Embed Size (px)

Citation preview

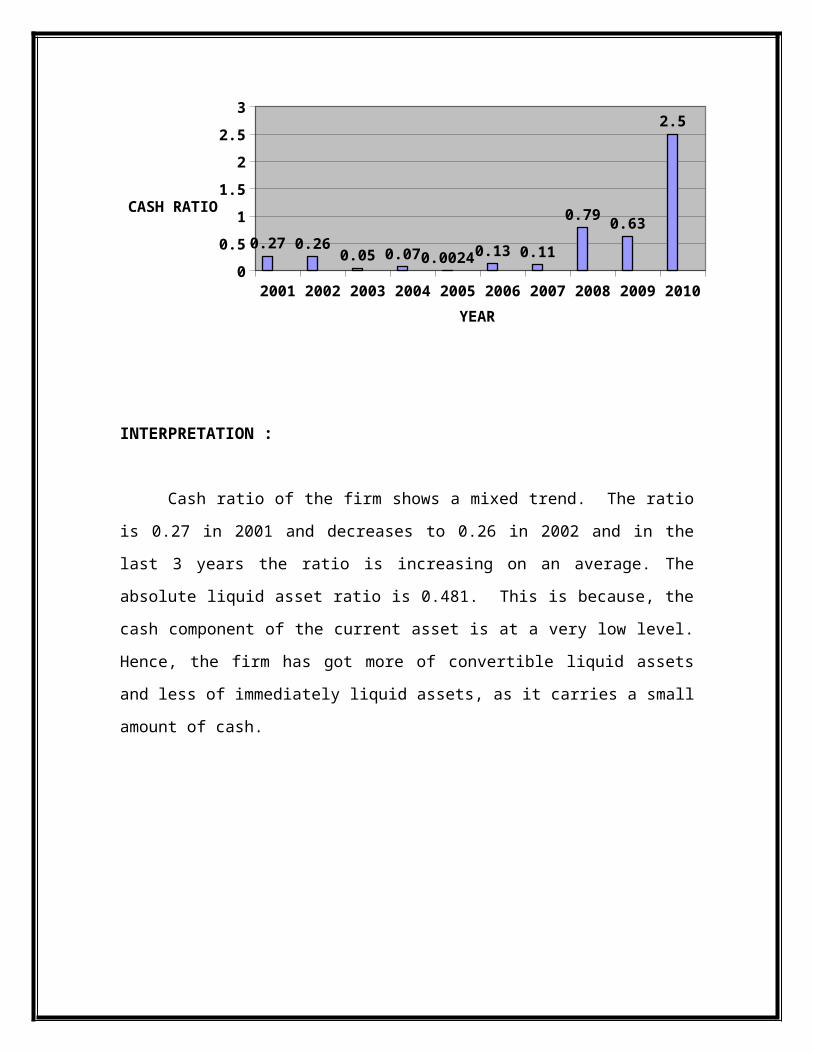

1.1 INTRODUCTION TO THE STUDY

The importance of working capital in any industry needs no special emphasis.

Working capital is considered to be life-giving force to an economic entity. Management

of working capital is one of the most important functions of corporate management.

Every organization, whether profit oriented or not, irrespective of its size and nature of

business, needs requisite amount of working capital.

Working capital management is the process of planning and controlling the level

and mix of the current assets of the firm as well as financing theses assets. Specifically

working capital management requires financial managers to decide what quantities of

cash, other liquid assets, accounts receivables, and inventories the firm will hold at any

point in time. In addition, financial managers must decide how there currents assets are

to be financed. Financing choices includes the mix of current as well as long term

liabilities. The main aim of the study is to find out whether the company is efficiently

managing its working capital. The effective working capital necessitates careful handling

of assets to ensure short term liquidity and solvency of the business.

Keeping in view the pragmatic importance of working capital management as a

gray area of corporate financing function, an attempt has been made to examine working

capital management practices and the problems faced by Metal Industries Ltd in working

management process. In this study, also analyze the working capital management and

profitability position of the Metal Industries Ltd by using financial reports and other

documents given by the company.

1.2 EXECUTIVE SUMMARY

The project study gives analysis and interpretation about the short term solvency

and to ascertain about the liquidity of Metal Industries Ltd, Shoranur. Utmost care has

been taken at all the levels of project work right from the beginning of analyzing

accounting information provided by profit and loss account and balance sheet.

The main aim of the study is to find out whether the company is efficiently

managing its working capital. Inorer to accomplish the aim, secondary data is used for

the preparation. This helps to understand the company’s strength and weakness.

This analysis leads me to the conclusion that the working capital of the firm

shows a decreasing trend. This shows the improvement in the steps taken by the

management.

1.3 STATEMENT OF THE PROBLEM

Each and every decision requires the interpretation and evaluation of

information. A problem statement is the discrepancy between some current state of

affairs and the desired state. For each and every business organization, it is necessary for

them to know the working capital management in the organization, to take decisions for

now and the future.

The problem of the undergone study states that “Metal Industries Ltd,

Shoranur” is eager to know about their working capital management for the ten years.

The finance department recommended that the ratio analysis to conduct the research with

the help of balance sheet and profit & loss account for the year 2001-2010.

1.4 OBJECTIVES OF THE STUDY

The study is mainly intended to analyze the working capital position of Metal

Industries Ltd, Shoranur. Following are the main objectives of the study:

Primary objectives:

To study the position of working capital of Metal Industries Ltd, Shoranur.

Secondary objectives:

1. To ascertain the liquidity position of the firm.

2. To study about the various factors affecting the working capital management of

the firm.

1.5 SCOPE OF THE STUDY

The study was conducted over a period of six weeks entitled “A study on

Working Capital Management of Metal Industries Ltd, Shoranur. In order to accomplish

the aim descriptive research has been taken. As the researcher must be able to define

clearly what he wants to measure and must find adequate methods for measuring it. It is

the research of fact finding.

The management of working capital plays an important role in maintaining the financial

health of the firm during the normal course of business. It portrays the flow of resources

through the firm. Certain aspects covered in the research are to determine whether the

firm is able to carry its operations. To ascertain the liquidity position of the firm, to

evaluate the financial performance of the firm and to identify the factor that affecting

working capital management. Such an analyis is expected is to show and highlight the

streangth and weakness regarding various aspects of its liquidity and working capital

management.

1.6 LIMITATIONS OF THE STUDY

In any study or research conducted there would be some limitations associations with it.

Hence for the proper understanding of the project it is inevitable to specify the limitatios

of the study.

The time frame for the project is about six weeks ,had there been sufficient time

the study could have been more elaborate.

Data taken was for the period of five years as it was available only for those

years.

Only audited records are considered for analysis.

Non monetary factors like human behaviour, their relations etc.are not considered.

The study does not take into account the other areas of finance such as capial

budgeting, costing and cash management etc.

1.7 THEORITICAL BASIS

WORKING CAPITAL MANAGEMENT

The management of working capital plays an important role in maintaining the

financial health of the firm during the normal course of business. Working capital

management is the process of planning and controlling the level and mix of the

current assets of the firm as well as fianncing these assets. Specifically working

capital management requires fiancial managers to decide what quantities of cash,

other liquid assets, accounts receivable and inventories of the firm will hold at any

point in time. In addition, financial managers must decide how there currents are to

ne financed.

According to Shubin, “ working capital is the amount of funds necessary to cover

the cost of operating the enterprize”.

Working capital is the difference between inflow and outflow of funds. In other

words, it is the net cash flow. It is the assets and liabilities required to operate a

business on day to day basis.

Financial managers devote a considerable amount of attention to the management

of working capital. Net working capital provides a accurate assessment of the

liquidity position of the firm. An examination of the components of working capital

is helpful because of the preoccupation of management with the proper combination

on assets and liabiliities constitute the portion of funds which have been planned for

and raised.

CONCEPT OF WORKING CAPITAL

There are two concepts of working capital

a) Gross working capital

b) Net working capital

Gross working capital refers to the firm’s investment in current asset. The

current asset, which can be converted into cash with in an accounting year. It

includes cash short-term security, debenture ans stock.

Net working capital refers difference between current asset and current

liability. Current liabilities are those claims out side’s which ae expected to mature

for payment with in an accounting year and it’s include creditirs, bills payable and

outstanding expenses. Alternatively networking capital is a portion of current asset,

which finances with long term funds. Net working capital measures liquidity of the

firm.

Net working capital may be

a) Positive working capital

b) Negative working capital

When curent assets exceeds current liability that will be positive net

working capital. When current liability exceeds current assets that will be negative

working capital. Gross working capital is a going concept and net working capital is

a accounting concept, some time gross working capital is used because,

1. It shows current amount of working capital at right time.

2. Management is more interested in the total asset than source from where it’s made

available.

3. Every increase in the funds of enterprize would increase its working capital as per

gross concept.

4. It is more useful in determine rate of return.

Net working capital is also important because:

1. It is qualitative concept.

2. It indicates the excess current assets and current liability.

3. It indicate fiancial soundness.

4. It suggest need for financing as a part of working capital from permanent sources.

On the basis of time working capital is classified in to

Permanent / fixed working capital

Temporary / variable working capital

Permanent working capital is the maximum amount required for the effective

utilization fixed capacity and for maintain circulation of curretn asset. Always a

maximum level of current asset, which is continously required by the enterprize to carry

out normal business operation.

For e.g. Raw material,finished goods in work in progree and cash balances.

Temporary working capital is the capital required to meet the seasonal demend

and special exigencies. Temporary working may be seasonal and special working capital

is required for short period and cannot permanently employed. Seasonal working capital

may be need where the raw material is seasonal or the business is in seasonal nature.

IMPORTANCE OF ADEQUATE WORKING CAPITAL

A business firm must maintain an adequate level of working capital in order to

run its businesss moothly. It is worthy that both excessive and inadequate working

capital postions are harmful. However, out of the two, inadequacy of working capital is

more dangerous for a firm. Excessive working capital results in idle funds no profit is

earned. Similarly inefficiency of working capital results in interruption. This will ,lead

to inefficiencies, increase in costs and reduction in profits.

Working capital is just like the heart of business. It it becomes a week, the

business can hardly and surv ices. No business can run succesfully without an adequate

amount of working capital. The following are a few advantages of adequate working

capital in the business:

Advantage of maintain adequate working capital

Increases the solvency of business

Increase goodwill of the business

Get easy loan

Firm get cash discount on purchase hence reduce cost

Regular supply of raw materials

Regular payment of wages and salaries

Exploitation of faavourable market conditions

Quick and regular return and investment

Adequate working capital create an environment of confidence and high morale.

DANGER OF INADEQUATE WORKING CAPITAL

When working capital is inadequate, a firm faces the following problems;

It may not be able to take advantage of cash discount.

It cannot by its requirements in bulk and unable to utilize the production

facilities fully.

It may not be able to take advantage of profitable business opportunities.

It may fail to pay its dividend because of non availability of funds.

Its low liquidity may lead to low profitability.

Short term liabilities cannot be paid because of inadequate working capital.

Credit-worthiness of the firm may be damaged because of lack of liquidity.

Low liqudity position may lead to liquidation of firm.

DANGER OF EXCESSIVE WORKING CAPITAL

When there is too much working capital, it is also dangerous. Excessive working capital

raises the following problems:

A firm may be tempted to over and loss heavily.

The situtation may lead to unnecessary purchases and accumulation of

inventories.

There arises an imbalance between liquidity and profitability.

Excessive working capital means funds are idle.

The situation leads to greater production which may not have matching demand.

