp prices (NBSK) 30 months into the future.

uNIQuE fORECAST MODELThe Index is a unique proprietary developed forecast model for (NBSK) pulp based on ar-tificial neural networks (ANN). The model distinguishes itself by including a large amount of fundamental data and taking into account the frequencies of market fluctuations. This makes it unique in the commodity market.

Bright Market Index forecasts indicate the correct price directions more than 80% of the time for all time horizons longer than 6 months. The model is also able to identify whether the price will increase or decrease in nearly 80–85 percent of cases where long-range forecasts are made. In a 24-month range, the forecast is very close to the actual price trend. The model predicted two years ahead the deep dip in 2009 and 2011 as well as the increase during the autumn 2012.

PROfESSIONAL AND EXPERIENCED STAffThe Bright Market Insight is produced in close collaboration with academia and the forest products industry and its editorial board includes Anders Anders Luthbom, former BI Director of SCA, Henrik Essén, BI Manager at Billerud and Mikael Jåfs, Senior Analyst at Credit Agricole Chevreux in Stockholm.

The editorial staff are very professional and experienced business journalists around the world. They each cover the following areas:

– The international biorefinery market with analyses, inteviews and news about new capacities and shut-down capacities as well as trend reports.

– Downturn in the biorefinery and pulp markets in Europe, Latin America, North America, and China and Asia.

– Reports on prices, inventories, supply and demand with market analyses.– R&D&I – the latest research news from leading international research centers.

DON´T MISS THE wEbSITEIn addition, Bright Market Insight's website, which requires individual login credentials, is updated with industry-specific news, interviews, market analyses and long-term forecasts 12 months a year. The package also enables subscribers to download key diagrams for their companies' internal powerpoint presentations via brightmarketinsight.com.

We hope you enjoy an insightful read

WELCOME TO A BRIGHT fUTURE

Bright Market Insight

CONT

ENT

CAr l JohAr dE d itor-i n-Ch i E f

4 BRIGHT MARKET INSIGHT

MORE EffICIENT AND fLEXIBLE PRODUCTION

WITH STRICTER CONTROL Of RAW MATERIALS

AND ENERGy

In this interview, Peter Berg, forest industry expert at McKinsey & Company describes four distinct, major development trends currently taking place in the forest industry: 1. Radical change in consumption habits. 2. Geographic shift in production. 3. Competition for raw materials. 4. Greater demand for sustainability.

HOw IS gLObAL CONSuMPTION Of PAPER PRODuCTS CHANgINg?“In the west we’re seeing a stagnating or falling market, with less paper being used (particularly graphic paper) than before, while consumption of paper is still growing strongly in emerging economies. Reports in-dicate a decline of as much as 40-50 percent per capita in the west in the past decade, which is putting the industry under im-mense strain. In my view, the decline in the consumption of print and writing paper will be even faster than it has been in the past. In developing countries, people tend to adopt technological innovations faster and switch directly to reading newspapers on mobile phones and the Internet, i.e. technological leap-frogging. If you look at where the penetration of mobile subscriptions is the highest, it’s in the emerging markets where people have simply bypassed landline telephony and its costly infrastructure. On the packaging side the picture is brighter, with growth more or less all over the world. However, growth in the west remains slow and hesitant.”

HOw QuICkLy ARE CONSuMPTION HAbITS CHANgINg?“We usually see a critical threshold for adopting new technology at around 20-25 percent. Above this level, the trend accele-rates. When the penetration of broadband reaches around 25 percent, the Internet

has become a natural part of everyday life. When 25 percent of employees use e-readers at work, the number of uses increase and the spread rate accelerates, which has a direct impact on paper consumption. Technology is constantly developing and in the last two years the number of magazine apps for e-readers has increased twenty-fold, while books and magazines have gone digital and are now available online. The one thing that has prevented e-book reading from spreading even faster are the critical legal issues about rights and pricing. It now appears as though the big US publishing firms and newspapers have found a workable method for paid information.”

wHAT PRODuCTION CHANgES DO yOu ANTICIPATE fROM THIS SHIfT IN TECHNOLOgy?“Production is largely being built up where the consumption is. This means that much of the production is shifting to Asia, and in particular China, which from its previously modest levels has become the world’s largest market for paper consumption. Asia previously accounted for one-third of the global production of graphic paper, today it accounts for half.

However, new question marks have arisen about future pulp production in South America and Asia.

In South America, per-country prices and payroll expenses have risen drastically

Peter Berg’s advice to the forest industry about the paradigm shift:

PARADIGM SHIFT

CONSUMERDECLINE PER CAPITAIN THE wEST IN THE PAST DECADE

50%

Author: Carl Johard, Stockholm

5BRIGHT MARKET INSIGHT

while in China the government has signal-led that it intends to limit the production of paper in certain regions while stimula-ting domestic pulp production.”

DO yOu THINk THAT MILLS wILL bECOME MORE DIVERSIfIED, wITH MORE NEw PRODuCTS AND bROADER PRODuCT PORTfOLIOS?“Yes. We’re in the middle of a paradigm shift. The problem for the forest industry is that it operates in markets mainly for the production of commodities, where investments are high, margins low and it’s far too easy for competitors to build new, more efficient capacity. For future success, the industry needs to develop unique, in-demand and higher-value products in new, smaller segments and niche areas where not everyone can or wants to get involved.”

DO yOu EXPECT gREATER COMPETITION fOR RAw MATERIALS?“Yes. It’s becoming absolutely vital to keep the costs of raw materials and energy under control. Expansion will take place where the prices of raw materials are at their lowest.

If Europe and other regions and countries are to meet their environmental goals, the use of biomass for heating and power will rise sharply. Meanwhile we’re seeing the quality of recycled fibres go down, which will result in the price of recycled fibre, and consequently also fresh fibre, go up. We’re also seeing rising demand for stronger material and reinforcement pulp, which is good news for long-fibre pulp mills in the Nordic region and North Ame-rica. This all means that locally there may be fierce competition for wood materials.

PARADIGM SHIFT

gLOb

AL

You must be lighter on your feet and able to respond quickly to structural changes, says Peter Berg, McKinsey.

the various segment of the pulp market.

Wood demand will increase in Europe, with the main driver being energy source applications.

800

750

700

650

600

550

500

450

400

350

300

2010 2015 2020 2025 2030

m3 million

Paper & Board392 million t

Pulp167 million t

Recycled Fibre224 million t

43%57%

80%20%

34 %66 %

54 %46 %

64 %36 %

Chemical134 million t

Mechanical33 million t

Market Pulp46 million t

Integrated Mills85 million t

Hardwood24 million t

Softwood / Other22 million t

Eucalyptus16 million t

Acacia / Other8 million t

PuLP MARkET STRuCTuRE

EuROPEAN DEMAND fOR wOOD BIOenergy TrADITIOnAl wOOD usAge

sOurce: eu wOOD

sOurce: FIBrIA

6 BRIGHT MARKET INSIGHT

There are still significant expansion oppor-tunities in the southern hemisphere. China, which is a major pulp importer, is the ‘joker in the pack’. The country intends to expand its short-fibre pulp capacity and there are clear directives from the government for the country to increase its pulp production, which means more plantations but also an increase in imported raw materials. At the same time, the fear is that, because of the high cost of land, the price of Chinese fibre

will remain high by international standards.

Brazilian plan-tation eucalyptus is much cheaper than Chinese fibre. However, Brazil is currently experiencing a period of great uncertainty, with rising land costs

and payroll expenses. Today you need to venture further inland to find suitable locations, which in turn requires more infrastructure investments and means higher transport costs. We will probably also be seeing an increased cost base in this part of the world.

Russia, on the other hand, has around 20 percent of the world’s timber stocks. But it has no infrastructure and the cost of buil-ding the necessary road and rail networks would be gigantic. International interest in Russia has also been dampened as a result of reports of uncertain owner relationships, cumbersome legal structures and business difficulties.”

HOw wILL SuSTAINAbILITy REQuIREMENTS AffECT THE MARkETS?“It’s hard to say – it depnds on the situa-tion. Growing environmental awareness and CSR initiatives are fuelling demand for sus-tainable materials. This could lead to plastic being replaced by paper, paperboard and other sustainable bio-materials, but also, in some cases, to paperboard being replaced by plastic. In all, the general trend is a reduced need for packaging.”

wHAT DO yOu THINk wILL HAPPEN TO THE PRICE Of PuLP?“There’s a limit to how far pulp prices can can increase. The paper producers must either see their margins shrink or they will need to increase their paper prices. In many paper and paperboard segments, it’s the wrong time to increase prices. It would only lead to reduced demand. Margins are at breaking point, which will probably help to accelerate the market trend towards more refined products.”

