Embed Size (px)

Citation preview

Issue no 213JanFeb 2016

-600

-400

-200

0

200

400

600

2010 2011 2012 2013 2014 2015

10

20

30

40

RMm

RMbn

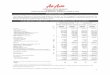

AIRASIA X FINANCIALS

Opera ng ResultPBT

Total Revenues

AirAsia X was established in 2007as part of the AirAsia Group andis based at Kuala Lumpur at thelow cost terminal KLIA2 which wasopened in 2014 It currently flies to18 des na ons in Asia (SapporoTokyo Osaka Seoul Busan TaipeiXian Beijing Hangzhou ChengduShanghai Colombo and Kathmandu)Australia (Sydney Melbourne Perthand Gold Coast) and the Middle East(Jeddah) It operates a corefleet of 26A330-300s each configured with 12Premium Flatbeds and 365 Economyseats Average sector length is about4800km or 55 flying hours persector

Towards the end of 2015 the air-line declared in a presenta on to an-alysts that its turnaround plan hadstarted to bear fruit and that the air-line was on its way to profitability In-deed fourth quarter results for 2015were promising even taking into ac-count that this is the peak travel pe-riod for the carriermdashpre-tax profit ofRM1516m on revenues of RM853mcompared to a loss of RM1685m onrevenues of RM8168m in the previ-ous year

Nevertheless AirAsia X remainsvery unprofitable mdash unaudited re-sults released at the end of Februaryshowed a loss for 2015 of RM3602m

($86m) at the PBT level on revenuesof RM306bn ($728m) represen ngamargin of -142 which was some-what be er than the -206 mar-gin recorded in 2014 Results fromthe parent company AirAsia Berhad(theMalaysia-basedA320opera onsplus equity accoun ng for the vari-ous overseas associates) were alsonot par cularly brilliant mdash a pretaxprofit of RM215m ($51m) represent-ing a 34 margin on revenues ofRM63bn ($15bn) The opera ng re-sult actuallywas strong at RM109bnbut there were heavy losses from allof the associates

Despite net proceeds of RM391mfrom a rights issue last summer AirA-sia Xrsquos balance sheet remains weakLong-term debt as at December 2015was RM14bn and net current liabili-es totalled RM12bn Non-current

assets totalled RM32bn leavingbook equity of RM621m but its

Published by Aviation Strategy Ltd

This issue includes

Page

Long Haul Low Cost 1

Air France-KLM TemporaryReprieve 5

Jetstar the future of Qantas 8

Deltarsquos empire buildingstrategic economic andtax benefits 14

Boeing and Airbus orders 2015 20

AirAsia X Long-haulaspiration and reality

A A Xrsquosmission is ldquoto further solidify our posi on as the globalleader in long-haul low-cost avia on and create the first globalmul -hub low-cost carrier networkrdquo So farhowever it has failed

to find a profitable opera ng model and has reported heavy losses forthe past three years The stock price has been in con nuous declinesince the company was floated on the Bursa Malaysia in July 2013 atRM125 trading at RM025 at the end of February 2016

Aviation StrategyISSN 2041-4021 (Online)

This newsle er is published ten mes a yearby Avia on Strategy Limited JanFeb andJulAug usually appear as combined issuesOur editorial policy is to analyse and covercontemporary avia on issues and airlinestrategies in a clear original and objec-ve manner Avia on Strategy does not

shy away from cri cal analysis and takes aglobal perspec ve mdash with balanced cover-age of the European American and Asianmarkets

PublisherKeithMcMullanJames Halstead

Editorial TeamKeithMcMullankgmavia onstrategyaero

James Halsteadjchavia onstrategyaero

Tel +44(0)207-490-4453Fax +44(0)207-504-8298

Subscriptionsinfoavia onstrategyaero

Copyrightcopy2016 All rights reserved

Avia on Strategy LtdRegisteredNo 8511732 (England)RegisteredOffice137-149 Goswell RdLondon EC1V 7ETVATNo GB 162 7100 38ISSN 2041-4021 (Online)

The opinions expressed in this publica ondonotnecessarily reflect theopinionsof theeditors publisher or contributors Every ef-fort is made to ensure that the informa oncontained in this publica on is accurate butno legal reponsibility is accepted for any er-rors or omissions The contents of this pub-lica on either in whole or in part may notbe copied stored or reproduced in any for-mat printed or electronic formwithout thewri en consent of the publisher

AIRASIA X RESULTS BY REGION

Results (RMm) Margins

2013 2014 2015 2013 2014 2015

North

Asia

Revenues 1147 1409 1470

EBITDAR 176 191 235 153 136 160

PBT (83) (263) (488) -72 -187 -332

Australia

Revenues 903 1048 927

EBITDAR 94 (1) 177 104 -01 191

PBT (113) (369) (232) -125 -352 -250

Others

Revenues 256 478 665

EBITDAR 67 153 413 262 320 621

PBT (14) 26 286 -55 54 430

Total Revenues 2306 2935 3062

EBITDAR 337 343 825 146 117 269

PBT (210) (606) (434) -91 -206 -142

assets include RM520m of deferredtax assets which only become usefulwhenif the airlines starts to makesubstan al profits

Erra c route development

It is impossible to iden fy which ifany of its routes AirAsia X is mak-ing money on However the regionalbreakdownprovided by the companyshows thaton the twomajor route re-gionsAirAsia Xmadehuge losses lossmargins at the PBT level of -332 onNorth Asia and -25 on Australia re-lying on an ill-defined ldquoothersrdquo profitmarginof43tobring theoverall sys-tem to a loss of -142

AirAsia Xrsquos network evolu on issummarised in the maps on the fac-ing page In its early years the airlinea empted to build a European net-work opera ng to London and Parisbut a er suffering heavy losses AirA-sia Xwas forced toabandon this oper-a on in 2013 It appears to have beenunable to find a niche between the

MiddleEast super-connectors captur-ingprice-sensi ve trafficonMalaysia-UKroutesontheonesideandflagcar-riers BA and MAS filtering off pre-mium traffic on the other AirAsia Xthen concentrated on amajor expan-sion into Australia Japan South Ko-rea and China again suffering ma-jor losses as it came up against lowcost compe on in the form of Jet-star (see pages 8-13) and ldquoirra onalcompe on from industry peersrdquo bywhich it meant that MAS despite itsde facto bankrupt state was not cut-ng capacity as rapidly as it should

haveAlthough the core Malaysian op-

era on was deeply problema c theairline persisted with its strategy ofse ng up long-haul associate carri-ers alongside the short haul asso-ciates in IndonesiaandThailand IAAXand TAAXrsquos results are not included inthose of AirAsia X bhd but theymadea combined net loss of $31m in thefirst three quarters of 2015

2 wwwaviationstrategyaero JanFeb 2016

AIRASIA X ROUTEDELOPMENT

Auckland

ChongqingChengduDelhi

Bali

Hangzhou

Tokyo HNDSeoul

Jeddah

Osaka

Kathmandu

Kuala Lumpur

Melbourne

Nagoya

Tokyo NRT

Gold Coast

Beijing

Perth

Busan

Shanghai

Sydney

Taipei

Xian

2016

Adelaide

Colombo

Chengdu

Hangzhou

Tokyo HNDSeoul

Jeddah

Osaka

Kathmandu

Kuala Lumpur

Melbourne

Male

Nagoya

Gold Coast

Beijing

Perth

Busan

Shanghai

Sydney

Taipei

Xian

2014

Mumbai

Christchurch

ChengduDelhi

Hangzhou

Tokyo HNDSeoul

TehranOsaka

Kuala Lumpur

London LGW

Melbourne

Gold Coast

Paris

Perth

London STN

Taipei

Tianjin

2011

Abu DhabiChengdu

Hangzhou

Kuala Lumpur

Melbourne

Gold CoastPerth

London STN

Taipei

Tianjin

2009

As part of what it describes asldquostrategic capacity managementrdquoAirAsia X in 2015 closed down routesto Tokyo Narita Nagoya and Ade-laide and downsized Colombo andChongqing to A320s Frequencieswere cut on Sydney MelbournePerth Gold Coast and HangzhouOn the other hand it launched Sap-poro and announced the re-launchof Delhi for February 2016 NewZealand dropped in 2012 was rein-stated this me as a tag to Aucklandfrom the Gold Coast

Overall seat capacitywas reducedby 6 between 2014 and 2015 butpassengers carried fell by 15 from515m to 485m with the result thatload factor dropped from82 to 75mdash a serious deteriora on especiallyfor an LCC though the company wasable to report a 83 load factor forthe fourthquarterup from81in thesame period of 2014

A fundamental issue for AirAsiaX appears to be establishing a coreof profitable routes on which it canbase its expansion This has been apre-requisite for the successful short-haul LCCs mdash they didnrsquot just suc-ceed because of their lower costsbut also because they had defensi-ble niches (Southwestrsquosmonopoly onintra-Texas services is the classic ex-ample) Finding such a niche in long-haul markets characterised by mul -airlinecompe on isprovingverydif-ficult

There has been specula onabout AirAsia taking over AirAsia Xto assure connec ng traffic for itsshort-haul LCCs mdash a sort of reversalof the European network modelwhere loss-making short haul feed isrequired for the long-haul network

S ll an LCC

It could be argued that LCC strategyis coming to resemble more that of

a networklegacy carrier than that ofan LCC

Looking at the make-up of AirA-sia Xrsquos revenues the airline is relyingmore and more on tradi onal long-haul charter as it cuts back its sched-uled network mdash RM422m or 14 ofits revenues came fromcharters com-pared to 6 in 2014 Perhaps moresignificant is the amount of revenuegenerated from leasing A330s out toother parts of AirAsia X mdash in 2015this accounted for RM275m or 9of revenues and the increase in thisincome source between 2014 and2015RM185mwas just aboutequiv-alent to the reduc on in PBT lossesbetween the two years