The excess of working capital lead to carelessness about cost of production.

SOURCES OF WORKING CAPITAL

The financial manager is always interested in obtaining the working capital at the right

time, at a reasonable cost and the best possible favourable terms. In any concern a part of

the working capital investments are permanent investments in fixed assets. Because there

is always a minimum level of current assets which are continously required by the

enterprise to carry its day to day operations. The minimum level cannot be expected to

reduce at any time. The minimum level of current assets gives rise to permanent working

capital, which is permanently blocked in current assets.

FINANCING OF LONG TERM WORKING CAPITAL

Long term working capital should be provided in such a manner that the enterprize may

have its unintrrupted use for a long time. It can be conveniently financed by the

following sources:

1. Issue of shares:

Issue of shares is the most important sources for raising the permanent working

capital. Maximum amount of permanent capital should be raised by the issue of shares.

2. Floating of shares:

A debenture is an instrument issued by the company acknowledgement its debt to

its holder. It is also important source of long term working capital.

3. Ploughing back of profit:

It means reinvestment by a concern of its surplus earning in its business. That is,

a part of the earned profit may be ploughed back by the firm, in meeting their working

capital needs.

4. Long term loans:

Financial institution such as commerical banks , Life Insurance Corporation of

India etc provide all types of loans long-term, medium term and short term loans.

5. Accepting public deposits:

Public deposits are the fixed deposits accepted by a concern enterprize directly

from public.

Financing short-term working capital

The category of funds covers the need of working capital for financing day-to-day

business requirements. There are two types- Internal source and External source.

A. Internal sources

Depreciation funds: Depreciation reserve provides a source of funds for

working capital.

Provision for taxation: The provision for taxation can also be used by the

concern as a source of working capital during intermittent periods.

Accrued expenses: The firm can postponed the payment of expenses for short

periods.

B. External sources

Trade credit

Credit papers

Bank credit

Customer’s credit

Government assistance

Loan from directors

Security of employees

DETERMINANTS OF WORKING CAPITAL

Nature of business:

Working capital requires of the firm basically influence by the nature of its

business. Trading and fiancial firms have very small investment in fixed assets but

require a large sum of money to be invested in working capital. Manufacturing and

construction firms also have to invest substancially in working capital and a nominal

amount in fixed assets.

Production cycle:

Production cycle comprises of the purchases and use of raw material and the

production of finished goods. Longer the manufacuring cycle, large will be the firm’s

working capital requirement. A study prodution policy will cause inventories to

accumulate during off-season periods and the firm will be exposed to greater inventory

cost and risks.

Production policy:

Working capital need of the firm is related to its sales. Sales depend on demand

condition. Most firm experience seasonal and cyclical variation in the demand for those

product and service. These business variations affect the working capital requirement

specially the temporary working capital requirement of the firm.

Growth and expansion:

Growth and expansion of the firm will affect the working capital. Growth and

expansion of the business in the future will lead more working capital requirement.

Credit policy of the firm:

Credit policy of the firm affects the working capital by influencing the label of

debtors.

Credit policy will be affect in two ways.

1). Credit term granted to customers.

2). Credit term available to firm from creditors.

The firm should be prompt in making collection’s high collection period will

mean tie up of large funds in book debt. Stock collection procedure can increase chances

of bead debt.

Availability of raw materials:

Raw materials availability also affects the working capital requirement. The

availability of raw material is an seasonal the temporary working capital is needed high in

the season.

Price level changes:

Rise in the price level require a firm to maintain higher amount of working capital

and aslo same level of current asset is needed, increased investment when price are

increasing. So the company which can immediately revise these product prices with

rising price level will not face a serve working capital problem.

Operating efficiency:

Operating efficiency of the firm related to the optimal utilization of resources at

minimum cost of the firm will effectively contributing in keeping the working capital

investment at a lower level if it is efficient in controlling the operating cost and utilizing

current asset. Better utilization of resources improves the profitability and this helps in

realizing the pressure on working capital.

INVENTORY MANAGEMENT

Inventory is stock of product a company is manufacturing for sales and

component that make up the product. The various forms of inventory are raw material,

work in progress and finished goods. Other material consumable stores etc. proper

planning of purchasing handling storing and accounting should form a part of inventory

management.

Efficient system of inventroy management determined

a). What to purchase

b). How to purchase

c). From where to purchase

d). Where it store.

Objectives:

1. Determine and maintain optimal level of inventory investment to eliminate duplication

in ordinary or replenishing.

2. Minimize loss through deterioration, wastage and damage.

3. Ensure right quality of goods at reasonable price.

4. Facilitating and finishing of data or short term and term planning and control of

inventory.

5. Ensure continous supply of raw materials to facilitate uninterrupted production.

6. Maintain sufficient finished goods inventory for smooth sales operation and efficient

customer service.

Mainly cost os managing inventory is two parts:

a). Ordering cost

b). Carrying cost

ordering cost is entire cost incurred for acquiring raw materia. These costs

include purchase requisition, purchase ordering, transporting, receiving and storing.

Ordering cost increases in proportion to the number of orders placed.

Carrying cost: Costs incurred for maintaining a given level of inventory are

called carrying cost. It includes cost of storage, insurance recording inspection. It

increases in proportion to the volume of inventory.

IMPORTANT WORKING CAPITAL MANAGEMENT RATIOS

The working capital magnitude of a concern should neither be too inadequate nor

too excessive as cpmpared to its requirement. Maintaining adequate working capital

ensures the improvement of profitability. The finance managers always tries to maintain

the adequate working capital at every time so as to carry on the operations succesfully

and maximize the return on investment. The following are the important ratios to

measure the efficiency of working capital management.