IS THE PuLP MARkET bECOMINg LIgHTER ON ITS fEET?“Yes. The forest industry has always had a long planning horizon when it comes to raw material purchases, and this culture has often also filtered through to forest industry companies and their marketing. But this ap-proach is becoming harder to sustain as the market is changing more quickly as a result of rapidly changing consumer habits and financially unstable producers.

China’s pulp buyers have been very opportunistic in the last ten years, causing a change in the market with greater price fluctuations and shorter planning horizons. So today you need to be lighter on your feet and must be able to respond quickly to structural changes.”

HOw wILL THIS CuLTuRAL CHANgE MANIfEST ITSELf?“What we’ll probably see is further conver-sion of machinery and a growing number of swing machines. More companies, some of them Chinese, are considering switching to flexible pulp mills, which can quickly switch from paper pulp to dissolving pulp and back. This will make it even harder for us to understand and anticipate the dynamic in the market.”

wHAT ADVICE wOuLD yOu gIVE yOuR CLIENTS IN THIS uNCERTAIN MARkET?“To survive, you need to be highly mobile and light on your feet, have your own production flexibility and an in-depth understanding of how to improve production efficiency in a volatile market. It’s also a good idea to supplement your basic strategy by guaranteeing a long-term supply of raw materials.”

PARADIGM SHIFT

THE CRITICAL25%FOR ADOPTING NEw TECHNOlOGy

THRESHOLD

7BRIGHT MARKET INSIGHT

The viscose market is experiencing global growth. All the plans for new capacity for dissolving pulp in China, South-East Asia, Latin America and North America entail an imminent risk of a drop in price.

“You need to have a clear and distinct market for your products, otherwise you risk ending up in an open, less attractive spot market where prices could fluctuate con-siderably,” says Peter Berg, forest industry expert at McKinsey in Stockholm.

In the first half of the 20th century, the viscose fibre industry had a period of strong growth, but this was followed by an equally dramatic decline in the second half of the century because of the success of the oil industry‘s newer synthetic fibres. However, in recent years the industry has been show-ing signs of recovery.

Today, 60 percent of the world’s textiles are oil-based synthetic fabrics, around 30 percent are cotton-based while around 5 percent are viscose-based, depending on the sub-segment.

RISINg TEXTILE CONSuMPTIONWith a growing global population, the consumption of textiles will continue to increase. Cotton production, on the other hand, has reached its ceiling and will strugg-le to keep up with demand. More agricul-tural land is needed for food products, while countries such as India and Pakistan recently introduced export restrictions on cotton.

“Despite shrinking crop areas, greater efficiency in cotton harvests is expected to help keep cotton production at today’s sales

MAjOR CAPACITy INCREASES CAUSE VOLATILITy IN THE VISCOSE MARKET

that the price differential in relation to regular pulp will decrease with time,” says Peter Berg, forest industry expert at McKinsey in Stockholm.

‘NORMAL’ PRICE DIffERENCESThe price of dissolving pulp has recently been hit by short-term dynamic changes.

“The rise in the price of dissolving pulp in 2007, and most recently in 2010, was caused by an increase in the price of oil – and therefore also the price of polyester – while the price of cotton also rose as a result of years of poor harvests. The market has subsequently adjusted and prices have dropped. The difference in price between paper pulp and dissolving pulp is now, as before, USD 200-250 over the long term.

levels, which are equivalent to 26-28 mil-lion tonnes per year. In a growing market, the natural alternative will instead be viscose and oil-based fibre,” says Lars Winter, CEO of Aditya Birla Domsjö.

gROwINg INTEREST IN DISSOLVINg PuLPThis market trend has precipitated a gro-wing interest in dissolving pulp. The viscose market is experiencing global growth. New greenfield plants are being built in South-East Asia, while in Europe and in North America, older pulp mills are being conver-ted for dissolving pulp production.

“The volume trend for regular paper pulp and rising prices are persuading more people to switch to dissolving pulp. But when the capacity increases, there is a risk

Author: Carl Johard, Stockholm

gLOb

AL

in a growing market, the natural alternative to cotton will be viscose fibre, says lars winter, CEO of Aditya Birla Domsjö.

VISCOSE

8 BRIGHT MARKET INSIGHT

This means that when pulp prices go up, so do dissolving pulp prices, and vice versa,” says Peter Berg.

IMPORTANCE Of STRONg MARkET POSITIONPeter Berg says that mills in the Nordic region and North America that are considering converting to the production of dissolving pulp will not necessarily hit the jackpot.

“It will be hard for them to compete with low-cost companies, so they'll need to find their own unique position in the market where they can manufacture some form of specialised dissolving pulp or find a collaboration partner further along the refinement chain. You need to have a clear and distinct market for your products, otherwise you risk ending up in an open, less attractive spot market, where prices can fluctuate considerably,” says Peter Berg.

fOCuS ON gREEN PROCESSESThere is one cloud on the horizon for viscose: like its competing fibres: polyester polyester and cotton, it is associated with certain environmental problems.

“The viscose process contains carbon disulphide, a chemical which is hard to eliminate and which makes the product less eco-friendly. From an environmental perspective, it’s better than cotton and polyester, but today there is considerable interest in other chemical processes such as Lyocell, which does not contain this chemical,” says Peter Berg.

Viscose has been refined in recent years, which has resulted first and foremost in greater comfort, a superior fit and higher quality.

“But to succeed in the highly competitive textile market, the forest industry needs to develop a material that is far superior to cotton and also cheaper, greener and stronger. The research-driven trend of developing new fibre variants will continue,” says Peter Berg.

You need to have a clear and distinct market for your products, otherwise you risk ending up in an open, less attractive spot market, where prices can fluctuate considerably, says Peter Berg, McKinsey.

VISCOSE

9BRIGHT MARKET INSIGHT

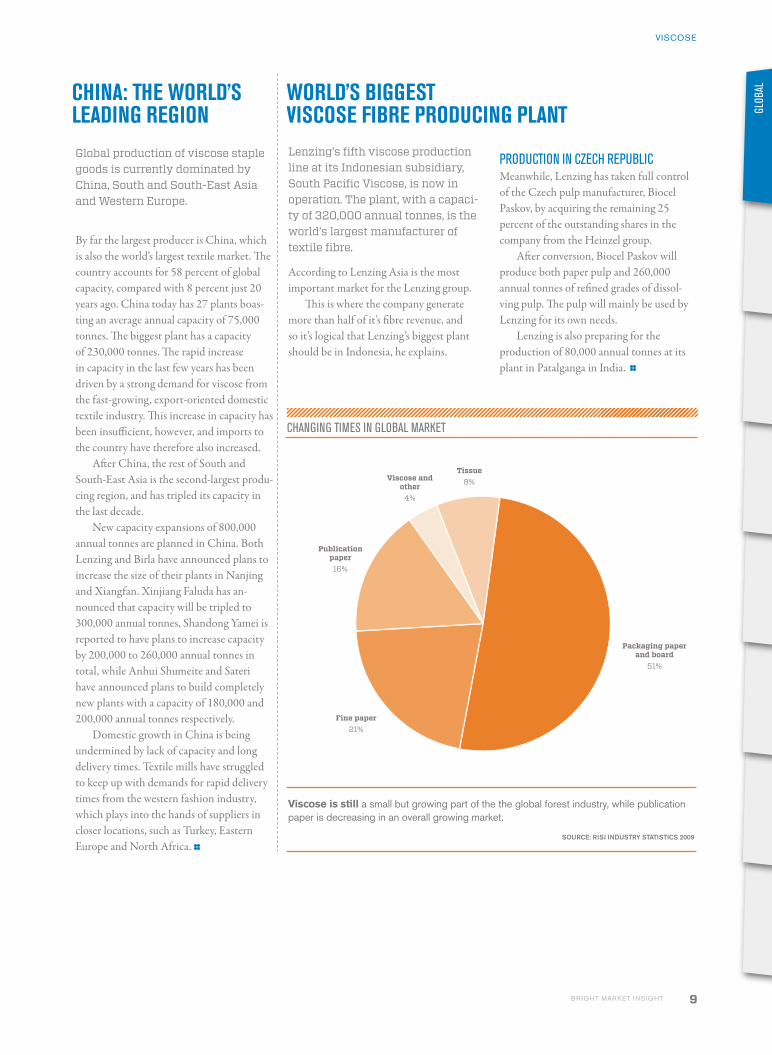

Global production of viscose staple goods is currently dominated by China, South and South-East Asia and Western Europe.