Capacity restraint with the aim ofincreasing yields and reducing capexis at the core of the strategy Lastyear the airline cancelled 12 A330swhich had been due for delivery dur-ing 2016-18 leaving two remainingA330ceos on order for 2016 whichwillprobablygoto IndonesiaAirAsiaXand Thai AirAsia X so the core air-line will have no growth for the nexttwo years There are s ll 55 A330-900neos on order but the deliveryschedule is being pushed further andfurther out the first two A330neosare now slated for late 2018 then 5-8per year up to 2026

There was a surge in yields inthe third quarter of last year par c-ularly on China and Australia whichseems to have been sustained intothe fourth quarter but the airline isalso facing cost pressure Par cularlyworrying is the upward trend in unitcosts excluding fuel up 30 in thefourth quarter compared to the sameperiod in 2014 This is largely due tothe steep devalua on of the Ringgitversus the US dollar which has im-pacted A330 rentals With no growthin the system it will be difficult forAirAsia X to manages its unit costs

JanFeb 2016 wwwaviationstrategyaero 3

0

2

4

6

8

10

12

14

16

2013 2014 20152012

RM

AIRASIA X UNIT REVENUE ANDCOST TRENDS

Unit Revenue

Unit Cost

Ex Fuel

01

02

03

04

05

060708091011

2014 2015

08

15

20

25

30

10

2016

RM(lo

gscale) RM

(logscale)

AIRASIA X SHARE PRICE PERFORMANCE

2013

AirAsia X

AirAsia

rather it plans to focus on improv-ing yields by concentra ng sales instronger currency markets like Aus-tralia

The other element in AirAsia Xrsquosstrategy is driving connec ons withthe rest of the AirAsia network Cur-rently about 56 of it passengers areconnec ng mdash 29 self-connec ngand27paying fees for theldquoFly-thrurdquoproduct Fly-thru facilitates transfersfor both Interna onal to Interna-onal and Domes c to Interna onal

at KLIA2 with through-baggage ser-vicesMinimumconnec ng me is 90minutes though themaximumcan be18 hours The aim is increase Fly-Thrupassengers by 10 a year hopefullyavoiding the yield dilu on effects of aconnec ng hub opera on

Looking forward AirAsia X devel-opment is looking less like that of anLCC and more like well MAS MASrsquosstrategy is now to focus capacity onthe Asia-Pacific maintaining compet-i ve pressure on AirAsia X One so-

lu on might be to grow outside theMalaysian base market though In-donesia and Thailand are proving tobe problema c markets not leastfor regulatory reasons The future atleast partly depends on MAS itself ifits turnaround does not work out by2017-18 the Malaysian governmentmightwell conclude that itwouldbeagood idea for a merger to take placeThis could create an MAS30 brandwhich could be poli cally acceptableas the MAS name would be retainedbut the management of the new hy-brid carrier would pass to AirAsiaMaybe the best solu on for both setsof shareholders

4 wwwaviationstrategyaero JanFeb 2016

Wewelcome feedback fromsubscribers on the analysescontained in the newsle er Ifyouwould like to suggest a

company or a subject that youwould like to see covered

please contact us

Emailinfoavia onstrategyaero

or go towwwavia onstrategyaero

-1500

-1000

-500

0

500

1000

2009 2010 2011 2012 2013 2014 2015

eurom

AIR FRANCE-KLM OPERATING PROFITS BY AIRLINEKLM

AF

Group

S years on from the globalfinancial crisis and Air France-KLM has finally produced a

full year net income worth wri nghome about For the year endedDecember 2015 the franco-dutchgroup announced net income ofeuro118m up from a loss of euro(225)min the prior year on revenues up by46 to euro261bn Opera ng profitscame in at euro816m (against a euro(129)mloss) More importantly it is the firstyear since 2008 that Air France itselfhas managed to generate a full yearopera ng profit

Both Air France and KLM fellinto opera ng loss in the year endedMarch 2009 in the wake of the fullimpact of the crisis and the oil pricehike In the following years KLM wasable to produce opera ng profits(albeit at lowmargins) but Air Francepersistently generated losses at thislevel (see chart below) However in2015 Air France published an oper-a ng result of euro462m represen ng anear 3 margin on revenues whileKLM returned euro384m (a 4margin)

The group figures for the year areadmi edly distorted by comparisonswith a strike-torn period in 2014 (thepilotsrsquo strike in that year is es matedto have cost the group some euro425mat the opera ng level) inflated bynon-current items such as the prof-its on sale of shares in Amadeus ofeuro218m sale of Heathrow slots (sixpreviously-leased daily slot pairs tocash-rich partner Delta) for euro230mand deflated by unrealised currencylosses of euro(360)m accoun ng treat-ment of the change in value of thehedging por olio of euro(225)m and re-

structuringcostsofeuro(159)mAs this isall so confusing the grouphelps us bysta ngthatonanldquoadjustedbasisrdquo thenet resultwouldhavebeeneuro220mupfrom a euro(540)m loss in the prior year

The headline numbers show rev-enues up by 46 to euro261bn on theback of a 2 increase in seat capac-ity a 3growth inpassengerdemand(andahalf point improvement in loadfactor to 851) and a 3 nominalincrease in passenger unit revenuesTotal opera ng expenses increasedby 34 helped by a near 7 (oreuro500m) fall in fuel costs to euro62bn de-spite a 28 increase in staff costsUnit costs (in the passenger networkdivision) fell by 2 in nominal terms

Two major macro-economic de-velopments worked against the com-pany in the year foreign exchangemovements and fuel( The Air France-KLM group is ef-fec vely cash flow nega ve in dol-lars and the rise in the value of the

greenback last year had a nega veimpact on the results Overall 26 ofrevenues are generated but 36 ofcosts are expensed in US Dollars ordollar-related currencies As the dol-lar has appreciated over the last twoyears the group encountered cashflow ldquolossesrdquo in 2015 equivalent toeuro178m( Although the average marketprice of jet kerosene fell by nearly50 in the year (from $908tonne to$527tonne) which implies a euro3bnfall in the fuel bill the increase in thevalue of the dollar exchange rate andthe level of group fuel hedging at out-of-the-market prices each wiped outeuro25bn of the poten al saving Themanagement states that for the yearas awhole it recovered 30of the fallin the fuel price (or conversely gaveaway 70) but that in the secondhalf of the year recovered 60 of thedecline through pricing

The Group has marginally

JanFeb 2016 wwwaviationstrategyaero 5

Air France-KLMTemporary Reprieve

-1500

-1000

-500

0

500

1000

1500

2000

2500

20042005

20062007

20082009

20102011

20122013

20142015

2016dagger2017dagger

2018dagger

05101520

15

20

25

30

AIR FRANCE-KLM FINANCIAL RESULTS

Opera ng result

Net result

Revenues

EBITDARmargin

eurom

eurobn

Note 2004-2010 Years endingMarch in following year 2011 on years ending December SourceCompany reports dagger HSBC forecasts

AIR FRANCE-KLMOPERATING RESULTS BY DIVISION

eurom 2013 2014 2015

Passen

ger

Network Long Haul 800 740 1140

Hub-feed (400) (320) (230)

European point-to-point (220) (120) (70)

174 289dagger 842

Transavia (23) (36) (35)

Cargo

Full freighter (101) (97) (42)

Belly-hold (101) (91) (203)

(202) (188)dagger (245)

Maintenance 159 196dagger 214

Catering 24 18 37

Total Group 130 296 816

Notes Split of Passenger Network profits are company es matesdagger2014 excludes es mated impact of strikes Passenger network euro(383)m Cargo euro(24)m MROeuro(22)m

changed its segment repor ng struc-ture In light of its ambi on to growits LCC subsidiary Transavia it hasrenamed its passenger division toldquoPassenger Networkrdquo and separatelyreports results from the low costcarrier

Furthermore in the passengernetwork division it is providingmore detail of es mated opera ngprofitability by type of opera on(see table below) In the year to endDecember 2015 the group es matesthat the long haul opera ons ofthe passenger network generatedopera ng results of euro114bn up fromeuro740m in the prior year period thehub opera ons at CDG and AMSlosses of euro(230)m down from lossesof euro(320)m and that European point-to-point services generated losses ofeuro(70)m as against euro(120)m

Transavia in line with the com-panyrsquos Transform 2020 plan is theonly airline opera on in the group tosee growth Overall capacity was upby 5 but 25 in Transavia France

with total passenger numbers rising9 to around 11m (up from 6m in2011) The company has been repo-si oning itself in the Netherlandswith charter flying down by 13 andscheduled capacity up by 17 yearon year It boasts a unit cost not toodissimilar from that of easyJet but

with unit revenues below unit costs itagain lost euro35mat the opera ng level(a -3margin)

Meanwhile it has made its firstmove out of its home marketsbravely establishing a base in Mu-nich from March 2016 (using theDutch Transavia AOC and not that ofTransavia France) mdash a broadsworda ack against Lu hansa that iseither a brilliant strategic move orwill a ract aggressive compe vereac on as the German carrier triesto build its own low cost opera onThe group has plans to con nuestrong expansion building the corefleet from the current 53 737s to over65 by 2017 by which me it expectsto break even

Among the other divisions MRO(which benefits overall from dollarstrength) and catering did reasonablywell in the year respec vely generat-ing profits of euro214mup by euro40m yearover year and euro37magainst euro18m