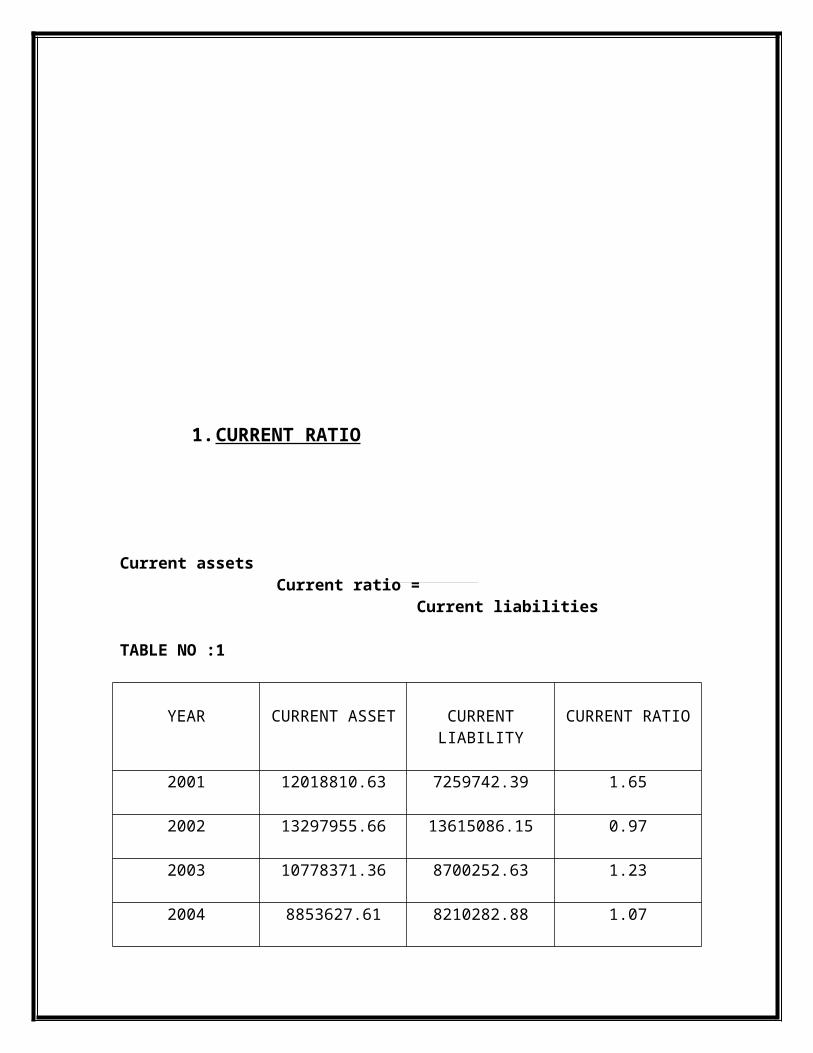

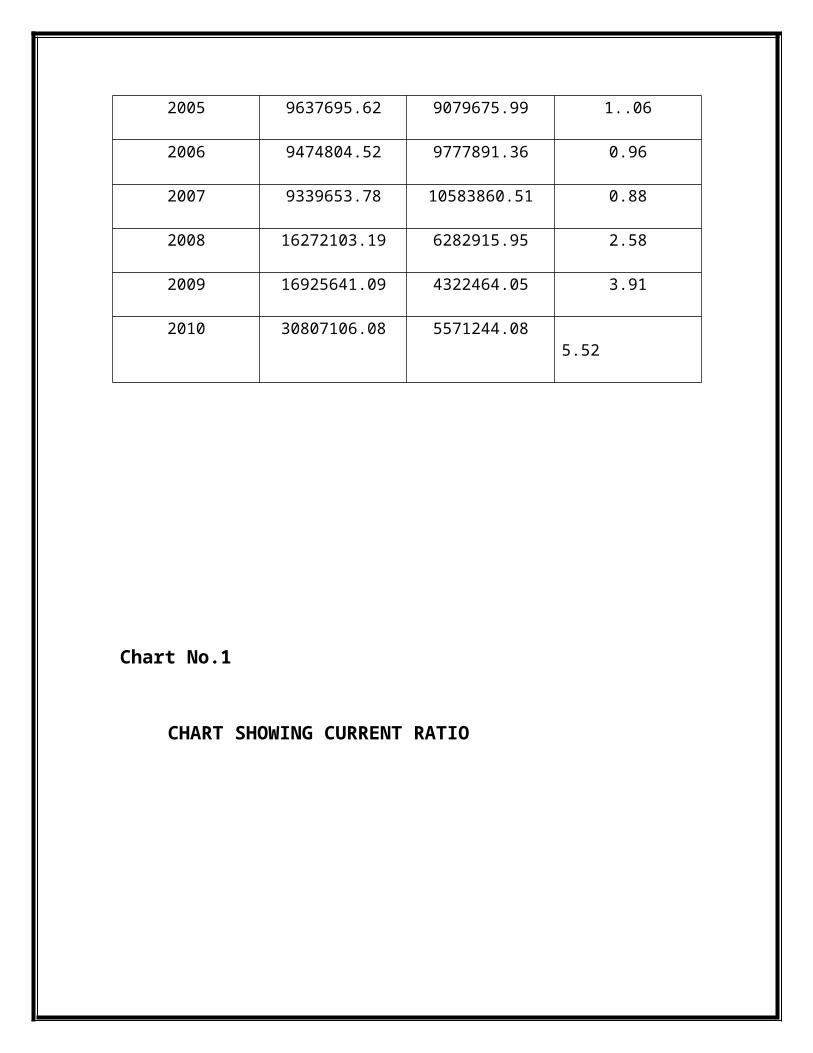

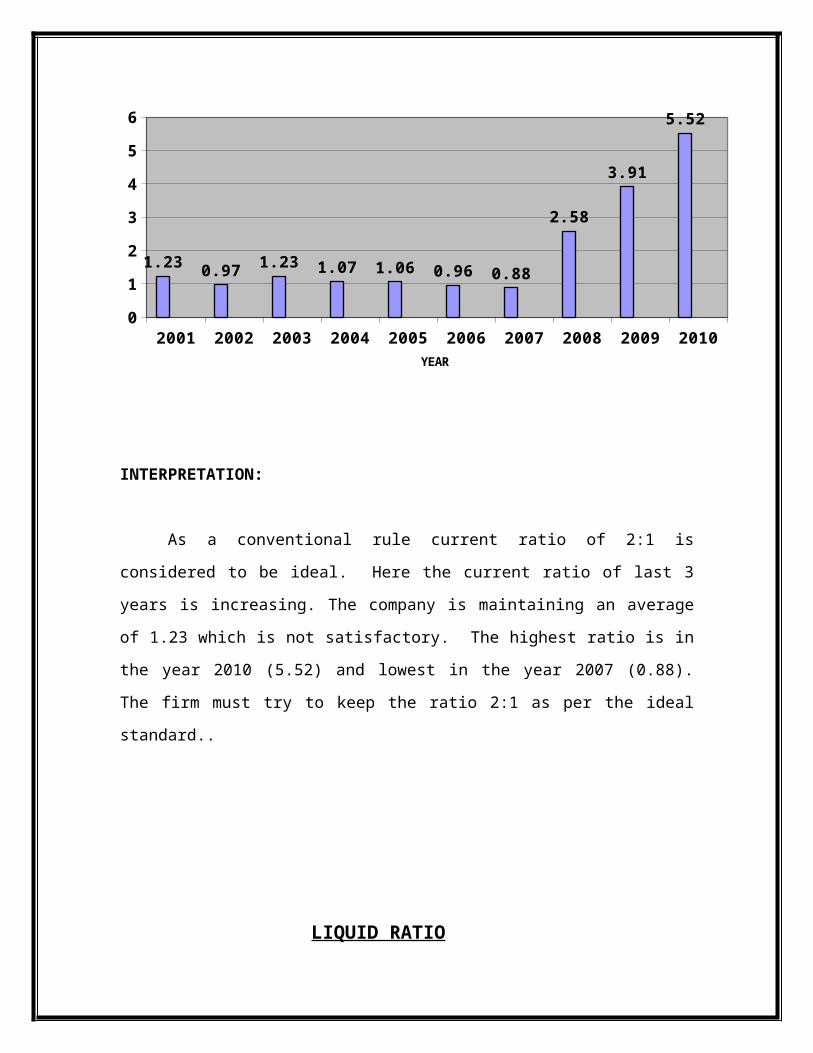

1. CURRENT RATIO

It is the ratio of current assets to current liabilities. It shows the relationship

between total current assets and total current liabilities. It is a measure of firm’s short

term solvency. Current ratio is also called working capital ratio.

Current assets Current ratio =

Current liabilities

Current assets mean cash or those assets which can be converted into cash within

a year. Current asset normally include cash in hand and cash at bank, marketable

securities, stock, suntry debtors, bills receivables and prepaid expenses. Current

liabilities are those liabilities which are to be repaid within a year. Current liabilities

include suntry creditors, bills payable, bank overdraft, provision for taxation etc.

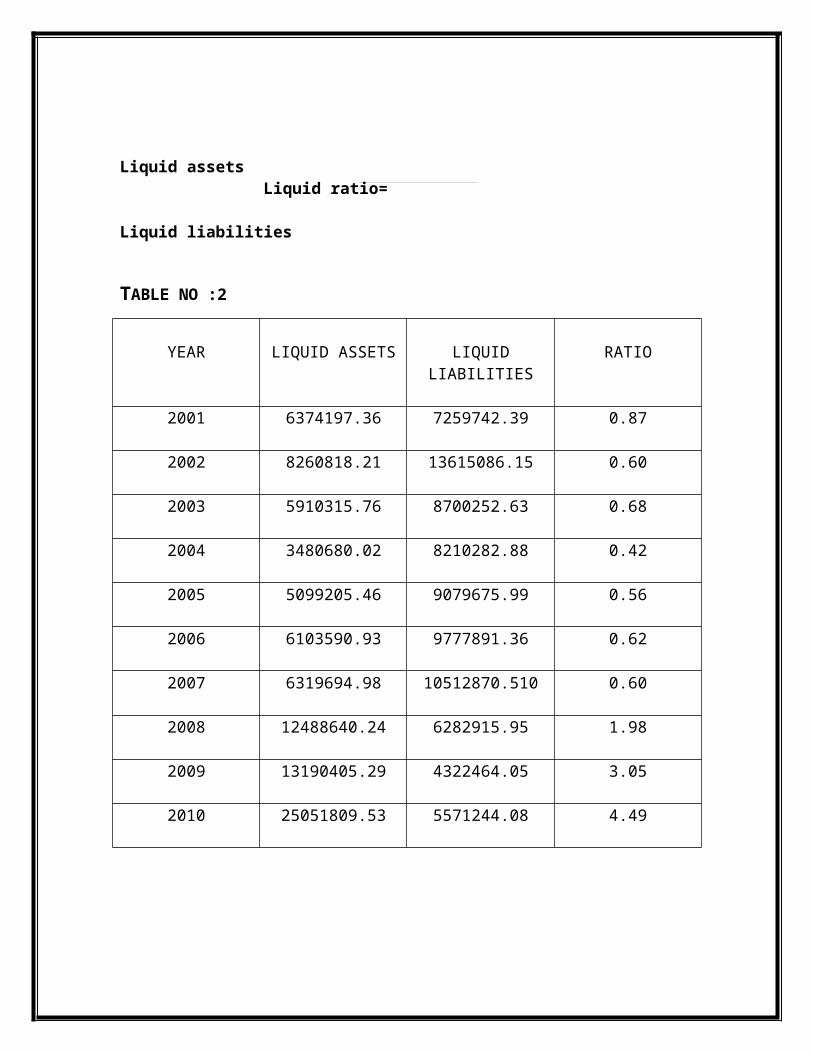

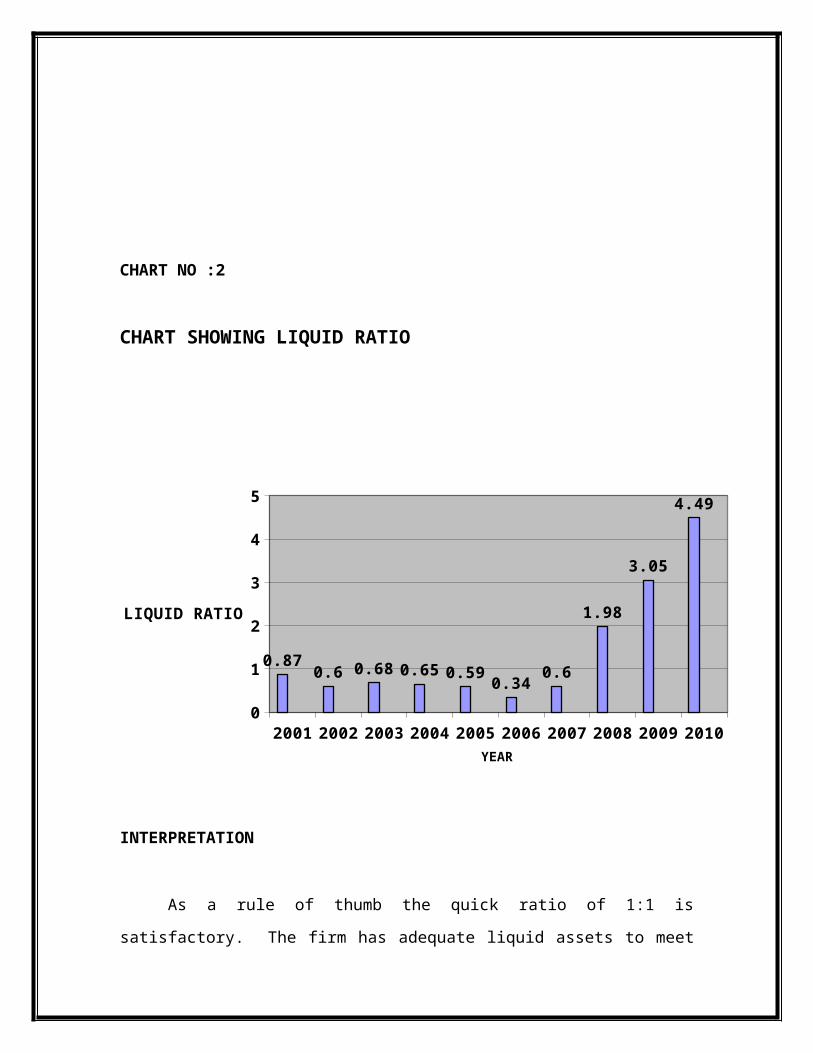

2. LIQUID RATIO

It is the ratio of liquid assets to liquid liabilities. It established the relationship

between quick assets and quick liabilities. It is also known as acid test ratio. It is

computed as follows:

Liquid assetsLiquid ratio=

Liquid liabilities

Liquid or quick assets include cash, bank balances, debtors, bills receivables and short

term marketable securities. In other words, they are current assets minus stock and

prepaid expenses. Stock cannot be included in quick assets because it is not easily and

readily convertible into cash. Perpaid expenses by their nature cannot be used for

payment of quick liabilities. Liquid liabilities are current liabilities minus bank overdraft.

The exclusion of bank overdraft is due to the fact that it tends become a permenant mode

of financing.

3. DEBTORS TURNOVER RATIO

It is also called receivables turnover ratio. It related net credit sales to suntry

debtors. It measures how fast debts are collected. It is calculated as follows:

Total sales Debtors turnover ratio= Average debtors

Average debtors

×365Avarage collection period= Total sales

4. CREDITORS TURNOVER RATIO:

It is the ratio between net credit purchases and the amount of suntry creditors. It

implies the credit period enjoyed by the firm in paying creditors. It is computed by using

the following formula:

Net credit purchasesCreditors turnover ratio =

Creditors

Accounts payable Avarage payment period = × 365 Net credit purchases

5. WORKING CAPITAL TURNOVER RATIO:

This ratio is computed to test the efficiency with which the net working capital is

utilized. In other words, this ratio indicates whether working capital is effectively used in

making sales. It is calculated as follows:

Net SalesWorking capital turnover ratio = Net working capital

6. INVENTORY TURNOVER RATIO

This ratio is also known as stock turnover ratio. It establishes the relationship

between cost of goods sold and avarage inventory. Besides help in determining the

liquidity of a business concern, this ratio indicates how many times during the period the

firm has turned its inventory. In other words, it shows the rate at which inventories are

converted into sales and then into cash. It is computed as follows:

Cost of goods soldInventory turnover ratio =

Average inventory

7. FIXED ASSETS TURNOVER RATIO:

Fixed assets turnover ratio shows the relationship between sales and fixed

assets. It shows whether fixed assets are fully utilized. To be more clearly, this ration

measures the efficiency with which the firm is utilizing its fixed assets in generating the

sales. It is computed as follows:

SalesFixed assets turnover ratio =

Fixed assets

8. GROSS PROFIT RATIO:

This ratio is also known as gross margin. This is the ratio of profit to net

sales. It is usually expressed as percentage. It is computed as follows:

Gross profit Gross profit ratio = ×100

Net sales

Net sales means total sales minus return. Gross profit means sales minus

cost of goods sold. In the case of trading concern, cost of goodssold would be equal to

opening stock plus purchases plus all direct expenses charged to Trading Account minus

closing stock. In the case of manufacturing concerns, it would be equal to the sum of

cost of material consumed, wafes, direct expenses and all factory or manufacturing

expenses.