By far the largest producer is China, which is also the world’s largest textile market. The country accounts for 58 percent of global capacity, compared with 8 percent just 20 years ago. China today has 27 plants boas-ting an average annual capacity of 75,000 tonnes. The biggest plant has a capacity of 230,000 tonnes. The rapid increase in capacity in the last few years has been driven by a strong demand for viscose from the fast-growing, export-oriented domestic textile industry. This increase in capacity has been insufficient, however, and imports to the country have therefore also increased.

After China, the rest of South and South-East Asia is the second-largest produ-cing region, and has tripled its capacity in the last decade.

New capacity expansions of 800,000 annual tonnes are planned in China. Both Lenzing and Birla have announced plans to increase the size of their plants in Nanjing and Xiangfan. Xinjiang Faluda has an-nounced that capacity will be tripled to 300,000 annual tonnes, Shandong Yamei is reported to have plans to increase capacity by 200,000 to 260,000 annual tonnes in total, while Anhui Shumeite and Sateri have announced plans to build completely new plants with a capacity of 180,000 and 200,000 annual tonnes respectively.

Domestic growth in China is being undermined by lack of capacity and long delivery times. Textile mills have struggled to keep up with demands for rapid delivery times from the western fashion industry, which plays into the hands of suppliers in closer locations, such as Turkey, Eastern Europe and North Africa.

Lenzing’s fifth viscose production line at its Indonesian subsidiary, South Pacific Viscose, is now in operation. The plant, with a capaci-ty of 320,000 annual tonnes, is the world’s largest manufacturer of textile fibre.

According to Lenzing Asia is the most important market for the Lenzing group.

This is where the company generate more than half of it’s fibre revenue, and so it’s logical that Lenzing’s biggest plant should be in Indonesia, he explains.

PRODuCTION IN CzECH REPubLICMeanwhile, Lenzing has taken full control of the Czech pulp manufacturer, Biocel Paskov, by acquiring the remaining 25 percent of the outstanding shares in the company from the Heinzel group.

After conversion, Biocel Paskov will produce both paper pulp and 260,000 annual tonnes of refined grades of dissol-ving pulp. The pulp will mainly be used by Lenzing for its own needs.

Lenzing is also preparing for the production of 80,000 annual tonnes at its plant in Patalganga in India.

gLOb

ALWOrLD’S BiGGESt viScOSE FiBrE prODucinG pLAnt

cHinA: tHE WOrLD’S LEADinG rEGiOn

VISCOSE

Fine paper21%

Viscose andother

4%

Tissue8%

Publicationpaper16%

Packaging paper and board

51%

CHANgINg TIMES IN gLObAL MARkET

Viscose is still a small but growing part of the the global forest industry, while publication paper is decreasing in an overall growing market.

sOurce: rIsI InDusTry sTATIsTIcs 2009

10 BRIGHT MARKET INSIGHT

SCA Ortviken has stepped up its product development work to find new products to succeed publication paper.

“We have a bright outlook on our future. Ten years from now we will remain strong, we will have wider product portfolio, a skilled staff and be well-positioned in terms of the raw material,” says Kristina Enander, Mill Manager at SCA Ortviken.

Frantic activity at Ortviken

Ortviken paper mill, just outside Sundsvall, manufactures 880,000 tonnes of coated pub-lication paper, LWC, and uncoated paper grades on four machines. The raw material is fresh spruce pulpwood, mainly from SCA's own forests in northern Sweden.

As the global market for publication pa-per is shrinking, SCA Ortviken is reviewing its future strategy. The strategy review has led to two parallel development lines.

“In the short term we need to develop and refine the products we already have. In the slightly longer term we also need to find alternative products for our production machinery, which in due time can succeed the production of publication paper," says Kristina Enander, Mill Manager at SCA Ortviken.

The latest product in the family is Grapho-Invent, a new 90-gramme uncoated offset paper. It is part of the Bright Future project, where last year PM5 was rebuilt to produce higher-quality uncoated paper. The project, which was completed in the autumn of 2012, included the expansion of the plant’s bleaching capacity and the rebuilding of both PM5 and the water treatment plant.

STRuCTuRAL CHANgESThe structural change of the last few years, with fewer people reading newspapers, has prompted SCA to begin probing for alternative products. “We are seeing dramatic changes in the market and we need to do something about our situation. We need to find new pro-

ducts for Ortviken. It is a process we have already begun and will be stepping up in the near future. We will be raising the tempo of this development work significantly,” says Enander.

INCREASED EffICIENCyIn other respects the plant is continuing its endeavour of increasing productivity and reducing costs.

“We can hold our own in the industry when it comes to factors such as develop-ment, lower costs and increased producti-vity, but we will not rest on our laurels. We are now focusing on making our mainte-nance work more efficient,” says Enander.

SCA will invest some USD 57 million in expanded cooperation between its ope-rations in Sundsvall – SCA Ortviken and SCA Östrand – and the energy company Sundsvall Energi, increasing its deliveries of energy to Sundsvall's district heating grid.

STRONg OuTLOOk fOR THE fuTuREOver its 150-year history, Ortviken has completed several successful product renewals and the plant has every possibility of being a strong and successful industry in the future.

“We have access to a fantastic fresh fib-re; we have an industry that infrastructural-ly-speaking is located near our raw material and we have our own port. It is also a good position to be in when it comes to other developed products, and we will continue producing publication paper at Ortviken for a long time to come,” says Enander.

The energy extracted from Ortviken's flue gas condenser provides surplus heat to the district heating network corresponding to the heating requirements of 5,000 single-family houses per year. And three years ago a new mechanical pulp line was opened, which paves the way for significant quality improvements and increased capacity.

"Ten years from now we will remain strong, we will have a broader product port-folio, a skilled staff and be well-positioned in terms of the raw material,” says Enander.

Author: Carl Johard, Sundsvall

We are seeing dramatic changes in the market and we need to find new products for Ortviken, says Kristina Enander, Mill Manager at SCA Ortviken.

SCA

11BRIGHT MARKET INSIGHT

The winds of change are blowing through the SCA R&D Centre in Sundsvall, Sweden. Alongside the traditional product development work, more and more time is being spent on researching new materials and new business. And this research has already come a long way in some areas.

Full FOcus On new materials and new business

Major changes have taken place on the research front over the past year, due to the continuing dip in the market for publica-tion paper and the sale of SCA’s packaging business. This has prompted SCA to restructure its research operations.

"We are now set to further develop the organisation, making it more business-oriented and more closely tailored to gene-rating new innovations and new business. Our task for the future will be to develop and propose new products, materials and processes. We need to find new applications for the fantastic forest raw material that we have,” says Örjan Petterson, adding that SCA R&D Centre will increasingly work with the whole of SCA, including the hygiene business, the new energy division and also SCA Timber.

NEw R&D AgENDAThe research centre has been working on a handful of transformation projects over the past two years.

“We’ve identified a number of transfor-mation areas that we’re now working on. In many cases, these are areas that we’ve never researched before.”

The areas identified include packaging, construction materials, composites, chemi-cals, microfibrillated (nano)cellulose and pharmaceuticals.

Packaging is an interesting area of research, and a field in which both the SCA R&D Centre and Mid Sweden University have material and design expertise.

“Future Packaging products. Our strength at SCA is that our fresh fibre raw material is not only renewable, but also recyclable and biodegradable. We are one of few European producers of kraftliner from fresh wood fibre.”

bELIEf IN bIOREfINERIESOn the chemical front, Ortviken has been delivering extremely high-quality turpen-tine at a rate of 300 cubic metres per year since 1984.

“We are the only forest industry manufacturer in the world to produce turpentine of such high quality.”

Together with Mid Sweden University and the Fibre Science and Communication Network (FSCN), SCA R&D Centre is now investigating the potential to manufacture other chemicals.

“There are a number of substances that we can make use of, both from the wood and the wastewater. This is set to be a growth area of the future,” says Örjan Petterson.