However cargo opera onssuffered an increase in losses toeuro(245)m The group is trying des-perately to restructure the freightbusiness and has been disposing

6 wwwaviationstrategyaero JanFeb 2016

3

4

5

6

7

8

9101112

2012 2013 2014 2015 2016

AIR FRANCE-KLM SHARE PRICE PERFORMANCE

of its full freighter fleet In 2015it reduced full-freight flying by aquarter (five freighters were phasedout during the year) and total freightcapacity fell by 6 With con nuedweakness in the sector no pricingpower in what is a commodity busi-ness and many compe tors pricingatmarginal rates or being unhedgedfully benefi ng from the fall in thefuel price unit revenues fell by 13on a ˝like-for-like˝ basis

The losses on the full freight op-era on are stated to have halved toeuro(42m) implying that losses on belly-hold opera ons more than doubledto euro(203)m (a large part of theselosses no-doubt relate to themethodofaccoun ng forbelly-holdcapacity)The group will have reduced its fullfreight fleet to five units by mid 2016and is targe ng break even on thefreighter opera on by 2017

On the balance sheet the groupreduced net debt further (under itsdefini on) to euro43bn downeuro1bn overthe year equivalent to 33x EBITDARThe net asset value on the balancesheet went posi ve to the tune ofeuro225m (although this is fla ered bya euro600mperpetual loan and goodwilland intangiblesofeuro125bn) It is prob-

ably embarassing to recall that theNAV at the end of March 2008 stoodat over euro10bn

What now

This is one year of profit andmanyel-ements of the grouprsquos opera ons ap-pear to be going in the right direc onBut the group has a long way to go toget to achieve compe veness Un-like the other twomajor network car-riers in Europe it is s ll making heavylosses on short haul European opera-ons

Two of the major elements ofthe companyrsquos ˝Perform 2020˝ plan(see Avia on Strategy September2014) have yet to be put fully inac on nego a on of produc vityagreements with the troublesomeAir France unions and a firm foo ngfor an annual 15 reduc on incontrollable unit costs

A renewed offer of nego a onsfor produc vity improvements posedin Januarywhichwould have alloweda resump on of growth from 2017seems to have been rejected out ofhand (with strike threats) Recentlyhowever Air France won an appealin the courts which appears to haveconfirmed the right of the Air France

CEO Freacutedeacuteric Gagey tomake strategicdecisionsmdash the pilotsrsquo union had ap-parently suggested that these shouldbeoverturned if less seniormanagersor other staff disagreed (This surelycould only happen in France) Mean-while at the end of February theAir France management started dis-cussing with the worksrsquo council an-other round of 1600 voluntary re-dundancies primarily among groundstaff

At the results mee ng the man-agement did not give a huge amountof guidance but plans con nued ca-pacity ˝discipline˝ with network air-line capacity growth of around 1-15 (down at Air France and up atKLM) and points to its fuel bill fallingeuro15bn to euro47bn with non-fuel unitcosts down by 1 The key for thisyearwill behowmuchof the fuelben-efit it gives away to passengers

At the me of the results groupCEO Alexandre de Juniac stated ˝ourposi on rela ve to our main rivalshasnrsquot changed We s ll need to askfor addi onal reforms if we want tobridge the gap in compe veness ifwe want to lower costs and be ableto buy planes hire workers and growin a sustainable mannerrdquo The fearmaybe is that they will not now beable toconvince theunionsquitehowfar those reforms have to go Fromtheunionsrsquo perspec ve theupturn infinancial performance jus fies theirprotec onist stance

]

JanFeb 2016 wwwaviationstrategyaero 7

QANTAS AIRLINE DIVISIONS

Qantas Airways LtdAustralia

Qantas Interna onal Qantas Domes c Qantas Freight Jetstar Group

Jetstar AirwaysAustralia

100

Jetstar AsiaSingapore

WestbrookInvestments

51

49

Jetstar JapanJapan

JAL

33

Mitsubishi

167

CTLC

167

33

Jetstar PacificVietnam

VietnamAirlines

70

30

Qantas Loyalty

T J group of LCCs postedimpressive results in the last fi-nancial year and itrsquos now a key

part of Qantasrsquos brand strategy bothin Asian domes c and long-haul mar-kets With Jetstarrsquos long-haul fleetnow comprising 787s how importantwill the LCC be to the Qantas grouprsquosinterna onal expansionover thenextfew years

The Jetstar group of LCCs cur-rently consists of four airlines mdashMelbourne-based Jetstar AirwaysSingaporersquos Jetstar Asia AirwaysVietnam-based Jetstar Pacific Air-lines and Jetstar Japan All of themare well-established Jetstar is thelargest low-cost airline in Aus-traliaNew Zealand and Japan andthe second-largest in Vietnam andSingapore

The first carrier with the Jetstarbrandwas Jetstar Airways whichwaslaunched as a low cost subsidiary ofQantas in 2003 Today it operates71 aircra comprising 53 A320s sixA321s 11 787-8s and a single Dash8 The fleet has an average age ofsix years and operates to 19 domes-c des na ons and 14 interna on-

ally in New Zealand Japan Singa-pore China Thailand Indonesia Fijiand the US In its 201415 financialyear (the12monthsending June30th2015) Jetstar Airways carried 179mpassengers 43 up on the previous12-month period

Jetstar Japan is based at Naritaand was launched in 2012 as a jointventure between Qantas and JALwho each have a 475 ldquoeconomicinterestrdquo in the carrier though for-mally the equity is split 333 each

for Qantas and JAL (as this is the limitfor foreign ownership in Japaneseairlines) withMitsubishi Corpora onowning 167 and Century TokyoLeasing Corpora on another 167It operates to 11 domes c des -na ons and just two interna onalones mdash Hong Kong and Taipei (bothstarted in the second half of 2015) mdashwith 20 A320s that have an averageage of just three years

JetstarAsiaAirwayswas launchedin 2004 before merging with rivalValuair in 2005 It operates 18 A320s(with an average age of six years) on26 routes to 12 des na ons through-out Asia Via a holding group calledNewstar Holdings Qantas owns 49of the airline with 51 belonging toWestbrook Investments a companythat is controlled by Singaporeanbusinessman Dennis Choo who alsoowns a major Singaporean travelagency In the 201415 financial yearthe airline carried 4m passengers mdashactually a drop of 9000 comparedwith 201314 But average stage

length rose during the year and ASKsincreased by 68 with load factorrising to 778 in FY 1415

Based in Ho Chi Minh City JetstarPacific Airlines was formed in 1991as Pacific Airlines a cargo operatorthat was the first Vietnamese car-rier to have a foreign investor In theyears a er launch it had a colourfulhistory including na onalisa on be-fore Qantas acquired an 18 stake in2007 which has since risen to 30(with the rest held by Vietnam Air-lines) Theairline changed its name toJetstar in 2008 and today operates 10A320s and two A321s (with an aver-age age of nine years) to 17 des na-ons domes cally and in China Hong

Kong ThailandMacau and TaiwanAltogether Jetstarrsquos fleet cur-

rently stands at 121 aircra including101 A320s eight A321s 11 787-8sand a single Dash-8 In terms of ex-pansion in August 2011 the Qantasgroup placed an order for 110 A320s(comprising 78 A320neos and 32classic A320s) which according to

8 wwwaviationstrategyaero JanFeb 2016

Jetstarthe future of Qantas

-3000

A$m

-500

0

500

1000

1500

2007 2008 2009 2010 2011 2012 2013 2014 2015 2014 2015

80100

125

150

175

A$bn

Year ended June

QANTASGROUP FINACIAL RESULTS

Underlying EBIT

Statutory Net Profits

Revenues

6mos end Dec

-1000

-500

0

500

1000

1500

2012 2013 2014 2015 2014 2015

Year ended June

QANTASGROUP SEGMENTUNDERLYING EBIT

QFDomes c

QF Interna onal

QF Freight

Jetstar

QF Loyalty

Group elimina ons

6months endedDec

A$m

Qantas ldquoJetstar has access to in orderto facilitate its growthrdquo The firstaircra will arrive in the second halfof 2016A turnaround

In FY 1415 (ending June 30th) theJetstar Group reported revenue ofA$35bn (euro24bn) 75 up on FY1314 and based on a 33 rise inpassengers carried to 218m a 37rise in Group ASKs and an increase inload factor from 779 to 799 Inthe July 2014 to June 2015 period theJetstar Group posted an underlyingEBIT of A$230m (euro160m) signifi-cantly be er than the A$116m loss itposted in the previous financial year

Qantas says the turnaround wasdue to( A 2 reduc on in ldquocontrollablerdquounit cost at the overall Group level(chiefly excluding fuel and forex)( Growth in yield on domes c Aus-tralian routes thanks to be er brandco-ordina on with Qantas Domes cin what the group calls ldquostabilisedmarket condi onsrdquo( New Zealand domes c routesbreaking through into profitability( A turnaround at the Singaporeanopera on that improved its EBITyear-on-year substan ally and brokeinto the black( The 787s driving be er perfor-mance (both in terms of units costandappeal tocustomers)at long-haulroutes out of Australiarsquos Jetstar( Jetstar Pacific repor ng aprofit attheEBIT level in the secondhalf of thefinancial year( Jetstar Japan ldquosignificantly im-provingrdquo its unit revenue and costposi on helping it to reduce losses

This recovery con nued in thefirst half of FY 2016 For the sixmonths ended December 2015 rev-enueswere upby 8 toA$19bnwitha 4 growth in capacity 7 increase

in demand and a 2 point increase inload factor to 822 Unit revenueson domes c Australian routes wereupby 10year on year compoundingthe benefit from the falling fuel priceand the group generated a record un-derlying opera ng profit of A$262mup from A$81m in the prior yearperiod mdash a margin of nearly 14 mdashdespite an es mated A$23m impactfrom Indonesian volanic erup onsEven Jetstar Japan was profitable forthe first me