Gross profit ratio indicates the margin of profit on sale. This ratio

indictes the efficiency of production or trading operations. It is useful to ascertain

whether the average percentage of the mark-up on the goods sold is maintained. A high

G/P ratio is a sign of good management.

9. NET PROFIT RATIO:

Net profit ratio is the ratio of net profit to sales. It is also known as profit

margin. It is usually expressed as percentage. It is calculated as follows:

Net profit Net profit ratio = ×100

Net sales

Here, net profit is the balance of profit and loss account after adjusting interest

and taxes and all non oerating expenses like loss on sale of fixed assets, provisions for

contigent liability etc. and all non operating income like profit on sale of assets, interest

on investment, dividend received etc.

Net profit ratio indicates management’s efficiency in manufacturing,

administrating and selling of the product. This is a measure of overall profitability. This

ratio also indicates the firm’s capacity to withstand adverse economic conditions. A high

N/P rtio would indicated higher overall efficiency of the business, better utilization of

limited resources and reasonable return to owners. A low N/P ratio would mean low

efficiency and inadequate return to owners.

10. OPERATING RATIO:

This is the ratio of cost of goods sold plus operating expenses to net sales. This

ratio shows the percentage of sales absobed by the cost of goods sold and operating

expenses. Operating expenses include office and administrative expenses and selling and

distribution expenses. A low ratio is favourable because it will leave a large amount of

operating income to meet interest, tax and fair return to owners.

(Cost of goods sold + Operating expenses)Operating ratio = ×100

Net sales

1.8 DEFINITION OF TERMS

Profitability

Profitability analysis comprises the study of sales, analysis of cost of

goods sold, analysis of gross margin on sales, analysis of operating expenses, analysis of

operating profit and analysis of profit in relation to sales and capital. Profit margin ratios

reflect the relationship between profit and investments. Profitability ratios can be

determined on the basis of either sales or investments.

Liquidity

Liquidity is a business, economics or investment term that refers to an

assets ability to be easily converted through an act of buying or selling without causing a

significant movement in the price and with minimum loss of value. An act of exchange

of a less liquid asset is called liquidation. Liquidity also refers both to that quality asset is

called liquidation. Liquidity also refers both to that quality of business which enables it

to meet its payment obligations, in terms of processing sufficient liquid assets and to such

assets themselves.

Inventory

The raw materials, work-in-progress goods and completely finished goods

that are considered to be the portion of a business’s assets that is ready or will be for

selling. Inventory represents one of the most important assets that most businesses

possess, because the turnover of inventory represents one of the primary sources of

revenue generation and subsequent earning for the company’s shareholders or owners.

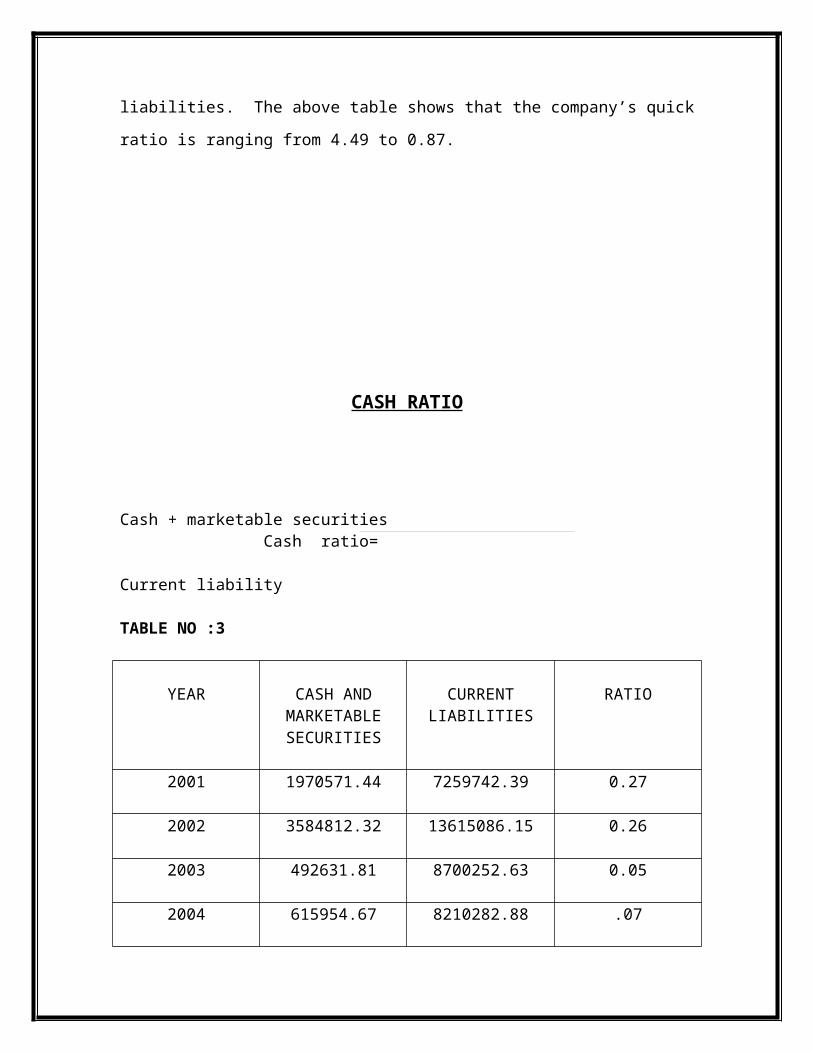

Cash management

Identify the cash balances which allow for the business to meet day to day

expenses, but reduces cash holding costs. When liquidity is highly restricted in terms of

cash and cash equaivalents, this ratio should be calculated. Liquidity ratio measures the

relationship between cash and near cash items at one hand, and immediately maturing

obligations on the other.

Debtors

Identify the appropriate credit policy, i.e.credit terms which attract

customers, such that any impact on cash flows and the flows and the cash converstion

cycle will be offset by increased revenue and hence return on capital (or vice versa).

Creditors

A business firm usually purchases on credit goods, raw materials and

services from other firms. The amount of total payable of a concern depends upon the

purchase policy of the concern. Longer the period of outstanding payable is, lesser is the

problem of working capital of the firm. But when the firm does not pay off its creditors

within time, it may have adverse effect on business.

Accounts receivables

Accounts receivable is one of the series of accounting transactions

dealing with the billing og customers who owe money to a person, company or

organization for goods and services that have been provided to the customer. In most

business entities this is typically done by generating an invoice and mailing electronically

delivering it to the customer which is to be paid within as established time frame called

credit or payment terms.

Accounts payable

Accounts payable is a file or account that contains money that a person

or company owes to suppliers, but hasn’t paid yet when you receive and invoice you add

it to the file, and then you remove it when yopu pay. Thus, A/P is a form of credit that

suppliers offer to their purchasers by allowing them to pay for a product or service after it

has already been received.

INDUSTRY PROFILE

METAL INDUSTRY

The Metal Industry is primarily concerned with metallurgy and metal working.

At first the metals are extracted from the metal- ores found in their natural state deep

within the earth and then these ores are purified a detailed procedure to obtain the metals

in their pure form of the metals in their pure form, these processes comprise metallurgy.

Then the pure form of the metal so obtained is used to manufacture structures as well as

different machines and parts of machines. The procedures which involve the

manufacturing of machines and other useful items form the so obtained through the

metallurgical processes constitute metalworking.

The manufacturing of alloys is also carried out in the Metal Industry through the

proportionate homogeneous mixing of two of more metallic elements 9metal in the pure

state). The alloys so formed are mainly manufactured in order to enhance the natural

properties of the metals by combining together. Steel is one of the most popular as well

as useful alloys of iron, formed through the chemical combination of mainly iron and

carbon. In addition, it may also contain other metals, as added to the combination in

order to attain desired properties form the alloy. Metal industries are indispensable part

of an economy; they from the backbone of industrial development of any country.

HISTORY

India ought to be known as the Great Grandfather of the World Metallurgical

Industry. However due to the unfortunate Historical circumstances many Indians

themselves remain ignorant of this fact. The art of Bronze Casting had been practiced in

India several centuries before the Modern World Discovered “Metallurgy’. Copper and

bronze were perhaps the earliest Non- Ferrous Metals which man shaped into tools.

Metal is the part of the Indian mystique as each Metal has its own alchemic and healing

powers as documented in ancient Indian Scriptures written over 5000 years ago. Metal in

India has been used as a way of expressing Art in several forms using techniques such as

Inlay, Casting, Carving, Appliqué Enameling, Engraving etc. Metal craft has also been

and integral part of Indian culture.Indian “Metallurgists” had perfected the complex

process of extracting Zinc from its ores by the Downward Distillation method that

required exceptional care in the type of furnace, retorts and a reducing atmosphere as

well as temperature management, as evidenced by the archaeological finds at Zawar in

Rajasthan as early as the 4th century BC. It may be noted that it was only in the 18 th

century AD that the same process was re-adopted in Britain, and patented too. In the

classical age of India, the metallurgy of Copper also assumed macro-dimensions. In the

field of Copper Metallurgy too, the huge 5th century Copper Statue of the Buddha, over

two meters in height and one tone in weight, (now in the Safe Custody of Birmingham

Museum) is a remarkable product of macro technology.

An equally remarkable micro technology, namely the production of High quality

Steel now known as Wootz Steel (an Iron Carbon alloy with 1.3 to 1.6 percent Carbon is

also in use). This production was particularly prevalent in South India and emerged as an

accomplished Metallurgical technique by about the 6th century, after which India steel

was sought after for the production of what was termed the Damascus Sword in West

Asia, around the 10th century AD. Metallurgists in the Universities of Stanford and Lowa

State (USA0 have investigate Wood Steel with a view to reproducing the ancient India

process. The former have even patented a process for the production of Utah- high-

Carbon Steel (1.3 to 1.6 % carbon that could be used for certain automobile and aero

plane components.

CLASSIFICATION OF METAL INDUSTRIES

METAL FABRICATION INDUSTRY

The main function of the Metal Fabrication Industry is to produce component

metal parts will fit in along with other parts, to form larger machinery. In this way the

Metal Industry proves to be an essential section of the entire global metal industry as it

produces minute spare parts of larger heavy machinery and equipments, which cannot be

manufactured simultaneously with the manufacturing of the heavy machines.The process

involved in the manufacture of tools and machine parts in the Metal Fabrication Industry.

The construction of fine and minute machine parts involve several procedures

which require a lot of concentration on the part of the person involved in it. They are

therefore not carried out by the large scale metal industries are in the fact manufactured

in the small scale Metal Fabrication Industry. The production of minute machine parts

(most commonly, smaller constituents of a heavy machine) includes the processes as

given below:

Cutting

Molding

Finishing

The Metal sheets that used in the Metal Fabrication Industry are at first cut in to

finer sections, in order to the fit the size of the parts or the finished products that are to be

manufactured in the Metal Fabrication Industry.

METAL CASTING INDUSTRY

The Metal Casting Industry employs the process of pouring molten metals

(“hot metal” in industry parlance into casts (or models), which takes a definite permanent

shape after cooling. The industrial casting procedure that is followed in the Metal

Casting Industry is be classified as non-disposable, as it involves processes that retain

that cast (or mold) for several applications, in contrast to the use of molds made of sand,

plaster or plastics etc, which cannot be used more than once, and are therefore unfit for

application in the Metal Casting Industry. These rather domestic mold casting

procedures are termed as disposable mold casting.