MICROfIbRILLATED CELLuLOSEMicrofibrillated cellulose, or nanocellulose, is another research area that is helping to develop stronger fibres and materials. This cellulose is of specific interest when it comes to construction and composite materials.

“Composite materials are particularly interesting to us, especially if they can be manufactured on a large scale on existing paper machines. Many of the paper pro-ducts that we already produce are a kind of composite material, comprising – as they do – fibre, pigments and various surface layers,” says Örjan Petterson.

Author: Carl Johard, Sundsvall

EuRO

PE

OF HIGH quAlITy TuRPENTINE SINCE 1984

300the SCA r&d Centre has been working on a handful of transformation projects over the past two years.

SCA

PER yEAR CUBIC METRES

12 BRIGHT MARKET INSIGHT

SCA Östrand produces different pulp grades, energy and chemicals. With a modern, efficient and flexible production apparatus in place, new products and expansion are on the agenda.

SCA Östrand is already a fully-functional biorefinery with a capacity of 430,000 ton-nes of totally chlorine free (TCF) bleached kraft pulp, 95,000 tonnes of chemical thermo-mechanical (CTMP) pulp and 450 GWh of green electricity, while also ma-nufacturing and selling district heating and chemicals, such as turpentine and tall oil.

“We have gradually increased our capacity over the last 20 years and refined this concept even further. It is an integral part of the sulphate process, where half the wood is turned into pulp and the other half is processed into energy and chemicals. We invest substantial research resources in creating new – and developing existing – pulp business with our raw material, using our processes as the starting point. Being part of a company with such a broad, deep expertise about the whole product and production chain is a huge competitive ad-vantage for us,” says Ingela Ekebro, CEO of SCA Östrand and Pulp Division Manager.

The development of new products is closely interlinked with SCA Östrand’s his-torical growth and future expansion plans.

“Our long-term goal is to double our production capacity to 800,000 tonnes of kraft pulp, 110,000 tonnes of CTMP pulp and 500 GWh of energy plus additional bi-products. It is necessary in order for us to have a strong production economy in the future.”

HALf INTERNALLyApproximately half of the produced kraft pulp is used in the production of SCA’s own hygiene and printing paper. The rema-inder is sold to external customers. CTMP

pulp is used in products such as sanitary towels, printing paper, board products and tissue.

gOOD AT PROMOTIONAL bATCHESBut what makes SCA Östrand truly unique is the mill’s long experience of alternating production.

“When we stopped producing short-fibre pulp, we were quick off the mark to produce alternating batches of softwood kraft pulp. Today we manufacture several different grades of softwood pulp so that we can customise the fibre properties for the end-products they are intended for,” says Ekebro.

Switching between campaigns, which involves the whole production chain from choice of wood raw material to finished product is based on customer orders and a carefully timed delivery plan.

“Here we have the help of our process design, which can handle these rapid switches. This has been a major success factor for us,” says Ekebro.

PRODuCTSSCA Östrand has developed special pulp grades with properties tailored for printing and tissue paper. Today the plant has a number of different kraft pulp products and even more on the CTMP side.

“We are striving to find good pulp products for highly dedicated end-users. Our hallmark is developing and being able offer customised grades for tissue, kraft board and printing products,” says Ekebro and continues:

“In recent years we have also been focu-sing on our own brand names and in this context, our strong environmental profile has been particularly significant for our customers. Our brand name work has helped us create knowledge in the organisa-tion and a clarity in the communication to our customers.”

Accordingly, SCA Östrand recently presented some of its latest grades such as Luna and Celeste Filter, which is a kraft pulp particularly suitable for filter products.

EffICIENCy ENHANCEMENT A CHALLENgEIn order to reach its future capacity targets and to be profitable in long term perspec-tive and continue being a strong player in the forest industry, SCA Östrand focuses firmly on efficiency enhancement.

We are sriving to find good pulp products for highly dedicated end-users, says Ingela Ekebro, Mill Manager at SCA Östrand.

SCA

EqUIPPED fOR THE fUTURE

Author: Carl Johard, Sundsvall

13BRIGHT MARKET INSIGHT

“These are turbulent times for the industry. Products vanish and new ones appear. Whatever we do really well today may not be good enough tomorrow. This is why we need to be supremely efficient in everything we do. We are extremely committed to maintaining a high produc-tivity level and optimising the fibre for the right end-product,” says Ingela Ekebro and continues:

“We are working hard on our Lean implementation and are becoming skilled in making day-to-day improvements. This includes a more strategic and structured skills development for our 360 employees. Processes and technology can all be bought, but our competitive advantage is our personnel.”

RESEARCH AND DEVELOPMENT Research and development initiatives are equally as important.

“We need to be even more flexible and better at solving problems for our existing customers. We work closely with SCA R&D Centre and Mid-Sweden University and we have our own development unit which serves as a link between the research and our mills. We also have a product group, headed by our Marketing Manager where we combine resources from marke-ting, R&D and production, which decides which products we should focus on. It is an approach that we see as our competitive advantage.”

But SCA Östrand does not limit its innovation work to products. It is equally important to be innovative in process development.

“We pursue both product and process development and we focus on developing efficient processes as well as good products. Energy efficiency enhancement is also part of the process work, i.e. consuming as little energy as possible and selling the energy we do not use.”

bRIgHT fuTuREIngela Ekebro believes in a bright future for SCA Östrand.

“We have high level of competence, a well-invested mill with dynamic plans for the future and demand for wood-fibre based pulp is only getting stronger. It is a market where we should be competing in earnest,” says Ekebro.

EuRO

PE

the wind farms will contribute to around 3,000 Gwh of energy per year.

SCA

heavy investments in wind pOwerSCA Energy develops renewable energy and produces refined and unre-fined forest-based biofuels, in addition to managing SCA’s wind-power assets. SCA is one of Europe’s largest suppliers of forest-based biofuels.

SCA Energy also includes SCA’s ventures regarding wind power, whether they are set up as land leases, joint ventures or own development projects.

HEAVILy INVESTMENTSStatkraft and SCA are jointly planning the construction of 360 wind turbines in northern Sweden. Planning has also begun on a further 300 wind turbines together with Norwegian company Fred Olsen Renewab-le and 270 turbines are being planned presently in collaboration with E.ON. In total the investments may amount to around SEK 30 billion for more than 900 wind turbines.

“With all our projects we can achieve close to 5 percent of Sweden’s electricity consumption today. In the wind park areas, only a few per cent of the land is actually used for roads and wind turbine foundations. The rest of the land in the area is managed for forestry as elsewhere. We are thrilled about being able to combine two lines of business – energy production and forest management, where we among other things get access to good roads for timber transports. This increases the value of our forest,” says Head of SCA Energy Åke Westberg.

14 BRIGHT MARKET INSIGHT

WE ARE IN THE MIDDLE Of A SEVERE

STORM – BUT THE END IS IN SIGHT

In these difficult economic times, SCA Forest Products continues with unwavering commitment to innova-tion work.

“We’re not seeing any growth in demand for publication paper, so to keep production moving forward, we need to put all the major invest-ments we’ve already made at our plants into use for developing the next generation of products,”says Ulf Larsson, President of SCA Forest Products, in this interview.

wHAT kIND Of SHAPE IS TODAy’S fOREST INDuSTRy IN?“We’re going through tough times and this is affecting every business that is export-led. The Western forest industry is currently in the middle of a severe storm caused by low economic activity, combined with a struc-tural downturn, particularly in publication paper. In Sweden, we’re also suffering the consequences of a very strong domestic currency, which has a negative impact on all the Swedish exporting industries. Although there are strong indications that the end is in sight, it’s going to take a long time before we see any significant recovery.”

HOw ARE yOu DEALINg wITH THIS?“We’re working on it constantly. We want to avoid the big gestures. A healthy organisation has a constantly ongoing de-velopment process. We always try to work consistently on our rationalisation and improvement work.”

HOw RObuST ARE SCA fOREST PRODuCTS’ INDuSTRIAL PLANTS?“We have large and robust production plants and access to fresh fibre raw material of fantastic quality. Thanks to our forward-thinking energy investments, we’ve been able to build up a cost-efficient internal energy supply, which has given a huge boost to the competitiveness of the factories. The mills in Sweden are located close to the supply of raw material, but they have toug-her conditions to contend with in terms of long distribution routes to their customers.”

yOu HAVE CHOSEN TO fOCuS STRONgLy ON INNOVATIONS...“Yes. Whatever our circumstances, and ir-respective of any other decisions, we need to come up with the products of tomorrow in order to maintain production and put the major investments we’ve already made at our plants to best use. Since we’re not seeing any growth in demand for publication pa-per, we’ve launched an innovation process aimed at developing the next generation of products.