At the core of the turnaroundis Jetstarrsquos implementa on of a so-

called lsquoLowest seat costrsquo programmepart of a bigger cost-cu ng effortcalled ldquoQantas Transforma onrdquo Forexample the Jetstaropera on inAus-traliahas reduced its controllableunitcosts at a CAGR of more than 2since FY 0708 and this trend is likelyto con nue thanks to the transi onof the long-haul fleet to 787s (com-pleted in September 2015) The firstof the model arrived in November2013 (making Jetstar the first AsianLCC to operate 787s) and they havereplaced ageingA330s thatwere sentback to parent Qantas

JanFeb 2016 wwwaviationstrategyaero 9

0

5

10

15

20

25

2011 2012 2013 2014 2015

Pax(m

)

Year ended June

QANTASGROUPAUSTRALIAN TRAFFICQantas Domes c

Jetstar Domes c

Qantas Interna onal

Jetstar Interna onal

0

5000

10000

15000

20000

25000

2011 2012 2013 2014 2015

70

75

80

Year ended June

JETSTAR AIRWAYS INTERNATIONAL TRAFFIC STATISTICS

ASK RPK

Load Factor

The 787s have 335 seats are con-figured with two cabins (economyand business) and have transformedthe economics on Jetstarrsquos interna-onal routes In addi on on short-

haul A320neos will be introduced toJetstar Airways from 2017 which willachieve a 15 reduc on in averagefuel consump on comparedwith theclassic A320s

Jetstarrsquos focus in the current fi-nancial year is specific to each of thefour airlines but for the biggest car-rier mdash Australiarsquos Jetstar Airways mdashone goal is be er u lisa on of A320son domes c routes where Qantasbelieves its Jetstar subsidiary has al-ready built a substan al network ad-vantage over other domes c Aus-tralian LCCs (in par cular TigerairAustralia) based on higher frequen-cies in every domes c airport it op-erates at For long-haul the aim is tostrengthen its brand in key markets(thanks to the new 787s) and moreghtly integrate its strategy with that

of its parent Qantas

Long-haul strategy

Qantas has been restructuring itsown problema c long-haul oper-a on for a while partly by closing

loss-making routes (such as Sydneyto Frankfurt) and postponing orcancelling aircra orders Theselong-haul changes have been partof a fundamental restructuring ofthe company under Qantas CEO AlanJoyce (appointed to the posi on in2008 he had previously been CEOof Jetstar Airways since 2003) thattook six years to complete mdash withinterna onal being a par cular focusover the last three years

In the201415financialyearQan-tas Interna onal realised ldquomore thanA$400m of transforma on benefitsrdquo

says the company also thanks partlyto be er aircra u lisa on and newpay and condi ons with long-haul pi-lots thathasdeliverproduc vitygainsof around 30 There is even evi-dence that Qantas may have gonetoo far in trimming its long-haul op-era on Last summer mdash just a fewmonths a er comple ng a 5000 re-duc on in its workforce mdash Qantashad to offer crews working on its in-terna onal flights incen ves to workon their days off following a shortageof staff for new long-haul routes

Nevertheless Qantasrsquos in-terna onal opera ons recordedunderlying EBIT of A$267m in FY1415 comparedwith a A$497m lossin FY1314mdashwhichwas itsfirstprofitsince 2008 However part of the rea-son for was this was the significantfall in fuel prices aswell as a lesseningof compe on on long-haul routesto and from Australia the la er duepartly to the weakening Australianeconomy and Dollar As Joyce puts itldquothe interna onal environment thatwe have now is very different fromthe environment that we had twothree years ago We are not going tobe seeing the sort of situa on wersquovehad where wersquove got [up to] 10 ca-

10 wwwaviationstrategyaero JanFeb 2016

JETSTARGROUP ROUTENETWORKS

Avalon

Christchurch

Nha Trang

Denpasar Bali

Dunedin

Haikou

Hobart

Hong Kong

KumamotoKagoshima

Mackay

Matsuyama

Okinawa

Bilinga (Gold Coast)

Ho Chi Minh City

Singapore

Sydney

Taipei

Bangkok

Hanoi

Hangzhou

HonoluluMacau

Nagoya

Yangon

Shantou

Takamatsu

Adelaide

Ballina

Jakarta

Phuket

Kuala Namu

Launceston

Melbourne

Oita

Perth

Proserpine

Phu Quoc

Queenstown

Auckland

Cairns

Darwin

Haiphong

Hamilton Island

Kuala Lumpur

Sunshine Coast

Nadi

Penang

Surabaya

Tuy Hoa

Townsville

Qui Nhon

Wellington

Fukuoka

Hue

Phnom Penh

Thanh Hoa

Dong HoiVinh City

Sapporo

Siem Reap

Banmethuot

Brisbane

Da Nang

Osaka

Manila

Tokyo

Newcastle

Ayers Rock

Jetstar Airways

Jetstar Pacific

Jetstar Asia

Jetstar Japan

QANTASGROUP FLEET

Qantas Jetstar Group Orders

Qantas QantasLink Jetstar Jetstar Asia Jetstar Japan Jetstar Pacific Total 2016-2020 2021-2026

717 18 18737-800 67 67747-400 13 13

787 11 11 8A320 53 18 20 10 101 31 70A321 6 2 8A330 28 28A380 12 12 8

Total 120 18 70 18 20 12 258 39 78

pacity growth into the interna onalmarket and the currency is one ofthe big drivers of that mdash Australia ismuch less a rac ve place for foreigncarriers to put aircra rdquo

Meanwhile this recovery also

con nued into the current financialyear For the sixmonths to December2015 revenues at QF Interna onalwere up by 75 to A$295bn withcapacity growth of 65 and animprovement in load factors of 1

point to 833 Underlying opera ngprofitsmore than trebled toA$270m

Looking forward Qantasrsquos plansfor long-haul are based partly aroundthe replacement of its 747-400 fleetwith 787-9s of which it has eighton order They will start arriving atQantas Interna onal from the end of2017 and a fleet of 45 is possible inthe long-term if it exercises all its op-ons and purchase rights

In the short-term the majorityof interna onal expansion will bethrough the adding of new frequen-cies to exis ng des na ons andwhile there will be new routes thatexpansion will be selec ve In thecurrent year it is realloca ng aircra˝in response to shi ing demand˝broadening its US network throughits alliance with American on thePacific (and re-opening a route to SFOlast December) while pu ng addi-onal services into Asia (par cularly

Japan Hong Kong Singapore andManila)

However once the 787-9s arrivethis will allow Qantas Interna onalto expand on longer thinner routeswith the smaller more efficient air-cra enabling profitability on routesto des na ons that it has previouslytried and failed to make profitable in

JanFeb 2016 wwwaviationstrategyaero 11

0

5

10

15

20

25

30

35

2006 2007 2008 2009 2010 2011 2012 2013 2014 2015

MARKET SHARES IN INTERNATIONALMARKETSTOFROMAUSTRALIA

28 27 2623

20 19 18 17 16 16

2 5 67

8 8 8 8 8 9

Qantas

Jetstar

-10

-5

0

5

10

15

2012 2013 2014 2015 2016

Year ended June

YEARON YEAR CHANGE IN CAPACITY

Jetstar Domes c

Qantas Domes c

Jetstar Interna onal

Qantas Interna onal

the past mdash such as to Beijing ButQantas is also eyeing new routes intoUS and Europe and Joyce has citedMelbourne-Dallas (a great circle dis-tance of 14500km) as an example ofa route where a 787-9 service couldmake economic sense

Jetstarrsquos role

Clearly Jetstar is an important partof Qantasrsquos overall por olio strategyand what Qantas calls ldquodual brandco-ordina onrdquo has already ldquounlockedsignificant valuerdquo In Australia the fu-ture is about building higher frequen-cies on long-haul des na ons andleveraging the brand both ways mdash iemarke ng campaigns that encourageeven traffic flows on Jetstar routesrather than relying onAustralian trav-ellers

There clearly will also be interna-onal growth (and China is one mar-

ket that Jetstar will increase routesto) but given Qantas Interna onalrsquosplans for expansion once the 787-9sarrive itrsquos probable that the signifi-cant difference in the rela ve growthrates between Jetstar Airways andQantas Interna onal seen up un lnowwill reduce

Over the last few years (other

than FY 1314) Jetstar Airwaysrsquointerna onal capacity has grownmuch faster than Qantasrsquos interna-onal ASKs (see chart below) As a

result mdash and as can be seen in thechart above mdash Qantasrsquos share ofthe interna onal market tofromAustralia has fallen substan ally inthe last nine years while Jetstarrsquosshare has remained stable So whileJetstarrsquos domes c passengers total inAustralia is significantly lower thanthe passengers carried by Qantasdomes cally in 1415 (129m versus

215m) mdash its interna onal total of5m tofrom Australia is not far offQantasrsquos interna onal passengerscarried of 58m

But Qantas Interna onalrsquos mar-ket share is likely to rise in the futureonce the787-9expansionoccurs andso while Jetstar will also grow inter-na onally it will be on carefully tar-geted sectors

Outside Australia the strategyfor Jetstar is to build strong ldquoinde-pendentrdquo airlines in partnership withlocal shareholders in key AsiaPacificmarkets and with low levels of capexcoming from Qantas Markets de-fined as key are those that have highGDP per capita or high growthmdash andwith low tomedium LCC penetra onThat defini on clearly excludesThailand Malaysia Indonesia andthe Philippines (where AirAsia isdominant) but does include (otherthan themarkets Jetstar is already in)countries such as China Hong KongSouth Korea and Taiwan