WORLD METAL INDUSTRY

The World Metal Industries in fact provide an overview of the different metal

industries which are making the lives of people easier around the globe through their

advanced innovations. In fact, we should not forget that all the industries around the

globe are dependent upon metallic elements. Metals are an indispensable part of every

industry for all machinery and equipment are made from metallic elements of alloys.

The products of World Metal Industries have now become and almost

indispensable part of our lives for everything we use are either directly made of metallic

elements or alloys (which are proportionate homogeneous mixtures of alloys), or they ere

manufactured through the use of machinery, that is made of metals or alloys.

METAL STAMPING INDUSTRY

The Metal Stamping Industry looks set to replace the machining die casting,

fabricating and forging processes which were the traditional methods into definite shapes.

The Metal Stamping Industry is more affordable and cost effective in comparison to all

the other processes followed to give desired shapes to the metal and alloy sheets that are

in vogue. Even the machinery used for pressing the metals into shapes, in the metal

stamping industry actually involves the method of bending, clipping and molding

metallic and alloy sheets in to definite forms. These procedures of bending, clipping and

molding are carries out in the Metal Stamping Industry to actually give definite form to

the larger metal and alloy sheets. The major products of the Metal Stamping Industry

consists of finer components of larger machinery, equipments and bigger metal

structures, and these smaller items may also be used as spare parts of the same machines.

The metal or alloy sheets are stamped or pressed in to definite fixed shapes and

than the shaped metal is plated with nickel, tin, or some other metallic elements to protect

it from corrosion. Basically alloys of an iron (steel), zinc, nickel, and aluminum are used

in the Metal Stamping Industry as these alloys are strong, durable, do not break easily,

portable, non-poisonous, and affordable at same time.The business is classified under

metal manufacturing are

Metal furniture, shelves, lockers, cabinets and fixtures

Primary metal products

Fabricated metal products

Machinery including electrical and electronic machinery, equipment and supplies.

Storage of primary batteries.

Motor vehicle parts and accessories

Measuring, analyzing, or controlling equipment

Other metals items such as clocks and watches, costume and precious metal

jewelry, needles, pins, and similar notions, signs and advertising displays, burial

caskets,. Silverware or stainless steel flatware.

Metal Industries also include facilities that are involved in metal working

activities such as

Rolling, drawing, and extruding of non-ferrous metals

Heat treating

Coating, engraving and allied services.

Metal Industries businesses performs many different processes including

Machining

Polishing

Forming

Forging

Enameling

Finishing

Grinding

Welding etc.

METAL INDUSTRIES IN INDIA

Metal Industries are the indispensable part of an economy; they form the

backbone of industrial development of any country. In India the industrial development

began with the setting up of Tata Iron and Steel Company (TISCO) at Jamshedpur in

1907. it started its production in 1912. then came up Burnpur and Bhadrawathi Steel

Plants in 1919 and 1923 respectively. It was, however, only after the independence that

the steel industry has been able to find its feet. Barring the Jamshadpur plant of the

Tatas, all are in public sector and looked after by the steel Authority of India Ltd.(SAIL).

Bhilai and Bokaro plants were set up with the Soviet collaboration. Durgapur and

Rourkela came up with British and German technology know-how respectively.

Iron and steel industry is be nature a heavy industry. Proximity to raw materials

and access to efficient transportation network are crucial to this industry. The

Chotanagpur plateau boarding West Bengal, Bihar, Orissa and Madhya Pradesh therefore

has been the natural core of this industry. Besides iron and steel industry, heavy

engineering and machine tools industries are the main dealers of metals. These industries

have witnessed a phenomenal growth and produce a whole range of capital goods and

consumer durables. The capital industry required for textile industry, fertilizer plants,

mining, construction and agricultural machineries such as equipment for irrigation

projects, diesel engines, pumps and tractors, transport vehicles etc. are being produced

indigenously.

The heavy Engineering Corporation Limited., set up at Ranchi in 1958 fabricates

huge machines required for the iron and steel industry. Locomotives are manufactured

by three units, viz, Locomotive Works, Chitharanjan (West Bengal), Diesel Locomotive

Works, Varanasi (Uttar Prdesh), and Tata Engineering and Locomotive Co.Ltd.(TELCO),

Jamshadpur. The Hindustan Machine Tools Ltd (HMT) is a major manufacture of a wide

range of machines and tools. It has in units in Banglore, Pinjore (Hariyana) Kalamassery

(Kerala), and Hyderbad. The HMT also produces a wide range of watches.

The Bhart Heavy Electricals Limited (BHEL) is a public sector undertaking

which produces power generation equipments. Its manufacturing plants are located at

Bhopal, Thiruchirapally, Hyderbad, Haridwar, Ranipet, Banglore and Jagadishpur (Uttar

Pradesh). The Hindustan Aeronautics Ltd., Banglore has acquired capability of

manufacturing aircrafts of different types. It has its manufacturing units are Banglore,

Kanpur, Nazik, Koraput, Hyderbad and Lucknow, Vishakhapattanam, Mumbai, Calcutta

and Kochi are the major center of ship-building industry.

THREE TOP PLAYERS IN KERALA

CHESTER METAL INDUSTRIES

Chester Metal Industries, in their ceaseless pursuit of excellence have made major

advances and perfected ferrous& non ferrous casting into a fully proven process for a

wide range of precision casting for various engineering, automobile and industrial sectors

we are calibrating to deliver moldest products as desired by customers. Crafted from

high quality and various metals, they offer line of products in various precise geometrics.

D-TECH ENGINEERING INDUSTRIES LIMITED

D-TECH engineering Ltd is a steel fabrication unit engaged in structural steel roof work,

skylights, general steel fabrication work, manufacture of steel door frames, doors,

windows and ventilators, steel furniture, sheet metal work, kitchen cabinets, steel bridges

etc their products are widely used in industries, residential and commercial buildings,

educational institutions, hospitals and government departments.

STEEL AND INDUSTRIAL FORGINGS LIMITED

Steel and Industrial Forgings Limited (SIFIL) is an ISO 9001:2008 certified

Public Sector Undertaking fully owned by Government of Kerala, incorporated in 1983

and started commercial production in 1986, SIFIL rapidly forged ahead to become a

name to reckon with. We are master in Titanium and Special alloy forgings. Untiring

efforts of two decades as saddled SIFL firmly in the Forgings Industry of India and

abroad with best ratings for its products and services. Forgings with exquisite designs

and shapes, flawless forms of contours, broad bands and spectra of metals like alloy steel,

super alloys, aluminum and titanium. All in wide range of weights and unmatched

equality made have SIFL the most sought after forging company in the country for

critical components.SIFL’s diverse product mix caters to a wide range of sectors. These

include complex and high precision aerospace forgings, specialized forgings for defense,

Heavy Forgings for Commercial vehicles, railways and other components for

automobiles etc.

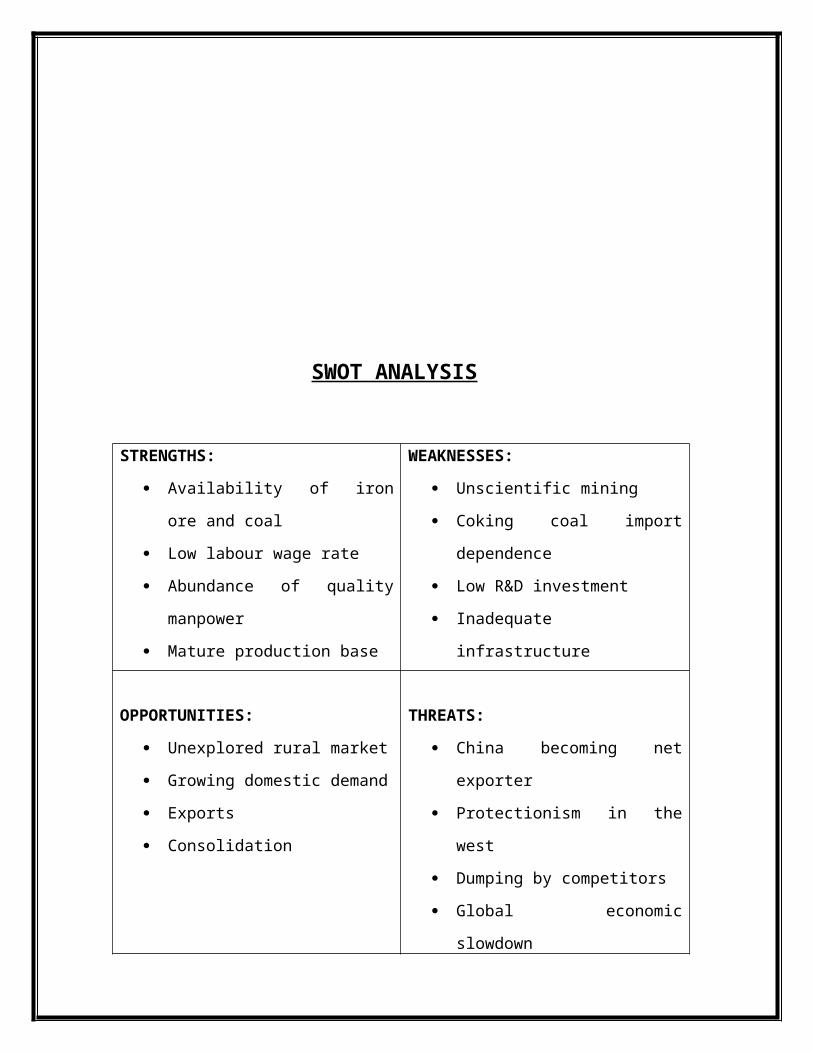

SWOT ANALYSIS

STRENGTHS:

Availability of iron ore and coal

Low labour wage rate

Abundance of quality manpower

Mature production base

WEAKNESSES:

Unscientific mining

Coking coal import dependence

Low R&D investment

Inadequate infrastructure

OPPORTUNITIES:

Unexplored rural market

Growing domestic demand

Exports

Consolidation

THREATS:

China becoming net exporter

Protectionism in the west

Dumping by competitors

Global economic slowdown

RECENT TRENDS

It’s been a Luke warm year for manufacturing. Sort of, let’s dip the big toe and

see how cold the water still is, kind of thing. It’s difficult to look at how well the

industry is actually doing without looking at the past few years to compare. So based on

some research, I’m going to point out a few key points of where the industry was, and

where it’s headed for 2011. Rumors of a double dip recession are still being circulated,

which would be another blow to the industry, but most economists are keeping the glass

half full in this regard against it.Raw materialsPrices have clearly fluctuated with the

crash of the market in 2008, and are slowly starting to creep back to pre-recession prices.

COMPANY PROFILE

INTRODUCTION TO THE COMPANY

The Metal Industries Limited, METIND Nagar, Shoranur, Palakkad, India- 679122 is a

Kerala state Public Sector Undertaking Unit established in the year 1928 perhaps the one

among the first few pioneer industries in pre independent India and the first one in south

India. The activities of the company are to manufacture and market various agricultural

implements and tools required for agro farming, handicrafts and artisans community.

The major clients of the products are Public and Government sectors. The factory is

located at Shoranur, a major industrial destination of Malabar Region of Kerala in 24

acres of land. The ownership of the unit as a public sector undertaking owned and

promoted by the Government of Kerala.