“The important thing is for us to take a clearly innovative approach to our business, constantly reviewing it in a drive to improve efficiency and profitability. Innovation always involves hard work with a long-term focus. Successful innovation work leads to differentiation and added value for SCA’s customers and consumers, which in turn establishes strong, market-leading and value-creating products and brands.”

HOw ARE yOu HANDLINg THE STRuCTuRAL DOwNTuRN IN PubLICATION PAPER?“For one thing, we’ve sold off our Laakir-chen paper mill in Austria and our Ayles-ford paper mill in the UK, which has re-duced our exposure to standard newsprint. At the same time, we’re working intensively at Ortviken to gradually reposition our product portfolio.

“We have several exciting projects in the pipeline, where we’re working with a number of strategic customers. In some cases, we’re even at the point of test runs with customers.

“In parallel with this, we’ve invested a massive SEK 350 million in PM5 to increase its capacity and manufacture brand new grades of publication paper with higher grammages.”

HOw IS THE INNOVATION PROCESS gOINg fOR SCA’S PubLICATION PAPER fACILITIES?“The large industrial sites have previously enjoyed fantastic margins and stable market trends. However, we can no longer take continued market growth for granted, so I’ve asked the organisation to review the core processes and look into the possibility of generating revenue from supplemen-tary product flows. Alongside this, we’ve established an organisation and a process for developing products that may come to replace the existing ones. The aim is to ensure that our plants remain robust in the future.

Ulf Larsson, President of SCA Forest Products:

Author: Carl Johard, Sundsvall

SCA

15BRIGHT MARKET INSIGHT

“We’re taking a short, medium and long-term approach to our development work. We have skilled and committed people who know our business inside out and it’s important to draw on all the great ideas and resources that we have internally.”

wILL wE SEE CONTINuED INVESTMENT IN ENERgy?“Absolutely. We’re currently sharpening our strategic focus on energy. Demand for renewable energy is bound to rise, and the desire to switch to greener technology is expected to remain strong. We’ve set up the new business unit SCA Energy to run and develop our business in renewable energy. We’re planning a large number of wind tur-bines. On top of this, we’ll be looking at a range of other processes through the prism

of our strong position as a major European owner of production facilities with surplus heat, forests and watercourses.”

wHAT OTHER AREAS ARE IN THE SPOTLIgHT?“We’re taking a very open-minded ap-proach to identifying new products for the future, based on our relative strengths compared with our competitors. Packaging is, of course, an area of interest. We have a competitive raw material structure, we have existing production processes and we have an in-house organisation and expertise in research and marketing with a focus on packaging. As a group, SCA has a long-term focus on developing its leading positions in advanced packaging in segments with a high degree of refinement. These segments

have a more stable rate of growth and offer us future expansion prospects with good growth. We’re also reviewing the potential in complementary product flows.”

wHAT IS THE TIME HORIzON HERE – wHEN wILL ORTVIkEN CHANgE ITS PRODuCTION STRATEgy?“Publication paper will remain at Ortviken for a good while yet. In terms of higher quality publication paper, we’ve been successful in developing popular products even in a weak market and that work will continue. We’ll also be continuing our move towards more value-added products. These things tend not to involve abrupt switch-overs. SCA Ortviken will see a cautious and gradual change and transition to other products.”

EuRO

PE

We will continue our move towards more value-added products, says ulf larssson, President of SCA Forest Products.

SCA

SCA ORTVIKEN WILL SEE A CAUTIOUS AND GRADUAL CHANGE AND TRANSITION TO OTHER PRODUCTS

PH

OTO

: SC

A

16 BRIGHT MARKET INSIGHT

ADITyA BIRLA HAS BIG PLANS fOR THE DOMSjÖ BIOREfINERyAditya Birla Group has big plans for the Domsjö Fabriker Biorefinery in Örnsköldsvik in Sweden. The Birla group has acquired Domsjö to develop the company and its products, opening up new possibilities for the future.

Since 2011, Domsjö Fabriker has been a part of the Aditya Birla Group, which is one of India’s leading commercial spheres. The group is also the world’s largest manu-facturers of viscose staple fibre. In addition to Domsjö Fabriker, the Pulp and Fiber business area runs three plants in Canada – of which the latest addition, Terrace Bay, was acquired this year – and one in China with similar manufacturing of viscose staple fibres and viscose filaments.

SIgNIfICANT INVESTMENTS In the last ten years Domsjö Fabriker has invested more than EUR 180 million in the expansion of one of Sweden’s first bio-refi-neries which produces specialty cellulose, lignin, bioethanol, biogas, bioresins and carbon dioxide.

“The latest expansion programme includes investments in a new wood room, a second lignin dryer and a capacity increase in the manufacturing process of specialty

cellulose.” says Lars Winter, CEO of Domsjö Fabriker. He adds: “We are now continuing an investment plan that was begun by the previous owners.”

LEADINg MANufACTuRER Of SPECIALTy CELLuLOSEThe development programme will increase Domsjö Fabriker’s cellulose annual capacity from today’s figure of around 200,000 to 255,000 tonnes.

“This means we can grow alongside our customers in the expanding textile market. We will also be able to increase our products’ refinement value,” Winter says.

Specialty cellulose is today Domsjö

Author: Carl Johard, Sundsvall

Specialty cellulose is today Domsjö Fabriker´s main product.

ADITyA BIRlA

17BRIGHT MARKET INSIGHT

ADITyA BIRLA HAS BIG PLANS fOR THE DOMSjÖ BIOREfINERy

Fabriker’s main product. “We are one of the world’s leading ma-

nufacturers of viscose, with a seven percent share of the world market,” he says.

Specialty cellulose is used mainly in viscose fabrics and in hygiene products, where it serves as an alternative to cotton. But it can also be found in pharmaceuticals, as a binding agent in food products and has long been used in the heat shields of NASA’s space capsules.

INCREASED MARkET PRESENCEWith Aditya Birla, the company’s market presence has increased.

“We now have access to market chan-nels that benefit us greatly, and also a competent organisation that is enormously strong on resources.”

As well as being a strategic supplier of specialty cellulose to the Aditya Birla group’s globally expanding viscose fibre production, Domsjö also supplies the open and growing global viscose market.

“Cotton production is reported to have reached its ceiling and will have difficulty keeping up with rising demand. Viscose is the natural alternative,” says Winter.

RANkED NuMbER TwO gLObALLy IN DRIED LIgNINDomsjö Fabriker’s other main product is lignin, which is primarily used as an additi-ve for concrete. Lignin improves the liquid properties of concrete and thereby reduces the need for cement. This is beneficial for the environment since the manufacture of cement causes considerable emissions of carbon dioxide.

A single kilo of lignin added to a mixture of concrete is calculated to reduce carbon emissions caused by the manufactu-re of cement by 20 kg. The manufacturing capacity of dried lignin will double to some 120,000 tonnes with the investment in a second lignin dryer.

“Consequently, we will have a 10% share of the world market and become the second largest supplier in the world for dried lig-nin,” says Lars Winter. “During the autumn of 2012 we launched a new product on the market. It is the first lignin product to be based on a proprietary and patent-pending technology and it provides Domsjö with access to a new market segment.”

PROgRESS AT THE ETHANOL PANT Bioethanol is the Domsjö biorefinery’s third business area and it is currently being produced at unprecedented levels in the ethanol plant.

In past years, the process has been fine-tuned, which has led to capacity increases. The goal is to increase annual production to 14,000 tonnes. With the planned increase

in the manufacture of specialty cellulose, a continued positive trend is expected for the ethanol plant, which has an absolute maximum annual capacity of 20,000 tonnes of ethanol.

SwEDEN’S LARgEST PRODuCER Of bIOgASIn addition to the three products, Domsjö also produces methane gas from the bio-treatment of effluents and smaller volumes of bioresin and carbon dioxide. Biogas from the biological treatment plant fuels the two own lignin dryers and supplies heating which covers 20 percent of the plant’s energy needs.