Qantashas longwanted to launcha Jetstar airline in Hong Kong but ef-forts to gain an AOC that began backin 2012 have been thwarted at ev-ery turn largely due to fierce objec-

12 wwwaviationstrategyaero JanFeb 2016

100

125

150

200

250

300

350

400450500

2008 2009 2010 2011 2012 2013 2014 2015 2016

A$(lo

gscale)

QANTASGROUP SHARE PRICE

ons by incumbent airlines CathayPacific Dragonair Hong Kong Airlinesand Hong Kong Express In June 2015the latest a empt mdash made in part-nershipwithChinaEasternanda localinvestor mdash was turned down by theregulatory authori es and in AugustQantas said it was abandoning its at-tempt to launch Jetstar in Hong Kongwri ng off the fledgling Jetstar HongKongbusiness in its FY1415accountsat a cost of A$21m (euro15m)

With China tricky poli callySouth Korea and Taiwan are likely tobe the focus of any a empt to launcha new subsidiary in the short-termthough Qantas believes there is s llplenty of room for expansion at itsexis ng Asian ventures

Qantaswants to increasethefleetat the Vietnamese subsidiary JetstarPacific Airlines to 30 aircra by 2020but the market with the greatest po-ten al appears to be Japan WhileQantas says Jetstar Japan has arounda60shareof thedomes c JapaneseLCCmarket intense compe onwithother LCCs (which include Peach Avi-a on and Skymark Airlines) and arela vely high-cost environment hasmeant that Jetstar Japan has strug-gled tobreakeven Jetstar Japan is re-

ducing its losses and the goal is totake an even firmer grip on the LCCmarket by increasing its fleet to 50 inthe long-term Joyce says that the LCCshare of the total Japanese market isjust 8 so ldquothis is a fantas c busi-ness in a market with significant fu-ture growth opportuni esrdquo

The dual brand strategy

Qantas is unique in having success-fully created a low cost subsidiary(originally perhaps as a union-bashing exercise) seemingly in directcompe on with the legacy full ser-vice brand However the two brandsare being increasingly closely coordi-nated with ˝dynamic managementof capacity to op mise in a shi ingdemand environment˝ Even theJetstar Grouprsquos Asian subsidiaries arepursuing a similar close coordina onwith the legacy partners in eachrespec ve country And this certainlyseems to have worked to generatesuperior returns in the current year

For the six months to Decemberthe group announced a doubling inunderlyingopera ngprofits toA$1bnandpretaxprofits ofA$09bnup fromA$367m in the prior year period Asa consequence it reported an RoIC

on a twelve-month rolling basis ofa stomping 228 (compared withits target through the cycle of 10)and announced a A$500m share buyback

In the short term the group is em-phasising that the Qantas and Jetstarbrands provide product segmenta-on and superior margins Qantas as

a full service carrier concentra ng onthe high yield business oriented mar-ketsmaintainingnetwork frequencyand product for a premium customerbase Jetstar with a leading low faresposi on in domes c and outboundAustralian market and a strengthen-ing panAsian por olio

In the longer run it may be ques-oned whether they really need the

two separate brands whether the fu-ture of Qantas is in fact Jetstar

JanFeb 2016 wwwaviationstrategyaero 13

Reminder

All back issues of

Avia on Strategy

are available on ourwebsite

wwwavia onstrategyaero

If you need login details contactus

infoavia onstrategyaero

-2000

-1000

0

1000

2000

3000

4000

5000

6000

7000

2008 2009 2010 2011 2012 2013 2014 2015

0

5

10

15

25

30

35

40

45

$m

$bn

DELTA AIR LINES FINANCIAL RESULTS

Opera ng Result

Net Result

Revenues

Adj Opera ngmargin

D is quite unique in the USindustry for its post-2010strategy of acquiring minor-

ity equity stakes in airlines aroundthe world as part of long-term ldquoex-clusiverdquo commercial alliances orimmunised joint ventures

In addi on to the con nueddevelopment of the transatlan cJV with Air France-KLM and AlitaliaDelta has acquired equity stakesin Aeromeacutexico (August 2011) GOL(December 2011) Virgin Atlan c(June 2013) and China Eastern (July2015)

Deltarsquos investment ac vity onthat front has intensified in recentmonths In July in addi on to in-ves ng $450m for a 36 stake inChina Eastern Delta helped outits cash-strapped partner GOL bypar cipa ng in GOLrsquos rights offeringto the tune of $56mwhich increasedits ownership stake in the Braziliancarrier to 9 Delta also guaranteed$300m in GOL loans secured by GOLrsquosshares in its publicly listed SMILESloyalty programme

In the summer Delta alsoworkedwith the lessor Intrepid Avia on on adeal that would have given it an eq-uity stake in Japanrsquos Skymark Airlineswhich needed a strategic partner tohelp it out of bankruptcy But Deltalost that opportunity in August whenSkymarkrsquos creditors voted in favour ofan alterna ve plan backed by ANA

InNovemberDeltadisclosed thatit was seeking to increase its stakein Aeromeacutexico from 41 to up to49 subject to regulatory approvalsIn March 2015 Delta and Aeromeacutex-ico applied for an trust immunity

(ATI) for a new $15bn JV in the US-Mexico market which is expected tobegrantedwhenanopenskies agree-ment is implemented

There have been some cases ofminority cross-border investmentsproviding significant economicbenefits to the inves ng airline Con-nentalrsquos 1998-2008 investment in

Panamarsquos Copa was such a deal Butthe general thinking is that at leastsmallminority ownership stakes tendnot to offer many benefits Manysuch investments have been eitherrescue deals or to take advantage ofsome rare opportunity

In June United spent $100m toacquire a 5 stake in Brazilrsquos AzulThat deal was widely expectedgiven the huge size and long-termimportance of the Brazilian marketto US carriers With American part-nered with TAM and Delta with GOLUnited-Azul was a virtual certaintyAnd Azul needed cash because its

IPO is now delayed probably un l2017

No other US airline has consid-ered itworthwhile topursueminoritycross-border equity stakes on a largerscale Sowhy is Delta doing it

The benefits of that strategyto Delta actually seem quite com-prehensive They include long-termstrategic benefits clear economicbenefits and poten ally even taxbenefits which can be summarisedas follows

( Gaining access tomajormarkets

In the first place the China EasternGOLandAeromeacutexico investments areaimedat securing long-termaccess tosome of the worldrsquos largest domes cair travel marketsmdashChina Brazil andMexico

Delta is talking about establish-ing hubs at Shanghai and Satildeo Paulowhich are its partnersrsquo home basesDelta CEO Richard Anderson stated

14 wwwaviationstrategyaero JanFeb 2016

Deltarsquos empire building strategic economicand tax benefits

0

1

2

3

4

5

6

7

8

9

UK China Canada Mexico Germany Brazil Japan France India Italy

2014

Revenu

es($bn

)

TOP TENUS-48 INTERNATIONALMARKETS

7774

4744 43 41 39 38

3330

Delta equity partnerand or joint venture

Delta hub

Source Delta

0

2000

4000

6000

8000

10000

12000

14000

2010 2015 2020F 2025F0

20

40

60

80

100

Dailypa

x(eachway)

US-CHINADAILY PASSENGERS BY POINTOF SALE

US point of sale

China point of sale

Chinese POSas of total

recently ldquoUl mately joint ventureswill give us the founda on to buildthe leading US gateways to China andBrazil including hubs in Shanghai andSatildeo Paulo with our great partnersChina Eastern China Southern andGOLrdquo

The Skymark investment wouldhave accomplished a similar goal mdashgaining access to Japanrsquos large do-mes c market as well as Skymarkrsquosslot holdings at Tokyo Haneda Deltais severely disadvantaged in theUS-Japan market because it doesnot have a Japanese partner (unlikeAmerican and United which haveimmunised JVs with JAL and ANArespec vely

China is vitally important to Deltabecause it has surpassed Japan asthe largest transpacific market fromthe US and because it is expected tobe the fastest-growing interna onalmarket in the future Total daily US-China passengers are forecast to dou-ble between 2010 and 2020 and thepropor on of passengers origina ngin China on the route is projected tosurge from41of the total in 2010 to68 in 2025 (see chart on the right)Delta said recently that China would

become the ldquosecond key pillarrdquo inits Asia-Pacific franchise but that theChina EasternShanghai hub buildingwould be a ldquodecade-long processrdquo

At Deltarsquos latest investor dayin December 2015 the execu vesnoted that Delta is now ldquowell-representedrdquo in seven of the top tenUS interna onal markets meaningthat in those seven markets it eitherhas equity stakes in local carriers (UKChina Mexico and Brazil) an impor-tant JV partner (France and Italy) or a

hub (Japan) And the four countrieswhere the equity investments havebeen made are among the top six USinterna onal markets (see chart onthe le )

( Network and revenue diversifi-ca on

Deltaviews its interna onal alliancesjoint ventures and airline equity in-vestments as a key part of efforts tobuild a geographically balanced net-workanddiversify revenuesmdashstrate-gies that reduce business risk

Delta generally puts more em-phasis on diversifica on than itspeers For example it acquired itsown oil refinery in Pennsylvania mdashthe Trainer facility which is nowproducing profits

( Capital-efficient interna onalexpansion

Another reason Delta is increas-ingly relying on alliances and jointventures as noted by one of itsexecu ves ldquoEquity investments andcommercial collabora onwith globalpartners have allowed for capital-efficient interna onal expansionrdquo