“METIND” is known for Quality, Durability and Reliability of its products and is still

remains on the zenith. A special type of alloy steel used as raw materials of

manufacturing, which undergoes a series of scientific forging and treatment processes to

refine the grain structure and thus makes our implements resistance to wear, tear and

corrosion. This unique feature of the products has sky rocketed the fame of our company

in capturing the local market within the country and now capable to tap the global market

in agricultural implements sector.

The development of Indian economy mainly depends on the agricultural income of the

country. Being the developing nation, almost all the states from top to bottom even

thought some states have advanced to some extend by way of industrialization are

utilizing a major portion of their areas for agricultural purpose in Southern States; the

agricultural activities have a strong impact because the majority of villages are engaged

in agricultural activities. This factor gives an immense scope for the production and

marketing of agricultural implements.

HISTORY OF THE COMPANY

The Metal Industries Limited, a public company was established in the 6th March 1928

with the main object of manufacturing agricultural implements, state tools, horticulture

implements and hand tools etc. the founder of the company was Late Shri C.K Menon.

The Metal Industries Ltd is a SSI established in 1928, perhaps one among the first few

pioneer industries of pre independent India and the first one of south India to cater all

sorts of implements and hand tools needed for agriculture, estate and artisan workers of

our country. Due to various reasons, Shoranur was considered as an ideal place for the

business of agricultural implements manufactured. Most important is the presence of

large number of conventional artisans and blacksmith, who are extended in

manufacturing the agricultural implements. There is a 11 KV sub station at Kulappully,

which provide uninterested supply of electric which is an indispensable facility to be

acquired by the company in order to overcome the power crisis. Company installed a

diesel generator, set 125 KVA capabilities. In the beginning, company has good market

throughout South India. The company markets its product under the brand name

“TUSKERS”. Generally known as METIND. The main raw materials of the company

are rejected rails and billet. The quality and reputation maintained by the company

throughout these years were remarkable.

The company uses special type of alloy, steel uses a raw materials for manufacturing

implements undergoes a series of scientific heat treatment and gorging process to refine

the grain structure and thus to make the implements resistance to wear, tear, corrosion, a

rare phenomenon not seen in any alien products. The company has developed certain

technologists for advanced solid removing equipment and vehicle suitable for urban area.

The company uses simple but economical in design with most technology and quality

with robust in structure to isolates its products from others. The company are now in on a

fresh move for building and fabricating bodies of passenger buses suitable for private and

KSRTC, mini and tourist buses used by KTDC… etc.

For about 30 years in corporation METIND was the pioneer in the market of these

products in South India and Srilanka. However during 1960s and 1970s the company

faced many problems which led to intermittent stoppage of its operation and the company

closed down in 1975 for working capital. With a view to revive, the state Government

made any discussions with Canara Bank, as a result, the bank agreed to grant financial

assistance and needed for rehabilitation. With effect from 18th October 1980, METIND

was converted as a Public Sector Unit under the Government of Kerala, with an equity

participation of 58.78%; the government of Kerala acquired the majority state in the

company. The production was started in the year 1982 with board of

direction nominated by government. Again in 1989 the unit is struggled due to lack of

order from government department. Then the company entered into private market. The

Government of Kerala instructed to other government concern and local bodies to

purchase the required product from this company. Now the company has established

itself in the, market and facing unhealthy competition from numerous units in Kerala,

Tamil Nadu, Karnataka and Andhra Pradesh. Now the company is facing stiff

competition from private owned company like SIMCO, MAYIL VAHANAM.. At

present 95% of the share is held by the Government of Kerala and the balanced by its

shareholders. Slowly the company increased the production and achieved their target

level.

The major products of the company are double faced sledge hammers of all types,

different varieties of mamma ties, pick axes, mammatty forks, wedges, digging forks,

rubber taping knifes etc…, which are mainly used in agricultural operation, quarry works

and industry.

The company has already established reputation of quality. South India is considered as

the pioneer manufacture of the agriculture implements. The reputation is mainly because

of the quality of the products and workmanship. The two important competitors of the

company are MAYILVAHANAM & SIMCO, both these company are situated nearest to

the company. The three important products produced by the company are:

Sledge hammer

Mammatties

axes

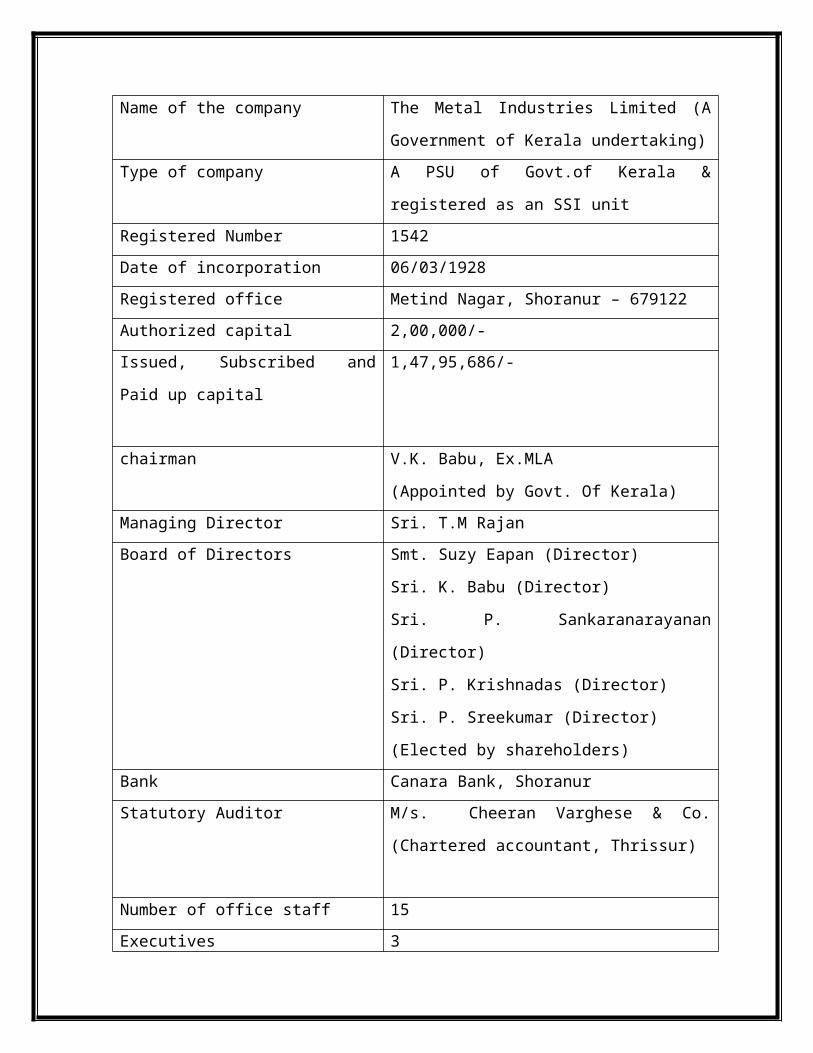

COMPANY DETAILS

Name of the company The Metal Industries Limited (A Government of

Kerala undertaking)

Type of company A PSU of Govt.of Kerala & registered as an SSI

unit

Registered Number 1542

Date of incorporation 06/03/1928

Registered office Metind Nagar, Shoranur – 679122

Authorized capital 2,00,000/-

Issued, Subscribed and Paid up capital 1,47,95,686/-

chairman V.K. Babu, Ex.MLA

(Appointed by Govt. Of Kerala)

Managing Director Sri. T.M Rajan

Board of Directors Smt. Suzy Eapan (Director)

Sri. K. Babu (Director)

Sri. P. Sankaranarayanan (Director)

Sri. P. Krishnadas (Director)

Sri. P. Sreekumar (Director)

(Elected by shareholders)

Bank Canara Bank, Shoranur

Statutory Auditor M/s. Cheeran Varghese & Co. (Chartered

accountant, Thrissur)

Number of office staff 15

Executives 3

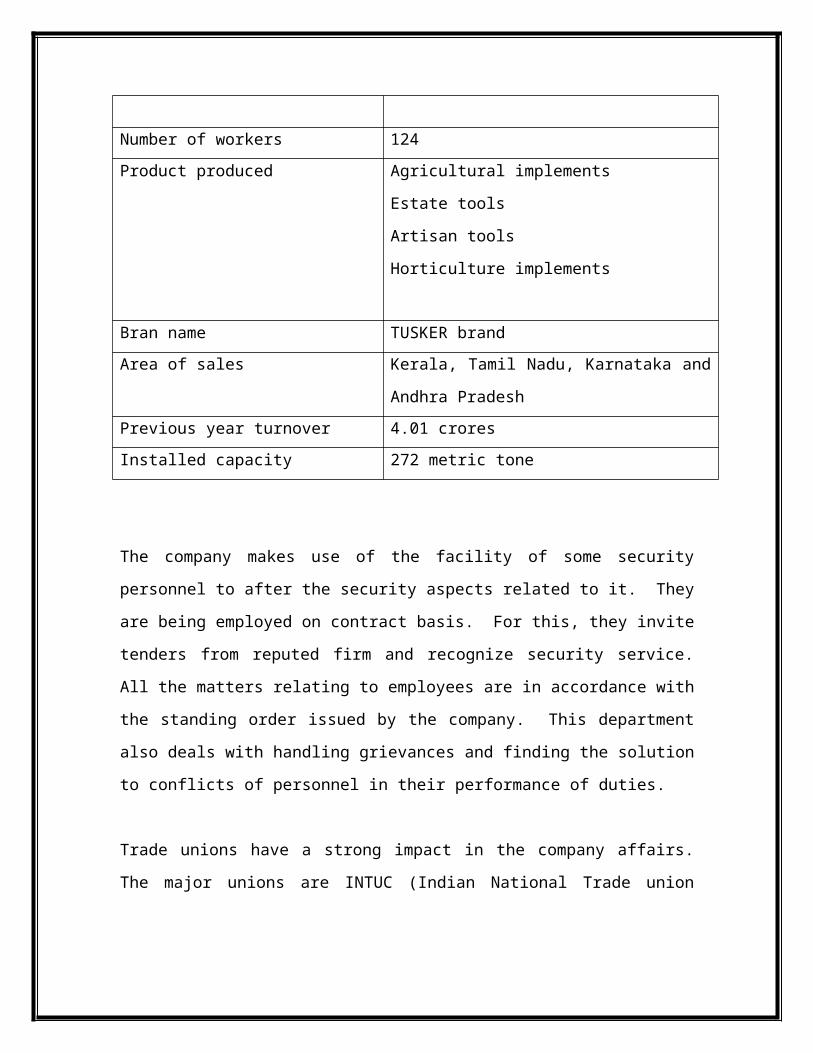

Number of workers 124

Product produced Agricultural implements

Estate tools

Artisan tools

Horticulture implements

Bran name TUSKER brand

Area of sales Kerala, Tamil Nadu, Karnataka and Andhra

Pradesh

Previous year turnover 4.01 crores

Installed capacity 272 metric tone

The company makes use of the facility of some security personnel to after the security

aspects related to it. They are being employed on contract basis. For this, they invite

tenders from reputed firm and recognize security service. All the matters relating to

employees are in accordance with the standing order issued by the company. This

department also deals with handling grievances and finding the solution to conflicts of

personnel in their performance of duties.

Trade unions have a strong impact in the company affairs. The major unions are INTUC

(Indian National Trade union Congress), CITU (Centre of Indian Trade unions) and BMS

(Bharatiya Mazdoor Sangh)

OBJECTIVES OF THE COMPANY

To maximize capacity utilization of existing products.