Domsjö is also planning to manufacture cellulose nanofibre from the plant’s cellulose sludge.

The proportion of recovered sludge from the manufacturing of cellulose nano-fibre is 95 percent. Specialty cellulose from Domsjö is very pure, which means that the fibre does not need be treated before manufacturing. The goal is to create new material made from residual products, the-reby increasing the value across the whole production chain.

“All combined, these factors give us good cause for our motto, ‘We make more from the tree,’” says Lars Winter.

EuRO

PE

The India-based Aditya birla group is a leading multinational conglomerate, comprising some 50 companies and 120 produc-tion units on six continents and in 36 countries. It is also the world’s largest manufacturer of viscose fibre. group sales total uSD 35 billion and the group has 133,000 employees.

Aditya Birla manufactures viscose staple fibre in India, China,

laos, Domsjö Fabriker in Sweden and at three plants in Ca-

nada: Nackawic, AV Cell in New Brunswick and Terrace Bay.

Domsjö Fabriker occupies an unique position among Adi-

tya Birla’s pulp mills, being the only mill to have an advanced

research operation.

The Group plans to expand capacity by the equivalent of

120,000 annual tonnes in India and 142,000 annual tonnes in

South-East Asia.

number One in the wOrld

domsjö fabriker occupies an unique position among Aditya Birla´s pulp mills, being the only mill to have an advanced research operation.

ADITyA BIRlA

18 BRIGHT MARKET INSIGHT

STEADy INCREASE IN WOOD GROWING

COSTS IN SOUTHERN CHINA

China has temporarily lost its appetite for Western logs due to the economic slowdown. But there are signs that a recovery is on its way.

The slowdown of the Chinese economy, combined with worries about a “bubble” in the big cities’ housing markets, led to a cont-raction in construction activities in China during 2012. This caused reduced demand for lumber, and a sharp decline in imports of softwood logs and lumber to the country.

TIME fOR RECOVERyWith reduced demand for logs in the lumber industry in China, log prices fell throughout most of 2012. According to Wood Resources Quarterly (WRQ),

Author: Jan Hökerberg, Shanghai

120

100

80

60

40

20

0

2000 2005 2010 2015e

tonnes m

CHINESE fIbRE uSAgE wAsTe pAper nOn-wOOD pulp wOOD pulp

China will continue to see rising wood pulp production along with rising imports of wood chips to make that pulp.

luMBER DEMAND

sOurce: cHInA pAper AssOcIATIOn, MIIT

19BRIGHT MARKET INSIGHT

Steelmakers, cement producers and con-struction machinery manufacturers saw their sales soar as the stimulus plan opened the spigots on funding for roads, railways, ports, airports and power plants, among other things.

In the spring of 2009, the collapse of the US housing market forced log prices in the states of Oregon and Washington to their lowest levels since the early 1980s.

When Chinese traders discovered that US logs were a bargain, they started to aggressively buy them to support the construction boom in China. Prices went up for 18 months and peaked in May 2011, after more than a 100 per cent increase.

In 2011, China used almost 10 per cent of the softwood lumber produced globally. Canada and Russia are the two dominant suppliers of softwood lumber to China, together accounting for 84 per cent of total imports, with the US, Chile and New Zealand comprise most of the remaining import volume.

RISINg PuLP PRODuCTIONChina will continue to see rising wood pulp production along with rising imports

average import softwood log prices in the third quarter of 2012 were down 13 per cent from a year ago, and domestic Chine-se-fir log prices have fallen about 6 per cent in 12 months.

WRQ also reported that China’s im-ports of logs and lumber fell by 19 per cent in the first eight months in 2012 compared to the same period a year earlier. By volume, log imports were down 17 per cent and lumber imports down 5 per cent.

However, the Wood Markets’ China Bulletin has reported that China’s wood product sector is expanding again, after hitting bottom in the first quarter of 2012, and predicts “that China is working its way out of its housing construction slowdown”.

TEN PERCENT Of THE gLObAL SOfTwOOD LuMbERWhen the global financial crisis hit both the US’ and Europe’s economies in the fourth quarter of 2008, China’s central government launched an enormous stimu-lus package of RMB4 trillion (US$586 billion) to boost domestic demand in both infrastructure investment and consumption during 2009 and 2010.

of wood chips to make that pulp. A new study released by RISI concludes that, large-scale papergrade market pulp produc-tion in China is not a sustainable business over time.

A steady upward trend in wood growing costs in southern China will keep China's pulp producers purchasing ever-increasing volumes of wood chips from greater distan-ces, including North and South America, at very high costs.

Wood costs in China are already almost the highest in the world, and account for as much as 70% of cash costs for bleached hardwood kraft (BHK) market pulp produ-cers in China. Market BHK producers in China have some of the newest and largest pulp lines in the world, and yet are still the high cost producers, even in their own market.

The RISI report indicates that wood growing costs in southern China will pro-bably outpace growing costs in Brazil by a wide margin over the next decade, and this suggests that large-scale papergrade market pulp production in China is not a sustaina-ble business over time.

CHIN

A &

ASIA

120

100

80

60

40

20

0

2000 2005 2010 2015e

tonnes m

luMBER DEMAND

Wood costs in China are already almost the highest in the world.

PH

OTO

: Ju

lIA

NA

yO

ND

T

20 BRIGHT MARKET INSIGHT

NEW EMISSIONSTANDARDS SET fOR CHINA’S PAPERMAKERSChina’s pulp and paper industry is one of the government’s five tar-geted sectors for stricter policies to save energy and cut emissions.

Historically, China’s pulp and paper industry has been plagued by environmen-tal problems, traditionally caused by the widespread use of outdated technology and lack of environmental awareness.

However, in recent years, China has worked hard to modernise the industry in an effort to achieve its overall environ-mental goals. The country has launched campaigns to close old machines nation-wide to reduce pollution and realise cleaner production.

20 MILLION TONNES TO bE PHASED OuTFrom 2006 to 2010, China shut down altogether more than 2,000 pulp and paper enterprises, and eliminated outdated pro-duction capacity of over 10 million tonnes. In the 12th Five-Year Plan, for 2011-2015, China plans to phase out another 10 mil-lion tonnes of backward capacity.

“The most modern machines are instal-led here in China. Actually, you have two

kinds of pulp and paper companies. You have the old ones that might be challenging regarding energy efficiency and pollution. But you have also got the ones that have been installed with facilities that are state-of-the-art. They are more modern than the ones in Europe or North America,” Pasi Laine, Metso's President of Pulp, Paper and Power, told the China Daily recently.

kEy COMPONENT Of THE CHINESE ECONOMyChina’s paper industry’s total output in 2010 stood at nearly RMB600 billion (US$ 95 billion) in value. Even if the market has slowed down since then, the industry is clearly one of the key components of the Chinese national economy.

This was reflected in the fact that the papermaking industry was one of five targeted sectors when China’s State Council issued specific energy-saving and emission-cutting policies in conjunction with the 12th Five-Year Plan in early August 2012.

Local media said that it was the first time the government had set such detailed goals for an individual industry.

HAND-IN-HAND wITH ENVIRONMENTAL PROTECTION

For pulp and paper producers, con-sumption of standard coal for making a tonne of paper and board will be slashed to 0.53 tonnes in 2015, compared with 0.68 tonnes in 2010, according to the plan.

Similarly for the production of a tonne of pulp, the plan is for 0.37 tonnes of stan-dard coal to be used in 2015, down from 0.45 tonnes in 2010.

Regarding pollutants in waste water, the pulp and paper sector will have to cut rates of both chemical oxygen demand (COD), a water emission factor describing the amount of oxygen consumed when dis-solved matter in effluent water oxidises, and ammonia nitrogen emissions by 10 per cent.

The industry-wide discharge of COD emissions will be lowered from 720,000 tonnes in 2010 to 648,000 tonnes in 2015.

For ammonia nitrogen, emissions will be reduced from 21,400 tonnes in 2010 to 19,300 tonnes in 2015.