Since its Chapter 11 reorgani-sa on and merger with Northwest

JanFeb 2016 wwwaviationstrategyaero 15

Delta has adopted very conserva vespending and balance sheet man-agement policies by most airlinestandards Despite having a rela velyold fleet Delta has kept fleet capex toa minimum and sought to maximisefree cash flow which it has used todeleverage the balance sheet andreward shareholders

Delta has also led the industry inkeeping capacity growth restrainedIn the spring of 2015 an cipa ng dif-ficult condi ons in interna onal mar-kets it was the first tomove to cut in-terna onal capacity growth this win-ter

In the fourth quarter Deltarsquos in-terna onal ASMs fell by 45 whichincluded a steep 11 capacity reduc-on on the Pacific and small 1 and

05 reduc ons on the Atlan c andLa n route areas respec vely Thebiggest cuts were in challenging mar-kets such as Japan Brazil and Russiawhile key strategic markets such asChina and Mexico con nued to seegrowth

Delta currently expects its sys-tem capacity to inch up by only 0-2 in 2016 but interna onal ASMswould be flat-to-down 2 Growthwill focus on markets with strong de-mand (US domes c UK Mexico andthe Caribbean) with offse ng re-duc ons in weaker markets (BrazilJapanMiddle East)

Relying on alliances and jointventures fits in perfectly with thosestrategies For example in the US-UKjoint venture growth in 2015 (about10) was led by Virgin Atlan cwhich reallocated aircra from itslossmaking AsiaPacific and Africanetworks to the transatlan cmarket

( Healthy profit contribu on

While exact financial figures are notavailable (treated as confiden al in-forma on in the case of the joint ven-

tures) the public commentsmade byDeltarsquosmanagement indicate that thetwo transatlan c joint ventures arehighly profitable

Deltahasnoted ineveryquarterlycall in the past 12 months that theJVs with AF-KLM and Virgin Atlan chave allowed it to con nue to expandtransatlan c profit margins despitea challenging environment Many ofthose markets have seen significantcurrency pressures reduced fuel sur-chargesandexcessive industrycapac-ity growth

The JV with AF-KLM benefitsfrom being the oldest and probablythe most deeply integrated of thetransatlan c alliances The JV has 25aircra devoted to it and achievesdouble-digit profitmargins

The Virgin Atlan c deal whichinvolved Delta buying SIArsquos 49stake for $385m has fixed DeltarsquosHeathrow access problem and madeit a credible player in the importantNew York-London business travelmarket Thanks to the JV and otherini a ves (new JFK terminal La-Guardia facility improvements andexpansion slot swaps etc) Deltamade its first profit in New York in2014

Deltarsquos management said re-cently that the $385m investmentin Virgin Atlan c in 2013 producedabout $150m of cash returns in 2015and would achieve full cash paybackby the end of this year It is producinga ldquominimum 50 return on invest-mentrdquo The execu ves described it asldquoprobably the single best investmentwersquovemade in terms of our returnsrdquo

It is worth recalling that threeyears ago many in the financial com-munity were scep cal of the valueof the Virgin Atlan c stake purchaseAt that me Virgin was losing moneyto the tune of $150m annuallyDeltarsquos ini al projec on had been

only $120m annual run-rate benefitswhen the JVwas fully developed

This year Delta is bringing VirginAtlan c to its technology pla ormmeaning that Delta will operate Vir-ginrsquos reserva ons systemTheairlinesexpect it to result in a seamless cus-tomer experience

The success of the transatlan cJVs has given Delta the confidenceto seek similar deals elsewhere Themanagement has said that the carrieris using those JVs as the model fordeepening rela onships with part-ners in other regions

The Aeromeacutexico and GOL al-liances are already contribu ngmaterially to Deltarsquos revenues mdash acombined $33m incremental rev-enue contribu on in last yearrsquos Q1and $25m in Q2 But it is s ll earlydays neither deal yet benefits froman open skies agreement or ATI

Delta expects this yearrsquos planned$750m addi onal investment inAeromeacutexico to be even more lu-cra ve with ldquoquick and immediatereturnrdquo given Mexicorsquos rela velyrobust economic fundamentals andAeromeacutexicorsquos strongmarket posi onBut like the GOL and China Easterninvestments it is a long-term project(more on it in the last sec on of thisar cle)

( Long-term cost savings

Delta also hopes that the Aeromeacutex-ico and GOL investments in par c-ular will facilitate cost reduc ons inthe long-term

In the first place savings arederived through a joint-ventureMROfacility that Delta and Aeromeacutexicoopened in Quereacutetaro Mexico inMarch 2014 The airlines disclosedin 2012 that they had invested $50mto build the facility which Delta saidwould ldquousher in lower maintenancecostsrdquowithout compromising quality

16 wwwaviationstrategyaero JanFeb 2016

0

5

10

15

20

2009 2010 2011 2012 2013 2014 2015 2020 target

$bn

DELTArsquoS ADJUSTEDNET DEBT

170

150

129117

94

7367

40

Note Debt and capitalised leases less cash and short-term investments

( Poten al tax savings

For many years Delta like most of itsUS peers has been able to avoid pay-ing federal corporate taxes by u lis-ing its net opera ng losses (NOLs) ac-cumulated during earlier lossmakingyears But thanks to a recent stringof record profits Delta expects to ex-haust its NOLs by 2018 and become afull taxpayer that year

In the US the statutory federalcorporate tax rate is rela vely high at35 andmost airlinespayabout38mdash the book rate that Delta has beenusing But many European countrieshavemuch lower corporate tax ratestypically in the low-to-mid 20s

At the 2014 investor day Deltahinted at the possibility that it couldobtain tax savings in the futureby tak-ing advantage of its interna onal JVsIt could set up a foreign subsidiaryfor those ac vi es in a countrywith alower tax rate

CEO Richard Anderson remarkedat that me that ldquoAmsterdam is agood placerdquo as Delta has large JVsthat are euro-denominated a 49stake in a London-based airline andalready a large commercial office in

Amsterdam for joint venture pricingand yield management The corpo-rate tax rate in the Netherlands is25

At the latest investor day Deltacommented on what it described asa ldquotransatlan c business reorganisa-onrdquo It has involved expanding the

Amsterdam office which now han-dles all decision-making for Deltarsquostransatlan c opera ons The pur-pose is to improve the effec venessof the JVs andaccelerate thebenefitsldquoStrong local brands require localdecision making capabili esrdquo theairline said The execu ves indicatedthat similar moves might follow inother parts of theworld

ldquoThat structure is going to allowus to make sure that interna onalcomponent is interna onalrdquo the air-line said As a result Delta expectsits 2016 book tax rate to be 35-36down slightly from the 37-38 up to2015 It is one way to lower book andcash taxes supplemen ng the morecommon methods such as acceler-ateddeprecia onandexcess pensionfunding

Strong financial posi on

Last but not least Delta is buyingthe equity stakes in other carriers be-cause it can easily afford such invest-ments As an addi onal plus pointthe financial community is not com-plaining

Delta was fortunate in that it hada mul -year head-start over Unitedand American on the merger front Itcompleted a successful merger withNorthwest in 2008 and accomplisheda quick and smooth integra on Soit was able quickly to reap the bene-fits of the merger and achieve stellarprofitability

In recent years Delta has beatenits US legacy carrier peers hand-somely on all financial fronts be itprofit margins ROIC debt reduc onor returning capital to shareholdersAnd Delta is now also claiming thatits financial metrics rank among thetop 10of SampP industrials

In the past six years Delta hasearned $134bn in aggregate netprofits before special items Thatincludes a $37bn ex-item net profitin 2015 Annual opera ng marginsare now in the high-teens And Deltaearned a ROIC of 283 in the 12months to December 31

The long term targets outlinedby Delta in May 2015 are to deliverannual EPS growth of at least 15achieve a ROIC of 20-25 and gener-ate annual opera ng cash flow of $7-8bn of which $4-5bn would be freecash flow

The equity investments in otherairlines are a small part of what Deltacalls a ldquobalanced capital deploy-mentrdquo First of all Delta is reinves ngabout 50 of its opera ng cash flowin the business That includes in-ves ng $25-3bn annually into fleetproducts facili es and technology

JanFeb 2016 wwwaviationstrategyaero 17

Second Delta con nues tostrengthen its balance sheet Havingreduced its adjusted net debt bymore than $10bn since 2009 from$17bn to less than $7bn the airlineis on track to reach its target of $4bnin net debt by 2020 (see chart on theprevious page) Annual interest costswith $4bn net debt will be around$200m down $11bn from the 2009level

On February 11Delta achieved itslong-term goal of becoming invest-ment grade whenMoodyrsquos upgradedthe companyrsquos debt ra ng from Ba3to Baa3 Delta joined a very exclusiveclub in North America only threeother airlines mdash Southwest West-Jet and Alaska mdash currently have in-vestment grade credit ra ngs Itmusthave been par cularly gra fying forCEORichardAndersonwho is re ringinMay

Third having returned nearly$4bn of cash to shareholders since2013 Delta has announced a new$5bn share repurchase programmeto be completed by the end of 2017

Last year Delta returned 70 ofits free cash flow to shareholderswhich was well above its 50 targetWith an es mated $3bn fuel tailwindin 2016 (at the $40bbl price) the air-line expects to ldquovastly exceedrdquo thelong-termfinancial goals this year

Delta is also commi ed to fund-ing its pension plans to the tune of$1bn annually It has a generous em-ployee profit-sharing programme inplace In mid-February Delta made a$15bn employee profit-sharing pay-ment for2015which it claimedbrokeall records of corporate profit sharingpayouts in the US