To maintain and improve the existing cordial relationship between

employees and management by mutual interaction at various at various

levels and to further improve the efficiency of executives, supervisors and

workers to meet future challenges.

To increase the sales.

To ensure strict quality control on all products competing in the market.

To minimize costs.

To increase the profit in order to reduce the accumulated losses.

LOCATIONAL FACTORS

After the formation of Metal Industries Ltd, the location the company is known as

METIND NAGAR. Several other similar industries are located here. The main reason

for locating similar industries at Shoranur is the uninterrupted supply of raw materials.

Main raw materials used for the production are rail and billets. These companies are

situated near to Shoranur Railway Station. Other reason is the prompt study of power,

plenty of labour, transportation facility etc. The peculiarity of this area is that there are a

number of conventional artisans and blacksmiths who are expert in manufacturing these

types of products. Time has approved that this kind of industries can become a success

around this area. All over India the dealers and users of these kinds of products believe

that

“If the products are manufactured at Shoranur, it will be of good quality”.

PRODUCT DESCRIPTION

“A company’s product is what it has to sell.” It is the main link between company and

the consumer public. The Metal Industries Ltd is mainly engaged in the production of the

following products:

Products in Metal Industries are:

Agricultural Implements

Artisan tools

Horticulture Implements

AGRICULTURAL IMPLEMENTS

Agricultural equipment consists of farm field and farmstead machinery used for

the production of crops and agricultural livestock. It includes:

Pickaxe

Hoe

Wedges

Sledge hammer

Claw hammer

Crowbar

Garden rake

Chisel

hatchet

Digging Fork

PICKAXE

A pickaxe or pick is a hand tools with a hard head attached perpendicular to the handle.

Some people make the distinction that a pickaxe has a head with a pointed end, and a

pick has both ends pointed, or only end; but most people use the words to mean the same

thing. The head is usually made of metal, and the commonly wood, metal or fiberglass.

A pickaxe handle without the head, is sometimes used, often unofficially, as a baton. A

normal pickaxe handle is made of ash or hickory wood and is about three feet long and

weights account 2.5 pounds.

HOE

A hoe is an ancient and versatile agricultural tool used to move small amounts of soil.

Common goals include weed control, by agitating the surface of the soil around plants,

pilling soil around the base of plants (hilling), creating narrow furrows (drills) and

shallow trenches for planting seeds and bulbs, to chop weeds, roots and crop residues,

and even to dig or move soil, such as when harvesting root crops like potatoes.

WEDGES

A wedge is a triangular shaped tool, a compound and portable inclined plane, and of the

six classical simple machines. It can be used to separate two objects or portions of an

object, lift an object, or hold an object in place. It functions by converting a force applied

to its blunt end into forces perpendicular 9normal) it its inclined surfaces. The

mechanical advantage of the wedge is given by the ratio of the length of its slope to its

width. Although a short wedge with a wide angle may do a job faster, it requires more

force than long wedge with a narrow angle.

SLEDGE HAMMER

A sledge hammer is a tool consisting of a large, flat head attached to a lever (or handle).

The head is typically made of metal. The sledge hammer can apply more impulse than

other hammers, due to its large size. Along with the mallet, it shares the ability to

distribute force over a wide area. This is in contrast to other types of hammer, which

concentrate force in a relatively small area.

CLAWHAMMER

A claw hammer is a tool primarily used for pounding nails into, or extracting nails from,

some other object. Generally, a claw hammer is associated with wood working but is not

limited to use with wooden products. It is not suitable for heavy hammering on metal

surfaces (such as in machining work), as the steel of its head is somewhat brittle; the ball

peen hammer is more suitable for such metalwork.

CROWBAR

A crowbar is a tool consisting of a metal bar with a single curved end and flattened

points, often with a small fissure on one or both ends for removing nails. It is used as a

lever either to force apart two objects or to remove nails. Crowbars are commonly used

to open nailed wooden crates. Common uses for larger crowbars are: removing nails,

prying apart boards, and generally breaking things. Crowbars can be used as any of the

three classes but the curved end is usually used a first- class lever, and the flat end as a

second class lever.

DIGGING FORK

A garden fork, digging fork or graip is a gardening implement, with a handle and

several (usually four) short, sturdy tines. It is used for loosening, lifting and turning over

soil in gardening and farming. It is used similarly to a spade, but in many circumstances

it is more appropriate than a spade: the tines allow the implement to be pushed more

easing in to the ground, it can take out stones and weeds and break up clods, it is not so

easily stopped by stones, and it does not cut through weed roots or root-crops.

GARDEN RAKE OR GARDEN TOOL

A garden tool is any one of many tools made for gardens and gardening and

overlaps with the range of tools made for agriculture and horticulture. Garden tools can

also apply be hand tools and power tools. The hand tools stills used by gardeners

originated with the earliest agricultural implements used by man: the spade, the garden

hoe, the pitchfork, the garden fork, the garden rake and the plough. The earliest tools

were made of wood. Flint and bone. The development of metal working, first in copper

and later in iron and steel, enabled the manufacture of more durable tools. Industrial

metal working enables the manufacture of cutting tools, including pruning shears. The

first power tools to become popular with gardeners were the lawn mower. This has been

followed by a wide range of power tools, including cultivating, string trimmer, irrigation

sprinklers, hedge trimmers, lawn aerators, leaf sweepers, leaf blowers, chainsaws and

mini-tractors.

HATCHET

A hatchet is single handed striking tool with a sharp blade used to cut and split

wood. Hatches may also be used for hewing when making flattened surfaces on logs;

when the hatchet head is optimized for this purpose it is called a broad axe.

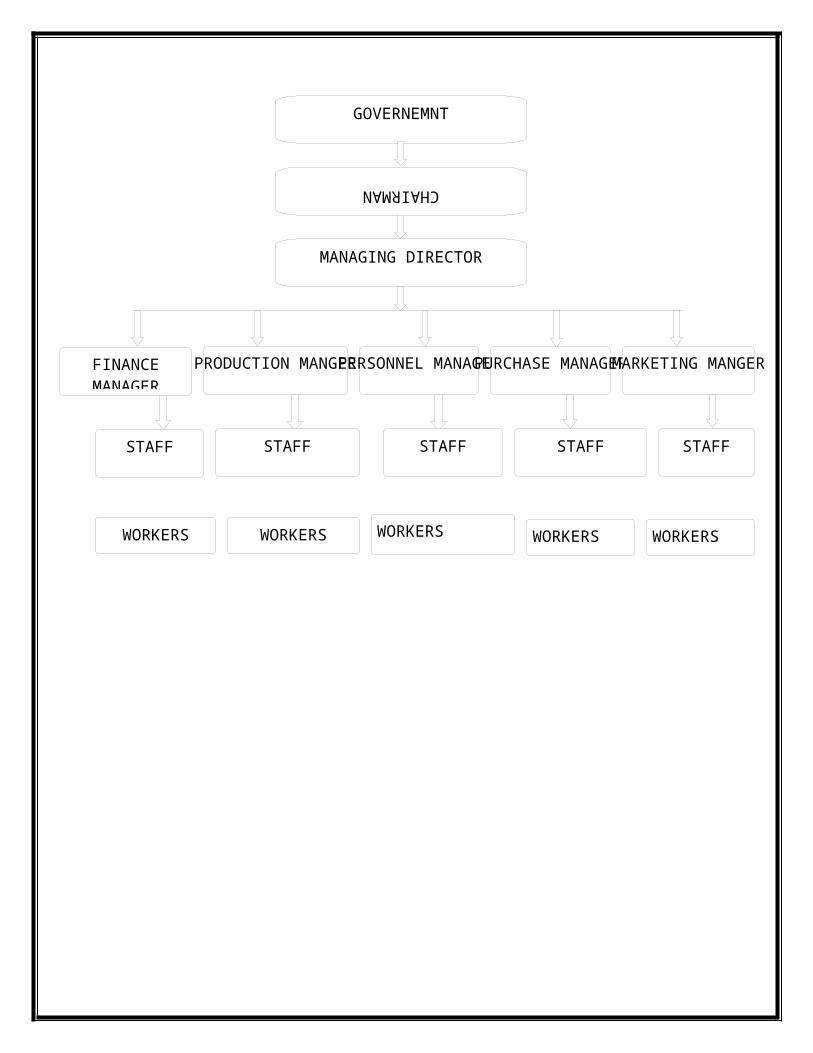

ORGANIZATIONAL CHART

GOVERNEMNT

CHAIRMAN

MANAGING DIRECTOR

PRODUCTION MANGERPERSONNEL MANAGERPURCHASE MANAGERMARKETING MANGER

ORGANISATIONAL STRUCTURE

FINANCE MANAGER

STAFF STAFF STAFF STAFF STAFF

WORKERS WORKERS WORKERS WORKERS WORKERS

The administrative affairs of the company are managed by Board of Directors

comprising of seven members headed by the Chairman. One of the board members are

elected shareholders and others are nominated by government. Managing directors are

responsible for taking decisions regarding framing of policy and its implementation etc.

the Board Meeting is held in every 3 months. For the administrative purpose, the

company is divided into five departments namely production, purchase, sales and

marketing, finance and personnel department.

FUNCTIONAL DEPARTMENTS

1. HUMAN RESOURCE DEPARTMENT

Human resource is the most valuable resource in any organization because it can

function only thorough people. The success depends upon the ability of its human

resource. Human resource management has been presented as a radical alternative to

personnel management consisting of exciting of modern ideas, which would replace the

out of data and ineffective thoughts of personnel management. Personnel manager is

related with the management of workers or employees of the organization. Personal

management is also known as personnel administration. The human resource department

is responsible for the organizational structure in the way which will ensure better working

environment and quality. They deal with the personnel administration (keeping records,

wage agreement etc) in their usual course of operation. Human resource department

keeps an overall record and workers. It works in such a manner to create an atmosphere

in which free exchange of ideas and information between management and workers is

possible.

NUMBER OF EMPOLYEES

There are totally 142 employees in this unit. The employees are divided in to

factory and office employees. There are 124 factory employees and 18 staffs belong to

office and administration department. The factory employees include skilled, semi-

skilled and unskilled workers.

TRAINING

Training is a process of learning a sequence of programmed behaviour. Training

of employees is essential because work force is invaluable asset to an organization. It is

necessary to provide training for both existing and new employees which increase the

skill of the employees. The training facility provided by the company is apprentice

training and health and safety training.

INCENTIVES

The company provides both monetary and non monetary benefits to employees.

It includes bonus, dearness allowance, provident fund, gratuity, labour welfare, canteen

facility, traveling allowance, medical benefits, uniform contribution to labour; HRA,

festival allowance, pension etc are provided to employees.The wages are paid on the

basis of piece rate and time rate system. They are given incentives for extra production

in weekly basis.

INDUSTRIAL SAFETY

Safety means freedom from the occurrence of risks of injury or loss. Industrial

safety of employees safety refers to the protection of workers from the danger of

industrial accidents. Industrial safety is one of the important responsibilities of the

management in the modern industrial set up. The importance of industrial safety was

realized because number of employees is injured while doing job which is caused to

partial or total disablement. In Metal Industries Limited, a safety committee is existed. It

is the responsibility of the committee to safeguard of each and every employee while

doing their job; the employees are strictly advised to take safety measures, such as

goggles for protecting eyes, gloves for protecting hand, apron for the whole body, nose

mask for inhaling suffocating gases.