"We should always bear in mind that economic growth should go hand-in-hand with environmental protection. Envi-ronmental protection policies should be

Author: Jan Hökerberg, Shanghai

seven FOcused areas in china’s Five-year plan

China’s 12th Five-year Plan (FyP) for the pulp and paper industry was released on 30 December, 2011. The ambitious plan

targets balanced growth of total paper and board consumption and production, putting an emphasis on rebalancing demand and

supply. The FyP identifies seven focused areas for the industry:

• Improve the raw material supply. • Increase indigenous innovation, improve technological structure. • Optimize regional development, allocate resources properly. • Conduct clean production, protect environment. • Optimise enterprise structure, promote mergers and acquisitions and implement efforts to improve industrial consolidation. • Improve product structure and product quality. Develop new and environment-friendly products, speed up the upgrading of low-end products. • Establish saving mechanisms, promote appropriate consumption. In addition, the FyP also identifies three key projects and nine support policies.

NEw EMISSION STANDARDS

21BRIGHT MARKET INSIGHT

MERGER BETWEEN TAIWANESE PULP AND PAPERMAKERS YFY Paper spins off its printing paper business to Chung Hwa Pulp.

The merger of the fine-paper business unit of Yuen Foong Yu Paper Manufac-turing Company (YFY Paper), the largest papermaker in Taiwan by revenue, into the Chung Hwa Pulp Corporation came into effect in the end of 2012.

The merger was announced in March 2012, with Yuen Foong Yu spinning off its printing paper business unit to Chung Hwa Pulp in exchange for 640 million new shares worth TND 6.68 billion (USD 230 million) to boost its ownership of Chung Hwa to 55 per cent.

SAfEguARD AgAINST PRICE fLuCTuATIONSThe deal will help to fuel revenue growth of both companies, according to analysts.

Institutional investors told the Taiwan-based China Economic News Service

(CENS) that acquiring the fine-paper business unit would enable Chung Hwa Pulp to enhance self-efficiency in supply of the material as a safeguard against price fluctuations, while heavily utilising wet pulp in papermaking to cut energy costs used in evaporating of secondary condensates. The company could see its sales revenue increase to TND 20 billion in 2013 and its profits double.

A LEADINg POSITIONYFY Paper was founded in 1950 and rose to a leading position in the domestic paper manufacturing industry. The company has introduced a number of different products to the market, including fine paper, indust-rial paper, paper container and household paper products.

Besides being the owner of many mills

in Taiwan, YFY Paper has also invested in pulp and paper mills abroad in China and Vietnam. YFY Paper also exports its products to other parts of Asia as well as to the Middle East and Central and South America.

A RENEwED ATTEMPTChung Hwa Pulp engages in the manufac-ture and sale of paper products for cultural, sanitation, and industrial uses in Taiwan. It provides picking pulp, bulky pulp, and high-opacity pulp products. The company was founded in 1968 and is headquartered in Hualien, Taiwan.

YFY Paper and Chung Hwa Pulp origi-nally tried to merge operations in 2001, but had to cancel the plan. In a statement at the time, the two companies attributed “inapp-ropriate political interference” and disagre-ements over labour issues as the reasons for the decision to end the planned merger.

Author: Jan Hökerberg, Hongkong

CHIN

A &

ASIA

implemented in the context of promoting consumption, investment and exports," said Environmental Protection Minister Zhou Shengxian.

A COMPLETE TRANSfORMATIONIt is not only government initiatives that are helping to consolidate and modernise the Chinese paper industry. The companies themselves are also upgrading their facilities.

In a China report by Asia Pulp & Paper (APP), one of the world’s leading pulp and paper producers, the company concludes: “Today’s paper industry has undertaken a complete transformation. Amid techno-logical advances, as well as rising national standards and increased awareness of corporate responsibility, China’s modern paper enterprises are taking active measures to modernise the industry by employing renewable resources within a cleaner production process.” Chan hwa Pulp engages in the manufacture and sale of paper products for cultural,

sanitation and industrial uses in Taiwan.

CHANG HwA PulP

22 BRIGHT MARKET INSIGHT

today 700 people work at the Stora Enso´s plantation schools and eucalyptus forests in China.

STORA ENSO

PH

OTO

: Ju

lIA

NA

yO

ND

T

23BRIGHT MARKET INSIGHT

Countdown to Stora Enso’s Investment in

Stora Enso will be investing around EUR 1,6 billion in a greenfield pulp mill for the production of pulp and paperboard in the city of Beihai in Guangxi province in southern China. Further expansions are in the pipe-line and China is well on the way to becoming one of the group’s largest and most important markets.

Stora Enso began operations in Guangxi in 2002 and, since then has invested EUR 200 million in building up its 120,000 hectares of eucalyptus plantations in the province. Today 700 people work at the plantation schools and in the Chinese eucalyptus forests.

“This is land ideally suited for growing eucalyptus,” says Mats Nordlander, Executi-ve Vice President of Stora Enso’s Renewable Packaging business area.

PAPERbOARD PRODuCTION AND CAPACITyThe forests are now ready for harvesting. Stora Enso’s management and board recently continued the Chinese initiative by investing EUR 1.6 billion in a new greenfield mill in Beihai in Guangxi. The mill will produce 900,000 annual tonnes of pulp, and will include a new, state-of-the-art paperboard machine with a capacity of 450,000 annual tonnes. The mill is expected to deliver liquid packaging board and va-rious types of consumer product packaging to the whole of China.

“In 2007 we signed a letter of intent to build the mill, and we have spent the last five years planning the project and nego-tiating the terms. It’s a gigantic investment – one of the largest that a Nordic company

has ever made outside the Nordic region,” says Mats Nordlander.

The operation will be conducted in the form of a joint-venture company, of which 85 percent will be owned by Stora Enso and 15 percent by the state-owned Guangxi Forestry Group.

CHINA gROwINg IN IMPORTANCEWith the current investment, China’s importance for the group will increase significantly. China including Hong Kong accounted for around five percent of Stora Enso’s total turnover of around EUR 11 billion in 2011.

“We are already one of the market-leading forest industry players in the count-ry and we have ambitious growth plans in China. If the Chinese market continues to grow until 2020 at the rate that we expect, there will be opportunities for further expansion,” says Mats Nordlander.

In the future, when the market allows, the ultimate objective is to increase capacity at the new mill to 900,000 annual tonnes.

STRONg gROwTHThe global packaging market is currently growing by 3 to 8 percent a year. The fastest growth is being recorded in countries such as China, India and Pakistan.

“All these countries, which are emerging from poverty, need packaging. We antici-pate that 50 percent of the global growth in our key paperboard segment by 2020 will be in China. The number of families in China that are eating hygienically packaged food is rising by 25 percent per year. This is the driving force behind our operation here. With this project we will significantly

increase our sales in the Chinese market,” says Mats Nordlander.

RECRuITMENT CAMPAIgN uNDER wAyToday, Stora Enso has 4,500 employees in China. When the mill in Guangxi is completed, the number of employees in the country will rise to 6,500. This can be compared with the group’s total workforce of 30,000, of which 6,000 are in Sweden.

”We anticipate that in five years’ time, China will be one of the countries where we have the most employees. And that’s not including the 10,000 people who will be working there during the construction phase. In all, we expect that the investment in Guanxi, with contractors, suppliers and auxiliary operations, will create 30,000 new job opportunities in the province,” says Mats Nordlander.

The first recruitment drive for the mill is under way, with vacancies for 300 university graduates to be filled, and 500 more to join them in the spring of 2013.

“The great majority of them will be learning the ropes from scratch and will start off as operators,” he says.

ALL SySTEMS gO IN 2014Construction work on the plant will begin as soon as the formalities are complete.

“All the preliminary decisions have been made but we have yet to receive the final framework decision. Work will commence as soon as the permit arrives. The construc-tion phase is expected to take two years and the company plans to start production at the end of 2014,” he concludes.

CHIN

A &

ASIA

CHINA Author: Carl Johard

STORA ENSO

24 BRIGHT MARKET INSIGHT

wHAT IS yOuR VIEw Of THE fOREST INDuSTRy’S fuTuRE, gIVEN THE STRONg PRESSuRE fOR CHANgE THAT CHARACTERISES THE INDuSTRy? “There is undoubtedly a lot of pressure for change, and it is being driven by two strong trends. Firstly, some of our products, parti-cularly newsprint, have passed their sell-by date and have reached the end of their product lifecycles. Sooner or later all products eventually reach maturity in their respective lifecycles. The time has come for some of ours. Despite this, I believe we’re still fairly fortu-nate in having slow, relatively lengthy lifecycles compared with, say, the electronics and mobile phone industries.

The second trend is the rising global population and growing middle class, which is shifting the focus of consumption away from North America and Europe to the emerging countries.”