Delta is also taking steps to im-provewages It hasgranted its groundworkers andflight a endants a145base pay increase effec ve from thebeginning of December However as

a setbackDeltarsquos pilots failed to ra fyanewcontract in the summer as a re-sult of which Delta decelerated its al-ready slowfleet renewal it droppedatenta veorder for40smallernarrow-bodies (including 737-900ERs) andopted to keep 14 of its aging 757-200s

However in December Delta un-expectedly reinstated a big part ofthatorder saying that itwouldaddupto 20 Boeing-held E190s and 20 new737-900ERs This me the order isnot con ngent on a pilot deal ldquoWersquorenot going to limit our growth oppor-tuni esrdquo the execu ves said point-ing out that the new deal also hadldquomore compelling economicsrdquo

In short Delta is genera ng enor-mous cash flow and doing a decentjob in deploying it in an equitable andbalanced fashion It can be expectedto con nue acquiring stakes in air-lines around the world given the rel-a vely modest outlays involved thecapital-efficient nature of such ex-pansion the healthy profits gener-ated by such ventures and the likelytax benefits derived from having as-sets based outside the US

The nextmoves

Asia could be an area of special fo-cus for Delta China Eastern was agood start but Delta could do withmore partners in that vast and im-portant region Themanagement hasreportedly talked of the possibilityof strengthening the exis ng partner-shipwith Korean Air

But the La n American ventureswill also keep Delta busy in the nearterm because the impending openskies agreements will make it possi-ble to greatly strengthen the rela on-shipswith GOL and Aeromeacutexico

However uncertain es aboundThe US-Brazil open skies agreementwas supposed to take effect in Octo-

ber 2015 but its ra fica on by Brazilhasbeendelayedevidentlydue to thepoli cal and economic turmoil in thatcountry Nevertheless Delta execu-ves said recently that they expected

open skies to come into force in 2016and that Delta and GOL would file forATI ldquoshortly therea errdquo

The financial assistance thatDelta provided to GOL in the sum-mer (the addi onal stake purchaseand loan guarantee) facilitated anextension of the carriersrsquo exclusivecodeshare agreement Although themain upsidemay be in the long termone would expect an immunised JVto help both carriers in the currenttough market condi ons on Brazilianroutes

In recent weeks the three mainra ng agencies have all raised con-cern about GOLrsquos ability to meet itsfinancial obliga ons in the next 12-18months given its con nued cashburn due to Brazilrsquos economic crisisMoodyrsquos and Fitch have both down-graded GOLrsquos ra ngs and SampP hasplaced it on ldquocreditwatch nega verdquoAlso the Brazilian government isconsidering gran ng President DilmaRousseff emergency powers to waivethe current foreign ownership limitson airlines on a case-by-case basis

So Delta might be called to helpout its partner again Back in De-cember Delta execu ves noted thatthe next two years would be toughin Brazil that the GOL investmentwas for the longer term and thatthis was a good me to invest inBrazil They said that theywerework-ing with GOLrsquos leadership in ldquobuild-ing a durable model so that 24 to 36months fromnow yoursquore going to seesome significant returns from that in-vestmentrdquo

Delta is going a er Aeromeacutexicoreally aggressively with its Novemberproposal to increase its ownership

18 wwwaviationstrategyaero JanFeb 2016

75

10

20

30

40

50

2012 2013 2014 2015 2016

US$

(logscale)

DELTA SHARE PRICE PERFORMANCE

DAL

Rela ve to ARCAAirline Index

stake from the current 17 (includingDeltarsquos 41 stake op ons and Deltapension trustrsquos holdings) to up to49through a cash tender offer which ithopes to commence in the June quar-ter It would be a $750m cash deal

It would solidify Deltarsquos posi onin what is the largest US-La n Amer-ica market and one of the regionrsquosstronger economies On December18 the US andMexico signed a moreliberalised ASA which will becomeeffec ve once Mexico ra fies itDelta has also suggested that anopen skies agreement could be ap-

proved in 2016 The JV would makeDeltaAeromeacutexico the number oneairline systemonUS-Mexico routes

But Delta also believes thatAeromeacutexico will be an even morelucra ve investment than VirginAtlan c because Aeromeacutexico has asubstan al domes c marketplaceMexico is a ldquoneighbour countrywith a marketplace that is s llrela vely underdevelopedrdquo andAeromeacutexico is the ldquoflag carrier witha number one slot posi on [in slot-constrained Mexico City] much likeBA at Heathrowrdquo Yet Aeromeacutexico is

only a ldquo6opera ngmargin businesstodayrdquo

Delta execu ves stated at the in-vestor day ldquoWe feel rela vely con-fident just as wersquove done with Vir-gin that with our know-how our in-vestment and our co-loca on of re-sources that we can double thosemargins over the next 3-5 years Andthatrsquos going to provide a very nice re-turn on that capital investmentrdquo

Delta may be forge ng some-thing Mexico has a vibrant LCCsector with the three leading LCCsaccoun ng for 63 of Mexicorsquos do-mes c traffic (and therefore havingpricing power) and 41 of interna-onal traffic to and fromMexico (July

2015 DGAC data) The high level ofLCC compe on is one reason whyAeromeacutexicorsquos opera ng margins arelagging The LCCs have done a lot todevelop the domes c market andwill fight tooth and nail to retain theirmarket shares That said Aeromeacutexicocould s ll be a successful investmentfor Delta

By Heini Nuu nenheinitheavia oneconomistcom

JanFeb 2016 wwwaviationstrategyaero 19

The Principals and Associates of Avia on Strategy apply a problem-solving crea veand pragma c approach to commercial avia on projects Our exper se is in strategicand financial consul ng in Europe the Americas Asia Africa and theMiddle East

Start-up business plans Due diligence An trust inves ga ons Credit analysis IPO prospectuses

Turnaround strategies Priva sa on projects Mergertakeover proposals Corporate strategy reviews An trust inves ga ons

State aid applica ons Asset valua ons Compe tor analyses Market analyses Trafficrevenue forecasts

For further informa on please contactJames Halstead or KeithMcMullan Avia on Strategy Ltd

e-mail infoavia onstrategyaero

Boeing Orders 2015

Customer 737 767 777 787 747 BBJ Total

NG MAX

AsiaPacific

Air Tahi Nui 2 2ANA 5 3 8

EVAAir 7 18 25Korean Air 30 7 37

Qantas 5 5Ruili Airlines 30 30

SilkWay Airlines 3 3SilkAir 6 6

Sriwijaya Air 2 2Virgin Australia 4 4

AsiaPacific Total 7 70 14 28 3 122

Europe

AirBridgeCargo 2 2

Enter Air 1 1Jet2com 30 30

Norwegian 19 19Ryanair 3 3

Swiss Global 3 3TUI Travel 1 1

THY 10 10Europe Total 33 11 3 20 2 69

Lan

America

Air Austral 2 2COPA 51 51GOL 9 9

La n America Total 60 2 62

Middle

EastAfrica

EL AL 3 3

Ethiopian 6 6E had 2 2

OmanAir 20 20Qatar 14 14

Middle EastAfrica Total 20 16 9 45

North

America

Alaska 6 6Atlas Air 1 1

Delta 20 20FedEx 49 49United 10 10

North America Total 26 49 10 1 86

Lessors

AerCap 100 100

ALC 8 8BOC 13 11 24

GECAS 2 2SMBC 10 10

Lessor Total 15 129 144Business JetVIP 2 2 2 1 7

Uniden fied 151 117 15 38 321USNavy 13 13

Gross Orders 247 409 49 58 99 6 1 869

Cancella ons Conversions

(68) (28) (4) (100)

Net orders 588 49 58 71 2 1 769

Airbus Orders 2015

Customer A320 A330 A350 A380 Total

ceo neo

AsiaPacific

Air New Zealand 2 2AirAsia (9) 9

ANA 4 3 7Asiana 25 25Indigo 250 250

Korean Air 30 30Lion Air (9) 9

Peach Avia on 3 3Philippine Airlines (10) 12 2

SIA 4 4Tigerair (2) 2

Vietjet Air 15 21 36AsiaPacific Total (6) 361 4 359

Europe

Acropolis Avia on 1 1Aer Lingus 2 2

Atlan c Airways 1 1Bri sh Airways 15 15Croa a Airlines (4) 4

easyJet 6 30 36Groupe Dubreuil 1 1 2

Iberia 20 5 8 33Lu hansa (1) 1

TAP 39 14 53THY 20 4 24

Vueling 15 15Wizz Air (10) 110 100

Europe Total (8) 255 26 9 282Avianca 100 100

La n America Total 100 100

Middle

EastAfrica

Israir 1 1Middle East Airlines 1 1

Rwandair 2 2South African Airways 5 5

Middle EastAfrica Total 1 8 9Fron er Airlines 12 12

North America Total 12 12

Lessors

ALC 3 30 26 1 60ACG 1 1

Avolon 4 4BOCAvia on 3 2 5

CALC 2 2CASC 30 30CIT 5 5

GECAS 60 60IAC 30 20 50

Standard Chartered 2 2Lessor Total 47 91 80 1 219

Private Customer 1 4 2 7Undisclosed 13 50 27 2 3 95Gross Orders 60 861 143 16 3 1083Cancella ons (13) (11) (3) (19) (1) (47)