INDUSTRIAL RELATIONS

Industrial relation is very essential for rapid industrialization of every nation. The

means the relationship between employer and employee in industrial organizations.

Good industrial relationship helps to avoid disputes between employers and employees

and helps to create co-operation, partnership and mutual understanding. Industrial

relation describes the relationship between management and individual employee. It

embraces the relationship between management and trade unions. It includes the relation

between employees and the government. The factory maintains a harmonious relation

between superiors and subordinates. There exists co-operation among the workers.

2. PRODUCTION DEPARTMENT

This is the main functional department of the organization. Production is the process by

which raw materials are converted into finished products. Here the finished products are

agricultural implements, estate tools and hand tools. All the decisions regarding the

production are taken by Work Manager with necessary consultation with Managing

Directors. Production department is sub divided into three sections that is, forging and

maintenance. Production department means the creation of utilities and covers all the

activities of procurement, equipment and machinery etc. Utilities are goods and service

which have want satisfying power.

Production management involving planning, organizing, directing and controlling the

production function or production system- a subsystem if its environment.

According to A.W FIElD “production management is the process of planning and

regulating of the operation of the part of an enterprise which is responsible for actual

transformation of materials into finished products.”

The company METIND has an installed capacity of production of 218 metric tones per

annum of forged agricultural implements ant tools on a single shift basis.

The main raw material of the company are rejected rail, billet

Both these are available at cheaper are art the ancient time. But now, cost of raw material

is increased. Other raw materials are steam cool and petroleum coke used as fuel. The

raw materials are mainly available form North India.

The company had established three manufacturing section:

Forging division

Foundry and Engineering Division

A cutlery division

The first two divisions located adjacently is sprawling acre landscape and third division

was located in three acres of compounded at Lakkidi.

The various products are manufactures in the company are

Double faced sledge hammer

Different varieties of mammaties

Pick axes

Crowbars

Axes

Bill hooks, mainly used in agricultural operation, quarry works and industries.

The sizes of above products are differing according to geographical area. That means of

slight changes in usages of quantity of raw material for producing varieties of products in

different geographical area.

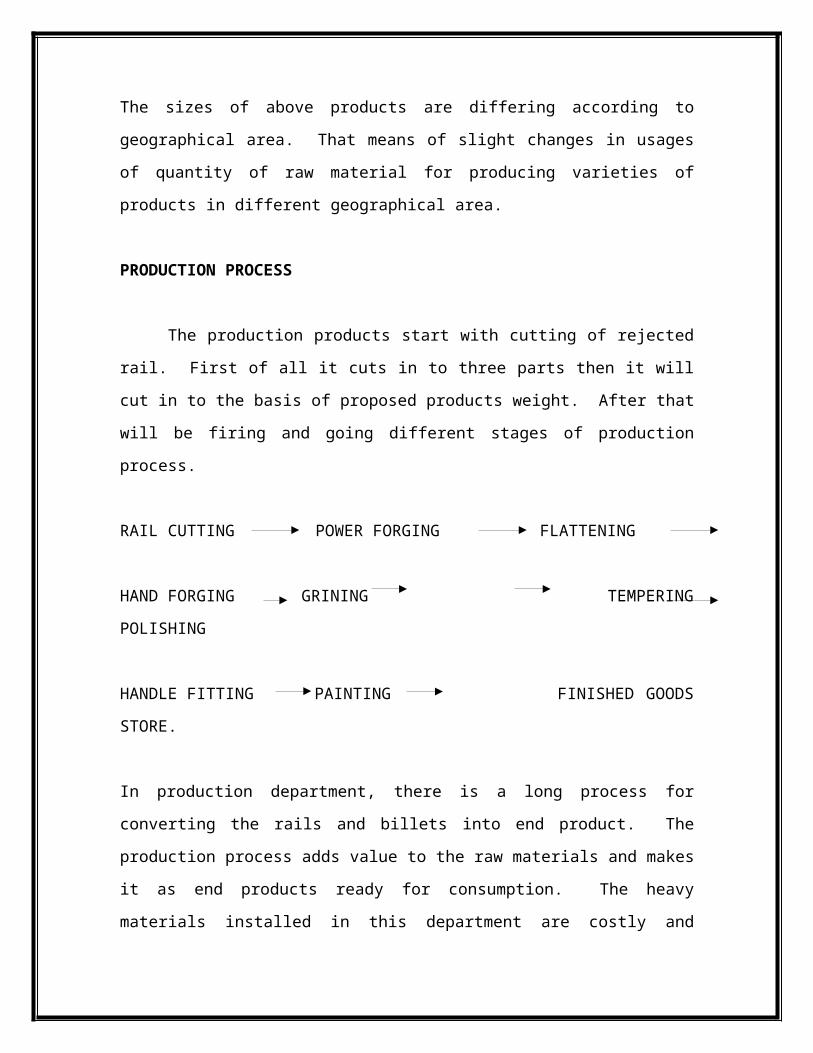

PRODUCTION PROCESS

The production products start with cutting of rejected rail. First of all it cuts in to

three parts then it will cut in to the basis of proposed products weight. After that will be

firing and going different stages of production process.

RAIL CUTTING POWER FORGING FLATTENING

HAND FORGING GRINING TEMPERING POLISHING

HANDLE FITTING PAINTING FINISHED GOODS STORE.

In production department, there is a long process for converting the rails and billets into

end product. The production process adds value to the raw materials and makes it as end

products ready for consumption. The heavy materials installed in this department are

costly and imported from Beche Company in Germany. In this unit, only raw materials

having ferrous content are needed. The steel requited may be carbon steel or alloy steel.

Here only carbon steel is used for manufacturing products. There is low carbon steel is

used for manufacturing products. There is low carbon steel, medium carbon steel, high

carbon steel. In this unit, high carbon steel is used as raw materials for making good

products. The reason is that the product is high carbon steel. This is important for the

use of end products for long duration. The whole process of production is generally

called FORGING.

Agricultural implements are produced in this section. The main raw materials used in

this section are rejected rails, billets etc. This section uses machineries such as power

hammers, grinding machines, shaping machines etc. During the review of the production

has decreased to 226.3 MT as against the production of 245 MT during the previous year.

3. PURCHASE DEPARTMENT

Purchase department has a vital role in the company. All the purchasing activity of the

company is headed by this department. This department is controlled by the Purchase

Officer. It has two sections- purchase and store. The purchase officer is assistant by a

store keeper who is in charge of store. The store keeper receives, inspects and checks all

the materials purchased by the company. The duty of purchase manager in a company is

to purchase the raw materials from suppliers in a proper way at reasonable price.

Purchasing process starts with purchase manager and send quotation to the supplier of

raw materials and select least one by purchase manager and then he sends purchase order.

The purchase of raw materials is on the basis of production requirements.

Purchase order includes the following:

Address of the party

Units of raw materials

Quantity of the raw materials

Rate of the raw materials

Excise duty

Sales tax

Mode of dispatch

Freight

Delivery schedule

Payment terms

An efficient purchasing ensures the procurement of materials of the right quality, in the

right quantity, at the right time, from the right source at a right place.

Payment terms will be two months, one month or two weeks. The raw materials of the

company are rejected rail and billet. Steam coal and petroleum coke used as fuel.

There are two types of purchasing- Centralized and Decentralized. The purchase is

entrusted with the important function of purchasing of materials for the entire

organization. Centralized purchasing refers to the purchase of materials by a purchase

manager. Under centralized purchasing, all purchases are made by the purchase

department to avoid duplication, overlapping and non-uniform procurements. A

company has to follow the centralized purchasing of raw materials for ensuring proper

materials control as well as efficient store keeping. Under this system, the purchasing

department purchases the required materials for all the departments and branches of the

company.

When the purchasing function is entrusted for a single person, it is said to be centralized

purchasing. It means all purchasing are made by the purchasing officer. Generally large

and medium size organizations accept centralized purchasing.

Decentralized purchasing refers to the purchasing materials by all departments and

branches independently to fulfill their needs. Such a purchasing occurs when

departments and branches purchase separately and individually. Under decentralized

purchasing, there is no one purchasing manager who has the right to purchase materials

for all departments and divisions. The defects of centralized purchasing can be overcome

by decentralized purchasing system. Decentralized purchasing helps to purchase the

materials immediately in case of an urgent situation

The raw materials used by this company are Rails and Billet. They also purchase steam

coal, coke, firewood, charcoal and paint.

4. MARKETING DEPARTMENT

The primary function of a business enterprise is to create and maintain a satisfied

customer. No longer is profit operational goal or the sole criterion of effective marketing

performance. Marketing management usually represent all managerial efforts and

function to operate the marketing concepts not only in letter but also in spirit. The

survival and growth of every business depends up on profitability and growth are duly

assured.

The company has a marketing department. The company has no scope for advertising of

these products because they produced only agricultural products.

According to Ducker, marketing is the not merely a function of a business enterprise

units or view of the entire business as the economic organ to provide goods and services.

The marketing of METIND COMPANY is done through some agents. The company

recruits agents of agencies. They are working on commission basis. The agents are

made a contract with the company. The agents have their own respected area: it may be

district or zone wise. The represented district agents collect information from consumers

regarding the requirements of the products. The customers include private owned

shoppers and government institutions like Panchayat, Municipality, and Corporation etc.

After collecting the information, the agents communicate with the company and the

company will send the products to the customers according to their demand. If the

products reached to the consumers hand, the agents collect money from consumers and

give money to the company and they collect their commission. The company sells their

products through cash as well as credit basis. Normally the credit period allowed to

consumers is sixty days.

5. FINANCE AND ACCOUNTS DEPARTMENT

All the accounting transactions are maintained under this department. Books and

recording of cash and credit transactions are maintained under this department. Finance

manager is the head of the department. Finance manager gives necessary instructions and

suggestions for the smooth and proper functioning of the department. The company

follows the double entry accounting. The accounts of the company are prepared on

account basis under the historical cost conventions. Finance requires proper planning and

control to achieve the objectives of the business. This gives birth to financial

management as separate discipline. Financial management simply means management of

finance. Financial management may be defined as planning, organizing, directing and

controlling of the financial activity in a business enterprise. Financial management is

concerned with management of finance and smooth running and successful achievement

of the enterprise. The company has a sound finance department under financial manager.

The main function of the financial department is to control the day to day receipts and

payments of the company. The main source of the company is to generate the finance

through selling of its product. Through this, the company captures its working capital

and paying its liabilities.

REVIEW OF LITERATURE

Many researchers have studied working capital from different views and in

different environments. The following ones are useful for our research:

(Eljelly, 2008) elucidated that efficiency liquidity management involves planning

and controlling current assets and current liabilities in such a manner that eliminates the

risk of inability to meet due short-term obligations and avoids excessive investment in

these assets. The relation between profitability and liquidity was examined, as measures

by current ratio and cash gap (cash converstion cycle) on a sample of joint stock

companies in India using correlation and regression analysis. The study found that the

cash conversion cycle was more importance as a measure of liquidity than the current

ratio that affects profitability. The size variable was found to have significant effect on

profitability at the industry level. The results were stable and had important implications

for liquidity management in various Indian companies. First, it was clear that there was a

negative relationship between profitability and liquidity indicators such as current ratio

and cash gap in the India samle examined. Second, the study also revealed that there

was great variation among industries with respect to the significant measures of liqudity.

(Deloof, 2008) discussed that most firms had a large amount of cash invested in

working capital. It can therefore be expected that the way in which working capital is

managed will have a significant impact on profitability of those firms. Using correlation

and regression tests he found a significant negative relationship between gross operating