SCANDINAVIAN fORESTS TAkE bETwEEN 50 TO 60 yEARS TO gROw. ISN’T THE fOREST INDuSTRy by TRADITION A SLOw-MOVINg AND CONSERVATIVE PLAyER AMONg MORE LIgHT-fOOTED MARkETS, wITH LONg PLANNINg HORIzONS AND LONg INVESTMENTS DECISIONS?“Not really. For one thing, the forest industry’s investment deci-sions are not dictated by the pace of tree growth. The forest is a base of raw materials. When our industry invests we’re talking about huge investments and long lifecycles. The forest industry’s specially targeted capital investments have a very long maturity time. Flexi-bility is low and capital sizeable, so you need to be very careful and the investments are only made possible by a relatively slow product lifecycle. This means big machines, where the capital cost per unit gets high priority. With a faster cycle, investments as large as these would not be possible, and instead the investments would be in much smaller, more numerous machines.

Globally I also believe that company size is significant. In a changing world, bigger companies are more competitive and have a better survival rate than smaller ones. This is because they can operate on several continents, have a large assortment of machinery and can therefore add flexibility to the structure. Our newsprint operation has been good at creating a network of paper machines,

THE fOREST IS OUR

“All players should agree on a common view and conviction that the forest industry is vitally important to world’s prosperity, economy and development. It is our green oil,” says Mats Nordlander, Executive Vice President of Stora Enso’s most important business area, Renewable Packaging.

where it is possible to shift production to the unit which at the time is most cost-efficient or is otherwise more flexible in its production.”

LARgE COMPANIES ALSO HAVE THE RESOuRCES TO bE MORE EffICIENT IN THEIR PRODuCTION.“Yes, this is the logical outcome of a more flexible organisation. Generally in our industry, production is calibrated on a plant-by-plant basis. Stora Enso is trying to build a network of machines and plants instead, where we create flexibility between plants and try to take advantage of a brutal benchmarking between individual units.”

IN EuROPE, STORA ENSO HAS DIffERENT MAINTENANCE STRATEgIES. wHICH STRATEgy IS bEST?“Maintenance is an area that we have chosen to develop on the basis of geography. We’re constantly striving to expose all our external and internal processes to competition – not just maintenance. We’re convinced that exposure to competition is healthy. We conti-nuously benchmark and monitor our systems, on the maintenance side too. It’s a question of flexibility and we cannot rule anything out in the future. It’s important to have a philosophy of continuous

Author: Carl Johard

GREEN OIL

Stora Enso is trying to build a network of machines and plants and take advantage of a brutal benchmark, says Mats Nordlander, Executive Vice President Stora Enso Renewable Packaging.

PROFIlE

PH

OTO

: Ju

lIA

NA

yO

ND

T

25BRIGHT MARKET INSIGHT

improvement. Getting bogged down in philosophical discussions and principle-based deadlock on certain decisions would be fatal. This is not a religion and in this respect we are strict non-believers in all political currents. Our philosophy is total flexibility.

We’re constantly striving to expose all our external and internal processes to competition – not just maintenance. We’re convinced that exposure to competition is healthy.”

HOw HIgH IS SAfETy ON STORA ENSO’S LIST Of PRIORITIES TODAy?“Protection, safety and the work environment are all top of our list of priorities and our agenda. It is discussed first at all our meetings, and it is our most important KPI that we use to measure our own performance. We implement the same approach all over the world and we have produced a toolbox with ten tools that we are currently implementing across the group.”

IN OTHER wORDS, yOu HAVE THE SAME APPROACH TO SAfETy AT ALL yOuR PLANTS AROuND THE wORLD?“Yes. We emphasise it in all situations. Our policy is that this is not a cultural issue: a Chinese, Pakistani, or Finnish worker is no different to a Brazilian worker in our safety culture. Protection and safety is one area where we are slightly fundamentalist in our ap-proach – here, we make no compromises. Our employees must feel confident that they will come home unharmed.”

DOES SuSTAINAbILITy HAVE THE SAME PRIORITy ON THE AgENDA?“Yes I think so. We are a company that is shifting towards the emerging countries and high-risk markets. This makes sustainability work increasingly important. It always did have high priority, but the current shift has brought new dimensions and is moving new items up the agenda.

CHIN

A &

ASIA

GREEN OIL

"We continuously benchmark and monitor our systems. Our philosophy is total flexibility.”

stOra ensO’s new strategy

Stora Enso is one of the world’s leading manufacturers of

paperboard and paper.

The group has 30,000 employees in 35 countries all

over the world, and annually produces 4.9 million tonnes of

chemical pulp, 11.8 million tonnes of paper and paper-

board, 1.3 billion square metres of corrugated board and

6 billion cubic metres of sawn wood products. Sales

totalled EuR 11 billion in 2011.

Stora Enso’s operations are now divided into four

business areas:

– Printing and Reading – newsprint, magazine and

book paper and fine paper.

– Biomaterials – production of fibre-based pulp and

bi-products from pulp production.

– Stora Enso Building and living – wood products for

construction and interiors, and bio-fuels.

– Stora Enso Renewable Packaging – fibre-based

packaging and innovative packaging solutions for

consumer products and industrial applications.

in its new strategy, Stora Enso has decided to invest in

fibre-based packaging and plantation-based pulp produc-

tion in emerging markets such as China and latin America.

By offering sustainable new solutions for customers,

fibre-based packaging ensures steady, long-term growth in

most segments and has considerable innovation potential.

Plantation-based pulp is based on fibres that grow ten

times faster than trees in the northern hemisphere. Planta-

tions will allow Stora Enso to secure costs and efficiency

in order to meet future needs for paper and paperboard

production.

The Printing and Reading business area will remain

part of Stora Enso, even if the group will become more

concentrated with fewer production lines. Focus will be

oriented towards manufacturing top grades with the

help of investments and initiatives to promote cost and

energy efficiency.

“Our overarching strategy is to continue growing in

growth areas. Packaging and bio-materials are two such

areas we are investing in. Business areas such as Printing

& Reading and Building & living generate sufficient cash

flow to allow us to generate growth in other areas,” says

Mats Nordlander, Executive Vice President of Stora Enso’s

Renewable Packaging business area.

Given that we often tend to act quickly and have earned the reputation of being a pathfinder in new markets, we also break new ground and face new challenges. It’s always easier to be second or third in a new market, leaving someone else to plough the furrows, make the mistakes and go through the learning curve. Our strategy is to be first.”

PROFIlE

26 BRIGHT MARKET INSIGHT

AfTER THE MARUBENI AGREEMENTRussia is strengthening its commercial ties with Asia in the forestry industry. Recently, Japan’s Marubeni Corporation signed an agreement to build the gigantic Angara Paper pulp mill in Siberia and a Chinese wealth fund has invested in a Siberian timber company. With this new deal the initial partner Sodra leaves the project.

Angara Paper, a massive Russian pulp mill project in Siberia, got a much-needed welcomed boost in September 2012, when the Japanese trading company Marubeni Corporation signed an agreement with the Russians, taking responsibility for machinery, procurement as well as overseeing the construc-tion of a production facility in Lesnosibirsk in the region of Krasnoyarsk, Sibiria.

The contract was signed in conjunction with the summit meeting of the Asia-Pacific Economic Cooperation (APEC) in Vladivostok, where the leaders of the 21 member econo-mies met to discuss future trade and cooperation issues.

ONE Of THE wORLD'S LARgEST PuLP MILLSAngara Paper is intended to become one of the world’s largest pulp mills. Angara Paper was founded in 2006 to implement the pulp mill project. In 2008, Russia’s Industry and Trade Ministry included the project in the list of priority investment projects but construction was halted because of the global financial crisis.

According to initial plans, the mill will produce 1.2 million tonnes pulp per year, comprising 900,000 tonnes of northern bleached softwood kraft pulp (NBSK) based on birch and aspen and 300,000 tonnes of dissolving pulp (textile pulp), in addition to 380,000 cubic metres of sawn timber.

About 80 per cent of the output is earmarked for export to China, Japan, and other Asian regions. The partners put the cost of the investment project at JPY 280 billion (USD 3.5 billion).

Japan currently imports most of its softwood pulp from North America and northern Europe. Japanese and other Asian paper companies will be able to cut transportation costs by switching to supplies from Russia.

Author: Jan Hökerberg, Hongkong