NetOrders 47 850 140 (3) 2 1036

DELIVERIES 2015

Boeing Airbus

Type No Ratedagger Type No Ratedagger

737 495 412 A320 491 409767 16 13777 98 82 A330 103 86787 135 112 A350 14 12747 18 15 A380 27 22

Total 762 Total 635

dagger permonth

A beat Boeing in the an-nual PR race for orders in2015 In the year it achieved

announced net sales of 1036 air-cra (a er allowing for cancella onsand conversions) down from 1456in 2014 compared with the Sea le-based manufacturerrsquos 769 (half theprevious yearrsquos 1432) Total industrynet orders are es mated to have to-talled 2193 in the year down from a

peak of 3698 in 2014Airbus gained from two par cu-

larly large orders in the narrowbodysegment Indigo the indian LCC putin an order for 250 A320s and WizzAir for another 110 of the type TotalA320 orders (neo and ceo) amountedto just short of 900 units On top ofthis were net orders for 140 A330snet cancella ons of 3 A350s and amere net two newA380 orders

20 wwwaviationstrategyaero JanFeb 2016

Boeing and Airbus orders 2015

0

500

1000

1500

2000

2500

3000

3500

4000

1965 1970 1975 1980 1985 1990 1995 2000 2005 2010 2015 20200

2

4

6

8

10

AIRCRAFT DELIVERY CYCLE

Deliveries

Net Orders

Deliveries Ac ve fleet

0

2000

4000

6000

8000

10000

12000

14000

16000

2000 2005 2010 2015 20200

2

4

6

8

10

12

Units

Years

AIRCRAFTORDER BACKLOG

Backlog

Yearsrsquo Produc on

0

200

400

600

800

1000

1200

1400

1600

1800

2016 2020 2025 2030

AIRCRAFT BACKLOGDATEDDELIVERIES

Lessorsrsquo orders

Airline orders

Source Airline Strategy AirlineMonitor (airlinemonitorcom

Boeing meanwhile received netnew orders for 588 737s 49 767Fs(from FedEx) 58 777s (including teneach from Qatar and United) and 71787s

On deliveries however Boeingoutshone Airbus with an overallproduc on of 762 aircra against635 On narrowbodies the two wereevenly matched delivering 495 737sand 491 A320s respec vely (equiv-alent to around 40 aircra a montheach)

Overall the outstanding industrybacklog is es mated at nearly 14700aircra to be delivered from 2016This is upby 400units from the endof2014 and represents some nine yearsof current produc on The backlogschedule of deliveries suggest pro-duc on levels of around 1600 air-cra a year for the next four years

In February the doyen of equip-ment forecas ng Ed Greensletpublished his Airline Monitor updateof long term projec ons Contro-versially he has brought forwardhis expecta on of the next industrydownturn from 2021 to 2018 addingin an assump on that with low oilprices there will be a lower rateof re rement of older equipmentand that the combina on of slowergrowth inChina collapse in commod-ity prices and US Dollar strength willhave amaterial impact on demand

As a result his new forecasts sug-gest that 2015 will be the peak foraircra deliveries in this cycle More-over he is sugges ng that total deliv-eries over the next few years may beless than those suggested by the or-der backlog implying that the man-ufacturersrsquo plans to build produc onrates (par cularly of the narrowbod-ies)may bemistaken

JanFeb 2016 wwwaviationstrategyaero 21

The Principals and Associates of Avia on Strategy apply a problem-solvingcrea ve and pragma c approach to commercial avia on projects

Our exper se is in strategic and financial consul ng in Europe the Americas AsiaAfrica and theMiddle East covering

Start-up business plans Due diligence An trust inves ga ons Credit analysis IPO prospectuses

Turnaround strategies Priva sa on projects Mergertakeover proposals Corporate strategy reviews An trust inves ga ons

State aid applica ons Asset valua ons Compe tor analyses Market analyses Trafficrevenue forecasts

For further informa on please contact

James Halstead or KeithMcMullan

Avia on Strategy Ltd

e-mail infoavia onstrategyaero

Entermy Avia on Strategy subscrip on for 1 year (10issues ndash JanFeb and JulAug are combined)

( UK pound475 + VAT

( EU euro610 +VAT (unless valid VATnumber supplied)

( USA and Rest of world US$780

star ngwith the issue

o I enclose a Sterling or Euro cheque made payable toAvia on Strategy Ltd

o Please invoicemeo Please charge my VisaMastercardAmerican Ex-

press credit card pound475+VATCard number Expiry

Name on Card CV2

o I amsendingadirectbank transferof the the relevantsum net of all charges to Avia on Strategyrsquos bank ac-countMetro Bank Ltd 1 Southampton Row LondonWC1B 5HAIBAN GB04MYMB2305 8013 1203 74Sort code 23-05-80 Account no 13120374Swi MYMBGB2L

Delivery AddressNamePosi onCompanye-mailTelephoneVATNo

Invoice Address

NamePosi onCompanyAddress

CountryPostcode

DATA PROTECTIONACTThe informa on you providewil be held on our database andmay be usedtokeepyou informedofourproductsandservicesor for selectedthirdpartymailings

PLEASE RETURN THIS FORMTOAvia on Strategy Ltd Davina House 137-149 Goswell Road

London EC1V 7ET UKe-mailinfoavia onstrategyaero

Tel +44(0)207-490-4453 Fax +44(0)207-504-8298VAT Registra onNo GB 162 7100 38

Aviation StrategyISSN 2041-4021 (Online)

This newsle er is published ten mes a yearby Avia on Strategy Limited JanFeb andJulAug usually appear as combined issuesOur editorial policy is to analyse and covercontemporary avia on issues and airlinestrategies in a clear original and objec-ve manner Avia on Strategy does not

shy away from cri cal analysis and takes aglobal perspec ve mdash with balanced cover-age of the European American and Asianmarkets

PublisherKeithMcMullanJames Halstead

Editorial TeamKeithMcMullankgmavia onstrategyaero

James Halsteadjchavia onstrategyaero

Tel +44(0)207-490-4453Fax +44(0)207-504-8298

Subscriptionsinfoavia onstrategyaero

Copyrightcopy2016 All rights reserved

Avia on Strategy LtdRegisteredNo 8511732 (England)RegisteredOffice137-149 Goswell RdLondon EC1V 7ETVATNo GB 162 7100 38ISSN 2041-4021 (Online)

The opinions expressed in this publica ondonotnecessarily reflect theopinionsof theeditors publisher or contributors Every ef-fort is made to ensure that the informa oncontained in this publica on is accurate butno legal reponsibility is accepted for any er-rors or omissions The contents of this pub-lica on either in whole or in part may notbe copied stored or reproduced in any for-mat printed or electronic formwithout thewri en consent of the publisher

AIRASIA X RESULTS BY REGION

Results (RMm) Margins

2013 2014 2015 2013 2014 2015

North

Asia

Revenues 1147 1409 1470

EBITDAR 176 191 235 153 136 160

PBT (83) (263) (488) -72 -187 -332

Australia

Revenues 903 1048 927

EBITDAR 94 (1) 177 104 -01 191

PBT (113) (369) (232) -125 -352 -250

Others

Revenues 256 478 665

EBITDAR 67 153 413 262 320 621

PBT (14) 26 286 -55 54 430

Total Revenues 2306 2935 3062

EBITDAR 337 343 825 146 117 269

PBT (210) (606) (434) -91 -206 -142

assets include RM520m of deferredtax assets which only become usefulwhenif the airlines starts to makesubstan al profits

Erra c route development

It is impossible to iden fy which ifany of its routes AirAsia X is mak-ing money on However the regionalbreakdownprovided by the companyshows thaton the twomajor route re-gionsAirAsia Xmadehuge losses lossmargins at the PBT level of -332 onNorth Asia and -25 on Australia re-lying on an ill-defined ldquoothersrdquo profitmarginof43tobring theoverall sys-tem to a loss of -142

AirAsia Xrsquos network evolu on issummarised in the maps on the fac-ing page In its early years the airlinea empted to build a European net-work opera ng to London and Parisbut a er suffering heavy losses AirA-sia Xwas forced toabandon this oper-a on in 2013 It appears to have beenunable to find a niche between the

MiddleEast super-connectors captur-ingprice-sensi ve trafficonMalaysia-UKroutesontheonesideandflagcar-riers BA and MAS filtering off pre-mium traffic on the other AirAsia Xthen concentrated on amajor expan-sion into Australia Japan South Ko-rea and China again suffering ma-jor losses as it came up against lowcost compe on in the form of Jet-star (see pages 8-13) and ldquoirra onalcompe on from industry peersrdquo bywhich it meant that MAS despite itsde facto bankrupt state was not cut-ng capacity as rapidly as it should

haveAlthough the core Malaysian op-

era on was deeply problema c theairline persisted with its strategy ofse ng up long-haul associate carri-ers alongside the short haul asso-ciates in IndonesiaandThailand IAAXand TAAXrsquos results are not included inthose of AirAsia X bhd but theymadea combined net loss of $31m in thefirst three quarters of 2015

2 wwwaviationstrategyaero JanFeb 2016

AIRASIA X ROUTEDELOPMENT

Auckland

ChongqingChengduDelhi

Bali

Hangzhou

Tokyo HNDSeoul

Jeddah

Osaka

Kathmandu

Kuala Lumpur

Melbourne

Nagoya

Tokyo NRT

Gold Coast

Beijing

Perth

Busan

Shanghai

Sydney

Taipei

Xian

2016

Adelaide

Colombo

Chengdu

Hangzhou

Tokyo HNDSeoul

Jeddah

Osaka

Kathmandu

Kuala Lumpur

Melbourne

Male

Nagoya

Gold Coast

Beijing

Perth

Busan

Shanghai

Sydney

Taipei

Xian

2014

Mumbai

Christchurch

ChengduDelhi

Hangzhou

Tokyo HNDSeoul

TehranOsaka

Kuala Lumpur

London LGW

Melbourne

Gold Coast

Paris

Perth

London STN

Taipei

Tianjin

2011

Abu DhabiChengdu

Hangzhou

Kuala Lumpur